Embed Size (px)

Citation preview

Research & Forecast Report

ATLANTAQ2 2016 | Multifamily

Atlanta Market Fundamentals Continue to Drive GrowthKey Takeaways > Projected annual supply in 2017: 13,700 units

> 2nd quarter 2016 unemployment: 4.6%

> GE relocates North American headquarters to Midtown: 250 IT jobs + $3M investment

> Occupancy rate increases in 2nd Qtr 2016: 94.8%

Atlanta Multifamily MarketThe Atlanta apartment market is continuing to thrive as a result of strong economic fundamentals. Growth in employment has increased the demand for more units, decreasing vacancy rates and fostering higher rent rates. While there is bifurcation between inner-perimeter submarkets and those submarkets outside the perimeter, the metro area is benefiting from a well-educated workforce and strong business community. New and existing employers such as Mercedes, State Farm, Global Payments and General Electric continue to expand their presence in the area, providing high paying jobs and driving economic development. Most notable is General Electric’s plan to relocate 250 high-paying IT jobs to Midtown as a part of its North American headquarters consolidation, which will include a $3 million investment. Unemployment has continued to fall precipitously for the past 3 years to 4.8% as of April 2016. With low unemployment and renters with more spending power, the demand for multifamily housing near in-town amenities has sustained upward pressure on market rents.

RENT

Annual rent growth levels remain historically high, averaging between 6%-8% over the last several quarters. This increase was well above the five-year average of 4.5% and the national overall of 4.6% during the same period. Higher rents are mostly being realized in the Midtown and northern submarkets where new class A product is in high demand. There seems to be a direct correlation between close proximity to major employment centers and higher rent. Residents are seeking to rent in places where there is a live, work, play component, enjoying amenities near their jobs and residences. Submarkets south of the downtown continue to experience stagnant rent growth as fewer employers are reluctant to move in these areas.

US SOUTH ATLANTA Source: MPF Research

Historical Apartment Occupancy & Rents

Market IndicatorsRelative to prior period

ATLQ2 2016

ATLQ3 2016*

VACANCY

RENTS

CONCESSIONS

TRANSACTIONS

PRICE PER UNIT

CAP RATES

*Projected

90%

91%

92%

93%

94%

95%

96%

97%

2014

2015

2016

Occ

upan

cy %

$400

$600

$800

$1,000

$1,200

$1,400

2014

2015

2016

AVG

Mon

thly

Ren

t

2 Research & Forecast Report | Q2 2016 | Atlanta Multifamily | Colliers International

DEMAND

Atlanta posted strong demand over the past year. Annual demand was 9,692 units, which topped annual supply by 2,284 units. As a result, occupancy rates increased 60 basis points year-over-year, to 94.8%. In terms of quarterly performance, occupancy improved 80 basis points which is a swing of 1.8% over the 1st quarter 2016. Demand in Atlanta’s highly sought after areas inside the perimeter continue to trend upward as long as there remains a healthy job market. Going forward, this trend will continue while other submarkets to the south and outside the perimeter struggle to progress.

SUPPLY

Supply remains strong as developers continue to experience rent growth, particularly in Midtown and Northern submarkets. Quarterly supply topped the previous quarter as an additional 489 units hit the market, (1,873 units vs. 1,384 units), representing an increase of 35% quarter over quarter. Outer perimeter submarkets will remain untouched as most of the new product will be concentrated in Midtown and Buckhead.

OCCUPANCY

Atlanta occupancy has remained strong due to strong demand. For

the past several years, demand has topped supply leading to a steady increase in occupancy. In the 2nd quarter 2016, occupancy posted 94.8%, up 60 basis points year-over –year. While national occupancy in the 2nd quarter topped 96.2%, Atlanta has gained ground in recent months as a result of a strong economy and favorable business climate. Occupancy rates are highest in central and northern submarkets as other areas outside the perimeter remained challenged from a lack of employment.

OUTLOOK FOR 2016

Atlanta’s employment growth is expected to continue to outshine other similar sized metro markets due to its stellar economic fundamentals and corporate headquarter expansions. New supply will continue to hit the market through end of 2016 and beginning of 2017 but this will begin to put pressure on rent growth as oversupply ensues. Look for overall rent growth to settle between 3% and 4% next year while occupancy rates stabilize around 94%. Expansion of new supply is expected to complete upwards of nearly 13,700 units in the coming year. Things to look for in the next year as rent growth tapers is the increasing pressure of single-family housing and apartment overbuilding , particularly in Midtown and Buckhead.

Historical Investment Volume & Cap Rates

UPDATE - Recent Transactions in the Market

Notable Sales Activity

PROPERTY SUBMARKET SALES DATE SALE PRICE SIZE (UNITS) PRICE / UNIT BUYER

WestHaven at Vinings Northwest Atlanta 6/20/2016 $91,000,000 610 $149,180 GoldOller Real Estate Inv.

70 Perimeter Ctr. E Central Perimeter 7/12/2016 $79,000,000 380 $207,894 Bell Partners

Arium Westside Midtown 7/18/2016 $74,500,000 336 $221,726 Carroll Organization

The District at Vinings Northwest Atlanta 6/16/2016 $68,750,000 464 $148,168 Sutter Hill Developments

3505 Windy Ridge Pky. Northwest Atlanta 6/23/2016 $68,175,000 434 $157,085 Hudson Group

Stoneleigh at Deerfield North Fulton 6/15/2016 $60,750,000 372 $164,189 IMT Capital

Rock Creek at Vinings Northwest Atlanta 6/22/2016 $57,400,000 403 $142,431 Atlantic | Pacific Co.

1377 Dresden Buckhead 6/24/2016 $51,000,000 215 $237,209 AVR Realty

The Artisan Luxury Apartments Northlake 6/16/2016 $50,000,000 340 $147,058 Fowler Property Acquisition

Oakbrook Pointe Northeast Atlanta 4/28/2016 $49,250,000 684 $72,002 Cortland Partners

Sales Volume AVG Cap Rate

ATLANTA MULTIFAMILY

Atlanta apartment investment volume year-to-date 2016 is right in line with this time last year and on track to finish the year with another $6 billion-plus transacted. Activity was steady in Q2 with $1.7 billion of multi-family projects sold. The average price per unit was $96,075 in Q2 according to Real Capital Analytics. Atlanta’s average cap rate for apartments remained steady at 6.4%.

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

0

1

2

3

4

5

6

7

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

YTD

16

Billions

Atlanta Multifamily Market (continued)

Source: Real Capital Analytics

Source: CoStar Comps

3 Research & Forecast Report | Q2 2016 | Atlanta Multifamily | Colliers International

Metro Atlanta Employment Comparison

METRO AREA RANK Y-O-Y EMPLOYMENT

Y-O-Y PERCENT

UNEMPLOYMENTRATE

Los Angeles/OC 1 154,500 2.7% 4.1%

New York/NNJ 2 143,800 1.5% 4.4%

Dallas-Fort Worth 3 125,300 3.7% 3.5%

Atlanta 4 76,600 3.0% 4.6%

Seattle 5 67,300 3.6% 4.8%

San Francisco 6 64,800 2.9% 3.4%

Miami 7 64,500 2.6% 4.6%

DC-Arlington 8 61,900 1.9% 3.6%

Chicago 9 61,500 1.3% 5.4%

Phoenix 10 58,700 3.1% 4.7%

Philadelphia 11 58,600 2.1% 5.1%

Orlando 12 48,200 4.2% 4.0%

U.S. Total 2,324,000 1.6% 4.5%

> General Electric Co. has picked Atlanta for a $3 million global digital operations center — a project that will create 250 jobs in Midtown. The roughly 30,000 SF center — GE’s first — is a part of the company’s Industrial Internet initiative.

> Marketing software firm Terminus will invest $1.5 million in an expansion that will create more than 100 jobs over the next few years. As part of the expansion, Terminus will sublease nearly 24,000 SF at the Terminus 100 office tower in Buckhead.

> Amazon.com Inc. will build a new 600,000 SF, large item, fulfillment center in Braselton, creating more than 500 jobs.

> Santa Rosa, Calif.-based Keysight Technologies (NYSE: KEYS) will invest $14 million in an Atlanta software development center and create 250 jobs. Keysight will receive up to $100,000 in incentives and have an estimated economic impact of nearly $93 million.

> Buckhead will land a new Fortune 1000 headquarters of the Sandy Springs based fintech company, Global Payments, which is codenamed “Spinoza” in economic development circles, will result in a $18 million investment. In return for bringing 150 high-paying jobs – average annual salaries top $200,000- to Atlanta, the company will receive up to $75,000 in economic incentives from the city.

Metro Atlanta Housing Permit Activity

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD16

Multifam

ily Permits

Issued

Source: U.S. Census Bureau

Metro Atlanta Employment Overview

‐42.2‐23.0

30.2

69.4 66.248.9

‐26.8

‐136.6

‐20.9

35.6 42.459.9

89.0 82.474.0

‐150.0

‐100.0

‐50.0

0.0

50.0

100.0

150.0

Jobs Add

ed/Lost (thou

sand

s)

Source: US Dept. of Labor Statistics/Moody’s Analytics

Source: Bureau of Labor Statistics; Metro Level Data May 2016(p) Average, not Seasonally Adjusted

Notable Atlanta Job Relocations

4 Research & Forecast Report | Q2 2016 | Atlanta Multifamily | Colliers International

Marietta St NW

Gra

y St

NW

Hunnicutt St NW

Mills St NW

Luck

ie S

t NW

Tech

woo

d D

r NW

Tech Pkwy

North Ave NE

Bed

ford

Pl N

E

Myr

tle S

t NE

Peac

htre

e St

NE

Pied

mon

t Ave

NE

Juni

per S

t NE

Penn

Ave

NE

Ponce De Leon Ave NE

Cha

rles

Alle

n D

r NE

4th St NE

8th St NE

9th St NE

10th St NE

7th St NE

6th St NE

5th St NE

Sprin

g St

NW

W P

each

tree

St N

E

10th St NW

Stat

e St

NW

Atla

ntic

Dr N

W

Hemphill Ave NW

Fow

ler S

t NW

Cen

ter S

t NW

Campbellton Rd SW

11th St NE

12th St NE

Felto

n Dr

NE

Bou

leva

rd N

E

3rd St NE

North Ave NW

Pine St NW

26th St NW

28th St NW

Collier Rd NW

Hun

tingt

on R

d N

E

Ottley Dr N

E

Brighton Rd NE

Camden Rd NE

Peachtree St NEDeering Rd NW

Hascall Rd NW

Bishop St NW

Beverly Rd NE

Peachtree Cir NE

17th St NE

16th St NE

Mec

aslin

St N

W

Wal

thal

l Dr N

W

Flagler Ave NEM

onroe Dr NE

Rock Springs Rd NE

Wimbledon Rd NE

BarnesdaleWay NE

Inman Cir NE

NW

Dellwood D

r NW

Peachtree ParkDr NE

Armour Dr NE

Plasters Ave NE

Mon

tgomery Ferry Dr NE

Robin Hood Rd NE Fria

r Tuc

kR

d N

E

Piedmon

t Ave

NE

Westminster Dr NE

14th St NW

13th St NW

Mon

roe

Dr N

E

St Charles Ave NE

Dur

ant P

l NE

Linden Ave NE

Morgan St NE

Pine St NE

Angier Ave NE

Gle

n Iri

s D

r NE

John St NW

Vena

ble

St N

W

Dal

ney

St N

W

14th St NW Mec

aslin

St N

W

16th St NW

Fran

cis

St N

W

Bar

nes

St N

W

Hol

ly S

t NW

Fow

ler S

t NW

Trabert Ave NW

Golf View Rd NW

Bennett St

Maddox Dr NE

17th St NE

Peac

htre

e W

alk

NE

Cre

scen

t Ave

NE

W Hotel

PeachtreePointe

AmtrakStation

Tech

woo

d D

r NW

Midtown

CentennialPlace

CentralPark

SoNo

CentennialHill

AtlanticStation

LoringHeights

TechnologySquare

AnsleyPark

BrookwoodHills

HomePark

CivicCenterPark

BedfordPine Park

PiedmontPark

Winn Park

AnsleyPark

McClatcheyPark

17thStreetPark

LoringHeightsPark

HomePark

Bobby JonesGolf Course

TanyardCreekPark

ArdmorePark

AnsleyGolf Course

GEORGIAINSTITUTE OFTECHNOLOGY

F O R S Y T H C O .

F U L T O N C O .

. O

C

B

B

O

C

COBB CO. DOUGLAS CO.

A

L C

T

Y

. O

C

N

O

FUL T ON CO. COWET A CO.

L U F T . O C N O

F A . O C E T T E Y

.O

C BL

AKE

DL

UFT

.O

C N

O

DEKALB CO. HENR Y CO.

R

N

E

H

Y

. O

C

A

L C

T

Y

. O

C

N

O

. O C S

T T U B

. O

C

B L A K E D

. O

C

E L A D

K C

O

R

. O C E L A D K C O

R

T W

E N

. O C N O

T T

E N

N I W

G

. O C W L

A T

. O C N

O

T T

E N

N I W

G

. O C

. O C B

L A

K E

D

P

. O

C

G

N

I D

L

U

A

R

A

B

T .

O

C

W

O

.

O

C

E

E

K

O

R

E

H

C

L U

F

T .

O

C

N

O

.

O

C

H

T Y

S

R

O

F

DA WSON CO. FORSYTH CO.

PICKENS CO. CHEROKEE CO.

. O C B

B O

C LUFT

.OC NO

L L A H . O C

T T E N N I W G

. O C

OW CO. . O C E E K O R E H C

CHEROKEE CO.

C h a t t a c

h o o c h e

e

R i v e r

C h a

t t a c h o o c h e e

R i v

e r

Allatona Lake

Lake Lanier

316

675

Cartersville

Acworth

W oodstock

Canton

Alpharetta

Cumming

Sugar Hill

Buford

Duluth

Lawrenceville

GAINESVILLE

Braselton

Norcross

Snellville

Stone Mountain

Lithonia

Conyers

Covington

McDonough

Jonesboro

Fayetteville

Peachtree City

Palmetto

DORAVILLE

CHAMBLEE

Clarkston

DECATUR

SMYRNA

Powder Springs

Austell

Douglasville

Lithia Springs

EAST POINT

COLLEGE P ARK HAPEVILLE

Riverdale

FOREST P ARK

Stockbridge

Union City

Fairburn

ATLANTA

Roswell

Mountain Park

MARIETT A

Hartsfield-Jackson International Airport

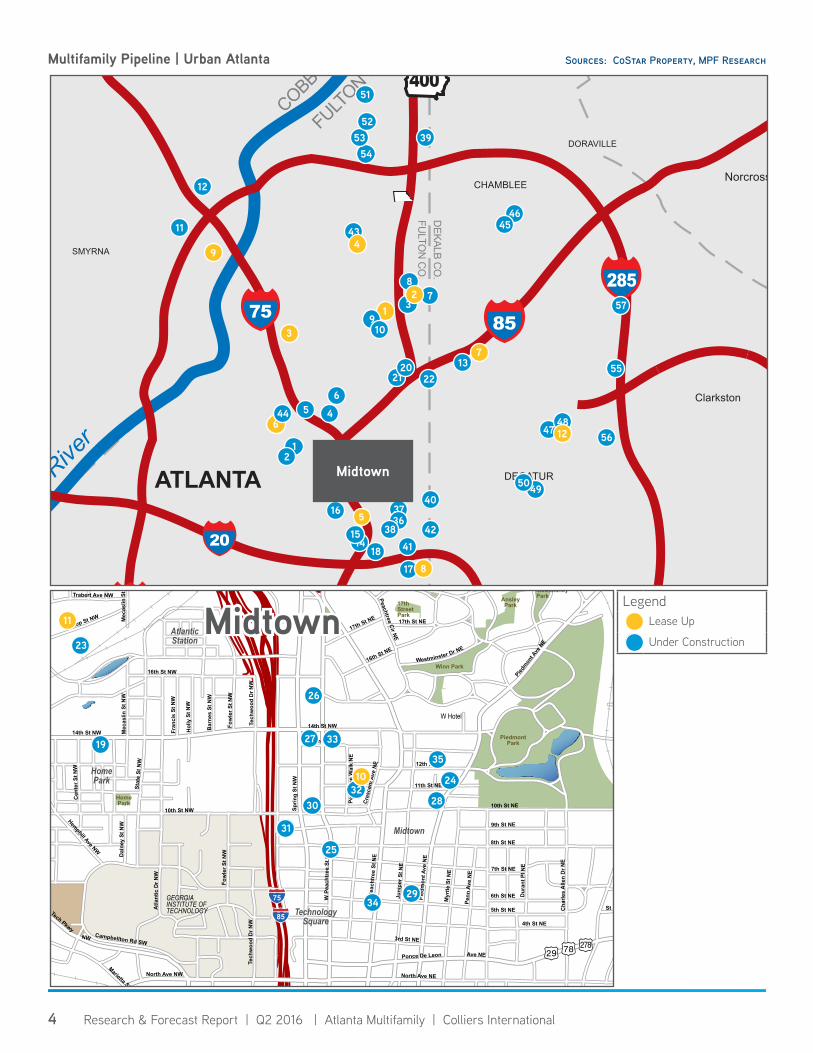

Multifamily Pipeline | Urban Atlanta Sources: CoStar Property, MPF Research

4

55

9

12

3

54

11

7

6

14

1

1

5

9

53

22

18

46

8

47

16

24

3

19

48

17 8

23

2

21

49

6

7

2

11

12

25

26

27

29

30

31

32

51

33

10

10

50

39

3736

42

57

35

52

41

56

38

40

13

34

15

43

20

44

45

5

28

4

LegendLease Up

Under Construction

Midtown

Midtown

5 Research & Forecast Report | Q2 2016 | Atlanta Multifamily | Colliers International

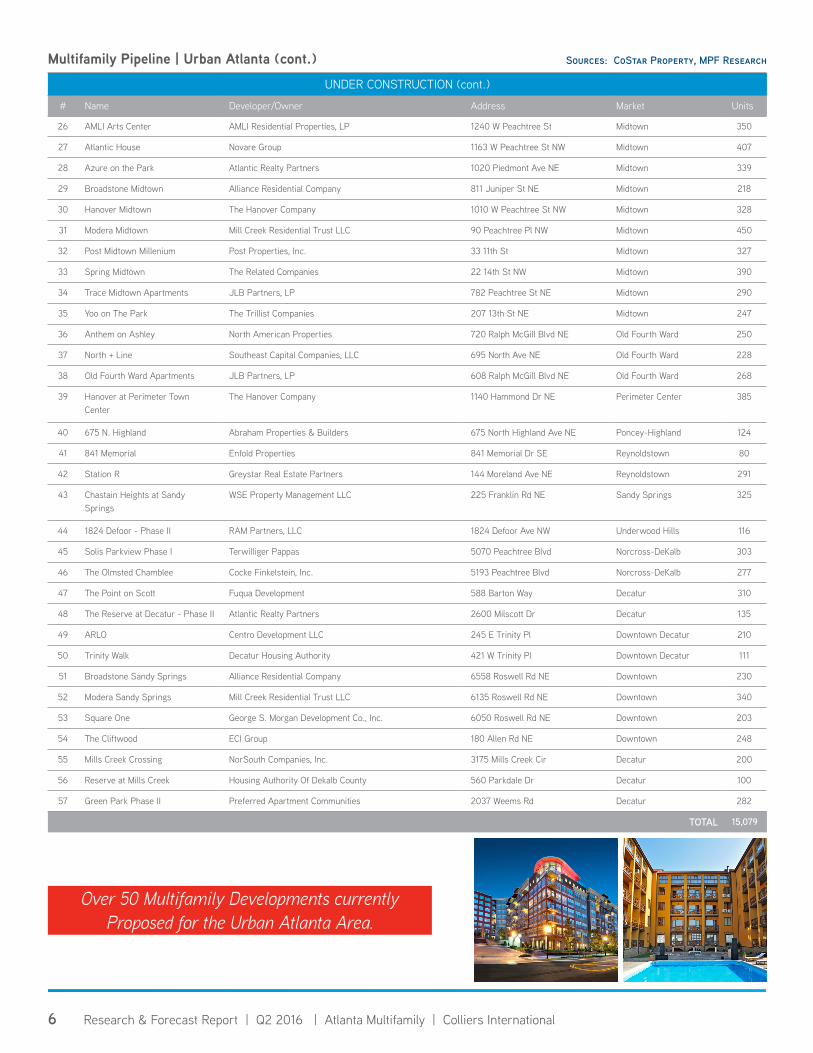

Multifamily Pipeline | Urban Atlanta (cont.) Sources: CoStar Property, MPF Research

UNDER CONSTRUCTION

# Name Developer/Owner Address Market Units

1 Accent Waterworks Westplan Investors 1390 Northside Dr NW Berkeley Park 114

2 Westside Heights WSE Property Management LLC 903 Huff Rd NW Blandtown 282

3 Gables Brookhaven - Phase II 4420 Peachtree Rd NE Brookhaven 242

4 Ardmore & 28th - Phase II Cocke Finkelstein, Inc. 306 Ardmore Cir NW Brookwood 109

5 Millworks Pollack Shores Real Estate Group 1900 Emery St NW Brookwood 345

6 Venue Brookwood Grayco Partners 2140 Peachtree Rd Brookwood 250

7 AMLI 3464 AMLI Residential Properties, LP 3464 Roxboro Rd NE Buckhead 240

8 Domain at Phipps Plaza Columbus Realty Partners, Ltd. 705 Phipps Plz NE Buckhead 320

9 Hanover Buckhead Village The Hanover Company 3116 Roswell Rd NW Buckhead 351

10 Hanover Park Place The Hanover Company 400 Pharr Rd NE Buckhead 375

11 The Battery - Residential Pollack Shores Real Estate Group 2675 Cobb Pky SE Cumberland 550

12 The Metro Audubon Communities 1500 Parkwood Cir SE Cumberland/Galleria 200

13 Accent North Druid Hills - Phase II

Westplan Investors 7 Executive Park Dr NE Decatur 79

14 200 Edgewood Sanctuary Residential LLC 200 Edgewood Ave NE Downtown Atlanta 144

15 Piedmont Central Corvias Campus Living 82 Piedmont Ave NE Downtown Atlanta 376

16 Post Centennial Park Post Properties, Inc. 325 Centenial Olympic Park Dr NW

Downtown Atlanta 438

17 Alexan Glenwood Trammell Crow Residential Company 860 Glenwood Ave SE Grant Park 216

18 The George Urban Realty Partners 301 Memorial Dr SE Grant Park 85

19 The Local On 14th Pollack Shores Real Estate Group 455 14th St NW Home Park 375

20 Overture Linbergh Greystar Real Estate Partners 690 Lindbergh Dr NE Lindbergh-Morosgo 190

21 Piedmont Heights - Phase II AMLI Residential Properties, LP 2323 Piedmont Rd NE Lindbergh-Morosgo 355

22 Cheshire Bridge Apartments Catalyst Development Partners, LLC 2470 Cheshire Bridge Rd NE Lindridge-Martin Manor 282

23 464 Bishop Paces Holdings, LLC 464 Bishop St NW Loring Heights 232

24 Alta at the Park Wood Partners 223 12th St Midtown 198

25 Alta Midtown Wood Partners 915 W Peachtree St NW Midtown 369

LEASE UP

# Name Developer/Owner Address Market Units

1 Broadstone Court Alliance Residential Company 3091 Maple Dr Buckhead 250

2 Gables Brookhaven Gables Residential 4420 Peachtree Rd NE Brookhaven 242

3 Solis Downwood Terwilliger Pappas 3201 Downwood Cir NW West Paces 280

4 The Collection JLB Partners, LP 4600 Roswell Rd Sandy Springs 316

5 The Office Apartments De Bartolo Holdings LLC 250 Piedmont Ave NE Downtown Atlanta 327

6 1824 Defoor RAM Partners, LLC 1824 Defoor Ave NW Underwood Hills 116

7 Accent North Druid Hills Westplan Investors 7 Executive Park Dr NE Decatur 231

8 Alexan EAV Trammell Crow Residential Company 1205 Metropolitan Ave SE East Atlanta 120

9 Alexan Vinings Trammell Crow Residential Company 3330 Cumberland Blvd SE Vinings 232

10 Sixty11th Selig Enterprises, Inc. 60 11th St NE Midtown 320

11 The Heights at West Midtown WSE Property Management LLC 507 Bishop St NW Loring Heights 240

12 The Reserve at Decatur Atlantic Realty Partners 2600 Milscott Dr Decatur 135

TOTAL 2,809

6 Research & Forecast Report | Q2 2016 | Atlanta Multifamily | Colliers International

UNDER CONSTRUCTION (cont.)

# Name Developer/Owner Address Market Units

26 AMLI Arts Center AMLI Residential Properties, LP 1240 W Peachtree St Midtown 350

27 Atlantic House Novare Group 1163 W Peachtree St NW Midtown 407

28 Azure on the Park Atlantic Realty Partners 1020 Piedmont Ave NE Midtown 339

29 Broadstone Midtown Alliance Residential Company 811 Juniper St NE Midtown 218

30 Hanover Midtown The Hanover Company 1010 W Peachtree St NW Midtown 328

31 Modera Midtown Mill Creek Residential Trust LLC 90 Peachtree Pl NW Midtown 450

32 Post Midtown Millenium Post Properties, Inc. 33 11th St Midtown 327

33 Spring Midtown The Related Companies 22 14th St NW Midtown 390

34 Trace Midtown Apartments JLB Partners, LP 782 Peachtree St NE Midtown 290

35 Yoo on The Park The Trillist Companies 207 13th St NE Midtown 247

36 Anthem on Ashley North American Properties 720 Ralph McGill Blvd NE Old Fourth Ward 250

37 North + Line Southeast Capital Companies, LLC 695 North Ave NE Old Fourth Ward 228

38 Old Fourth Ward Apartments JLB Partners, LP 608 Ralph McGill Blvd NE Old Fourth Ward 268

39 Hanover at Perimeter Town Center

The Hanover Company 1140 Hammond Dr NE Perimeter Center 385

40 675 N. Highland Abraham Properties & Builders 675 North Highland Ave NE Poncey-Highland 124

41 841 Memorial Enfold Properties 841 Memorial Dr SE Reynoldstown 80

42 Station R Greystar Real Estate Partners 144 Moreland Ave NE Reynoldstown 291

43 Chastain Heights at Sandy Springs

WSE Property Management LLC 225 Franklin Rd NE Sandy Springs 325

44 1824 Defoor - Phase II RAM Partners, LLC 1824 Defoor Ave NW Underwood Hills 116

45 Solis Parkview Phase I Terwilliger Pappas 5070 Peachtree Blvd Norcross-DeKalb 303

46 The Olmsted Chamblee Cocke Finkelstein, Inc. 5193 Peachtree Blvd Norcross-DeKalb 277

47 The Point on Scott Fuqua Development 588 Barton Way Decatur 310

48 The Reserve at Decatur - Phase II Atlantic Realty Partners 2600 Milscott Dr Decatur 135

49 ARLO Centro Development LLC 245 E Trinity Pl Downtown Decatur 210

50 Trinity Walk Decatur Housing Authority 421 W Trinity Pl Downtown Decatur 111

51 Broadstone Sandy Springs Alliance Residential Company 6558 Roswell Rd NE Downtown 230

52 Modera Sandy Springs Mill Creek Residential Trust LLC 6135 Roswell Rd NE Downtown 340

53 Square One George S. Morgan Development Co., Inc. 6050 Roswell Rd NE Downtown 203

54 The Cliftwood ECI Group 180 Allen Rd NE Downtown 248

55 Mills Creek Crossing NorSouth Companies, Inc. 3175 Mills Creek Cir Decatur 200

56 Reserve at Mills Creek Housing Authority Of Dekalb County 560 Parkdale Dr Decatur 100

57 Green Park Phase II Preferred Apartment Communities 2037 Weems Rd Decatur 282

TOTAL 15,079

Multifamily Pipeline | Urban Atlanta (cont.) Sources: CoStar Property, MPF Research

Over 50 Multifamily Developments currently Proposed for the Urban Atlanta Area.

7 North American Research & Forecast Report | Q4 2014 | Office Market Outlook | Colliers International

Copyright © 2016 Colliers International.The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.

Multifamily Advisory Group | East RegionColliers International | AtlantaPromenade | Suite 8001230 Peachtree Street, NEAtlanta, Georgia | USA+1 404 888 9000

FOR MORE INFORMATIONRon CameronSenior Vice President | Atlanta+1 404 877 [email protected]

Will MathewsVice President | Atlanta+1 404 877 [email protected]

CONTRIBUTORSScott AmosonDirector of Research | Atlanta

Jaime SlocumbTransaction Coordinator | Atlanta

Chevene King, IIIFinancial Analyst | Atlanta

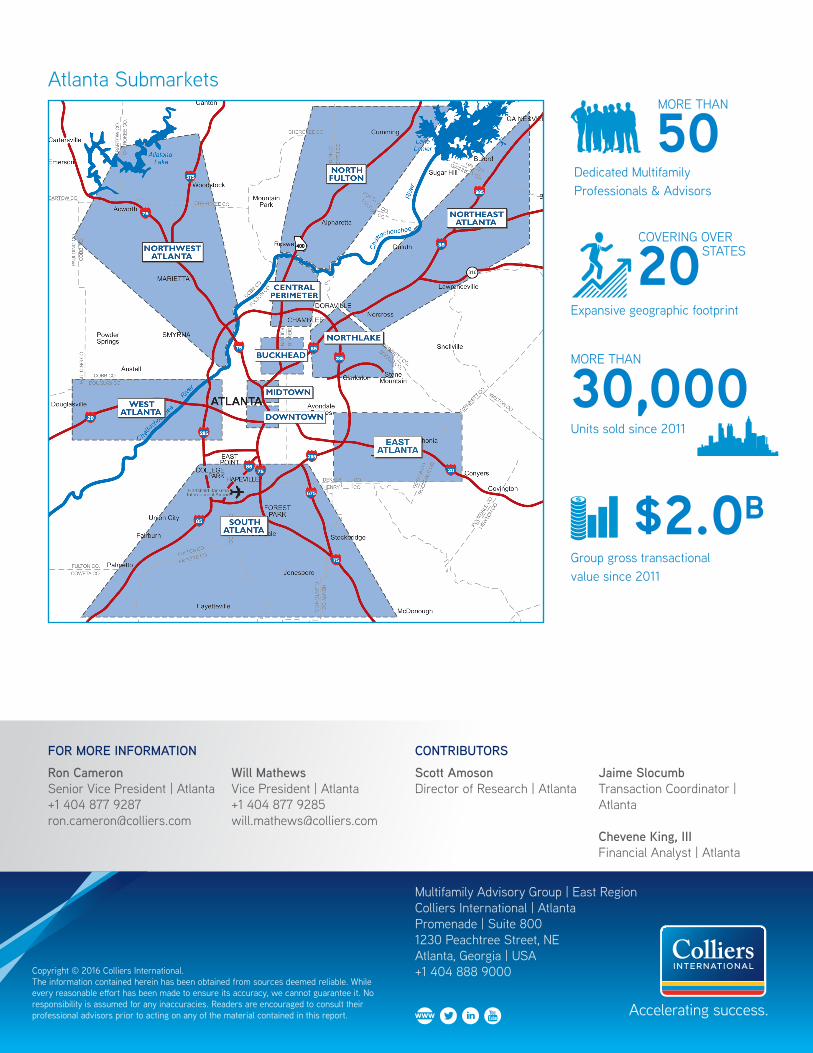

Atlanta Submarkets

Units sold since 2011

30,000MORE THAN

Group gross transactional value since 2011

$2.0B

Dedicated Multifamily Professionals & Advisors

50MORE THAN

Expansive geographic footprint

20COVERING OVER

STATES