Embed Size (px)

Citation preview

ITEM 3B

CURRENT STEEL MARKET

DEVELOPMENTS

Steel Committee, September 2017 Fabien Mercier, Hokuto Otsuka, Filipe Silva Emails: [email protected], [email protected]

1. Consumption

2. Production

3. Trade

4. Prices

5. Financial performance

6. Steel intensive sectors

7. Concluding remarks

2

Outline

3

Consumption

Consumption of hot-rolled steel products, major economies % change from one year earlier

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Note: Combined consumption of hot-rolled steel products of the following economies: Brazil, China, Germany, India, Japan, Korea, Russia and the United States. Consumption of hot-rolled products defined as the sum of production and net imports. Only first two months of 2017 where available.

4

Production

World crude steel production developments in 2016 and 2017

The increase of production was mostly felt in the Middle East, in Africa, in China and in Other Europe, whereas North America stagnated and the CIS production dropped.

% change, year-on-year

June 2017 2016 June 2017 2016 Jan-Jun 2017 / 2016

EU 14,237 162,145 2.8 -2.4 3.9

Other Europe 3,236 35,919 4.4 5.6 11.5

CIS 7,639 102,230 -8.0 0.8 -2.5

North America 9,662 110,624 0.2 -0.3 2.9

South America 3,412 40,220 3.4 -8.4 10.6

Africa 1,051 12,189 5.5 -4.7 11.0

Middle East 2,662 29,025 9.4 7.6 9.4

Asia, of which: 98,892 1,110,865 4.7 1.9 4.5

China 73,231 807,612 5.7 1.1 4.2

Oceania 504 5,837 -13.2 2.1 5.0

World 141,294 1,609,053 3.4 1.0 4.3

% change, year-on-yearLevel, thousand mmt

5

Trade

World exports of steel: monthly volume (mmt) and export ratio (% of production, 3-month moving averages)

A. Including intra-EU trade B. Excluding intra-EU trade

The export ratio, excluding intra-EU trade, continues to decline.

6

Prices

Margin between steel and raw materials prices

It seems that each time high margin occurs, both prices end up on a downward trend

0

200

400

600

800

1000

1200

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Margin (LHS,%) Basket (RHS) Steel (RHS) USD/tonne

7

Financial performance

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Average Quartiles 1&3 Quartile 2

0%

10%

20%

30%

40%

50%

60%

Average Quartiles 1&3 Quartile 2

Evolution of net profits between 2000 and 2016

Evolution of indebtedness between 2000 and 2016

• Real estate construction will probably not be able to prop up

steel demand, since construction indicators remain at similar

levels than during previous years.

• Car production has continued to fall in the United States, to

increase in China, and to remain flat in most of the other

markets.

• The shipbuilding sector will remain in excess capacity for the

next 15 years (OECD study: “Imbalances in the shipbuilding

industry and assessment of policy responses").

• Oil ring counts are still low, and gas and oil prices could have

reached a plateau.

8

Steel intensive sectors

• The market situation of the steel industry has improved only

modestly compared to its 2015 lows and its recovery is expected

to remain sluggish

• Industry should take advantage of this breathing space to

deleverage and restructure, to focus on quality rather than

quantity, to adapt to the digitalisation of the economy and to

address pressing environmental challenges

• Policymakers should seek to remove barriers to exit, to abstain

from direct and indirect forms of support, and to ensure that

adequate bankruptcy regulations are in place while mitigating

specific closure costs

9

Concluding remarks

10

Thank you for your attention

11

ANNEXES: steel intensive sectors

ANNEXES: steel intensive sectors

12

Steel intensive sectors

Flows to Chinese and Indian real estate: A. China (y-o-y growth rate) B. India (in million rupees)

-10%

0%

10%

20%

30%

Total Investment Planned for Real Estate Development

Investment of Real Estate, Land Acquisition Costs

Investment of Real Estate, excluding land acquisitions

0

100000

200000

300000

400000

500000

600000

700000

-20%

-10%

0%

10%

20%

30%

40%

US new building permits Japan new house started Germany building permits by m2 area

New building permits or house started in the U.S., Japan and Germany:

13

Steel intensive sectors

Car production in selected economies Units, monthly production (United States on the right side scale)

0

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

China (LHS) Japan (LHS) Germany (LHS) Korea (LHS) United States (RHS)

14

Steel intensive sectors

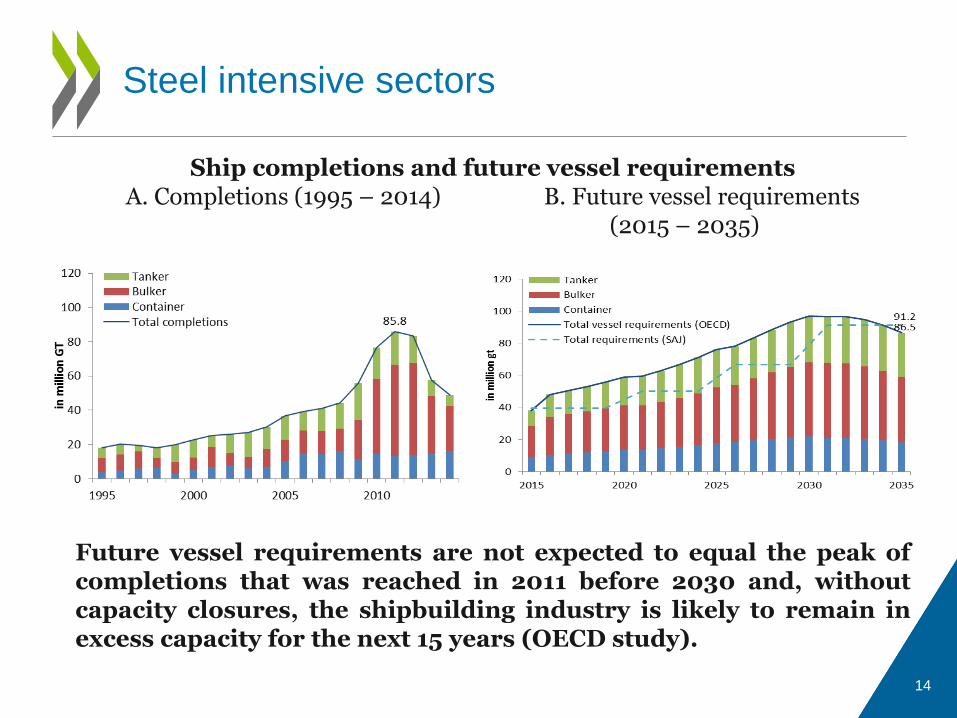

Ship completions and future vessel requirements A. Completions (1995 – 2014) B. Future vessel requirements

(2015 – 2035)

Future vessel requirements are not expected to equal the peak of completions that was reached in 2011 before 2030 and, without capacity closures, the shipbuilding industry is likely to remain in excess capacity for the next 15 years (OECD study).

15

Steel intensive sectors

Oil rig count, and oil and gas prices A. World rig count B. Oil and gas prices

0

1

2

3

4

5

6

0

20

40

60

80

100

120

Europe Brent Spot FOB, USD/Barrel (LHS)

Natural Gas, Henry Hub, USD/Million British Thermal Unit (RHS)

0

500

1000

1500

2000

2500

3000

3500

4000

US Middle East Canada Latin America

Asia Pacific Africa Europe World total