Embed Size (px)

DESCRIPTION

Transfer Pricing: Current Developments in U.S., Canada and Mexico February 15, 2007 Course 3B MODERATOR Jim Hill, Esq., Deloitte & Touche SPEAKERS Lic. Simón Somohano John Breen, Esq. Mr. Thomas A. Vidano. Intercompany Services Regulations and Ownership of Intangibles. - PowerPoint PPT Presentation

Citation preview

Transfer Pricing: Current Developments in U.S., Canada and Mexico

February 15, 2007Course 3B

MODERATORJim Hill, Esq., Deloitte & Touche

SPEAKERSLic. Simón Somohano

John Breen, Esq.Mr. Thomas A. Vidano

Intercompany Services Regulations and Ownership

of Intangibles

Historical Background• Current services regulations (§1.482-2) were promulgated in

1968 and are not as relevant for service based economies

• Proposed services regulations issued in September, 2003 for intercompany services transactions and ownership of intangibles

• Temporary and Final Regulations issued on July 31, 2006

– On December 21, 2006, IRS issues Notice 2007-5 and Rev. Proc. 2007-13 clarifying rules and addressing taxpayer concerns

Background (cont’d)

• Effective date (discussed below)

Temporary Regulations related to intercompany

services transactions

Temp Regs (cont’d) • Broad definition of what constitutes a service

– Regulations apply to a Controlled Services Transactions (“CST”):

• CST is an “activity” that results in a “benefit” to other member of the controlled group

– “Activity” is very broadly defined:• Performance of functions• Assumption of risks• Use by renderer of tangible or intangible property or other

resources, capabilities or knowledge• Making available to the recipient any property or resources

Temp Regs (Cont’d) • General benefit approach abandoned so that a specific benefit

must have been conferred to service recipient.• “Benefit” defined.

– reasonably identifiable increment of economic or commercial value that enhances the recipient’s commercial position, or may reasonably be anticipated to do so

– Benefit will generally exist if recipient would be willing to pay for the same activity or perform the activity itself

• Passive association is generally not a benefit• Narrowed definition of “shareholder” activities

Temp Regs (Cont’d)• Temp Regulations seek to address IRS concern that

intangible/tangible transfers may be disguised as services transactions– Provision of service which effects intangible must generally be

determined or corroborated by an analysis under the rules for transfers of intangibles

– Preamble provides that Commensurate With Income only applies to material intangible transfers

• Special rules for contingent payment arrangements and integrated transactions

Overview – Temp Regs (Cont’d)

Sets forth specified methods to analyze provision/receipt of intercompany services

1. Services Cost Method – major change from 2003 Proposed Regulations

2. Comparable uncontrolled services price 3. Gross services margin4. Cost of services plus5. Comparable profits 6. Profit split 7. Unspecified Methods

Methods 2 – 7 generally consistent with existing U.S. rules (for tangibles and intangibles) and OECD Guidelines (all)

Replacing “Cost Safe-harbor”

Charging cost for routine, administrative services

Simplified Method vs. Cost Safe-harbor

• 2003 Proposed regulations introduced Simplified Cost Based Method– Allowed taxpayers to charge cost in certain circumstances– Widely criticized as unworkable and costly to implement

• 2006 Temporary Regulations respond to criticisms by introducing– Services Cost Method (SCM)– Shared Services Arrangements (SSA)

Services Cost Method (SCM)

• Arm’s length charge is equal to the total service cost (w/out markup) for:

• Specified covered services:– Provided by IRS (Rev. Proc. 2007-13) OR

• Low margin covered services:• Median mark-up less than or equal to 7% AND

• Services do not contribute significantly to key competitive advantages, core capabilities or fundamental risks of renderer, recipient or both AND

• Not an excluded category of high value services AND• Taxpayer maintains required documentation

SCM – Specified Covered Services

• Rev. Proc. 2007-13 lists Specified Services– 101 activities in 20 categories

• Listed services are largely administrative, back office services , such as: – Compiling and posting employee time and other information

needed to calculate periodic compensation– Compiling and recording billing, accounting, and other

numerical data for billing purposes

SCM – Low Margin Services

• Median mark-up on total service costs of comparable companies is less than or equal to 7%.

• Specifically excluded services (see below) do not qualify even if median less than 7%

SCM – Specifically Excluded Services

• Services that contribute to key competitive advantages, core capabilities or fundamental risks or success of the business of the renderer or recipient or both do not qualify for the SCM

– IRS will respect Taxpayer’s reasonable judgment (per the preamble)

SCM – Specifically Excluded Services

• Manufacturing• Production Extraction, exploration, or processing of

natural resources• Construction• Reselling, distribution, acting as a sales or purchasing

agent, or acting under a commission or similar arrangement

• Research, development, or experimentation• Engineering or scientific• Financial transactions, including guarantees• Insurance or reinsurance

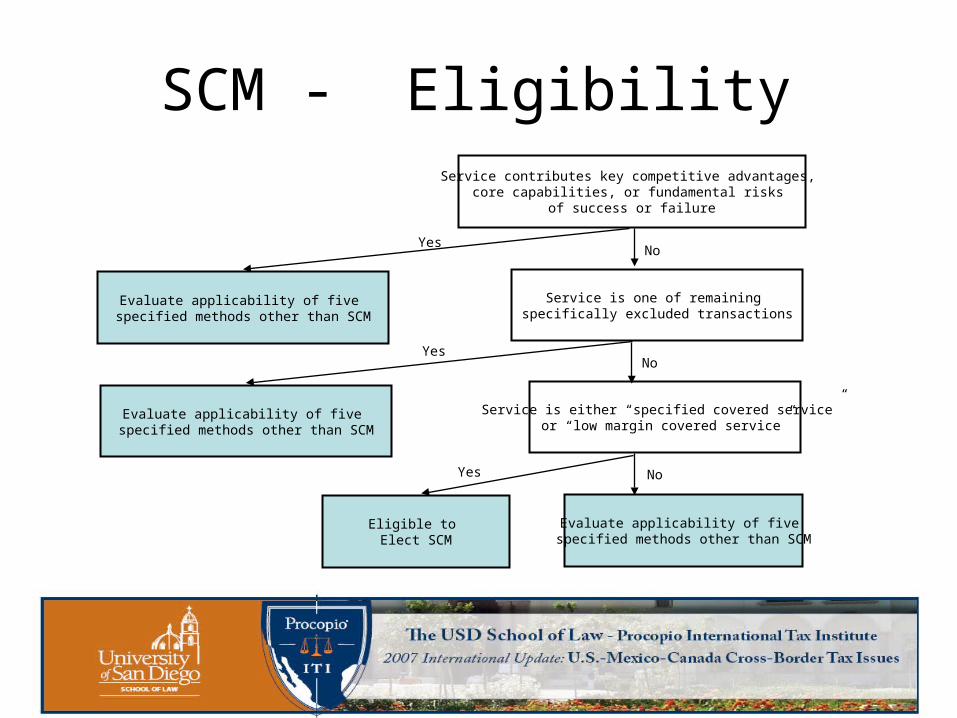

SCM - EligibilityService contributes key competitive advantages,

core capabilities, or fundamental risks of success or failure

Service is one of remaining specifically excluded transactions

Evaluate applicability of five specified methods other than SCM

Evaluate applicability of five specified methods other than SCM

Service is either “specified covered service” or “low margin covered service”

Evaluate applicability of five specified methods other than SCM

Eligible to Elect SCM

Yes

Yes

Yes

No

No

No

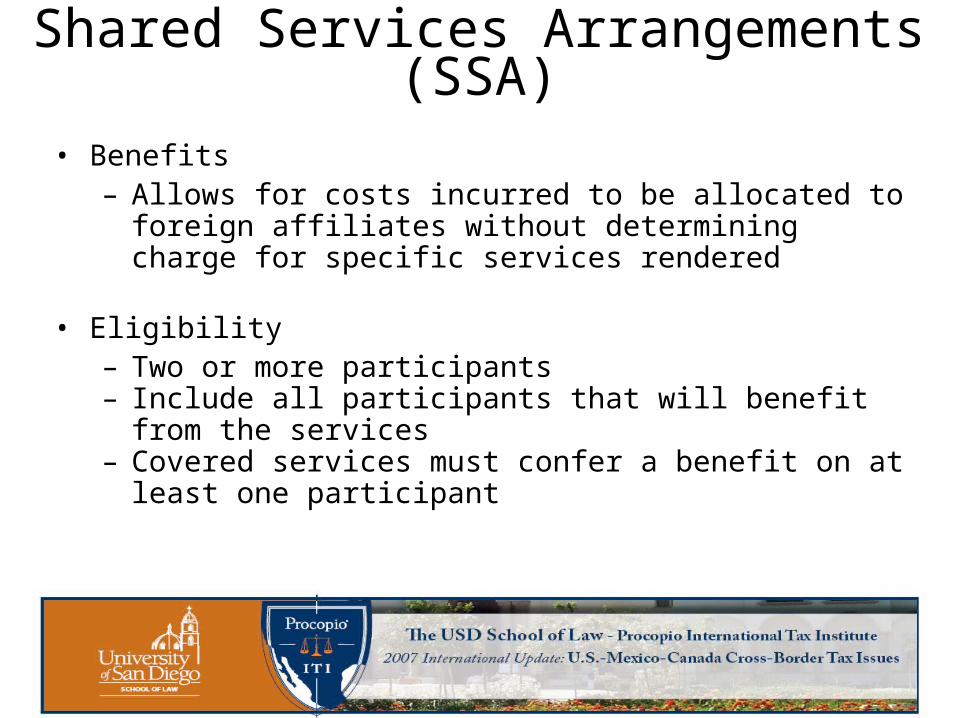

Shared Services Arrangements (SSA)

• Benefits– Allows for costs incurred to be allocated to foreign affiliates

without determining charge for specific services rendered

• Eligibility– Two or more participants– Include all participants that will benefit from the services– Covered services must confer a benefit on at least one

participant

SSA (cont’d)• Services must be allocated based on reasonably anticipated

benefits– Allocation keys such as sales, head count, assets, etc.

• Special Aggregation rule– Permitted to aggregate a group of services even though

each participant will not benefit equally as long as overall allocation is reasonable

• Taxpayers must maintain documentation, including a statement that it intends to apply SCM under the SSA

Temporary Regulations related to ownership of intangibles

Overview – Temp Regs (Cont’d)

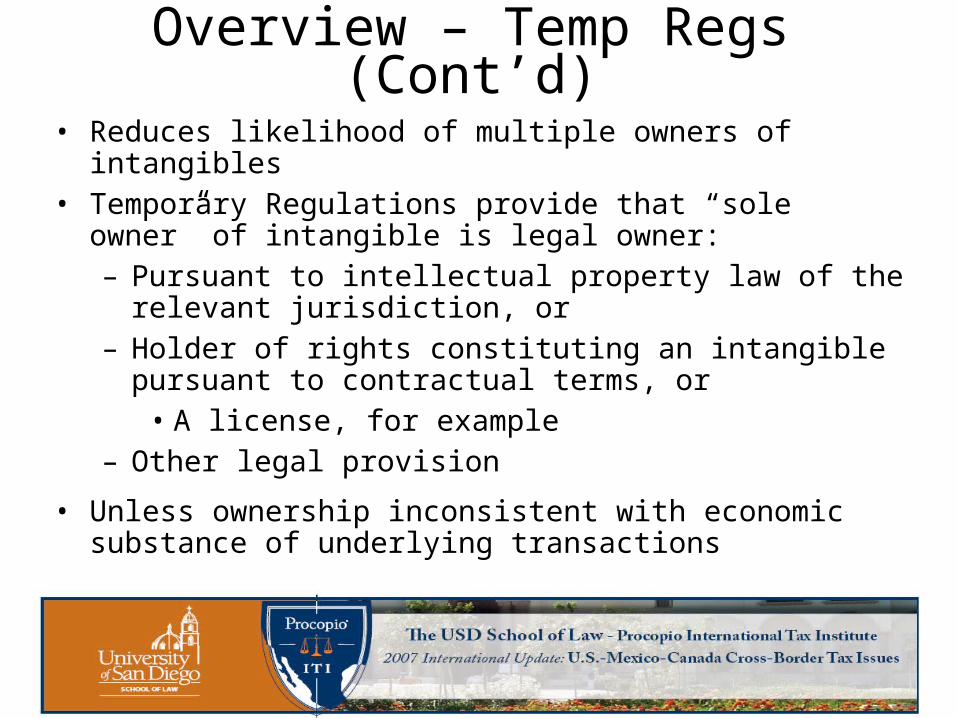

• Reduces likelihood of multiple owners of intangibles • Temporary Regulations provide that “sole owner” of intangible

is legal owner:– Pursuant to intellectual property law of the relevant

jurisdiction, or– Holder of rights constituting an intangible pursuant to

contractual terms, or• A license, for example

– Other legal provision

• Unless ownership inconsistent with economic substance of underlying transactions

Overview – Temp Regs (Cont’d)

• If none of the above, then taxpayer that has control of intangible will be sole owner

– Example: Subsidiary owns its customer list, which is not covered under contract or local law

Conclusions• Increased consistency between analysis for services and

tangible and intangible property

• SCM and SSA allow for charge outs at cost

• How will foreign countries react?

– charge out for shareholder activities, stock based compensation

• Temporary regulations place substantially more emphasis on advance planning, written agreements and documenting economic substance

James M. Hill, LL.M., CPA is a Senior Manager in the Los Angeles transfer pricing practice of Deloitte. James received his LL.M., in

Taxation, from New York University, and his J.D. from the University of Notre Dame Law School. He is also a California Certified Public

Accountant. The observations and opinions expressed in this presentation, as well as any errors or omissions, are the author’s

own and should not be attributed to Deloitte & Touche, its partners, or other employees

James can be reached by phone at (213)688-3224 or by e-mail at: [email protected].

The information contained in this publication is for general purposes only and is not intended, and should not be construe, as legal,

accounting, or tax advice or opinion provided by Deloitte & Touche and the presenter, to the reader. This material may not be

applicable or suitable for, the reader’s specific circumstances or needs. Therefore, the information should not be used as a

substitute for consultation with professional accounting, tax, or other competent advisors. Please contact the presenter, or local

Deloitte & Touche office, before taking any action based upon this information.