Embed Size (px)

Citation preview

General Audit Internship Report1

TABLE OF CONTENTS

LIST OF ABBREVIATIONS

LIST OF CHARTS, GRAPHICS AND TABLES

FOREWORD

CHAPTER 1: OVERVIEW OF UHY AUDIT & ADVISORY LIMITED................. 8

1.1. DEVELOPMENT HISTORY …………………………………………………... 9

1.2. OPERATION CHARACTERISTICS............................................................... 10

1.2.1 Clients and Market........................................................................................ 10

1.2.2 Services ........................................................................................................ 11

1.3. MANAGEMENT OF BUSINESS ACTIVITIES .............................................. 13

1.3.1. Management Apparatus................................................................................... 13

1.3.2. Professional staff.............................................................................................. 15

CHAPTER 2: AUDIT ORGANISING IN UHY AUDIT & ADVISORY LIMITED 19

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report2

2.1. ENGAGEMENT TEAM ORGANISING .......................................................... 20

2.2. AUDIT PROGRAM ORGANISING................................................................. 24

2.2.1. Audit approach determination ........................................................................ 24

2.2.2. Internal control system assessment ................................................................... 24

2.2.3. Audit tests ......................................................................................................... 27

2.2.4. Audit completion .............................................................................................. 28

2.3 AUDIT PROFILE ORGANISING …................................................................ 31

2.4 QUALITY CONTROL ORGANISING ............................................................... 36

2.4.1 Quality control in audit preparation……………………………………………..

2.4.2 Quality control in audit performation……………………………………………..

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report3

2.4.3 Quality control in audit completion……………………………………………..

CHAPTER 3: COMMENTS AND RECOMENDATION ON AUDIT ORGANISING OF UHY AUDIT & ADVISORY LIMITED …………........................................... 37

3.1. COMMENTS ON ENGAGEMENT TEAM ORGANISING ........................... 38

3.1.1. Advantages ...................................................................................................... 38

3.1.2. Disadvantages .................................................................................................. 39

3.2 COMMENTS ON AUDIT PROGRAM & QUALITY CONTROL .................... 40

3.2.1. Advantages ...................................................................................................... 38

3.2.2. Disadvantages .................................................................................................. 39

3.3 RECOMMENDATIONS ON AUDIT ORGANISING OF UHY AUDIT & ADVISORY LIMITED

CONCLUSION........................................................................................................... 42

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report4

APPENDIX ............................................................................................................... 4

REFERENCES ........................................................................................................... 14

LIST OF ABBREVIATIONSUHY LtdIFCVND Viet Nam DongCIT Corporate Income Tax

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report5

UAA UHY Audit approach

LIST OF CHARTS, GRAPHIC AND TABLES

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report6

FOREWORD

In 2007, Vietnam became an official member of World TradeOrganization. Several years after that witness anexplosion in Vietnam audit market with the birth of alarge number of auditing firms. However in recent years,global economy as well as Vietnam economy has to sufferdeep and long crisis. At the same time quality requirementfrom publicity is becoming stricter. Auditmarket ,therefore, turn to be more competitive than everbefore. In this context, as a final year student inauditing class of National Economic University, the authorrecognize challenges of high criteria on auditor as wellas many opportunities in working as an audit trainee in anaudit firms. By passing several hard round, I haveopportunity to understand audit in context of reality inUHY Audit & Advisory Services Company Limited.

This paper aims to express new knowledge I have learntafter several first weeks of discovering an audit firm andhow it organize a typical audit. In preparation of thisreport, I did apply interviewing and documentinvestigation method to get understood about the history,operation of UHY Ltd. Working as an audit assistant in anrealistic audit, I have learn a lot about the methodapplied to organize an audit in UHY Ltd. that isrepresented shortly in my report. At the same time, insome sections analytical procedures are used to giveclearer view to reader. In addition, the reportproactively give some suggestion to improve auditorganizing method in UHY Ltd based on my knowledge I havelearn in the university.

General information of UHY Ltd, audit organizingmethodology in UHY Ltd. and my comments is that all what I

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report7

hope to express informatively. The paper will reach thisobjectives by structuring itself as follow

CHAPTER 1: OVERVIEW OF UHY AUDIT & ADVISORY LIMITEDCHAPTER 2: AUDIT ORGANISING IN UHY AUDIT & ADVISORY LIMITEDCHAPTER 3: COMMENTS AND RECOMENDATION ON AUDIT ORGANISING OF UHY AUDIT & ADVISORY LIMITED

Several weeks of internship period gave me many chances toapply my academic knowledge in reality as well as discoverabout one of large auditing firm in Vietnam. However,within a short time and because of my limitation inacademic knowledge, surely my report still traps into somemistakes. Any comment is valuable to me in make my paperbecome more perfect.

Finally, I actually feel grateful to enthusiastic andprecise assistances of my respectful lecturer Professor ToVan Nhat, Board of Direcitor of UHY Ltd, and many brothersin department one in guiding me complete the paper.

Sincerely!

CHAPTER 1

OVERVIEW OF UHY AUDIT & ADVISORY SERVIECS COMPANY LIMITED

1.1. DEVELOPMENT HISTORY

UHY Audit & Advisory services Company Limited (UHY Ltd) -is an independent member and the sole representative ofUHY International in Vietnam. With headquarter based inHanoi and Ho Chi Minh City branch, in Vietnam UHY Ltd isone of large audit firms and has contributed to thedevelopment of the auditing in particular and financialsector in general. UHY Ltd was founded in 2006 under thebusiness registration certificate number 0102021062, firstregistration on 08.29.2006 issued by the Planning and

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report8

Investment Department of Hanoi. In 6th change on11.26.2012, charter capital was raised from 2 to 5 billionVND with 6 capital contributing members. Now, main office ofUHY Vietnam is on 9th Floor, HL building - Duy Tan - Cau Giay - Ha Noi.Contact details and further information can be reached atthe company website http://uhyvietnam.com.vn.

In 2006, the top leaders of the International Auditing& Financial Consulting Company - IFC decided to split themajority of capital contributing members in order to forma new member of UHY International in Vietnam. Thisimportant decision was consented by all capitalcontributing members of IFC in an uniform meeting held on10/08/2006. UHY is also retained IFC headquarters at thattime 25A, Tran Duy Hung, Hanoi, majority of assets so asto operate. New UHY international member have massivesacrifices from IFC: 7/12 capital contributing members(representing 55 % of total capital), Chairman of capitalcontributing council, three Deputy Director with 8/10senior managers, 40/52 staff, in which there are nine CPAauditor and the most valuable thing – the considerablenumber of IFC clients being about seventy main clients.

In 6/2007, the company moved the office to 136 Hoang QuocViet, Cau Giay , Ha Noi to serve increasing number ofstaff as well as the rapid development of the company.However, the need of comfortable and professionalenvironment encourage to one more time move headquartersto 9th Floor, HL building - Duy Tan - Cau Giay - Ha Noi in2012, then the company has a new and professionalworkplace.

In 2007, State Securities Committee allowed UHY Ltd. toaudit listed companies. This was remarkable leaf indevelopment history of UHY Vietnam. At that time, the

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report9

scope of company was mainly in northern and middle ofVietnam. Recognizing great potential in the South, in 2009June, the company decided to open a representative officein Ho Chi Minh City. Today, UHY has over 120 employees inboth offices with staff of young and professional capacityas well as good moral character.

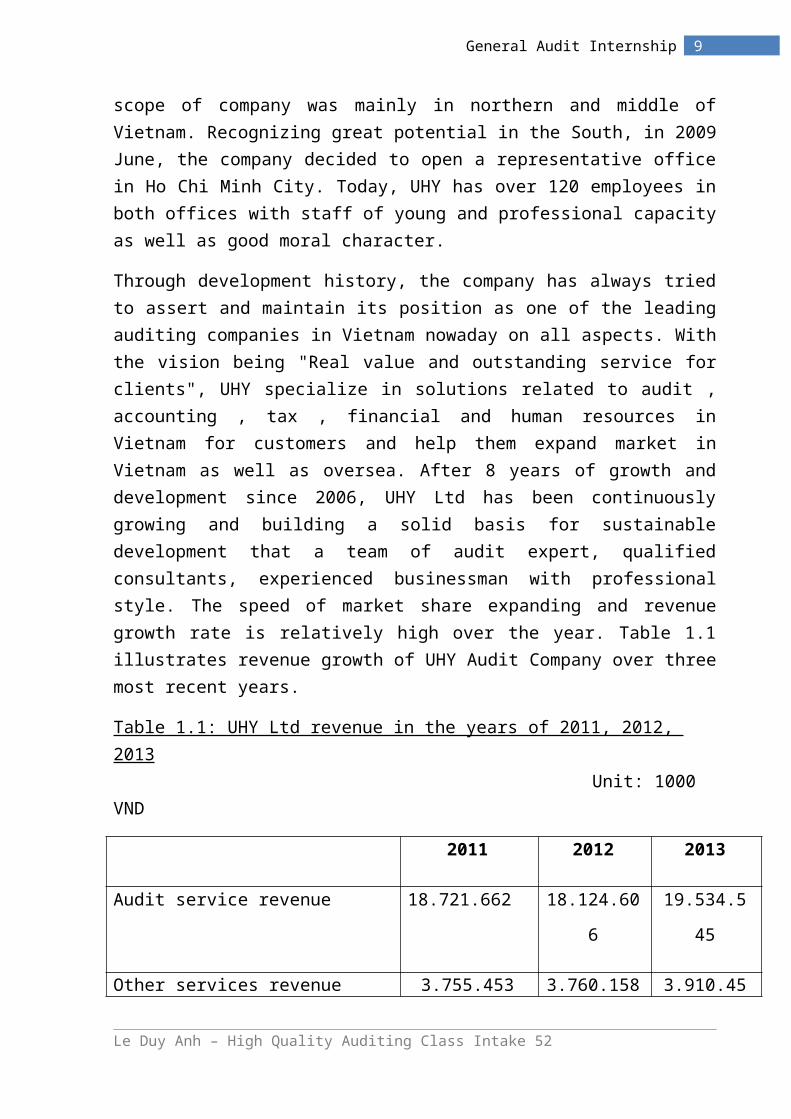

Through development history, the company has always triedto assert and maintain its position as one of the leadingauditing companies in Vietnam nowaday on all aspects. Withthe vision being "Real value and outstanding service forclients", UHY specialize in solutions related to audit ,accounting , tax , financial and human resources inVietnam for customers and help them expand market inVietnam as well as oversea. After 8 years of growth anddevelopment since 2006, UHY Ltd has been continuouslygrowing and building a solid basis for sustainabledevelopment that a team of audit expert, qualifiedconsultants, experienced businessman with professionalstyle. The speed of market share expanding and revenuegrowth rate is relatively high over the year. Table 1.1illustrates revenue growth of UHY Audit Company over threemost recent years.

Table 1.1: UHY Ltd revenue in the years of 2011, 2012, 2013

Unit: 1000 VND

2011 2012 2013

Audit service revenue 18.721.662 18.124.60

6

19.534.5

45

Other services revenue 3.755.453 3.760.158 3.910.45

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report10

5

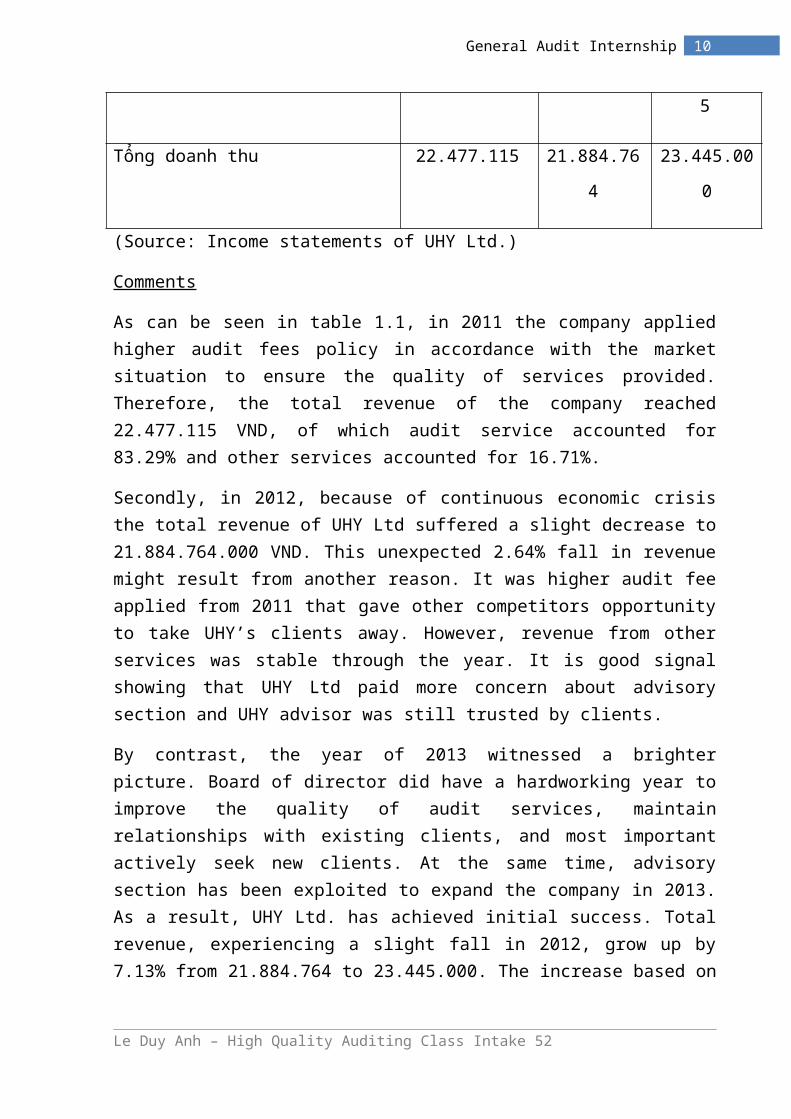

Tổng doanh thu 22.477.115 21.884.76

4

23.445.00

0

(Source: Income statements of UHY Ltd.)

Comments

As can be seen in table 1.1, in 2011 the company appliedhigher audit fees policy in accordance with the marketsituation to ensure the quality of services provided.Therefore, the total revenue of the company reached22.477.115 VND, of which audit service accounted for83.29% and other services accounted for 16.71%.

Secondly, in 2012, because of continuous economic crisisthe total revenue of UHY Ltd suffered a slight decrease to21.884.764.000 VND. This unexpected 2.64% fall in revenuemight result from another reason. It was higher audit feeapplied from 2011 that gave other competitors opportunityto take UHY’s clients away. However, revenue from otherservices was stable through the year. It is good signalshowing that UHY Ltd paid more concern about advisorysection and UHY advisor was still trusted by clients.

By contrast, the year of 2013 witnessed a brighterpicture. Board of director did have a hardworking year toimprove the quality of audit services, maintainrelationships with existing clients, and most importantactively seek new clients. At the same time, advisorysection has been exploited to expand the company in 2013.As a result, UHY Ltd. has achieved initial success. Totalrevenue, experiencing a slight fall in 2012, grow up by7.13% from 21.884.764 to 23.445.000. The increase based on

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report11

revenues from audit revenue growth and other servicerevenue climb, namely 7.78% and 4% in comparison with2012.

In conclusion, through the period of three years UHY Ltd.have tendency of growing stably. However, the growth ofcompany mainly base on prestige of directors. The authorrecognizes that UHY should take advantage of availablereputation to widen market and apply long term policy todevelop client network. Whereby, the company can achievebig leaf in the near future.

1.2. OPERATION CHARACTERISTICS

1.2.1 Clients and Market

After becoming separate from IFC, the UHY's market islimited in the north and a few clients in the Middle ofVietnam. Through continuous effort of board of directors,UHY Ltd’s market spread from small companies, mostlyfamiliar clients of IFC to national market with many bigclients such as Airport Corporation of Vietnam, SaigonTourism, LICOGI Corporation ….

With the vision being "Real value and outstanding servicefor client", the company's strategy is fast approachingand catching up with customer requirements. At the sametime, leaders of the company provide advice and materialfor potential client actively. Many open relationship isbuilt is the foundation for more contracts . The company's customers increasingly rise and diverse from manydifferent sectors of economy including

Enterprises with foreign investment State enterprises Business was established and operated under corporate

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report12

law, insurance law and other Financial institution International funding project The social organizations Corporation, Partnership, Limited

In conclusion, UHY’s client is various in term of economicsector as well as business size. Client may be acorporation, an individual trader or a hospital ... Evenit is able that clients can also be a project orprogram ... with the participation of many internationalparties. Because of diversity in clients, UHY Ltd devideclient in type of service to develop its own customers.From 2007, the State Securities Committee decided toaccept UHY to provide audit services to listed companies,public companies, securities exchange companies.

1.2.2 Services

When starting operation, UHY LTD mainly serve clients fromIFC. At this time, the company primarily providesfinancial audit services. Over 8 years of operation, withthe continuing efforts of the leaders and staff, systemservices provided by the Company has been developing,expanding, fully meet the needs of clients. Currently, theCompany is providing the following services: auditservices and assurance services, business financialconsultancy, tax consultancy, internal audit and riskmanagement; and other services.

1.2.2.1 Audit and assurance services

This is the strength of the company, revenue from auditand assurance services accounted for a large proportion ofthe company's total revenue. The company offer statutoryaudit and other compliance audit with Vietnamese

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report13

accounting standards, legal regulations in Vietnam as wellas internationally, or audit in specific requirements ofstakeholders. In an audit before accept a client auditrisk is considered in many aspects internal controlsystems, inherent risks in business environment. In mostaudits, UHY Ltd. also issues a management letter.Management letter explain the advantages and disadvantagesof management system in client’s company clearly, so thatthe client can improve management system and reduceeconomic risk. Besides, UHY Ltd. also performs audits onbehalf parent company, or supervises internal audit of acorporation. In present, audit and assurance services ofUHY Ltd can be listed namely as follow

Review of financial statements Review of internal controls. Preparation of financial statements Risk assessment and advisory Compliance Audit Financial Audit

In this service, clients will be satisfied by professionalauditors. In addition, the company's clients also havechance to hear advice from UHY global experts, dependingon the specific requirements of the audit.

1.2.2.2 Business financial consultancy

UHY clients are primarily the businesses consideringbuying or selling a part of other companies or itself topartners, companies planning to become listed companies.Financial expert of UHY will help customers evaluate,identify and select the appropriate strategy based on theinformation collected make the most effective decisions.Business financial consulting services aim at figure out

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report14

most effective decisions for client. To specify, in thiskind of service, UHY will add value to clients

Strategic Business Consulting: Strategic businessdevelopment, financial strategy long term financial plan,financial structure design, financial policy forenterprise –large scale corporations.

Management Consultancy: cash flow planning, budgetpreparation and management, working capital optimization

Stock issuance consulting: Support services beforelisted, equitization planning, business appraisal forequitization…

Buying or merging business advisory: Business appraisal,business operation assessing, business negotiationsupport, during and after purchase and merger financialsolution...

Selling business consultancy: Sell the business or partof business plan contructing, connecting potentialinvestors, planning, reasonable prices determination,before and after selling business financial advice....

Consulting uses derivative instruments in order to makebest use of the opportunities and minimize the risks incorporate financial management .

1.2.2.3 Tax consultancy

In the complex business environment, the reformationprocess in taxation system in Vietnam is accelerated.Recognizing the significant challenges related to taxissues, with a team of experienced consultants, UHYupdates new policies regularly and have a deepunderstanding of the tax laws in Vietnam and the

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report15

international practices. UHY assures that clients grow andprotect themselves from fluctuations in the mechanisms andpolicies to take advantage of taxation system in mosteffective way , the tax consultant of the company willspend adequate time to guide the method of applying thetax regime of Vietnam appropriately and effectively. UHYprovides tax services for wide range of clients frompublic companies to individual traders.

Prepare and submit tax reports Make use of the capital reserve account Buying or selling business tax consultancy Minimize loss, reduce costs for intangible assets International Tax Planning Mergers and acquisitions tax consultancy VAT and personal taxes for foreigners

1.2.2.4 Internal audit and risk management

The need of internal audit and risk management isincreasing, especially in the private sector, listedcompanies, foreign investment business, large statecorporations and international organizations. UHY Companywill assist businesses to improve the efficiency andeffectiveness of the internal control system throughinternal audit services and risk management consultancy.UHY Vietnam regularly exchanges expert with other memberfirms to provide unique services with high quality andenhance internal management for the client.

Perform all functions of the internal audit department for client.

Internal control system construction and operation consultancy

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report16

Business risk assessment, risk management analysis, corporate governance.

Internal audit and risk management training

1.2.2.5 Other services

From 2007, Vietnam become an official member of WTO, manykind of business came into existence. However they are inlack of knowledge and professional in managing theirbusiness. Based on this need of market, UHY Ltd. alsoprovide

Professional training service: Client’s staff can absorbup to date knowledge and many practical experience fromUHY experts

Accounting system design: UHY have sufficient experienceto help client build up the most suitable and economicalaccounting system to match with each clients

1.3. MANAGEMENT OF BUSINESS ACTIVITIES

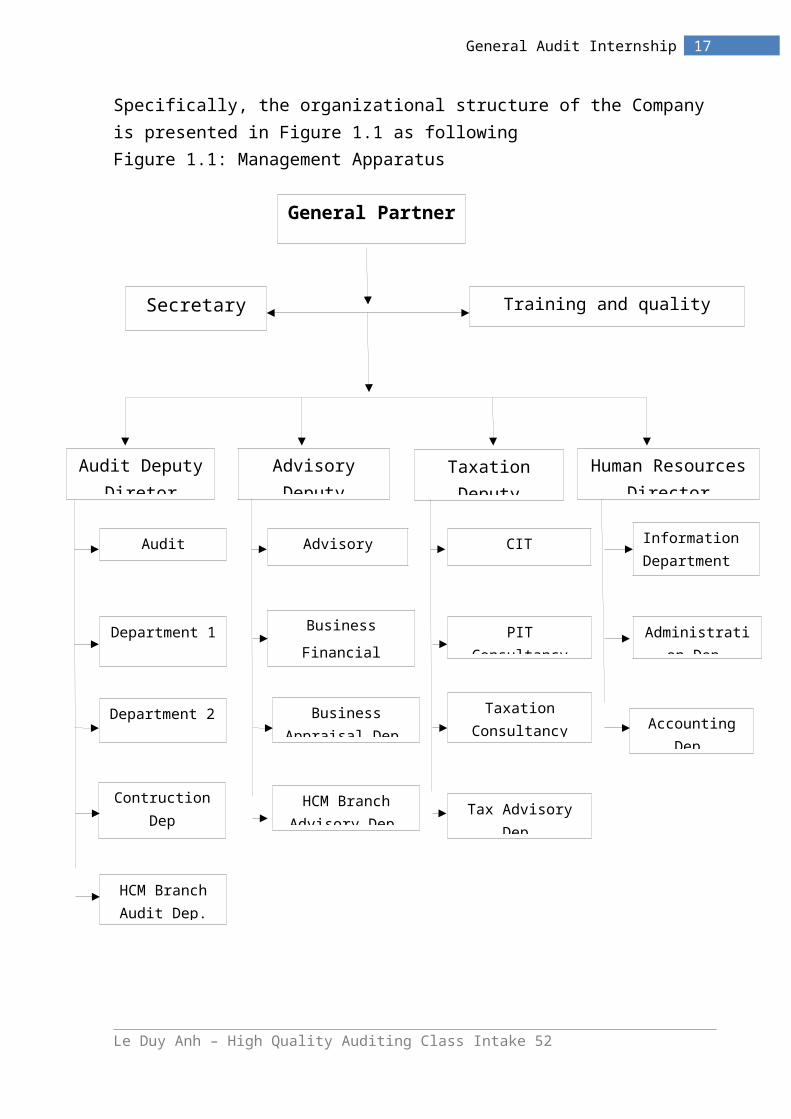

1.3.1. Management Apparatus

The organizational structure is one of the factors leadingto the success of the company. Management apparatus isorganized according to the global model of UHYInternational. UHY International have researched to builda complete engine management appropriate to ensure theeffectiveness and improve the competitiveness of theoperation. The model adopted by the company is operatingunder the direct function model, in which the Director isresponsible for macroeconomic management, issuing thedecision, and the functional parts duty to advise andcomments and perform assigned work.

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report17

Specifically, the organizational structure of the Company is presented in Figure 1.1 as followingFigure 1.1: Management Apparatus

Le Duy Anh – High Quality Auditing Class Intake 52

Secretary Training and qualitycontrol board

Audit DeputyDiretor

Human ResourcesDirector

AdvisoryDeputy

TaxationDeputy

AuditManager

Department 1

Department 2

ContructionDep

HCM BranchAudit Dep.

AdvisoryManager

BusinessFinancial

BusinessAppraisal Dep.

HCM BranchAdvisory Dep.

CITConsultancy

PITConsultancy

TaxationConsultancy

Tax AdvisoryDep.

Information Department

Administration Dep.

AccountingDep.

General Partner

General Audit Internship Report18

All department is coordinate with each others to make UHYLtd operate smoothly, but each part have it’s ownresponsibility

▪ General Partner is representative of company law,directly lead the entire operation of the company and heis responsible for reporting to capital contributingcouncil and the authority about all operations of theCompany.

▪ Deputy Directors are members of the Board of directorsas consider vice partners. They are responsible for eachservice line assigned by the General Director. On behalfof the company, they are allowed to sign contracts toprovide services within their assigned service line or onbehalf of the Company, they responsible for handling thecontract and negotiating with client.

▪ Secretary help Director Board in the administrating andmanaging of the Company

▪ Training and quality control directly operated by theGeneral director, is in charge of updating andinvestigating new accounting auditing regulation to trainpersonel within UHY company and outside UHY. This board isa group of senior auditor or directors. It can work asprofessional advisor for clients, especially to ensureservices such as : financial audit, advisory services.Furthermore, it is also responsible for observing the workdone by UHY auditor and suggesting appropriate solutions.In case of necessity, quality control can mobilize expertsfrom other departments to perform their duties.

▪ Expertise manager are in charge of expertise in eachspecific areas of the company including auditing services,

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report19

tax consulting, financial advisory, management consultingand training services.

▪ Audit departments are the divisions that directlyprovide professional audit services and other assuranceservices. The departments often have 20 to 30 employeesand serve various kind of business from commercialenterprises and tourism agencies are mainly client ofAudit department one to real estate and constructioncompanies managed by audit department two. Now, financialinstitute and project by international organizations isalso audited by audit departments’ professional staff

▪ Financial consultancy department is a parts professionalstaff provide financial advisory services to clients andis divided into the following specific arrays

Key value of the department come from corporate financeconsultancy including long-term financial strategybuilding, long-term financial planning, investmentprojects assessing and consultancy solutions to mobilizecapital for projects, risk management consulting, andfinancial management services.

Besides, financial consultancy department also providebusiness appraisal, asset appraisal for acquisitions,business appraisal for equitization of state enterprises,corporate restructuring advice, …

▪ The tax consulting department operate as a professionaldivision specializing in tax consulting services to itsclients, divided into common taxes such as corporateincome tax (CIT), personal income tax (PIT), import taxand other taxes. In addition, tax consulting departmentalso participated in the review of audit records with thetax issue.

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report20

▪ Branch in Ho Chi Minh City is under management of DeputyDirector. However, the organizational structure in thebranch is built based on service line such as: auditdepartment, financial advisory unit and tax consultingdepartment. Professional guidance will be provided by theDirectors in charge of each professional field.

▪ Accounting Department processes and records everyeconomic transactions and provide information about thefinancial position of business to support management boardin making decision.

▪ Administration department is responsible for managinghuman resource and archival document, ensure communicationin the company, administrative transactions, updateinformation, new text, tracking, labor allocation, servecomfortable conditions for staff to work.

In conclusion, this model enable director to supervisesubordinates, simultaneously each staff will be managed bythe department manager. The strict model helps thecompany operate more flexibly, management procedure willnot caught of overlap each other. Quality controlactivities are implemented strictly to ensure highefficiency. Even though every division of UHY Ltd has itsown mission, they mutually support, closely link to eachother. UHY have a strong structure close together to moveforward the success of the company.

1.3.2. Professional staff

UHY is always proud of outstanding board of directors andprofessional and experienced audit team is really goodprofessional , experienced in the field of audit andfinancial consultancy, who had been through a challengingtime and become very successful in the world's largest

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report21

auditing firms. UHY's key members are Masters inaccounting, auditing and business administration frompremier university in Vietnam as well as internationaluniversities in United State of America, United Kingdom,Australia.

In addition, employees of the company has alsoparticipated in international certification course likeACCA, CPA Australia and periodical training courses by UHYInternational.

Currently, UHY has over 115 professional staff , including17 certified public Acountant (CPA) and the majority ofthem come from the top audit companies in the world. Notonly does invaluable human resource entitle the companygrow and attract potential staff but it also meets theincreasingly high demands of clients. It is human resourcethat helps UHY Ltd become one of largest auditing firmsin Vietnam.

CHAPTER 2

AUDIT ORGANISING IN UHY AUDIT & ADVISORY LIMITED

2.1. ENGAGEMENT TEAM ORGANISING

Engagement organizing is a very important phase in an audit. It requires accurate time management, economical but still effective. From December to April is considered as audit season. In this time of the year, every auditing firms including UHY are always in the severe shortage of personnel.

Department Manager select engagement team and team leaderin accordance with the requirements of the audit contract.

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report22

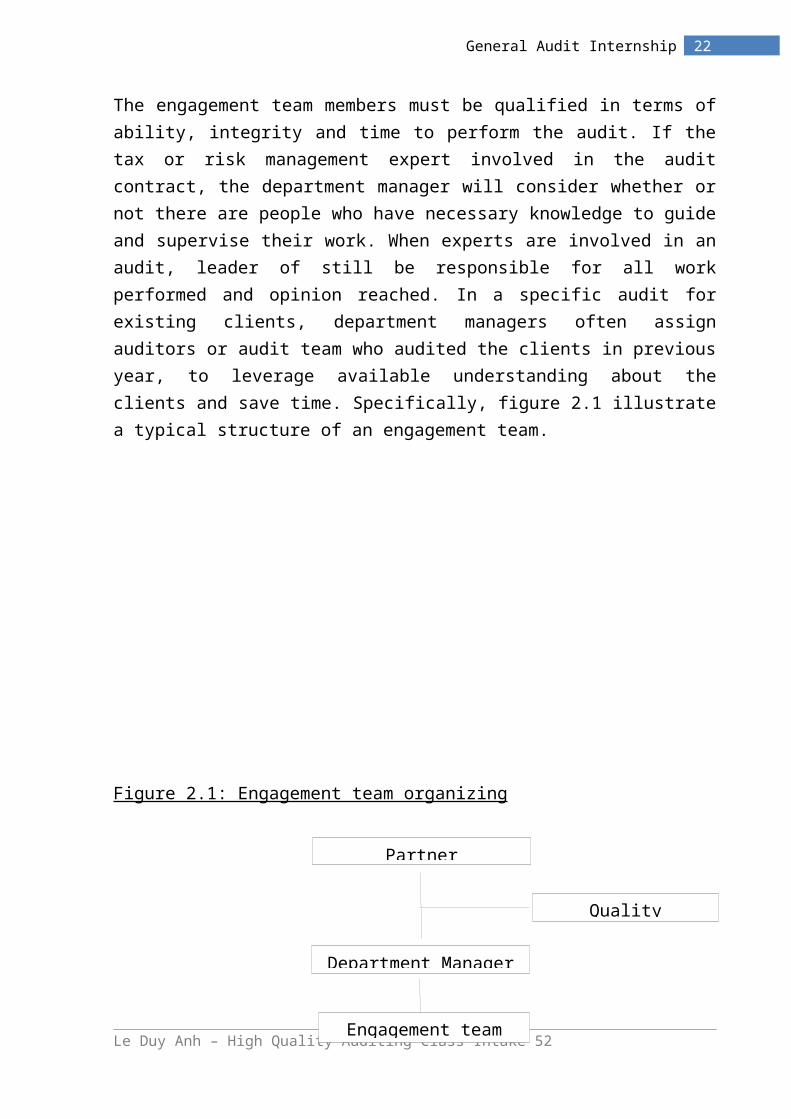

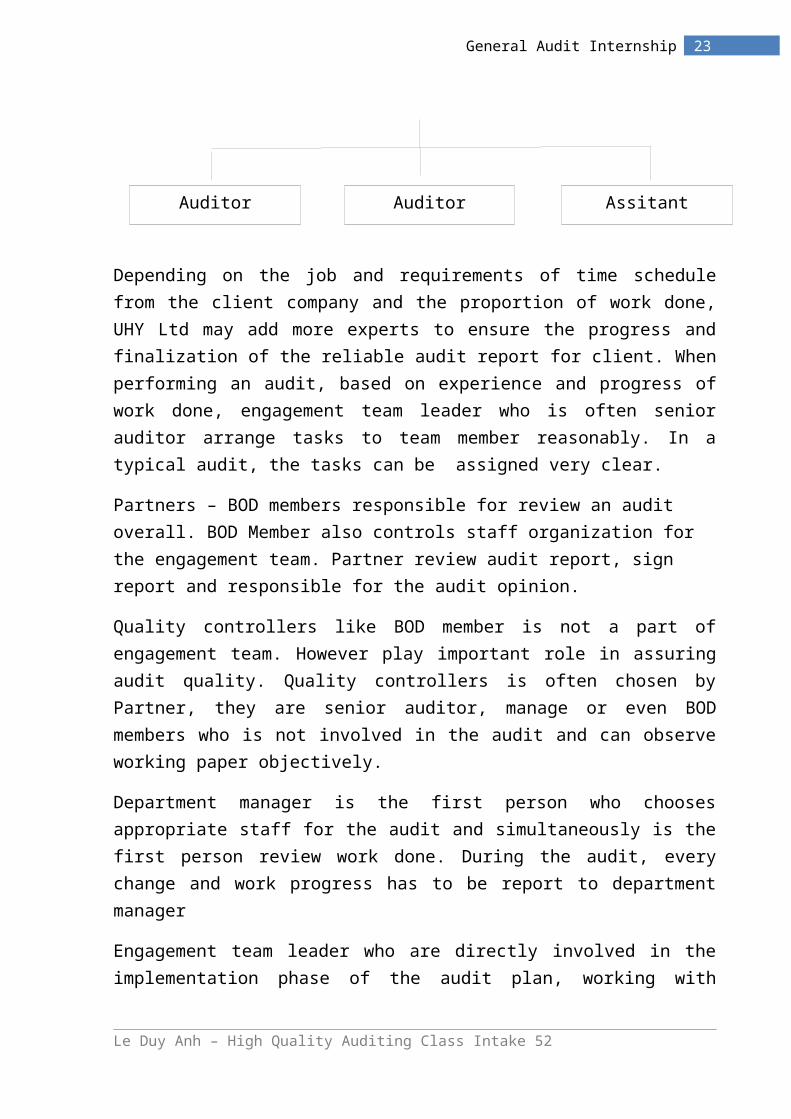

The engagement team members must be qualified in terms ofability, integrity and time to perform the audit. If thetax or risk management expert involved in the auditcontract, the department manager will consider whether ornot there are people who have necessary knowledge to guideand supervise their work. When experts are involved in anaudit, leader of still be responsible for all workperformed and opinion reached. In a specific audit forexisting clients, department managers often assignauditors or audit team who audited the clients in previousyear, to leverage available understanding about theclients and save time. Specifically, figure 2.1 illustratea typical structure of an engagement team.

Figure 2.1: Engagement team organizing

Le Duy Anh – High Quality Auditing Class Intake 52

Partner

Quality

Engagement team

Department Manager

General Audit Internship Report23

Depending on the job and requirements of time schedulefrom the client company and the proportion of work done,UHY Ltd may add more experts to ensure the progress andfinalization of the reliable audit report for client. Whenperforming an audit, based on experience and progress ofwork done, engagement team leader who is often seniorauditor arrange tasks to team member reasonably. In atypical audit, the tasks can be assigned very clear.

Partners – BOD members responsible for review an audit overall. BOD Member also controls staff organization for the engagement team. Partner review audit report, sign report and responsible for the audit opinion.

Quality controllers like BOD member is not a part ofengagement team. However play important role in assuringaudit quality. Quality controllers is often chosen byPartner, they are senior auditor, manage or even BODmembers who is not involved in the audit and can observeworking paper objectively.

Department manager is the first person who choosesappropriate staff for the audit and simultaneously is thefirst person review work done. During the audit, everychange and work progress has to be report to departmentmanager

Engagement team leader who are directly involved in theimplementation phase of the audit plan, working with

Le Duy Anh – High Quality Auditing Class Intake 52

AssitantAuditorAuditor

General Audit Internship Report24

client, contacting clients when there are some lack ofrequired documents. Leader will deal with several complexparts and observe other auditor to ensure the audit is runsmoothly and on schedule.

Assistant are less experienced staff directly involved inthe implementation phase of the audit plan, assistant willundertake a number of easy action requested by theengagement team leaders.

2.2. AUDIT PROGRAM ORGANISING

Audit Methodology used by UHY called UHY Audit Approach -UAA is based on the International auditing standard,Vietnam auditing standards and selectively applying themethod applied by leading audit firms in Vietnam.Systematic methodology is designed on deep understandingof operation and internal control system of Vietnameseclients. UAA audit approach is based on risk assessment,allowing auditors to focus more on the risky sectioninstead of non- critical item. UAA aims to improve auditquality and save time, which increases the effectivenessof the entire audit. Specifically, UAA guide auditors inproviding financial audit services.

2.2.1. Audit approach determination

In this stage, UHY Ltd collects and integrates informationabout clients, as well as the operating environment theclients. At the same time, senior auditor will determinesections that contain the high risk of materialmisstatement and figure out the parts of the financialstatements under effect of accounting estimates andjudgments of the clients.

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report25

In the next step, the company will analyze materiality ofthe risks identified and set out the procedures to becarried out. Planning matrix shows the relationshipbetween risk of misstatement in significant accounts andmanagement assertion involved in financial statements, andhow to determine audit objectives. Audit objective isoften based on corresponding reasonable assertionsincluding: completeness, existence, accuracy andvaluation, right and obligation, presentation anddisclosure... For each objective, the auditors willdetermine the level of risk and make preliminary decisionof combinations of control testing, analytical proceduresand substantive test for each transaction lines and theaccount with a view of achieving high efficiency.

In summary, the audit planning stage is implemented everynecessary procedures. The planning stage will help thecompany to plan audits process.UHY always consider thisstage as a key phase of an audit, it make engagement teammanage time and auditing methods proactively. Where, theaudit will be conducted favorably, keep up the progress.

2.2.2. Internal control system assessment

In each audit, UHY Ltd assesses internal controlenvironment and control procedures for important types oftransactions and material balances. How the auditor relieson the client’s internal control will determine thenature, time and extent of the audit test. Therefore, theassessment of the company's control is not limited.Auditors must understand about the attitude of BOD towardinternal control, design of control and control proceduresare actually applied in continuous basis. Specifically,engagement team can evaluate the design and implementationof control procedures in each department, each transaction

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report26

line through interviewing, investigating document andvouchers. Furthermore, auditor can check compliance withthe internal control systems of the company with theEnterprise Law, Securities Law and temporary regulationrelating to the current operations of the company.

2.2.3. Audit tests

During the audit, the auditors perform audit proceduresinclude detailed test of control and substantive test. Anaudit will be performed at the client office.

First, basing on level of reliance on internal controldetermined in last step, control testing is designed.Voucher flow will be check to ensure existence of control.Internal control structure is also evaluated in term ofeffectiveness. Furthermore, transaction and document havechance to be checked. UHY Ltd builds test of control basedon characteristics of each client. At the same time,materiality and risk factor is also considered when testsof control are conducted.

Secondly, nature time and extent of substantive tests aredetermined by senior auditors. The senior auditors giveoverall assessment on the internal control systems ofclient’s company in order to so. After that substantivetesting procedures are performed. To specify, the auditorscan review accounting records and accounting books ofclients, analyze fluctuations in equity, dividends andlong-term debts if any. Besides, independent confirmationletter for bank accounts , receivables and payable isvital procedures to achieve reasonable assurance ofaccount balances. Another procedure seem to beindispensable is to witness cash counting, inventorycounting, fixed asset recording at the end of the

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report27

financial year. In addition, the auditor can analyzeprofitability, solvency, business efficiency and financialviability through the year to detect unreasonable things.However, UHY engagement team always faces up with tradeoff because of time and resource limitation. To ensurequality of the audits, UHY engagement team leader andmanager determine materiality threshold carefully and setup suitable priorities when performing substantive test.

In summary, through implementing these above tests, UHYengagement team will consider and assess whether theevidence collected is adequate and appropriate enough, andwhether there is need to conduct additional testingprocedures mainly based on materiality and riskassessment. When seeing a problem occurs or exceptions notcovered by collected evidence, engagement team willimplement further investigation.

2.2.4. Audit completion

Audit completion may be the most challenging phase of theaudit. At this time, all staff of UHY Ltd has to workovertime to complete reliable audit report and managementletter for clients.

Specifically, each engagement team will summarize allworking paper and resolve issues arising after the auditprocess. After that, leader have a more important duty tofulfill is to prepare draft audit report and managementletter on the key issues that the team discovered in theaudit. It is important that, in UHY the team leader has tointerpret every issue she or he consider as important toBOD. Manager and leader of engagement team responsible forsupporting Partners in review the audit reports.

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report28

Besides, UHY Ltd may negotiate with client’s board ofdirector about adjusting entries. In addition, there aremany problems about the effectiveness of management andaccounting system need to be discuss.

In addition, the Company will assess the audit differencesthat clients still reluctant to adjust. If afterimplementing further audit procedures, UHY’s team stillbelieves that if not corrected, the differences can leadto the existence of a material misstatement, Auditor willdiscuss this issue with board of directors of client andconsider the probable impact on the audit report if theydo not fully reflect this problem in the financialstatements. The difference may not material in isolationbut aggregated differences are probably critical. In UHYconsidering this issue is compulsory, the auditor willperform some additional audit procedures or require mustadjust the difference this audit.

In summary, audit completion is the most important phaseof an audit. Under the pressure of client and legalconstraint, UHY’s auditors carefully observe work done inthe audit, arising problems and discuss with clientcleverly. Client’s satisfaction and a reliable auditreport always meet congruence in UHY Ltd.

2.3 AUDIT PROFILE ORGANISING

Audit profile is very important to an audit and auditorsas well. The evidences that is basis for auditor giveopinion is almost save in audit profile. Audit profilehelp auditor explain their conclusion in a convincing way,and enable to Ministry of finance control quality of auditin a large scale. It contains all the information about anaudit, greatly affects the quality of an audit.

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report29

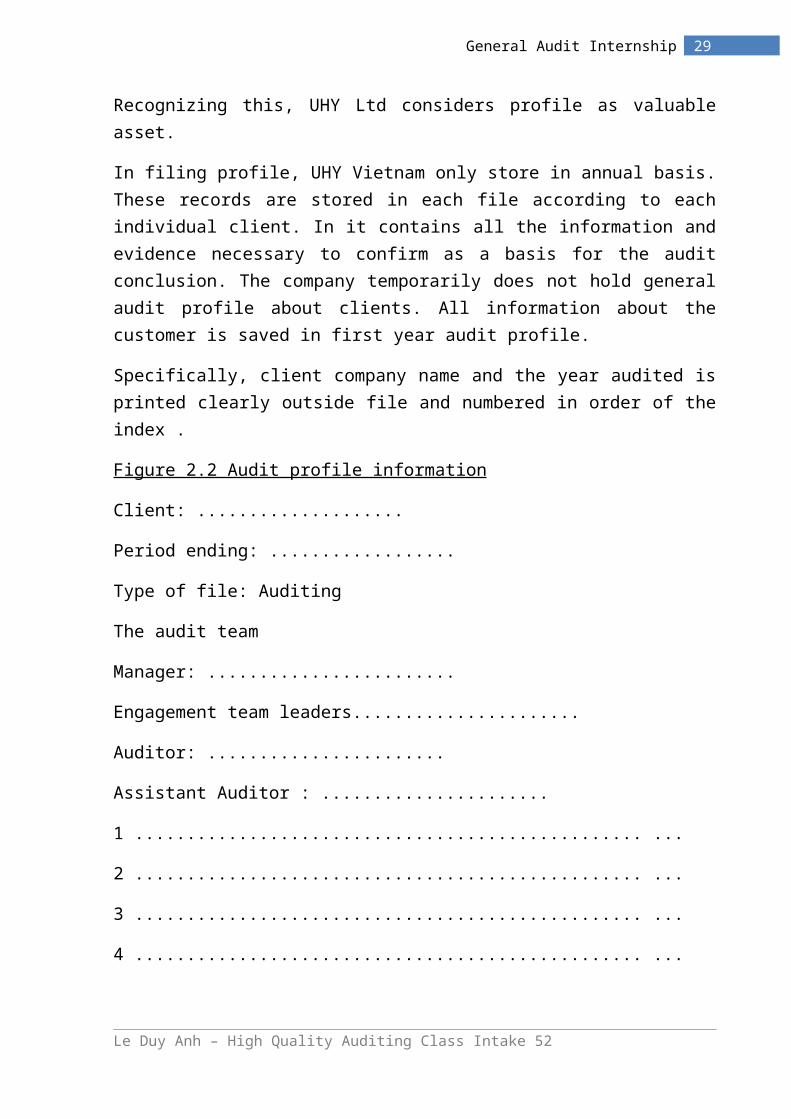

Recognizing this, UHY Ltd considers profile as valuableasset.

In filing profile, UHY Vietnam only store in annual basis.These records are stored in each file according to eachindividual client. In it contains all the information andevidence necessary to confirm as a basis for the auditconclusion. The company temporarily does not hold generalaudit profile about clients. All information about thecustomer is saved in first year audit profile.

Specifically, client company name and the year audited isprinted clearly outside file and numbered in order of theindex .

Figure 2.2 Audit profile information

Client: ....................

Period ending: ..................

Type of file: Auditing

The audit team

Manager: ........................

Engagement team leaders......................

Auditor: .......................

Assistant Auditor : ......................

1 ................................................. ...

2 ................................................. ...

3 ................................................. ...

4 ................................................. ...

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report30

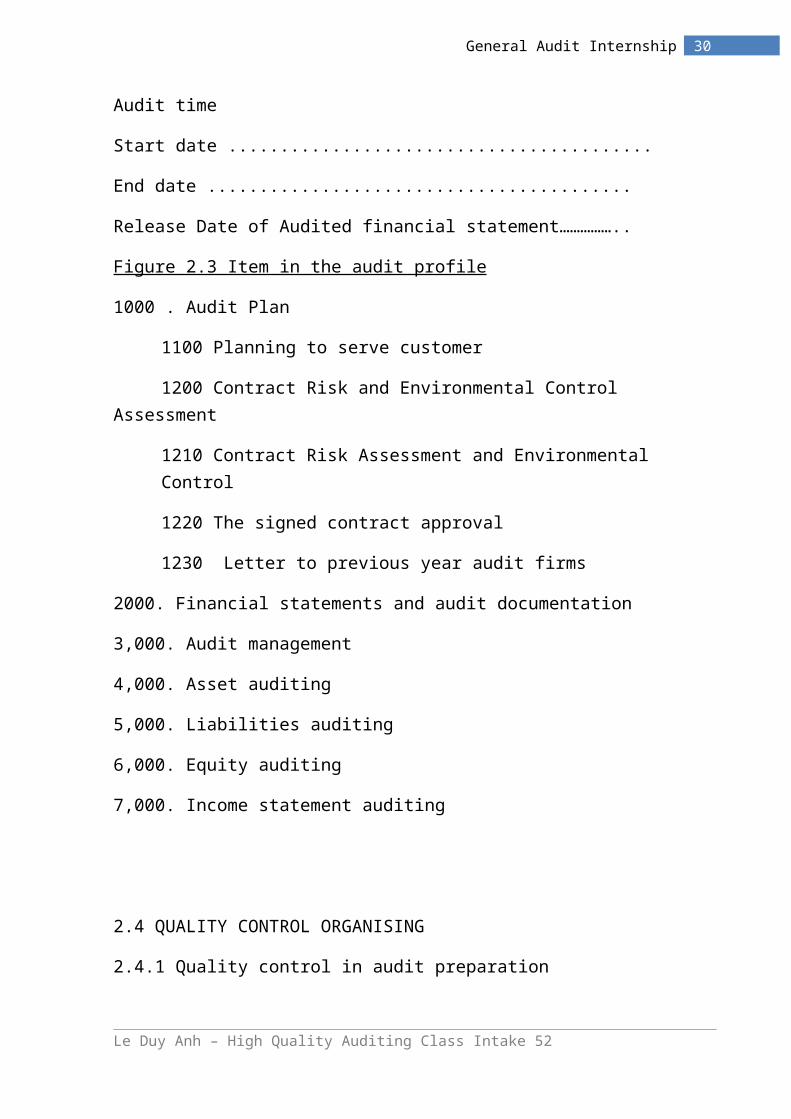

Audit time

Start date .........................................

End date .........................................

Release Date of Audited financial statement……………..

Figure 2.3 Item in the audit profile

1000 . Audit Plan

1100 Planning to serve customer

1200 Contract Risk and Environmental Control Assessment

1210 Contract Risk Assessment and Environmental Control

1220 The signed contract approval

1230 Letter to previous year audit firms

2000. Financial statements and audit documentation

3,000. Audit management

4,000. Asset auditing

5,000. Liabilities auditing

6,000. Equity auditing

7,000. Income statement auditing

2.4 QUALITY CONTROL ORGANISING

2.4.1 Quality control in audit preparation

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report31

2.4.2 Quality control in audit performation

2.4.3 Quality control in audit completion

CHAPTER 3

COMMENTS AND RECOMENDATION ON AUDIT ORGANISING OF UHY AUDIT & ADVISORY LIMITED

3.1. COMMENTS ON ENGAGEMENT TEAM ORGANISING

3.1.1. Advantages

Organization model of UHY Ltd is in accordance with the characteristics and size of company. Whereby, UHY Vietnam exploited specialization by sector management so that management decisions are made properly and timely to achieve high efficiency. The management apparatus is effective and suitable.

In organizing engagement team, the company organizes auditteam in scientific and reasonable way. Staff are carefullyrecruited and reasonably allocated for each audit. The

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report32

company's human resources are dynamic, enthusiastic, deep understanding of work and have professional style.

The success of the company has contributed mainly by engagement team in a scientific way. Leader of the team ishighly skilled and experienced, can control the entire audit. The audit assistants are assigned tasks that are suitable with their strengths, and at the same time can help each other in different section of the job as well asshare experience to increase solidarity within the company.

The assignments of each member of the audit team specifically can help team members understand and fulfill their duties better. With the division of work is assignedbased on actual experience of the auditors and assistants helped audit run smoothly and quickly.

3.1.2. Disadvantages

From December to April, work pressure is very intensive, the auditors often have to work overtime to ensure progress of job. This causes huge work pressure on staff, leading to inefficient work. The company always creates conditions for staff to take rest in the leisured season for them to re-create their health. In pressure season, UHY Ltd always hire new employees to reduce pressure of the job and trained them to develop the company in the future.

3.2 COMMENTS ON AUDIT PROGRAM & QUALITY CONTROL

3.2.1. Advantages

Audit program of the company audit is implemented well, there are many levels of management, each task in the process is closely monitored by the board of director and

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report33

engagement team leader of the audit. But most important thing is the self-examination of the auditors who directlyconduct the audit. Thanks to the strict control, UHY Ltd. ensures that auditors detect all material misstatement in the audit. Whereby, auditors as well as the company's reputation is enhanced through the time.

In addition, on the organization filing, audit profile is kept at the office of the company makes it easy for auditor find data about clients, especially the planning stage of the audit and after the audit.

Furthermore, profiles are numbered in systematic way. Thathelps auditor easily find the information contained in audit profile

Quality control the company has established quality control board to control the quality of audits take place faster and easier while maintaining efficiency . The members of the quality control are leading experts in the auditing industry , and is the direct management of the CEO . In case of necessity, the quality control departmentcan mobilize experts from other departments to carry out their duties to ensure the quality of the audit.

The quality control takes place in three stages:

- Planning the audit .

- Perform audit plan .

- Prepare financial statements .

At each stage divided into specific tasks are assigned jobs , and revised guidance should ensure the quality of the audit .

3.2.2. Disadvantages

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report34

Audit process: Process audit of the company has been builtin accordance with company standards but more attention should be paid to the audit plan for the audit season due to lack of personnel to this job has not been focused, audit program not been implemented specifically for each audit and each specific customer. This affects the resultsof collecting evidence as well as innovative features of the KTV.

On filing: The filing office immediately at ease in the company but finding but if the number of records, it will cause many difficulties in preservation. The company should have separate records storage room, just done in the office storage for frequently used documents.

3.3 RECOMMENDATIONS ON AUDIT ORGANISING OF UHY AUDIT & ADVISORY LIMITED

In the trend of international economic integration , our country's economy is growing strongly and transparency requirements on financial information of users increasing . This requires the Company in general audit and audit company UHY in particular to improve the qualityof routine activities . With the knowledge learned with knowledge accumulated during practice at the company , I would like to present some proposals first improve the quality of audit work at UHY LTD as follows :

For audit planning , this is a very important job in an audit , because this work may KTV work most efficiently , saving time and costs . The company should focus on planning the audit . The chairman and members of the AuditDirectorate should develop a standard form audit program and then apply to each specific audit may change a few

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report35

jobs . This will save time while ensuring audit can be done with the schedule and the best quality .

On the season the audit, the auditors often have to work overtime to make up the work pressure makes the KTV easilylead to errors, we always create conditions for staff restof the season to date no test renewable energy accounting for their labor, while mode suitable for KTV. However, theCompany need to recruit new staff and training to meet therequirements of the audit contract.

Regarding the filing, the company should have separate records storage room, just done in the office storage for frequently used documents, avoid misplaced documents.

CONCLUSION

Le Duy Anh – High Quality Auditing Class Intake 52

General Audit Internship Report36

REFERENCES

Le Duy Anh – High Quality Auditing Class Intake 52