Embed Size (px)

Citation preview

Quarterly UpdateQ4 - 2020

J a n u a r y 1 3 , 2 0 2 0

This material was used by Elliott Davis during an oral presentation; it is not a complete record of

the discussion. This presentation is for informational purposes and does not contain or convey

specific advice. It should not be used or relied upon in regard to any particular situation or

circumstances without first consulting the appropriate advisor. No part of the presentation may be

circulated, quoted, or reproduced for distribution without prior written approval from Elliott Davis.

Disclaimer

• Polling questions to complete

• Certificates will be emailed

CPE Credit• Submit questions during the

presentation

• Questions will be addressed at end or via email

Questions

• Sent out subsequent to presentation

• PowerPoint will also be available

Replay Link• Please submit any feedback

• Goal of always getting better

Feedback Welcomed

Housekeeping

Agenda

• Tax Update

• Financial Reporting Update

• PPP Update

Presenters

Jon Sutter Jennifer Goodman Kristin Kakidas Richard Battle Nick AnnanS e n i o r M a n a ge r,

A s s u ra n c eP r i n c i p a l , A s s u ra n c e

P r i n c i p a l ,A s s u ra n c e

S h a re h o l d e r, Tax

S e n i o r M a n a ge r, A c c e l e rate

[email protected]@elliottdavis.com [email protected]@[email protected]

HostFinancial Reporting

Update

Financial Reporting

Update

Tax Update

PPPUpdate

Financial Reporting Considerations for 2020 and Planning for the Future

EVERY company must perform a going concern

analysis at each reporting period regardless of

financial performance. True or False?

• Step 1 - Identify conditions that, in aggregate, raise substantial

doubt about ability to continue as going concern• Assessment period – 1 yr from report date

• Step 2 – Is it probable management’s plans will be effective

and relieve the substantial doubt?

Going Concern

Going Concern Footnote DisclosuresFinancial conditions footnote:

• (Required) Conditions raise substantial doubt about the ability to continue as agoing concern and it is probable management’s plans will mitigate thoseconditions

• (Required) Close-call scenarios that do not raise substantial doubt BUT requiredsignificant judgments/estimates

• (Optional) Conditions do not raise substantial doubt, but it would be helpful to theusers of the financial statements to understand financial results

Substantial doubt footnote:• It is not probable management’s plans will be effective and will alleviate

substantial doubt• Add emphasis-of-matter paragraph to audit opinion or accountants report

Financial Condition Footnote DraftWhile COVID-19 has negatively impacted financial results for all three ABC entities, ABC #3 has beenmost impacted due to low demand from its largest customer. ABC #3 has experienced operationallosses and negative operating cash flows for 2020. Production was impacted by COVID-19 plantshutdowns, global pricing pressures and product model changes.

As a result of these conditions, ABC #3 was closed for a period during 2020 and there was asignificant reduction in employee headcount. ABC #3 has relied on its existing working capital andshort-term lending from ABC #1 to help fund 2020 operations. Additionally, it obtained funding fromthe Paycheck Protection Program for $1 million.

During the fourth quarter of 2020, ABC #3 saw increases in production as management negotiatedfavorable pricing of products. Additionally, newly designed models were approved by the majorcustomer. Management was able to rehire many of the employees that had been furloughed orterminated as plant shutdowns and production delays caused by COVID-19 began to stabilize,although still not to pre-pandemic levels.. As of January 8, 2021, the short-term lending from ABC #1had been paid up to the current amount due and the note payments to ABC #1 were being made inaccordance with the agreement. No long-lived asset or goodwill impairment has been recognized as aresult of these matters as of December 31, 2020.

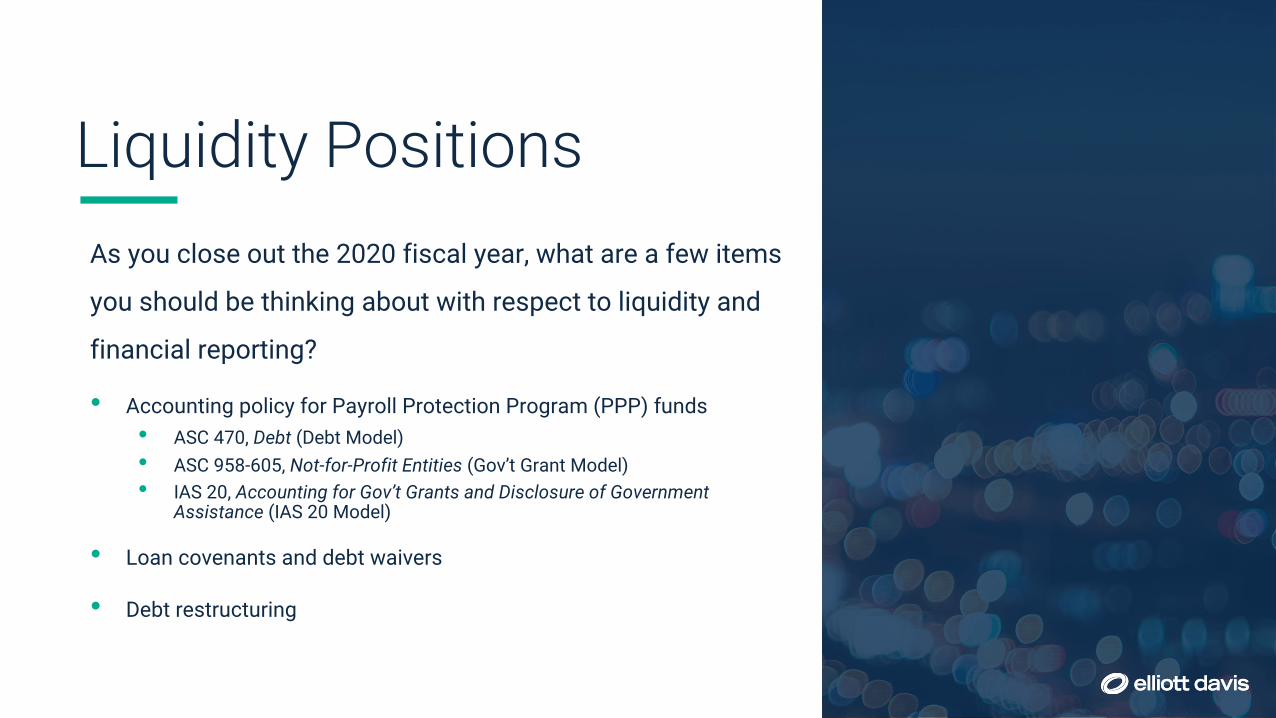

As you close out the 2020 fiscal year, what are a few items

you should be thinking about with respect to liquidity and

financial reporting?

• Accounting policy for Payroll Protection Program (PPP) funds• ASC 470, Debt (Debt Model)• ASC 958-605, Not-for-Profit Entities (Gov’t Grant Model)• IAS 20, Accounting for Gov’t Grants and Disclosure of Government

Assistance (IAS 20 Model)

• Loan covenants and debt waivers

• Debt restructuring

Liquidity Positions

Comparison of Forgiveness AccountingASC 470-50/405-20 ASC 958-605 IAS 20

Recognition threshold

When the debtor is legally released from being the primary obligor under the liability, either judicially or by the creditor (Legal defeasance)

When the conditions have been substantially met (when the conditional promise becomes unconditional)

When there is reasonable assurance the entity will comply with the conditions and the grants will be received

Timing and pattern of recognition

Immediately once the debtor is legally released

Immediately once the condition is substantially met (conditions could be met in stages, but would not be systematic recognition)

On a systematic basis over the periods in which the entity recognizes as expenses the related costs for which the grants are intended to compensate.

Presentation of income

Presented on a gross basis as gain or loss on extinguishment of debt

Presented on a gross basis (i.e., grant revenue or other income)

May be reported separately as “other income” or deducted from the related expense

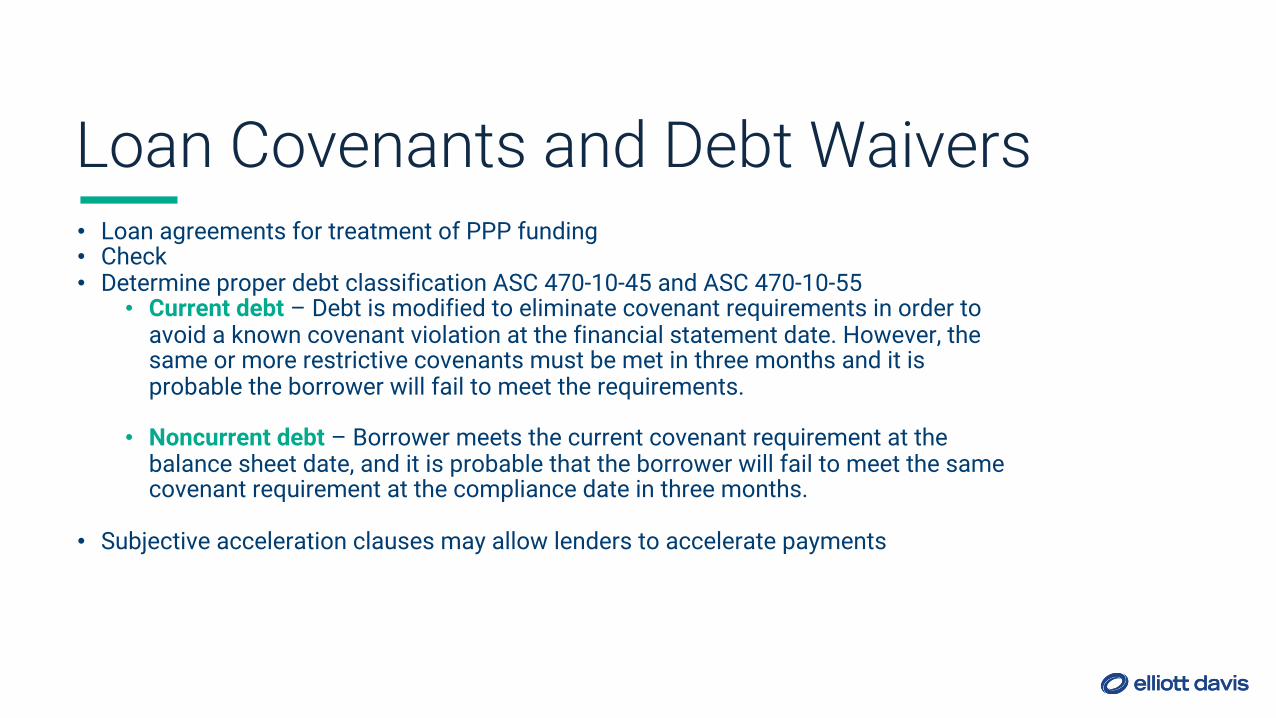

Loan Covenants and Debt Waivers• Loan agreements for treatment of PPP funding• Check• Determine proper debt classification ASC 470-10-45 and ASC 470-10-55

• Current debt – Debt is modified to eliminate covenant requirements in order to avoid a known covenant violation at the financial statement date. However, the same or more restrictive covenants must be met in three months and it is probable the borrower will fail to meet the requirements.

• Noncurrent debt – Borrower meets the current covenant requirement at the balance sheet date, and it is probable that the borrower will fail to meet the same covenant requirement at the compliance date in three months.

• Subjective acceleration clauses may allow lenders to accelerate payments

Debt Restructuring• There are 3 different accounting models: troubled debt restructuring, extinguishment

accounting and modification accounting.

• Depending on the model, you may have a gain/loss on the event

• Substantially different treatment of debt costs under each model

Accounting Model Fees between lender and borrower

Cost incurred with third parties

Unamortized debt discount/premium and

issuance cost on old debt

Extinguishment accounting Expensed Deferred as a debt issuance cost and amortized over term of new loan

Write off

Modification accounting

Deferred as a debt discount/premium and amortized over term of new loan

Expensed Continue to amortize over the term of the modified loan

Private companies need to start your assessment of ASU 2016-02 Leases Topic 842

Implementation date:

• Was – Years beginning after 12/15/2019

• Now – Years beginning after 12/15/2021

Modified retrospective transition approach for calendar year companies:

• Comparative method – apply at the beginning of earliest year presented (January 1, 2021)

• Effective date method – apply at beginning of reporting period in year of adoption (January 1, 2022)

Looking Ahead

Adopting Leases Topic 842 - Start Now!1. Create implementation timeline with all key steps

2. Review policy elections and practical expedients

3. Discuss your planned implementation approach with stakeholders

4. Educate and coordinate with functional departments (rental agreements ARE leases!)

5. Some areas may require more time than you think: determining the discount rate, identifying embedded leases, determining the lease term

6. Do you need to invest in specialized software?

Polling Question

#1

Insights into Potential Tax Policy Shifts under a New Administration

Election Recap

53 Republicans

Senate

47 Democrats

232 DemocratsPresident Trump

White House House

197 Republicans

211 Republicans

50 Republicans

50 Democrats

222 Democrats

Biden declared winner with 306 Electoral College

Votes

2 unfilled

Currently

Election Status

Election results are (mostly) final with a mix of winners and losers

• Biden/Harris will take the White House (will be sworn in on January 20th)

• Democrats take control of the Senate (VP Harris will be the tie breaking vote)

• Democrats keep House, but lose some seats (may change some more based on Biden

appointments and special elections)

• Democrats will narrowly control both chambers of Congress

• This increases the likelihood of major legislative tax policy changes being enacted during this

Congress (117th Congress) but still not a clear and/or easy path

Election Recap

• As a general matter, to accomplish tax policy change, the House, Senate and president all need to agree to the same version of legislation

• With small margins of control, getting this agreement can be challenging

• Focus likely to be first on COVID relief and then Business/Individual provisions

• Biden’s tax policy agenda is grounded in the belief that the TCJA of 2017 was heavily skewed to large corporations and wealthy individuals

• Core belief that the federal income tax system should be changed to ensure these taxpayers are paying their “fair share”

Legislative Prospectus

Likelihood of enactment…..

• Prioritization of competing legislative action (many of which are outside of the tax realm)• Under current Senate rules, 60 votes generally needed to avoid a filibuster of legislation, resulting in

need for bipartisan support• Elimination of the filibuster is extremely controversial and would require support from ALL Senate

Democrats• If filibuster rule is not eliminated, Senate Democrats would need to use budget reconciliation

procedures to pass any tax bill that lacks Republican support• Even if filibuster rule is eliminated or budget reconciliation rules are used, leadership in House and

Senate would need to take into account differing political considerations• Likely to cause a lot of “horse trading” that may balance out some of the more progressive aspects of

proposed policy changes• Possible that changes could be retroactive to January 1, 2021 but far from certain

Legislative Prospectus

Highlights of President-Elect Biden’s Tax Proposals

Tax Area Proposed CurrentIncome tax rate 28% 21%

Alternative minimum tax Book net income of $100M or higher, 15% of book net income None

Global Intangible Low Tax Income (GILTI) tax rate

21%; removal of aggregation and removal of 10% QBAI exclusion 10.5%, increasing to 13.125% after 2025

Made In America Credit

Advanceable tax credit of 10% for business that invest in revitalizing closed

or nearly closed facilitates, retooling/expanding facilities, and bringing

jobs back to the U.S.

N/A

Surtax

10% surtax (rate of 30.8%) would apply to companies that sell products to U.S.

customers from a U.S. company’s foreign affiliate

N/A

Corporate Income Tax

Highlights of President-Elect Biden’s Tax Proposals

Individual Income TaxTax Area Proposed Current

Tax rate on ordinary incomeRevert top marginal rate

39.6% for taxable income over $400K

Top marginal rate of 37% (sunsets to 39.6% after

2025)

Tax rate on long-term capital gains & qualified dividends

Tax capital gains and dividends at 39.6% on

income above $1 million

20% max rate in 2020 for taxable income over

$441,450 (Single) and $496,600 (MFJ)

Itemized deductionsCaps Value at 28%,

reinstate Pease limitation for income over $400K

Pease limitation repealed (sunsets after 2025)

§199A Qualified Business Income Deduction

Phase out deduction for taxable income over $400K

20% deduction on QBI, phase out for SSTB’s (expires after 2025)

Carried interests Tax as ordinary income If held at least 3 years, taxed at LTCG rates

Highlights of President-Elect Biden’s Tax Proposals

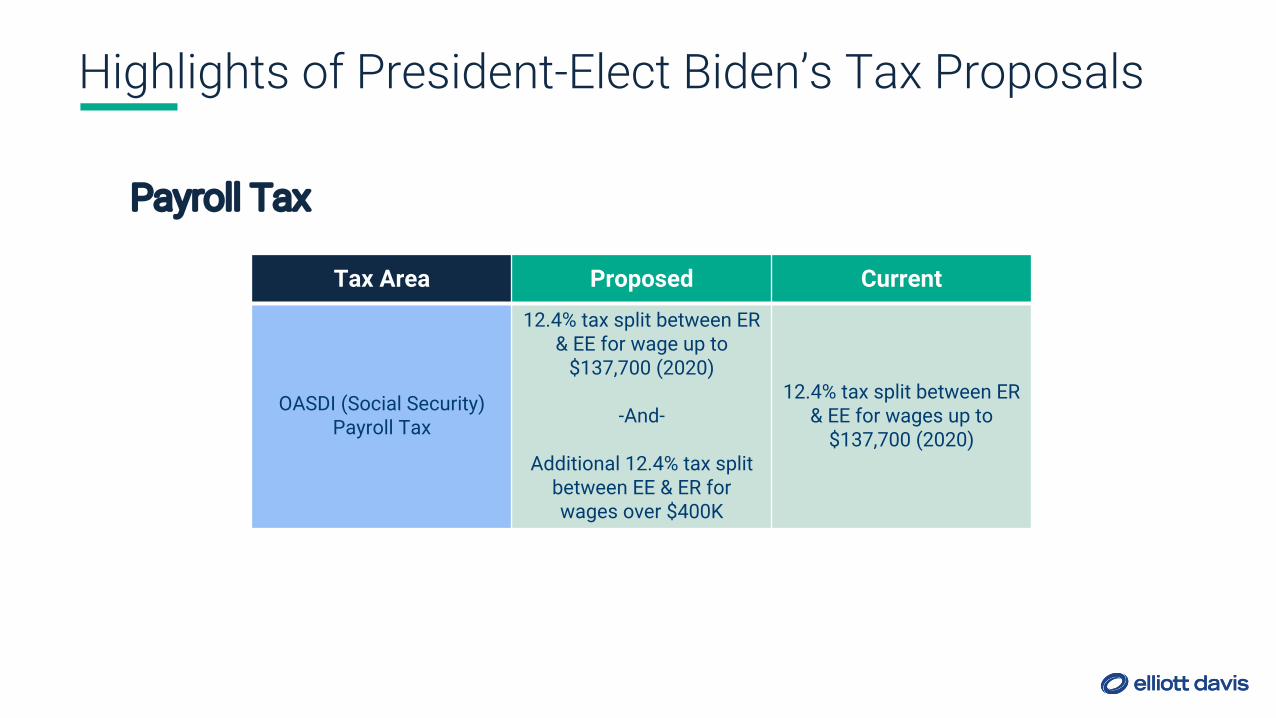

Payroll Tax

Tax Area Proposed Current

OASDI (Social Security) Payroll Tax

12.4% tax split between ER & EE for wage up to

$137,700 (2020)

-And-

Additional 12.4% tax split between EE & ER for wages over $400K

12.4% tax split between ER & EE for wages up to

$137,700 (2020)

• Some taxpayers are exploring options to accelerate income into 2020/defer deductions to future years.

• After consulting with your tax advisor, if this still makes sense for your situation there are many ways to effect this result (ex – slower depreciation, expanding cost capitalized under Section 263A, amortizing R&D expenses, etc)

• Alternatively, some taxpayers are exploring options to accelerate deductions into 2020 and defer income to future years.

• Could increase an NOL in 2020, allowing for a refund for a five-year carryback and rate arbitrage opportunity

• Near Term – keep an eye on tax extenders and temporary tax provisions, several of which are expiring in 2021. Take advantage of these and make sure the adjustments don’t impact your tax strategy.

• Long Term – keep an eye on Biden campaign proposals such as climate change, healthcare, infrastructure, and college affordability as any major movement in these areas would require additional spending and a likely offset by additional revenue raisers – tax increases.

• Look at potentially modeling potential outcomes and impacts to your business or personal situation and talking with your tax advisor on strategies that can be employed if and when changes to occur.

Post Election Planning Considerations

• New Tax Provisions• The Act allows PPP borrowers to fully deduct their covered expenses, while also not reducing tax basis or tax attributes,

and not recognizing taxable income on the forgiveness of the loan• Allows business meals to be fully deductible (100% instead of 50%) for expenses incurred after December 31, 2020

through end of 2022 as long as expense if for food or beverages provided by a restaurant

• Tax Modifications• Employee Retention Credit modifications • Payroll Tax Credits extended (paid sick and family leave payroll tax credit)

• Tax Extenders• Extends increased charitable contribution limits through 2021• Extends many energy credits that were set to expire • Extends New Markets Tax Credit and Work Opportunity Tax Credits through December 31, 2025

Tax Considerations of Consolidated Appropriations Act 2021

Polling Question

#2

PPP Update

PPP Update – New Guidance• New Interim Final Rules released

• Interim Final Rule on PPP as Amended by Economic Aid Act (consolidates all previous IFRs into one

document)

• Interim Final Rule on Second Draw Loans

• SBA Guidance on Accessing Capital for Minority, Underserved, Veteran, and Women-

Owned Business Concerns

PPP Update – New Eligible Expenses• Expanded use of PPP funds

• Covered worker protection and facility modification expenditures, including personal protective

equipment, to comply with COVID-19 federal health and safety guidelines.

• Expenditures to suppliers that are essential at the time of purchase to the recipient’s current

operations.

• Covered operating costs such as software and cloud computing services and accounting needs.• Also available to first round borrowers that have not yet submitted forgiveness

application

• Borrower must still spend 60% on eligible payroll expenses

PPP Update – Eligibility Changes• Certain entities are now eligible

• Certain 501(c)(6) organizations which include chambers of commerce and destination marketing

organizations

• Housing cooperatives

• Certain entities are ineligible

• Publicly traded companies

• Recipients of the “Shuttered Venue Operator Grant”

• Entities primarily engaged in political or lobbying activities

• Entities that are permanently closed

• Entities not in operation on February 15, 2020

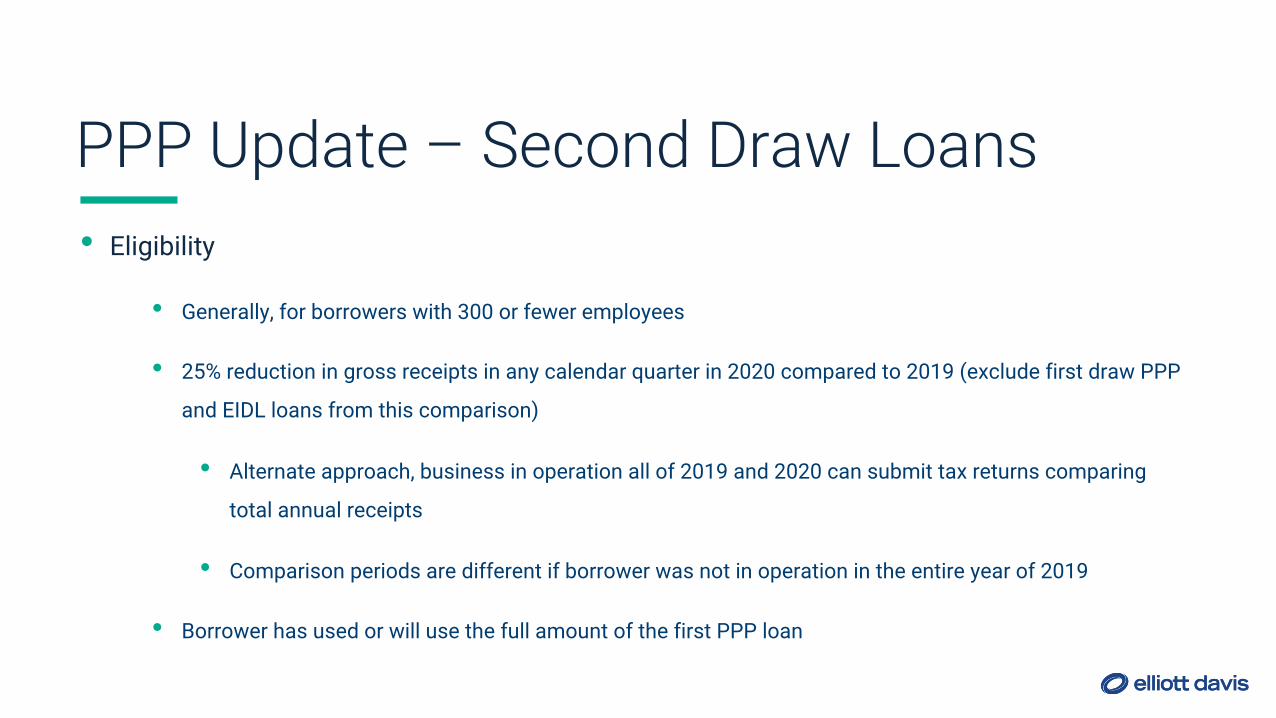

PPP Update – Second Draw Loans• Eligibility

• Generally, for borrowers with 300 or fewer employees

• 25% reduction in gross receipts in any calendar quarter in 2020 compared to 2019 (exclude first draw PPP

and EIDL loans from this comparison)

• Alternate approach, business in operation all of 2019 and 2020 can submit tax returns comparing

total annual receipts

• Comparison periods are different if borrower was not in operation in the entire year of 2019

• Borrower has used or will use the full amount of the first PPP loan

PPP Update – Second Draw Loans• Loan calculation

• Can receive 2.5x average monthly payroll, up to $2 million

• 3.5x payroll for entities with NAICS code starting with “72” (restaurants, hotels, accommodations and

hospitality)

• Can use 2019, 2020, or trailing 12 months prior to application for payroll costs

• If borrower uses same lender and same calendar 2019 figures for second draw loan calculation, then no additional documentation is necessary to substantiate costs

• Borrower will choose a covered period that is between 8 and 24 weeks

• Loans under $150k, borrower can certify 25% loss without documentation but will have to submit documentation of revenue loss when applying for forgiveness

PPP Update - Forgiveness Updates • Simplified forgiveness for loans under $150,000

• One page certification

• To include description of number of employees retained and estimated amount spent on

eligible costs

• No supporting documents submitted with application

• EIDL advance will not be deducted from PPP loan forgiveness

• Forgiven loans are not taxable and all expenses are tax deductible

• EIDL advances are also not taxable

• Concept of “Alternative Covered Period” eliminated

Polling Question

#3

Q&A

Thank You

Elliott Davis LLC is a leading business solutions firm offering a full

spectrum of services in the areas of tax, comprehensive assurance,

and specialized consulting services to diverse businesses,

organizations, and individuals. The firm, which has been providing

innovative solutions since its founding in 1920, leverages a network

of nearly 800 forward-thinking professionals in major domestic

markets and alliance resources across the globe.

Visit elliottdavis.com for more information.

About Elliott DavisElliott Davis LLC is a leading business solutions firm offering a full

spectrum of services in the areas of tax, comprehensive assurance,

and specialized consulting services to diverse businesses,

organizations, and individuals. The firm, which has been providing

innovative solutions since its founding in 1920, leverages a network

of nearly 800 forward-thinking professionals in major domestic

markets and alliance resources across the globe.

Visit elliottdavis.com for more information.

About Elliott Davis