Embed Size (px)

Citation preview

1

The Top 10 Preparer

And Other Penalties: Not Going

To Jail, But It Still Hurts

Givner & Kaye, A Professional [email protected]

2

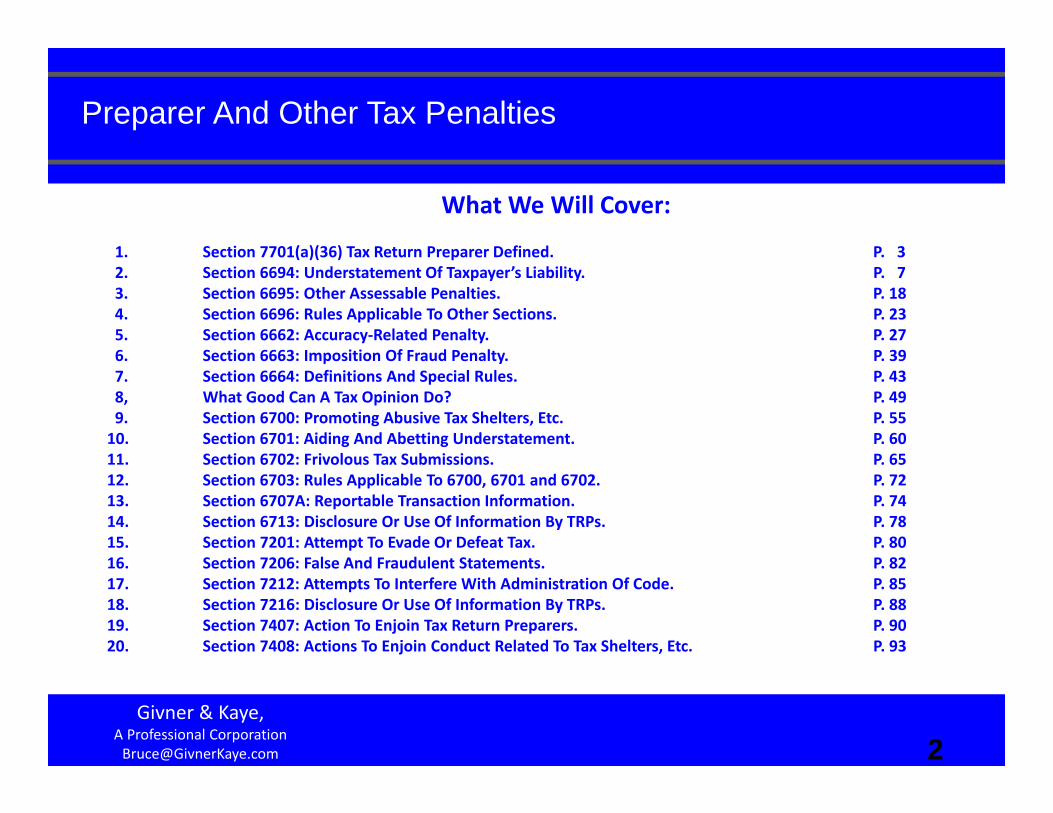

Preparer And Other Tax Penalties

Givner & Kaye, A Professional [email protected]

What We Will Cover:

1. Section 7701(a)(36) Tax Return Preparer Defined. P. 32. Section 6694: Understatement Of Taxpayer’s Liability. P. 73. Section 6695: Other Assessable Penalties. P. 184. Section 6696: Rules Applicable To Other Sections. P. 235. Section 6662: Accuracy‐Related Penalty. P. 276. Section 6663: Imposition Of Fraud Penalty. P. 397. Section 6664: Definitions And Special Rules. P. 438, What Good Can A Tax Opinion Do? P. 499. Section 6700: Promoting Abusive Tax Shelters, Etc. P. 5510. Section 6701: Aiding And Abetting Understatement. P. 6011. Section 6702: Frivolous Tax Submissions. P. 6512. Section 6703: Rules Applicable To 6700, 6701 and 6702. P. 7213. Section 6707A: Reportable Transaction Information. P. 7414. Section 6713: Disclosure Or Use Of Information By TRPs. P. 7815. Section 7201: Attempt To Evade Or Defeat Tax. P. 8016. Section 7206: False And Fraudulent Statements. P. 8217. Section 7212: Attempts To Interfere With Administration Of Code. P. 8518. Section 7216: Disclosure Or Use Of Information By TRPs. P. 8819. Section 7407: Action To Enjoin Tax Return Preparers. P. 9020. Section 7408: Actions To Enjoin Conduct Related To Tax Shelters, Etc. P. 93

2

3

Section 7701(a)(36) – Tax Return Preparer [“TRP”]

(A) In General. The term “TRP” means any person who prepares for compensation,or who employs one or more persons to prepare for compensation, any return of tax….….[T]he preparation of a substantial portion of a return or refund claim shall be treated asif it were the preparation of such return or claim for refund.

(B) Exceptions. A person shall not be a “TRP” merely because such person –

(i) furnishes typing, reproducing, or other mechanical assistance,

(ii) prepares a return or refund claim of the employer (or of an officer or employee ofthe employer) by whom he is regularly and continuously employed),

(iii) prepares as a fiduciary a return or claim for refund for any person, or

(iv) prepares a refund claim for a taxpayer in response to any deficiency noticeissued to such taxpayer or in response to any waiver of restriction after thebeginning of an audit of such taxpayer or another taxpayer if a determinationin that audit directly or indirectly affects the tax liability of such taxpayer.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

3

4

Section 7701(a)(36) – Tax Return Preparer [“TRP”] (cont’d)Before May 25, 2007, the penalty only applied to income tax return preparers.

This penalty does not apply to preparers of FinCen 114, which is required not under theInternal Revenue Code but under the Bank Secrecy Act.

TAM 8731004: A corporation was considered to be a preparer even though, under its franchiseagreement, it was prohibited from physically preparing returns.

A person who reviews a return for substantive correctness is considered a preparer, whether ornot the review results in any changes to the return. Rev. Rul. 84-3.

A person who renders tax advice on a position that is directly relevant to the determination ofthe existence, characterization, or amount of an entry on a return or claim for refund will be regarded ashaving prepared that entry. Reg. Section 301.7701-15(b)(3).

An advisor who conducted a study of the taxpayer's allowable research credits for prior yearsis a preparer where the results of the study, including the improper election and computation, formed thebasis of the taxpayer's reporting on his tax return. FAA 20032601F.

A company that furnishes computerized tax return preparation services (and the computerprogrammer) is treated as preparing the tax returns that utilized the program where the program goesbeyond mere mechanical and clerical assistance and makes substantive determinations concerning theapplication of the tax law to the information provided. Rev. Ruls. 85-187; 85-188; and 85-189.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

4

5

Section 7701(a)(36) – Tax Return Preparer [“TRP”] (cont’d)A tax return preparer as to one return is not considered a tax return preparer of another return

merely because one or more entries reported on the first return may affect an entry reported on the otherreturn.

If, however, the entries reported on the first return are directly reflected on the other return andconstitute a “substantial portion” of the other return, the preparer is also considered a preparer of the otherreturn. Reg. Section 301.7701-15(b)(3)(iii).

The sole preparer of a partnership or S corporation income tax return is considered a preparerof the returns of a partner or shareholder, if the entries on the partnership or S corporation return that arereportable on the partner's or shareholder's return constitute a substantial portion of such returns. Reg.Section 301.7701-15(b)(3)(iii). Goulding v. U.S., 957 F.2d 1420 (7th Cir. 1992).

The tax return preparer of a return showing an NOL is also a preparer of each return thatreflects a carryback or carryover of that loss as a substantial portion of such return. Rev. Rul. 81-171.

A single tax entry may constitute a substantial portion of the tax required to be shown on thereturn. Reg. Section 301.7701-15(b)(3)(i).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

5

6

Section 7701(a)(36) – Tax Return Preparer [“TRP”] (cont’d)After December 31, 2008, the regulations distinguish between a “signing” and “nonsigning” tax

return preparer. Reg. Section 301.7701-15(b)(1), as amended by T.D. 9436.

A “nonsigning tax return preparer” is any TRP who is not a signing TRP but who prepares all ora substantial portion of a return or claim for refund as to events that have occurred when the advice isrendered. Reg. Section 301.7701-15(b)(2).

In determining whether an individual is a nonsigning TRP, any time spent on advice that is givenas to events that have occurred that represents less than 5% of the total time spent by the individual as tothe positions giving rise to the understatement is not considered. Reg. Section 301.7701-15(b)(2). Theless-than-5% test is intended to encourage tax professionals who principally rendered advice regardingevents that have not yet occurred to provide follow-up advice requested by the taxpayer without theconcern that, by providing such advice, the professional would become a TRP.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

6

7

Section 6694 Understatement of taxpayer’s liability by tax return preparer

(a) Understatement due to unreasonable positions.

(1) In General.

If a tax return preparer –

(A) prepares any return or claim of refund with respect towhich any part of an understatement of liability is due to a position described inparagraph (2), and

(B) knew (or reasonably should have known) of the position,

such tax return preparer shall pay a penalty with respect to each such return or claimin an amount equal to the greater of $1,000 or 50% of the income derived (or to bederived) by the tax return preparer with respect to the return or claim.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

7

8

Section 6694 [continued]

(2) Unreasonable position.

(A) In General. Except as otherwise provided in this paragraph, aposition is described in this paragraph unless there is or was substantial authority forthe position.

(B) Disclosed positions. If the position was disclosed as provided inSection 6662(d)(2)(B)(ii)(I) and is not a position to which subparagraph (C) applies, theposition is described in this paragraph unless there is a reasonable basis for theposition.

(C) Tax shelters and reportable transactions. If the position is withrespect to a tax shelter (as defined in Section 6662(d)(2)(C)(ii) or a reportabletransaction to which Section 6662A applies, the position is described in thisparagraph unless it is reasonable to believe that the position would more likely thannot be sustained on its merits.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

8

9

Section 6694 [continued]

(3) Reasonable cause exception. No penalty shall be imposed underthis subsection if it is shown that there is reasonable cause for the understatementand the TRP acted in good faith.

(b) Understatement due to willful or reckless conduct.

(1) In general. Any TRP who prepares any return or refund claim as towhich any part of an understatement is due to a conduct described in paragraph (2)shall pay a penalty as to such return or claim in an amount equal to the greater of –

(A) $5,000, or

(B) 50% of the income derived (or to be derived) by the TRPas to the return or claim.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

9

10

Section 6694 [continued]

(2) Willful or reckless conduct. Conduct described in this paragraphis conduct by the TRP which is –

(A) a willful attempt in any manner to understate the liabilityfor tax on the return or claim, or

(B) a reckless or intentional disregard of rules or regulations.

(3) Reduction in penalty. The amount of any penalty payable by anyperson by reason of this subsection for any return or claim for refund shall bereduced by the amount of the penalty paid by such person by reason of subsection(a).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

10

11

Section 6694 [continued]

(c) Extension of period of collection where preparer pays 15% of penalty.

(1) In general. If, within 30 days after the day on which notice anddemand for any penalty under subsection (a) or (b) is made against any person who isa tax return preparer, such person pays an amount which is not less than 15% of theamount of such penalty and files a claim for refund of the amount so paid, no levy orproceeding in court for the collection of the remainder of such penalty shall be made,begun, or prosecuted until the final resolution of a proceeding begun as provided inparagraph (2). Notwithstanding the provisions of section 7421(a), the beginning ofsuch proceeding or levy during the time such prohibition is in force may be enjoinedby proceeding in the proper court. Nothing in this paragraph shall be constructed toprohibit any counterclaim for the remainder of such penalty in a proceeding begun asprovided in paragraph (2).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

11

12

Section 6694 [continued]

(2) Preparer must bring suit in district court to determine his liability for penalty.If within 30 days after the day on which his claim for refund of any partial payment ofany penalty under subsection (a) or (b0 is denied (or, if earlier, within 30 days after theexpiration of 6 months after the day on which he filed the claim for refund), the taxreturn preparer fails to being a proceeding in the appropriate U.S. district court for thedetermination of his liability for such penalty, paragraph (1) shall cease to apply withrespect to such penalty, effective on the day following the close of the applicable 30-day period referred to in this paragraph.

(3) Suspension of running of period of limitations on collection. The running ofthe period of limitations provided in section 6502 on the collection by levy or by aproceeding in court in respect of any penalty described in paragraph (1) shall besuspended for the period during which the Secretary is prohibited from collecting bylevy or a proceeding in court.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

12

13

Section 6694 [continued]

(d) Abatement of penalty where taxpayer’s liability not understated. If at anytime there is a final administrative determination or a final judicial decision that therewas no understatement of liability in the case of any return or claim for refund withrespect to which a penalty under subsection (a) or (b) has been assessed, suchassessment shall be abated, and if any portion of such penalty has been paid theamount so paid shall be refunded to the person who made such payment as anoverpayment of tax without regard to any period of limitations which, but for thesubsection, would apply to the making of such refund.

(e) Understatement of liability defined. For purposes of this section,“understatement of liability” means any understatement of the net amount payablewith respect to any tax imposed by this title or any overstatement of the net amountcreditable or refundable with respect to any such tax. Except as otherwise providedin subsection (d), the determination of whether or not there is an understatement ofliability shall be made without regard to any administrative or judicial action involvingthe taxpayer.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

13

14

Section 6694 - UpdatesU.S. v. Hand-Bostick, (2011, DC TX) 108 AFTR 2d 2011-6235.TRPs were granted in part and denied in part summary judgment on

govt.'s complaint for injunctive relief under §§7408, 7407 and 7402 from theirpromotion of fraudulent nonconventional fuel source tax credit scheme: TRPswere entitled to summary judgment as to their alleged conduct subject to §6701penalty because they lacked actual knowledge of fraudulent scheme, materialfact issues remained as to whether they engaged in conduct subject to §6700penalty due to complex issues and govt.'s evidence suggested they furnishedgross valuation overstatements for scheme and later loss deductions tocustomers via assignment agreements and production reports. Evidence showedTRPs didn't engage in fraudulent or deceptive conduct under §7407(b)(1)(D),questions existed as to whether they had reasonable cause for understatementson returns within meaning of §6694(a) and as to whether their conduct wasreasonable under §6694(b).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

14

15

Section 6694 - Updates

U.S. v. Aparicio, (2011, DC CA) 108 AFTR 2d 2011-5502.

Stipulated order of permanent injunction was entered againstTRP barring him and his employees from acting as preparers, instructingor advising others to violate tax laws, engaging in conduct subject topenalty under §§6694. 6700 and 6701 and representing others beforeIRS. TRP was also ordered to send injunction copy to clients. Whileprohibited from owning, controlling or managing any tax preparationbusiness, he wasn't precluded from working in non-professional capacityin any such business.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

15

16

Section 6694 - Updates

U.S. v. Littrice, (2011, DC IL) 108 AFTR 2d 2011-5710.

Govt.'s complaint for broad injunction, permanently barring TRPand her solely owned accounting business from preparing returns forothers and from violating tax laws, was granted on summary judgment:injunction was warranted under §7407 when considering her prior§7206(2) conviction and other evidence that she had engaged in conductsubject to penalty under §6694 and 6695, by recklessly or willfullyunderstating client liabilities and by using someone else's PTIN; thatshe kept doing so even after learning of IRS investigation; and that shewas likely to continue absent injunction. Alternately, evidencesupported injunction under either §7408 or 7402.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

16

17

Section 6694 - Updates

U.S. v. Giroud, (2011, DC CA) 108 AFTR 2d 2011-6372.

Permanent injunction was entered against TRP, barring him andthose acting with him from acting as preparers, engaging in conductsubject to penalty under §6694 and 6701, preparing his own returns withfalse tax withholding and refunds based on amounts shown in Forms1099-OID, filing or abetting filing of frivolous returns, and engaging inconduct subject to penalty under IRC or that otherwise interfered with taxlaw administration and enforcement. TRP was ordered to inform clientsof injunction order and provide govt. with client list.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

17

18

Section 6695 Other Assessable penalties with respect to the preparation

of tax returns for other persons

(a) Failure to furnish copy to taxpayer. Any person who is a TRP as to anyreturn or claim for refund who fails to comply with section 6107(a) as to such return orclaim shall pay a penalty of $50 for such failure, unless it is shown that such failure isdue to reasonable cause and not due to willful neglect. The maximum penaltyimposed under this subsection on any person with respect to documents filed duringany calendar year shall not exceed $25,000.

(b) Failure to sign return. Any person who is a TRP with respect to any returnor claim for refund, who is required by regulations prescribed by the Secretary to signsuch return or claim, and who fails to comply with such regulations with respect tosuch return or claim shall pay a penalty of $50 for such failure, unless it is shown thatsuch failure is due to reasonable cause and not due to willful neglect. The maximumpenalty imposed under this subsection on any person with respect to documents filedduring any calendar year shall not exceed $25,000.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

18

19

Section 6695 [continued]

(c) Failure to furnish identifying number. Any person who is a TRP as to anyreturn or claim for refund and who fails to comply with section 6109(a)(4) with respectto such return or claim shall pay a penalty of $50 for such failure, unless it is shownthat such failure is due to reasonable cause and not due to willful neglect. Themaximum penalty imposed under this subsection on any person with respect todocuments filed during any calendar year shall not exceed $25,000.

(d) Failure to retain copy or list. Any person who is a tax return preparer withrespect to any return or claim for refund who fails to comply with section 6107(b) withrespect to such return or claim shall pay a penalty of $50 for each such failure, unlessit is shown that such failure is due to reasonable cause and not due to willful neglect.The maximum penalty imposed under this subsection on any person with respect toany return period shall not exceed $25,000.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

19

20

Section 6695 [continued]

(e) Failure to file correct information returns. Any person required to make areturn under section 6060 who fails to comply with the requirements of such sectionshall pay a penalty of $50 for (1) each failure to9 file a return as required under suchsection, and (2) each failure to set forth an item in the return as required under suchsection, unless it is shown that such failure is due to reasonable cause and not due towillful neglect. The maximum penalty imposed under this subsection on any personwith respect to any return period shall not exceed $25,000.

(f) Negotiation of check. Any person who is a tax return preparer whoendorses or otherwise negotiates (directly or through an agent) any check made inrespect of the taxes imposed by this title which is issued to a taxpayer (other than thetax return preparer) shall pay a penalty of $500 with respect to each such check. Thepreceding sentence shall not apply with respect to the deposit by a bank…of the fullamount of the check in the taxpayer’s account in such bank for the taxpayer’s benefit.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

20

21

Section 6695 [continued]

(g) Failure to be diligent in determining eligibility for earned income credit. Anyperson who is a tax return preparer with respect to any return or claim for refund whofails to comply with due diligence requirements imposed by the Secretary byregulations with respect to determining eligibility for, or the amount of, the creditallowable by section 32 shall pay a penalty of $500 for each such failure.

$500 for returns required to filed after 12/31/2011 due to H.R. 3080, the U.S.-KoreaFree Trade Agreement Implementation Act just signed by the president.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

21

22

U.S. v. Penny Lea JonesJuly 7, 2011 Dist. Ct. Idaho

Ms. Jones submitted phony IRS Forms 1099-OID which purport to havebeen issued to or received by the taxpayer from a creditor that withholds nearly allof the interest income reported on the returns in the amount of the debt, usually amortgage, car loan, or credit card balance owed by the taxpayer. Based on what iscommonly referred to as “redemption theories,” which claim taxpayers are entitledto access a secret treasury account to satisfy their tax liabilities by using IRS forms.Under this theory there exists an “unrestricted right for collections and return offunds/securities” issued to every child born in the U.S. The birth certificates issuedto the children become a registered security representing that child’s life-long laboron a general average basis. The security is held in trust by the U.S. government, inwhom the children are its stockholders, as a redeemable bond. Etc.

She filed 437 returns claiming $168 million in refunds. So she violated§6694 by understating her customers’ liabilities and §6695 by failing to remit a list ofcustomers or copies of returns to the IRS when requested (IRC §6107(b)).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

22

23

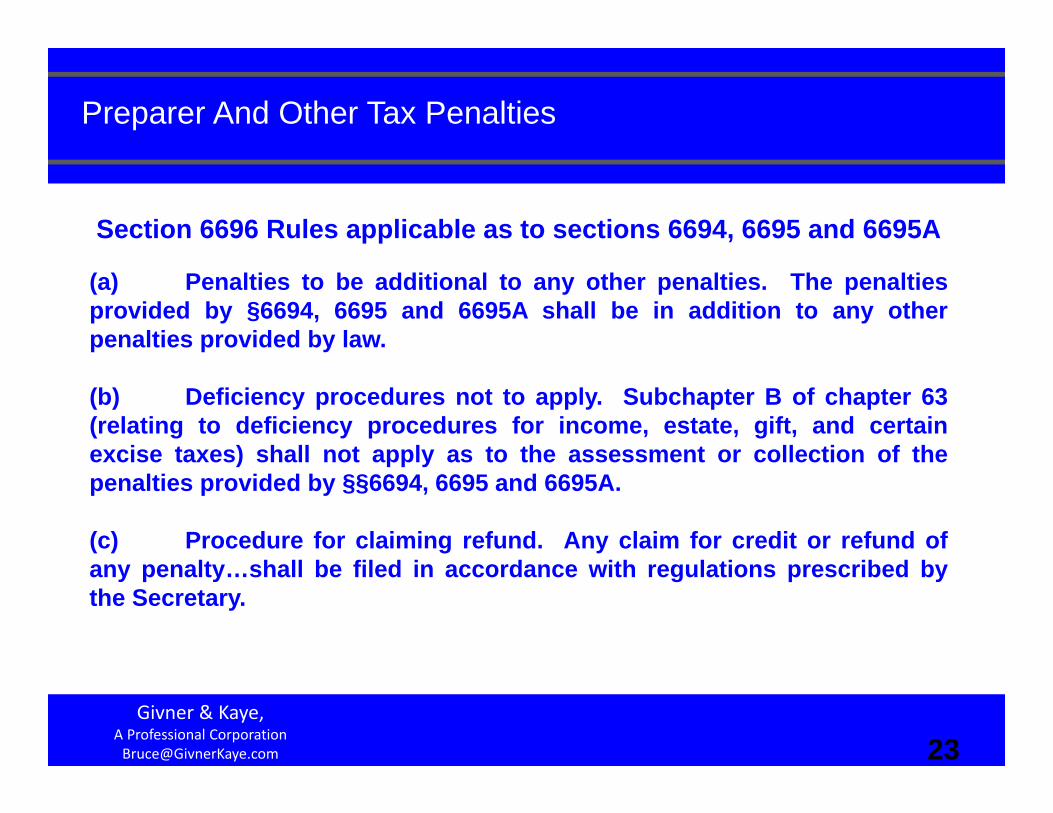

Section 6696 Rules applicable as to sections 6694, 6695 and 6695A

(a) Penalties to be additional to any other penalties. The penaltiesprovided by §6694, 6695 and 6695A shall be in addition to any otherpenalties provided by law.

(b) Deficiency procedures not to apply. Subchapter B of chapter 63(relating to deficiency procedures for income, estate, gift, and certainexcise taxes) shall not apply as to the assessment or collection of thepenalties provided by §§6694, 6695 and 6695A.

(c) Procedure for claiming refund. Any claim for credit or refund ofany penalty…shall be filed in accordance with regulations prescribed bythe Secretary.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

23

24

Section 6696 Rules applicable to sections 6694, 6695 and 6695A [continued]

(d) (1) Assessment. The amount of any penalty under §6694(a), 6695or 6695A shall be assessed within 3 years after the return or claim forrefund as to which the penalty is assessed was filed, and no proceeding incourt without assessment for the collection of such tax shall be begunafter the end of such period. In the case of any 6694(b) penalty, it may beassessed or a court proceeding for the collection may be begun withoutassessment at any time.

(2) Claim for refund. Except as provided in section 6694(d), anyrefund claim for an overpayment of any penalty…shall be filed within 3years from the time the penalty was paid.

(e) Definitions. [not the same as 7701(a)(36)]

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

24

25

Section 6696 Rules applicable to sections 6694, 6695 and 6695A [Regulations]

The IRS may, within the applicable period of limitations, credit anyamount of an overpayment by a TRP or appraiser of a penalty (or penalties) paidunder §6694 and Reg. §1.6694-1, under §6695 and Reg. §1.6695-1, or under§6695A (and any later issued regulations) against any outstanding liability forany tax (or for any interest, additional amount, addition to the tax, or assessablepenalty) owed by the TRP or appraiser making the overpayment. If a portion ofan overpayment was so credited, only the balance will be refunded to the TRP orappraiser. Reg. §1.6696-1(h).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

25

27

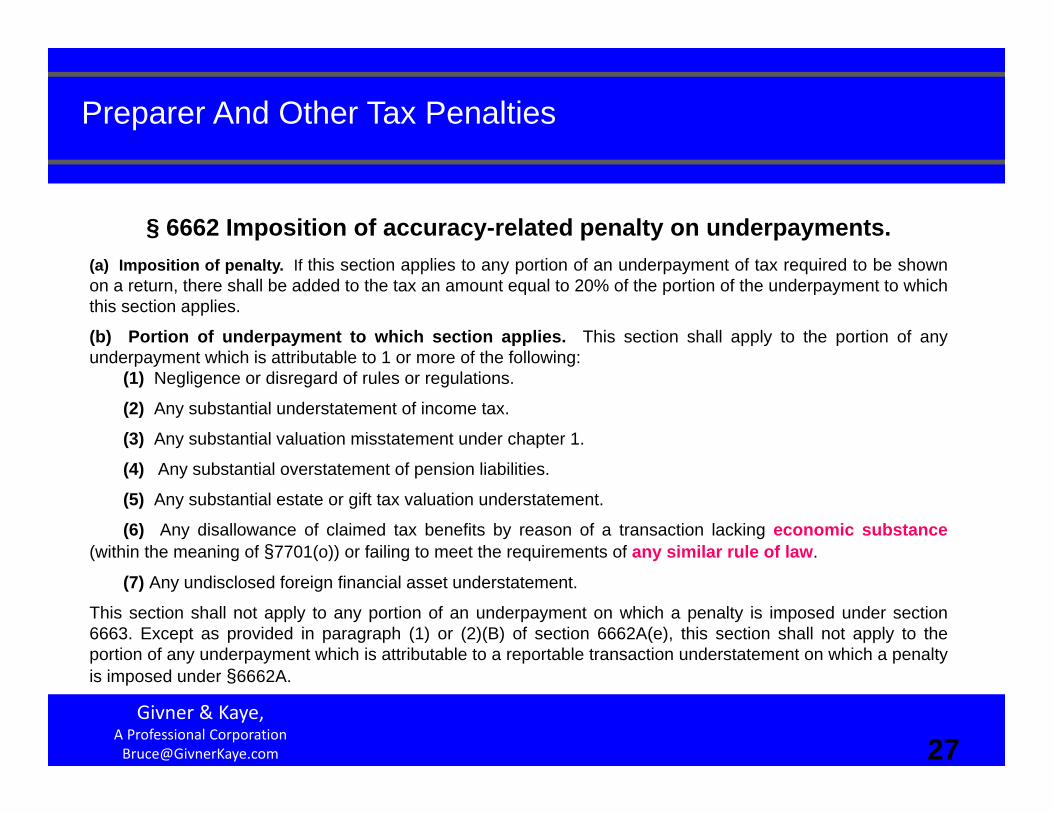

§ 6662 Imposition of accuracy-related penalty on underpayments.(a) Imposition of penalty. If this section applies to any portion of an underpayment of tax required to be shownon a return, there shall be added to the tax an amount equal to 20% of the portion of the underpayment to whichthis section applies.

(b) Portion of underpayment to which section applies. This section shall apply to the portion of anyunderpayment which is attributable to 1 or more of the following:

(1) Negligence or disregard of rules or regulations.

(2) Any substantial understatement of income tax.

(3) Any substantial valuation misstatement under chapter 1.

(4) Any substantial overstatement of pension liabilities.

(5) Any substantial estate or gift tax valuation understatement.

(6) Any disallowance of claimed tax benefits by reason of a transaction lacking economic substance(within the meaning of §7701(o)) or failing to meet the requirements of any similar rule of law.

(7) Any undisclosed foreign financial asset understatement.

This section shall not apply to any portion of an underpayment on which a penalty is imposed under section6663. Except as provided in paragraph (1) or (2)(B) of section 6662A(e), this section shall not apply to theportion of any underpayment which is attributable to a reportable transaction understatement on which a penaltyis imposed under §6662A.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

27

28

§ 6662 [continued].(c) Negligence. For purposes of this section, “negligence” includes any failure to make a reasonableattempt to comply with the provisions of this title, and “disregard” includes any careless, reckless, orintentional disregard.(d) Substantial understatement of income tax.

(1) Substantial understatement.—(A) In general. For purposes of this section, there is a substantial understatement of income tax

for any taxable year if the amount of the understatement for the taxable year exceeds the greater of—(i) 10 percent of the tax required to be shown on the return for the taxable year, or(ii) $5,000.

(B) Special rule for corporations. In the case of a corporation other than an S corporation or apersonal holding company (as defined in section 542), there is a substantial understatement of incometax for any taxable year if the amount of the understatement for the taxable year exceeds the lesser of—

(i) 10% of the tax required to be shown on the return for the taxable year (or, if greater,$10,000), or

(ii) $10,000,000.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

28

29

§ 6662 [continued].(2) Understatement.

(A) In general. For purposes of paragraph (1), “understatement” means the excess of—(i) the amount of the tax required to be shown on the return for the taxable year, over(ii) the amount of the tax imposed which is shown on the return, reduced by any rebate (within the

meaning of §6211(b)(2)).The excess under the preceding sentence shall be determined without regard to items to which §6662Aapplies.

(B) Reduction for understatement due to position of taxpayer or disclosed item. The amount of theunderstatement under subparagraph (A) shall be reduced by that portion of the understatement which isattributable to—

(i) the tax treatment of any item by the taxpayer if there is or was substantial authority for suchtreatment, or

(ii) any item if—(I) the relevant facts affecting the item's tax treatment are adequately disclosed in the return or

in a statement attached to the return, and(II) there is a reasonable basis for the tax treatment of such item by the taxpayer.

For purposes of clause (ii)(II), in no event shall a corporation be treated as having a reasonable basis for its taxtreatment of an item attributable to a multiple-party financing transaction if such treatment does not clearlyreflect the income of the corporation.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

29

30

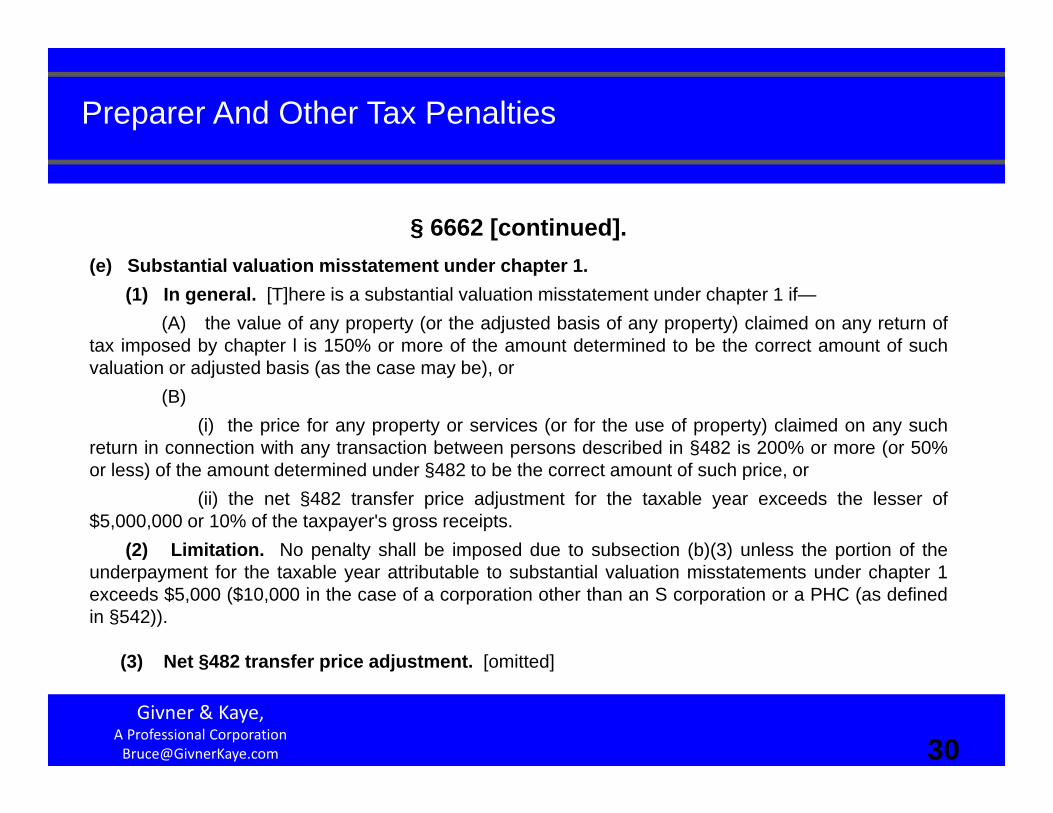

§ 6662 [continued].(e) Substantial valuation misstatement under chapter 1.

(1) In general. [T]here is a substantial valuation misstatement under chapter 1 if—(A) the value of any property (or the adjusted basis of any property) claimed on any return of

tax imposed by chapter l is 150% or more of the amount determined to be the correct amount of suchvaluation or adjusted basis (as the case may be), or

(B)(i) the price for any property or services (or for the use of property) claimed on any such

return in connection with any transaction between persons described in §482 is 200% or more (or 50%or less) of the amount determined under §482 to be the correct amount of such price, or

(ii) the net §482 transfer price adjustment for the taxable year exceeds the lesser of$5,000,000 or 10% of the taxpayer's gross receipts.

(2) Limitation. No penalty shall be imposed due to subsection (b)(3) unless the portion of theunderpayment for the taxable year attributable to substantial valuation misstatements under chapter 1exceeds $5,000 ($10,000 in the case of a corporation other than an S corporation or a PHC (as definedin §542)).

(3) Net §482 transfer price adjustment. [omitted]

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

30

31

§ 6662 [continued].(f) Substantial overstatement of pension liabilities. [omitted]

(g) Substantial estate or gift tax valuation understatement.

(1) In general. For purposes of this section, there is a substantial estate or gift tax valuationunderstatement if the value of any property claimed on any return of tax imposed by subtitle B is 65percent or less of the amount determined to be the correct amount of such valuation.

(2) Limitation. No penalty shall be imposed due to subsection (b)(5) unless the portion of theunderpayment attributable to substantial estate or gift tax valuation understatements for the taxableperiod (or, in the case of the tax imposed by chapter 11, as to the decedent’s estate) exceeds $5,000.

(h) Increase in penalty in case of gross valuation misstatements.

(1) In general. To the extent that a portion of the underpayment to which this section applies isattributable to one or more gross valuation misstatements, subsection (a) shall be applied to suchportion by substituting “40%” for “20%”.

(2) Gross valuation misstatements. [omitted]

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

31

32

§ 6662 [continued].(i) Increase in penalty in case of nondisclosed noneconomic substance transactions.

(1) In general. In the case of any portion of an underpayment which is attributable to one or morenondisclosed noneconomic substance transactions, subsection (a) shall be applied as to such portion bysubstituting “40%” for “20%”.

(2) Nondisclosed noneconomic substance transactions. …“nondisclosed noneconomicsubstance transaction” means any portion of a transaction described in subsection (b)(6) as to which therelevant facts affecting the tax treatment are not adequately disclosed in the return nor in a statementattached to the return.

(3) Special rule for amended returns. In no event shall any amendment or supplement to a returnof tax be taken into account for purposes of this subsection if the amendment or supplement is filed afterthe earlier of the date the taxpayer is first contacted by the Secretary regarding the examination of thereturn or such other date as is specified by the Secretary.

(j) Undisclosed foreign financial asset understatement. [omitted]

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

32

33

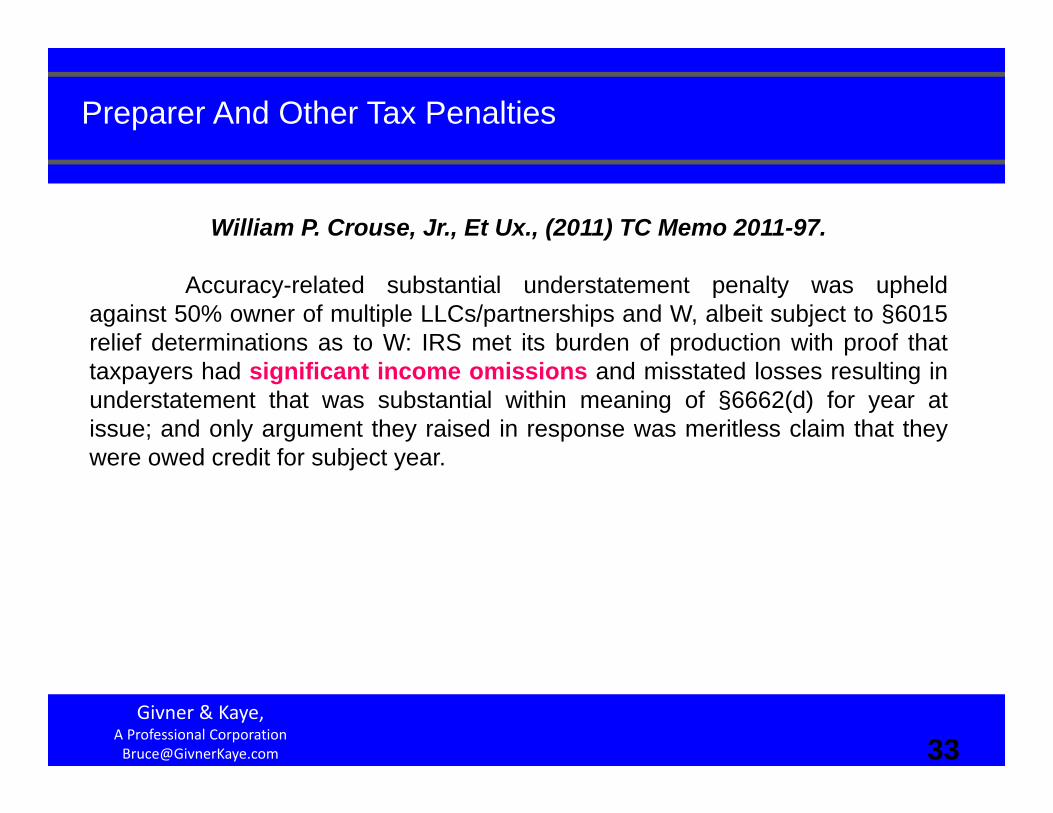

William P. Crouse, Jr., Et Ux., (2011) TC Memo 2011-97.

Accuracy-related substantial understatement penalty was upheldagainst 50% owner of multiple LLCs/partnerships and W, albeit subject to §6015relief determinations as to W: IRS met its burden of production with proof thattaxpayers had significant income omissions and misstated losses resulting inunderstatement that was substantial within meaning of §6662(d) for year atissue; and only argument they raised in response was meritless claim that theywere owed credit for subject year.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

33

34

Donald T. Robinson, Et Ux., (2011) TC Memo 2011-99.

Accuracy-related substantial understatement penalties were upheldagainst married couple/professor and marketing co. manager for years for whichthey claimed multiple unsubstantiated deductions: IRS met its burden ofproduction on penalties' applicability with proof that taxpayers hadunderstatements that were substantial within meaning of §6662(d)(1) for eachyear at issue; and they didn't offer any substantial authority or other groundsfor reducing understatements.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

34

35

Wadsworth v. Comm., (10/25/10, CA9) 106 AFTR 2d 2010-6879.

Tax Court properly upheld accuracy-related substantial understatementpenalties against partner and spouse for years for which they filed amendedreturns claiming refunds to which they weren't entitled: taxpayers' argument thatIRS failed to present any evidence of underpayments failed in face of facts thattheir refund claims led to underpayments, which in turn were due to substantialunderstatements on which §6662 penalties were based. And alternativearguments that §6662 penalties couldn't apply because understatements arosefrom refunds rather than returns or that §6676 vs. §6662 was proper statute forimposing penalties were misguided.

Also, taxpayers didn't explain why they disregarded longtimepreparer's advice to not amend returns, didn't show reasonable basis for theirposition, and didn't support or made insupportable claims about TEFRA issuesand deficiency notice invalidity.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

35

36

Khatchatour Akopian, Et Ux., (2011) TC Memo 2011-237.

Accuracy-related substantial understatement and negligence penaltieswere upheld against movie producer/investor and TRP who had unreportedincome from personal use of movie production/investment corps.' funds: IRS metits burden of production as to both substantial understatement and negligence;and taxpayers didn't address §6662(a) at trial or show reasonable cause fornegligence or underpayment.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

36

37

Frederick D. Todd, Ii, Et Ux., (2011) TC Memo 2011-123.

Accuracy-related penalty was upheld against neurosurgeon and W asto underpayment from H’s unreported welfare benefit fund distribution, whichhe improperly treated as nontaxable loan: IRS met its burden of production byshowing both that taxpayers' understatement was substantial within meaning of§6662(d) and that they negligently disregarded rules and regs, by failing to makereasonable attempt to ascertain correctness of distribution's treatment; and theyhad no reasonable cause for same.

Although they claimed reliance on CPA/return preparer, such wasunavailing absent evidence that CPA has some expertise in benefit plans, wasgiven all relevant information, and actually advised taxpayers on subjecttransaction.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

37

38

Weekend Warriors Trailers, Inc., Et Al., (2011) TC Memo 2011-105.

Accuracy-related negligence or substantial understatement penaltieswere largely upheld against solely owned travel trailer manufacturing S corp. andowner for years for which they misreported income and deductions; IRS met itsburden of production as to substantial understatement component of penalties asto both corp. and owner for all years save one, for which owner's understatementdidn't qualify as substantial under §6662(d); and, foregoing understatementaside, no reasonable cause or good faith excusing penalties was shown.

Although taxpayers did claim reliance on return preparers and otherbusiness/tax advisors, such wasn't sufficient to show reasonable cause orgood faith absent proof that advisors gave specific advice about pertinenttransactions or that preparers had background and justifying taxpayers'reliance. Also, preparers weren't given all relevant information.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

38

39

§ 6663 Imposition of fraud penalty.

(a) Imposition of penalty. If any part of any underpayment of tax required tobe shown on a return is due to fraud, there shall be added to the tax an amountequal to 75% of the portion of the underpayment which is attributable to fraud.

(b) Determination of portion attributable to fraud. If the Secretaryestablishes that any portion of an underpayment is attributable to fraud, theentire underpayment shall be treated as attributable to fraud, except with respectto any portion of the underpayment which the taxpayer establishes (by apreponderance of the evidence) is not attributable to fraud.

(c) Special rule for joint returns. In the case of a joint return, this sectionshall not apply with respect to a spouse unless some part of the underpayment isdue to the fraud of such spouse.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

39

40

Rick Fishman, (2011) TC Memo 2011-102.

A criminal investigation was began but dropped. Fraud penaltiesweren't upheld against ins. sales division leader for years for which he workedas independent contractor for sales assn. doing business through his soleproprietorship: IRS failed to prove that taxpayer even had any underpayments forstated years on which to base penalties. Rather, IRS based its determination onunsupported gross income recharacterization of reimbursements which taxpayerreceived for certain expense payments he made on behalf of othersalespersons/independent contractors and which evidence showed to be nothingmore than nontaxable loan repayments. Evidence included taxpayer's and othercontractors' contractor status and manner in which expenses were treated.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

40

41

William Norris, Et Ux., (2011) TC Memo 2011-161.

Fraud penalties were upheld against husband/welder for 1 of 2 years forwhich he and wife/bookkeeper operated gas station/convenience store and out ofwhich he ran illegal poker machine: IRS proved there was underpayment andhusband was estopped by his guilty plea to §7201 offense for that year fromdenying fraud. IRS didn't clearly prove fraud for 2d year. IRS showed some fraudfactors, including that H understated income and engaged in illegal activities as topoker machines, countervailing factors that he wasn't uncooperative, didn't try toconceal income, gave consistently credible testimony, and regularly dealt in cash aspart of normal business rather than in effort to avoid reporting requirements,outweighed fraud indicators. IRS failed to prove fraudulent intent on W’s part foreither year. IRS largely rested penalties against her on assumptions that she musthave known of H’s illegal poker machines and underreporting of gas station receipts,but even if she were aware of machines, that knowledge in itself didn't provefraudulent intent; moreover, she gave plausible explanation for underreportingmistake; and IRS failed to counter with any proof of intentionality.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

41

42

Charles L. Garavaglia, Et Ux., (2011) TC Memo 2011-228.

Fraud penalties were upheld against owner of consulting S corp. andother related businesses who used same in connection with scheme to defraudworker's compensation ins. cos. and Treas. Dept.: IRS proved owner hadunderpayments for each year, from unreported passthrough income, that wereattributable to fraud. Evidence included letters indicating owner knew payrollswere “scaled down” and worker's compensation liabilities were understated; heengaged in pattern of underreporting and instructed accountants to destroyrecords; he pled guilty to mail fraud and conspiracy offenses relating to subjectscheme; he engaged in and gave implausible and inconsistent behavior andexplanations; he tried to conceal his misdeeds from and didn't cooperate withCriminal Investigation Division; and he didn't file accurate returns.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

42

43

§6664 Definitions and special rules.

(a) Underpayment. For purposes of this part, “underpayment” means the amount bywhich any tax imposed by this title exceeds the excess of—

(1) the sum of—(A) the amount shown as the tax by the taxpayer on his return, plus(B) amounts not so shown previously assessed (or collected without

assessment), over(2) the amount of rebates made.

For purposes of paragraph (2), “rebate” means so much of an abatement, credit, refund, orother repayment, as was made on the ground that the tax imposed was less than theexcess of the amount specified in paragraph (1) over the rebates previously made.(b) Penalties applicable only where return filed. The penalties provided in this partshall apply only in cases where a return of tax is filed (other than a return prepared by theSecretary under the authority of §6020(b)).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

43

44

§6664 Definitions and special rules [continued].

(c) Reasonable cause exception for underpayments.(1) In general. No penalty shall be imposed under §6662 or 6663 as to any portion of an

underpayment if it is shown that there was a reasonable cause for such portion and that the taxpayeracted in good faith with respect to such portion.

(2) Exception. Paragraph (1) shall not apply to any portion of an underpayment which isattributable to one or more transactions described in §6662(b)(6).

(3) Special rule for certain valuation overstatements. In the case of any underpaymentattributable to a substantial or gross valuation overstatement under chapter 1 with respect to charitablededuction property, paragraph (1) shall not apply. The preceding sentence shall not apply to asubstantial valuation overstatement under chapter 1 if—

(A) the claimed value of the property was based on a qualified appraisal made by a qualifiedappraiser, and

(B) in addition to obtaining such appraisal, the taxpayer made a good faith investigation ofthe value of the contributed property.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

44

45

§6664 Definitions and special rules [continued].

(4) Definitions. For purposes of this subsection —

(A) Charitable deduction property. The term “charitable deduction property”means any property contributed by the taxpayer in a contribution for which adeduction was claimed under §170. For purposes of paragraph (3), such termshall not include any securities for which (as of the date of the contribution)market quotations are readily available on an established securities market.

(B) Qualified appraisal. The term “qualified appraisal” has the meaninggiven such term by §170(f)(11)(E)(i).

(C) Qualified appraiser. The term “qualified appraiser” has the meaninggiven such term by §170(f)(11)(E)(ii).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

45

46

§6664 Definitions and special rules [continued]. (d) Reasonable cause exception for reportable transaction understatements.

(1) In general. No penalty shall be imposed under section 6662A as to any portion of a reportabletransaction understatement if it is shown that there was a reasonable cause for such portion and thatthe taxpayer acted in good faith with respect to such portion.

(2) Exception. Paragraph (1) shall not apply to any portion of a reportable transactionunderstatement which is attributable to one or more transactions described in §6662(b)(6).

(3) Special rules. Paragraph (1) shall not apply to any reportable transaction understatementunless—

(A) the relevant facts affecting the tax treatment of the item are adequately disclosed inaccordance with the regulations prescribed under section 6011,

(B) there is or was substantial authority for such treatment, and(C) the taxpayer reasonably believed that such treatment was more likely than not the proper

treatment.A taxpayer failing to adequately disclose in accordance with section 6011 shall be treated as meeting therequirements of subparagraph (A) if the penalty for such failure was rescinded under §6707A(d).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

46

47

§ 6664 Definitions and special rules [continued]. (4) Rules relating to reasonable belief. For purposes of paragraph (3)(C) —

(A) In general. A taxpayer shall be treated as having a reasonable belief with respect to the taxtreatment of an item only if such belief—

(i) is based on the facts and law that exist at the time the return of tax which includes such taxtreatment is filed, and

(ii) relates solely to the taxpayer's chances of success on the merits of such treatment anddoes not take into account the possibility that a return will not be audited, such treatment will not beraised on audit, or such treatment will be resolved through settlement if it is raised.

(B) Certain opinions may not be relied upon.

(i) In general. An opinion of a tax advisor may not be relied upon to establish the reasonablebelief of a taxpayer if—

(I) the tax advisor is described in clause (ii) , or

(II) the opinion is described in clause (iii) .

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

47

48

§ 6664 Definitions and special rules [continued]. (ii) Disqualified tax advisors. A tax advisor is described in this clause if the tax advisor—

(I) is a material advisor (within the meaning of §6111(b)(1)) and participates in the organization,management, promotion, or sale of the transaction or is related (within the meaning of §267(b) or707(b)(1)) to any person who so participates,

(II) is compensated directly or indirectly by a material advisor as to the transaction,(III) has a fee arrangement as to the transaction which is contingent on all or part of the intended

tax benefits from the transaction being sustained, or(IV) as determined under regulations prescribed by the Secretary, has a disqualifying financial

interest with respect to the transaction.(iii) Disqualified opinions. For purposes of clause (i) , an opinion is disqualified if the opinion—

(I) is based on unreasonable factual or legal assumptions (including assumptions as to futureevents),

(II) unreasonably relies on representations, statements, findings, or agreements of the taxpayeror any other person,

(III) does not identify and consider all relevant facts, or(IV) fails to meet any other requirement as the Secretary may prescribe.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

48

49

What Good Can A Tax Opinion Do?The IRS effective recognizes five levels of

(i) Frivolous.

(ii) Colorable.

(iii) Reasonable Basis.

(iv) Substantial Authority.

(v) More Likely Than Not.

If the taxpayer’s position on the return is either Frivolous or Colorable, the taxpayer should beprepared to be hit with an accuracy-related penalty. Similarly, the tax return preparer who signs thereturn should assume that he or she will be hit with the IRC Section 6694 preparer penalty.

By contrast, if the taxpayer’s position has a Reasonable Basis – generally viewed as having a 20%to 1/3rd chance of prevailing on the merits – then the position should not be penalized as long as theposition is disclosed on an IRS Form 8275 or 8275-R attached to the return.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

49

50

What Good Can A Tax Opinion Do?If the taxpayer’s position has Substantial Authority – generally viewed as having a 40% or

greater chance of prevailing on the merits – then the taxpayer should not be subject to the accuracy-related penalty even in the absence of disclosure.

Of course Nirvana is to have a position that is More Likely Than Not going to prevail on themerits.

One problem is: how do you know what the chances are that a taxpayer’s position willprevail on the merits? One answer is to have an opinion written by a tax lawyer (some CPAs will alsoprepare opinion letters). Of course, the fact that the taxpayer possesses such a letter does not insulatethe taxpayer from a penalty since there is no guaranty that the IRS (and the FTB) will agree. However,depending upon the dollars involved in a potential penalty and the cost of the opinion letter, this is oftenan attractive expenditure.

There are many concerns about the creation of an opinion letter, e.g., that it must be firmlybased on the taxpayer’s actual facts, not suppositions about intent; that is must be grounded in theInternal Revenue Code; regulations; rulings; case law; and other independent authority. And, of course,the opinion letter writer must not have a contingent interest in the outcome.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

50

55

§ 6700 Promoting abusive tax shelters, etc.(a) Imposition of penalty. Any person who –

(1)

(A) organizes (or assists in the organization of –

(i) a partnership or other entity,

(ii) any investment plan or arrangement, or

(iii) any other plan or arrangement, or

(B) participates (directly or indirectly) in the same of any interest in an entity or plan orarrangement referred to in subparagraph (A), and

(2) makes or furnishes or causes another person to make or furnish (in connection with suchorganization or sale -

(A) a statement with respect to the allowability of any deduction or credit, the excludabilityof any income, or the securing of any other tax benefit by reason of holding an interest in the entity orparticipating in the plan or arrangement which the person knows or has reason to know is false orfraudulent as to any material matter, or

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

55

56

§ 6700 Promoting abusive tax shelters, etc. [continued](B) gross valuation overstatement as to any material matter,

shall pay, as to each activity described in paragraph (1), a penalty equal to $1,000 or, if the personestablishes that it is lesser, 100% of the gross income derived (or to be derived) by such person fromsuch activity. …activities described in paragraph (1)(A) as to each entity or arrangement shall be treatedas a separate activity and participation in each sale described in paragraph (1)(B) shall be so treated.

Despite the first sentence, if an activity as to which a penalty imposed under this subsection involves astatement described in paragraph (2)(A), the amount of the penalty shall be equal to 50% of the grossincome derived (or to be derived) from such activity by the person on which the penalty is imposed.

(b) Rules relating to penalty for gross valuation overstatements. …

(c) Penalty in addition to other penalties. The penalty imposed by this section shall be in addition toany other penalty imposed by law.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

56

57

In Re: Settles, Sr., (2011, Bktcy Ct TN) 107 AFTR 2d 2011-2552.

Taxpayer/attorney-CPA/tax scheme promoter's liabilities for back taxes,penalties and interest: he was collaterally estopped by prior disbarmentproceedings from seeking abatement of §6700 and 6662 penalties. Taxpayerhad been given opportunity to litigate penalties issues during disbarmentproceedings; those issues were central to disbarment; and decision and itsaffirmance on appeal comprised final judgment on merits. Argument thattaxpayer was denied due process in those proceedings because he couldn'tafford to hire counsel to represent him was meritless. To extent he was seekingabatement of §6662 penalties on grounds of substantial authority for his taxshelter, his position was meritless since there was no such authority. No validclaim for abatement of additional §6651(a) failure to pay penalties whenconsidering that he had substantial income at his disposal and used same fordiscretionary items at time he was obligated, but failed, to pay taxes.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

57

58

U.S. v. Sommerstedt, (2011, CA6) 107 AFTR 2d 2011-2422.

District court summary judgment decision to permanently enjoin prose TRP from promoting, organizing and selling abusive tax evasion and shelterproducts was affirmed in part and vacated and remanded in part. Court wascorrect insofar as finding that TRP failed to raise material fact issue as towhether tax avoidance plans that he promoted constituted conduct subject topenalty under §6700. TRP improperly invoked his 5th Amendment privilegeagainst self-incrimination as to requirement that he notify clients ofinjunction. However, court erred in compelling TRP to provide govt. withclient list as such could lead to incriminating evidence in laterinvestigation.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

58

59

U.S. v. Boone, (2011, DC FL) 107 AFTR 2d 2011-2385.

Abusive tax scheme promoter/TRP and those acting with him werepermanently enjoined from preparing or giving advice about Form 1099-OIDor other tax forms, owning or operating any website that participates inpreparing false documents, promoting tax shelters or abusive arrangementsincluding abusive Form 1099-OID scheme, posting any scheme-related materialon any website, and engaging in other activity that was subject to penalty under§6700, et seq. or that otherwise interfered with tax law administration. TRP wasalso barred from making any false Form 1099-OID claims on his own returnsand was ordered to provide clients with injunction copy.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

59

60

§ 6701 Penalties for aiding and abetting understatement of tax liability.

(a) Imposition of penalty. Any person –

(1) who aids or assists in, procures, or advises as to, the preparation or presentationof any portion of a return, affidavit, claim or other document,

(2) who knows (or has reason to believe) that such portion will be used inconnection with any material matter arising under the internal revenue laws, and

(3) who knows that such portion (if so used) would result in an understatement ofthe liability for tax of another person,

shall pay a penalty as to each document in the amount determined under subsection (b).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

60

61

§ 6701 Penalties for aiding and abetting understatement of tax liability.[continued]

(b) Amount of penalty.

(1) In general. Except as provided in paragraph (2), the amount of the penaltyimposed by subsection (a) shall be $1,000.

(2) Corporations. If the return, affidavit, claim or other document relates to the taxliability of a corporation, the amount of the penalty imposed by (a) shall be $10,000.

(3) Only 1 penalty per person per period. If any person is subject to a penalty under(a) with respect to any document relating to any taxpayer for any taxable period (or wherethere is no taxable period, any taxable event), such person shall not be subject to a penaltyunder subsection (a) with respect to any other document relating to such taxpayer for suchtaxable period (or event).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

61

62

§ 6701 Penalties for aiding and abetting understatement of tax liability.[continued]

(c) Activities of subordinates.

(1) In general. For purposes of (a), the term “procures” includes –

(A) ordering (or otherwise causing) a subordinate to do an act, and

(B) knowing of, and not trying to prevent, participation by a subordinate in an act.

(2) Subordinates. For purposes of paragraph (1), “subordinate” means any otherperson (whether or not a director, officer, employee, or agent of the taxpayer involved) overwhose activities the person has direction, supervision or control.

(d) Taxpayer not required to have knowledge. Subsection (a) shall apply whether or notthe understatement is with the knowledge or consent of the persons authorized or requiredto present the return, affidavit, claim, or other document.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

62

63

§ 6701 Penalties for aiding and abetting understatement of tax liability.[continued]

(e) Certain actions not treated as aid or assistance. For purposes of (a)(1), a personfurnishing typing, reproducing, or other mechanical assistance as to a document shall notbe treated as having aided or assisted in the preparation of the document due to suchassistance.

(f) Penalty in addition to other penalties.

(1) In General. Except as provided in (2) and (3), the penalty imposed by thissection shall be in addition to any other penalty provided by law.

(2) Coordination with return preparer penalties. No penalty shall be assessedunder 6694(a) or (b) on any person as to any document for which a penalty is assessed onsuch person under subsection (a).

(3) Coordination with section 6700. No penalty shall be assessed under §6700on any person as to any document for which a penalty is assessed on such person undersubsection (a).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

63

64

U.S. v. William Alexander, (2011, DC CA) 107 AFTR 2d 2011-1793.

Final judgment of permanent injunction was entered against tax schemepromoter and those acting with him from selling or promoting abusive schemessuch as described welfare benefit scheme, making false statements aboutdeductions, providing tax advice about pension or welfare benefit plans,engaging in other conduct subject to penalty under §6700 or 6701, preparingreturns for fee, and representing others before IRS.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

64

65

§ 6702 Frivolous tax submissions.

(a) Civil penalty for frivolous tax returns. A person shall pay a penalty of $5,000 if –

(1) such person files what purports to be a return of a tax imposed by this title butwhich

(A) does not contain information on which the substantial correctness of the self-assessment may be judged, or

(B) contains information that on its face indicates that the self-assessment issubstantially incorrect, and,

(2) the conduct referred to in paragraph (1) –

(A) is based on a position which the Secretary has identified as frivolous undersubsection (c), or

(B) reflects a desire to delay or impede the administration of Federal tax laws.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

65

66

§ 6702 Frivolous tax submissions [continued].

(b) Civil penalty for specified frivolous submissions.

(1) Imposition of penalty. Except as provided in paragraph (3), any person whosubmits a specified frivolous submission shall pay a penalty of $5,000.

(2) Specified frivolous submission. For purposes of this section –

(A) Specified Frivolous Submission. The term “specified frivolous submission”means a specified submission if any portion of such submission –

(i) is based on a position which the Secretary has identified as frivolousunder subsection (c), or

(ii) reflects a desire to delay or impede the administration of Federal taxlaws.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

66

67

§ 6702 Frivolous tax submissions [continued].

(B) Specified submission. The term “specified submission” means –

(i) a request for a hearing under –

(I) §6320 (relating to notice and opportunity for hearing upon filing of notice of lien),or

(II) §6330 (relating to notice and opportunity for hearing before levy), and

(ii) an application under –

(I) §6159 (relating to agreements for payment of tax liability in installments),

(II) §7122 (relating to compromises), or

(III) §7811 (relating to taxpayer assistance orders).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

67

68

§ 6702 Frivolous tax submissions [continued].

(3) Opportunity to withdraw submission. If the Secretary provides a person withnotice that a submission is a specified frivolous submission and such person withdraws suchsubmission within 30 days after such notice, the penalty imposed under paragraph (1) shallnot apply with respect to such submission.

(c) Listing of frivolous positions. The Secretary shall prescribe (and periodically revise) alist of positions which the Secretary has identified as being frivolous for purposes of thissubsection. The Secretary shall not include in such list any position that the Secretarydetermines meets the requirement of §6662(d)(2)(B)(ii)(II).

(d) Reduction of penalty. The Secretary may reduce the amount of any penalty imposedunder this section if the Secretary determines that such reduction would promote compliancewith and administration of the Federal tax laws.

(e) Penalties in addition to other penalties. The penalties imposed by this section shall bein addition to any other penalty provided by law.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

68

69

Notice 2010-33, 2010-17 (4/07/2010)Identifies 46 frivolous positions, with 21 subparts, including:(6) A taxpayer has been untaxed, detaxed, or removed or redeemed from the Federal tax systemthough the taxpayer remains a United States citizen or resident, or similar arguments described asfrivolous in Rev. Rul. 2004-31, 2004-1 C.B. 617.

(10) A taxpayer is not a “person” within the meaning of Section 7701(a)(14) or other provisions of theInternal Revenue Code, or similar arguments described as frivolous in Rev. Rul. 2007-22, 2007-1 C.B.866.

(12) Federal Reserve Notes are not taxable income when paid to a taxpayer because they are not goldor silver and may not be redeemed for gold or silver.

(33) A Notice of Federal Tax Lien is invalid because it is not signed by a particular official (such as by theSecretary of the Treasury), or because it was filed by someone without delegated authority.

(45) The Service is not an agency of the United States government but rather a private-sectorcorporation or an agency of a State or Territory without authority to administer the internal revenue laws.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

69

70

California Revenue and Taxation Code Section 19179

(a) A penalty shall be imposed for filing a frivolous return and shall be determinedin accordance with §6702 of the Internal Revenue Code, except as otherwiseprovided.

(b) §6702 of the Internal Revenue Code shall be applied to returns required to befiled under this part.

(c) §6702 of the Internal Revenue Code is modified as follows:

…

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

70

71

Minor L. McNeil, (2011) TC Memo 2011-150.

IRS's administrative determination to proceed with collection of §6702penalties for years for which nurse filed zero returns was upheld. Penaltiesliability was shown by evidence that taxpayer's purported returns were based onfrivolous protester-type arguments that he had been warned against makingand that returns lacked sufficient information for IRS to be able to judgesubstantial correctness of self-assessments thereon. And collectiondetermination was supported by evidence that appeals officer complied with all§6330 CDP requirements, including requirement to verify that all applicable legaland administrative requirements were met and that levy balanced IRS's efficientcollection needs against taxpayer's intrusiveness concerns.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

71

72

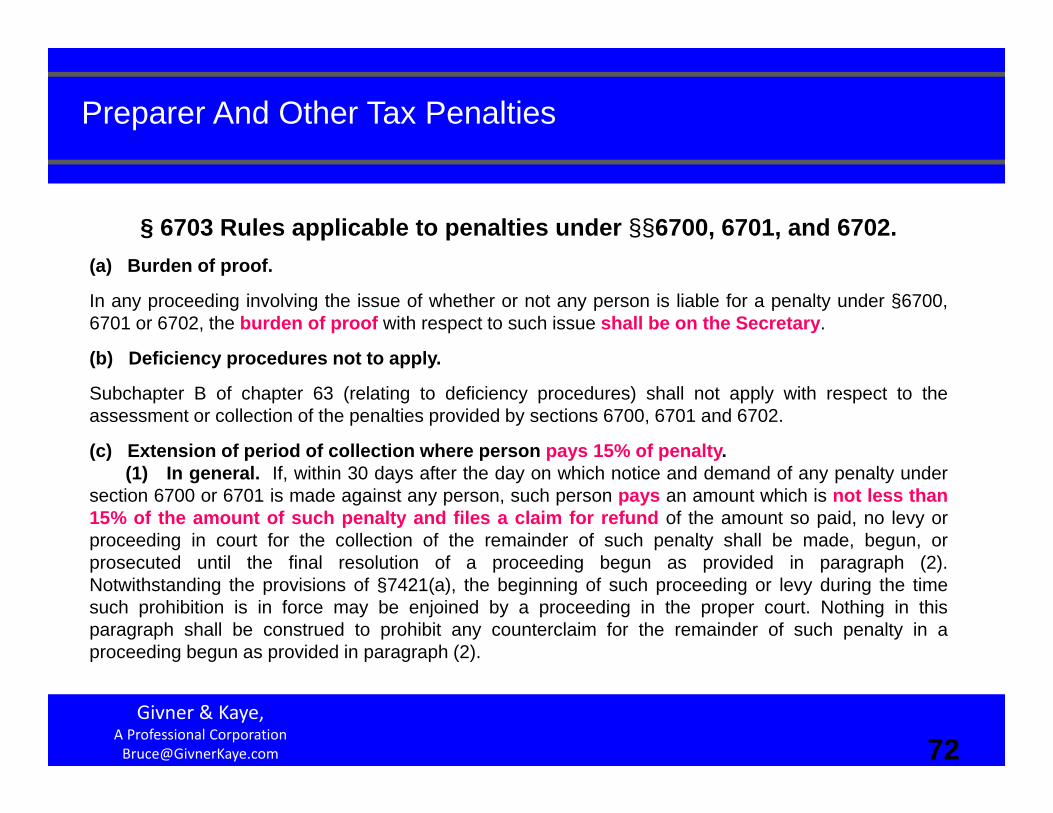

§ 6703 Rules applicable to penalties under §§6700, 6701, and 6702.(a) Burden of proof.

In any proceeding involving the issue of whether or not any person is liable for a penalty under §6700,6701 or 6702, the burden of proof with respect to such issue shall be on the Secretary.

(b) Deficiency procedures not to apply.

Subchapter B of chapter 63 (relating to deficiency procedures) shall not apply with respect to theassessment or collection of the penalties provided by sections 6700, 6701 and 6702.

(c) Extension of period of collection where person pays 15% of penalty.(1) In general. If, within 30 days after the day on which notice and demand of any penalty under

section 6700 or 6701 is made against any person, such person pays an amount which is not less than15% of the amount of such penalty and files a claim for refund of the amount so paid, no levy orproceeding in court for the collection of the remainder of such penalty shall be made, begun, orprosecuted until the final resolution of a proceeding begun as provided in paragraph (2).Notwithstanding the provisions of §7421(a), the beginning of such proceeding or levy during the timesuch prohibition is in force may be enjoined by a proceeding in the proper court. Nothing in thisparagraph shall be construed to prohibit any counterclaim for the remainder of such penalty in aproceeding begun as provided in paragraph (2).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

72

73

§ 6703 Rules applicable to penalties under §§6700, 6701, and 6702.[continued]

(2) Person must bring suit in district court to determine his liability for penalty.If, within 30 days after the day on which his claim for refund of any partial payment of anypenalty under §6700 or 6701 is denied (or, if earlier, within 30 days after the end of 6months after the day on which he filed the claim for refund), the person fails to begin aproceeding in the appropriate U.S. district court for the determination of his liability for suchpenalty, paragraph (1) shall cease to apply as to the penalty, effective on the day after theclose of the applicable 30-day period referred to in this paragraph.

(3) Suspension of running of period of limitations on collection.The running of the period of limitations provided in §6502 on the collection by levy or by aproceeding in court in respect of any penalty described in paragraph (1) shall besuspended for the period during which the Secretary is prohibited from collecting by levy ora proceeding in court.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

73

74

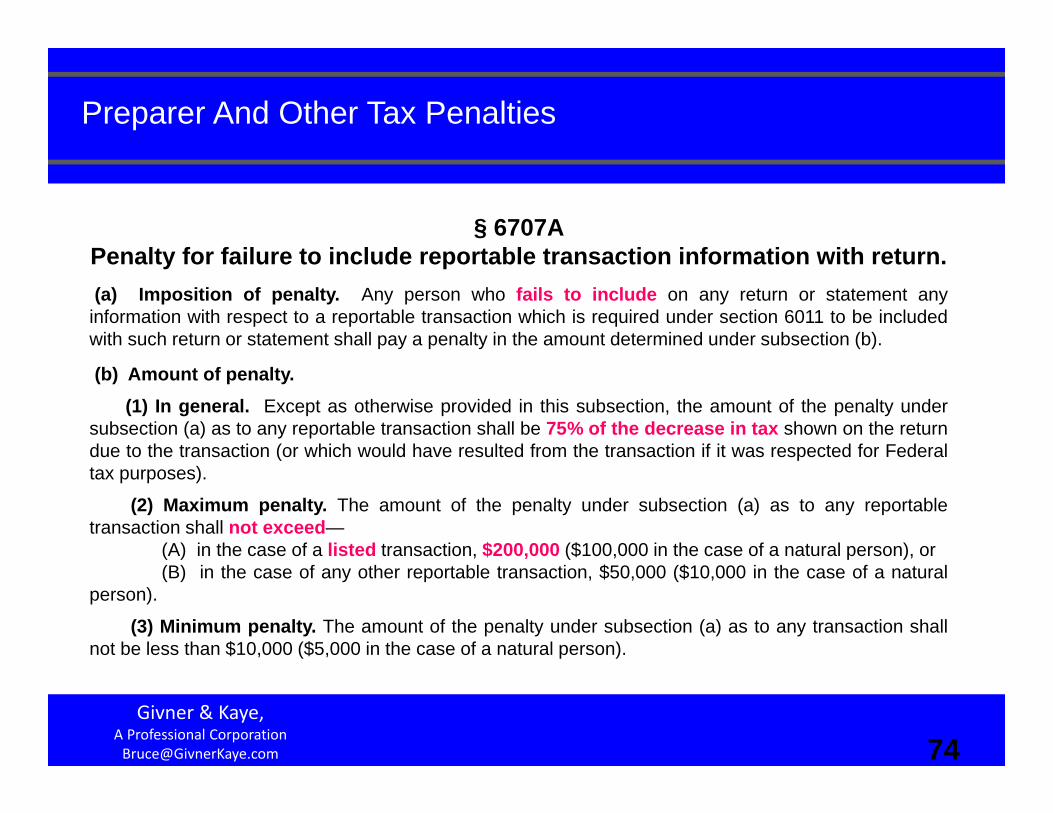

§ 6707A Penalty for failure to include reportable transaction information with return.(a) Imposition of penalty. Any person who fails to include on any return or statement any

information with respect to a reportable transaction which is required under section 6011 to be includedwith such return or statement shall pay a penalty in the amount determined under subsection (b).

(b) Amount of penalty.(1) In general. Except as otherwise provided in this subsection, the amount of the penalty under

subsection (a) as to any reportable transaction shall be 75% of the decrease in tax shown on the returndue to the transaction (or which would have resulted from the transaction if it was respected for Federaltax purposes).

(2) Maximum penalty. The amount of the penalty under subsection (a) as to any reportabletransaction shall not exceed—

(A) in the case of a listed transaction, $200,000 ($100,000 in the case of a natural person), or(B) in the case of any other reportable transaction, $50,000 ($10,000 in the case of a natural

person).

(3) Minimum penalty. The amount of the penalty under subsection (a) as to any transaction shallnot be less than $10,000 ($5,000 in the case of a natural person).

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

74

75

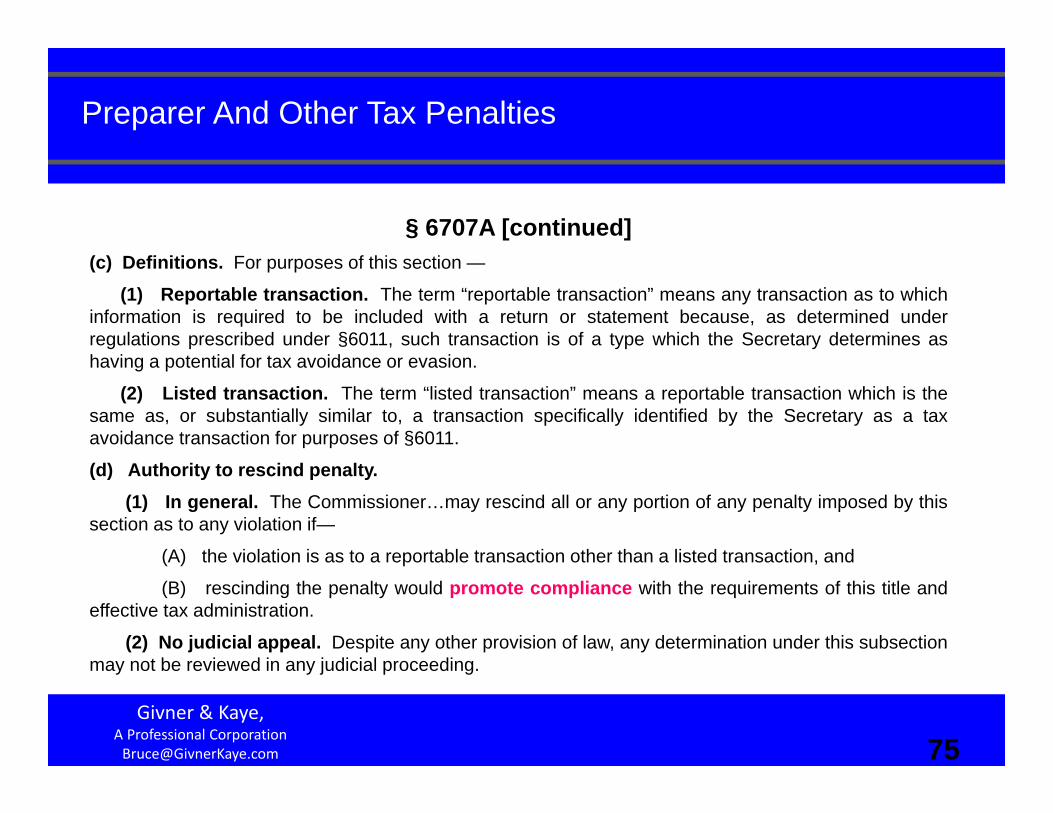

§ 6707A [continued](c) Definitions. For purposes of this section —

(1) Reportable transaction. The term “reportable transaction” means any transaction as to whichinformation is required to be included with a return or statement because, as determined underregulations prescribed under §6011, such transaction is of a type which the Secretary determines ashaving a potential for tax avoidance or evasion.

(2) Listed transaction. The term “listed transaction” means a reportable transaction which is thesame as, or substantially similar to, a transaction specifically identified by the Secretary as a taxavoidance transaction for purposes of §6011.

(d) Authority to rescind penalty.(1) In general. The Commissioner…may rescind all or any portion of any penalty imposed by this

section as to any violation if—

(A) the violation is as to a reportable transaction other than a listed transaction, and

(B) rescinding the penalty would promote compliance with the requirements of this title andeffective tax administration.

(2) No judicial appeal. Despite any other provision of law, any determination under this subsectionmay not be reviewed in any judicial proceeding.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

75

76

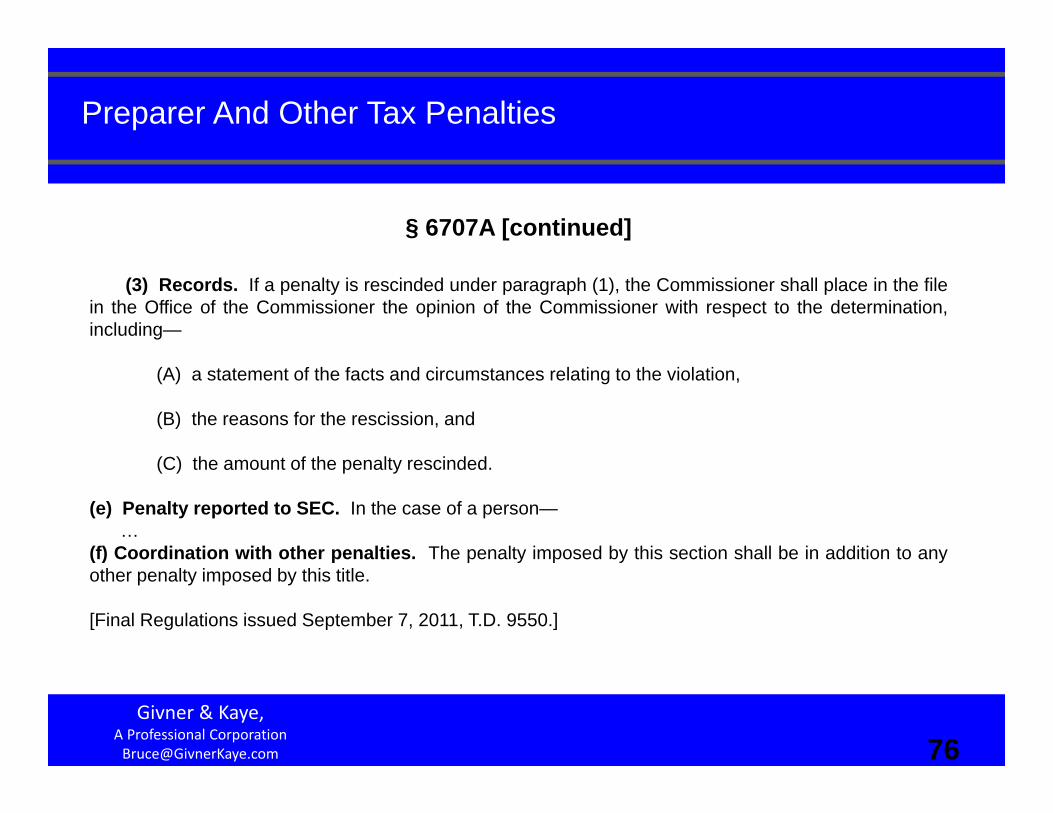

§ 6707A [continued]

(3) Records. If a penalty is rescinded under paragraph (1), the Commissioner shall place in the filein the Office of the Commissioner the opinion of the Commissioner with respect to the determination,including—

(A) a statement of the facts and circumstances relating to the violation,

(B) the reasons for the rescission, and

(C) the amount of the penalty rescinded.

(e) Penalty reported to SEC. In the case of a person—…

(f) Coordination with other penalties. The penalty imposed by this section shall be in addition to anyother penalty imposed by this title.

[Final Regulations issued September 7, 2011, T.D. 9550.]

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

76

77

Mcgehee Family Clinic, P.A., Et Al., (2010) TC Memo 2010-202.

§6662A penalties were upheld against family clinic and shareholder and spousein respect to understatements arising from their engagement in multiemployer welfarebenefit trust transaction that promised virtually unlimited deductions: IRS met itsburden of production on penalties' general applicability with proof that transaction wasfactually similar to that identified in Notice 95-34, and thus listed transaction under§6707A(c)(2), and that clinic and shareholder both claimed improper tax treatment ofitems/deductions and income omissions attributable thereto; IRS further showedapplicability of enhanced 30% penalty as against clinic with proof that it didn't attach toreturn disclosure statement described in Reg § 1.6011-4T(c); and taxpayers didn'tprovide credible evidence to support their claims to contrary. Also, constitutionalarguments that penalties were effectively being imposed retroactively without fair warningand in violation of taxpayers' due process rights were belied by facts that penalties wereimposed for tax years ending after §6662A’s effective date; and contrary to their claims,IRS wasn't obligated to give taxpayers warning or “personalized notice” of same.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

77

78

§ 6713 Disclosure or use of information by preparers of returns.

(a) Imposition of penalty. If any person who is engaged in the business of preparing or providingservices in connection with the preparation of, returns of tax imposed by chapter 1, or any person whofor compensation prepares any such return for any other person, and who—

(1) discloses any information furnished to him for, or in connection with, the preparation of anysuch return, or

(2) uses any such information for any purpose other than to prepare, or assist in preparing,any such return,

shall pay a penalty of $250 for each such disclosure or use, but the total amount imposed under thissubsection on such a person for any calendar year shall not exceed $10,000.

(b) Exceptions. The rules of §7216(b) shall apply for purposes of this section.

(c) Deficiency procedures not to apply. Subchapter B of chapter 63 (relating to deficiencyprocedures for income, estate, gift, and certain excise taxes) shall not apply in respect of theassessment or collection of any penalty imposed by this section.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

78

79

Rev. Rul. 2010-4.

Use of return information by TRPs to contact taxpayers to inform themof tax law change or issuance of new temporary regs that might affect liability onpreviously filed returns or future reasonably anticipated accounting serviceswon't subject preparers to penalties under §6713 or 7216. Nor will penaltiesapply to situations where preparer discloses return information (as limited toinformation listed in Reg. §301.7216-2(n)) to 3rd party service provider whoprovides educational information on general business and economic matters topublic for purposes of soliciting more work for tax preparers.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

79

80

§7201 Attempt to evade or defeat tax.

Any person who willfully attempts in any manner to evade or defeat anytax imposed by this title or the payment thereof shall, in addition to otherpenalties provided by law, be guilty of a felony and, upon conviction thereof,shall be fined not more than $100,000 ($500,000 in the case of a corporation), orimprisoned not more than 5 years, or both, together with the costs ofprosecution.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

80

81

U.S. v. Ganias, (2011, DC CT) 108 AFTR 2d 2011-5851.

Taxpayer-former IRS agent/return preparation business owner wasdenied motion for judgment of acquittal on charges he willfully tried to evade hispersonal income tax liabilities for certain years by filing false returns: convictionwas sufficiently supported by evidence that taxpayer's failure to reportsignificant income on subject returns wasn't simple mistake resulting frominnocent reliance on profit and loss statement that he didn't realize was incorrect,but rather part of larger pattern of willful evasion. Evidence included facts thattaxpayer was experienced in tax matters and recordkeeping, yet underreportedhis income both in stated years and before. There was also evidence that he hadpreviously used accounting records/accounting entries in manner that allowedpayments to not show up as income.

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

81

82

§7206 Fraud and false statements.

Any person who—

(1) Declaration under penalties of perjury. Willfully makes and subscribes any return, statement, orother document, which contains or is verified by a written declaration that it is made under the penaltiesof perjury, and which he does not believe to be true and correct as to every material matter; or

(2) Aid or assistance. Willfully aids or assists in, or procures, counsels, or advises the preparation orpresentation under, or in connection with any matter arising under, the internal revenue laws, of areturn, affidavit, claim, or other document, which is fraudulent or is false as to any material matter,whether or not such falsity or fraud is with the knowledge or consent of the person authorized orrequired to present such return, affidavit, claim, or document; or

(3) Fraudulent bonds, permits, and entries. Simulates or falsely or fraudulently executes or signsany bond, permit, entry, or other document required by the provisions of the internal revenue laws,or by any regulation made in pursuance thereof, or procures the same to be falsely or fraudulentlyexecuted, or advises, aids in, or connives at such execution thereof; or

Givner & Kaye, A Professional [email protected]

Preparer And Other Tax Penalties

82

83

§7206 Fraud and false statements [continued].

(4) Removal or concealment with intent to defraud. Removes, deposits, or conceals, or isconcerned in removing, depositing, or concealing, any goods or commodities for or in respect whereofany tax is or shall be imposed, or any property upon which levy is authorized by §6331, with intent toevade or defeat the assessment or collection of any tax imposed by this title; or

(5) Compromises and closing agreements. In connection with any compromise under §7122, or offerof such compromise, or in connection with any closing agreement under §7121, or offer to enter into anysuch agreement, willfully—

(A) Concealment of property. Conceals from any officer or employee of the United States anyproperty belonging to the estate of a taxpayer or other person liable in respect of the tax, or