Embed Size (px)

Citation preview

The AMERICAN TEXTILE INDUSTRY

• COMPETITION • STRUCTURE • FACILITIES • COSTS

By L.D. Howell

Agricultural Economist

Economic Research Service

Marketing Economics Division

Issued November 1964

UNITED STATES DEPARTMENT OF AGRICULTURE »WASHINGTON, D.C.

For sale by the Superintendent of Documents, U.S. (Jovernment Printing Office Washington, D.C, 20402 - Price 75 cents

PREFACE

This report, prepared by the Economic Research Service of U.S. Depart- ment of Agriculture, extends and brings up to date the information in Technical Bulletin 891, "Marketing and Manufacturing Margins for Textiles," published in 1945 and now out of print; Teclinical Bulletin 1062, "Marketing and Manu- facturing Service and Margins," published in 1952 and now out of print ; and Technical Bulletin 1210, "Changes in American Textile Industry—Competi- tion, Structure, Facilities, Costs," published in 1959 and now out of print. The information presented was brought up to date through 1962, or as near that date as data available in 1963 would permit.

The data were compiled mainly from secondary sources, including govern- ment and private agencies. Data made available by the Bureau of the Census, the Bureau of Labor Statistics, Federal Trade Commission, International Cotton Advisory Committee, U.S. Tariff Commission, National Association of Textile and Apparel Wholesalers, National Retail Merchants Association, Dun and Bradstreet, Inc., and National Cotton Council of America were especially useful in the preparation of this report.

Inadequate funds for publication necessitated the deletion of many tables prepared for this report. Other tables were reduced and combined. But the text is based on the tabulations before the deletions and reductions.

Credit is due Amos D. Jones for contributions to the section on marketing wool, Joseph L. Ghetti for contributions to the section on ginning cotton, and Evelina K. Southworth of the U.S. Tariff Commission for contributions to the section on manufacturing knit goods.

Contents

Pase Summary and conclusions v Competition and market outlets 1

American and foreign-grown cottons 1 American cotton and manmade fibers 2 American and foreign wool 4 American wool and manmade fibers 6 Prospects and related problems 6

Marketing channels and division of consumer's dollar 7

Cotton and cotton products 7 Marketing channels 8 Division of consumer's dollar 9

Wool and wool products 10 Marketing channels 10 Division of consumer's dollar 12

Marketing raw cotton 14 Margins in eluded in farm prices 14

Hauling from farm to gin 14 Ginning and bailing 16

Cotton merchandisers' margins 21 Receiving and related services 22 Compression of cotton 23 Storage and insurance 24 Transportation 24 Financing 25 Other services 26 Importance of reduction in costs 26

Marketing raw wool 27 Method and practices 28 Charges or costs 31 Means and importance of improvement_ 32

Yarn, except wool, and thread manufacturing 35 Nature and practices 35

Size and organizations 35 Man ufacturing methods 40 Machinery and equipment 42

Charges or costs involved 44 Means of improvement 45

Adjustments in quality 46 Improvements in manufacturing opera-

tions 48 Importan ce of improvement 51

Cotton fabric manufacturing 51 Nature and practices 51

Size and organizations 52 Man uf acturing methods 56 Machinery and equip ment 57

Charges or costs involved 58 Means and importance of improvement 63

Means of improvement 63 Importance of improvement 65

Page Wool products manufacturing 66

Nature and practices ~_ 66 Size and organization ] 67 Manufacturing methods 70 Machinery and equipment 73

Charges or costs 73 Means and importance of improvement 78

Adjustments in quality 78 Improvements in manufacturing opera-

tions 80 Manmade fiber and silk product manufacturingj.. 81

Nature and practices 81 Size and organization 82 Manufacturing methods 84 Machinery and equipment 84

Charges or costs involved 85 Means and importance of improvement 89

Dyeing and finishing 89 Nature and practices "__ 90

Size and organization 91 Methods and practices [ 93 Machinery and equipment ^__ 94

Charges or costs involved 94 Means and importance of improvement 95

Knit-goods manufacturing 95 Nature and practices 95

Size and organization 96 Manufacturing methods '_ 100 Machinery and equipment ~ 101

Charges or costs involved 102 Means and importance of improvement """"" IQ^

Manufacturing fabricated products 105 Nature and practices 106

Size and organization 106 Manufacturing methods __l no Machinery and equipment I 112'

Charges or costs involved '_ 114 Means and importance of improvement 118

Wholesaling textile products 121 Partially manufactured products IIIIII 121

Methods and practices 121 Charges or costs involved ~_ 122 Means and importance of improvement.. 124

Products for ultimate consumers 125 Methods and practices 125 Charges or costs involved ~_ 127 Means and importance of improvement ~ 130

Retailing textile products 132 Methods and practices "IIIII 132 Charges or costs involved HI 135 Means and importance of improvement ~~~ 140

Literature cited 143

HI

SUMMARY AND CONCLUSIONS

Cotton and wool produced in the United States continue to be confronted by greatly increased competition from other fibers. Expandmg pro- duction of foreign-grown cotton and wool and of manmade fibers, improvements in the quality or suitability of these fibers, and availability of m- creased quantities of the competing products at attractive prices are among the factors that ad- versely affect market outlets for American cotton and wool.

Trends in this competition are indicated by changes in supplies, prices, and consumption of competing products. The proportion of total world production of cotton, wool, and manmade fibers accounted for by American cotton decreased from more than one-half in the early 1930's to about one-fifth in the early 1960-s. The corre- sponding proportion for domestic wool decreased from 1.4 percent to 0.4 percent; whereas that for manmade fibers increased from less than 5 per- cent to more than 25 percent during this period.

Prices of American ^ cotton and wool in the United States in most of the recent years have been maintained above their normal free-market relationship to comparable prices in other coun- tries, as a result of price-support programs for cotton and import tariffs on apparel wool. Prices of manmade fibers have declined in relation to domestic prices of cotton and wool. Prices of rayon staple fiber in cotton equivalent pounds, for example, declined from more than twice those of Middling 1%6-inch cotton during the late 1930's to 10 percent lower than those in the early 1950's and to 27 percent lower than those in 1962. Prices of rayon staple fibers, as proportions of domestic prices of Fine Good French Combing and Staple wool, declined from about 36 percent in the late 1930's to 20 percent in 1954, and amounted to 21 percent in 1962. Prices of other manmade fibers, particularly the newer noncellulosic ones, declined relatively more during the 1950's and early 1960's than did those of rayon.

Changes in price relationships were associated with substantial increases in the consumption of foreign-grown cotton and wool and manmade fibers in relation to consumption of American cot- ton and wool. The proportion of total world mill consumption of cotton accounted for by American cotton decreased from more than one-half during the early 1930's to less than a third in the early

^The terms "American cotton" and "American wool" or "domestic wool" are used to designate cotton or wool produced in the United States.

1960's. Annual mill consumption of wool in the United States decreased from 17 percent of the world total during the late 1930's to 13 percent m 1962. U.S. consumption of manmade fibers in- creased from about 23 percent of that for cotton, and 151 percent of that for wool, in 1947 to 58 percent of that for cotton, and to more than 5 times that for wool, in 1962.

Inroads made on market outlets for Ameri- can cotton and wool indicate that the threat of increased competition is serious and that it is be- coming progressively more so. These develop- ments and prospects emphasize the importance of exploring alternative means of strengthening the competitive position of American cotton and wool

Prospective demands for textiles indicate the possibility of maintaining or expanding consump- tion of American cotton and wool, if all potential market outlets are fully exploited. To exploit these outlets fully would require that adequate and dependable supplies of suitable qualities of cotton and wool and their products be made readily available to consumers at attractive prices. To meet these requirements, improvements are needed in the adequacy and efficiency of the serv- ices involved at each stage in producing and mar- keting cotton and wool and in manufacturing and distributing the products.

Data on margins for marketing textiles sup- ply a basis for evaluating problems involved in reducing costs and in expanding market outlets. These margins cover charges made for assembling a.nd merchandising raw cotton and wool, manu- facturing these products into yams and fabrics, fabricating apparel and household textiles, and distributing the finished products to ultimate con- sumers. Combined margins for these services for cotton products decreased from about 91 percent of the consumer's dollar in 1938 to about 82 per- cent in 1951, and amounted to about 85 percent in 1962. Similar margins for wool products de- creased from about 90 percent in 1938 to 75 per- cent in 1951, and amounted to about 88 percent in 1962. These margins tended to increase from the early 1950's to the early 1960's.

The size of these margins emphasizes the importance of information to show the distribu- tion of the consumer's dollar among important services and cost items. Estimates, based on of- ficial data and other information, were made to

"" Italic figures in parentheses refer to items in Litera- tiie Cited, p. 143.

IV

show average distribution of the consumer's dollar paid for textile products in 1939, 1947, 1954,1958, and 1962. Data available for this purpose are not complete, and some adjustments were required in making these estimates. Furthermore, the com- bined margins for the different services were ad- justed to approximate the farm-to-retail price spread, as calculated by the Economic Research Service of the U.S. Department of Agriculture.

The farmer's share of the consumer's dollar paid for apparel and household textiles made of cotton increased, with advances in prices, from about 9 percent in 1938 to 18 percent in 1951, and amounted to 15 percent in 1962. The farmer's share of the consumer's dollar paid for textiles made of wool increased from 10 percent in 1938 to 25 percent in 1951, and amounted to about 12 percent in 1962. Gross margins for merchandis- ing the raw fibers, including ginning and baling for cotton, but not including the scouring of wool, increased in recent years and averaged about 3 percent of the consumer's dollar in the early 1960's. Combined gross margins for spinning yarns, weav- ing fabrics, and dyeing and finishing cotton cloth decreased in recent years and averaged 12 percent of the consumer's dollar in 1962. The correspond- ing proportion for manufacturers of wool fabrics varied irregularly and amounted to 14 percent in 1962. Similar proportions for fabricators oí ap- parel and household textiles increased in recent years, and amounted to about 30 and 31 percent respectively for cotton and wool in 1962. Mar- g;ins for w^holesale and retail distribution of tex- tile products have increased since 1947 and in 1962 averaged about 41 percent of the consumer's dollar.

Marketing margins for raw cotton increased from about 2.5 cents a pound of lint in 1939 to 7.2 cents in 1962. Charges for ginning and baling increased from about 0.8 cent a pound of lint in 1939 to 3.2 cents in 1962. Charges for other mer- chandising services increased from about 1.7 cents a pound in 1939 to 4.1 cents in 1962. The propor- tion of total cost of cotton to mills accounted for by these margins decreased from about 23 percent in 1939 to 12 percent in 1947, and then increased to about 20 percent in 1962.

Means of improving the marketing of cotton include (1) more general use of suitable condition- ing, cleaning, and ginning equipment, well orga- nized and operated; (2) utilization of this equip- ment to nearer full capacity for a longer time each year; (3) development and use of suitable auto- matic samplers and higher density presses at gins; (4) increased use of improved facilities and equip- ment for handling cotton at compresses and ware- houses ; (5) improved bagging and handling prac- tices for bales to reduce waste and contamination of lint; and (6) development of more adequate and dependable classification and market informa- tion services, upon the basis of which the sale and purchase of cotton on description can be expanded.

Marketing margins for wool in 1946 averaged 5.7 cents a pound, or about 12 percent of the Boston price, for grease wool in original bags; 6.8 cents a pound, or 16 percent of the Boston price, for graded wool bought in the grease; and 27.1 cents a pound, or 25 percent of the Boston price, for scoured wool. Data for more recent years indicate that charges for handling, grading, and trans- portation increased considerably from 1946 to the middle 1950's. They were reduced somewhat by the early 1960's. Apparently charges for scour- ing and carbonizing during the late 1950's and early 1960's were low^er than they were in 1946.

Means of improving the marketing of wool include (1) more and improved preparation of wool for marketing and manufacture at or near points of origin; (2) increased use of improved facilities and equipment for handling, preparing, and storing wool at warehouses; (3) improved packaging of wool, including use of suitable bag- ging to prevent contamination and waste, and compressing into suitable bales to facilitate han- dling, transportation, and storage; and (4) devel- opment of more adequate and dependable classi- fication and market information services, upon the basis of which the sale and purchase of wool on description can be expanded.

Adequate classification and market informa- tion services for cotton and wool would require (1) that differences in all important quality ele- ments of these fibers be ascertained and evaluated ; (2) that the sample used be truly representative of the quality or qualities of fibers included in the bale or lot and that it be correctly identified with the bale or lot from which it was taken; (3) that the evaluations be in accordance with uniform standards upon the basis of which differences in all iniportant quality elements of the fibers can be described for commercial purposes with reason- able accuracy; (4) that the evaluations be made by competent and reliable classifiers under condi- tions conducive to accurate evaluations; and (5) that facilities be provided for assembling the samples, recording the evaluations on convenient forms, and making this information available in time for its use in selling and buying the cotton and wool.

Mergers and acquisitions in the textile in- dustry in recent years have changed the organiza- tion and management of many operating units. These changes were associated with some decrease in average size of textile manufacturing establish- ments as measured by the number of employees. Census data for 1958 show that 34 percent of the weaving mills processing cotton and manmade fibers, with 11 percent of the looms, did weaving only. About 53 percent of the mills with 74 per- cent of the looms and 83 percent of the spindles had spinning and weaving machinery or throwing, spinning, and weaving machinery. About 13 per- cent of the mills with 15 percent of the looms and 17 percent of the spinning spindles had weaving

and finishing or spinning, weaving, and finishing machinery. In wool manufacture in 1958, about 78 percent of the mills with 79 percent of the looms had equipment for both spinning and weaving. A comparison of these data for both cotton and wool with similar data for 1954 shows a consider- able increase in vertical integration, a combination of two or more successive stages.

Gross margins of manufacturers of yarns and fabrics, as proportions of the wholesale value of the products, decreased, on the average, from 1947 to 1958, but the changes varied considerably from one type of product to another. With ad- vances in wage rates and other developments, the proportion of these margins accounted for by sal- aries and wages in 1958 averaged higher for cotton and wool products and lower for manmade fiber products than in 1947. Average value added by manufacture per dollar of payroll decreased from 1947 to 1954, despite substantial improvements in plants and equipment, and then increased to 1962.

Improvements in the manufacture of textile yarns and fabrics may result from using the qualities of raw materials relatively best adapted, physically and economically, to the production of specified products, and from modernizing equip- ment and manufacturing operations. Better ad- justments in qualities of cotton and wool used, for example, could be based on detailed analysis of mill operations, under controlled conditions, to show differences in value, for mill purposes, of cotton and wool of different qualities but physically usable in the production of specified products. Differences in value for mill purposes are made up of a combination of differences in processing costs and in quality or value of the products as a result of differences in quality of the cotton or wool used. Data showing such differences in value for mill purposes, along with data showing differences in the cost of cotton or wool as a result of differ- ences in quality, would need to be taken into ac- count in determining the quality of cotton or wool relatively best adapted to the production of speci- fied products.

A basic requirement for determining the qualities of cotton and wool relatively best adapted to the production of specified products is that differences in all important quality elements of cotton and wool be ascertained and evaluated. Techniques and equipment would need to be devel- oped for accurately measuring differences in these quality elements, and in the quality or value of the products, and for relating differences in these quality elements of cotton and wool to differences in processing performance and in quality or value of the products. Considerable progress has been made in developing techniques for measuring dif- ferences in some properties of cotton and wool fibers, but at least some of the known quality fac- tors need to be more accurately measured and eval- uated, and perhaps other important ones need to be identified, measured, and evaluated.

Adjustments in quality of cotton and wool to mill requirements would need to be based on more complete information than is now available to show not only the influence of differences in the various quality elements of the fibers on their value for use in the manufacture of specified products but also the influence of these differences on costs of raw fibers to mills, on costs of producing the cotton and wool, and on prices to farm producers. When reasonably complete and integrated, such information would supply a basis for arriving at approximations to the best adjustments in the qual- ity of cotton and wool to mill requirements. But developments in technology, in farm production, in marketing, and in other factors may result in considerable changes in qualities of cotton and wool that are relatively best adapted to the produc- tion of specified products.

Improvements in manufacturing operations have been made in recent years, but further mod- ernization is greatly needed. A report in 1958 indicated that during the 10-year period, 1948-57, the textile industry spent $4.4 billion for new plants and equipment, and productivity per man- hour rose 67 percent. Yet it was estimated that fully 65 percent of the textile manufacturing equipment was obsolete in 1957. Of the textile manufacturers who were replacing old facilities with new plant and equipment in 1958, 37 percent expected these replacement expenditures to pay for themselves in 1 or 2 years, 47 percent in 3 to 5 years, and 16 percent in 6 or more years (^^). A report in 1958 on operating costs in the textile in- dustry indicated that labor costs to mills can be cut as much as 80 percent in opening and picking, 10 to 33 percent m carding, 75 to 80 percent in drawing, 60 to 70 percent in roving, 40 to 60 per- cent in spinning, 65 to 70 percent in slashing, 30 percent in weaving, and 50 to 75 percent in man- ufacturing knit goods (63), A foUowup report in 1961 emphasized the continuing need for further improvements and pointed out specific means that have been and are being developed to greatly in- crease the efficiency of the manufacturing opera- tions (i).

Research in the carded cotton yarn industry in 1950 also indicated possibilities for substantial improvements, particularly in labor costs. Pos- sible reductions in costs in individual establish- ments ranged up to 60 percent in labor costs and up to 40 percent in total manufacturing costs. The more promising improvements included use of new and modern machinery, especially opening and picking equipment, long-draft fly frames, and larger long-draft package spinning machines; some rearrangement of machinery in most of the buildings then in use; installation of evaporative cooling systems, including more modern humidi- fying systems and better lighting equipment; in- creased machine assignment per man; an equal- ization of reasonable workloads as determined by competent specialists; and adjustments in size of mills and in number of counts of yarn spun (105).

VI

Similar information is needed for other im- portant segments of the textile manufacturing industry as a basis for indicating the means by which and the extent to which it would be feasible to increase efficiency and reduce costs of manufac- turing operations. Eeports indicate that results of similar studies of other segments of the textile industry are likely to present an even more star- tling picture than those presented for manufac- turers of carded cotton yarn {93). Case studies and other developments reported in 1958 and 1961 confirm the need for, and possibilities of, further improvements {63^ 1), A report in 1961 indicated that much of the textile machinery in place in 1960 was installed prior to 1940 and less than one-fourth was installed since 1950 {1), This situation apparently indicates that economic ap- plications are lagging far behind technological developments in the textile manufacturing indus- try. Manufacturing costs are therefore substan- tially higher than they would be if technological developments were fully utilized.

Integration in industries manufacturing ap- parel and related products in recent years has resulted in some changes in organization and management of operating units. Changes in de- gree of vertical integration are indicated by increases in the proportion of the establishments, employees, and value added by manufacture ac- counted for by multi-industry companies engaged in different segments of the textile industry. Changes in degree of horizontal concentration, on a company basis, from 1947 to 1958 showed in- creases in 12 industries, decreases in 6 industries, and no changes in 3 industries. Average value added by manufacture per dollar of payroll in 1954 and 1958 varied directly with degree of verti- cal and horizontal integration in both the men's and boys' and the women's and children's clothing industries {10).

Gross margins for manufacturers of apparel and other fabricated textile products increased from about 48 percent of the value of the products in 1939 to about 57 percent in 1958. These pro- portions varied considerably from one kind of product to another. The proportion of gross mar- gins accounted for by costs of wages decreased from 40 percent in 1939 to 36 percent in 1947, and amounted to 37 percent in 1958. Average value added by manufacture per dollar of wages de- creased from $1.76 in 1947 to $1.61 in 1954, despite substantial improvements in machinery used, in- creased to $2.24 in 1961, and amounted to $2.21 in 1962.

Improvements in the manufacture of apparel and related products might well include more attractive styling and good construction of prod- ucts, installation and use of modern facilities and equipment, adjustments in sizes of plants to facil- itate effective use of the more efficient equipment and methods, and development of labor-relations programs that would enlist the cooperation of both

labor and management in formulating and carry- ing out plans to modernize establishments for effi- cient operation. Modernization of plants might well be supplemented by in-service training pro- grams for improving the skill of employees. Uti- lization of employees to their full potentialities, to the mutual benefit of employees and management, may be an effective means of reducing costs of manufacturing and distributing textile products.

Combining two or more of the successive links in the chain of manufacturing and dis- tributing processes for textile products may be an important means of achieving economies and a closer linkage between production planning and ultimate consumer requirements. Developments during World War II were favorable in some respects to the extension of unified control. Inte- gration in the textile industry in the 1950's and early 1960's apparently indicates a continuing and perhaps growing interest in possibilities of further combinations. But additional informa- tion relating to economic possibilities of and limi- tations to both horizontal and vertical integration is needed as a basis for adequate appraisals.

Gross margins of textile and apparel whole- salers increased in recent years and averaged about 17 percent of net sales in 1962, compared with 16 percent in 1939 and a high of almost 19 percent m the early 1940's. Operating expenses of these wholesalers averaged about 15 percent of net sales in 1962, about the same as in other recent years but higher than in the late 1940's and early 1950's. Expenses of manufacturers' sales branches and offices also increased, and averaged 9 percent of net sales in 1958. These expenses per dollar of sales usually average less for estab- lishments with a large volume of sales than for those with a small volume. Selling and adminis- trative expenses account for most of the whole- salers' gross margins. Profits during the 1950's and early 1960's averaged less than 2 percent of net sales.

Gross margins of department stores averaged 36.1 percent of net sales in 1962, slightly lower than in other recent years, but somewhat above the low point of 35.2 percent reached in 1949. Payroll expenses, the largest item of costs, aver- aged 18.1 percent of net sales in 1962, about the same as in other recent years, but somewhat higher than the low point of 15.4 percent reached in 1945. Operating profits, amounting to 2.4 per- cent of net sales in 1962, were lower than those in the 5 years immediately preceding this period and were lower than in any other recent year. Gross margins of men's and boys' clothing and furnishing stores, women's and children's cloth- ing stores, and family clothing stores average considerably less than those of department stores.

Means of reducing costs of distributing tex- tile products include methods for increasing the general efficiency of existing agencies, concen- trating services in the hands of agencies or com-

Vll

binations of agencies that can perform them most efficiently, and reducing "unnecessary" services. Improvements in general efficiency of the agencies involve problems of organization and operation, selection and management of personnel, loca- tion of places of business, number and kinds of commodities handled, volume of operations, and purchase and sales policies, among others. De- tailed information on the influences of each im- portant factor on efficiency and costs is needed to indicate the extent to which and the most effective means by which it would be feasible to bring about improvements. Research of the type indicated for carded cotton yarn, with appropriate modifica- tions, should supply the information needed {105).

Wholesalers^ gross margins may be reduced by increasing to more nearly optimum the vol- umes handled by the smaller operators and by concentrating a larger proportion of the services in the hands of the larger and more efficient estab- lishments. In 1958, operating expenses per dol- lar of net sales of apparel by merchant wholesalers averaged about half as much for operators with annual sales of over $2 million as for those with annual sales of less than $50,000. Although factors other than size may also be involved, it appears likely that at least a part of these dif- ferences in operating expenses is attributable to differences in efficiency that arise from differences in volume of sales.

Retailers' margins may be reduced by simpli- fying the selling process so as to permit and encourage self-selection and self-service by cus- tomers. This simplification may be facilitated by open display of merchandise, arranged on the basis of consumers' primary interests, and by ar-

rangements for payment at a convenient desk set up for that purpose. Such simplification makes possible reductions in retail margins mainly by reducing payroll costs, which average more than half of the total operating expenses of retailers. Accurate labeling to show the quality and size of the products, on the basis of adequate standards, would facilitate self-service methods. These and other economies in retailing would make possible substantial reductions in costs of distributing tex- tile products. These reductions would be to the advantage of farm producers and consumers.

The relative importance, from the viewpoint of costs, of increasing efficiency and of reduc- ing the margins for manufacturing and distrib- uting textile products may be indicated by data showing that a reduction of 10 percent in these combined margins during 1939, 1947, 1954, 1958, and 1962 would have amounted to about 8.5 per- cent of the costs of the finished products to ulti- mate consumers, to about two-thirds of the gross returns to farmers for the cotton and wool used, and to about three times the total costs of market- ing the raw fibers, including the ginning and baling of cotton but excluding the scouring of wool. A reduction of 10 percent in costs of man- ufacturing textiles, including the fabrication of apparel and household textiles, would have amounted to about a third of the gross returns to farmers for the cotton and wool used and substan- tially more than the total costs of marketing the raw fibers. A reduction of 10 percent in costs of retailing during this period would have amounted to more than total costs of marketing the raw fibers used and to more than a fourth of the gross returns to farmers for the cotton and wool used.

Vlll

THE AMERICAN TEXTILE INDUSTRY COMPETITION—STRUCTURE—FACILITIES—COSTS

By

L. D. HowELL, Agricultural Economist, Marketing Economics Division, Economic Research Service

COMPETITION AND MARKET OUTLETS

Market outlets for American cotton and wool continue to be adversely affected by greatly in- creased competition from cotton and wool pro- duced in other countries and from manmade fibers produced in the United States and abroad. Con- tinuing increases in production of foreign-grown cotton and wool and of manmade fibers, improve- ments in the quality or suitability of these fibers, and the availability of these competing products at attractive prices are among the factors that adversely affect market outlets for American cotton and wool.

Trends in the nature and extent of this competi- tion are indicated by data showing recent changes in supplies, prices, and consumption of these com- peting products. Data are presented on changes in supplies, prices, and consumption of American cotton in relation to those for foreign-grown cot- ton and for manmade fibers; on similar changes for wool produced in the United States in relation to those for foreign wool and for manmade fibers ; and on prospects and related problems.

American and Foreign-Grown Cotton The proportion of world production of cotton

accounted for by production in the United States- has decreased markedly in recent years (table 1). During the 5 years ended wâth 1932, cotton pro- duced in the United States accounted for about 57 percent of the world total. Following inaugu- ration of the agricultural adjustment program in this country in the early 1930's, production of cot- ton in the United States was reduced, but that in other countries continued to increase and, during the 5 years ended with 1939, cotton produced in the United States accounted for only about 44 per- cent of the world total. Production of cotton in the United States and in other countries decreased during World War II and then increased in the early postwar period. During the 5 years ended with 1952, cotton produced in the United States accounted for about 45 percent of the world total. Production of cotton in this country decreased

from 16.4 million bales in 1953 to 10.9 million in 1957, and then increased to 14.9 million in 1962; but that in other countries continued to increase with the result that during the 5 years ended with 1962 cotton produced in the United States ac- counted for only about 30 percent of the world total.

Prices of American cotton in the United States in most of the years since 1933 have been main- tained above the normal free-market relationship with those of other countries, as a result of price- support operations. These differences in relative prices, except as offset by export payments; short- ages of dollar exchange; and other developments have resulted in considerable shifts in foreign con- sumption from American to cotton of other growths {4S). During the 5 years ended with July 1932, American cotton accounted for 56 percent of total world mill consumption of all growths and for about 42 percent of mill consumption out- side the United States. During the 5 years ended July 1939, after initiation of price-support loan and agricultural adjustment programs in the United States in 1933, American cotton accounted for about 42 percent of total world mill consump- tion of all growths and for about 25 percent of mill consumption outside the United States.

During and after World War II, the adverse effects of differences between prices of American cotton and of foreign-grown cottons, shortages of foreign exchange, and other factors related to for- eign outlets for American cotton have been offset to some extent by financial aid from the U.S. Govern- ment for exports of American cotton. These aids include (1) grants, gifts, and sales for local cur- rency; (2) short-term credit sales repayable in dollars; (3) barter transactions; and (4) export subsidies or payments (60).

From 1945 to 1951, domestic prices of American cotton averaged substantially more than the gov- ernment loan rate. Financial aids for cotton ex- ports averaged 44 percent of the value of American cotton exported, and American cotton accounted for about 45 percent of total world mill consump-

r86-S0'6—64-

TABLE 1.—World production of cotton^ wool^ and manmade fibers^ 193^-38 and 1938-62

Year

Cotton 2 Wools Manmade fibers *

Ameri- All Total Domes- Foreign Total Rayon, All Total can other tic acetate other

Million Million Million Million Million Million Million Million Million pounds pounds pounds pounds pounds pounds pounds pounds pounds 6,146 7,805 13, 951 207 2,021 2,228 1,401 0 1,401 5, 554 15, 216 20, 770 130 2,921 3,051 5,027 1,048 6, 075 6,974 15, 360 22, 334 140 3,082 3,222 5, 557 1,453 7,010 6,851 15, 796 22, 647 145 3,079 3,224 5,738 1,792 7,530 6,873 15, 115 21, 988 143 3, 112 3,255 5,931 2,053 7,984 7, 136 16, 274 23, 410 134 3,128 3,262 6,314 2,634 8,948

Total

Average:1934-38 1958 1959 1960 1961 1962

Average:1934-38 1958 1959 1960 1961 1962

Million pounds 17, 580 29, 896 32, 566 33, 401 33, 227 35, 620

Proportion of total

Percent 34. 9 18. 6 21.4 20. 5 20.7 20.0

Percent Percent Percent Percent Percent Percent Percent Percent 44.4 79.3 1. 2 11.5 12.7 8.0 0 8.0 50.9 69.5 .4 9.8 10. 2 16. 8 3.5 20.3 47. 2 68.6 . 4 9.5 9.9 17.0 4.5 21.5 47.3 67. 8 . 4 9.2 9. 6 17. 2 5. 4 22.6 45.5 66.2 .4 9. 4 9.8 17.8 6.2 24.0 45.7 65. 7 . 4 8.8 9.2 17.7 7.4 25. 1

Percent 100. 0 100.0 100.0 100.0 100. 0 100, 0

1 Year for cotton begins August 1; that for wool and manmade fibers January 1.

2 Commercial cotton. Excludes the quantities pro- duced for household use. Based on estimates of the

tion of all growths and for about 21 percent of total mill consumption outside the United States.

During the 7 years ended July 1958, domestic prices of American cotton averaged near the gov- ernment loan rate, government financial aids for exports averaged 60 percent of the value of Ameri- can cotton exported, and American cotton ac- counted for about 33 percent of total world mill consumption of all growths and for about 14 per- cent of mill consumption outside the United States.

Domestic prices of American cotton averaged higher than the choice B loan rate and lower than the choice A rate during the 2 years ended July 1961. They averaged near the single loan rate ap- plicable during the year ended July 1962. During these 3 years, aids for exports averaged 57 percent of the value of American cotton exported. Dur- ing the same years, American cotton accounted, on the average, for about 32 percent of total world mill consumption of cotton of all growths and for about 16 percent of mill consumption outside the United States.

Prices of cotton to manufacturers continue to be considerably higher in the United States than they are in other countries. In 1960, for example, net cotton costs per linear yard of fabric in the United States exceeded those in Japan by about 6 percent for cotton used in sheeting and print cloth and by about 14 percent for cotton used in broadcloth and gingham (tables 33 and 34, pp. 60, 61). With the costs of raw cotton, labor, and other items in other countries lower than those in the United States,

International Cotton Advisory Committee and Bureau of the Census reports.

3 From reports and publications of the Commonwealth Committee.

* From Textile Organon.

the raw cotton equivalent of U.S. imports of cot- ton products increased from 67,500 bales in 1952 to about 645,500 bales in 1962, a total increase of about 856 percent. Exports of cotton products by domestic manufacturers decreased from the equivalent of 703,900 bales of cotton in 1952 to the equivalent of 459,000 bales in 1962, a decrease of about 35 percent.

The information presented clearly indicates that cotton price-support operations m the United States have been associated with substantial in- creases in consumption of foreign-grown cotton in relation to that of American cotton. They have also been associated with large increases in im- ports of cotton products manufactured in other countries in relation to exports of cotton prod- ucts manufactured in this country. These devel- opments and prospects of further expansions in production of cotton and cotton products outside the United States emphasize the importance of exploring alternative means of strengthening the competitive position of American cotton and cot- ton products manufactured in the United States

American Cotton and Manmade Fibers

The competitive position of American cotton is also adversely affected by continuing increases in supplies and improvements in quality or suitability of manmade fibers available at reduced prices. World production of these fibers, in pounds, in- creased from about 10 percent of that for cotton in

1934-38 to 38 percent in 1962 (table 1). In the United States^ production of manmade fibers in- creased from about 4.5 percent of that for cotton in 1934-38 to 16 percent in 1947-49 and to 33 per- cent in 1962. Although no satisfactory measures of changes in quality of manmade fibers are avail- able, improvements in the quality or suitability of at least some of these fibers are generally recognized.

A pound of manmade fibers is equivalent to more than a pound of cotton for use in comparable fabrics. Adjusting these fibers to cotton equiv- alents shows that total world production of man- made fibers increased from the equivalent of about 14 percent of that for cotton in 1934-38 to 26 per- cent in 1947-49 and to 55 percent in 1962. In the United States, production of manmade fibers in- creased from the equivalent of about 7 percent of that for cotton in 1934-38 to 24 percent in 1947- 49 and to 54 percent in 1962.

Per capita consumption of cotton and manmade fibers varies widely from one contintent and coun- try to another (table 2). In most instances, per capita consumption of both fibers has increased in recent years, but usually the increases for man- made fibers were proportionally greater than those for cotton. For the world as a unit, per capita consumption of manmade fibers on a poundage basis increased from 14 percent of that for cotton in 1938 to 31 percent of that in 1959. Corresponding proportions by specified areas show increases from about 33 to 55 percent in Western Europe, from 3 to 34 percent in Eastern Europe and Russia, from about 11 to 40 percent

in North America, from 6 to 21 percent in Central and South America, from 5 to 14 percent in Asia, and from 8 to 46 percent in Africa. The propor- tions in Oceania (islands in the South Pacific, not in Asia or America, including Malaysia, Australia, and Polynesia, among others) varied irregularly from year to year (table 2).

Prices of many, if not most, manmade fibers have been reduced in recent years; whereas do- mestic prices of American cotton have been and continue to be maintained at relatively high levels as a result of loan and adjustment programs. Dur- ing the 5 years ended July 1939, equivalent prices of rayon staple fibers averaged 118 percent higher than those of Middling i%6-inch cotton, but dur- ing the 5 years ended July 1952 they averaged 12 percent lower. During the 5 years ended July 1961 they averaged 21 percent lower, and during the year ended July 1962 they averaged 28 percent lower. Similar changes occurred in the relation- ship between prices of rayon staple fibers and prices of Strict Middling li/ig-inch cotton. De- clines in prices of acetate, nylon, Dacron, Orion, and other manmade fibers during the 1950's and early 1960's were about as great as or greater than those for rayon.

The declines in prices of manmade fibers in rela- tion to domestic prices of American cotton were associated with substantial increases in mill con- sumption of these fibers in relation to consumption of cotton in the United States (table 3). Average annual mill consumption of manmade fibers in- creased from 2.7 pounds per capita in 1935-39, or the equivalent for use in comparable fabrics

TABLE 2.—Per carita consumption {net available for home icse) of cotton^ wool^ and Trmnmade fibers^ specified areas and years^ 1938-69

Item and 3^ear Western Europe

Eastern Europe

and USSR

North America

Central and

South America

Asia Africa Oceania * World

Cotton : 1938

Pounds 8.8 9.0

10.4 10.4

3.3 3.5 3.5 3.5

2.9 3.4 5.4 5.7

15. 0 15. 9 19. 3 19.6

Pon/nds 6.8 7.5

12. 1 12.3

1.3 1. 1 2.0 2.0

0.2 1. 1 3.9 4.2

8.3 9.7

18. 0 18. 5

Pounds 20.7 25.8 21.6 21. 8

2.4 4.0 2.4 2.6

2.2 7.4 9.3 8.8

25.3 37. 2 33.3 33.2

Pounds 6.4 6.6 7.1 7. 1

0.9 1.1 .9 .9

0.4 1. 1 1.7 1. 5

7.7 8.8 9.7 9. 5

Pounds 4.2 2.6 4.9 5. 1

0.2 . 1 . 2 .2

0.4 . 2 .6 .7

4.8 2.9 5. 7 6. 0

Pounds 2.4 2.4 2.4 2. 4

.2

. 2

0. 2 .2

1.4 1. 1

2.8 3.0 4.0 3.7

Pounds 8.4

10.1 9.7

10.6

2.9 7. 1 4. 2 4.4

2.9 3.3 4. 0 4.4

17. 0 20.5 17.9 19.4

Pounds 6.4 6.0 7.3 7.4

0.9 1.0 1. 0 1.0

0.9 1. 2 2. 2 2.3

8.3 8. 2

10. 5 10.7

1949 . 1958 1959__ .

Wool: 1938 1949 1958 1959 ._

Manmade fibers: 1938 1949___ 1958 1959

Total: 1938 1949 1958 1959 _

1 Includes Near East and Far East. In 1958 and 1959 Aden, Cyprus, Jordan, and Libya are also included. Adapted from reports of Food and Agriculture Organization of the United Nations.

(p. 3) of about 16 percent of that for cotton, to 9 pounds in 1948-52, or the equivalent of about 48 percent of that for cotton. In 1956-60, it increased to 10.6 pounds, or the equivalent of about 62 per- cent of that for cotton, and in 1962 to 13.1 pounds, or the equivalent of about 92 percent of that for cotton.

TABLE 3.—Mill consumption of cotton^ loool^ and mauTYiade fhers^ United States^ specified years^ 193J^-62

Cotton Wooli

Manmade fibers

Year Ray- Total on, Oth- All ace- er 2 tate

Million Million Million Million Million Million Average: pounds pounds pounds pounds pounds pounds

1934-38._ 3,090 344 283 16 299 3,733 1947 4,666 698 988 70 1,058 6,422 1958 3,867 331 1, 127 637 1, 764 5,962 1959 4,334 435 1, 252 812 2,064 6, 833 1960 4, 191 411 1,055 823 1,878 6,480 1961 4,082 412 1, 127 936 2,063 6,557 1962 4, 190 429 1,264 1,160 2,424 7,043

Proportion of total

Average: Percent Percent Percent Percent Percent Percent

1934-38-_ 82.8 9.2 7.6 .4 8.0 100.0 1947 72. 6 10. 9 15. 4 1. 1 16.5 100.0 1958 64.9 5.5 18.9 10.7 29.6 100.0 1959 63.4 6. 4 18.3 11.9 30. 2 100.0 1960 64. 7 6.3 16.3 12.7 29.0 100.0 1961 62. 2 6.3 17.2 14.3 31. 5 100.0 1962 59. 5 6. 1 17.9 16. 5 34.4 100.0

1 Apparel and carpet wool on scoured basis, as reported by Bureau of the Census.

2 Includes noncellulosic and manmade waste. Adapted from reports of Bureau of the Census and

Textile Organon.

The relationship of changes in domestic mill consumption of cotton to changes in consumption of manmade fibers also is indicated by statistical analysis of data for the years 1920-40 and 1947-52 {61). The analysis shows that after adjustments for the inñuence of other factors, a change of 1 percent in consumption of manmade fibers was as- sociated, on the average, with a change of about 0.1 percent in consumption of cotton in the op- posite direction. During the two periods, per capita consumption averaged 26 pounds of cotton and 3 pounds of manmade fibers. Taking these differences into account, it appears that a change of 1 pound in consiunption of manmade fibers was associated, on the average, with a change in the opposite direction of about 0.86 pound of cot- ton consumed. Analysis of data for the periods 1927-32, 1935-40, and 1948-60 indicates that, with other factors constant, an increase or decrease of

1 percent in domestic consumption of noncellulosic manmade fibers in cotton equivalent pounds was associated, on the average, with a decrease or in- crease respectively of about 0.14 percent of cotton consumed {32),

Changes in the proportion of manmade fibers to cotton consumed in the United States in the manufacture of specified end-use products vary considerably from one product to another (table 4). Consumption of manmade fibers in all end- use products combined, on a poundage basis, in- creased from about 9 percent of that for cotton in 1937 to about 57 percent of that in 1962. Cot- ton's competitive position apparently was rela- tively strongest in children's and infants' wear, but the proportion of the market regained since 1951 was relatively greater in women's and misses' apparel. Gains made by manmade fibers were relatively greater in industrial products and in home furnishings.

Continuing improvements in the competitive position of manmade fibers in relation to cotton in the united States may be accounted for mainly by increases in production of these fibers, improve- ments in their quality or suitability, and reduc- tions in prices of manmade fibers in relation to prices of cotton. These developments and pros- pects of further increases in production and im- provements in the quality or suitability of manmade fibers emphasize the importance of ex- ploring alternative means of strengthening Amer- ican cotton's position in competition with these fibers {IfS),

American and Foreign Wool

The proportion of world production of wool ac- counted for by the United States decreased from about 10 percent in 1934-38 to 6 percent in 1947-54 and to 4 percent in 1962 (table 1, p. 2). Produc- tion of domestic wool decreased from an annual average of about 207 million pounds, clean basis, in 1934-38 to 120 million pounds in the early 1950's, and amounted to 134 million pounds in 1962. Annual production of wool in all other countries combined increased from less than 2 bil- lion pounds, clean basis, in 1947 to more than 3 billion pounds in 1962.

Annual mill consumption of wool in the United States increased from an average of 344 million pounds, clean basis, or 17 percent of the world total, in 1934-38 to a high of 698 million pounds in the postwar period, or 29 percent of the world total in 1947, and amounted to 427 million pounds, or about 13 percent of the world total, in 1962. At least a part of the decrease indicated may be ac- counted for by relatively high prices of apparel wool in the United States, despite incentive pay- ments, associated with import tariffs on apparel wool and to increases in imports of wool products.

Prices of apparel wool in the United States have been and continue to be maintained above their free-market relationships to wool in other

countries by import tariffs. From 1930 to 1948 the import duties ranged up to 37 cents a pound, scoured basis, but since 1948 they have ranged up to 27.75 cents a pound. In addition, prior to the National Wool Act of 1954, prices of domestic wool were supported by Government loan and pur- chase programs. As a result of these price sup- ports, substantial quantities of domestic wool were

accumulated in Government stocks, while manu- facturers in the United States imported apparel wool for consumption.

Incentive payments under the provisions of the ISTational Wool Act of 1954 began in 1955, and price-support loans and purchase programs for wool were discontinued. Consequently, during the late 1950's and early 1960's, American wool com-

TABLE 4.—Fiber coTisumption in the manufacture of specified end-use products^ specified years ,1937-62'

End use and fiber 1937 1949 1959 1961 1962

Apparel : Men's and boys' :

Cotton._ _ _

Million pounds

808 210 34

Million pounds

835 168 111

Million pounds

1,091 181 167

Million pounds

1,093 154 198

Million pounds

1 1 P;Q Wool 168 Manmade_ 232

Total- ______ 1, 052 1,114 1,439 1,445 1,559

Women's and misses': Cotton 270

90 172

321 152 324

498 161 380

447 155 427

457 Wool 168

470 Manmade_

Total _ 532 797 1,039 1,029 1, 095

Children's and infants': Cotton _ _ 178

19 11

192 31 27

311 26 50

322 25 53

337 26 60

Wool Manmade

Total 208 250 387 400 423

All apparel: Cotton__ _ 1,256

519 217

1,348 351 462

1,900 368 597

1,862 334 678

1,953 362 762

Wool Manmade

Total 1,792 2, 161 2,865 2,874 3.077

Homef urnishings : Cotton- 817

162 29

759 190 79

1,055 178 431

1, Oil 157 494

1,046 159 600

Wool Manmade _

TotaL_ _ __ _ 1,008 1,028 1,664 1,662 1,805

Other consumer type Products: Cotton _ _ _ 322

25 77

400 42

146

399 24

227

375 23

242

383 22

256 Wool Manmade

Total 424 588 650 640 661

Industrial uses: Cotton __ 1,255

50 14

893 48

300

656 12

630

600 11

563

599 11

639 Wool- __ Manmade

Total 1,319

3,650 556 337

1, 241 1,298 1, 174 1, 249

All end uses: Cotton 3, 400

631 987

4, 010 582

1,885

3,848 525

1, 977

3,981 554

2,257 Wool Manmade

Total 4, 543 5, 018 6,477 6, 350 6,792

1 End-use consumption of wool shown exceeds mill consumption plus semimanufactured imports as a result of double counting.

Adapted from Textile Organon (91).

peted more effectively with imported apparel wools in domestic markets, consumption of domes- tic wool increased, imports of apparel wool for consumption decreased, and Government stocks of wool were liquidated.

Despite the discontinuance of price-support loans and purchase programs, costs of apparel wool to manufacturers in the United States con- tinue to be substantially higher than they are in other countries. In 1960, for example, net costs of wool used in the manufacture of worsted shark- skin averaged 35 percent higher in the United States than in the United Kingdom and 15 per- cent higher than in Japan (table 48, p. 75). Net costs of wool used in the manufacture of high- grade woolen flannel averaged 30 percent higher in the United States than in the United Kingdom, and similar costs of wool used in the manufacture of lower grade woolen flannel averaged 74 percent higher in the United States than in Italy (table 48, p. 75). With costs of raw wool, labor, and other items in other countries substantially lower than those in the United States, imports of manu- factured wool products into this country from 1954 to 1962 increased more than 100 percent and domestic exports of wool products decreased 22 percent.

American Wool and Manmade Fibers

Marked increases in production, improvements in quality or suitability, and reductions in prices of manmade fibers continue to adversely affect market outlets for wool as well as for cotton. World production of manmade fibers increased from about 63 percent of that for wool in 1934-38 to about the same as that for wool in 1947 and to 260 percent of that for wool in 1962 (table 1). In the United States, production of manmade fibers increased from less than twice that of wool in 1934-38 to about 7 times that of wool in 1947 and about 18 times that of wool in 1962.

Domestic prices of manmade fibers advanced less than prices of wool during the late 1940's and early 1950's, and declined less during the late 1950's and early 1960's. Prices of rayon staple fiber, for example, as proportions of prices of Fine Good French Combing and Staple wool, averaged 36 percent during the 5 years ended 1938, declined to an average of 20 percent in 1954, and amounted to 21 percent in 1962. Prices of other manmade fibers, especially the newer noncellulosic ones, such as nylon, Orion, Dacron, Acrilan, and Dynel, declined more during the late 1950's and early 1960's than did those for rayon.

Mill consumption of manmade fibers has in- creased more rapidly in recent years than that for wool. In the United States, mill consumption of manmade fibers increased from about 87 percent of that for wool in 1934-38 to more than three times that for wool in 1950-54 and to more than five times that for wool in 1962. The greatest

increases since 1950 have been in the newer non- cellulosic fibers, which apparently are more di- rectly competitive with wool for many uses than are rayon and acetate. Analysis of data for the period 1920-40 and 1948-60 mdicates that, with other factors constant, an increase or decrease of 1 percent in domestic consumption of noncellu- losic staple fibers on a wool equivalent basis was associated, on the average, with a decrease or in- crease respectively of about 0.28 percent of apparel wool consumed {S2).

World per capita consumption of wool has shown no definite trend in recent years ; whereas that for manmade fibers has increased markedly. World consumption of manmade fibers increased from about the same amount as that for wool in 1938 to more than tv/ice as much in 1959 (table 2, p. 3). Per capita consumption of both wool and manmade fibers varies widely from one con- tinent to another. In most instances, no definite trends in recent years are indicated for wool, but per capita consumption of manmade fibers on most of the continents increased markedly. Consump- tion of manmade fibers in Western Europe in- creased from 88 percent of that for wool in 1938 to 173 percent in 1959. Corresponding propor- tions for other areas show increases from. 15 to 210 percent in Eastern Europe and Russia, from 92 to 338 in North America, from 44 to 166 per- cent in Central and South America, from 200 to 350 percent in Asia, and from 100 to 550 percent in Africa. In Oceania the proportions varied ir- regularly from one year to another (table 2, p.

Changes in proportions of manmade fibers to wool consumed in the United States in the manu- facture of specified end products vary consider- ably from one product to another (table 4, p. 5). For all end-use products combined, consumption of manmade fibers increased from about 61 percent of wool consumed in 1937 to 344 percent in 1961. The competitive position of wool was relatively weakest in industrial products and was strong- est in women's and misses' apparel.

Relatively higher prices of wool than of man- made fibers and associated relatively higher costs of finished v/ool products in the United States than in other countries are accounted for, at least in part, by tariffs on apparel wool imported into this country. Changes in relative prices and in con- sumption of wool and manmade fibers and pros- pects of further increases in production and im- provements in quality or suitability of these fibers emphasize the importance of exploring alternative means of strengthening the competitive position of wool with these fibers (J^).

Prospects and Related Problems

Developments and trends outlined above clearly indicate that cotton and wool produced in the United States are confronted by greatly increased

competition as a result of (1) continuing expan- sion in production of foreign-grown cotton and wool and of manmade fibers, (2) improvements in the quality or suitability of these fibers, and (3) increased availability of the competing prod- ucts at reduced prices. With further expansion in production of competing products in prospect, inadequate market outlets for American cotton and wool at remunerative prices may continue to handicap the cotton and wool industries in this country, unless prompt and effective actions are taken to maintain or expand these outlets. Given a reasonably prosperous peacetime economy and continued increases in population, prospective deraands for textiles indicate the possibility of maintaining or expanding consumption of cotton and \Yool, if all potential market outlets are fully exploited.

To exploit fully these outlets for cotton and wool would require: (1) adequate and dependable sup- plies of suitable qualities of raw cotton and wool, readily available to manufacturers at attractive prices; (2) efficient manufacture of a variety of suitable and attractive cotton and wool yams and fabrics, appropriately finished and made available at attractive prices for use in industry and in fabricating apparel and household products; (3) suitable and attractive styling and good construc- tion of apparel and household products made of suitable cotton and wool fabrics; (4) education of consumers regarding the quality, variety, and adaptability of these products; (5) timely adjust- ments in the manufacture and distribution of these products to meet consumer requirements; and (6) increased efficiency in the entire chain of market- ing, manufacturing, and distributing procedures so that a variety of suitable and attractive products made of cotton and wool are readily available to consumers at attractive prices.

Cotton and wool compete with manmade fibers and other products as raw materials, as yams and fabrics, and as fabricated products. The effec- tiveness of this competition may be largely in- ñuenced by differences between the quality, suit- ability, and prices of cotton, wool, and their prod- ucts and the quality, suitability, and prices of competing products. Among important factors that may affect the quality, suitability, and cost of textile products at each stage of the marketing, manufacturing, and distribution procedure are (1) the size, organization, and control of the op-

erating units; (2) kind and arrangement of build- ings, machinery, and equipment used; (3) kind and effectiveness of the labor used; (4) operating methods and practices; and (5) kinds, qualities, and suitability of the materials used.

The problem of making available adequate sup- plies of suitable qualities of cotton and wool and their products at attractive prices involves consid- eration of the costs at each stage from farm pro- duction of the raw fibers to retail distribution of the finished products. The importance of market- ing services and costs may be indicated by data showing that gross margins for assembling and merchandising raw cotton and wool, manufactur- ing yarns and fabrics, fabricating apparel and household textiles, and distributing the finished products to ultimate consumers account, on the average, for about seven-eighths of the consumer's dollar paid for apparel and household textiles made of cotton and wool. It is apparent from the width of these margins that reductions in them may have important influences on returns to farm producers, on costs of finished products to ultimate consumers, and on market outlets for cotton and wool.

The size of these margins and the seriousness of the threat of increased competition from manmade fibers and other products emphasize the impor- tance of information that will show the influence of the different factors on the adequacy, efficiency, and costs of the marketing, manufacturing, and distributing services required and that will indi- cate means of improvement. Data are presented in this report to show changes in size and organiza- tion of the operating units, in machinery and equipment used, in operating methods and prac- tices, and in charges or costs for the services ren- dered at each important stage involved in taking cotton and wool from farms and delivering the finished textile products to ultimate consumers. The data presented are designed to show the rela- tive importance of these margins from the view- point of cost, to indicate some of the factors re- sponsible for or associated with differences in ade- quacy and costs of services, and to serve as a basis for suggesting feasible means of improvement.

Information on marketing channels and the division of the consumer's dollar paid for cotton and wool products is presented as a background for the more detailed data relating to specific stages of the marketing procedure.

MARKETING CHANNELS AND DIVISION OF CONSUMER S DOLLAR

The data for cotton and wool begin with the movement of these items from the farm and with prices to farmers; those for manmade fibers and related products begin with the delivery of fibers and prices paid for them by manufacturers of textile products.

Cotton and Cotton Products Taking cotton from farms and delivering it in

the form of finished clothing and household tex- tiles to ultimate consumers require the services of many different types of middlemen. They include

ginners, warehouse and compress operators, trans- portation agenices, and merchandisers of raw cotton ; manufacturers of cotton yarns and fabrics ; fabricators of cotton apparel and household tex- tiles ; and wholesale and retail distributors. These services begin w^hen seed cotton is hauled from farms to gins where such services as conditioning and cleaning of seed cotton, separating the lint from the seed, cleaning the lint cotton, and pack- ing and wrapping it into bales of approximately 500 pounds are rendered.

MARKETING CHANNELS

From the gin, cotton usually moves to ware- houses, which may be operated in connection with compresses, where it is assembled and stored. Much of the cotton, particularly in central and western areas of the Cotton Belt, is compressed to a higher density to facilitate storage and transpor- tation. From warehouses and compresses it usu- ally moves to mills by railroad or motortruck or by some combination of truck, rail, and water trans- portation. Taking cotton from gins and deliver- ing it to mills involves merchandising services such as assembling, compressing, storing, insuring, transporting, financing, and risk-bearing.

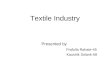

At the mill, bales are opened and the cotton is cleaned, carded, combed (for fine yarns), and spun into yarn. On the average, about 4 percent of the gross weight of the bale is tare, less than 3 percent is nonlint waste, and most of the re-

mainder, which amounts to about 93 percent, is made into yarn (fig. 1). According to census reports for 1958, for example, about 81 percent of the yarn was woven into cloth, 10 percent was used by the knit-goods industry, 3 percent was made into carpet and tufting yams, 2 percent was used in thread, and 4 percent was used in making other yarns.

Census reports indicate that in 1958 about 18 percent of the woven cloth was used in the gray or unfinished form, less than 6 percent was colored yarn fabric, and about 76 percent was finished from the gray (97). Finishing gray goods in- cludes bleaching, dyeing, and printing. Of the total linear yardage finished in 1958, about 44 per- cent was bleached and white finished, 33 percent was plain dyed and finished, and 23 percent was printed and finished. In 1962 the corresponding proportions were 44, 34, and 22 percent respec- tively (76^6^). Styling and finishing of a large part of the cotton cloth is controlled by converters (persons who take gray goods and have them finished), but substantial proportions are con- trolled by mills, with or without the coUaboration of the fabricators.

Much of the finished cloth usually goes to cut- ters, where it is made into wearing apparel and household goods. Estimates of cotton consump- tion by end uses show^ that the proportion that went into apparel increased from 36 percent in 1947 to about 54 percent in 1962; that used in

Consumed in U. S.

APPROXIMATE DISTRIBUTION OF A TYPICAL BALE OF COTTON, 1958

TARE 20 LB

WASTE

(NONLINT) 13 LB.

feiJa^^u^^ fe^^ M?nA HOUSEHOLD GOODS INDUSTRIAL USERS

U. S. DEPARTMENT OF AGRICULTURE NEC. ERS 2763-64(4) ECONOMIC RESEARCH SERVICE

Figure 1

household goods increased from 28 percent in 1947 to 29 percent in 1962 (70), The remainder went into industrial uses. Clothing and house- hold textiles usually go either directly or in- directly through wholesalers, jobbers, or other agencies, to retailers.

DIVISION OF THE CONSUMER'S DOLLAR

Charges for the many services performed in transforming raw cotton into finished cotton goods and in making them available to the consumer ac- count, in most instances, for a large share of the consumer's dollar paid for the finished products. Data on retail values of a group of 25 cotton articles of clothing and household furnishings and on receipts by farmers for equivalent quantities of cotton indicate that from 1935 to 1962 returns to farm producers for the cotton used amounted, on the average, to about 15 percent of the con- sumer's dollar. Marketing margins amounted to 85 percent of the consumer's dollar (fig. 2) (72), The proportion of the consumer's dollar repre- sented by the farm value of the cotton usually varied irregularly with prices of cotton. It ranged from about 9 percent in 1938, when farm prices of cotton averaged about 8.60 cents a pound, to 18 percent in 1951, when farm prices of cotton averaged about 38.88 cents a pound, and amounted to 15 percent in 1962, when farm prices averaged 31.80 cents a pound. From the early 1950's to

the early 1960's, the farmer's share tended to decrease.

The proportion of the consumer's dollar ac- counted for by the farm value of cotton varies widely among products. During the 10-year period, 1953-62, the proportion for clothing averaged 12 percent, and ranged from 11 percent in 1960 and 1961 to 13 percent in 1954 and 1955. For household furnishings, the proportion aver- aged 23 percent for the 10-year period and ranged from 21 percent in 1960 to 25 percent in 1954 and 1955. During the 11 years 1952-62, the farmer's share of the retail price averaged 7 percent for business shirts, 16 percent for work shirts, and 34 percent for sheets.

The large proportions of the consumer's dollar accounted for by marketing margins emphasize the importance of breakdowns to show the items included. Estimates, based on official data and other information, were made to show the average distribution of the consumer's dollar paid for cot- ton apparel and household goods in 1939, 1947, 1954, 1958, and 1962. Data available for this pur- pose are not complete, and in some instances they are not strictly comparable. Consequently, some adjustments were required in approximating margins on the basis of these data and other in- formation. Furthermore, estimated margins were adjusted to approximate the farm-to-retail price spreads for cotton clothing, household textiles.

MARGINS FOR COTTON PRODUCTS

2.40

COTTON USED ANNUALLY I PER FAMILY IN |

25 COTTON ARTICLES

' ' ' ' ' I I ' ' I I ■ ' ' I I ' I ■ I 11 I ' I ' I ' I

1940 1950 1960 1940 1950 1960 ^RETA/L VALUE OF A CROUP OF 25 COTTON CLOTHING AND HOUSEHOLD ARTICLES EQUIVALENT TO 1 LB. LINT COTTON.

^■ESTIMATED PRICES RECEIVED BY FARMERS FOR COTTON OF GRADE AND STAPLE LENGTHS REQUIRED IN THE MANUFACTURE OF VARIOUS ARTICLES.

U. S. DEPARTMENT OF AGRICULTURE NEC. ERS 2764-64(4) ECONOMIC RESEARCH SERVICE

Figure 2

9

and yard goods, as calculated by the Economic Eesearch Service, U.S. Department of Agriculture.

Approximations were made to show the average distribution of the consumer's dollar paid for these products on the basis of the specific conversions made or services rendered. Eesults show that charges for marketing services in dollars increased markedly during the 1940's. The proportion of the consumer's dollar that went to cotton growers for farm production (receipts by farmers less ginning charges) increased, on the average, from about 9 percent in 1939 to 15 percent in 1954, and then decreased to about 14 percent in 1962. The proportions accounted for by margins for ginning, baling, and merchandising raw cotton, and for wholesale and retail distribution, decreased from 1939 to 1947, and then increased to 1962. The proportions accounted for by margins for spinning yarns, weaving cloth, and dyeing and finishing fabrics decreased markedly from 1939 to 1954, and then decreased gradually to 1962. The pro- portion accounted for by margins for manufactur- ing apparel and household textiles continued to increase, and amounted to about 30 percent in 1958 and 1962 (fig. 3).

Information on specific items of cost is not com- plete, and in some instances data for the different agencies are not strictly comparable. But ap- proximations based on available information in- dicate that, of the spread between retail prices of cotton apparel and household goods and returns to growers for the cotton used, the proportion ac- counted for by wages and salaries decreased from about 53 percent in 1939 to 51 percent in 1947, and then increased to about 56 percent in 1962. The proportion of these spreads accounted for by profits increased from about 5 percent in 1939 to 16 percent in 1947, and then increased to about 6 percent in 1962. Proportions accounted for by alJ other items decreased from about 42 percent in 1939 to 32 percent in 1947, and then increased to 37 percent in 1962 (fig. 4). During the years for which estimates were made, wages and salaries of employees engaged in marketing, manufactur- ing, and distributing cotton and cotton products averaged almost four times as much as returns to growers for farm production of the cotton, and profits to these intermediate agencies averaged about half as much.

Data on the distribution of the consumer's dol- lar paid for apparel and household goods made of cotton may indicate the relative importance, from the viewpoint of costs, of increasing efficiency and reducing costs for the different services. During the years studied, margins for ginning and baling, combined with those for merchandising cotton, amounted, on the average, to less than 7 percent of the combined margins for manufacturing and finishing cloth and for fabricating it into apparel and household goods, or for wholesale and retail distribution of these products. Thus, a reduction of only 4 percent, for example, in the margins for

wholesaling and retailing, or for manufacturing and finishing cloth and fabricating it into apparel and household goods, would have reduced the spread between retail prices to consumers and prices to growers for the cotton more than a 50-percent reduction in total margins for ginning, baling, and merchandising the raw cotton.

Although these differences in size of margins are important, they may not reflect accurately the rela- tive opportunities for making savings in market- ing costs that can be passed back to cotton growers or on to consumers of the finished products. A determination of the extent to which it would be feasible to reduce these margins would require detailed studies of each important segment of the marketing, manufacturing, distribution proce- dures to evaluate the influence of the factors affect- ing the adequancy, efficiency, and costs of the services, and to discover the most feasible means of improving the adequancy and efficiency of the services and of reducing costs for the various agencies. Eesults of such studies are not available for many of the agencies, but the available in- formation on margins and costs and on means of reducing them is presented in this report in about the order in which the marketing services are rendered, beginning with movement of cotton from farms.

Wool and Wool Products Wool utilized in the United States is of two

rather distinct kinds, apparel and carpet wools. Apparel wool includes the finer fibers used mainly in the manufacture of apparel yams and fabrics. Carpet wool consists of the coarser fibers used mainly in the manufacture of carpets and rugs. In 1962, apparel wool accounted for about 65 per- cent, and carpet wool for about 35 percent, of all wool consumed by mills in the United States. All of the carpet wool and substantial proportions of the apparel wool were imported. About seven- eighths of the wool produced in the United States in 1962 was shorn wool, obtained from shearing live sheep. The remainder was pulled wool, ob- tained by pulling the wool from the skins of slaughtered sheep. Production of both kinds of wool is widely distributed throughout the United States.

MARKETING CHANNELS

Soon after sheep are shorn, fleeces are usually packed for shipment in bags weighing from. 175 to 300 pounds when filled. Some of this wool is assembled by local dealers or handlers and sold to merchants in central markets or to manufac- turers, but many growers, particularly the large producers, sell directly to merchants in central markets or to mill buyers. A large portion of the wool usually moves out of producing areas to cen- tral markets or to mills soon after it is clipped. Producers of pulled wool usually sort it into uni- form lots and put it in bags or bales which range

10

Where it Goes

THE CONSUMER'S COTTON DOLLAR, BY OPERATIONS OR SERVICES

Paid for Apparel and Household Goods, Selected Years

$1.00 ^Retailing

Wholesaling

Manuf. apparel and

► household goods

Manuf., dyeing, and finishing-

(yarns and fabrics

/AMerchandising cotton

y^Ginning and baling

Farm production

1939 1947 1954 1958 1962 BASED ON OFFICIAL AND OTHER DATA. AND PARTLY ESTIMATED.

U.S. DEPARTMENT OF AGRICULTURE NEC. ERS 2765-64 ( 4 ) ECONOMIC RESEARCH SERVICE

Figure 3

Where it Goes

THE CONSUMER'S COTTON DOLLAR, BY COST ITEMS

Paid for Apparel and Household Goods, Selected Years

I Profits '

lAll other

■ Salaries and wages

Farm production

1939 1947 1954 1958 1962 BASED ON OFFICIAL AND OTHER DATA, AND PARTLY ESTIMATED. *NET PROFITS OF ALL AGENCIES, EXCEPT FARM

PRODUCERS, AFTER DEDUCTION OF FEDERAL INCOME AND EXCESS-PROFIT TAXES. O INCLUDES DEDUCTIONS FOR FEDERAL INCOME AND EXCESS-PROFIT TAXES.

U.S. DEPARTMENT OF AGRICULTURE NEC. ERS 2766-64(4) ECONOMIC RESEARCH SERVICE

Figure 4

11

in weight from 140 to 800 pounds when filled. Much of it is sold directly to mill buyers {S6).

Most of the imported apparel wool goes to cen- tral markets, where it is handled by the same mer- chants and manufacturers who handle the wool produced in the United States. Imported carpet wool also goes directly to central markets, where it is handled by a specialized group of merchants and manufacturers, most of w4iom are located in Philadelphia.

Domestic and imported wools are assembled in warehouses, at concentration points, or in central markets, where they are sorted into lots of uniform quality and stored until needed by manufacturers. Most of the wool required by manufacturers, par- ticularly those producing w^orsted fabrics, is bought in the grease. But considerable quantities, particularly that used by woolen mills, are bought in the scoured state. This wool usually is scoured by dealers or processors.

The apparel wool manufacturing industry con- sists of two major divisions, the worsted and the woolen. Of the virgin apparel wool consumed in the United States, the worsted division ac- counted for about 66 percent in 1948 ; the propor- tion decreased to 49 percent in 1957, and then increased to 62 percent in 1962. Worsted manu- facturers sort, blend, and scour wool ; card, comb, and convert it into semimanufactured products known as tops; and spin the tops into yarn. Woolen manufacturers combine and mix the wool and other materials used, card it, and spin it into yarn without combing it and converting it into tops. If wool manufacturers do not buy the wool on a scoured basis, they have it scoured.