Embed Size (px)

Citation preview

Company presentation

Santander Consumer Bank AS, Nordic

Nov 2016

• Santander Consumer Bank AS (“Santander”) is a private limited liability company incorporated under the laws of Norway subject to supervision by the Norwegian Financial

Supervision Authority (the “Finanstilsynet”), having its registered office at Strandveien 18, 1366 Lysaker, Norway with registration number 983 521 592.

• No transaction or services related hereto are contemplated without a subsequent formal agreement with the Santander and/or its affiliates.

• This document has been prepared by Santander for information purposes only and its contents are proprietary information and are strictly private and confidential. You agree that

this document should not be reproduced (in whole or in part), delivered or distributed to others or replicated without the prior written consent of Santander and is intended to be

read by market professionals (eligible counterparties and professional clients) and should not be disclosed to nor relied upon by retail clients and/or investors.

• This document is not being distributed to and must not be passed on to the general public in the United Kingdom. This communication is only directed to those persons in the

United Kingdom who are within the definition of Investment Professionals (as defined in the Financial Services and Markets Act 2000 (Financial Promotions) Order 2005) (the

“FPO”). As such this communication is directed only at persons having professional experience in matters relating to investments. Outside of the UK, it is only directed at

Professional Clients or Eligible Counterparties within the meaning of the Markets in Financial Instruments Directive 2004/39/EC, as amended (“MiFID”) and is not intended for

distribution to or use by Retail Clients (as defined in MiFID).This document is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where

such distribution or use would be contrary to law or regulation.

• By accessing this document you shall be deemed to have represented to us that (a) you have understood and agreed to the terms set out herein, (b) you consent to delivery of

this document by electronic transmission, (c) you are not a US person (within the meaning of Regulation S) or acting for the account or benefit of a US person and the email

address that you have given to us and to which this email has been delivered is not located in the United States, its territories and possessions or the District of Columbia and (d)

if you are a person in the United Kingdom, then you are a person who is (i) an investment professional within the meaning of Article 19 of the FPO or (ii) a high net worth entity

falling within Article 49(2)(a) to (d) of the FPO.

• Neither the information nor any opinion expressed constitutes a prospectus, offering document, an underwriting commitment or an offer, or an invitation to make an offer, to buy or

sell any securities, other investment or any options, futures or derivatives related to securities or investments. No offering of securities shall be made in the United States except

pursuant to registration under the United States Securities Act of 1933 (as amended the “Act”) or any exemption from such registration provided by Rule 144A or Regulation S of

the Act.

• The information presented herein is an advertisement and does not constitute a prospectus for the purposes of EU Directive 2003/71/EC (as amended) (the “Prospectus

Directive”) and/or Part VI of the Financial Services and Markets Act 2000. Neither the information nor any opinion expressed constitutes a prospectus, offering document, an

underwriting commitment or an offer, or an invitation to make an offer, to buy or sell any securities, other investment or any options, futures or derivatives related to securities or

investments. The information herein has not been reviewed or approved by any rating agency, government entity, regulatory body or listing authority and does not constitute

listing particulars in compliance with the regulations or rules of any stock exchange.

• This presentation is provided on the basis of your acceptance of the terms of this disclaimer. This document contains certain tables and other statistical analyses (the "Statistical

Information") which may have not been audited. Numerous assumptions have been used in preparing the Statistical Information, which may or may not be reflected in this

document or be suitable for the circumstances of any particular recipient. As such, no assurance can be given as to the Statistical Information's accuracy, appropriateness or

completeness in any particular context, or as to whether the Statistical Information and/or the assumptions upon which they are based reflect present market conditions or future

market performance. The Statistical Information should not be construed as either projections or predictions or as legal, tax, financial, investment or accounting advice.

Disclaimer

2

• Any historical information contained in this document is not indicative of future performance. Opinions and estimates (including statements or forecasts) constitute Santander’s

judgement as of the date indicated, are subject to change without notice and involve a number of assumptions which may not prove valid. This document may include "forward-

looking statements". Such statements contain the words "anticipate", "believe", "intend", "estimate", "expect", "will", "may", "project", "plan" and words of similar meaning. All

statements included in this document other than statements of historical facts, including, without limitation, those regarding financial position, business strategy, plans and

objectives of management for future operations (including development plans and objectives) are forward-looking statements. Such forward-looking statements involve known and

unknown risks, uncertainties and other important factors that could cause actual results, performance or achievements to be materially different from future results, performance or

achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding present and future

business strategies and the relevant future business environment. These forward-looking statements speak only as of the date of this presentation and Santander expressly

disclaims to the fullest extent permitted by law any obligation or undertaking to disseminate any updates or revisions to any forward-looking statements contained herein to reflect

any change in expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based. Nothing in the foregoing is intended

to or shall exclude any liability for, or remedy in respect of, fraudulent misrepresentation.

• Likewise, certain information contained herein may use indicative valuations based on certain market conditions and information that can be subject to further verifications,

amendments or additions by Santander or its affiliates. Clients and /or investors are advised to make an independent review of the information and financial facts included in this

document. Certain transactions may give rise to substantial risks and are not suitable for all clients or investors. Each party is advised to reach their own conclusions regarding

the legal, tax and accounting aspects of a proposed transaction as it relates to their asset, liability, or other risk management objectives and risk tolerance.

• Santander is not recommending or making any representations as to the suitability of any securities. This document is not intended to provide personal investment advice and it

does not take into account the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. Each party should

seek independent financial advice regarding the suitability and/or appropriateness of making an investment or implementing the investment strategies discussed in this document

and should understand that statements regarding future prospects may not be realised. Each party should note that income from investments, if any, may fluctuate and that the

value of such investments may rise or fall, accordingly, they may receive back less than they originally invested. All investment decisions must be made on the basis of the

information that is contained in the final prospectus for the securities to be prepared and delivered to prospective investors at or prior to the time of sale.

• The information contained in this document (other than disclosure information relating to the Santander Group) has been obtained from, or are based on, sources believed to be

reliable, but no representation or warranty, express or implied, is made that such information, assumptions, performance data, modelling or scenario analysis is accurate,

complete or up to date and it should not be relied upon as such.

• To the fullest extent permitted by law, Santander does not accept any liability whatsoever (including in negligence) for any direct or consequential loss arising from any use of or

reliance on material contained in this document. In addition neither Santander nor any of their affiliates makes any representation or warranty as to the fairness, accuracy,

completeness, adequacy or comprehensiveness of the information contained in this document and expressly waives any responsibility arising from any lack of accuracy,

comprehensiveness and adequacy of the information contained in this document.

• Please note the publication date of this document. It may contain specific information that is no longer current and should not be used to make an investment decision. There is no

intention to update this document.

• This document has been sent to you in an electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of

electronic transmission and consequently neither Santander nor any director, officer, employee or affiliate of any such person accepts any liability or responsibility whatsoever in

respect of any difference between the document distributed to you in electronic format and the hard copy version available to you on request from Santander.

Disclaimer

3

1. Santander Consumer Bank AS, Nordic (“SCB Nordic”)

2. Risk Management

3. Financial information

4. Appendix: Banco Santander & Santander Consumer Finance

5. Appendix: Contacts

Content

4

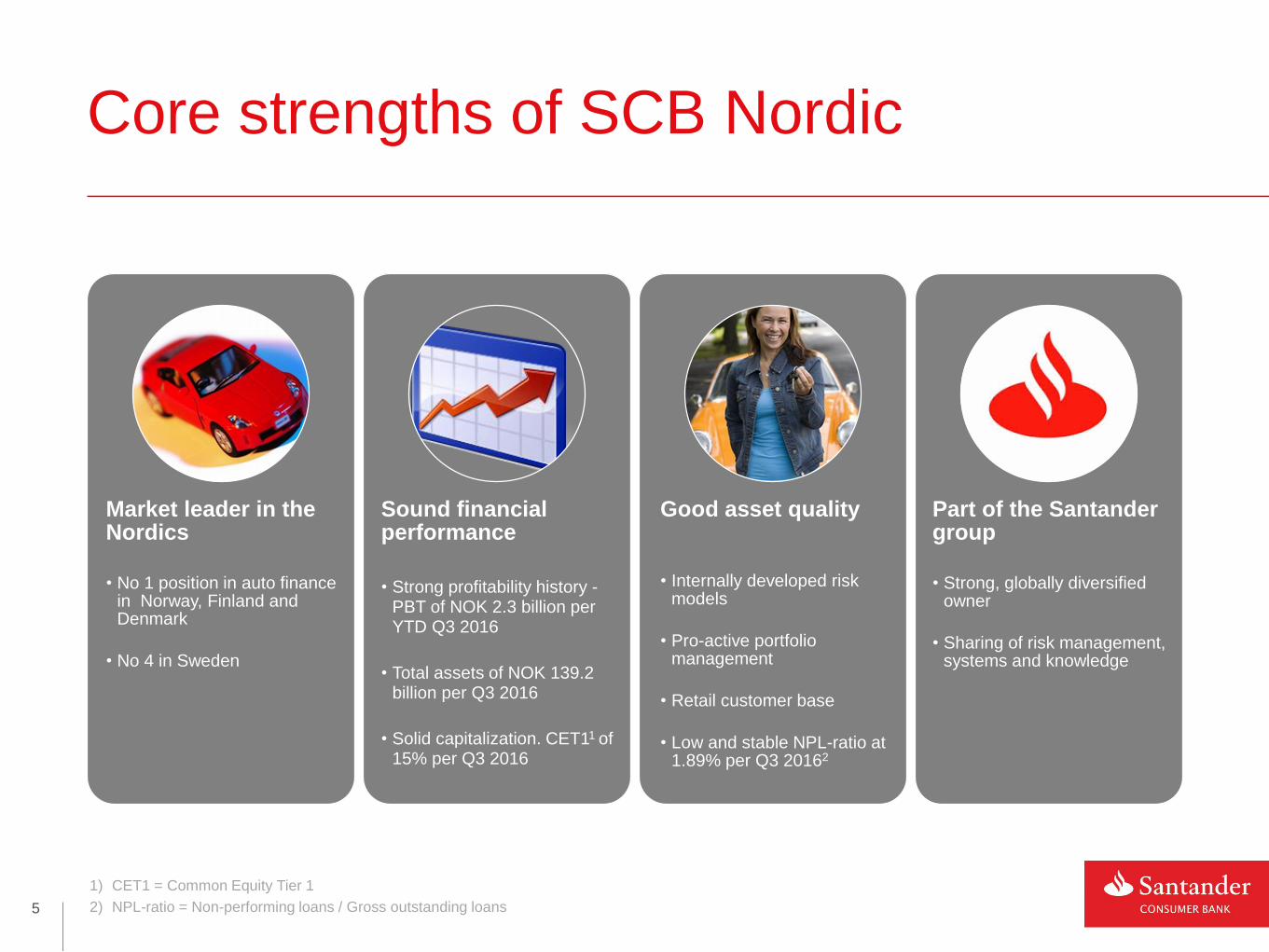

Market leader in the Nordics

• No 1 position in auto finance in Norway, Finland and Denmark

• No 4 in Sweden

Sound financial performance

• Strong profitability history -PBT of NOK 2.3 billion per YTD Q3 2016

• Total assets of NOK 139.2 billion per Q3 2016

• Solid capitalization. CET11 of 15% per Q3 2016

Good asset quality

• Internally developed risk models

• Pro-active portfolio management

• Retail customer base

• Low and stable NPL-ratio at 1.89% per Q3 20162

Part of the Santander group

• Strong, globally diversified owner

• Sharing of risk management, systems and knowledge

Core strengths of SCB Nordic

5

1) CET1 = Common Equity Tier 1

2) NPL-ratio = Non-performing loans / Gross outstanding loans

Banco Santander

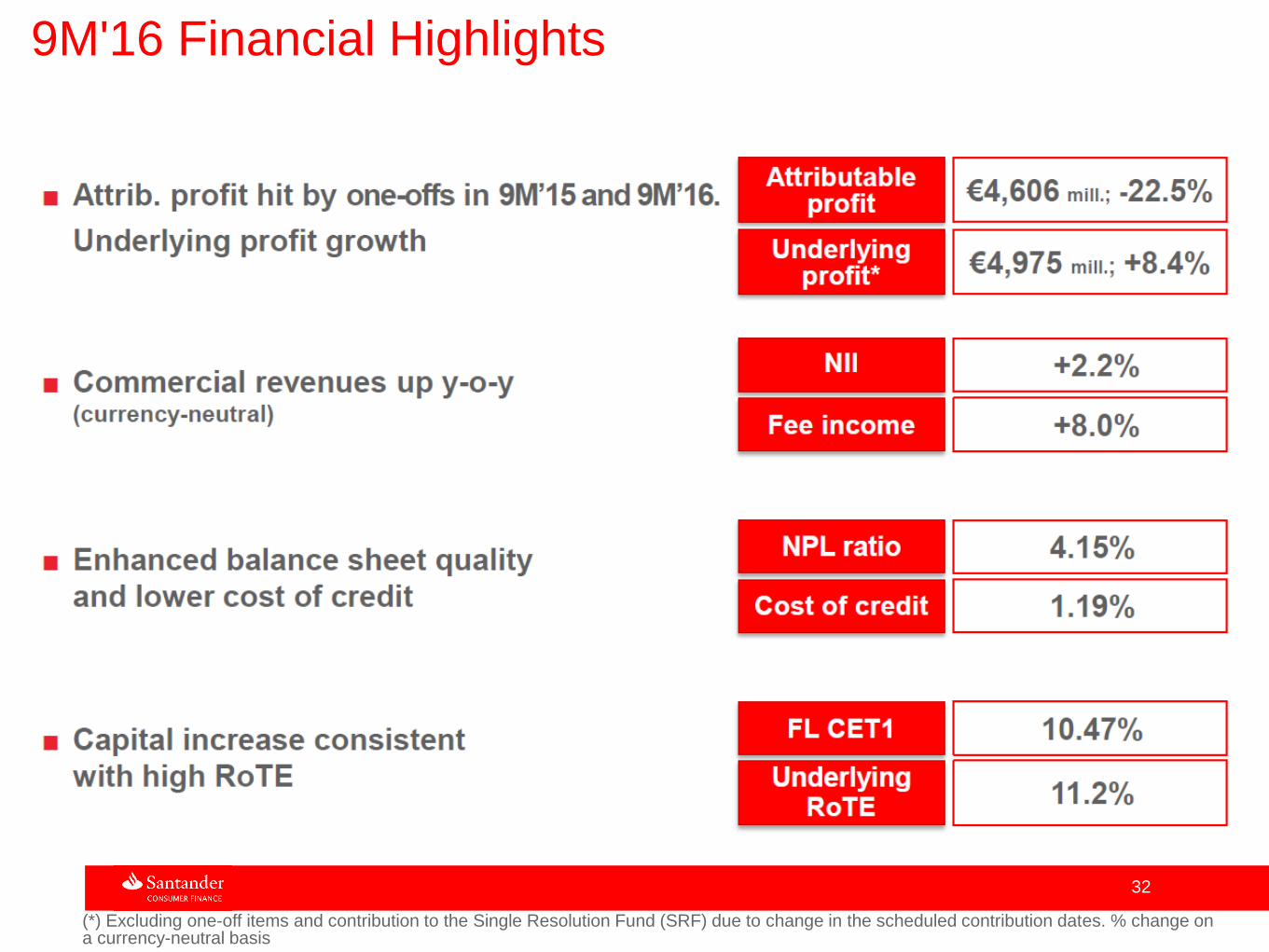

• Underlying Attributable Profit of EUR 4,606 million YTD Q3 2016

• Underlying Attributable Profit of EUR 6,566 million per FY 2015

• Total Assets of EUR 1.33 trillion (30.09.2016)

• Serving more than 124 million customers through 12,391 branches

• Wide geographic diversification in key markets in Europe, Latin

America and the United States

Santander Consumer Finance (SCF)

• Fully owned by Banco Santander

• Attributable Profit of EUR 935 million per YTD Q3 2016

• Attributable Profit of EUR 1,093 million per FY 2015

• Outstanding Loans of EUR 93 billion (30.09.2016)

• Wide geographic diversification in key markets in Germany, Nordics,

UK, Poland, Spain, Italy, Portugal, Austria, Benelux, Switzerland and

France

A leading financial group worldwide

Part of the Santander group

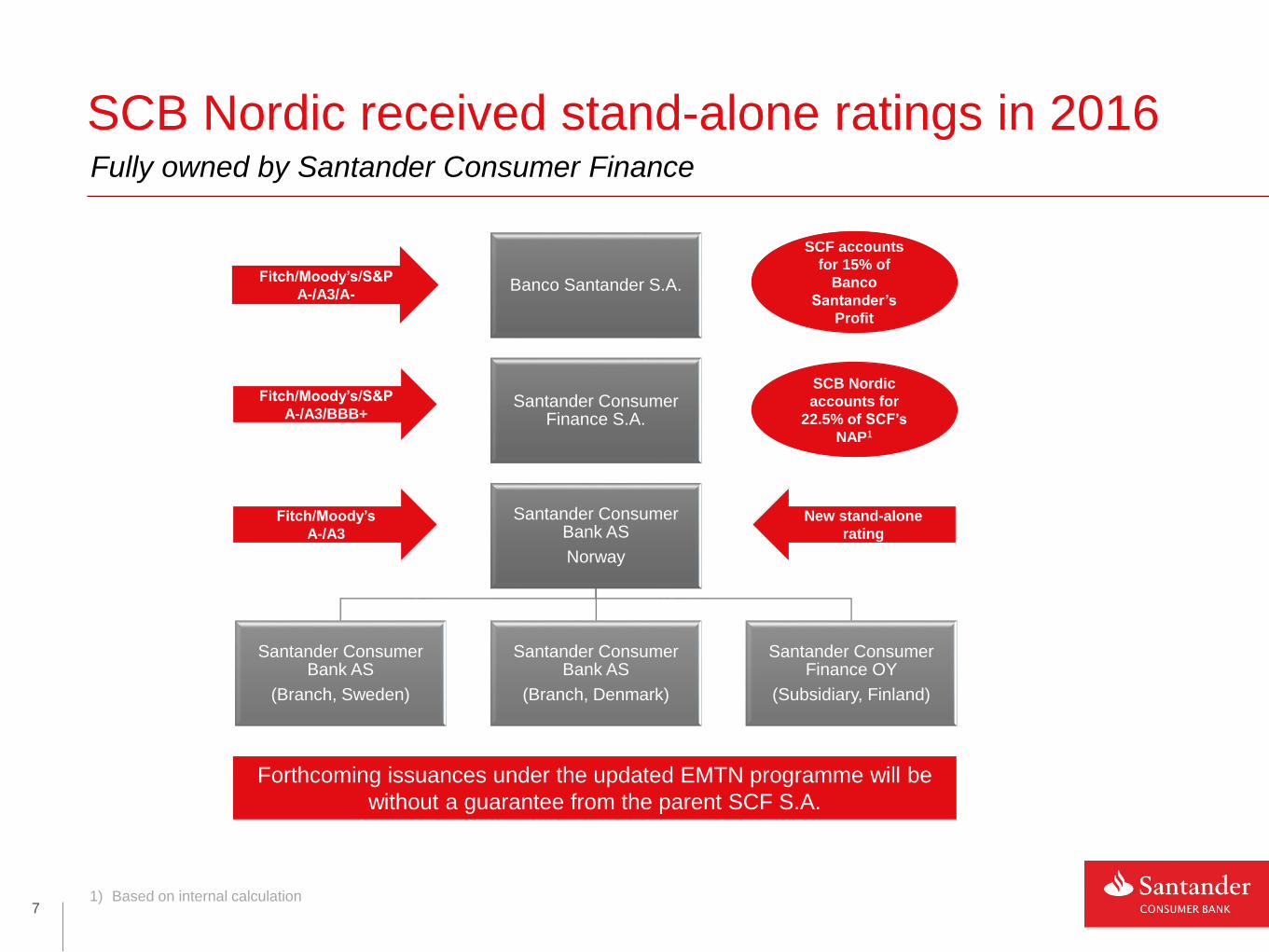

SCF: Management perimeter (includes SCUK)6

Banco Santander S.A.

Santander Consumer Finance S.A.

Santander Consumer Bank AS

Norway

Santander Consumer Bank AS

(Branch, Sweden)

Santander Consumer Bank AS

(Branch, Denmark)

Santander Consumer Finance OY

(Subsidiary, Finland)

SCB Nordic received stand-alone ratings in 2016Fully owned by Santander Consumer Finance

Fitch/Moody’s/S&P

A-/A3/A-

Fitch/Moody’s/S&P

A-/A3/BBB+

Fitch/Moody’s

A-/A3

Forthcoming issuances under the updated EMTN programme will be

without a guarantee from the parent SCF S.A.

New stand-alone

rating

7

SCB Nordic

accounts for

22.5% of SCF’s

NAP1

SCF accounts

for 15% of

Banco

Santander’s

Profit

1) Based on internal calculation

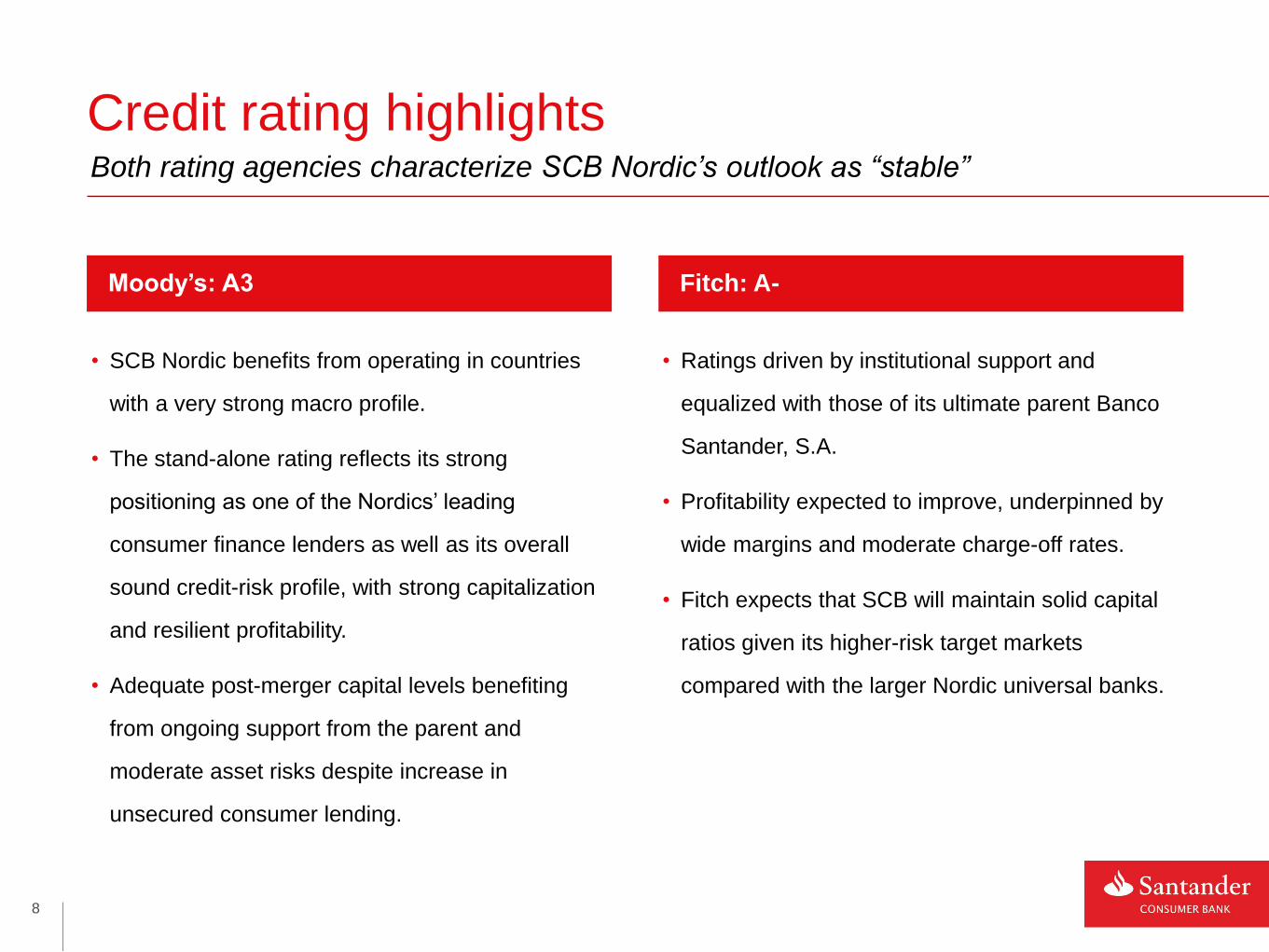

• SCB Nordic benefits from operating in countries

with a very strong macro profile.

• The stand-alone rating reflects its strong

positioning as one of the Nordics’ leading

consumer finance lenders as well as its overall

sound credit-risk profile, with strong capitalization

and resilient profitability.

• Adequate post-merger capital levels benefiting

from ongoing support from the parent and

moderate asset risks despite increase in

unsecured consumer lending.

• Ratings driven by institutional support and

equalized with those of its ultimate parent Banco

Santander, S.A.

• Profitability expected to improve, underpinned by

wide margins and moderate charge-off rates.

• Fitch expects that SCB will maintain solid capital

ratios given its higher-risk target markets

compared with the larger Nordic universal banks.

8

Both rating agencies characterize SCB Nordic’s outlook as “stable”

Credit rating highlights

Moody’s: A3 Fitch: A-

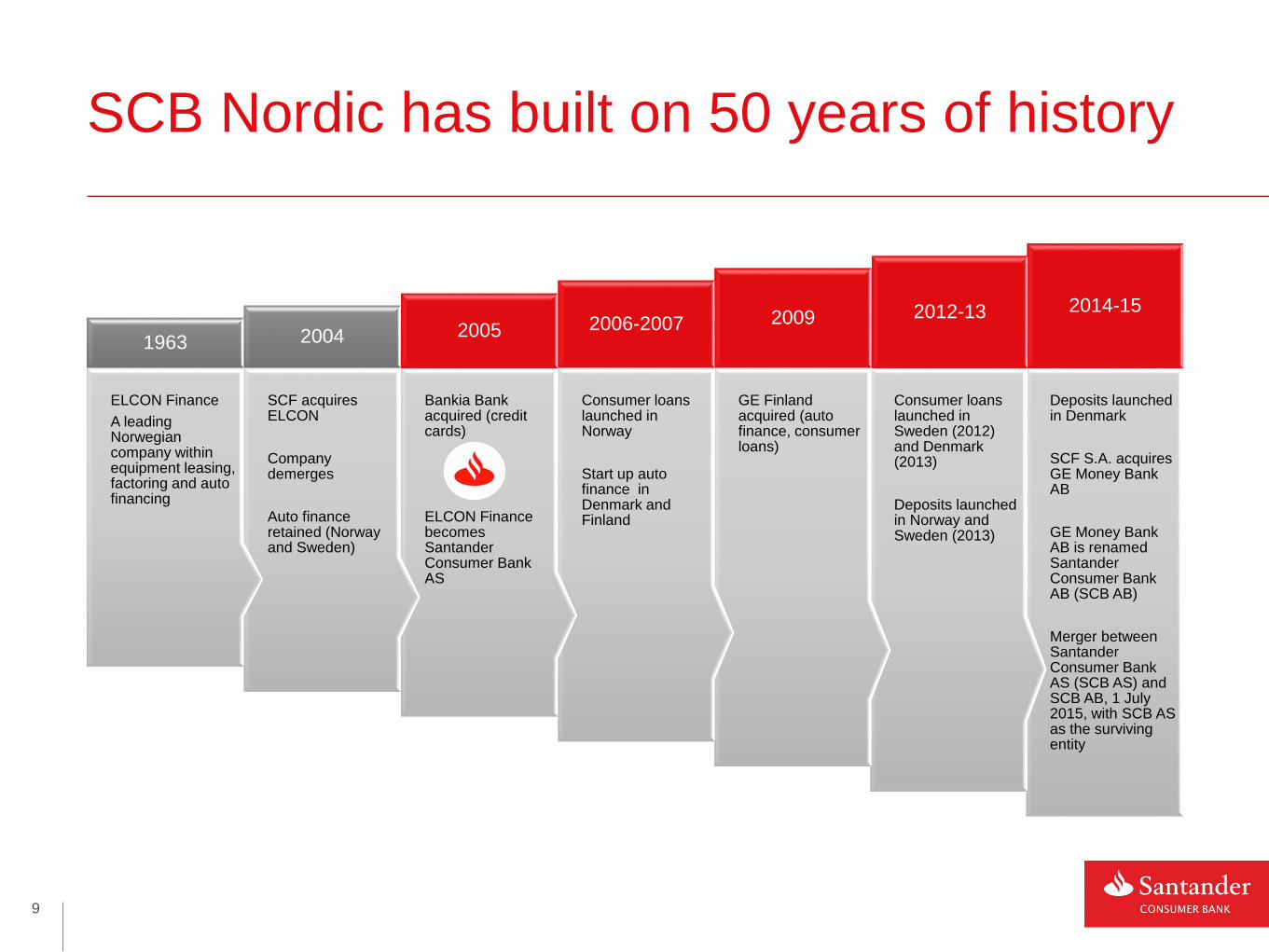

Deposits launched in Denmark

SCF S.A. acquires GE Money Bank AB

GE Money Bank AB is renamed Santander Consumer Bank AB (SCB AB)

Merger between Santander Consumer Bank AS (SCB AS) and SCB AB, 1 July 2015, with SCB AS as the surviving entity

2014-15

Consumer loans launched in Sweden (2012) and Denmark (2013)

Deposits launched in Norway and Sweden (2013)

2012-13

GE Finland acquired (auto finance, consumer loans)

2009

Consumer loans launched in Norway

Start up auto finance in Denmark and Finland

2006-2007

Bankia Bank acquired (credit cards)

ELCON Finance becomes Santander Consumer Bank AS

2005

SCF acquires ELCON

Company demerges

Auto finance retained (Norway and Sweden)

2004

ELCON Finance

A leading Norwegian company within equipment leasing, factoring and auto financing

1963

SCB Nordic has built on 50 years of history

9

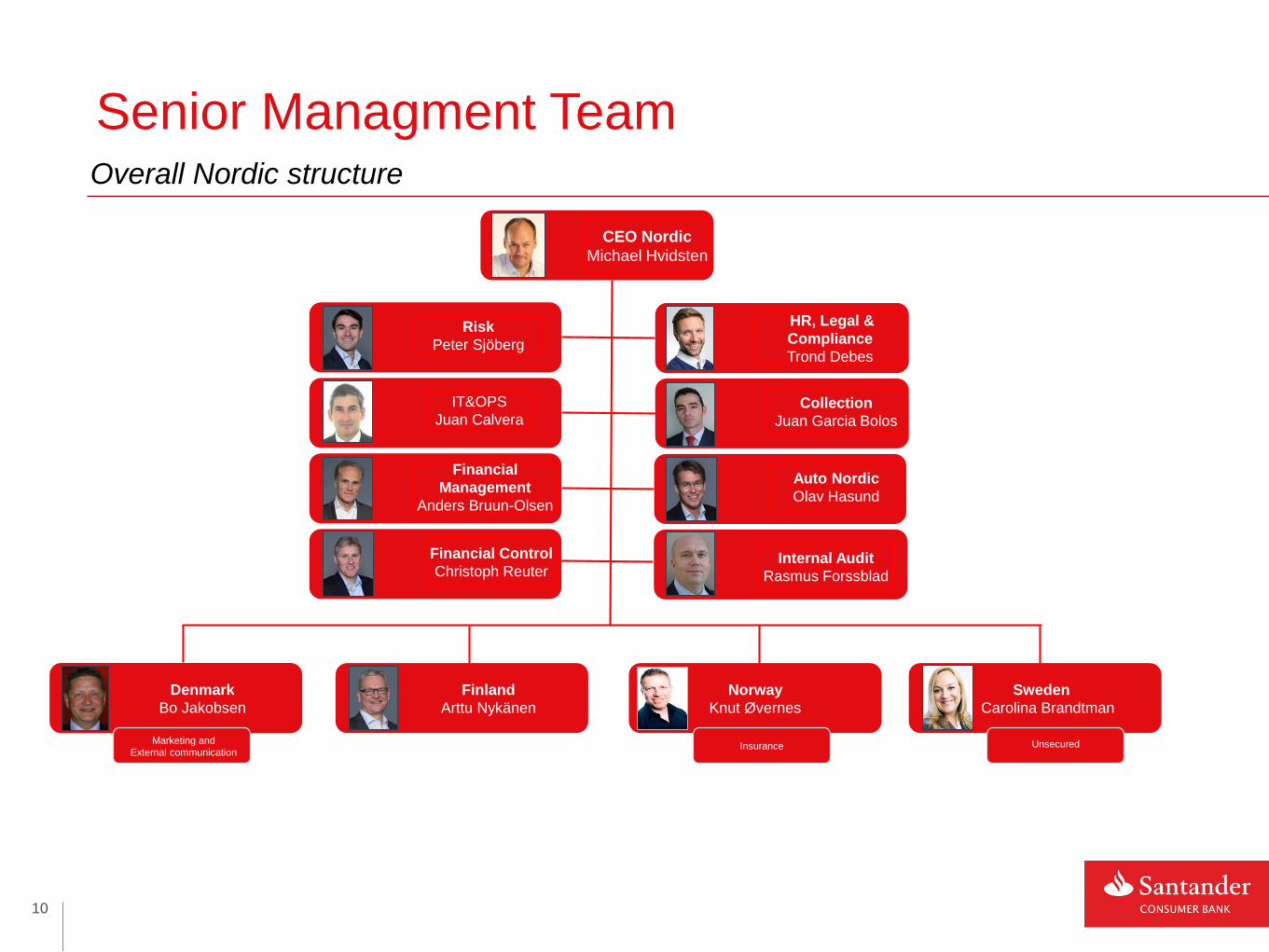

Denmark

Bo Jakobsen

Finland

Arttu Nykänen

Norway

Knut Øvernes

Sweden

Carolina Brandtman

Financial

Management

Anders Bruun-Olsen

Risk

Peter Sjöberg

IT&OPS

Juan Calvera

Financial Control

Christoph Reuter

HR, Legal &

Compliance

Trond Debes

Collection

Juan Garcia Bolos

Internal Audit

Rasmus Forssblad

CEO Nordic

Michael Hvidsten

Auto Nordic

Olav Hasund

Marketing and

External communicationUnsecuredInsurance

Senior Managment TeamOverall Nordic structure

10

The merger with GE in 2015 strengthened the unsecured business significantly

Diversification is central to our business model

Geographical distribution of Gross OutstandingLoans H1 2016

Product distribution of Gross Outstanding Loans H1 2016

43%

23%

15%

20%

Norway Sweden Finland Denmark

75%

25%

Secured Unsecured

11

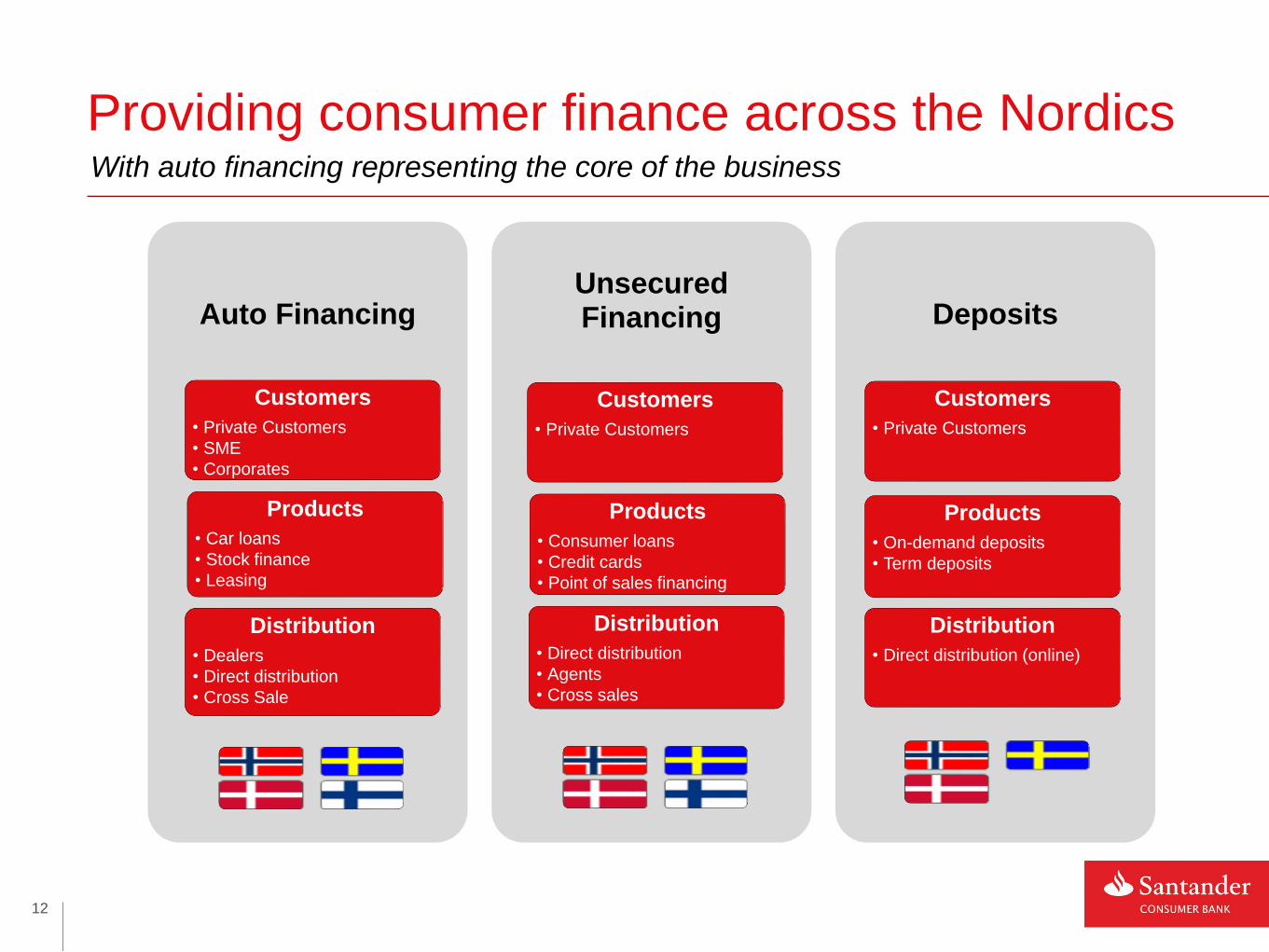

Secured: Auto and Stock Finance

Unsecured: Sales Finance, Credit Cards and Direct Lending

Providing consumer finance across the NordicsWith auto financing representing the core of the business

Auto Financing

Customers

• Private Customers

• SME

• Corporates

Products

• Car loans

• Stock finance

• Leasing

Distribution

• Dealers

• Direct distribution

• Cross Sale

Unsecured Financing

Customers

• Private Customers

Products

• Consumer loans

• Credit cards

• Point of sales financing

Distribution

• Direct distribution

• Agents

• Cross sales

Deposits

Customers

• Private Customers

Products

• On-demand deposits

• Term deposits

Distribution

• Direct distribution (online)

12

The Nordic auto finance marketSantander’s market share and main competitors

53 %

Market leading position provides

economy of scale

33%

12%19%

31%

Market shares

and position

Market shares

and position

Market shares

and position

Market shares

and position

#1

#1

#1

#4

13

•Source Norway: Internal calculations based on data from Finansieringsselskapenes Forening

•Source Finland: Internal calculations based on data from Finnish Transportation Safety Agency (Trafi)

•Source Denmark: Internal calculations based on data from Finans og Leasing

•Source Sweden: Internal calculations based on data from Finansbolagens Förening

31 %

20 %

10 %

9 %9 %

21 %

Norwegian market

Santander Consumer Bank DNB Finans

Nordea Finans Norge Sparebank 1 Gruppen

VW Møller Bilfinans Others (incl captives)

19 %18 %15 %

9 %39 %

Danish market

Santander Consumer BankJyske FinansNordea FinansNordaniaOthers (incl captives)

33 %

26 %

12 %7 %

22 %

Finnish market

Santander Consumer Bank OP Financial Group

Nordea Danske Finance

Others (incl captives)

12 %22 %15 %

14 %37 %

Swedish market

Santander Consumer Bank Volvo Finans

Volkswagen Finans DNB

Others (incl captives)

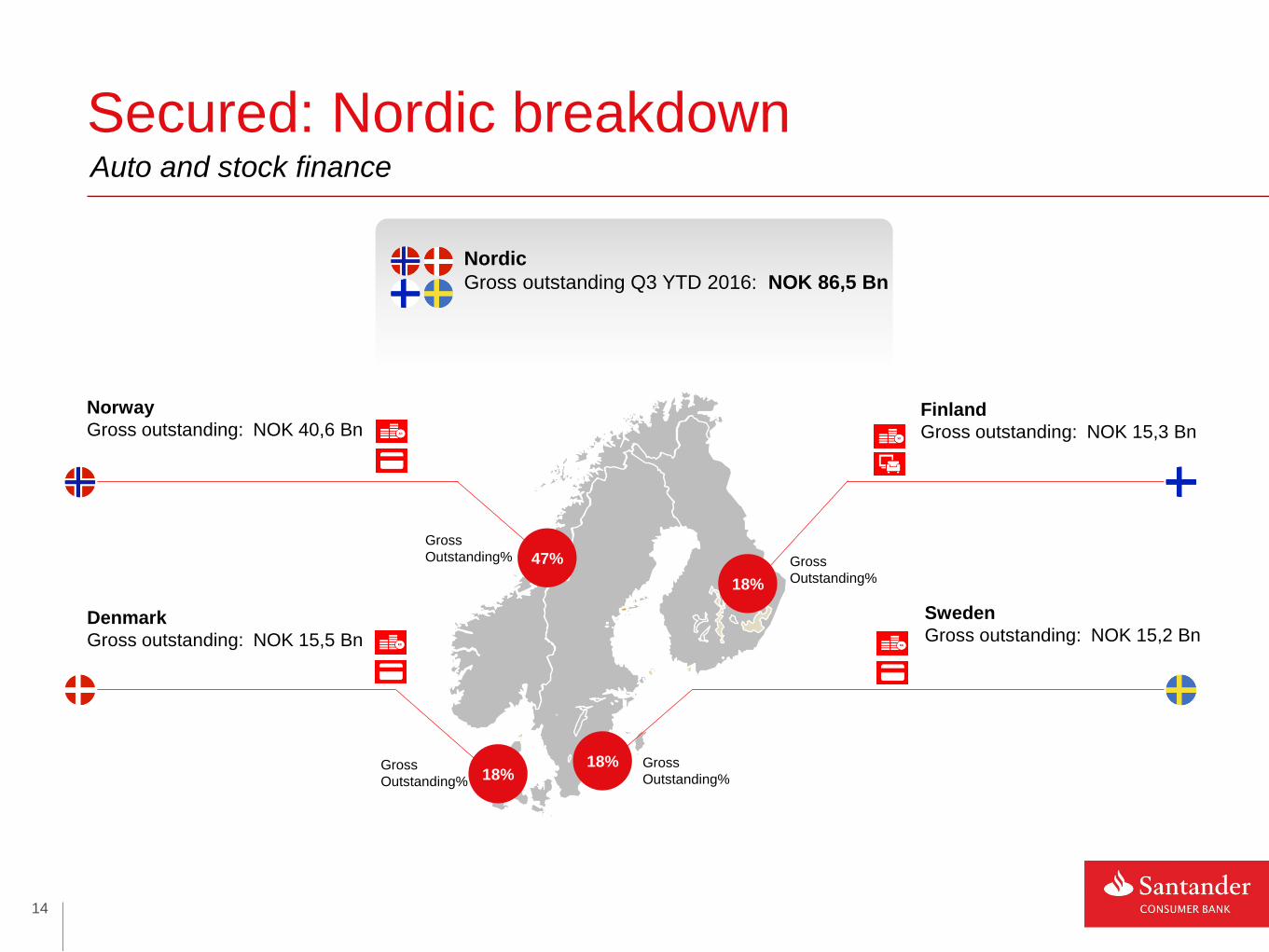

Secured: Nordic breakdownAuto and stock finance

53 %

Norway

Gross outstanding: NOK 40,6 Bn

Denmark

Gross outstanding: NOK 15,5 Bn

Finland

Gross outstanding: NOK 15,3 Bn

Sweden

Gross outstanding: NOK 15,2 Bn

Nordic

Gross outstanding Q3 YTD 2016: NOK 86,5 Bn

Gross

Outstanding%18%

Gross

Outstanding%

18%18%

Gross

Outstanding% 47%

Gross

Outstanding%

14

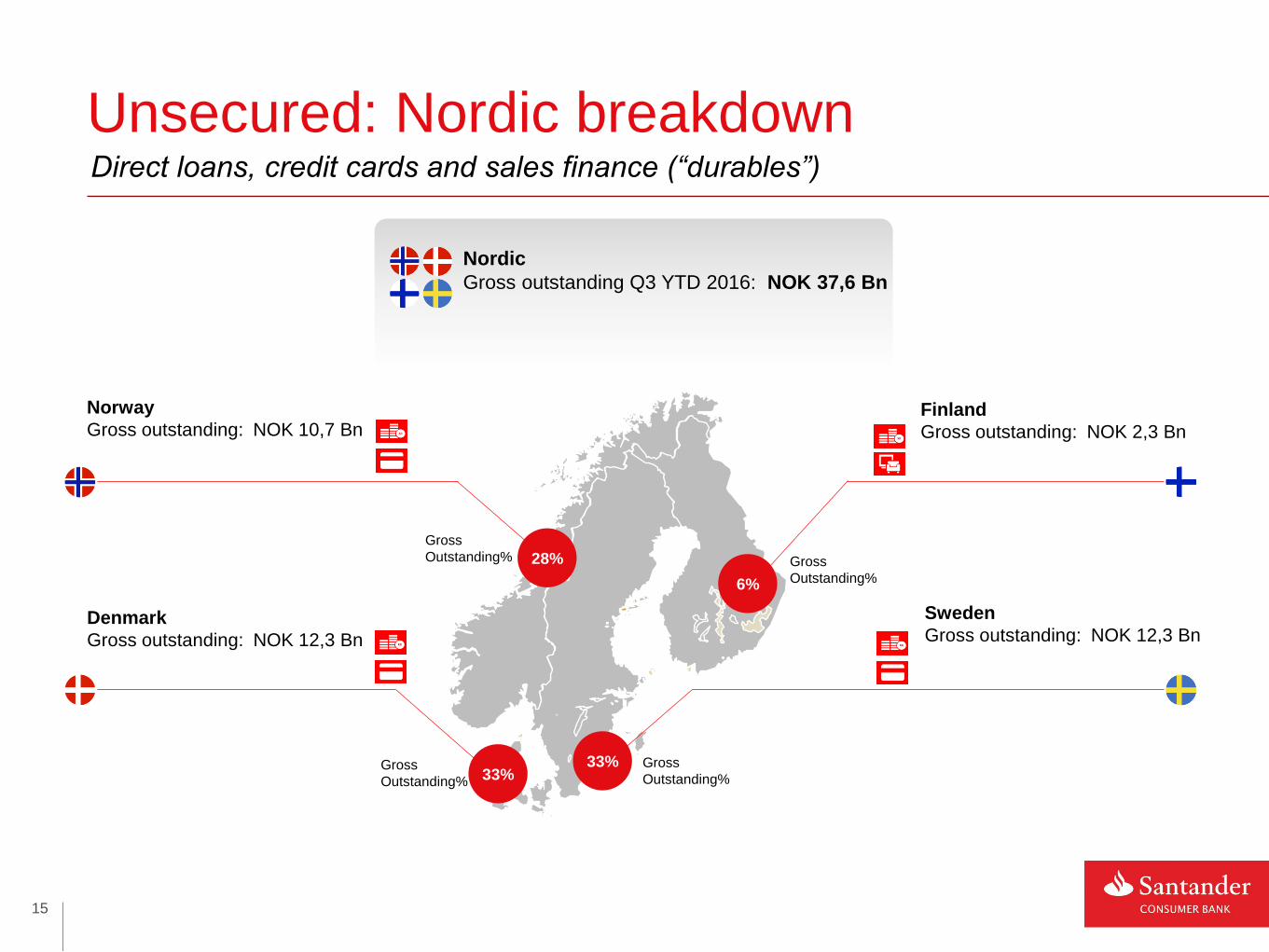

Unsecured: Nordic breakdownDirect loans, credit cards and sales finance (“durables”)

53 %

Norway

Gross outstanding: NOK 10,7 Bn

Denmark

Gross outstanding: NOK 12,3 Bn

Finland

Gross outstanding: NOK 2,3 Bn

Sweden

Gross outstanding: NOK 12,3 Bn

Nordic

Gross outstanding Q3 YTD 2016: NOK 37,6 Bn

Gross

Outstanding%6%

Gross

Outstanding%

33%33%

Gross

Outstanding% 28%

Gross

Outstanding%

15

1. Santander Consumer Bank AS, Nordic (“SCB Nordic”)

2. Risk Management

3. Financial information

4. Appendix: Banco Santander & Santander Consumer Finance

5. Appendix: Contacts

Content

16

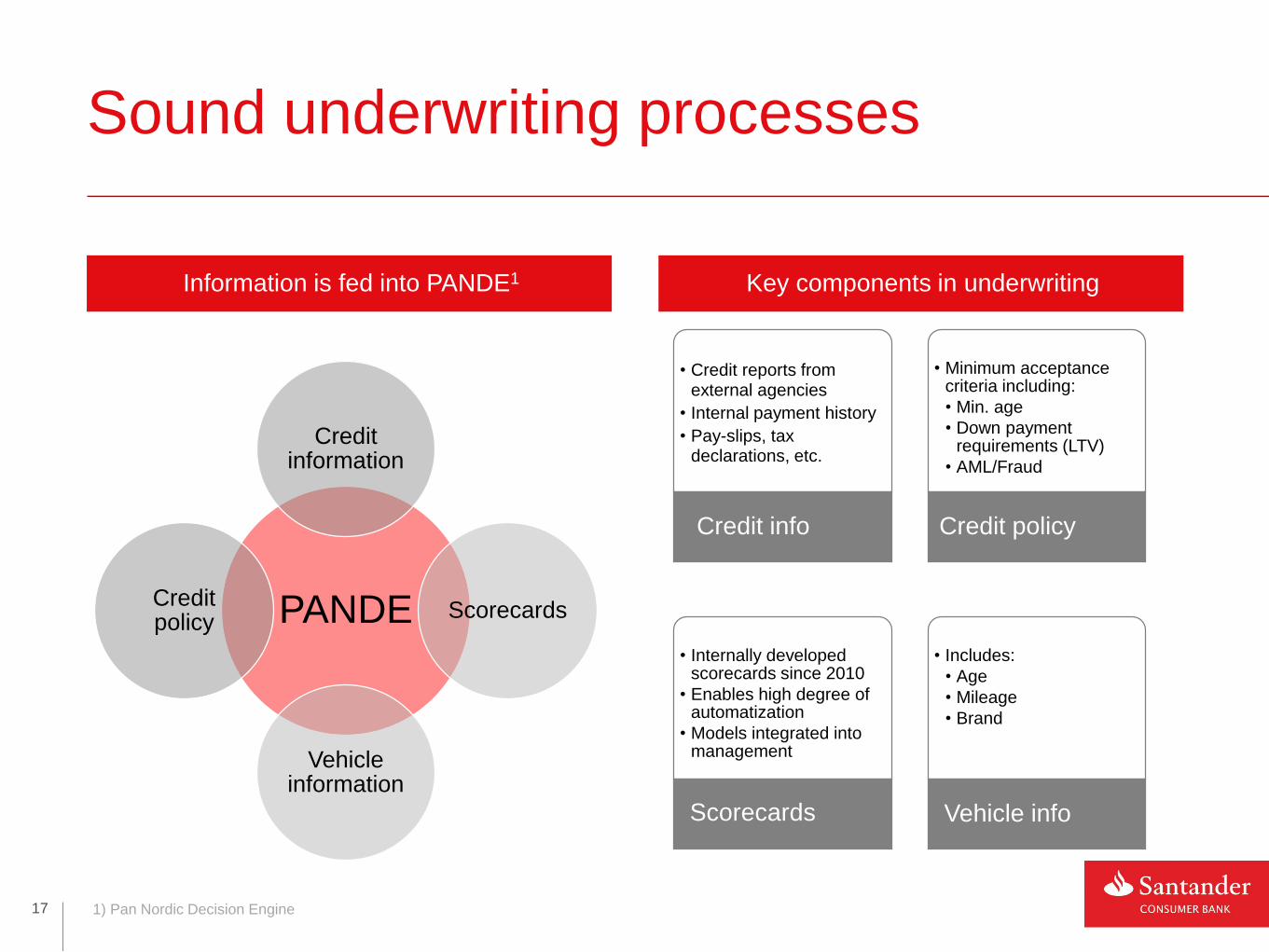

PANDE

Credit information

Scorecards

Vehicle information

Credit policy

Sound underwriting processes

Information is fed into PANDE1 Key components in underwriting

• Credit reports from external agencies

• Internal payment history

• Pay-slips, tax declarations, etc.

Credit info

• Minimum acceptance criteria including:

• Min. age

• Down payment requirements (LTV)

• AML/Fraud

Credit policy

• Internally developed scorecards since 2010

• Enables high degree of automatization

• Models integrated into management

Scorecards

• Includes:

• Age

• Mileage

• Brand

Vehicle info

17 1) Pan Nordic Decision Engine

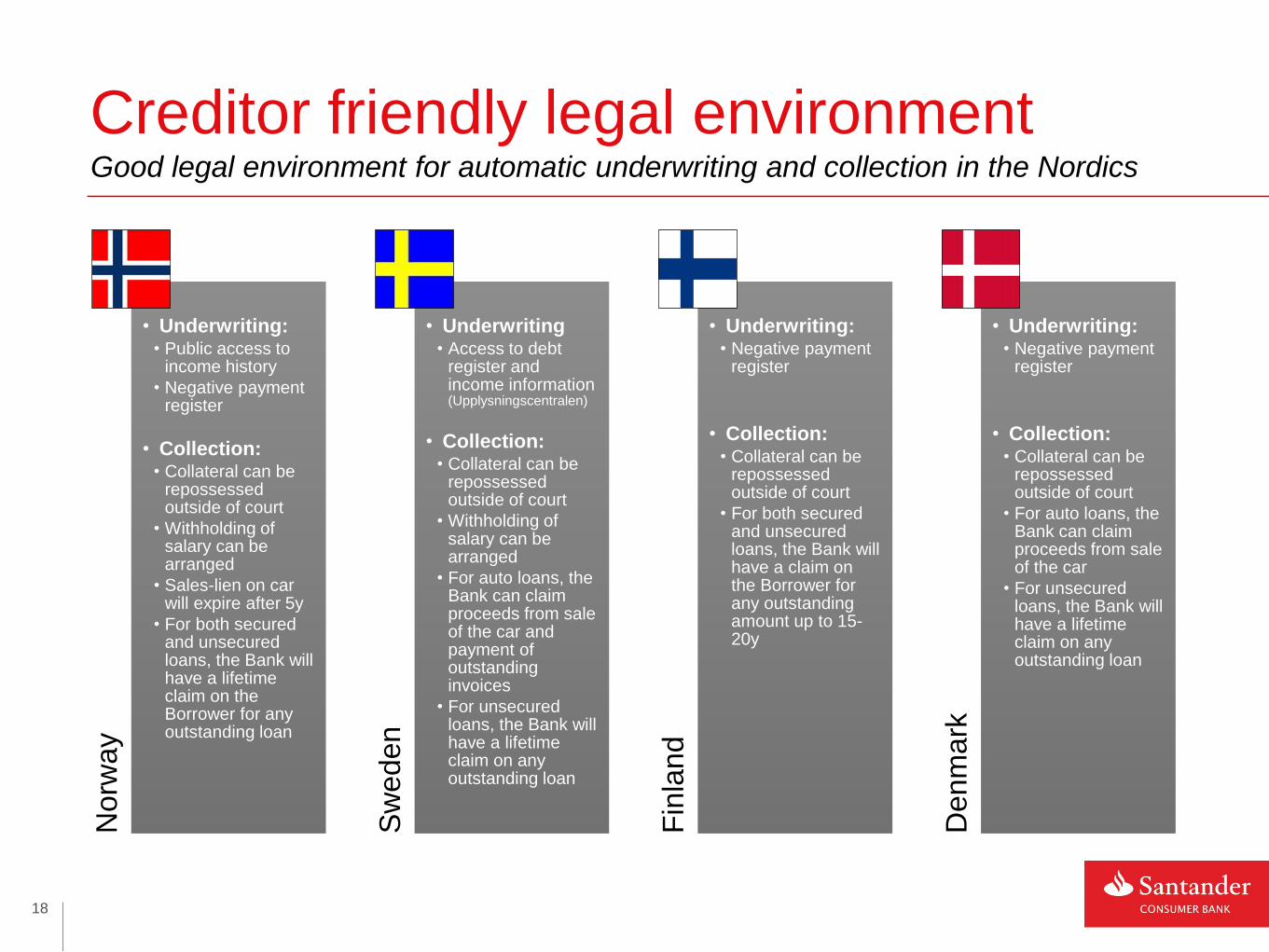

Norw

ay

• Underwriting:• Public access to

income history

• Negative payment register

• Collection:• Collateral can be

repossessed outside of court

• Withholding of salary can be arranged

• Sales-lien on car will expire after 5y

• For both secured and unsecured loans, the Bank will have a lifetime claim on the Borrower for any outstanding loan

Sw

eden

• Underwriting• Access to debt

register and income information (Upplysningscentralen)

• Collection:• Collateral can be

repossessed outside of court

• Withholding of salary can be arranged

• For auto loans, the Bank can claim proceeds from sale of the car and payment of outstanding invoices

• For unsecured loans, the Bank will have a lifetime claim on any outstanding loan

Fin

land

• Underwriting:• Negative payment

register

• Collection:• Collateral can be

repossessed outside of court

• For both secured and unsecured loans, the Bank will have a claim on the Borrower for any outstanding amount up to 15-20y

Denm

ark

• Underwriting:• Negative payment

register

• Collection:• Collateral can be

repossessed outside of court

• For auto loans, the Bank can claim proceeds from sale of the car

• For unsecured loans, the Bank will have a lifetime claim on any outstanding loan

Creditor friendly legal environment Good legal environment for automatic underwriting and collection in the Nordics

18

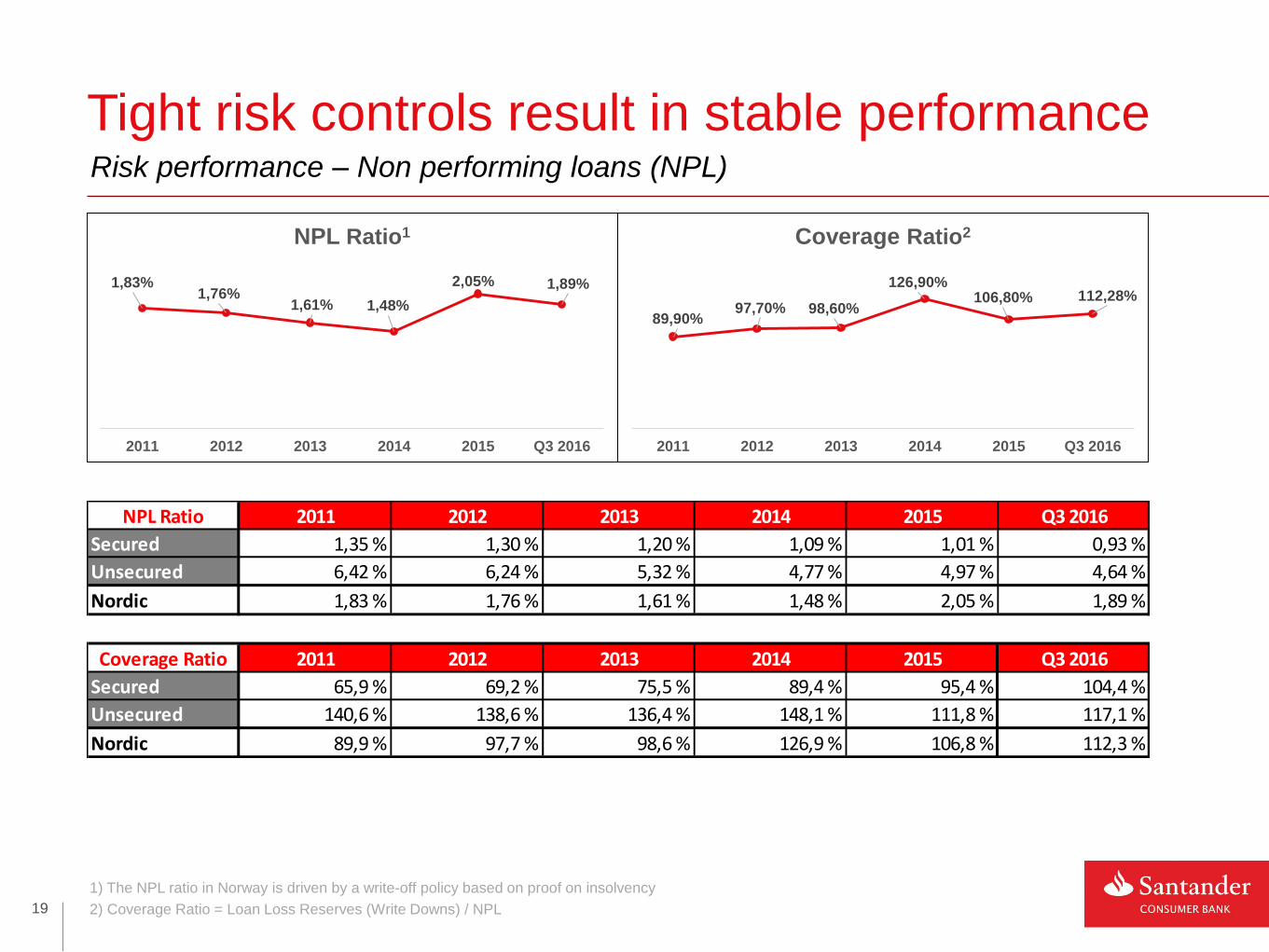

Risk performance – Non performing loans (NPL)

Tight risk controls result in stable performance

1,83%1,76%

1,61% 1,48%

2,05% 1,89%

2011 2012 2013 2014 2015 Q3 2016

NPL Ratio1

89,90%97,70% 98,60%

126,90%106,80% 112,28%

2011 2012 2013 2014 2015 Q3 2016

Coverage Ratio2

19

1) The NPL ratio in Norway is driven by a write-off policy based on proof on insolvency

2) Coverage Ratio = Loan Loss Reserves (Write Downs) / NPL

NPL Ratio 2011 2012 2013 2014 2015 Q3 2016

Secured 1,35 % 1,30 % 1,20 % 1,09 % 1,01 % 0,93 %

Unsecured 6,42 % 6,24 % 5,32 % 4,77 % 4,97 % 4,64 %

Nordic 1,83 % 1,76 % 1,61 % 1,48 % 2,05 % 1,89 %

Coverage Ratio 2011 2012 2013 2014 2015 Q3 2016

Secured 65,9 % 69,2 % 75,5 % 89,4 % 95,4 % 104,4 %

Unsecured 140,6 % 138,6 % 136,4 % 148,1 % 111,8 % 117,1 %

Nordic 89,9 % 97,7 % 98,6 % 126,9 % 106,8 % 112,3 %

1. Santander Consumer Bank AS, Nordic (“SCB Nordic”)

2. Risk Management

3. Financial information

4. Appendix: Banco Santander & Santander Consumer Finance

5. Appendix: Contacts

Content

20

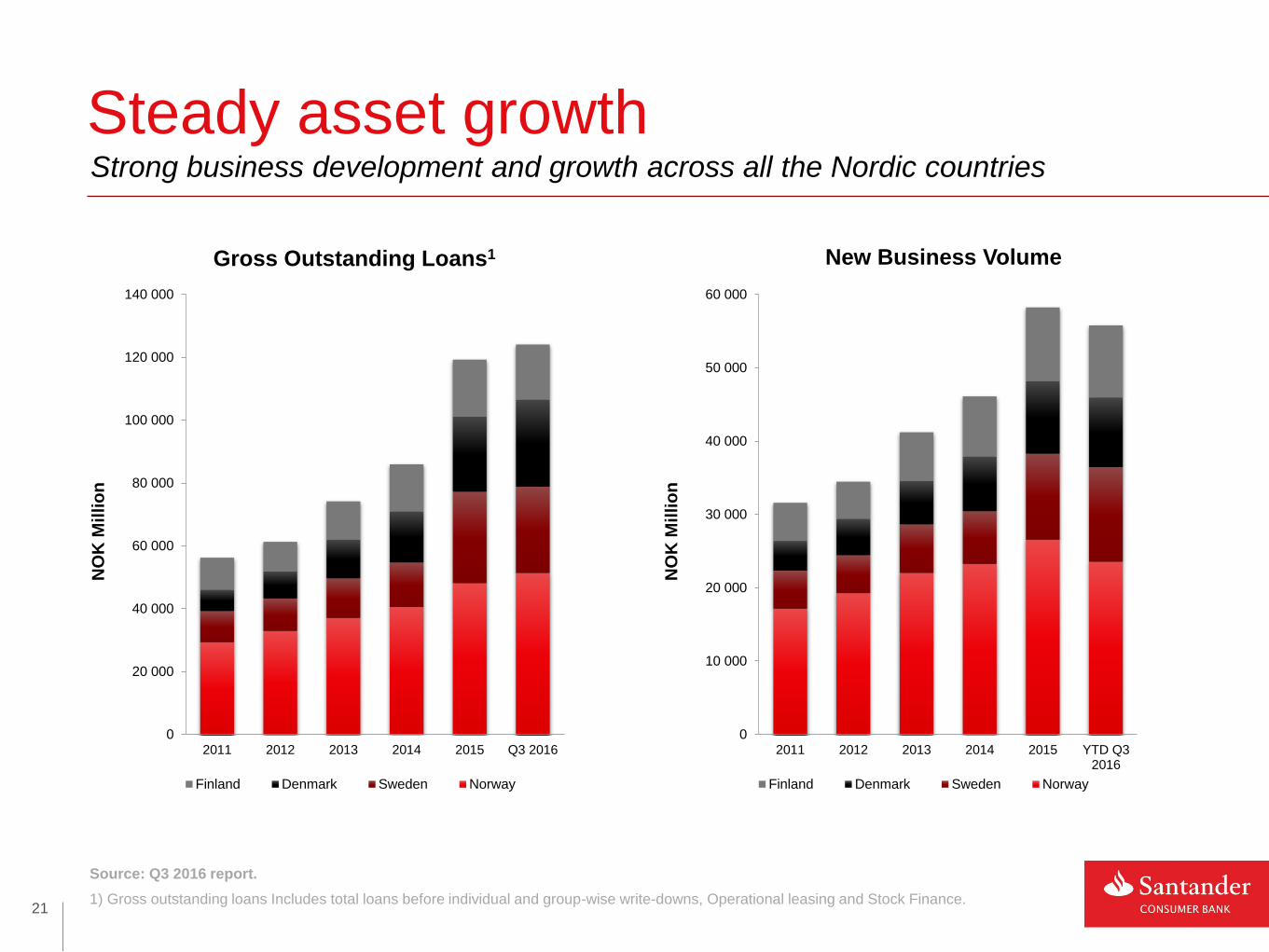

Strong business development and growth across all the Nordic countries

Steady asset growth

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

2011 2012 2013 2014 2015 Q3 2016

NO

K M

illio

n

Gross Outstanding Loans1

Finland Denmark Sweden Norway

0

10 000

20 000

30 000

40 000

50 000

60 000

2011 2012 2013 2014 2015 YTD Q32016

NO

K M

illio

n

New Business Volume

Finland Denmark Sweden Norway

21

Source: Q3 2016 report.

1) Gross outstanding loans Includes total loans before individual and group-wise write-downs, Operational leasing and Stock Finance.

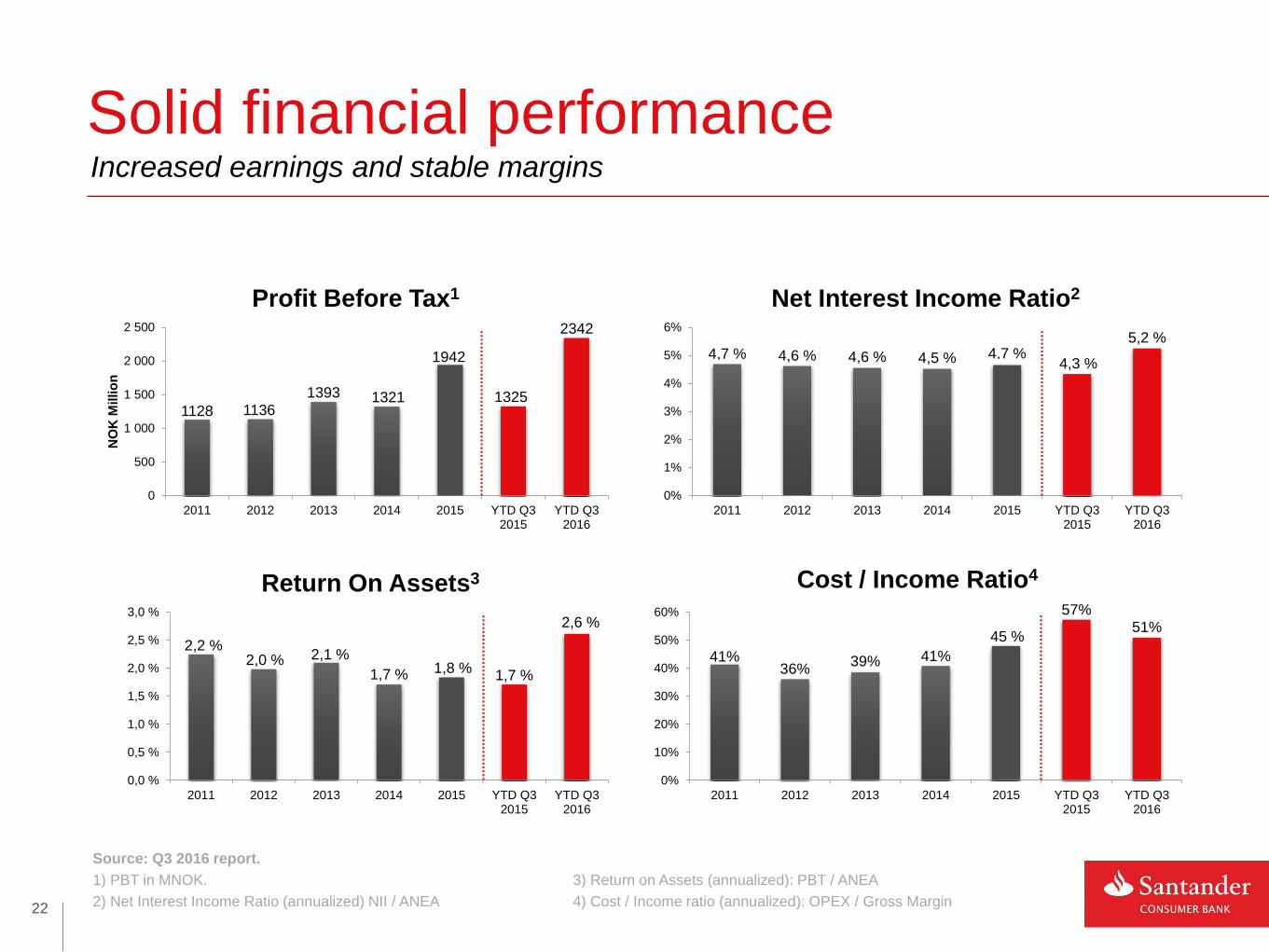

Increased earnings and stable margins

Solid financial performance

4,7 % 4,6 % 4,6 % 4,5 % 4,7 %4,3 %

5,2 %

0%

1%

2%

3%

4%

5%

6%

2011 2012 2013 2014 2015 YTD Q32015

YTD Q32016

Net Interest Income Ratio2

41%36%

39% 41%

45 %

57%51%

0%

10%

20%

30%

40%

50%

60%

2011 2012 2013 2014 2015 YTD Q32015

YTD Q32016

Cost / Income Ratio4

1128 1136

1393 1321

1942

1325

2342

0

500

1 000

1 500

2 000

2 500

2011 2012 2013 2014 2015 YTD Q32015

YTD Q32016

NO

K M

illio

n

Profit Before Tax1

2,2 %2,0 % 2,1 %

1,7 % 1,8 %1,7 %

2,6 %

0,0 %

0,5 %

1,0 %

1,5 %

2,0 %

2,5 %

3,0 %

2011 2012 2013 2014 2015 YTD Q32015

YTD Q32016

Return On Assets3

22

Source: Q3 2016 report.

1) PBT in MNOK.

2) Net Interest Income Ratio (annualized) NII / ANEA

3) Return on Assets (annualized): PBT / ANEA

4) Cost / Income ratio (annualized): OPEX / Gross Margin

9,69%10,90%

15,26% 14,99%

13,06%13,86%

17,77% 17,46%

13,71%14,12%

19,14% 18,80%

10,27%10,78%

11,43% 11,25%

0%

5%

10%

15%

20%

25%

2013 2014 2015 Q3 2016

CET1 Tier 1 Tier 2 Leverage ratio

• Santander Consumer Bank AS is regulated by the

Norwegian FSA

• Norway follows the CRD IV framework with national

adjustments

• The national adjustments represent stricter requirements

than the CRD IV framework

• Capital ratio requirements under Pillar 1 in Norway are

(including buffer requirements):

• CET1-ratio should be minimum 11,5%1

• Tier1-ratio should be minimum 13%

• Tier2-ratio should be minimum 15%

• In addition the bank also needs to meet capital

requirements under Pillar 2 (CET1)

• SCB reports leverage ratio to the Norwegian FSA, but

this is not yet a requirement

• SCB has a strong leverage ratio compared with peers

Capital management

Capital ratios evolution Capital requirements in Norway

Meeting stricter Capital Requirements

23

1) From October 2016, the countercyclical buffer requirement in Norway will be calculated as a weighted average of the buffer requirements applicable in the countries where the bank operates. Due to this change, the CET1 requirement for SCB will fall from 11.5% to about 11% from October 2016

Key developments

• SCB Nordic approved as an A-IRB1 bank in December 2015

• The A-IRB approach is now used for the private auto portfolios in Norway, Sweden and Finland

• The remaining portfolios will gradually change from standard approach to A-IRB approach

• The change from standard approach to A-IRB- approach improved CET1-ratio from 13,5% to 15,26% per

December 2015

• We do not expect similar capital relief for the remaining portfolios

Capital managementSCB AS is now an A-IRB bank

24 1) A-IRB = Advance Internal Rating Based

Steadily increasing our self-funding share

Funding

Securitization

• 10 outstanding transactions across the Nordics

• Represents a stable funding source

• We expect securitization to account for approx. 20-25% of funding going forward

Senior Unsecured

• NOK 6 billion outstanding in the Norwegian bond market

• SEK 3,5 billion outstanding in the Swedish bond market

• EUR 1,75 billion outstanding from three Benchmark transactions issued under the EMTN Programme

Deposits

• In Norway deposits are guaranteed up to MNOK 2. In EU countries the guarantee is up to EUR 100,000

• NOK 39 billion across Norway, Sweden and Denmark

Self-funding pillars Funding composition

Self-funding ratio

22%

28%

50%

62%

70%

67%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2011 2012 2013 2014 2015 Q3 2016

33%

11%

34%

22%

-

20

40

60

80

100

120

2011 2012 2013 2014 2015 Q3 2016

NO

K b

illi

on

Parent funding Securitization Deposits Unsecured Bonds

Existing EMTN transactions benefit from parent guarantee. After the

stand-alone rating any new EMTN issuances will be without parent

guarantee.

25

1. Santander Consumer Bank AS, Nordic (“SCB Nordic”)

2. Risk Management

3. Financial information

4. Appendix: Banco Santander & Santander Consumer Finance

5. Appendix: Contacts

Content

26

27

Subjects

Banco Santander

Santander Consumer Finance

28

Santander, a leading financial group

Key Figures

Headcount 189,675

Branches (units) 12,391

Shareholders (millions) 3.92

Customers (millions) 124

Total assets (trill. €) 1.33

Sep’16

Attributable Profit 9M’16 (mill. €) 4,606

Underlying Profit* 9M’16 (mill. €) 4,975

(*) Excluding one-off items and contribution to the Single Resolution Fund (SRF) due to change in the scheduled contribution dates.

29

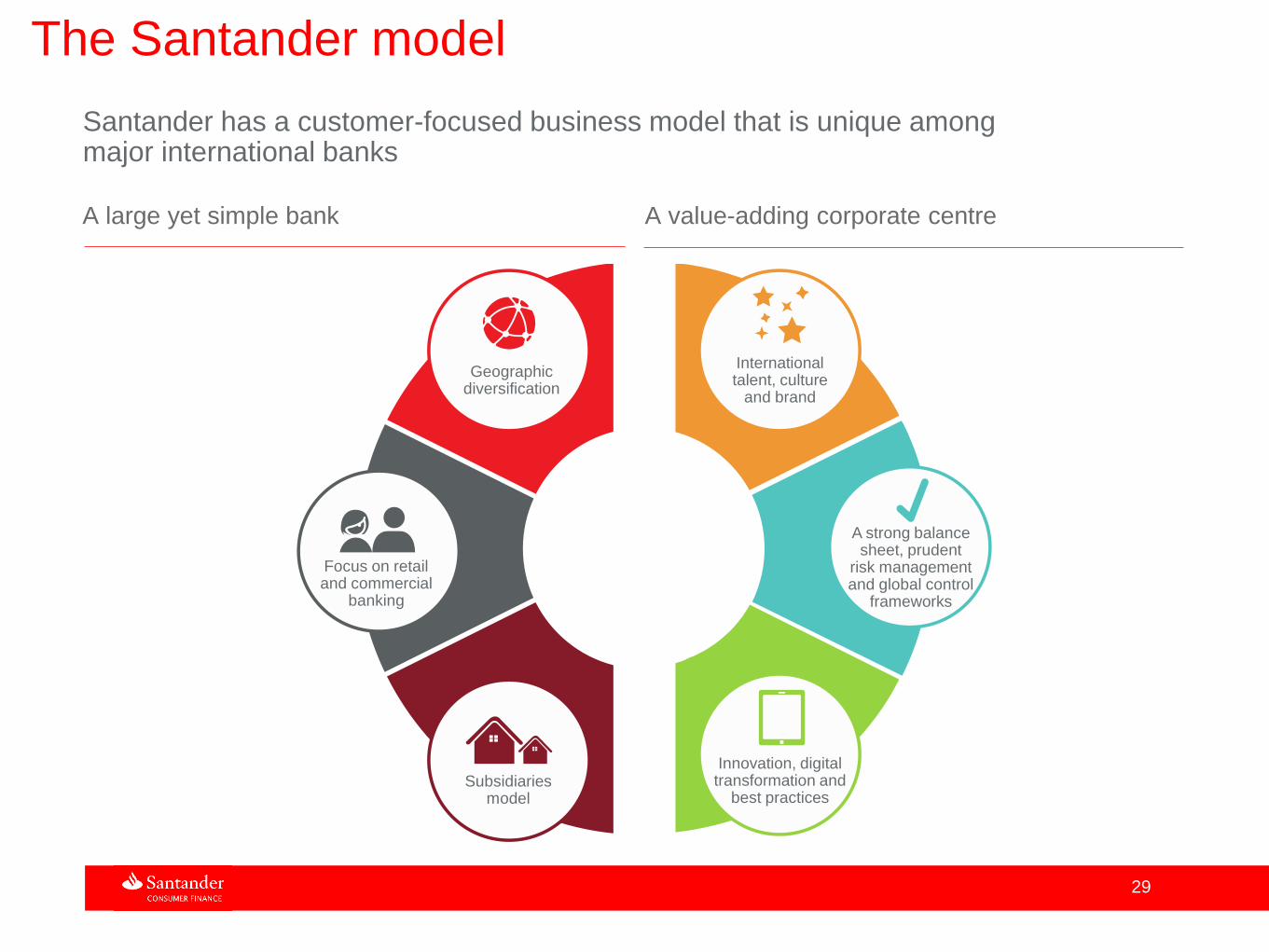

The Santander model

Santander has a customer-focused business model that is unique among major international banks

Geographicdiversification

Internationaltalent, culture

and brand

A strong balancesheet, prudent

risk managementand global control

frameworks

Focus on retailand commercial

banking

Subsidiariesmodel

Innovation, digitaltransformation and

best practices

A large yet simple bank A value-adding corporate centre

30

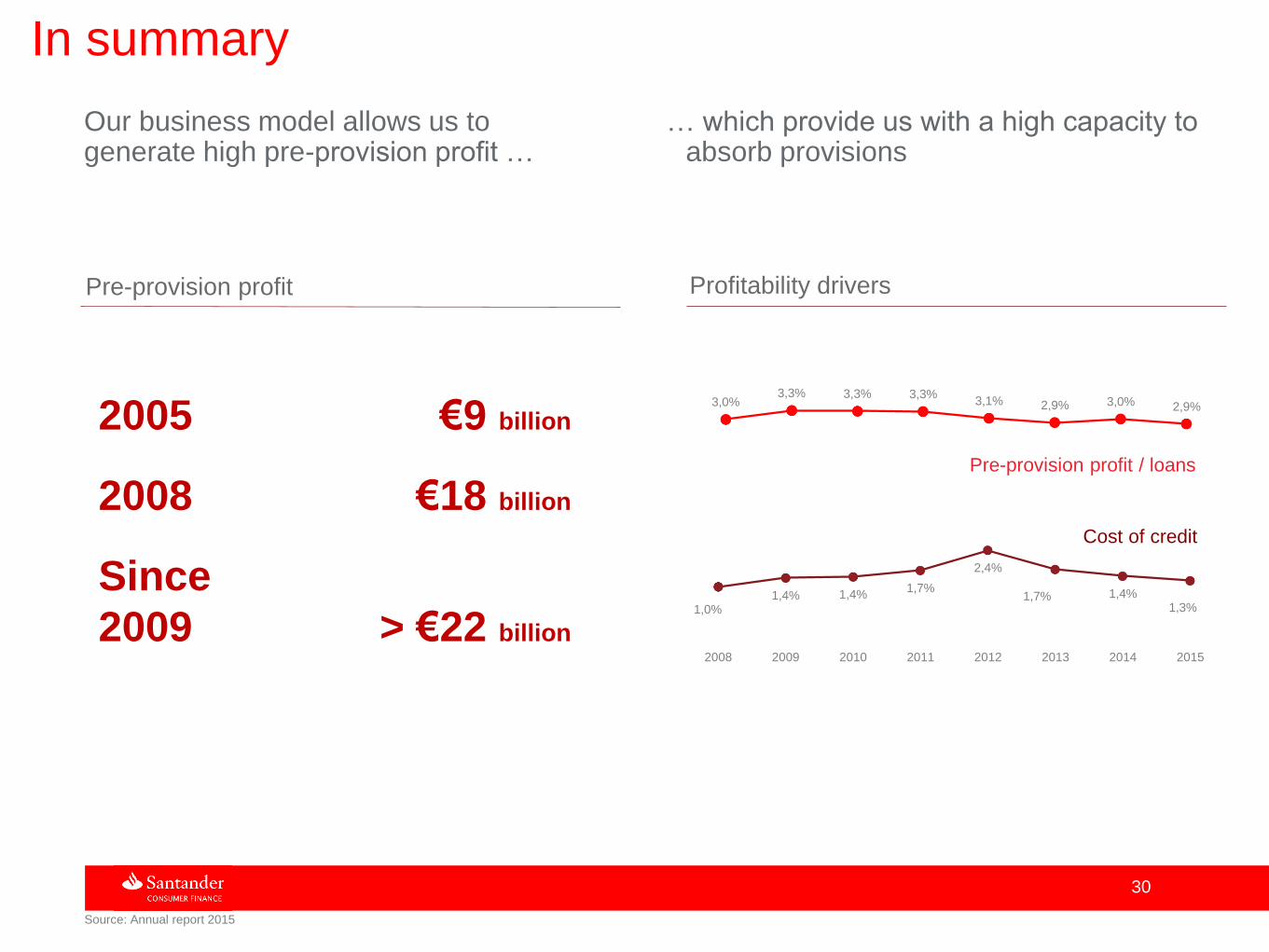

In summary

… which provide us with a high capacity to absorb provisions

Pre-provision profit Profitability drivers

Our business model allows us to generate high pre-provision profit …

Cost of credit

Pre-provision profit / loans

2005 €9 billion

2008 €18 billion

Since

2009 > €22 billion1,0%

1,4% 1,4%1,7%

2,4%

1,7% 1,4%1,3%

2008 2009 2010 2011 2012 2013 2014 2015

3,0%3,3% 3,3% 3,3%

3,1% 2,9% 3,0% 2,9%

Source: Annual report 2015

31

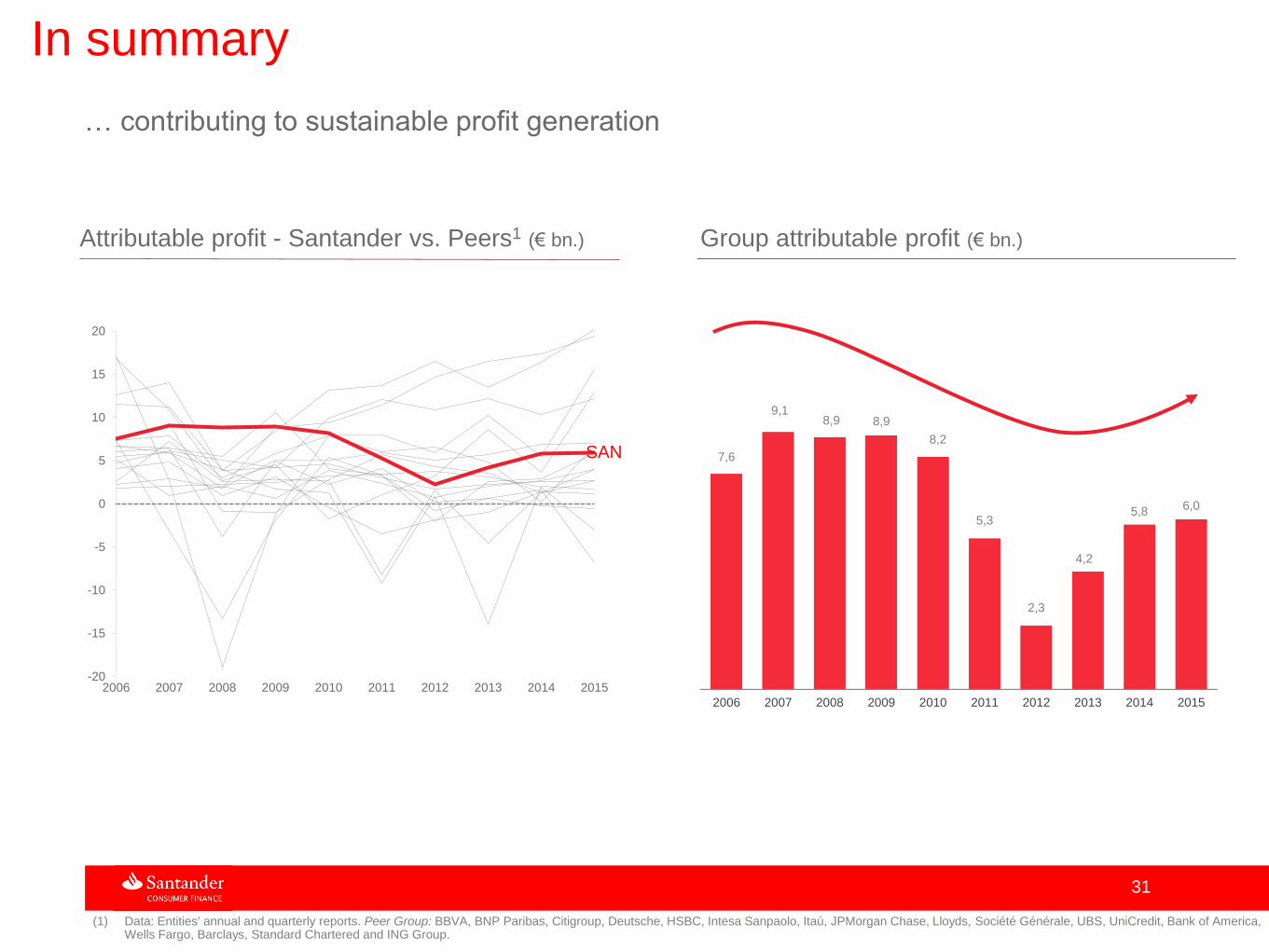

In summary

Attributable profit - Santander vs. Peers1 (€ bn.)

-20

-15

-10

-5

0

5

10

15

20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Group attributable profit (€ bn.)

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

7,6

9,18,9 8,9

8,2

5,3

2,3

4,2

5,8 6,0

SAN

(1) Data: Entities' annual and quarterly reports. Peer Group: BBVA, BNP Paribas, Citigroup, Deutsche, HSBC, Intesa Sanpaolo, Itaú, JPMorgan Chase, Lloyds, Société Générale, UBS, UniCredit, Bank of America, Wells Fargo, Barclays, Standard Chartered and ING Group.

… contributing to sustainable profit generation

32

9M'16 Financial Highlights

(*) Excluding one-off items and contribution to the Single Resolution Fund (SRF) due to change in the scheduled contribution dates. % change ona currency-neutral basis

33

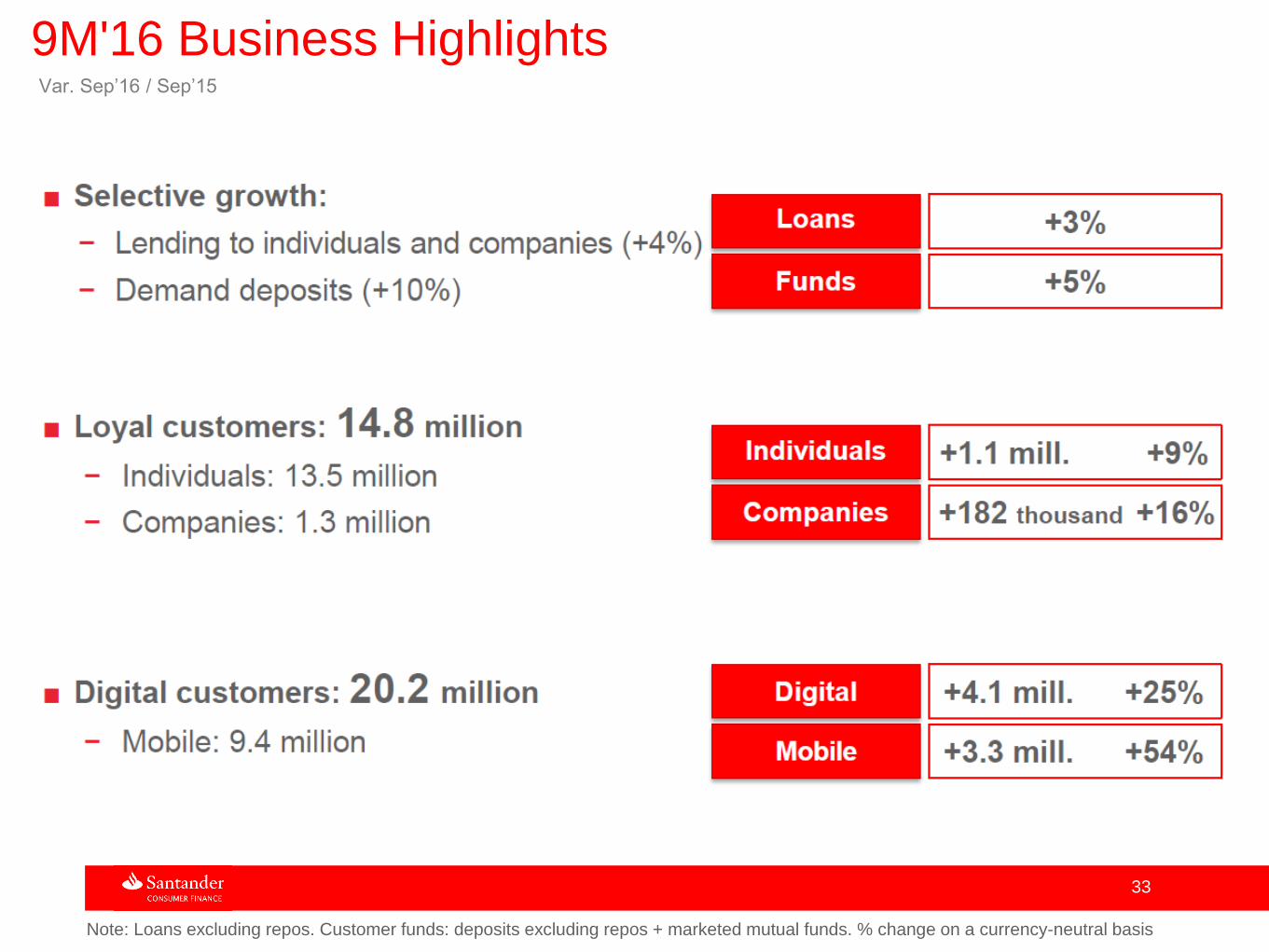

9M'16 Business HighlightsVar. Sep’16 / Sep’15

Note: Loans excluding repos. Customer funds: deposits excluding repos + marketed mutual funds. % change on a currency-neutral basis

34

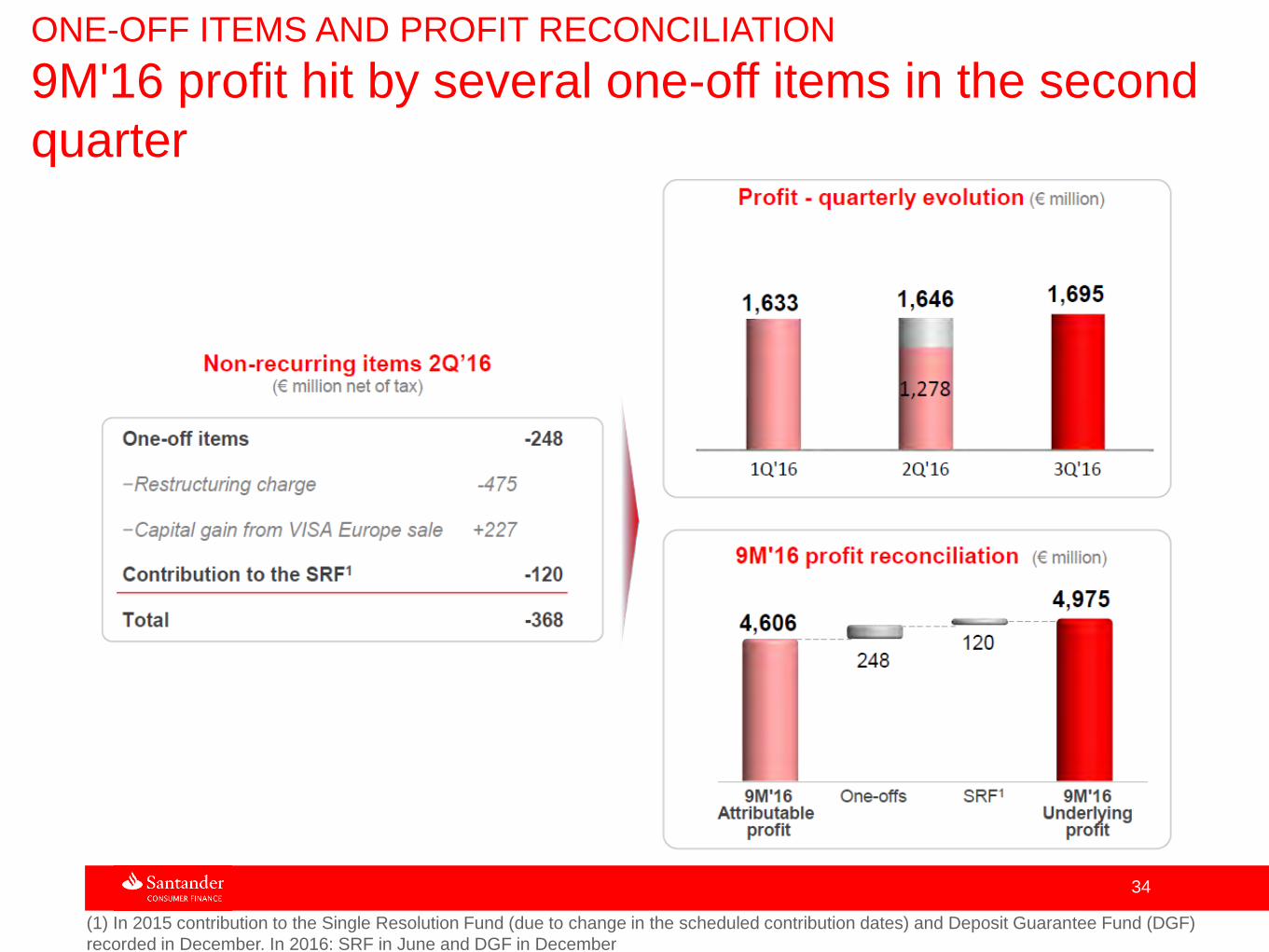

ONE-OFF ITEMS AND PROFIT RECONCILIATION

9M'16 profit hit by several one-off items in the second

quarter

(1) In 2015 contribution to the Single Resolution Fund (due to change in the scheduled contribution dates) and Deposit Guarantee Fund (DGF)

recorded in December. In 2016: SRF in June and DGF in December

35

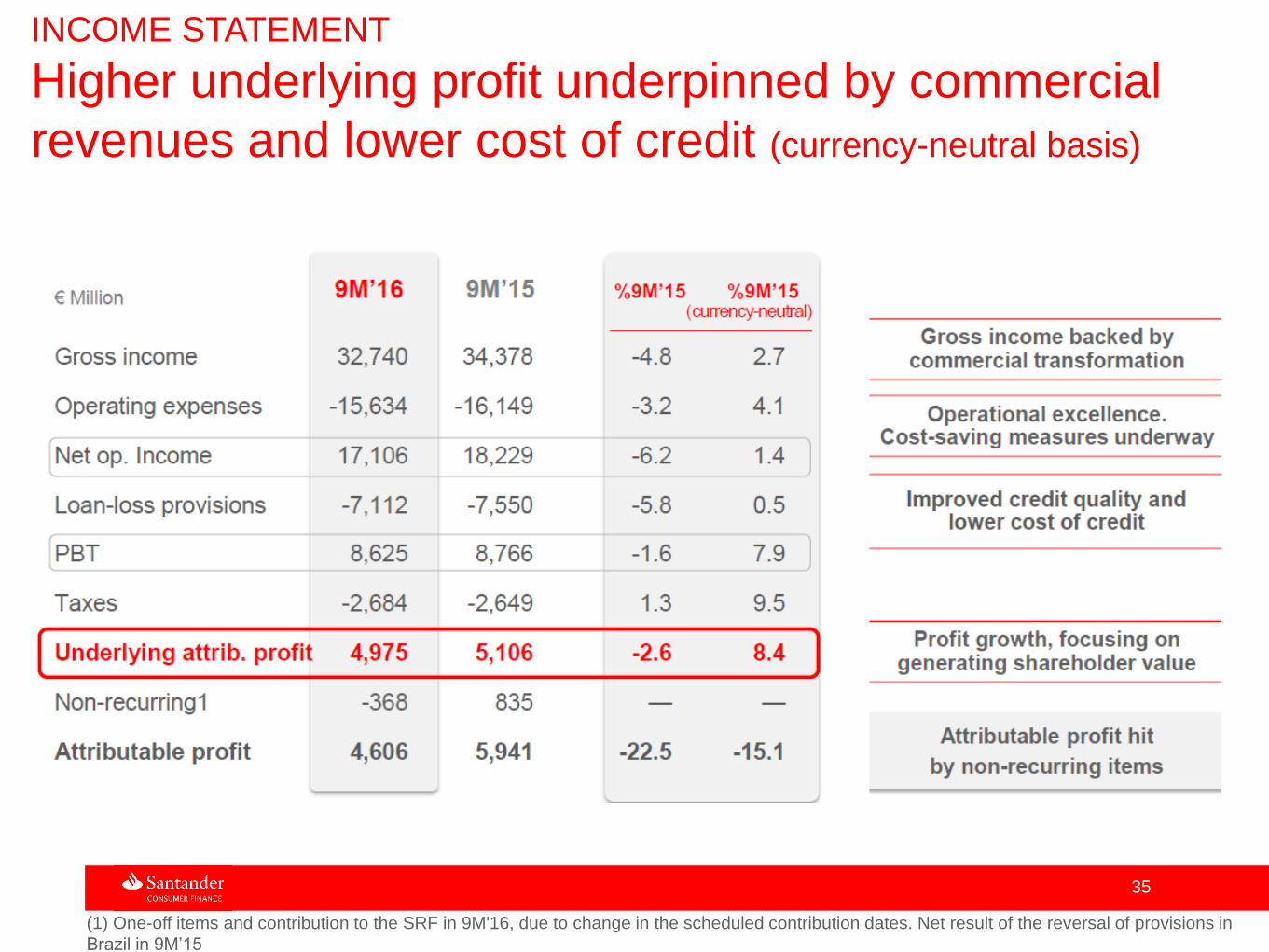

INCOME STATEMENT

Higher underlying profit underpinned by commercial

revenues and lower cost of credit (currency-neutral basis)

(1) One-off items and contribution to the SRF in 9M'16, due to change in the scheduled contribution dates. Net result of the reversal of provisions in

Brazil in 9M’15

36

On plan to deliver our 2016/2017 targets

(1) Currency neutral y-o-y change. (2) 2016(e), assuming an acceptance percentage of the script dividend equal to that in 2015

37

Subjects

Santander Consumer Finance

Banco Santander

38

Santander Consumer Finance

Santander Consumer Finance is the European leader

in the consumer finance industry …

… fully owned by Santander, one of the largest

financial groups in the world

Its core businesses are car finance and consumer

finance (durables financing, personal loans and

credit cards) …

… distributed mainly through point-of-sales, and

direct-to-consumer channels such as internet,

telemarketing platforms and branches.

39

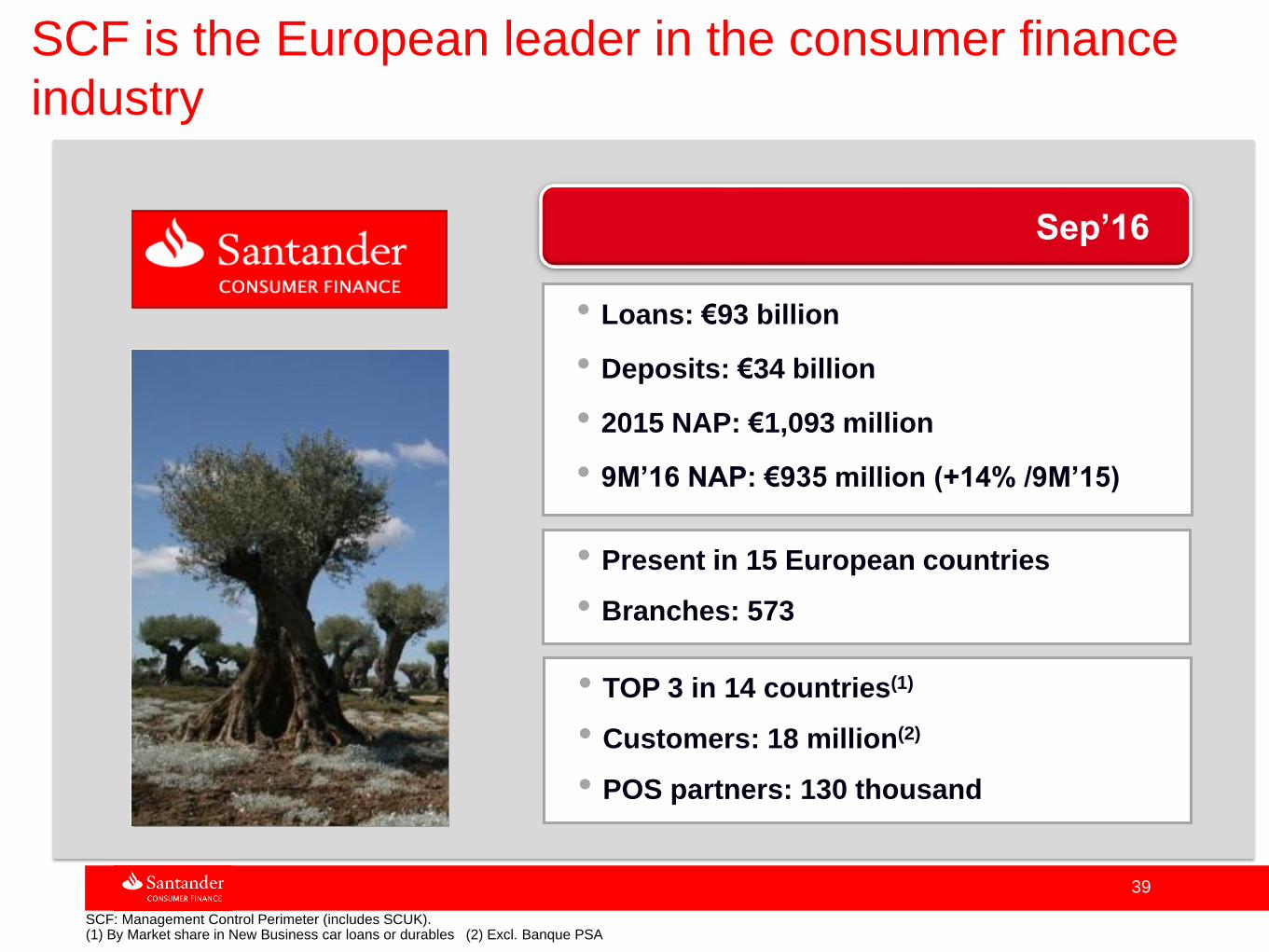

SCF is the European leader in the consumer finance

industry

SCF: Management Control Perimeter (includes SCUK).(1) By Market share in New Business car loans or durables (2) Excl. Banque PSA

Sep’16

• Present in 15 European countries

• Branches: 573

• Loans: €93 billion

• Deposits: €34 billion

• 2015 NAP: €1,093 million

• 9M’16 NAP: €935 million (+14% /9M’15)

• TOP 3 in 14 countries(1)

• Customers: 18 million(2)

• POS partners: 130 thousand

40

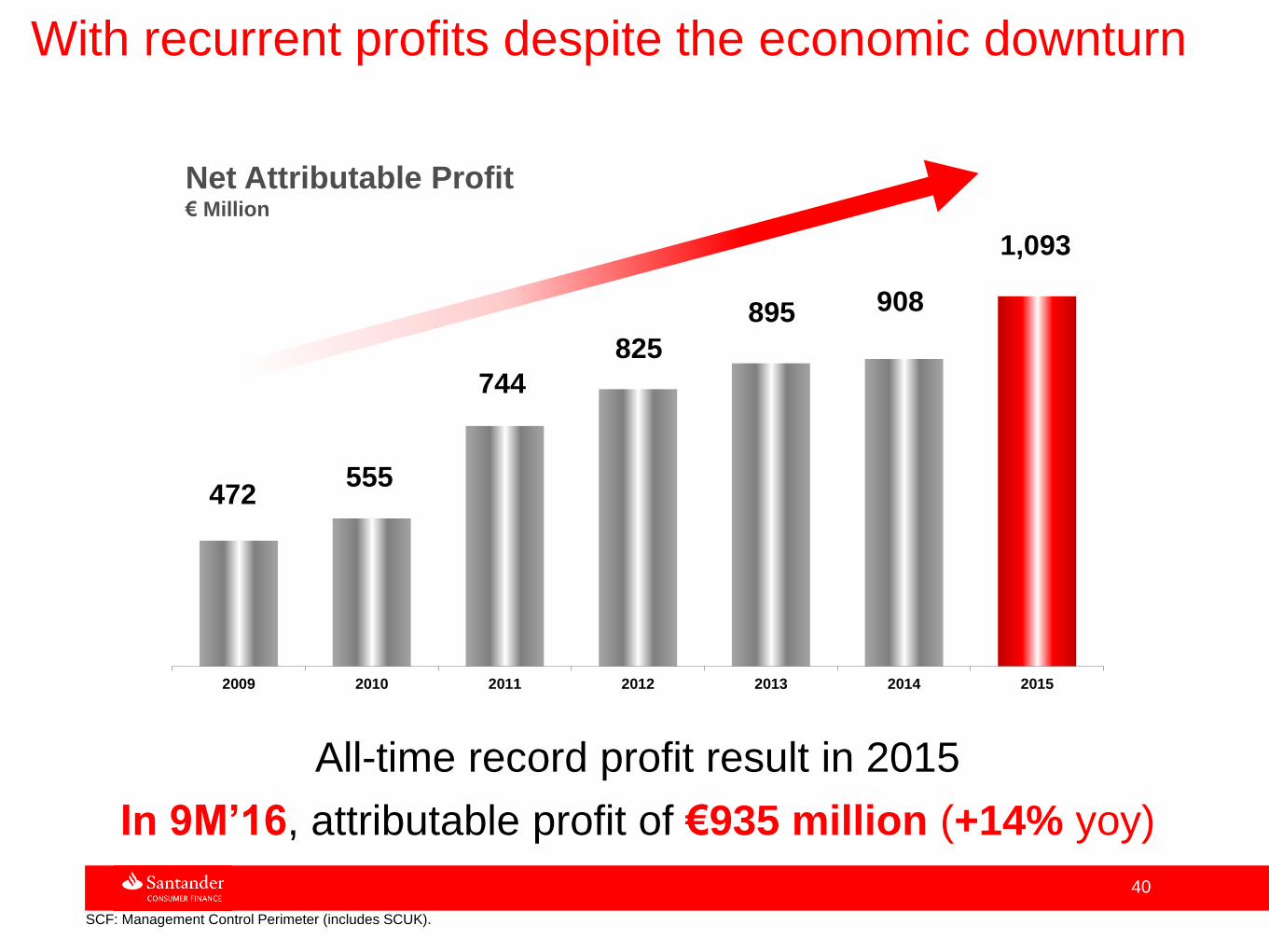

With recurrent profits despite the economic downturn

SCF: Management Control Perimeter (includes SCUK).

Net Attributable Profit€ Million

2009 2010 2011 2012 2013 2014 2015

All-time record profit result in 2015

In 9M’16, attributable profit of €935 million (+14% yoy)

472555

744

825

895 908

1,093

41

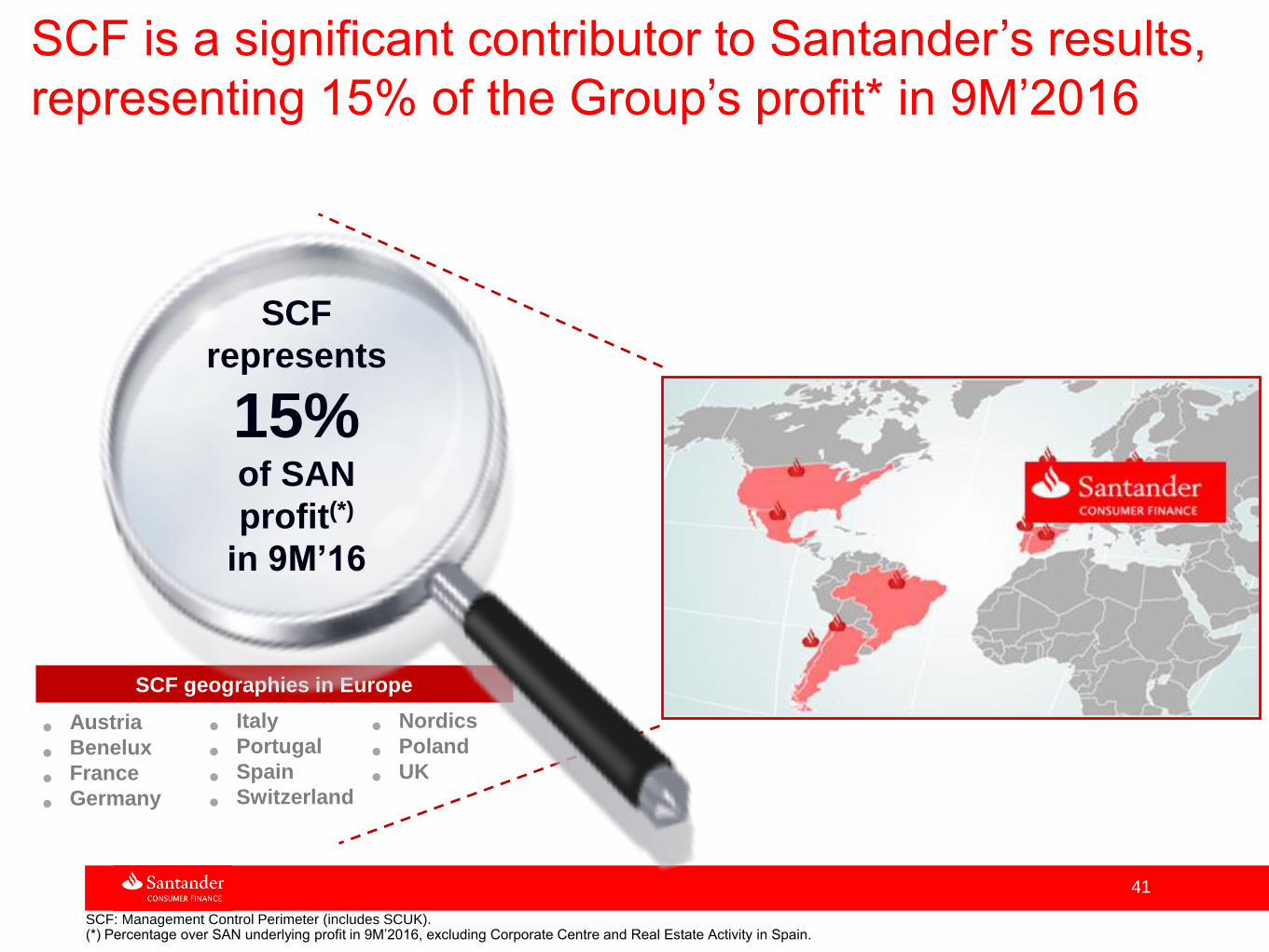

SCF is a significant contributor to Santander’s results,

representing 15% of the Group’s profit* in 9M’2016

SCF: Management Control Perimeter (includes SCUK).(*) Percentage over SAN underlying profit in 9M’2016, excluding Corporate Centre and Real Estate Activity in Spain.

SCF geographies in Europe

SCF

represents

15%of SAN

profit(*)

in 9M’16

• Austria

• Benelux

• France

• Germany

• Nordics

• Poland

• UK

• Italy

• Portugal

• Spain

• Switzerland

42

These results have been achieved thanks to

SCF’s proven business model

43

Well balanced between car and consumer loans, and

well spread across EuropeA

SCF: Management perimeter (i.e. including SCUK)

Diversification by products

Auto

-New

Auto-UsedDirect

Mortgages

Car Stock

Finance

Durables

Credit Cards

34%

22%

13%

4%

3%

8%

5%

10%

Other

Auto Finance Consumer Finance

Outstanding = €93 bn

(Sep’16)

Diversification by geographies

Germany

37%

15%12%

10%

8%

7%

4%7%

UK

Italy

Nordic

Countries

PolandOther

Spain

France

Outstanding = €93 bn

(Sep’16)

44

A

March 2016. Source: Internal estimates (Austria, Belgium, Germany, Netherlands, Nordics, Poland, Portugal, UK) and local associations (rest) France data as of Dic’15Management Control Perimeter (includes SC UK)

Critical mass and leadership in auto loans and

durables financing

• Critical mass and TOP 3 in 11 markets

• Top position in the 5 biggest European

auto markets: Germany, France, UK,

Italy and Spain. Accounts for 75% of

Europe’s car registrations

• Proven strategy in durables

• Key lever for customer capturing

and conversion activities

45

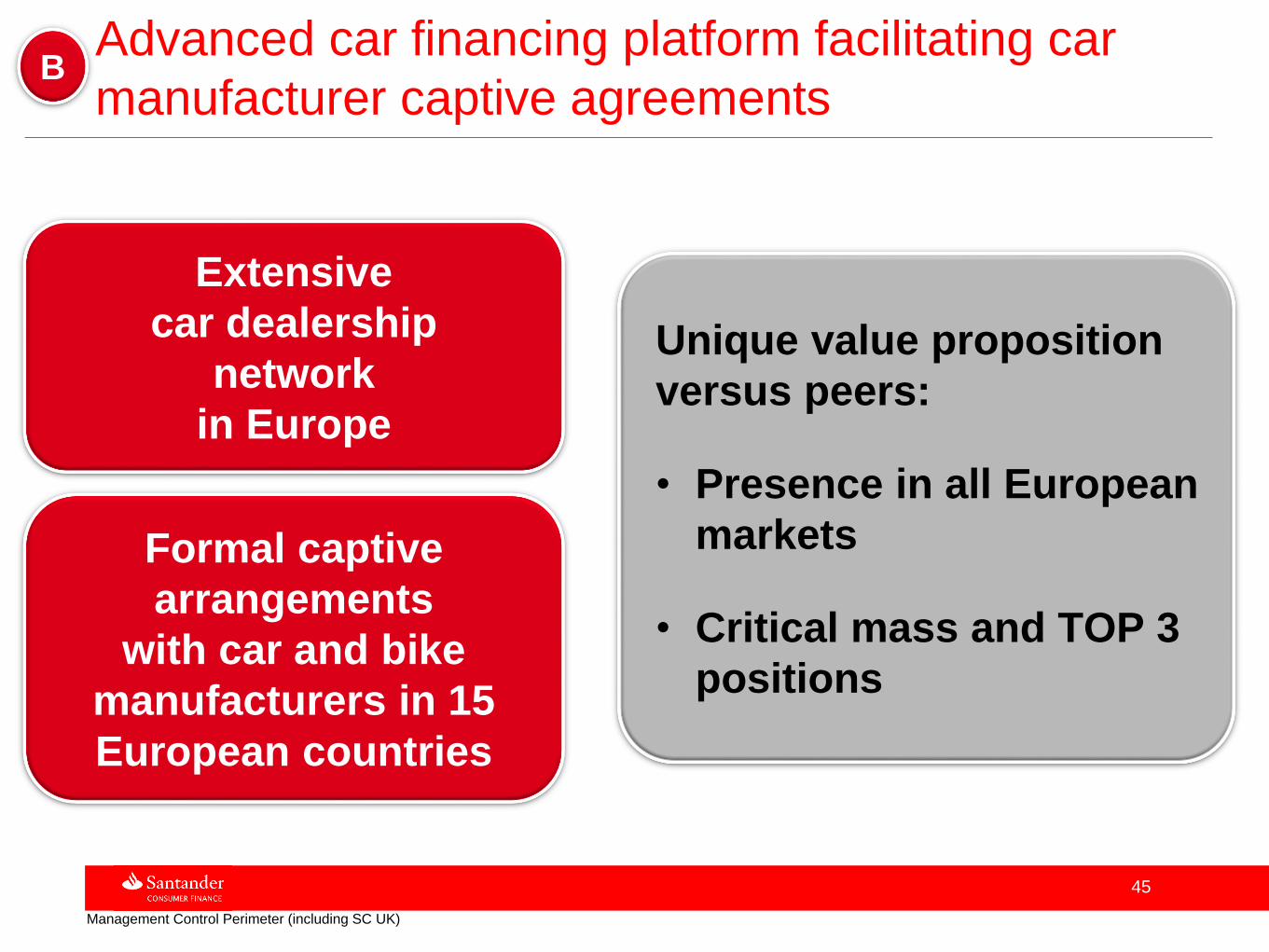

B

Management Control Perimeter (including SC UK)

Advanced car financing platform facilitating car

manufacturer captive agreements

Unique value proposition

versus peers:

• Presence in all European

markets

• Critical mass and TOP 3

positions

Extensive

car dealership

network

in Europe

Formal captive

arrangements

with car and bike

manufacturers in 15

European countries

46

BHigh network of retailers with a successful customer

conversion model

47

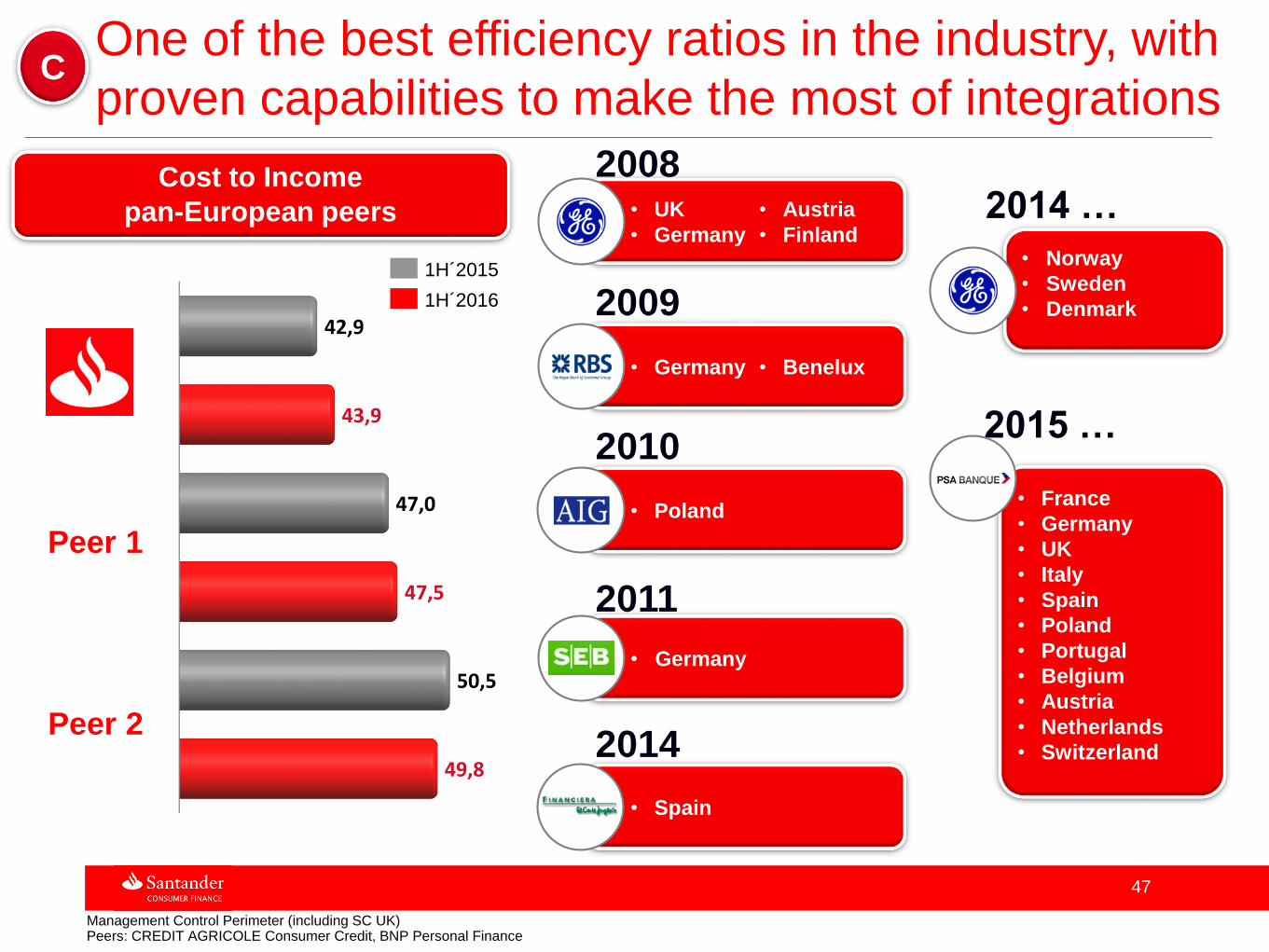

COne of the best efficiency ratios in the industry, with

proven capabilities to make the most of integrations

Management Control Perimeter (including SC UK)Peers: CREDIT AGRICOLE Consumer Credit, BNP Personal Finance

49,8

50,5

47,5

47,0

43,9

42,9

Cost to Income

pan-European peers

• Germany

2008

2009

• Poland

2010

2011

• Spain

2014

• Germany • Benelux

• UK

• Germany

• Austria

• Finland

1H´2016

1H´2015• Norway

• Sweden

• Denmark

2014 …

• France

• Germany

• UK

• Italy

• Spain

• Poland

• Portugal

• Belgium

• Austria

• Netherlands

• Switzerland

2015 …

Peer 1

Peer 2

48

D

Management Control Perimeter (including SC UK). Risk Premium: Ratio (%) of average VMG (last 12 months variation in delinquency balance minus Net Write Offs for the period) to average portfolio (for a period of twelve months). (12-month VMG / 12-month Average Managed Loans) * 100.

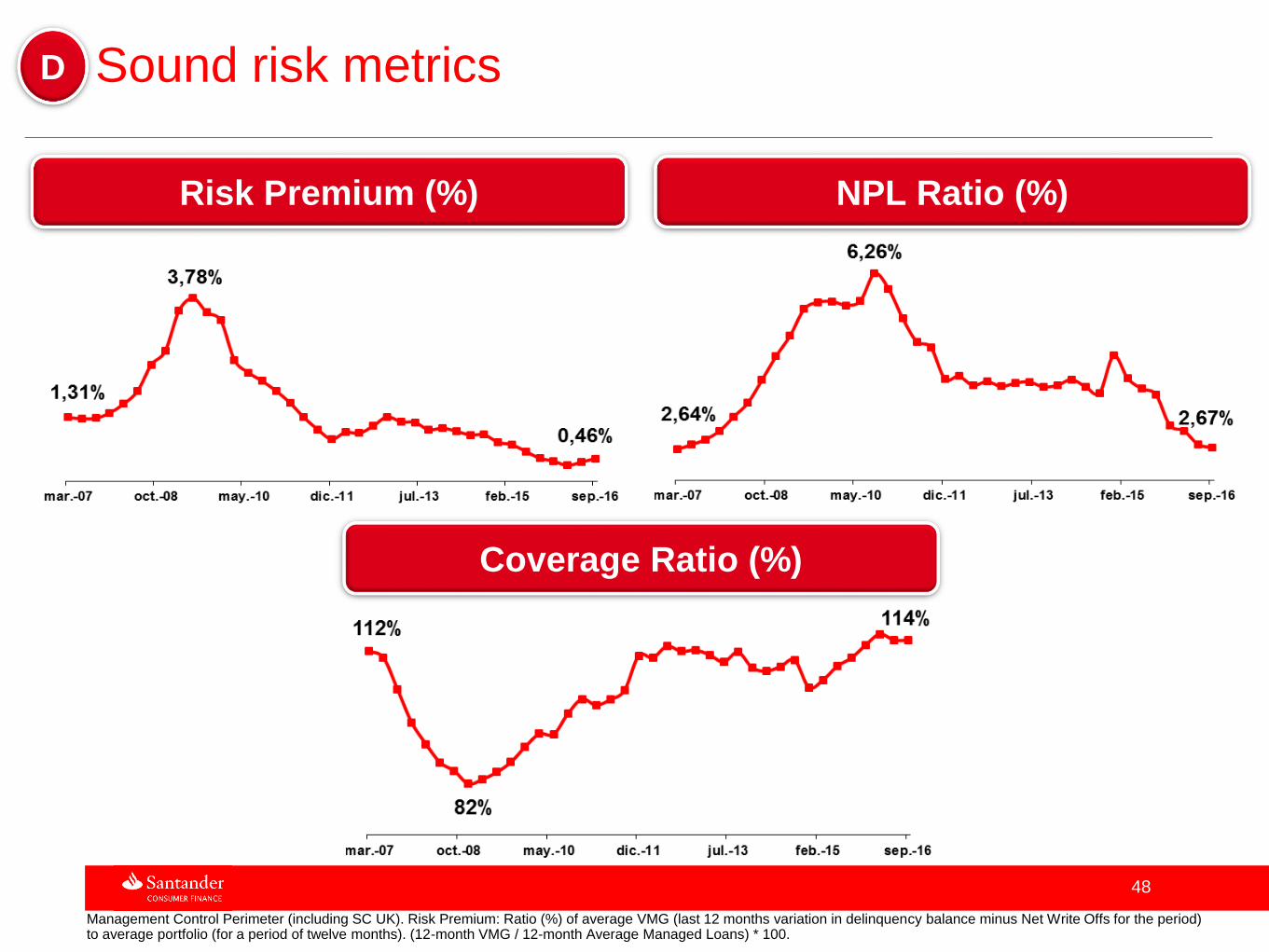

Sound risk metrics

Risk Premium (%) NPL Ratio (%)

Coverage Ratio (%)

49

E

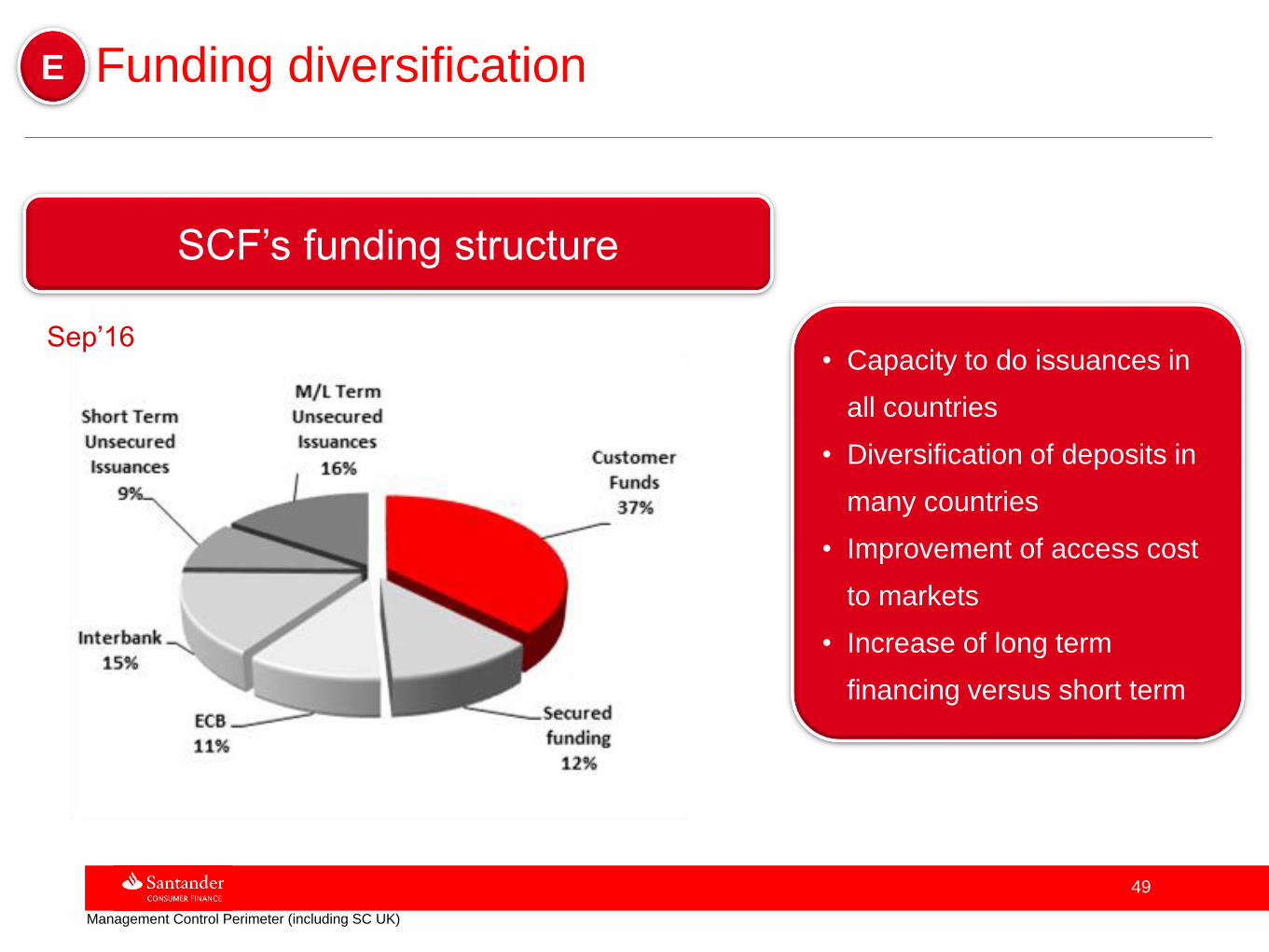

Management Control Perimeter (including SC UK)

Funding diversification

SCF’s funding structure

Sep’16• Capacity to do issuances in

all countries

• Diversification of deposits in

many countries

• Improvement of access cost

to markets

• Increase of long term

financing versus short term

50

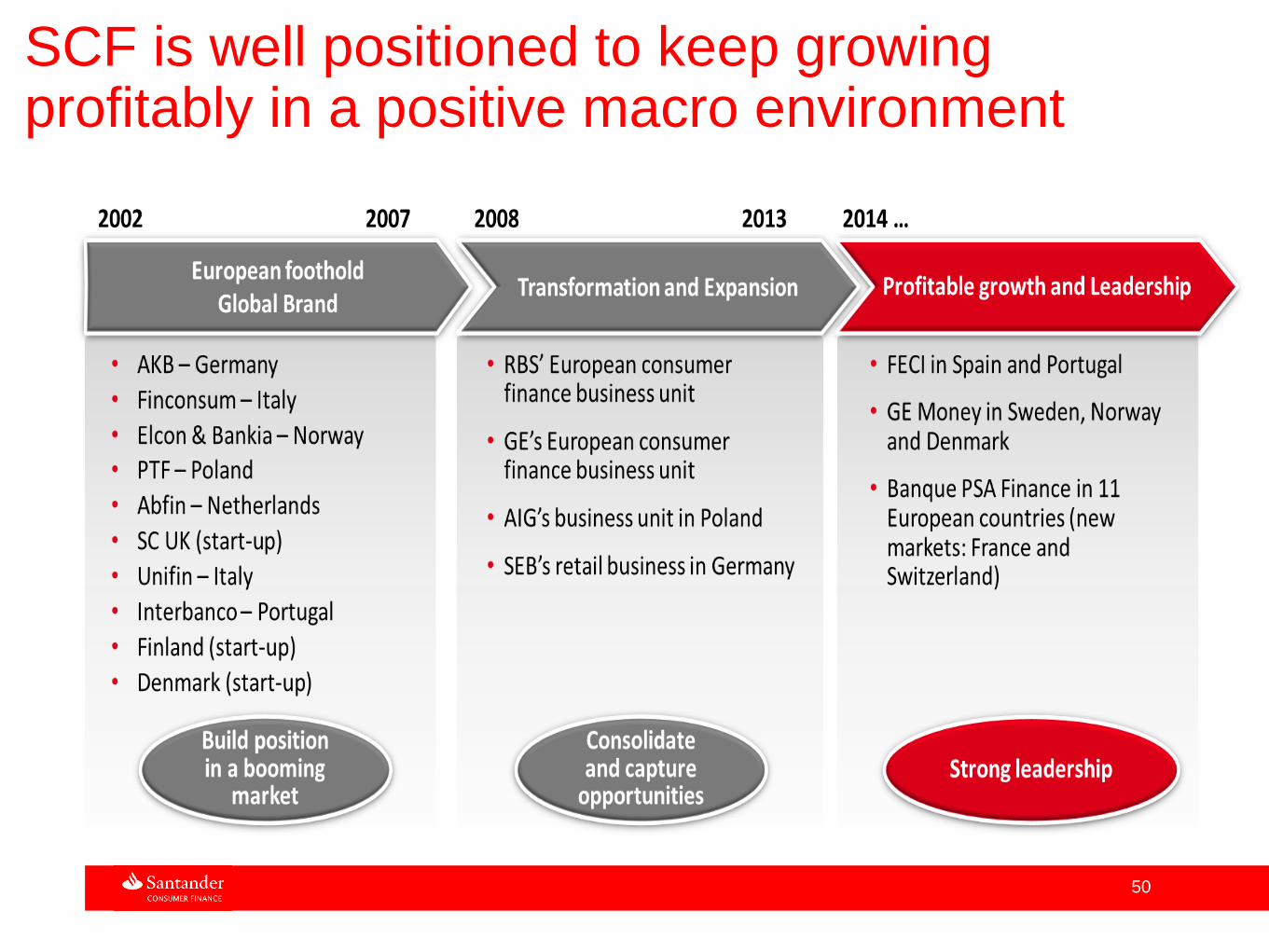

SCF is well positioned to keep growing profitably in a positive macro environment

1. Santander Consumer Bank AS, Nordic (“SCB Nordic”)

2. Risk Management

3. Financial information

4. Appendix: Banco Santander & Santander Consumer Finance

5. Appendix: Contacts

Content

51

• Anders Bruun-Olsen, CFO

• Phone: +47 21 08 37 70

• Mobile: :+47 95 76 83 28

• E-mail: [email protected]

• Priscilla Halverson, Capital Markets Director, Nordic

• Phone: +47 21 08 37 72

• Mobile: +47 92 06 58 75

• E-mail: [email protected]

• Anders Fuglsang, Capital Markets Manager, Nordic

• Phone: +47 21 08 30 44

• Mobile: :+47 950 42 128

• E-mail: [email protected]

• Joachim Joveng Rogne, Capital Markets Analyst, Nordic

• Mobile: :+47 48 23 86 32

• E-mail: [email protected]

• For more information:

• Santander Consumer Banks AS: www.santanderconsumer.no

• Santander Consumer Bank AB: www.santanderconsumer.se

• Santander Consumer Finance SA: www.santanderconsumer.com

• Banco Santander: www.santander.com

Contacts

52

Thank you!