Embed Size (px)

Citation preview

1

Transfer Pricing and Customs ValuationCurrent WCO and international developments

2

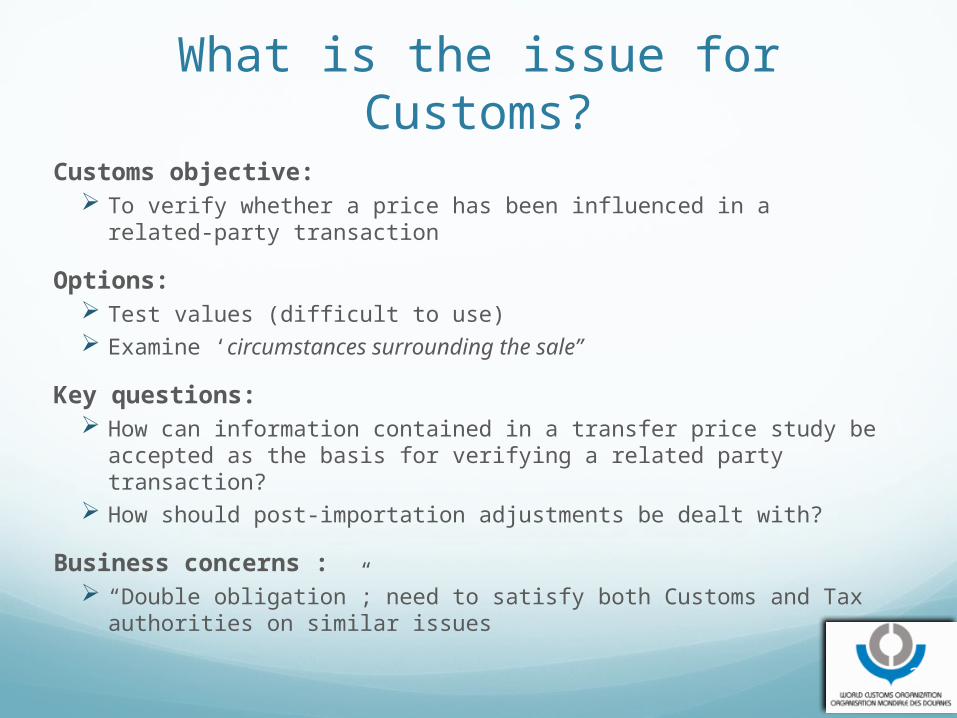

What is the issue for Customs?

Customs objective: To verify whether a price has been influenced in a related-party

transaction

Options: Test values (difficult to use) Examine ‘circumstances surrounding the sale”

Key questions: How can information contained in a transfer price study be

accepted as the basis for verifying a related party transaction? How should post-importation adjustments be dealt with?

Business concerns : “Double obligation”; need to satisfy both Customs and Tax

authorities on similar issues

3

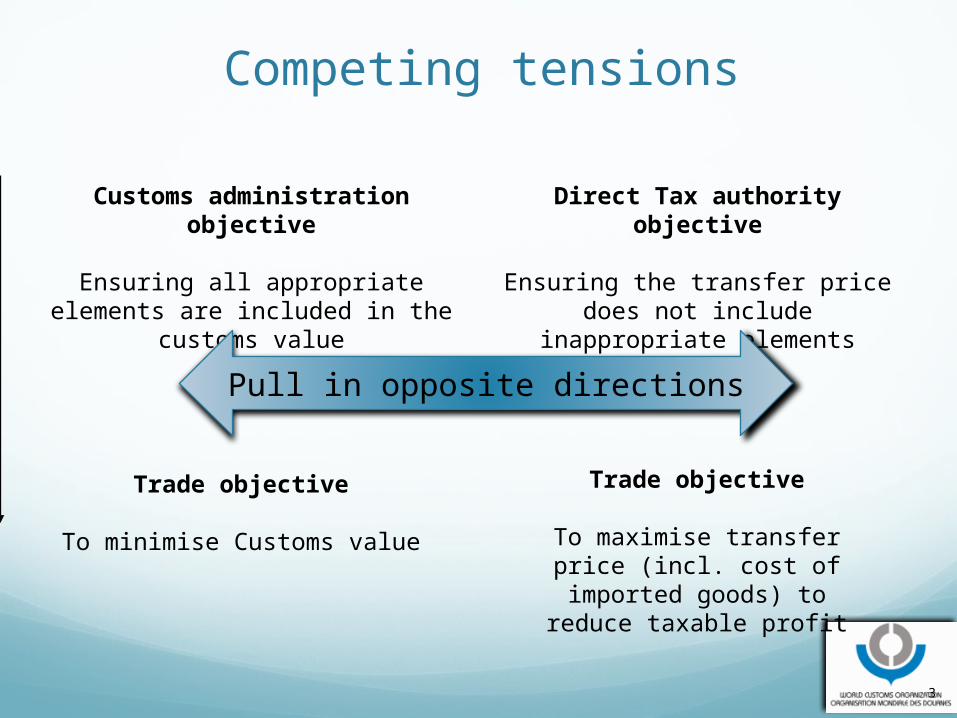

Competing tensions

Customs administration objective

Ensuring all appropriate elements are included in the

customs value

Direct Tax authority objective

Ensuring the transfer price does not include inappropriate

elements

Trade objective

To minimise Customs value

Pull in opposite directions

Trade objective

To maximise transfer price (incl. cost of imported

goods) to reduce taxable profit

4

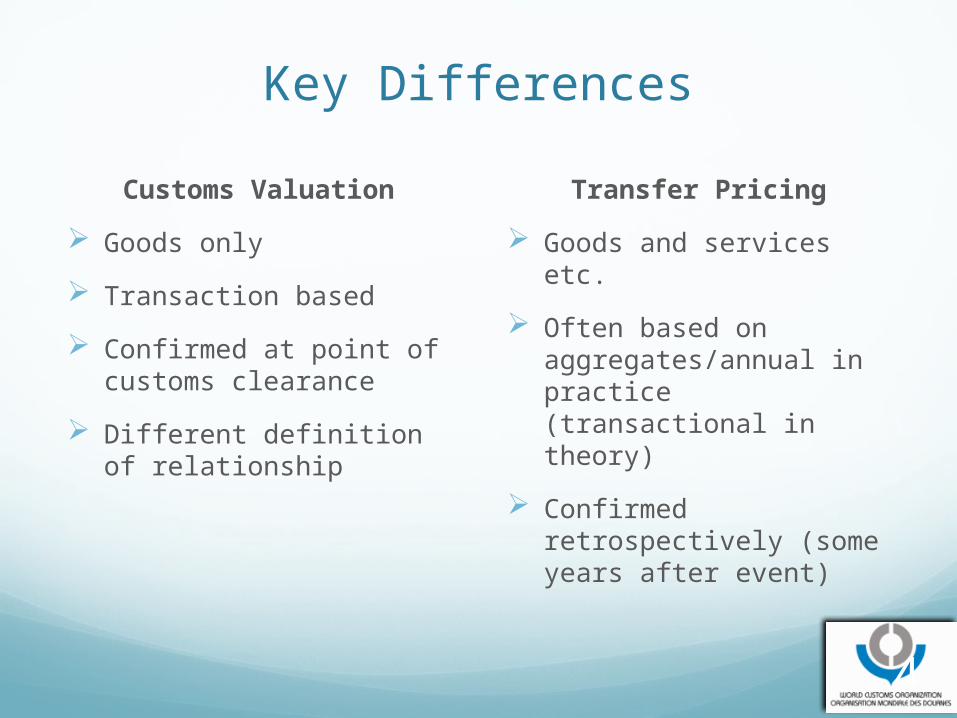

Key Differences

Customs Valuation

Goods only

Transaction based

Confirmed at point of customs clearance

Different definition of relationship

Transfer Pricing

Goods and services etc.

Often based on aggregates/annual in practice (transactional in theory)

Confirmed retrospectively (some years after event)

Activities to date Two joint WCO/OECD

conferences (2006, 2007) Full alignment not possible/

realistic

Focus Group – identified key technical issues

On agenda of TCCV Commentary 23.1 Draft case studies

WCO producing guidance material

6

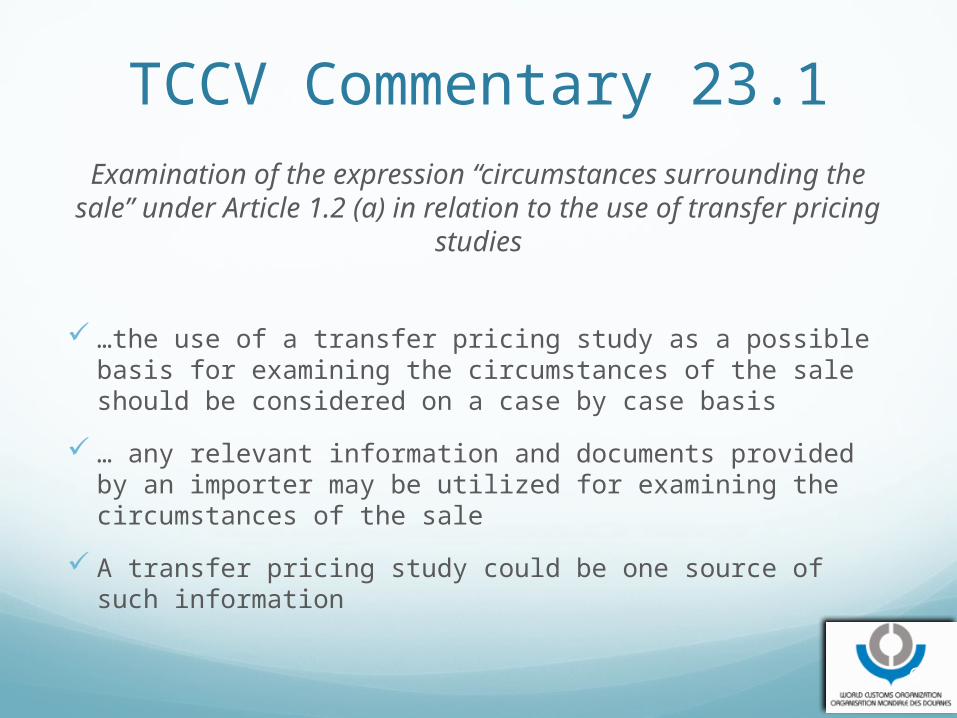

TCCV Commentary 23.1Examination of the expression “circumstances

surrounding the sale” under Article 1.2 (a) in relation to the use of transfer pricing studies

…the use of a transfer pricing study as a possible basis for examining the circumstances of the sale should be considered on a case by case basis

… any relevant information and documents provided by an importer may be utilized for examining the circumstances of the sale

A transfer pricing study could be one source of such information