Embed Size (px)

Citation preview

IRS Preparer Penalties and the Strategies to Avoid Them

• All audio is streamed through your computer speakers. • There will be several attendance verification questions

during the LIVE webinar that must be answered via the online quiz at the conclusion to qualify for CPE.

• Today’s webinar will begin at 2:00pm EDT• Please note: You will not hear any sound until the

webinar begins.

Avoiding Preparer Penalties

Robert E. McKenzie312.876.6927www.mckenzielaw.com

2

Learning Objectives

At the end of this webinar, you should be able to:•Recognize the importance of due diligence•Evaluate the risks and rewards of relying on client information •Assess office review policies •Review tax return approval mechanisms•Identify issues arising out of e-filing•Reduce the risk of preparer penalties and contest them when proposed by the IRS. •Know your rights when confronted with a proposed penalty.

New Preparer Complaint Form

Form 14157

4

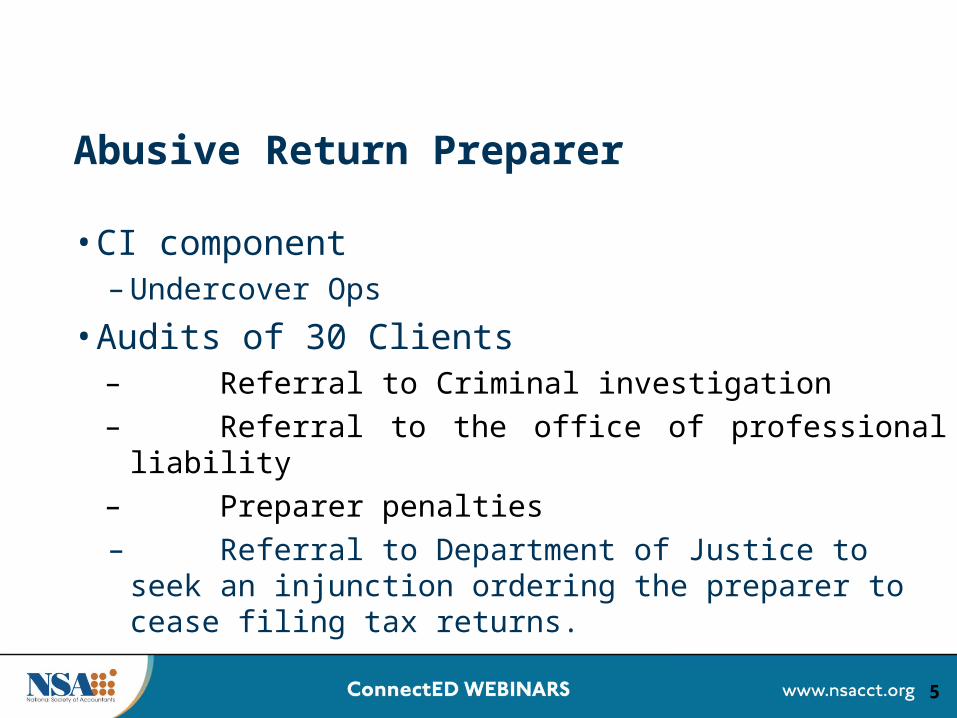

Abusive Return Preparer

• CI component– Undercover Ops

• Audits of 30 Clients – Referral to Criminal investigation– Referral to the office of professional liability– Preparer penalties – Referral to Department of Justice to seek an injunction

ordering the preparer to cease filing tax returns.

5

Abusive Return Preparer

6

FY 2014 FY 2013 FY 2012

Investigations Initiated 305 309 443

Prosecution Recommendations

261 281 276

Indictments/Informations

230 233 202

Convictions 193 207 178

Sentenced 183 186 172

Incarceration Rate* 86.3% 78.0% 84.3%

Average Months to Serve

28 27 29

Tax Return Preparer Penalty

• IRC Sec 6694• 2007 act expanded the definition of a tax return

preparer to cover the preparation of a return or claim for refund of any federal tax, including estate and gift taxes, employment taxes, excise taxes and the returns of exempt organizations.

7

2007 Higher Standards

• Prior standard realistic possibility: A position satisfies the standard if a reasonable and well-informed analysis by a person knowledgeable in the tax law would lead that person to conclude that the position has an approximately one in three,

• Temporarily, the penalty applied in the case of ANY understatement arising from a position the preparer did not reasonably believe met the “more likely than not” test, unless there was a reasonable basis for the position and the position is disclosed.

8

2008 Modification of Penalty on Understatement of Taxpayer’s Liability by Tax Return Preparer.

• Changes the standards for imposition of the tax return preparer penalty. The preparer standard for undisclosed positions is reduced to “substantial authority.”

• The preparer standard for disclosed positions is “reasonable basis.”

• For tax shelters and reportable transactions to which section 6662A applies (i.e., listed transactions and reportable transactions with significant avoidance or evasion purposes), a tax return preparer is required to have a reasonable belief that such a transaction was more likely than not to be sustained on the merits.

• Retroactively effective for returns prepared after May 25, 2007.

9

Standards

•Prior to 2007 “realistic possibility”•2007: “more likely than not”•2008: revised retroactively to “substantial

authority”

10

Definitions

•More likely than not– More than 50%

•Substantial authority– 40% or more

•Realistic possibility– 33% or more

•Reasonable basis– 20% or more– Must make a disclosure Form 8275

•Frivolous

11

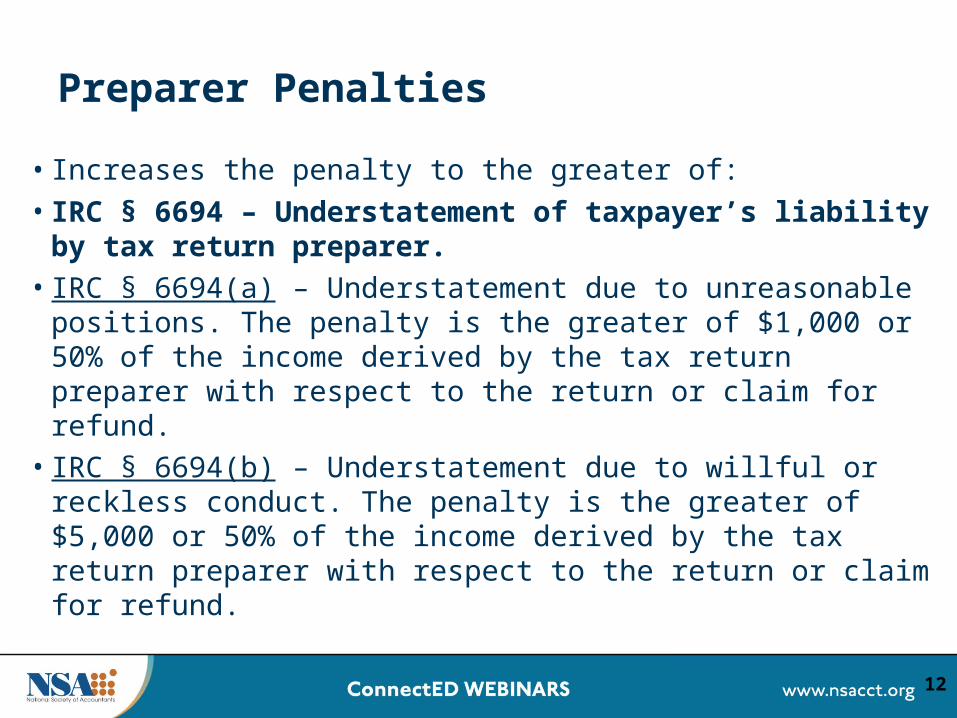

Preparer Penalties

• Increases the penalty to the greater of: • IRC § 6694 – Understatement of taxpayer’s liability by tax return

preparer.• IRC § 6694(a) – Understatement due to unreasonable positions. The

penalty is the greater of $1,000 or 50% of the income derived by the tax return preparer with respect to the return or claim for refund.

• IRC § 6694(b) – Understatement due to willful or reckless conduct. The penalty is the greater of $5,000 or 50% of the income derived by the tax return preparer with respect to the return or claim for refund.

12

(a) Understatement due to unreasonable positions

• (1) In general • If a tax return preparer—

– (A) prepares any return or claim of refund with respect to which any part of an understatement of liability is due to a position described in paragraph (2), and

– (B) knew (or reasonably should have known) of the position,– such tax return preparer shall pay a penalty with respect to each such return or

claim in an amount equal to the greater of $1,000 or 50 percent of the income derived (or to be derived) by the tax return preparer with respect to the return or claim.

13

(2) Unreasonable position

•In general •Except as otherwise provided in this paragraph, a position is described in this paragraph unless there is or was substantial authority for the position.•(B) Disclosed positions •If the position was disclosed as provided in section 6662(d)(2)(B)(ii)(I) and is not a position to which subparagraph (C) applies, (tax shelters) the position is described in this paragraph unless there is a reasonable basis for the position.

14

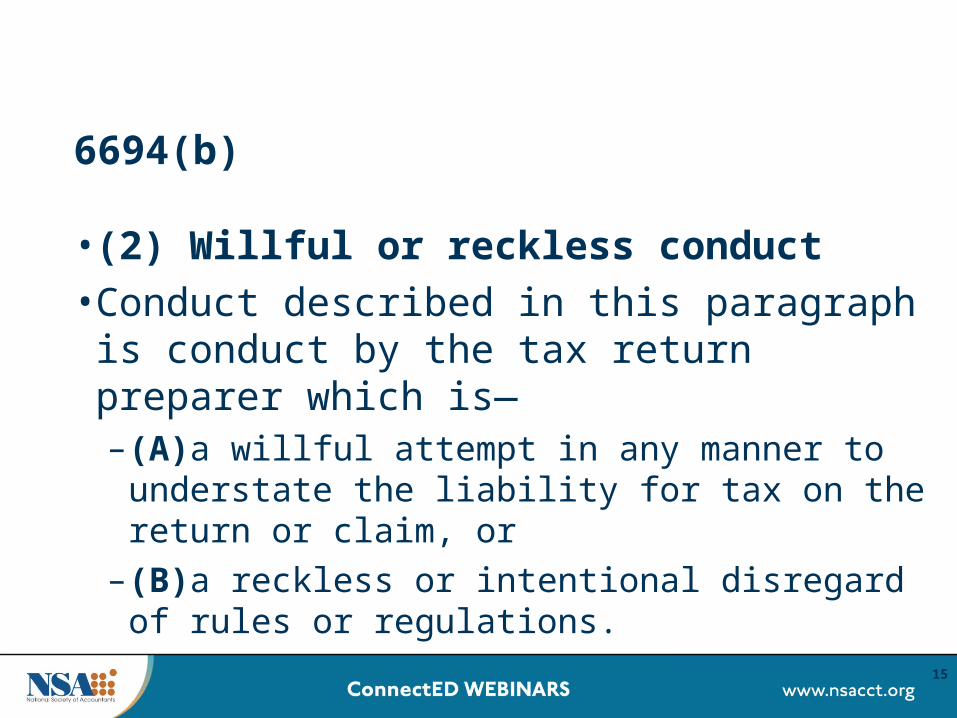

6694(b)

•(2) Willful or reckless conduct •Conduct described in this paragraph is conduct

by the tax return preparer which is—– (A)a willful attempt in any manner to understate the

liability for tax on the return or claim, or – (B)a reckless or intentional disregard of rules or

regulations.

15

Adequate Disclosure

• Disclosure is adequate with respect to the tax treatment of an item (or group of similar items, such as amounts paid or incurred for supplies by a taxpayer engaged in business) or a position on a return if the disclosure is made on a properly completed Form 8275 (or Form 8275-R, if the position is contrary to a reg) that is attached to the return or to a qualified amended return

• Must have at least a reasonable basis

16

UNREASONABLE POSITION• (A) IN GENERAL - Except as otherwise provided in this paragraph, a

position is described in this paragraph unless there is or was substantial authority for the position.

• (B) DISCLOSED POSITIONS - If the position was disclosed as provided in section 6662(d)(2)(B)(ii)(I) and is not a position to which subparagraph (C) applies, the position is described in this paragraph unless there is a reasonable basis for the position.

• (C) TAX SHELTERS AND REPORTABLE TRANSACTIONS - If the position is with respect to a tax shelter (as defined in section 6662(d)(2)(C)(ii)) or a reportable transaction to which section 6662A applies, the position is described in this paragraph unless it is reasonable to believe that the position would more likely than not be sustained on its merits.

17

REASONABLE CAUSE EXCEPTION -

No penalty shall be imposed under this subsection if it is shown that there is reasonable cause for the understatement and the tax return preparer acted in good faith.'.

18

IRC §6695

• IRC § 6695(a) – Failure to furnish copy to taxpayer. The penalty is $50 for each failure to comply with IRC § 6107 regarding furnishing a copy of a return or claim to a taxpayer. The maximum penalty imposed on any tax return preparer shall not exceed $25,000 in a calendar year.

• IRC § 6695(b) – Failure to sign return. The penalty is $50 for each failure to sign a return or claim for refund as required by regulations. The maximum penalty imposed on any tax return preparer shall not exceed $25,000 in a calendar year.

19

IRC §6695

• IRC § 6695(c) – Failure to furnish identifying number. The penalty is $50 for each failure to comply with IRC § 6109(a)(4) regarding furnishing an identifying number on a return or claim. The maximum penalty imposed on any tax return preparer shall not exceed $25,000 in a calendar year.

• IRC § 6695(d) – Failure to retain copy or list. The penalty is $50 for each failure to comply with IRC § 6107(b) regarding retaining a copy or list of a return or claim. The maximum penalty imposed on any tax return preparer shall not exceed $25,000 in a return period.

20

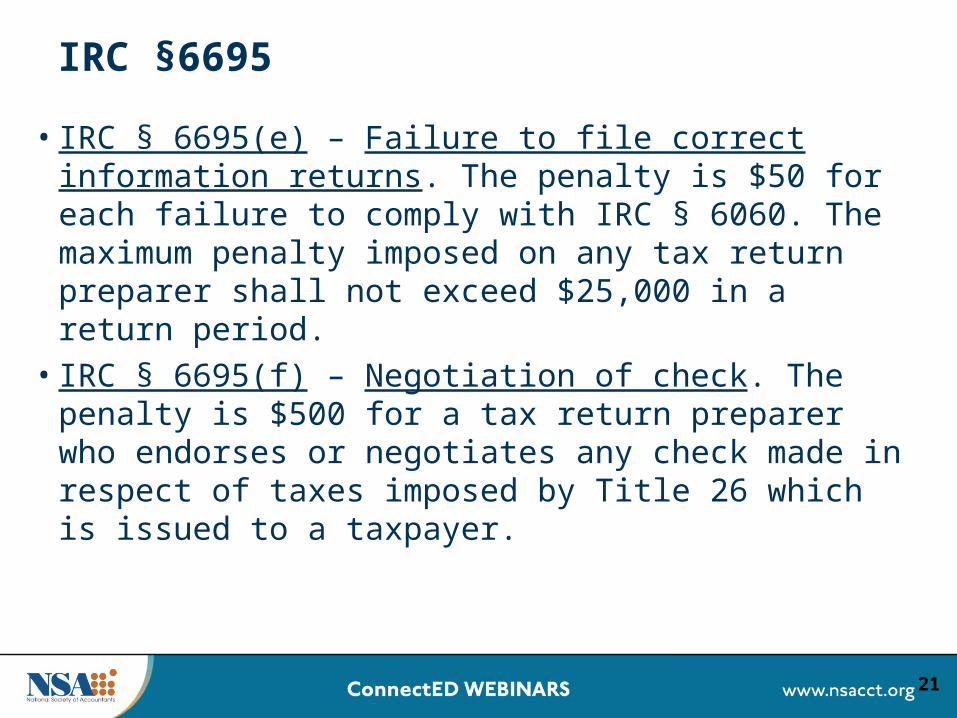

IRC §6695

• IRC § 6695(e) – Failure to file correct information returns. The penalty is $50 for each failure to comply with IRC § 6060. The maximum penalty imposed on any tax return preparer shall not exceed $25,000 in a return period.

• IRC § 6695(f) – Negotiation of check. The penalty is $500 for a tax return preparer who endorses or negotiates any check made in respect of taxes imposed by Title 26 which is issued to a taxpayer.

21

IRC §6695(g)

•EIC Due Diligence Penalty•IRC § 6695(g) – Failure to be diligent in

determining eligibility for earned income credit. The penalty is $500 for each failure to comply with the EIC due diligence requirements imposed in regulations.

•$500 up from $100

22

EITC Due Diligence

8867 Form

23

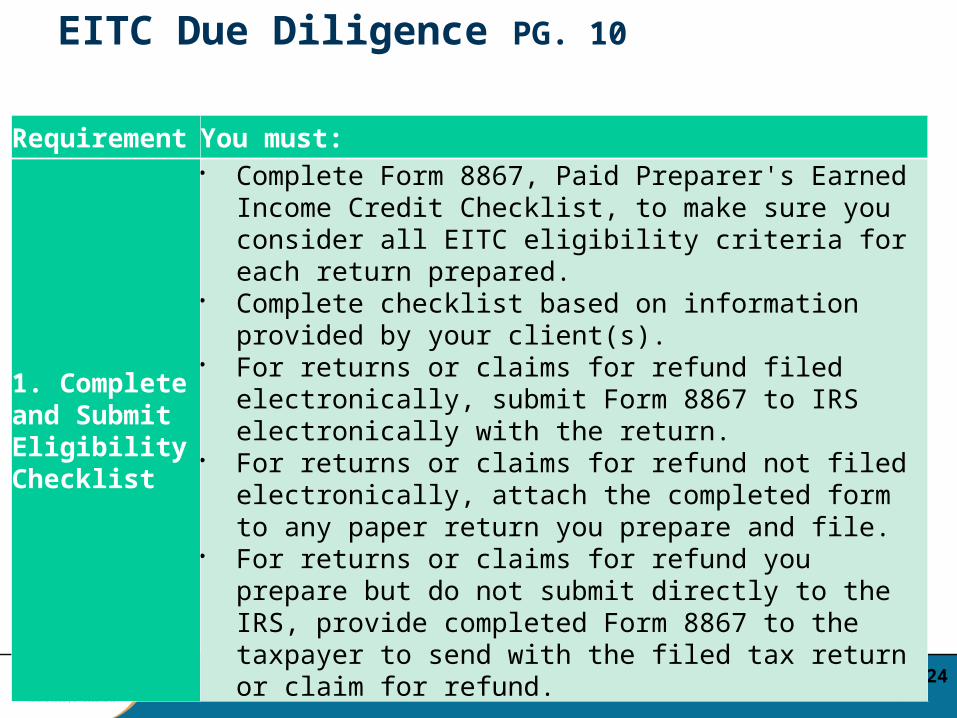

EITC Due Diligence PG. 10

24

Requirement You must:

1. Complete and Submit Eligibility Checklist

Complete Form 8867, Paid Preparer's Earned Income Credit Checklist, to make sure you consider all EITC eligibility criteria for each return prepared.

Complete checklist based on information provided by your client(s).

For returns or claims for refund filed electronically, submit Form 8867 to IRS electronically with the return.

For returns or claims for refund not filed electronically, attach the completed form to any paper return you prepare and file.

For returns or claims for refund you prepare but do not submit directly to the IRS, provide completed Form 8867 to the taxpayer to send with the filed tax return or claim for refund.

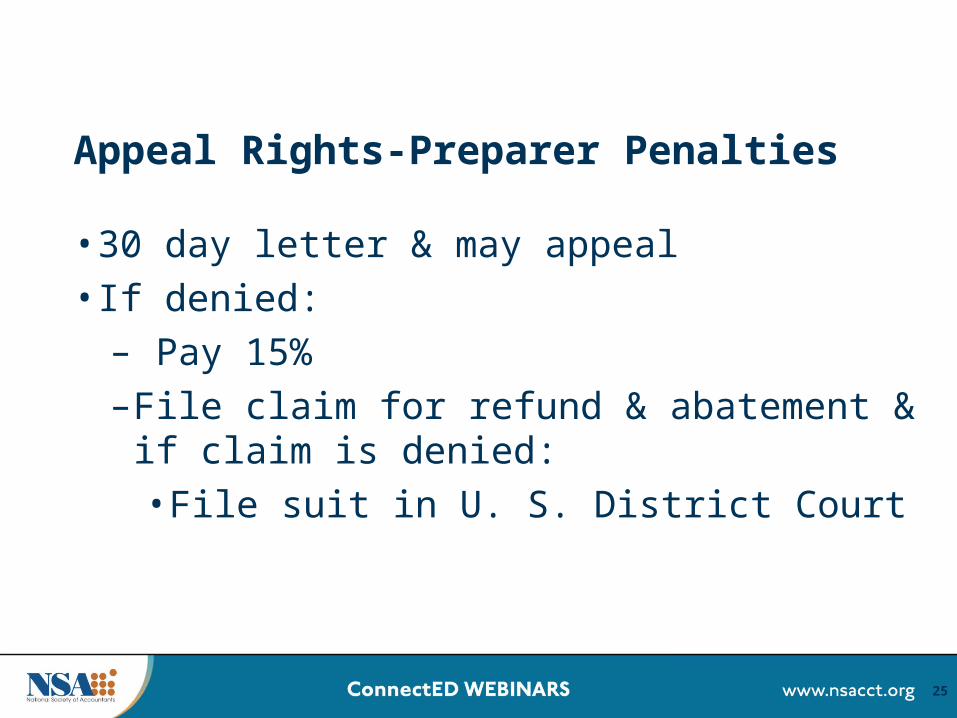

Appeal Rights-Preparer Penalties

• 30 day letter & may appeal• If denied:

– Pay 15%– File claim for refund & abatement & if claim is

denied:• File suit in U. S. District Court

25

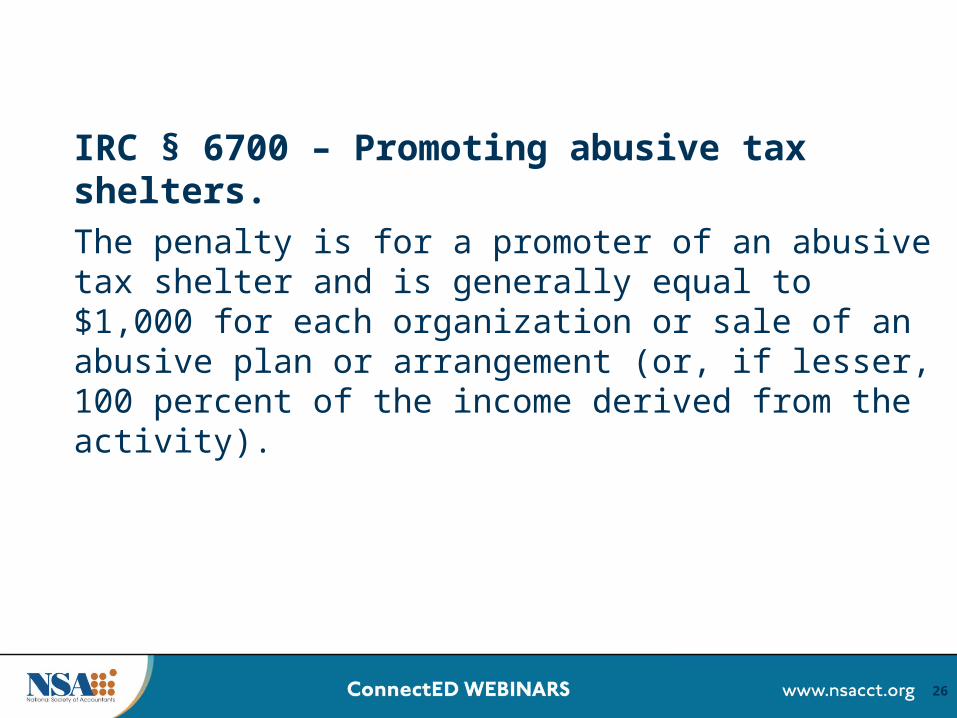

IRC § 6700 – Promoting abusive tax shelters.

The penalty is for a promoter of an abusive tax shelter and is generally equal to $1,000 for each organization or sale of an abusive plan or arrangement (or, if lesser, 100 percent of the income derived from the activity).

26

IRC § 6701 – Penalties for aiding and abetting understatement of tax liability.

The penalty is $1000 ($10,000 if the conduct relates to a corporation’s tax return) for aiding and abetting in an understatement of a tax liability. Any person subject to the penalty shall be penalized only once for documents relating to the same taxpayer for a single tax period or event.

27

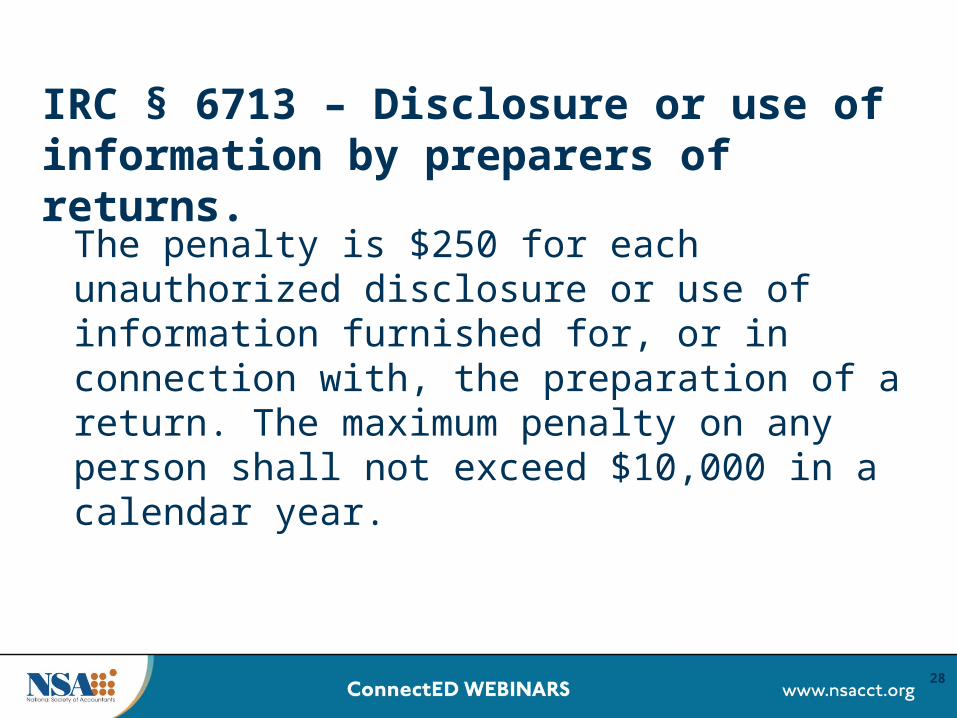

IRC § 6713 – Disclosure or use of information by preparers of returns.

The penalty is $250 for each unauthorized disclosure or use of information furnished for, or in connection with, the preparation of a return. The maximum penalty on any person shall not exceed $10,000 in a calendar year.

28

IRC § 7206 – Fraud and false statements.

Guilty of a felony and, upon conviction, a fine of not more than $100,000 ($500,000 in the case of a corporation), imprisonment of not more than three years, or both (together with the costs of prosecution).

29

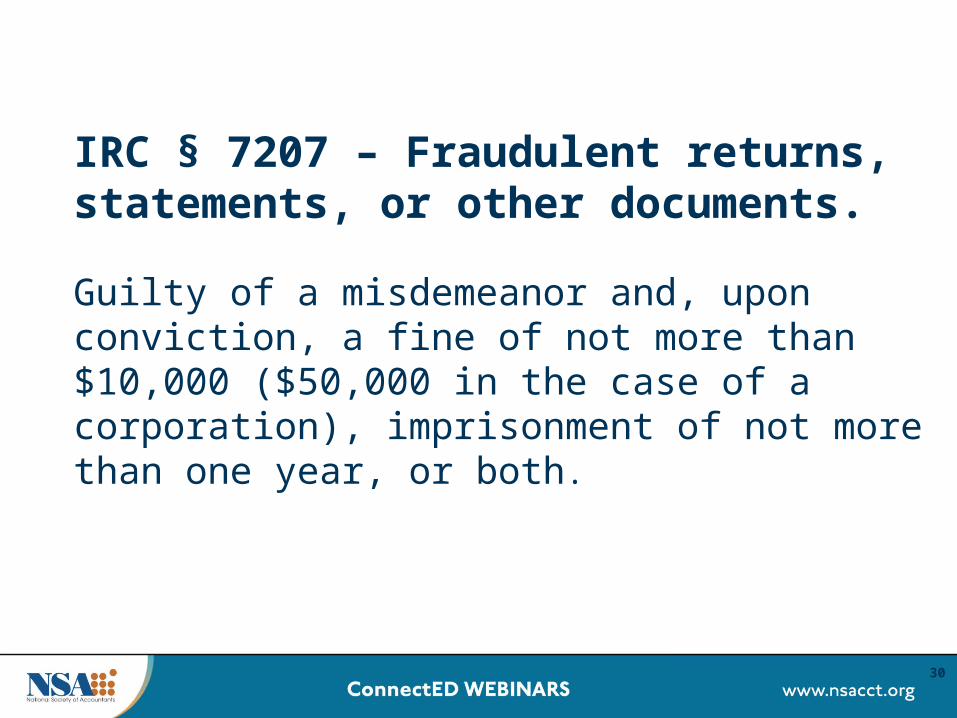

IRC § 7207 – Fraudulent returns, statements, or other documents.

Guilty of a misdemeanor and, upon conviction, a fine of not more than $10,000 ($50,000 in the case of a corporation), imprisonment of not more than one year, or both.

30

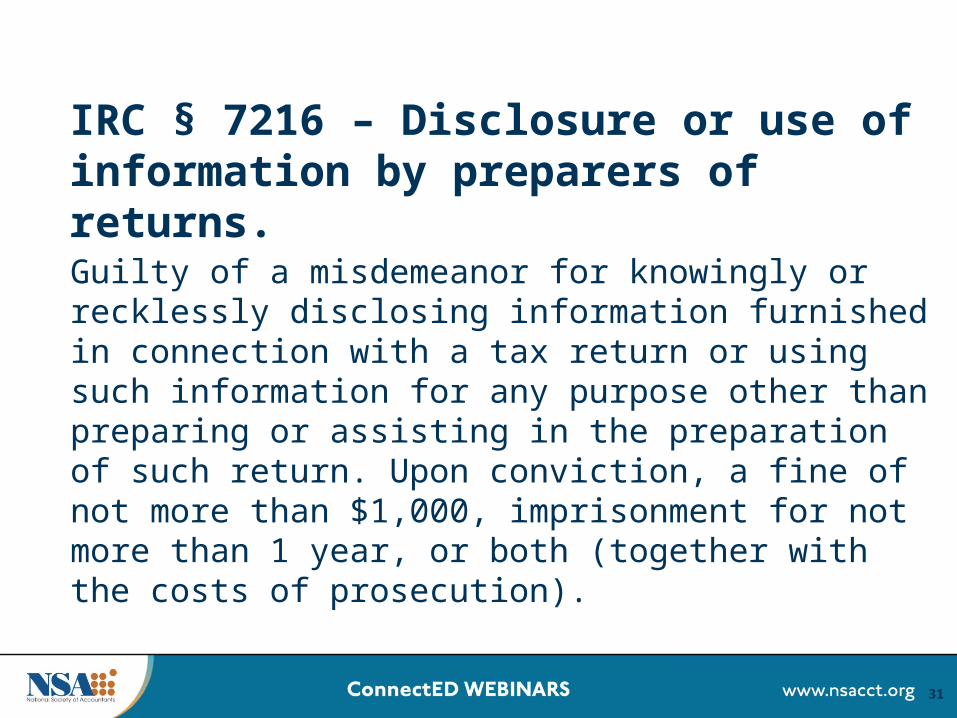

IRC § 7216 – Disclosure or use of information by preparers of returns.

Guilty of a misdemeanor for knowingly or recklessly disclosing information furnished in connection with a tax return or using such information for any purpose other than preparing or assisting in the preparation of such return. Upon conviction, a fine of not more than $1,000, imprisonment for not more than 1 year, or both (together with the costs of prosecution).

31

Injunctions

• IRC § 7407 – Action to enjoin tax return preparers.• A federal district court may enjoin a tax return preparer from

engaging in certain proscribed conduct, or in extreme cases, from continuing to act as a tax return preparer altogether.

• IRC § 7408 – Action to enjoin specified conduct related to tax shelters and reportable transactions.

• A federal district court may enjoin a person from engaging in certain proscribed conduct (including any action, or failure to take action, which is in violation of Circular 230).

32

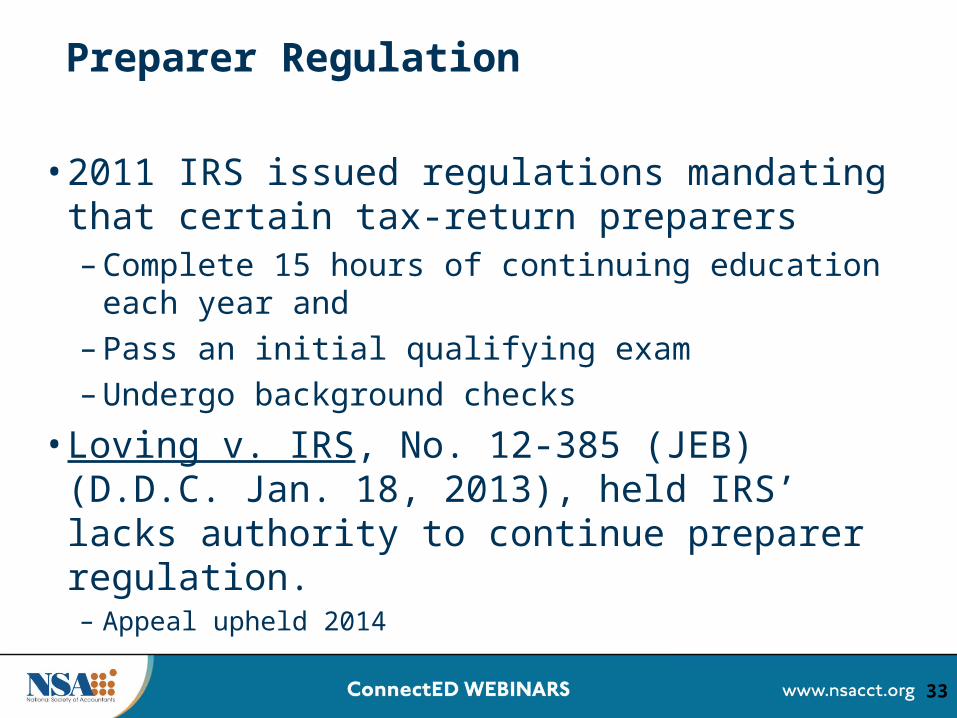

Preparer Regulation

• 2011 IRS issued regulations mandating that certain tax-return preparers – Complete 15 hours of continuing education each year and – Pass an initial qualifying exam – Undergo background checks

• Loving v. IRS, No. 12-385 (JEB) (D.D.C. Jan. 18, 2013), held IRS’ lacks authority to continue preparer regulation.– Appeal upheld 2014

33

Due Diligence

• Karen Hawkins, Director of OPR, has made several speeches warning of enhanced enforcement of due diligence and has specifically mentioned FS’s & CDP’s

• She has hired more attorneys to do enforcement

34

Discipline

If you receive a return-related penalty, you can also face:

– Suspension or expulsion of you or your firm from IRS e-file

– Other disciplinary action by the IRS Office of Professional Responsibility

– Injunctions barring you from preparing tax returns or imposing conditions on the tax returns you may prepare

35

New Return Preparer Office (RPO)• Carol A. Campbell, Director• New return preparer office was created to administer PTIN

applications, competency testing, and continuing education. • IRS decided that an office dedicated solely to the matters will

allow the IRS to best serve tax return preparers and taxpayers by providing efficiency and expertise in this area.

• Concurrently, the Office of Professional Responsibility will continue to enforce the Circular 230 provisions relating to practitioner conduct and discipline.

36

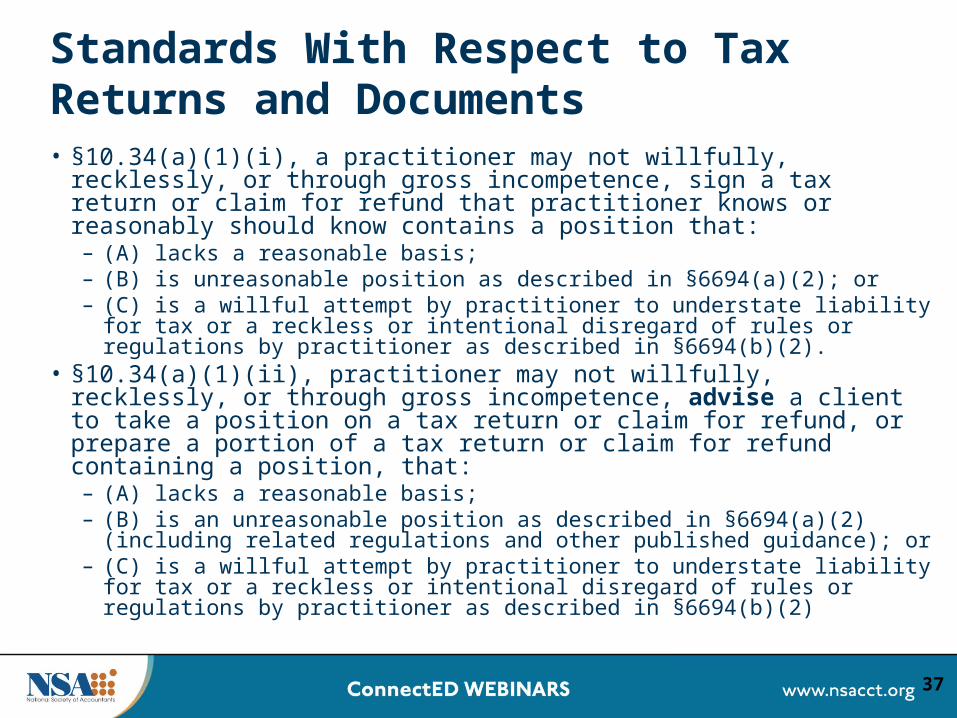

Standards With Respect to Tax Returns and Documents • §10.34(a)(1)(i), a practitioner may not willfully, recklessly, or through gross

incompetence, sign a tax return or claim for refund that practitioner knows or reasonably should know contains a position that:

– (A) lacks a reasonable basis; – (B) is unreasonable position as described in §6694(a)(2); or – (C) is a willful attempt by practitioner to understate liability for tax or a reckless or

intentional disregard of rules or regulations by practitioner as described in §6694(b)(2).

• §10.34(a)(1)(ii), practitioner may not willfully, recklessly, or through gross incompetence, advise a client to take a position on a tax return or claim for refund, or prepare a portion of a tax return or claim for refund containing a position, that:

– (A) lacks a reasonable basis; – (B) is an unreasonable position as described in §6694(a)(2) (including related

regulations and other published guidance); or – (C) is a willful attempt by practitioner to understate liability for tax or a reckless or

intentional disregard of rules or regulations by practitioner as described in §6694(b)(2)

37

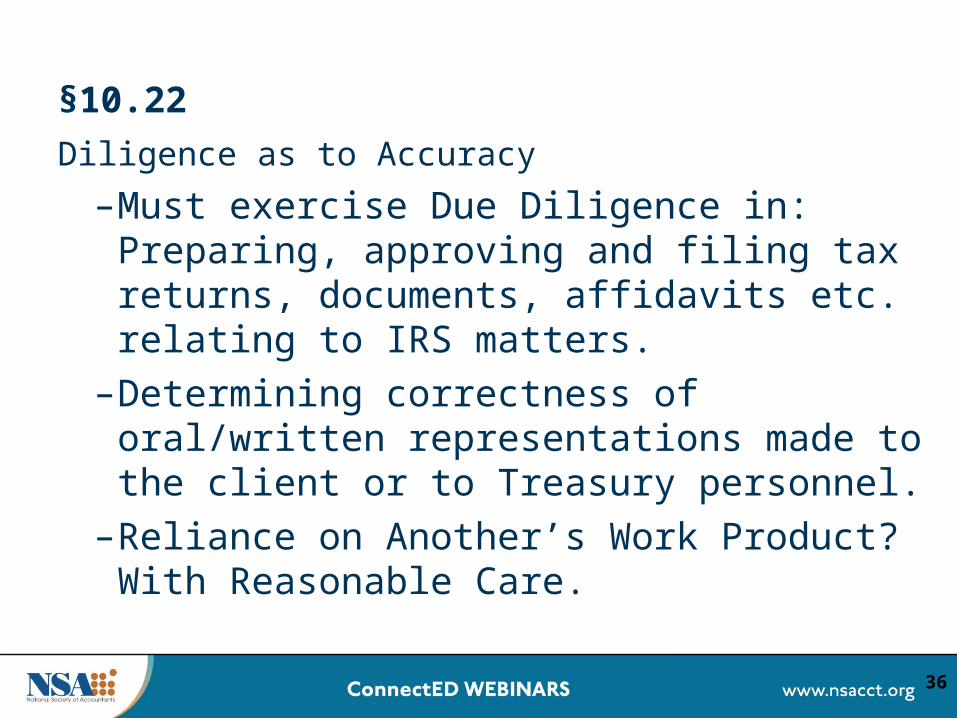

§10.22Diligence as to Accuracy

– Must exercise Due Diligence in: Preparing, approving and filing tax returns, documents, affidavits etc. relating to IRS matters.

– Determining correctness of oral/written representations made to the client or to Treasury personnel.

– Reliance on Another’s Work Product? With Reasonable Care.

36

Procedures to Ensure Compliance

• §10.36(b) provides that firm management with principal authority and responsibility for overseeing a firm’s practice of preparing tax returns, claims for refunds and other documents filed with the IRS must take reasonable steps to ensure that the firm has adequate procedures in effect for purposes of complying with Circular 230.

• Treasury and IRS believe that expansion of §10.36 to require firm procedures for tax return preparation practice, in addition to the pre-existing application to covered opinions, will help ensure compliance and encourage firms to self-regulate.

• Firm responsibility is a critical factor in ensuring high quality advice and representation for taxpayers.

39

§10.21Knowledge of client’s omission

– A practitioner who, having been retained by a client with respect to a matter administered by the Internal Revenue Service, knows that the client has not complied with the revenue laws of the United States or has made an error in, or omission from, any return, document, affidavit, or other paper which the client submitted or executed under the revenue laws of the United States, must advise the client promptly of the fact of such noncompliance, error, or omission. The practitioner must advise the client of the consequences as provided under the Code and regulations of such noncompliance, error, or omission.

38

7-15-13 Press Report

The Director of Practice will use certain information to ensure that: 1)enrolled agents properly complete continuing education requirements to obtain renewal; 2)2) practitioners properly obtain consent of taxpayers before representing conflicting interests; 3)3) practitioners do not use e-commerce to make misleading solicitations.

41

HAVE A LESS HAVE A LESS

TAXING YEAR!!!!!TAXING YEAR!!!!!

Thank You!!Thank You!!

42

Thank you for participating in this webinar.Below is the link to the online survey and CPE quiz:

http://webinars.nsacct.org/postevent.php?id=15781Use your password for this webinar that is in your email confirmation.

You must complete this survey and the quiz or final exam (for the recorded version) to qualify to receive CPE credit.

National Society of Accountants1010 North Fairfax Street

Alexandria, VA 22314-1574Phone: (800) 966-6679