Embed Size (px)

Citation preview

Economics 1: Fall 2010

J. Bradford DeLong, Michael Urbancic, and a cast of thousands...

hAp://delong.typepad.com/econ_1_fall_2010/

Economics 1: Fall 2010: Downturns and Financial Markets: Keynesians and

Monetarists J. Bradford DeLong

September 8, 2010, 12-‐1 Wheeler Auditorium, U.C. Berkeley

The Employment-‐to-‐PopulaQon RaQo, Seasonally Adjusted

Ladies and Gentlemen, to Your i>Clickers...

• Who is your favorite actor in the Harry PoAer movie series? – A. David Radcliffe – B. Kenneth Branagh – C. Emma Watson

– D. Alan Rickman – E. Maggie Smith

Alan Rickman

• Playing Sir Alexander Dane playing Dr. Lazarus in Galaxy Quest...

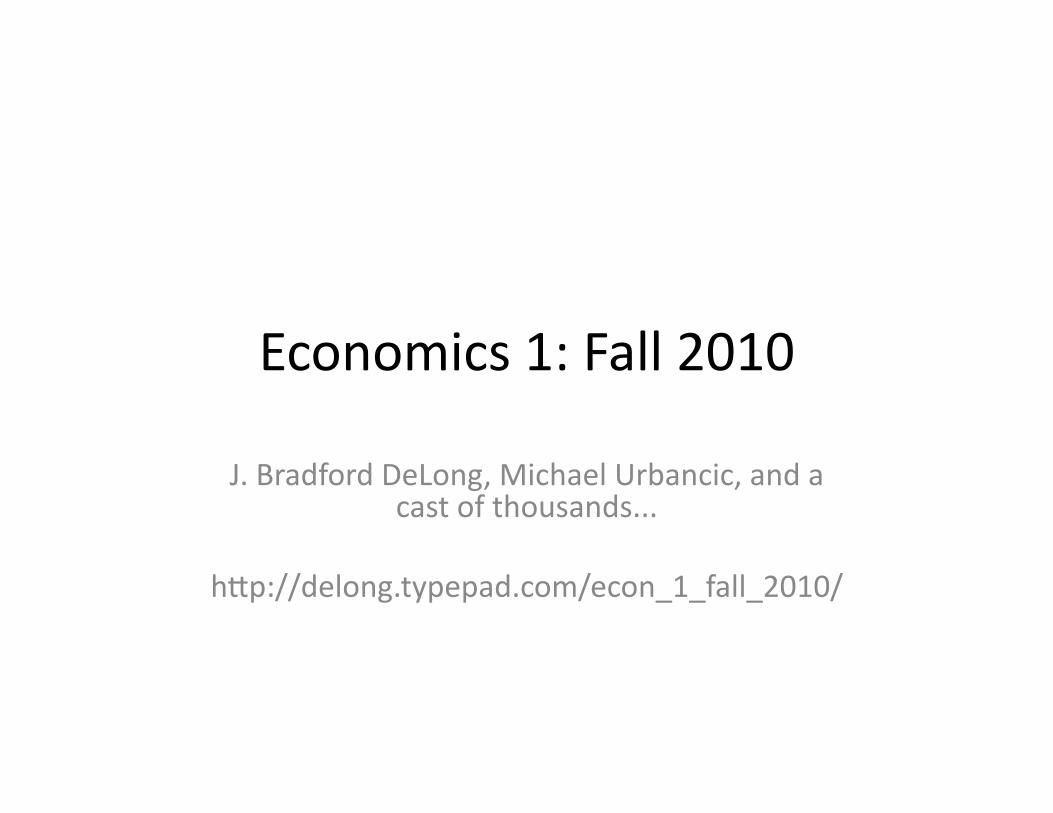

Associated with Fall-‐Offs in the Pace of Spending

Jean-‐BapQste Say vs. Thomas Robert Malthus

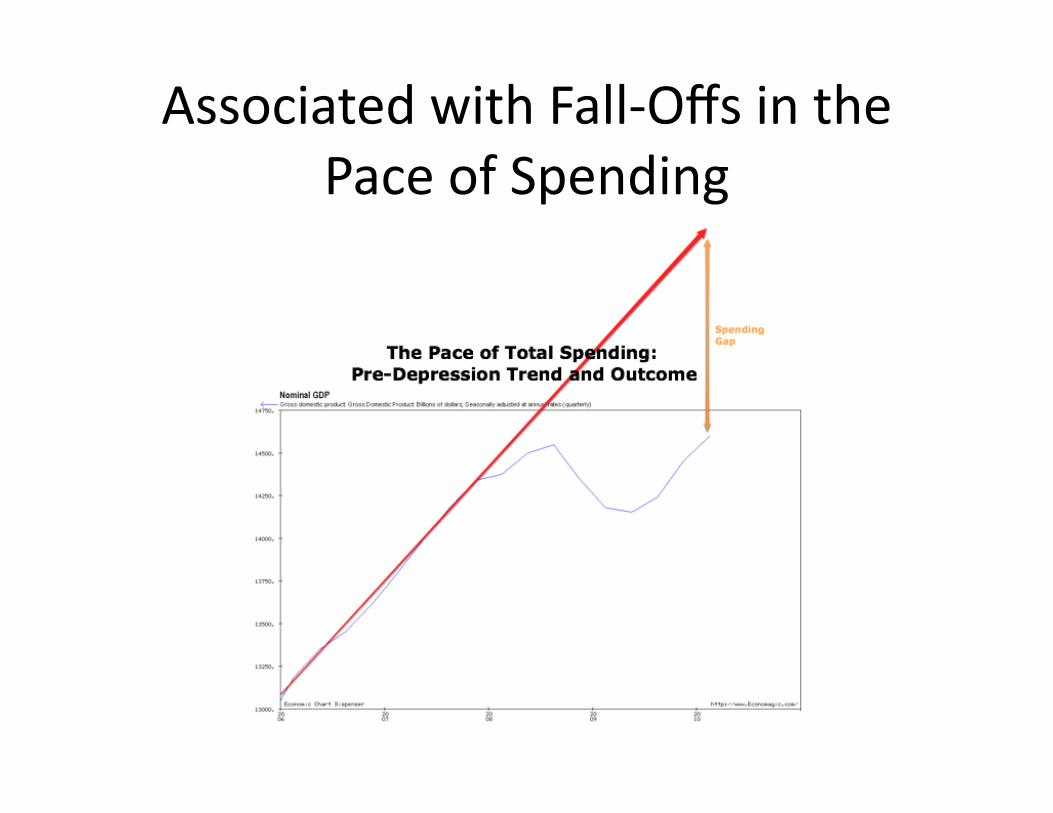

John Stuart Mill : Excess Supply of Goods Is Excess Demand for Money

• What they called a general superabundance was... of all commodiQes relaQvely to money... Persons... from a general expectaQon of being called upon to meet sudden demands, liked beAer to possess money.... Money... was in request... other commodiQes... in... disrepute. In extreme cases, money is collected in masses, and hoarded... the result is, that all commodiQes fall in price, or become unsaleable... No... impropriety in saying that there is a superabundance of all or most commodiQes...

Demand for Cash

$$$

Barista Employment Shrinks, Nothing Grows

$$$

And Then as Barista Spending Shrinks, All Employment Shrinks

$$$

The Income-‐Expenditure Framework

• E = Y • E = C + O • C = c0 + cy x Y • Y = (c0 + O)/(1 -‐ cy) • Dynamics:

– E > Y, inventories are falling and firms are hiring... – E < Y, inventories are rising and firms are firing... – Only if E = Y is the economy in balance, in equilibrium.

• This does a good job at gegng at the essence of what is going on...

Ladies and Gentlemen, to your i>Clickers...

• Why these symbols c0 and cyin C = c0 + cy x Y? Why not simply “$3.5T/yr” and “0.5”? – A. If we economists use more and more complicated math than necessary, the

poliQcal scienQsts will be scared of us and won’t apply for the jobs we want for our students.

– B. If we economists use more and more complicated math than necessary, the poliQcal scienQsts will be scared of us and won’t quesQon our conclusions in books and seminars.

– C. We economists paid aAenQon in math when younger: it has to be good for something!

– D. If we had “$3.5T/yr” and “0.5” we would have to redo the enQre analysis from scratch everyQme either of those numbers changed. If we keep c0 and cy then we can keep reusing our old analysis over and over again, simply plugging in the current values at the end. That’s what algebra is good for: it enables you to do not just one calculaQon but enQre families of calculaQons all at once and easily—and then whenever you need one member of that family you have it on the shelf to pick up and use.

The SoluQon to Our Model • Y = (O + c0)/(1 – cy)

– Take the flow of “other spending”: net exports NX plus business investment I plus government purchases G

– Add to that the amount of consumpQon spending that depends on “confidence” and like factors c0

– Divide by 1 – cy – You are done. That’s the level of spending—and incomes, and producQon—at which the economy is going to seAle.

Financial Markets and Economic Downturns

• Our “mulQplier” framework works

• SQll les unanswered: – What causes these declines in other spending O—I + G + NX—investment + government purchases + net exporst—or in the “confidence” component of consumpQon spending c0 anyway?

– How do these declines fit in with our discussion of excess demand for financial assets as the necessary counterpart of excess supply in the markets for currently-‐produced goods and services?

Excess Demands That Can Disrupt the Circular Flow

• Three kinds: – Demand for liquid cash money – Demand for bonds—i.e., for places to store your wealth because you don’t want to spend it now, you want to save it and spend it in the future

– Demand for high-‐quality assets: places where you can be sure that your money won’t melt away

• We had the first in 1982, the second in 2001, and we have the third type today

Economics May Call Itself a Science, But It Is Not a Very Good Science...

• This has been true for a long, long Qme: – John Stuart Mill: “there is no opinion so absurd as not to have been

maintained by some person of reputaQon. There even appears to be on this subject a peculiar tenacity of error – a perpetual principle of resuscitaQon in slain absurdity...”

• Four schools of economists • Actually “schools” is the wrong word, “sects” or “cults” is beAer:

– Sect #1: Excess supply? Deficient demand? “General glut”? What are you talking about?

• “Great forgegng”, “great vacaQon”, “great confusion”, “great immobilizaQon” schools

• No significant market failure—hence no cause for government acQon • All part of a “pain caucus”

– Three sects, sects #2, #3, #4, agree that there is an aggregate demand problem

• And agree that government can help • But disagree about the exact diagnosis and the cure

Sects 2, 3, and 4: Keynesians, Monetarists, and Minskyites

• Keynesians: downturn triggered by an excess demand for bonds – Long-‐duraQon assets that carry purchasing power into the future – An excess of planned savings over planned investment

• RepresentaQve members: Knut Wicksell, John Maynard Keynes (in some of his moods), John Hicks, James Tobin

• Fix it by anything that creates more bonds (or reduces the demand for bonds)

• Monetarists: downturn triggered by an excess demand for liquid cash money – Oh, and by the way, the mulQplier is not important

• RepresentaQve members: John Stuart Mill, Irving Fisher, John Maynard Keynes (in some of his moods), Milton Friedman

• Fix it by making more money

• Minskyites: downturn triggered by an excess demand for safe high-‐quality assets – And a collapse of confidence that some assets thought to be safe are in fact safe

• RepresentaQve members: Walter Bagehot, Hyman Minsky, Charles Kindleberger, Ben Bernanke, Ricardo Caballero

• Fix it by creaQng more safe assets or reducing the panic demand for safe assets

Keynesians, ProducQon and Spending, (Planned) Savings and Investment

• Our income-‐expenditure framework: – Y = (I + G + NX + c0)/(1-‐cy)

• What does this have to do with an excess demand for bonds, with an excess of (planned) savings?

• Savings and investment: Sd -‐ NX = I + D – Sd = Y – C – T; D = G – T; C = c0 + cy x Y

• SubsQtute in: – Y – (c0 + cy x Y) – T – NX = I + G – T – Y x (1 – cy) – NX = I + G +NX + c0 – Y = (I + G + NX + c0)/(1-‐cy)

• Planned savings equals planned investment when income equals expenditure: the income-‐expenditure framework and the theory that depressions are the result of excess demand for bonds are preAy much the same thing

• The math gets us there quickly and accurately—if we have set up the problem correctly

• We could (and should) also get there in words: that is what Say and Mill did

Keynesian Policies to Get Us Out of a Downturn

• Central bank lower interest rates to convince businesses to increase their investment spending I

• Other incenQves, like special tax credits, to increase investment spending I • Increase government purchases G • Central bank lower interest rates to weaken the currency, making

foreigners more eager to buy exports and increasing NX • Subsidies for businesses to export more or for domesQc buyers to import

less, raising NX • Claim that prosperity is just around the corner, making businesses and

households more confident about the future and hence raising investment spending I and also c0

• Cut taxes, thus giving households more money in their pockets and hence raising the baseline consumpQon-‐spending confidence term c0 – But be careful, this could backfire: if the tax cut convinces households that the

government has no sensible long-‐term plan, it will not improve but diminish confidence and so lower c0

Monetarists, Money Demand, and Money Supply

• No significant mulQplier – So income-‐expenditure framework uninformaQve

• E = (M/P) x V • Y = E • Y = (M/P) x V • According to monetarists, the Keynesians were looking at

the tail and thinking it was wagging the dog – It’s not an excess demand for bonds, rather what is going on in

the bond market generates interest rates so low that there is an excess demand for money...

Monetarist Policies to Get Us Out to a Downturn

• Central bank buys bonds for cash • This raises the real money stock • When the real money stock is high enough that there is no longer any excess demand for liquid cash money...

• ...then spending, output, and incomes—and employment—will once again be back at normal levels.

The Keynesian CriQque of Monetarism

• It might work – Central bank expansions of the money supply lower interest

rates – At lower interest rates firms want to undertake more investment

spending—and issue more bonds to finance it – Perhaps this expansion in the supply of bonds eliminates the

excess demand for bonds, the excess of (planned) saving over investment, and gets the economy back to full employment

• But not if there is a big downturn – What happens when interest rates hit rock-‐boAom and there is

sQll an excess demand for bonds? – Then there is sQll excess supply for currently-‐produced goods

and services – And the depression conQnues

The Monetarist CriQque of Keynesianism

• Policies to boost the supply of bonds lower the price of bonds—and that means that they raise interest rates

• When interest rates are higher, holding liquid cash money is more expensive – It has a higher opportunity cost – And so the demand for money falls

• Perhaps this decline in the demand for money brings the money market back into balance, and eliminates the excess demand for liquid cash money – But not if the excess demand for money is large

• NoQce a certain symmetry? – Each side thinks the other is trying to fix a problem in the wrong part

of the financial sector – And so is pursuing a relaQvely ineffecQve policy

Which You Prefer Is an Empirical QuesQon

• Do most downturns come about because something has happened to change the quanQty of money? – If so, we should be monetarists first – Focus on keeping the money stock growing along a stable, predictable

path – That’s the best way to avoid depressions – That is a strategic intervenQon to keep the economy on an even keel

• Do most downturns come about because people cutback on spending in order to try to build up their holdings of bonds? – Then monetarism is a sideshow – And we ought to be pursuing other strategic intervenQons to keep

employment on a stable path – Strategic intervenQons that affect the balance of supply and demand

for bonds, for saving and investment

Stable Velocity of Money, 1963-‐1978

Unstable Velocity of Money, 1978-‐

Minskyites, “IrraQonal Exuberance,” Panic, Revulsion, and Discredit

• A sudden excess-‐demand for high-‐quality assets

• Assets where people can park their wealth and be sure it will sQll be there when they come back...

• This excess demand acts like... – ...the excess demand for liquid cash money in monetarist theories...

– ...the excess demand for bonds, the excess of (planned) savings over investment in Keynesian theories...

• And generates the downturn

Where Do These Financial Excess Demands Come From?

• For monetarists, a drain of cash (internal or external) or a contracQonary mistake by central banks or a banking crisis that causes banks to turn away deposits...

• For Keynesians, a fall in business confidence that reduces their willingness to issue bonds and build capacity (or something else that hits the savings-‐investment balance)...

• For Minskyites: a panic...

Test Your Knowledge • Why, empirically, did Jean-‐BapQste Say come to the conclusion by 1829 that he was

wrong in 1803 to claim that we did not have to worry about episodes like the one that we are in—episodes in which supply does not create its own demand, and there is economy-‐wide excess supply of currently-‐produced goods and services?

• Why, theoreQcally, did John Stuart Mill claim back in 1829 that Jean-‐BapQste Say should have realized that there was a hole in his argument?

• Why is it allowable for us to assumethat E, total expenditure, total economy-‐wide spending, is or soon will be equal to Y, income and output?

• What kinds of financial excess demand produce “general gluts”—produce economic downturns and high unemployment rates?

• What is our equaQon, if we are Keynesians, for figuring out how much producQon and incomes Y will fall if there is a fall in either I, G, NX, or the “confidence” component of consumpQon spending c0?

• What is our equaQon, if we are monetarists, for figuring out what the level of producQon and incomes Y will be?

• Why are neither Keynesian nor monetarist approaches terribly good fits to our current situaQon?