Embed Size (px)

Citation preview

Managing taxBalancing current challenge with future promiseThe EYE, Amsterdam, 30 November – 1 December 2016

Opportunities and risks for tax in global business

services (GBS)/shared service centers

(SSCs)

Guido Lubbers, Deloitte NetherlandsJulie Richard, Deloitte Netherlands

3

Contents

Trends in GBS/SSC 4

Integrating tax in the GBS/SSC journey 14

How do you deal with integration of tax in set-up of GBS/SSC? 22

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

Trends in GBS/SSC

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

5

Main challenge for a GBS/SSC is the transformation to a new operating model, which consists of closely interconnected elements

Geographies in which location, e.g., offices, service center locations; Service Line A Agreements (SLAs)

LOCATION

Requiring what; resources and skills, e.g., Full time employees (FTEs), costs culture and capabilities.

PEOPLE

End-to-end processes. Supported by which processes, handovers.

PROCESSES

Business agility. Products and/customers and their distribution channels.

BUSINESS MODEL

System landscape: ERP, process enabling tooling, reporting systems.Architecture, integrated, development.

TECHNOLOGY

Structure, governance. roles and responsibilities. In which way are you organized to deliver.

ORGANIZATION

SSC/GBS

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

6

Introduction to survey

• Deloitte’s 2015 Global Shared Services survey attracted 311 respondents

• Manufacturing continues to be the top industry represented in the biennial survey, accounting for approximately 27% of respondents

• Tech/Telecomm, Financial Services and Consumer Products are the next most represented industries accounting for 13%, 11% and 10% of respondents respectively

• Average revenue of participant organizations was approximately $11 billion

• Over 50% of respondents had organizations over 10,000 FTEs

• Respondents represent organizations headquartered in 35 countries across the globe (West Europe 43% and US/Canada 30%

• Number of SSCs of the respondents who currently have Shared Services Centers, the average number of SSCs per company was 3.3 which is similar to 2013

• SSCs Represented in this survey have varying sizes and different levels of maturity

• Similar to previous years, smaller centers are the most common deployment method with 57% of the respondents indicating that they have less than 100 employees in their SSCs

• The average age of all shared services centers was 5.5 years

• Of the SSC organizations that have been operating for less than three years:

– Over 70% have less than 100 employees

– Over half have one SSC

– Over 60% have multi-function SSCs

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

7

Objectives: why are new SSCs being created and what factors are most important in selecting a future location?

Deloitte 2015 Global Shared Services survey results – Copyright @ 2015 Deloitte Development LLC. All rights reserved.

Addresstax/regulatory issues

Improve labor qualityand retention

Reduce risk

Expand languageskills

Improve service

Consolidate intoexisting SSC

Accommodate growth

Reduce cost 34%

23%

17%

11%

6%

6%

What are the primary reasons for opening a new SSC or relocating a SSC?

2%

1%

8

Scope: which functions are recognized in your SSC?

Deloitte 2015 Global Shared Services survey results – Copyright @ 2015 Deloitte Development LLC. All rights reserved.

Which functions are performed in your organization’s SSC?

Engineering

R&D

Marketing Insight & Support

Supply Chain/Manufacturing Support

Sales Administration

Real Estate/Facilities Management

Legal

Customer Service/Contact Center

Procurement

Tax

Information Technology

Human Resources

Finance 91%

66%

52%

39%

39%

34%

20%

20%

18%

15%

14%

9%

8%

9

Location: what is the global reach of your centers?

Deloitte 2015 Global Shared Services survey results – Copyright @ 2015 Deloitte Development LLC. All rights reserved.

What is the geographical coverage of your SSCs?

Local: provide services for a single country only, 22%

Regional: provides services across

countries but in a single continent only,

41%

Multi-regional:provide services to

two continents, 18%

Global: provide services to three

or more continents, 19%

10

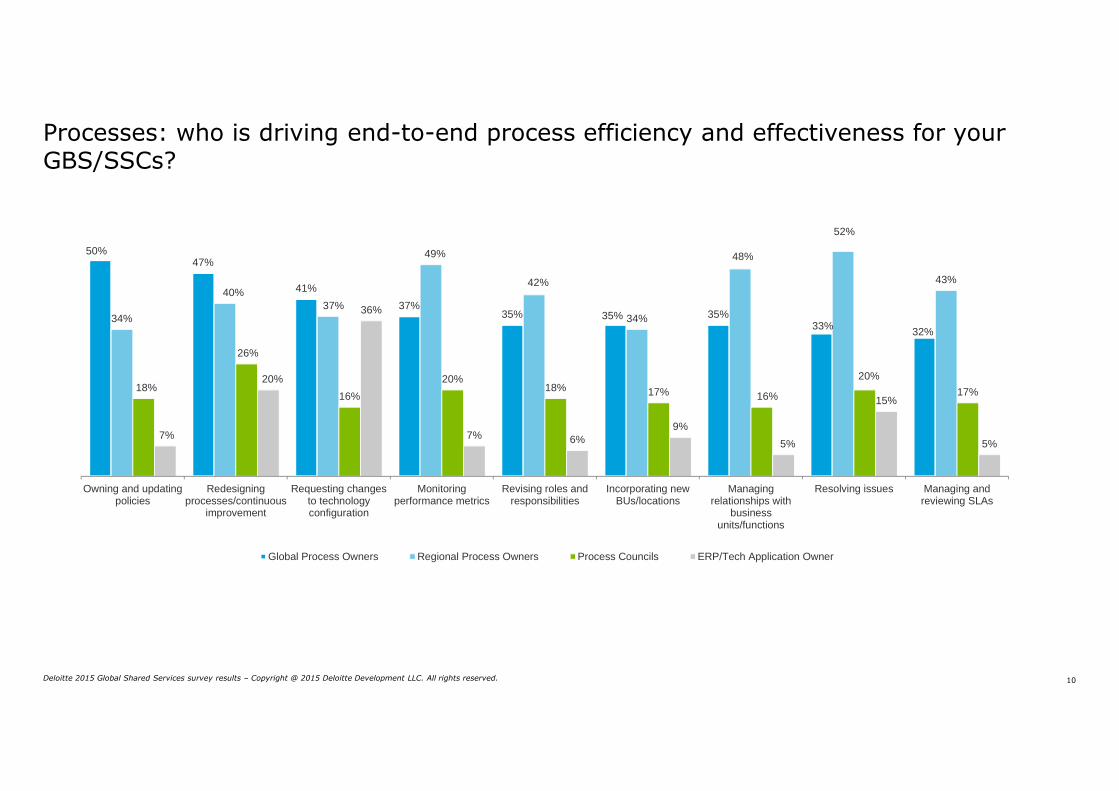

Processes: who is driving end-to-end process efficiency and effectiveness for your GBS/SSCs?

Deloitte 2015 Global Shared Services survey results – Copyright @ 2015 Deloitte Development LLC. All rights reserved.

50%47%

41%

37%35% 35% 35%

33%32%

34%

40%37%

49%

42%

34%

48%

52%

43%

18%

26%

16%

20%18% 17% 16%

20%

17%

7%

20%

36%

7% 6%9%

5%

15%

5%

Owning and updatingpolicies

Redesigningprocesses/continuous

improvement

Requesting changesto technologyconfiguration

Monitoringperformance metrics

Revising roles andresponsibilities

Incorporating newBUs/locations

Managingrelationships with

businessunits/functions

Resolving issues Managing andreviewing SLAs

Global Process Owners Regional Process Owners Process Councils ERP/Tech Application Owner

11

Processes: how has process standardization and technology impacted your move to shared services?

Deloitte 2015 Global Shared Services survey results – Copyright @ 2015 Deloitte Development LLC. All rights reserved.

Did you standardize processes before, during, or after the move to shared services?

Did you move processes before, during, or after technology change?

Timing of process move to SSC

Prior to technology

change

During technology

change

After technology

change

Timing of process standardization

Prior to move to SSC

5% 7% 5%

During move to SSC

6% 13% 3%

After move to SSC

34% 14% 13%

Standardized processes after move to SSC, 61%

Standardized processes and moved to shared services at the same time, 22%

Standardized processes prior to move to SSC, 17%

Moved processes before technology change, 45%

Moved processes at the same time as the technology change, 34%

Moved processes after technology change, 21%

12

Technology: what will be the role of analytics within a SSC/GBS organization?

Deloitte 2015 Global Shared Services survey results – Copyright @ 2015 Deloitte Development LLC. All rights reserved.

What role does your SSC/GBS organization perform or anticipate performing in data analysis or analytics?

What are the top challenges of adding analytics as a capability within your SSC/GBS organizations?

How do you plan to increase automation capabilities in the future?

22%

26%

28%

40%

42%

52%

53%

Absence of leadership focus

Data availability

Securing financial resources for required investment

Access to skilled talent

Understanding of business background

Supporting technology platform

Data reliability and consistency

23%

32%

49%

71%

76%

34%

31%

20%

10%

11%

Perform predictive analytics and/or optimization

Develop and deliver business insights to help enterpriseleaders run the business more effectively

Analyze historical data to discover trends

Gather and aggregate enterprise data

Provide requested reports to the enterprise

Perform currently Anticipate performing in two years

13%

32%

36%

44%

71%

Invest in robotics

Leverage outsourced technologycapabilities

Leverage cloud computing

Use bolt-on tools

Use our current ERP system

13

Results: to what degree has your organization achieved its objectives for shared services?

Deloitte 2015 Global Shared Services survey results – Copyright @ 2015 Deloitte Development LLC. All rights reserved.

Short of meeting objectives Exceeded objectives

18%

16%

13%

14%

15%

28%

20%

17%

26%

28%

26%

40%

29%

24%

23%

19%

17%

29%

20%

14%

19%

19%

13%

19%Technology automation

Size of retained organization

Technology standardization

Time to implement—fully deployed

One-time costs

Time to implement—center set up

Headcount reduction

Number of geographies served

Number of business units served

Types of processes in scope

Number of processes in scope

Service quality

14

Tax: for what areas was tax considered during SSC formation?

Deloitte 2015 Global Shared Services survey results – Copyright @ 2015 Deloitte Development LLC. All rights reserved.

2%

11%

11%

16%

17%

21%

25%

30%

33%

52%

Unclaimed property

Other federal, state or international considerations

Accounting method

Employee benefits

Planning to reduce global tax burden (e.g. transfer pricing, etc.)

VAT considerations

Availability of federal, state and/or local credits and incentives

Tax considerations were not taken into account

Legal entity type

Location of SSC

Integrating tax in the GBS/SSC journey

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

16

Identifying tax touch points

GBS/SSC Methodology

Process

Technology, cyber and data

Delivery model

People and organization

Stakeholder alignment and change management

Understanding and commitment across the organization, culture and change management

Program control Standard PMO activities and management of inflight and dependent projects

Activities and controls performed to produce the function and/or SSC Services

Technology, cyber and data solutions to support delivery

The optimum delivery model, including physical locations, delivery structure and sourcing

SSC and retained organization

Service management and governance

Service operations and effective governance (e.g., appropriate committees, forums, decision rights, SLAs and KPIs, etc.)

Value and business case Strategic role of SSC, value drivers and business case

Customer engagement Continually improving customer experience, engagement, relationship and satisfaction

Tax, risk and compliance Proactive and comprehensive treatment of tax risk and compliance elements

Ali

gn

men

t an

d c

on

trol

In

teg

rate

dserv

ice d

eli

very

Valu

e

The objective is to develop a design and approach for a Finance and HR Service Center to support growth ambition

Design Build and testImplement

roll inOptimize

Assessfeasibility

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

17

What can you transition?

Tax in GBS/SSC setup

Tax function

Shared service center

Tax management

• Financial close for tax

• Reconciliations

• Indirect tax

• Accounting analyses for tax

• Management reporting on tax

Tax compliance

• Master data management

• Tax return data

• Local statutory accounts

• Return preparations

• Compliance outsourcing

• TP documentation preparation

Tax accounting and reporting

• Controls operation and internal audit

• Technology tools

• Compliance manual

• Tax risk register

• Tax audit support

Tax operations and risks

• Tax objectives

• Tax strategy

• Technology strategy

• Tax risk framework

• Process determination

Supported by

Standardization

Data optimization

Efficiencies and automation

People

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

18

Trends for activities in scope

Tax in GBS/SSC setup

Group Tax SSC Outsource*

Tax strategy, policy, etc.

Organization and people

Knowledge management

Technology

Planning

Transfer pricing

Financial reporting

Statutory reporting

Tax compliance

Enquiries and audit

Tax advisory

Primary role

Support/review role

*Outsource analysis shown for completeness

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

19

GBS/SSC components

Design Build and testImplement

roll inOptimize

Assessfeasibility

Geographies in which location, e.g., offices, service center locations; SLAs

LOCATION

Requiring what; resources and skills, e.g., FTEs, costs culture and capabilities.

PEOPLE

End-to-End processes. Supported by which processes, handovers,

PROCESSES

Business agility. Products and /Customers and their distribution channels

BUSINESS MODEL

• System landscape: ERP, process enabling tooling, reporting systems

• Architecture, Integrated, development

TECHNOLOGY

• Structure, Governance. Roles and Responsibilities. In which way are you organized to deliver

ORGANIZATION

SSC/GBS

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

20

Example – overall approach and timeline

Tax in GBS/SSC setup

Prepare questionnaire

Discuss and confirm questionnaire

Draft processes

Phase I: Preparation and assessment requirements

Phase II: Processes Phase III: Process review and TP

Deloitte Client Deloitte

Validate and categorize requirements

Investigate local requirementsDistribute questionnaire

Verify local requirements Verify/clarify input to questionnaire

Desk research

Prepare the draft reportDiscuss the draft report with IBM

Prepare final report

Discuss the final report with IBM and optionally customer

Report and next steps definition

Review of draft processes

Contact local authorities

Maintain local regulatory requirements

Processes Review Transfer Pricing

Lift and shift – transfer pricingPrepare for new Oracle system

Lift and shift – processes

Ongoing project management and project budget control

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

21

Challenges, risks & opportunities

Tax in GBS/SSC setup

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

Challenges Risks Opportunities

• Onboarding – Understanding GBS project

• Onboarding - Involvement

• Onboarding – Timing

• Onboarding – tax scope

• Resources – people

• Resources – budget

• 3rd party BPO

• Geographical – global/regional

• Impact – tax department and resources in tax process

• Failure to meet local legal requirements (e.g., document storage)

• Removal of local expertise/ways of working

• Complexity of local indirect tax regime compared with EU model

• Handoffs between SSC and local business

• Lack of end user training/awareness

• Failure of systems to support SSC in making VAT decisions

• Reduction in manual intervention during transactional processing

• Freedom for local business to focus on strategy/planning rather than compliance

• Realization of benefits from technology investments

• Creation of a single ‘best practice’ indirect tax processing model

• Lower cost per indirect tax return

How do you deal with integration of tax in set-up of GBS/SSC?

23

Sharing experience

Do/Did you take tax into account when setting up SSC/GBS?

What are/were the biggest challenges?

What would you have done differently?

Which tax elements did you integrate and how?

How did you integrate with the rest of the project?

24

Faculty

Guido Lubbers, Deloitte Netherlands

Partner – Indirect Tax

Julie Richard, Deloitte Netherlands

Senior Manager – Indirect Tax

+31 (0) 612581583

+31 (0) 682019070

©2016. For information, contact Deloitte Touche Tohmatsu Limited.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about to learn more about our global network of member firms.

Deloitte provides audit, consulting, financial advisory, risk advisory, tax and related services to public and private clients spanning multiple industries. Deloitte serves four out of five Fortune Global 500® companies through a globally connected network of member firms in more than 150 countries and territories bringing world-class capabilities, insights, and high-quality service to address clients’ most complex business challenges. To learn more about how Deloitte’s approximately 245,000 professionals make an impact that matters, please connect with us on Facebook, LinkedIn, or Twitter.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2016. For information, contact Deloitte Touche Tohmatsu Limited.