Embed Size (px)

Citation preview

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 1

www.researchjournali.com

John MacCarthy

PhD Candidate, Lecturer, Zenith University College,

Ghana

The Effect Of Cash

Reserve Ratio (CRR)

On The Financial

Performance Of

Commercial Banks And

Their Engagement In

CSR In Ghana

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 2

www.researchjournali.com

ABSTRACT

It is perceived that reserve requirements promote the financial performance of commercial banks and their

engagement in corporate social responsibility. However, not all empirical studies support this perception. This

study therefore examines the effect of cash reserve ratio on the financial performance of banks and their level

of engagement in corporate social responsibility. Data on banks’ cash reserve ratios from Bank of Ghana and

data on corporate social responsibility engagement and return on investment from the 2013 annual reports of

20 commercial banks in Ghana are used. It is found that cash reserve ratio positively relates to the financial

performance of commercial banks, but it negatively relates to banks’ level of engagement in corporate social

responsibility. Also, cash reserve ratio significantly and strongly predicts financial performance of

commercial banks in terms of return on investment. It is recommended that banks enhance their engagement

in corporate social responsibility activities that improve bank-customer relationship and customer patronage.

Keywords: Reserve requirement, cash reserve ratio, return on investment, financial performance, corporate

social responsibility, Central Bank

1. INTRODUCTION

In most economies of the world, the Central Bank has the basic role of regulating banking activities and using

monitory policy to ensure a vibrant stable economy (Hoggson, 1926; Gorton & Winton, 2002). The Central

Bank serves as a moderator of activities of banking through its regulations (Investopedia, 2014). It sets up

regulatory standards for banks’ entry in the industry, as well as the management of banks (Gorton & Winton,

2002). This is to ensure that the economic interests of banks, their customers and the economy at large are not

jeopardised by banking activities and customer behaviour (Peydr´o, 2010). The Central Bank’s banking

regulation is premised on two ideas: to insure banks against bank-runs and therefore against the risk of

systemic failure (Hoggson, 1926; Gray, 2011), and to protect liability and capital providers (depositors and

shareholders) from corporate governance problems resulting from the inability of depositors and shareholders

to monitor banks (Gray, 2011). The Central Bank’s regulatory role is critical for the survival of banks because

asset transformation activities, which include liquidity and maturity transformations, expose banks to several

risks, including bank runs and banking panics (Francis & Osborne, 2009).

Embedded in the framework of Central Bank’s regulatory policies is the reserve capital requirement. Capital

requirements determine the capital level maintained by banks in proportion to their assets (King, 2010). The

reserve requirement, also called cash reserve ratio, is a central bank regulation employed by most, but not all,

of the world's Central Banks (Jablecki, n.d.). It sets the minimum fraction of customer deposits and notes that

each commercial bank must hold as reserves rather than lend out (Peydr´o, 2010; Gray, 2011). These required

reserves are normally in the form of cash stored physically in a bank vault (vault cash) or deposits made with

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 3

www.researchjournali.com

a central bank. The required reserve ratio is sometimes used as a tool in monetary policy that affects the

country's borrowing and interest rates by changing the amount of funds available for banks to make loans

with (Ronitaille, 2011).

Recognizing the important role of the banking sector in the payment system and the various impacts of

banking crises on the economy, regulators impose mandatory capital requirements that may differ from

market generated optimal capital structure. From the viewpoint of Central Banking, the reserve requirement

secures banks, their customers, shareholders and the economy at large (Glocker & Towbin, 2012). In essence,

the reserve requirement provides security of all stakeholders and associated parties in the lifeline of a bank.

Nonetheless, not all researches have justified that the reserve requirement does not lay negative effects on the

operational activities, liquidity and financial performance of banks (Gray, 2011; Ma et al. 2011).

Whiles some researches have revealed that reserve requirements impact banks’ financial performance (Gray

2011; Jablecki, n.d., King, 2010), some have confirmed that reserve requirements are the basis of the poor

financial performances of some banks in the world (Ma, Xiandong & Xi, 2011); Nacuer & Kandil, n.d.).

Based on some empirical studies, Ma et al. (2011) argue that reserve requirement, in many situations,

minimises banks’ level of engagement in corporate social responsibility. Moreover, the reserve requirement is

likely to prevent employment or call for the withdrawal of existing employees (King, 2010; Nacuer & Kandil,

n.d.). The negative influence of reserve requirement on banks’ financial performance, engagement in CSR

and employment are often driven by liquidity problems faced by banks in the face of cash reserves (Gray,

2011; Ma et al. 2011).

Though it forms the basis for the existence of commercial banks, not much is known about the effect of the

reserve requirement on the financial performance of commercial banks and their contribution to economic

development through corporate social responsibility (CSR) engagement. In view of this situation, it is argued

that the level of research needed to identify the credibility of the reserve requirement of the Central Bank is

grossly lacked (Derina, 2011; Glocker & Towbin, 2012). This situation is worse from a Ghanaian perspective

(Antwi-Asare & Addison, 2000). Thus researches that delve into the impact of Bank of Ghana’s reserve

requirement on the performance of banks and their contribution to economic development through CSR

engagement are few. This is a major problem because opinions about the relevance of the reserve requirement

and its suitability for Ghana’s banking sector are always conflicting from the standpoint of commercial banks,

the public, researchers and the Central Bank (Antwi-Asare, 2000; Robitaille, 2011). Moreover, though it is

perceived by commercial banks and some part of the public that the reserve requirement comes with much

more of challenges and disadvantages to commercial banks, not all research studies justify it. It is therefore

believed that increased number of researches on the subject can bring to light the relevance of reserve

requirement and its impact on banks’ performance and economic development through CSR engagement.

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 4

www.researchjournali.com

2. RESEARCH OBJECTIVE

The objective of this study is to investigate the effect of cash reserve ratio on the financial performance of

commercial banks in Ghana and their level of engagement in corporate social responsibility. This paper seeks

to contribute to the public’s scant knowledge about the relevance of Bank of Ghana’s reserve requirement.

The specific objectives of this study include:

To identify the basic role of reserve requirement of the Bank of Ghana; and

To assess the effect of the reserve capital requirement on financial performance in terms of return on

investment (ROI) and engagement in corporate social responsibility (CSR).

3. LITERATURE REVIEW

The existence of many banking sectors is driven by the reserve requirement of the Central Bank (Peydr´o,

2010; Robitaille, 2011). Invariably, the Central Bank’s reserve requirement is a primary security measure that

serves as a warranty for the existence of commercial banks. Research has shown that most of the world’s

banking sectors are regulated in the light of the reserve requirement (Santos, 2000). Reserve requirements of

the Central Bank are important for avoiding bank runs (Bianchi & Bigio, 2013; Bouwman, 2013; Calomiris,

Heider & Hoerova, 2012; Robitaille, 2011); thus it plays a role of preventing the bankruptcy of commercial

banks through a regulation of customer behaviour and the provision of access to the discount window of

interbank lending and borrowing (Glocker & Towbin, 2012; Bech & Keiser, 2012). The reserve requirement

characteristically affects the liquidity of banks. This happens in two dimensions, namely from the

perspectives of bank customers or depositors and commercial banks ((Glocker & Towbin, 2012). Liquidity to

customers or depositors is basically needed to avoid bank runs caused by a situation where banks use too

much of deposits to finance their operational activities (Bindseil, Manzanares &Weller, 2004). Reserve

requirement provides systems for making customers’ deposits accessible to them, while ensuring that banks

make substantial funds for their operational activities through the discount window. Through the reserve

requirement, the Central Bank is able to implement its monitory policies towards a stable economy (Gray,

2011; Bianchi & Bigio, 2013; Bouwman, 2013; Calomiris, Heider & Hoerova, 2012; Robitaille, 2011). From

the perspective of Central Banking, the reserve requirement secures banks, their customers, shareholders and

the economy at large (Glocker & Towbin, 2012).

Surprisingly, there is no clear-cut position of researchers about the effect of research requirements on banks’

financial performance and their contribution to economic growth through corporate social responsibility. On

the one hand, some researches have shown that reserve requirements impact banks’ financial performance in

terms of return on investment (ROI) (Gray 2011; Jablecki, n.d., King, 2010). On the other hand, a section of

empirical studies have shown that reserve requirements negatively influence banks’ financial performance

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 5

www.researchjournali.com

and engagement in corporate social responsibility (Ma, Xiandong & Xi, 2011); Nacuer & Kandil, n.d.). Based

on some empirical studies, Ma et al. (2011) argue that reserve requirement, in many situations, minimises

banks’ level of engagement in corporate social responsibility. Moreover, the reserve requirement could

prevent employment or call for the withdrawal of existing employees as a result of ready access to funds to

reward employees (King, 2010; Nacuer & Kandil, n.d.). The negative influence of reserve requirement on

banks’ financial performance, engagement in CSR and employment are often driven by liquidity problems

faced by banks in the face of cash reserves (Gray, 2011; Ma et al. 2011).

4. HYPOTHESES

Based on the above theoretical and empirical literature, the study seeks to test the following hypotheses:

H0: There is no relationship between cash reserve ratio (CRR) of commercial banks and their financial

performance in terms of return on investment (ROI).

H1: There is a significant relationship between cash reserve ratio (CRR) of commercial banks and their

financial performance in terms of return on investment (ROI).

H02: There is no relationship between cash reserve ratio (CRR) of commercial banks and their level of

enjoyment in corporate social responsibility (CSR).

H12: There is a significant relationship between cash reserve ratio (CRR) of commercial banks and their

level of enjoyment in corporate social responsibility (CSR).

H03: Cash reserve ratio (CRR) of commercial banks does not significantly predict financial performance

in terms of return on investment (ROI).

H13: Cash reserve ratio (CRR) of commercial banks significantly predicts financial performance in

terms of return on investment (ROI).

5. METHODOLOGY

This paper adopts a mixed research technique that comprises of quantitative and qualitative research

approaches. The quantitative research approach provides a platform for testing hypotheses, deriving reliability

for this study and ensuring rigor in using randomisation methods in generalising findings over the commercial

banking sector of Ghana. In terms of the qualitative research technique, content analysis is used to identify the

role and relevance of reserve requirements. Content analysis is a method of analysing written, verbal or visual

communication messages (Elo & Kyngas, 2008; Kondracki et al. 2002). This study focuses on an examination

of related academic papers and policy documents on reserve requirement of the Bank of Ghana.

To make room for generalising findings in this study, the simple random sampling method is used to select 20

commercial banks that constitute about 71% of commercial banks in Ghana. In the sampling process, it is

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 6

www.researchjournali.com

assumed that the population of commercial banks in Ghana is homogeneous, or all banks in Ghana are under

the influence of the same regulatory policies and environment. Secondary data are used in this paper. These

data involve cash reserve ratios, CSR and ROI of each of the 28 commercial banks in Ghana. These data are

accessed from the banks and double-checked for accuracy from the Bank of Ghana and the 2013 annual

reports of the participating commercial banks.

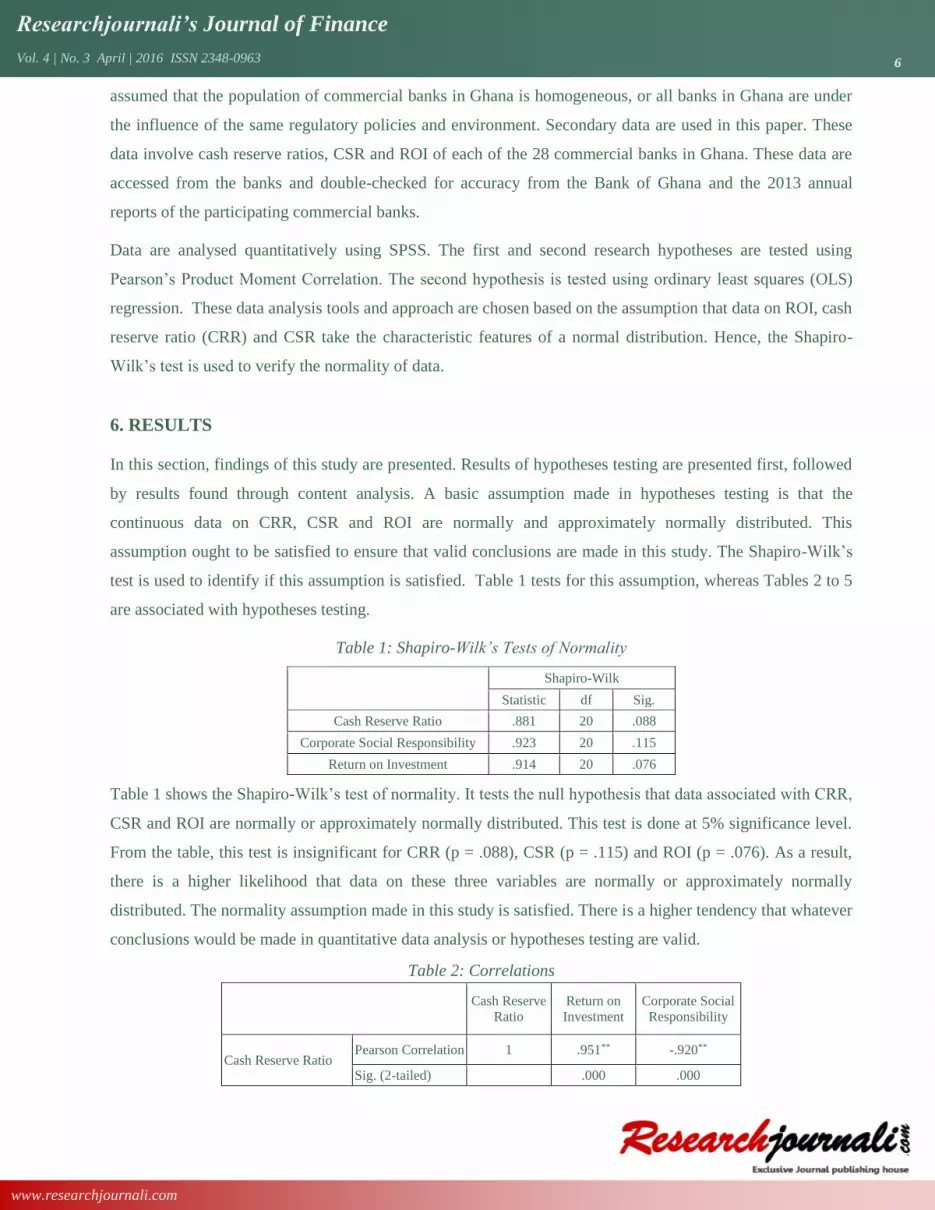

Data are analysed quantitatively using SPSS. The first and second research hypotheses are tested using

Pearson’s Product Moment Correlation. The second hypothesis is tested using ordinary least squares (OLS)

regression. These data analysis tools and approach are chosen based on the assumption that data on ROI, cash

reserve ratio (CRR) and CSR take the characteristic features of a normal distribution. Hence, the Shapiro-

Wilk’s test is used to verify the normality of data.

6. RESULTS

In this section, findings of this study are presented. Results of hypotheses testing are presented first, followed

by results found through content analysis. A basic assumption made in hypotheses testing is that the

continuous data on CRR, CSR and ROI are normally and approximately normally distributed. This

assumption ought to be satisfied to ensure that valid conclusions are made in this study. The Shapiro-Wilk’s

test is used to identify if this assumption is satisfied. Table 1 tests for this assumption, whereas Tables 2 to 5

are associated with hypotheses testing.

Table 1: Shapiro-Wilk’s Tests of Normality

Shapiro-Wilk

Statistic df Sig.

Cash Reserve Ratio .881 20 .088

Corporate Social Responsibility .923 20 .115

Return on Investment .914 20 .076

Table 1 shows the Shapiro-Wilk’s test of normality. It tests the null hypothesis that data associated with CRR,

CSR and ROI are normally or approximately normally distributed. This test is done at 5% significance level.

From the table, this test is insignificant for CRR (p = .088), CSR (p = .115) and ROI (p = .076). As a result,

there is a higher likelihood that data on these three variables are normally or approximately normally

distributed. The normality assumption made in this study is satisfied. There is a higher tendency that whatever

conclusions would be made in quantitative data analysis or hypotheses testing are valid.

Table 2: Correlations

Cash Reserve

Ratio

Return on

Investment

Corporate Social

Responsibility

Cash Reserve Ratio Pearson Correlation 1 .951** -.920**

Sig. (2-tailed) .000 .000

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 7

www.researchjournali.com

N 20 20 20

Return on Investment

Pearson Correlation .951** 1 -.916**

Sig. (2-tailed) .000 .000

N 20 20 20

Corporate Social

Responsibility

Pearson Correlation -.920** -.916** 1

Sig. (2-tailed) .000 .000

N 20 20 20

**. Correlation is significant at the 0.05 level (2-tailed).

Table 2 shows Pearson’s correlations between CRR and ROI and CRR and CSR. Statistics in this table are the

outcomes for testing the first and second research hypotheses of this study. The first hypothesis is that

commercial banks’ cash reserve ratios do not have any significant relationship to bank growth in terms of

return on investment. The second hypothesis is that commercial banks’ cash reserve ratios do not have any

significant relationship to level of corporate social responsibility engagement. These hypotheses are tested at

5% significance level. From the table, the first hypothesis test is significant, r (20) = .951, p = .000, likewise

the second hypothesis, r (20) = -.916, p = .000. The two null hypotheses are therefore not accepted. It can be

said that banks’ cash reserve ratio positively relates to return on investment. This means that the reserve

requirement of the Central Bank promotes the financial growth or performance of banks. On the contrary, the

reserve requirement negatively relates to the level of engagement in CSR. Thus, the reserve requirement

minimizes the level of banks’ engagement in CSR. Based on outcome of the first hypothesis, it is highly

likely that CRR predicts ROI. Tables 3 to 5 confirms this assertion using ordinary least squares (OLS)

regression.

Table 3: Model Summary

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .951a .905 .900 18939.30290

a. Predictors: (Constant), Cash Reserve Ratio

Table 3 is the model summary of the prediction of ROI by CRR. In the table, CRR account for about 90.5%

of variance on ROI. This statistic indicates that financial performance of banks is strongly predicted by banks’

cash reserve ratios. This confirms the strong positive relationship between cash reserve ratio and return on

investment in Table 2.

Table 4: ANOVAb

Model Sum of Squares df Mean Square F Sig.

1 Regression 6.159E10 1 6.159E10 171.699 .000a

Residual 6.457E9 18 3.587E8

Total 6.804E10 19

a. Predictors: (Constant), Cash Reserve Ratio

b. Dependent Variable: Return on Investment

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 8

www.researchjournali.com

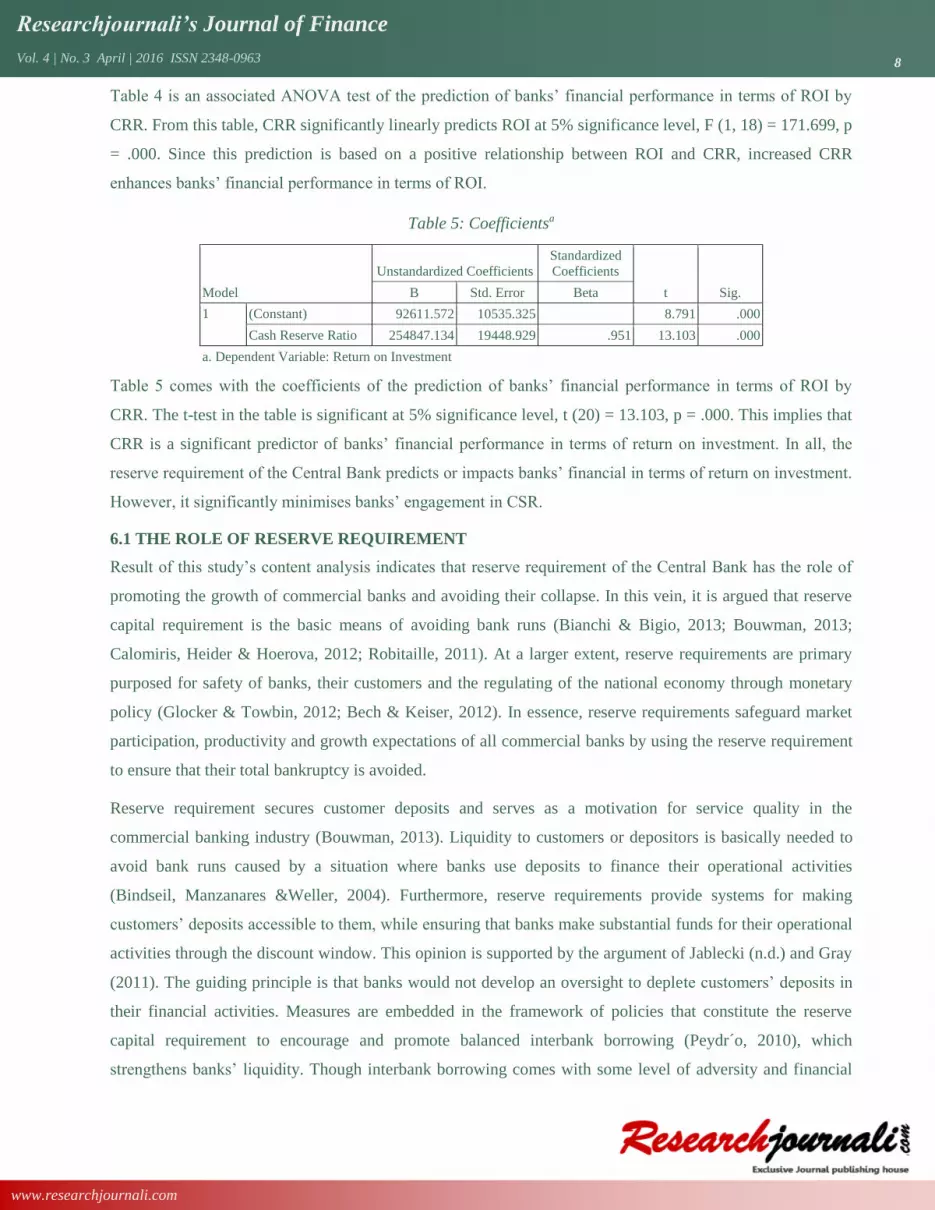

Table 4 is an associated ANOVA test of the prediction of banks’ financial performance in terms of ROI by

CRR. From this table, CRR significantly linearly predicts ROI at 5% significance level, F (1, 18) = 171.699, p

= .000. Since this prediction is based on a positive relationship between ROI and CRR, increased CRR

enhances banks’ financial performance in terms of ROI.

Table 5: Coefficientsa

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) 92611.572 10535.325 8.791 .000

Cash Reserve Ratio 254847.134 19448.929 .951 13.103 .000

a. Dependent Variable: Return on Investment

Table 5 comes with the coefficients of the prediction of banks’ financial performance in terms of ROI by

CRR. The t-test in the table is significant at 5% significance level, t (20) = 13.103, p = .000. This implies that

CRR is a significant predictor of banks’ financial performance in terms of return on investment. In all, the

reserve requirement of the Central Bank predicts or impacts banks’ financial in terms of return on investment.

However, it significantly minimises banks’ engagement in CSR.

6.1 THE ROLE OF RESERVE REQUIREMENT

Result of this study’s content analysis indicates that reserve requirement of the Central Bank has the role of

promoting the growth of commercial banks and avoiding their collapse. In this vein, it is argued that reserve

capital requirement is the basic means of avoiding bank runs (Bianchi & Bigio, 2013; Bouwman, 2013;

Calomiris, Heider & Hoerova, 2012; Robitaille, 2011). At a larger extent, reserve requirements are primary

purposed for safety of banks, their customers and the regulating of the national economy through monetary

policy (Glocker & Towbin, 2012; Bech & Keiser, 2012). In essence, reserve requirements safeguard market

participation, productivity and growth expectations of all commercial banks by using the reserve requirement

to ensure that their total bankruptcy is avoided.

Reserve requirement secures customer deposits and serves as a motivation for service quality in the

commercial banking industry (Bouwman, 2013). Liquidity to customers or depositors is basically needed to

avoid bank runs caused by a situation where banks use deposits to finance their operational activities

(Bindseil, Manzanares &Weller, 2004). Furthermore, reserve requirements provide systems for making

customers’ deposits accessible to them, while ensuring that banks make substantial funds for their operational

activities through the discount window. This opinion is supported by the argument of Jablecki (n.d.) and Gray

(2011). The guiding principle is that banks would not develop an oversight to deplete customers’ deposits in

their financial activities. Measures are embedded in the framework of policies that constitute the reserve

capital requirement to encourage and promote balanced interbank borrowing (Peydr´o, 2010), which

strengthens banks’ liquidity. Though interbank borrowing comes with some level of adversity and financial

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 9

www.researchjournali.com

consequences (Ma, Xiandong & Xi, 2011), it serves as a better option to depending on customers’ deposit, a

situation that has a high tendency for bank runs (Bianchi & Bigio, 2013; Bouwman, 2013; Calomiris, Heider

& Hoerova, 2012; Robitaille, 2011).

However, reserve requirements limit banks’ potential to contribute to socio-economic development through

tax payment, employment and engagement in corporate social responsibility (CSR). The argument is that

banks could be able to effectively use reserves as financial tools, leading to business growth. Business growth

facilitates employment, enlarged level of tax payment and engagement in corporate social responsibility.

According to (Bianchi & Bigio, 2013), the introduction of the reserve requirement based on the mere

assumption that a bank could overuse customers’ savings or/and lend excessively could discourage

engagement in CSR. This is because reserve capitals do not originally exist with interest against banks

(Bouwman, 2013; Calomiris, Heider & Hoerova, 2012), but most financial tools used to buttress banks’

liquidity such as interbank lending and borrowing, as well as discount window come with higher risks and

financial demerits (Bianchi & Bigio, 2013; Bouwman, 2013; Calomiris, Heider & Hoerova, 2012). This

argument touches on the drawbacks associated with reserve capital.

Reserve requirements are perceived and considered by banks as a source of limitation to their operational and

financial activities and growth. A review of researches by Bianchi & Bigio (2013) and Robitaille (2011)

indicates that opposing views are held about this; thus whether reserve requirements come to hinder banks’

growth and output. In this study, it is made evident that reserve requirements may limit banks’ operational

and financial activities at a time, but their role as measures to safeguard the banking sector and the economy

is relatively weightier in importance than the growth and financial interests of individual banks. The paradox

is that reserve requirements are instituted to promote the success of banks and their bankruptcy (Bianchi &

Bigio, 2013; Bouwman, 2013; Calomiris, Heider & Hoerova, 2012; Robitaille, 2011).

7. DISCUSSION

This investigation is aimed at examining the effect of reserve requirements on the financial performance of

banks and their contribution to economic development through CSR engagement. This investigation is driven

by the fact that no obvious and indisputable position has been taken by researchers on the subject. Broadly,

there are two bodies of researches that explain the effect of the reserve requirement on banks financial

performance and their engagement in CSR. While one body of researches uphold the impact of reserve

requirement on financial performance of banks and their contribution to economic development through CSR

engagement, the other body of researches refute this. This study therefore builds to evidences available on the

subject.

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 10

www.researchjournali.com

Three hypotheses are tested in this study. The first hypothesis states that commercial banks’ cash reserve ratio

(CRR) does not have any significant relationship to bank growth in terms of return on investment (ROI). The

second hypothesis states that commercial banks’ cash reserve ratio (CRR) does not have any significant

relationship to level of corporate social responsibility (CSR) engagement. These hypotheses are tested at 5%

significance level. The first hypothesis test is significant, r (20) = .951, p = .000, likewise the second

hypothesis, r (20) = -.916, p = .000. In the case of the first research hypothesis, banks’ cash reserve ratio

positively relates to return on investment. This means that the reserve requirement of the Central Bank

promotes the financial growth or performance of banks. The realisation of this result is supportive to the body

of researches that project that reserve capital requirement impacts the financial performance of commercial

banks (Gray 2011; Jablecki, n.d., King, 2010). Regarding the second research hypothesis, the reserve

requirement negatively relates to the level of engagement in CSR. Thus, the reserve requirement minimizes

the level of banks’ engagement in CSR. This outcome supports the empirical findings of Ma et al. (2011);

Nacuer & Kandil, (n.d.).

The third research hypothesis states that cash reserve ratio do not significantly predict the financial

performance in terms of return on investment. In line with this hypothesis, it is found that CRR account for

about 90.5% of variance on ROI. This statistic indicates that financial performance of banks is strongly

predicted by banks’ cash reserve ratio. This confirms the strong positive relationship between cash reserve

ratio and return on investment. Moreover, the t-test associated with the test of the third hypothesis is

significant at 5% significance level, t (20) = 13.103, p = .000. This implies that CRR is a significant predictor

of banks’ financial performance in terms of return on investment. There is therefore ample evidence that cash

reserve ratio (CRR) doe not only positively relate to banks’ financial performance in terms of ROI but also

significantly predicts it. This buttresses the predictive value of CRR on business performance found in

previous studies (Gray, 2011; Nacuer & Kandil, n.d.).

8. CONCLUSIONS AND RECOMMENDATIONS

Based on findings of this study, cash reserve ratio (CRR) highly positively relates to return on investment

(ROI) among commercial banks in Ghana. Also, CRR negatively relates to level of engagement in corporate

social responsibility (CSR). Return on investment also negatively relates to level of engagement in corporate

social responsibility. As a result, it can be concluded that the reserve requirement of Ghana promotes or

impacts the financial performance of commercial banks in terms of return on investment. However, it limits

the level of engagement in corporate social responsibility by commercial banks in the country.

It is recommended that banks enhance their level of engagement in corporate social responsibility activities

that improve customer-bank relationship. This is a result of the fact that participating in this category of

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 11

www.researchjournali.com

corporate social responsibility activities is likely to improve financial performance among banks in the face of

Bank of Ghana’s reserve requirement. It is also suggested that future studies examine the extent to which

findings of related studies would differ in terms of such factors as bank size and sector of operation. The

influence of these factors should also be controlled for.

9. REFERENCES

Adrian, T., and H. S. Shin. (2010). Financial Intermediaries and Monetary Economics. Forthcoming in Handbook of Monetary

Economics, Vol. 3B, ed. B. M. Friedman and M. Woodford. New York, NY: Elsevier.

Amadeo, K. (2013). Reserve requirement; Definition and Principle, Retrieved from

http://useconomy.about.com/od/glossary/g/Reserve_Require.htm on 30/03/2014 at 17:07 PM.

Barreiro, P. L., Albandoz, J. P. (2001). Population and sample: Sampling Techniques, Management Mathematics for European

Schools, pp. 3-18.

Bartlett, J. E., Kotrlik, J. W., and Higgins, C. C. (2001). Organisational Research: Determining Appropriate Sample Size in Survey

Research, Information Technology, Learning, and Performance Journal, 19 (1): 1-8.

Bianchi, J., Bigio, S. (2013). Banks, Liquidity Management and Monetary Policy, pp. 2-12.

Bindseil, U., Manzanares, A., Weller, B. (2004). The Role of Central Bank Capital Revisited, European Central Bank, Working Paper

Series, No. 392, September 2004, pp. pp. 7-30.

Bech, M., Keiser, T. (2012). On the liquidity coverage ratio and monetary policy implementation, BIS Quarterly Review, pp. 49-61.

Bouwman, C.H.S. (2013). Liquidity: How Banks Create It and how it should be Regulated, Oxford handbook of Banking, 2nd

Edition; A.N. Berger, P. Molyneux, and J.O.S. Wilson (eds.).

Calomiris, C.,Heider, F., Hoerova, M. (2012). The Theory of Bank Liquidity Requirements, pp. 2-20.

Derina, R. (2011). The Impact of Changes of Capital Regulations on Bank Capital and Portfolio Risk Decision: A case study of

Indonesian Banks, Doctoral Dissertation, University of Adeladei, Business School.

Francis, W. Osborne, M., (2009). Bank regulation, capital and credit supply: Measuring the impact of Prudential Standards,

Occasional Paper Series, No. 36, pp. 23-45.

Glocker, C., Towbin, P. (2012). Reserve Requirements for Price and Financial Stability: When Are They Effective? International

Journal of Central Banking, 8 (1): 65-113.

Golafshani, N. (2003). Understanding reliability and validity in qualitative research, International Journal of Education and Research,

3 (12): 521-532.

Gorton, G., Winton, A. (2002). Financial Intermediation, NBER Working Paper Series, National Bureau of Economic Research, No.

8928, pp. 34-78.

Gray, S. (2011). Central Bank Balances and Reserve Requirements, IMF Working Paper, No. 11, pp. 5-20.

Hoggson, N. F. (1926). Banking Through the Ages, New York, Dodd, Mead & Company

Investopedia (March, 2014). Definition of Reserve Ration, Retrieved from http://www.investopedia.com/terms/r/reserveratio.asp, on

30/03/2014 at 7:09 PM.

Jablecki, J. (n.d.). The impact of Basel I capital requirements on bank behaviour and the efficacy of monetary policy, International

Journal of Economic Sciences and Applied Research, 2 (1): 16-35.

Kichenham, B. and Pfleeger L. F. (2002). Principles of survey research, populations and samples, Software Engineering Notes, 27 (5):

17

King, M. (2010). Mapping capital and liquidity requirements to bank lending spreads, BIS Working Papers, No. 324, pp. 21-34.

Researchjournali’s Journal of Finance

Vol. 4 | No. 3 April | 2016 ISSN 2348-0963 12

www.researchjournali.com

Krejcie, R. V., Morgan, D. W. (1970). Determining sample size for research activities, Educational and Psychological Measurement,

6 (6): 232-256.

Ma, G., Xiandong, Y., Xi, L. (2011). China’s evolving reserve requirements, BIS Working Paper, No. 360. Pp. 1-33.

Maxwell, J. A. (2008). Applied Research Deigns, Designing a Qualitative Study, pp. 215-232.

Morse, J. M., (2002). Verification strategies for establishing reliability and validity in research, Journal of Educational Research, 6

(9): 56-63.

Nacuer, S.B., Kandil, M. (n.d.). The Impact of Capital Requirements on Banks’ Cost of Intermediation and Performance: The Case of

Egypt, pp. 1-34.

Ocra, B. T. (2010). Statistical Methods for Quantitative Researchers, Combert Impression, Acrra Ghana, pp. 34-56.

Peydr´o, J. (2010). Discussion of “The Effects of Bank Capital on Lending: What do we know, and what does it mean? International

Journal of Central Banking, 6 (4): 55-69.

Robitaille, P. (2011). Liquidity and Reserve Requirements in Brazil, International Finance Discussion Papers, pp. 3-70.

Santos, A.C. (2000). Bank Capital Regulation in Contemporary Banking Theory: A review of the literature, BIS Working Papers, No.

90. Pp. 3-44.