Embed Size (px)

Citation preview

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

Karvy Comtrade Ltd.

Energy Quarterly Outlook Q4 2010

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

TECHNICAL RECOMMENDATIONS

CRUDE OIL

STAY SHORT WITH STOP LOSS ABOVE $US87

NATURAL GAS

Short term: Natural gas NYMEX: Sell below $3.50 TP $3.13-3.00 SL $3.90

Long term: Natural gas NYMEX: Buy at $2.80-3.00 TP $4.12 then $5 SL $1.90

Short term: Natural gas MCX: Sell at `168-170 TP `140 SL `186

Long term: Natural gas MCX: Buy at `130-135 TP `195 then `210 SL `117

SUMMARY:

Third quarter of CY 2010 was the official hurricane season, which was

expected to fuel the energy prices this year. But, it failed to impact the oil market to a larger

extent as effect of tropical storms was very little. Weakness in economic growth also kept

the oil market under pressure. Energy producing companies drilled more oil on speculation

that summer driving season would create more demand for energy products. However,

demand could not match with the supply due to slower growth of major world economies

thereby resulting to bearish trend for the crude oil prices. During the quarter, natural gas

futures prices fell drastically whereas crude oil prices showed a mixed trend. In Q4 CY10,

crude oil futures may show a positive trend but a rally could be limited by rising inventory

level and on economic concern whereas natural gas prices are likely to show a recovery on

winter demand.

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

CRUDE OIL

Crude oil futures prices movement formed a reverse V-shape in first two months of last

quarter and fell by 1% from penultimate quarter’s close on MCX. However, NYMEX

crude oil futures displayed a different direction wherein prices improved a tad on

depreciating dollar index. In September, dollar index depreciated by -6%, whereas

Indian rupee appreciated by 4.5%, making MCX oil futures to recover in a lower pace

than NYMEX oil price. Active hurricane season in North Atlantic and US summer driving

season failed to create more demand for the oil. In our last quarterly report, we had

presented a bearish outlook and market moved as per our expectation at the beginning

of the quarter. However, later it recovered tracking firm equity market. Prices climbed

to three month high in August, but it lasted for one week only. Build up in inventory and

dissipating hurricanes threat led the oil prices to fall from the monthly high in August.

Higher volatility was seen in September for oil price movement with upward bias.

Table 1: Crude oil price change (*Data collected till Sep 29, 2010)

Commodity July Aug Sep QTD YTD

NYMEX Crude Oil 0.04 -0.09 0.08 0.03 -0.02

MCX Crude Oil 0.04 -0.06 0.02 -0.004 -0.06

Source: Bloomberg & KCTL Research

Table 2: USD INR movement

Currencies JUL AUG SEP

INR 0% 1% -5%

DOLLAR -5% 2% -6%

Figure 1: Crude oil price movement

Source: Bloomberg & KCTL Research

The US benchmark WTI Light Sweet Crude Oil futures prices climbed more than 4% in

July. NYMEX oil price made a monthly high of $78.95/bbl while on MCX it climbed to

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

`3654. Future contract prices traded higher the most in beginning of August. Oil prices

climbed $83/bbl in NYMEX by rising more than 12% from opening of third quarter.

Similarly oil prices increased to `3796 with a rise of more than 11%. However, the

trend could not continue and prices fell to two months low in August end declining by

more than 13%. High volatility in oil prices is witnessed in the month of September. Oil

future contracts made a high of `3618 and a low of `3336 in September.

Figure 2: Crude Oil price & Hurricane Season

Source: National Hurricane Centre ,Bloomberg

Hurricane season in North Atlantic region runs between June and November.

About 30% of US crude oil production comes from Gulf of Mexico. Hence, occurrence of

storms and hurricane in this region will disturb the supply and production of oil. The

National Oceanic and Atmospheric Administration (NOAA) had projected 14-23 named

storm for the current season. In last four months, more than 13 storms (6 hurricanes

and 7 storms) have appeared. Figure 2 shows impact of hurricane and storm on the

crude oil price movement. Crude oil prices showed a marginal rise in July as Hurricane

Alex, Storm Bonnie and Colin hit the Gulf of Mexico and had a very little effect on

production. As a result of hurricane, oil prices surged by more than 12% on NYMEX and

by more than 7% on MCX. As the effect of hurricane started easing, prices tumbled in

the beginning of August. Crude oil prices rose once again in September following

production threat by Hurricane Igor and Julia. Crude oil production between June and

August average at 47,000 barrels per day in US, which was about half of EIA’s forecast of

96,000 barrels per day. There are still ten named storms to appear in north Atlantic,

which may disrupt oil supply and production. Hence, oil prices may take positive

cues.

Calendar Spread: The spread difference increased more than 51 percent in the

last quarter. In the month of July, prices of near month contract increased more than far

month contract which made spread to fall. Thereafter prices spread difference started

rising the most as prices of near month contract fell the most in comparison to far

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

month contract. However, spread fall from quarterly high as prices of near month

contract increased more than far month contract. As we are expecting prices to rise

slowly, this may push the spread in a higher side. However, a pull back can be seen in

later period.

Figure3: Spread chart

Source: Bloomberg & KCTL

Major Economy

Crude oil prices are often seen as being connected with inflation as a cause and effect.

Crude oil is considered as major input for the economy as most of the countries are

dependent on import of energy. It not only used for fueling engines but also being used

in manufacturing sector. Hence, an increase in crude oil price will ultimately lead to rise

in input, which translates into higher price for end products (means higher inflation).

Being the world largest economy, US are also largest producer and consumer of crude

oil. Let us have a brief review of US economic performance in last quarter. The US

Federal Reserve has indicated that employment rate in US is growing at much lower

pace than expected. Industrial production increased but at a slower pace in last quarter.

Consumer confidence increased slower-than-market expectation and the same trend is

likely to continue in this quarter. Unemployment rate continued to remain cause of

concern as it still above 9%. The US manufacturing activity has picked up in the last

quarter and remains above 50. However, Institute for Supply Management (ISM)

manufacturing index declined significantly during the quarter and Consumer price

index grew by only 0.1%.

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

China, the second largest oil consumer overtook Japan as the second largest economy

last quarter. Chinese GDP is at 7.4% of the world economy. Manufacturing in China

recovered in the month of August and Foreign Direct Investment in China climbed to

29.2% in July. Indian economy continued to exhibit strong growth in third quarter, as

both manufacturing and service expanded. The second quarter growth rate of Japan

(third largest oil consumer) is recorded only 0.40%. Japanese exports are likely to

advance and economic growth may remain in weak despite sizeable stimulus efforts.

The Euro-zone second quarter GDP growth stood at 1%. Only 7 of the banks failed in the

stress test, which is indicating potential for European economy to grow. However, retail

sales of Euro-zone declined and unemployment rate remains at 10% for the fifth

consecutive month.

Thus a slow growth of major economies is witnessed in the last quarter. However;

economic growth rate of the US is forecast to increase by 2.6% and 2.3% for 2010 and

2011 respectively. This data are revised from 2.8% and 2.5%. However, Euro-zone

growth for 2010 is expected to increase 1.2% from 0.8% forecasted previously. China

growth rate will remain unchanged from 9.5%.

Dollar Index and Oil price Movement

The Dollar Index, which measures the dollar aginst six currencies has a negative

corelation with international crude oil price movement. The oil in international market

is priced in US dollars, hence, crude oil price movement carry a negative correlation

with the dollar. Historically, it is proven that whenever dollar index increases the crude

oil prices fall and vice versa. In July, dollar index slipped by 4% while crude oil prices

rose by more than 9% on weekly basis. In August, dollar index climbed to 83.29 lvels,

which led the oil prices to slip by 7%. However, the inverse relation could not worked

out in September as dollar index movement was very thin. As per the economic

expectations, dollar index may recover in a lower pace, which will pressure oil price

movement.

Figure 4: Crude oil price & Dollar Index Movement

Source: Bloomberg & KCTL

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

CFTC report: As per the report released by Commodity Futures Trading

Commission (CFTC) total short positions of crude oil futures contracts increased by 1%,

which was more than total long positions since July. Speculators have increased short

positions last quarter by 20%, whereas commercial short positions climbed by 10%.

Long positions also increased by both speculator and hedger, but, at much lower pace.

Thus, rise in short positions more than long positions indicates a bearish trend for

crude oil prices.

FUNDAMENTAL FACTORS: Oil prices in the last quarter were driven basically

by the fundamental factors like inventory and supply-demand. The continuing

hurricane season and summer driving season could not be effective on the back of

sluggish economic growth.

Figure 5: Crude oil Inventory & Price Movement

Source: US Energy Department Bloomberg & KCTL

According to US Energy Department, average crude oil inventory fell more than 7000

million barrels in July due to increase in refinery utilization. Refining companies

processed more crude oil during the month on speculation that demand for refined

products would increase ahead of summer driving season. Contrary to this, gasoline and

distillate inventories rose more than 3000 and 8000 million barrels, respectively.

Decline in inventory, speculative demand and supportive economic situation supported

the oil prices to trade higher by more than 4% in July. Surprisingly, distillate inventories

rose more than one-year’s average in August due to decline in import by the second

largest importing nation. This has resulted into a sharp decline in oil prices by 13% by

third week of August. But, in last week, oil prices recovered on anticipation of supply

disruption by Hurricane Karl and Danielle. With the end of summer demand, refinery

utilization declined as refineries went for maintenance. However, gasoline and distillate

inventories decline despite lower refinery utilization. In September, total crude oil

inventory declined for two consecutive weeks, but, stood higher than August average.

As per the crude oil inventory seasonality chart, we may expect further rise in

inventory in the next quarter. Thus rising inventory may be a negative price driver.

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

However, before the year end inventory is expected to decline in a lower pace which

may lead to recovery in oil prices.

Figure:6 Total Crude oil inventory Seasonality

Source: US Energy Department & Bloomberg

Crude Oil Supply & Demand

The discouraging economic growth of developed countries made weaker oil demand in

comparison to last quarter. It is not only the US, which is playing major role in the world

oil consumption; but declining oil demand in China also acting as a backup in lower

world consumption. Oil consumption has declined in the Europe by more than 1% last

month. Demand for crude oil has declined in China to 8.79 million barrels per day in

August though it has climbed to more than 9 million in July. Similarly consumption from

Asian countries also declined to 9.38 million barrels per day.

Figure 7: Total World Oil Production & Consumption with price

movement

Source: US Energy Department & Bloomberg

Summer driving season in the US could not boost oil consumption as expected though

gasoline consumption increased slightly. In the month of July, oil consumption declined

to 19.10 million barrels per day from 19.22 million barrels per day recorded in June. Jet

fuel consumption declined more than 5% in August, whereas distillates consumption

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

declined to more than 7% in July. Slowing economic activities have been affecting oil

consumption. US car and light vehicle sales reached a 28-year low in August. The world

consumption is forecast to remain at 86.37 mb/d, which is revised lower. European

oil demand forecast to contract by 0.35 mb/d. The world supply is forecasted to

remain at 85.9 mb/d. However, the US crude oil supply is expected to increase more

than 3%, though demand is expected to decline. Oil supply from OPEC is forecast to

rise from last quarter to 35 million barrels per day. Thus rising supply with lower

demand may pull down oil prices.

Figure 8:World Supply & Demand Forecast

Source: US Energy Department & Bloomberg

WTI and Brent- relation

As we know, WTI (West Texas Intermediate) light sweet crude oil is used as a

benchmark in oil pricing in the US. Brent crude, the benchmarks for ICE

(InterContinental Exchange), Europe which gets sourced from North Sea. This bench

mark crude oil is priced at about $4 per barrel premium to the OPEC basket

price or about a $1 or $2 per barrel discount to WTI. The daily basis pricing

relationship can vary. The most unusual and interesting thing happened in the last

quarter was spread between WTI and Brent declined the most. The difference started

declining from mid of August, which fell near $5. WTI has historically been more of a US

crude oil basket. It is not only used for US traded oil futures, but also for US production.

Therefore, WTI more closely reflects US supply/demand fundamentals, while Brent

tends to be more influenced by global events and international supply/demand

fundamentals.

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

Figure 9: WTI & Brent Spread

Source: Bloomberg &KCTL

North Sea quarterly production is expected to decline from the last quarter. In the third

quarter it was at 3.89 million barrels per day and is expected to 3.72 millions. Thus a

positive indication can be seen in Brent prices in a short- term.

Gold/Crude Ratio

Interrelationship between Gold and Oil found historically; Oil is the most important

commodity on earth because of economies’ dependence on this tangible commodity

while gold has been the ultimate form of money through centuries. It has been found

that these two moved in tandem with basically crude oil prices driving bullion prices.

Crude oil mainly adds to inflation numbers which further instigates the demand for gold

as an inflation-hedge. Therefore, if crude oil prices rise, gold also tends to march higher.

However, history shows that relationship imploded when the co-relation between gold

and crude oil dived into negative territory in 1992, 1993, 1996 and 1999-2001.Thus

occasional break-up between these commodities which have been mostly found trading

in tandem with each other. Current year 2010 is witnessing another year of those few

years when the relationship broken. The second quarter of the year 2010 saw European

debt crisis deepening which sent crude oil prices lower but lifted the bullion prices as a

safe haven instrument during the same time and it is continuing. Gold –crude ratio is

expected to rise in the next quarter, as demand for gold is expected to rise, where as

prices of crude futures will be under pressure.

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

Figure 10: Gold and Crude Oil Ratio

Source: Bloomberg & KCTL

CRUDE OIL TECHNICAL SNAPSHOT

Case1: View: Downside

Strategy: STAY SHORT TILL $87 MARK. We firmly believe if market fails to breach

$87 then a good correction can be expected. However, the fall also is likely to be limited.

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

If market clears $87.00 on higher side our wave analysis needs to give rethink. Since, we

were bearish from mid 2009 and our views have been correct we expect $87.00 mark

should be an important factor to watch out. On the down side the support can be seen at

$70.

Recent wave: Minor wave 2 of intermediate wave (2) of primary wave C, which is

corrective in nature.

Description: As expected in last quarter market declined after making a top of $82.97 in

august end considered as intermediate wave 2 of primary wave C. The key level to watch is

at $87 levels and market can extend its correction till the same. Incase market fails to

breach the resistance at $87 would possible to see a correction. Supports are at $78

followed by $70 levels. However, a significant break above $87 would confirm the fresh

trend.

(OR)

Case 2: Why we are considering Case 2?

As per the case 1 discussion market should not breach the resistance at $83-87. At present

market is trading at $83.66 levels suggesting upside bias. However, market is in

consolidation phase with unfolded counts. On the topside the key level to watch is at $87

levels. A significant break above $87 is likely to extend its gains and we need to consider

the case 2.

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

Natural Gas

Gas prices have fallen aberrantly more than fifteen percent on quarterly basis.

Hurricane season increased the speculation of lower supply which made producers to

increase storage. However, dissipating storms and steadily growing economy lead a

decline in demand, thus inventory climbed and ultimately prices declined. Fundamental

factors drive gas prices more than economical factors. Let’s see how gas prices tumbled

on the back of various fundamentals.

Table 3: Natural Gas Price Movement

Commodity July Aug Sep QTD YTD

NYMEX Natural Gas 7% -22% 4% -14% -29%

MCX Natural Gas 6% -20% -2% -16% -29%

Source: Bloomberg, KCTL Research

Natural gas future traded in a bullish trend at the beginning of third quarter. Gas prices

climbed more than 6% on the back of tropical storm threat. Gas prices made a high of

Rs.232/mmbtu (MCX) and $4.9/mmbtu (NYMEX) in July. Tropical storm threat from

Bonnie and Colin after hurricane Alex in the month of July supported gas prices.

Thereafter, gas prices started declining as supply increased as no disruption happened

due to dissipating storms. Prices fell more than 20% in August in Indian market. In the

month of September, prices recovered on account of rising storm threat in Gulf of

Mexico. Tropical storm Matthew and tropical depression sixteen led gas prices to rise

more than 8% in mid of September. However, growth in prices was capped by

appreciating currencies. Though earlier gains eroded on the back of strengthening

currencies, NYMEX gas future prices climbed 4% in September. Rising INR in India

market capped the growth of natural gas prices. Gas supply may disrupt as there are

still ten named storms to appear in north Atlantic, which may lead prices in a

positive trend.

Figure 11: Natural Gas Price movement

Source: Bloomberg & KCTL

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

Figure 11:Natural Gas Price movement with Hurricane

Source: Bloomberg & KCTL

Natural gas future contracts calendar spread difference was lower in the month of July.

In August, near month contract September futures traded in a higher range than August

contract, which lead spreads to rise more than Rs.15. Thereafter, a slow recovery was

witnessed in gas prices, which made spread to decline in September. However, the

current trend say spread is expected to rise, though recovery may happen in the US

winter season starting in November.

Figure 12:Natural Gas Spread

Source: Bloomberg & KCTL

As per CFTC report, a continuous rise in short positions is witnessed in the last

quarter. Total long positions have been declined than short positions in September,

which indicates a negative sign for natural gas in near term.

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

Inventory and Consumption

One of the important price driver of gas prices –Inventory; which is always in a rising

trend. The US is the largest producer and consumer of Natural gas. However, Europe,

Asia and UAE are in the queue as world’s large gas consumer. As per the US energy

department, natural gas storage increased more than 3000 billion cubic feet, up 20%

last quarter. Total dry gas production in the month of August increased from July,

whereas declined in the month of September. Baker’s Hughes US rig counts increased to

967 in September standing at two month’s low. while the number of rigs sprouting up

each year is decreasing, natural gas production is on the rise, with many of the shale

wells coming online with their sources fresh and untapped.Not only the industrial and

residential sectors consume gas, commercial, electric power plants and vehicles also use

natural gas in different form. Oversupply on demand pressured gas price movement in

the month of August. There has been more than 40% decline in consumption pattern,

while inventories have build up by more than 25% in the year 2010. The consumption

pattern remains low until the end of September as per the seasonality index and prices

are tending to rise with rising demand thereafter. In US, winter season starts in the

month of November which generally boosts demand of natural gas. Thus we are

expecting a rise in demand in the coming months, which will tend prices upward.

Figure 13: Natural Gas Consumption Vs. Inventory

Source: Bloomberg & KCTL

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

Figure 14: Natural gas Supply & Consumption Forecast

Source: Bloomberg & KCTL

NATURAL GAS TECHNICAL SNAPSHOT

Natural gas quarterly futures prices ended in bearish note loss by -14% with previous

quarter close. As per continues chart prices it made high of $4.636 and ended at lower -

$3.65.Since last seven quarters natural gas prices are trading in a consolidation phase

i.e. 3.412 -5.778 levels. As per the chart prices never closed below the $3.412 i.e23.6%

Fibonacci projections. As per Fibonacci retracement projections may consider $3.475

levels as major support for the prices. Unless and until market sustains above the

mentioned levels, may remains in consolidation phase in coming quarter. However, if

prices breach and sustains below the $3.412 levels may see a further bearishness in the

markets. Momentum indicator quarterly RSI is treading at 0.41 levels and a decline in

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

futures prices along with the decline volumes is suggesting that future prices may trade

sideways in coming quarter (i.e. may trade in previous ranges only) . Currently prices

are trading below the all short term and midterm EMA’s i.e. (9, 18 and 45) days.

Momentum indicator Stochastic also suggesting prices to trade sideways to lower

as %K at 11.91 and %D at 14.80 levels Over all the natural gas futures may trade

sideways in coming quarter.

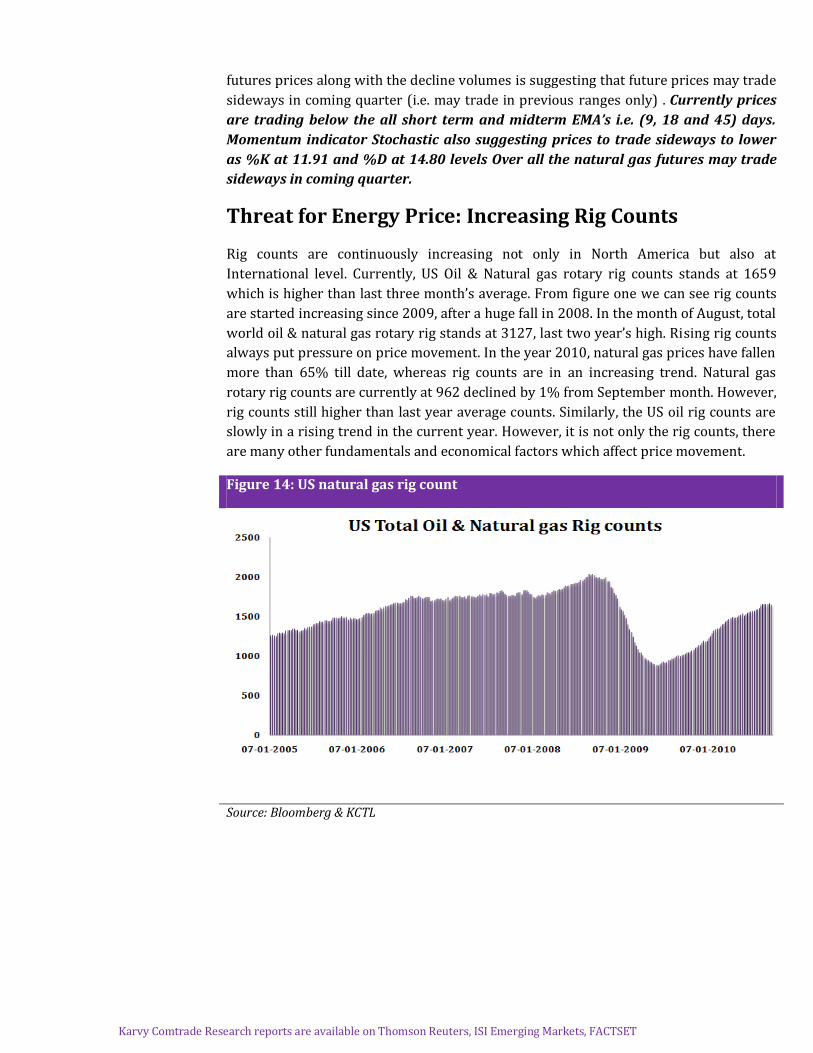

Threat for Energy Price: Increasing Rig Counts

Rig counts are continuously increasing not only in North America but also at

International level. Currently, US Oil & Natural gas rotary rig counts stands at 1659

which is higher than last three month’s average. From figure one we can see rig counts

are started increasing since 2009, after a huge fall in 2008. In the month of August, total

world oil & natural gas rotary rig stands at 3127, last two year’s high. Rising rig counts

always put pressure on price movement. In the year 2010, natural gas prices have fallen

more than 65% till date, whereas rig counts are in an increasing trend. Natural gas

rotary rig counts are currently at 962 declined by 1% from September month. However,

rig counts still higher than last year average counts. Similarly, the US oil rig counts are

slowly in a rising trend in the current year. However, it is not only the rig counts, there

are many other fundamentals and economical factors which affect price movement.

Figure 14: US natural gas rig count

Source: Bloomberg & KCTL

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

Crude Oil- Natural Gas Ratio

Market price of crude oil divided by market price of natural gas gives the crude/natural

gas ratio. The ratio gets stronger if prices of crude oil rise higher than natural gas prices.

In the last quarter, the ratio has been increased more than yearly average, as gas prices

fell more than oil prices. In the end of September, the ratio was stronger, as crude oil

prices improved whereas gas prices fell from its month high. In coming two to three

months, crude prices are expected to decline whereas gas prices are expected to

improve, which may weak the ratio. However, ratio is expected to make a high in

recent period.

Figure 15: Crude Oil & Natural Gas Ratio

Source: Bloomberg & KCTL

Karvy Comtrade Research reports are available on Thomson Reuters, ISI Emerging Markets, FACTSET

To unsubscribe please mail us at [email protected]

Disclaimer

The report contains the opinions of the author that are not to be construed as investment advice. The author, directors and other employees of Karvy, and its affiliates, cannot be held responsible for the accuracy of the information presented herein or for the results of the positio ns taken based on the opinions expressed above. The above-mentioned opinions are based on the information which is believed to be accurate and no assurance can be given for the accuracy of this information. There is risk of loss in trading in derivatives. The author, directors and other employees of Karvy and its affi liates cannot be held responsible for any losses in trading.

Commodity derivatives trading involve substantial risk. The valuation of the underlying may fluctuate, and as a result, clients may lose their entire original investment. In no event should the content of this research report be construed as an express or an implied promise, guarantee or implication by, or from, Karvy Comtrade that you will profit or that losses can, or will be, limited in any manner whatsoever. Past results are no indicatio n of future performance. The information provided in this report is intended solely for informative purposes and is obtained from sources believed to be reliable. Information is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted.

We do not offer any sort of portfolio advisory, portfolio management, or investment advisory services. The reports are only f or information purposes and not to be construed as investment advice.

For a detailed disclaimer please go to following URLs:

http://www.karvycomtrade.com/disclaimer.asp

http://www.karvycomtrade.com/riskDisclaimer.asp