Embed Size (px)

Citation preview

Santander Consumer Bank

Q1 2018 Investor Presentation

Who we areSantander Consumer Bank is a Nordic bank with more than

1,400 colleagues in Sweden, Norway, Denmark and Finland, with a long history

in the Nordics, and with global strength by being a part of Banco Santander.

We are one of the largest Nordic banks providing loans and credits,

credit cards, deposits and insurance to private customers.

We work with the best people in an engaged, challenging and passionate

organization that provides great opportunities for professional growth.

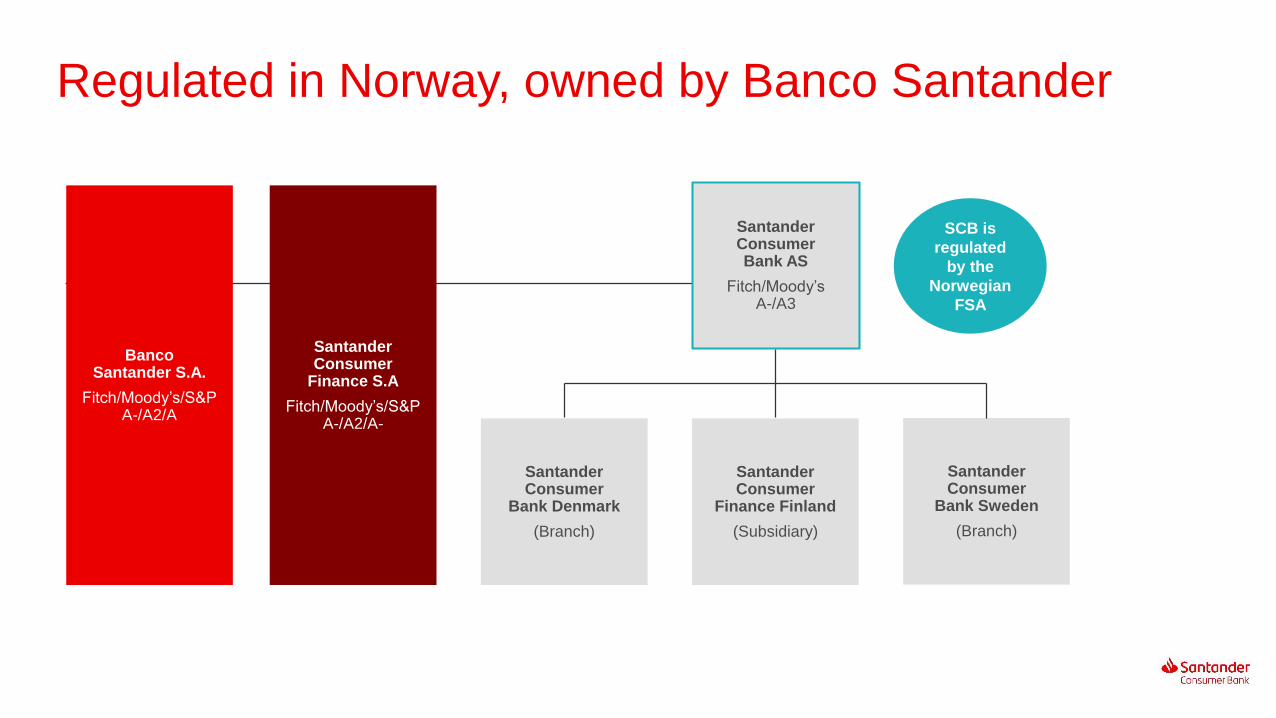

Regulated in Norway, owned by Banco Santander

SCB is

regulated

by the

Norwegian

FSA

Santander Consumer

Finance S.A

Fitch/Moody’s/S&PA-/A2/A-

Santander Consumer Bank AS

Fitch/Moody’sA-/A3

Santander Consumer

Bank Denmark

(Branch)

Santander Consumer

Finance Finland

(Subsidiary)

Santander Consumer

Bank Sweden

(Branch)

BancoSantander S.A.

Fitch/Moody’s/S&PA-/A2/A

Q1 Key figures

Total

deposits

52.2NOK Bn

Gross

Outstanding

Loans

144.5NOK Bn

Profit Before

Tax

744NOK million

Core capital

CET1

15.5per cent

People

1,432employees

Customers

1.41million

Return on

Asset

2.1per cent

Partners

4,785merchants

+4,200car dealers

Source: SCB Q1 2018 Report and Management Figures as per Q1 2018

History

Bankia Bank acquired

(credit cards)

ELCON Finance becomes

Santander Consumer

Bank AS (SCB)

ELCON Finance

A leading Norwegian

company within equipment

leasing, factoring and auto

financing

Santander Consumer

Finance (SCF) acquires

ELCON

Company

demerges

Auto finance retained in

Norway and Sweden

Launch consumer

loans Norway

Start up auto finance in

Denmark and Finland

GE Finland acquired

(auto finance,

consumer loans)

Consumer loans in

Sweden (2012) and

Denmark (2013)

Deposits launched in

Norway and Sweden (2013)

Deposits launched in

Denmark in 2014

1963

2004

2005

2006/07

2009

2012/13

2015

SCB merges with

GE Money Bank

SCB becomes

leader within car

finance and

unsecured loans in

the Nordic region

€

€

Main product areas

Auto & Leisure Unsecured InsuranceDeposits

Saving products

with high interest

rates provided to

private customers

Insurance products

related to payment

protection, auto,

health and travel,

offered to private

customers

Loans, credit cards and sales

finance services offered to private

customers

Loans and financial services

provided to private customers and

car dealers

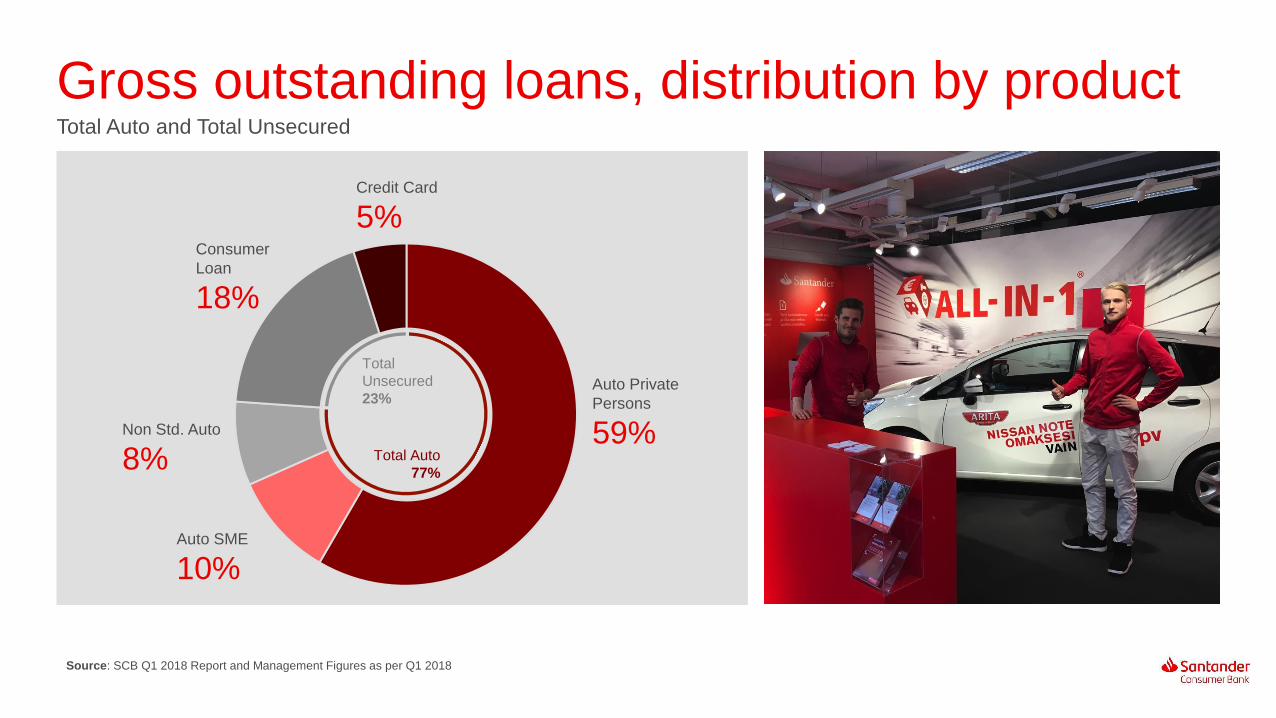

Gross outstanding loans, distribution by productTotal Auto and Total Unsecured

Auto SME

10%

Non Std. Auto

8%

Consumer

Loan

18%

Credit Card

5%

Auto Private

Persons

59%

Total

Unsecured

23%

Total Auto

77%

Source: SCB Q1 2018 Report and Management Figures as per Q1 2018

Our auto products

Saving products with high interest

rates provided to private customers

Auto &

Leisure

Loans and financial services

provided to private

customers SMEs and car dealers

Distribution

Online

Dealers

Cross sale

Auto Loans & Hire Purchase

Customers

• Private Customers

• Business Customers

Distribution

• Online direct distribution

• Indirect distribution with

dealers and importers

Stock & Demo Financing

• Finance of dealer inventories

• Importer agreements (new)

• Direct to dealers (used)

Customers

• Private Customers

• Business Customers

Distribution

• Dealers

• Direct SME

Auto Leasing

Position within Auto

Source Norway: Internal calculations based on data from Finansieringsselskapenes Forening as per Q1 2018

Source Finland: Internal calculations based on data from Finnish Transportation Safety Agency (Trafi) as per Q1 2018

Source Denmark: Internal calculations based on data from Finans og Leasing as per Q1 2018

Source Sweden: Internal calculations based on data from Finansbolagens Förening as per Q1 2018

Partnerships with

21brands

+4.200dealers

Position and market share in the Nordics

#1Position

24%market share

#1Position

23%market share

#1Position

39%market share

#4Position

9%market share

Unsecured products

Sales finance Credit cardsDirect loans

Unsecured

Loans, credit cards and sales finance services

offered to private customers

Distribution

Online

Stores

Cross sale

Portfolio Management

Distribution

Online

Stores

Cross sale

Distribution

Online

Agents

Cross sale

GDPRPSD2

Partnerships a key success factor

4,785 merchants

+4,200 car dealers and 30 brokers

“We started working with

Santander as an exclusive

partner two years ago.

Since then, we have

reached targets we didn’t

think were possible”

— Paal Jahrmann,

CEO Birger N. Haug

“I’ve seen Santander work in a way that is not typical to a bank. You always take and run with our targets”

— Stefan Andström, Sales Director, Nissan Nordic,

Helsinki

Financials

Q1 2018 | Santander Group key figures

Banco Santander S.A.

Total assets 1.44 (trillion €)

Branches globally13,637 (units)

Headcount 201,900

Customers139 (million)

Profit After Tax 2,054 (million €)

Santander Consumer Finance S.A.

Loans 100 (billion €)

European countries15

Headcount 15,850

Customers 20 (million)

Profit After Tax 351 (million €)

Source: Banco Santander and SCF Q1 2018 Institutional Presentation

Q1 2018 | SCB overview

NordicQ1 2018 results

144.5 Bn Gross Outstanding

Loans

744 MMProfit Before Tax

Norway

Auto Loans

Unsecured Loans

Profit Before Tax

45.9 Bn

11.5 Bn

291 MM

Denmark

Auto Loans

Unsecured Loans

Profit Before Tax

23.5 Bn

5.7 Bn

211 MM

Finland

Auto Loans

Unsecured Loans

Profit Before Tax

23.2 Bn

2.6 Bn

97 MM

Sweden

Auto Loans

Unsecured Loans

Profit Before Tax

18.6 Bn

13.4 Bn

144 MM

40% Norway

20% Denmark

22% Sweden

18% Finland

Source: SCB Q1 2018 Report

% of Gross Outstanding Loans

Growing presence in the NordicsWith a doubling of Gross Outstanding Loans in the past 5 years

Source: SCB Annual Reports (2012 –2017) and Q1 2018 Report

59,575(mNOK)

71,891(mNOK)

83,322(mNOK)

116,297(mNOK)

124,625(mNOK)

143,615(mNOK)

59,575

71,891

83,321

116,297124,625

143,615149,053

2012 2013 2014 2015 2016 2017 Q1 2018

mNOK

mNOK

mNOK

mNOKmNOK

mNOK mNOK

16%

40%7%

15%

21%

4%

Solid profitabilityStrong profitability, especially since the merger with GE Money Bank in 2015

PBT development NOK MM

1 1361 393 1 321

1 942

3 250¹

3 995¹

744

2012 2013 2014 2015 2016 2017 Q1 2018

Source: SCB Annual Reports (2012 –2017) and Q1 2018 Report

1) The Group reclassified issued AT1 capital of 2,25 Bn NOK from liabilities to equity in 2017. Interest expenses for 2017 of 169 MM NOK are consequently presented in equity instead of profit and

loss, with related tax impact presented as part of other equity. Comparison figures are changed similarly. Please see principle 6) on page 40 in the 2017 Annual Report for further details.

23%

CAGR

Strong financial performanceEvidencing well-managed growth

Source: SCB Annual Reports (2012 –2017) and Q1 2018 Report

ROA = PBT / ANEA (Annualized)

NII Ratio = Net Interest Income / ANEA (Annualized)

Cost/Income Ratio = OPEX / Gross Margin (OPEX: Total Operating Costs)

4.5 4.54.8

5.24.9 4.7

2013 2014 2015 2016 2017 Q1 2018

42 4448

3740 39

2013 2014 2015 2016 2017 Q1 2018

2.1

1.71.9

2.73.0

2.1

2013 2014 2015 2016 2017 Q1 2018

Return on AssetsPer cent

Net Interest Income RatioPer cent

Cost / Income RatioPer cent

Group Balance Sheet summaryRobust balance sheet driven by growth in loans to customers

Q1 2018• Deposits with external institutions: Significant increase due to

repayment of EUR bond maturity in April.

• Loans to customers: Growth in gross loans are partially off-set

by IFRS9 impact on LLR

• Other financial assets: Increased liquidity portfolio due to bond

purchases in Q1 2018

• Other assets: Change mainly driven by decreased consignment

• Debt to credit institutions: Increased levels of intragroup funding

due to large EUR bond maturity

• Deposits from customers: Increase in deposits in accordance

with funding strategy

• Debt established by issuing securities: Increase issuance in

unsecured bonds

NOK MM Q1 2018 Q4 2017 Δ 18/17 %

Deposits with external institutions 7 357 3 291 4 066 124 %

Loans to customers (net) 140 979 140 793 186 0 %

Other financial assets 8 557 7 119 1 438 20 %

Other assets 7 446 7 896 -450 -6 %

Total assets 164 339 159 100 5 239 3 %

Debt to credit institutions 33 654 31 020 2 634 8 %

Deposits from customers 52 244 50 617 1 627 3 %

Debt established by issuing securities 53 009 51 270 1 739 3 %

Other liabilities 2 876 3 260 -384 -12 %

Subordinated loan capital 1 709 1 753 -44 -3 %

Total equity 20 848 21 179 -331 -2 %

Total liabilities and equity 164 339 159 100 5 239 3 %

Source: SCB Q1 2018 Report

Group Income Statement summaryP&L showing steady growth with increasing profits

NOK MM Q1 2018 Q1 2017 Δ 18/17 %

Interest income and similar income 2 036 1 895 141 7 %

Interest expenses and similar expenses -340 -302 -38 13 %

Net interest income 1 696 1 593 103 6 %

Commissions and fees 105 135 -30 -22 %

Other product and funding related income and cost 27 -23 50 217 %

Gross margin 1 828 1 705 123 7 %

Salaries and personnel expenses -315 -282 -33 12 %

Administrative expenses -369 -377 8 -2 %

Depreciations and amortisation -28 -26 -2 8 %

Net operating income 1 116 1 020 96 9 %

Other incomes and costs -1 -1 0 0 %

Total losses on loans, guarantees etc. -372 -108 -264 244 %

Profit before tax 744 911 -167 -18 %

Income tax -187 -216 29 -13 %

Profit after tax 557 695 -138 -20 %

Source: SCB Q1 2018 Report

Q1 2018• Net Interest Income: Increased due to higher volumes and

lower cost of funding

• Commissions and fees: Single premium insurance product

closed in Norway

• Salaries personnel and administrative expenses: Increase in

salaries and personnel expenses reflects a higher activity level

throughout the Nordic region in Q1 2018 compared to Q1 2017

• Total losses: Significantly increase in loan losses mainly driven

by the effect of the new methodology in IFRS 9 which results in

higher reserves coverage for the same credit risk levels

Self-funding is a strategic focusThree pillars approach provides funding flexibility

Self-funding pillars¹

Securitization Unsecured Deposits

6 outstanding

transactions across

Nordics

Represents a low-cost

and stable funding

source

NOK 8.101 billion

outstanding in the

Norwegian bond market

including NOK 850 MM

in Commercial Paper

SEK 5.45 billion

outstanding in the

Swedish bond market

EUR 2.75 billion

outstanding from four

Benchmark

transactions

In Norway deposits are

guaranteed up to NOK

2 MM

In EU countries the

guarantee is up to EUR

100,000

NOK 52.2 billion in total

deposits across

Norway, Sweden and

Denmark

2011 2012 2013 2014 2015 2016 2017 Q1 2018

Parent funding Securitization Deposits Unsecured Bonds

22% 28%

50%62%

70% 70% 77% 76%

2011 2012 2013 2014 2015 2016 2017 Q1 2018

Funding Composition

Self-funding ratio

Source: SCB Q1 2018 Report

1) Outstanding amounts/transactions as per Q1 2018

24%

29%

38%

9%

Deposits at a glanceConsolidated total balance: NOK 50.6 Bn

43%of total balance

Saving account

29%of total balance

Saving account

Notification product

Term deposits

28%of total balance

Saving account

Notification product

Source: SCB Q1 2018 Report

Deposit guarantees: Norway NOK 2 million | Sweden SEK 950,000 | Denmark EUR 100,000 equivalent

Saving account• Floating interest rates

• Full flexibility

Notification product• Withdrawals with 31 days notice

• Floating interest rates

Term deposits• Fixed interest rates

• Balance locked for 24 months

• Fees for withdrawals within term period

Unsecured Senior & Commercial Paper Funding2017 and 2018 YTD summary

New Issuances

Repurchases

Net New funding

Maturities

Total Outstanding¹

Preferred Format

Preferred Tenor

850 million

-

850 million

1,850 million

8,101 million

FRN

3 – 5 year

1,000 million

-

1,000 million

-

5,450 million

FRN

3 – 5 year

500 million

-

500 million

-

2,750 million

FXD

5 year

Source: Bloomberg

1) Outstanding amounts as per Q1 2018

2) Outstanding amounts as per Q4 2017

20181 NOK SEK EUR

New Issuances

Repurchases

Net New funding

Maturities

Total Outstanding²

Preferred Format

Preferred Tenor

20172

4,050 million

800 million

3,250 million

-

9,101 million

FRN

3 – 5 year

2,000 million

-

2,000 million

2,410 million

4,450 million

FRN

3 – 4 year

500 million

-

500 million

-

2,250 million

FXD

3 year

NOK SEK EUR

Unsecured FundingMaturity profile 2018 – 2022 for Senior Unsecured and Commercial Paper

Total Maturity (EUR MM)

88

357

16636

19197

141

97

146

750

1,000

500

2018¹ 2019 2020 2021 2022

EUR

SEK

NOK

750

1,000

500

2018¹ 2019 2020 2021 2022

850

3,451

1,600

350

1,850

2018¹ 2019 2020 2021 2022

1,0001,450

1,000

1,500

2018¹ 2019 2020 2021 2022

Source: Bloomberg as per Q1 2018

FX: SEK/NOK 0.9409 | EUR/NOK 9.6770 | EUR/SEK 10.2843

1) Remaining maturities for 2018

NOK MM

SEK MM

EUR MM

Strict capital requirements in Norway

1) Portfolio allocation per 31.03.18, show a countercyclical buffer requirement for SCB Group of 1,14% and SCB AS of 1,46%

Ensuring strong capitalization of the bank

~11.3%

Pillar 1 CET1-requirement

2.3%

Pillar 2 CET1-requirement

~13.6%

Minimum CET1 requirement 4.5%

Conservation buffer 2.5%

Countercyclical buffer ~1.3%1

Systemic risk buffer 3%

~11.3%

CET1-ratio requirement for 2018 Capital requirements in Norway

• Strict requirements in Norway with the

inclusion of additional buffer requirements and

a high countercyclical buffer requirement

• Pillar 2 requirement for SCB was set to 2.3%

by the Norwegian FSA, applicable from

January 2018

• Countercyclical buffer requirement is

calculated as a weighted average of the risk

weighted assets in the countries where the

bank operates

• For 2018 the countercyclical buffer for SCB will

be 2% in Norway and Sweden and 0% in

Denmark and Finland¹

Strong Capital PositionCET1 ratio of 15.5%

Capital ratios evolution SCB GroupPer cent

15.3 15.1 15.5 15.2 15.5

17.8 17.4 17.5 17.2 17.5

19.1 18.7 19.1 18.8 19.1

11.4 11.5 12.011.5 11.7

2015 2016 2017 Q1 2018 Q1 2018

CET 1 Tier 1 Tier 2 Leverage ratio

Source: SCB Q1 2018 Report

Full IFRS9

impact

With IFRS9

transitional rules

• Net capital impact of

implementation of IFRS9 was

NOK 457 million for SCB

Group

• SCB has notified the FSA that

we will use the transitional

rules for IFRS9 capital impact

when calculating capital ratios

• SCB Group had a CET1-ratio

of 15.5% per year end using

transitional rules for IFRS9

impact

• SCB Group had a strong

Leverage Ratio per year end

of 11.7%

Risk Management Recent developments

• Answer to the BIS initiative

on risk data aggregation

and risk reporting

• Risk data captures all types

of risks with appropriate

accuracy and timeliness

• Complete, precise and

regular data for effective

risk management

• SCB was approved an IRB

bank in 2015

• The operational benefits of

IRB are related to improved

client information

• IRB requires the bank to

increase the accuracy of

models, improve scoring,

processes and routines

and in general the risk

management practice of

the bank

• IFRS9 parameters are

developed leveraging from

the IRB system

• Strong governance in place

including internal validation

and audit

• Engine developed, tested,

in use to face the new

impairment requirements

• Business strategy defined

by risk appetite.

• All risks to be managed

• Forward-looking approach

• Independent risk function

• Robust data management

• Risk culture (greater

synergy and integration of

IRB into management)

Tight risk controls result in stable performance Risk ratio breakdown

NPL Ratio 2013 2014 2015 2016 2017 Q1 2018

Denmark 0.71% 0.61% 0.98% 1.24% 1.17% 1.29%

Finland 1.04% 0.89% 0.72% 0.71% 0.74% 0.77%

Norway 2.47% 2.36% 3.40% 3.36% 3.50% 3.66%

Sweden 0.48% 0.61% 1.53% 1.22% 1.12% 1.19%

Nordic 1.61% 1.48% 2.05% 2.01% 1.96% 2.08%

NPL ratio3

Coverage ratio4

Source: Management Figures as per Q1 2018

1) Auto includes Stock Finance

2) Unsecured includes Direct Loans, Credit Cards and Sales Finance (“Durables”)

3) NPL ratio = Non-performing loans / Gross outstanding loans

4) Coverage Ratio = Loan Loss Reserves (Write Downs) / NPL

1.61 1.482.05 2.01 1.96 2.08

2013 2014 2015 2016 2017 Q1 2018

98.6126.9

107.7 113.696.9

114.1

2013 2014 2015 2016 2017 Q1 2018

NPL Ratio 2013 2014 2015 2016 2017 Q1 2018

Auto1 1.20% 1.09% 1.03% 1.10% 1.07% 1.14%

Unsecured2 5.32% 4.77% 4.95% 4.89% 4.92% 5.28%

Nordic 1.61% 1.48% 2.05% 2.01% 1.96% 2.08%

Coverage Ratio 2013 2014 2015 2016 2017 Q1 2018

Auto1 75.5% 89.4% 95.4% 90.4% 91.8% 111.5%

Unsecured2 136.4% 148.1% 111.8% 113.1% 100.6% 115.9%

Nordic 98.6% 126.9% 107.7% 113.6% 96.9% 114.1%

Per cent

Per cent

Key takeaways

Anchored by a global

banking franchise

Sustained market

leader in auto

Building out position in

unsecured space

Robust financial results

Stable credit risk

Santander & Santander Consumer Finance

April 2018

Section divider

01

1. Santander

Santander, a leading financial group

31

Headcount 201,900

Branches (units) 13,637

Shareholders (millions) 4.11

Customers (millions) 139

Total assets (trill. €) 1.44

Key Figures Mar’18

Attributable Profit 2017 (mill. €) 6,619

Attributable Profit Q1’18 (mill. €) 2,054

The Santander vision

32

to help people and businesses prosper

to be the best retail and commercial bank, earning the lasting

loyalty of our people, customers, shareholders and communities

Our

purpose

Our aim

A bank

that is

We are committed to generating growth

in a sustainable, predictable and responsible manner

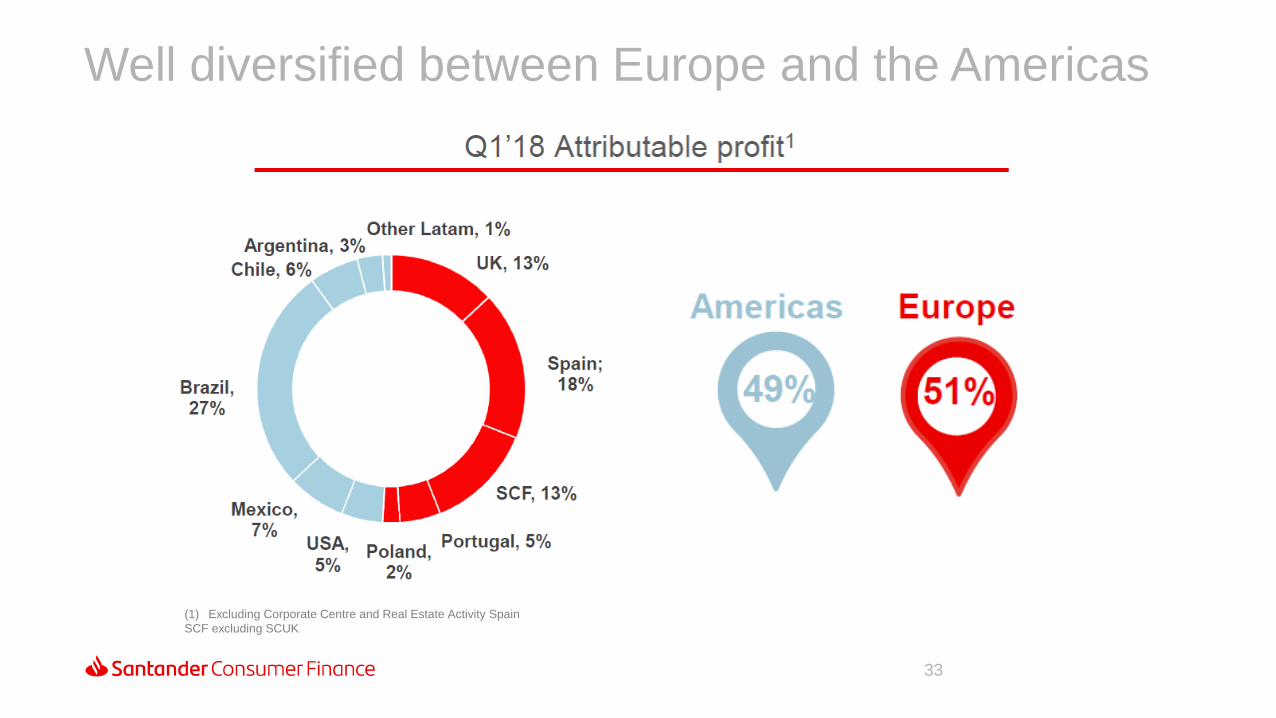

Well diversified between Europe and the Americas

33

(1) Excluding Corporate Centre and Real Estate Activity Spain

SCF excluding SCUK

With leading positions in its core markets

34

USA

Mkt. share1,4: 3%

Branches: 683

Argentina

Mkt. share1: 10%

Branches: 482

Mkt. share1: 16%

Branches: 563

PortugalBrazil

Mkt. share1: 9%

Branches: 3,465

UK

Mkt. share2: 10%

Branches: 808

Mkt. share1,6: 18%

Branches: 2,843

Spain

Mkt. share1: 19%

Branches: 439

Chile

Mkt. share1,3: 10%

Branches: 576

Poland

Mkt. share1: 13%

Branches: 1,401

Mexico

Nº countries5: 15

Branches: 546

SCF

7

(1) Lending (2) UK mortgages (excluding Social Housing), Consumer credit and commercial lending (excluding Financial Institutions) (3) Including Santander Consumer Finance business (SCF)

• (4) In the states where the Group operates. (5) Including SCF UK (6) Including Banco Popular. Excluding it: 13% (7) Argentina and Portugal only include private sector banks.

• Data: Dec’17 or latest available. Branches do not include Santander Consumer Finance business

Q1’18 Highlights

35

(1) Underlying attributable profit change vs. Q4’17: +7% (+10% in constant euros)

(2) Total dividends charged to 2018 earnings are subject to the Board and AGM approval

Predictable growth and balance sheet strength

36

Note: YoY change, including Popular in 2018. % change in constant euros. Loans excluding reverse repos. Funds: deposits excluding repos + marketed mutual funds

Q1’18 performance

Excellent YoY performance driven by strong top-line growth and lower provisions

37

Note: Contribution to the SRF (net of tax) recorded in Q2’17 (EUR -146 mn). Contribution to the DGF (net of tax) in Q4’17 (EUR -186 mn)

Q1’18 performance

On track to meet our 2018 targets

38

Q1’18 performance

(1)% change in constant euros (2)Total dividends charged to 2018 earnings are subject to the Board and AGM approval (3) Underlying RoTE: 11.8%

Section divider

02

2. Santander Consumer Finance

40

PoS partnerts (thousand) >130

Market positions1 Top 3

Loans (bill. €) 100

Deposits (bill. €) 37

European countries 15

Underlying Attrib. Profit Q1’18 (mill. €) 351

Customers (million) 20

Grupo Santander is the

main and unique

shareholder of SCF ...

… and at the same time,

SCF acts as a holding

for its subsidiaries

through a banking license

Operations are mainly

done through points-of-

sale (dealers and

retailers)

Key Figures Mar’18

Santander Consumer Finance, European leader in the consumer finance industry

Underlying Attrib. Profit 2017 (mill. €) 1,373

SCF: Management perimeter (i.e. including SCUK)

Attributable profit without non-recurring (provisions or capital gains) (1) In its main geographies by market share in New Business car loans or durables

41

With recurrent profits through the cycle

2009 2010 2011 2012 2013 2014 2015 2016 2017

472555

744825

895 908

1 093

1 238

1 373

Q1’2018

Underlying Attrib. Profit

€351 million

(+2% YoY)

Underlying Attributable Profit€ Million

SCF: Management perimeter (i.e. including SCUK)

Attributable profit without non-recurring (provisions or capital gains)

42

A differential and proven business model based on five key levers

High diversification and European leadership

A

Advanced car financing platform and strong foothold in consumer finance

B

Efficiency leadership with proven integration capabilities

C

Best-in-class risk and collections capabilities

Sound funding structure

SCF’s

business model

D

E

43

Well spread across Europe and well balanced between car and consumer loans

A

SCF: Management perimeter (i.e. including SCUK). NOTE: SCF’s portfolio also includes mortgages (6%), corporate loans (1%) and other loans (1%).

SCF Portfolio: €100 bnMar’18

Well spread across 15 European

countries

Important foothold in the largest

economies

74% portfolio in AAA & AA countries

Car financing represents the biggest

share of the portfolio: 70%

Consumer lending (durables financing,

cash loans and credit cards): 21%

44

Advanced car financing platform and strong foothold in consumer finance

B

TOP retail chain agreements throughout

Europe

>55,000 POS partners

>4 MM consumer loans per year

TOP 3 in core geographies

Digital direct business platforms

Strong foothold in consumer finance

Consumer Finance: Durable financing, Personal loans and Credit Cards

Presence in all main European markets

TOP positions in its geographies,

including the 5 biggest European auto

markets: Germany, France, UK, Italy

and Spain

>75.000 POS (captive and non-captive)

The longest European captive

agreements base: more than 100

agreements with 15 manufacturers

Advanced car financing platform

45

One of the best efficiency in the industry, with proven capabilities to make the most of integrations

C

• Germany

• Germany

• Austria

• Finland

• Germany

• Benelux

• Norway

• Sweden

• Denmark

• France• Germany• Italy• Poland

• Spain• Portugal• Belgium• Austria

• Netherlands• Switzerland• UK

Integrations 2008 2009 2011 20142014

• Spain

2015 …

43,4

47,548,7

43,3

46,3

48,4FY2016 FY2017

Cost-to-Income

ratio

SCF: Management perimeter (including SCUK) . Peers: Crédit Agricole Consumer Finance, BNP Personal Finance. Source: company websites.

Note.- BNP Personal Finance 'Share of Earnings of Equity-Method Entities’ reported after gross income. CA Consumer Finance Gross Operating Income in their accounts is Revenues minus

Operating Expenses, not including "equity affiliates results“. Both are reclassified for comparative purposes with SCF. Public report FY 2017 C/I ratios: CA=51,0%; BNP 49,3%

(%)

46

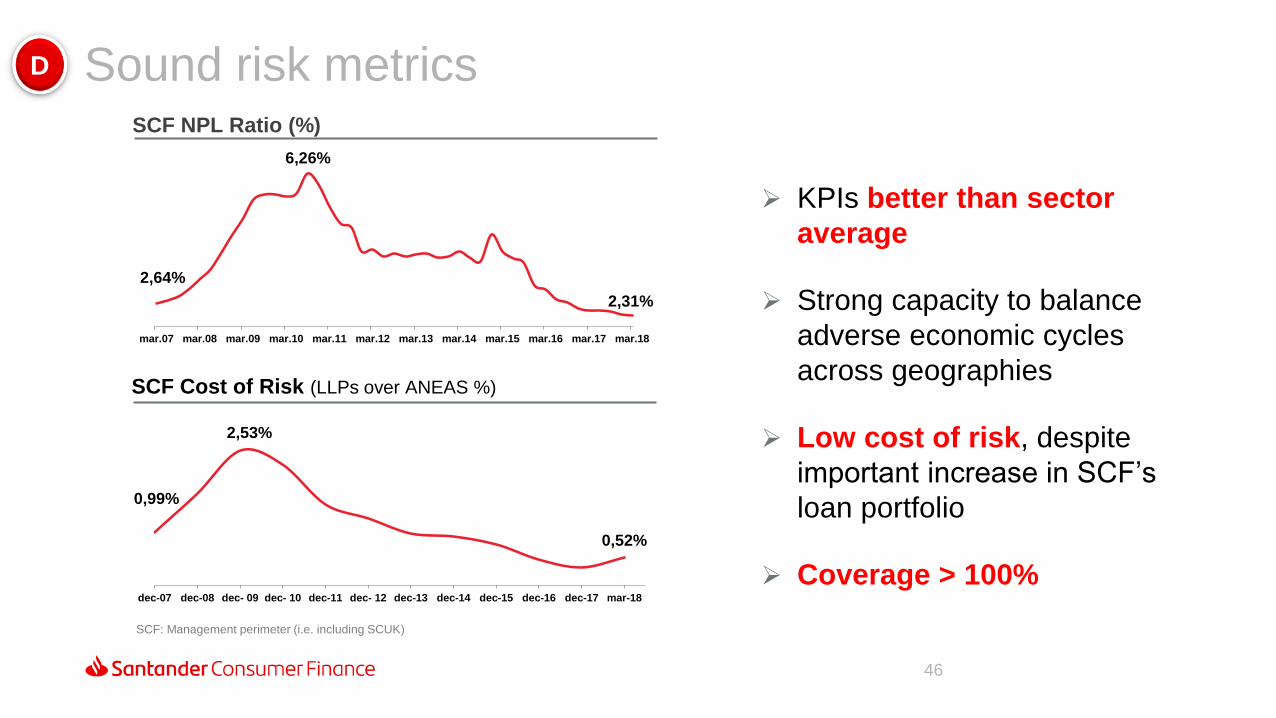

Sound risk metricsD

KPIs better than sector

average

Strong capacity to balance

adverse economic cycles

across geographies

Low cost of risk, despite

important increase in SCF’s

loan portfolio

Coverage > 100%

2,64%

6,26%

2,31%

mar.07 mar.08 mar.09 mar.10 mar.11 mar.12 mar.13 mar.14 mar.15 mar.16 mar.17 mar.18

0,99%

2,53%

0,52%

0%

1%

2%

3%

dec-07 dec-08 dec- 09 dec- 10 dec-11 dec- 12 dec-13 dec-14 dec-15 dec-16 dec-17 mar-18

SCF NPL Ratio (%)

SCF Cost of Risk (LLPs over ANEAS %)

SCF: Management perimeter (i.e. including SCUK)

47

Funding diversificationE

SCF’s funding structure (%)

High diversification of

funding sources

Capacity to do issuances in

all countries

Diversification of deposits

in many countries

Increasing long-term

finance vs short term

Mar’18

SCF: Management perimeter (i.e. including SCUK)

48

SCF is a significant contributor to Santander’s results, representing 13% of the Group’s profit1 in Q1’2018

SCF excluding SCUK. Including SCUK, SCF represents 14% of SAN profit1

(1) Percentage over SAN attributable profit in Q1’18, excluding Corporate Centre and Real Estate Activity Spain

SCF, 13%

Contacts

• Anders Bruun-Olsen, Nordic CFO

• Mobile: +47 95 76 83 28

• E-mail: [email protected]

• Priscilla Halverson, Director Capital Markets

• Mobile: +47 92 06 58 75

• E-mail: [email protected]

• Anders Fuglsang, Senior Manager Capital Markets

• Mobile: +47 95 04 21 28

• E-mail: [email protected]

• Thomas Andrén-Johansen, Senior Manager Capital Markets

• Mobile: +47 91 82 42 44

• E-mail: [email protected]

• Morten Christopher Freberg Holme, Capital Markets Manager (Paternity leave)

• Mobile: +47 92 82 38 33

• E-mail: [email protected]

• Joachim Joveng Rogne, Capital Markets Analyst

• Mobile: :+47 48 23 86 32

• E-mail: [email protected]

To learn more about Santander visit

Santanderconsumer.no | Santanderconsumer.dk | Santanderconsumer.se | Santanderconsumer.fi

Our purpose is to help people and

businesses prosper.

Our culture is based on the belief that

everything we do should be

![Santander Consumer Bank AG...2020/07/01 · MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS Key Indicators Exhibit 2 Santander Consumer Bank AG (Unconsolidated Financials) [1] 12-182](https://img.dokumen.tips/doc/110x75/601f182c6168690b1d515512/santander-consumer-bank-ag-20200701-moodys-investors-service-financial.jpg)