Embed Size (px)

Citation preview

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

1

Management Meeting Note – September 2014

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

2

Corporate Factsheet

Promoter Background Promoted by the Anna Group, Kitex Garments Limited (KGL) is currently

managed by second generation entrepreneur Mr. Sabu M Jacob whose father

Mr.M.C Jacob founded the group in 1968.

Presence KGL currently has no retail presence in India however is expected to launch its

own retail brand in USA shortly. The company caters directly to wholesalers and

retailers based out of the United States and European Union.

Management depth Number of Promoter Directors: 1; Mr. Sabu M Jacob - Chairman & Managing

Director ; Other Directors: Prof. E.M Paulose ;Mr. Benni Joseph; Mr. C Mohan;

Mr. K.L.V Narayanan

Business KGL is primarily engaged in contract manufacturing of infantwear (less than 24

months of age) to apparel wholesalers & retailers based out of the US and UK.

The company also manufactures fabric which in addition to being used captively

is also sold to the group entities.

Corporate Structure The Company is a part of the larger Anna-Kitex Group, which has diversified

interests in aluminum vessels, home appliances, spice trading and textiles. Sister

concerns within the industry include Kitex Ltd, Kitex Childrenswear Limited (KCL)

and Kitex bags. Group Entity KCL holds a ~15.5% stake in KGL.

Revenue Model (FY14) KGL derived around 80% of its revenues (in FY14) from contract manufacturing

for wholesalers and retailers while the remaining was derived from sale of fabric.

Capacity Fully integrated manufacturing facility at Kizhakkambalam (Kerala) with a facility

to manufacture ~0.32 million pieces per day and a fabric processing capacity of

48 MT. However, including KCL’s capacity, total capacity stands at ~0.55 million

pieces/day.

Key Clientele Mothercare, Jockey, Wal-Mart,Kohls, The Childrens’ Place, Gerber, Carter’s,

Toys R Us are the major customers of the Kitex group.

Key Brands The company plans to launch its own retail brand in the US shortly.

Credit Rating ICRA A+/Stable (long term facilities)

ICRA A1 (Short term facilities)

Corporate Bankers State Bank of India

Auditors M/S Kolath & Co.

Market Data

Market Cap Rs.~16bn

Shareholding Promoter: 54.3%; Others:

45.6%

52-week High-Low (Rs.) Rs.359.70 (Aug 27,2014);

Rs.54.30 (September 6, 2013)

All time High-Low (Rs.) Rs.359.70 (Aug 27,2014);

Rs.0.04 (October 10,2001)

3M Average daily

Volume 195,931

Stock Return (%)

Correction from 52WH 6%

Rise from 52WL 522%

F&O NA

FII limit 24%

Stock exchange list BSE,NSE

3M 6M 1Y YTD

35% 276% 505% 311%

Fundamental View

Current Market Price Rs.338

Recommended entry

price NA

Target Price NA

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

3

Key takeaways from the management interaction and Plant Visit (1/2)

Industry dynamics and growth potential: KGL is engaged in manufacturing of ‘infantwear’ majorly exporting its produce to USA and UK. USA consumes

~20% of all the childrenwear manufactured globally making it the largest and most lucrative market to operate in. Management pointed out that higher purchase

frequency makes infantwear the most profitable among childrenwear offerings. KGL noted that USA is more design oriented with lots of colours and various

styling; the market though continues to offer the cheapest infantwear offering in the world. However, customer friendly return and easy claims policy makes

quality a paramount feature. KGL ventured into USA market supplying mass market offerings to Gerber and only in the last few years has entered into sourcing

agreements with Carter’s (premium segment player). Management also noted that quality is a key purchase consideration in infantwear; thereby trusted brands

as Carter, Babies-R-Us, Gerber, The Children's Place, Mothercare and a few others have only endured over several decades. KGL products are currently limited

to only infantwear offering, but has offlate also started manufacturing innerwear incorporating OUTLAST® technology on a specific request from Jockey.

Sources of economic moat: Having been exploited in its initial years by the buyers, KGL deciphered the ‘right’ business model and began investing in the

Safety-Security- Social and Environmental compliance norms, which they believe have given them a significant competitive moat over competition. Management

pointed that buyers too have graduated to look beyond pricing and have begun to look on additional factors as quality and timeliness of delivery. KGL noted that

for the first two years vendors and suppliers assess performance and execution of each other beyond which the relationship really matures; KGL noted that all

their buyers are either in the $13-15mn or $28-30mn range. Management also iterated that buyers face considerable exit barriers in-terms of quality, price and

comfort, which assists vendors as KGL enjoying lower buyer attrition.

……..with financials confirming the robustness of the business model

Profitable Growth: Sales grew 13% CAGR in FY10-14 complimented by Net Profit growth of 33% CAGR for the same period.

Enviable Balance Sheet - Cash Flows : Cash surplus in FY14- Rs. ~1032mn (~6% of current market capital), Debt/Equity as on March 31,2014 - 0.7,

Positive Cash flow from operations for the last five years except in 2011 indicate the sound fundamentals of the balance sheet.

Healthy Return Ratios: FY10-FY14, Avg. ROCE ~ 20% Avg.ROE ~ 36%-comparable to that of top notch branded players.

Sustained Operating profitability: Based on its moderate pricing power, established relationship with clients and growing infantwear sector globally coupled

with the economic moat the company derives, we expect KGL to continue to benefit from healthy operating profitability in the range of 20-25%.

No dilution of capital: Despite consistently growing at 5x in 10 years, there has been no dilution of capital by the promoters indicating the management’s

ability to grow even without funding of external sources

Management stated that they plan to become debt free in the medium term and pointed out that they are already debt free on a net debt basis.

Competitive Landscape: According to the management, Kitex group is the third largest manufacturer of infantwear in the world and one among the only twelve

entities globally with a capacity to manufacture more than 0.5 million units per day. Though wages are lower in Bangladesh, higher machine productivity and

process in infantwear provides KGL a natural moat. KGL did acknowledge that wholesalers/retailers constantly pressurise suppliers for lower pricing, given that

not many of the wholesalers/retailers themselves are profitable. KGL however believes informing in advance on yarn costs, trims & accessory costs, labour

costs, and the dollar-Rupee equation does assist in further price negotiations. KGL also iterated in avoiding single client concentration risk.

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

4

Key takeaways from the management interaction and Plant Visit (2/2)

Growth plans: Management indicated that the infantwear market in India, China and Middle East is rapidly growing and most of the global brands would

derive a significant portion of revenues from these markets in the medium term. Population and growth potential in emerging economies continue to present

attractive opportunities. Mothercare has established many stores in India under both the company owned model and franchisee operations. When the market

further opens up in India over the next 3-5 years, Management expects similar initiatives from the other players as Carter’s, Gerber and Walmart look to

establish their presence in India.

Geographical concentration and customer concentration in revenue profile: Three-fourths of KGL’s revenues are derived from US and rest from Europe.

However, management downplayed this geographical risk, as majority of customers to whom they supply have global presence. Though KGL faces significant

customer concentration with three players (Gerber, Jockey and Toys R US) accounting for majority of revenues till last year, the company’s recent addition of

major customers like Kohl’s and Children’s Place and management’s stance of not supplying more than $~30-40 million to a single customer should

addressed this concern.

Capex Plans: KGL confirmed that the current fabric capacity at 48 MT is sufficient to see through the targeted garmenting capacity of 1.1 Mn pieces/day in 2-3

years. The management plans to increase the capacity of the group from the current 0.55 million pieces to 1.1 million pieces over the medium term. In this

regard the company is expected invest heavily towards cutting and sewing machinery. The management expects capital outlay of Rs.300-400 million for the

group as a whole and Rs.150 million for KGL exclusively over the next 18-20 months. Management indicated that current utilisation/efficiency levels are close

to 50-60% with ~8000 employees (KGL and KCL).

Our views on KGL:

We commend KGL for doing a phenomenal job of scaling revenues ~6x in 10 years in a difficult B2B business without any capital dilution. Institutional

drivers provide strong economic moat and should reflect in healthy earnings growth. The management believes that revenues could grow ~20-25% in near

term, though weakening USD could be a dampener.

We however believe increasing competitive intensity from India and emergence of other outsourcing markets leads to challenging industry climate. While

clients constantly pressurizing on price could also lead to subdued revenue growth, we believe current economic moat established by KGL should assist

them in maintaining earnings momentum in medium term.

KGL’s sister entity KCL also operates in the infantwear industry supplying to players like Carter’s and Mothercare. Though there is a conflict of interest

given that both the entities operate in the same space and managed by the same team with KCL being unlisted; we take solace that management

underscored that KCL would be merged with KGL at the appropriate time. However, valuation, timing of merger and pay-out method (Cash/share swap )

remains ambiguous.

KGL plans to launch its own brand in the US which can further improve the business profile of the company, the risks and concerns in managing and

succeeding in the same are critical factors to watch out for adding to the fact that this might be detrimental to KGL’s relationship with its existing clients.

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

5

Kitex revenues are based on demand for infantwear apparels

Source: Company, Spark Capital

Overview of Kitex Limited

Having established as a strong supplier, direct entry being mulled

Source: Company, Spark Capital

Revenues have been driven by acquisition of new clients

Source: Company, Spark Capital

Revenue profile currently hinges on developed markets infantwear

offtakes

Source: Company, Spark Capital

USA, 80.0%

UK, 20.0%

Contract Manufacturers

Apparel Wholesalers & Retailers

Customers

KGL (India), Wing Lu

(China), Gin Mill

(Singapore), Jay Jay

Mils (India), etc…

Gerber, Carter, Toys

R Urs, Jockey,

Mothercare, etc…

Across North

America and Europe

2014 •Expected to launch own brand in US market shortly

2005 •Company split face value of its shares from Rs.10 to Rs.1

2004 • Increased focus on recession proof Infantwear industry; garment unit began manufacturing infantwear only

1995 •KGL goes Public; listed on NSE and BSE

1992 • Incorporated as a public limited company by the Anna group

0.80 1.11

1.62 1.93 1.99

2.68 2.56 3.15 3.17

4.42

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

FY 05 FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.b

n

Revenue

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

India Population: ~1.27 billion

India Population growth rate:1.2%

India Kids and babywear Market Size: ~$8bn

Source: Carter Annual report and Industry sources ,Spark Capital

6

World Infant wear and Kidswear Market – Major Countries

Brazil Population: ~203 million

Brazil Population growth rate:0.9%

Brazil Baby and kidswear Market Size: NA

USA Population: ~323 million

USA Population growth rate:0.7%

USA Baby and kidswear Market Size: ~$19bn

UK Population: 64 million

UK Population growth rate:0.6%

UK Kids and babywear market Size: ~5.2bn

pounds

China Population: ~1.40 billion

China Population growth rate:0.5%

China Kids and babywear Market Size:

~RMB 116.4bn

World Population: ~7.26 billion

World population growth rate: 1.14%

World Baby and kidswear Market Size : ~$155 billion

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

7

Industry sources peg childrenswear market to record ~6% CAGR (5 years)

Source: Bloomberg Business Intelligence, Spark Capital

Global childrenswear market to grow at a quicker pace in the next 6 years

Prominent players in the Infantwear market

Source: Industry sources, Spark Capital

10

30

50

70

90

110

130

150

170

190

210

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014E

2015E

2016E

2017E

2018E

US

D b

n

Childrenswear market contribution to apparels to increase in near term

Source: Bloomberg Business Intelligence, Spark Capital

Baby and Toddler Wear 22%

Boys' Apparel 36%

Girls' Apparel 42%

Infantwear market currently is about ~22% of the childrenswear market

globally

Source: Bloomberg Business Intelligence, Spark Capital

89.1% 89.1% 89.0% 88.8% 88.9% 89.0% 89.0% 89.0% 88.9%

10.9% 10.9% 11.0% 11.2% 11.1% 11.0% 11.0% 11.0% 11.1%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013

Others as a % of apparels market Childrens Wear as a % of apparels market

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

8

USA remains a prominent market given it consumes ~1/5th of

childrenwear apparel manufactured…

Source: Bloomberg business intelligence, Spark Capital

USA remains one of the key markets for apparel consumption driven by higher income and propensity to spend

USA infantwear market has largely remained resilient to macro

economic fluctuations

Source: Carter Annual reports, Spark Capital

…led by plethora of players – market plagued by wide unorganized and

fragmented market

Source: Bloomberg business intelligence, Spark Capital

Facts, Figures and trends in the US Infantwear market

• Increase in double income earning families and working population are

believed to be the leading growth drivers.

• We see that this industry displayed strong resilience to economic slow-down

and new fashion trends. An average family is estimated to spend ~$107.28 on

children's clothing annually.

• In contrast to the changes in baby clothing market, traditional dress is still

preferred for the toddlers with only colour as the change manifested

• As per industry reports, households with an income under $10,000 spend an

average of $24.67 on boys' clothes and $49.75 on girls' clothes annually, while

households that earn $70,000 or more spend an average of $167.04 on

boys' clothes and$216.57 on girls' clothes annually.

• Advent of character-licensed clothing such as Barbie Princess and Spiderman

nightwear has enhanced value of a category that was traditionally

characterized by low-cost basic clothing.

• Moderate level of competition

Carter 12%

GAP 8%

Children's Place 4%

Private Label 4%

Gymboree 4%

Target 3%

Others 65%

77% 76% 78% 79% 79% 80% 82% 82% 82%

23% 24% 22% 21% 21% 20% 18% 18% 18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013

Rest Of World Contribution USA Contribution

1.54

2.85 3.27

3.62

2.50% 1.80%

2.80%

1.90%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

2010 2011 2012 2013

In R

s.B

n

US Infantwear Retail Sales US GDP growth rate

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

9

Domestic manufacturing accounts for a miniscule portion…

Source: Industry sources, Spark Capital

Despite being one of the biggest apparel markets globally, majority of apparels in USA are imported from several developing countries

India’s share in Infantwear exports more significant with ~5% share

Source: Office of Textiles and Apparel - US, Spark Capital

…with India being the 6th largest exporter of apparel and clothing to US

Source: Office of Textile and Apparel - US, Spark Capital

Domestic Manufacturing,

3%

Outsourced Manufacturing,

97%

(In mn $) 2012 2013

Country Imports % of Total Imports Imports % of Total Imports

China 1257 53% 1262 52%

Bangladesh 195 8% 208 9%

Cambodia 127 5% 182 7%

Vietnam 121 5% 152 6%

India 116 5% 126 5%

(In USD bn) CY07 CY08 CY09 CY10 CY11 CY12 CY13 Market

Share

China 22.75 22.92 23.5 27.97 29.39 29.06 29.78 37%

Vietnam 4.36 5.22 5.07 5.88 6.64 7.1 8.13 10%

Indonesia 3.98 4.03 3.86 4.42 5.05 4.94 4.98 6%

Bangladesh 3.1 3.44 3.41 3.93 4.51 4.47 4.95 6%

Mexico 4.52 4.01 3.39 3.54 3.8 3.7 3.68 5%

India 3.17 3.07 2.85 3.11 3.32 3.04 3.21 4%

Honduras 2.51 2.6 2.03 2.41 2.62 2.56 2.50 3%

El Salvador 1.49 1.53 1.3 1.64 1.74 1.84 1.86 2%

Pakistan 1.5 1.49 1.31 1.49 1.65 1.47 1.48 2%

Total 73.92 71.57 63.1 71.4 77.66 76.81 79.80

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

Timeline of contract manufacturing for USA based apparel players

Source: Industry, Spark Capital

10

Post end of the quota regime, developing economies as India gained far greater prominence as contract manufacturers for several US based wholesalers/retail apparels.

After effects of quota abolition regime on Indian apparel exports

Post the abolition of quota regime, it was anticipated that the world textile base

would be shifted to Asia. It was expected that China along with India would be the

major gainers of quota elimination. However, in the post ATC regime, conflicting

information began to emerge on one hand that there were signals that India was

going to have the seamless market and on the other hand some reports indicated

that India was losing its share to other cost effective destinations like China,

Bangladesh, Vietnam etc.

In the year 2004 -05 when quota was abolished, India’s textile export decreased

as compared to 2003-04. This was least expected. It was the first indication that

India was not ready to take on the opportunity. Furthermore, Indian export of

textiles & clothing was not able to compete with China especially in the US

market. China ranked at first place as its market share was 47.8% in total textile

imports by US, followed by India at second place with a market share of 11.8%,

way behind China. Likewise Indian share in US had increased in clothing segment

but the growth rate was low compared to other suppliers like China, Indonesia,

and Bangladesh etc.

It can be inferred that after the quota free environment commenced, textiles &

clothing has opened the door for global competition and if India is to compete with

global players, it has to pull up its socks and deliver or other low cost destinations

would eat into its market share.

Source: Industry reports , Spark Capital

Till 1950

North America and Western

Europe manufactured

apparel and textile

domestically

1950’s and 1960’

Shift in production to Japan which was the primary exporter of Apparel to the US and Europe 1970’s and

1980’s

Shift in production and

outsourcing from Japan to other

South East Asian countries like Hong Kong,

Taiwan, China and Korea

Late 1980’s and 1990’s Shift in production from China, Korea etc to other developing economies in South Asia and Latin America though manufacturing continued in traditional South East Asian countries.

Brief on Multi Fibre Arrangement and Quota System

The Multi Fibre Arrangement (MFA) was an international trade agreement on

textiles and clothing which prevailed from 1974 to 2004. The agreement imposed

quotas on the amount that developing countries could export in the form of yarn,

fabric and clothing to developed countries.

Under the MFA, developed countries restricted imports from developing

countries in an effort to protect their own domestic industries. Under the

agreement, each developed country was assigned a quota or quantities of a

specific item which could be exported to the U.S. and EU.

According to an IMF study, the system has cost the developing world 27 million

jobs and $40 billion a year in lost exports.

Source: Industry, Spark Capital

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

11

Given its strong economic moat built over time, Kitex Garments Limited (KGL) remains at a significant advantage

What is KITEX’s

competitive advantage?

#2 - Stable distribution

partners

#1 - Strong Economic Moat

#3 - Robust supply chain

process

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

12

With time, KGL has managed to build long lasting relationship with

clients through its consistent quality adherence and sturdy capex

expansion

Source: Company, Spark Capital

#1 - KGL has managed to build a strong economic moat which has translated into strong entry barriers for new entrants to come into the industry

Competitive advantage derived from its strong economic moat – Growth

Heuristics

KGL

Economic

Moat

Relationship

with key

customers

f

India

Economic

Moat

Acts as a strong entry barrier

given that almost all the MNCs

prefer doing business with

suppliers whom they are

comfortable. Larger and older

players tend to enjoy this moat

f

function of (f) Weight Outlook

Capacity f

With several of the retailers

mentioning capacity as a key

criteria for selection, building and

maintaining huge CAPEX acts as

a strong entry barrier

f

Conformance

Quality f

Adhering to strict performance

and conformance norms set by

MNC’s come posses a key

hindrance for new players to

venture into the market

f

Competitive

Pricing f

Given the wide range of suppliers

operating from India, maintaining

a competitive pricing that can

also be margin lucrative in the

long run deters several entrants

f

Employee

Strength f

Current strength - ~4000

permanent employees; managing

labour cost and attrition remains a

challenge for the Industry. Kitex

currently recruits from

neighbouring areas

f

Low Cost

Advantage f

India for its cheap availability of

labour and raw materials remains

one of the preferred destination

for hosiery/textile exports.

f

- Negative - Strong - Weak - Positive - Neutral

Relationship with Customers

Gross Block & Capacity

Conformance Quality

Competitive Pricing

Technology and R&D

Employee Strength

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

13

USA baby & toddler market expected to significantly outperform…

Source: Company, Spark Capital

#2 – Stable distribution partners

…so does liaison with retailers/wholesalers.

Source: Office of Textiles and Apparel - US, Spark Capital

…and with KGL’s customers accounting for ~19% of the market, growth to

remain robust

Source: Company, Spark Capital

Sourcing norms to act as a strong entry barrier…

Source: Company, Spark Capital

2006-13 CAGR 2013-2018E CAGR

Apparel 0.9% 3.5%

Childrenswear 1.3% 4.7%

Baby and Toddler Wear 1.9% 4.9%

Boys' Apparel 1.0% 2.2%

Girls' Apparel 1.0% 1.7%

Apparel Accessories 2.1% 3.7%

Kitex Clients Market Share

19%

Others 81%

Sourcing Norms - Compliance seen for sourcing:

* Worldwide Responsible Apparel Production certification

* JCPenney and Walmart certification

* WRAP certified in six (6) months?

* CTPAT (Customs Trade Partnership Against Terrorism) certification

* CPSIA and childrenswear expertise

Other factors:

* Quality standards on fabric and dyes are strict since the clothing should be infant –friendly.

* KGL co- developed the OUTLAST® technology with jockey for innerwear and T-Shirts. The product regulates skin temperature and helps the person wearing feel cooler in everyday situations.

* All safety, security, social and Environmental norms to be complied with for establishing and sustenance of relationship with customers.

* Global organic textile certification and OCOTEX certifications key to entry in various geographies.

•The time taken for an apparel exporter to tie up with a supplier to an international wholesaler/retailer can take up to 5 years. so, the wholesaler/retailer would not want to forego the relationship easily with existing supplier.

Comfort

•Given that the product being manufactured is for infants and production process involves usage of special dyes and complying with tough quality benchmarks, it might be challenging for the entity to find another supplier who is capable of meeting all quality requirements.

Quality

•Pricing is another issue since the wholesaler/retailer operates in the fragmented infantwear industry with high competition. Given the minimal operational expertise and economies of scale, pricing offered by a new supplier often does not match that of an existing supplier

Pricing

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

14

Company Description Headquarters Area of Operation Financials

About the company: Gerber Childrenswear LLC is a leading

marketer of infant and toddler apparel globally.

Brands: Onesies

Distribution Network: majorly a wholesaler supplying to ~15,000

retail outlets.

USA Major source of revenue from

US but also present globally

NA

About the company: Globally a leading toy and baby products

retailer.

Brands: Toys R US, Kids R US , Babies R US,

Distribution Network: 872 Toys R US stores in US and Puerto

Rico; 715 international stores and over 180 licensed stores in 35

countries.

USA

Present all over the world with

US however accounting for

majority of revenues

CY13 revenues: $12.54 billion

(Kitex’s share: $13 million - $30

million)

About the company: Largest branded marketer of baby and

children’s clothing in the U.S dating back to 1865.

Brands: Carter’s and OshKosh B’gosh

Distribution Network: The Company’s brands are sold in over 18,000 doors in the United States..

USA

Present all over the world with

US however accounting for

majority of revenues

CY13 revenues: $2.6 billion

(Kitex’s share: $13 million - $30

million)

About the company: One of the leading retailers of babywear,

apparel for ‘mothers to be’ , toys and furniture & equipment for

babies.

Brands: Mothercare and Early learning centre

Distribution Network: The company globally (including UK where it

is headquartered) operates 1441 stores with a total retail space of

~44 million square in over 60 countries.

UK

Global presence with

International sales (other than

home country UK) accounting

for 61% of consolidated sales.

FY14 revenues :1192 million

pounds

(Kitex’s share: $13 million - $30

million)

About the company: Second largest US departmental store

company and was the 20th largest retailer in US in terms of

revenue.

Brands: Retailer of multiple brands

Distribution Network: Operates 1,160 family oriented departmental

stores in 49 states across the US.

USA Only USA

CY13 revenues: $19 billion

(Kitex’s share: $13 million - $30

million)

About the company: Largest pure play children’s speciality apparel

retailer in North America.

Brands: Retailer

Distribution Network: Company operates 1,113 stores in the

United States, Canada and Puerto Rico, an online store, and had 54

International stores operated by its franchise partners.

USA

Franchisee stores present

across the world with US

however accounting for

majority of revenues

CY13 revenues: $1.77 billion

(Kitex’s share: $13 million - $30

million)

Source: Company Filings, Spark Capital

#2 – Stable distribution partners – KGL caters to a few of Industry leaders, signifying their quality and relationship with key clients

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

Yarn Fabric Dying/Bleaching Knitting Cutting &

Sewing

Low wastage and

energy efficient

machinery used

15

Company uses high

quality, superior

grade yarn based on

Okeo Tex Class I.

Jersey, Ribbed and

interlock are kinds of

yarn used.

Organic dyes used;

Clariant and

Huntsman – Key

suppliers. OCOTEX

certification is the

key criteria for

selection. State of art machinery

for robust quality

control of fabric Controlled by

Advanced robotic

machines

Superior open

width bleaching

process used

High speed, low

power consuming

machinery used

Advanced Italian

machinery used

Kitex Facility – A Video

https://www.youtube.com/watch?v=biv1-lfWso4

Source: Youtube, Spark Capital

Case study on Kitex Employee Model – video

https://www.youtube.com/watch?v=GEFzq8CIhm0

Source: Youtube, Spark Capital

#3 - Manufacturing – Strong Value Chain with KGL processing most of its products in its own facility

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

16

Revenues in FY14 have really taken off…

Source: Company, Spark Capital

Favorable Dollar growth coupled with increasing contribution from garments leading to strong revenue platform

…while among offerings, regular use body suits form a chunk of revenues

Source: Company, Spark Capital

…led by ~20% non-dollar growth

Source: Company, Spark Capital

Fabric sales less than ~20% of the overall revenue…

Source: Company, Spark Capital

-4% 5%

13% 11%

-24%

21% 1%

20%

-28%

26%

15%

31%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

FY 11 FY 12 FY 13 FY 14

Dollar growth Non-dollar growth

96%

71% 73% 83% 81%

4%

29% 27% 17% 19%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY10 FY 11 FY 12 FY 13 FY 14

Garment Fabric

Body Suits, 40%

Sleep Suits, 20%

Playwear, 20%

Others, 20%

2.47 2.42 2.96 2.97

4.03

0

1

2

3

4

5

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.b

n

Net Sales

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

17

Gross margins way-ward due to timing of contracts

Source: Company, Spark Capital

Gross margins have been volatile given that they are largely dependent on price contracts; price of key raw material component Cotton has been largely stable

…so have been processing charges

Source: Company, Spark Capital

14% Imported raw material naturally hedged against dollar revenues

Source: Company, Spark Capital

Power & Fuel costs as a percentage of sales has been coming down with

increasing economies of scale

Source: Company, Spark Capital

13% 20%

13% 15% 14%

87% 80%

87% 85% 86%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY 10 FY 11 FY 12 FY 13 FY 14

Imported Raw material Indigeneous Raw material

82

108

141 138

164

3.3%

4.2%

4.5% 4.4%

3.7%

0%

1%

1%

2%

2%

3%

3%

4%

4%

5%

5%

0

20

40

60

80

100

120

140

160

180

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.m

n

Power and Fuel Power & Fuel as a % of Sales

236

142 114 124

121

9.5%

5.5%

3.7% 3.9%

2.7%

0%

2%

4%

6%

8%

10%

12%

0

50

100

150

200

250

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.m

n

Processing Charges Processing charges as a % of Sales

1.13 1.25

1.40 1.52

2.06

45.5%

48.9%

44.8%

47.9%

46.6%

42%

43%

44%

45%

46%

47%

48%

49%

50%

0.0

0.5

1.0

1.5

2.0

2.5

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.b

n

Gross Profit Gross Margin

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

18

Operating margins expected to remain robust…..

Source: Company, Spark Capital

Operating margins to improve with increased scale and cost containment initiatives

…with operating expenses being contained

Source: Company, Spark Capital

…led by rationalization of employee cost

Source: Company, Spark Capital

Revenue per employee too on the higher trend…

Source: Company, Spark Capital

438 368 378

438

570

17.7%

14.4% 12.1%

13.8% 12.9%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

100

200

300

400

500

600

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.m

n

Employee Cost Employee cost as a % of sales

3,163

2,609 2,453

3,100

3,700

0.78

0.93

1.21

0.96 1.09

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

0

500

1000

1500

2000

2500

3000

3500

4000

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.M

n

No.of Employees Revenue/Employee

134

181 182 218

257

5.4%

7.1% 5.8%

6.9%

5.8%

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

50

100

150

200

250

300

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.m

n

Other Expenses Other Expenses as a % of Sales

236

454

582 601

951

9.5%

17.7% 18.7% 19.0%

21.5%

0%

5%

10%

15%

20%

25%

0

100

200

300

400

500

600

700

800

900

1000

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.m

n

EBITDA EBITDA Margin

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

19

PAT margins have risen to their all time high in FY14

Source: Company, Spark Capital

With reduction interest cost, PAT growing at a quicker pace than operating income despite rise in effective tax rate

Higher taxes despite EOU status

Source: Company, Spark Capital

Depreciation increase inline with increase in gross block…

Source: Company, Spark Capital

…while interest costs decreased with reduction in debt

Source: Company, Spark Capital

152

125

176

115 106

6.2%

4.9%

5.6%

3.6%

2.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0

20

40

60

80

100

120

140

160

180

200

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.M

n

Interest Expense % of sales

185 206 271 294

574 7.5%

8.1% 8.7%

9.3%

13.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

100

200

300

400

500

600

700

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.m

n

PAT PAT Margin

66 69 69

86 97

2.6% 2.7%

2.2%

2.7%

2.2%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0

20

40

60

80

100

120

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.M

n

Depreciation % of sales

93 106 130

147

308

33.4% 34.0% 32.4% 33.3%

35.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

0

50

100

150

200

250

300

350

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.M

n

Tax Effective tax rate

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

20

5X revenue growth in ten years without any equity dilution….

Source: Company, Spark Capital

Internal accruals have largely been used over the past few years for CAPEX and repayment of loans

…leading to consistent high return ratios

Source: Company, Spark Capital

…so have been debt repayment controlled leverage inspite of growth

Source: Company, Spark Capital

Sales rising in tandem with gross block addition…

Source: Company, Spark Capital

47.5

47.5 47.5 47.5 47.5 47.5 47.5 47.5 47.5 47.5

47

86 173 251 336 505 689 927 1,176 1,694

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Equity Share Capital Reserves and Surplus

697

880 884 918

1,194

1.26 1.19

0.91

0.75 0.69

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

0

200

400

600

800

1000

1200

1400

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.m

n

Total Debt Debt-Equity ratio

1.44 1.51 1.59 1.61

2.34

2.47 2.42

2.96 2.97

4.03

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.b

n

Gross Block Net Sales

40%

32% 32%

27%

39%

17% 18% 20%

17%

23%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

FY 10 FY 11 FY 12 FY 13 FY 14

ROE ROCE

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

21

Working capital days remain sporadic…

Source: Company, Spark Capital

With improvements in working capital days, cash flows too seem to be on the uptrend

…leading to FCF also improving significantly off-late

Source: Company, Spark Capital

…though in FY14, working capital days significantly reduced

Source: Company, Spark Capital

Significant improvement in OCF on account of healthy margins and better

working capital management…

Source: Company, Spark Capital

33

81

61

53

9 8

56

37

58

44

35

46

31 26 20

0

10

20

30

40

50

60

70

80

90

FY 10 FY 11 FY 12 FY 13 FY 14

Inventory Days Debtor Days Creditor Days

6

91

67

85

33

0

10

20

30

40

50

60

70

80

90

100

FY 10 FY 11 FY 12 FY 13 FY 14

Days

Working Capital Days

873

-156

626

244

1158

0.35

-0.06

0.21

0.08

0.29

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

-400

-200

0

200

400

600

800

1000

1200

1400

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.M

n

OCF OCF/Net Sales

850

-263

558

196

437

0.34

-0.11

0.19

0.07

0.11

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

-400

-200

0

200

400

600

800

1000

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.M

n

FCF FCF/Net Sales

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

22

Promoter holding consistent over a period of time…

Source: Company, Spark Capital

Corporate governance issues have been regularly addressed by the management

…board composition in adherence to the stipulated norms

Source: Company, Spark Capital

…with proportion of sales to group company reducing

Source: Company, Spark Capital

Healthy dividend pay-out history coupled with…

Source: Company, Spark Capital

54.2% 54.2% 54.2% 54.2% 54.2% 54.2% 54.2% 54.2%

0.4%

0.01%

45.8% 45.8% 45.8% 45.8% 45.8% 45.8% 45.8% 45.4%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

Promoter group FII DII Others

68% 79%

86% 84%

32% 21%

14% 16%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014

Contract Manufacturing Group company sales

11 16

22

33

44

4.7%

7.9% 8.1%

11.3%

7.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

5

10

15

20

25

30

35

40

45

50

FY 10 FY 11 FY 12 FY 13 FY 14

In R

s.M

n

Dividend Dividend payout

Directors #nos

Promoter Directors 1

Independent Directors 3

Non-Executive 1

Total 5

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

23

Dividends declared growing inline with increase in MD’s remuneration

Source: Company, Spark Capital

Management polices have until now been friendly to minority share holders too

CSR – A snapshot of activities undertaken in 2014

Source: Company filings, Spark Capital

Historically results have been pronounced on time allaying non-minority

friendly concerns indicating healthy business practices and internal

controls

Source: Company, Spark Capital

KGL Vs KCL Financial Snapshot

Source: Company, Spark Capital

Rs.mn 2011 2012 2013 2014 CAGR

MD's Remuneration 16.4 21.1 23.2 44.6 40%

Dividends 16.2 22.1 33.1 44.5 40%

MD’s payout

as a % of dividends 101% 96% 70% 100% -

EBITDA 454 582 601 951 28%

% of EBITDA 3.6% 3.6% 3.9% 4.9% -

1Q 2Q 3Q 4Q

FY14 17-Jul-13 22-0ct-13 09-Jan-14 03-Apr-14

FY13 18-Jul-12 15-0ct-12 09-Jan-13 04-Apr-13

FY12 30-Jul-11 28-0ct-11 27-Jan-12 21-Apr-12

FY11 31-Jul-10 16-Nov-10 07-Feb-11 25-Apr-11

Sector Impact

Healthcare 3800 families benefited from medical camps

463 surgeries conducted

Drinking Water 6 bore wells dug; 1.02 liters of water storage

Housing 40 houses renovated

Agriculture 300 acres of participative farming and multi crop harvesting

Education 2278 of school bags given to financially backward students

Food Security 65 tones of food material given to 500 families

2012 2013

Rs.mn KGL KCL KGL KCL

Revenues 3120 2067 3170 1435

EBITDA 582 410 601 338

PAT 271 167 294 126

EBITDA (%) 19% 20% 19% 24%

PAT (%) 9% 8% 9% 9%

Net worth 974 489 1224 615

Debt 884 909 918 699

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

24

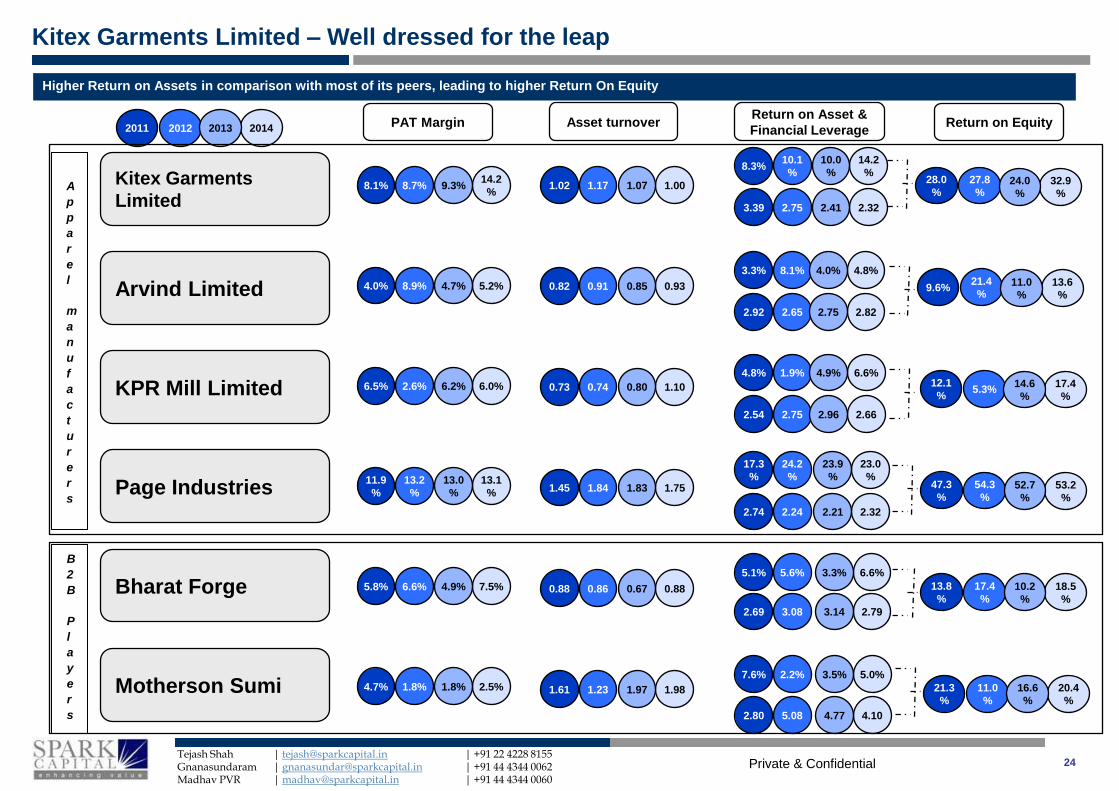

Higher Return on Assets in comparison with most of its peers, leading to higher Return On Equity

2011 2014 2012 2013

8.1% 14.2

% 8.7% 9.3% 1.02 1.00 1.17 1.07

8.3% 14.2

%

10.1

%

10.0

%

3.39 2.32 2.75 2.41

PAT Margin Asset turnover Return on Asset &

Financial Leverage Return on Equity

28.0

% 32.9

%

27.8

% 24.0

%

4.0% 5.2% 8.9% 4.7% 0.82 0.93 0.91 0.85 9.6% 13.6

%

21.4

% 11.0

%

6.5% 6.0% 2.6% 6.2% 0.73 1.10 0.74 0.80 12.1

% 17.4

% 5.3%

14.6

%

11.9

%

13.1

%

13.2

%

13.0

% 1.45 1.75 1.84 1.83 47.3

% 53.2

%

54.3

% 52.7

%

5.8% 7.5% 6.6% 4.9% 0.88 0.88 0.86 0.67 13.8

%

18.5

%

17.4

%

10.2

%

4.7% 2.5% 1.8% 1.8% 1.61 1.98 1.23 1.97 21.3

%

20.4

%

11.0

%

16.6

%

3.3% 4.8% 8.1% 4.0%

2.92 2.82 2.65 2.75

4.8% 6.6% 1.9% 4.9%

2.54 2.66 2.75 2.96

17.3

%

23.0

%

24.2

%

23.9

%

2.74 2.32 2.24 2.21

5.1% 6.6% 5.6% 3.3%

2.69 2.79 3.08 3.14

7.6% 5.0% 2.2% 3.5%

2.80 4.10 5.08 4.77

Kitex Garments

Limited

Arvind Limited

KPR Mill Limited

Page Industries

Bharat Forge

Motherson Sumi

A

p

p

a

r

e

l

m

a

n

u

f

a

c

t

u

r

e

r

s

B

2

B

P

l

a

y

e

r

s

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

25

Major risks relate to adherence to quality in delivery as even slight error could jeopardies the business model

Source: Company, Spark Capital

Key Business Risks

Absence of Long term

contracts with key customers

Raw material (primarily

Cotton) cost impact

Additional imposition of

stringent quality measures

Environmental and pollution

issues

Capex plans and funding

norms

Loss of business to

other low cost manufacturing destinations

Impact of INR-Dollar volatility on Revenues and earnings

Significant customer

concentration risk

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

26

Niche business model coupled with concerns over group holdings remain our key concern

Source: Company, Spark Capital

Prime Concerns

Plan of launching own brand in USA:

In addition to the fact that the business model would totally be different affecting the working capital management and diverting management’s focus, launching of own brand in the same infantwear space could complicate and terminate relationships with existing customers.

Track ability of drivers:

Since KGL derives majority of its revenues from outside India , trackability of growth drivers and future potential becomes very difficult in an ever evolving global scenario

KGL & KCL:

KGL and KCL operating in the same industry lead to doubts on corporate governance and management’s order of preference for business etc. However, we believe if MD’s medium term plan of merging both the entities would happen, it would significantly benefit minority holders and provide comfort on governance. However, concerns on valuation and proportion of share allotment prevail.

Tractability of competition:

Though we know that there are 11 players globally who are direct competitors to KGL, emergence of new competition and constant monitoring of competitors becomes difficult

Private & Confidential

Kitex – Well dressed for the leap

Abridged Financial Statements

Rs. mn FY11 FY12 FY13 FY14 FY11 FY12 FY13 FY14

Profit & Loss Growth Ratios (%)

Revenue 2,561 3,120 3,170 4,422 Revenues 4% 22% 2% 40%

EBIDTA 454 582 601 951 EBIDTA 101% 28% 3% 58%

Other Income 52 63 40 133 Normalised PAT -14% 31% 8% 95%

Depreciation 69 69 86 97 Margins (%)

EBIT 437 577 555 988 Gross 48.9% 44.8% 47.9% 46.6%

Interest 125 176 115 106 EBIDTA 17.7% 18.7% 19.0% 21.5%

PBT 312 401 440 882 Normalised PAT 8.1% 8.7% 9.3% 13.0%

Normalised PAT 206 271 294 574 Leverage Ratios (x)

Balance Sheet Debt to Equity 1.2 0.9 0.8 0.7

Net Worth 736 974 1,224 1,742 Current Ratio 1.7 2.2 2.7 2.5

Loan Funds 880 884 918 1,194 Return Ratios (%)

Deffered Tax Liabilities 157 163 161 216 RoCE 18.2% 20.4% 17.0% 23.4%

Sources of Funds 1,786 2,037 2,328 3,175 RoE 32.0% 31.7% 26.7% 38.7%

Net Block 1,212 1,220 1,168 1,809 Total Asset Turnover (x) 1.5 1.6 1.4 1.5

Capital WIP 9 4 23 7 Per Share

Goodwill - - - - EPS (Rs.) 4.3 5.7 6.2 12.1

Investments 38 38 106 45 Dividend (Rs.) 0.3 0.5 0.7 1.5

Total Current Assets 1,229 1,405 1,648 2,173 Valuation Metrics

Total Current Liabilities 714 637 621 862 Current Market Price 338

Net Current Assets 515 768 1,027 1,311 Shares Outstanding (mn) 48 48 48 48

Application of Funds 1,786 2,037 2,328 3,175 Market Cap. (Rs. mn) 16,055

Cash Flow Enterprise Value (Rs. mn) 16,835 16,546 16,459 16,172

Cash Flow from Operation (156) 626 244 1,158 EV /Sales (x) 6.6 5.3 5.2 3.7

Cash Flow from Investments (107) (68) (48) (720) Price/Earnings (x) 77.8 59.2 54.7 28.0

Free Cash Flow (263) 558 196 437 Price/Book (x) 21.8 16.5 13.1 9.2

Cash Flow from Financing 244 (267) (153) 183 EV/EBIDTA (x) 37.1 28.4 27.4 17.0

Closing Cash Balance 62 355 408 1,032 FCF Yield -1.6% 3.5% 1.2% 2.7%

27

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

Spark Disclaimer

Spark Capital Advisors (India) Private Limited (Spark Capital) and its affiliates are engaged in investment banking, investment advisory and institutional equities. Spark Capital is registered with SEBI as a Stock Broker and Category 1 Merchant Banker.

This document does not constitute or form part of any offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Nothing in this document should be construed as investment or financial advice, and nothing in this document should be construed as an advice to buy or sell or solicitation to buy or sell the securities of companies referred to in this document.

Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Spark Capital and/or its affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to a certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such applicable restrictions. This material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

Spark Capital makes no representation or warranty, express or implied, as to the accuracy, completeness or fairness of the information and opinions contained in this document. Spark Capital , its affiliates, and the employees of Spark Capital and its affiliates may, from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report.

This report has been prepared on the basis of information, which is already available in publicly accessible media or developed through an independent analysis by Spark Capital. While we would endeavour to update the information herein on a reasonable basis, Spark Capital and its affiliates are under no obligation to update the information. Also, there may be regulatory, compliance or other reasons that prevent Spark Capital and its affiliates from doing so. Neither Spark Capital nor its affiliates or their respective directors, employees, agents or representatives shall be responsible or liable in any manner, directly or indirectly, for views or opinions expressed in this report or the contents or any errors or discrepancies herein or for any decisions or actions taken in reliance on the report or the inability to use or access our service in this report or for any loss or damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits that may arise from or in connection with the use of or reliance on this report.

Spark Capital and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency, Spark Capital has incorporated a disclosure of interest statement in this document. This should however not be treated as endorsement of views expressed in this report:

Absolute Rating Interpretation

Buy Stock expected to provide positive returns of >15% over a 1-year horizon

Add Stock expected to provide positive returns of >5% – <15% over a 1-year

horizon

Reduce Stock expected to provide returns of <5% – -10% over a 1-year horizon

Sell Stock expected to fall >10% over a 1-year horizon

Recommendation History

Date CMP Target price Rating

28

Private & Confidential

Kitex Garments Limited – Well dressed for the leap

Tejash Shah | [email protected] | +91 22 4228 8155 Gnanasundaram | [email protected] | +91 44 4344 0062 Madhav PVR | [email protected] | +91 44 4344 0060

Analyst Certification of Independence

The views expressed in this research report accurately reflect the analyst’s personal views about any and all of the subject securities or issuers; and no part of the research analyst’s compensations was, is or will be, directly or indirectly, related to the specific recommendation or views expressed in the report.

Additional Disclaimer for US Institutional Investors

This research report prepared by Spark Capital Advisors (India) Private Limited is distributed in the United States to US Institutional Investors (as defined in Rule 15a-6 under the Securities Exchange Act of 1934, as amended) only by Decker & Co, LLC, a broker-dealer registered in the US (registered under Section 15 of Securities Exchange Act of 1934, as amended). Decker & Co accepts responsibility on the research reports and US Institutional Investors wishing to effect transaction in the securities discussed in the research material may do so through Decker & Co. All responsibility for the distribution of this report by Decker & Co, LLC in the US shall be borne by Decker & Co, LLC. All resulting transactions by a US person or entity should be effected through a registered broker-dealer in the US. This report is not directed at you if Spark Capital Advisors (India) Private Limited or Decker & Co, LLC is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available to you. You should satisfy yourself before reading it that Decker & Co, LLC and Spark Capital Advisors (India) Private Limited are permitted to provide research material concerning investment to you under relevant legislation and regulations;

Disclosure of interest statement Yes/No

Analyst ownership of the stock No

Group/directors ownership of the stock No

Broking relationship with the company covered No

Investment banking relationship with the company covered No

29