Embed Size (px)

Citation preview

Chapter 7 – Summary, Findings and Conclusion

335

Chapter Seven

Summary, Findings and Conclusion

Introduction

Summary

Major Findings

Recommendations

Conclusion

Chapter 7 – Summary, Findings and Conclusion

336

INTRODUCTION

Globalization and liberalization have increased the international trade and financial

transactions manifold in the recent years. It has, in turn, raised all types of risks including

market risk, liquidity risk, price risk and interest rate risk. Managing these risks has

become a major task for finance managers worldwide and it spurred financial innovations

to mitigate risks. This has led to the emergence of a class of innovative financial

instruments called „derivatives‟.

Financial derivative is a widely discussed topic in the recent years due to its

tremendous growth in terms of volume of trade, number of contracts traded and variety of

products. However the complex nature of the product, uncertainties involved in trading and

lack of knowledge about trading techniques are some of the critical issues to be solved.

Moreover house mortgage issue in U.S, fall of Lehman brothers, US recession which in

turn led to global recession, has all created a negative image to financial derivatives.

Skillful use of derivatives is essential to mitigate the loss suffered from spot market.

Hence it is necessary for anyone who handles derivatives to know the art of dealing with

derivatives in an efficient way. The process of reducing loss by efficient use of derivatives

assumes importance and is known as hedging.

This chapter provides a summary of the study and gives some recommendations

based on research findings. This chapter is subdivided into three main sections:

A) Summary

B) Major findings of the study

C) Recommendations.

Chapter 7 – Summary, Findings and Conclusion

337

A) SUMMARY

This study is an earnest attempt to understand some aspects of financial

derivatives as a hedge tool. Though financial derivatives were introduced as a hedge tool, it

is still not widely used. In spite of the measures taken by the regulatory authorities in our

country to control the volume of speculative transactions, derivatives segment remains

mostly a domain of speculators.

Statement of the Research Problem

Existing research literatures do not conclusively present the extent of hedge usage

among individual derivative traders and how far they help in mitigating the risk. Present

study is an earnest attempt to cover this research gap. Following research questions bring

the problem into sharp focus:

• Does Indian derivatives market exhibit hedge effectiveness? If so, to what extent?

• What is the extent of use of derivatives for hedging by traders?

• Is there any room for promoting hedge habits among individual traders?

Objectives

1. To assess the extent of hedge effectiveness of financial derivatives traded in India.

2. To examine the attitude of individual derivative traders towards hedge.

3. To compare the general profile, awareness level and trading beliefs of hedgers and

non-hedgers

4. To identify and evaluate the perceived problems of derivative traders.

5. To analyse the nature of influence of various intermediaries on trading decisions of

individual traders.

6. To make recommendations to improve the functioning of financial derivatives

market, if needed.

Chapter 7 – Summary, Findings and Conclusion

338

Scope and Significance of the Study

Scope of the study is limited to some selected stock and index futures. The study is

confined to the use of derivatives by individual share traders in Kerala. Though derivatives

were introduced as a risk management tool its usage for hedge purpose by individual

traders seems to be lacking. Speculative activities are gaining popularity in the derivative

segment. Hence it is necessary to assess the usage level of derivatives for hedging among

individual traders. This study covers mainly three different aspects 1) extent of hedge

effectiveness 2) need for promoting derivatives as a hedge tool and 3) how to fill the gap if

any, between the hedge effectiveness and the present level of adoption of derivatives to

hedge.

Models Developed for the Study

1. Conceptual model for the study.

2. Working model.

3. Model showing present scenario of Indian derivative market.

4. Financial derivatives as a hedge tool – An acceptance model

Variables for the study

Based on the conceptual model developed for the study, relevant variables were

identified such as coverage of potential loss, satisfaction level, hedge attitude, future

behaviour, awareness, probable loss, risk level, percentage of risk coverage, stock prices,

duration of contracts, variety of contracts and frequency of awareness programs.

Chapter 7 – Summary, Findings and Conclusion

339

Hypotheses

As part of the study, 11 hypotheses were developed and tested using appropriate

tools. A summary of the results of hypothesis testing is given below:

Table 7.1: Summary of Hypothesis Testing

Null Hypothesis Test of

Hypothesis

Result

(95% Confidence Level)

There is no significant

difference in the awareness

level of hedgers and non-

hedgers regarding different

aspects of derivatives trading.

T test p value is less than .05 and null

hypothesis is rejected.

There is no significant

difference in the composition of

hedgers and non-hedgers in

different regions of Kerala.

Chi-Square Test p value is greater than .05 and

hence accept null hypothesis

There is no significant

difference in the demographic

pattern of hedgers and

non-hedgers

Chi-Square Test p value is greater than .05 and

hence accept null hypothesis

There is no significant

difference in the distribution of

ranks given by respondents to

different problems in

derivatives trading.

Chi-Square Test p value is less than .05 and hence

reject null hypothesis

Frequency of hedge is

independent of satisfaction on

hedge coverage.

Chi-Square Test p is less than .05. Hence null

hypothesis is rejected

Chapter 7 – Summary, Findings and Conclusion

340

Future behaviour of hedgers is

independent of satisfaction on

hedge coverage

Chi-Square Test Out of four aspects identified for

future behavior, in case of one

aspect „Future use of hedge‟ p

value is less than .05. Hence reject

null hypothesis. But in case of

other three aspects „Recommend

hedge‟, „Would continue to trade‟,

„Welcome new products‟, p value

is greater than .05 and hence null

hypothesis is accepted.

There is no significant

difference in the assistance

obtained by hedgers and non-

hedgers from stock broking

firms.

T test p value is less than .05 in case of

„Advice to hedge‟ hence null

hypothesis is rejected and in other

two cases, „Number of awareness

programs‟ and „Proper training on

how to hedge‟ p value is greater

than .05 and hence accept null

hypothesis.

There is no significant

difference in the distribution of

ranks given by hedgers for the

most influencing intermediaries

Chi-Square Test p value is less than .05 and hence

reject null hypothesis

There is no significant

difference in the distribution of

ranks given by non-hedgers for

the most influencing

intermediaries

Chi-Square Test p value is less than .05 and hence

reject null hypothesis

Futures and spot series are

non-stationary

Unit Root -

Dickey Fuller

Test

p value is less than .05 for first

difference series and hence reject

null hypothesis. Thus futures and

Chapter 7 – Summary, Findings and Conclusion

341

spot series are stationary at first

difference.

Futures and spot series are not

cointegrated

Engle-Granger

test of

Cointegration

p value is less than .05 and hence

reject null hypothesis. Thus futures

and spot series are cointegrated.

Research Design

The study used descriptive research design. Hedge effectiveness was verified with

relevant data and tools. It also involves analyzing the risk perception, risk assumption and

risk mitigation with risk management tools by individual traders.

Sample design for primary data

The respondents for the study were investors/traders of financial derivatives market

with special reference to Kerala. From among the defined population of 65 SBFs only 26

SBFs were having offices in northern, southern and central regions of Kerala. Hence, these

26 SBFs formed the sample frame for selection of respondents. Multi-Stage sampling

technique was used for the selection of respondents from stock broking firms. The whole

of Kerala state was divided into three regions north, south and central. Two districts from

each region were selected using random sampling. From north Kerala Kozhikkode and

Malappuram were selected, from Central Kerala, Ernakulam and Thrissur were selected

and Kottayam and Trivandrum from the South Kerala. From the 26 stock broking firms, 15

were selected on random basis and two branches of these 15 SBFs from each region were

selected at random. Thus, a total of 90 branches were selected for the study. Respondents

from these branches were selected randomly.

Chapter 7 – Summary, Findings and Conclusion

342

Sample size

In case of non-hedgers, standard deviation of pilot study was 13.46. Expected

standard error is taken as 1.5 and Z value at 95% confidence level is 1.96. Hence sample

size of non-hedgers is found to be 310. In case of hedgers, standard deviation of pilot study

was 3.27. Expected standard error is taken as .92 and Z value at 95% confidence level

1.96. Hence sample size of hedgers is 50 respondents.

Tools for data collection

Structured questionnaire, participant and non-participant observation, unstructured

interviews were used for collecting data. Both ranking and scaling questions were included

in the questionnaire. Five point Likert scale was used to measure the awareness while

attitude of investors was measured using semantic differential scale. Behavioural

intentional scale was also used to understand the predictable future behaviour of

respondents.

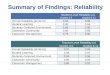

Pilot Study and Reliability Test

Based on the pilot study a reliability test was conducted and Cronbach alpha of

0.85 for questionnaire 1 and 0.809 for questionnaire 2 was obtained which shows that the

questionnaires are reliable.

Sample Design for Secondary Data

From the sample frame of stock futures in 24 sectors, near month expiry hedge

efficiency was calculated by selecting a sample of 24 stock futures each from 24 different

sectors on random basis. Overall hedge efficiency for three expiries were calculated based

on 15 stock futures randomly selected from the 24 stock futures. Out of the seven market

indices, three were selected, to assess the hedge efficiency.

Chapter 7 – Summary, Findings and Conclusion

343

Tools for analysis

Apart from percentages and descriptive statistics like Mean, Median, Mode,

Standard Deviation etc., tools like Multi-Dimensional Scaling, Cointegration, Error

Correction Model, Z test, Chi-Square test, Friedman test etc. were also used to arrive at

meaningful conclusions.

Period of the study

Secondary data for assessing the hedge effectiveness were compiled for five years

from April 2007 to March 2012. Primary data were collected from the sample respondents

in 2010 and 2011.

Limitations of the study

1. As there were no related studies, difficulty was experienced in developing appropriate

methodology and techniques for the study. Effort has been taken to avoid mistakes.

Alternative techniques can also be used to analyse the data and test the hypotheses to

establish relationships between the variables.

2. There may be a number of variables affecting the trading habits of individuals but

study focuses only on selected number of variables. Hence, there may be inadequate

coverage of some dimensions of derivative application.

3. Financial derivatives are a wider topic with variety of products, but the present study is

limited to hedge effectiveness of only two products, stock futures and index futures.

4. Since the derivative traders using financial derivatives for hedge are few in number, a

small sample size of 50 hedgers could only be collected.

Chapter 7 – Summary, Findings and Conclusion

344

Chapter Scheme

Chapter 1 gives an introduction to the present study and also explains the design of

the study. Chapter 2 presents the literature review, which provides a setting for the study,

gathered from different sources based on which research gap for the study was found out.

Chapter 3 is a theoretical framework of the study covering different concepts and theories,

trends in global scenario, Indian scenario, Hedge mechanism etc. Chapter 4 gives the

analysis of hedge effectiveness of Indian futures market. Chapters 5 assess the hedge

effectiveness of Index futures in Indian derivatives market. Chapter 6 deals with the

analysis of attitude and behaviour of individual traders in Kerala. It covers demographic

profile, awareness level, influence of intermediaries, hedge habits. Chapter 7 concludes the

study with a listing of major findings and recommendations.

B) MAJOR FINDINGS OF THE STUDY

Major findings of this study are summarised below. It is categorised under two

main sections Hedge effectiveness and Attitude of derivative traders.

a) HEDGE EFFECTIVENESS

Assessing the extent of hedge effectiveness of Indian derivatives was one of the

main objectives of the study. This section is again divided into three subsections; Hedge

efficiency of Indian stock futures and indices, Hedge effectiveness of Indian stock futures

and indices, Satisfaction level of hedgers.

Hedge Efficiency of Indian Stock Futures and Indices

Results of analysis on hedge efficiency of near month expiries and all expiries

combined together are presented here separately.

Chapter 7 – Summary, Findings and Conclusion

345

Near Month Hedge Efficiency:

1. Vast majority of stock futures (96%) shows average hedge efficiency of 80% and

above.

2. 38% of stock futures exhibit an average hedge efficiency of 100% and above, while

50% exhibit an average hedge efficiency of 90 to 100% and 8% of the stock futures

exhibit an average hedge efficiency of 80 to 90% and only 4% have hedge

efficiency of less than 80%.

3. Backwardation and Contango analysis shows that in Indian stock futures market,

instances of hedge efficiency were more than the instances of hedge inefficiency

between the periods 2007-08 to 2011-12.

4. October-December quarter seems to be the efficient quarter with highest ratio of

hedge efficiency.

Overall Hedge Efficiency:

5. Regarding overall hedge efficiency, 80% of Indian stock futures exhibit an average

hedge ratio of 80% or above

6. Around 70% of stock futures show that near month contracts are more efficient

while the rest 30% shows that next month futures are more efficient. Hedge

efficiency of far month contracts is comparatively less and seems to be more

volatile.

7. Backwardation and Contango analysis shows that in case of 73% of stock futures,

instances of hedge efficiency are more than the instances of hedge inefficiency.

8. In a vast majority of stock futures (86%), frequency of positive hedges is higher for

near month contracts followed by next month and then far month contracts.

Chapter 7 – Summary, Findings and Conclusion

346

Hedge Effectiveness of Stock Futures and Index Futures

9. Based on the average hedge efficiency of near month futures, 95.8% of Indian

stock futures are found to be effective as per the standard ratio 80% to 120% set by

SFAS 133.

10. Based on yearly average hedge efficiency of near month futures, 67% of stock

futures are found to be effective in all the five years under study.

11. Based on the overall hedge efficiency of three expiries for the last five years from

2007-08 to 2011-12, 80% of stock futures are found to be effective when compared

with the standard ratio.

12. Error correction model shows that the hedge efficiency of S&P CNX Nifty is

82.29% which can be inferred as effective according to standard set by SFAS 133.

However Bank Nifty and CNX IT have a hedge efficiency of only 72.97% and

50.67% respectively. Hence they are found to be ineffective as it is less than the

standard set by SFAS 133.

Satisfaction Level of Hedgers

13. Majority, 60% of hedgers have a regular habit of hedging.

14. On an average, hedgers are having only 50% hedge coverage.

15. Hedgers are found to be satisfied in all aspects of hedging except awareness

programs conducted by stock broking firms.

16. Chi-Square test of hypothesis shows that frequency of hedge is dependent on

satisfaction of hedge coverage.

Chapter 7 – Summary, Findings and Conclusion

347

17. Hypothesis testing shows that future use of derivatives for hedge is dependent on

the satisfaction of hedge coverage.

18. Regarding preference of products for hedge, 34% of hedgers prefer stock options

while 26% each prefer index futures and index options equally. Least preferred is

stock futures.

b) ATTITUDE OF DERIVATIVE TRADERS

This subsection presents the results of analysis of five different aspects;

Demographic profile, behavior of derivative traders, Beliefs and emotions, Problems in

derivative trading and Role of intermediaries.

Demographic Profile of Respondents

19. Demographic details show that 43.05% of derivative traders are in the age group 30

to 45 years, 42.22% are having Degree as their educational qualification and

50.56% are Employees in private or public sector.

20. Majority of the respondents, 53.61%, have less than five years of experience in

stock market and 38.9% have 1 to 2 years of experience in derivatives market.

21. Chi-Square test result shows that there is no significant difference in the

demographic pattern of hedgers and non-hedgers.

Behaviour of Derivative Traders

22. Regarding the trading habit, 36.94% are having a habit of frequently trading in

derivatives while 28.61% trade occasionally, 20.28% trade always and 14.17%

trade rarely in this segment.

Chapter 7 – Summary, Findings and Conclusion

348

23. Regarding preference of products for trading, out of 360 respondents 119

respondents (33%) give first preference to stock futures, 77respondents (21%) give

first preference to stock options, 81(23%)to index futures and 83(23%) to index

options.

24. Regarding future behaviour of traders study finds that hedgers are of the opinion

that they will definitely continue to trade in derivatives while non-hedgers are of

the opinion that they may probably continue to trade.

Beliefs, Emotions and Feelings of Derivative Traders

25. Mean score of awareness level of non-hedgers is 20.98 and of hedgers is 27.82 in a

scale with maximum score 40which shows that non- hedgers are aware of different

aspects of derivatives trading while hedgers are fairly aware. T test result shows

that there is significant difference in the awareness level of hedgers and non-

hedgers. It is inferred that hedgers are more aware than non-hedgers, as the mean

score is higher for hedgers.

26. Around 56% of non-hedgers are least aware about the concept called Hedge. Vast

majority of non-hedgers 87% have given preference to trade in derivatives due to

several reasons like profit making, fund leverage, to supplement income etc. Only

13% have given first preference for „covering the loss from spot market‟ as the

primary reason for trading on derivatives.

27. Mean score of attitude of hedgers towards derivative trading is 39.18 and mean

scores of attitude of non-hedgers is 37.66 in a scale with maximum score of 60.This

can be inferred as both hedgers and non-hedgers are having mildly positive belief

towards different aspects of trading.

Chapter 7 – Summary, Findings and Conclusion

349

28. 66.1% of non-hedgers are of the opinion that lack of awareness about hedge is the

reason for not using derivatives for hedge. Vast majority of non-hedgers (83%) are

interested in learning hedge techniques.

Problems Faced by Derivative Traders

29. Chi-Square test shows that there is significant difference in the ranking given by

respondents to different problems faced in derivatives trading.

30. The study found that problems faced by derivative traders can be viewed from two

different dimensions. Firstly based on Services provided and secondly on the basis

of Market mechanism. From the point of view of Services provided, „lack of

training‟ was found to be the most crucial problem while from the point of view of

Market mechanism, „maintenance of margin money‟ was found to be the most

severe problem faced by derivative traders.

Role of Intermediaries

31. Both hedgers and non-hedgers are of the opinion that stock brokers should promote

hedge. It was found that lack of support from SBFs was the main reason why non -

hedgers are not doing hedge.

32. Both hedgers and non-hedgers rarely get assistance from SBFs and both are neutral

regarding the opinion about effect of such assistance, awareness program etc.

33. Friedman test result shows that for hedgers „experienced people‟ seems to be the

most influencing one followed by SBFs. For non-hedgers, SBFs seems to be the

most influencing intermediary followed by experienced people.

34. Hedgers are of the opinion that friends and relatives have influenced them to hedge

rather than SBFs, awareness programs, etc.

Chapter 7 – Summary, Findings and Conclusion

350

Thus, based on the above findings, present scenario of financial derivatives

segment can be depicted as follows:

GAP

80% to 95% Satisfaction of

hedgers

Fig.7.1: Present Scenario – A Schematic Representation

Hedge

Effectiveness

On an average

hedge ratio is

only 50%

LOW USAGE LEVEL

LOW AWARENESS

LESS TRAINING

LESS SUPPORT FROM

SBFs

FUTURE BEHAVIOUR

„PROBABLY‟

MARGIN MONEY

DISSATISFED with the

outcome OF

AWARENESS

PROGRAMS

Chapter 7 – Summary, Findings and Conclusion

351

From the study it was found that there is a wide gap between hedge effectiveness

on one side and lack of its usage by traders on the other side as clearly depicted in fig.7.1.

Hence the question arises, why hedge habits are lacking when there is enough logic for it?

Some of the reasons for this are lack of promotional activities, lack of awareness and lack

of training on technical aspects of hedge. As far as the hedgers are concerned their hedge

coverage ratio is only around 50% while the secondary result shows that a good strategy

of hedge may even result in 80% to 95% hedge coverage. How can this gap be reduced?

How can the hedge habits be promoted? How can the hedge coverage ratio be increased?

These questions lead to the necessity of providing recommendations for improving the

efficiency of financial derivatives market

C) RECOMMENDATIONS

To mitigate the gap between hedge effectiveness on one side and less usage of

derivatives for hedge on the other side, several promotional measures need to be taken.

An important problem to be solved is how to improve the average hedge coverage

ratio from 50% to 80% or more. Proper guidance should be given to hedgers in this regard.

Most of the hedgers are not aware of their optimal hedge ratio. If a proper hedge portfolio

is created hedge coverage can be increased to around 80 to 90%. Following steps is

recommended to be followed to increase the hedge coverage:

1. Identify the amount exposed to risk.

2. Calculate optimal hedge ratio.

3. Hedge the amount based on optimal hedge ratio.

4. Select proper combination of derivative products for hedge.

Chapter 7 – Summary, Findings and Conclusion

352

Lack of training and Maintenance of margin money is yet another problem. Stock

broking firms should play a significant role by providing proper training sessions to

traders. Opportunities to have special forums for discussions with experts in derivatives

trading should be available. Daily settlement and maintenance of margin money has to be

modified. Traders can be given more time to fill the variation in the margin money. This

will simplify the risk to traders and as a result more traders will be attracted to trade.

Awareness level of derivative traders on hedge concepts, especially non-

hedgers‟, is very poor. To increase the awareness on hedge, stock broking firms should

conduct awareness programs with special focus on hedge strategies. A demo trading

session can be conducted. Special focus should be given to extent of risk exposure, extent

of coverage, hedge ratio, popular strategies like straddle, strangle, delta hedge etc. People

entering derivatives market should have a basic knowledge about different aspects of

trading. Special training sessions on technical aspects need to be conducted on regular

basis and course completion certificates can be issued. Stock exchanges should introduce

new certification programs with special focus to hedge.

Non-hedgers are mostly influenced by stock broking firms. Hence role played by

stock broking firms in promoting hedge habits of non-hedgers should be improved. Special

aid can be given by regulatory authorities to stock broking firms, to take promotional

measures.

Lack of experts in this field is yet another problem. To solve this problem a panel

of investment experts who are specialized in different trading strategies can be formed.

Each stock broking firm may have an investment expert who can guide the traders in

selecting proper hedge position.

Chapter 7 – Summary, Findings and Conclusion

353

The major recommendations can be summarised as follows:

1. Practice of hedge based on optimal hedge ratio is to be popularized.

2. Separate training sessions on hedge can be conducted.

3. Stock exchanges can introduce new certification programs with special focus to

hedge.

4. Each stock broking firm may have an investment expert who can guide the traders

in selecting proper hedge strategy.

5. Present system of maintenance of margin money need to be simplified so as to

reduce the burden of traders. Traders can be given more time to fill the variance in

margin money.

6. Stock broking firms, as a major influencing intermediary, should undertake more

advertising campaigns and use of celebrities to advertise can attract more attention

from general public.

7. A group of investment experts can be made available to clear the doubts of traders

through different media like telephone, emails, online communication etc.

8. SEBI, which is the regulatory body and stock exchanges like NSE and BSE and

regional stock exchanges, may set up separate funds to promote the role of SBFs.

AN ACCEPTANCE MODEL

The study has developed a notable model for promoting financial derivatives as a

hedge tool. By undertaking proper measures, the gap between hedge effectiveness and its

usage level can be reduced. Following Acceptance Model Fig 7.2 depicts how the critical

issues can be handled efficiently for a better functioning of financial derivatives market.

Chapter 7 – Summary, Findings and Conclusion

354

Fig.7.2: Financial Derivatives as a Hedge Tool – An Acceptance Model

Awareness Programs

Technical Training Sessions

Sessions on Hedge Strategies

Increase in awareness level

of Non-hedgers

Optimal Hedge Ratio-

Proper combination

of derivative products

Increase in Hedge

coverage ratio to 80%

and above

Satisfaction on Hedge coverage

Satisfaction on Training sessions by SBFs

Satisfaction on Margin money

Special forums to

clear clarifications

of investors

Hedge Management and

Promotional Measures

Reduction in Margin

money

Increase in usage

level of Hedge

Future behaviour will

shift from “probably”

to “definitely”

Financial

Derivatives as a

Hedge Tool

Increasing role of Stock

Broking Firms (SBFs)

Chapter 7 – Summary, Findings and Conclusion

355

CONCLUSION

Derivatives are one of the fastest growing and widely used financial innovations

which have their impact on financial markets, monetary policies, investment avenues,

regulatory framework and even on research and academics. Derivatives segment has

emerged as an area of utmost care and concern due to its anomalous behaviour.

Innovations in financial theory, increased computerization and changes in capital market

have all contributed to the growth of financial derivatives market.

It was noted that Korean exchange stood first among the world exchanges in terms

of the volume of derivative contracts traded in 2011 while the Indian exchange, NSE, was

in the fifth position. But in 2012, Chicago Mercantile Exchange – CME Group occupied

the top position and NSE has come up to the third position. It is interesting to note that

NSE secures the top five positions in case of all the three products namely stock futures,

Index futures and index options except stock options. While comparing the derivatives

traded in different regions, it was noted that Asia pacific region has the major share. Equity

derivatives have the maximum growth rate when compared to other categories like

commodity derivatives, currency derivatives etc. On an average the annual growth rate of

derivatives traded in India is 24%. It was noted that index options have the maximum

growth rate in 2012 when compared to index futures, stock options and stock futures.

This study has mainly focused on the hedge effectiveness of Indian futures market

and also the attitude and behaviour of financial derivative traders. From the detailed

analysis of primary and secondary data it is concluded that, on one side Indian derivatives

market is effective in hedging while on the other side majority of traders are unaware of

Chapter 7 – Summary, Findings and Conclusion

356

proper hedge techniques. Over use of speculation will dampen the efficient derivative

system and hence steps should be taken to improve the hedge habits of derivative traders.

Study also assessed traders‟ beliefs and behavioural patterns and arrived at the conclusion

that there is a need to popularize hedge habits among derivative traders.

Thus, it can be concluded that by undertaking several innovative measures the

usage level of financial derivatives for hedge can be increased. By reducing some of the

complexities in the system like lack of training, margin money maintenance etc. new

traders will be attracted to hedge. It is necessary to maximize the participants in the

derivatives segment so as to have a smooth flow of Indian derivatives segment. Study

concludes that promoting financial derivatives as a hedge tool is need of the hour. This is

possible by bridging the gap between extent of hedge effectiveness on one side and its less

popularity among derivative traders on the other side.