Embed Size (px)

Citation preview

1

Concentration in the media industry:

drivers and quantitative analysis

The case of the French media industry

The case of the French Television

The case of the French Telecommunications

Paper, International Seminar on the Media,

Columbia University, New-York, March 2010

P.-Y. Badillo et J.B. Lesourd

IRSIC, Université de la Méditerranée, Marseille, France

�� Version non définitive, ne doit pas être Version non définitive, ne doit pas être citée. / citée. / Draft version, should not be quoted.Draft version, should not be quoted.

INTRODUCTION

2

Bibliography

• Forthcoming:

• P.Y. Badillo and J.B. Lesourd (Editors), The

Media Industries and their Markets.

Quantitaive Studies. Palgrave-MacMIllan,

London, forthcoming 2010.

INTRODUCTION

• Globalisation

• New technologies

• New regulation

3

A new environment

• No frontiers

• A meltdown industry

Technology and media concentration in France

• New entrant (which controls ICT): Lagardère/

Hachette; Dassault/ Socpresse

• Media concentration: press freedom and free

markets?

4

Organisation of the presentation

*MARKET POWER, DIVERSITY AND THEIR

MEASUREMENTS

*THE CASE OF THE FRENCH PRESS

*THE CASE OF THE FRENCH TV

CONCENTRATION IN THE MEDIA:

MARKET POWER, DIVERSITY AND

THEIR MEASUREMENTS

5

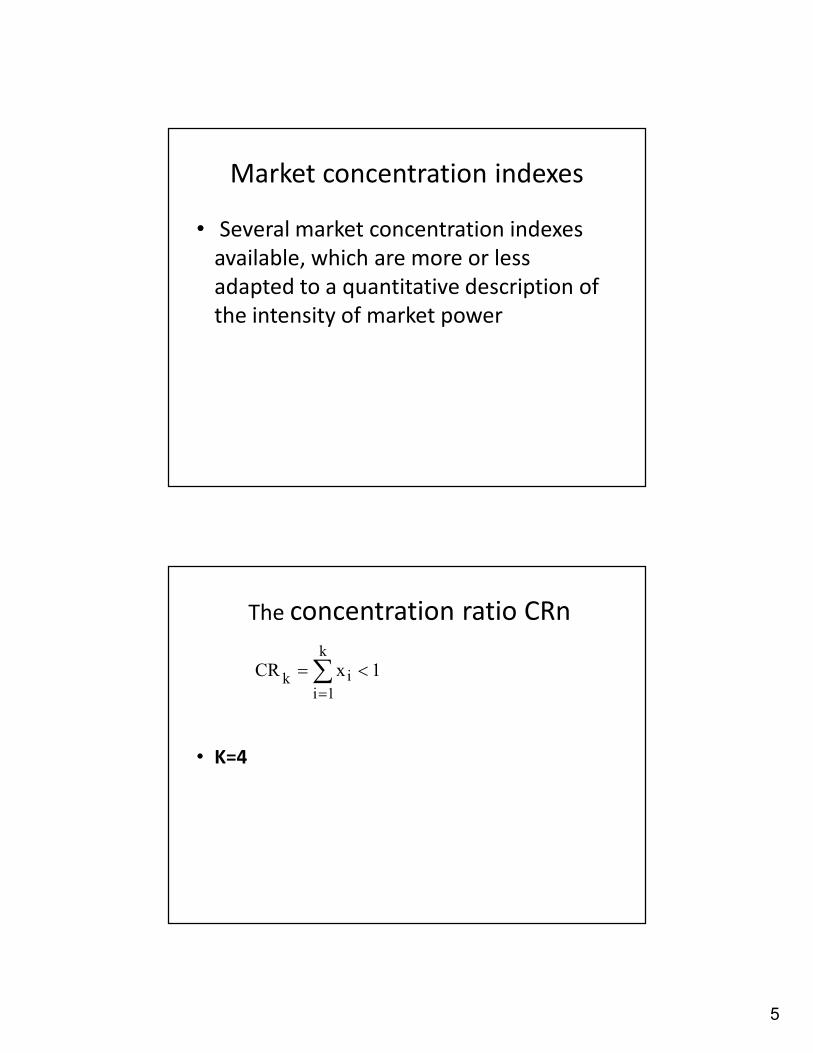

Market concentration indexes

• Several market concentration indexes

available, which are more or less

adapted to a quantitative description of

the intensity of market power

The concentration ratio CRn

• K=4

1xCRk

1i

ik<=∑

=

6

THE HERFINDAHL-HIRSCHMANN

CONCENTRATION INDEX

• Herfindahl-Hirschman concentration index (HHI),defined as follows:

• 1 monopoly;

• HHI = 0 perfect competition

1)x(H H In

1i

2i ≤= ∑

=

DI Index

� The US Federal Trade Commission also introduced a so-

called diversity index (DI)

� This DI index enables one to distinguish between the

diversity of titles, and of radio and TV stations under the

control of given owners

1)y(DIm

1i

2i ≤=∑

=

7

THE NOAM INDEX

• Noam proposes a media-secific diversity index, the

Noam index (NI). Let m be the total number of

independent media outlets. Some of these outlets

with too small audiences (below a given threshold,

for example 1%) are not taken into account. Under

these conditions, the Noam index NI is defined as

the ratio of HHI to the square root of m :

m

)x(

m

H H IN I

n

1i

2

i∑=

==

THE CASE OF THE

FRENCH PRESS

8

Historically…

• …the 19th century, and the beginning of the

20th century can be considered as a golden

age for the French press, which, since the end

of the first world war, has entered into a

period of relative decline. In 1914, there used

to be 322 dailies France, 179 in 1945, but only

66 in 2000. The number of national daily

newspapers, which used to be 26 in 1945,

was only about 10 in 2000.

Magazines

• Magazines, and the specialised general

public press, has grown from 754 titles in

1985 to 1595 titles in 2001.

• The professional specialised technical press is

another strongly growing segment of the

market, from 1109 titles to 1504 titles during

the same period.

• Important evolution in the French press and

media industry (example Dassault/Socpresse)

9

French press compared with other international

media groups

• Sales :

• Le Monde 700 million €;

• Pearson 7 billion €

• Bertelsmann 20 billion €

• Lagardère 14 billion €.

FRENCH PRESS CARTOGRAPHY

• Lagardère media segment (Lagardère Active,

Lagardère Publishing, Lagardère

Services)Lagardère Group (Aerospatial

industry)

• La Provence, Nice-Matin, Paris-Match, Elle

• 1848 (sales)

• G

• 17.80%

10

Larger international groups

• Larger media groups, whether national,international, or global (G) are today veryimportant and even dominant in the Frenchpress and media as they represent almosthalf of the sales (62.1%).

• However, independent groups, some ofwhich are comparatively large, and smallerfamily-owned firms (FI) still account for asizable share of the sales (31.3%).

• Groups in a situation of financial recoveryaccount for 6.6% of our sales.

GLOBAL INDICATORS

• Finally, we calculated several concentration

indexes on the firms, including the market

shares of the largest four, and of the largest

ten groups, and the Herfindahl-Hirschman

Index for all of them.

• CR4 = 45%

• Herfindahl-Hirschman Index (HHI) : 791.4;

11

Various indicators

The largest 4 press firms account for 45% of sales;

the HHI of 791.4 leads to the conclusion that the concentrationin the French press industry is still low, knowing that, a highconcentration starts at a HHI index of 1800.

This estimate can be compared to the HHI estimated Noam(2003) for all American media enterprises, which was of 750for 2002, which is a little smaller than in the French caseaccording to our calculations.

Excluding regional papers and thus taking into account onlythe national press, one can calculate a HHI index of 1206.3,which corresponds to moderate concentration.

• We have therefore restricted ourselves

to the French daily national press, with

11 titles (excluding the Herald Tribune).

French daily national pressFrench daily national press

12

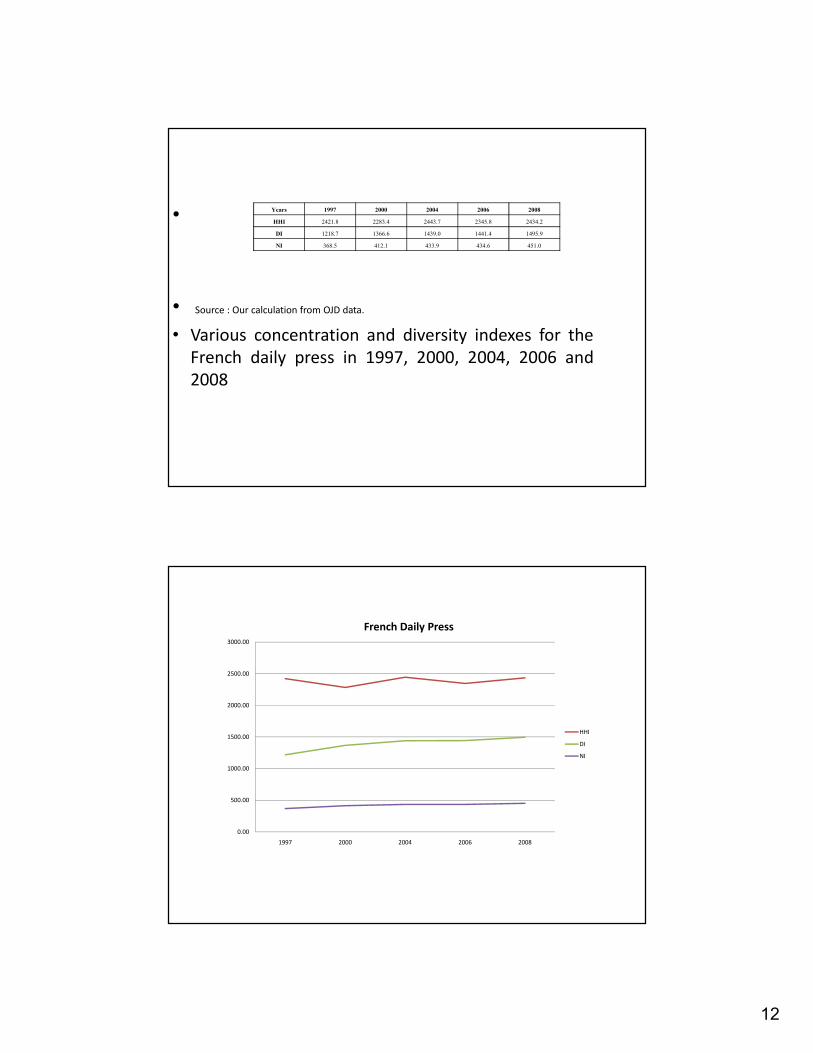

•

• Source : Our calculation from OJD data.

• Various concentration and diversity indexes for the

French daily press in 1997, 2000, 2004, 2006 and

2008

Years 1997 2000 2004 2006 2008

HHI 2421.8 2283.4 2443.7 2345.8 2434.2

DI 1218.7 1366.6 1439.0 1441.4 1495.9

NI 368.5 412.1 433.9 434.6 451.0

0.00

500.00

1000.00

1500.00

2000.00

2500.00

3000.00

1997 2000 2004 2006 2008

French Daily Press

HHI

DI

NI

13

French daily national press,

• The Herfindahl-Hirschman index was found

to be equal to 2434.2 (2008), a quite high

figure, reflecting a strong concentration of

French press groups on the segment of

national dailies. However, with 11 titles, the

Noam diversity index is at a much lower

value of 451.

The regional press: a very high concentration

• If we discuss the case of the regional press, in most

regions, there is just one daily newspaper. These

monopoly situations are expected, since there are

important economies of scale in the production of

information.

•

14

The regional press (2)

• One can, however, calculate HHI and NI in two regions where

there is more than one daily : Alsace, with two competing

titles (L’Alsace-Le Pays and Les Dernières Nouvelles d’Alsace),

et la Lorraine with three competing titles (L’Est Républicain, Le

Républicain Lorrain, and Est Eclair).

The regional press (3)

• This calculation leads to HHI estimates of 5343.5 and 4415.9

in 2008 for, respectively, Alsace and Lorraine, which

correspond as expected to very high concentrations and

duopoly situations (two competitors). A similar conclusion can

be drawn from the evaluations of the NI indexes, which are of

3778.4 and 2549.5 for, respectively, Alsace and Lorraine.

These figures can be compared with the HHI of 7621 (Noam,

2004) in the case of the American local press, with the same

phenomenon of a quasi-monopoly situation in most states

and cities.

15

CONCLUSIONS

CONCLUSIONS

• For the whole press industry, HHI shows a concentration process, but competition is still important (HHI< 1000)

• New entrants and higher competition:

– Prisma-Bertelsmann, EMAP, PRISA.

• Some French groups (Lagardère) are very present at the world level.

• HHI very high for the French national press (2434.2), varying little since 2000.

• French regional press= monopolies in most regions.

16

The case of the French Television

The case of the French Television

• An interesting methodological questions:

– Metamorphosis of the sector wtih new technology

and new entrants

• Hertzian television (traditional television)

• New entrant like Canal Plus in Hertzian television

(1984)

• New technology like Cable launched in 1982

• Satellite in the 1980’s

• And TNT (Digital Terrestrial Television) which will be

substituted to Hertzian Television by the end of 2011

17

Technological evolution and Technological evolution and

concentration in the TV industryconcentration in the TV industry

• So we have not solve the methodological

question i.e. how to evaluate concentration when

such quick changes are changing the context

technological frontiers and new markets?

• We propose an analysis (and evaluation of the

concentration when data were collected ) of

the different sectors of the television

(Hertzian, Cable, Satellite, Terrestrial TV)

The case of the French Television

Hertzian Television only

Market share (audience) 1989-2009

18

New entrants

• LA 5 (Berlusconi) until 1991 (10,9% of the

market)

• ARTE since 1993 (1,7% in 2007)

• La 5ème France 5 since 1995 (3% in 2007)

19

• Evolution of the HHI

• More concentration when Berlusconi stopped

• And then a constant level

0

5

10

15

20

25

30

35

40

45

50

Share of Public TV

part des chaînes publiques

Part des chaînes publiques (hors nouvelles

chaînes)

20

2009 1 2

France 2 16,7 0,23226704France 3 11,8 0,16411683

France 5 3,1 0,04311544

Arte 1,7 0,02364395

Public 33,3 0,46314325 0,46314325 0,21450167

TF1 26,1 0,36300417 0,36300417 0,13177203

M6 10,8 0,15020862 0,15020862 0,02256263Canal + 1,7 0,02364395 0,02364395 0,00055904

71,9 HHI 0,36939537

HHI for Hertzian TV only

HHI

2800

2900

3000

3100

3200

3300

3400

3500

3600

3700

3800

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

21

Importance of other TVs

New HHI (including other TV)

2 0 09 1 2

F ra nc e 2 16 ,7 0 ,1 6 7F ra nc e 3 11 ,8 0 ,1 1 8

F ra nc e 5 3 ,1 0 ,0 3 1

A r te 1 ,7 0 ,0 1 7P ub l ic 33 ,3 0 ,3 3 3 0 ,3 3 3 0 ,11 0 8 89

T F 1 26 ,1 0 ,2 6 1 0 ,2 6 1 0 ,06 8 1 21

M 6 10 ,8 0 ,1 0 8 0 ,1 0 8 0 ,01 1 6 64C an a l + 1 ,7 0 ,0 1 7 0 ,0 1 7 0 ,00 0 2 89

1 00 28 ,1 0 ,2 8 1 0 ,2 8 1 0 ,07 8 9 61

71 ,9 N H H I 0 ,26 9 9 24

22

HHI, NHHI and NI (Noam Index)

2.2/ Cable industry from competition to monopoly

2000: HHI= 2124

Noos 26% 0 ,0676F rance

T é lé com

C âble 25% 0 ,0625N um ériC âble 23% 0 ,0529UPC 13% 0 ,0169N TL 2% 0 ,0004D ive rs 11% 0 ,0121

100% 2124

23

Cable industry : in 2009 Numericable

owns the whole cable sector

HHI~10000

2.3/ Different market segments

24

Methodological stakes: a mix of technologies and uses

(television, telecommunications and Internet internet

IssuesIssues

• It will be necessary to aggregate various

segments :

• Methodological stakes: a mix of technologies

and uses (television, telecommunications and

Internet ).

25

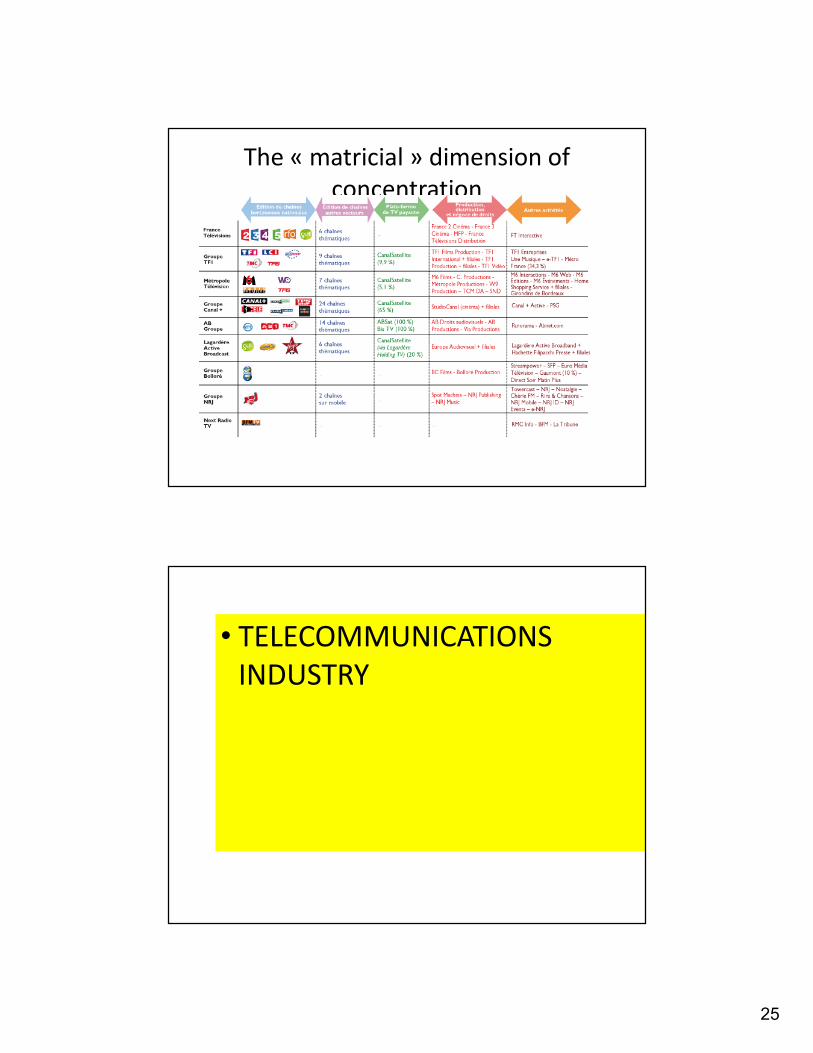

The « matricial » dimension of

concentration

• TELECOMMUNICATIONS

INDUSTRY

26

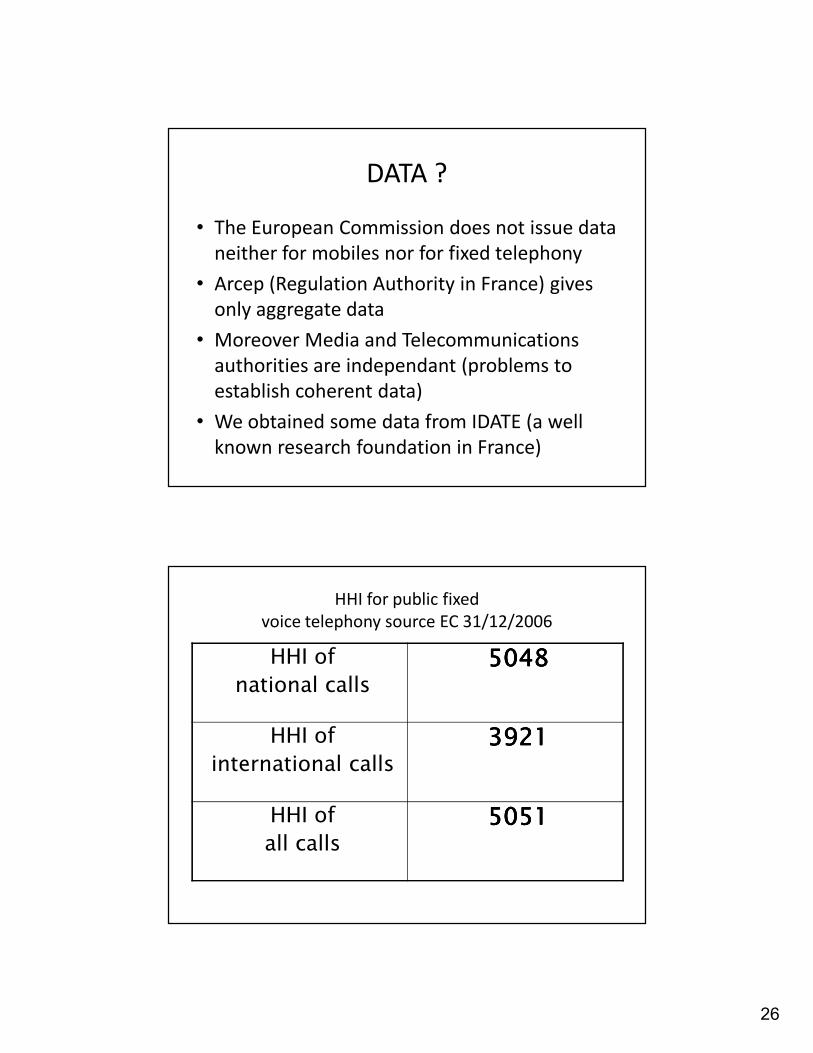

DATA ?

• The European Commission does not issue data

neither for mobiles nor for fixed telephony

• Arcep (Regulation Authority in France) gives

only aggregate data

• Moreover Media and Telecommunications

authorities are independant (problems to

establish coherent data)

• We obtained some data from IDATE (a well

known research foundation in France)

HHI for public fixed

voice telephony source EC 31/12/2006

HHI of

national calls

5048504850485048

HHI of

international calls

3921392139213921

HHI of

all calls

5051505150515051

27

Data from ARCEP (aggregate)Data from ARCEP (aggregate)

DATA FROM IDATE

• Data related to fixed telephony are

aggregated with only three groups

–Historical operator= France Telecom First

group of alternative operators= SFR+

Bouygues

– Second group of alternative operators =

Tele2, Cegetel, Neuf Telecom

28

0

1000

2000

3000

4000

5000

6000

7000

2002 2003 2004 2005 2006 2007 2008

Trafic téléphonie fixe

HHI

Noam

Fixed telephone HHI and NI

Mobile

• From monopoly to triopoly

– Orange

– SFR

– Bouygues

– And MVNO (~5%)

– Emergence of new entrants: MVNO

– Data from IDATE distinguished these four groups

29

30

HHI and NI for the mobile HHI and NI for the mobile

phone industryphone industry

0

1000

2000

3000

4000

5000

6000

7000

8000

1990 1991 1992 1993 1994 1995 1996 1997 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Parc clients mobiles

HHI

Noam

Internet/TelecomDATA FROM IDATE

FT/Wanadoo/Orange

Noos

NC Numericable

UPC France

cegetel/SFR

Neuf

Free

club internet

AOL

tiscali

Alice (TI France)

Tele2

31

HHI for internet access HHI for internet access

0

1000

2000

3000

4000

5000

6000

2001 2002 2003 2004 2005 2006 2007 2008 2009

Parc abonnés haut débit

HHI