Embed Size (px)

Citation preview

Thomas Weisel Partners does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Customers of Thomas Weisel Partners in the United States can receive independent, third-party research on the company or companies covered in this report, at no cost to them, where such research is available. Customers can access this independent research at www.tweisel.com or can call (877) 921-3900 to request a copy of this research. Investors should consider this report as only a single factor in making their investment decision.

Please see analyst certification and other important disclosures

starting on page 70 and continuing through page

70.

Equity Research

A Primer on Energy Efficiency Conservation Gets a New Name

A White Paper on a Facet of the Industrial Growth Sector

Alternative Energy Jeff Osborne 212.271.3577 [email protected] Scott Reynolds 212.271.3429 [email protected] Dilip Warrier 415.364.2983 [email protected] January 31, 2008

A Primer on Energy Efficiency Conservation Gets a New Name

Table of Contents

Executive Summary.........................................................................................................................................................5 Alarming Expected Energy Use Calls for A Response...............................................................................................6 The Commercial and Industrial Market for Green Buildings....................................................................................8 The Healthcare Market for Green Buildings ............................................................................................................ 12 The Education Market for Green Buildings ............................................................................................................. 13 The Residential Market For Green Buildings ........................................................................................................... 13 Leadership in Energy and Environmental Design Standards Becoming Synonymous with Green Building.. 17 Regulation: Government Is Stepping Up to the Plate for Energy Efficiency ...................................................... 20 The 2007 Energy Bill.................................................................................................................................................... 21 Materials: Major Products and Trends in Energy Efficiency.................................................................................. 23 Lighting .......................................................................................................................................................................... 23 Types of Lights.............................................................................................................................................................. 27 Heating, Ventilation and Air-Conditioning (HVAC)............................................................................................... 37 Understanding Efficiency Measures........................................................................................................................... 42 HVAC Controls ............................................................................................................................................................ 48 Equipment ..................................................................................................................................................................... 51 Water Use....................................................................................................................................................................... 56 The Building Envelope ................................................................................................................................................ 57 Windows ........................................................................................................................................................................ 57 Insulation ....................................................................................................................................................................... 62 Foundations................................................................................................................................................................... 65 Roofs .............................................................................................................................................................................. 66 Walls ............................................................................................................................................................................... 67 Examples of “Green Buildings” ................................................................................................................................. 68

January 31, 2008 Thomas Weisel Partners LLCPage 5 of 71 Jeff Osborne 212.271.3577

A Primer On Energy Efficiency Conservation Gets a New Name

EXECUTIVE SUMMARY

Conservation gained a bad name in the 1980’s when President Ronald Reagan referred to it as being “cold in the winter and hot in the summer”. With the resurgence of high energy prices, however, energy usage has once again been pushed to the front burner, but this time with a new name and concept. Energy efficiency is the idea that energy can be used in a better way, while providing a product that is superior to the previous at little or no extra cost. It is essentially educating people that the products and services needed to reduce energy use exist now and do not involve turning down lights or wearing several sweaters in the winter. The purpose of this white paper is to present a comprehensive overview of energy efficiency as well as the opportunities that exist for the “Green” building market.

Energy consumption is expected to increase some 25 quadrillion Btu by 2030, according to the International Energy Agency (IEA), which carries an estimated price tag of $10 trillion for electricity generation, transmission and distribution assets alone. A significant amount of progress toward addressing tomorrow’s energy needs can be met through efficiency measures. Today’s buildings and appliances are horribly inefficient. For example, an incandescent light bulb wastes 90-95% of the energy it uses in the form of heat, a major problem in areas that have heavy cooling loads. Also, the majority of the electricity used by buildings is generated by coal combustion, a process in which 70-80% of the energy consumed is given off in the form of waste heat. Producing energy close to the source would allow that wasted heat to be recovered and used in heating and cooling, thereby increasing the efficiency to over 90%. Because buildings account for 40% of all the energy used in the United States and 72% of all the electricity consumed, their efficiency is slated to become an increasing social and political issue.

In total, the residential and commercial building market is close to a $1.2 trillion per year market. Yet, green commercial buildings only represent roughly 2% of the overall market; this percentage is even lower on the residential side. Given an expected 10% per year growth in the green buildings market, this area represents one of the greatest business opportunities of the 21st century.

Perhaps the most striking thing about the energy efficiency concept is relevant products not only exist today, but they are typically superior and achieve this at little or no extra cost (all without the need for government subsidies). The multidisciplinary nature of the industry, however, will require products, installers and services to work together to be effective. So, in this industry, we favor companies offering fully integrated energy solutions that are able to prove their cost effectiveness, while improving the product they are replacing. In the past, many consumers have been burned by promises of energy conservation that resulted in the acceptance of sub par products; such a scenario is unlikely to play out today. The need to prove energy savings will also likely lead to the need for whole building software and metering solutions, a segment we also feel will grow in the coming years.

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 6 of 71 Jeff Osborne 212.271.3577

ALARMING EXPECTED ENERGY USE CALLS FOR A RESPONSE

At about $298 billion in sales in 2005, the electric power industry is one of the largest in the United States and represents roughly 3% of U.S. real GDP, according to the Edison Electric Institute. On a business as usual case, the Department of Energy estimates that by 2030, 508 coal steam plants, 31 nuclear plants, 330 combined cycle and 564 combustion turbine plants will need to be built to satisfy future expected demand: a tremendous amount of capital even for this large industry. Investment in generation, transmission and distribution assets to meet required demand is expected to be $10 trillion between 2005 and 2030, according to the International Energy Agency (IEA).

U.S. Electric Power Sector Power Plant Additions Needed to Meet Future Electricity Demand

Electric Generator Typical New Palnt Capacity (MW) 2010 2015 2020 2025 2030 TotalCoal Steam 600 19 30 70 147 242 508Combined Cycle 400 42 47 68 85 88 330Combusion Turbine 160 28 47 87 141 261 564Nuclear Power 1000 - 1 9 9 12 31Pumped Storage 142 - - - - - -Fuel Cells 10 - - - - - -Conventional Hydropower 5 4 4 30 42 42 122Geothermal 50 4 5 10 13 17 49Municipal Solid Waste 30 7 19 19 19 21 85Wood and Other Biomass 80 2 2 4 10 22 40Solar Thermal 100 1 2 2 2 2 9Solar Photovoltaic 5 9 21 37 55 72 194Wind 50 147 162 165 165 167 806Total 262 340 501 691 947 2741

Distributed generation 150 1 3 13 34 71 122

US Electric Power sector Power Plant additions Needed to Meet Future Electricity Demand

Source: 2007 Buildings Energy Data Book

U.S. Electricity New Generation by Plant Type (Billion kW Hours)

Electricity NGas Coal Renewable Nuclear Total1990 265 118 1560 324 577 29012000 399 98 1911 316 754 36382005 546 111 1956 323 780 38832010 658 82 2090 370 789 42092020 776 89 2418 416 885 47812030 609 92 3191 434 896 5402

US Electricity Net Generation by Plant Type

Source: 2007 Buildings Energy Data Book

Energy efficiency, especially in buildings, has a chance to supplant a meaningful proportion of the projected energy need. The EIA reports that in 2005, buildings consumed 40% of all energy in the United States and 72% of all the electricity produced; yielded 38% of all carbon dioxide emissions and 36% of all greenhouse gas emissions; and accounted for 80% (or $238 billion) of total U.S. electricity expenditures. A 5% increase in building efficiency would translate to roughly 78 billion kW hours of electricity saved at 2005 levels, or roughly $5 billion at a national $0.06-0.07 per kW price.

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 7 of 71 Jeff Osborne 212.271.3577

Consider these facts from the 2007 Buildings Energy Data Book concerning U.S. buildings:

• Buildings now use 72% of all electricity and account for 80% of all electric expenditures.

• “Internal gains” account for as much as 27% of a home’s cooling load.

• The average new single-family home has increased in size by about 700 square feet since 1980.

• In 2006, 50% of all new homes were built in the South, meaning the energy used in cooling is going up.

• U.S. buildings’ carbon dioxide emissions (630 million metric tons of carbon) approximately equal the combined emissions of Japan, France and the United Kingdom.

• Lighting uses more energy than cooling in the residential sector. This underscores the importance of breakthrough lighting technologies.

• In 2001, lighting consumed 756 Billion kWh, according to the U.S. Lighting Market Characterization Report 2002. In 2001, according to the Annual Energy Review 2003, the United States’ 104 nuclear generating units produced 769 billion kWh while operating at a capacity factor of 89%. Therefore, it takes the United States’ entire nuclear fleet to illuminate the country.

Energy efficiency, as opposed to the generation-focused side of the energy debate, is available now and at little or no extra cost to the consumer, all while typically increasing the levels of comfort and satisfaction of the products. Although it would possibly be the largest beneficiary of a move to increased energy efficiency, the building sector is wrought with issues with regard to implementing changes. The sector is highly fragmented and multidisciplinary. Local authorities, capital providers, developers, agents and owners all have a role in the construction of a building, with some having little incentive to change their building habits. Just as consumers have moved to more fuel-efficient vehicles with rising gas prices, they will also call for more efficient buildings when energy costs become too great to ignore.

The multidisciplinary nature of the industry will require products, installers and services to be effective. In the past, many consumers have been burned by promises of energy conservation that resulted in the acceptance of sub par products; such a scenario is unlikely to play out today. The need to prove energy savings will also likely lead to the need for whole building software and metering solutions, a segment we also feel will grow in the coming years. So, in this industry, we believe the companies most likely to succeed are those offering fully integrated energy solutions that are able to prove their cost effectiveness, such as incumbents General Electric, Honeywell, Johnson Controls, United Technologies and Siemens, as well as newer companies such as EnerNOC, Comverge, Orion Energy Systems, PowerSecure, Echelon and Verdiem, among others. We note the increasing level of venture capital interest in energy efficiency, which we expect to continue, should fuel the entrance of new companies into the space. We also expect to see increasing acquisition and investment activity by the incumbents, including buying companies to strengthen their position, just as GE has done with its stake in Orion Energy Systems.

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 8 of 71 Jeff Osborne 212.271.3577

THE COMMERCIAL AND INDUSTRIAL MARKET FOR GREEN BUILDINGS

In 2005, the value of commercial construction was $285.9 billion, while the value of building improvements and repairs was $177.4 billion. As of 2003, office space encompasses the largest portion of the market at 17%, with retail/malls second at 16%. Commercial floor space has its largest concentration in the southern part of the United States, with 37% of the overall space. If the market for green building was roughly 2% in 2005, as stated by the McGraw-Hill in its “The Greening of Corporate America” study, it would be approximately $5.7 billion, while the value of improvements and repairs would be $3.5 billion. With the relatively low penetration of green building into the traditional buildings market, we believe there is substantial room for growth in the coming years.

The median lifetime of a commercial building can range anywhere from 65 to 80 years, a substantial amount of time in terms of the innovation that takes place. As energy costs cut deeper into corporate budgets, we would expect the retrofit market for these older buildings to grow. While it is unlikely that a 40 year old building will have the same HVAC system and lighting system, it is a possibility that the insulation (or lack there of) and windows will be the same, and both represent substantial holes in the building envelope. In the future, integrated HVAC and lighting control systems should become more popular in the retrofit market as wireless systems arrive, eliminating the need to run wire through already existing walls (a time-consuming and expensive job).

Commercial Building Median Lifetimes and Commercial Floorspace by Region

Building TypeHealth Care 65Food Sales 65Food Service 65Lodging 69Mercantile and Service 65Assembly 80Large Office 73Small Office 73Education 80Warehouse 80Other 75

Commercial Building Median Lifetimes (years)

Region TotalNortheast 20%Midwest 25%South 37%West 18%

Share of Commercial Floorspace by Region

Source: 2007 Buildings Energy Data Book

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 9 of 71 Jeff Osborne 212.271.3577

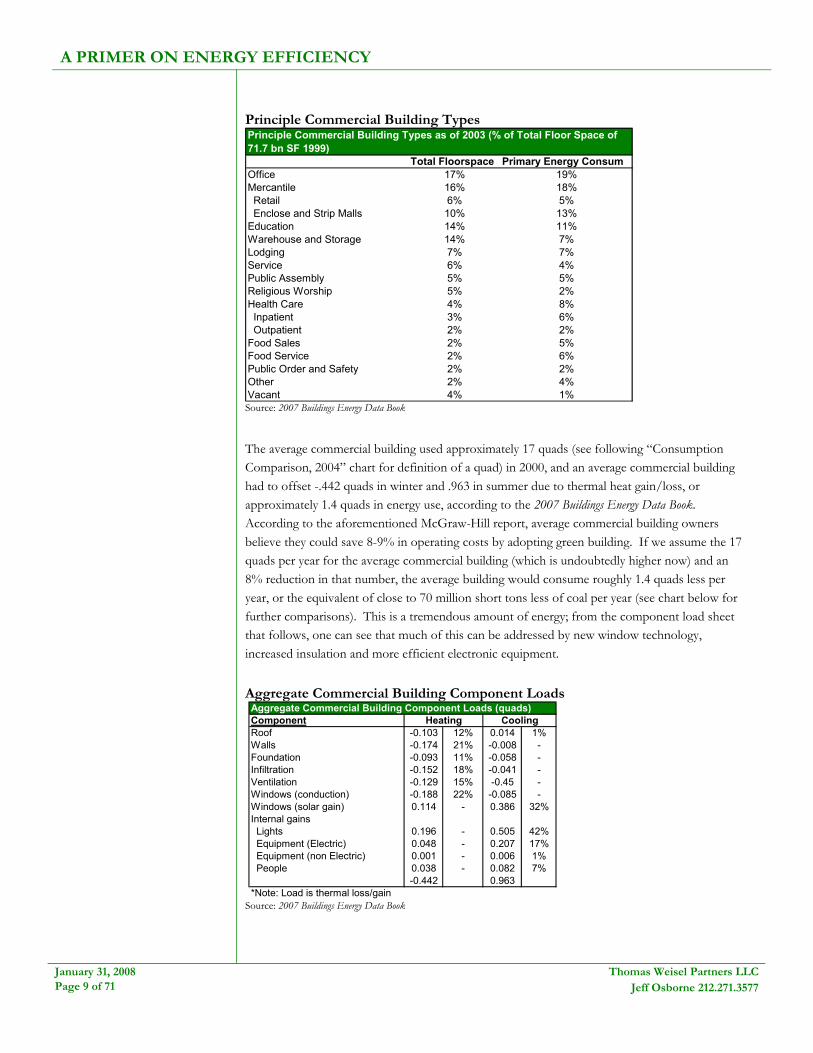

Principle Commercial Building Types

Total Floorspace Primary Energy ConsumOffice 17% 19%Mercantile 16% 18% Retail 6% 5% Enclose and Strip Malls 10% 13%Education 14% 11%Warehouse and Storage 14% 7%Lodging 7% 7%Service 6% 4%Public Assembly 5% 5%Religious Worship 5% 2%Health Care 4% 8% Inpatient 3% 6% Outpatient 2% 2%Food Sales 2% 5%Food Service 2% 6%Public Order and Safety 2% 2%Other 2% 4%Vacant 4% 1%

Principle Commercial Building Types as of 2003 (% of Total Floor Space of 71.7 bn SF 1999)

Source: 2007 Buildings Energy Data Book

The average commercial building used approximately 17 quads (see following “Consumption Comparison, 2004” chart for definition of a quad) in 2000, and an average commercial building had to offset -.442 quads in winter and .963 in summer due to thermal heat gain/loss, or approximately 1.4 quads in energy use, according to the 2007 Buildings Energy Data Book. According to the aforementioned McGraw-Hill report, average commercial building owners believe they could save 8-9% in operating costs by adopting green building. If we assume the 17 quads per year for the average commercial building (which is undoubtedly higher now) and an 8% reduction in that number, the average building would consume roughly 1.4 quads less per year, or the equivalent of close to 70 million short tons less of coal per year (see chart below for further comparisons). This is a tremendous amount of energy; from the component load sheet that follows, one can see that much of this can be addressed by new window technology, increased insulation and more efficient electronic equipment.

Aggregate Commercial Building Component Loads

ComponentRoof -0.103 12% 0.014 1%Walls -0.174 21% -0.008 -Foundation -0.093 11% -0.058 -Infiltration -0.152 18% -0.041 -Ventilation -0.129 15% -0.45 -Windows (conduction) -0.188 22% -0.085 -Windows (solar gain) 0.114 - 0.386 32%Internal gains Lights 0.196 - 0.505 42% Equipment (Electric) 0.048 - 0.207 17% Equipment (non Electric) 0.001 - 0.006 1% People 0.038 - 0.082 7%

-0.442 0.963*Note: Load is thermal loss/gain

Aggregate Commercial Building Component Loads (quads)Heating Cooling

Source: 2007 Buildings Energy Data Book

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 10 of 71 Jeff Osborne 212.271.3577

Consumption Comparison, 2004 Consumption Comparisons in 2004

One quad equals:49 million short tons of coalenough coal to fill a train of railroad cars 4,450 miles long (about one and a half times across the U.S.)971 billion cubic feet natural gas8 billion gallons of gasoline = 21 days of U.S. gasoline use19.8 million passenger cars each driven 12,500 miles17.0 million light-duty vehicles each driven 12,200 milesall new passenger cars and light-duty trucks sold, each driven 11,500 miles12.7 million stock passenger cars, each driven 11,500 miles = 9% of all passenger cars, each driven 11,500 milesall new passenger cars each making 6 round-trips from New York to Los Angeles172 million barrels of crude oil = 15 days of U.S. imports = 177 days of oil flow in the Alaska pipeline at full capacitythe amount of crude oil transported by 483 supertankers

the approximate annual primary consumption of any one of the following states: Arkansas, Connecticut, Iowa, Kansas, Mississippi, Oregon, or West Virginia

Quad: Quadrillion Btu (10^15 or 1,000,000,000,000,000 Btu)Generic Quad for the Buildings Sector: One quad of primary energy consumed in the buildings sector (includes the residential and commercial sectors), apportioned between the various primary fuels used in the sector according to their relative consumption in a given year. To obtain this value, electricity is converted into its primary energy forms according to relative fuel contributions (or shares) used to produce electricity in the given year.Electric Quad (Generic Quad for the Electric Utility Sector): One quad of primary energy consumed at electric utility power plants to supply electricity to end-users, shared among various fuels according to their relative contribution in a given year. (Note: The consumption of an electric quad results in the delivery of just under 1/3 the electric quad due to generation and transmission losses.)

21 hours of world energy usethe electricity delivered from 235 coal-fired power plants (200-MW each) in one yearthe electricity delivered from 37 nuclear power plants (1000-MW each) in one yearaverage annual per capita consumption of 2.9 million people in the U.S.

Primary Energy: The total energy consumed by an end-user, including the energy used in the generation and transmission of electricity. Also referred to as "source" energy.Delivered Energy: The energy consumed by an end-user on site, not including electricity generation and transmission losses.

Source: 2007 Buildings Energy Data Book

Corporate Sediment

It is not surprising that with energy costs at all-time highs, individuals and companies have acknowledged that energy efficiency and sustainable building techniques are going to be increasingly important going forward. According to a McGraw-Hill report entitled The Greening of Corporate America, 82% of surveyed corporations will be greening at least 15% of their real estate portfolio by 2009. Turner Construction supports that claim with its findings that 87% of industry executives report their green building activities will be increasing over the next three years, including 43% reporting a substantial increase. On the residential side, Turner predicts the market will be $20 billion by 2010, up substantially from an estimated $2 billion in 2005.

Although commercial and residential owners understand the benefits derived from sustainable building practices, many are not pursuing them. In the McGraw-Hill study, 80% of businesses have never conducted an energy audit, while only 29% have invested in energy efficient computers, according to research done by Intel. In 2006, the U.S. Green Building Council (USGBC) reported only 775 million square feet of commercial space registered under their LEED certification, or roughly 2% of the commercial space in the United States. Although it is likely the number of “green” buildings is greater than 2%, that figure shows the minimal

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 11 of 71 Jeff Osborne 212.271.3577

penetration of total building sustainability measures within the market. The 2005 McGraw-Hill Greening of Corporate America study estimates that green buildings will comprise 5-10% of the commercial construction market by 2010. In the 2007 report, McGraw-Hill’s poll of the commercial construction market place revealed the perceived business advantages in green building:

• Operating cost decreases: 8-9%

• Building value increase: 7.5%

• Return on investment improvement: 6.6%

• Occupancy ratio increases: 3.5%

• Rent ratio increases: 3%

According to the McGraw-Hill study, the largest groups of companies are concentrated on compliance and instituting profitable greening practices; overall there is still a heavy weighting to legally compliant only companies. Still important though is that 43% of all the survey respondents see green activities and building as being part of their company’s growth strategy. Also, as illustrated in the following charts, the percentage of companies “significantly” involved in green building continues to grow: from 7% in 2005 to 24% in 2007. The study projects that a “tipping point” will occur somewhere in the 2009 timeframe, when the number of companies dedicated to green building will overtake the segment exploring action: a move likely to accelerate the growth in the green building market.

Company’s Role in Green Actions Stage Description

Stage 1Green is not part of the company's mission and at times may weaken the company's effectiveness.

Stage 2Green enters into the company mission as it is legally required and is viewed as a cost.

Stage 3

The company considers the proactive applications of green to be consistent with the profit mission. However, the company has not built green concepts into its technologies, policies and operations on an institution-wide basis.

Stage 4

The company is transforming into a green organization. Green is viewed more as an opportunity than a cost. The company sees competitive advantage from sustainability initiatives.

Stage 5

The company is driven by a passionate value-based commitment to improving the well-being of the company, society and the environment. The company approaches business as a holistic, restorative company.

Company's Role in Green Actions

11%

32%

40%

15%

3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Stage 1 Stage 2 Stage 3 Stage 4 Stage 5

Source: McGraw-Hill study, The Greening of Corporate America

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 12 of 71 Jeff Osborne 212.271.3577

Level of Corporate Building Green Building Tipping Point Level of Corporate Green Building Over Time

37%27% 19%

56%62%

56%

7% 11%24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007

Signif icantly Involved (30%+ ofportfolio)

Moderate Involvement (up to30% of portfolio)

Exploring Action (lowinvolvement)

Corporate America Green Building Tipping Point

74%

60%

45%

30%

15%

2% 2%8%

14%20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2005 2006 2007E 2008E 2009E

% o

f Pop

ulat

ion

Exploring Action (<16% ofprojects green)Largely Dedicated to GreenBuilding (60%+ of portfolio)

Source: McGraw-Hill study, The Greening of Corporate America

While increasing energy costs continue to be the largest driver of the shift toward greening building practices, other sources are increasingly leading companies to view not going green as a liability. This is especially prevalent among larger businesses (i.e., revenue greater than $2.5 billion), which have faced increasing public and shareholder pressure. The McGraw-Hill study, The Greening of Corporate America, found that 75% of the respondents were primarily concerned with increasing energy costs, 40% considered government regulations and incentives and 26% were concerned about global influences. Large companies are also more likely to quickly embrace green practices because they can afford to hire the expertise necessary to do so. The number one reason for not fully implementing green practices was that it was “too-multi-disciplinary”, and did not fit within the current corporate structure. In the future, it is likely that energy management will be outsourced by companies too small to acquire the expertise, making it a more substantial part of corporate strategy.

THE HEALTHCARE MARKET FOR GREEN BUILDINGS

Healthcare construction is the fourth largest segment in the U.S. commercial construction segment; McGraw-Hill projected the market in 2007 was $23.7 billion and the green building segment is expected to grow 5-10% annually until 2010. In 2005, healthcare building peaked at 107 million square feet, and is likely to continue to pull in from those levels, but 2010 and beyond could see stronger growth as the aging population will provide a need for new facilities. A study done by McGraw-Hill Construction found that healthcare is viewed as likely to be the fifth fastest growing segment within green building.

A study done by Turner Construction Company perceived an increase in green building. According to the survey, 87% of construction industry respondents expect green building to increase over the next three years, with 34% expecting a rapid increase. Tied for the top reason to build green are enhanced staff and patient health as well as operational cost savings. Obstacles to the greening of healthcare are similar to other commercial construction: lack of knowledge or too multidisciplinary; cost and time of approval; and lack of product information. Hospitals do require a great deal of energy to run equipment, especially continuous monitors. This is, however, a relatively small cost for a typical hospital, so a large focus has not been placed on energy cost savings. Also, hospitals are 10 times the size of a typical commercial building, so the projects are particularly sensitive to perceived extra costs and possible budget

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 13 of 71 Jeff Osborne 212.271.3577

overruns. Because of their large size and position, hospitals tend to be very risk adverse, making it difficult to push them toward greener practices.

THE EDUCATION MARKET FOR GREEN BUILDINGS

In 2007, the education market was projected to be $53 billion, making it the largest share of commercial construction at 27% of the market. McGraw-Hill expects the green education market to grow at a faster rate (5-10% by 2010) than the underlying commercial construction market. Older K-12 schools (42 years old on average) in conjunction with higher enrolment in colleges should drive the education construction market going forward. A study done by McGraw-Hill Construction found that education is viewed as likely to be the fastest growing segment within green building.

Perceived advantages of green building were a 10% decrease in operating costs, 6% increase in building value and a 14% decrease in energy used. McGraw-Hill estimates that annual utility costs for new schools utilizing green building could actually decrease from 20-40%, while renovated schools could decrease from and 20-30%. McGraw-Hill also estimates that energy reduction would be 40% and anticipated water reduction of up to 30%. The largest reason cited for building green is lower operating costs, but the industry is working on educating the consumer about the environmental and health benefits also associated with such building.

THE RESIDENTIAL MARKET FOR GREEN BUILDINGS

After the record building of 2005, building starts fell to 1.33 million in 2006, and McGraw-Hill estimates that housing starts will end down further from that in 2007. Although McGraw-Hill predicts 2008 declines will be less than 2006 and 2007, and 2009 will stabilize, all indications suggest that the residential housing market is not what one would consider strong. Differentiation among builders will be increasingly important in this falling market, and it seems that the green builders could capture an advantage.

Single Family Housing Starts

Single Family Housing Starts

0

200

400

600

800

1000

1200

1400

1600

1800

2000 2001 2002 2003 2004 2005 2006 2007

Year

thou

sand

s of

uni

ts

Source: McGraw-Hill Construction, 2007

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 14 of 71 Jeff Osborne 212.271.3577

In 2005, the value of residential construction market was $490 billion, while the value of building improvements and repairs was $215 billion. Exhibited below is the total cost of a typical 2,150 square foot house as well as an illustration indicating that the average constructed house size in 2006 was 2,469 square feet. As can be seen by the cost breakdown, a relatively small portion of the overall cost of a house is attributed to HVAC, lighting and appliances, while the largest portions go to framing, walls/finish and property features. Here, it is important to recognize that the main features that will make a house more energy efficient are not large sellers of a home. HVAC, windows, insulation, etc. are not typically as large of a focus to the average home buyer as more noticeable things that enhance appearance. That is why such a large portion of the house’s overall cost is attributed to wall/finish and property features.

Construction Cost Breakdown and Construction Statistics

CostFinished Lot 62,539 24%Construction Cost Inspection/Fees 4,057 2% Shell/Frame Framing 29,928 11% Windows/Doors 9,940 4% Exterior Finish 10,939 4% Foundation 15,610 6% Wall/Finish Trim 27,301 10% Flooring 6,978 3% Equipment Plumbing 8,552 3% Electrical Wiring 5,456 2% Lighting Fixtures 1,510 1% HVAC 5,972 2% Appliances 2,095 1% Property Features 17,000 6%Financing 4,985 2%Overhead and General E 15,139 6%Marketing 3,716 1%Sales Commissions 8,940 3%Profit 24,350 9%Total 265,036 100%

1998 Cost Breakdown of a 2,150 Square Foot, New Single-Family Home (2005 dollars)

Construction Statistics1000 units Average Sq Ft

1990 966 20902000 1242 22662005 1636 24342006 1654 2469

Source: 2007 Buildings Energy Data Book

Unlike the residential building market, the residential remodeling and renovation market has remained relatively consistent; it is valued by the U.S. Census bureau at roughly $200 billion in 2006, with others estimating over $300 billion, according to McGraw-Hill. This places the residential remodeling and renovation market at approximately the same size as the entire commercial construction market. According to the Global Insight and Home Improvement Research Institute, the residential remodeling and renovation market should decline slightly by 1.3% in 2007, but has an expected long-term growth rate of 5% annually over the next four years. The Institute expects the market to grow to $394.1 billion by the end of 2012.

Remodeling is also dependent on the age of the housing stocks. As seen below, the Northeast and Midwest have a large number of houses built before 1939. Also, the Midwest happens to have the highest incidence of plumbing, cabinet and window replacement.

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 15 of 71 Jeff Osborne 212.271.3577

Age of Housing Stocks Age of House Stocks

0 2 4 6 8 10

Built 2000 or later

Built 1990 to 1999

Built 1980 to 1989

Built 1970 to 1979

Built 1960 to 1969

Built 1950 to 1959

Built 1940 to 1949

Built 1939 or earlier

million of units

MidwestNortheastSouthWest

Source: McGraw-Hill, The Green Home Owner Report

Green building activity in the residential space has largely centered on the South and the West. Though the largest gains in efficiency could potentially come from the East and Midwest, the majority of the new building has been concentrated in the South and West. The following exhibit shows the states with the largest penetration of Energy Star Qualified Homes as a percentage of new single-family housing permits. McGraw-Hill Construction, which has more stringent guidelines for its definition of a green home, puts Texas at the top of its list for 2006, followed by Florida, Washington, Colorado and Nevada. Buyers of green homes, as reported by McGraw-Hill, are highest in the South at 42%, with the West at 32%, Midwest at 16% and East at 10%.

Energy Star Qualified New Single Family Homes versus Homes Completed by Region

Nevada 18.9 71%Alaska 1 64%Iowa 5.9 57%Texas 60.8 37%Hawaii 2.1 37%Arizona 20.1 36%New Jersey 5.4 31%Delaware 1.2 24%Vermont 0.5 24%Connecticut 1.6 23%California 18.1 17%New Hampshire 0.8 17%Utah 3.6 16%Ohio 3.5 13%New York 2.6 13%Florida 3.3 2%

Market Indices for 2006 Energy Star Qualified New Single Family Homes (1000s)

Energy Star Qualified

Mkt Penetration

2006 New Homes Completed by RegionRegion Single Family Units %Northeast 128 8%Midwest 286 19%South 826 46%West 415 27%

Source: 2007 Buildings Energy Data Book

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 16 of 71 Jeff Osborne 212.271.3577

The average residential building used approximately 20.5 quads of energy in 2000, and an average household had to make up for approximately four quads in the winter and 1.1 quads in the summer, or roughly five quads in total. According to the 2007 Buildings Energy Data Book, roughly 25% of energy expenditures go to load management. Similar to commercial buildings, residential houses lose/gain much of their energy through the building envelope (outer-shell of the building) and would benefit greatly from advanced technology windows and insulation as well as the minimizing of weak thermal areas. Internal gains are also a concern in the summer as electronics and lighting become more energy intensive.

Aggregate Residential Building Component Loads

ComponentRoof -0.65 12% 0.16 14%Walls -1 19% 0.11 10%Foundation -0.76 15% -0.07 -Infiltration -1.49 28% 0.19 16%Windows (conduction) -1.34 26% 0.01 1%Windows (solar gain) 0.43 - 0.37 32%Internal gains 0.79 - 0.31 27%

-3.99 1.08

Heating CoolingAggregate Residential Building Component Loads (quads)

Source: 2007 Buildings Energy Data Book

Consumer Sentiment

The average green home buyer is from the East or West coasts, between the ages of 25-44 (mean of 45 but with large distribution), married, has above average income (two-thirds above $50,000 per year) and is female (71%), according to McGraw-Hill Construction, 2007. Word of mouth has overtaken TV as the main way people learn about green buildings, but that depends on demographics. People in the West are more likely than those in any other region of the country to contact a builder, while people in the South are more likely to obtain information via the TV than any other source. Education level is also a large determinate, as 80% of green home owners report some college experience and 60% report college or advanced degrees. The higher education level plays a large part in the way people receive information about green homes, as people with higher education levels tend to watch less TV and give advertisements less weight. It is reported that 40% of green homeowners are not at all interested in celebrities and television, something that will require a change from traditional consumer product advertisement.

The number one reason behind purchasing a green home in the residential arena is similar to commercial: operational cost savings, followed by environmental concerns, occupant health and potential higher resale. Lack of education in the residential space continues to be the main obstacle in a purchase, while cost and lack of available green homes come in a close second.

Cost continues to be a main concern. While Energy Star homes are efficient, they do cost more, (roughly $3,000-8,000 more depending on options) and energy efficiency is not typically at the top of the list for most consumers. Things like the paint job and granite countertops are still big sellers of homes. The U.S. Department of Energy, however, reported that the average family spends at least $1,291 on home energy per year, a number that will continue to rise. As energy prices rise, energy efficient appliances and building materials have more economic value because the cost is reduced to a payback of one to three years. A more competitive housing market coupled with a more educated consumer and higher energy costs will likely push energy efficient

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 17 of 71 Jeff Osborne 212.271.3577

housing as builders look to differentiate themselves and consumers learn about the benefits of green building.

The perception of a green home long after purchase is just as important for the industry as the reasoning for the initial purchase, given how many learn about the homes through word-of-mouth. Unlike commercial building owners, residential owners are most pleased with the improved health and wellbeing associated with a green home (i.e., higher air quality and improved family health). Overall, the top perceived benefits are home quality, easier maintenance, better indoor air quality, more efficient appliances and better health, with price having the lowest satisfaction level. With these benefits, 85% of green homeowners are likely to recommend a green home.

A change in consumer behavior and changes in demographics are also likely to continue to fuel the green building trend. According to a McGraw-Hill Construction study on the green homeowner (“The Green Home Owner Report”), sales of organic foods are expected to grow 20% annually over the next few years; the market for hybrid cars is increasing; socially responsible investing is on the rise; and two-thirds of Americans say they consider a company’s business practices before a purchase. Consumers from the age of 13-25 are even more likely to consider a company’s cause, business practices and social commitment when considering a purchase, something that is likely to spill over into their choices for home buying. While consumer behavior is still largely determined by brand and costs, these trends show a likely movement toward other intangible factors that will have a larger effect.

LEADERSHIP IN ENERGY AND ENVIRONMENTAL DESIGN STANDARDS BECOMING SYNONYMOUS WITH GREEN BUILDING

LEED (Leadership in Energy and Environmental Design) are standards for integrated green building design, construction and operation. LEED is quickly becoming synonymous with green, sustainable building techniques and will likely be a major determining factor in how new green building products will be developed. The program was first started in 1998 with loose guidelines, but now has specific codes for nine types of buildings.

The largest downside to building green continues to be the cost. According to Greentech Media, green building costs roughly $3 more per square foot than conventional building techniques, which can be a huge turnoff to builders that are concerned with delivering a product on budget. The estimated energy savings over time is $73 per square foot, however, a number that is usually not known or understood. Paperwork is also a headache for many builders (though everything is done on the internet), as each point must be documented. Currently, only 3% of new construction is LEED certified, with the private sector leading the way.

U.S. LEED Registered Projects

Private Sector Corps 33%Local Govt 25%Nonprofit Corp 14%State Govt 13%Federal Govt 10%Other 5%

US LEED Registed Project by Ownership Catergory

Source: Building Energy Data Book, 2007 (data sourced from 2003)

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 18 of 71 Jeff Osborne 212.271.3577

According to the World Business Council for Sustainable Development in a 2007 Building Efficiency report, the perceptions of the cost necessary to achieve greener buildings are significantly higher than the actual costs. The average perception was a 17% premium, when in fact cost studies have shown far lower numbers. For commercial properties, the Franunhofer Institute has shown that energy demand in a new building can be reduced by 50% without adding to traditional construction costs. The U.S. building council has done several studies and has shown that LEED certification cost is between 0% and 3%, and the cost of reaching a platinum level is less than 10%. Retrofitting existing building can also be extremely effective, according to the IEA. A study done on high-rise apartments in the European Union concluded that colder climates could achieve significant efficiency gains: 80% in the least efficient buildings with an average of 28% energy savings.

Cost Premium for LEED Buildings by Level Cost Premium by Location and Energy Efficiency Level

0%

2%

4%

6%

8%

10%

12%

UCSB, CA SanFrancisco, CA

Merced, CA Denver, CO Boston, MA Houston, TX

Cos

t pre

miu

m b

y lo

catio

n an

d LE

ED le

vel

SilverGoldPlatinum

Source: World Business Council for Sustainable Development in a 2007 Building Efficiency report

The LEED Ratings System

There are four levels of certification:

• LEED Certified: 26-32 points

• LEED Silver: 33-38 points

• LEED Gold: 39-51 points

• LEED Platinum: 52-69 points

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 19 of 71 Jeff Osborne 212.271.3577

U.S. LEED Certified Projects

Platinum Gold Silver Bronze CertifiedArizona 1 7 4 1 21California 12 37 31 0 120Colorado 2 11 15 0 41Georgia 2 10 19 0 41Illinois 4 8 14 0 40Maryland 1 6 5 0 20Massachusetts 3 6 9 0 41Michigan 0 13 11 0 34New Jersey 0 7 7 0 21New York 3 10 7 0 32Ohio 0 4 8 0 22Oregon 2 32 13 1 60Pennsylvania 3 28 31 0 78Texas 0 7 13 0 36Virginia 0 4 9 0 23Washington 1 20 23 0 70Wisconsin 0 5 6 0 20

US LEED Certified Projects by Certification

1) Project types include new construction, major renovations, existing building operations, interior design, homes, neighborhood development, development multi-building complexes, schools, and retail spaces. 2) Certified projects do not constitute the sum total of the other four categories, but rather designate an entirely separate category in and of itself. Source: United States Green Building Council Website, accessed August 2007

Sustainable Sites – 14 possible points, one prerequisite: This deals with the choosing of a site and the management of a site in a green way, with minimal effect on the surrounding ecosystem. Extra points are given for development or cleaning of existing sites or abandoned sites. Other standards include water runoff management, wildlife management, light pollution management and heat island effect reduction (creating an area that is 2-10 degrees Fahrenheit hotter than the surrounding area). Sites also should encourage public transportation, walking, biking and other ways to minimize personal vehicle travel. The prerequisite is that builders must plan and implement a construction activity pollution prevention plan to reduce environmental pollution associated with construction before the start of the project.

Water Efficiency – five possible points, no prerequisites: This deals with the management of water on the side and in the building. Points are awarded for a reduction in water use, a reduction in wastewater from the building and site as well as the use of rainwater and grey water.

Energy and Atmosphere – 17 possible points, three prerequisites: The site and building should address the amount of pollution produced by the building and the energy consumption. The building can receive points by implementing strategies that minimize energy used by increasing the efficiency of the building envelope (i.e., insulation, windows, sustainable design, etc.) and by utilizing renewable energy generating sources. The first prerequisite is an energy system installed and implemented in the building and verified for optimum performance as defined by a third-party commissioning agent with accurate and objective data collection. The second prerequisite, building standard 90.1-2004, is used to set minimum standards for building envelope efficiency. The third prerequisite is reducing ozone depletion through refrigerant management, essentially using zero CFCs in new construction and a phase out in renovations.

Materials and Resources – 13 possible points, one prerequisite: This deals with utilizing existing building and site materials, managing construction waste and using renewable materials

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 20 of 71 Jeff Osborne 212.271.3577

and local resources. The prerequisite is that the site must have recycling storage and collection plans that are executed by the occupants and be easily accessible to the entire building.

Indoor Environmental Quality – 15 possible points, two prerequisites: This is primarily concerned with the wellbeing of the building occupants. The first prerequisite is that all LEED buildings must have a no smoking policy, or a properly sealed and ventilated smoking area. The second prerequisite is that buildings must maintain a minimum level for indoor air quality and ventilation as defined by ASHRE code for Indoor Air Quality. Points can be awarded in construction by using low chemical emitting materials and properly ventilating spaces. Points are also awarded for the level of individual control on temperature and lighting as well as the incorporation of daylight into occupied spaces.

Innovation in Design and Process – five points possible, no prerequisite: This category is meant for going above and beyond the standards or addressing something not specifically in the LEED rating system. A point is awarded for having a LEED certified individual as a project principal.

REGULATION: GOVERNMENT IS STEPPING UP TO THE PLATE FOR ENERGY EFFICIENCY

The U.S. government has taken a proactive role in energy efficiency with the 2007 Energy Bill, which included a slew of new requirements, some the first changes in over a decade. According to the White House, the 2007 Energy Bill includes provisions to improve energy efficiency in lighting and appliances, as well as requirements for Federal agency efficiency and renewable energy use that will help reduce greenhouse gas emissions.

Recently, the Department of Energy (DOE) established regulations that require most new federal buildings to achieve at least 30% greater energy efficiency than that of the prevailing building codes. The new standards, which were published on December 21, 2007, are also 40% more efficient than the standards in the current code. Over the next 10 years, it is believed the standards could save more than 40 trillion Btu and reduce carbon dioxide emissions by two million metric tons, according to the DOE. The new regulation applies to any federal building that entered the “design for construction” phase by January 3, 2007. The new regulations took effect on January 22, 2008, and apply to new federal commercial buildings, multi-family high-rise residential buildings and low-rise residential buildings. The standards aim to address energy efficiency by looking at a building’s entire performance. The high standards put forth in the new regulations will also encourage federal builders to use an integrated approach when constructing new buildings.

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 21 of 71 Jeff Osborne 212.271.3577

THE 2007 ENERGY BILL

Federal/Municipal

The bill will require all general purpose lighting in Federal buildings to use Energy Star products or products designated under the Energy Department's Federal Energy Management Program (FEMP) by the end of Fiscal Year 2013. The federal government will designate energy managers to conduct comprehensive energy and water evaluations for each of the 500,000 federal facilities.

The Bill will establish an Office of High-Performance Green Buildings (OHPGB) in the U.S. General Services Administration. This office will promote green building technology implementation in Federal buildings.

Residential Buildings

The Bill will update the Energy Policy and Conservation Act to set new appliance efficiency standards. The Act amends the Energy Policy and Conservation Act to prescribe or revise standards affecting regional efficiency for heating and cooling products, procedures for new or amended standards, energy conservation, energy efficiency labeling for consumer electronic products, residential boiler efficiency, electric motor efficiency, and home appliances.

Commercial Buildings

The Bill sets a national goal to reduce commercial building energy use and achieve zero-net energy by 2030. All existing buildings are also expected to meet that same goal by 2050. That means facilities such as the Integrated Design Associates’ zero-energy and zero-carbon emissions building in San Jose can be replicated all over the country.

Industrial Buildings

There’s now a program to identify and recover industrial waste heat and energy, which will include grants and a registry of sites with economically feasible situations. The government also will promote the use of new materials, processes, technologies and operating techniques to optimize efficiency in energy-intensive businesses.

School Buildings

The bill contains grants to states to provide technical assistance for programs that address environmental issues and include standards for school design, construction and renovation.

Appliance Standards

Lamp Efficiency Standards: These new standards require incandescent bulbs to use 25-30% less energy than today’s most common bulbs by 2012-2014, and use at least 60% less energy by 2020. Initial targets can be met with advanced incandescent lamps that manufacturers are

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 22 of 71 Jeff Osborne 212.271.3577

currently introducing into the space, along with compact fluorescent lamps and light-emitting diodes.

DOE Rulemakings: Required the DOE to complete revised standards for refrigerators by 2011; clothes washers by 2012; external power supplies and battery chargers by July 2011 and again by July 2015; dishwashers by 2015; walk-in coolers and freezers by 2012; and metal halide lamp fixtures and general service lamps by 2017 and 2022. The standards require that most products include energy use in standby and off modes.

Heating and Cooling (HVAC): Allows for regional standards for HVAC. The rules provide authority for the Secretary to: set a national minimum standard and one additional regional standard for residential furnaces and heat pumps; develop enforcement plans; and grant new authority for States to enforce regional standards.

Electronics: The new bill requires the Federal Trade Commission to develop new energy consumption labeling programs for televisions, personal computers, cable and satellite set-top boxes, stand-alone digital video recorders, computer monitors, etc. This is an important standard as current requirements are only to display max power and say little about consumption. Energy Star requirements do not effectively address standby power usage, which will be updated.

Other provisions in the Bill give the DOE the power to expedite the process of rule making based on consensus recommendations, but does not require a Federal Register notice and legal review as was necessary before. This takes the timeline for approval down by 10 months, a process that typically takes three years and gives the DOE significant amounts of power in setting standards.

The American Council for an Energy-Efficient Economy estimates that the standard provisions will save at least 2.0 quadrillion Btu’s in 2030, or 1.6% of total projected nationwide energy use that year. The bill is estimated to save 177 billion kWh per year in 2030, and reduce peak electricity demand by 33,000 MW, or 110 power plants at 300MW each.

Progress of State Regulation

• Thirty-two states have, through legislation or regulation, ordered utilities to design and fund programs that promote or deliver energy efficiency.

• Twelve states have implemented, or are in the process of implementing, Energy Efficiency Resource Standards, which generally require utilities to allocate funds to energy efficiency programs to meet near-term savings targets set by state governments or regulatory authorities. These states include California, Texas, Colorado, New Jersey and Illinois.

• In recent years, there has also been an increasing focus on “decoupling,” a regulatory initiative designed to break the linkage between utility kWh sales and revenues, in order to remove the disincentives for utilities to promote load reducing initiatives. Decoupling aims to encourage utilities to actively promote energy efficiency by allowing utilities to generate revenues and returns on investment from employing energy management solutions. To date, nearly half of all states have adopted or are adopting forms of decoupling for gas or electric utilities.

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 23 of 71 Jeff Osborne 212.271.3577

Funding

A number of new programs promoting energy efficiency have been created, but these programs need to be funded. With the EPA Act of 2005, many programs were forgotten as Congress did not provide the money for them. We are not holding our breath for all of these programs to take off, as it has historically been common for funding and ambition for such sweeping programs to dry up. We do feel, however, that a meaningful portion will find legs, given the overwhelmingly strong support.

An appropriations act signed into law in December 2007 provides $1.536 billion in direct support of the DOE Office of Energy Efficiency and Renewable Energy (EERE), a 4.2% increase over the funds that were provided earlier. The act provides roughly $26 million for the DOE’s National Renewable Energy Laboratory, including $5 million toward a new Energy Systems Integration Facility. While the appropriations act is difficult to interpret, and there are many areas left open, money has been earmarked, which is a positive sign for the programs.

MATERIALS: MAJOR PRODUCTS AND TRENDS IN ENERGY EFFICIENCY

Green, sustainable, energy efficient, or whatever the name may be, are descriptions of a growing trend in the market. When producing a LEED certified, high performance building, the whole building design process must be utilized. The whole building design considers all pieces of the building in terms of performance, both in terms of energy efficiency and comfort of its inhabitants. In the following section, we discuss each input into the whole building design with current market, products and R&D.

LIGHTING

Lighting now makes up between 20-30% commercial energy consumption on average.

Lighting Share of Overall Energy Use and Expenditure US Buildings Primary Energy and Expenditure and End Use

End Use Residential Commercial Residential CommercialSpace Heating 31% 14% 35% 16%Lighting 11% 26% 10% 23%Space Cooling 12% 13% 11% 8%Water heating 12% 7% 13% 12%Electronics 7% 6% 6% 4%Refrigeration 8% 4% 7% 6%Cooking 5% 2% 4% 2%Wet Clean 5% 0% 4% 0%Ventilation 0% 6% 0% 6%Computers 1% 3% 1% 3%Other 4% 13% 4% 13%

Energy Expenditure

Source: 2007 Buildings Energy Data Book

Increasing electricity prices have forced many commercial companies to reassess their strategies toward lighting in general. Historically, relatively cheep electricity prices have encouraged the building of sprawling commercial and industrial complexes that have no natural light sources and require full lighting for a significant portion of the day, if not the full 24 hours. In these instances, the fixtures installed by the building contractor are also typically the cheapest possible, or the standard florescent light set, further adding to the relative inefficiencies of the lighting.

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 24 of 71 Jeff Osborne 212.271.3577

Lighted Floorspace for Commercial Buildings 2003 Lighted Floorspace for the Stock of Commercial Buildings

Lighted Floorspace Percent of Type of Lamp (Bn SF) Lighted FloorspaceStandard Fluorescent 59.7 96%Incandescent 38.5 62%Compact Fluorescent 27.6 44%High-Intensity Discharge 20.6 33%Halogen 17.7 29% Note: Total lighted floor space 62.06 Billion SF. The percentage of Lighted floorspace totals more than 100% because most floor space is lighted by more than one type of lamp. Source: 2007 Buildings Energy Data Book

The standard incandescent bulb still plagues the residential and, to a smaller extent, commercial markets because it is one of the largest sources of lighting inefficiency. On the residential side, incandescent bulbs consumed 87% of an average home’s lighting expenditures in 2001, while only producing 66% of the total light. In the commercial market, only 6% of light was attributable to incandescents, while they consumed 26% of the overall lighting load. Ireland recently banned the sale of incandescent bulbs in 2009, moving toward a European Union pledge to use energy efficient lighting by 2010 and saving Irish households an estimated $269.3 million. With political pressure, utility rebates and environmental concerns, it is likely that the 100-year-old incandescent bulb will lose its place as the incumbent light producer in the residential market and be considerably scaled down in any C&I applications.

Lighting controls have a dramatic effect on the performance of many light bulbs. For instance, a halogen lamp will last four times longer (12,000 hours or roughly seven years at average usage) if dimmed by 30%, which is the average level by which most consumers dim their lights. Also, it goes without saying that if one dims the lights by 50%, there is a corresponding roughly 50% drop in energy consumption attributed to lights. Because the typical residential occupant prefers slightly dimmed lights, installing dimmers in each residence (a relatively low tech solution) could save a tremendous amount of electricity. Lutron, a lighting control company, estimates that if one of their dimmers was installed in every U.S. home, it would save roughly $230 million in electricity cost per year.

The U.S. Energy Information Administration Office estimates that 44% of the energy use in an office building is for lighting; this figure is 56% in education buildings. Lighting control systems such as the ones Cooper Lighting has been offering for years (controlling occupied/non-occupied light levels, shades, daylight levels and, in some cases, integrating it into a software solution) can provide paybacks of anywhere from one to three years. Also, they can typically provide a better working environment for occupants, thereby increasing productivity. Solutions with longer paybacks of six to eight years can also succeed in the market, provided that they provide superior technology (i.e., smaller size, longer life, reliability, quieter operation, better convenience, etc.).

While it seems completely intuitive to include these systems in an office or similar building, two major obstacles need to be overcome. First, retrofit equipment for these systems can be cumbersome. Every control and switch needs to be wired into a central control panel. This requires extensive wiring, and most office/education structures are not wiring friendly once built. Wireless machine-to-machine connectivity solutions will likely be the answer to this problem as they become increasingly cost effective in the market. The second hurdle in many offices has been ownership. The management company pushes energy costs through to the lessee and has little incentive to implement cost saving measures, while lessees find it difficult to

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 25 of 71 Jeff Osborne 212.271.3577

install systems in buildings they do not own. It is also common for a lessee to have energy billed by square foot and not by individual energy usage, again giving little incentive to install energy saving measures. The value of LEED certified buildings and various incentives for energy efficiency are likely to help the ownership issue, but with estimated costs for energy efficiency products typically overestimated, it becomes the job of the industry to sell its product to the consumer and overcome the barriers.

Lighting System’s Decision Tree

Source: National Renewable Energy Lab

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 26 of 71 Jeff Osborne 212.271.3577

Typical Efficacies and Lifetimes of Lamps Typical Efficacies and Lifetimes of Lamps

Efficacy Typical Rated Current Technology (Lumen/Watt) Lifetime (hours) CRI

Incandescent 10-19 750-2500 97Halogen 14-20 2000-3500 99Fluorescent T5 25-55 6000-7500 52-75 T8 35-87 7500-20000 52-90 T12 35-92 7500-20000 50-92 Compact 40-70 10000 82HID Mercury Vapor 25-50 29000 15-50 Metal Halide 50-115 30000-20000 65-70 HP Sodium 50-124 29000 22 LP Sodium 18-180 18000 0CRI = Color Rendition Index; indicating a lamp's ability to show natural colors Source: 2007 Buildings Energy Data Book

Relative output per watt and the lifetime of incandescents, halogens and standard Fluorescent T5 lighting lag other options. From the following chart (“2001 Total Lighting Technology Light Output vs. Consumption”), it appears as if T-12 and T-8 seem to be the most commonly used in the industrial and commercial setting, a solution that provides both long life, a good CRI (color rendition index) and efficacy. There is a wide range for each, however, suggesting widely varying product quality in the industry.

Lighting represents a major opportunity for creating more energy efficient buildings. Currently, there is 84 billion square feet of commercial building space, with 20 billion square feet in the commercial and industrial segments alone. If one assumed a standard fluorescent fixture every 200 square feet, and each fixture cost roughly $100, the market size for the C&I space would be roughly $10 billion dollars. Using Orion Energy’s HIF (high intensity fluorescent) technology, the company is able to place a fixture every 400-500 square feet, rather than the traditional 200 square feet, allowing it to garner double the traditional average selling price while providing considerable energy savings.

Light Output Versus Consumption by Lighting Technology 2001 Total Lighting Technology Light Output vs. Consumption

Output Consump Output Consump Output ConsumpIncandescent Standard 66% 87% 6% 26% 0% 2% Halogen 3% 3% 2% 5% 0% 0%Fluorescent T5 0% 0% 0% 0% T8 20% 13% 24% 21% T12 54% 40% 47% 45% Compact 1% 1% 3% 3% 0% 1% Miscellaneous 29% 9% 0% 0% 0% 0%HID Mercury Vapor 1% 0% 1% 2% 2% 3% Metal Halide 10% 9% 20% 23% HP Sodium 0% 0% 3% 1% 7% 5% LP Sodium 0% 0% 0% 0%Output in trillion Lumen-hour per yearConsumption in billion kWh per year

Residential Commercial Industrial

Source: 2007 Buildings Energy Data Book

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 27 of 71 Jeff Osborne 212.271.3577

TYPES OF LIGHTS

Incandescent

The over 100-year-old incandescent light bulb works from about 1.5-300 volts and 0.1-10,000 watts. It is characterized by a low cost to produce and electrical flexibility as it does not require external regulating equipment to operate.

Makeup of the Typical Incandescent

1. Glass bulb2. Low pressure inert gas3. Tungsten filament4. Contact wire (goes out of stem)5. Contact wire (goes into stem)6. Support wires7. Stem (Glass mount)8. Contact wire (goes out of stem)9. Cap (Sleeve)10. Insulation (Vitrit)11. Electrical contact

Source: Wikimedia Commons

The bulbs typically have a glass enclosure, which is filled with an inert gas that prevents filament oxidation and supports the glass. In the enclosure is a coiled tungsten filament wire (thickness suited to application) through which electricity is passed, heating the filament to high temperatures of roughly 3,000-4,000 degrees Fahrenheit, making the metal white hot and creating light (the process of incandescence). Because the filament produces a full spectrum of light (visual and non-visual), incandescent lights are largely considered the most natural sources of light, but they also waste a considerable amount of heat in the process (approximately 90-95% of the energy used in incandescent lights is wasted as heat). For this reason, they are also the most inefficient of the popular lighting sources. In addition, they only last about 750-1,000 hours because the tungsten evaporates and deposits itself on the glass, eventually creating a thin spot where the filament will break.

Long Life Incandescent Lights

The Centennial Light is widely recognized as the longest burning light bulb, operating since 1901. The reason for this is the light bulb is powered by only four watts, which is considerably below its maximum output. A 5% reduction in the operating voltage of a light bulb results in roughly a doubling in a light bulb’s life, and running a light bulb significantly below its rated capacity can make it last a very long time, as in the case of the Centennial Light. Many long-life bulbs take advantage of this fact and cut the voltage to the bulb so it will last longer. Unfortunately, it does not pay to dim an incandescent bulb. Because the value of the electricity during the life of a typical light bulb is so much more than the actual light bulb, it pays to make them more efficient, and thus run them at a higher wattage.

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 28 of 71 Jeff Osborne 212.271.3577

Suppose you have 10 100-watt light bulbs with a rated lifetime of 750 hours and, in total, they all use about 1 kW at a cost of $0.09 per hour (typical U.S. rate). A typical bulb costs $1.00 in many stores, so the average cost would be $67.50 for the electricity and $10 for the bulbs, or $77.50 in total. Now assume that we use 110 volts instead of 120 volts, the bulbs would produce 76% of their normal light output and consume 0.88 kW of electricity. To get the same light output as the 10 lights at full power you must now run roughly 13 lights at 110 volts. This results in a cost of $77 in electricity, higher than the cost of running the lights at full power and replacing them.

Opposition to Incandescent Lighting

The recent popularity of “green” thinking has brought about opposition to the relatively inefficient incandescent bulb. The European Union has proposed a ban on the sale of the bulbs, but it has yet to be approved by all of the member states. The first movers have been Italy, the Netherlands and Ireland, with others calling for phase outs, but not yet setting a firm date. In the United States, California will phase out the bulbs by 2018, while in Canada, the federal government has called for the phase out of “inefficient” incandescent lights (although not all incandescent bulbs) by 2012. Many other countries, including Brazil, Australia and Venezuela, have also moved to phase out the bulbs.

The elimination of incandescent bulbs has been met with opposition due to shortcomings with replacement technologies, specifically compact fluorescent lamps (CFL), related to their higher cost, operating performance and environmental issues (namely the small amounts of mercury in each bulb).

The 2007 Energy Bill included a new lamp efficiency standard for the incandescent industry. By 2012-2014, bulbs are required to use 25-30% less energy than today’s most common incandescent bulbs, and at least 60% less by 2020.

Halogen

A halogen is an incandescent light in which the filament is encapsulated by a small enclosure filled with a halogen gas. The gas allows the filament to operate at a higher temperature without oxidation, providing a slightly better operating life than traditional incandescents. The halogen gases also have another interesting property: when operating at a high temperature, the halogen will redeposit evaporated atoms back on the tungsten filament, essentially recycling the atoms and allowing for greater life.

A halogen bulb can be 10-20% more efficient than an ordinary incandescent bulb of similar properties. Halogen bulbs may also have a life that is two to three times longer than ordinary incandescent bulbs. The lifetime and efficiency is typically determined by the filler gas, usually krypton, xenon or argon.

Although the halogen’s life and efficiency are greater than a typical incandescent light, the relatively high operating temperature of halogen lights often require shields or cages, limiting the number of applications in which they are used. Similar issues with incandescent bulbs are also present in the use of dimmers with halogen lighting. Also, it is important to note that the halogen recycling process does not function as well when the light is not operating at full power. Major increases in bulb life necessitate a “soft-start” device, which keeps “necking” from

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 29 of 71 Jeff Osborne 212.271.3577

occurring at the ends of the filaments (creation of weak points due to power spikes on the starting of the lights).

Fluorescent

A fluorescent lamp is a gas-discharge lamp that uses electricity to excite mercury vapor in argon or neon gas, creating plasma that produces ultra-violet light, which is converted to visible light through the use of fluorescence. The fluorescent conversion occurs in the typical phosphor coating placed on the inner part of the tube, where high energy photons are absorbed by electrons in the phosphor’s atoms, creating visible light. The cathode is typically made of tungsten, typically coated with barium, strontium and calcium oxide. Fluorescent lights require a ballast to regulate voltage and amperage, which is typically incorporated into the lamp housing.

Makeup of a Fluorescent Bulb

Source: Tom Harris – “How Fluorescent Lamps Work”, December 7, 2001 via Howstuffworks.com

Fluorescent lighting finds its history in the early discovery that evacuated glass glowed when a current was passed through it. In 1856, a German glassblower named Heinrich Geibler created a mercury vacuum pump superior to what had been previously available, thereby creating a tube that produced significantly more light than was previously possible. Although at that time it was simply a phenomenon most popular as a source of amusement, continued work on the Geibler design led to superior products, and forced the innovation of GE’s incumbent incandescent bulb to a longer-lasting tungsten filament in the early 1900s. By the early 1930’s, GE had obtained the lion’s share of the patents in the space and established a massive R&D effort geared toward the technology. By 1938, GE commercialized the technology, and by 1951 more light was produced in the United States by fluorescents than by incandescents.

Florescent lighting has two main advantages over their incandescent counterparts: higher efficiency and longer life. Compared to incandescent lights, florescent lights convert a larger proportion of energy into useable light and less energy into heat. Typical fluorescent lamps will last 10 to 20 times longer as an equivalent incandescent lamp. These two large advantages are offset, however, by many disadvantages that have allowed incandescent bulbs to maintain a strong market share. Because fluorescent lights do not provide a steady light source when magnetic ballasts are used, fluctuating at twice the supply frequency, they present many environmental issues (electronic ballasts do not produce light flicker). Flicker has been associated with headache and fatigue, among other more serious issues. Flicker is also an issue in industrial settings with rotating equipment as makes the equipment appear as if it is not

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 30 of 71 Jeff Osborne 212.271.3577

moving, thereby creating a safety issue. Also, fluorescent lights produce UV light, which causes problems for individuals with sensitivity. Fluorescent lights require a voltage regulator or ballast, which adds an extra cost as well as added complexity to fluorescents. The ballast can also produce an audible buzzing noise and radio frequency noise, both of which can typically be addressed, but at an added cost. Furthermore, two main components of fluorescent lamps, phosphor and mercury, are toxic and present environmental and disposal issues. In 2006, a typical four foot lamp contained 12mg of mercury. In 2007, the National Electrical Manufacturers Association announced that it would establish a voluntary commitment to produce bulbs with less than 5-6mg of mercury (depending on wattage). Though this is a dramatic reduction in mercury, recycling programs will still be required, increasing the lifetime cost of the lighting system.

Compact Fluorescent Lights (CFLs)

CFLs are a basic fluorescent lamp, somewhat miniaturized, with an integrated ballast (although some have a modular ballast, which is less common). They are typically packaged to fit in a standard screw base for an incandescent bulb. CFLs typically last 7,500-20,000 hours, far longer than the 750-2,500 hours of a standard incandescent, while operating at a lower temperature and consuming approximately 75% less energy. The sales of Energy Star-qualified CFLs nearly doubled in 2007, according to Environmental Protection Agency (EPA) estimates. In 2007, 290 million CFLs were sold, and the bulbs now account for about 20% of the U.S. light bulb market. The EPA estimates that if every U.S. household replaced just one light bulb with a CFL, the United States would save more than $600 million each year in energy costs

Retailers such as Wal-Mart, Lowes, Home Depot, Costco, Menards, Ace Hardware and Sam’s Club have played a large role in the growth of the CFL, educating consumers and pushing the products in their stores.

Typical CFL Bulb

Source: Energy Star, Department of Energy

Issues with CFLs, however, are numerous. CFLs present all of the advantages and disadvantages of a typical fluorescent lamp, with a couple of other specific issues. CFLs continue to be larger than their incandescent counterparts, causing issues when a swap is attempted. CFLs do not work with dimmers, a problem with retrofitting. Also, the shapes required to fit a CFL in a conventional incandescent fixture are typically not optimal for light diffusion, causing lighting pattern issues. CFLs can take several minutes to reach full lighting and are best suited for applications during which they run for at least 15 minutes, if not more.

A PRIMER ON ENERGY EFFICIENCY

January 31, 2008 Thomas Weisel Partners LLCPage 31 of 71 Jeff Osborne 212.271.3577