Embed Size (px)

Citation preview

TARGET MARKET: BRAZIL

MARKETING STRATEGIES FOR TOURISM DESTINATIONS

A COMPETITIVE ANALYSIS

Marketing StrategiesFor Tourism Destinations

A Competitive Analysis

Target Market - Brazil

A report produced for European Travel Commission (ETC)by Tourism Development International

Brussels, 2014

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Published and printed by:European Travel CommissionRue du Marché aux Herbes, 611000 Brussels, BelgiumWebsite: www.etc-corporate.orgEmail: [email protected]

This report was compiled and edited by: Tourism Development International on behalf of the European Travel Commission.

The designations employed and the presentation of material in this publication do not imply the expression of any opinion whatsoever on the part of the European Travel Commission concerning the legal status of any country, territory, city or area, or of its authorities or concerning the delimitations of its frontiers or bound-aries.

Cover photo: Christ, symbol of Rio de Janeiro, standing on top of Corcovado Hill, overlooking Guanabara Bay and Sugarloaf, Rio de Janeiro, Brazil; Copyright: T photography.

Copyright © 2014 European Travel Commission.

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

ContentsForeword i

Introduction 1a. Defining the Competitive Environment for Destination Europe 2b. Destinations in the Global Market Place: a Comparative Analysis 2

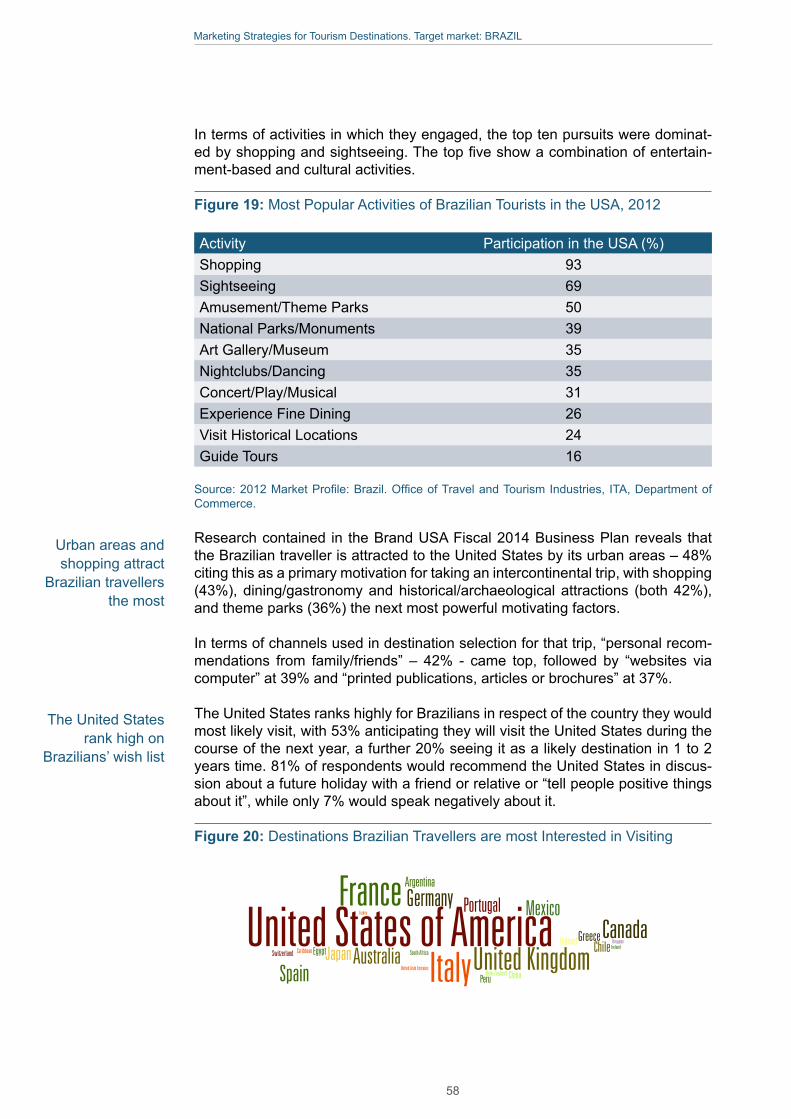

Summary of Brazil Market Study 10

1. The Brazil Outbound Market 151.1. A High Spending Market 151.2. Brazilian Tourism to Europe 171.3. Characteristics of the Brazilian Traveller 191.4. Drivers of Growth 211.5. Successful Destination Strategies 22

2. Travel Destinations in the Brazilian Market 242.1. Visa Regimes 242.2. Air Connections 262.3. Political, Economic and Socio-Cultural Links 292.4. Consumer Assessment (TripAdvisor) 32

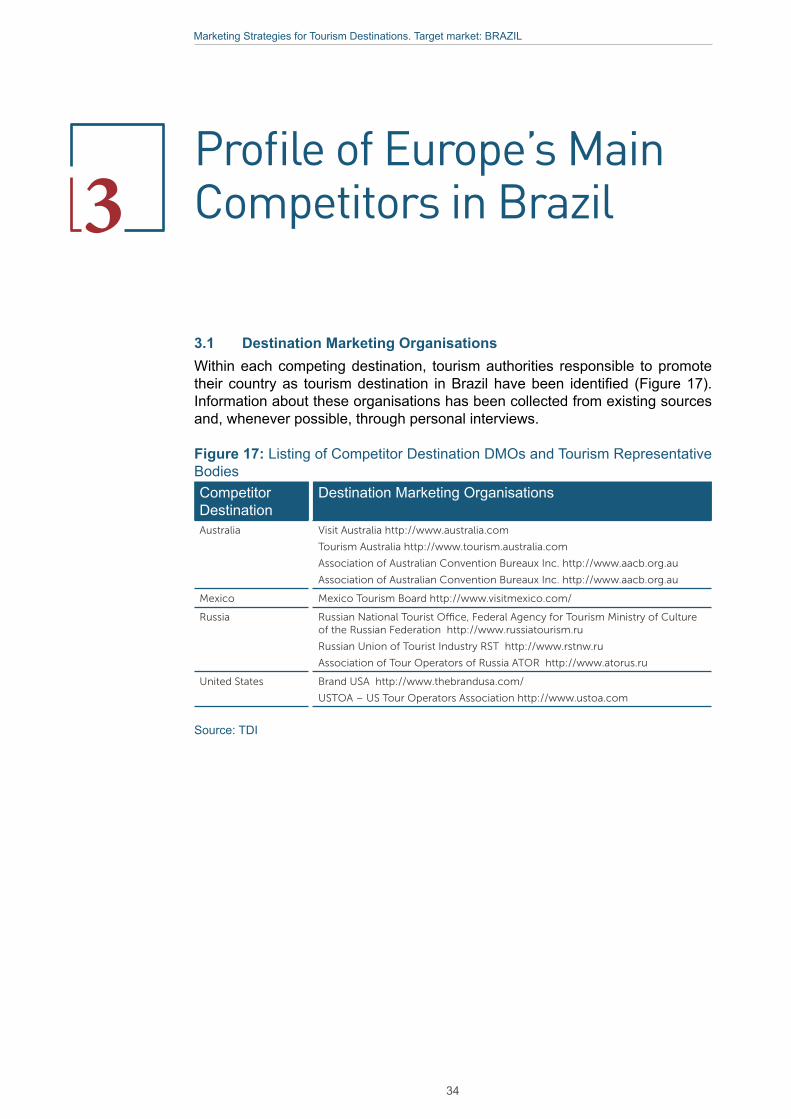

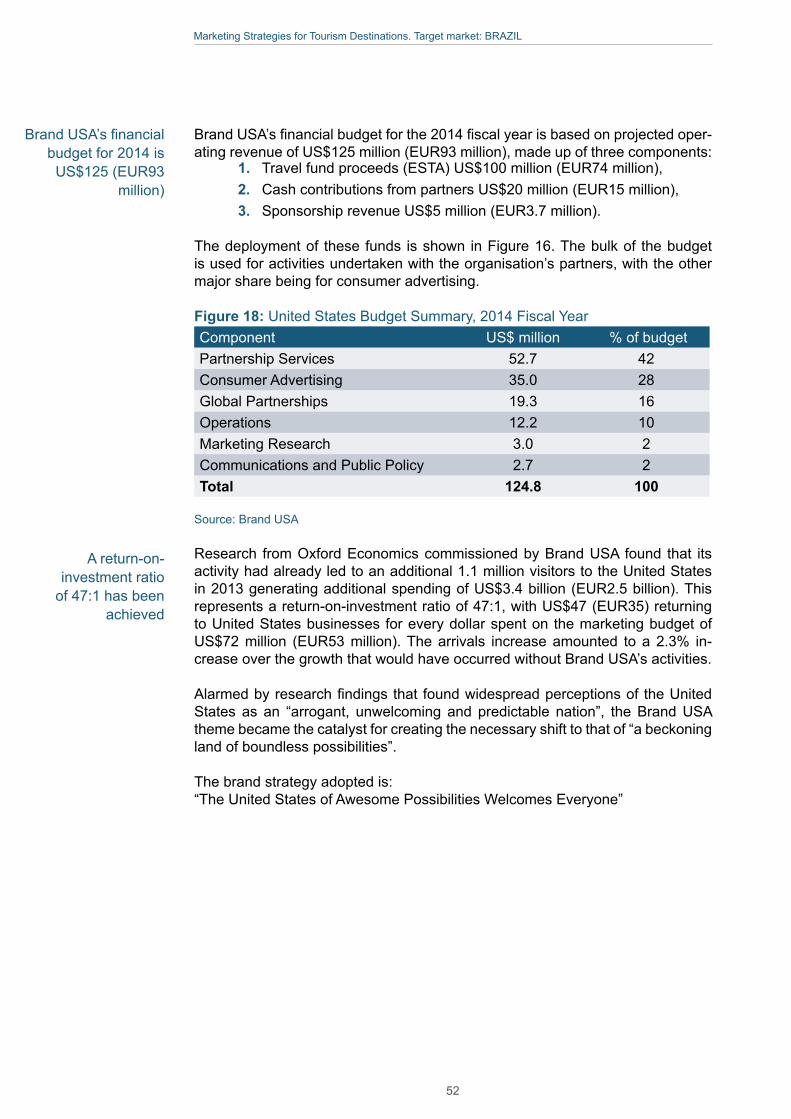

3. Profile of Europe’s Main Competitors in Brazil 343.1. Destination Marketing Organisations 343.2. The Australian Tourism Sector 353.3. The Mexican Tourism Sector 403.4. The Russian Federation Tourism Sector 463.5. The United States of America Tourism Sector 503.6. Conclusions

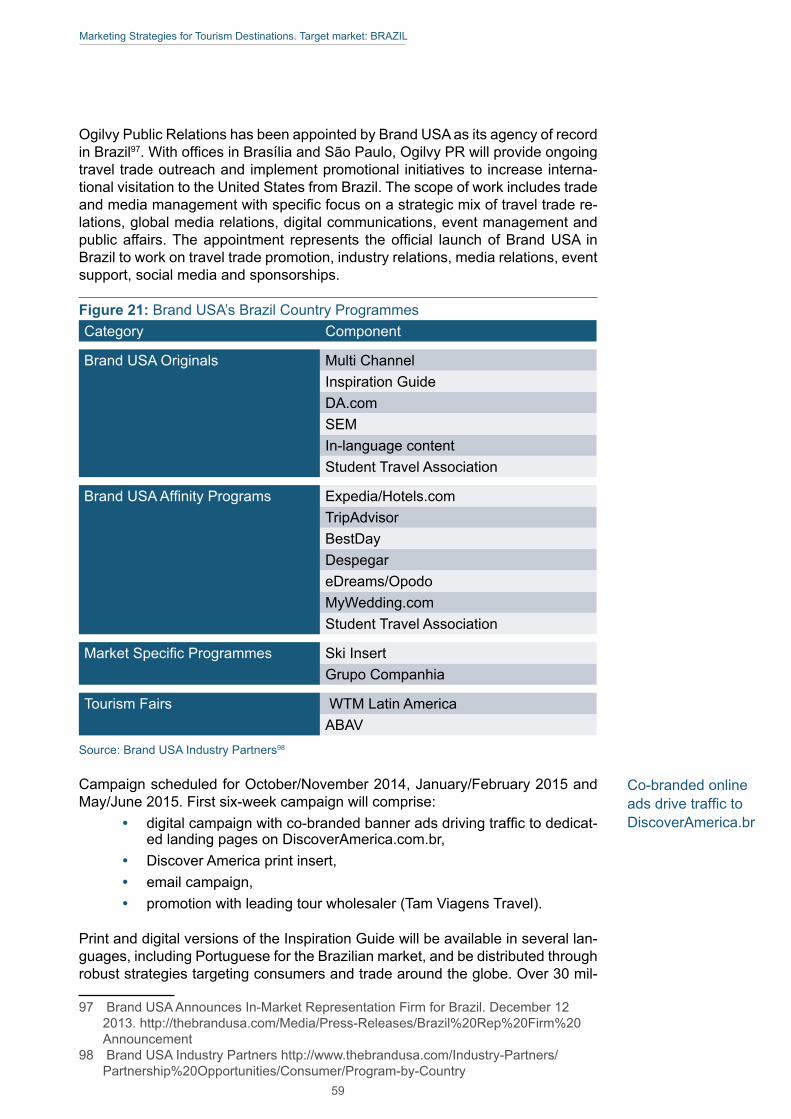

4. Marketing Strategy and Activities of Brand USA in Brazil 574.1. Brand USA’s Marketing and Promotional Activities in Brazil 574.2. Brand USA’s Success in Brazil 60

5. Key Factors in Destination Marketing in Brazil 625.1. Market Perceptions 625.2. Marketing Performance and Opportunities 63

Appendices

Appendix 1 European and Competing Destinations WET TTCI and 66 Bloom Country Brand Rankings Appendix 2 Weekly City-to-City Flights from Main Brazilian Centres 69Appendix 3 TripAdvisor Ratings 71Appendix 4 Bibliography and References 73

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

AcknowledgmentsThis report was prepared by Peter Mac Nulty and Robert Cleverdon of Tourism Development International on commission to the European Travel Commission (ETC), and was carried out under the supervision of Ms Valeria Croce, Head, Research and Development Department at ETC.

The report is part of a series of fact-finding reports on the tourism strategy de-veloped by destinations competing with Europe in select long-haul markets. The project was realised as part of the European Commission and ETC joint initiative “Destination Europe 2020”.

We would like to acknowledge the support and contributions of the many ETC members, marketing organisations and tour operators associations who contrib-uted to the realisation of this report.

We also gratefully acknowledge the support of ETC partners, who committedly contributed to the realisation of this project. A special note of thanks to Mr Charlie Ballard, Director of Advertising Research at TripAdvisor, Mr Xu Jing, Regional Director for Asia and the Pacific at UNWTO, and Mr Daniel Velasco, Consultant at Amadeus Travel Intelligence Unit, for their contributions.

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

ForewordIn an increasingly vibrant landscape, marked by new players, technological inno-vation and rapidly changing consumers, the need arises for European destina-tions to closely monitor others’ effort to win market shares in the global tourism market.

This compilation of best practice examples in tourism and promotion strategies is meant to provide insights relevant to ETC and its member countries through a better understanding of the environment in which they operate.

This series of reports provides insights into the strategic vision and the operation-al actions tourism destinations worldwide are developing to attract an increas-ing number of visitors from the most promising source markets. This fact-finding research offers a bird’s-eye view of the competitive environment, and a portrait of the tourism strategy and marketing activities of competing destinations. Ref-erences to official documents and publicly available reports facilitate access to detailed information, for those interested in achieving a higher level of knowl-edge. For Europe’s strongest competitors, portraits are enriched with first-hand information gathered through personal interviews with NTOs marketing directors, representatives of the travel trade and experts.

The common structure of reports facilitates cross-market comparisons. Key re-sults are synthesised in a highly visual executive summary, conceived for dis-semination to the public at large.

We trust these reports will become for ETC and its members an important tool to identify key opportunities and challenges, and to strengthen their comparative advantage in the global tourism market.

Executive UnitEuropean Travel Commission

i

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

IntroductionThis report’s aim is to collect meaningful knowledge about the tourism strategy of destinations competing with destinations in Europe in select long-haul markets. This study is part of a series of publications, which offer an overview of the en-vironment, in which European tourism destinations operate, and a profile of the tourism strategy and marketing activities of competing destinations. A listing of official documents, publicly available reports and media features is provided in an appendix and through the footnotes to permit more detailed examination of the information presented and issues raised. Each report also provides first-hand in-formation on a selection of competing destinations, gathered through interviews with NTOs’ marketing directors, travel trade and experts.

This project focuses on countries competing with European destinations in high potential long-haul markets, namely Brazil, Canada, China, Japan, Russia and the United States. In this analysis, Europe is defined as the 33 countries which are members of the European Travel Commission plus France, the Netherlands and the United Kingdom.

The analysis followed a three step approach.

The first step was to identify the key markets for Europe and the primary desti-nations competing with Europe in those markets. These markets are presented in Figure 1.

The second step consisted of assessing strengths and weaknesses of destina-tions, which are significant competitors to Europe in the six target markets. The assessment has been based on the following indicators:

• the World Economic Forum Travel and Tourism Competitive Index (WEF TTCI),

• travel trade interviews and expert opinion,• visa regimes and other visitor entry requirements,• air connectivity and capacity,• price competitiveness,• political, economic and socio-cultural links,• destination tourism development policy, • destination tourism marketing strategy.

The third step consisted of identifying those destinations which are the strongest competitors for Europe in each market, i.e. destinations which attract significant volumes of travellers and are actively investing in increasing their share in the market. A detailed profile of the organisations in charge of promoting inbound tourism to these destinations has been compiled. Information about the strongest competitors has been collected by the means of personal interviews as well as from secondary sources.

Defining the competitive environment for Destination Europe

1

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

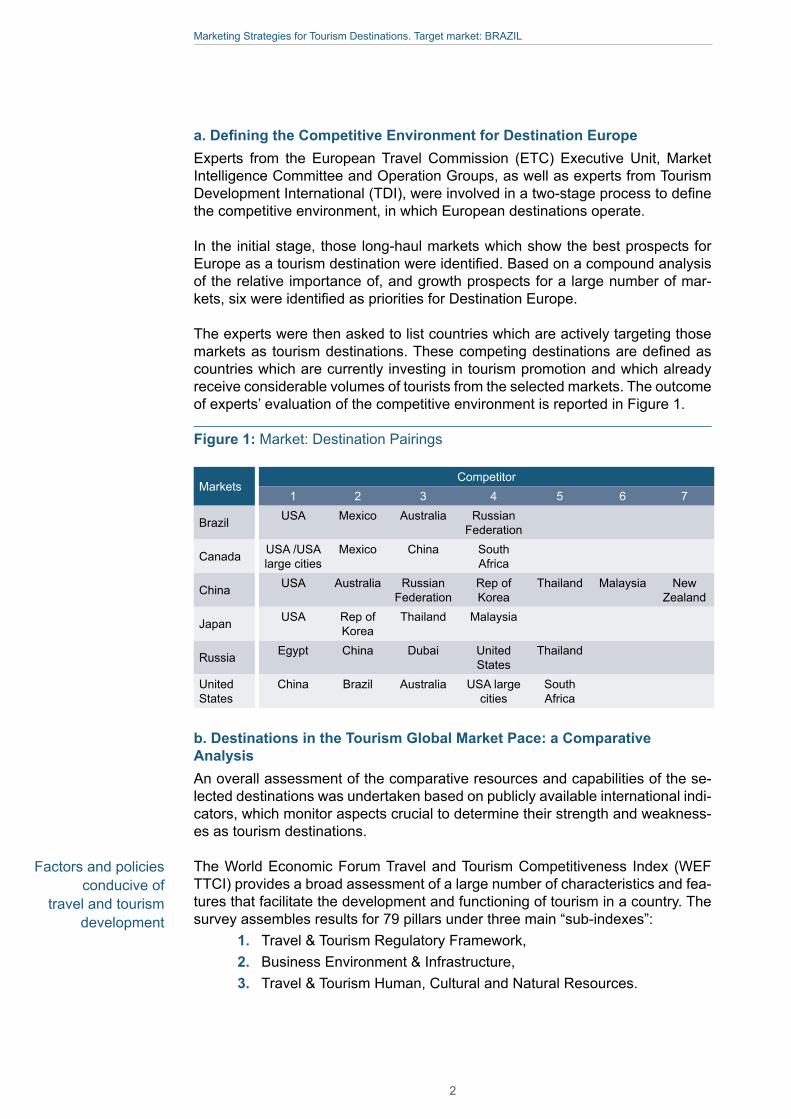

a. Defining the Competitive Environment for Destination Europe Experts from the European Travel Commission (ETC) Executive Unit, Market Intelligence Committee and Operation Groups, as well as experts from Tourism Development International (TDI), were involved in a two-stage process to define the competitive environment, in which European destinations operate.

In the initial stage, those long-haul markets which show the best prospects for Europe as a tourism destination were identified. Based on a compound analysis of the relative importance of, and growth prospects for a large number of mar-kets, six were identified as priorities for Destination Europe. The experts were then asked to list countries which are actively targeting those markets as tourism destinations. These competing destinations are defined as countries which are currently investing in tourism promotion and which already receive considerable volumes of tourists from the selected markets. The outcome of experts’ evaluation of the competitive environment is reported in Figure 1.

Figure 1: Market: Destination Pairings

MarketsCompetitor

1 2 3 4 5 6 7

Brazil USA Mexico Australia Russian Federation

Canada USA /USA large cities

Mexico China South Africa

China USA Australia Russian Federation

Rep of Korea

Thailand Malaysia New Zealand

Japan USA Rep of Korea

Thailand Malaysia

Russia Egypt China Dubai United States

Thailand

United States

China Brazil Australia USA large cities

South Africa

b. Destinations in the Tourism Global Market Pace: a Comparative AnalysisAn overall assessment of the comparative resources and capabilities of the se-lected destinations was undertaken based on publicly available international indi-cators, which monitor aspects crucial to determine their strength and weakness-es as tourism destinations.

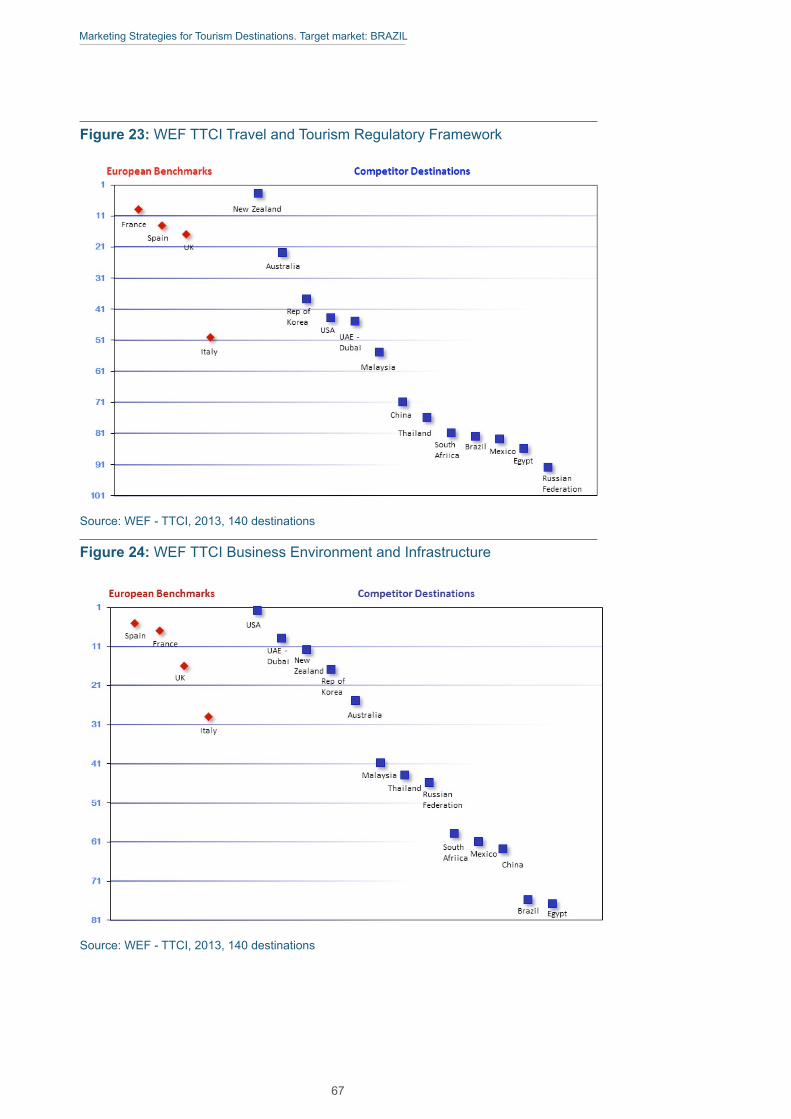

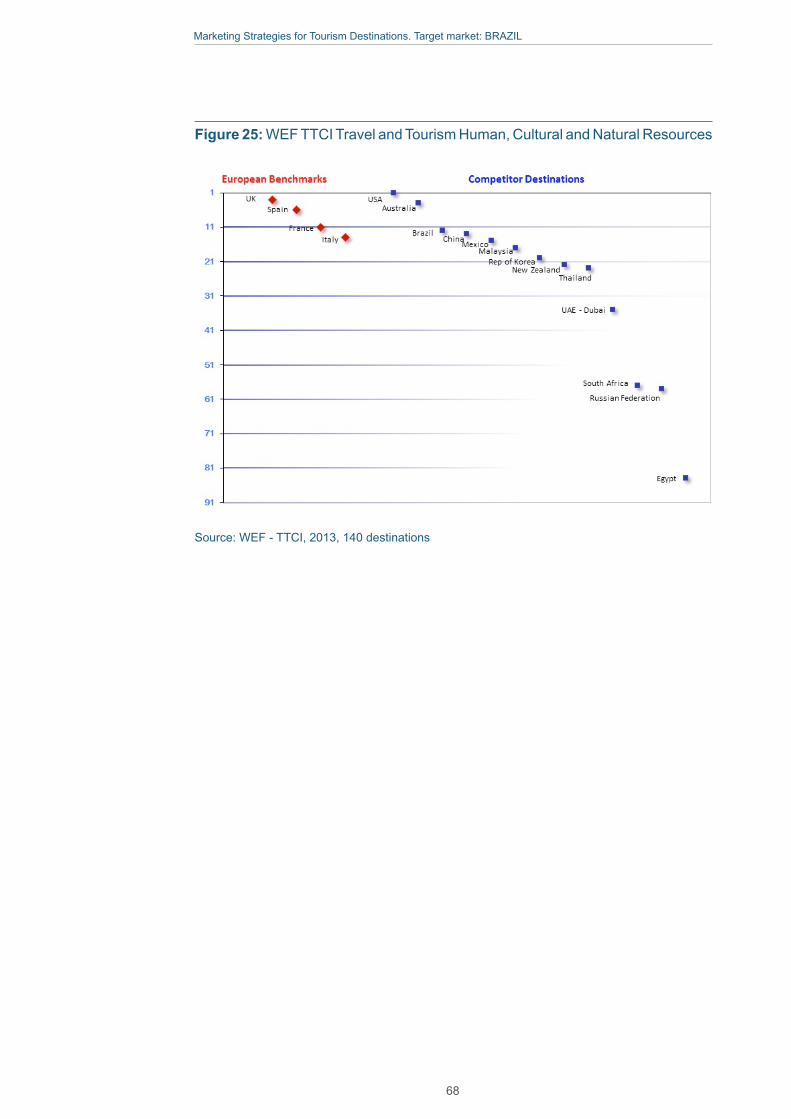

The World Economic Forum Travel and Tourism Competitiveness Index (WEF TTCI) provides a broad assessment of a large number of characteristics and fea-tures that facilitate the development and functioning of tourism in a country. The survey assembles results for 79 pillars under three main “sub-indexes”:

1. Travel & Tourism Regulatory Framework,2. Business Environment & Infrastructure, 3. Travel & Tourism Human, Cultural and Natural Resources.

Factors and policies conducive of

travel and tourism development

2

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

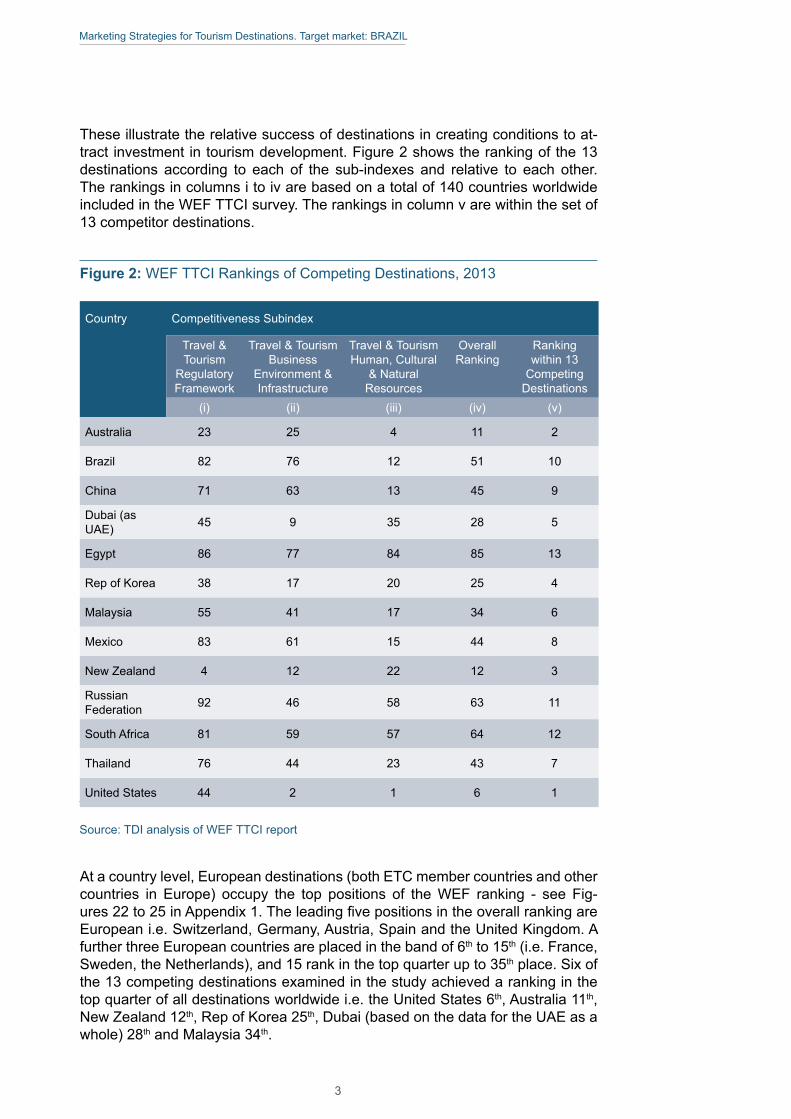

These illustrate the relative success of destinations in creating conditions to at-tract investment in tourism development. Figure 2 shows the ranking of the 13 destinations according to each of the sub-indexes and relative to each other. The rankings in columns i to iv are based on a total of 140 countries worldwide included in the WEF TTCI survey. The rankings in column v are within the set of 13 competitor destinations.

Figure 2: WEF TTCI Rankings of Competing Destinations, 2013

Country Competitiveness Subindex

Travel & Tourism

Regulatory Framework

Travel & Tourism Business

Environment & Infrastructure

Travel & Tourism Human, Cultural

& Natural Resources

Overall Ranking

Ranking within 13

Competing Destinations

(i) (ii) (iii) (iv) (v)

Australia 23 25 4 11 2

Brazil 82 76 12 51 10

China 71 63 13 45 9

Dubai (as UAE) 45 9 35 28 5

Egypt 86 77 84 85 13

Rep of Korea 38 17 20 25 4

Malaysia 55 41 17 34 6

Mexico 83 61 15 44 8

New Zealand 4 12 22 12 3

Russian Federation 92 46 58 63 11

South Africa 81 59 57 64 12

Thailand 76 44 23 43 7

United States 44 2 1 6 1

Source: TDI analysis of WEF TTCI report

At a country level, European destinations (both ETC member countries and other countries in Europe) occupy the top positions of the WEF ranking - see Fig-ures 22 to 25 in Appendix 1. The leading five positions in the overall ranking are European i.e. Switzerland, Germany, Austria, Spain and the United Kingdom. A further three European countries are placed in the band of 6th to 15th (i.e. France, Sweden, the Netherlands), and 15 rank in the top quarter up to 35th place. Six of the 13 competing destinations examined in the study achieved a ranking in the top quarter of all destinations worldwide i.e. the United States 6th, Australia 11th, New Zealand 12th, Rep of Korea 25th, Dubai (based on the data for the UAE as a whole) 28th and Malaysia 34th.

3

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

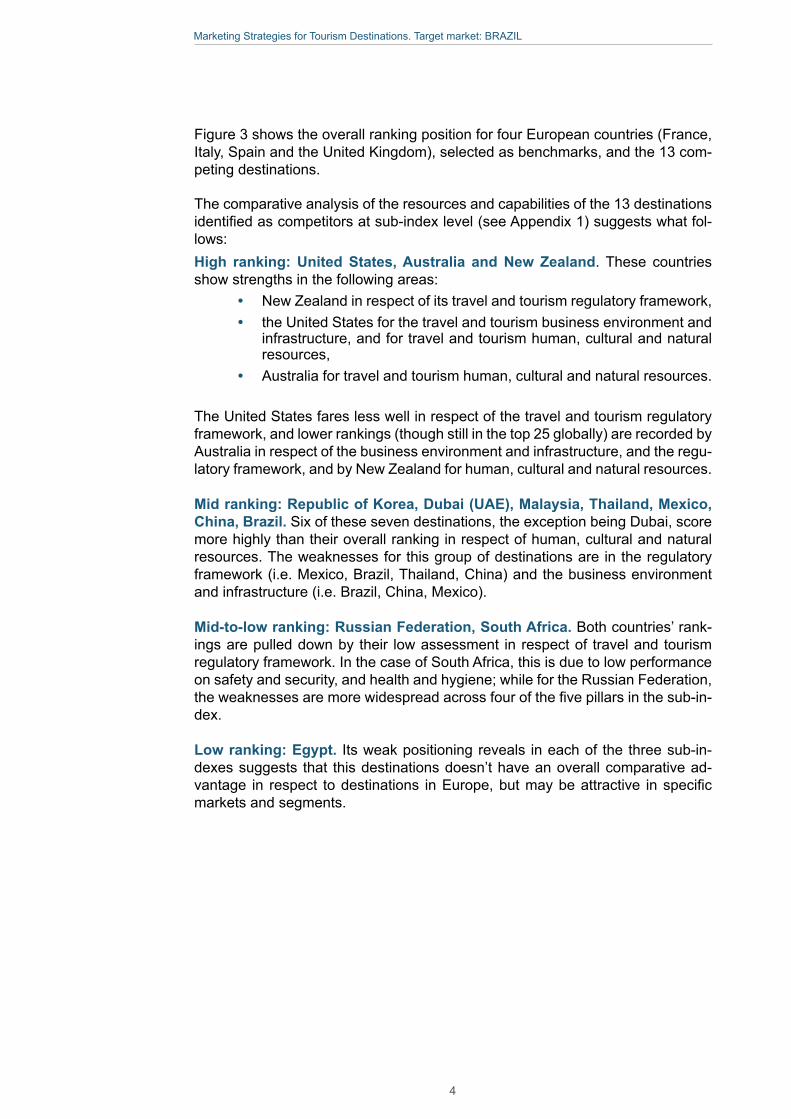

Figure 3 shows the overall ranking position for four European countries (France, Italy, Spain and the United Kingdom), selected as benchmarks, and the 13 com-peting destinations.

The comparative analysis of the resources and capabilities of the 13 destinations identified as competitors at sub-index level (see Appendix 1) suggests what fol-lows:High ranking: United States, Australia and New Zealand. These countries show strengths in the following areas:

• New Zealand in respect of its travel and tourism regulatory framework,• the United States for the travel and tourism business environment and

infrastructure, and for travel and tourism human, cultural and natural resources,

• Australia for travel and tourism human, cultural and natural resources.

The United States fares less well in respect of the travel and tourism regulatory framework, and lower rankings (though still in the top 25 globally) are recorded by Australia in respect of the business environment and infrastructure, and the regu-latory framework, and by New Zealand for human, cultural and natural resources.

Mid ranking: Republic of Korea, Dubai (UAE), Malaysia, Thailand, Mexico, China, Brazil. Six of these seven destinations, the exception being Dubai, score more highly than their overall ranking in respect of human, cultural and natural resources. The weaknesses for this group of destinations are in the regulatory framework (i.e. Mexico, Brazil, Thailand, China) and the business environment and infrastructure (i.e. Brazil, China, Mexico).

Mid-to-low ranking: Russian Federation, South Africa. Both countries’ rank-ings are pulled down by their low assessment in respect of travel and tourism regulatory framework. In the case of South Africa, this is due to low performance on safety and security, and health and hygiene; while for the Russian Federation, the weaknesses are more widespread across four of the five pillars in the sub-in-dex.

Low ranking: Egypt. Its weak positioning reveals in each of the three sub-in-dexes suggests that this destinations doesn’t have an overall comparative ad-vantage in respect to destinations in Europe, but may be attractive in specific markets and segments.

4

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Figure 3: WEF TTCI Overall Rankings

Source: WEF - TTCI, 2013, 140 destinations

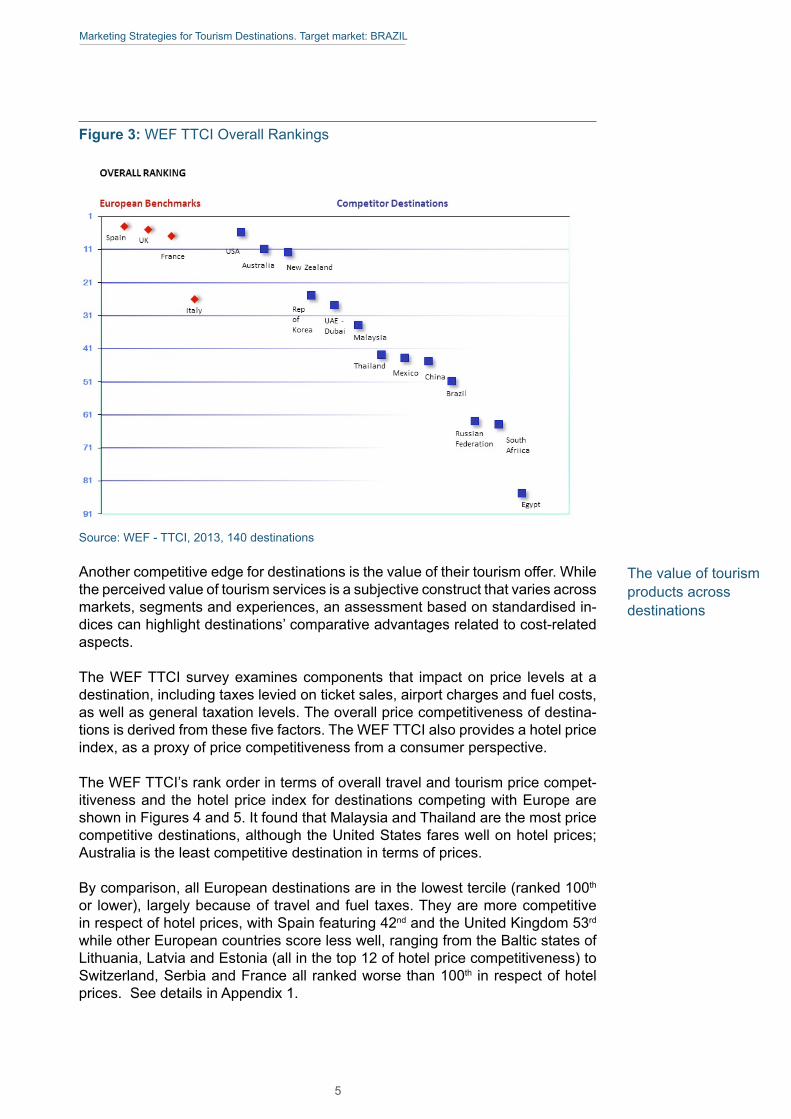

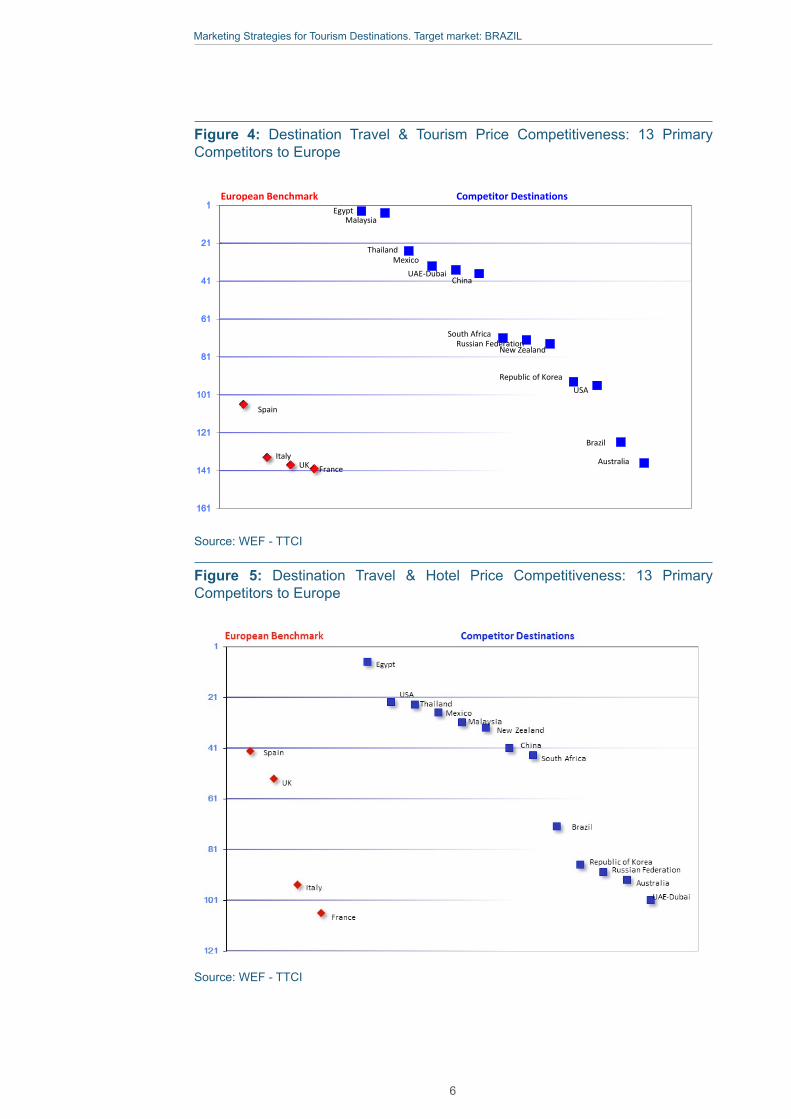

Another competitive edge for destinations is the value of their tourism offer. While the perceived value of tourism services is a subjective construct that varies across markets, segments and experiences, an assessment based on standardised in-dices can highlight destinations’ comparative advantages related to cost-related aspects.

The WEF TTCI survey examines components that impact on price levels at a destination, including taxes levied on ticket sales, airport charges and fuel costs, as well as general taxation levels. The overall price competitiveness of destina-tions is derived from these five factors. The WEF TTCI also provides a hotel price index, as a proxy of price competitiveness from a consumer perspective.

The WEF TTCI’s rank order in terms of overall travel and tourism price compet-itiveness and the hotel price index for destinations competing with Europe are shown in Figures 4 and 5. It found that Malaysia and Thailand are the most price competitive destinations, although the United States fares well on hotel prices; Australia is the least competitive destination in terms of prices.

By comparison, all European destinations are in the lowest tercile (ranked 100th or lower), largely because of travel and fuel taxes. They are more competitive in respect of hotel prices, with Spain featuring 42nd and the United Kingdom 53rd while other European countries score less well, ranging from the Baltic states of Lithuania, Latvia and Estonia (all in the top 12 of hotel price competitiveness) to Switzerland, Serbia and France all ranked worse than 100th in respect of hotel prices. See details in Appendix 1.

The value of tourism products across destinations

5

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Figure 4: Destination Travel & Tourism Price Competitiveness: 13 Primary Competitors to Europe

1

21

41

61

81

101

121

141

161

UK

Russian Federation

Malaysia

Thailand

New Zealand

European Benchmark Competitor Destinations

Source: WEF -‐ TTCI

USARepublic of Korea

Australia

Egypt

South Africa

China

MexicoUAE-‐Dubai

Spain

France

BrazilItaly

Source: WEF - TTCI

Figure 5: Destination Travel & Hotel Price Competitiveness: 13 Primary Competitors to Europe

Source: WEF - TTCI

6

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Country Brand Rankings

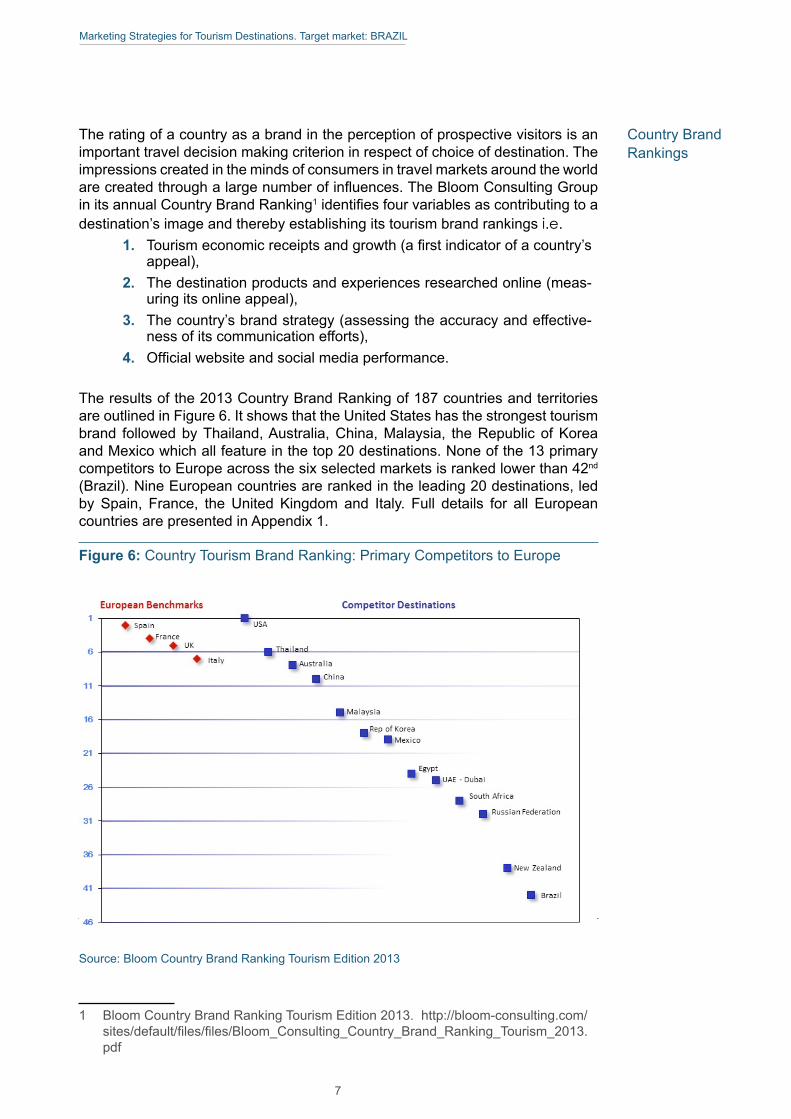

The rating of a country as a brand in the perception of prospective visitors is an important travel decision making criterion in respect of choice of destination. The impressions created in the minds of consumers in travel markets around the world are created through a large number of influences. The Bloom Consulting Group in its annual Country Brand Ranking1 identifies four variables as contributing to a destination’s image and thereby establishing its tourism brand rankings i.e.

1. Tourism economic receipts and growth (a first indicator of a country’s appeal),

2. The destination products and experiences researched online (meas-uring its online appeal),

3. The country’s brand strategy (assessing the accuracy and effective-ness of its communication efforts),

4. Official website and social media performance.

The results of the 2013 Country Brand Ranking of 187 countries and territories are outlined in Figure 6. It shows that the United States has the strongest tourism brand followed by Thailand, Australia, China, Malaysia, the Republic of Korea and Mexico which all feature in the top 20 destinations. None of the 13 primary competitors to Europe across the six selected markets is ranked lower than 42nd (Brazil). Nine European countries are ranked in the leading 20 destinations, led by Spain, France, the United Kingdom and Italy. Full details for all European countries are presented in Appendix 1.

Figure 6: Country Tourism Brand Ranking: Primary Competitors to Europe

Source: Bloom Country Brand Ranking Tourism Edition 2013

1 Bloom Country Brand Ranking Tourism Edition 2013. http://bloom-consulting.com/sites/default/files/files/Bloom_Consulting_Country_Brand_Ranking_Tourism_2013.pdf

7

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

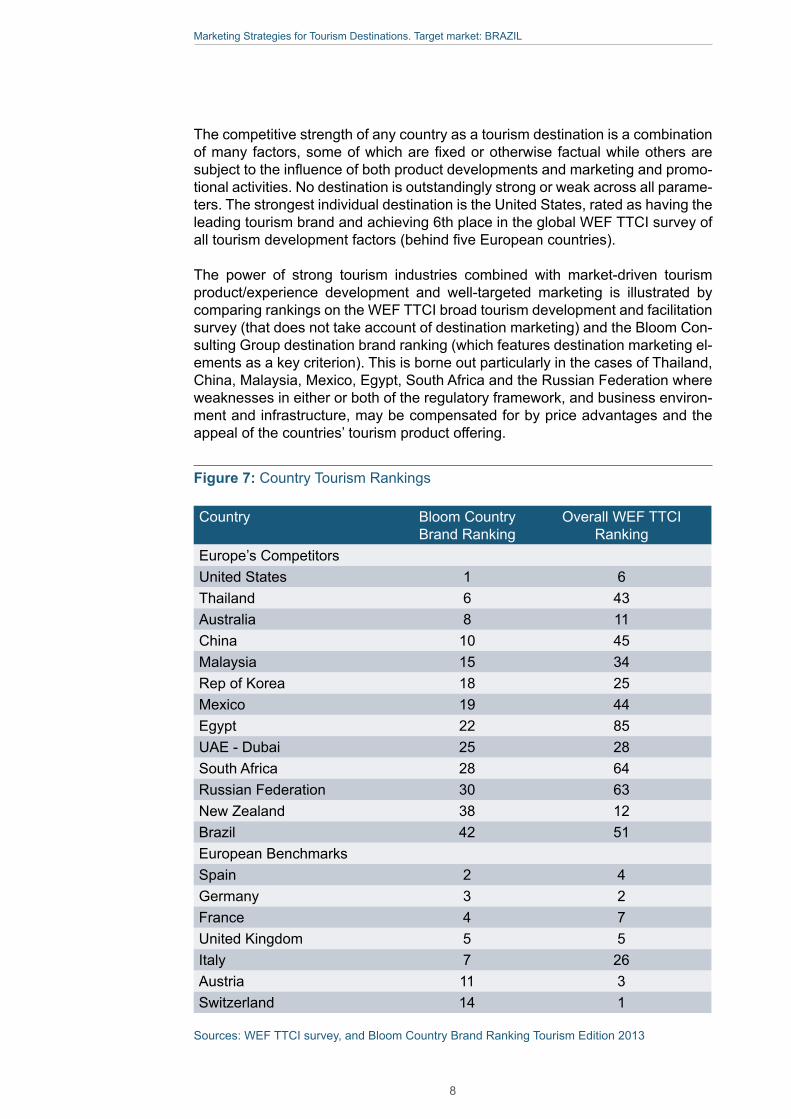

The competitive strength of any country as a tourism destination is a combination of many factors, some of which are fixed or otherwise factual while others are subject to the influence of both product developments and marketing and promo-tional activities. No destination is outstandingly strong or weak across all parame-ters. The strongest individual destination is the United States, rated as having the leading tourism brand and achieving 6th place in the global WEF TTCI survey of all tourism development factors (behind five European countries).

The power of strong tourism industries combined with market-driven tourism product/experience development and well-targeted marketing is illustrated by comparing rankings on the WEF TTCI broad tourism development and facilitation survey (that does not take account of destination marketing) and the Bloom Con-sulting Group destination brand ranking (which features destination marketing el-ements as a key criterion). This is borne out particularly in the cases of Thailand, China, Malaysia, Mexico, Egypt, South Africa and the Russian Federation where weaknesses in either or both of the regulatory framework, and business environ-ment and infrastructure, may be compensated for by price advantages and the appeal of the countries’ tourism product offering.

Figure 7: Country Tourism Rankings

Country Bloom Country Brand Ranking

Overall WEF TTCI Ranking

Europe’s CompetitorsUnited States 1 6Thailand 6 43Australia 8 11China 10 45Malaysia 15 34Rep of Korea 18 25Mexico 19 44Egypt 22 85UAE - Dubai 25 28South Africa 28 64Russian Federation 30 63New Zealand 38 12Brazil 42 51European Benchmarks Spain 2 4Germany 3 2France 4 7United Kingdom 5 5Italy 7 26Austria 11 3Switzerland 14 1

Sources: WEF TTCI survey, and Bloom Country Brand Ranking Tourism Edition 2013

8

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Information Note - Exchange Rates The monetary values quoted in the report are taken from the sources referenced, including amounts stated in the source document in US dollars. In all cases, conversion has been made to Euros. The conversion rates used are the average rates across the year between the local currency (or US dollar where that is the currency stated in the source document) and the Euro for the year of the data. For future forecasts/targets, the rate between the local currency and the Euro as at June 2014 have been used.

9

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

KEY DEMOGRAPHIC AND ECONOMIC DATA 2013

BRAZIL’S PERFORMANCE IN INTERNATIONAL TOURISM

OUTBOUND DESTINATIONS VISITED BY BRAZILIANS

International arrivals generated

2012: 7.9mn2013 : 8.4mnup 6%

Expenditure

Population

198.7mn (5th in the world)

BRL 23,927 €7,976

GDP PP per capita Current Prices

Fluctuating GDP growth over past decade with recovery of

Summary of Brazil Market StudyOUTBOUND TRAVEL AND COMPETITIVE ENVIRONMENT

BRL4,782 bn €1,594bn

GDP Data2

$250-$300 (€185-€225) a day on over sea trips

2013: $25bn (€19 bn)

up 13% on 2012

2World Economic Outlook Database, October 2013, IMF. 3 World Economic Outlook, April 2014, IMF

Total trips to Europe:

3 million aggregate arrivals, having grown at the rate of 14% a year between 2007 and 2013

Current Prices

BRL 12,118 €4,039

GDP PPP per capita Current Prices

in 2013 followed by growth of

and in 20153

6.0%1.8%2.7%

50%

33%

20%One fifth to the

United States

Half to other destinations in the Americas

One third to neighbouring countries

22%Average annual growth in Brazilian arrivals in the United States 2007 to 2013

3RDMaking it the United States’

most important visited destination

10

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

GROWTH DRIVERS

PURPOSE OF VISIT

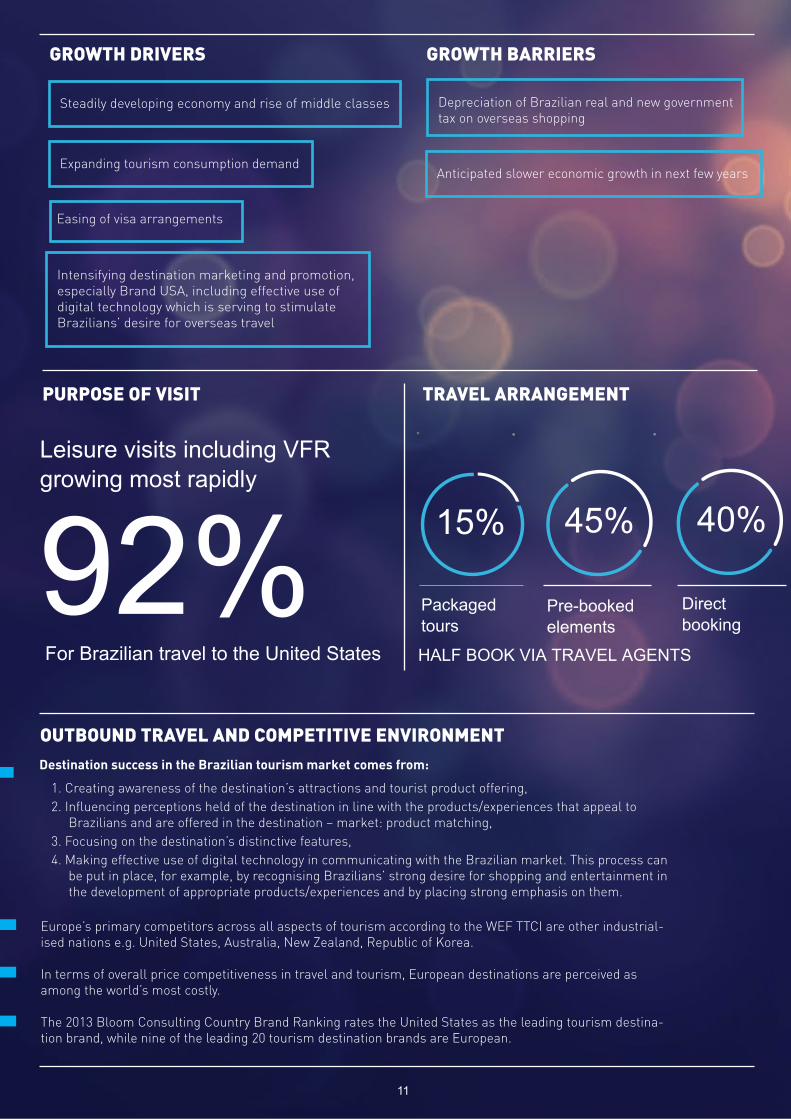

Steadily developing economy and rise of middle classes

Easing of visa arrangements

Expanding tourism consumption demand Anticipated slower economic growth in next few years

Depreciation of Brazilian real and new government tax on overseas shopping

OUTBOUND TRAVEL AND COMPETITIVE ENVIRONMENT

1. Creating awareness of the destination’s attractions and tourist product offering, 2. Influencing perceptions held of the destination in line with the products/experiences that appeal to

Brazilians and are offered in the destination – market: product matching, 3. Focusing on the destination’s distinctive features, 4. Making effective use of digital technology in communicating with the Brazilian market. This process can

be put in place, for example, by recognising Brazilians’ strong desire for shopping and entertainment in the development of appropriate products/experiences and by placing strong emphasis on them.

Europe’s primary competitors across all aspects of tourism according to the WEF TTCI are other industrial-ised nations e.g. United States, Australia, New Zealand, Republic of Korea.

In terms of overall price competitiveness in travel and tourism, European destinations are perceived as among the world’s most costly.

The 2013 Bloom Consulting Country Brand Ranking rates the United States as the leading tourism destina-tion brand, while nine of the leading 20 tourism destination brands are European.

Intensifying destination marketing and promotion, especially Brand USA, including effective use of digital technology which is serving to stimulate Brazilians’ desire for overseas travel

TRAVEL ARRANGEMENT

Destination success in the Brazilian tourism market comes from:

GROWTH BARRIERS

11

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Four destinations are shortlisted as significant competing destinations to Europe in the Brazilian market: Australia, Mexico, Russian Federa-tion, and the United States,

The United States is the most active and effective long haul competitor to Europe for the Brazilian tourist,

Brand USA’s achievement is in getting a return on investment of its US$3.8 million (EUR2.8 million) marketing budget in Brazil of 96:1 in respect of incremental earnings i.e. US$369 million (EUR273 million) spending attributable to the campaign. Brand USA opened its first office in Brazil early in 2014, which combined with the CVB activities of many US states and cities in Brazil, makes the United States a formidable competitor for Europe in that market,

The partnership approach is central to Brand USA’s marketing strategy and campaign components, giving a wide range of destination, travel trade and media partners the opportunity to piggyback on the digital and traditional marketing tools, public relations and promotional efforts developed and conducted by Brand USA,

In any destination marketing strategy based on partnerships, accounta-bility to its partners is vital. Brand USA has a rigorous system of moni-toring, assessing and evaluating its activities.

PRINCIPAL COMPETING DESTINATIONS

COMPETING DESTINATION ORGANISATIONS

Four destinations are shortlisted as signifi-cant competing desti-nations to Europe in the Brazilian market:

Australia, Mexico, Russian Federation, and the UnitedStates

The United States is the

most active and e�ective long haul competitor to Europe for the Brazilian tourist

2World Economic Outlook Database, October 2013, IMF. 3 World Economic Outlook, April 2014, IMF

1. Stressing the authenticity of their natural and cultural heritage in developing brand images and positioning,

2. Paying equal attention to established source markets and newly emerging ones, as Brazil, to achieve a balanced set of markets,

3. Seeking a market: product “matching” approach that provides high quality experiences in line with the needs and expectations of differ-ent market segments based on detailed research and analysis of such markets and segments, with the Brazilian market being a growing or newly emerging priority target for all destinations studied,

4. Focusing on a number of common segments across competitors e.g. cultural heritage, business/MICE, education but with special atten-tion in the United States to shopping and visits to the Brazilian diaspora,

5. Paying special attention to attracting high value/affluent tourists,

6. Showing a significant and continuing switch away from traditional advertising and promotional methods to electronic digital marketing systems and activities.

All four are making major efforts to support and increase the competitiveness of their travel and tourism industries by:

12

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

The United States and Europe are seen quite differently by Brazilians. The primary image of the countries of Europe in Brazilians’ minds is associat-ed with the various manifestations of culture and history. The opposite is the case for the United States which is perceived first and foremost as a destination for fun and shopping,

Europe and the United States are top of the list in terms of choice as first time overseas destinations,

Brazilians’ image of Europe includes academic studies, gastronomy, sports, historical and cultural attractions, religious sites, as well as glamour and prestige4. Europe’s advantages are its image as a sophisticat-ed and refined destination, access to part of Brazil’s cultural roots, a worthwhile cultural experience for the time and money, many religious sites, gastronomic delights and an image as a “liberal” destination5. However, many Brazilians are unaware that no visa is required to visit Schengen countries and other countries in Europe. This factor along with perceived low value-for-money, time spent queuing and language barriers are deterrents for Brazilian travellers to Europe6 , as is the relative lack of marketing of Europe and its constituent countries compared with that of the United States at national, state and city levels,

Though specific data are not available, trade respondents say that Europe is disadvantaged against the United States in Brazil through a far smaller marketing budget i.e. Brand USA plus regional CVBs vs ETC and individual European country tourist offices,

Given the range of attributes recognised by Brazilians in Europe - covering history, culture (original and contemporary), education, sports etc – and the presence of a large Brazilian diaspora in Europe, the potential for Brazilian travel to Europe is high. To realise this potential, Europe-wide marketing campaigns can create awareness of the opportunities and further measures to facilitate travel – e.g. transportation links – can create the conditions that the European country DMOs – either individually or in small partnerships according to the optimal structure of the tour – can build on. Brand USA and its partners, along with the nation’s CVBs, are already doing this for the United States. Europe’s potential is no less than that of the United States but at present lacks a Europe-wide positioning exercise to create awareness of the full spread of resources and visitor opportunities.

COMPARATIVE ASSESSMENT: EUROPE, THE UNITED STATES

The United States and Europe are seen quite di erently by

Brazilians. The primary image of the countries of Europe in Brazilians’ minds is associated with the various manifestations of culture and history

4Understanding Brazilian Outbound Tourism. UNWTO & ETC. 2013 5Ibid 6Ibid 13

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

14

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

The Brazilian Outbound Travel Market 1

Outbound travel volume is small but Brazilians remain high spenders

1.1 A High Spending MarketOutbound Brazilian tourism grew 9% in 2012 to reach a level of 7.9 million. Be-tween 2007 and 2012, outbound tourism from Brazil rose by 68% i.e. an average annual rate of growth of 11%, with a 6% rise during the first eight months of 20134 leading to a full year estimate of 8.4 million. The Brazilian Real fell sharply in value – by around one third - against both the United States dollar and the Euro between the peak in 2010/11 and late 2013. Nonetheless, overseas expenditure on travel and tourism continued to expand – by 13% - in 2013, reaching US$25 billion (EUR18.5 billion)5. This was a much sharper increase than the 4% recorded in 2012.

South Americans in general – and Brazilians in particular – are big spenders on international travel, with average spending per trip increasing in 2013 by 4% to EUR1,679, which is equivalent to EUR223 per night on an average 7.5 night trip6.

In volume terms, Brazil outbound travel amounts to between 8 and 9 million trips a year, which is below the level of most industrialised nations and the other fast expanding BRIC markets with their larger population base. In terms of outbound tourism levels, then, Brazil ranks outside the leading source markets but signifi-cantly higher in terms of expenditure. Brazilians are high spenders and entered the top ten by expenditure at tenth place in 2013, displacing Japan7.

Half of Brazilian outbound travel is to other destinations in the Americas, of which just under one-third goes to neighbouring countries (i.e. Argentina 17% in 2012, Uruguay 6%, Chile 5%, Paraguay 2%). On a country level, the main destination for Brazilians is the United States which accounted for 21% of all Brazilian out-bound trips in 2012. Mexico received 2% of the Brazilian market8.

4 ITB World Travel Trends Report December 2013. March 2014. IPK International http://www.itb-berlin.de/media/itb/itb_media/itb_pdf/WTTR_Report_2014_Web.pdf

5 International tourism generates US$1.4 trillion in export earnings. UNWTO Press Release, May 2014. http://media.unwto.org/press-release/2014-05-13/international-tourism-generates-us-14-trillion-export-earnings

6 ITB World Travel Trends Report 2013/14 IPK International Dec 2013 http://www.itb-berlin.de/media/itb/itb_media/itb_pdf/WTTR_Report_2014_Web.pdf

7 Ibid8 WTM Origin Market Seminar Brazil ETOA www.etoa.org/docs/default-

source/.../2013-wtm-presentation-brazil.pdf?

Half of Brazilian outbound travel is intra-regional

15

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Growth is forecast to decelerate as

the Brazilian travel market matures

Overseas travel remains appealing

but fiscal constraints may hamper

spending growth

Over the past decade the volume of short haul Brazilian arrivals in South America quadrupled, while long haul travel grew threefold. With strong economic growth and expanding consumer demand among its residents, including for overseas travel and tourism, all destination areas are sharing in the expansion of Brazilian outbound tourism. The main beneficiaries over the past decade have been other South American countries and the United States where the growth in Brazilian arrivals has been at the rate of 23% a year between 2007 and 2012. This rep-resents growth at a rate more than double that for total outbound Brazilian travel in the period, with a further rise of 15% in 2013. The 2 million Brazilian visitors to the United States in 2013 made Brazil the 3rd most important generating over-seas market for the country (after Japan and the United Kingdom, excluding the neighbouring countries of Canada and Mexico)9.

Despite rapid growth of the Brazilian economy in recent decades, with a continu-ing relatively weak currency and slower economic progress, outbound Brazilian travel may be maturing and growth is forecast to slow down to 4.4% over the next 5 years10. The US National Travel and Tourism Office is more optimistic antici-pating a 50% rise in the numbers of Brazilians visiting the United States between 2013 and 2018 i.e. an annual rise of close to 8.5% over the period11. This is more than double the UNWTO forecast of average growth rate of 4% worldwide for the 2010-2020 period, and four times that for North America (2% a year)12. The rate is also significantly above the United States’ own overall growth rate forecast for all inbound tourism between 2013 and 2018 of nearly 4% a year13.

Brazilians remain extremely positive about their future prospects for overseas travel. The slowdown in the country’s economic growth in 2011/12 led 31% of Brazilians to say that they intended to reduce international travel in 2013 (as against the corresponding figure of 20% in 2012)14, but this was not borne out in practice. The trend sees the bulk of growth to be for trips within the Americas (up 10% in the first eight months of 2013), with a lower 2% rise in trips outside the Americas. Short trips (less than 4 nights) – where shopping is a prime motivation – increased by 16% between January and August 2013, while longer trips rose by just 1%. For 2014, 43% of South Americans plan to travel more abroad15.

9 2011 Market Profile: Brazil. http://travel.trade.gov/outreachpages/download_data_table/2011_Brazil_Market_Profile.pdf, Fast Facts United States Travel and Tourism Industry 2009, 2010, 2011, 2012, 2013 and Top Ten International Markets: 2013 Visitation and Spending all available through

http://travel.trade.gov/outreachpages/inbound.general_information.inbound_overview.html. National Travel and Tourism Office, International Trade Administration, US Department of Commerce

10 European Tourism in 2014: Trends and Prospects. Quarterly Report (Q1 2014). May 2014. Tourism Economics. ETC

11 US Commerce Department Forecasts Continued Strong Growth for International Travel to the United States 2014-2018. April 2014. National Travel and Tourism Office, International Trade Administration, US Department of Commerce. http://travel.trade.gov/view/f-2000-99-001/forecast/Forecast_Summary.pdf

12 UNWTO Tourism Highlights, 2013 Edition, UNWTO.13 Forecast of International Travelers to the United States by Top Origin Countries. US

Department of Commerce, ITA, National Travel and Tourism Office. April 2014.14 ITB World Travel Trends Report 2012/13 IPK International Dec 2012 http://www.itb-

berlin.de/media/itbk/itbk_media/itbk_pdf/WTTR_Report_2013_web.pdf 15 Ibid

South American countries and the

United States most benefit from Brazilian

outbound travel growth

16

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Europe attracts 54% of total Brazilian long-haul arrivals

The significant risk to increased Brazilian outbound travel and spending is the December 2013 introduction of an additional 6% surcharge introduced by the Government of Brazil on credit card and traveller cheque purchases, as well as cash withdrawals made overseas16.

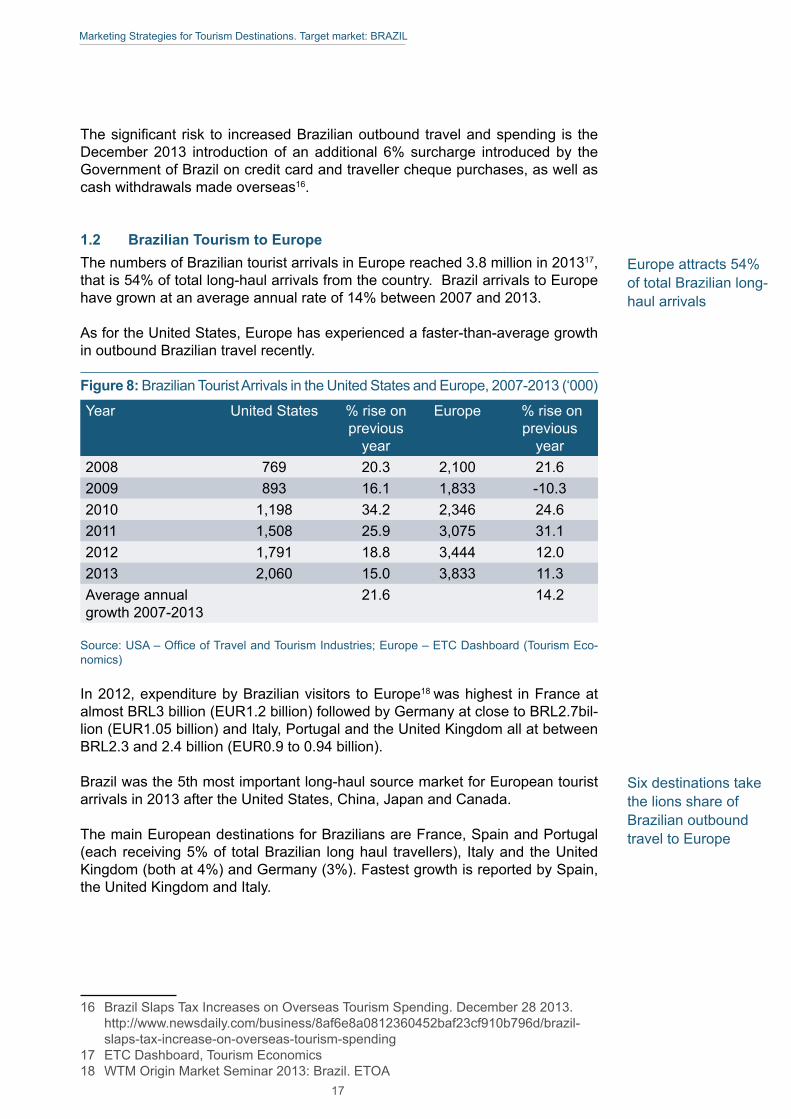

1.2 Brazilian Tourism to EuropeThe numbers of Brazilian tourist arrivals in Europe reached 3.8 million in 201317, that is 54% of total long-haul arrivals from the country. Brazil arrivals to Europe have grown at an average annual rate of 14% between 2007 and 2013.

As for the United States, Europe has experienced a faster-than-average growth in outbound Brazilian travel recently.

Figure 8: Brazilian Tourist Arrivals in the United States and Europe, 2007-2013 (‘000)

Year United States % rise on previous

year

Europe % rise on previous

year2008 769 20.3 2,100 21.62009 893 16.1 1,833 -10.32010 1,198 34.2 2,346 24.62011 1,508 25.9 3,075 31.12012 1,791 18.8 3,444 12.02013 2,060 15.0 3,833 11.3Average annual growth 2007-2013

21.6 14.2

Source: USA – Office of Travel and Tourism Industries; Europe – ETC Dashboard (Tourism Eco-nomics)

In 2012, expenditure by Brazilian visitors to Europe18 was highest in France at almost BRL3 billion (EUR1.2 billion) followed by Germany at close to BRL2.7bil-lion (EUR1.05 billion) and Italy, Portugal and the United Kingdom all at between BRL2.3 and 2.4 billion (EUR0.9 to 0.94 billion).

Brazil was the 5th most important long-haul source market for European tourist arrivals in 2013 after the United States, China, Japan and Canada.

The main European destinations for Brazilians are France, Spain and Portugal (each receiving 5% of total Brazilian long haul travellers), Italy and the United Kingdom (both at 4%) and Germany (3%). Fastest growth is reported by Spain, the United Kingdom and Italy.

16 Brazil Slaps Tax Increases on Overseas Tourism Spending. December 28 2013. http://www.newsdaily.com/business/8af6e8a0812360452baf23cf910b796d/brazil-slaps-tax-increase-on-overseas-tourism-spending

17 ETC Dashboard, Tourism Economics18 WTM Origin Market Seminar 2013: Brazil. ETOA

Six destinations take the lions share of Brazilian outbound travel to Europe

17

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Total arrivals to Europe will approach

4 million a year by 2019

Purchasing power is spreading lead by the most affluent cities in

South East Brazil

USA

Argentina

1.6mn

1.4mn

0.5mn

0.4mn

0.4mn

UK

Germany

0.4mn

0.4mn

0.3mn

0.3mn

0.2mn

Uruguay

France

Spain

Portugal

Chile

Italy

Source: ETOA WTM 2013 Presentation based on Euromonitor International StatisticsNote: Based on departures.

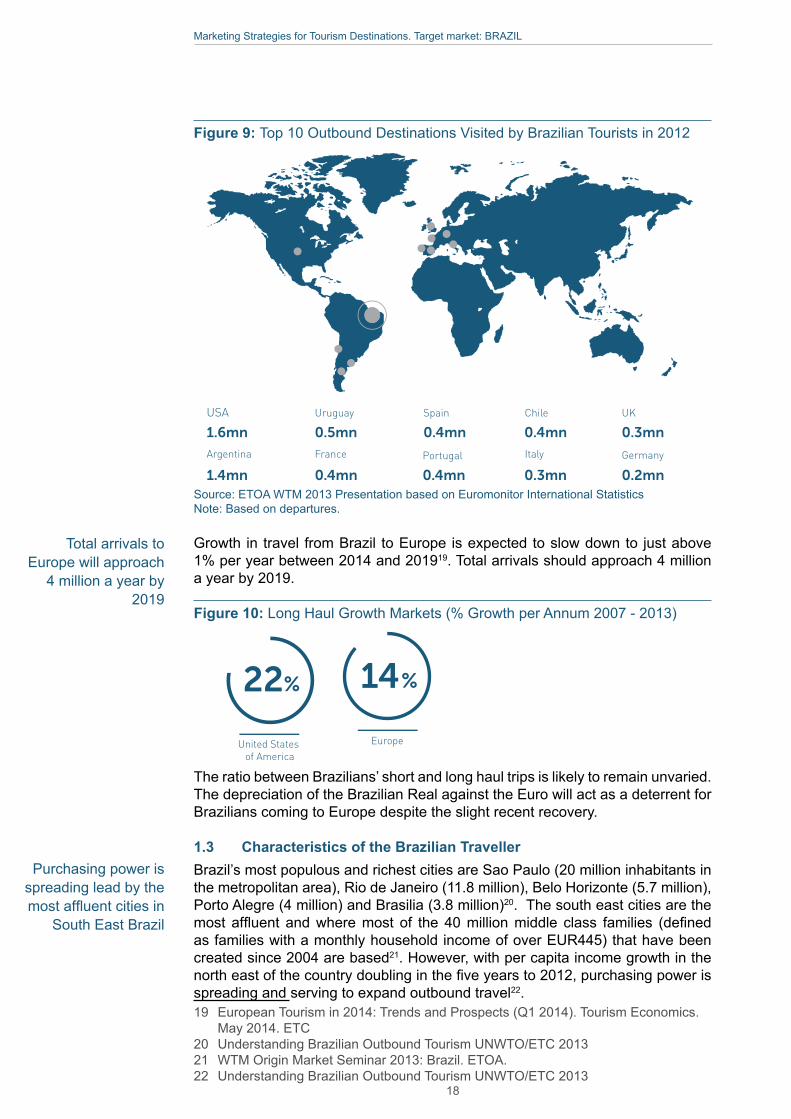

Growth in travel from Brazil to Europe is expected to slow down to just above 1% per year between 2014 and 201919. Total arrivals should approach 4 million a year by 2019.

Figure 10: Long Haul Growth Markets (% Growth per Annum 2007 - 2013)

22

United States of America

14

Europe

The ratio between Brazilians’ short and long haul trips is likely to remain unvaried. The depreciation of the Brazilian Real against the Euro will act as a deterrent for Brazilians coming to Europe despite the slight recent recovery.

1.3 Characteristics of the Brazilian TravellerBrazil’s most populous and richest cities are Sao Paulo (20 million inhabitants in the metropolitan area), Rio de Janeiro (11.8 million), Belo Horizonte (5.7 million), Porto Alegre (4 million) and Brasilia (3.8 million)20. The south east cities are the most affluent and where most of the 40 million middle class families (defined as families with a monthly household income of over EUR445) that have been created since 2004 are based21. However, with per capita income growth in the north east of the country doubling in the five years to 2012, purchasing power is spreading and serving to expand outbound travel22.19 European Tourism in 2014: Trends and Prospects (Q1 2014). Tourism Economics.

May 2014. ETC20 Understanding Brazilian Outbound Tourism UNWTO/ETC 201321 WTM Origin Market Seminar 2013: Brazil. ETOA.22 Understanding Brazilian Outbound Tourism UNWTO/ETC 2013

Figure 9: Top 10 Outbound Destinations Visited by Brazilian Tourists in 2012

18

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Figure 11: Demographic and Economic Facts

Brazilian long haul outbound travel tends to be concentrated in the Brazilian win-ter months – i.e. June to August – and the Christmas/New Year period (particu-larly to the United States) for shopping purposes. There is a more even pattern to European destinations with significant numbers of Brazilian students. In 2012 there were estimated to be 365,000 Brazilians studying overseas23.

The bulk of short haul and all long haul travel is by flight. Low cost carriers oper-ate principally on domestic routes; and their penetration on international routes is just 10%, with no services to long haul destinations24.

A cornerstone of Brazilian lifestyle is enjoying life to the fullest, having fun and being able to spend on material goods and experiences. Travelling abroad is a natural extension of this lifestyle, traditionally exercised by wealthy Brazilians, but fast becoming affordable to the masses25.

The greatest growth in Brazilian outbound travel is for leisure purposes which have increased market share. Business trips accounted for 30% of all departures in 2012.

The predominant motivation for Brazilians to visit the United States is shopping. The most common activities on trips to the United States were shopping (95% of visitors from Brazil), dining in restaurants (89%), visiting historical places (51%) and visiting amusement theme parks (47%). In all of these categories, the shares of Brazilian travellers were higher than the comparable average shares for all overseas visitors to the United States26.

23 Record Number of Brazilians Expected to Study Abroad in 2012. http://www.bmimedia.net/new/news-130116-record.php

24 Latin America Remains Drastically Under-served by Low Cost Carriers Outside Brazil and Mexico. CAPA Centre for Aviation. September 2013. http://centreforaviation.com/analysis/latin-america-remains-drastically-under-served-by-low-cost-airlines-outside-brazil-and-mexico-126325

25 Brazil Outbound – March 2012. Mintel. http://store.mintel.com/brazil-outbound-march-2012?cookie_test=true

26 The Boom in Brazilians Travelling to the United States. Riker, D. and Vila-Goulding, J. Journal of International Commerce and Economics. United States International

Travel abroad is a natural extension of the Brazilian lifestyle

The United States are the preferred shopping destination

19

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

This shows significant differences from the pattern of Brazilian travel to Europe. Apart from travel for educational and VFR purposes, Europe is seen as the re-gion of culture with the different manifestations expressed through cuisine, fash-ion and music and dance as key attractors. Brazilian travellers to Europe have a wider variety of motivations and interest than those choosing the United States.There is a large and growing Brazilian diaspora in Europe which, along with deep cultural and historical ties, constitutes an important generator of Brazilian travel to Europe. Cultural attractions, shopping and education are other important factors.

Brazilians are influenced by a number of media in the travel planning process, which also serve as main sources of information. These include: television, found by 69% of Brazilians to be the most relevant and reliable source of information, featuring telenovelas (television dramas based in different destinations) and oth-er forms of television27, social media – Brazilians being the most active social media community28 - which is used to share experiences, and travel agents who are consulted by almost three-quarters of Brazilians planning an overseas trip29. People tend to buy international flight tickets, lodging and other services after they have selected their destination, rather than buying an entire package30.

About 15% of outbound trips are packages, about 45% involve pre-booked ac-commodation or local travel, and 40% involve neither31. Though three-out-of-four Brazilians consult a travel agent, only half book via an agent32.

Overall, leisure departures are split as follows: 42% alone, 23% couples, 15% families (but less on long haul trips), 19% groups33.

The Brazilian overseas travel market divides into three broad categories based on their travel preferences34 i.e.

• Group Travellers, most likely to take package tours,• Semi-independent Travellers, buying air and hotel packages but

with freedom on how to spend their time at the destination, including visits to friends and relatives,

• Independent Travellers, likely to search out the best deals and make reservations online, personalising their itineraries.

Trade Commission. January 2013. http://www.usitc.gov/journals/JICE_Boom_in_Brazilians_Traveling_to_US.pdf

27 Understanding Brazilian Outbound Tourism UNWTO/ETC 201328 Ibid29 The Travel Habits of Brazilians: U.S. Tops As Most Popular, Skift.com30 Understanding Brazilian Outbound Tourism UNWTO/ETC 201331 ETC Market Insights Brazil, 200932 The Travel Habits of Brazilians: U.S. Tops As Most Popular, Skift.com33 WTM Origin Market Seminar Brazil ETOA on Euromonitor data34 Understanding Brazilian Outbound Tourism UNWTO/ETC 2013

Travelling alone is common amongst

Brazilians

Television and social media are main sources of

information

Europe perceived as a region of

culture manifested in cuisine, fashion and

music

20

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Rapid economic expansion created a growing middle class interested in travelling abroad

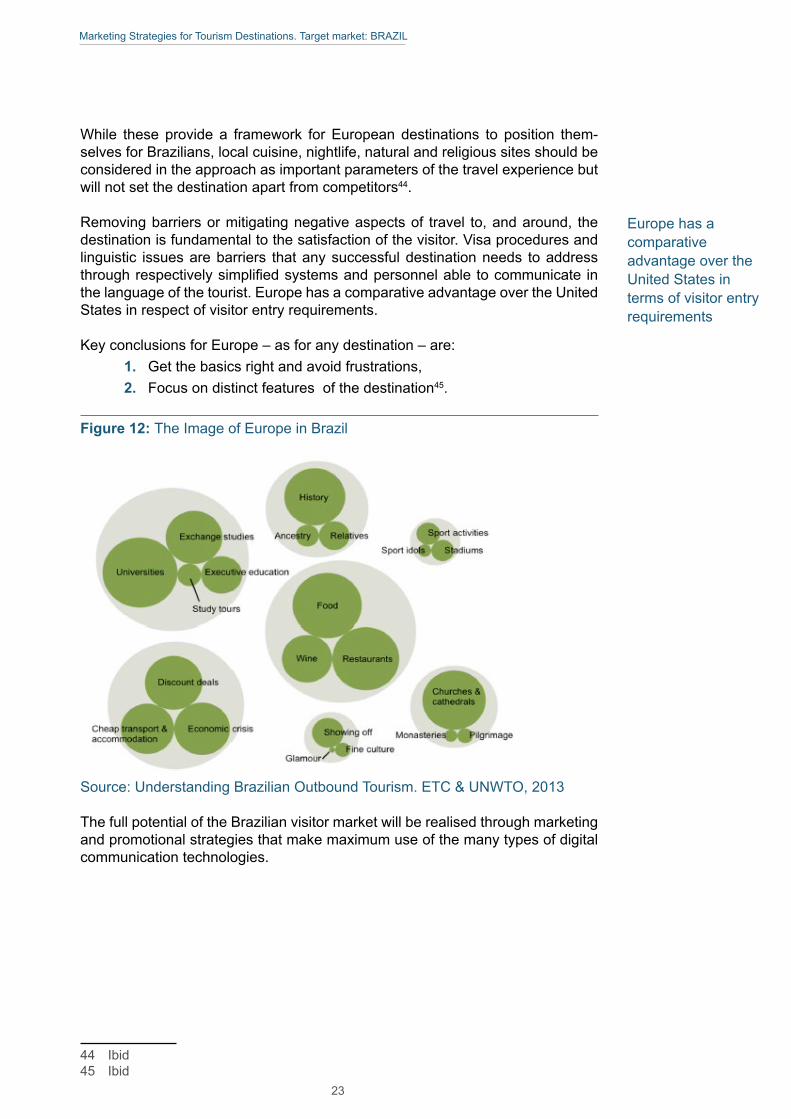

In the blogosphere, the discussion about Europe revolves around a select num-ber of themes and interests that are associated with Europe as a tourist destina-tion:35

• educational programmes,• seeking their roots – through the Brazilian diaspora in Europe esti-

mated at between three quarters of a million and a million,• glamour and prestige – all aspects of traditional and modern culture

i.e. performing arts, plastic arts, historic sites and buildings,• gastronomy,• religious tourism,• sports tourism.

There are three categories of Brazilian outbound traveller, each with their own preferences of things to do36 i.e.

• Status-related Motivations – visit as many places as possible, pho-tos posted online, exclusive artifacts purchased,

• Experience-centered Motivations – specific types of experience including relaxation, religious tourism, knowledge acquisition, gastro-nomic interests, sports, cultural origins and historical roots,

• People-centered Motivations – social connections, visits to friends and relations, seek historical roots.

1.4 Drivers of GrowthBrazil is the seventh largest economy in the world and the largest in Latin Amer-ica. In recent years, the country has been one of the fastest-growing economies in the world primarily due to its export potential. The country’s trade is driven by its extensive natural resources and diverse agricultural and manufacturing production. Also, rising domestic demand, and an increasingly skilled workforce along with scientific and technological development, have attracted foreign direct investment. The rapid expansion of the Brazilian economy has created an expanding middle class with both the resources (i.e. growth in household incomes and relatively easy access to credit) for, and interest in, foreign travel. With a growing dispos-able income but a tax system that puts high levies on imported products, many Brazilian consumers also like to travel for shopping. Currently, the United States is the high-end shopping destination of choice for Brazilian consumers37.

The Brazilian outbound travel market is maturing with outbound travel becoming accessible to more than the affluent and the Brazilian middle class expanding – with over 40 million additions since 200338. As a consequence, there is occurring growing diversification and segmentation.

35 Ibid36 Ibid37 Understanding Brazilian Outbound Tourism UNWTO/ETC 201338 WTM Origin Market Seminar Brazil ETOA on IMF data

Exploring European origins is a popular theme in the Brazilian blogosphere

21

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Though shopping is also an important element in Brazilians’ travel to Europe, the historical ties, the cultural heritage of the countries, and sports sites, theme parks and gambling are also strong draws39. Brazilian travel to Europe is affected by a large and growing diaspora, so it is common for Brazilian travellers to visit relatives and friends and to seek their roots on the Old Continent.

Key for destination marketers in Brazil is use of electronic media to supplement and complement traditional media in influencing prospective travel decisions. While the majority of Brazilians consult with a travel agent in considering their travel choice – 82% in the case of trips to Canada40 - and half book through agents, the main influences on trip planning are television travel shows, websites, magazine articles and travel advertising. Television remains the prime source of information and entertainment in the country41.

There are 70 million Brazilian internet users, and over 90% of long haul travellers use Facebook and other social networking sites, looking for special offers and sharing thoughts and opinions about travel destinations42. An example is travel to Canada43 where over a quarter of Brazilian travellers to the country recall having seen or heard about the destination through friends and family via social network.

1.5 Successful Destination StrategiesDestinations are intensifying their efforts to attract Brazilian tourists.

There are two key challenges for destinations:1. To ensure Brazilians are aware of the destination and its attractions

and tourism product offering, 2. To influence the perceptions held of the destination in line with the

products/experiences that appeal to Brazilians and which the desti-nation can provide.

This then provides destinations with the opportunity to clearly identify the aspects that resonate most with Brazilians and to focus on realising the potential in these segments.

For the leading long haul destination – the United States – the principal attrac-tions for Brazilians are shopping and entertainment experiences. Europe has a much broader range of prospective draws, but the variety of this offer is frequent-ly unknown to Brazilians.

Creating awareness of the range of tourist experiences across European coun-tries is the overriding need. Findings from the Brazilian blogosphere indicate that destinations in Europe can distinguish themselves in the eyes of the Brazilian traveller in three ways by focusing on either:

• culture and history,• shopping and recreation, • sports sites, theme parks and gambling.

39 ibid40 Ibid41 Ibid42 Ibid43 Ibid

Europe has a broad range of prospective draws for Brazilians

Digital technology is essential to

complement traditional media

22

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

While these provide a framework for European destinations to position them-selves for Brazilians, local cuisine, nightlife, natural and religious sites should be considered in the approach as important parameters of the travel experience but will not set the destination apart from competitors44.

Removing barriers or mitigating negative aspects of travel to, and around, the destination is fundamental to the satisfaction of the visitor. Visa procedures and linguistic issues are barriers that any successful destination needs to address through respectively simplified systems and personnel able to communicate in the language of the tourist. Europe has a comparative advantage over the United States in respect of visitor entry requirements.

Key conclusions for Europe – as for any destination – are:1. Get the basics right and avoid frustrations, 2. Focus on distinct features of the destination45.

Figure 12: The Image of Europe in Brazil

Source: Understanding Brazilian Outbound Tourism. ETC & UNWTO, 2013

The full potential of the Brazilian visitor market will be realised through marketing and promotional strategies that make maximum use of the many types of digital communication technologies.

44 Ibid45 Ibid

Europe has a comparative advantage over the United States in terms of visitor entry requirements

23

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Based on the investigations and research conducted into recent trends in Bra-zilian visitor flows and the comparative assessment that introduces this report, a short list of four destinations was selected for further examination in respect of the Brazilian markets. The four – in alphabetical order – are:

1. Australia,2. Mexico,3. Russian Federation,4. United States.

The remainder of this chapter illustrates the positioning of these countries in the Brazilian market as compared to Europe. The positioning is assessed on factors that facilitate tourism flows, such as visa regimes, transport routes, and the polit-ical, socio-economic and cultural links between Brazil and each destination.

This section is enriched by an analysis of TripAdvisor ratings on accommodation, attractions and eateries, presented in Appendix 3. While not representative of Brazilian travellers, TripAdvisor ratings are used as a proxy for consumers’ ap-preciation of key aspects of a holiday experience across competing destinations.

2.1 Visa RegimesThe detailed comparison of visitor entry requirements for the selected 13 destina-tions competing with Europe considered three elements:

1. Whether the destination imposes a visa requirement for entry to the country,

2. The documentation and other details demanded for issuance of a visa,

3. A qualitative assessment of the “hassle” factor involved in obtaining the visa.

Among the four countries selected as prime competitors to Europe in the Bra-zilian market, Brazilian travellers require visa for entry to the United States and Australia whereas there is no such requirement for travel to Mexico, the Russian Federation or ETC member countries.

The United States’ visa process is a major barrier for growth compared to com-petitor destinations. Brazilians have to obtain visas in advance of arrival in what is considered a complex process, though recent steps have sought to ease the complexity and speed up the process for Brazilians obtaining their entry visas to the United States. This streamlining of the United States visa process, through the expansion of processing facilities, and increased consular staffing, is one of the factors behind the strong growth of tourism flows from Brazil to the United States.

Travel Destinations in the Brazilian Market2

24

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Australia also imposes visa entry requirement for Brazilians in advance of travel though application can be made online and no interview is required under normal circumstances.

Mexico and Russia do not impose a visa requirement on Brazilians unless stay-ing for over 90 days (in the case of Russia) or 180 days (for Mexico).

Since 2010, Russian and Brazilian tourists are not required to have visas for en-try, exit, transit or stay in the territory of each other’s state for up to 90 days within each 180-day period from the first entry.

In 2013, the governments of Mexico and Brazil agreed to the exemption of the short-stay visas in ordinary passports for their citizens, a move designed to in-crease the flow of travellers between the two nations. The visa requirement for Brazilians had been in force since 2005, and from May 2010 Mexico permit-ted entry to Brazilian citizens with a United States visa; moreover, the Migration Documentation Information System (SIDOMI) and the System of Electronic Au-thorisation (SAE) allowed Brazilian tourists and businessmen to obtain electronic visas.

By contrast Brazilians do not require visas when travelling to European countries. European Union countries grant visa free access through the Schengen agree-ment while other ETC members and non-ETC member European countries have followed suit and grant visa free entry to Brazilians. There are no particular medical requirements in the form of certificates or other aspects imposed on Brazilian tourists by any of the four destinations.

Figure 13: Visa Requirements of Brazilian Travellers in Key Destinations

Destination Yes/No (Y/N) Requirements/ProcessAustralia Y Prior to travel, application to Australian

authorities in Brazil, in person or online. Visitor visa sub-class 600 required. Travel documentation required from a recognised authority. AUD130 (US$121, EUR90

Mexico N No visa required unless staying over 180 days. Advisable to have onward ticket.

Russian Federation

N No visa required for stays of up to 90 days; visa required for stays of 90 to 180 days. Onward travel documentation required.

United States Y Prior to travel application to US authorities in Brazil. Attend interview with passport. Between 2 and 7 days interview, followed by one week plus processing. From US$160- EUR118.

ETC Members N No visa required for stays of up to 3 months in Schengen member countries. No visa required for visits to non-Schengen ETC members (Bulgaria, Croatia, Ireland, Romania, Serbia) nor to non-Schengen, non-ETC members e.g. the United Kingdom

25

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

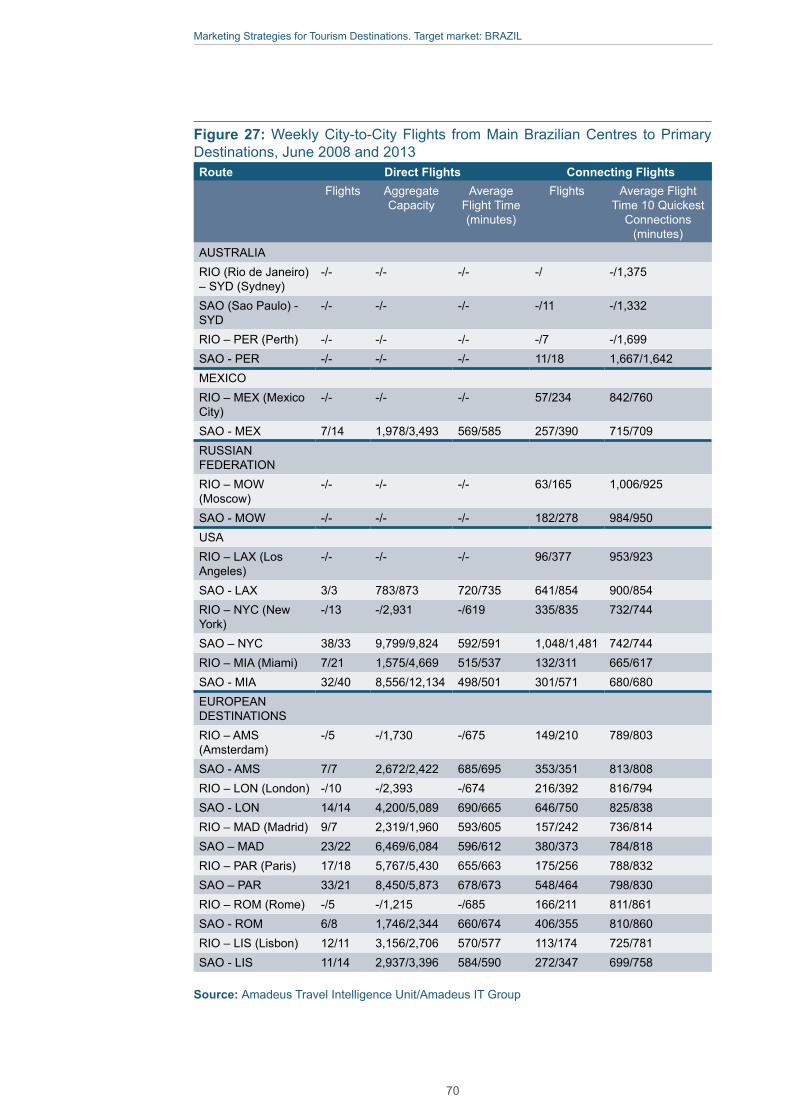

Frequent direct flights to US cities

Capacity to European gateways

may be improved

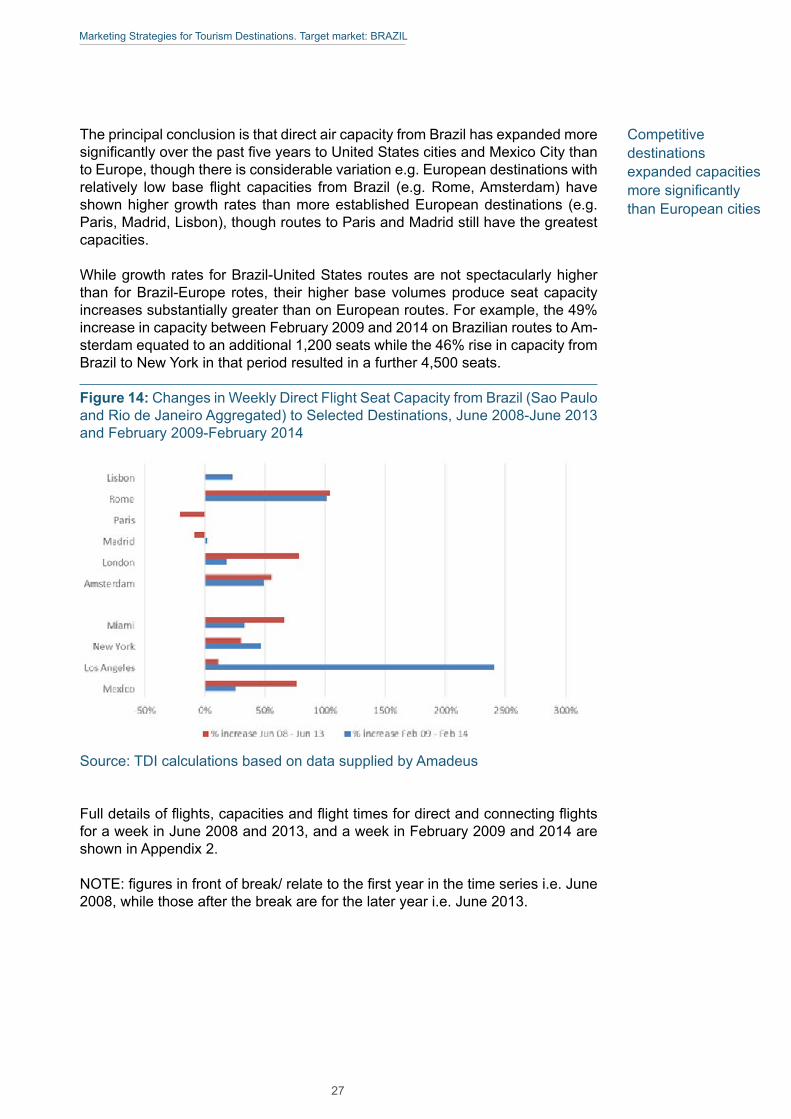

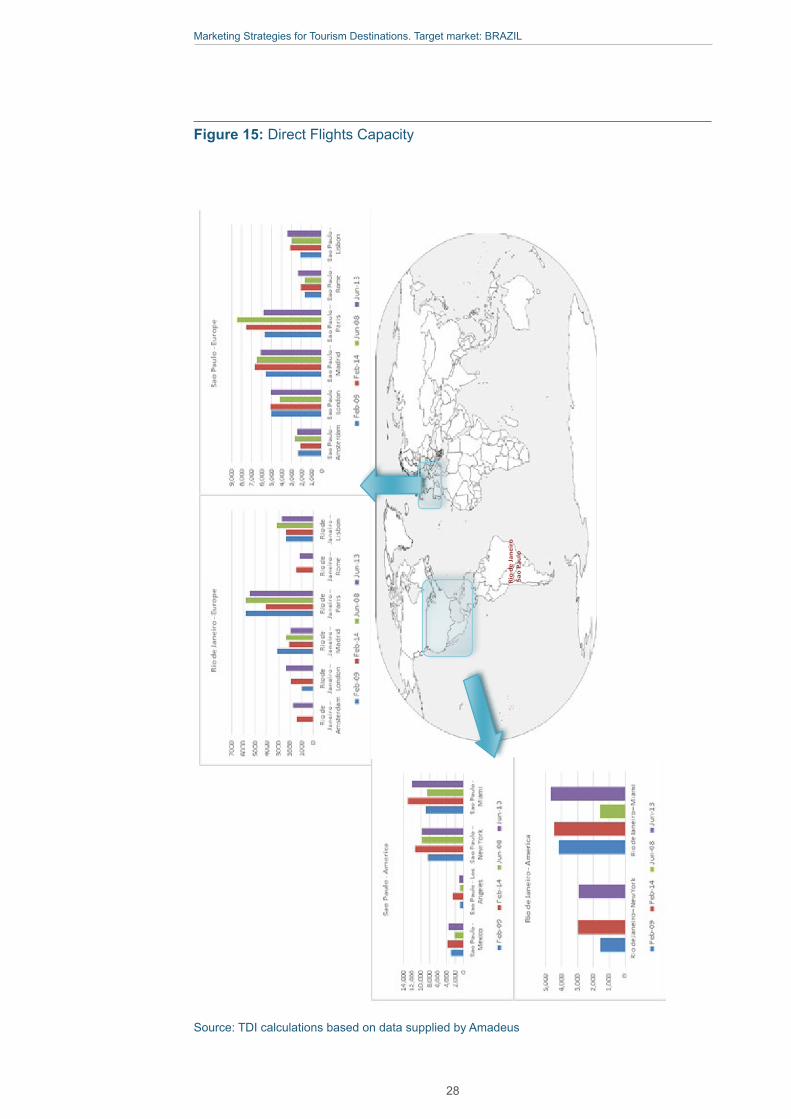

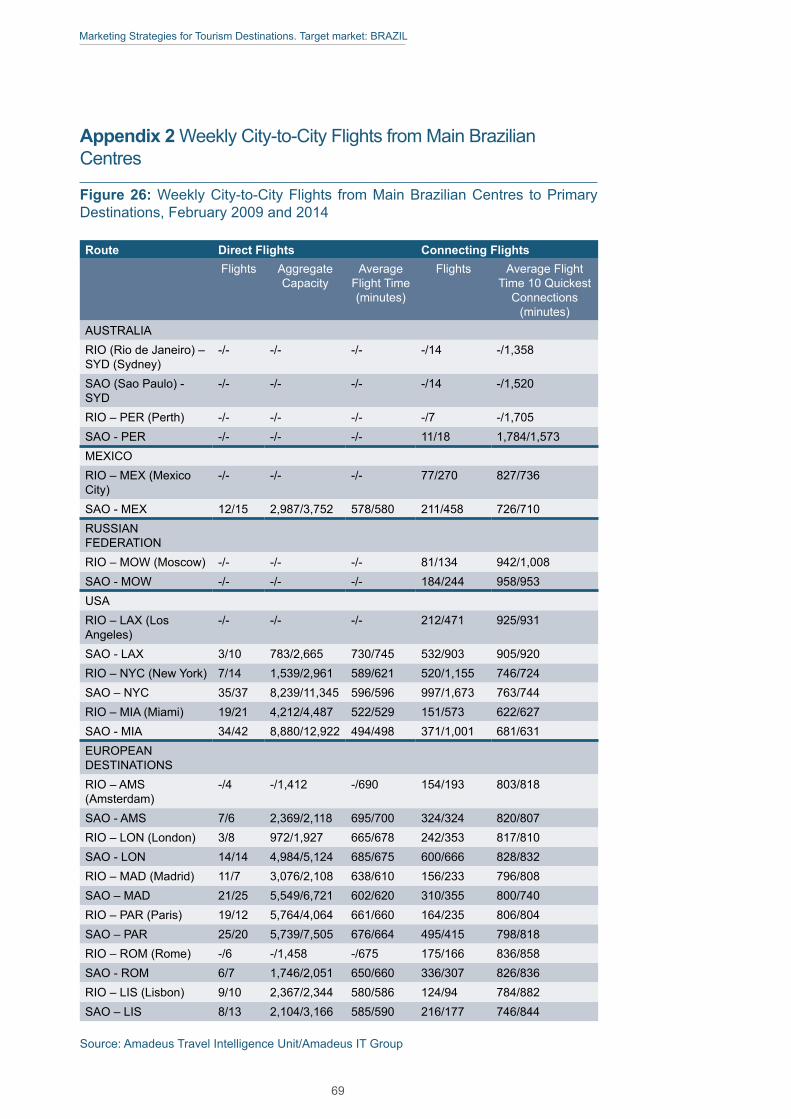

2.2 Air ConnectionsThe scheduled air capacity from Brazil’s two principal international air gateways to both shortlisted competing destinations and major European cities was mon-itored on ETC’s behalf by Amadeus. Two points in the year were examined – week 24 in 2013 (broadly corresponding to high season) and week 6 in 2014 (low season), though this can only be taken as an approximate measure given the difference in northern and southern hemisphere climates at the different times of the year. Data for two years were considered in order to provide an indication of the trend in capacity on the various routes i.e. June 2008/June 2013, and Febru-ary 2009/February 2014.

Of the observed destinations, those with the greatest frequencies of direct flights and capacities are the United States cities of Miami and New York. The aggre-gate direct flight seat capacity from the two main Brazilian airports of Sao Paulo and Rio de Janeiro to these United States cities ranges between 29,500 (June 2013) and 31,700 (February 2014), having grown over the five year period ex-amined by between 39% (February) and 48% (June). The west coast city of Los Angeles has no direct air service from Rio de Janeiro but is served through air capacity from Sao Paulo by between 900 and 2,700 seats depending on the time of the year. These levels rose by 11% between June 2008 and June 2013, and over threefold between February 2009 and the same month in 2014, as a new American Airlines flight started operations in November 2013.

The leading European destinations are Paris, Madrid, Lisbon and London. Direct seat capacity to Paris from the two Brazilian airports was 11,300 on June 2013, and slightly higher at 11,600 on February 2014, but while the February-February capacity remained the same between 2009 and 2014, the June–June seats fell by over 20% between 2008 and 2013. Direct service seat capacity to Madrid ranges between 8,000 (June 2013) and 8,800 (February 2014). There was a small decline in the numbers of direct seats available. For Lisbon, aggregate direct seat capacity from the two Brazilian airports ranges between 5,500 and 6,000 depending on time of year and has shown little change over the five-year period. For London, direct seat capacity from Brazil has increased – from 4,200 in June 2008 when no direct flights were operated between Rio de Janeiro and London - to 7,400 in June 2013; and from 5,900 to 7,000 between February 2009 and 2014, rises of 76% and 18% respectively.

Direct air seat capacity from Sao Paulo to Mexico City totaled 3,500 in June 2013 and 3,800 in February 2014, up by 75% and 25% respectively over the corre-sponding months in 2008 and 2009. There are no direct air services between Rio de Janeiro and Mexico City.

There are no direct air services between the two main Brazilian airports and the principal airports in Australia (i.e. Sydney, Perth) or to the Russian Federation.

The average travel time for the best 10 connecting services between Brazil and Australia involves a journey time of 24 hours, while for Moscow the flight time is between 16 and 17 hours. This contrasts with the average direct flight times to the east coast United States cities and Mexico City of between 8.5 and 10 hours, and to European destinations of between 10 and 11.5 hours.

26

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Competitive destinations expanded capacities more significantly than European cities

The principal conclusion is that direct air capacity from Brazil has expanded more significantly over the past five years to United States cities and Mexico City than to Europe, though there is considerable variation e.g. European destinations with relatively low base flight capacities from Brazil (e.g. Rome, Amsterdam) have shown higher growth rates than more established European destinations (e.g. Paris, Madrid, Lisbon), though routes to Paris and Madrid still have the greatest capacities.

While growth rates for Brazil-United States routes are not spectacularly higher than for Brazil-Europe rotes, their higher base volumes produce seat capacity increases substantially greater than on European routes. For example, the 49% increase in capacity between February 2009 and 2014 on Brazilian routes to Am-sterdam equated to an additional 1,200 seats while the 46% rise in capacity from Brazil to New York in that period resulted in a further 4,500 seats. Figure 14: Changes in Weekly Direct Flight Seat Capacity from Brazil (Sao Paulo and Rio de Janeiro Aggregated) to Selected Destinations, June 2008-June 2013 and February 2009-February 2014

Source: TDI calculations based on data supplied by Amadeus

Full details of flights, capacities and flight times for direct and connecting flights for a week in June 2008 and 2013, and a week in February 2009 and 2014 are shown in Appendix 2.

NOTE: figures in front of break/ relate to the first year in the time series i.e. June 2008, while those after the break are for the later year i.e. June 2013.

27

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Figure 15: Direct Flights Capacity

Source: TDI calculations based on data supplied by Amadeus

Tourism Strategy of Europ

e’s Main Co

mpe

titors– Brazil R

eport

32

Fig

ure

12

- D

ire

ct

Flig

hts

Ca

pa

city

So

urc

e:

TDI c

alc

ula

tio

ns

ba

sed

on

da

ta s

up

plie

d b

y A

ma

de

us

Rio de Jane

iro

Sao

Pau

lo

28

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Relationship between Brazil and Australia has grown closer in recent years

Brazil and Mexico do not have an extensive history of bilateral socio-cultural links

2.3 Political, Economic and Socio-Cultural LinksWith the rapid growth of the Brazilian economy in recent decades, the large pop-ulation base – just under 200 million – with a rapidly expanding middle class, and the presence of a large diaspora around the world, Brazilians’ desire and ability to engage in foreign travel is being encouraged and facilitated by many destinations. Travel for family, education and business purposes is an important supplement and complement to leisure purposes travel.

Australia and Brazil entered into a Strategic Partnership in 2012 “with a view to giving expression to the deepening ties and growing shared role of the two countries in the world”46. It encompasses political, social and economic relations, in areas such as trade, investment, energy, agriculture, science and technology, education, judicial affairs, sports and culture.

Brazil is Australia’s largest trading partner in South America, with two-way mer-chandise trade between Australia and Brazil totalling AUD1.628 billion in 2012 (EUR1.28 billion), of which imports from Brazil amounted to AUD638 million (EUR502 million), mainly comprised of civil engineering equipment and parts, medicaments, coffee and fruit juices.

According to the 2011 Census, over 14,500 Australians were born in Brazil while more than 12,000 claimed Brazilian ancestry47. There have been two waves of immigration, one in the 1970s and the other starting in the 1990s and continuing to the present day.

Though tourist flows between Australia and Brazil are relatively small at present – just 34,200 Brazilians visiting Australia in 2013 – and will not increase substan-tively without direct scheduled air services, both countries are determined to step up their promotion and facilitation of travel between their nations. Australia is seen very positively by Brazilians. Global Tourism Watch 2012 found that 73% of Brazilians who had visited Australia would recommend it for a holiday – NB this is a net score subtracting detractors from promoters – the highest rating across all long haul destinations48

Mexico and Brazil represent more than half of the population, territory and eco-nomic development in Latin America and, as such, are considered as regional powers by analysts. Relations between the two countries remain good. In the economic area, both are members of the Latin American Integration Association (ALADI), the G8+5 (Brazil and Mexico being two of the 5 leading emerging econ-omies added to the eight major industrialised nations), and the G-20 group of Finance Ministers and Central Bank Governors.

46 Brazil-Australia Strategic Partnership, July 2012. http://www.brazil.embassy.gov.au/bras/StrategicPartnershipStrategicPartnership.html

47 Australian Government - Department of Immigration and Border Protection.48 Brazil Market Profile, January 2013. Canadian Tourism Commission. http://en-

corporate.canada.travel/sites/default/files/pdf/Research/Market-knowledge/Market-profile/Brazil/br_market_profile_2013_jan-2013.pdf

29

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Brazil-Mexico trade is relatively small, at US$8 billion (EUR6 billion) in goods and services annually. That compares to United States trade of US$500 billion (EUR370 billion) with Mexico and US$50 billion (EUR37 billion) with Brazil. The 2010 agreement at presidential level for a special economic pact stalled, in part because Mexican businesses were uneasy about encouraging competition from Brazil’s booming economy, and because of Brazilian concerns about the high level of Mexican car imports – US$2.4 billion (EUR1.8 billion) in 2011 – resulting in a quota being imposed on the import of Mexican cars into Brazil49.

Brazilian investment in Mexico is relatively small. Brazil‘s Odebrecht (which works in fields including construction, chemicals, and engineering) plans to in-vest US$8.1 billion (EUR6 billion) in Mexico’s infrastructure in the next five years, almost seven times the level of investment of Brazilian companies in Mexico since 199950. Colonised by opposing European nations, Brazil and Mexico do not have a long or extensive history of bilateral socio-cultural links.

Brazil-Russia relations have seen a significant improvement in recent years, demonstrated through the signing of a Strategic Alliance in 2005. Trade between the two countries is presently valued at close to US$6 billion (EUR4.5 billion), and a goal was set at the 6th Russia-Brazil cooperation commission in February 2013 to increase the level to US$10 billion (EUR7.4 billion) over the next three years. Brazil is a major supplier of agricultural products to Russia while Russia is seek-ing to be involved in Brazil’s plans to build new nuclear power stations to meet surging demand for electricity that has overwhelmed its generating capacity.

The two states are cooperating in sectors like aircraft building, metals, chemical and pharmaceutical industries, biotechnologies, and energy, including atomic en-ergy, as well as space.

The two countries signed visa exemption agreements in 2008.

There are few historical or cultural links between the two countries – and only a small number of Brazilians live in Russia. In consequence, Brazilians are not well informed about Russia. In a 2012 Pew Global Attitudes Project survey, 29.5% of Brazilians stated that they viewed Russia favourably as against 57% who saw it unfavourably51.

The United States and Brazil have enjoyed generally close relations for 200 years. The two countries currently cooperate on trade issues, HIV/AIDS efforts, regional concerns, and the international peacekeeping operation in Haiti.

49 Mexico’s next leader wants more trade with Brazil, not less. Reuters. 20 September 2012. http://www.reuters.com/article/2012/09/20/us-mexico-brazil-autos-idUSBRE88J1FD20120920

50 Brazil Institute, Wilson Center. http://brazilportal.wordpress.com/tag/brazil-mexico-relations/

51 Brazil Russia Relations. http://en.wikipedia.org/wiki/Brazil%E2%80%93Russia_relations

Brazil is a major supplier of

agricultural products to Russia

Brazil-Russia relations are

manifested in mutual visa exemption

30

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

Brazil is the world’s seventh largest economy and the United States’ eighth-largest merchandise trading partner. Two way trade in 2012 was a record US$76 billion (EUR58 billion). The United States had a record US$11.6 billion (EUR8.9 billion) trade surplus with Brazil in 2012 representing the sixth highest surplus market for the United States. Brazil’s main imports from the United States are machinery, chemicals, aircraft/spacecraft, and computer and electronic products52..

The United States is Brazil’s second largest export market. The United States is the leading foreign investor in Brazil, with an accumulated foreign direct invest-ment stock in 2012 of US$79 billion (EUR61 billion). Brazilian investment in the United States has grown rapidly. In 2012, Brazil was named one of ten countries for the SelectUSA pilot programme to attract foreign investment to the United States. As the world’s largest biofuels producers, the United States and Brazil have worked together to help make sustainable biofuels a global commodity53.

There is a large Brazilian population in the United States. Of the total Brazilian diaspora of 1.5 million, almost one third – 450,599 – live in the United States. In addition there were a quarter of a million Brazilian Americans recorded in the 2007 American Community Survey. Estimates of the total numbers of people living in the United States with Brazilian heritage range up to over 1 million. The heaviest concentrations are in Florida, New York, other north eastern states and California.

Global Tourism Watch 2012 found that 59% of Brazilians who had visited the United States would recommend it for a holiday (i.e. net score after deducting detractors from promoters), the same level as for Canada but lower than record-ed for the European destinations of France (71%), Italy (70%), and the United Kingdom (63%)54.

The relationship between EU and Brazil is moving towards a strategic one based on shared interests and values, and greater coherence between different areas of cooperation. Three windows of opportunity are identified. In the bilateral sphere, a greater convergence in renewable energies beckons. At the interregional level, a formula needs to be found for a free trade agreement to be signed. In terms of the global agenda, Brazil and the EU can strengthen cooperation in Africa and adopt closer positions on matters of democracy and human rights55.

The EU is Brazil’s first trading partner, accounting for 1% of its total trade and Brazil is the EU’s eight trading partner, accounting for 2% of total EU trade (2012). EU imports from Brazil are dominated by primary products, in particular agricul-tural products (44%) and fuels and mining products (28%); while EU’s exports to Brazil consist mainly of manufactured products, such as machinery, transport equipment and chemicals.

52 US Relations with Brazil. October 2 2013. US Department of State. http://www.sate.gov/r/pa/ei/bgn/35640.htm

53 Ibid54 Brazil Market Profile, January 2013. Canadian Tourism Commission. http://en-

corporate.canada.travel/sites/default/files/pdf/Research/Market-knowledge/Market-profile/Brazil/br_market_profile_2013_jan-2013.pdf

55 Brazil and Europe Towards 2015. FRIDE Policy Brief. Gratius, S. http://www.fride.org/descarga/PB_67_Brazil_Europe_2015_Eng.pdf

The EU is Brazil’s first trading partner and foreign investor

The United States is Brazil’s second largest export market

One third of the total Brazilian diaspora live in the United States

31

Marketing Strategies for Tourism Destinations. Target market: BRAZIL

The EU is the biggest foreign investor in Brazil with investments in many sectors of the Brazilian economy. Around 50% of the FDI flows received by Brazil during the last 5 years originated in the EU56.

Brazil retains strong ties with Portugal, of which it was a colony, and there are close cultural links between the populations of the two countries. They have a common language, share much cultural heritage and are strong trading partners. There are 86,000 Brazilians living in Portugal, though if Brazilian Portuguese are included the figure is nearer 140,000. Other European countries with significant volumes of Brazilian diaspora are Spain, the United Kingdom, Germany, Italy, France, Switzerland, Belgium and the Netherlands which in total account for be-tween half and three quarters of a million57.

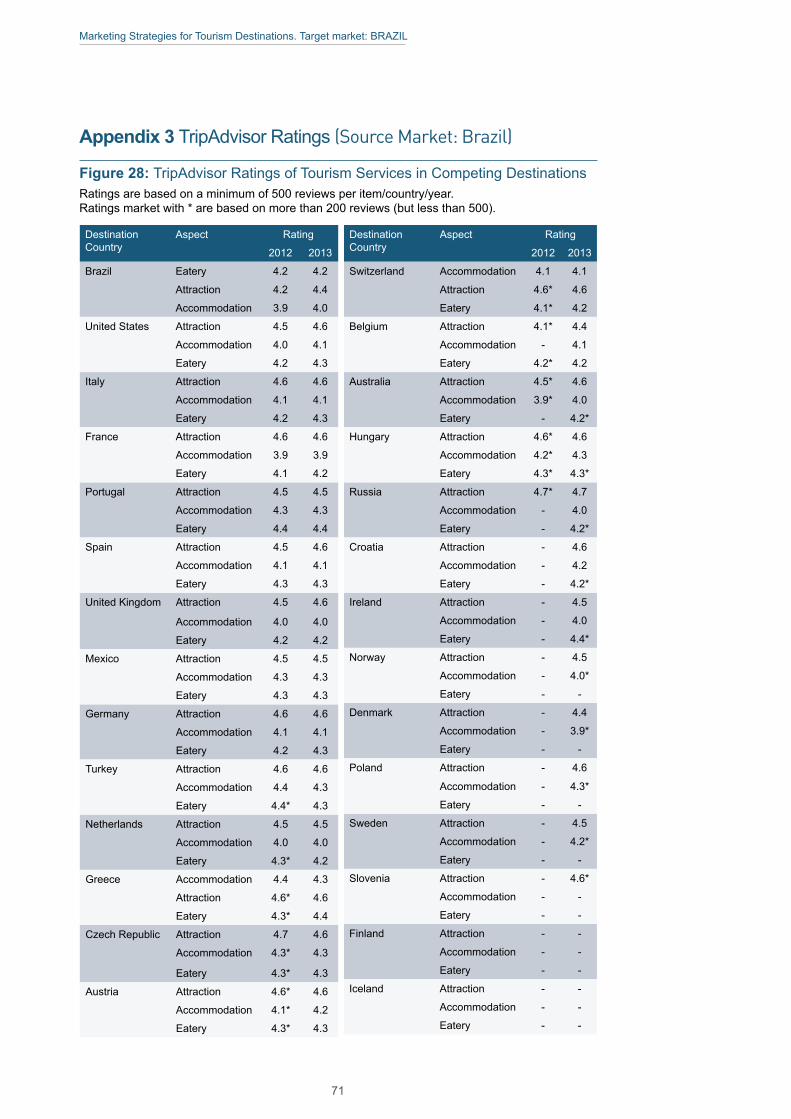

2.4 Consumer Assessment (TripAdvisor)This section presents an analysis of ratings provided by TripAdvisor users from Brazil on three elements of a visitor experience: attractions, accommodation and eateries. While not representative of Brazilian visitors’ behaviour, TripAdvisor rat-ings allow for cross-destination comparisons on components of a holiday experi-ence. The analysis covers the four destinations competing with Europe in Brazil (i.e. Australia, Mexico, Russian Federation and the United States), and four Euro-pean destinations used as benchmark in this study (i.e. France, Italy, Spain and United Kingdom). The results for European countries and competing destinations are presented in Appendix 3.

On average, TripAdvisor users from Brazil rate accommodation lower than either attractions or eateries, a finding that is common to all destinations. The highest rating (4.3) was achieved by Portugal and Mexico, followed by Spain and Italy at 4.1. Compared to quality of accommodation in their own country (4.0), Tri-pAdvisor users from Brazil are more satisfied with accommodation in these four destinations, equally satisfied with accommodation services in the United States, the United Kingdom, and the Russian Federation, while quality in France and Australia is slightly less satisfactory (3.9).

Average ratings for all destinations in Europe suggest that TripAdvisor users from Brazil were in general satisfied with accommodation (4.1). These visitors were most satisfied with the location (4.4), cleanliness and quality of sleep (both 4.3), and quality of service (4.2). They tended to be slightly less positive when evalu-ating the quality and value for money of the rented room (4.1).