Embed Size (px)

Citation preview

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

The Canadian Loss Experience Automobile Rating

Arthur Tabachneck, Ph.D., ManagerArthur Tabachneck, Ph.D., ManagerAbdul Sattar Al-Khalidi, Ph.D., Senior StatisticianAbdul Sattar Al-Khalidi, Ph.D., Senior Statistician

Statistical Research and DevelopmentStatistical Research and Development

CLEAR

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

Canada

Total Area: 3.9 mil sq miles

Total Area: 3.7 mil sq miles

Population: 298 mil

Population: 33 mil

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

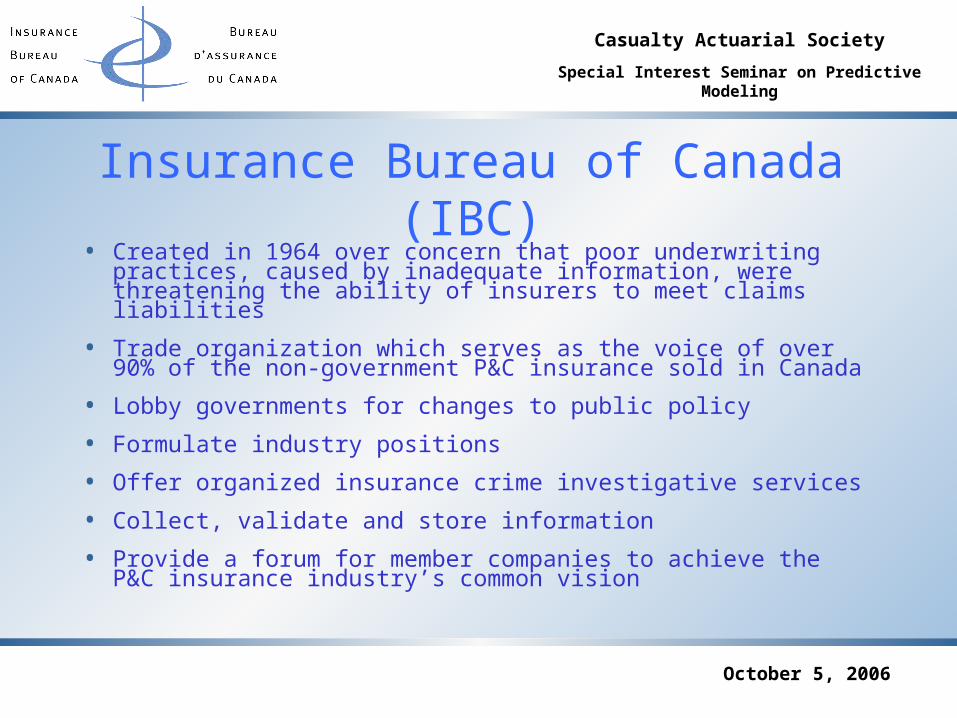

Insurance Bureau of Canada (IBC)• Created in 1964 over concern that poor underwriting practices,

caused by inadequate information, were threatening the ability of insurers to meet claims liabilities

• Trade organization which serves as the voice of over 90% of the non-government P&C insurance sold in Canada

• Lobby governments for changes to public policy

• Formulate industry positions

• Offer organized insurance crime investigative services

• Collect, validate and store information

• Provide a forum for member companies to achieve the P&C insurance industry’s common vision

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

Government Insurers

Non-Government Insurers

Government vs Non-Government Auto Insurance in Canada

BI Only

Man

dato

ry C

over

ages

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

0.25 mil vehicles

0.076 mil vehicles

0.53 mil vehicles

0.45 mil vehicles

4.2 mil vehicles

6.8 mil vehicles

0.62 mil vehicles0.66 mil vehicles

2.2 mil vehicles

2.2 mil vehicles

0.024 mil vehicles

Total Private Passenger Vehicles: 18,123,885

0.003 mil vehicles

0.021 mil vehicles

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

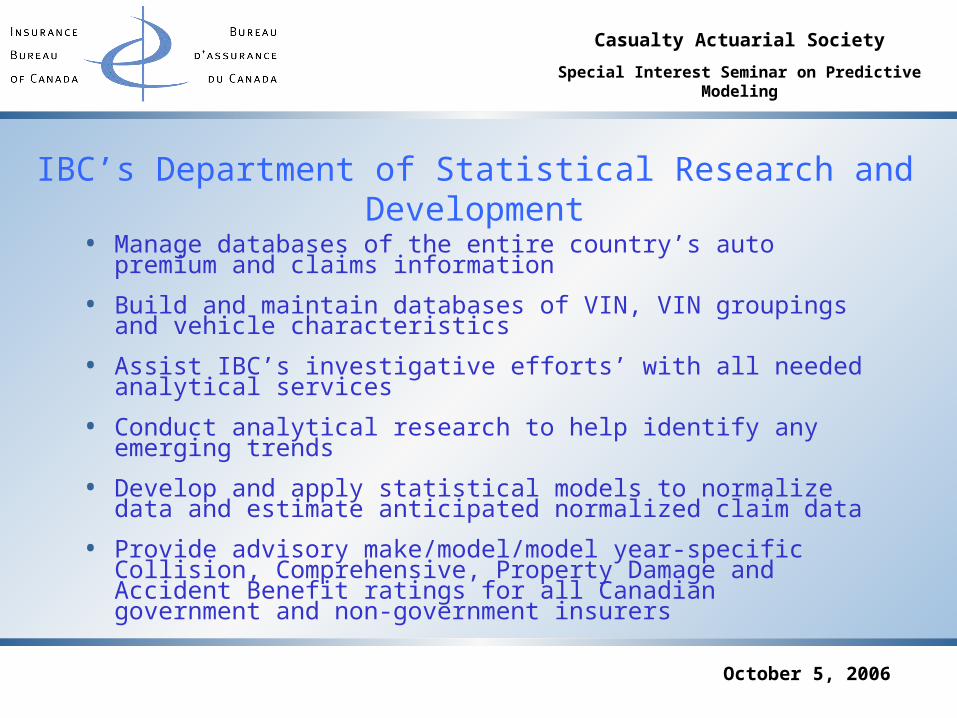

IBC’s Department of Statistical Research and Development

• Manage databases of the entire country’s auto premium and claims information

• Build and maintain databases of VIN, VIN groupings and vehicle characteristics

• Assist IBC’s investigative efforts’ with all needed analytical services

• Conduct analytical research to help identify any emerging trends

• Develop and apply statistical models to normalize data and estimate anticipated normalized claim data

• Provide advisory make/model/model year-specific Collision, Comprehensive, Property Damage and Accident Benefit ratings for all Canadian government and non-government insurers

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

Canadian Loss Experience Automobile Rating (CLEAR)

•What

•Why

•How

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

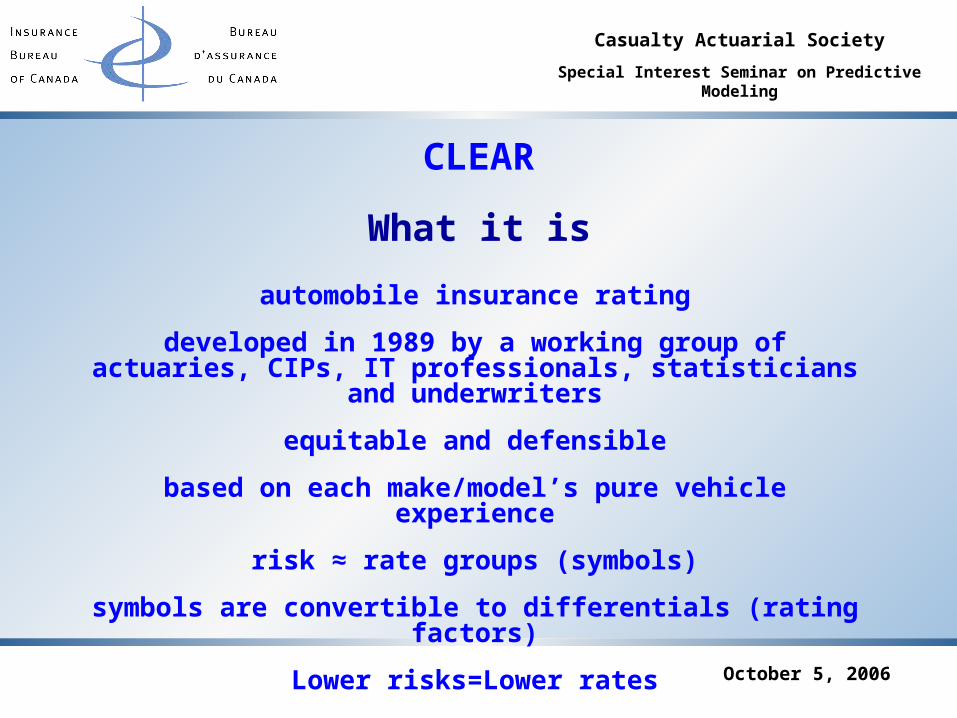

What it is

CLEAR

automobile insurance rating

developed in 1989 by a working group of actuaries, CIPs, IT professionals, statisticians and underwriters

equitable and defensible

based on each make/model’s pure vehicle experience

risk ≈ rate groups (symbols)

symbols are convertible to differentials (rating factors)

Lower risks=Lower rates

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

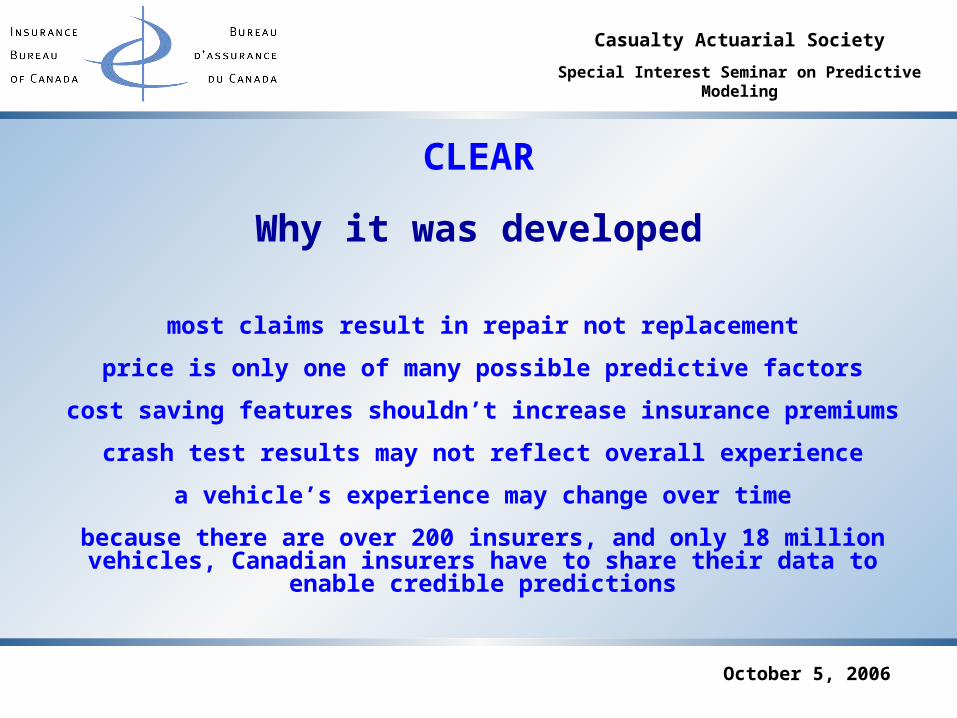

CLEAR

Why it was developed

most claims result in repair not replacement

price is only one of many possible predictive factors

cost saving features shouldn’t increase insurance premiums

crash test results may not reflect overall experience

a vehicle’s experience may change over time

because there are over 200 insurers, and only 18 million vehicles, Canadian insurers have to share their data to enable credible predictions

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

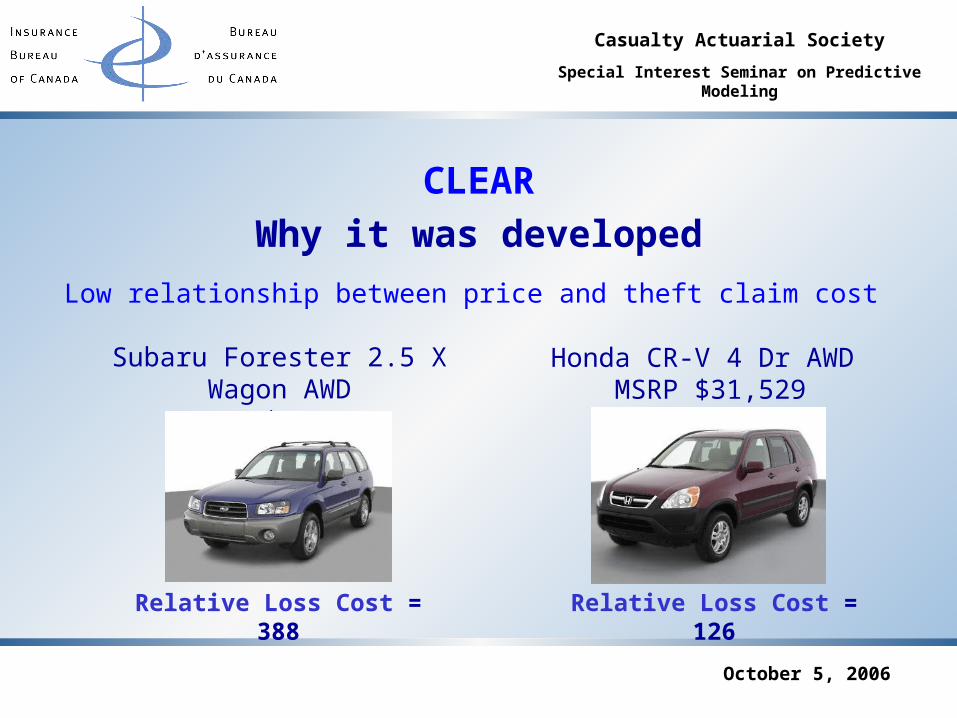

Low relationship between price and theft claim cost

CLEAR

Why it was developed

Honda CR-V 4 Dr AWD MSRP $31,529

Relative Loss Cost = 126

Subaru Forester 2.5 X Wagon AWD

MSRP $30,543

Relative Loss Cost = 388

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

Low relationship between price and collision claim cost

CLEAR

Why it was developed

Subaru Impreza WRX 4 Dr AWD

MSRP $39,335

Volkswagen Passat GLS V6 4 Dr

MSRP $36,113

Relative Loss Cost = 295

Relative Loss Cost = 51

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

CLEAR - How it works•Body style

•Drivetrain

•Wheelbase

•Weight

•Engine displacement

•Engine horsepower

•MSRP

•Indexed MSRP

•Type of brakes

•Theft deterrent system

•Track width

•Height

•Types of airbags

•Manufacturer

•Seating capacity

•Brake assistance

•Ground clearance

•Traction control

•Stability control

•Types of headrestraints

•Seatbelt pretensioners

•Lane departure warning

•Tracking system

•Parts marking

•Engine type

•Engine placement

•Age

•General model and model

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

Ad ju st RLCs fo r Risk Lo ad ing an dco ntro l chan ge w ith p r io r RLC

Ad jRLC=(ip r ice >=65k)*[EstRLC((ip r ice -45k)/i5k)*10]

CLEAR - How it works

Balan ce Tab le

Ad ju st RLCsto ach ie v erate le v e ln e u trality

Acco mplishRe v e rsal Co n tro l

Assu re re v e rsalsare ju stifie d

Co n v e rt Ad jRLCs to Rate G ro u p s

Rate Gro u p =1*(Ad jRLC<34.5)+(Ad jRLC/10-1.95)*(34.5<=Ad jRLC<=304)+(Ad jRLC/20+13.275)*(Ad jRLC>304)

Calcu lateLC & Re l LC

(Ad jEstF *Ad jEstS)/

W t Av g LC

Ap prov alPro ce ss

Ens ure RateLe ve l Ne utralityand Acce ptable

Dis location

Adjust e stimate s tore fle ct actual e xpe rie nce

Ad jESTF=ESTF(1+M AFF)Ad jESTS=ESTS(1+M AFS)

Est Cla im s=Actua l # Cla im s le ss e ffe ctsdue to ta riffs &/or discounts

Est Loss=Actua l Loss le ss e ffe cts dueto due to ta riffs &/or discounts

Build /Incorpo rateData Normalization M od e ls

Pro je ct Pu b lica tio n Ye a r F le e t

Use link m ode l ba se d on thre em ost re ce nt a ccide nt ye a rs'

e x posure s (a s a t De ce m be r 31stof e a ch ye a r), curre nt ye a r

e x posure s (a s a t June 30th), a ndsa le s e stim a te s

Assu re re aso n ab ility o f in su ran ced ata (fo r a ll co v e rag e s)

Sta t P la ns V IN De codingError Che cking Re a sona bility Che ck

# Ex posure s P re m ium s # Cla im s Loss

De ve lop a nd m a inta inve hicle cha ra cte ristics

W he e lba se : 2718 TDS: NoW e ight: 1889 S tyle : S UVDrive tra in: 4 ABS: Ye sPrice : $43,356 Doors: 4VCODE: 6706 Ye a r: 2007Airba g: Ye s Pow e r: 190

De v e lo p /Re v ie w /Ap p lyStatistical M o d e ls

De v e lo p an d ap p ly fo rmu laeto e stimate n o rmalize d claim

fre q u e n cy an d se v e rityfro m v e h icle ch aracte r istics

Casualty Actuarial Society

Special Interest Seminar on Predictive Modeling

October 5, 2006

VINlink

Loss Cost Data

Modelling

Vehicle Characteristics

Formulae

RecentClaims

Experience

Loss Cost Estimates

ExperienceAdjustment

Controls andBalancing

NVAPResults

RateGroup Tables

+

CLEAR - How it works

ReviewProcess