Embed Size (px)

Citation preview

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HD012-WDD

REPORT ON EXAMINATION OF FINANCIAL STATEMENTS

AND SUPPLEMENTAL INFORMATION

AT MARCH 31, 2018

l

I I

l

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT l 15-HD012-WDD

CONTENTS

AUDITOR'S TRANSMITTAL LETTER

INDEPENDENT AUDITOR'S REPORT

FINANCIAL STATEMENTS

ST A TEMENT OF FINANCIAL POSITION

ST A TEMENT OF ACTIVITIES AND CHANGES IN NET ASSETS

STATEMENT OF CASH FLOWS

NOTES TO FINANCIAL STATEMENTS

SUPPLEMENTARY INFORMATION

SUPPLEMENTARY INFORMATION REQUIRED BY HUD

SCHEDULE OF EXPENDITURES OF FEDERAL AW ARDS

NOTES TO SCHEDULE OF EXPENDITURES OF FEDERAL AW ARDS

INDEPENDENT AUDITOR'S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN

3

4-5

6

7

8-9

10-12

13

14-23

24

25

ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS 26-27

INDEPENDENT AUDITOR'S REPORT ON COMPLIANCE FOR EACH MAJOR PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY THE UNIFORM GUIDANCE 28-29

SCHEDULE OF FINDINGS AND QUESTIONED COSTS 30

DIRECTORS' CERTIFICATION 31

MANAGING AGENT'S CERTIFICATION 32

INDEPENDENT ACCOUNT ANT'S REPORT ON APPL YING 33-35 AGREED-UPON PROCEDURE

-2-

JEFFREYS. BULLINGTON, CPA RAY PARKER, CPA

KARIN NELSON, CPA

Members American Institute of Certified Public Accountants

HUD Field Office 106 S. St. Mary's Street San Antonio, Texas 78205

Cundiff Rogers+Solt PC A PROFESSIONAL CORPORATION

CERTIFIED PUBLIC ACCOUNTANTS

June 28, 2018

6243 1H 10 West, Suite 950 San Antonio, Texas 78201 (210) 734-9500 Fax (210) 736-9500 email: [email protected] www.crs-cpas.com

The accompanying audit of Lasker Village Apartments for the year ended March 31, 2018 was performed by:

-3-

Wesley Ray Parker, CPA Cundiff, Rogers & Solt, PC 6243 IH-10 West, Suite 950 San Antonio, TX 78201

Telephone: (210) 734-9500

Employer's Identification Number 74-2517804

JEFFREYS. BULLINGTON, CPA RAY PARKER, CPA

KARIN NELSON, CPA

Members American Institute of Certified Public Accountants

To The Board of Directors Lasker Village Apartments San Antonio, Texas

Cundiff Rogers+Solt PC A PROFESSIONAL CORPORATION

CERTIFIED PUBLIC ACCOUNTANTS

INDEPENDENT AUDITOR'S REPORT

Report on the Financial Statements

6243 lH 10 West, Suite 950 San Antonio, Texas 78201 (210) 734-9500 Fax (210) 736-9500 email: [email protected] www.crs-cpas.com

HUD Field Office San Antonio, Texas

We have audited the accompanying financial statements of Lasker Village Apartments (a Texas Non-Profit Corporation), HUD Project No. 115-HD012-WDD, which comprise the statement of financial position as of March 31, 2018, and the related statements of activities and changes in net assets, and cash flows for the year then ended, and the related notes to the financial statements.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

-4-

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Lasker Village Apartments as of March 31, 2018, and the changes in its net assets and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matters

Other Information

Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The accompanying supplementary information shown on pages 15 to 23 is presented for purposes of additional analysis as required by the Consolidated Audit Guide for Audits of HUD Programs issued by the U.S. Department of Housing and Urban Development, Office of the Inspector General, and is not a required part of the financial statements. The accompanying schedule of expenditures of federal awards, as required by Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administration Requirements, Cost Principles, and Audit Requirements for Federal Awards, is presented for purposes of additional analysis and is not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated, in all material respects, in relation to the financial statements as a whole.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated June 28, 2018 on our consideration of Lasker Village Apartments' internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Lasker Village Apartments internal control over financial reporting and compliance.

San Antonio, Texas June 28, 2018

-5-

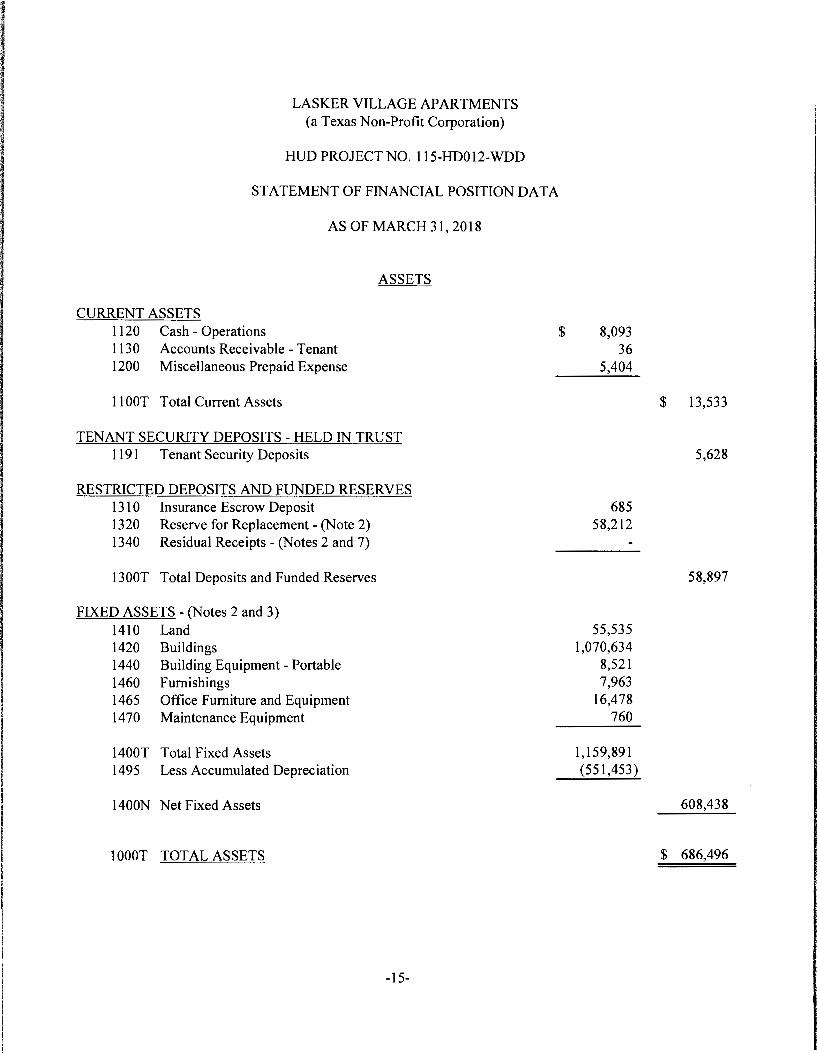

l LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. l 15-HD0I2-WDD

STATEMENT OF FINANCIAL POSITION

AS OF MARCH 31, 2018

CURRENT ASSETS Cash - Operations Accounts Receivable - Tenant Miscellaneous Prepaid Expense

Total Current Assets

ASSETS

TENANT SECURITY DEPOSITS - HELD IN TRUST Tenant Security Deposits

RESTRICTED DEPOSITS AND FUNDED RESERVES Insurance Escrow Reserve for Replacement - (Note 2) Residual Receipts - (Notes 2 and 7)

Total Deposits and Funded Reserves

FIXED ASSETS - (Notes 2 and 3) Land Buildings Building Equipment - Portable Furnishings Office Furniture and Equipment Maintenance Equipment

Total Fixed Assets Less Accumulated Depreciation

Net Fixed Assets

TOT AL ASSETS

$ 8,093 36

5,404

685 58,212

55,535 1,070,634

8,521 7,963

16,478 760

1,159,891 (551,453)

The accompanying notes to financial statements are an integral part of this financial statement. -6-

$ 13,533

5,628

58,897

608,438

$ 686,496

l l

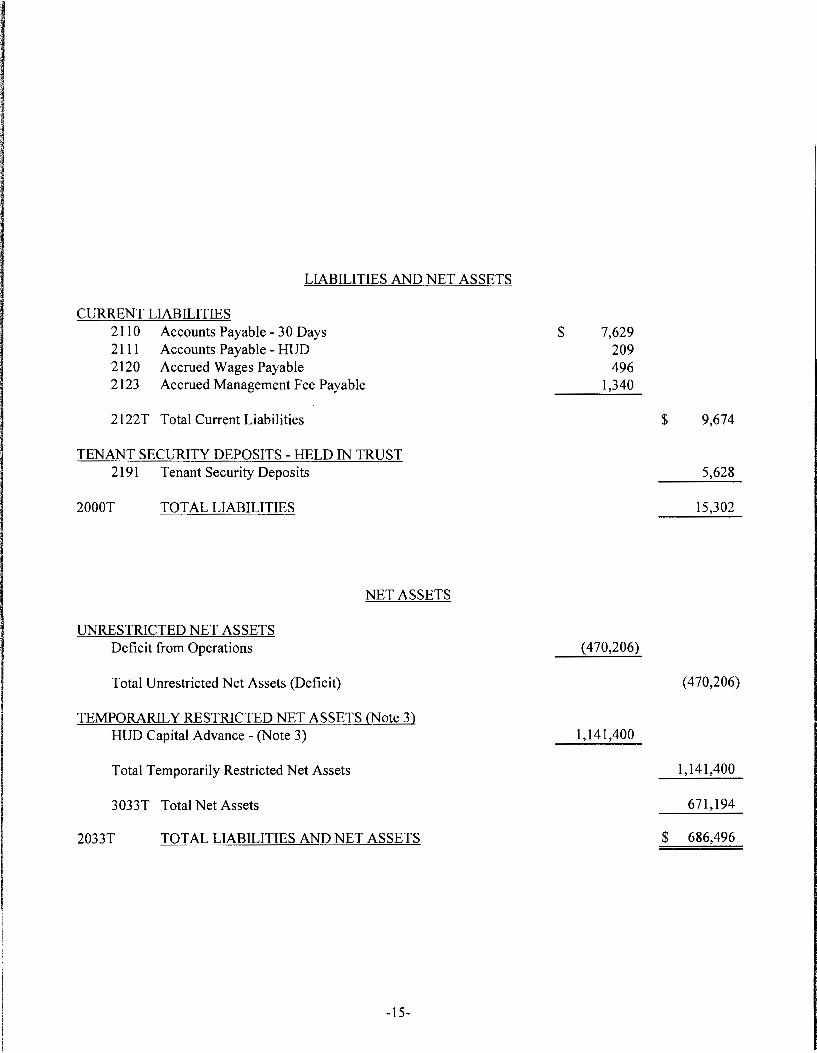

LIABILITIES AND NET ASSETS

CURRENT LIABILITIES Accounts Payable - 30 Days Accounts Payable - HUD Accrued Wages Accrued Management Fee Payable

Total Current Liabilities

TENANT SECURITY DEPOSITS - HELD IN TRUST Tenant Security Deposits

TOT AL LIABILITIES

UNRESTRICTED NET ASSETS Deficit from Operations

Total Unrestricted Net Assets (Deficit)

NET ASSETS

TEMPORARILY RESTRICTED NET ASSETS (Note 3) HUD Capital Advance - (Note 3)

Total Temporarily Restricted Net Assets

Total Net Assets

TOT AL LIABILITIES AND NET ASSETS

$ 7,629 209 496

1,340

(470,206)

1,141,400

The accompanying notes to financial statements are an integral part of this financial statement. -6-

$ 9,674

5,628

15,302

(470,206)

1,141,400

671,194

$ 686,496

l j

l l

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HD012-WDD

STATEMENT OF ACTIVITIES AND CHANGES IN NET ASSETS

FOR THE YEAR ENDED MARCH 31, 2018

REVENUE: Rent - net Interest Tenant charges

Total revenue

EXPENSES: Administrative Utilities Operating and maintenance Taxes and insurance Depreciation

Total expense

Change in Unrestriced Net Assets

Unrestricted Net Assets (Deficit) Beginning of Year

Unrestricted Net Assets (Deficit) End of Year

Temporarily Restricted Net Assets Beginning of Year

Temporarily Restricted Net Assets End of Year

Total Net Assets

The accompanying notes to financial statements are an integral part of this financial statement. -7-

$ 124,054 22

1,541

125,617

41,049 12,676 38,124

8,118 29,398

129,365

(3,748)

(466,458)

$ (470,206)

$ 1,141,400

$ 1,141,400

$ 671,194

I LASKER VILLAGE APARTMENTS

(a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HD012-WDD

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED MARCH 31, 2018

CASH FLOW FROM OPERATING ACTIVITIES: Rental Receipts Interest Receipts Commercial Rents Receipts Tenant Charges

Total Receipts

Administrative Disbursements Management Fees Utilities Salaries and Wages Operating and Maintenance Property Insurance Miscellaneous Taxes and Insurance

Total Disbursements

Net Cash Provided by Operating Activities

CASH FLOW FROM INVESTING ACTIVITIES: Net Deposits to Insurance Escrow Net Deposits to the Reserve for Replacement and Interest Retained in Account Approved withdrawals from Residual Receipts $ Deposits to Residual Receipts Net withdrawal from the Residual Receipts Account Net Purchase of Fixed Assests

Net Cash Used by Investing Activities

NET INCREASE IN CASH AND CASH EQUIVALENTS

BEGINNING CASH AND CASH EQUIVALENTS

ENDING CASH AND CASH EQUIVALENTS

6,083 10

The accompanying notes to financial statements are an integral part of this financial statement. -8-

$ 123,994 22

1,295 246

125,557

(11,182) (18,367) (I 4,188) (24,802) (27,750)

(9,583) (2,941)

(108,813)

16,744

3566 23,740

6,093 (47,819)

(14,420)

2,324

5,769

$ 8,093

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HD012-WDD

STATEMENT OF CASH FLOWS, CONTINUED

FOR THE YEAR ENDED MARCH 31, 2018

ADJUSTMENT TO RECONCILE CHANGE IN NET ASSETS TO NET CASH USED BY OPERA TING ACTIVITIES:

Change in Total Net Assets from Operations Adjustment to Reconcile Change in Net Assets to Net Cash Used by Operating Activities:

Depreciation Decrease (Increase) in:

Tenant Account Receivable Prepaid Expenses Tenant Security Deposit Cash

Increase (Decrease) in: Accounts Payable Accrued Liabilities Tenant Security Deposit Liability Prepaid Revenue

NET CASH PROVIDED BY OPERA TING ACTIVITIES

$

$

The accompanying notes to financial statements are an integral part of this financial statement.

-9-

(3,748)

29,398

(36) (4,406)

375

(3,186) (1,045)

(375) (233)

16,744

I LASKER VILLAGE APARTMENTS

(a Texas Non-Profit Corporation)

HUD PROJECT NO. l 15-HD012-WDD

NOTES TO FINANCIAL STATEMENTS

FOR THE YEAR ENDED MARCH 31, 2018

NOTE 1 - S3100-010 ORGANIZATION AND PRESENTATION

The Corporation was organized as a nonprofit entity on December 22, 1994. The Corporation entered into an agreement with the Department of Housing and Urban Development to acquire an interest in real property located in San Antonio, Texas, and to construct and operate thereon an apartment complex of 24 units, under Section 811 of the National Affordable Housing Act of 1990 with Sec. 8 Housing Assistance. Such projects are regulated by HUD as to rent charges and operating methods.

NOTE 2 - S3 l 00-040 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The following significant accounting policies have been followed in the preparation of the financial statements:

Use of estimates - the preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Cash equivalents - highly liquid investments, money-market accounts and U.S. Treasury Securities are considered to be cash equivalents by the Corporation.

Depreciation is provided using the straight-line method over the estimated useful lives of the assets (3 to 40 years). Assets are recorded at cost.

Maintenance, repairs and minor renewals and betterments are charged to expense as incurred. Equipment and furnishings of $250 or more and useful lives of 3 years or more are capitalized.

Allowance for doubtful accounts - Bad debts are provided on the allowance method based on management's evaluation of outstanding accounts receivable. At March 31, 2018, the corporation's management has reserved no allowance for doubtful accounts related to balances due from HUD and tenants.

Advertising-Advertising costs, except for costs associated with direct-response advertising, are charged to operations when incurred. The costs of direct-response advertising are capitalized and amortized over the period during which future benefits are expected to be received, if any. Advertising costs in fiscal year ended March 3 1, 2018 was $0.

The Corporation is a non-profit entity and has no authorized capital stock nor owners. No provision has been made for income taxes due to the nonprofit nature of the Corporation. The Corporation is exempt from income tax under Sec. 50l(c)(3) of the Internal Revenue Code.

-10-

I I LASKER VILLAGE APARTMENTS

(a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HD012-WDD

NOTES TO FINANCIAL ST A TEMENTS

FOR THE YEAR ENDED MARCH 31, 2018

NOTE 2 - S3100-040 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES-Cont'd

The Project is required to make monthly deposits to a reserve for replacements account. These funds are to be used for replacements or other costs and require HUD's approval for release.

Residual receipts (as defined by HUD) are required to be deposited in a reserve fund. Disbursements from this fund may only be made with the written consent of HUD. The balance at March 31, 2018 was $0. See Note 7.

NOTE 3 - S3 l 00-240 CONTINGENT LIABILITY

The project was funded by a capital advance under Section 811 of the National Affordable Housing Act of 1990, as amended. Under this program a mortgage note is issued that shall bear no interest and payment is not required so long as the housing remains available for very low-income elderly persons or very low-income persons with disabilities in accordance with Section 811 of the National Affordable Housing Act of 1990, as amended.

Providing that there have been no defaults in the terms of the advance the note will mature and be deemed to be paid and discharged on October 1, 2036.

If default be made by the owner under the terms of this Note, the Regulatory Agreement or the Regulations, at the option of the holder of this Note, the entire principal sum of $1,141,400 shall at once become due and payable without notice. Interest per annum at a rate equal to 7.875%, shall be payable on demand with respect to the payment of principal upon default.

NOTE 4 - S3100-240 ENTITY RISKS

The entity is subject to the normal risks of owning and operating an apartment complex. All insurable risks are covered by private insurers.

NOTE 5 - S3 l 00-240 TEMPORARILY RESTRICTED NET ASSETS

The capital advance from HUD is subject to donor-imposed restrictions. Accordingly, these net assets are accounted for as temporarily restricted net assets. See Note 3 for restriction.

NOTE 6 - S3100-230 MANAGEMENT FEE

The Project pays a management fee of 13.5% of gross revenues to R.C. Management, Inc. The management fee P.U.P.M. was $58.76. The total management fee for the year was $16,922.

-11-

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. l 15-HD012-WDD

NOTES TO FINANCIAL STATEMENTS

FOR THE YEAR ENDED MARCH 31, 2018

NOTE 7 - S3 l 00-240 LOSS CONTINGENCY

For certain Section 8 assisted projects, when a project's Section 8 contract is terminated or expires and is not renewed, HUD may request the project owners or managing agent to return to HUD the funds remaining in the Residual Receipts account. It is reasonably possible that HUD will request any balance of Residual Receipts to be transferred back to HUD. The current contract expires September 30, 2018.

NOTE 8 - S3 l 00-240 FUNCTIONAL ALLOCATION OF EXPENSES

Expenditures incurred in connection with project operations and expenditures made for corporate purposes have been summarized on a functional basis in the statement of activities and changes in net assets.

NOTE 9 - S3 l 00-240 CURRENT VULNERABILITY DUE TO CERTAIN CONCENTRATIONS

The Project's sole asset is a 24-unit apartment complex. The Project's operations are concentrated in the multifamily real estate market. In addition, the Project operates in a heavily regulated environment. The operations of the Project are subject to the administrative directives, rules and regulations of federal, state and regulatory agencies, including, but not limited to, HUD. Such administrative directives, rules and regulations are subject to change by an act of congress or an administrative change mandated by HUD. Such changes may occur with little notice or inadequate funding to pay for the related costs, including the additional administrative burden, to comply with a change. Thirty-seven percent of the project's revenue is received from HUD.

NOTE 10- S3100-200 RELATED PARTY INFORMATION

The management company has a wholly owned subsidiary, HAPSCO, Inc., that purchases all supplies in bulk in order to obtain volume discounts. The supplies are then sold to the properties at cost. Total purchases from HAPSCO, Inc. by the property for the year ended March 31, 2018 were $40.

NOTE 11 - S3100-240 SUBSEQUENT EVENTS

Subsequent events have been evaluated by Management through June 28, 2018 which is the date financial statements were available to be issued.

NOTE 12 - S3100-240 IMPAIRMENT OF LONG LIVED ASSETS

The Project reviews its rental property for impairment whenever events or changes in circumstances indicate that the carrying value of an asset may not be recovered. If the fair value is less than the carrying amount of the asset, an impairment loss is recognized for the difference. No impairment loss has been recognized during the year ended March 31, 2018.

-12-

SUPPLEMENTARY INFORMATION

-13-

I LASKER VILLAGE APARTMENTS

(a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HD012-WDD

INDEX TO SUPPLEMENTARY INFORMATION REQUIRED BY HUD

ITEM PAGE

Statement of Financial Position Data 15

Statement of Activities Data 16-17

Statement of Changes in Net Assets Data 18

Statement of Cash Flows Data 19-20

Calculation of Surplus Cash 21

Schedule of Changes in Fixed Assets 22

Schedule of Reserve for Replacements 23

Schedule of Residual Receipts 23

-14-

l l LASKER VILLAGE APARTMENTS

(a Texas Non-Profit Corporation)

HUD PROJECT NO. l 15-HD012-WDD

STATEMENT OF FINANCIAL POSITION DA TA

AS OF MARCH 31, 2018

CURRENT ASSETS 1120 Cash - Operations 1130 Accounts Receivable - Tenant 1200 Miscellaneous Prepaid Expense

11 00T Total Current Assets

ASSETS

TENANT SECURITY DEPOSITS - HELD IN TRUST 1191 Tenant Security Deposits

RESTRICTED DEPOSITS AND FUNDED RESERVES 13 10 Insurance Escrow Deposit 1320 Reserve for Replacement - (Note 2) 1340 Residual Receipts - (Notes 2 and 7)

1300T Total Deposits and Funded Reserves

FIXED ASSETS - (Notes 2 and 3) 1410 Land 1420 Buildings 1440 Building Equipment - Portable 1460 Furnishings 1465 Office Furniture and Equipment 14 70 Maintenance Equipment

1400T Total Fixed Assets 1495 Less Accumulated Depreciation

1400N Net Fixed Assets

1 000T TOT AL ASSETS

-15-

$ 8,093 36

5,404

685 58,212

55,535 1,070,634

8,521 7,963

16,478 760

1,159,891 (551,453)

$ 13,533

5,628

58,897

608,438

$ 686,496

LIABILITIES AND NET ASSETS

CURRENT LIABILITIES 2110 Accounts Payable - 30 Days 2111 Accounts Payable - HUD 2120 Accrued Wages Payable 2123 Accrued Management Fee Payable

2122T Total Current Liabilities

TENANT SECURITY DEPOSITS - HELD IN TRUST 2191 Tenant Security Deposits

2000T TOT AL LIABILITIES

UNRESTRICTED NET ASSETS Deficit from Operations

Total Unrestricted Net Assets (Deficit)

NET ASSETS

TEMPORARILY RESTRICTED NET ASSETS (Note 3) HUD Capital Advance - (Note 3)

Total Temporarily Restricted Net Assets

3033T Total Net Assets

2033T TOT AL LIABILITIES AND NET ASSETS

-15-

$ 7,629 209 496

1,340

(470,206)

1,141,400

$ 9,674

5,628

15,302

(470,206)

1,141,400

671,194

$ 686,496

Statement of Activities Data

U. S. Department of Housing and Urban development Office of Housing

Public Reporting Burden for this collection of infonnation is estimated to average 1.0 hours per response, including the time for reviewing instructions, searching existing data sources, gathefing and maintaining the

data needed, and completing and reviewing the collection of information. Send comments regarding this burden estimate or any other aspect of this collection of information, including suggestions for reducing this

burden, to the Reports Management Officer, Office of Information Policies and Systems, U.S. Department of housing and Urban Development, Washington, D.C. 20410-3600 and to the Office of Management and Budget. PapeMOrk Reduction Project (2502-0052), Washington O.C., 20503. Do not send this completed form to either of these addresses.

For Period Project Number: Project Name: Beginning

04/01/17 Part I

Rental

Income

5100

Vacancies

5200

Financial

Revenue

5400

Other

Revenue

5900

Ending

03/31/18

Description of Account

115-HD012

Rent Revenue - Gross Potential

Rent Revenue / Insurance

S ecial Claims Revenue

Retained Excess Income

Total Rent Revenue

A artments

Stores and Commercial

Total Vacancies

Net Rental Revenue - Rent Revenue less vacancies

Eldert and Con re ate Services Income - 5300

Total Service Income ( Page 24)

Financial Revenue - Pro"ect O erations

Revenue from Investments - Residual Receipts

Revenue from Investments - Replacement Reserve

Revenue from Investments - Miscellaneous

Total Financial Revenue

Revenue

Tenant Charges

Interest Reduction Pa ent Revenue

Miscellaneous Revenue

Total Other Revenue

Total Revenue

Conventions and Meetin s

Office Salaries

Office Expense

Office or Model Apartment Rent

Administrative Management Fee

Expenses

6200/6300

Manager or Superintendent Salaries

Administrative Rent Free Unit

Legal Expense - Pro·ect

Audit Ex ense

Bookkeeping Fees/Accountin Services

Bad Debts

Misc Administrative E

-16-

Acct. No.

5120

5121

5140

5170

5180

5190

5191

5192

5193

5194

5100T

5220

5240

5250

5270

5290

5200T

5152N

5300

5410

5430

5440

5490

5400T

5910

5920

5945

5990

5900T

5000T

6203

6204

6210

6250

6310

6311

6312

6320

6330

6331

6340

6350

6351

6370

6390

6263T

LASKER VILLAGE APARTMENTS

Amount*

57,007

68,129

0

0

0

0

0

0

0

0

1,082

0

0

0

0

0

0

0

22

0

1,295

246

0

0

60

0

0

403

0

5,586

0

16,922

10,913

0

516

3,700

2,016

0

933

-------$41,049

form HUD-92410

Utilities

Expense

6400

Operating

and

Maintenance

Expenses

6500

Taxes

and

Insurance

6700

Financial

Expenses

6800

Corporate or

Mortgagor

Entity

Expenses

7100

Fuel Oil / Coil

Electricity (Light and Misc. Power)

Water

Gas

Sewer

Total Utilities Ex ense

Contracts

Operating & Maintenance Rent Free Unit

Garbage & Trash Removal

Security Payroll/Contract

Security Rent Free Unit

Heating/Coolin Repairs & Maintenance

Snow Removal

Vehicle & Maintenance Equipment Operation & Repairs

Miscellaneous O eratin and Maintenance Ex enses

Total Operating and Maintenance Expenses

Real Estate Taxes

Payroll Taxes

Property and Liabili Insurance Hazard)

Fidelity Bond Insurance

Workmen's Compensation

Health Insurance and Other Employee Benefits

Misc. Taxes, License, Permits and Insurance

Total Taxes and Insurance

Interest on Mort a e Pa able

Interest on Notes Payable (Long Term)

Interest on Notes Payable Short Term

Mortgage Insurance Premium/Service Charge

Miscellaneous Financial Ex ense

Total Financial Expenses

Total Service Expenses

Total Cost of Operations Before Depreciation

Profit (Loss) Before Depreciation

Depreciation (Total - 6600 (specify

Amortization Expense

Operating Profit or (Loss)

Officer Salaries

LegalExpenses(Enti

Taxes Federal-State-Entity)

Other Expenses (Enti

Total Corporate Expense

NET PROFIT OR (LOSS)

6420 0

6450 5,668

6451 3,202

6452 0

6453 3,806

6400T

6510 14,080

6515 5,784

6520 13,830

6521 0

6525 945

6530 962

6531 0

6546 1,895

6548 0

6570 628

6590 0

6500T

6710 0

6711 1,496

6720 4,973

6721 204

6722 536

6723 909

6790 0

6700T

6820 0

6830 0

6840 0

6850 0

6890 0

6800T

6900

6000T

5060T

6600

6610

5060N

7110 0

7120 0

7130-32 0

7190 0

7100T

3250 Warning: HUD v.ill prosecute false claims and statements. Conviction may result in criminal and/or civil penalties. (18 U.S.C. 1001, 1010, 1012;31 U.S.C. 3729, 3802) Miscellaneous or other Income and Expense Sub-account Groups. ff miscellaneous or other income and/or expense sub-accounts (5190, 5290, 5490, 5990, 6390, 6590, 6729 6890 & 7190) exceed the Account Grouping by 10% or more attach a separate schedule describing or explaining the miscellaneous income or expense

Part II 1. Total principal payments required under the mortgage, even if payments under a Workout Agreement are less or more

than those required under the mortgage.

2. Replacement Reserve deposits required by the Regulatory Agreement or Amendments thereto, even if payments may be temporarily suspended or waived.

3. Replacement Reserve or Residual Receipts releases which are included as expense items on this Profit and Loss statemer 4. Project Improvement Reserve Releases under the Flexible Subsidy Program that are included as expense items on this

Profit and Loss Statement.

$0

0

$99,967

$25,650

$29,398

$0

($3,748)

$0

$17,556

$0

$0 form HUD-92410

-17-

Sl 100-060

3247

3131

Sl 10-070

3132

SI 100-050

3250

3130

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HUD012-WDD

STATEMENT OF CHANGES IN NET ASSETS DATA

FOR THE YEAR ENDED MARCH 31, 2018

Previous Year Unrestricted Net Assets

Change in Unrestricted Net Assets from Operations

Unrestricted Net Assets

Previous Year Temporarily Restricted Net Assets

Temporarily Restricted Net Assets

Previous Year Total Net Assets

Change in Total Net Assets from Operations

Total Net Assets

-18-

$ (466,458)

(3,748)

$ (470,206)

$ 1,141,400

$ 1,141,400

$ 674,942

(3,748)

$ 671,194

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HD012-WDD

STATEMENT OF CASH FLOWS DATA

FOR THE YEAR ENDED MARCH 31, 2018

CASH FLOWS FROM OPERA TING ACTIVITIES: S1200-010 Rental Receipts S 1200-020 Interest Receipts S1200-030 Commercial Rents Receipts S1200-030 Tenant Charges

S 1200-040 Total Receipts

S1200-050 Administrative Disbursements S1200-070 Management Fees S 1200-090 Utilities S1200-100 Salaries and Wages S 1200-110 Operating and Maintenance S 1200-140 Property Insurance S1200-150 Miscellaneous Taxes and Insurance

S1200-230 Total Disbursements

S1200-240 Net Cash Provided by Operating Activities

CASH FLOWS FROM INVESTING ACTIVITIES: S1200-245 Net Deposits from the Mortgage Escrow S 1200-250 Net deposits to the Reserve for Replacement Account S1200-260 Net Deposits to Residual Receipts Sl200-330 Net Purchase of Fixed Assets

S1200-350 Net Cash Used by Investing Activities

S 1200-4 70 NET INCREASE IN CASH AND CASH EQUIVALENTS

S 1200-480 BEGINNING CASH AND CASH EQUIVALENTS

S 1200T ENDING CASH AND CASH EQUIVALENTS

-19-

$ 123,994 22

1,295 246

125,557

(11,182) (18,367) (14,188) (24,802) (27,750)

(9,583) (2,941)

(108,813)

16,744

3,566 23,740

6,093 (47,819)

(14,420)

2,324

5,769

$ 8,093

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HD012-WDD

STATEMENT OF CASH FLOWS DATA, (Continued)

FOR THE YEAR ENDED MARCH 31, 2018

ADJUSTMENT TO RECONCILE CHANGE IN NET ASSETS TO NET CASH USED BY OPERATING ACTIVITIES:

3250 Change in Total Net Assets from Operations Adjustment to Reconcile Change in Net Assets to

6600

S1200-490 S1200-520 S1200-530

S1200-540 S1200-560 S1200-580 S1200-590

S1200-610

Net Cash Used by Operating Activities: Depreciation Decrease (Increase) in:

Tenant Account Receivable Prepaid Expenses Tenant Security Deposit Cash

Increase (decrease) in: Accounts Payable Accrued Liabilities Tenant Security Deposit Liability Prepaid Revenue

Net Cash Provided By Operating Activities

-20-

$ (3,748)

29,398

(36) (4,406)

375

(3,186) (1,045)

(375) (233)

$ 16,744

Sl300-010 1135

S 1300-030

Sl300-040

S 1300-075 Sl300-100

2191

Sl300-140

S1300-150

Sl300-210

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. l 15-HD012-WDD

SUPPLEMENTARY INFORMATION REQUIRED BY HUD

CALCULATION OF SURPLUS CASH

FOR THE YEAR ENDED MARCH 31, 2018

Cash Tenant Subsidy Due for the Period Covered by Financial Statement Other

Total Cash

Accounts Payable - Operations Accrued Expenses (Not escrowed) Tenant Security Deposit Liability

Total Current Obligations

Surplus Cash (Deficiency)

Deposits Due Residual Receipts

-21-

$ 13,721

$ 13,721

$ 7,629 2,045 5,628

$ 15,302

$ (1,581)

$

LAND 1410P 1410AT 1410DT 1410

BUILDINGS 1420P 1420AT 1420DT 1420

LASKER VILLAGE APARTMENTS

(a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HD012-WDD

SUPPEMENTARY INFORMATION REQUIRED BY HUD

SCHEDULE OF CHANGES IN FIXED ASSETS

FOR THE YEAR ENDED MARCH 31, 2018

Beginning Balance for 1410 Additions for 1410 Deductions for 1410 Land

Beginning Balance for 1420 Additions for 1420 Deductions for 1420 Buildings

BUILDING EQUIPMENT (PORT ABLE) 1440P Beginning Balance for 1440 1440AT Additions for 1440 1440DT Deductions for 1440 1440 Building Equipment (Portable)

FURNISHINGS 1460P Beginning Balance for 1460 1460AT Additions for 1460 1460DT Deductions for 1460 1460 Furnishings

OFFICE FURNITURE AND EQUIPMENT 1465P Beginning Balance for 1465 1465AT Additions for 1465 1465DT Deductions for 1465 1465 Office Furniture & Equipment

MAINTENANCE EQUIPMENT 1470P Beginning Balance for 14 70 1470AT Additions for 14 70 1470DT Deductions for 14 70 1470 Maintenance Equipment

TOT AL FIXED ASSETS 1400PT Total Beginning Balance for Fixed Assets 1400AT Total Asset Additions 1400DT Total Asset Deductions 1400T Total Fixed Assets

1495P Beginning Balance for Accumulated Depreciation 6600 Total Provisions for Depreciation 1400ADT Total Accumulated Depreciation from Disposed Assets 1495 Ending Balance for Accumulated Depreciation

1400N Total Net Book Value

-22-

$ 55,535

55,535

1,068,505 44,516

(42,387) 1,070,634

8,090 431

8,521

7,963

7,963

13,606 2,872

16,478

760

760

1,154,459 47,819

(42,387) $ 1,159,891

$ 564,442 29,398

(42,387) $ 551,453

$ 608,438

I ,$

I I

l LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. l 15-HD012-WDD

OTHER SUPPLEMENTARY INFORMATION REQUIRED BY HUD

FOR THE YEAR ENDED MARCH 31, 2018

RESERVE FOR REPLACEMENT

In accordance with the provisions of the regulatory agreement, restricted cash is held in savings accounts with local banks, to be used for replacement of property with the approval of HUD as follows:

1320P 1320DT 1320NT 1320WT 1320OWT

1320

1340P 1340DT 1320INT 1340WT 1340OWT

1340

Schedule of Reserve for Replacements Balance, March 3 I, 2017 Deposits Other deposits - interest income HUD Approved Withdrawals Other withdrawals - bank service charges

Balance, March 3 1, 2018

Schedule of Residual Receipts

Balance, April 1, 2017 Total Deposits Other deposits - interest income HUD Approved Withdrawals Other withdrawals - bank service charges

Balance, March 31, 2018

ELDERLY AND CONGREGATE SERVICES INCOME {5300)- None

ELDERLY AND CONGREGATE SERVICES EXPENSE {6900)- None

-23-

$

$

$

$

81,952 17,556

22 (41,286)

(32)

58,212

6,093

(6,083) (10)

l l I l I

l I

l

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. l 15-HD012-WDD

SCHEDULE OF EXPENDITURES OF FEDERAL AW ARDS

FOR THE YEAR ENDED MARCH 31, 2018

FEDERAL GRANTOR/ PROGRAM TITLE

U.S. DEPARTMENT OF HUD

Section 8 - Housing Assistance Payments

FEDERAL CFDA NUMBER

14.195

YEAR ENDED MARCH 31, 2018

$ 68,129

*Section 811 - of the National Affordable Housing Act Capital Advance Program 14.181 1,141,400

TOTAL FEDERAL FINANCIAL ASSISTANCE $ 1,209,529

See accompanying notes to schedule of expenditures of federal awards.

-24-

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. l 15-HD012-WDD

NOTES TO SCHEDULE OF EXPENDITURES OF FEDERAL AW ARDS

FOR THE YEAR ENDED MARCH 31, 2018

NOTE A-BASIS OF PRESENTATION

The accompanying schedule of expenditures of federal awards includes the federal award activity of Lasker Village Apartments (a Texas Non-Profit Corporation) HUD Project No. 115-HD012-WDD and is presented on the accrual basis of accounting. The information in this schedule is presented in accordance with the requirements of Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance). Because the Schedule presents only a selected portion of the operations of Lasker Village Apartments (a Texas Non-Profit Corporation), it is not intended to and does not present the financial position, changes in net assets, or cash flows of Lasker Village Apartments (a Texas Non-Profit Corporation).

NOTE B-SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Expenditures reported on the Schedule are reported on the accrual basis of accounting. Such expenditures are recognized following the cost principles contained in the Uniform Guidance, wherein certain types of expenditures are not allowable or are limited as to reimbursement. Lasker Village Apartments (a Texas Non-Profit Corporation) had elected not to use the 10-percent de minimis indirect cost rate allowed under Uniform Guidance.

NOTE C-U.S. Department of Housing and Urban Development Capital Advance Program

Lasker Village Apartments (a Texas Non-Profit Corporation) Section 81 lCapital Advance balance of $1,141,400 since its final funding in 1996. There are no pass through entities or expenditures to subrecipients. The project is contingently liable on the balance of the capital advance at March 31, 2018 which was $1,141,400- See Note 3.

-25-

JEFFREYS. BULLINGTON, CPA RAY PARKER, CPA

KARIN NELSON, CPA

Members American Institute of Certified Public Accountants

Cundiff Rogers+Solt PC A PROFESSIONAL CORPORATION

CERTIFIED PUBLIC ACCOUNTANTS 6243 1H 10 West, Suite 950 San Antonio, Texas 78201 (210) 734-9500 Fax (210) 736-9500 email: [email protected] www.crs-cpas.com

INDEPENDENT AUDITOR'S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

Board of Directors Lasker Village Apartments San Antonio, Texas

HUD Field Office San Antonio, Texas

We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of Lasker Village Apartments, HUD Project No. 115-HD012-WDD, which comprise the statement of financial position as of March 31, 2018, and the related statements of activities and changes in net assets, and cash flows for the year then ended, and the related notes to the financial statements, and have issued our report thereon dated June 28, 2018.

Internal Control Over Financial Reporting

In planning and performing our audit of the financial statements, we considered Lasker Village Apartments internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of Lasker Village Apartments internal control. Accordingly, we do not express an opinion on the effectiveness of Lasker Village Apartments internal control.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

-26-

I I

Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

Compliance and Other Matters

As part of obtaining reasonable assurance that Lasker Village Apartments' financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity's internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity's internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

San Antonio, Texas June 28, 2018

-27-

I Cundiff Rogers+Solt PC

JEFFREYS. BULLINGTON, CPA RAY PARKER, CPA

KARIN NELSON, CPA

Members American Institute of Certified Public Accountants

A PROFESSIONAL CORPORATION

CERTIFIED PUBLIC ACCOUNTANTS 6243 1H 10 West, Suite 950 San Antonio, Texas 78201 (210) 734-9500 Fax (210) 736-9500 email: [email protected] www.crs-cpas.com

INDEPENDENT AUDITOR'S REPORT ON COMPLIANCE FOR EACH MAJOR PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY THE UNIFORM

GUIDANCE

Board of Directors Lasker Village Apartments San Antonio, Texas

Report on Compliance for Each Major Federal Program

HUD Field Office San Antonio, Texas

We have audited Lasker Village Apartments, HUD Project No. 115-HD012-WDD, compliance with the types of compliance requirements described in the 0MB Compliance Supplement that could have a direct and material effect on each of Lasker Village Apartments major federal programs for the year ended March 31, 2018. Lasker Village Apartments major federal programs are identified in the summary of auditor's results section of the accompanying schedule of findings and questioned costs.

Management's Responsibility

Management is responsible for compliance with the requirements of laws, regulations, contracts, and grants applicable to its federal programs.

Auditor's Responsibility

Our responsibility is to express an opinion on compliance for each of Lasker Village Apartments major federal programs based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and the audit requirements of Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance). Those standards and the Uniform Guidance require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about Lasker Village Apartments compliance with those requirements and performing such other procedures as we considered necessary in the circumstances.

-28-

I We believe that our audit provides a reasonable basis for our opinion on compliance for each major federal program. However, our audit does not provide a legal determination of Lasker Village Apartments compliance.

Opinion on Each Major Federal Program

In our opinion, Lasker Village Apartments complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs for the year ended March 31, 2018.

Report on Internal Control Over Compliance

Management of Lasker Village Apartments is responsible for establishing and maintaining effective internal control over compliance with the types of compliance requirements referred to above. In planning and performing our audit of compliance, we considered Lasker Village Apartments internal control over compliance with the types of requirements that could have a direct and material effect on each major federal program to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for each major federal program and to test and report on internal control over compliance in accordance with the Uniform Guidance, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of Lasker Village Apartments internal control over compliance.

A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance.

Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

The purpose of this report on internal control over compliance is solely to describe the scope of our testing of internal control over compliance and the results of that testing based on the requirements of the Uniform Guidance. Accordingly, this report is not suitable for any other purpose.

San Antonio, Texas June 28, 2018

-29-

1

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. 115-HD012-WDD

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE YEAR ENDED MARCH 31, 2018

Summary of Auditor's Results:

1. Type of report - Unmodified opinion.

2. No reportable conditions or material weaknesses were identified.

3. No noncompliance that is material to the financial statements was identified.

4. No reportable conditions in internal control over major program and, consequently, no material weaknesses were identified.

5. Type of report on compliance for major programs - Unmodified opinion.

6. There were no audit findings relating to the major program that are required to be reported in accordance with 2 CFR section 200.516(a).

7. Major programs tested: (a) CFDA number 14.181 - Sec. 811 -Capital Advance Program $1,141,400

8. The dollar threshold to distinguish between Type A and Type B programs was $750,000.

9. The auditee did not qualify as a low-risk auditee.

Findings relating to items 2 and 3 above - None.

Findings and questioned costs referred to in items 4, 5, and 6 above relative to the major programs - None.

-30-

LASKER VILLAGE APARTMENTS (a Texas Non-Profit Corporation)

HUD PROJECT NO. l 15-HD012-WDD

MARCH 31, 2018

ATTACHMENT TO INDEPENDENT ACCOUNTANT'S REPORT ON APPL YING AGREED-UPON PROCEDURE

UFRS Rule Information Hard Copy Document(s)

Balance Sheet, Revenue and Expense and Supplemental Schedules with Cash Flow Data (account numbers 1120 to Statement Data 7 IO0T and the S 1200 series)

Surplus Cash (S 1300 series of accounts) Computation of Surplus Cash, Distributions and Residual Receipts (Annual)

Footnotes (S3 l 00 series of accounts) Notes to the Financial Statements

Type of Opinion on the Financial Statements Auditor's Reports on the Financial and Auditor Reports (S3400, S3500 and Statements, Compliance and S3600 series of accounts) Internal Control

Type of Opinion on Supplemental Data Auditor's Report on Supplemental (account number S3400-100) Data

Audit Findings Narrative (S3800 series of Schedule of Findings and accounts) Questioned Costs

General information (S3300, S3700 and Schedule of Findings and S3 800 series of accounts) Questioned Costs and 0MB Data

Collection Form

-35-

Findings

Agrees

Agrees

Agrees

Agrees

Agrees

Agrees

Agrees

I

I

![Capablanca - Lasker Match 1921 [Capablanca, 1921]](https://img.dokumen.tips/doc/110x75/577cda471a28ab9e78a54085/capablanca-lasker-match-1921-capablanca-1921.jpg)