Embed Size (px)

Citation preview

Learning Objectives

• Understand the Business– LO1 Explain why adjustments are needed.

• Study the accounting methods– LO2 Prepare adjustments needed at the end of the

period.– LO3 Prepare an adjusted trial balance.– LO4 Prepare financial statements.– LO5 Explain the closing process.

• Evaluate the results– LO6 Explain how adjustments affect financial results.

• Review the chapter1© McGraw-Hill Ryerson. All rights reserved.

Making Required Adjustments

• Adjustments are not made every day because it is more efficient to do them all at once at the end of each period.

LO22© McGraw-Hill Ryerson. All rights reserved.

• The unadjusted trial balance is a key starting point for the adjustment process.

• Compare the unadjusted balance with the desired balance to determine the required adjusting entry.

LO23© McGraw-Hill Ryerson. All rights reserved.

Deferral Adjustments

LO2

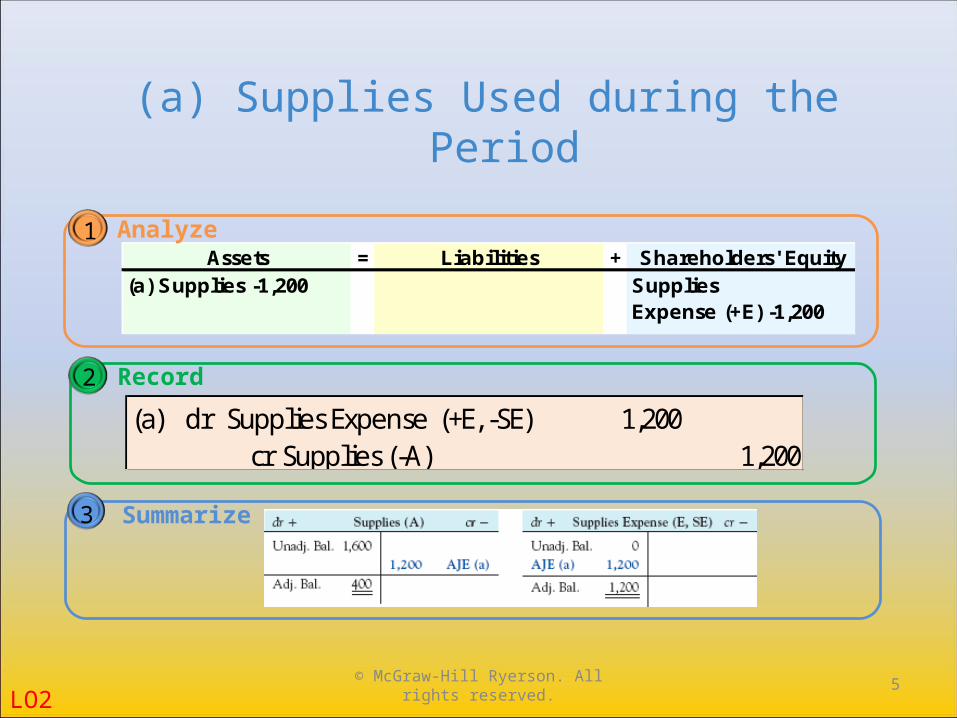

(a) Supplies Used during the PeriodOf the $1,600 in supplies received in early September, $400 remain on

hand at September 30.

4© McGraw-Hill Ryerson. All rights reserved.

Assets = Liabilities + Shareholders' Equity(a) Supplies -1,200 Supplies

Expense (+E) -1,200

1 Analyze

2 Record(a) dr Supplies Expense (+E, -SE) 1,200 cr Supplies (-A) 1,200

3 Summarize

LO2

(a) Supplies Used during the Period

5© McGraw-Hill Ryerson. All rights reserved.

(b) Rent Benefits Expired during the PeriodThree months of rent were prepaid on September 1 for $7,200, but

one month has now expired, leaving only two months prepaid at September 30.

1/3 x $7,200 = $2,400 expense used up as of Sept. 30

2/3 x $7,200 = $4,800 asset remains prepaid as of Sept. 30

LO26© McGraw-Hill Ryerson. All rights reserved.

Assets = Liabilities + Shareholders' Equity(b) Prepaid Rent Rent -2,400 Expense (+E) -2,400

1 Analyze

2 Record(b) dr Rent Expense (+E, -SE) 2,400 cr Prepaid Rent (-A) 2,400

3 Summarize

LO2

(b) Rent Benefits Expired during the Period

7© McGraw-Hill Ryerson. All rights reserved.

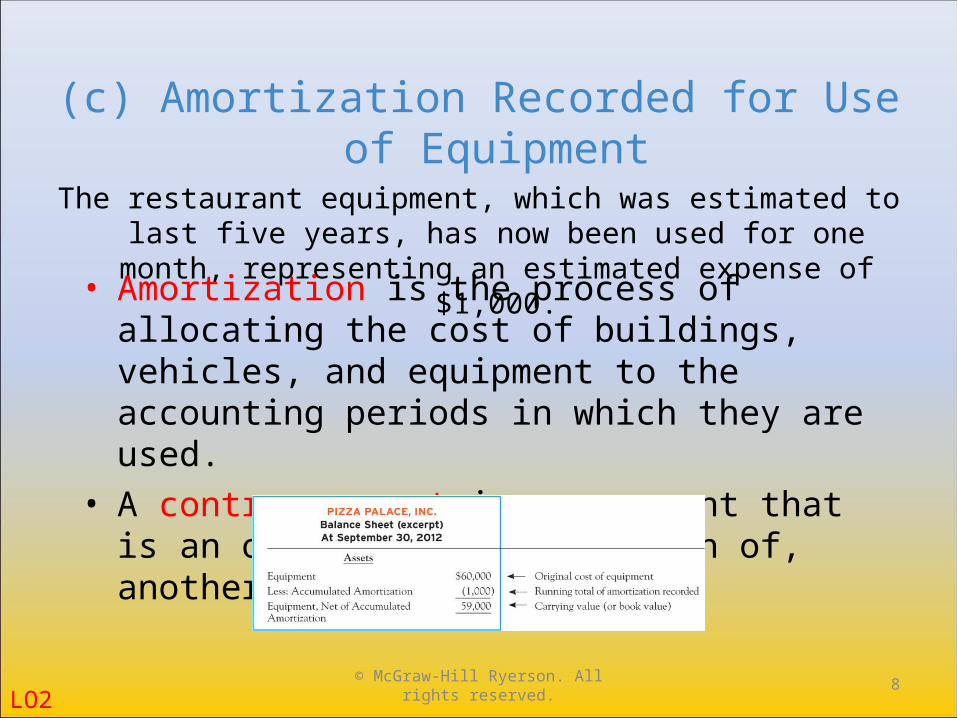

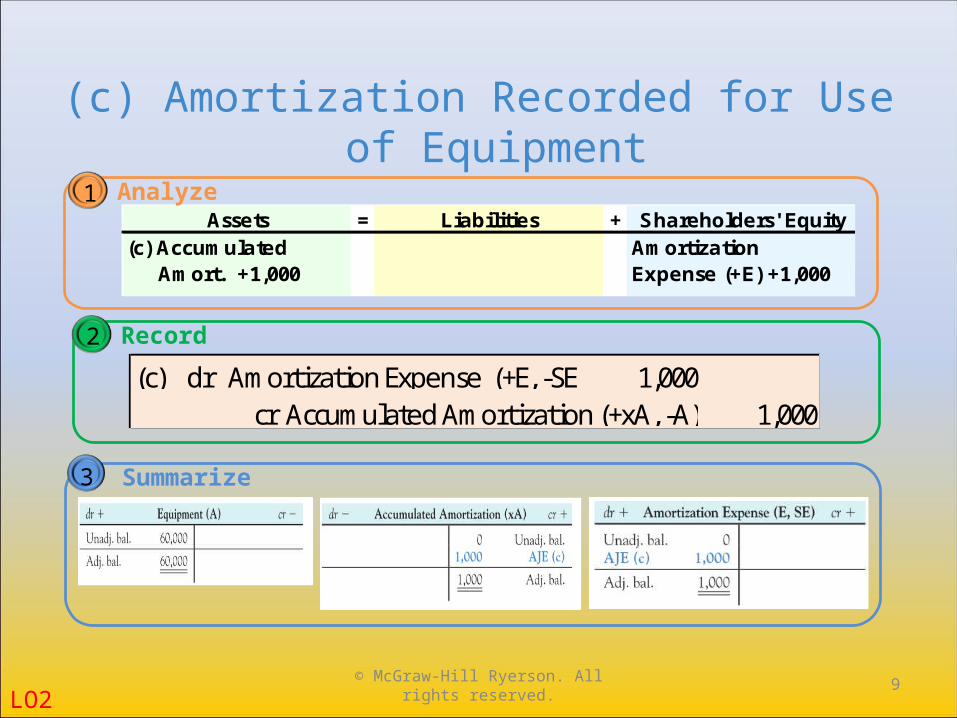

(c) Amortization Recorded for Use of EquipmentThe restaurant equipment, which was estimated to last five years, has

now been used for one month, representing an estimated expense of $1,000.

• Amortization is the process of allocating the cost of buildings, vehicles, and equipment to the accounting periods in which they are used.

• A contra-account is an account that is an offset to, or reduction of, another account.

LO28© McGraw-Hill Ryerson. All rights reserved.

(c) Amortization Recorded for Use of Equipment

Assets = Liabilities + Shareholders' Equity(c) Accumulated Amortization Amort. +1,000 Expense (+E) +1,000

1 Analyze

2 Record(c) dr Amortization Expense (+E, -SE) 1,000 cr Accumulated Amortization (+xA, -A) 1,000

3 Summarize

LO29© McGraw-Hill Ryerson. All rights reserved.

• Accumulated Amortization is a balance sheet account and Amortization Expense is an income statement account.

• The Accumulated Amortization account allows you to report both the original cost of equipment and a running total of the amount that has been amortized.

• The normal balance in a contra-account is always the opposite of the account it offsets.

• The amount of amortization depends on the method used for determining it.

LO210© McGraw-Hill Ryerson. All rights reserved.

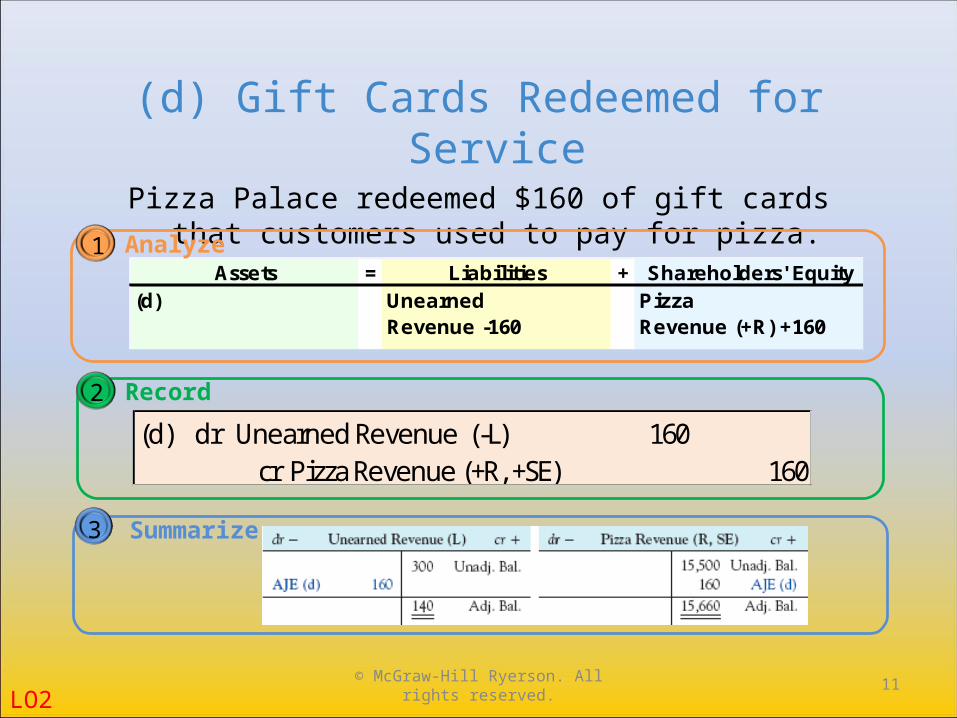

(d) Gift Cards Redeemed for ServicePizza Palace redeemed $160 of gift cards that customers used to

pay for pizza.

Assets = Liabilities + Shareholders' Equity(d) Unearned Pizza

Revenue -160 Revenue (+R) +160

1 Analyze

2 Record(d) dr Unearned Revenue (-L) 160 cr Pizza Revenue (+R, +SE) 160

3 Summarize

LO211© McGraw-Hill Ryerson. All rights reserved.

Accrual Adjustments

LO2

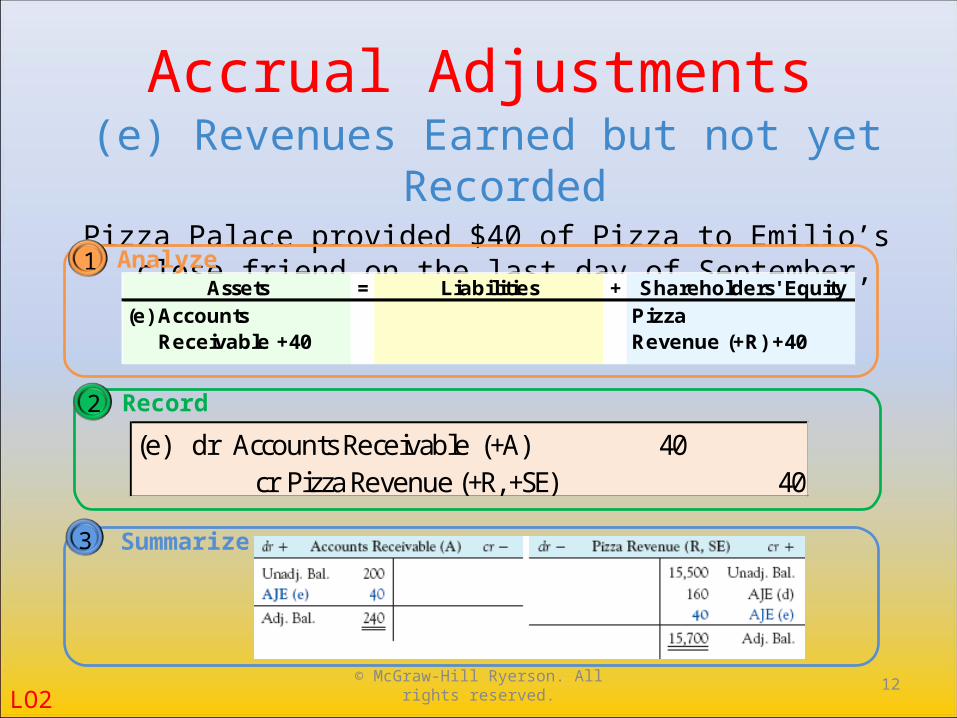

(e) Revenues Earned but not yet RecordedPizza Palace provided $40 of Pizza to Emilio’s close friend on the last

day of September, with payment to be received in October.

Assets = Liabilities + Shareholders' Equity(e) Accounts Pizza Receivable +40 Revenue (+R) +40

1 Analyze

2 Record(e) dr Accounts Receivable (+A) 40 cr Pizza Revenue (+R, +SE) 40

3 Summarize

12© McGraw-Hill Ryerson. All rights reserved.

(f) Wage Expense Incurred but not yet Recorded

Pizza Palace owes $300 of wages to employees for work done on the last day of September.

LO2

Assets = Liabilities + Shareholders' Equity(f) Wages Wages Payable +300 Expense (+E) -300

1 Analyze

2 Record(f) dr Wages Expense (+E, -SE) 300 cr Wages Payable (+L) 300

3 Summarize

13© McGraw-Hill Ryerson. All rights reserved.

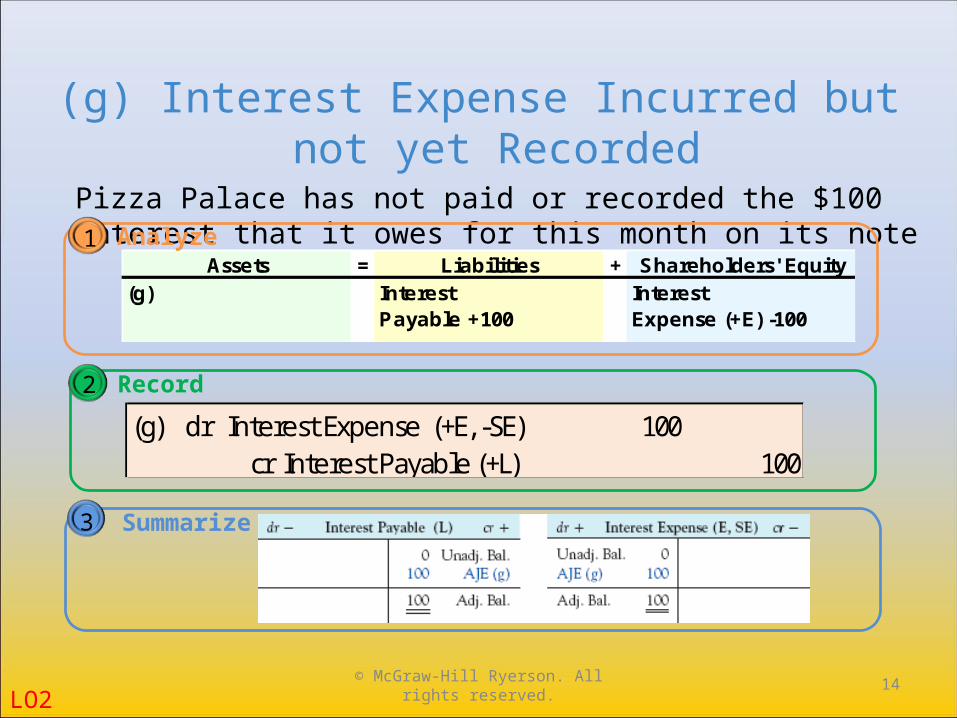

(g) Interest Expense Incurred but not yet RecordedPizza Palace has not paid or recorded the $100 interest that it owes for

this month on its note payable to the bank.

LO2

Assets = Liabilities + Shareholders' Equity(g) Interest Interest Payable +100 Expense (+E) -100

1 Analyze

2 Record(g) dr Interest Expense (+E, -SE) 100 cr Interest Payable (+L) 100

3 Summarize

14© McGraw-Hill Ryerson. All rights reserved.

• Income tax is calculated by multiplying the company's adjusted income by the company’s tax rate.

• Calculate income tax expense after all revenue and expense adjustments.

• Pizza Palace’s income tax is $1,000 x 40% = $400

(h) Income Taxes Incurred but not yet RecordedPizza Palace pays income tax at an average rate equal to 40 percent of the

company’s income before taxes.

LO215© McGraw-Hill Ryerson. All rights reserved.

(h) Income Taxes Incurred but not yet Recorded

LO2

Assets = Liabilities + Shareholders' Equity(h) Income Tax Income Tax Payable +400 Expense (+E) -400

1 Analyze

2 Record(h) dr Income Tax Expense (+E, -SE) 400 cr Income Tax Payable (+L) 400

3 Summarize

16© McGraw-Hill Ryerson. All rights reserved.

LO2

(i) Dividend Declared and PaidPizza Palace declares and pays a $500 cash dividend. Dividends are

actually a daily transaction, but are included here for convenience.

Assets = Liabilities + Shareholders' Equity(i) Cash -500 Dividends Declared (+D) -500

1 Analyze

2 Record(i) dr Dividends Declared (+D, -SE) 500 cr Cash (-A) 500

3 Summarize

17© McGraw-Hill Ryerson. All rights reserved.

• Adjusting journal entries never involve cash.

• Adjusting journal entries always include one balance sheet account and one income statement account.

• Dividends are not expenses; they are a reduction of retained earnings.

LO218© McGraw-Hill Ryerson. All rights reserved.

![U2.2 lesson3[lo2]](https://img.dokumen.tips/doc/110x75/58731caf1a28ab673e8b67f1/u22-lesson3lo2-591d13e75c6d0.jpg)