Embed Size (px)

Citation preview

ECONOMIC TURMOIL PLANNINGECONOMIC TURMOIL PLANNING

RXRXTAKING STEPS TO TAKE CONTROLTAKING STEPS TO TAKE CONTROL

Janice A. Forgays, J.D., CLUJanice A. Forgays, J.D., CLU(Advanced Underwriter - June, 2009) (Advanced Underwriter - June, 2009)

CRN201009-125315

For education purposes only. Not for use with general public.

For Education Purposes Only. Not for Use with the General Public.

The information contained in this presentation is not written or intended to be interpreted as specific legal or tax advice and may not be relied on for purposes of avoiding any federal tax penalties. Neither MassMutual nor any of its employees or representatives are authorized to give legal or tax advice. Individuals are encouraged to seek the guidance of their own legal or tax counsel. Any individuals involved in the estate planning process should work with an estate planning team, including their own personal legal or tax counsel.

Disclosure

For Education Purposes Only. Not for Use with the General Public.

ECONOMIC TURMOIL PLANNING

Changes in Economic Conditions

Creates Opportunities to Meet With Clients

WHY?

Asset values may have changed

Low interest rate environment

For Education Purposes Only. Not for Use with the General Public.

STEPS TO TAKE

1. Will Review

2. Trust Review

3. Estate Planning

4. Gift Planning

5. Charitable Giving

6. Sales to Intentionally Defective Grantor Trusts

7. Grantor Retained Annuity Trusts

8. Split Dollar Loan Treatment

*PLRs cannot be relied upon as precedent by anyone other than the taxpayer requesting the letter

For Education Purposes Only. Not for Use with the General Public.

WILL REVIEW

CLIENTS: Married with 2 adult children

INTENT: Treat children equally

WILL PROVISIONS: Commercial Real Estate to Child 1

Stock Portfolio to Child 2

PROBLEM: Stock portfolio value down 50%

STRATEGY: Review and rebalance will bequests*

*Should be reviewed regularly – provides good opportunity to meet with client

For Education Purposes Only. Not for Use with the General Public.

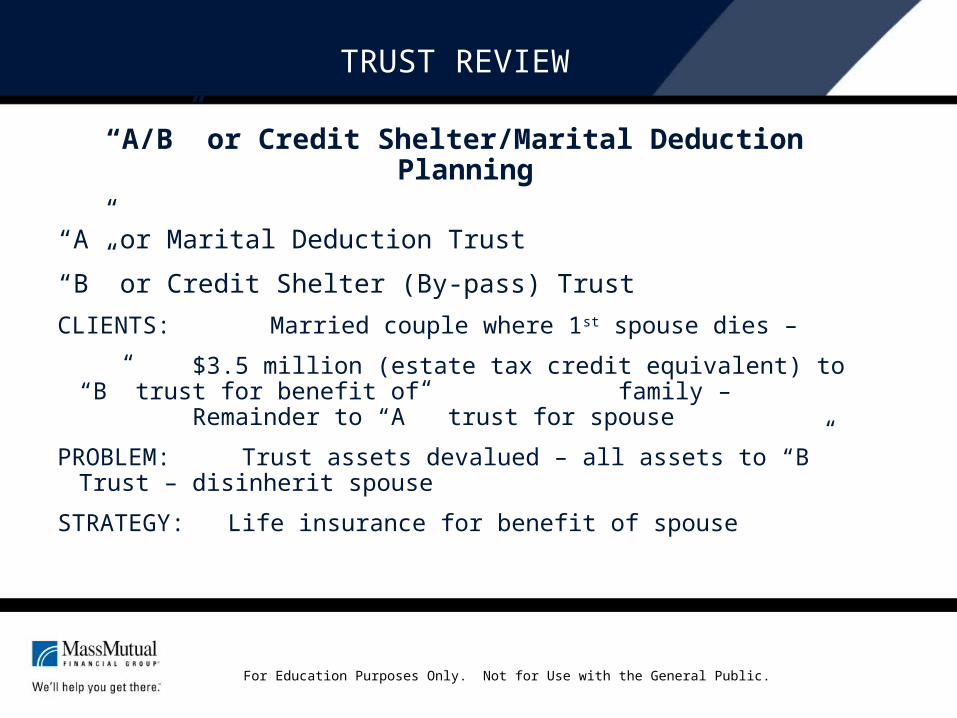

TRUST REVIEW

“A/B” or Credit Shelter/Marital Deduction Planning

“A” or Marital Deduction Trust

“B” or Credit Shelter (By-pass) Trust

CLIENTS: Married couple where 1st spouse dies –

$3.5 million (estate tax credit equivalent) to “B” trust for benefit of family –

Remainder to “A” trust for spouse

PROBLEM: Trust assets devalued – all assets to “B” Trust – disinherit spouse

STRATEGY: Life insurance for benefit of spouse

For Education Purposes Only. Not for Use with the General Public.

ESTATE PLANNING

State of the Estate Tax

Current Law: Estate tax replaced by capital gains tax in 2010 only

& no step up in basis

* in 2011 $1million estate tax credit/ 55% top tax rate

Estate Tax Proposals in Congress Senate 722 - freeze ’09 ($3.5 million/45% top rate) & reunification of gift and estate tax

exemptions at $3.5 million

House 2032 - $2 million credit/55% top tax rate

House 436 – freeze ’09 and limit FLP Valuation Discounts

For Education Purposes Only. Not for Use with the General Public.

ESTATE PLANNING

State of the Estate Tax

No proposals to eliminate estate tax

Freeze ’09 price tag = $238 billion over 10 years (per Congressional Budget Office)

For Education Purposes Only. Not for Use with the General Public.

ESTATE PLANNING

Goes beyond planning for the estate tax….

CLIENT: Has special needs child

INTENT: Provide for child without diminishing family lifestyle

PROBLEM: Support costs are depleting family wealth

STRATEGY: Special needs trust funded with life insurance on parent(s) for benefit of special needs child

For Education Purposes Only. Not for Use with the General Public.

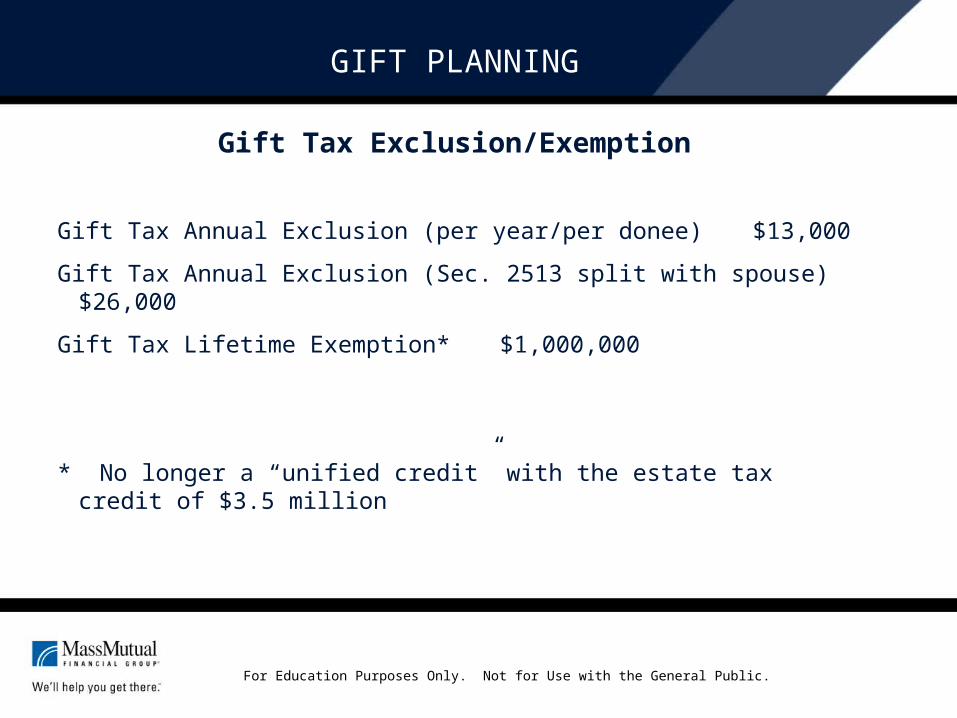

GIFT PLANNING

Gift Tax Exclusion/Exemption

Gift Tax Annual Exclusion (per year/per donee) $13,000

Gift Tax Annual Exclusion (Sec. 2513 split with spouse) $26,000

Gift Tax Lifetime Exemption* $1,000,000

* No longer a “unified credit” with the estate tax credit of $3.5 million

For Education Purposes Only. Not for Use with the General Public.

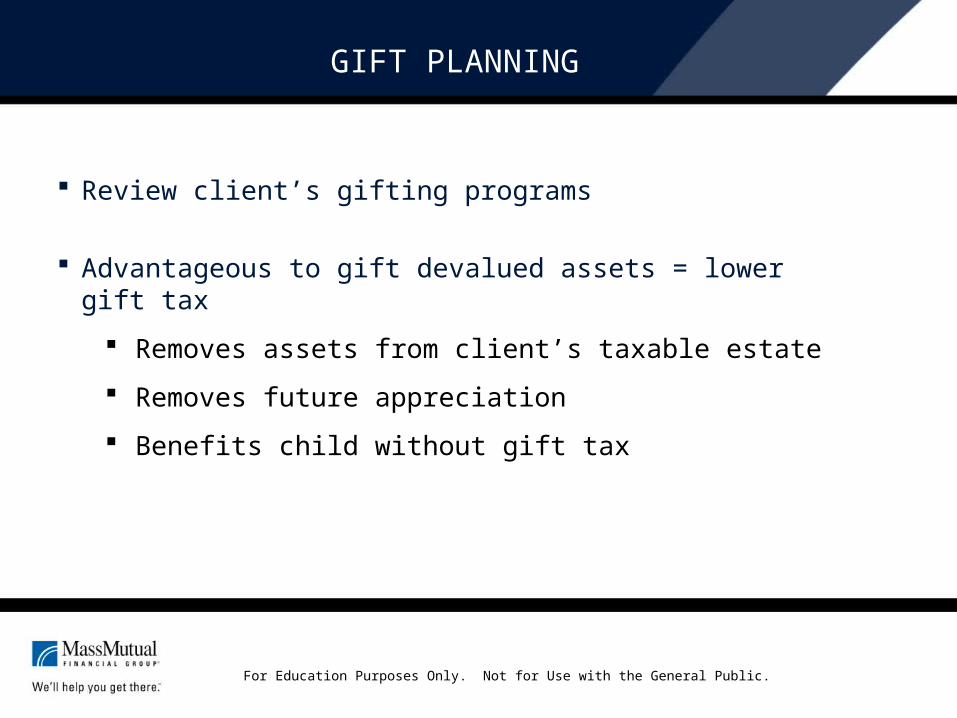

GIFT PLANNING

Review client’s gifting programs

Advantageous to gift devalued assets = lower gift tax

Removes assets from client’s taxable estate

Removes future appreciation

Benefits child without gift tax

For Education Purposes Only. Not for Use with the General Public.

CHARITABLE GIVING

In 2008:

According to the National Philanthropic Trust – 2/3 of charities experienced drops in giving

Tactical Philanthropy Advisor reports that charitable giving in the US suffered the largest percentage drop on record

For Education Purposes Only. Not for Use with the General Public.

CHARITABLE GIVING

Make gifts in will (can amend will as circumstances change)

Adopt charitable giving strategy:

Charitable gift annuities

Charitable remainder trusts

For Education Purposes Only. Not for Use with the General Public.

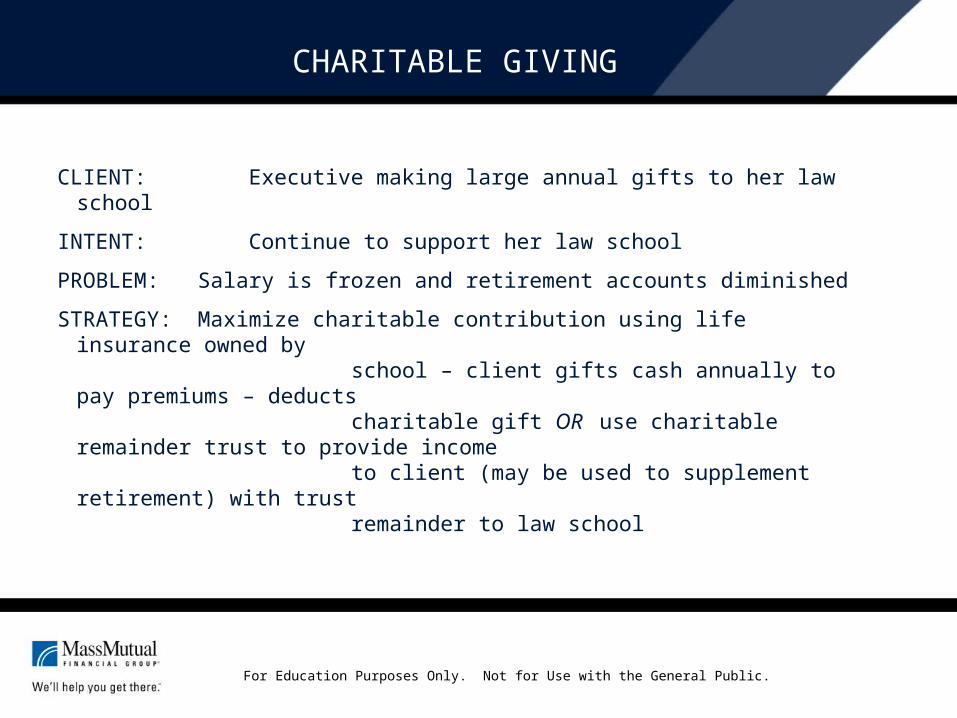

CHARITABLE GIVING

CLIENT: Executive making large annual gifts to her law school

INTENT: Continue to support her law school

PROBLEM: Salary is frozen and retirement accounts diminished

STRATEGY: Maximize charitable contribution using life insurance owned by school – client gifts cash annually to pay premiums – deducts charitable gift OR use charitable remainder trust to provide income to client (may be used to supplement retirement) with trust remainder to law school

For Education Purposes Only. Not for Use with the General Public.

SALE TO INTENTIONALLY DEFECTIVE TRUST (IDIT/IDGIT)

Leveraged Wealth Transfer Tool

IDIT = “Intentionally defective irrevocable trust” or “Grantor Trust”

Example: trust income used to pay premiums Is no tax on sale of property between IDIT and Grantor – considered sale to self

for income tax purposes (Revenue Ruling 85-13) All trust income/loss taxed to Grantor Seller does not pay tax on gain (if any) Interest payments not taxed to Grantor (payments to self)

For Education Purposes Only. Not for Use with the General Public.

INTEREST RATES

APPLICABLE FEDERAL RATES (AFR)September 2009

IRC 1274(d) rates apply to loans sales (IDITs/Split Dollar Loans) Demand or short term (up to 3 years) 0.84% Mid-term (from 3 up to 9 years) 2.87% Long-term (9 or more years) 4.38%

IRC 7520 rate applies to GRATs and CRTs 120% of Federal mid-term rate

For Education Purposes Only. Not for Use with the General Public.

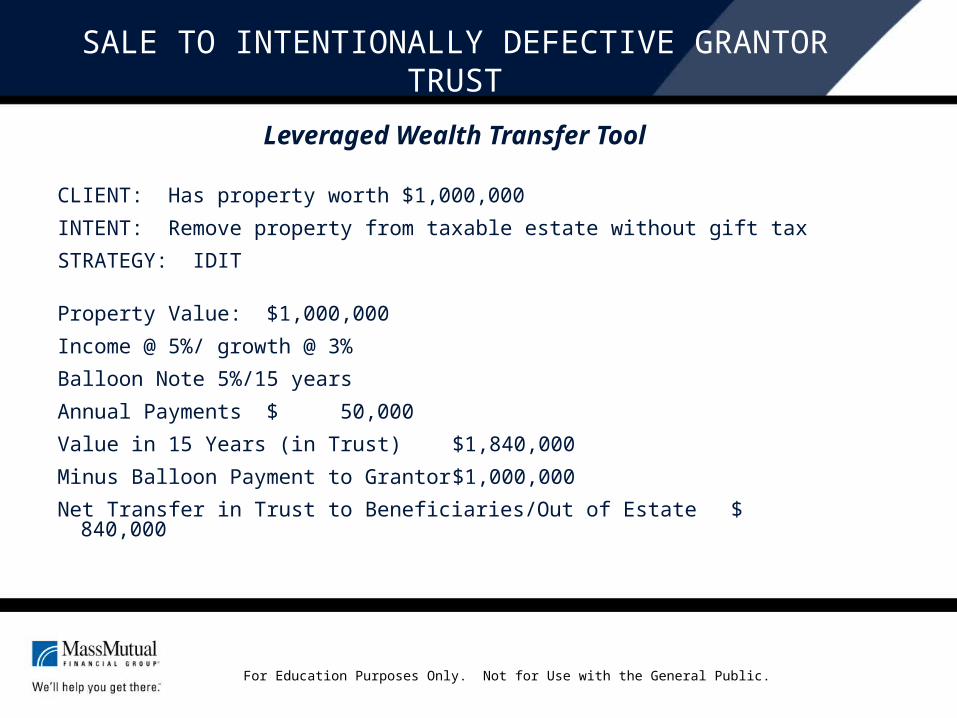

SALE TO INTENTIONALLY DEFECTIVE GRANTOR TRUST

Leveraged Wealth Transfer Tool

CLIENT: Has property worth $1,000,000

INTENT: Remove property from taxable estate without gift tax

STRATEGY: IDIT

Property Value: $1,000,000

Income @ 5%/ growth @ 3%

Balloon Note 5%/15 years

Annual Payments $ 50,000

Value in 15 Years (in Trust) $1,840,000

Minus Balloon Payment to Grantor $1,000,000

Net Transfer in Trust to Beneficiaries/Out of Estate $ 840,000

For Education Purposes Only. Not for Use with the General Public.

GRANTOR RETAINED ANNUITY TRUSTS (GRATS)

Leveraged Wealth Transfer Tool

Parent transfers devalued property to GRAT

Pays gift tax on lowered property value

Trust pays parent fixed amount each year for set number of years – trust remainder to children

Market recovery transfers to children at end of trust term without additional gift tax

If parent dies w/i trust term – trust assets in taxable estate

RULE: The lower the Section 7520 rate the greater the remainder interest in trust for beneficiaries

For Education Purposes Only. Not for Use with the General Public.

GRANTOR RETAINED ANNUITY TRUSTS

QPRT = Qualified Personal Residence Trust

Type of GRAT used for personal residences

Used to leverage market recovery on depressed value homes

For Education Purposes Only. Not for Use with the General Public.

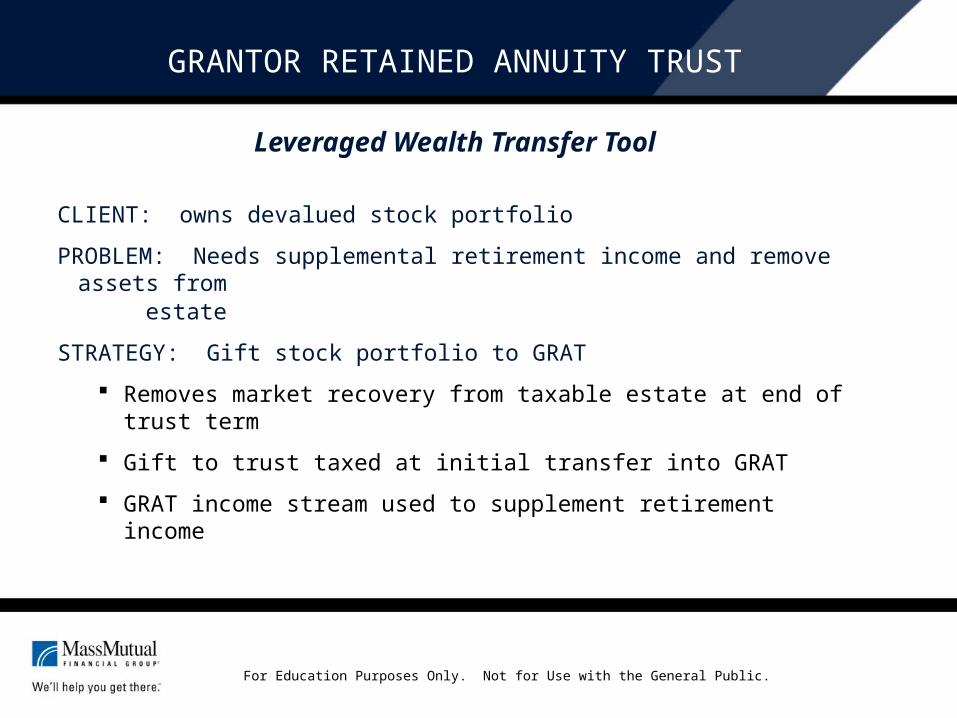

GRANTOR RETAINED ANNUITY TRUST

Leveraged Wealth Transfer Tool

CLIENT: owns devalued stock portfolio

PROBLEM: Needs supplemental retirement income and remove assets from estate

STRATEGY: Gift stock portfolio to GRAT

Removes market recovery from taxable estate at end of trust term

Gift to trust taxed at initial transfer into GRAT

GRAT income stream used to supplement retirement income

For Education Purposes Only. Not for Use with the General Public.

GRANTOR RETAINED ANNUITY TRUSTS

Obama Administration’s 2010 Revenue Proposals

Limit use of short term GRATs (used to minimize chance of death and estate inclusion of trust assets during trust term)

Imposes minimum GRAT term of 10 years

NO BILL YET so still time….so still time….

For Education Purposes Only. Not for Use with the General Public.

SPLIT DOLLAR LOAN TREATMENT

Replaced equity split dollar (after Final Split Dollar regulations)

Employer makes premium loans to employee

Interest rate = AFR

Employee benefits from low interest rate environment

Employee entitled to policy equity in excess of premium loans plus interest

NOTE: Split dollar loans may also be made between family members or to an Irrevocable Life Insurance Trust

For Education Purposes Only. Not for Use with the General Public.

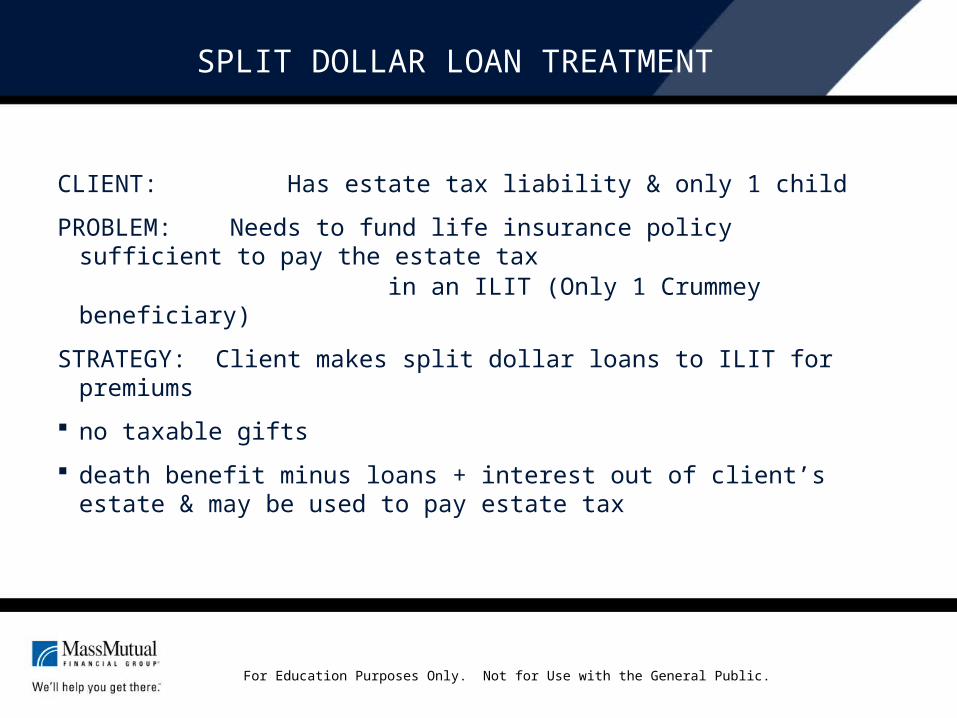

SPLIT DOLLAR LOAN TREATMENT

CLIENT: Has estate tax liability & only 1 child

PROBLEM: Needs to fund life insurance policy sufficient to pay the estate tax in an ILIT (Only 1 Crummey beneficiary)

STRATEGY: Client makes split dollar loans to ILIT for premiums

no taxable gifts

death benefit minus loans + interest out of client’s estate & may be used to pay estate tax

For Education Purposes Only. Not for Use with the General Public.

©2009 Massachusetts Mutual Life Insurance Company, Springfield, MA. All rights reserved. www.massmutual.com. MassMutual Financial Group is a marketing name for Massachusetts Mutual Life Insurance Company (MassMutual) and its affiliated companies and sales representatives

Thank You