Embed Size (px)

Citation preview

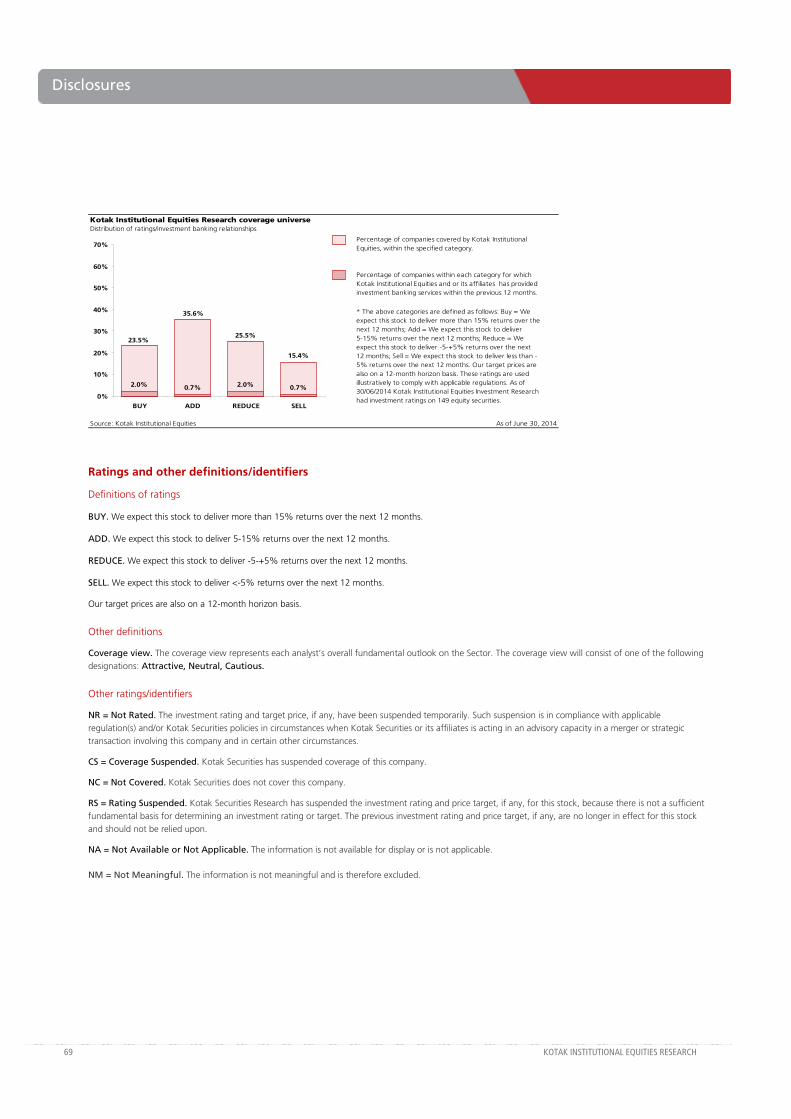

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

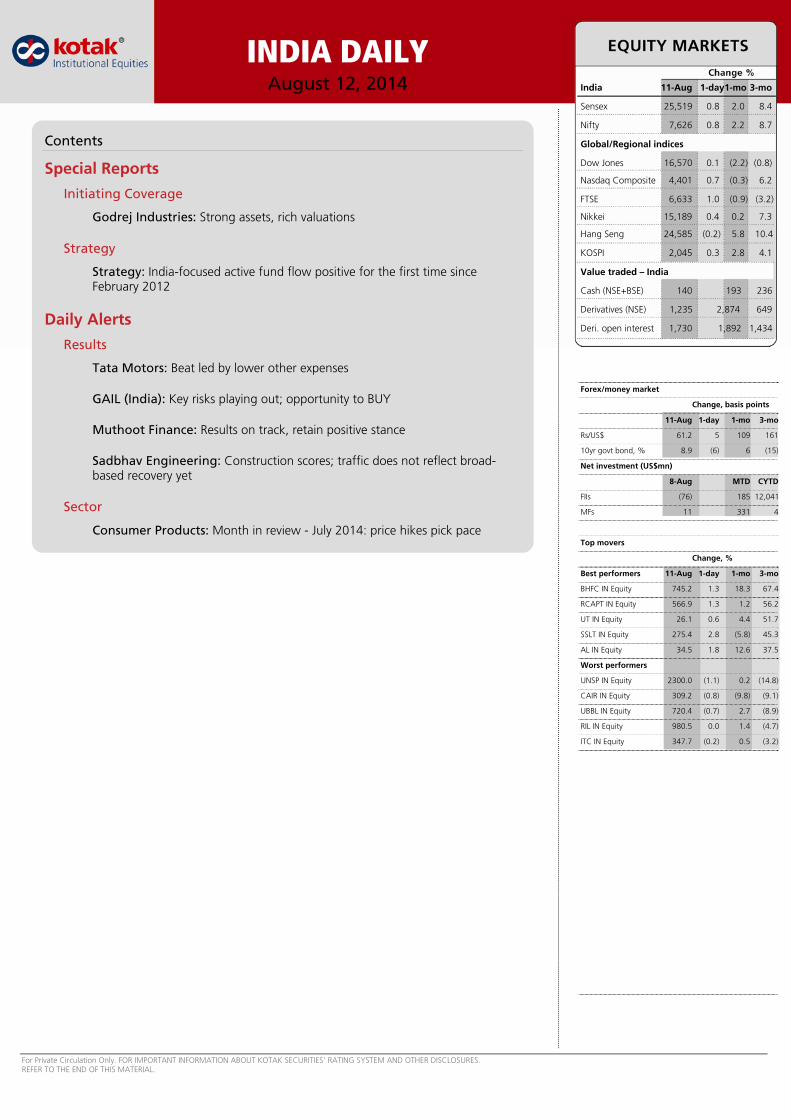

INDIA DAILYAugust 12, 2014 India 11-Aug 1-day1-mo 3-mo

Sensex 25,519 0.8 2.0 8.4

Nifty 7,626 0.8 2.2 8.7

Global/Regional indices

Dow Jones 16,570 0.1 (2.2) (0.8)

Nasdaq Composite 4,401 0.7 (0.3) 6.2

FTSE 6,633 1.0 (0.9) (3.2)

Nikkei 15,189 0.4 0.2 7.3

Hang Seng 24,585 (0.2) 5.8 10.4

KOSPI 2,045 0.3 2.8 4.1

Value traded – India

Cash (NSE+BSE) 140 193 236

Derivatives (NSE) 1,235 2,874 649

Deri. open interest 1,730 1,892 1,434

Forex/money market

Change, basis points

11-Aug 1-day 1-mo 3-mo

Rs/US$ 61.2 5 109 161

10yr govt bond, % 8.9 (6) 6 (15)

Net investment (US$mn)

8-Aug MTD CYTD

FIIs (76) 185 12,041

MFs 11 331 4

Top movers

Change, %

Best performers 11-Aug 1-day 1-mo 3-mo

BHFC IN Equity 745.2 1.3 18.3 67.4

RCAPT IN Equity 566.9 1.3 1.2 56.2

UT IN Equity 26.1 0.6 4.4 51.7

SSLT IN Equity 275.4 2.8 (5.8) 45.3

AL IN Equity 34.5 1.8 12.6 37.5

Worst performers

UNSP IN Equity 2300.0 (1.1) 0.2 (14.8)

CAIR IN Equity 309.2 (0.8) (9.8) (9.1)

UBBL IN Equity 720.4 (0.7) 2.7 (8.9)

RIL IN Equity 980.5 0.0 1.4 (4.7)

ITC IN Equity 347.7 (0.2) 0.5 (3.2)

Contents

Special Reports

Initiating Coverage

Godrej Industries: Strong assets, rich valuations

Strategy

Strategy: India-focused active fund flow positive for the first time since February 2012

Daily Alerts

Results

Tata Motors: Beat led by lower other expenses

GAIL (India): Key risks playing out; opportunity to BUY

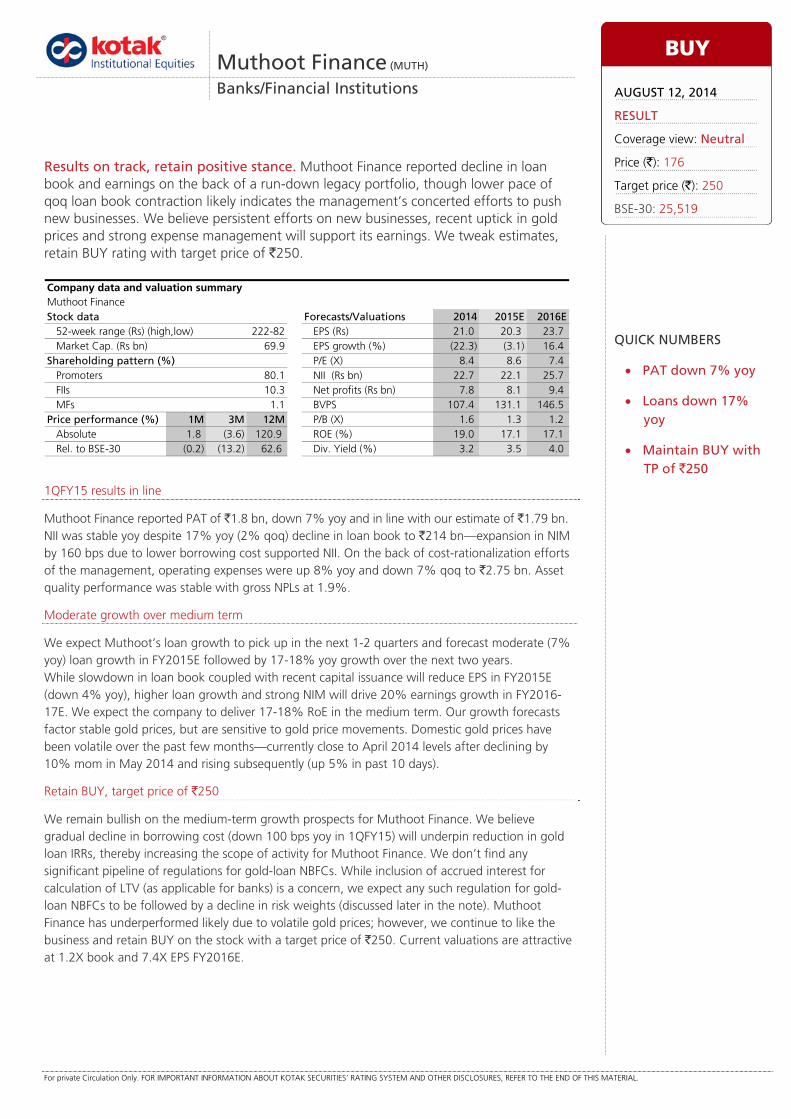

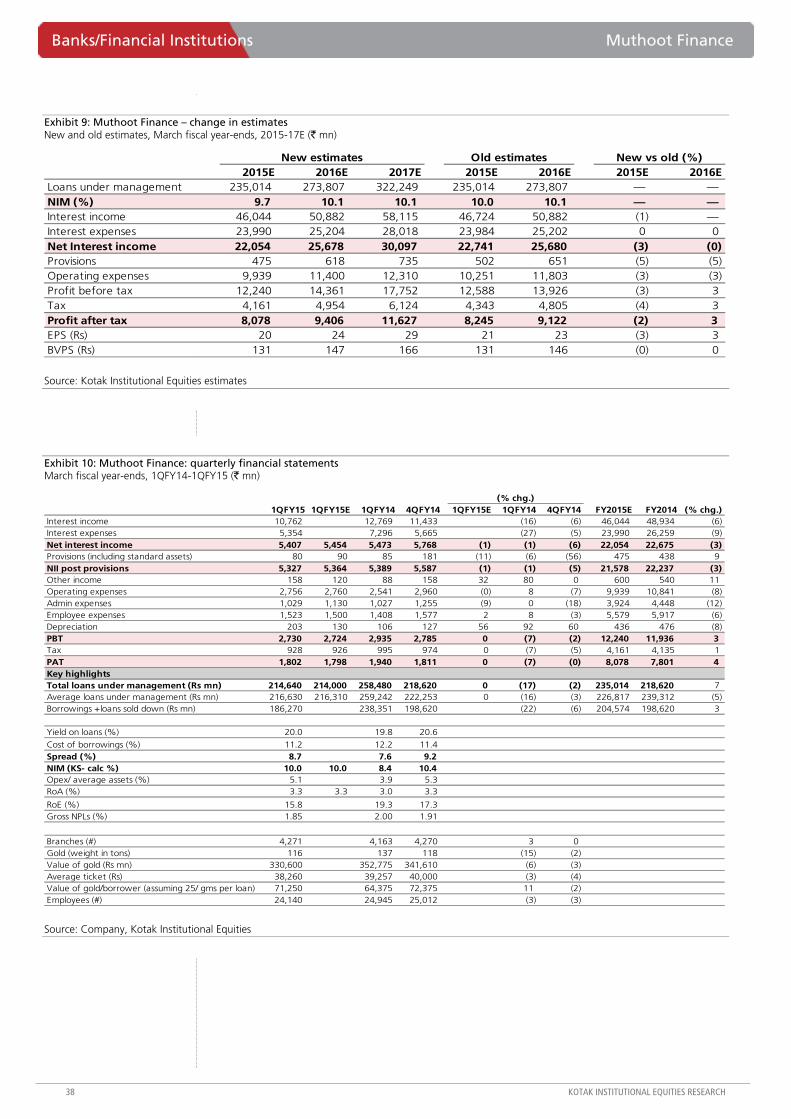

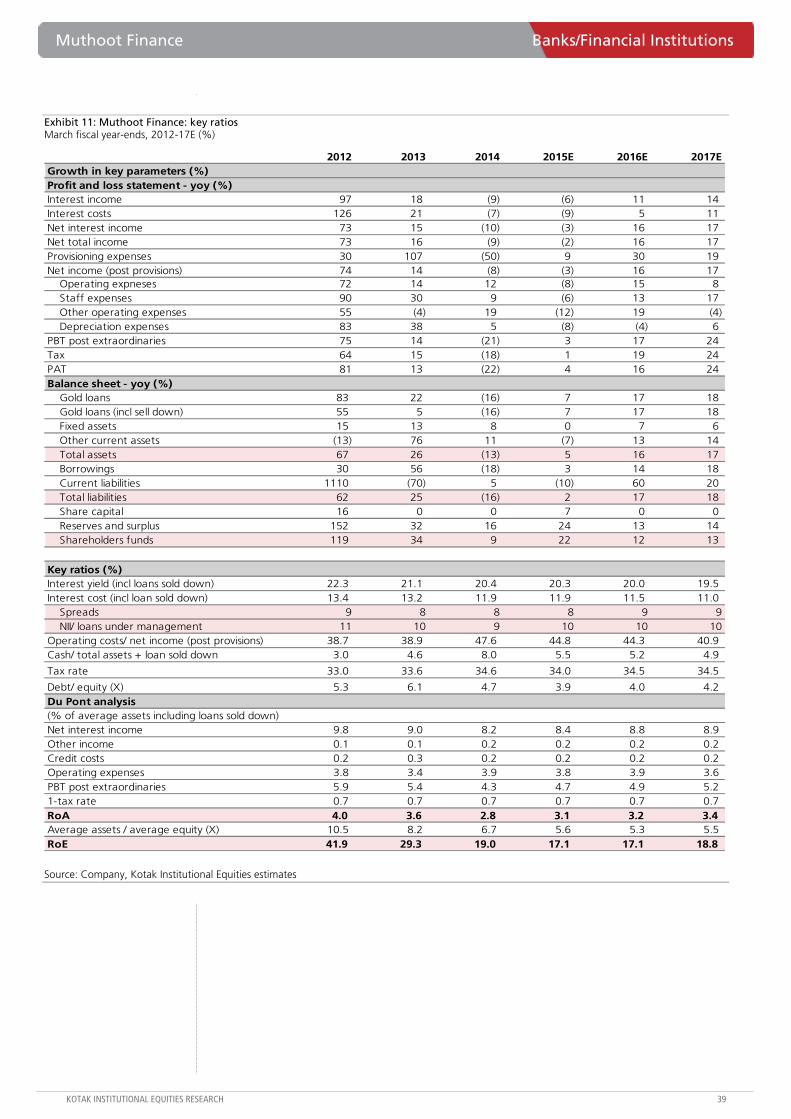

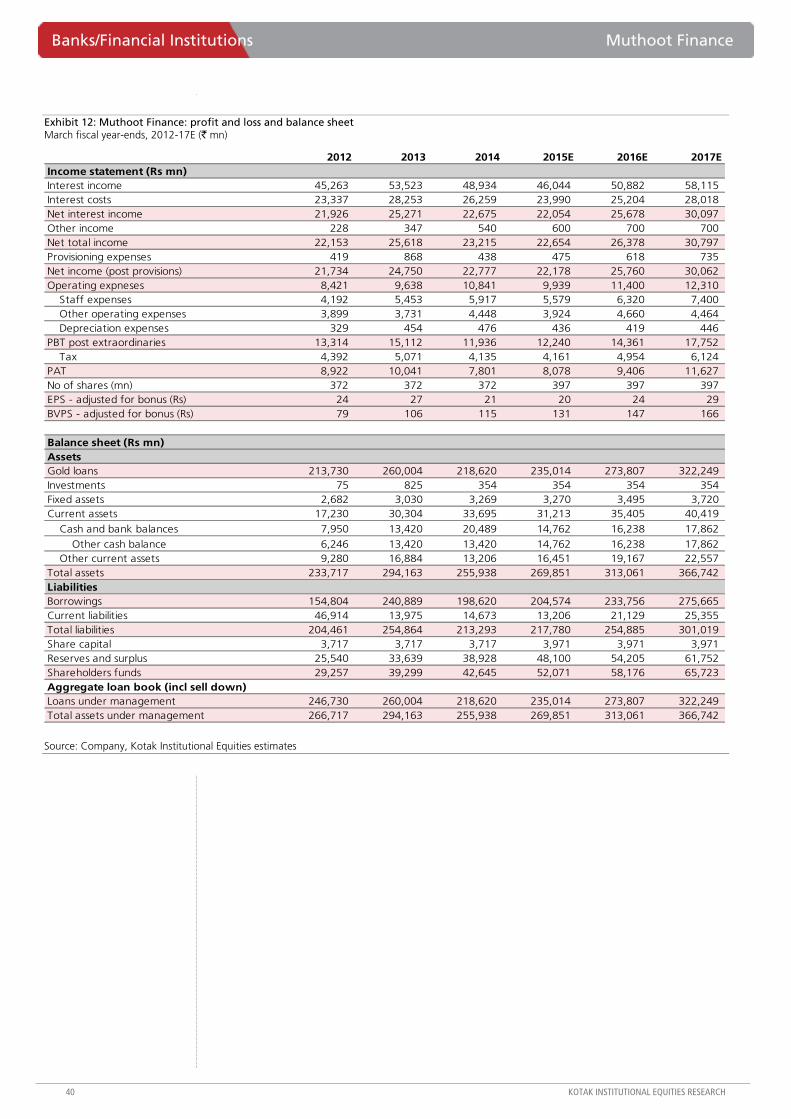

Muthoot Finance: Results on track, retain positive stance

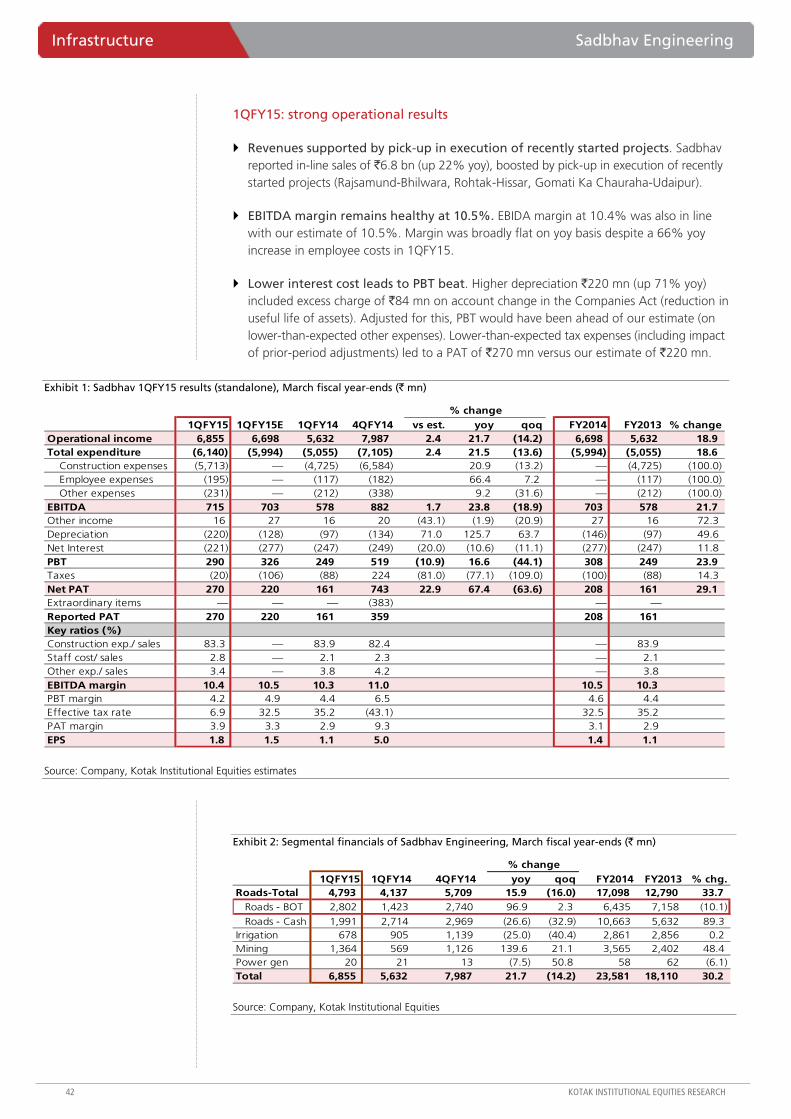

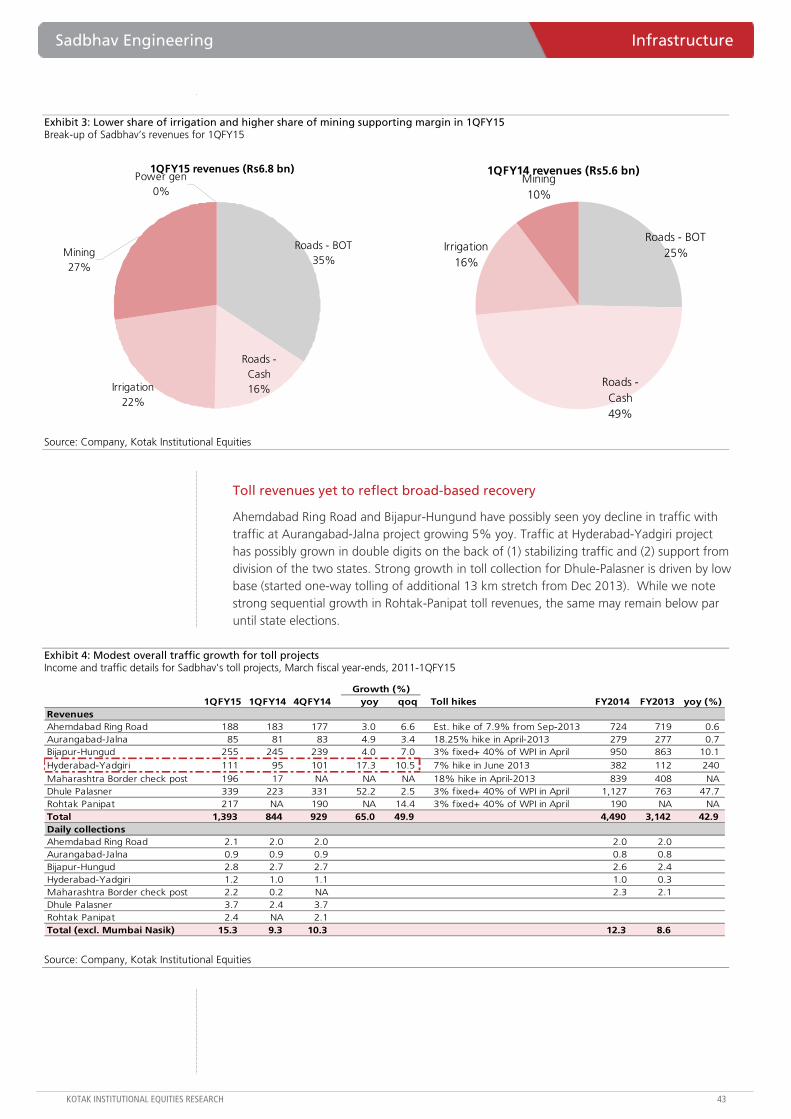

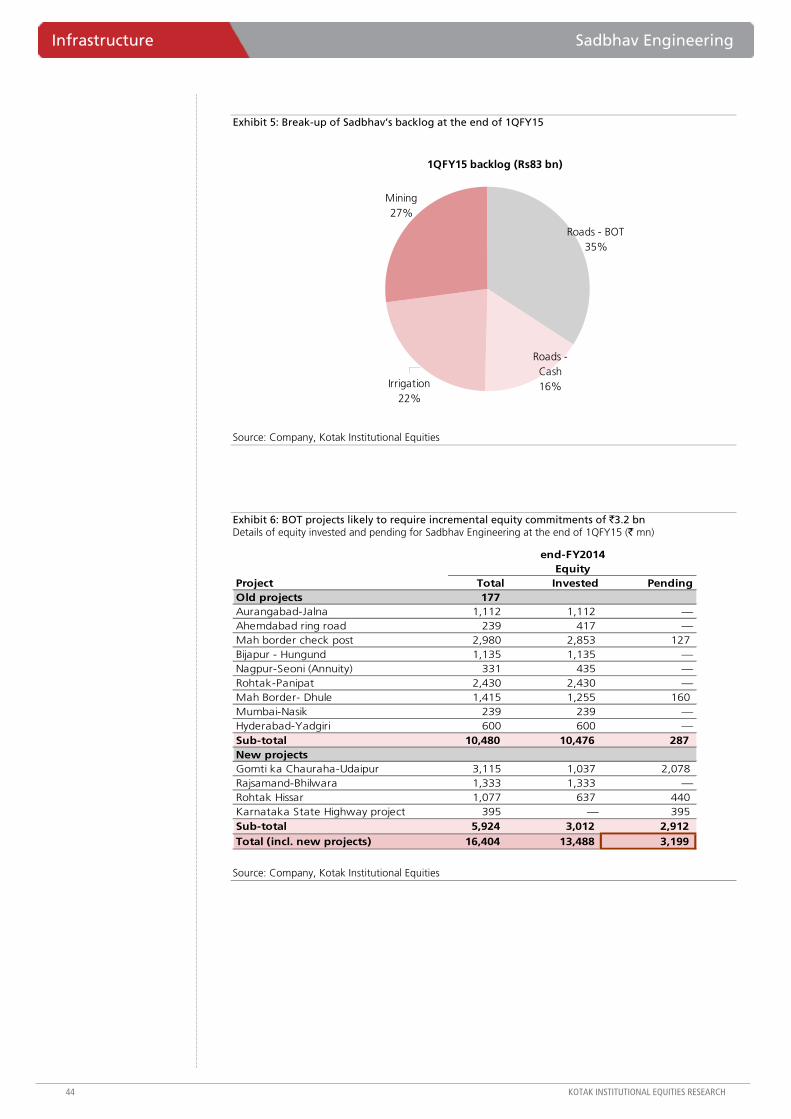

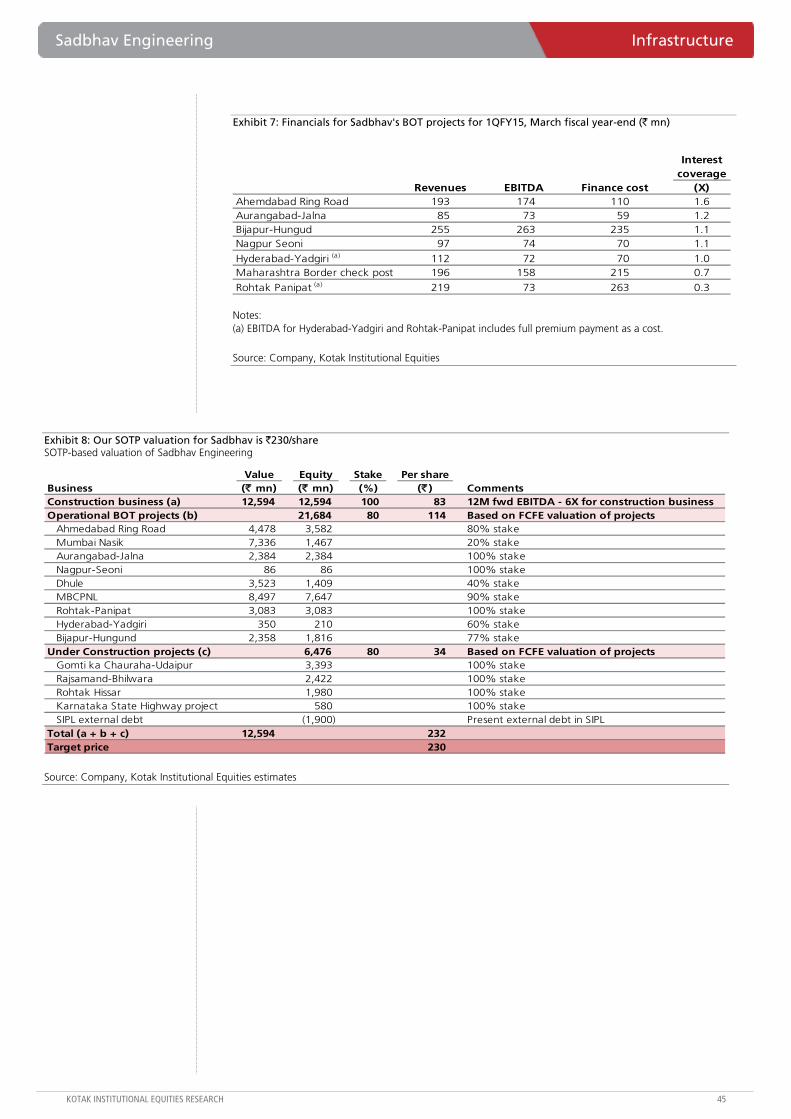

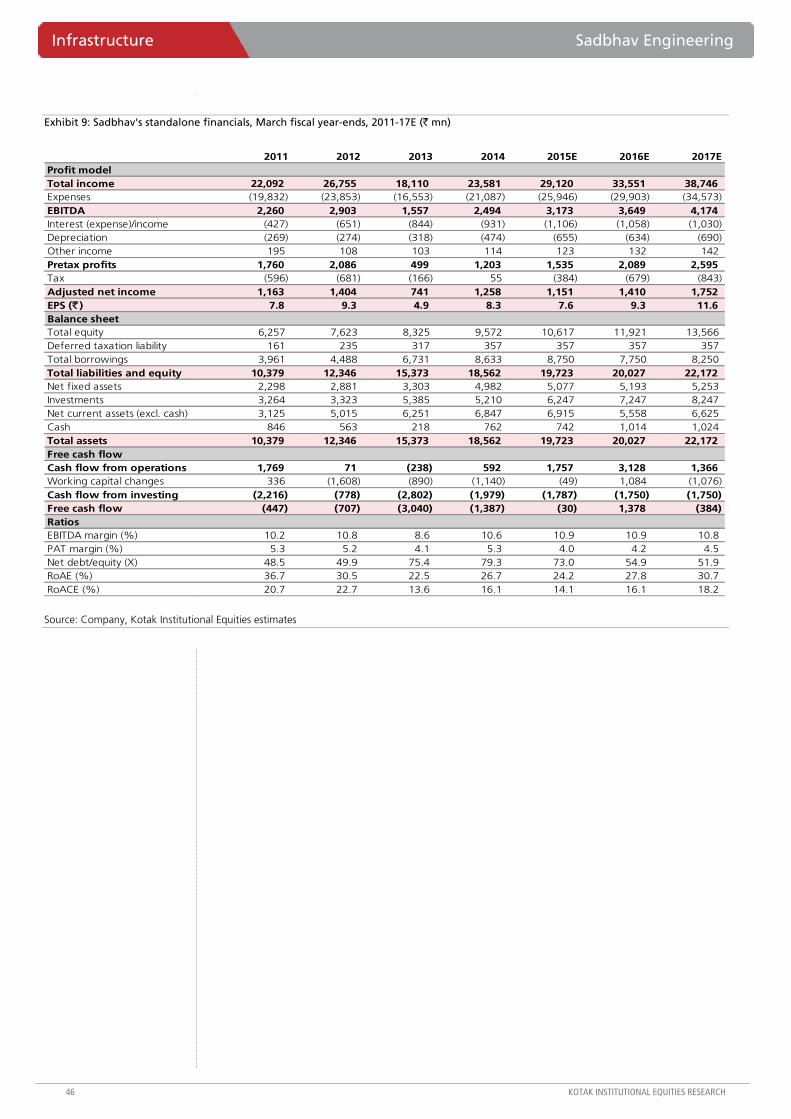

Sadbhav Engineering: Construction scores; traffic does not reflect broad-based recovery yet

Sector

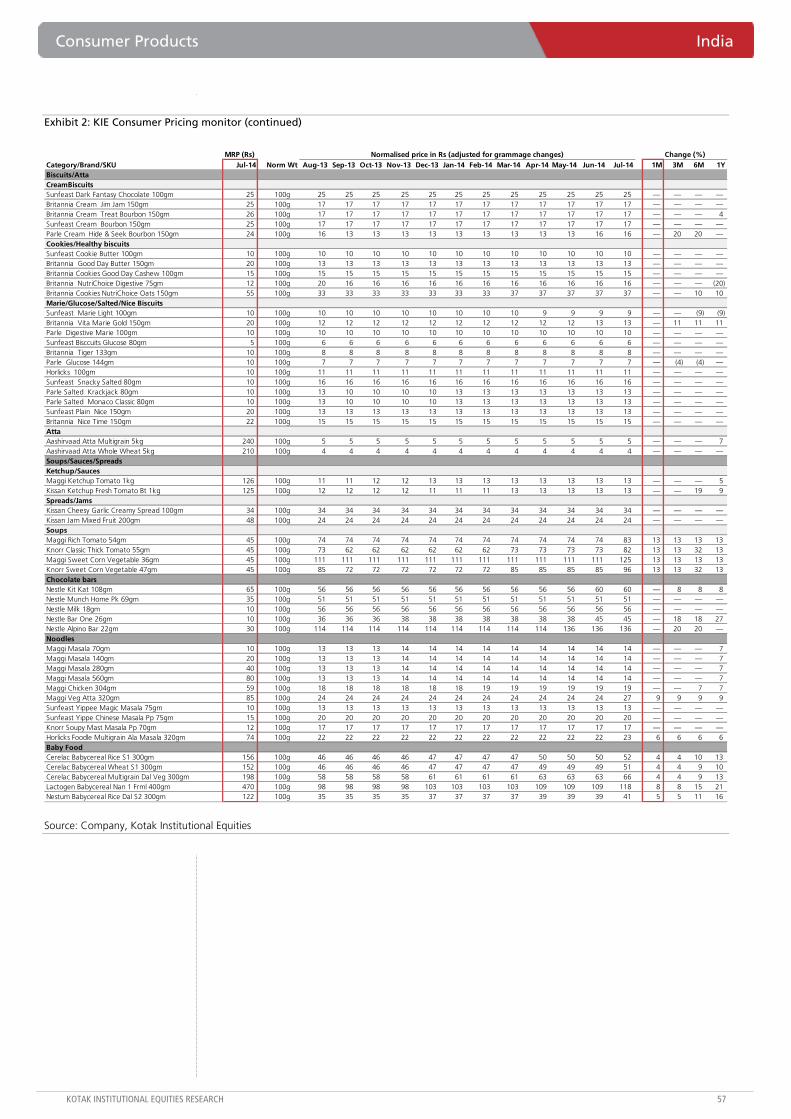

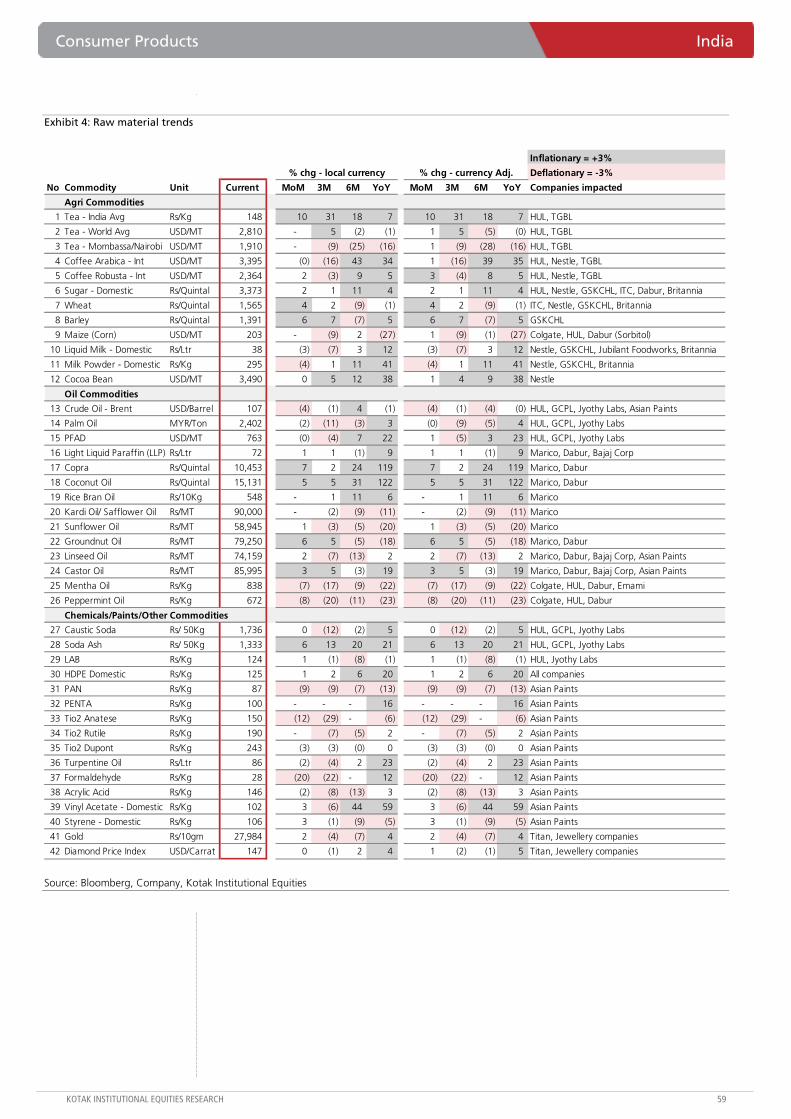

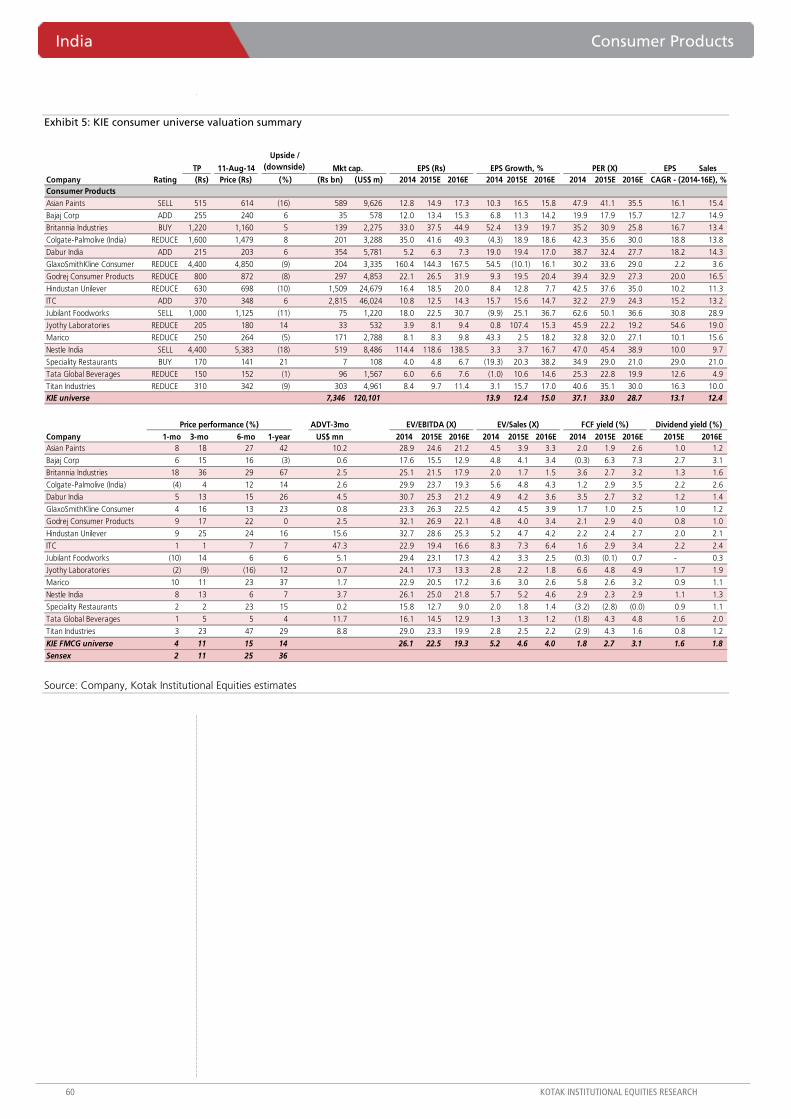

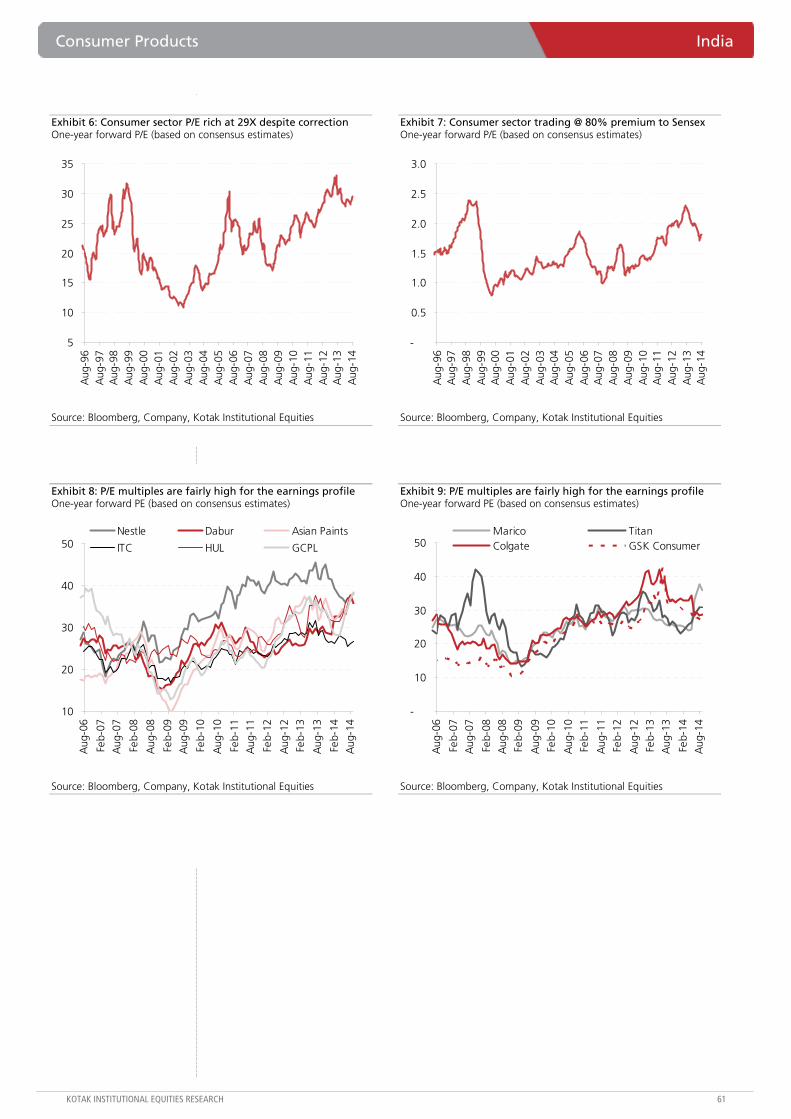

Consumer Products: Month in review - July 2014: price hikes pick pace

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

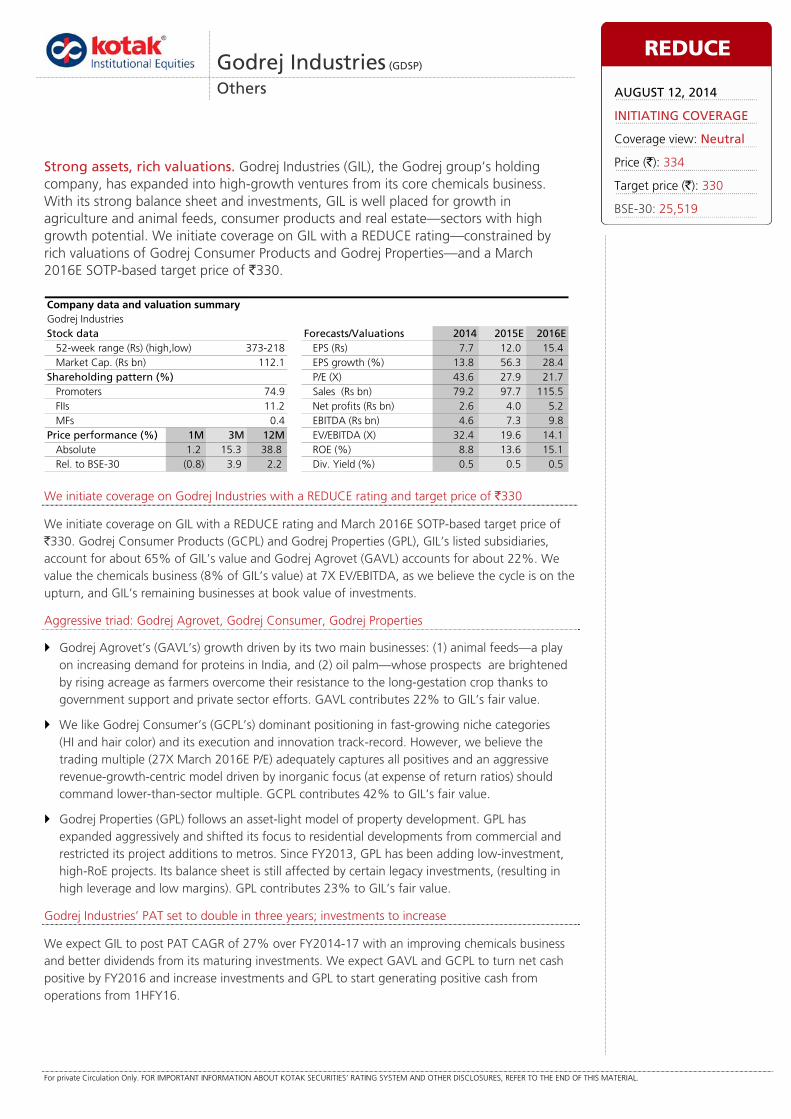

We initiate coverage on Godrej Industries with a REDUCE rating and target price of `330

We initiate coverage on GIL with a REDUCE rating and March 2016E SOTP-based target price of `330. Godrej Consumer Products (GCPL) and Godrej Properties (GPL), GIL’s listed subsidiaries, account for about 65% of GIL’s value and Godrej Agrovet (GAVL) accounts for about 22%. We value the chemicals business (8% of GIL’s value) at 7X EV/EBITDA, as we believe the cycle is on the upturn, and GIL’s remaining businesses at book value of investments.

Aggressive triad: Godrej Agrovet, Godrej Consumer, Godrej Properties

Godrej Agrovet’s (GAVL’s) growth driven by its two main businesses: (1) animal feeds—a play on increasing demand for proteins in India, and (2) oil palm—whose prospects are brightened by rising acreage as farmers overcome their resistance to the long-gestation crop thanks to government support and private sector efforts. GAVL contributes 22% to GIL’s fair value.

We like Godrej Consumer’s (GCPL’s) dominant positioning in fast-growing niche categories (HI and hair color) and its execution and innovation track-record. However, we believe the trading multiple (27X March 2016E P/E) adequately captures all positives and an aggressive revenue-growth-centric model driven by inorganic focus (at expense of return ratios) should command lower-than-sector multiple. GCPL contributes 42% to GIL’s fair value.

Godrej Properties (GPL) follows an asset-light model of property development. GPL has expanded aggressively and shifted its focus to residential developments from commercial and restricted its project additions to metros. Since FY2013, GPL has been adding low-investment, high-RoE projects. Its balance sheet is still affected by certain legacy investments, (resulting in high leverage and low margins). GPL contributes 23% to GIL’s fair value.

Godrej Industries’ PAT set to double in three years; investments to increase

We expect GIL to post PAT CAGR of 27% over FY2014-17 with an improving chemicals business and better dividends from its maturing investments. We expect GAVL and GCPL to turn net cash positive by FY2016 and increase investments and GPL to start generating positive cash from operations from 1HFY16.

Godrej Industries (GDSP)

Others

Strong assets, rich valuations. Godrej Industries (GIL), the Godrej group’s holding company, has expanded into high-growth ventures from its core chemicals business. With its strong balance sheet and investments, GIL is well placed for growth in agriculture and animal feeds, consumer products and real estate—sectors with high growth potential. We initiate coverage on GIL with a REDUCE rating—constrained by rich valuations of Godrej Consumer Products and Godrej Properties—and a March 2016E SOTP-based target price of `330.

Godrej IndustriesStock data Forecasts/Valuations 2014 2015E 2016E

52-week range (Rs) (high,low) EPS (Rs) 7.7 12.0 15.4Market Cap. (Rs bn) 112.1 EPS growth (%) 13.8 56.3 28.4

Shareholding pattern (%) P/E (X) 43.6 27.9 21.7Promoters 74.9 Sales (Rs bn) 79.2 97.7 115.5FIIs 11.2 Net profits (Rs bn) 2.6 4.0 5.2MFs 0.4 EBITDA (Rs bn) 4.6 7.3 9.8

Price performance (%) 1M 3M 12M EV/EBITDA (X) 32.4 19.6 14.1Absolute 1.2 15.3 38.8 ROE (%) 8.8 13.6 15.1Rel. to BSE-30 (0.8) 3.9 2.2 Div. Yield (%) 0.5 0.5 0.5

Company data and valuation summary

373-218

REDUCE

AUGUST 12, 2014

INITIATING COVERAGE

Coverage view: Neutral

Price (`): 334

Target price (`): 330

BSE-30: 25,519

Godrej Industries Others

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

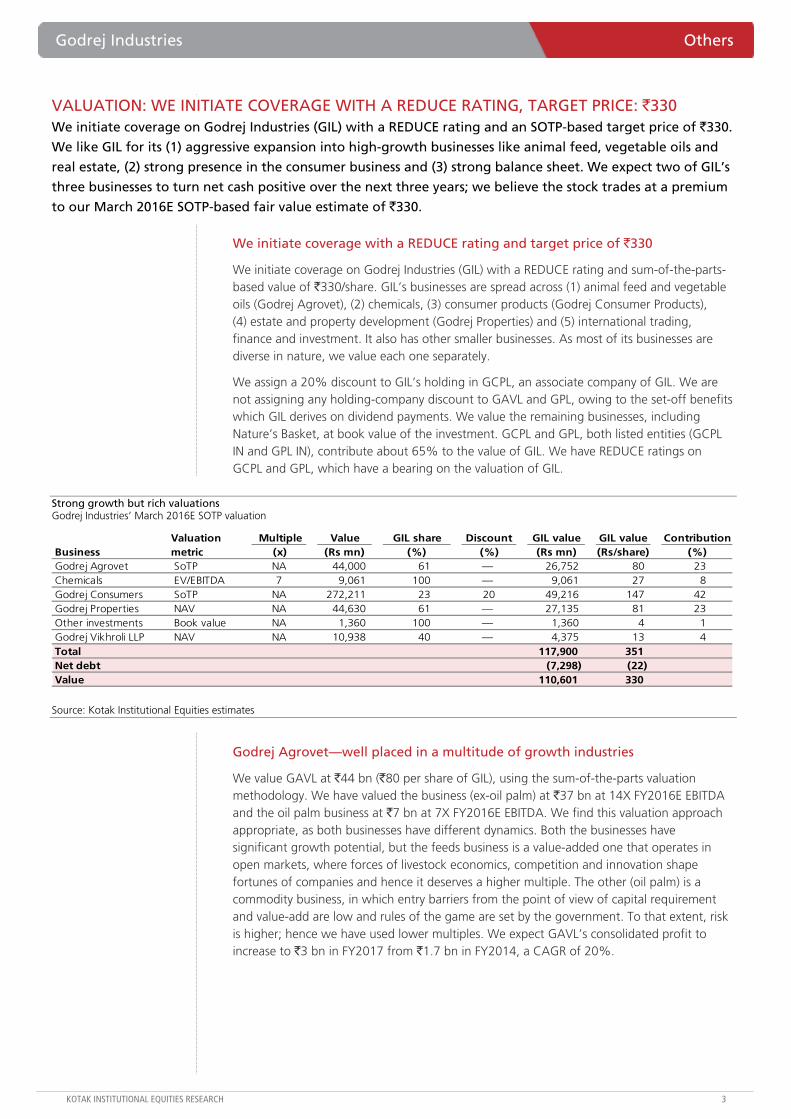

VALUATION: WE INITIATE COVERAGE WITH A REDUCE RATING, TARGET PRICE: `330 We initiate coverage on Godrej Industries (GIL) with a REDUCE rating and an SOTP-based target price of `330.

We like GIL for its (1) aggressive expansion into high-growth businesses like animal feed, vegetable oils and

real estate, (2) strong presence in the consumer business and (3) strong balance sheet. We expect two of GIL’s

three businesses to turn net cash positive over the next three years; we believe the stock trades at a premium

to our March 2016E SOTP-based fair value estimate of `330.

We initiate coverage with a REDUCE rating and target price of `330

We initiate coverage on Godrej Industries (GIL) with a REDUCE rating and sum-of-the-parts-based value of `330/share. GIL’s businesses are spread across (1) animal feed and vegetable oils (Godrej Agrovet), (2) chemicals, (3) consumer products (Godrej Consumer Products), (4) estate and property development (Godrej Properties) and (5) international trading, finance and investment. It also has other smaller businesses. As most of its businesses are diverse in nature, we value each one separately.

We assign a 20% discount to GIL’s holding in GCPL, an associate company of GIL. We are not assigning any holding-company discount to GAVL and GPL, owing to the set-off benefits which GIL derives on dividend payments. We value the remaining businesses, including Nature’s Basket, at book value of the investment. GCPL and GPL, both listed entities (GCPL IN and GPL IN), contribute about 65% to the value of GIL. We have REDUCE ratings on GCPL and GPL, which have a bearing on the valuation of GIL.

Strong growth but rich valuations Godrej Industries’ March 2016E SOTP valuation

Multiple Value GIL share Discount GIL value GIL value ContributionBusiness (x) (Rs mn) (%) (%) (Rs mn) (Rs/share) (%)Godrej Agrovet SoTP NA 44,000 61 — 26,752 80 23Chemicals EV/EBITDA 7 9,061 100 — 9,061 27 8Godrej Consumers SoTP NA 272,211 23 20 49,216 147 42Godrej Properties NAV NA 44,630 61 — 27,135 81 23Other investments Book value NA 1,360 100 — 1,360 4 1Godrej Vikhroli LLP NAV NA 10,938 40 — 4,375 13 4Total 117,900 351Net debt (7,298) (22)Value 110,601 330

Valuation metric

Source: Kotak Institutional Equities estimates

Godrej Agrovet—well placed in a multitude of growth industries

We value GAVL at `44 bn (`80 per share of GIL), using the sum-of-the-parts valuation methodology. We have valued the business (ex-oil palm) at `37 bn at 14X FY2016E EBITDA and the oil palm business at `7 bn at 7X FY2016E EBITDA. We find this valuation approach appropriate, as both businesses have different dynamics. Both the businesses have significant growth potential, but the feeds business is a value-added one that operates in open markets, where forces of livestock economics, competition and innovation shape fortunes of companies and hence it deserves a higher multiple. The other (oil palm) is a commodity business, in which entry barriers from the point of view of capital requirement and value-add are low and rules of the game are set by the government. To that extent, risk is higher; hence we have used lower multiples. We expect GAVL’s consolidated profit to increase to `3 bn in FY2017 from `1.7 bn in FY2014, a CAGR of 20%.

Others Godrej Industries

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

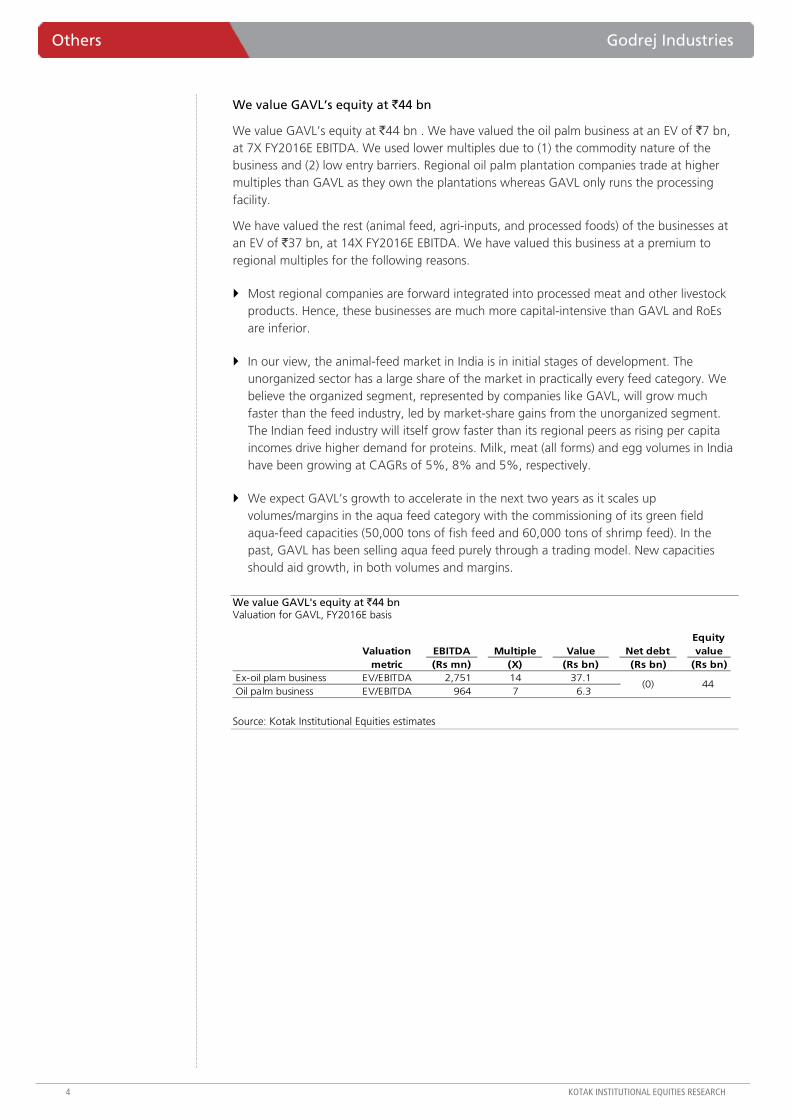

We value GAVL’s equity at `44 bn

We value GAVL’s equity at `44 bn . We have valued the oil palm business at an EV of `7 bn, at 7X FY2016E EBITDA. We used lower multiples due to (1) the commodity nature of the business and (2) low entry barriers. Regional oil palm plantation companies trade at higher multiples than GAVL as they own the plantations whereas GAVL only runs the processing facility.

We have valued the rest (animal feed, agri-inputs, and processed foods) of the businesses at an EV of `37 bn, at 14X FY2016E EBITDA. We have valued this business at a premium to regional multiples for the following reasons.

Most regional companies are forward integrated into processed meat and other livestock products. Hence, these businesses are much more capital-intensive than GAVL and RoEs are inferior.

In our view, the animal-feed market in India is in initial stages of development. The unorganized sector has a large share of the market in practically every feed category. We believe the organized segment, represented by companies like GAVL, will grow much faster than the feed industry, led by market-share gains from the unorganized segment. The Indian feed industry will itself grow faster than its regional peers as rising per capita incomes drive higher demand for proteins. Milk, meat (all forms) and egg volumes in India have been growing at CAGRs of 5%, 8% and 5%, respectively.

We expect GAVL’s growth to accelerate in the next two years as it scales up volumes/margins in the aqua feed category with the commissioning of its green field aqua-feed capacities (50,000 tons of fish feed and 60,000 tons of shrimp feed). In the past, GAVL has been selling aqua feed purely through a trading model. New capacities should aid growth, in both volumes and margins.

We value GAVL's equity at `44 bn Valuation for GAVL, FY2016E basis

EBITDA Multiple Value Net debtEquity value

(Rs mn) (X) (Rs bn) (Rs bn) (Rs bn)Ex-oil plam business EV/EBITDA 2,751 14 37.1 Oil palm business EV/EBITDA 964 7 6.3

Valuation metric

44(0)

Source: Kotak Institutional Equities estimates

Godrej Industries Others

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

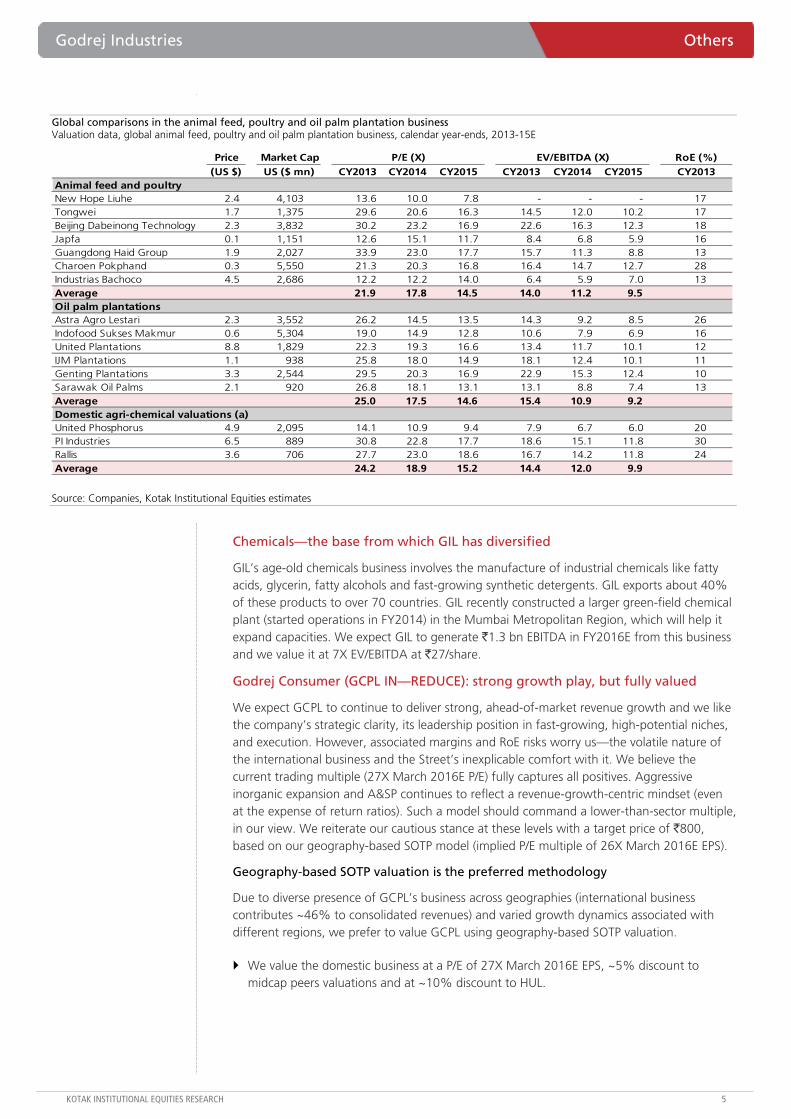

Global comparisons in the animal feed, poultry and oil palm plantation business Valuation data, global animal feed, poultry and oil palm plantation business, calendar year-ends, 2013-15E

Price RoE (%)(US $) CY2013 CY2014 CY2015 CY2013 CY2014 CY2015 CY2013

Animal feed and poultryNew Hope Liuhe 2.4 4,103 13.6 10.0 7.8 - - - 17 Tongwei 1.7 1,375 29.6 20.6 16.3 14.5 12.0 10.2 17 Beijing Dabeinong Technology 2.3 3,832 30.2 23.2 16.9 22.6 16.3 12.3 18 Japfa 0.1 1,151 12.6 15.1 11.7 8.4 6.8 5.9 16 Guangdong Haid Group 1.9 2,027 33.9 23.0 17.7 15.7 11.3 8.8 13 Charoen Pokphand 0.3 5,550 21.3 20.3 16.8 16.4 14.7 12.7 28 Industrias Bachoco 4.5 2,686 12.2 12.2 14.0 6.4 5.9 7.0 13 Average 21.9 17.8 14.5 14.0 11.2 9.5 Oil palm plantations Astra Agro Lestari 2.3 3,552 26.2 14.5 13.5 14.3 9.2 8.5 26 Indofood Sukses Makmur 0.6 5,304 19.0 14.9 12.8 10.6 7.9 6.9 16 United Plantations 8.8 1,829 22.3 19.3 16.6 13.4 11.7 10.1 12 IJM Plantations 1.1 938 25.8 18.0 14.9 18.1 12.4 10.1 11 Genting Plantations 3.3 2,544 29.5 20.3 16.9 22.9 15.3 12.4 10 Sarawak Oil Palms 2.1 920 26.8 18.1 13.1 13.1 8.8 7.4 13 Average 25.0 17.5 14.6 15.4 10.9 9.2 Domestic agri-chemical valuations (a)United Phosphorus 4.9 2,095 14.1 10.9 9.4 7.9 6.7 6.0 20 PI Industries 6.5 889 30.8 22.8 17.7 18.6 15.1 11.8 30 Rallis 3.6 706 27.7 23.0 18.6 16.7 14.2 11.8 24 Average 24.2 18.9 15.2 14.4 12.0 9.9

P/E (X) EV/EBITDA (X) Market CapUS ($ mn)

Source: Companies, Kotak Institutional Equities estimates

Chemicals—the base from which GIL has diversified

GIL’s age-old chemicals business involves the manufacture of industrial chemicals like fatty acids, glycerin, fatty alcohols and fast-growing synthetic detergents. GIL exports about 40% of these products to over 70 countries. GIL recently constructed a larger green-field chemical plant (started operations in FY2014) in the Mumbai Metropolitan Region, which will help it expand capacities. We expect GIL to generate `1.3 bn EBITDA in FY2016E from this business and we value it at 7X EV/EBITDA at `27/share.

Godrej Consumer (GCPL IN—REDUCE): strong growth play, but fully valued

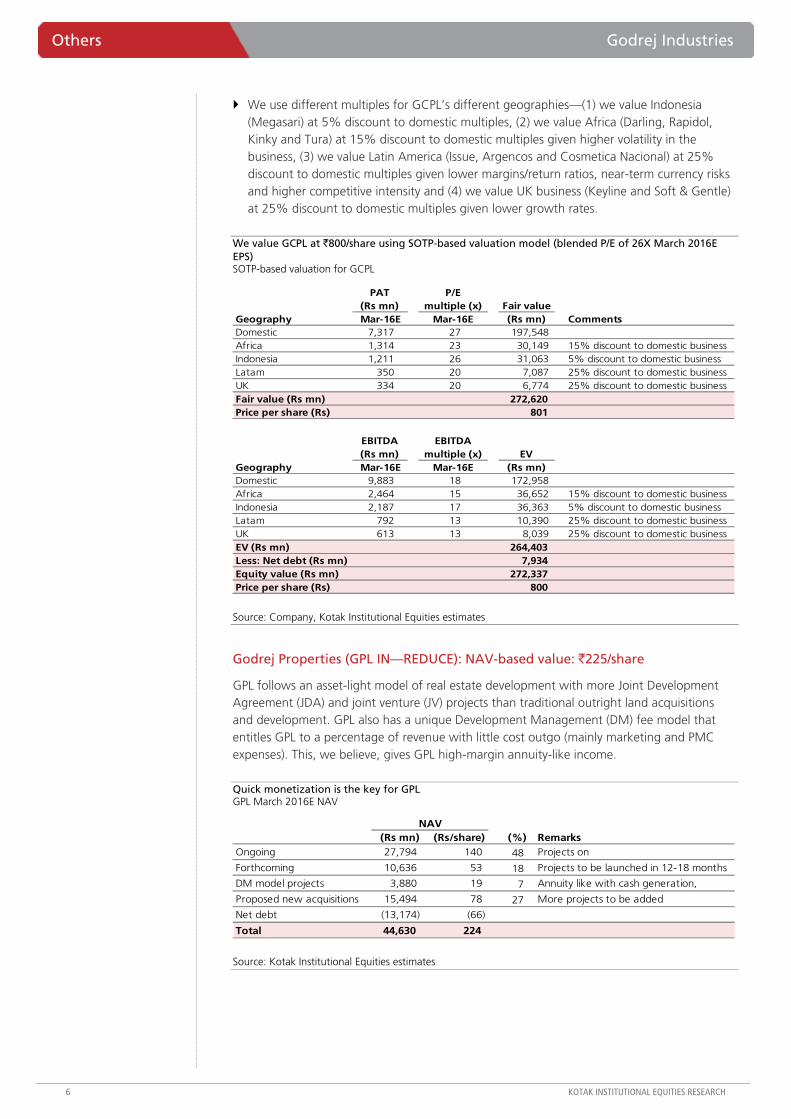

We expect GCPL to continue to deliver strong, ahead-of-market revenue growth and we like the company’s strategic clarity, its leadership position in fast-growing, high-potential niches, and execution. However, associated margins and RoE risks worry us—the volatile nature of the international business and the Street’s inexplicable comfort with it. We believe the current trading multiple (27X March 2016E P/E) fully captures all positives. Aggressive inorganic expansion and A&SP continues to reflect a revenue-growth-centric mindset (even at the expense of return ratios). Such a model should command a lower-than-sector multiple, in our view. We reiterate our cautious stance at these levels with a target price of `800, based on our geography-based SOTP model (implied P/E multiple of 26X March 2016E EPS).

Geography-based SOTP valuation is the preferred methodology

Due to diverse presence of GCPL’s business across geographies (international business contributes ~46% to consolidated revenues) and varied growth dynamics associated with different regions, we prefer to value GCPL using geography-based SOTP valuation.

We value the domestic business at a P/E of 27X March 2016E EPS, ~5% discount to midcap peers valuations and at ~10% discount to HUL.

Others Godrej Industries

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

We use different multiples for GCPL’s different geographies—(1) we value Indonesia (Megasari) at 5% discount to domestic multiples, (2) we value Africa (Darling, Rapidol, Kinky and Tura) at 15% discount to domestic multiples given higher volatility in the business, (3) we value Latin America (Issue, Argencos and Cosmetica Nacional) at 25% discount to domestic multiples given lower margins/return ratios, near-term currency risks and higher competitive intensity and (4) we value UK business (Keyline and Soft & Gentle) at 25% discount to domestic multiples given lower growth rates.

We value GCPL at `800/share using SOTP-based valuation model (blended P/E of 26X March 2016E EPS) SOTP-based valuation for GCPL

Fair valueGeography (Rs mn) CommentsDomestic 7,317 27 197,548 Africa 1,314 23 30,149 15% discount to domestic businessIndonesia 1,211 26 31,063 5% discount to domestic businessLatam 350 20 7,087 25% discount to domestic businessUK 334 20 6,774 25% discount to domestic businessFair value (Rs mn) 272,620 Price per share (Rs) 801

EVGeography (Rs mn)Domestic 9,883 18 172,958 Africa 2,464 15 36,652 15% discount to domestic businessIndonesia 2,187 17 36,363 5% discount to domestic businessLatam 792 13 10,390 25% discount to domestic businessUK 613 13 8,039 25% discount to domestic businessEV (Rs mn) 264,403 Less: Net debt (Rs mn) 7,934 Equity value (Rs mn) 272,337 Price per share (Rs) 800

PAT (Rs mn)Mar-16E

EBITDA (Rs mn)Mar-16E

EBITDA multiple (x)

Mar-16E

P/E multiple (x)

Mar-16E

Source: Company, Kotak Institutional Equities estimates

Godrej Properties (GPL IN—REDUCE): NAV-based value: `225/share

GPL follows an asset-light model of real estate development with more Joint Development Agreement (JDA) and joint venture (JV) projects than traditional outright land acquisitions and development. GPL also has a unique Development Management (DM) fee model that entitles GPL to a percentage of revenue with little cost outgo (mainly marketing and PMC expenses). This, we believe, gives GPL high-margin annuity-like income.

Quick monetization is the key for GPL GPL March 2016E NAV

(Rs mn) (Rs/share) (%) RemarksOngoing 27,794 140 48 Projects on

Forthcoming 10,636 53 18 Projects to be launched in 12-18 months

DM model projects 3,880 19 7 Annuity like with cash generation,

Proposed new acquisitions 15,494 78 27 More projects to be added

Net debt (13,174) (66)

Total 44,630 224

NAV

Source: Kotak Institutional Equities estimates

Godrej Industries Others

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

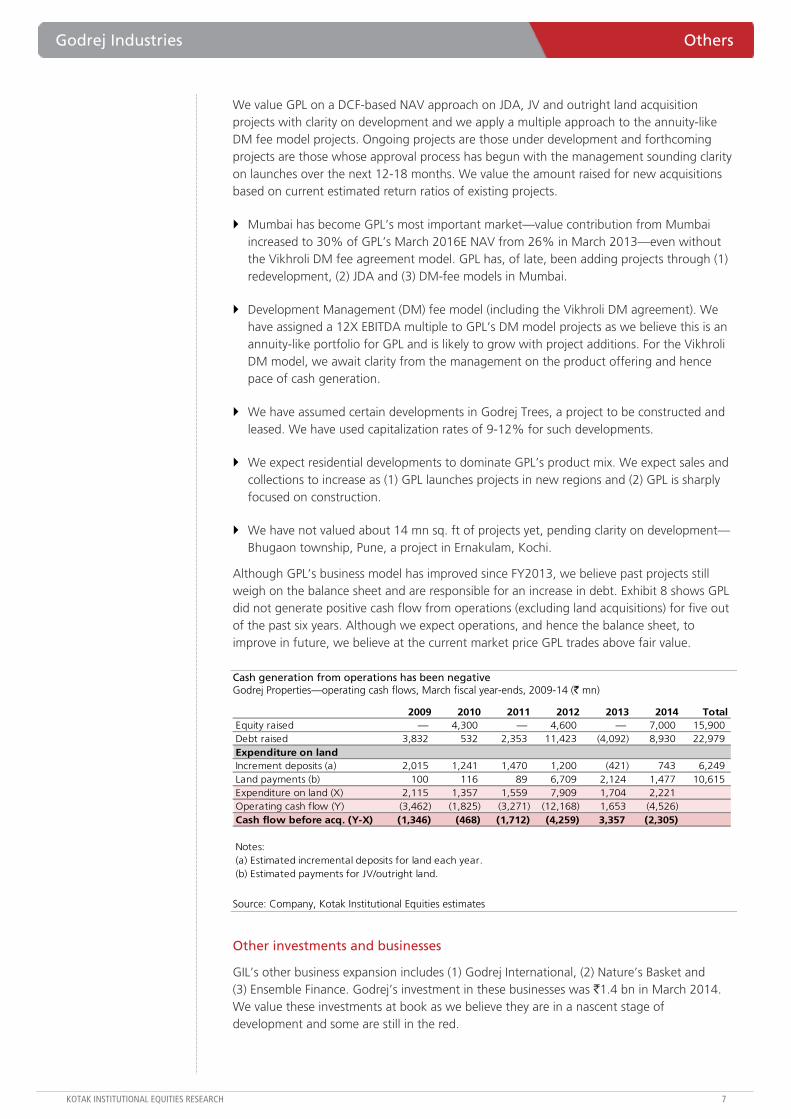

We value GPL on a DCF-based NAV approach on JDA, JV and outright land acquisition projects with clarity on development and we apply a multiple approach to the annuity-like DM fee model projects. Ongoing projects are those under development and forthcoming projects are those whose approval process has begun with the management sounding clarity on launches over the next 12-18 months. We value the amount raised for new acquisitions based on current estimated return ratios of existing projects.

Mumbai has become GPL’s most important market—value contribution from Mumbai increased to 30% of GPL’s March 2016E NAV from 26% in March 2013—even without the Vikhroli DM fee agreement model. GPL has, of late, been adding projects through (1) redevelopment, (2) JDA and (3) DM-fee models in Mumbai.

Development Management (DM) fee model (including the Vikhroli DM agreement). We have assigned a 12X EBITDA multiple to GPL’s DM model projects as we believe this is an annuity-like portfolio for GPL and is likely to grow with project additions. For the Vikhroli DM model, we await clarity from the management on the product offering and hence pace of cash generation.

We have assumed certain developments in Godrej Trees, a project to be constructed and leased. We have used capitalization rates of 9-12% for such developments.

We expect residential developments to dominate GPL’s product mix. We expect sales and collections to increase as (1) GPL launches projects in new regions and (2) GPL is sharply focused on construction.

We have not valued about 14 mn sq. ft of projects yet, pending clarity on development—Bhugaon township, Pune, a project in Ernakulam, Kochi.

Although GPL’s business model has improved since FY2013, we believe past projects still weigh on the balance sheet and are responsible for an increase in debt. Exhibit 8 shows GPL did not generate positive cash flow from operations (excluding land acquisitions) for five out of the past six years. Although we expect operations, and hence the balance sheet, to improve in future, we believe at the current market price GPL trades above fair value.

Cash generation from operations has been negative Godrej Properties—operating cash flows, March fiscal year-ends, 2009-14 (` mn)

2009 2010 2011 2012 2013 2014 TotalEquity raised — 4,300 — 4,600 — 7,000 15,900 Debt raised 3,832 532 2,353 11,423 (4,092) 8,930 22,979 Expenditure on landIncrement deposits (a) 2,015 1,241 1,470 1,200 (421) 743 6,249 Land payments (b) 100 116 89 6,709 2,124 1,477 10,615 Expenditure on land (X) 2,115 1,357 1,559 7,909 1,704 2,221 Operating cash flow (Y) (3,462) (1,825) (3,271) (12,168) 1,653 (4,526) Cash flow before acq. (Y-X) (1,346) (468) (1,712) (4,259) 3,357 (2,305)

Notes:(a) Estimated incremental deposits for land each year.(b) Estimated payments for JV/outright land.

Source: Company, Kotak Institutional Equities estimates

Other investments and businesses

GIL’s other business expansion includes (1) Godrej International, (2) Nature’s Basket and (3) Ensemble Finance. Godrej’s investment in these businesses was `1.4 bn in March 2014. We value these investments at book as we believe they are in a nascent stage of development and some are still in the red.

Others Godrej Industries

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

GODREJ INDUSTRIES FINANCIALS—INVESTMENTS MADE, PAYBACK TIME IS HERE! Godrej Industries invested over `10.5 bn to set up and expand its businesses over the past four years,

additionally some of the individual businesses raised equity. We believe Godrej Properties has a year to go

before turning operating-cash positive, GCPL and GAVL are generating positive cash from operations and we

believe they will be net cash by FY2016 (excluding heavy investments/new acquisitions). In the chemicals

business, we believe an improving market and recent capacity addition will boost volumes and margins and

Godrej Industries’ other businesses, like Nature’s Basket, will drain cash for at least two years.

Godrej Agrovet, Godrej Properties lead growth from a low base

In addition to the chemicals business, Godrej Industries’ consolidated revenues include revenue from Godrej Agrovet, Godrej Properties, Godrej Trading, Godrej International Trading and Finance and Nature’s Basket. Godrej Agrovet and Godrej Properties account for about 55% of revenue and 95% of operating margins. We estimate net income CAGR of 20% over FY2014-17 due to strong growth in the two companies. Godrej Properties is also Godrej Industries’ fastest growing business and contributes the best margins (operating margins of about 25%). With Godrej Properties’ strong focus on construction and increase in pace of launches (and hence sales), we expect its contribution to Godrej Industries’ revenue to increase from 15% in FY2014 to 29% in FY2017. We believe this will improve Godrej Industries’ consolidated margins.

Strong revenue growth for Godrej Industries due to Godrej Agrovet and Godrej Properties Godrej Industries (consolidated) profit model, March fiscal year-ends, 2013-17E (` mn)

2013 2014 2015E 2016E 2017ETotal revenues 69,643 79,179 97,685 115,493 136,250 Cost of goods sold (55,688) (63,191) (76,591) (90,185) (106,086) Employee costs (2,698) (2,942) (3,501) (3,888) (4,270) SG&A costs (7,484) (8,469) (10,336) (11,634) (13,074) EBITDA 3,774 4,577 7,257 9,787 12,819 Other income 528 1,558 1,777 1,902 2,111 Interest (1,103) (1,457) (1,503) (1,247) (1,020) Depreciation / amortisation (595) (704) (837) (924) (1,015) Pre-tax profits 2,604 3,973 6,694 9,517 12,895 Extraordinary items 1,654 694 854 828 908 Current tax (1,215) (1,712) (2,214) (3,177) (4,064) Deferred tax (128) — — — —Net income 2,916 2,955 5,334 7,168 9,739 Minority interests (762.4) (1,430.0) (2,588.6) (3,745.8) (6,003.3) Share of profit from associates 1,758.1 1,738.5 2,104.2 2,533.4 2,957.4 Adjusted net income 3,912 3,264 4,850 5,956 6,693 EPS (Rs)Fully diluted 11.7 9.7 14.5 17.8 20.0 DPS (Rs) 1.8 1.8 1.8 1.8 1.8 Shares outstanding (mn)Fully diluted 335 335 335 335 335 Cash flow per share (Rs)Fully diluted 13.8 12.4 16.9 20.5 23.0 Margins (%)EBITDA 5.4 5.8 7.4 8.5 9.4 Adjusted net income 5.6 4.1 5.0 5.2 4.9 Cash tax rate (%) 46.6 43.1 33.1 33.4 31.5 Effective tax rate (%) 51.5 43.1 33.1 33.4 31.5 Growth (%)Total revenues 24.1 13.7 23.4 18.2 18.0 Net adjusted income 34.1 (16.6) 48.6 22.8 12.4

Source: Company, Kotak Institutional Equities estimates

With expect Godrej Agrovet to become net cash positive in another two years and Godrej Properties to start generating positive cash flow from operations from FY2016.

Godrej Industries Others

KOTAK INSTITUTIONAL EQUITIES RESEARCH 9

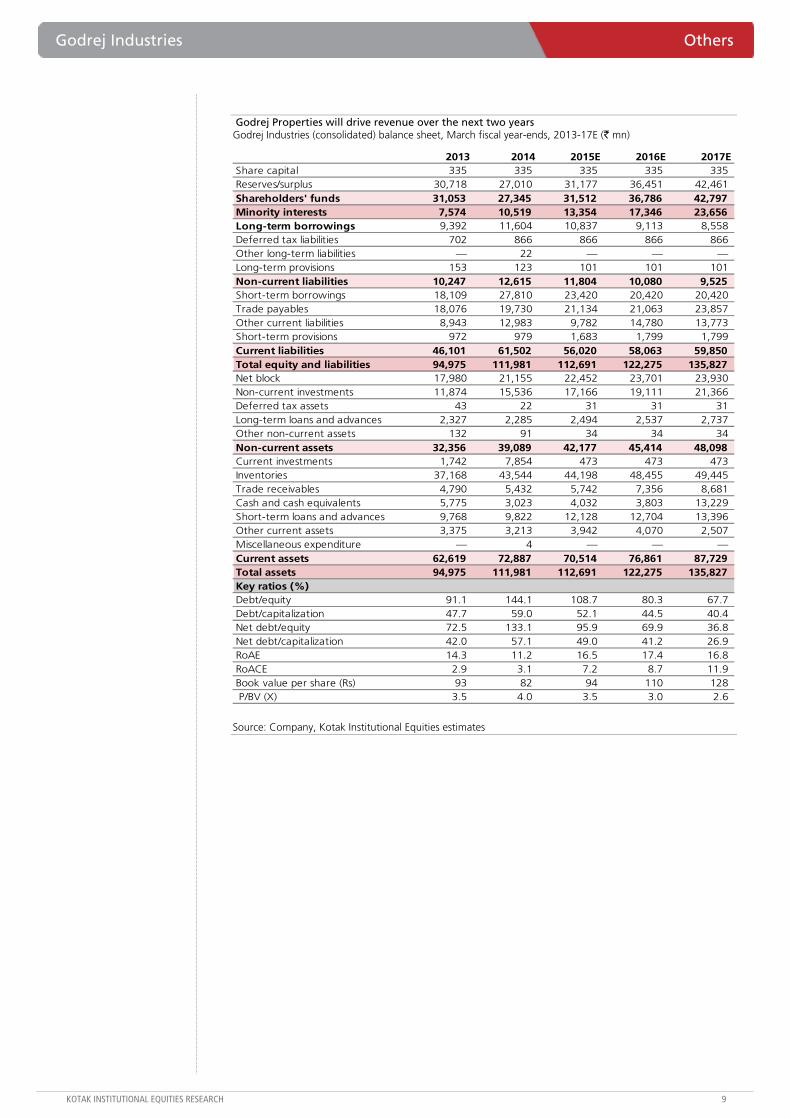

Godrej Properties will drive revenue over the next two years Godrej Industries (consolidated) balance sheet, March fiscal year-ends, 2013-17E (` mn)

2013 2014 2015E 2016E 2017EShare capital 335 335 335 335 335 Reserves/surplus 30,718 27,010 31,177 36,451 42,461 Shareholders' funds 31,053 27,345 31,512 36,786 42,797 Minority interests 7,574 10,519 13,354 17,346 23,656 Long-term borrowings 9,392 11,604 10,837 9,113 8,558 Deferred tax liabilities 702 866 866 866 866 Other long-term liabilities — 22 — — —Long-term provisions 153 123 101 101 101 Non-current liabilities 10,247 12,615 11,804 10,080 9,525 Short-term borrowings 18,109 27,810 23,420 20,420 20,420 Trade payables 18,076 19,730 21,134 21,063 23,857 Other current liabilities 8,943 12,983 9,782 14,780 13,773 Short-term provisions 972 979 1,683 1,799 1,799 Current liabilities 46,101 61,502 56,020 58,063 59,850 Total equity and liabilities 94,975 111,981 112,691 122,275 135,827 Net block 17,980 21,155 22,452 23,701 23,930 Non-current investments 11,874 15,536 17,166 19,111 21,366 Deferred tax assets 43 22 31 31 31 Long-term loans and advances 2,327 2,285 2,494 2,537 2,737 Other non-current assets 132 91 34 34 34 Non-current assets 32,356 39,089 42,177 45,414 48,098 Current investments 1,742 7,854 473 473 473 Inventories 37,168 43,544 44,198 48,455 49,445 Trade receivables 4,790 5,432 5,742 7,356 8,681 Cash and cash equivalents 5,775 3,023 4,032 3,803 13,229 Short-term loans and advances 9,768 9,822 12,128 12,704 13,396 Other current assets 3,375 3,213 3,942 4,070 2,507 Miscellaneous expenditure — 4 — — —Current assets 62,619 72,887 70,514 76,861 87,729 Total assets 94,975 111,981 112,691 122,275 135,827 Key ratios (%)Debt/equity 91.1 144.1 108.7 80.3 67.7 Debt/capitalization 47.7 59.0 52.1 44.5 40.4 Net debt/equity 72.5 133.1 95.9 69.9 36.8 Net debt/capitalization 42.0 57.1 49.0 41.2 26.9 RoAE 14.3 11.2 16.5 17.4 16.8 RoACE 2.9 3.1 7.2 8.7 11.9 Book value per share (Rs) 93 82 94 110 128 P/BV (X) 3.5 4.0 3.5 3.0 2.6

Source: Company, Kotak Institutional Equities estimates

Others Godrej Industries

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

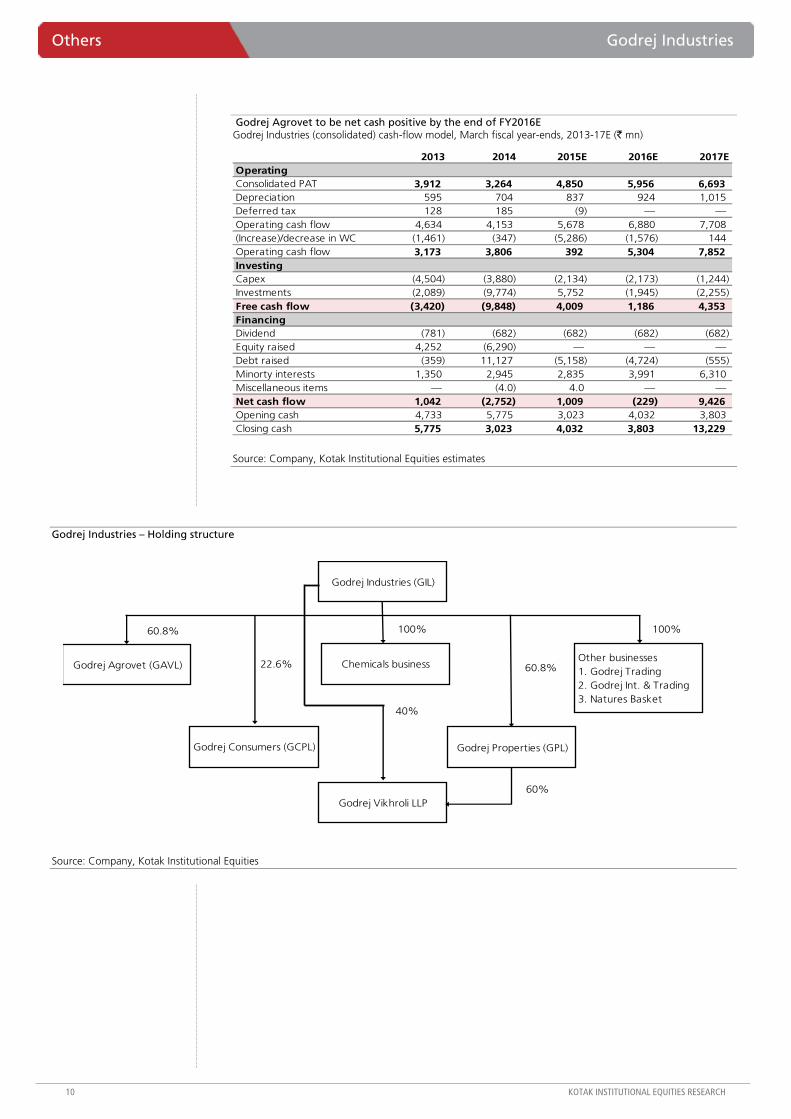

Godrej Agrovet to be net cash positive by the end of FY2016E Godrej Industries (consolidated) cash-flow model, March fiscal year-ends, 2013-17E (` mn)

2013 2014 2015E 2016E 2017EOperatingConsolidated PAT 3,912 3,264 4,850 5,956 6,693 Depreciation 595 704 837 924 1,015 Deferred tax 128 185 (9) — —Operating cash flow 4,634 4,153 5,678 6,880 7,708 (Increase)/decrease in WC (1,461) (347) (5,286) (1,576) 144 Operating cash flow 3,173 3,806 392 5,304 7,852 InvestingCapex (4,504) (3,880) (2,134) (2,173) (1,244) Investments (2,089) (9,774) 5,752 (1,945) (2,255) Free cash flow (3,420) (9,848) 4,009 1,186 4,353 FinancingDividend (781) (682) (682) (682) (682) Equity raised 4,252 (6,290) — — —Debt raised (359) 11,127 (5,158) (4,724) (555) Minorty interests 1,350 2,945 2,835 3,991 6,310 Miscellaneous items — (4.0) 4.0 — —Net cash flow 1,042 (2,752) 1,009 (229) 9,426 Opening cash 4,733 5,775 3,023 4,032 3,803 Closing cash 5,775 3,023 4,032 3,803 13,229

Source: Company, Kotak Institutional Equities estimates

Godrej Industries – Holding structure

Godrej Industries (GIL)

Chemicals business

Godrej Consumers (GCPL)

Other businesses1. Godrej Trading2. Godrej Int. & Trading3. Natures Basket

Godrej Properties (GPL)

Godrej Agrovet (GAVL)

60.8%

22.6%

100%

60.8%

100%

Godrej Vikhroli LLP 60%

40%

Source: Company, Kotak Institutional Equities

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Country flows—India-focused active funds turn positive after 28 months

India-focused active funds have seen net inflows for the first time in the past 28 months. After witnessing outflows worth US$4.9 bn since February 2012, these funds attracted capital worth US$88 mn in July. Total listed fund flows into India amounted to US$0.95 bn during the period. ETF participation was India-focused (US$0.13 bn) as well as EM-focused (US$0.38 bn). With total net FII inflows into India (US$2.5 bn) superseding listed fund activity substantially, other market participants were active in July as well.

Country allocations—allocations to India continue to climb

Allocations to India by Asia ex-Japan funds touched 12.7% in June 2014, which was 0.3% higher than May (12.4%). China, India and Taiwan were the preferred investment destinations in the Asia ex-Japan region in June. GEM funds have seen allocations to India stabilize at 10.6%. Taiwan and Russia saw an increase in allocations over the past three months. Korea saw reduction in allocations by Asia ex-Japan funds and GEM funds.

Fund flows—‘smart’ beta being preferred within the Indian ETF space

Smart beta is being preferred over plain vanilla products in the India ETF landscape with WisdomTree India Earnings Fund (EPI) attracting US$0.6 bn over the past three months. While most prevalent index methodologies base their index construction on free-float and investability, EPI allocates higher weights to more profitable companies thereby offering cheaper benchmark valuations. EM-focused ETFs continued to attract capital with ~US$3.5 bn inflows over the month. EM-focused active funds also picked up the mantle, seeing inflows worth US$1.4 bn during the same period.

Strategy.dot

Strategy Foreign fund-flow tracker

India-focused active fund flow positive for the first time since February 2012. KIE’s foreign fund-flow tracker gives us a comprehensive view of market flow activity by listed funds into India and its emerging market peers. These market participants are further classified based on their investment styles (passive ETFs or active Non-ETFs) in an attempt to understand the intent and sentiments governing the flows.

INDIA

AUGUST 12, 2014

UPDATE

BSE-30: 25,519

QUICK NUMBERS

• Listed funds saw inflows worth US$0.95 bn in July

• Allocations to India by Asia ex-Japan up to 12.7% in June

• WisdomTree India Earnings fund has seen inflows worth US$0.6 bn in the past three months

• EM-focused ETFs saw inflows worth US$3.5 bn in the month

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

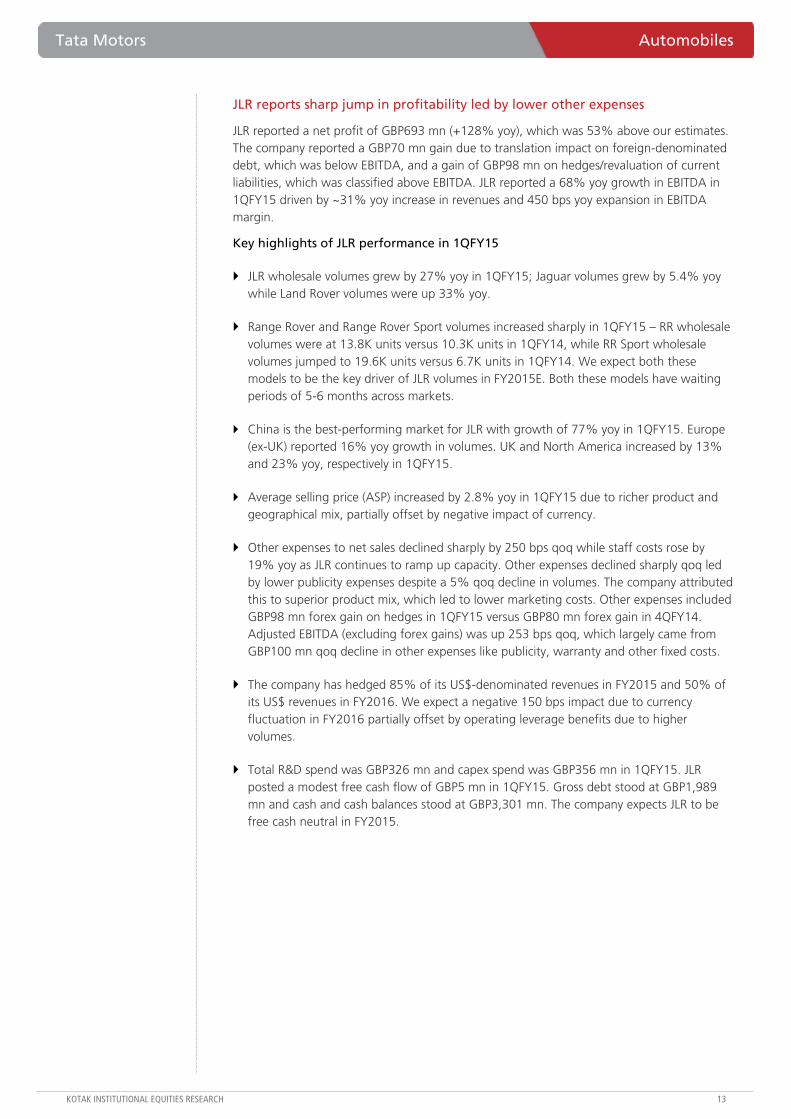

JLR surprises again but this time it’s lower publicity expenses

JLR reported net profit of GBP693 mn (+128% yoy), which was 53% above our estimates. JLR reported 68% yoy growth in EBITDA in 1QFY15 driven by ~31% yoy increase in revenues and 450 bps yoy expansion in EBITDA margin. The key surprise was lower-than-expected other expenses. Other expenses declined sharply qoq led by lower publicity expenses despite a 5% qoq decline in volumes. The company attributed this to superior product mix, which led to lower marketing costs. Other expenses included GBP98 mn forex gain on hedges in 1QFY15 versus GBP80 mn forex gain in 4QFY14. Adjusted EBITDA (excluding forex gains) was up 253 bps qoq, which largely came from GBP100 mn qoq decline in other expenses like publicity, warranty and other fixed costs.

Standalone business remains under pressure

Standalone business reported an adjusted PBT loss of `11,302 mn in 1QFY15, which was higher than our estimate of a loss of `10,241 mn led by 15.4% yoy decline in net sales. EBITDA margin in standalone business at -3.9% declined by 510 bps yoy as passenger vehicle losses increased. We expect standalone EBITDA margin to improve over the coming quarters due to lower discounting in the commercial vehicle business and pick-up in volumes of passenger vehicle business led by Zest launch.

We continue to stay bullish; Street underestimating JLR’s upcoming model launch potential

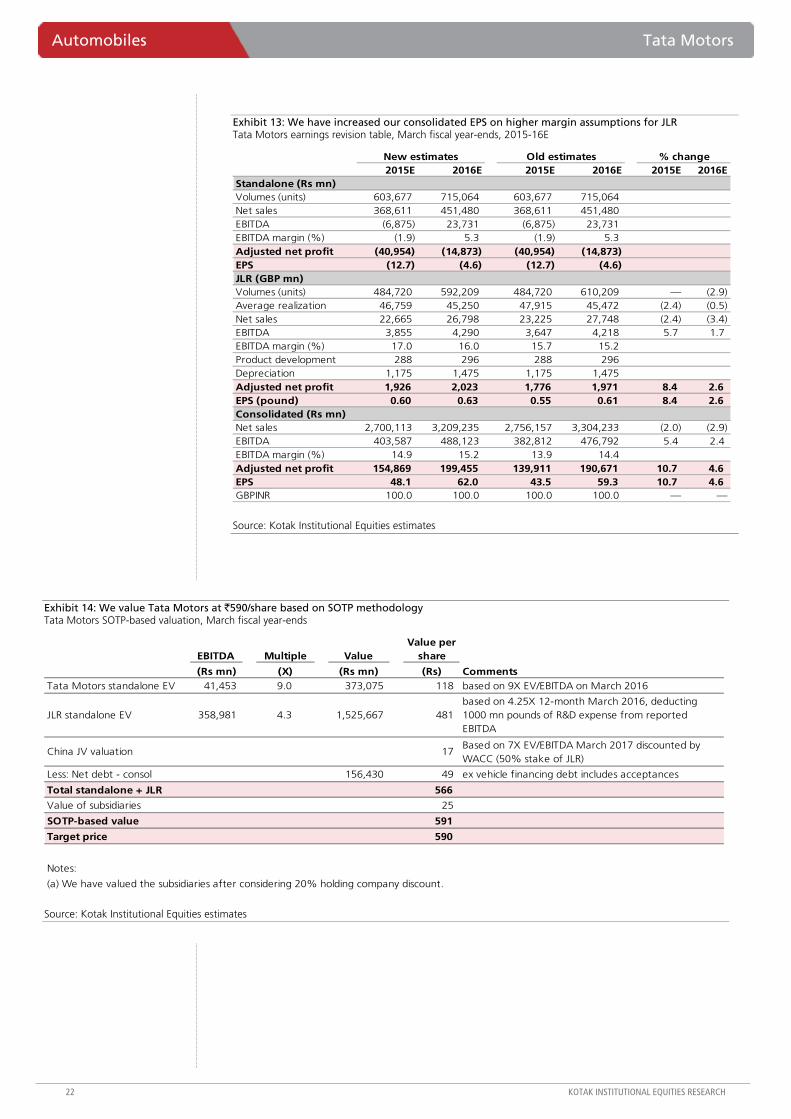

We maintain our BUY rating on the stock as we continue to expect positive surprises on JLR volume growth. We expect new launches to improve JLR volume growth. Jaguar XE and Jaguar SUV will be the key launches for the company over the next two years, in our view. We have increased our consolidated earnings estimates by 5-11% over FY2015/16E led by increase in our EBITDA margin assumptions for JLR. We have thus increased our target price to `590 (from `575) based on sum-of-the-parts valuation methodology.

Tata Motors (TTMT)

Automobiles

Beat led by lower other expenses. JLR reported EBITDA growth of 68% yoy in 1QFY15, which

was 24% above our estimates led by lower other expenses. The company indicated that other expenses were lower by ~GBP100 mn excluding forex gains on a qoq basis due to lower marketing costs because of a superior product mix. We maintain our BUY rating on the stock as we believe volume growth of JLR will continue to surprise the Street positively led by new model launches. We have increased our target price to `590 (from `575) as we have increased our JLR EBITDA margin assumptions.

Tata MotorsStock data Forecasts/Valuations 2014 2015E 2016E

52-week range (Rs) (high,low) EPS (Rs) 46.5 48.1 62.0Market Cap. (Rs bn) 1,347.8 EPS growth (%) 51.4 3.4 28.8

Shareholding pattern (%) P/E (X) 9.6 9.3 7.2Promoters 34.3 Sales (Rs bn) 2,328.3 2,700.1 3,209.2FIIs 27.1 Net profits (Rs bn) 149.8 154.9 199.5MFs 0.9 EBITDA (Rs bn) 348.4 403.6 488.1

Price performance (%) 1M 3M 12M EV/EBITDA (X) 4.8 4.2 3.7Absolute 0.1 4.5 60.2 ROE (%) 28.7 21.1 21.9Rel. to BSE-30 (1.8) (5.9) 17.9 Div. Yield (%) 0.4 0.0 0.0

Company data and valuation summary

488-276

BUY

AUGUST 12, 2014

RESULT

Coverage view: Attractive

Price (`): 447

Target price (`): 590

BSE-30: 25,519

Tata Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 13

JLR reports sharp jump in profitability led by lower other expenses

JLR reported a net profit of GBP693 mn (+128% yoy), which was 53% above our estimates. The company reported a GBP70 mn gain due to translation impact on foreign-denominated debt, which was below EBITDA, and a gain of GBP98 mn on hedges/revaluation of current liabilities, which was classified above EBITDA. JLR reported a 68% yoy growth in EBITDA in 1QFY15 driven by ~31% yoy increase in revenues and 450 bps yoy expansion in EBITDA margin.

Key highlights of JLR performance in 1QFY15

JLR wholesale volumes grew by 27% yoy in 1QFY15; Jaguar volumes grew by 5.4% yoy while Land Rover volumes were up 33% yoy.

Range Rover and Range Rover Sport volumes increased sharply in 1QFY15 – RR wholesale volumes were at 13.8K units versus 10.3K units in 1QFY14, while RR Sport wholesale volumes jumped to 19.6K units versus 6.7K units in 1QFY14. We expect both these models to be the key driver of JLR volumes in FY2015E. Both these models have waiting periods of 5-6 months across markets.

China is the best-performing market for JLR with growth of 77% yoy in 1QFY15. Europe (ex-UK) reported 16% yoy growth in volumes. UK and North America increased by 13% and 23% yoy, respectively in 1QFY15.

Average selling price (ASP) increased by 2.8% yoy in 1QFY15 due to richer product and geographical mix, partially offset by negative impact of currency.

Other expenses to net sales declined sharply by 250 bps qoq while staff costs rose by 19% yoy as JLR continues to ramp up capacity. Other expenses declined sharply qoq led by lower publicity expenses despite a 5% qoq decline in volumes. The company attributed this to superior product mix, which led to lower marketing costs. Other expenses included GBP98 mn forex gain on hedges in 1QFY15 versus GBP80 mn forex gain in 4QFY14. Adjusted EBITDA (excluding forex gains) was up 253 bps qoq, which largely came from GBP100 mn qoq decline in other expenses like publicity, warranty and other fixed costs.

The company has hedged 85% of its US$-denominated revenues in FY2015 and 50% of its US$ revenues in FY2016. We expect a negative 150 bps impact due to currency fluctuation in FY2016 partially offset by operating leverage benefits due to higher volumes.

Total R&D spend was GBP326 mn and capex spend was GBP356 mn in 1QFY15. JLR posted a modest free cash flow of GBP5 mn in 1QFY15. Gross debt stood at GBP1,989 mn and cash and cash balances stood at GBP3,301 mn. The company expects JLR to be free cash neutral in FY2015.

Automobiles Tata Motors

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

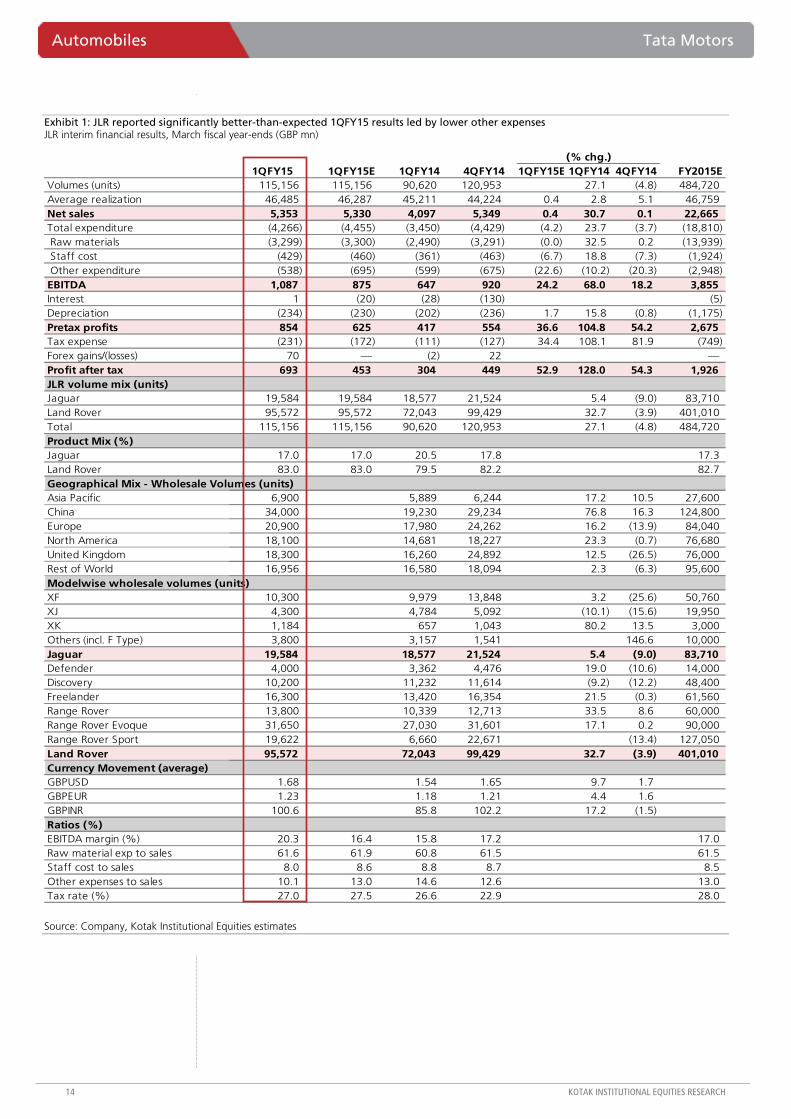

Exhibit 1: JLR reported significantly better-than-expected 1QFY15 results led by lower other expenses JLR interim financial results, March fiscal year-ends (GBP mn)

(% chg.)1QFY15 1QFY15E 1QFY14 4QFY14 1QFY15E 1QFY14 4QFY14 FY2015E

Volumes (units) 115,156 115,156 90,620 120,953 27.1 (4.8) 484,720 Average realization 46,485 46,287 45,211 44,224 0.4 2.8 5.1 46,759 Net sales 5,353 5,330 4,097 5,349 0.4 30.7 0.1 22,665 Total expenditure (4,266) (4,455) (3,450) (4,429) (4.2) 23.7 (3.7) (18,810) Raw materials (3,299) (3,300) (2,490) (3,291) (0.0) 32.5 0.2 (13,939) Staff cost (429) (460) (361) (463) (6.7) 18.8 (7.3) (1,924) Other expenditure (538) (695) (599) (675) (22.6) (10.2) (20.3) (2,948) EBITDA 1,087 875 647 920 24.2 68.0 18.2 3,855 Interest 1 (20) (28) (130) (5) Depreciation (234) (230) (202) (236) 1.7 15.8 (0.8) (1,175) Pretax profits 854 625 417 554 36.6 104.8 54.2 2,675 Tax expense (231) (172) (111) (127) 34.4 108.1 81.9 (749) Forex gains/(losses) 70 — (2) 22 —Profit after tax 693 453 304 449 52.9 128.0 54.3 1,926 JLR volume mix (units)Jaguar 19,584 19,584 18,577 21,524 5.4 (9.0) 83,710 Land Rover 95,572 95,572 72,043 99,429 32.7 (3.9) 401,010 Total 115,156 115,156 90,620 120,953 27.1 (4.8) 484,720 Product Mix (%)Jaguar 17.0 17.0 20.5 17.8 17.3 Land Rover 83.0 83.0 79.5 82.2 82.7 Geographical Mix - Wholesale Volumes (units)Asia Pacific 6,900 5,889 6,244 17.2 10.5 27,600 China 34,000 19,230 29,234 76.8 16.3 124,800 Europe 20,900 17,980 24,262 16.2 (13.9) 84,040 North America 18,100 14,681 18,227 23.3 (0.7) 76,680 United Kingdom 18,300 16,260 24,892 12.5 (26.5) 76,000 Rest of World 16,956 16,580 18,094 2.3 (6.3) 95,600 Modelwise wholesale volumes (units)XF 10,300 9,979 13,848 3.2 (25.6) 50,760 XJ 4,300 4,784 5,092 (10.1) (15.6) 19,950 XK 1,184 657 1,043 80.2 13.5 3,000 Others (incl. F Type) 3,800 3,157 1,541 146.6 10,000 Jaguar 19,584 18,577 21,524 5.4 (9.0) 83,710 Defender 4,000 3,362 4,476 19.0 (10.6) 14,000 Discovery 10,200 11,232 11,614 (9.2) (12.2) 48,400 Freelander 16,300 13,420 16,354 21.5 (0.3) 61,560 Range Rover 13,800 10,339 12,713 33.5 8.6 60,000 Range Rover Evoque 31,650 27,030 31,601 17.1 0.2 90,000 Range Rover Sport 19,622 6,660 22,671 (13.4) 127,050 Land Rover 95,572 72,043 99,429 32.7 (3.9) 401,010 Currency Movement (average)GBPUSD 1.68 1.54 1.65 9.7 1.7 GBPEUR 1.23 1.18 1.21 4.4 1.6 GBPINR 100.6 85.8 102.2 17.2 (1.5) Ratios (%)EBITDA margin (%) 20.3 16.4 15.8 17.2 17.0 Raw material exp to sales 61.6 61.9 60.8 61.5 61.5 Staff cost to sales 8.0 8.6 8.8 8.7 8.5 Other expenses to sales 10.1 13.0 14.6 12.6 13.0 Tax rate (%) 27.0 27.5 26.6 22.9 28.0

Source: Company, Kotak Institutional Equities estimates

Tata Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

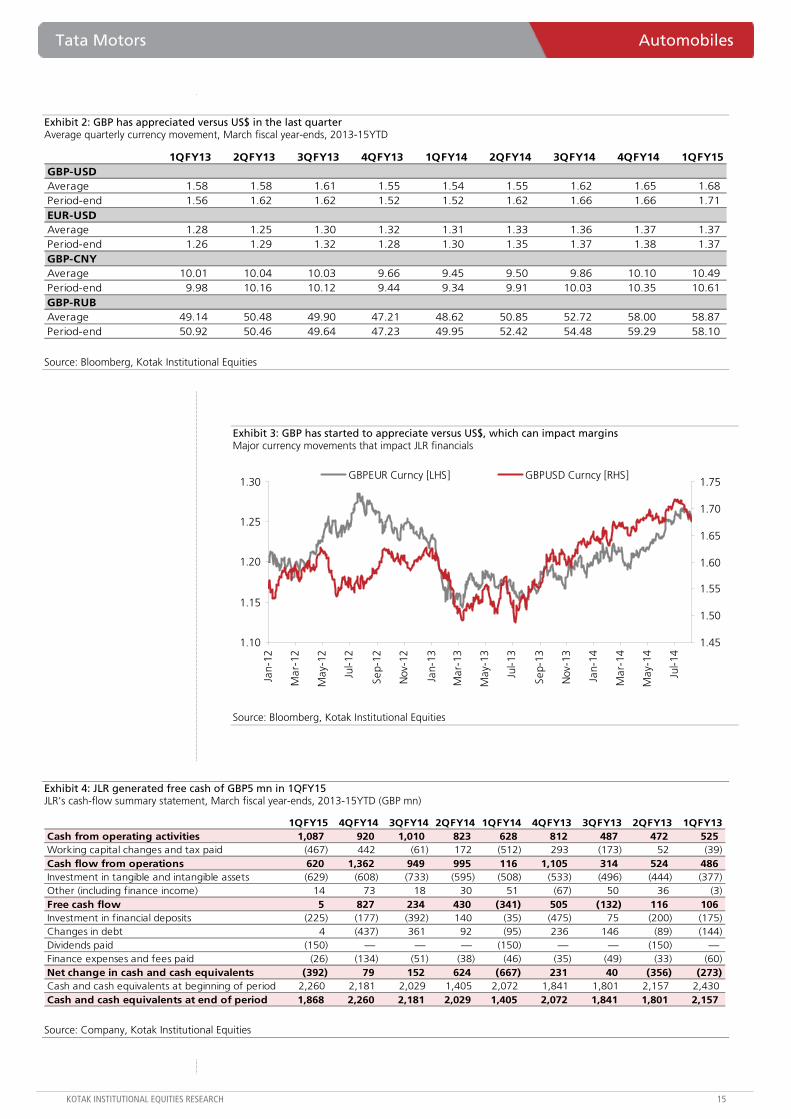

Exhibit 2: GBP has appreciated versus US$ in the last quarter Average quarterly currency movement, March fiscal year-ends, 2013-15YTD

1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15GBP-USDAverage 1.58 1.58 1.61 1.55 1.54 1.55 1.62 1.65 1.68 Period-end 1.56 1.62 1.62 1.52 1.52 1.62 1.66 1.66 1.71 EUR-USDAverage 1.28 1.25 1.30 1.32 1.31 1.33 1.36 1.37 1.37 Period-end 1.26 1.29 1.32 1.28 1.30 1.35 1.37 1.38 1.37 GBP-CNYAverage 10.01 10.04 10.03 9.66 9.45 9.50 9.86 10.10 10.49 Period-end 9.98 10.16 10.12 9.44 9.34 9.91 10.03 10.35 10.61 GBP-RUBAverage 49.14 50.48 49.90 47.21 48.62 50.85 52.72 58.00 58.87 Period-end 50.92 50.46 49.64 47.23 49.95 52.42 54.48 59.29 58.10

Source: Bloomberg, Kotak Institutional Equities

Exhibit 3: GBP has started to appreciate versus US$, which can impact margins Major currency movements that impact JLR financials

1.10

1.15

1.20

1.25

1.30

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

1.45

1.50

1.55

1.60

1.65

1.70

1.75GBPEUR Curncy [LHS] GBPUSD Curncy [RHS]

Source: Bloomberg, Kotak Institutional Equities

Exhibit 4: JLR generated free cash of GBP5 mn in 1QFY15 JLR's cash-flow summary statement, March fiscal year-ends, 2013-15YTD (GBP mn)

1QFY15 4QFY14 3QFY14 2QFY14 1QFY14 4QFY13 3QFY13 2QFY13 1QFY13Cash from operating activities 1,087 920 1,010 823 628 812 487 472 525 Working capital changes and tax paid (467) 442 (61) 172 (512) 293 (173) 52 (39) Cash flow from operations 620 1,362 949 995 116 1,105 314 524 486 Investment in tangible and intangible assets (629) (608) (733) (595) (508) (533) (496) (444) (377) Other (including finance income) 14 73 18 30 51 (67) 50 36 (3) Free cash flow 5 827 234 430 (341) 505 (132) 116 106 Investment in financial deposits (225) (177) (392) 140 (35) (475) 75 (200) (175) Changes in debt 4 (437) 361 92 (95) 236 146 (89) (144) Dividends paid (150) — — — (150) — — (150) —Finance expenses and fees paid (26) (134) (51) (38) (46) (35) (49) (33) (60) Net change in cash and cash equivalents (392) 79 152 624 (667) 231 40 (356) (273) Cash and cash equivalents at beginning of period 2,260 2,181 2,029 1,405 2,072 1,841 1,801 2,157 2,430 Cash and cash equivalents at end of period 1,868 2,260 2,181 2,029 1,405 2,072 1,841 1,801 2,157

Source: Company, Kotak Institutional Equities

Automobiles Tata Motors

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 5: JLR expensed only ~16% of R&D in P&L in 1QFY15 Break-up of JLR R&D and capex spend, March fiscal year-ends, 2013-15YTD (GBP mn)

1QFY15 4QFY14 3QFY14 2QFY14 1QFY14 4QFY13 3QFY13 2QFY13 1QFY13R&D expenseCapitalized 273 258 271 259 242 198 229 218 215 Expensed 53 69 55 62 50 54 46 51 47 Total R&D expense 326 327 326 321 292 252 275 269 262 Investment in tangible and other intangible assets 356 350 462 336 266 335 267 226 162 Total product and other investment 682 677 788 657 558 587 542 488 424 R&D capitalized as % of total R&D 83.7 78.9 83.1 80.7 82.9 78.6 83.3 81.0 82.1

Source: Company, Kotak Institutional Equities

Exhibit 6: China share will continue to grow in the product mix Geography-wise volume mix, March fiscal year-ends, 2012-17E (units, %)

2012 2013 2014 2015E 2016E 2017EGeographyN.A 58,327 64,939 71,385 76,680 98,680 108,548 UK 61,796 68,028 75,856 76,000 96,000 105,600 Europe (excl Russia and UK) 71,580 78,809 82,711 70,000 90,000 94,500 Russia 15,201 16,721 13,000 14,040 21,040 24,196 China 54,532 79,458 103,910 124,800 176,800 231,520 Asia Pac (excl China) 14,467 18,280 22,693 27,600 32,600 37,600 Rest of World 38,530 45,827 60,306 95,600 107,089 85,030 Total Volumes 314,433 372,062 429,861 484,720 622,209 686,994 Yoy growth (%) 29.1 18.3 15.5 12.8 28.4 10.4 Geographical mix (%)N.A 18.5 17.5 16.6 15.8 15.9 15.8 UK 19.7 18.3 17.6 15.7 15.4 15.4 Europe (excl Russia and UK) 22.8 21.2 19.2 14.4 14.5 13.8 Russia 4.8 4.5 3.0 2.9 3.4 3.5 China 17.3 21.4 24.2 25.7 28.4 33.7 Asia Pac (excl China) 4.6 4.9 5.3 5.7 5.2 5.5 Rest of World 12.3 12.3 14.0 19.7 17.2 12.4 Total Volumes 100 100 100 100 100 100

Source: Company, Kotak Institutional Equities estimates

Tata Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

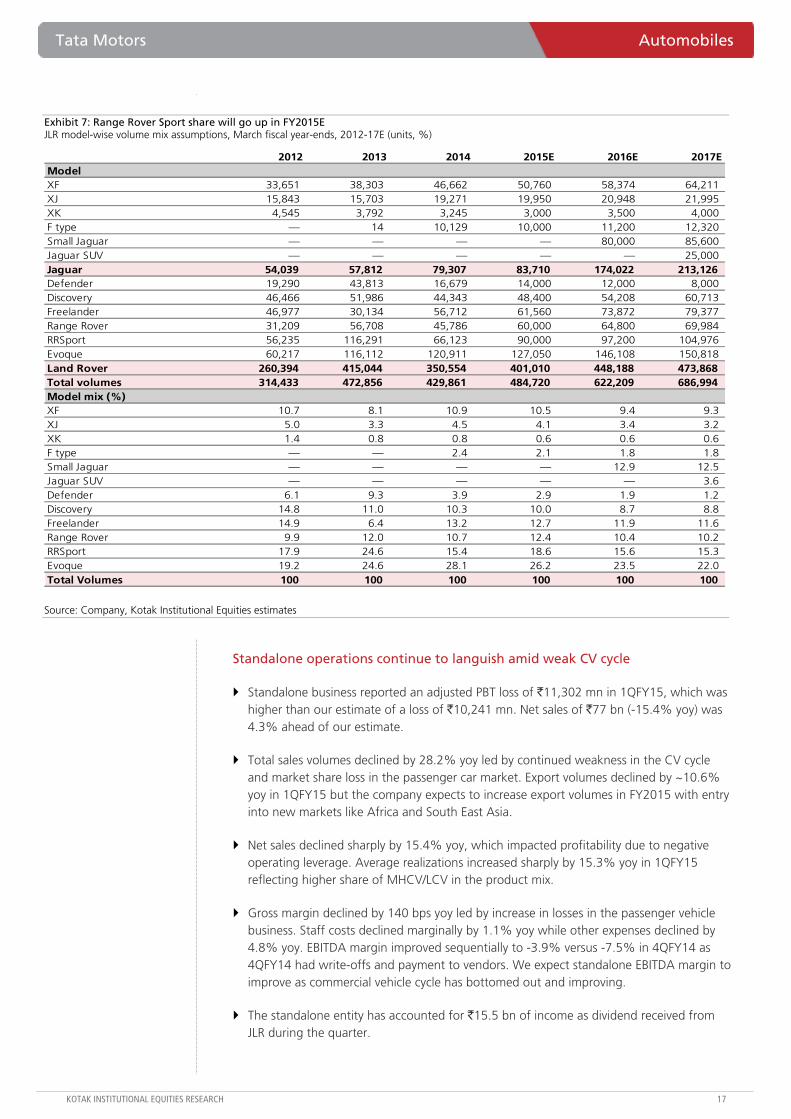

Exhibit 7: Range Rover Sport share will go up in FY2015E JLR model-wise volume mix assumptions, March fiscal year-ends, 2012-17E (units, %)

2012 2013 2014 2015E 2016E 2017EModelXF 33,651 38,303 46,662 50,760 58,374 64,211 XJ 15,843 15,703 19,271 19,950 20,948 21,995 XK 4,545 3,792 3,245 3,000 3,500 4,000 F type — 14 10,129 10,000 11,200 12,320 Small Jaguar — — — — 80,000 85,600 Jaguar SUV — — — — — 25,000 Jaguar 54,039 57,812 79,307 83,710 174,022 213,126 Defender 19,290 43,813 16,679 14,000 12,000 8,000 Discovery 46,466 51,986 44,343 48,400 54,208 60,713 Freelander 46,977 30,134 56,712 61,560 73,872 79,377 Range Rover 31,209 56,708 45,786 60,000 64,800 69,984 RRSport 56,235 116,291 66,123 90,000 97,200 104,976 Evoque 60,217 116,112 120,911 127,050 146,108 150,818 Land Rover 260,394 415,044 350,554 401,010 448,188 473,868 Total volumes 314,433 472,856 429,861 484,720 622,209 686,994 Model mix (%)XF 10.7 8.1 10.9 10.5 9.4 9.3 XJ 5.0 3.3 4.5 4.1 3.4 3.2 XK 1.4 0.8 0.8 0.6 0.6 0.6 F type — — 2.4 2.1 1.8 1.8 Small Jaguar — — — — 12.9 12.5 Jaguar SUV — — — — — 3.6 Defender 6.1 9.3 3.9 2.9 1.9 1.2 Discovery 14.8 11.0 10.3 10.0 8.7 8.8 Freelander 14.9 6.4 13.2 12.7 11.9 11.6 Range Rover 9.9 12.0 10.7 12.4 10.4 10.2 RRSport 17.9 24.6 15.4 18.6 15.6 15.3 Evoque 19.2 24.6 28.1 26.2 23.5 22.0 Total Volumes 100 100 100 100 100 100

Source: Company, Kotak Institutional Equities estimates

Standalone operations continue to languish amid weak CV cycle

Standalone business reported an adjusted PBT loss of `11,302 mn in 1QFY15, which was higher than our estimate of a loss of `10,241 mn. Net sales of `77 bn (-15.4% yoy) was 4.3% ahead of our estimate.

Total sales volumes declined by 28.2% yoy led by continued weakness in the CV cycle and market share loss in the passenger car market. Export volumes declined by ~10.6% yoy in 1QFY15 but the company expects to increase export volumes in FY2015 with entry into new markets like Africa and South East Asia.

Net sales declined sharply by 15.4% yoy, which impacted profitability due to negative operating leverage. Average realizations increased sharply by 15.3% yoy in 1QFY15 reflecting higher share of MHCV/LCV in the product mix.

Gross margin declined by 140 bps yoy led by increase in losses in the passenger vehicle business. Staff costs declined marginally by 1.1% yoy while other expenses declined by 4.8% yoy. EBITDA margin improved sequentially to -3.9% versus -7.5% in 4QFY14 as 4QFY14 had write-offs and payment to vendors. We expect standalone EBITDA margin to improve as commercial vehicle cycle has bottomed out and improving.

The standalone entity has accounted for `15.5 bn of income as dividend received from JLR during the quarter.

Automobiles Tata Motors

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

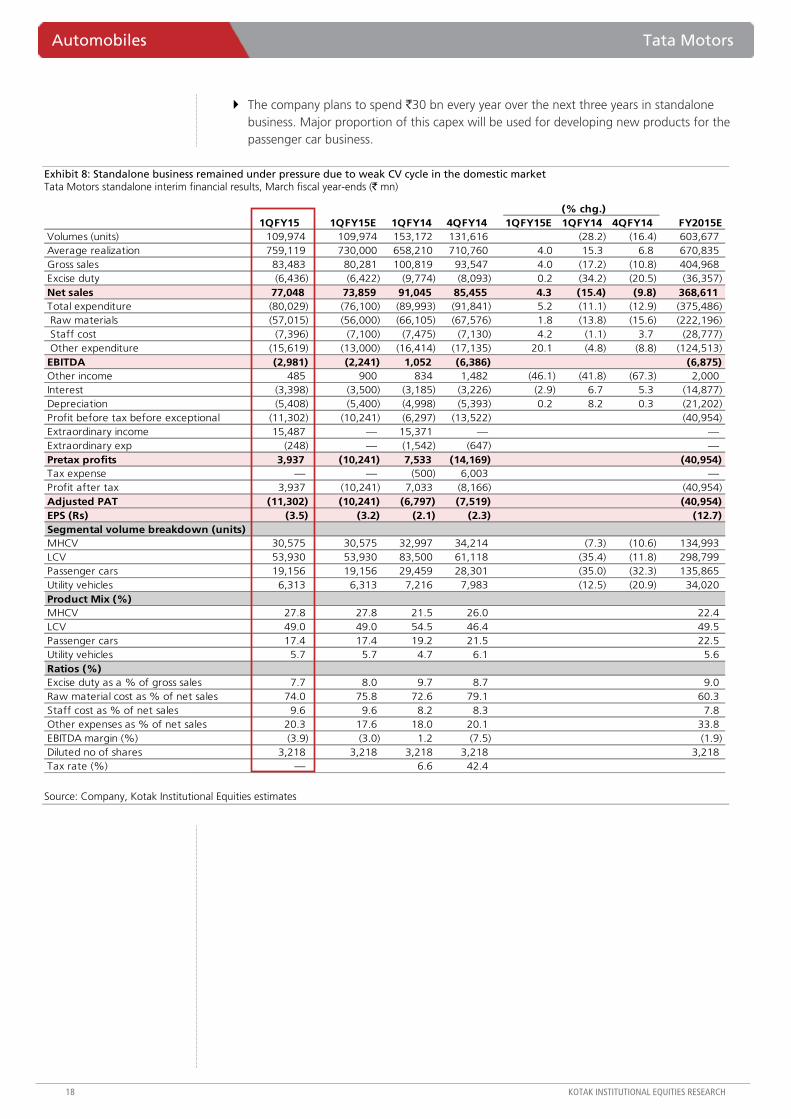

The company plans to spend `30 bn every year over the next three years in standalone business. Major proportion of this capex will be used for developing new products for the passenger car business.

Exhibit 8: Standalone business remained under pressure due to weak CV cycle in the domestic market Tata Motors standalone interim financial results, March fiscal year-ends (` mn)

(% chg.)1QFY15 1QFY15E 1QFY14 4QFY14 1QFY15E 1QFY14 4QFY14 FY2015E

Volumes (units) 109,974 109,974 153,172 131,616 (28.2) (16.4) 603,677 Average realization 759,119 730,000 658,210 710,760 4.0 15.3 6.8 670,835 Gross sales 83,483 80,281 100,819 93,547 4.0 (17.2) (10.8) 404,968 Excise duty (6,436) (6,422) (9,774) (8,093) 0.2 (34.2) (20.5) (36,357) Net sales 77,048 73,859 91,045 85,455 4.3 (15.4) (9.8) 368,611 Total expenditure (80,029) (76,100) (89,993) (91,841) 5.2 (11.1) (12.9) (375,486) Raw materials (57,015) (56,000) (66,105) (67,576) 1.8 (13.8) (15.6) (222,196) Staff cost (7,396) (7,100) (7,475) (7,130) 4.2 (1.1) 3.7 (28,777) Other expenditure (15,619) (13,000) (16,414) (17,135) 20.1 (4.8) (8.8) (124,513) EBITDA (2,981) (2,241) 1,052 (6,386) (6,875) Other income 485 900 834 1,482 (46.1) (41.8) (67.3) 2,000 Interest (3,398) (3,500) (3,185) (3,226) (2.9) 6.7 5.3 (14,877) Depreciation (5,408) (5,400) (4,998) (5,393) 0.2 8.2 0.3 (21,202) Profit before tax before exceptional (11,302) (10,241) (6,297) (13,522) (40,954) Extraordinary income 15,487 — 15,371 — —Extraordinary exp (248) — (1,542) (647) —Pretax profits 3,937 (10,241) 7,533 (14,169) (40,954) Tax expense — — (500) 6,003 —Profit after tax 3,937 (10,241) 7,033 (8,166) (40,954) Adjusted PAT (11,302) (10,241) (6,797) (7,519) (40,954) EPS (Rs) (3.5) (3.2) (2.1) (2.3) (12.7) Segmental volume breakdown (units)MHCV 30,575 30,575 32,997 34,214 (7.3) (10.6) 134,993 LCV 53,930 53,930 83,500 61,118 (35.4) (11.8) 298,799 Passenger cars 19,156 19,156 29,459 28,301 (35.0) (32.3) 135,865 Utility vehicles 6,313 6,313 7,216 7,983 (12.5) (20.9) 34,020 Product Mix (%)MHCV 27.8 27.8 21.5 26.0 22.4 LCV 49.0 49.0 54.5 46.4 49.5 Passenger cars 17.4 17.4 19.2 21.5 22.5 Utility vehicles 5.7 5.7 4.7 6.1 5.6 Ratios (%)Excise duty as a % of gross sales 7.7 8.0 9.7 8.7 9.0 Raw material cost as % of net sales 74.0 75.8 72.6 79.1 60.3 Staff cost as % of net sales 9.6 9.6 8.2 8.3 7.8 Other expenses as % of net sales 20.3 17.6 18.0 20.1 33.8 EBITDA margin (%) (3.9) (3.0) 1.2 (7.5) (1.9) Diluted no of shares 3,218 3,218 3,218 3,218 3,218 Tax rate (%) — 6.6 42.4

Source: Company, Kotak Institutional Equities estimates

Tata Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

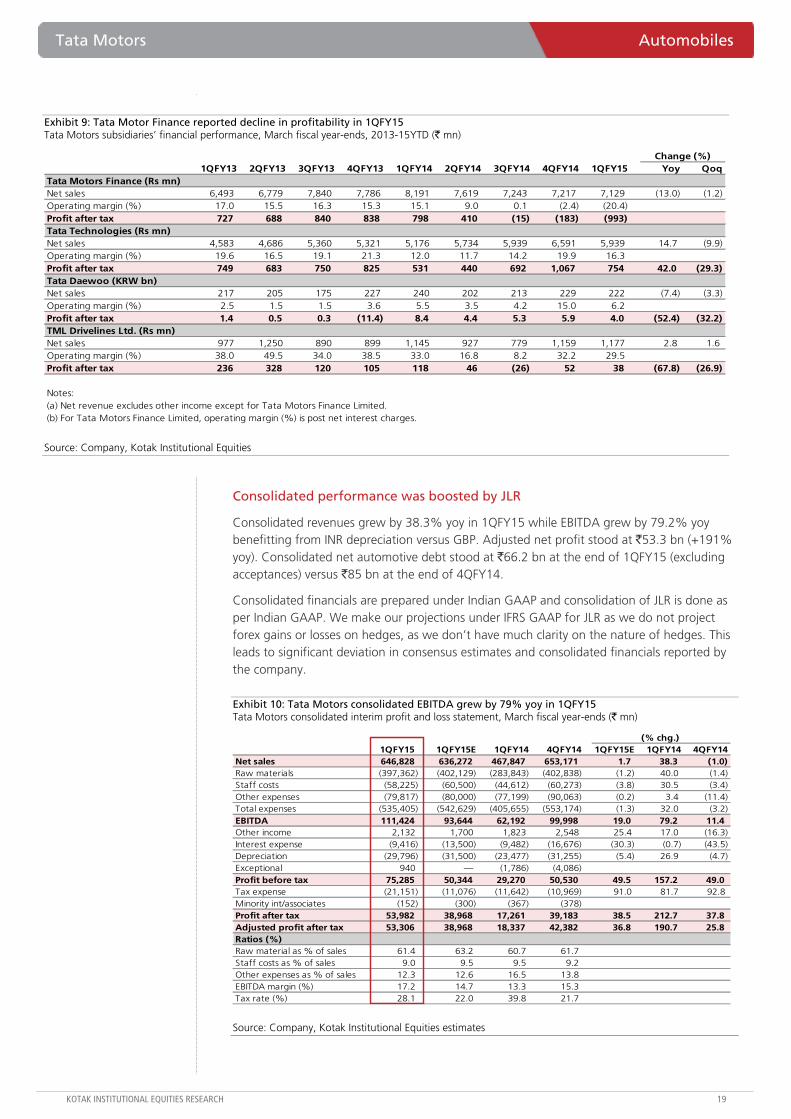

Exhibit 9: Tata Motor Finance reported decline in profitability in 1QFY15 Tata Motors subsidiaries’ financial performance, March fiscal year-ends, 2013-15YTD (` mn)

Change (%)1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15 Yoy Qoq

Tata Motors Finance (Rs mn)Net sales 6,493 6,779 7,840 7,786 8,191 7,619 7,243 7,217 7,129 (13.0) (1.2) Operating margin (%) 17.0 15.5 16.3 15.3 15.1 9.0 0.1 (2.4) (20.4) Profit after tax 727 688 840 838 798 410 (15) (183) (993) Tata Technologies (Rs mn)Net sales 4,583 4,686 5,360 5,321 5,176 5,734 5,939 6,591 5,939 14.7 (9.9) Operating margin (%) 19.6 16.5 19.1 21.3 12.0 11.7 14.2 19.9 16.3 Profit after tax 749 683 750 825 531 440 692 1,067 754 42.0 (29.3) Tata Daewoo (KRW bn)Net sales 217 205 175 227 240 202 213 229 222 (7.4) (3.3) Operating margin (%) 2.5 1.5 1.5 3.6 5.5 3.5 4.2 15.0 6.2 Profit after tax 1.4 0.5 0.3 (11.4) 8.4 4.4 5.3 5.9 4.0 (52.4) (32.2) TML Drivelines Ltd. (Rs mn)Net sales 977 1,250 890 899 1,145 927 779 1,159 1,177 2.8 1.6 Operating margin (%) 38.0 49.5 34.0 38.5 33.0 16.8 8.2 32.2 29.5 Profit after tax 236 328 120 105 118 46 (26) 52 38 (67.8) (26.9)

Notes:(a) Net revenue excludes other income except for Tata Motors Finance Limited.(b) For Tata Motors Finance Limited, operating margin (%) is post net interest charges.

Source: Company, Kotak Institutional Equities

Consolidated performance was boosted by JLR

Consolidated revenues grew by 38.3% yoy in 1QFY15 while EBITDA grew by 79.2% yoy benefitting from INR depreciation versus GBP. Adjusted net profit stood at `53.3 bn (+191% yoy). Consolidated net automotive debt stood at `66.2 bn at the end of 1QFY15 (excluding acceptances) versus `85 bn at the end of 4QFY14.

Consolidated financials are prepared under Indian GAAP and consolidation of JLR is done as per Indian GAAP. We make our projections under IFRS GAAP for JLR as we do not project forex gains or losses on hedges, as we don’t have much clarity on the nature of hedges. This leads to significant deviation in consensus estimates and consolidated financials reported by the company.

Exhibit 10: Tata Motors consolidated EBITDA grew by 79% yoy in 1QFY15 Tata Motors consolidated interim profit and loss statement, March fiscal year-ends (` mn)

(% chg.)1QFY15 1QFY15E 1QFY14 4QFY14 1QFY15E 1QFY14 4QFY14

Net sales 646,828 636,272 467,847 653,171 1.7 38.3 (1.0) Raw materials (397,362) (402,129) (283,843) (402,838) (1.2) 40.0 (1.4) Staff costs (58,225) (60,500) (44,612) (60,273) (3.8) 30.5 (3.4) Other expenses (79,817) (80,000) (77,199) (90,063) (0.2) 3.4 (11.4) Total expenses (535,405) (542,629) (405,655) (553,174) (1.3) 32.0 (3.2) EBITDA 111,424 93,644 62,192 99,998 19.0 79.2 11.4 Other income 2,132 1,700 1,823 2,548 25.4 17.0 (16.3) Interest expense (9,416) (13,500) (9,482) (16,676) (30.3) (0.7) (43.5) Depreciation (29,796) (31,500) (23,477) (31,255) (5.4) 26.9 (4.7) Exceptional 940 — (1,786) (4,086) Profit before tax 75,285 50,344 29,270 50,530 49.5 157.2 49.0 Tax expense (21,151) (11,076) (11,642) (10,969) 91.0 81.7 92.8 Minority int/associates (152) (300) (367) (378) Profit after tax 53,982 38,968 17,261 39,183 38.5 212.7 37.8 Adjusted profit after tax 53,306 38,968 18,337 42,382 36.8 190.7 25.8 Ratios (%)Raw material as % of sales 61.4 63.2 60.7 61.7 Staff costs as % of sales 9.0 9.5 9.5 9.2 Other expenses as % of sales 12.3 12.6 16.5 13.8 EBITDA margin (%) 17.2 14.7 13.3 15.3 Tax rate (%) 28.1 22.0 39.8 21.7

Source: Company, Kotak Institutional Equities estimates

Automobiles Tata Motors

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

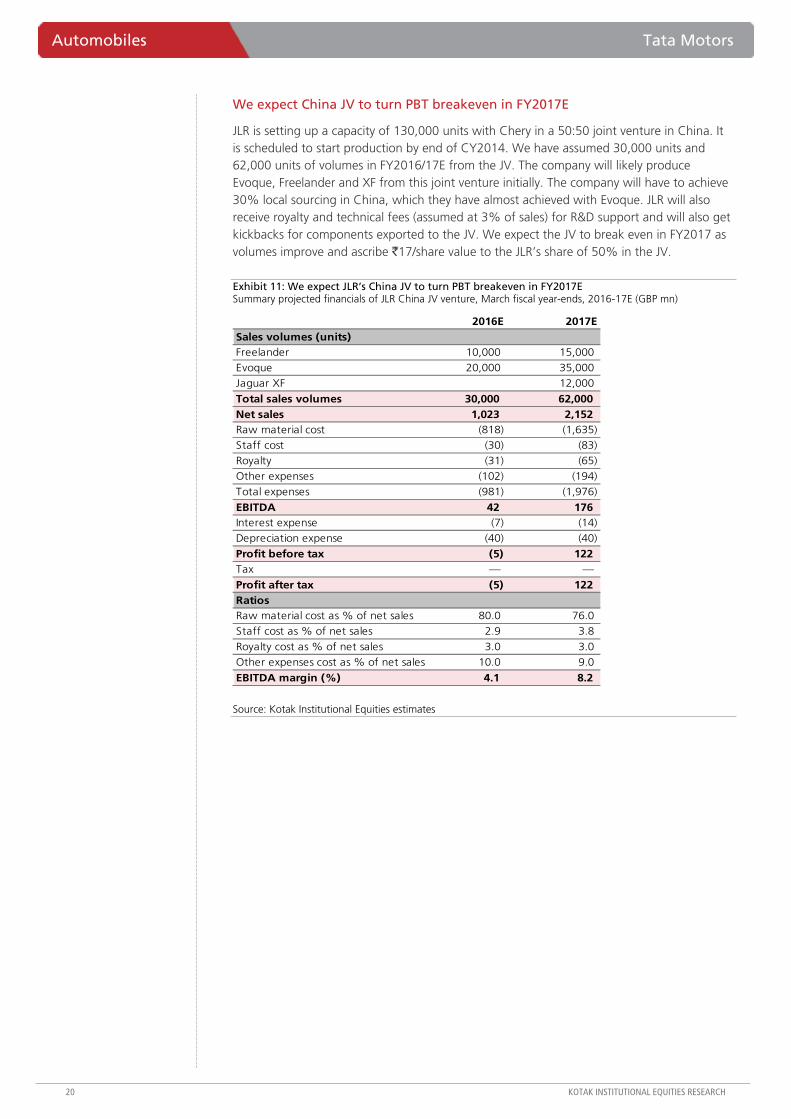

We expect China JV to turn PBT breakeven in FY2017E

JLR is setting up a capacity of 130,000 units with Chery in a 50:50 joint venture in China. It is scheduled to start production by end of CY2014. We have assumed 30,000 units and 62,000 units of volumes in FY2016/17E from the JV. The company will likely produce Evoque, Freelander and XF from this joint venture initially. The company will have to achieve 30% local sourcing in China, which they have almost achieved with Evoque. JLR will also receive royalty and technical fees (assumed at 3% of sales) for R&D support and will also get kickbacks for components exported to the JV. We expect the JV to break even in FY2017 as volumes improve and ascribe `17/share value to the JLR’s share of 50% in the JV.

Exhibit 11: We expect JLR’s China JV to turn PBT breakeven in FY2017E Summary projected financials of JLR China JV venture, March fiscal year-ends, 2016-17E (GBP mn)

2016E 2017ESales volumes (units)Freelander 10,000 15,000

Evoque 20,000 35,000

Jaguar XF 12,000

Total sales volumes 30,000 62,000 Net sales 1,023 2,152 Raw material cost (818) (1,635)

Staff cost (30) (83)

Royalty (31) (65)

Other expenses (102) (194)

Total expenses (981) (1,976)

EBITDA 42 176 Interest expense (7) (14)

Depreciation expense (40) (40)

Profit before tax (5) 122 Tax — —

Profit after tax (5) 122 RatiosRaw material cost as % of net sales 80.0 76.0

Staff cost as % of net sales 2.9 3.8

Royalty cost as % of net sales 3.0 3.0

Other expenses cost as % of net sales 10.0 9.0

EBITDA margin (%) 4.1 8.2

Source: Kotak Institutional Equities estimates

Tata Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

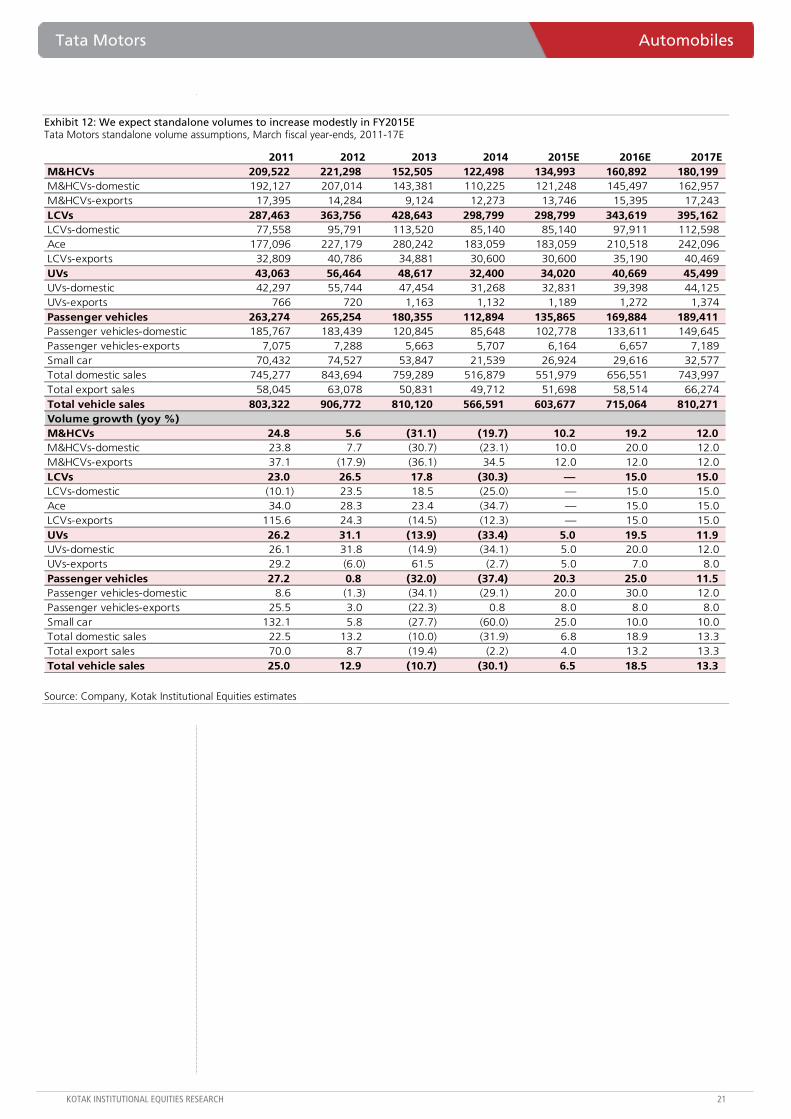

Exhibit 12: We expect standalone volumes to increase modestly in FY2015E Tata Motors standalone volume assumptions, March fiscal year-ends, 2011-17E

2011 2012 2013 2014 2015E 2016E 2017EM&HCVs 209,522 221,298 152,505 122,498 134,993 160,892 180,199 M&HCVs-domestic 192,127 207,014 143,381 110,225 121,248 145,497 162,957 M&HCVs-exports 17,395 14,284 9,124 12,273 13,746 15,395 17,243 LCVs 287,463 363,756 428,643 298,799 298,799 343,619 395,162 LCVs-domestic 77,558 95,791 113,520 85,140 85,140 97,911 112,598 Ace 177,096 227,179 280,242 183,059 183,059 210,518 242,096 LCVs-exports 32,809 40,786 34,881 30,600 30,600 35,190 40,469 UVs 43,063 56,464 48,617 32,400 34,020 40,669 45,499 UVs-domestic 42,297 55,744 47,454 31,268 32,831 39,398 44,125 UVs-exports 766 720 1,163 1,132 1,189 1,272 1,374 Passenger vehicles 263,274 265,254 180,355 112,894 135,865 169,884 189,411 Passenger vehicles-domestic 185,767 183,439 120,845 85,648 102,778 133,611 149,645 Passenger vehicles-exports 7,075 7,288 5,663 5,707 6,164 6,657 7,189 Small car 70,432 74,527 53,847 21,539 26,924 29,616 32,577 Total domestic sales 745,277 843,694 759,289 516,879 551,979 656,551 743,997 Total export sales 58,045 63,078 50,831 49,712 51,698 58,514 66,274 Total vehicle sales 803,322 906,772 810,120 566,591 603,677 715,064 810,271 Volume growth (yoy %)M&HCVs 24.8 5.6 (31.1) (19.7) 10.2 19.2 12.0 M&HCVs-domestic 23.8 7.7 (30.7) (23.1) 10.0 20.0 12.0 M&HCVs-exports 37.1 (17.9) (36.1) 34.5 12.0 12.0 12.0 LCVs 23.0 26.5 17.8 (30.3) — 15.0 15.0 LCVs-domestic (10.1) 23.5 18.5 (25.0) — 15.0 15.0 Ace 34.0 28.3 23.4 (34.7) — 15.0 15.0 LCVs-exports 115.6 24.3 (14.5) (12.3) — 15.0 15.0 UVs 26.2 31.1 (13.9) (33.4) 5.0 19.5 11.9 UVs-domestic 26.1 31.8 (14.9) (34.1) 5.0 20.0 12.0 UVs-exports 29.2 (6.0) 61.5 (2.7) 5.0 7.0 8.0 Passenger vehicles 27.2 0.8 (32.0) (37.4) 20.3 25.0 11.5 Passenger vehicles-domestic 8.6 (1.3) (34.1) (29.1) 20.0 30.0 12.0 Passenger vehicles-exports 25.5 3.0 (22.3) 0.8 8.0 8.0 8.0 Small car 132.1 5.8 (27.7) (60.0) 25.0 10.0 10.0 Total domestic sales 22.5 13.2 (10.0) (31.9) 6.8 18.9 13.3 Total export sales 70.0 8.7 (19.4) (2.2) 4.0 13.2 13.3 Total vehicle sales 25.0 12.9 (10.7) (30.1) 6.5 18.5 13.3

Source: Company, Kotak Institutional Equities estimates

Automobiles Tata Motors

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 13: We have increased our consolidated EPS on higher margin assumptions for JLR Tata Motors earnings revision table, March fiscal year-ends, 2015-16E

New estimates Old estimates % change2015E 2016E 2015E 2016E 2015E 2016E

Standalone (Rs mn)Volumes (units) 603,677 715,064 603,677 715,064 Net sales 368,611 451,480 368,611 451,480 EBITDA (6,875) 23,731 (6,875) 23,731 EBITDA margin (%) (1.9) 5.3 (1.9) 5.3 Adjusted net profit (40,954) (14,873) (40,954) (14,873) EPS (12.7) (4.6) (12.7) (4.6) JLR (GBP mn)Volumes (units) 484,720 592,209 484,720 610,209 — (2.9) Average realization 46,759 45,250 47,915 45,472 (2.4) (0.5) Net sales 22,665 26,798 23,225 27,748 (2.4) (3.4) EBITDA 3,855 4,290 3,647 4,218 5.7 1.7 EBITDA margin (%) 17.0 16.0 15.7 15.2 Product development 288 296 288 296 Depreciation 1,175 1,475 1,175 1,475 Adjusted net profit 1,926 2,023 1,776 1,971 8.4 2.6 EPS (pound) 0.60 0.63 0.55 0.61 8.4 2.6 Consolidated (Rs mn)Net sales 2,700,113 3,209,235 2,756,157 3,304,233 (2.0) (2.9) EBITDA 403,587 488,123 382,812 476,792 5.4 2.4 EBITDA margin (%) 14.9 15.2 13.9 14.4 Adjusted net profit 154,869 199,455 139,911 190,671 10.7 4.6 EPS 48.1 62.0 43.5 59.3 10.7 4.6 GBPINR 100.0 100.0 100.0 100.0 — —

Source: Kotak Institutional Equities estimates

Exhibit 14: We value Tata Motors at `590/share based on SOTP methodology Tata Motors SOTP-based valuation, March fiscal year-ends

EBITDA Multiple ValueValue per

share

(Rs mn) (X) (Rs mn) (Rs) CommentsTata Motors standalone EV 41,453 9.0 373,075 118 based on 9X EV/EBITDA on March 2016

JLR standalone EV 358,981 4.3 1,525,667 481 based on 4.25X 12-month March 2016, deducting 1000 mn pounds of R&D expense from reported EBITDA

China JV valuation 17 Based on 7X EV/EBITDA March 2017 discounted by WACC (50% stake of JLR)

Less: Net debt - consol 156,430 49 ex vehicle financing debt includes acceptances

Total standalone + JLR 566

Value of subsidiaries 25

SOTP-based value 591

Target price 590

Notes:

(a) We have valued the subsidiaries after considering 20% holding company discount.

Source: Kotak Institutional Equities estimates

Tata Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 23

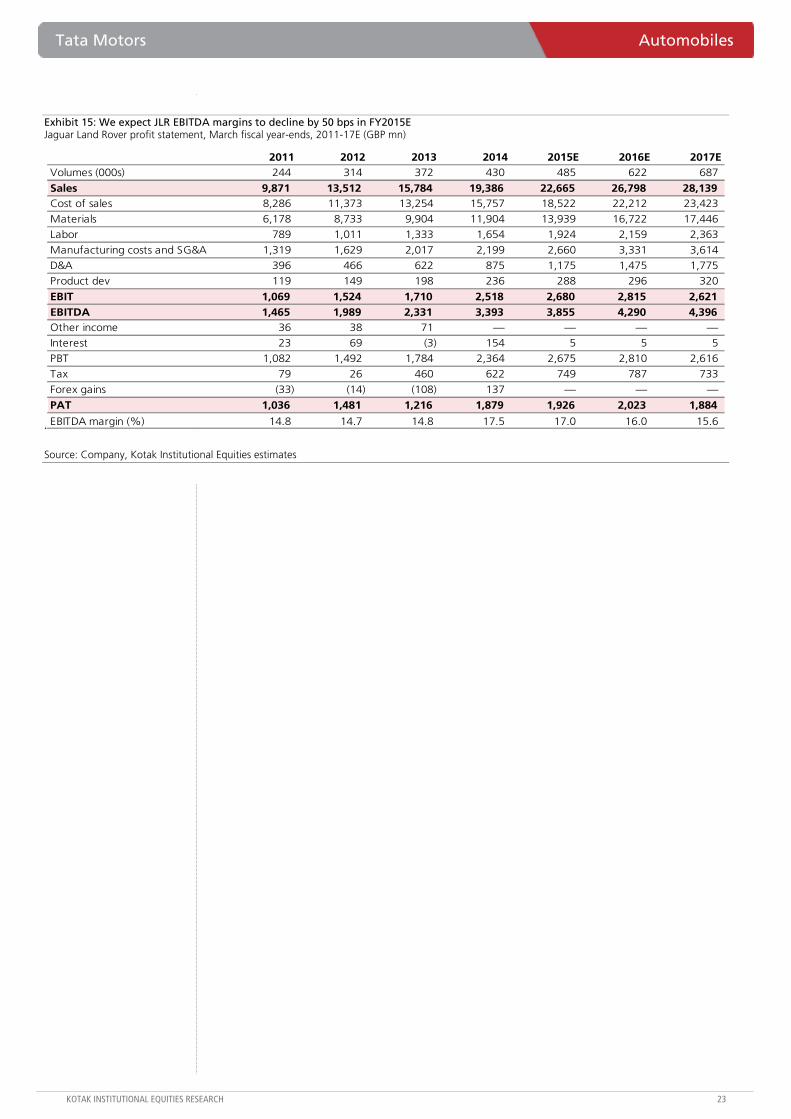

Exhibit 15: We expect JLR EBITDA margins to decline by 50 bps in FY2015E Jaguar Land Rover profit statement, March fiscal year-ends, 2011-17E (GBP mn)

.

2011 2012 2013 2014 2015E 2016E 2017EVolumes (000s) 244 314 372 430 485 622 687

Sales 9,871 13,512 15,784 19,386 22,665 26,798 28,139 Cost of sales 8,286 11,373 13,254 15,757 18,522 22,212 23,423

Materials 6,178 8,733 9,904 11,904 13,939 16,722 17,446

Labor 789 1,011 1,333 1,654 1,924 2,159 2,363

Manufacturing costs and SG&A 1,319 1,629 2,017 2,199 2,660 3,331 3,614

D&A 396 466 622 875 1,175 1,475 1,775

Product dev 119 149 198 236 288 296 320

EBIT 1,069 1,524 1,710 2,518 2,680 2,815 2,621 EBITDA 1,465 1,989 2,331 3,393 3,855 4,290 4,396 Other income 36 38 71 — — — —

Interest 23 69 (3) 154 5 5 5

PBT 1,082 1,492 1,784 2,364 2,675 2,810 2,616

Tax 79 26 460 622 749 787 733

Forex gains (33) (14) (108) 137 — — —

PAT 1,036 1,481 1,216 1,879 1,926 2,023 1,884

EBITDA margin (%) 14.8 14.7 14.8 17.5 17.0 16.0 15.6

Source: Company, Kotak Institutional Equities estimates

Automobiles Tata Motors

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

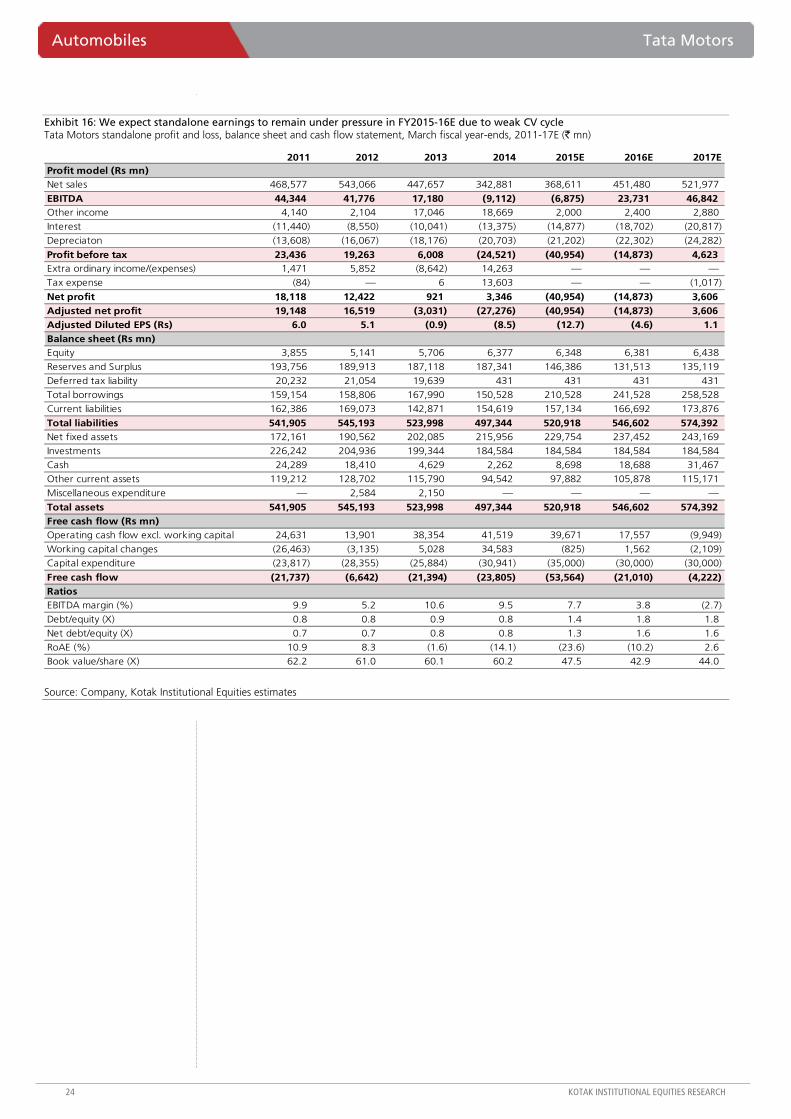

Exhibit 16: We expect standalone earnings to remain under pressure in FY2015-16E due to weak CV cycle Tata Motors standalone profit and loss, balance sheet and cash flow statement, March fiscal year-ends, 2011-17E (` mn)

2011 2012 2013 2014 2015E 2016E 2017EProfit model (Rs mn)Net sales 468,577 543,066 447,657 342,881 368,611 451,480 521,977

EBITDA 44,344 41,776 17,180 (9,112) (6,875) 23,731 46,842 Other income 4,140 2,104 17,046 18,669 2,000 2,400 2,880

Interest (11,440) (8,550) (10,041) (13,375) (14,877) (18,702) (20,817)

Depreciaton (13,608) (16,067) (18,176) (20,703) (21,202) (22,302) (24,282)

Profit before tax 23,436 19,263 6,008 (24,521) (40,954) (14,873) 4,623 Extra ordinary income/(expenses) 1,471 5,852 (8,642) 14,263 — — —

Tax expense (84) — 6 13,603 — — (1,017)

Net profit 18,118 12,422 921 3,346 (40,954) (14,873) 3,606 Adjusted net profit 19,148 16,519 (3,031) (27,276) (40,954) (14,873) 3,606 Adjusted Diluted EPS (Rs) 6.0 5.1 (0.9) (8.5) (12.7) (4.6) 1.1 Balance sheet (Rs mn)Equity 3,855 5,141 5,706 6,377 6,348 6,381 6,438

Reserves and Surplus 193,756 189,913 187,118 187,341 146,386 131,513 135,119

Deferred tax liability 20,232 21,054 19,639 431 431 431 431 Total borrowings 159,154 158,806 167,990 150,528 210,528 241,528 258,528

Current liabilities 162,386 169,073 142,871 154,619 157,134 166,692 173,876

Total liabilities 541,905 545,193 523,998 497,344 520,918 546,602 574,392 Net fixed assets 172,161 190,562 202,085 215,956 229,754 237,452 243,169

Investments 226,242 204,936 199,344 184,584 184,584 184,584 184,584 Cash 24,289 18,410 4,629 2,262 8,698 18,688 31,467

Other current assets 119,212 128,702 115,790 94,542 97,882 105,878 115,171

Miscellaneous expenditure — 2,584 2,150 — — — —

Total assets 541,905 545,193 523,998 497,344 520,918 546,602 574,392 Free cash flow (Rs mn)Operating cash flow excl. working capital 24,631 13,901 38,354 41,519 39,671 17,557 (9,949)

Working capital changes (26,463) (3,135) 5,028 34,583 (825) 1,562 (2,109)

Capital expenditure (23,817) (28,355) (25,884) (30,941) (35,000) (30,000) (30,000)

Free cash flow (21,737) (6,642) (21,394) (23,805) (53,564) (21,010) (4,222) RatiosEBITDA margin (%) 9.9 5.2 10.6 9.5 7.7 3.8 (2.7)

Debt/equity (X) 0.8 0.8 0.9 0.8 1.4 1.8 1.8

Net debt/equity (X) 0.7 0.7 0.8 0.8 1.3 1.6 1.6

RoAE (%) 10.9 8.3 (1.6) (14.1) (23.6) (10.2) 2.6 Book value/share (X) 62.2 61.0 60.1 60.2 47.5 42.9 44.0

Source: Company, Kotak Institutional Equities estimates

Tata Motors Automobiles

KOTAK INSTITUTIONAL EQUITIES RESEARCH 25

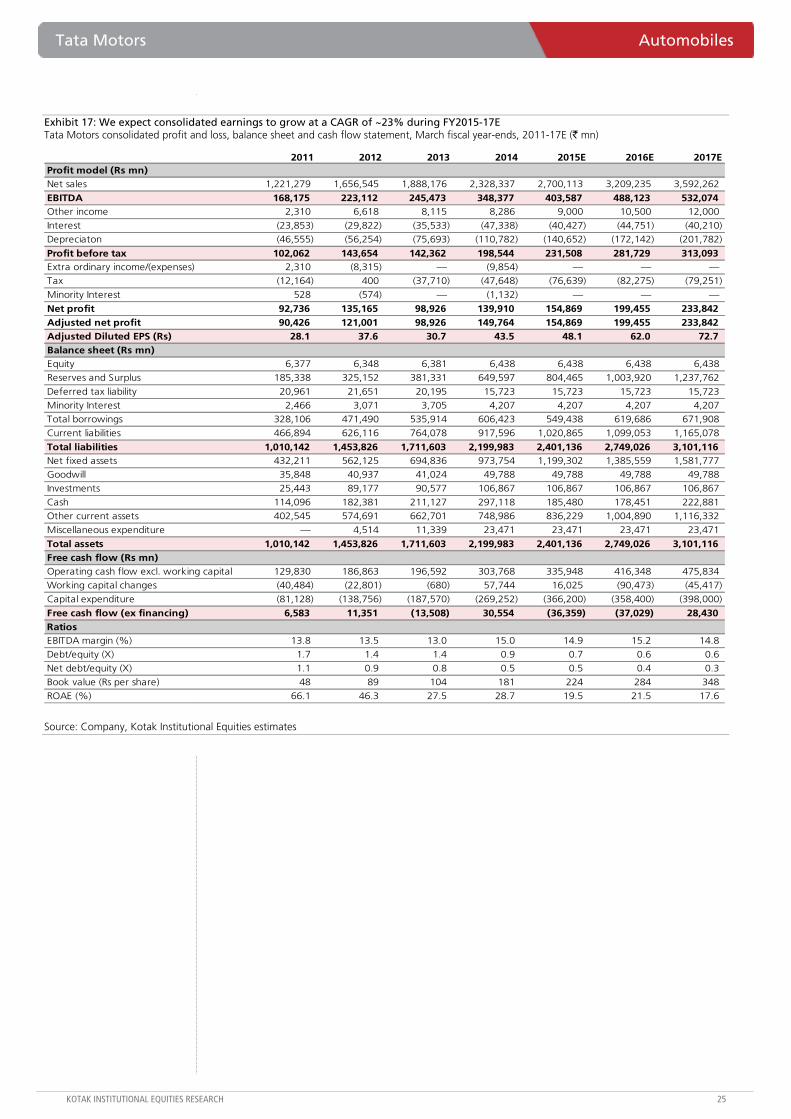

Exhibit 17: We expect consolidated earnings to grow at a CAGR of ~23% during FY2015-17E Tata Motors consolidated profit and loss, balance sheet and cash flow statement, March fiscal year-ends, 2011-17E (` mn)

2011 2012 2013 2014 2015E 2016E 2017EProfit model (Rs mn)Net sales 1,221,279 1,656,545 1,888,176 2,328,337 2,700,113 3,209,235 3,592,262

EBITDA 168,175 223,112 245,473 348,377 403,587 488,123 532,074 Other income 2,310 6,618 8,115 8,286 9,000 10,500 12,000

Interest (23,853) (29,822) (35,533) (47,338) (40,427) (44,751) (40,210) Depreciaton (46,555) (56,254) (75,693) (110,782) (140,652) (172,142) (201,782)

Profit before tax 102,062 143,654 142,362 198,544 231,508 281,729 313,093 Extra ordinary income/(expenses) 2,310 (8,315) — (9,854) — — —Tax (12,164) 400 (37,710) (47,648) (76,639) (82,275) (79,251)

Minority Interest 528 (574) — (1,132) — — —

Net profit 92,736 135,165 98,926 139,910 154,869 199,455 233,842 Adjusted net profit 90,426 121,001 98,926 149,764 154,869 199,455 233,842 Adjusted Diluted EPS (Rs) 28.1 37.6 30.7 43.5 48.1 62.0 72.7 Balance sheet (Rs mn)Equity 6,377 6,348 6,381 6,438 6,438 6,438 6,438 Reserves and Surplus 185,338 325,152 381,331 649,597 804,465 1,003,920 1,237,762

Deferred tax liability 20,961 21,651 20,195 15,723 15,723 15,723 15,723 Minority Interest 2,466 3,071 3,705 4,207 4,207 4,207 4,207 Total borrowings 328,106 471,490 535,914 606,423 549,438 619,686 671,908

Current liabilities 466,894 626,116 764,078 917,596 1,020,865 1,099,053 1,165,078

Total liabilities 1,010,142 1,453,826 1,711,603 2,199,983 2,401,136 2,749,026 3,101,116 Net fixed assets 432,211 562,125 694,836 973,754 1,199,302 1,385,559 1,581,777 Goodwill 35,848 40,937 41,024 49,788 49,788 49,788 49,788 Investments 25,443 89,177 90,577 106,867 106,867 106,867 106,867

Cash 114,096 182,381 211,127 297,118 185,480 178,451 222,881 Other current assets 402,545 574,691 662,701 748,986 836,229 1,004,890 1,116,332

Miscellaneous expenditure — 4,514 11,339 23,471 23,471 23,471 23,471

Total assets 1,010,142 1,453,826 1,711,603 2,199,983 2,401,136 2,749,026 3,101,116 Free cash flow (Rs mn)Operating cash flow excl. working capital 129,830 186,863 196,592 303,768 335,948 416,348 475,834 Working capital changes (40,484) (22,801) (680) 57,744 16,025 (90,473) (45,417)

Capital expenditure (81,128) (138,756) (187,570) (269,252) (366,200) (358,400) (398,000)

Free cash flow (ex financing) 6,583 11,351 (13,508) 30,554 (36,359) (37,029) 28,430 RatiosEBITDA margin (%) 13.8 13.5 13.0 15.0 14.9 15.2 14.8 Debt/equity (X) 1.7 1.4 1.4 0.9 0.7 0.6 0.6

Net debt/equity (X) 1.1 0.9 0.8 0.5 0.5 0.4 0.3 Book value (Rs per share) 48 89 104 181 224 284 348

ROAE (%) 66.1 46.3 27.5 28.7 19.5 21.5 17.6

Source: Company, Kotak Institutional Equities estimates

For private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

EBITDA miss led by dismal trading margins; PAT boosted by other income and lower depreciation

GAIL’s adjusted EBITDA at `14.8 bn (+2.6% qoq and -2.1% yoy) in 1QFY15 was 10.5% below our estimate of `16.5 bn led by (1) lower adjusted EBIT of gas trading segment at `1.5 bn (-46% qoq) reflecting erosion of trading margins on short-term/spot LNG volumes and (2) lower EBIT of petrochemicals segment at `1.2 bn (-36% qoq) reflecting a decline in sales volume and higher raw material costs due to increase in LNG off-take. However, adjusted net income at `9.2 bn (-5% qoq and +14% yoy) was ahead of our expected `8.8 bn, aided by higher-than-expected other income and lower depreciation charges. The company accounted (1) `2.4 bn of impact in revenues from retrospective implementation of regulated pipeline tariffs and (2) `1.9 bn of under-recovery due to balancing of overall gas portfolio—GAIL’s management indicated that the company has already recouped the amount in July and will account it in 2QFY15 results.

Reiterate BUY rating noting uptick in volumes and potential upside from revision in tariffs

We see the recent correction in stock price (14% in past one month) as an opportunity to BUY the stock noting medium-term triggers from (1) uptick in gas transmission volumes and (2) potential upside from an upward revision in tariffs, if the regulator were to account reasonable/actual gas volumes versus normative assumptions of volume divisor currently being used for determination of pipeline tariffs. We highlight that the legal principles including issues of volume divisor, based on which tariffs have been determined by PNGRB, are sub judice before the Appellate Tribunal of Electricity. We believe the key negatives are reflecting in the stock price as (1) gas transmission volumes have bottomed out in 4QFY14, (2) tariffs for majority of GAIL’s gas pipelines have been regulated by PNGRB over the past few years and (3) our concerns on sustainability of trading margins have played out in 1QFY15, albeit sooner than expectations.

Modest revision in estimates

We have revised our FY2015-17E estimates to `33.8, `38.2 and `43.5 from `35.3, `38.5 and `43 to factor in (1) higher LPG and petchem prices reflecting our assumption of higher crude prices, (2) delays in gas price hike, (3) lower gas trading margins, (4) changes in depreciation calculations and (5) other minor changes. We have factored in higher prices of domestic gas for GAIL’s internal consumption from 3QFY15 and accordingly, assumed nil under-recovery from then on.

GAIL (India) (GAIL)

Energy

Key risks playing out; opportunity to BUY. GAIL reported weak results led by (1) dismal gas trading margins and (2) one-offs from implementation of regulated tariffs and under-recovery on balancing of gas portfolio; adjusted net income was modestly ahead of our estimates at `9.2 bn. Lower trading margins will impact profitability, but it has limited impact on our SOTP of GAIL, as we have been ascribing lower multiple to factor such a risk. Reiterate BUY with a revised TP of `500 (`520 previously).

GAIL (India)Stock data Forecasts/Valuations 2014 2015E 2016E

52-week range (Rs) (high,low) EPS (Rs) 32.6 33.8 38.2Market Cap. (Rs bn) 495.2 EPS growth (%) (9.4) 3.7 12.8

Shareholding pattern (%) P/E (X) 12.0 11.5 10.2Promoters 56.1 Sales (Rs bn) 575.1 823.0 910.4FIIs 17.4 Net profits (Rs bn) 41.4 42.9 48.4MFs 2.5 EBITDA (Rs bn) 76.0 78.7 90.3

Price performance (%) 1M 3M 12M EV/EBITDA (X) 7.0 6.8 5.6Absolute (14.3) 5.2 28.8 ROE (%) 13.9 12.9 13.1Rel. to BSE-30 (16.0) (5.2) (5.1) Div. Yield (%) 2.7 2.7 3.2

Company data and valuation summary

475-272

BUY

AUGUST 12, 2014

RESULT

Coverage view: Neutral

Price (`): 390

Target price (`): 500

BSE-30: 25,519

QUICK NUMBERS

• Gas transmission volumes at 97 mcm/d in 1QFY15; implied tariffs at `1/cu m

• Adjusted EBITDA of `14.8 bn versus reported `10.4 bn; adjusted net income of `9.2 bn versus reported `6.2 bn

• Stock trading at 10X FY2016E EPS

GAIL (India) Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 27

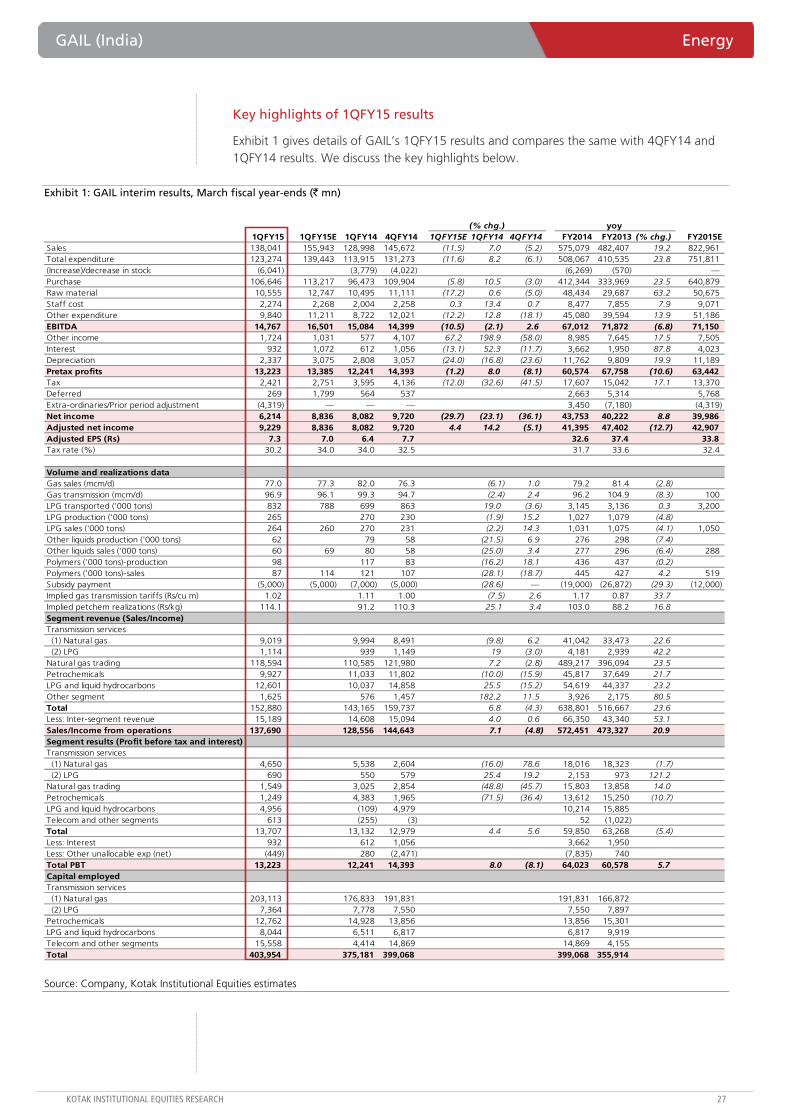

Key highlights of 1QFY15 results

Exhibit 1 gives details of GAIL’s 1QFY15 results and compares the same with 4QFY14 and 1QFY14 results. We discuss the key highlights below.

Exhibit 1: GAIL interim results, March fiscal year-ends (` mn)

(% chg.) yoy1QFY15 1QFY15E 1QFY14 4QFY14 1QFY15E 1QFY14 4QFY14 FY2014 FY2013 (% chg.) FY2015E

Sales 138,041 155,943 128,998 145,672 (11.5) 7.0 (5.2) 575,079 482,407 19.2 822,961Total expenditure 123,274 139,443 113,915 131,273 (11.6) 8.2 (6.1) 508,067 410,535 23.8 751,811(Increase)/decrease in stock (6,041) (3,779) (4,022) (6,269) (570) —Purchase 106,646 113,217 96,473 109,904 (5.8) 10.5 (3.0) 412,344 333,969 23.5 640,879Raw material 10,555 12,747 10,495 11,111 (17.2) 0.6 (5.0) 48,434 29,687 63.2 50,675Staff cost 2,274 2,268 2,004 2,258 0.3 13.4 0.7 8,477 7,855 7.9 9,071Other expenditure 9,840 11,211 8,722 12,021 (12.2) 12.8 (18.1) 45,080 39,594 13.9 51,186EBITDA 14,767 16,501 15,084 14,399 (10.5) (2.1) 2.6 67,012 71,872 (6.8) 71,150 Other income 1,724 1,031 577 4,107 67.2 198.9 (58.0) 8,985 7,645 17.5 7,505Interest 932 1,072 612 1,056 (13.1) 52.3 (11.7) 3,662 1,950 87.8 4,023Depreciation 2,337 3,075 2,808 3,057 (24.0) (16.8) (23.6) 11,762 9,809 19.9 11,189Pretax profits 13,223 13,385 12,241 14,393 (1.2) 8.0 (8.1) 60,574 67,758 (10.6) 63,442 Tax 2,421 2,751 3,595 4,136 (12.0) (32.6) (41.5) 17,607 15,042 17.1 13,370Deferred 269 1,799 564 537 2,663 5,314 5,768 Extra-ordinaries/Prior period adjustment (4,319) — — — 3,450 (7,180) (4,319) Net income 6,214 8,836 8,082 9,720 (29.7) (23.1) (36.1) 43,753 40,222 8.8 39,986 Adjusted net income 9,229 8,836 8,082 9,720 4.4 14.2 (5.1) 41,395 47,402 (12.7) 42,907 Adjusted EPS (Rs) 7.3 7.0 6.4 7.7 32.6 37.4 33.8 Tax rate (%) 30.2 34.0 34.0 32.5 31.7 33.6 32.4

Volume and realizations dataGas sales (mcm/d) 77.0 77.3 82.0 76.3 (6.1) 1.0 79.2 81.4 (2.8) Gas transmission (mcm/d) 96.9 96.1 99.3 94.7 (2.4) 2.4 96.2 104.9 (8.3) 100 LPG transported ('000 tons) 832 788 699 863 19.0 (3.6) 3,145 3,136 0.3 3,200LPG production ('000 tons) 265 270 230 (1.9) 15.2 1,027 1,079 (4.8) LPG sales ('000 tons) 264 260 270 231 (2.2) 14.3 1,031 1,075 (4.1) 1,050Other liquids production ('000 tons) 62 79 58 (21.5) 6.9 276 298 (7.4) Other liquids sales ('000 tons) 60 69 80 58 (25.0) 3.4 277 296 (6.4) 288Polymers ('000 tons)-production 98 117 83 (16.2) 18.1 436 437 (0.2) Polymers ('000 tons)-sales 87 114 121 107 (28.1) (18.7) 445 427 4.2 519Subsidy payment (5,000) (5,000) (7,000) (5,000) (28.6) — (19,000) (26,872) (29.3) (12,000) Implied gas transmission tariffs (Rs/cu m) 1.02 1.11 1.00 (7.5) 2.6 1.17 0.87 33.7 Implied petchem realizations (Rs/kg) 114.1 91.2 110.3 25.1 3.4 103.0 88.2 16.8 Segment revenue (Sales/Income)Transmission services (1) Natural gas 9,019 9,994 8,491 (9.8) 6.2 41,042 33,473 22.6 (2) LPG 1,114 939 1,149 19 (3.0) 4,181 2,939 42.2 Natural gas trading 118,594 110,585 121,980 7.2 (2.8) 489,217 396,094 23.5 Petrochemicals 9,927 11,033 11,802 (10.0) (15.9) 45,817 37,649 21.7 LPG and liquid hydrocarbons 12,601 10,037 14,858 25.5 (15.2) 54,619 44,337 23.2 Other segment 1,625 576 1,457 182.2 11.5 3,926 2,175 80.5 Total 152,880 143,165 159,737 6.8 (4.3) 638,801 516,667 23.6 Less: Inter-segment revenue 15,189 14,608 15,094 4.0 0.6 66,350 43,340 53.1 Sales/Income from operations 137,690 128,556 144,643 7.1 (4.8) 572,451 473,327 20.9 Segment results (Profit before tax and interest)Transmission services (1) Natural gas 4,650 5,538 2,604 (16.0) 78.6 18,016 18,323 (1.7) (2) LPG 690 550 579 25.4 19.2 2,153 973 121.2 Natural gas trading 1,549 3,025 2,854 (48.8) (45.7) 15,803 13,858 14.0 Petrochemicals 1,249 4,383 1,965 (71.5) (36.4) 13,612 15,250 (10.7) LPG and liquid hydrocarbons 4,956 (109) 4,979 10,214 15,885Telecom and other segments 613 (255) (3) 52 (1,022)Total 13,707 13,132 12,979 4.4 5.6 59,850 63,268 (5.4) Less: Interest 932 612 1,056 3,662 1,950Less: Other unallocable exp (net) (449) 280 (2,471) (7,835) 740Total PBT 13,223 12,241 14,393 8.0 (8.1) 64,023 60,578 5.7 Capital employedTransmission services (1) Natural gas 203,113 176,833 191,831 191,831 166,872 (2) LPG 7,364 7,778 7,550 7,550 7,897Petrochemicals 12,762 14,928 13,856 13,856 15,301LPG and liquid hydrocarbons 8,044 6,511 6,817 6,817 9,919Telecom and other segments 15,558 4,414 14,869 14,869 4,155Total 403,954 375,181 399,068 399,068 355,914

Source: Company, Kotak Institutional Equities estimates

Energy GAIL (India)

28 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Sequential improvement in operational performance. GAIL’s gas transmission volumes increased to 96.9 mcm/d from 94.7 mcm/d in 4QFY14 led by higher LNG imports. Gas sales volumes increased modestly to 77 mcm/d from 76 mcm/d in 4QFY14. Sales volume of LPG and other liquid hydrocarbons were at 324,000 tons versus 289,000 tons in 4QFY14 and 350,000 tons in 1QFY14. Polymer sales volume declined to 87,000 tons in 1QFY15 versus 107,000 tons in 4QFY14 and 121,000 tons in 1QFY14.

Lower EBIT of gas transmission segment. GAIL reported lower gas transmission revenues at `6.6 bn and EBIT at `2.2 bn in 1QFY15 led by one-off de-recognition of `2.4 bn of revenues due to retrospective implementation of regulated pipeline tariffs for Cauvery basin network (`1.5 bn), Chainsa-Jhajjar pipeline (`290 mn), Dabhol-Bangalore pipeline (`470 mn) and Kochi-Bangalore-Mangalore pipeline (`150 mn), as per the recent orders of PNGRB. The management has indicated a recurring quarterly impact of `150 mn. GAIL’s implied transmission tariffs for natural gas were expectedly lower at about `1/cu m versus FY2014 level of `1.17/cu m, reflecting removal of benefits from use-or-pay contracts from April 1, 2014.

Robust profitability of LPG and liquid hydrocarbons segment. GAIL reported sequentially flat EBIT of `5 bn for LPG and liquid hydrocarbons segment despite a sharp decline in realizations reflecting lower costs due to incremental allocation of domestic gas from April 2014. The company accounted subsidy burden of `5 bn in 1QFY15 versus `5 bn in 4QFY14 and `7 bn in 1QFY14. LPG sales volume was at 264,000 tons in 1QFY15 versus 231,000 tons in 4QFY14 and 270,000 tons in 1QFY14. Other liquid hydrocarbons volume was at 60,000 tons versus 58,000 tons in 4QFY14 and 80,000 tons in 1QFY14.

Lower adjusted EBIT of gas trading segment. Adjusted EBIT of GAIL’s gas trading segment was lower at `1.5 bn versus `2.9 bn in 4QFY14 and `3 bn in 1QFY14 reflecting dismal marketing margins on short-term/spot LNG volumes due to a sharp decline spot LNG prices. We note that GAIL’s reported EBIT for gas trading segment was negative at `355 mn led by one-off under-recovery of `1.9 bn on LNG imports due to higher-than-allocated sales of gas at domestic prices; we note that the company has already recouped the amount in July and will account it in 2QFY15 results.

Lower EBIT of petrochemicals segment. GAIL’s petrochemical segment EBIT declined to `1.2 bn (-36% qoq and -71% yoy) reflecting lower sales volume at 87,000 tons (-19% qoq and -28% yoy) and higher usage of re-gasified LNG as raw material. The management indicated that the volumes were lower during the quarter due to a maintenance-related shutdown and temporary power outage. Implied polymer realizations increased to `114.1/kg versus `110.3/kg in 4QFY14 and `91.2/kg in 1QFY14.

Higher EBIT of LPG transmission segment. The company reported an EBIT of `690 mn for LPG transmission segment, higher than `579 mn in 4QFY14 and `550 in 1QFY14. LPG transmission volumes were at 0.83 mn tons versus 0.86 mn tons in 4QFY14 and 0.7 mn tons in 1QFY14.

Other income boosted by write-back of provisions. GAIL has reported other income at `1.7 bn in 1QFY15 versus `4.1 bn in 4QFY14 and `577 mn in 1QFY14. The company has accounted `750 mn of reversal of provisions for litigations pertaining to issues with GSPC and others in 1QFY15 and `1.4 bn of reversal of provision for bad debts in 4QFY14.

Lower depreciation charges. GAIL’s depreciation expense declined to `2.3 bn in 1QFY15 from `3.1 bn in 4QFY14 and `2.8 bn in 1QFY14, as the company revised useful life of fixed assets as per Schedule II of the Companies Act, 2013.

GAIL (India) Energy

KOTAK INSTITUTIONAL EQUITIES RESEARCH 29

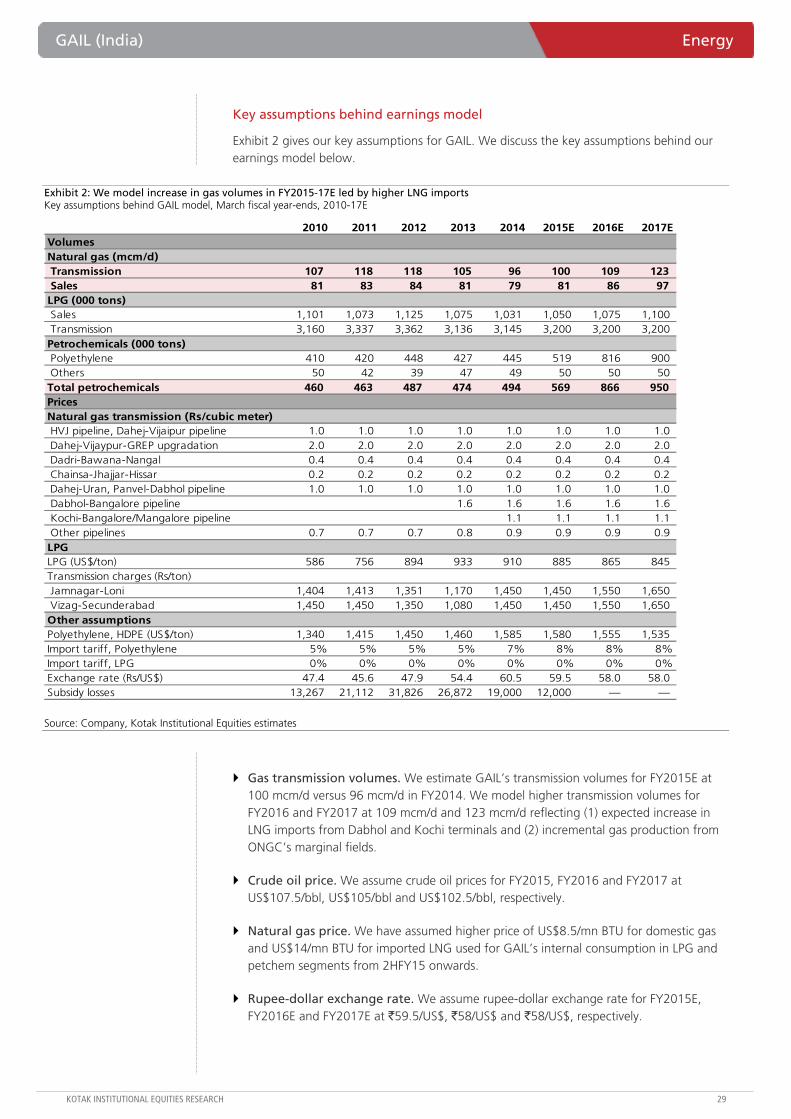

Key assumptions behind earnings model

Exhibit 2 gives our key assumptions for GAIL. We discuss the key assumptions behind our earnings model below.

Exhibit 2: We model increase in gas volumes in FY2015-17E led by higher LNG imports Key assumptions behind GAIL model, March fiscal year-ends, 2010-17E