Embed Size (px)

Citation preview

THE DAILY

Date: 06 August 2020

The Daily Viewpoint

Page 2

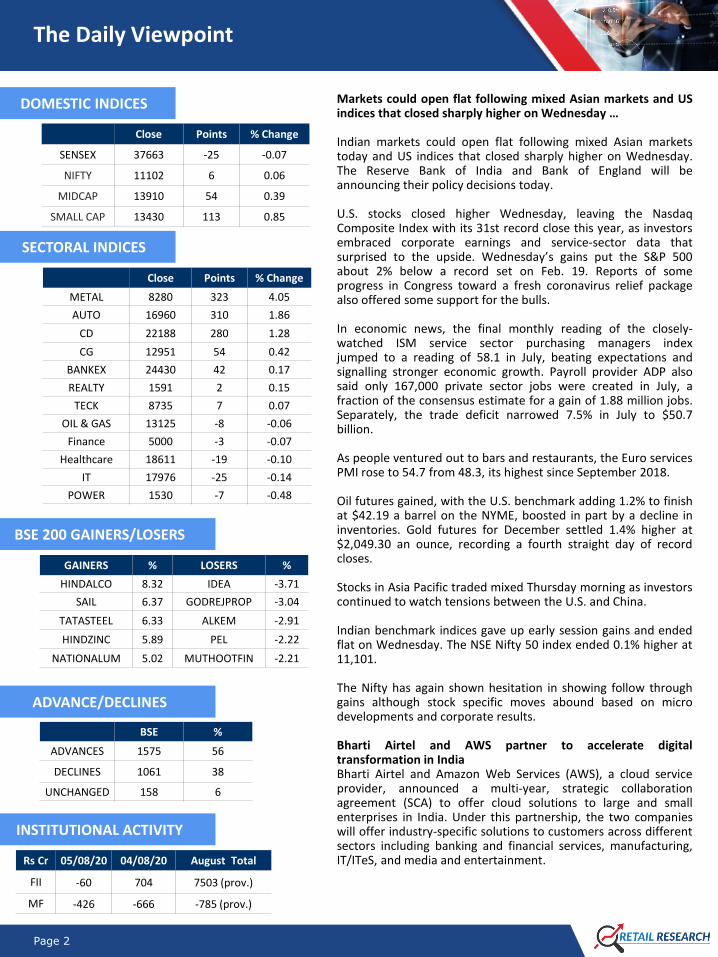

DOMESTIC INDICES

Close Points % Change

SENSEX 37663 -25 -0.07

NIFTY 11102 6 0.06

MIDCAP 13910 54 0.39

SMALL CAP 13430 113 0.85

SECTORAL INDICES

Close Points % Change

METAL 8280 323 4.05

AUTO 16960 310 1.86

CD 22188 280 1.28

CG 12951 54 0.42

BANKEX 24430 42 0.17

REALTY 1591 2 0.15

TECK 8735 7 0.07

OIL & GAS 13125 -8 -0.06

Finance 5000 -3 -0.07

Healthcare 18611 -19 -0.10

IT 17976 -25 -0.14

POWER 1530 -7 -0.48

BSE 200 GAINERS/LOSERS

GAINERS % LOSERS %

HINDALCO 8.32 IDEA -3.71

SAIL 6.37 GODREJPROP -3.04

TATASTEEL 6.33 ALKEM -2.91

HINDZINC 5.89 PEL -2.22

NATIONALUM 5.02 MUTHOOTFIN -2.21

ADVANCE/DECLINES

BSE %

ADVANCES 1575 56

DECLINES 1061 38

UNCHANGED 158 6

INSTITUTIONAL ACTIVITY

Rs Cr 05/08/20 04/08/20 August Total

FII -60 704 7503 (prov.)

MF -426 -666 -785 (prov.)

Markets could open flat following mixed Asian markets and USindices that closed sharply higher on Wednesday …

Indian markets could open flat following mixed Asian marketstoday and US indices that closed sharply higher on Wednesday.The Reserve Bank of India and Bank of England will beannouncing their policy decisions today.

U.S. stocks closed higher Wednesday, leaving the NasdaqComposite Index with its 31st record close this year, as investorsembraced corporate earnings and service-sector data thatsurprised to the upside. Wednesday’s gains put the S&P 500about 2% below a record set on Feb. 19. Reports of someprogress in Congress toward a fresh coronavirus relief packagealso offered some support for the bulls.

In economic news, the final monthly reading of the closely-watched ISM service sector purchasing managers indexjumped to a reading of 58.1 in July, beating expectations andsignalling stronger economic growth. Payroll provider ADP alsosaid only 167,000 private sector jobs were created in July, afraction of the consensus estimate for a gain of 1.88 million jobs.Separately, the trade deficit narrowed 7.5% in July to $50.7billion.

As people ventured out to bars and restaurants, the Euro servicesPMI rose to 54.7 from 48.3, its highest since September 2018.

Oil futures gained, with the U.S. benchmark adding 1.2% to finishat $42.19 a barrel on the NYME, boosted in part by a decline ininventories. Gold futures for December settled 1.4% higher at$2,049.30 an ounce, recording a fourth straight day of recordcloses.

Stocks in Asia Pacific traded mixed Thursday morning as investorscontinued to watch tensions between the U.S. and China.

Indian benchmark indices gave up early session gains and endedflat on Wednesday. The NSE Nifty 50 index ended 0.1% higher at11,101.

The Nifty has again shown hesitation in showing follow throughgains although stock specific moves abound based on microdevelopments and corporate results.

Bharti Airtel and AWS partner to accelerate digitaltransformation in IndiaBharti Airtel and Amazon Web Services (AWS), a cloud serviceprovider, announced a multi-year, strategic collaborationagreement (SCA) to offer cloud solutions to large and smallenterprises in India. Under this partnership, the two companieswill offer industry-specific solutions to customers across differentsectors including banking and financial services, manufacturing,IT/ITeS, and media and entertainment.

The Daily Viewpoint

Page 3

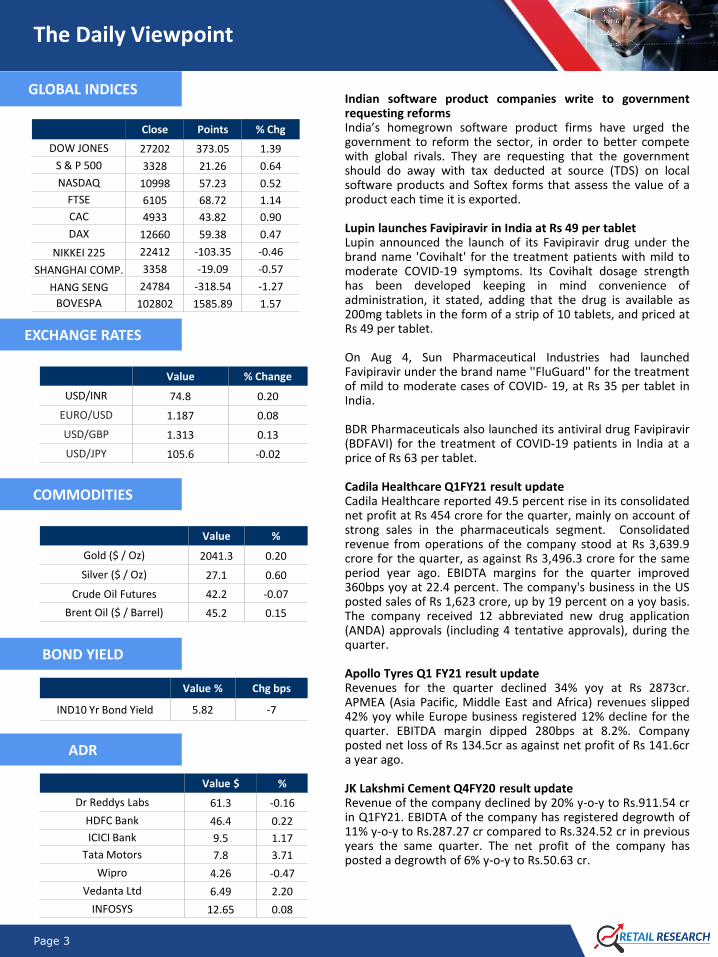

GLOBAL INDICESIndian software product companies write to governmentrequesting reformsIndia’s homegrown software product firms have urged thegovernment to reform the sector, in order to better competewith global rivals. They are requesting that the governmentshould do away with tax deducted at source (TDS) on localsoftware products and Softex forms that assess the value of aproduct each time it is exported.

Lupin launches Favipiravir in India at Rs 49 per tabletLupin announced the launch of its Favipiravir drug under thebrand name 'Covihalt' for the treatment patients with mild tomoderate COVID-19 symptoms. Its Covihalt dosage strengthhas been developed keeping in mind convenience ofadministration, it stated, adding that the drug is available as200mg tablets in the form of a strip of 10 tablets, and priced atRs 49 per tablet.

On Aug 4, Sun Pharmaceutical Industries had launchedFavipiravir under the brand name ''FluGuard'' for the treatmentof mild to moderate cases of COVID- 19, at Rs 35 per tablet inIndia.

BDR Pharmaceuticals also launched its antiviral drug Favipiravir(BDFAVI) for the treatment of COVID-19 patients in India at aprice of Rs 63 per tablet.

Cadila Healthcare Q1FY21 result updateCadila Healthcare reported 49.5 percent rise in its consolidatednet profit at Rs 454 crore for the quarter, mainly on account ofstrong sales in the pharmaceuticals segment. Consolidatedrevenue from operations of the company stood at Rs 3,639.9crore for the quarter, as against Rs 3,496.3 crore for the sameperiod year ago. EBIDTA margins for the quarter improved360bps yoy at 22.4 percent. The company's business in the USposted sales of Rs 1,623 crore, up by 19 percent on a yoy basis.The company received 12 abbreviated new drug application(ANDA) approvals (including 4 tentative approvals), during thequarter.

Apollo Tyres Q1 FY21 result updateRevenues for the quarter declined 34% yoy at Rs 2873cr.APMEA (Asia Pacific, Middle East and Africa) revenues slipped42% yoy while Europe business registered 12% decline for thequarter. EBITDA margin dipped 280bps at 8.2%. Companyposted net loss of Rs 134.5cr as against net profit of Rs 141.6cra year ago.

JK Lakshmi Cement Q4FY20 result updateRevenue of the company declined by 20% y-o-y to Rs.911.54 crin Q1FY21. EBIDTA of the company has registered degrowth of11% y-o-y to Rs.287.27 cr compared to Rs.324.52 cr in previousyears the same quarter. The net profit of the company hasposted a degrowth of 6% y-o-y to Rs.50.63 cr.

EXCHANGE RATES

Value % Change

USD/INR 74.8 0.20

EURO/USD 1.187 0.08

USD/GBP 1.313 0.13

USD/JPY 105.6 -0.02

COMMODITIES

Value %

Gold ($ / Oz) 2041.3 0.20

Silver ($ / Oz) 27.1 0.60

Crude Oil Futures 42.2 -0.07

Brent Oil ($ / Barrel) 45.2 0.15

BOND YIELD

Value % Chg bps

IND10 Yr Bond Yield 5.82 -7

ADR

Value $ %

Dr Reddys Labs 61.3 -0.16

HDFC Bank 46.4 0.22

ICICI Bank 9.5 1.17

Tata Motors 7.8 3.71

Wipro 4.26 -0.47

Vedanta Ltd 6.49 2.20

INFOSYS 12.65 0.08

Close Points % Chg

DOW JONES 27202 373.05 1.39

S & P 500 3328 21.26 0.64

NASDAQ 10998 57.23 0.52

FTSE 6105 68.72 1.14

CAC 4933 43.82 0.90

DAX 12660 59.38 0.47

NIKKEI 225 22412 -103.35 -0.46

SHANGHAI COMP. 3358 -19.09 -0.57

HANG SENG 24784 -318.54 -1.27

BOVESPA 102802 1585.89 1.57

The Daily Viewpoint

Page 4

VIP Industries Q1FY21 result updateConsolidated net revenue in of the company in Q1FY21 fell by 93% to Rs 40.3 crore. EBITDA stood at negative Rs 57.8crore in Q1FY21 against a profit of Rs 125.1 crore in Q1FY20. The consolidated net loss in Q1FY21 came in at Rs 51.3crore that declined by 246% yoy, as compared to Q1FY20, when it had reported consolidated net profit of Rs 35.1 crore.Board approved issue of NCDs worth Rs 50 crore on a private placement basis.

Inox Leisure Q1FY21 Results UpdateInox Leisure Ltd reported a consolidated net loss of Rs 73.64 crore for the June quarter as the film exhibition businesscame to a halt due to the COVID-19 pandemic. The company had posted a net profit of Rs 27.01 crore in the April-Juneperiod a year ago. Revenue from operations slumped 99.94 per cent to Rs 0.25 crore during the quarter under review,from Rs 493.01 crore in the corresponding period of the preceding fiscal.

The Board Of Directors have approved the Company's enabling resolution for fund raising up to Rs 250 Cr through theissuance of Equity Shares/other securities, subject to approval of Shareholders in the ensuing Annual General Meeting.

Cera Sanitaryware Q1FY21 Results UpdateRevenue was down by 46.2% from Rs 271.2cr to Rs 146cr, as the company's business was impacted due to the shutdowns, where its overall operations remained completely shut for over a month leading to loss of production and sales.It resumed its operations in a gradual manner. However, the company was able to maintain its zero debt status. EBITDAdropped by 89.3% from Rs 35.3cr to Rs 3.8cr. The company earned a loss of Rs 1.7cr as against a profit of Rs 17.2cr, i.e. a109.8% drop. EPS earned by the company was Rs 0.4 per share, compared to Rs 13.9 per share.

DLF Q1FY21 Results updateRevenue declined by 58.8% from Rs 1331.2cr to Rs 548.6cr, EBITDA also declined by 99.3% from Rs 239.7cr to Rs 1.7cr.Profitability of the company dropped by 117.3%, where it incurred a loss of Rs 71.5cr as against a profit of Rs 413.9cr.DLF earned a loss of Rs 0.3/- per share, compared to Rs 1.8/- per share. Issuance of the possession letters got adverselyaffected during the lockdown, and performance in the rental business was impacted owing to the retail malls remainingshut during the lockdown period and consequent rental waivers.

Asahi India Glass Q1FY21 result updateThe company reported consolidated net loss of Rs 63.7 crore compared to net profit of Rs 39.3 crore in Q1FY20. Netrevenue of the company declined substantially by 68.4% to Rs 221 crore. Other Income dipped by 34.9%. EBITDA stoodat a loss of Rs 30 crore as compared to a profit of Rs 125.9 crore a yer ago.

Adani Gas Ltd Q1FY21 results key takeawayAdani Gas Ltd Q1FY21 numbers were below estimates, consolidated net profit was down by 50.9 per cent YoY to Rs 38.9crore. Revenue from operation declined 58.8 per cent YoY to Rs 197.2 crore, impacted by demand disruption due toCOVID-19 pandemic.

Despite continued COVID-19 impact, its combined volume of CNG and PNG stood at 64 MMSCM vs 137 MMCM in Q1FY20. Volume in June’20 was at 0.71 MMSCMD compared to volume in April’20 at 0.35 MMSCMD showing significantvolume recovery trend. PNG Home Connection increased by 979 New Connections in Q1 FY21 to 4.38 Lac andCommercial & Industrial connection now increased to 4,448.

Dalmia Bharat Q1FY21 Result previewDalmia Bharat expected to post a 25% y-o-y decline in sales volume to 3.4 mnMT. Company's revenue expected to fallby 24.2% to Rs.1852 cr, y-o-y. EBIDTA is expected to post degrowth of 33.5% y-o-y to Rs.442.5 cr. PAT is expected topost degrowth of 97.1% y-o-y to Rs.4.3 cr. Also, EBIDTA (Rs./MT) expected to post degrowth of 11.3% y-o-y toRs.1297/MT.

Lupin Q1 FY21 result previewRevenue may decline 19% yoy at Rs 3578cr. EBITDA is expected to see sharp 40% dip at Rs 505cr. Company may record41% yoy decline in PAT at Rs 179cr. Domestic business may register 5% yoy decline while US revenues may remainsubdued in the quarter.

The Daily Viewpoint

Page 5

Hindustan Petroleum Corporation Ltd (Q1FY21), Results PreviewHindustan Petroleum is likely to report 52.0 per cent YoY and 48.5 per cent QoQ sales decline to Rs 34,100 crore and netprofit may fall to Rs 2,600 crore. Marketing volumes are likely to fall 25 per cent YoY at 7.6mmt. Blended marketingmargin could jump 16.0 per cent QoQ. Core GRM could be at US$ 1.2/bbl, excluding the impact of US$ 2.4/bbl ofinventory gain. Refinery crude throughput is likely to be at 4 mmt v/s 4.5 mmt in 4QFY20. Commentary on Visakhrefinery expansion project status will be key monitorable.

GSPL(Q1FY21), Results PreviewGSPL is likely to report 8.9 per cent YoY sales growth to Rs 600 crore and net profit may increase by 1 per cent YoY to Rs200 crore. Volume is expected to be 34mmscmd (-11/-7.6% YoY/QoQ). Commentary on ramp up in utilisation of Mundraand Dahej LNG terminals will be key monitorable.

Important news/developments to influence markets

India's dominant services industry, shrank for a fifth straight month in July. The Nikkei/IHS Services PurchasingManagers' Index increased to 34.2 in July from 33.7 in June.

Japan's services sector contracted for a sixth straight month in July. The final Jibun Bank Japan Services PurchasingManagers' Index (PMI) edged up to a seasonally adjusted 45.4 in July, hardly an encouraging change from 45.0 inJune.

The IHS Markit/CIPS UK Services PMI stood at 56.5 in July 2020, little-changed from a preliminary estimate of 56.6and well above June's final reading of 47.1.

The volume of retail sales in the Eurozone increased month-on-month by 5.7 per cent in June, according toseasonally adjusted figures from Eurostat — after a record 20.3 per cent jump the previous month. The May figurewas revised upwards from a previously reported 17.8 per cent. Compared with the same period of the previous year,eurozone retail sales were up 1.3 per cent in June.

Mortgage applications in the United States fell by 5.1 percent in the week ended July 31st, the second consecutiveperiod of decrease.

The US economy added 4.8 million jobs in June, the most on record and beating expectations of 3 million. It followsan upwardly revised 2.7 million rise in May reflecting a partial resumption of economic activity.

The US trade deficit narrowed to USD 50.7 billion in June 2020 from a revised one-and-a-half-year high of USD 54.8billion in the previous month Both exports and imports rebounded firmly as global demand recovers from thecoronavirus shock. Exports increased 9.4 percent, imports advanced 4.7 percent.

The IHS Markit US Services PMI was revised higher to 50.0 in July 2020 from a preliminary estimate of 49.6 andcompared to June's final reading of 47.9.

The ISM Non-Manufacturing PMI for the US jumped to 58.1 in July 2020 from 57.1 in the previous month

The ISM Non-Manufacturing employment index dropped -1.0 to 42.1, staying in contraction region.

U.S. crude oil inventories decreased during the week ending July 31, the U.S. Energy Information Administration (EIA)said in a report. According to the Weekly Petroleum Status Report, U.S. commercial crude oil inventories, excludingthose in the Strategic Petroleum Reserve, decreased by 7.4 million barrels from the previous week.

The Daily Viewpoint

Retail ResearchPage 6

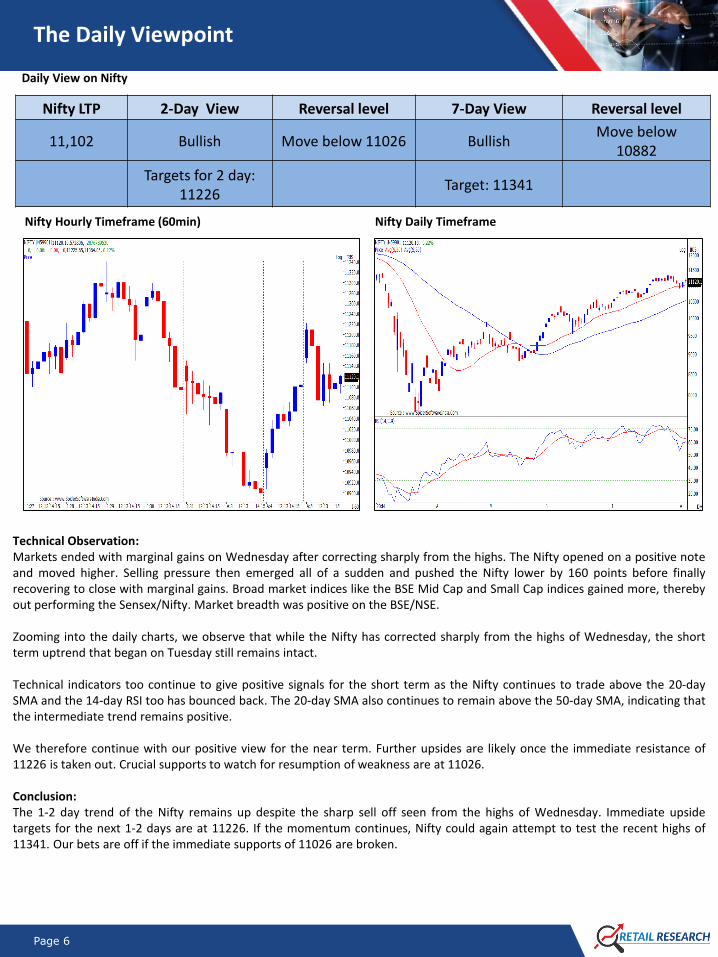

Daily View on Nifty

Nifty Hourly Timeframe (60min) Nifty Daily Timeframe

Technical Observation:Markets ended with marginal gains on Wednesday after correcting sharply from the highs. The Nifty opened on a positive noteand moved higher. Selling pressure then emerged all of a sudden and pushed the Nifty lower by 160 points before finallyrecovering to close with marginal gains. Broad market indices like the BSE Mid Cap and Small Cap indices gained more, therebyout performing the Sensex/Nifty. Market breadth was positive on the BSE/NSE.

Zooming into the daily charts, we observe that while the Nifty has corrected sharply from the highs of Wednesday, the shortterm uptrend that began on Tuesday still remains intact.

Technical indicators too continue to give positive signals for the short term as the Nifty continues to trade above the 20-daySMA and the 14-day RSI too has bounced back. The 20-day SMA also continues to remain above the 50-day SMA, indicating thatthe intermediate trend remains positive.

We therefore continue with our positive view for the near term. Further upsides are likely once the immediate resistance of11226 is taken out. Crucial supports to watch for resumption of weakness are at 11026.

Conclusion:The 1-2 day trend of the Nifty remains up despite the sharp sell off seen from the highs of Wednesday. Immediate upsidetargets for the next 1-2 days are at 11226. If the momentum continues, Nifty could again attempt to test the recent highs of11341. Our bets are off if the immediate supports of 11026 are broken.

Nifty LTP 2-Day View Reversal level 7-Day View Reversal level

11,102 Bullish Move below 11026 Bullish Move below

10882

Targets for 2 day: 11226

Target: 11341

The Daily Viewpoint

Page 7

DATA & EVENTS

OPEN SHORT-TERM TRADING CALLS

NOTE: ALL TRADING RECOMMENDATIONS GIVEN BY TEAM ARE ON REAL TIME BASIS. A TRADING RECOMMENDATIONSHOULD BE CONSIDERED CLOSED OR SQUARED OFF AS AND WHEN A STOPLOSS OR TARGET IS TOUCHED IN INTRADAYTRADING. DO NOT WAIT FOR TARGET ACHIEVED OR STOPLOSS MESSAGE TO CLOSE THE POSITIONS. REFER JAMMOONFOR TIMELY ENTRY AND EXIT FROM RECOMMENDATIONS.

NO. RECO DT. RECO COMPANY NAME ENTRY CMP SL TARGETUPSIDE

%VALID TILL

1 29-JUL-20 BUYDLF 142.50 AUG CALL

OPTION9.45 8.15 5 18 121 7-AUG-20

2 5-AUG-20 BUY MGL AUG FUT 966-977 990.5 959 1010 2 12-AUG-20

3 29-JUL-20 BUY COAL INDIA 131.55-126.50 128.7 125.25 139 8 7-AUG-20

4 30-JUL-20 BUY TCS 2317.10-2247 2259 2213 2456 9 10-AUG-20

5 30-JUL-20 BUY BRITANNIA INDS 3800-3863 3855 3760 4070 6 10-AUG-20

6 3-AUG-20 BUY BIOCON 410-416 409.9 403.6 428.4 5 12-AUG-20

7 4-AUG-20 BUY L&T 927.30-910 924 901 955.5 3 11-AUG-20

8 5-AUG-20 BUY ULTRATECH CEMENT 4092-3974 4035.05 3914 4342 8 19-AUG-20

9 5-AUG-20 BUY NIACL 114.45-110.25 115.5 109.25 122 6 14-AUG-20

10 5-AUG-20 BUY RAIN INDUSTRIES 92.50-94.15 95.8 91.4 105 10 14-AUG-20

OPEN CASH POSITIONAL CALLS

NO. RECO DT. RECO COMPANY NAME ENTRY CMP SL TARGET

1 TARGET

2TARGET

3UPSIDE

% VALID TILL

1 1-JUN-20 BUY AVANTI FEEDS** 442.0 478.0 403.0 481.0 520.0 575.0 20 1-DEC-20

2 6-JUL-20 BUYKNR

CONSTRUCTION216.2 204.3 196.0 238.0 260.0 - 27 4-OCT-20

3 20-JUL-20 BUY IDFC FIRST* 26.6 27.0 25.0 28.5 30.0 - 11 18-OCT-20

4 30-JUL-20 BUYGLENMARK

PHARMA445.9 448.9 415.0 483.0 530.0 18 28-OCT-20

5 4-AUG-20 BUY ABBOTT INDIA 16009.0 16215.0 14800.0 17290.0 18890.0 16 2-NOV-20

6 4-AUG-20 BUY METROPOLIS 1661.5 1640.0 1534.0 1860.0 2050.0 25 2-NOV-20

7 5-AUG-20 BUY HATSUN AGRO 707.4 724.1 640.0 779.0 849.0 17 3-NOV-20

The Daily Viewpoint

Page 8

DATA & EVENTS

*= 1st Target Achieved**= 2nd Target Achieved

OPEN DERIVATIVE POSITIONAL CALLS

NO. RECO DT. RECO COMPANY NAME ENTRY CMP SL TARGET 1TARGET

2TARGET

3UPSIDE

%VALID TILL

1 5-AUG-20 BUYMAX FINANCIAL

AUG FUT550.4 548.4 515 595.0 620.0 13

TILL 27TH AUG

2 5-AUG-20 BUYICICI BANK AUG

FUT360 355.2 345 375 390 10

TILL 27TH AUG

3 5-AUG-20 BUYADANIPORTS AUG

FUT324 329.0 303 355 - 8

TILL 27TH AUG

NO. RECO DT. RECOCOMPANY

NAMEENTRY CMP SL

TARGET 1

TARGET 2TARGET

3UPSIDE

%VALID TILL

1 28-JUL-20

BUYFEDERAL BANK

AUG FUT56.05 52.5 52.15 61 - - 16

TILL 27TH AUG

SELL PNB AUG FUT 32.35 32.55 34.6 29.5 - - 9

2 03-AUG-20

BUYTVS MOTOR AUG

FUT398 409.65 375 430 - - 5

TILL 27TH AUG

SELLEICHER MOTOR

AUG FUT21045 21825.2 22300 19400 - - 11

OPEN PAIR TRADING CALLS

OPEN E-MARGIN POSITIONAL CALLS

NO. RECO DT. RECO COMPANY NAME ENTRY CMP SL TARGET 1TARGET

2TARGET

3UPSIDE

%VALID TILL

1 12-JUN-20 BUYNAGARJUNA

CONSTRUCTION*30.0 31.3 27.0 33.5 36.0 - 15 12-SEP-20

2 20-JUL-20 BUY KAVERI SEEDS 603.6 593.5 550.0 665.0 - - 12 20-OCT-20

3 23-JUL-20 BUYMOTILAL OSWAL FINANCIAL SERV

696.0 670.1 632.0 770.0 810.0 - 21 23-OCT-20

4 4-AUG-20 BUY ICICI LOMBARD 1346.0 1348.2 1240.0 1480.0 1600.0 - 19 4-NOV-20

The Daily Viewpoint

Page 9

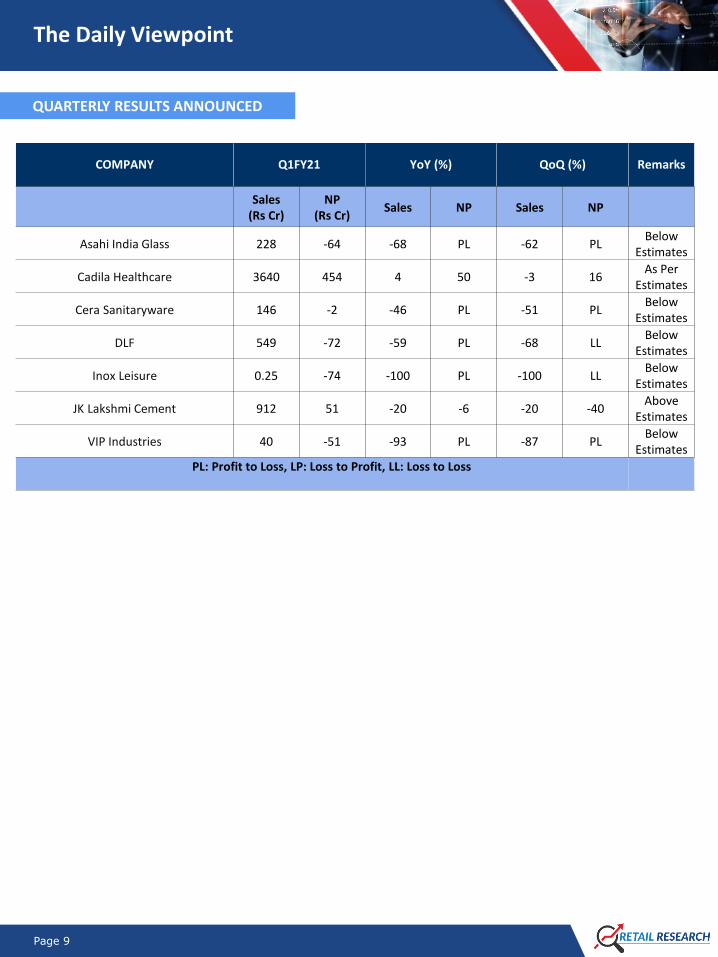

QUARTERLY RESULTS ANNOUNCED

COMPANY Q1FY21 YoY (%) QoQ (%) Remarks

Sales (Rs Cr)

NP (Rs Cr)

Sales NP Sales NP

Asahi India Glass 228 -64 -68 PL -62 PLBelow

Estimates

Cadila Healthcare 3640 454 4 50 -3 16As Per

Estimates

Cera Sanitaryware 146 -2 -46 PL -51 PLBelow

Estimates

DLF 549 -72 -59 PL -68 LLBelow

Estimates

Inox Leisure 0.25 -74 -100 PL -100 LLBelow

Estimates

JK Lakshmi Cement 912 51 -20 -6 -20 -40Above

Estimates

VIP Industries 40 -51 -93 PL -87 PLBelow

Estimates

PL: Profit to Loss, LP: Loss to Profit, LL: Loss to Loss

The Daily Viewpoint

Page 10

Disclaimer:This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. Theinformation and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith fromsources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty,express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to changewithout notice. This document is for information purposes only. Descriptions of any company or companies or their securitiesmentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation ofan offer, to buy or sell any securities or other financial instruments.This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any personor entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication,reproduction, availability or use would be contrary to law or regulation or what would subject HSL or its affiliates to any registration orlicensing requirement within such jurisdiction.If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored andbrought to the attention of the sender. This document may not be reproduced, distributed or published for any purposes withoutprior written approval of HSL.Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have anadverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values ofwhich are influenced by foreign currencies effectively assume currency risk.It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HSL may from time to time solicit from,or perform broking, or other services for, any company mentioned in this mail and/or its attachments.HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buyor sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities andearn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein oract as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to anyrecommendation and other related information and opinions.HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustaineddue to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices ofshares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc.HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities andfinancial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may dealin other securities of the companies / organizations described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have beenmandated by the subject company for any other assignment in the past twelve months.HSL or its associates might have received any compensation from the companies mentioned in the report during the period precedingtwelve months from t date of this report for services in respect of managing or co-managing public offerings, corporate finance,investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction in thenormal course of business.HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party inconnection with preparation of the research report. Accordingly, neither HSL nor Research Analysts have any material conflict ofinterest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchantbanking, investment banking or brokerage service transactions. HSL may have issued other reports that are inconsistent with andreach different conclusion from the information presented in this report.Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as anofficer, director or employee of the subject company. We have not received any compensation/benefits from the subject company orthird party in connection with the Research Report.

HDFC securities Limited, SEBI Registration No.: INZ000186937 (NSE, BSE, MSEI, MCX) |NSE Trading Member Code: 11094 | BSEClearing Number: 393 | MSEI Trading Member Code: 30000 | MCX Member Code: 56015 | IN-DP-372-2018 (CDSL, NSDL) | CDSL DP ID:12086700 | NSDL DP ID: IN304279 | AMFI Reg No. ARN -13549 | PFRDA Reg. No - POP 11092018 | IRDA Corporate Agent LicenceNo.CA0062 | Research Analyst Reg. No. INH000002475 | Investment Adviser: INA000011538 | CIN-U67120MH2000PLC152193

Registered Address: I Think Techno Campus, Building, B, Alpha, Office Floor 8, Near Kanjurmarg Station, Kanjurmarg (East), Mumbai -400 042. Tel -022 30753400. Compliance Officer: Ms. Binkle R Oza. Ph: 022-3045 3600, Email: [email protected].

Mutual Funds Investments are subject to market risk. Please read the offer and scheme related documents carefully before investing.

![[Kotak] India Daily, February 18, 2016 - Kotak Securities](https://img.dokumen.tips/doc/110x75/633a76e102bd8edb4701c87a/kotak-india-daily-february-18-2016-kotak-securities.jpg)