Embed Size (px)

Citation preview

American Bar AssociationTax Section

2011 Midyear MeetingBoca Raton, FL

January 20-22, 2011

An Update on OECD Transfer

Pricing Developments and Proposals

for the Taxation of Intangibles

This presentation is offered for informational purposes only and the contents should not be construed as legal advice on any matter

January 21, 2011 2

Panelists

Moderator:

A. W. Granwell,DLA Piper LLP (US)

Washington, DC

Panelists:

David Ernick

Associate International Tax Counsel

Department of Treasury

Washington, DC

Daniel J. Frisch

Managing Director

Horst Frisch Inc.

Washington, DC

Michelle LevacTransfer Pricing Specialist

Canada Revenue Agency

Chair, OECD Working Party 6,

Paris, France

Ramon Lopez De Haro

Garrigues,

Madrid, Spain

Janice McCart

Blake Cassels & Graydon LLP

Toronto, Canada

January 21, 2011 3

Agenda

• Business Restructurings (OECD)

• OECD Intangibles Project

• US Transfer Pricing Proposals

January 21, 2011 4

Business Restructurings

January 21, 2011 5

Introduction

• Business Restructuring is a cross-border redeployment of

assets, functions and risks among affiliated entities of a

multinational group (“MNC”).

• Business restructurings can enable an MNC to compete more

efficiently, preserve profits or limit losses in the global

economy.

• Business restructurings may result in the erosion of the tax

base of the host countries in which the restructured

companies are resident and therefore are under active

scrutiny by high tax countries and the OECD.

January 21, 2011 6

Business Models

• Vertically integrated business model. Under this business

model, MNCs conduct full-fledged manufacturing, distribution

activities and associated services through separate locally incorporated entities (H Cos). Each H Co is treated as the

entrepreneur in its local country.

• Supply chain management business model. This business

model entails centralizing in one company (E Co), resident in a tax friendly jurisdiction, overall responsibility for managing

and conducting a business segment, including R&D,

manufacturing, distribution and associated services.

• These are endpoints on a spectrum. Intermediate cases of

various sorts are common.

January 21, 2011 7

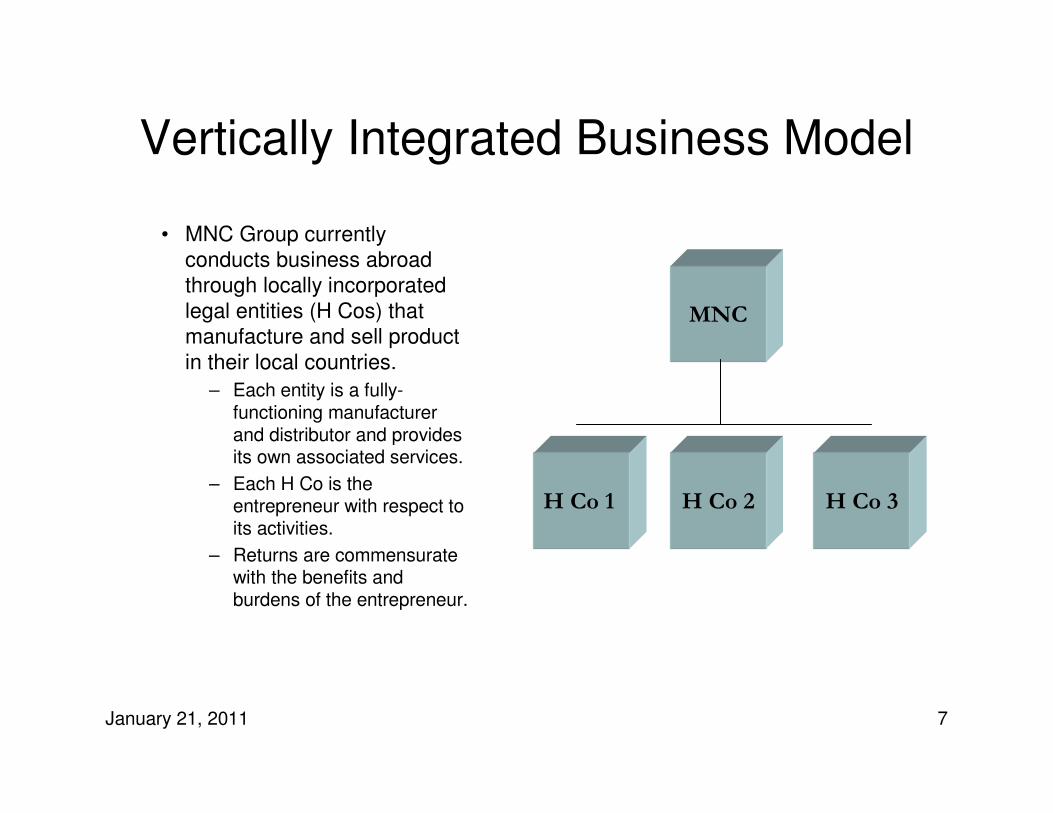

Vertically Integrated Business Model

• MNC Group currently

conducts business abroad

through locally incorporated

legal entities (H Cos) that

manufacture and sell product

in their local countries.

– Each entity is a fully-functioning manufacturer and distributor and provides its own associated services.

– Each H Co is the entrepreneur with respect to its activities.

– Returns are commensurate with the benefits and burdens of the entrepreneur.

MNC

H Co 1 H Co 2 H Co 3

January 21, 2011 8

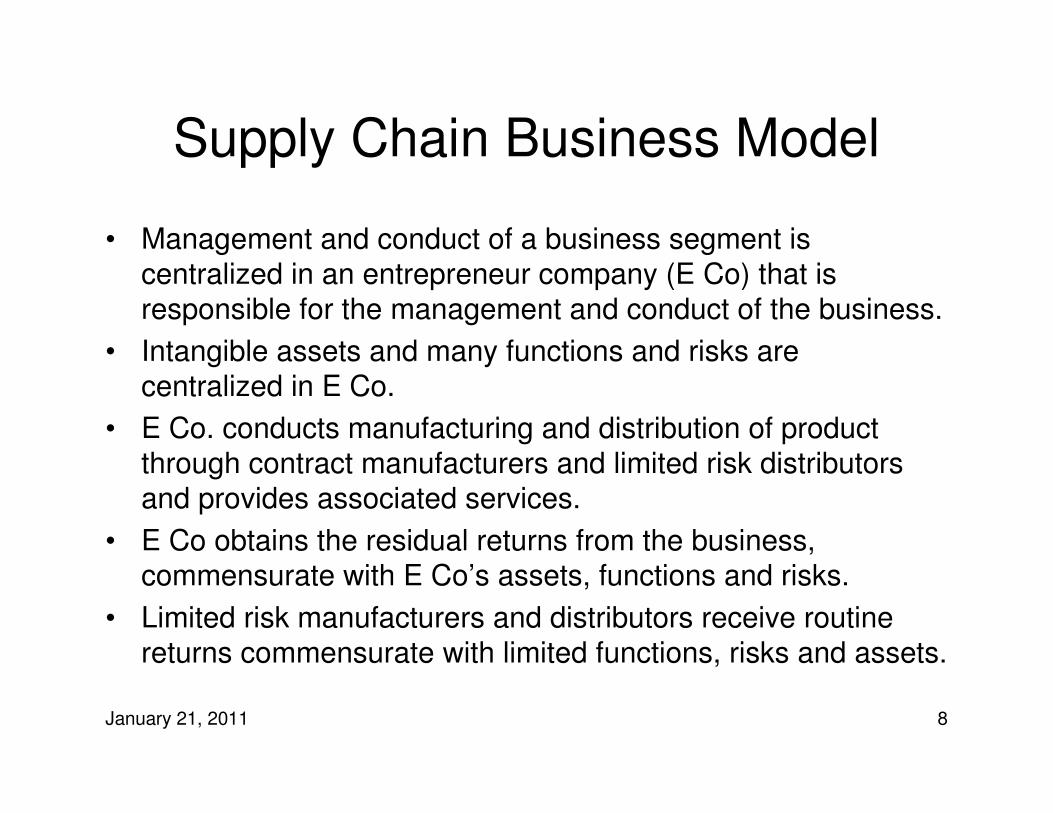

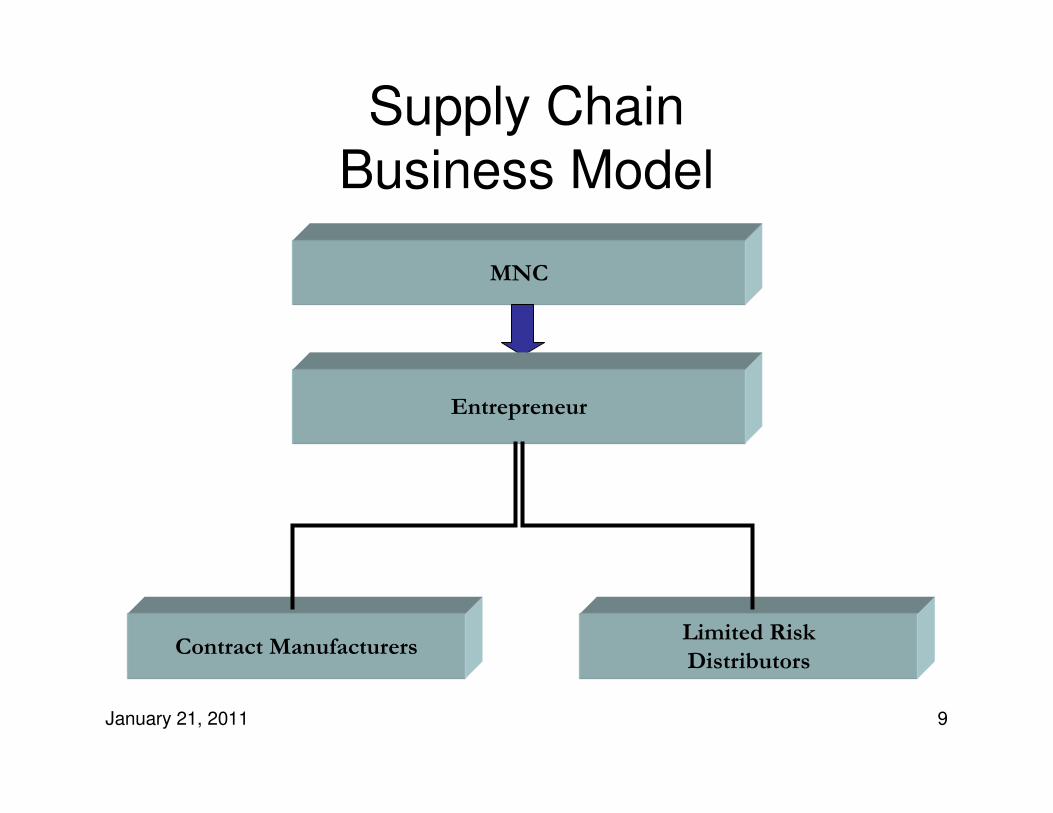

Supply Chain Business Model

• Management and conduct of a business segment is

centralized in an entrepreneur company (E Co) that is

responsible for the management and conduct of the business.

• Intangible assets and many functions and risks are

centralized in E Co.

• E Co. conducts manufacturing and distribution of product

through contract manufacturers and limited risk distributors

and provides associated services.

• E Co obtains the residual returns from the business, commensurate with E Co’s assets, functions and risks.

• Limited risk manufacturers and distributors receive routine

returns commensurate with limited functions, risks and assets.

January 21, 2011 9

MNC

Entrepreneur

Limited Risk

DistributorsContract Manufacturers

Supply Chain

Business Model

January 21, 2011 10

Restructuring

• The restructuring is achieved by “migrating” intangibles and

“stripping out” functions and risks from the H Cos and

centralizing these intangibles, functions and risks in E Co, which will function as the entrepreneur with respect to the

business segment that is the subject of the restructuring.

January 21, 2011 11

Migration of Intangibles

• Intangibles can be migrated through:

– Assignment.

– Licensing.

– Cost sharing.

– Transfer of employees.

– Virtual migration.

January 21, 2011 12

Manufacturing Operation Restructuring

• Manufacturing operations are restructured by converting full-

fledged manufacturers into contract or toll manufacturers.

• After restructuring, R&D is performed pursuant to a cost

sharing arrangement and/or on a reimbursable cost plus

basis.

January 21, 2011 13

Supply Chain Restructuring

• The supply chain is restructured by converting full-fledged

distributors into low-risk stripped distributors or

commissionaires, and the creation of central regional management logistics platforms and shared service centers.

January 21, 2011 14

Attributes: The Entrepreneur

• E Co will incur the benefits and burdens associated with the

centralized activities and be allocated the residual income or

loss from such activities.

• E Co will have the requisite substance to function as the

entrepreneur.

• E Co will be adequately capitalized to perform its functions

and to bear the risks that it will incur.

• E Co will have the tangible and intangible assets necessary to

perform its functions.

• E Co will have its own employees capable of conducting the

business resident in its office in the tax-friendly jurisdiction.

January 21, 2011 15

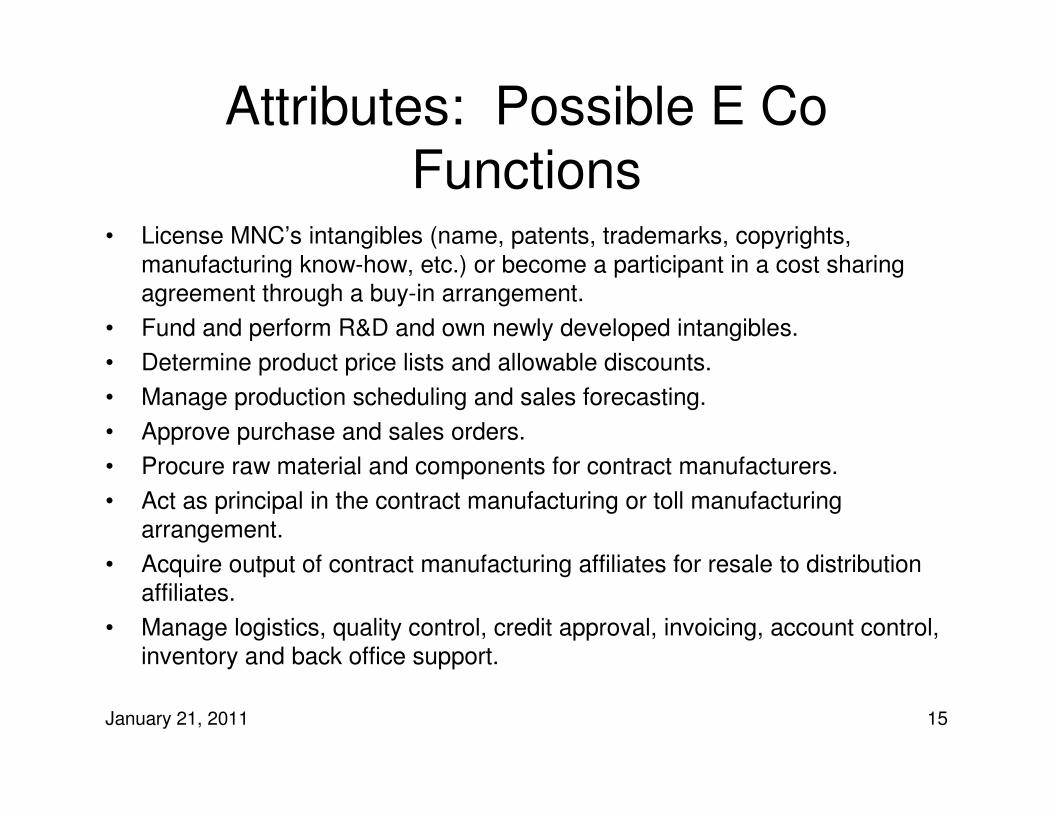

Attributes: Possible E Co

Functions• License MNC’s intangibles (name, patents, trademarks, copyrights,

manufacturing know-how, etc.) or become a participant in a cost sharing

agreement through a buy-in arrangement.

• Fund and perform R&D and own newly developed intangibles.

• Determine product price lists and allowable discounts.

• Manage production scheduling and sales forecasting.

• Approve purchase and sales orders.

• Procure raw material and components for contract manufacturers.

• Act as principal in the contract manufacturing or toll manufacturing

arrangement.

• Acquire output of contract manufacturing affiliates for resale to distribution

affiliates.

• Manage logistics, quality control, credit approval, invoicing, account control,

inventory and back office support.

January 21, 2011 16

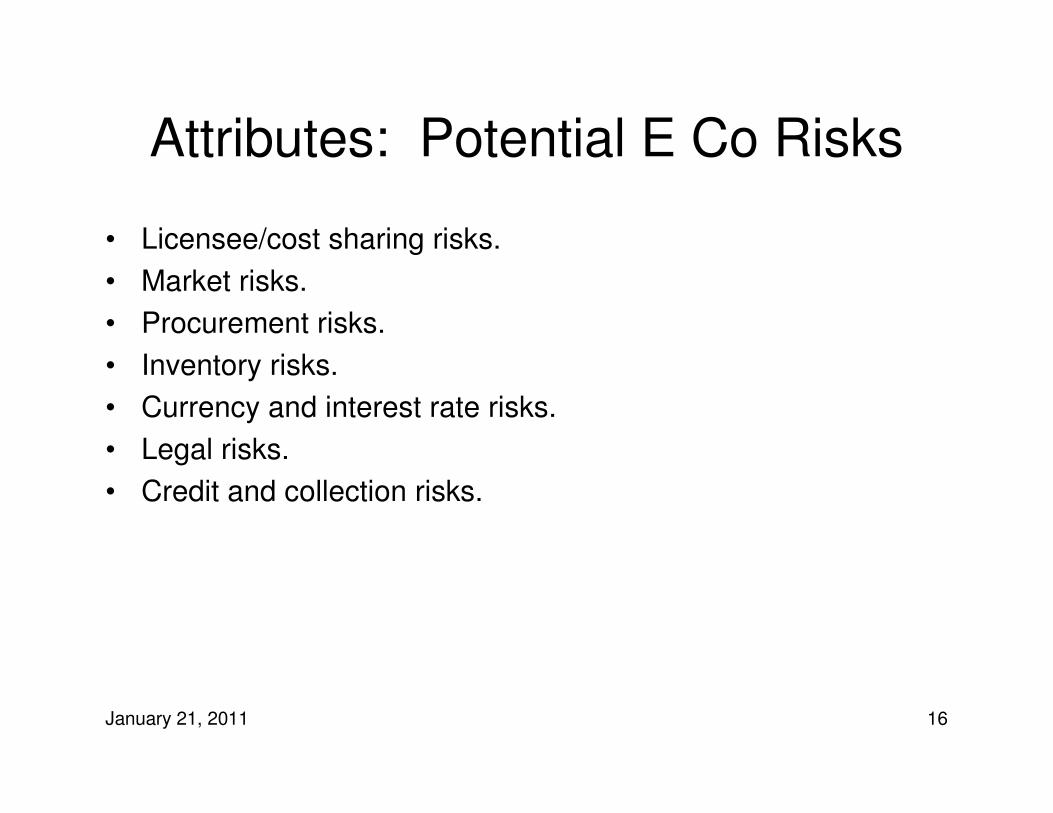

Attributes: Potential E Co Risks

• Licensee/cost sharing risks.

• Market risks.

• Procurement risks.

• Inventory risks.

• Currency and interest rate risks.

• Legal risks.

• Credit and collection risks.

January 21, 2011 17

E Co’s Return

• Entrepreneur’s residual profit or loss.

January 21, 2011 18

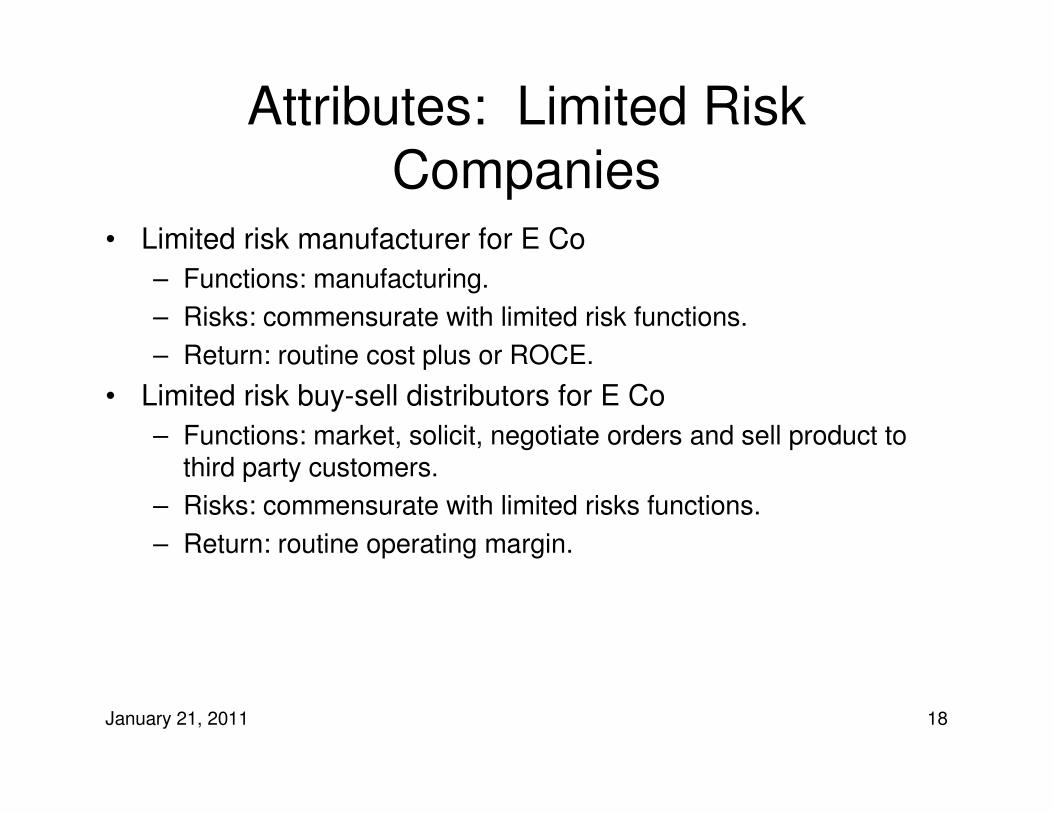

Attributes: Limited Risk

Companies• Limited risk manufacturer for E Co

– Functions: manufacturing.

– Risks: commensurate with limited risk functions.

– Return: routine cost plus or ROCE.

• Limited risk buy-sell distributors for E Co

– Functions: market, solicit, negotiate orders and sell product tothird party customers.

– Risks: commensurate with limited risks functions.

– Return: routine operating margin.

January 21, 2011 19

OECD Project

• On July 22, 2010, the OECD published final guidance (Final

Guidance) on business restructurings in the new Chapter IX

of the OECD Transfer Pricing Guidelines.

• Chapter IX is the culmination of the project begun in 2005.

January 21, 2011 20

Issues Considered

• Final Guidance covers four issues:

– The allocation and transfer of risks among related parties.

– Whether the internal business restructuring transaction requiresarm’s length compensation or indemnification.

– The application of transfer pricing rules to the parties post-business restructuring.

– When can a tax authority disregard a business restructuring?

January 21, 2011 21

General Comments

• Final Guidance is a consensus document endorsed by all

OECD members.

• Final Guidance is a more balanced document than the

Discussion Draft as a result of clarifications and efforts to

make the wording less subjective.

• The OECD acknowledges that a certain level of subjectivity is

inevitable in transfer pricing determinations.

January 21, 2011 22

Arm's Length Compensation

for Business Restructuring• Central Issue:

– Is there a transfer of “something of value” (rights or assets) or a termination or substantial renegotiation of existing arrangements?

– Would that transfer, termination or substantial renegotiation have been compensated between independent enterprises in comparable circumstances?

• Transfer → Compensation

• Termination → Indemnification

January 21, 2011 23

Arm's Length Compensation

for Business Restructuring• Arm’s length principle does not require compensation for a

mere decrease in the expectation of an entity’s future profit.

• No presumption that all contract terminations or substantial

renegotiations should be indemnified at arm’s length.

• “Profit potential” should not be interpreted as the profit or loss that would occur if the pre-restructuring arrangement would

continue indefinitely.

– Profit potential refers to expected future profits.

– Profit potential is not a right or an asset per se.

January 21, 2011 24

Arm’s Length Compensation

for Business Restructurings• OECD does not agree with the suggestion that compensation would

be provided only with regard to transfers of narrowly defined property interests.

• Rather, the OECD uses the phrase “a transfer of something of value,” which is vague and broad.

– Final Guidance expands on circumstances where a transfer of going concern may arise, viz., it is necessary to have transferred a functioning integrated business unit (i.e., a transfer of assets bundled with the ability to perform certain functions and bear certain risks).

– No guidance is provided on workforce in place.

• Final Guidance does not deal with whether compensation that would be paid at arm’s length constitutes a taxable event.

• Potential conflict with legal and accounting treatment where no discernable asset transfer can be identified (despite recognition of taxable event).

January 21, 2011 25

Arm’s Length Compensation

for Business Restructurings• Final Guidance clarifies that rights under commercial

legislation and case law should be a relevant consideration,

but not the only one, in determining whether indemnification should be provided in connection with a restructuring under

the arm’s length principle.

January 21, 2011 26

Arm’s Length Compensation

for Business Restructurings• Indemnification concept only relates to:

– Compensation for detriments suffered by restructured entity (restructuring or reconversion costs and/or loss of profit potential).

– Relevance of financial risk borne by restructured entity upon investment made for assessing whether the terms of the arrangement are arm’s length.

January 21, 2011 27

Options Realistically Available

• Concept plays a key role in Final Guidance.

• The concept has its most important application at the individual entity level (i.e., the alternatives theoretically

available to each party should be taken into account in

determining appropriate levels of compensation to be paid).

January 21, 2011 28

Options Realistically Available

• Concept has primary application in transfer pricing decisions

rather than in recharacterising transaction.

• The OECD considers that the concept is relevant in applying

the arm’s length principle to a business restructuring, although

it is not necessary to document all hypothetical options

realistically available.

• The use of hindsight is prohibited.

January 21, 2011 29

Options Realistically Available

• Commentators have suggested that the concept appears to be premised on the economic theories of opportunity cost and rational decision making.

• The concept creates tension between MNE group reasons for a business restructuring versus reasons for restructuring among the constituent MNE group members.

– No clear guidance is provided on how to resolve tension (i.e., if

individual members are compensated for the restructuring, economic

efficiency sought to be achieved may be jeopardized).

• Query, option not to restructure?

• Final Guidance seems to require that the parties to the businessrestructuring need to assess their realistically available options.

January 21, 2011 30

Allocation of Risk

• The issue is closely aligned with potential disregard of

transaction.

– Two critical factors that may lead to either TP adjustment or disregard of risk allocation are:

• Assessment on whether conduct of associated enterprises

conforms to the contractual allocation of risks.

• Assessment on whether contractual risk allocation is arm’s length.

• Analytical framework to allocate risks between associated

enterprises under Article 9, OECD Model Tax Convention,

differs from AOA developed for Article 7 profit attribution.

January 21, 2011 31

Allocation of Risk

• Risk is defined as the ability to make key decisions (see the new Example

3) and the decision to put capital at risk.

• The notion of control over risk was placed in a more limited context in the

Final Guidance, although the OECD continues to believe that the capacity

to assess the outcome of risk monitoring and risk administration is a

necessary element of controlling risk.

• Location of control over risk is an important determinant for transfer pricing

purposes.

• Discussion of financial capacity to assume risk expanded and clarified.

• Risk assumption:

– Capacity to bear consequences of risk should it materialize.

– Mechanism to cover risk.

• If purported risk bearer does not have the financial capacity to assume risk,

risk may be borne by another party.

January 21, 2011 32

Allocation of Risk

• Determination of risk allocation:

– By comparable evidence of how third parties actually divide risk(although no requirement to search for comparables).

– If no comparable evidence, then by how third parties would allocate risk.

– The absence of comparables for a particular risk allocation does not necessarily mean that it is not arm’s length.

• Determination generally made by location of control over risk

and financial capacity to bear risk, although these factors are

not intended as standard.

– OECD continues to believe that capacity to assess the outcome of risk monitoring and risk administration is a necessary element of controlling risk.

January 21, 2011 33

Allocation of Risk

• Choice of transfer pricing method for setting versus testing the

price:

– The choice of a certain TP method within a contractual relationship for setting the price of a given transaction may affect the allocation of risks and determine a low risk environment.

– However, when testing the prices, it is the risk allocation among the parties that dictates the selection of the most appropriate transfer pricing method and not the contrary.

• The Final Guidance is much less definitive on the ability of a transfer pricing policy to demonstrate the risk profile of a

transaction.

January 21, 2011 34

Allocation of Risk

• As a general rule, tax administrations should seek to address

risk allocation issues through pricing adjustments and

disregarding or modifying risk allocations in taxpayer agreements should be limited to exceptional circumstances.

– For example, where risk is in one entity and control in another entity.

– Definition of “exceptional” as rare or unusual.

January 21, 2011 35

Remuneration of Post-

Restructuring Transactions• Discussion Draft discussion was shortened substantially, due

to discussions in updated Chapters I – III.

• Fundamental Principal: Transactions among controlled

entities occurring after a business restructuring should be

governed by the same transfer pricing rules as apply to

controlled transactions that do not follow from a restructuring.

• Final Guidance retains:

– Discussion about sharing of location savings.

– Helpful transfer pricing approaches for procurement structures.

• Final Guidance has dropped the argument for use of two-

sided tests and profit splits to determine post-restructuring

transactions.

January 21, 2011 36

Documentation

• OECD believes that the preparation by taxpayers of

appropriately comprehensive and contemporaneous transfer

pricing documentation is a good practice that can assist taxpayers in their compliance efforts and assist tax

administrations in enforcing transfer pricing laws.

• Documentation requirements remain onerous for business

restructurings, but given the emphasis on written contracts, documentation is necessary.

January 21, 2011 37

Recognition of Transaction

• General Rule: MNEs are free to organise their business

operations as they see fit.

• Tax administrations have the right to determine the tax

consequences of the structure put in place by an MNE.

• Significant redrafting was undertaken in Final Discussion to clarify the material issues in order to provide a clearer

discussion of the notions of economic substance and of

commercial rationality, of the determination whether a

transaction or arrangement has an arm’s length pricing

solution, of the relevance of tax purpose and of the consequences of non-recognition of a transaction.

January 21, 2011 38

Host Country Audit Challenges

• Sham restructuring transaction.

• Transfer pricing.

• Imposition of one-time “exit taxes.”

• Permanent establishment (“PE”).

• Other.

January 21, 2011 39

Recognition of Transaction

• Transaction will be disregarded only when exceptional (i.e., in

rare or unusual circumstances).

• Exceptional circumstances:

– Substance differs from form.

– Independent parties in comparable circumstances would not have characterized or structured their affairs in a manner similar to associated enterprises and an arm’s length price can not be reliably determined.

January 21, 2011 40

Recognition of Transaction

• Recognition of the economic effects of a transaction will not

be challenged merely because:

– Third parties would not have entered into a similar transaction.

– The transaction may have been motivated by tax reasons (i.e., toachieve tax benefits).

• The transaction must be evaluated based on “commercially rational” standards.

– Use “options realistically available” standard.

– “Practically impedes” test.

January 21, 2011 41

PE Attribution

• Host countries are utilizing PE issues as a tool to circumvent the limitations that are imposed by the current OECD transfer pricing guidelines. For example, countries assert that limited risk manufacturers or distributors create dependent agent PEs of the entrepreneur in order to apply the OECD’s new profit attribution principles and thereby effectively permit tax authorities to disregard contracts and reallocate profits from the transfer of risks and assets.

• In other words, although it is possible to separate functions and risks on one hand from personnel on the other hand under a separate entity approach under Article 9 (Associated Enterprises) of the OECD Model Treaty, that is not possible under Article 7 (Business Profits).

January 21, 2011 42

Can “Crown Jewels” be Transferred Among Related Parties

• Discussion Draft supported controversial position that high

value intangibles could not be transferred.

• Final Guidance deleted “crown jewels” reference in

controversial example and adopted position that any dispute

can be addressed through pricing adjustment.

January 21, 2011 43

Effective Date

• Final Guidance does not provide an express date.

• Query, whether countries will apply Final Guidance to resolve prior business restructuring controversies?

OECD Intangibles Project

January 21, 2011 45

Why Now?

• Intangibles are central in business and often account for a

significant proportion of the market value of a company.

• Intangibles transfer pricing issues are uncertain, contentious

and difficult to resolve.

• Tax authorities globally have increased their focus on the transfer pricing aspects of intangibles.

• Guidance in OECD Transfer Pricing Guidelines (Chapter VI

and VIII) may require updating as it dates back to 1995-1998.

• The OECD Business Restructuring project identified

intangibles as a major concern.

January 21, 2011 46

OECD Timeline

• OECD requested comments on scope of project (by 9/15/10).

• OECD received almost 50 comments (see www.oecd.org/ctp/tp/intqangibles).

• OECD conducted a consultation in Paris (11/9/10).

• OECD is in process of finalizing and approving the scope of

the project at the end of January 2011; substantive discussion

commence in March 2011.

• Additional business community input will be solicited.

• It is likely that the project will result in a revision of the OECD

Transfer Pricing Guidelines.

• A discussion draft is expected by the end of 2013.

January 21, 2011 47

Issues Raised in Comments

• General Comments:

– The scope of the project.

• Issues to be considered.

• Issues that need not be considered.

– Consistency with the OECD Transfer Pricing Guidelines (Chapters I-III and IX).

– The level of documentation and compliance burdens to be imposed on taxpayers.

– The involvement of non-OECD economies and the business community.

– The format for reflecting the final output of the project; most likely a revision of the OECD Transfer Pricing Guidelines, illustrated by examples.

January 21, 2011 48

Issues Raised in Comments

• Definitional Issues:

– How should one determine that an intangible exists:

• By reference to an analytical framework or a list.

– If an analytical framework, what are the relevant characteristics: viz, that the intangible has value, is identifiable, is legally protected, is separately transferable, produces non-routine profits?

– Classification and scope of:

• Manufacturing intangibles.

• Marketing intangibles (see slide 56).

• Goodwill (see 52 & 54).

• Going concern (see slide 53 & 54).

• Soft” intangibles (see slide 57 & 58).

• Operating intangibles (see slide 55).

• Know-how.

– Interaction between intangibles and services (see slide 59).

January 21, 2011 49

Issues Raised in Comments

• Transactional Issues:

– How should intangible transfers be identified and characterized.

• Transfers of intangibles through services.

– Return from Intangibles:

• Developer.

• Legal Owner.

• Economic Owner.

• Licensee.

• R&D center.

– Cost Sharing (Cost Contribution) Arrangements:

• Platform contributions and future iterations of existing intangibles.

• Cost contribution arrangements for services.

• Cost measure.

January 21, 2011 50

Issues Raised in Comments

• Other Issues:

– Loss-making activities.

– Site closure.

– What are the implications of a transfers of an intangible to a low-tax or a high tax country.

– Arm’s length pricing vs. formulary apportionment.

– Should guidance be industry specific:

• Pharma.

• Financial services.

• E-commerce.

January 21, 2011 51

Issues Raised in Comments

• Valuation Issues:

– Type of guidance to be developed by OECD.

– The application of the “options realistically available” concept.

– Accepted valuation methods.

– Relevance of standards developed by accounting and valuation bodies?

• Financial accounting vs. transfer pricing.

– Comparability issues.

– Relevant parameters in a valuation model.

– The role, if any, of retrospective analyses (hindsight).

– Value chain analysis.

– How bundled transactions (complex intangibles; intangibles bundled

with goods and services) should be treated.

– Depreciation of intangibles.

January 21, 2011 52

Goodwill

• The element of value that inheres in the fixed and favorable

consideration of customers, arising from an established, well-

known and well-conducted business and includes every positive advantage that has been acquired by the firm in the

progress of its business, whether the business was previously

carried on, or with the name of the firm or with any other

matters carrying with it the benefit of the business.

January 21, 2011 53

Going Concern

• The amount of enhanced value associated with assets

because those assets are combined in an on-going business.

It is the result of such factors as the existence of a network of regular customers, a staff of trained employees, an

established routine for supplying goods and services, a

product line ready for sale and equipment ready for immediate

use.

January 21, 2011 54

Attributes

Goodwill and Going Concern• Goodwill is generally associated with the external competitive

position of a business in the marketplace.

• Going concern value is associated with the internal value a

business possesses by having its assets assembled in a

functioning unit.

• Significantly, goodwill and going concern represent the

residual value after all other tangibles and intangibles have

been identified and valued.

• Can these intangibles exist if there is no positive residual (and all transactions were at arm’s length)?

January 21, 2011 55

Operating Intangibles

• This encompasses IP of a type not ordinarily licensed or otherwise transferred for consideration in transactions with unrelated parties.

• These intangibles may be subdivided into three categories:

– Customer-based intangibles; i.e., any composition of market, market share, or

other value resulting from the future provision of goods or services pursuant to

contractual or other relationships in the ordinary course of business with

customers, such as customer lists or contracts to supply products.

– Supplier-based intangibles; i.e., goods or services that will be used by the

taxpayer in the ordinary course of business, such as favorable contracts for the

acquisition of components.

– Information-based intangibles; i.e., any customer-related information base

such as a list or other information with respect to current or prospective

customers, business books and records, operating systems and other

information bases. Other bases include technical manuals, training manuals, or

programs, data files, customer lists, subscription lists, lists of newspaper,

magazine, radio or TV articles.

January 21, 2011 56

Return from Intangibles

Marketing Intangibles• Query whether a high level of marketing expenditure alone is

sufficient for a distributor that does not own the trademark to obtain some interest in the trademark or other marketing intangibles?

• Where is the “bright line limit”?

• Would other factors be relevant such as the behaviour of the parties, e.g.:

– Whether the trademark owner had significant influence over marketing

expenditure;

– How marketing expenditure is spent; and

– What marketing expenditure is spent on?

• Would such marketing expenditure create an interest in the marketing intangibles where it is reimbursed indirectly, e.g., through the use of the TNMM to set transfer prices?

January 21, 2011 57

Soft Intangibles

• Query, how does one separate items which, while not

tangible, are not intangible assets?

• If such factors are not assets, or not separable assets, or

cannot be owned or transferred, they may simply be a

component of goodwill.

– For example:

• Work force in place.

• Network effects.

• Location savings.

• “Business opportunity” and “first mover advantage.” or

• Where commercial law protects a right that may not otherwise be

considered an intangible.

January 21, 2011 58

Return from Intangibles

Soft Intangibles• Experience reflects that tax authorities in a number of

jurisdictions sometimes assert a broad view of what might be

an intangible and then use that either to attempt to enforce an “exit tax,” transfer pricing adjustment or use of the profit split

method.

January 21, 2011 59

Differentiating an Intangible from

Services• Is a transaction that of a transfer of an intangible or a service?

– For example:

• Workforce in place.

• Agreement to undertake research.

• When intangibles may be associated or bundled with services?

• Examples:

– Whether a transaction which, for legal reasons, needs to be expressed

as a licence is, in economic terms, more akin to a sale of goods or

services (e.g., when certain types of software products are sold)?

– The transfer of an employee that uses intangible property in the

performance of services?

• Query, whether over time the license of an intangible can evolve to a service?

US Transfer Pricing Proposals

January 21, 2011 61

Administration’s Transfer Pricing

Proposals• Include workforce in place, goodwill, and going concern value in the

definition of intangible property for purposes of sections 482 and 367(d).

• In cases of multiple intangible property transfers, the Commissioner could combine the values of the properties on an aggregate basis to achieve a more reliable result.

• The Commissioner could also value intangible property taking into consideration the prices and profits that the controlled taxpayer could have realized by choosing a realistic alternative to the controlled transaction undertaken.

• If a US person transfers an intangible from the United States to a related controlled foreign corporation that is subject to a low foreign effective tax rate in circumstances that evidence excessive income shifting, then an amount equal to the excessive return would be treated as subpart F income in a separate foreign tax credit limitation basket.

January 21, 2011 62

Circular 230

In compliance with US Treasury Regulations, please be

advised that any tax advice given herein (or in any

attachment) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax penalties or

(ii) promoting, marketing or recommending to another person

any transaction or matter addressed herein.