Embed Size (px)

Citation preview

Modul ke:

Fakultas

Program Studi

Akuntansi Biaya Cost Systems and Cost Accumulation

Suryadharma Sim, SE, M. Ak

03 Ekonomi dan

Bisnis

S1 Manajemen

Cost Systems and Cost Accumulation

Flow of Costs in a manufacturing enterprise

Cost accounting’s functions include recording and measuring cost elements as

the related resources flow through the production process. All manufacturing

costs, regardless of their fixed or variable behavior, flow through the work in

process and finished goods inventory accounts.

The production process, the physical arrangement of the facility, and the

decision-making need of managers determine how costs will be accumulated.

Typically the general ledger accounts for manufacturing costs are Materials,

Payroll, Factory Overhead Control, Work in Process, Finished Goods, and Cost

of Goods Sold. These accounts are used to recognize and measure the flow of

costs, from the acquisition of materials, through factory operations, to the cost of

product sold.

Cost Systems and Cost Accumulation

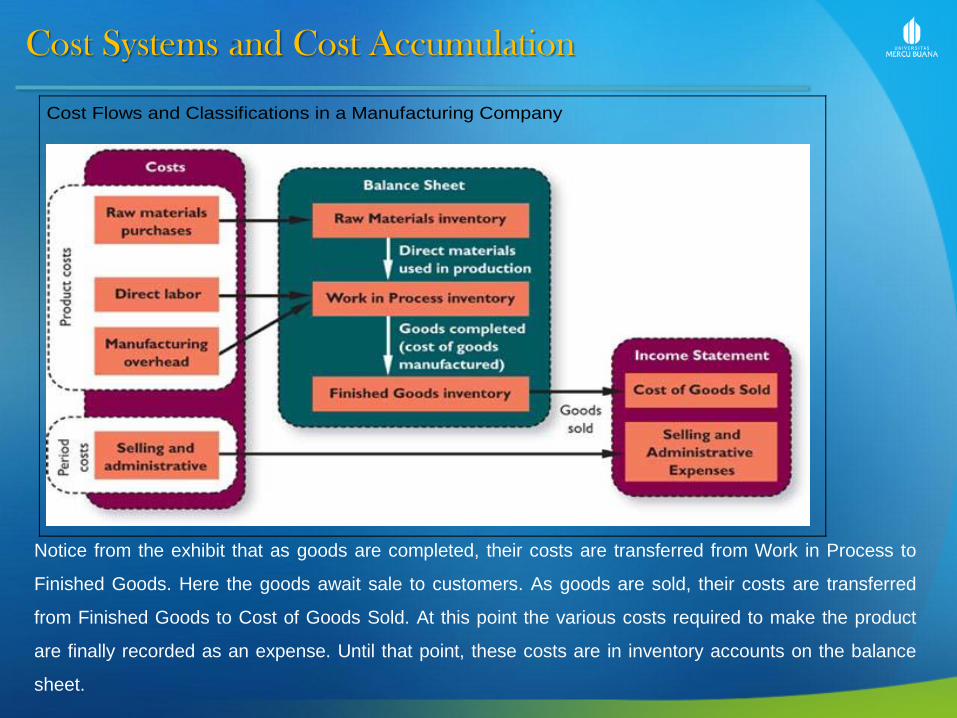

Cost Flows and Classifications in a Manufacturing Company

Notice from the exhibit that as goods are completed, their costs are transferred from Work in Process to

Finished Goods. Here the goods await sale to customers. As goods are sold, their costs are transferred

from Finished Goods to Cost of Goods Sold. At this point the various costs required to make the product

are finally recorded as an expense. Until that point, these costs are in inventory accounts on the balance

sheet.

Cost Systems and Cost Accumulation

An Example of Cost Flows

To provide an example of cost flows in a manufacturing company, assume that a

company’s annual insurance cost is $2,000. Three-fourths of this amount ($1,500)

applies to factory operations, and one-fourth ($500) applies to selling and

administrative activities. Therefore, $1,500 of the $2,000 insurance cost would be

a product (inventoriable) cost and would be added to the cost of the goods

produced during the year. This concept is illustrated in Exhibit 1-8, where $1,500

of insurance cost is added to Work in Process. As shown in the exhibit, this

portion of the year’s insurance cost will not become an expense until the goods

that are produced during the year are sold—which may not happen until the

following year or even later. Until the goods are sold, the $1,500 will be part of

inventories—Work in Process or Finished Goods—along with the other costs of

producing the goods.

Cost Systems and Cost Accumulation

EXHIBIT 1-8

An Example of Cost Flows in a Manufacturing Company

By contrast, the $500 of insurance cost that applies to the company’s selling and

administrative activities will be expensed immediately.

Cost Systems and Cost Accumulation

Reporting the Result of Operation

The results of operations of a manufacturing enterprise are reported

in the conventional financial statements just as they are for any other

form of business. These statements summarize the period’s

operations and show financial position at the end of the period:

Income Statement

Balance Sheet

Statement of Cash Flows

Cost Systems and Cost Accumulation

Cost Systems

Costs that are allocated to units of production may be actual costs or

standard costs. In an actual cost system or historical cost system, cost

information is accumulated as cost is incurred, but the presentation of

results is delayed until all operations of the accounting period have been

performed or, in a service business, until the period’s services have

been rendered. In a standard cost system, products, operations, and

processes are costed based on predetermined quantities of resources

to be used and predetermined prices of those resources. Actual costs

are also accumulated separately, and variances or differences between

actual costs and standard costs are collected in separate accounts.

Cost Systems and Cost Accumulation

The objective of a cost system or costing system is accumulate the

costs of goods or services. The information on the cost of a product

or service is used by managers to set the prices of the product,

control operations, and develop financial statements. Also, the cost

system improves control by providing information on the costs

incurred by each department or manufacturing process.

“COST SYSTEMS DEPENDING ON HOW COSTS OF

PRODUCTION ARE ACCUMULATED”

Cost Systems and Cost Accumulation

Cost Accumulation

Any of the previously mentioned cost system can be used

with job order costing, with process costing, or with other cost

accumulation methods. In job order costing, cost is traced to

an individual batch, lot, or contract. In process costing, cost is

traced to a department, operation, or some other subdivision

within the production facility. A third method, back flush

costing, differs markedly from job order and process costing

Cost Systems and Cost Accumulation

Job Order Costing

A job order cost system provides a separate record for the cost of each quantity of

product passing through the factory. A quantity of each particular product is called

order. A job order cost system fits better in the industries that develop products with

that have different specifications most of the time or that have a wide variety of

products in stock. Many service companies use this type of system for costing

orders by accumulating the costs associated with providing services to their

customers. Some characteristics of the job order cost systems are listed below:

- They accumulate in batches

- Production under specific orders

- Normally does not produces the same article

- Examples: Accounting firm, Construction Company, law practice, apparel

manufacturing, movie studio.

Cost Systems and Cost Accumulation

7 STEPS TO MAKE A JOB ORDER COSTING

1.- Identify the chosen cost-object

2.- Identify the direct costs the job

3.- Select the cost allocation bases

4.- Identify the indirect costs

5.- Calculate the rate per unit

6.- Calculate the indirect costs 7.- Calculate the total cost of the job

Cost Systems and Cost Accumulation

Process Costing

In a process cost system, costs are accumulated for each department or

process in the factory. A process cost system fits more in companies

manufacturing products which are not distinguishable with each other during a

process of continuous production. Some characteristics of process cost

systems are listed below:

- They accumulate costs by department

- Production continuous and homogeneous

- Examples: Oil Refinery, food processing, paper processing, soft drinks,

medicines, buckets, toys, pants.

"When" should the cost of production be determined?

- Before we begin the process - Default costs (estimated or standard)

- After or at the same time of the process - Actual costs (current or historical).

Cost Systems and Cost Accumulation

PROCESS COSTING FLOW

Cost Systems and Cost Accumulation

5 STEPS TO ACHIEVE A PROCESS COSTING

1.- Summarize the physical flow of the units to produce

2.- Calculate production in terms of equivalent units

3.- Calculate equivalent unit costs

4.- Summarize total costs to account for

5.- Assign total costs to the units already completed and to

units in ending work in process inventory (WIP).

Cost Systems and Cost Accumulation

Blended Methods

In some manufacturing, different units have significantly

different direct material costs, but all units undergo identical

conversion in large quantities. In these cases, direct

materials costs are accumulated using job order costing,

and conversion costs are accumulated using process

costing.

Cost Systems and Cost Accumulation

Backflush Costing

Backflush costing is a workable way to accumulate manufacturing costs in a

factory or part of a factory in which processing speeds are extremely fast, such

as in a mature Just In Time system. Backflush costing is workable because it

bypasses the routine cost accounting entries that are required in subsidiary

records for job order and process cost accumulation, thus saving considerable

data processing time. Where there is insufficient time and insufficient incentive

to track the detailed costs of work in process, backflushing provides a method

of cost accumulation by working backward through the available accounting

information after production is completed; that is, at the end of each accounting

period.

Terima Kasih Suryadharma Sim, SE, M. Ak