Embed Size (px)

Citation preview

ASIA PACIFIC JOURNAL OF MANAGEMENT VOL. 7, NO. 1:49 - 64

Profit Sharing Bonuses And The Cost Of Debt: Business Finance And Compensation

Policy In Japanese Electronics Firms +

Jay B Barney*

Pr@'t sharing bonuses can be thought of as a buffer to protect a firm's uncertain future cash flow. When positive cash flows are threatened, firms can reduce the cost of doing business by reducing the size of bonuses paid to employees. Such an action increases the likelihood that firms will be able to pay fixed debt obligations without the secondary negative consequences of other cost-saving activities, including laying off personnel. Such profit sharing bonus compensation plans shift risk from debt holders to employees. In an efficient capital market, this shift will be reflected in a lower cost of debt. Implications of this argument are tested using a sample of Japanese electronics firms.

INTRODUCTION

A variety of methods for allowing a firm's employees to share in a firm's economic success and prosperity have been examined in the literature. Much of this work has focused on different compensation schemes that might be implemented by firms, and how these compensation plans affect employee cooperation, commitment, and productivity (Ouchi, 1980; Howard, 1979; Frost, Wakeley and Ruh, 1974). Employee stock ownership, various types of stock options, profit sharing bonuses, and performance based bonuses have all been examined in this manner (Lawler, 198 t).

The relationship between compensation plans that allow employees to share in the economic benefits of a firm's success and employee cooperation, commitment, and productivity is important, and deserves further study. However, these compensation schemes may have an impact on relations between a firm

+ This research was supported by grants from the Office of Naval Research, the US- Japan Friendship Commission, and the Mellon Foundation. Additional support was provided by IBM, the General Electric Foundation, Amp. Inc., the Westinghouse Electric Corporation, and the Alcoa Foundation. Discussions with William G.Ouchi, Tom Copeland, Nick Benes, William Hesterly, and the Organisation Economics Seminar at UCLA have been valuable in the development of this work.

* Department of Management, Texas A & M University.

49

Profit Sharing Bonuses and the Cost of Debt: Barney

and its other stakeholders, besides employees. Several authors have begun to investigate these other effects of compensation. Most of this work has focused on how various forms of equity compensation affect relations between a firm and its stockholders (Lambert and Larcker, 1985).

The research reported here is an example of this second type of work on compensation policy. However, rather than focusing on the impact of compensation on relations between a firm's employees and its stockholders, this work focuses on relations between employees and debt holders. The particular compensation policy investigated is the profit sharing bonus 1. Profit sharing bonuses are one of a variety of ways that a firm's economic success can be shared with employees (Ouchi, 1981). The major hypothesis developed is that the total size of profit sharing bonuses in a firm will be negatively associated with a firm's cost of debt. The larger the bonus in total employee compensation, the lower is the cost of the debt, ceteris paribus.

The cost of debt is a dependent variable that has not received a great deal of attention in the management literature. Yet a firm's cost of debt, as a component of its cost of capital, can have an important impact on an organisation (Hannan and Freeman, 1977). To see this potential impact, one need only consider the competitive situation facing U.S. semiconductor manufacturers in the 1980's. In 1979, the weighted average cost of capital, both debt and equity, of six selected U.S. semiconductor firms was 16.3% (Ouchi, 1984). The weighted average cost of capital for five directly competitive Japanese semiconductor firms was 12.6%. This 3.7% differential in the cost of capital represented a significant competitive disadvantage for the U.S. firms, for it implied, among other things, that the Japanese firms could charge less for their semiconductor products and still be as profitable as their U.S. competitors. Indeed, Robert Noyce, President of Intel Electronics, a major U.S. semiconductor manufacturer, testified that access to low cost capital may be the decisive factor in determining world market share leadership in the semiconductor industry through the 1980's (Noyce, 1980). In this sense, the ability of a firm to reduce its cost of debt by adopting profit sharing bonus policies may have significant competitive implications for a firm.

The argument is developed in three parts. First, the role of a profit sharing bonus as a risk-reducing buffer for a firm's uncertain future cash flow is discussed. Second, the empirical implications of this view are examined using a sample of Japanese electronics firms that pay profit sharing bonuses. Finally, the arguments are summarised and their implications for the implementation of compensation schemes that share a finn's economic success with employees are discussed.

PROFIT SHARING BONUSES AND THE COST OF DEBT

Once a loan is made to a firm (either through bank debt, accounts payable, or bonds), repayment is contingent upon the ability of the firm to continue

50

ASIA PACIFIC JOURNAL OF MANAGEMENT VOL. 7, NO. 1

obtaining positive cash flow to fund repayment (Copeland and Weston, 1983) 2. Periodically, firms may experience significant reversals in their economic fortunes which may prohibit them from meeting their fixed debt obligations from current business revenues. Under these conditions, the payment of principle and interest obligations is in some jeopardy.

Debt holders of firms facing these economic trials are often forced to pressure a firm to engage in expense reducing activities in order to increase the likelihood of receiving payment. Some of these actions might include reducing marketing expenditures, reducing research and development expenditures, and employee layoffs.

Each of these actions reduce short-run business expenses, which may generate sufficient money to fund payment of current debt obligations. However, each of these actions also have important secondary costs which can decrease the long-term profitability of the firm, and can increase the likelihood of economic bankruptcy at some future date. Reducing marketing expenditures, for example, may risk the loss of current and future customers. In industries sensitive to market share economies of scale, such actions can have significant negative financial consequences for firms (Henderson, 1979). Reducing research and development expenditures may risk a firm's ability to stay abreast of possibly important technological innovations. In this way, firms risk technical obsolescence, a situation that can be very detrimental in some industries (Ouchi, 1981). Finally, laying off employees does reduce business expenses, but only at the cost of low employee morale, deteriorated employee motivation, and the possible loss of trained personnel who might leave the firm permanently to seek more secure employment (Hashimoto, 1975; Ouchi, 1981).

As an alternative to these, and related, ways of reducing the current cost of doing business, firms with a profit sharing bonus plan can reduce direct labour costs substantially by reducing the size of the bonuses paid to employees 3. This can be done without laying off personnel or reducing other vital organisational expenditures. In this sense, a profit sharing bonus plan can act to protect a firm's creditors from the uncertainty of a firm's future cash flow. Moreover, this is accomplished without the negative secondary consequences of other cost reducing approaches.

During times of strong economic performance, employees are paid their salary and a profit sharing bonus, and creditors receive payments from the firm's strong positive cash flow. During bad economic times, employee profit sharing bonuses can be substantially reduced, thereby reducing the cost of doing business and increasing the probability that creditors will still receive interest and principle payments. The larger the percentage of total employee compensation that takes the form of a profit sharing bonus, the greater the buffer for a firm's positive cash flow, and the more likely firms will be able to meet their debt obligations

51

Profit Sharing Bonuses and the Cost of Debt: Barney

during difficult financial times without engaging in activities that may hurt the tong-term financial viability of the firm.

In agreeing to a compensation scheme that includes profit sharing bonuses, employees increase the riskiness of their individual income streams by shifting some of the risk that would have been borne by outside debt holders to themselves. This shifting of risk from debt holders to employees, in an efficient capital market (Fama, 1970), will be reflected in a firm's lower cost of debt.

Obviously, the use of a profit sharing bonus policy cannot be expected to perfectly protect debt holders from risk. Certainly, a firm may have an extremely bad year, be forced not to pay a profit sharing bonus, but still have difficulty meeting its debt obligations. However, on the margin, the use of a profit sharing bonus can partially reduce (though not eliminate) a debt holder's risks. This reduction in risk will, in an efficient capital market, be reflected in a lower cost of debt.

Employees will typically only be willing to accept this increased risk if they are appropriately compensated. Compensation for this risk bearing can take many forms, both explicit and implicit (Azariadis and Stiglitz, 1983), including a corporate commitment to lifetime employment with no layoffs (Ouchi, 1981; Gordon, 1982), employee representation on a firm's board of directors (Tichy, 1983, p. 124), or a relatively high base salary (Gordon, 1982).

Because of the efficiency attributes of capital markets, a firm need never actually have reduced the size of its profit sharing bonuses in order to fund current debt obligations to obtain the reducing cost of debt benefits of such a compensation scheme. Rather, with a profit sharing bonus compensation plan in place, outside debt holders can anticipate these benefits should a firm ever face financial constraints. And these anticipated benefits, in an efficient capital market, will be reflected in a firm's current cost of debt. In this sense, a profit sharing bonus compensation plan is a reassuring signal (Spence, 1974) to creditors that if a firm begins to experience financial difficulties, a system is in place that increase the probability that debt obligations will be repaid without seriously jeopardising the firm's performance in some future period. A firm without a profit sharing bonus system in place does not send such a reassuring message to its creditors.

This observation has important implications for the empirical work reported below. If investors in capital markets anticipate future benefits of profit sharing bonus compensation plans in the current cost of debt, then it will not be necessary to find firms that have, in fact, reduced the size of their profit sharing bonuses to fund current debt obligations to test the argument. Rather, all that will be required is to isolate firms that have profit sharing bonuses in place and thus are reassuring debt holders.

52

ASIA PACIFIC JOURNAL OF MANAGEMENT VOL. 7, NO. 1

EMPIRICAL IMPLICATIONS

Hypothesis The ideas developed here suggest several testable hypotheses, the most

important of which is considered below.

Hypothesis: For firms employing a profit sharing bonus compensation plan, the larger the percentage of total employee compensation that takes the form of a profit sharing bonus, ceteris paribus, the lower the cost of debt for that firm.

The larger the percentage of employee compensation taking the form of a profit sharing bonus, the larger the potential buffer for a firm's uncertain future positive cash flow, and the greater the risk shifted from debt holders to employees. In an efficient capital market, this risk shifting will be reflected in a firm's lower cost of debt.

Alternative Hypotheses The risk shifting attributes of profit sharing bonuses are only one of several

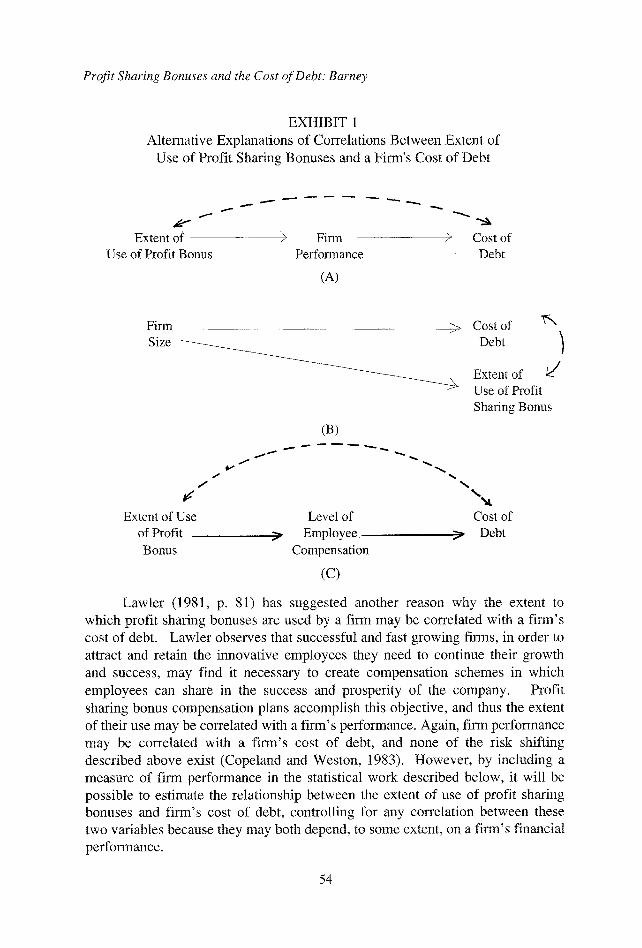

possible explanations of any empirical relationship that might exist between a firm's use of profit sharing bonus compensation and its cost of debt. Four of these alternative explanations, each of which suggest control variables that will be included in empirical tests of the hypothesis, are considered here. The first of these alternative hypotheses is summarised in Panel A of Exhibit 1, and builds on the relationship between profit sharing bonus compensation and firm performance studied by Ouchi (1981), Pascal and Athos (1981), and others. When the size of the profit sharing bonuses distributed to employees varies as a function of overall corporate performance, employees, as a group, have a strong incentive to improve the financial performance of the firm 4. The more successful a firm is financially, the larger the bc s pool is likely to be distributed among employees. Thus, there may be a strong correlation between the use of profit sharing bonuses and overall firm performance.

Previous research in finance (Copeland and Weston, 1983) has shown that a firm's cost of debt can depend on its financial performance, mad in particular, on the probability of a firm being able to meet its debt obligations in the future. Thus, firm performance and the cost of debt may be correlated.

Given the correlation between the extent of use of profit sharing bonuses and firm performance, on the one hand, a firm performance and the cost of debt, on the other, the extent of use of profit sharing bonuses may be correlated with the cost of debt. This correlation is represented by the dotted line in panel A of Exhibit 1. This correlation would not depend on any shifting of risk from debt holders to employees. To control for this possible correlation between the use of profit sharing bonuses and the cost of debt, a measure of firm performance will be included in the model specification below.

53

Profit Sharing Bonuses and the Cost of Debt: Barney

EXHIBIT 1 Alternative Explanations of Correlations Between Extent of

Use of Profit Sharing Bonuses and a Firm's Cost of Debt

f

Extent of ) Firm ) Cost of Use of Profit Bonus Performance Debt

(A)

Firm ~ Cost of Size ~ Debt }

Extent of k / vL Use of Profit

Sharing Bonus

(B)

v

Extent of Use Level of Cost of of Profit ~, Employee ~ Debt Bonus Compensation

(c)

Lawler (1981, p. 81) has suggested another reason why the extent to which profit sharing bonuses are used by a firm may be correlated with a firm's cost of debt. Lawler observes that successful and fast growing firms, in order to attract and retain the innovative employees they need to continue their growth and success, may find it necessary to create compensation schemes in which employees can share in the success and prosperity of the company. Profit sharing bonus compensation plans accomplish this objective, and thus the extent of their use may be correlated with a firm's performance. Again, firm performance may be correlated with a firm's cost of debt, and none of the risk shifting described above exist (Copeland and Weston, 1983). However, by including a measure of firm performance in the statistical work described below, it will be possible to estimate the relationship between the extent of use of profit sharing bonuses and firm's cost of debt, controlling for any correlation between these two variables because they may both depend, to some extent, on a firm's financial performance.

54

ASIA PACIFIC JOURNAL OF MANAGEMENT VOL. 7, NO. 1

A third alternative hypothesis stems from the observation that both the extent of profit sharing bonus compensation and a firm's cost of debt can be related to a firm's size. This alternative is depicted in Panel B of Exhibit 1. Fama and Jensen (1983) have suggested that decision-making in small firms is typically less complicated than decision-making in large firms, and thus does not require the decision-making specialisation common in large firms. Without specialisation, all phases of the decision-making process, from collecting and analysing information to implementing decisions and monitoring performance, are per~brmed by a single individual or a small group of individuals. Coordination of efforts in this setting is not difficult and can be done directly.

However, in large firms, where the complexity of the decision-making process is much greater, coordination becomes important and difficult. In such situations, profit sharing bonus plans, because they give separate employees a common interest in the overall financial performance of a firm, can be used by firms to enhance coordination among different groups and individuals responsible for different phases of the decision-making process. For Fama and Jensen, the larger the firm, the greater the complexity of the decision-making process, and the greater the need for employee coordination. The greater the need for coordination, the more likely a firm will adopt a profit sharing bonus compensation scheme. Thus, firm size may be associated with the extent of use of profit sharing bonus compensation in a firm.

Firm size has also been shown to be a determinant of a firm's cost of debt. The flotation costs of new debt offering are higher for smaller firms, reflecting the effects of economies of scale in the offering and selling of new debt issues (Copeland and Weston, 1983, p. 309). Thus, ceteris paribus, larger firms will have lower cost of debt than smaller firms.

Taken together, these arguments suggest that the size of a firm may be correlated with both the extent of use of profit sharing bonus compensation and a firm's cost of debt, and thus, indirectly, profit sharing bonuses and the cost of debt may be correlated. In order to control for this possible relationship, a measure of firm size will be included as an independent variable in statistical tests reported below.

A final alternative hypotheses, presented in Panel C of Exhibit 1, touches on the costs to firms of using profit sharing bonus forms of compensation. It was suggested earlier that employees will normally not accept the higher risk associated with profit sharing bonuses unless they are appropriately compensated. In general, the greater the extent to which profit sharing bonuses are used in a firm, the greater must be this compensation for risk bearing whatever form it takes. Thus, there may be a correlation between the extent of use of profit sharing bonuses and the level of employee compensation in a firm.

55

Profit Sharing Bonuses and the Cost of Debt: Barney

These economic commitments to employees may also have an impact on a firm's cost of debt. Employee compensation is a large part of the cost of doing business. Firms that use a profit sharing bonus will need to compensate employees for doing so, and thus will have a higher cost of doing business compared to firms that do not use a profit sharing bonus. This higher cost of business may be associated with a higher cost of debt (Copeland and Weston, 1983), for firms with a relatively high cost of doing business, all else equal, are riskier investments compared to lower cost fhans (Porter, 1980, 1985). To control for these relationships a measure of current employee compensation is included in the statistical work reported below.

Sample

To test the relationship between the extent of profit sharing bonus compensation in a firm and a firm's cost of debt and controlling for these alternative hypotheses, a sample of 34 Japanese electronics firms that use profit sharing bonus compensation plans was selected 5. Japanese firms were chosen to test the hypothesis because the widespread use of profit sharing bonuses is well- documented in Japan (Ouchi, 1981). As important, information about the total amount of profit sharing bonus paid to employees in Japanese finns, and what percentage these bonuses are of total employee compensation, is available at low cost to debt holders in Japan, and thus can be expected to be reflected in these firm's cost of debt (Fama, 1970). If this information was not readily available to debt holders, the relationship between the use of a profit sharing bonus and the cost of debt would not exist.

While the sample includes only Japanese firms, the test of the hypothesis does not rely on any special assumptions about the nature of self-interest of Japanese debt investors, Japanese managers, or Japanese firms. Rather, the traditional economic assumption that investors and managers attempt to maximise their personal wealth in their economic decision making is maintained (Hirshliefer, 1980). The test of the hypothesis also does not rely on the operation of capital market institutions peculiar to Japan, i.e., the Keidanren, MITI, the Ministry of Finance, the Keiretsu, etc. (Ouchi, 1984; Ballon, Tomita, and Usami, 1976), nor on the broad use of relational banking in Japan. Rather, all that is assumed is that the Japanese capital markets are efficient in the sense that all publicly available information about the value of debt (including information about the percentage of firm compensation that takes the form of a profit sharing bonus) will be reflected in the price of debt. If information about the percentage of compensation taking the form of a profit sharing bonus is available to debt investors at low cost (which it is), and if the extent of use of this form of compensation is relevant in valuing a firm's debt (which, as has been argued here, it is), then it would be irrational for Japanese debt investors to ignore

56

ASIA PACIFIC JOURNAL OF MANAGEMENT VOL. 7, NO. 1

information about the use of profit sharing bonuses in firms to whom they lend money. Empirical research throughout the world suggests that most capital markets are efficient in this semi-strong manner (Copeland and Weston, 1983).

Electronics firms were chosen for the sample for several reasons. First, the electronics industry is an important industry worldwide, and one with several segments dominated by Japanese firms (Ouchi, 1981). Understanding determinants of the relative cost position of Japanese versus other electronics firms may have important competitive implications for these other firms (Porter, 1980). Because the cost of debt is an important component of this cost structure, understanding the impact of compensation policy in general, and the use of profit sharing bonuses in particular, on the cost of debt may have important competitive implications for firms. On a more practical level, previous research contacts in Japanese electronics firms made the kinds of interviews that were required in computing the cost of debt for firms in this sample possible. Without these interviews, the impact of compensating balances, debt to equity ratios, etc. would have been difficult to include in the calculation of the cost of debt.

Model

The model used to examine the impact of the use of profit sharing bonuses on the cost of debt, controlling for the alternative hypotheses listed above, can be expressed in a regression format:

WCOD = B 0 + B~ BONUS + B 2 EPS + B 3 SALES + B 4 SERVICE (1)

where,

WCOD =

BONUS =

EPS =

SALES =

SERVICE =

the weighted after tax cost of debt for a firm in 1980;

the percentage of total employee compensation taking the form of a profit sharing bonus in 1980;

as a measure of firm performance, the annual compound rate of growth (loss) in earnings per share for the years 1970-1980;

a measure of firm size, total sales of the firm in 1980;

as a measure of employee compensation taking the form of a commitment to lifetime employment, the average years of employee service in a firm in 1980.

The test of the main hypothesis of this study depends upon the sign and significance of the regression coefficient for BONUS. The expected sign is negative.

The weighted cost of debt, WCOD, was computed using procedures outlined in Copeland and Weston (1983). First, the cost of debt, without considering

57

Profit Sharing Bonuses and the Cost of Debt: Barney

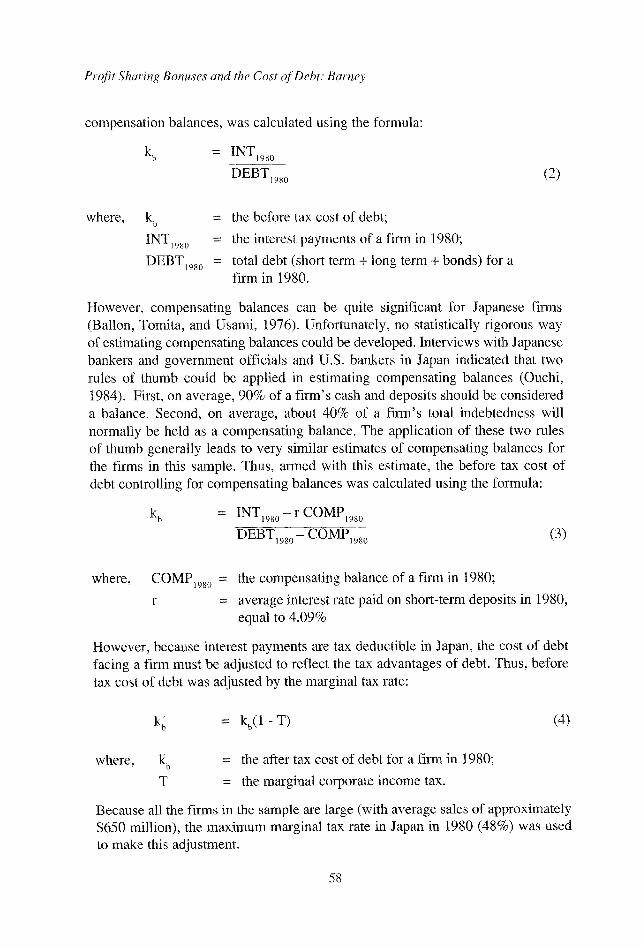

compensation balances, was calculated using the formula:

k b = INTIg~o

DEBT Iga0 (2)

where, k b = the before tax cost of debt;

INT1980 = the interest payments of a firm in 1980;

DEBT~980 = total debt (short term + long term + bonds) for a firm in 1980.

However, compensating balances can be quite significant for Japanese firms (Ballon, Tomita, and Usami, 1976). Unfortunately, no statistically rigorous way of estimating compensating balances could be developed. Interviews with Japanese bankers and government officials and U.S. bankers in Japan indicated that two rules of thumb could be applied in estimating compensating balances (Ouchi, 1984). First, on average, 90% of a firm's cash and deposits should be considered a balance. Second, on average, about 40% of a firm's total indebtedness will normally be held as a compensating balance. The application of these two rules of thumb generally leads to very similar estimates of compensating balances for the firms in this sample. Thus, armed with this estimate, the before tax cost of debt controlling for compensating balances was calculated using the formula:

k b = INTl9s0- r COMPI9s0

DEBT1980 - COMP198o (3)

where, COMP1980 = the compensating balance of a firm in 1980;

r = average interest rate paid on short-term deposits in 1980, equal to 4.09%

However, because interest payments are tax deductible in Japan, the cost of debt facing a firm must be adjusted to reflect the tax advantages of debt. Thus, before tax cost of debt was adjusted by the marginal tax rate:

k b = kb(1-T) (4)

where, 1% = the after tax cost of debt for a firm in 1980;

T = the marginal corporate income tax.

Because all the firms in the sample are large (with average sales of approximately $650 million), the maximum marginal tax rate in Japan in 1980 (48%) was used to make this adjustment.

58

ASIA PACIFIC JOURNAL OF MANAGEMENT VOL. 7, NO. l

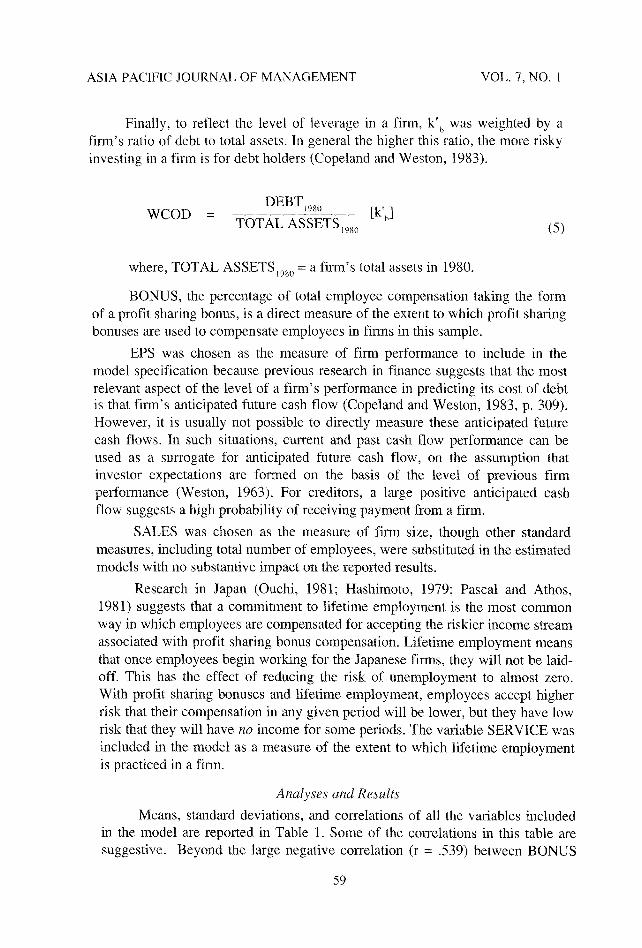

Finally, to reflect the level of leverage in a firm, k ' b was weighted by a firm's ratio of debt to total assets. In general the higher this ratio, the more risky investing in a firm is for debt holders (Copeland and Weston, 1983).

WCOD = DEBTIg~° [k' b] TOTAL ASSETS ~980 (5)

where, TOTAL ASSETSI98o = a firm's total assets in 1980.

BONUS, the percentage of total employee compensation taking the form of a profit sharing bonus, is a direct measure of the extent to which profit sharing bonuses are used to compensate employees in firms in this sample.

EPS was chosen as the measure of firm performance to include in the model specification because previous research in finance suggests that the most relevant aspect of the level of a firm's performance in predicting its cost of debt is that firm's anticipated future cash flow (Copeland and Weston, 1983, p. 309). However, it is usually not possible to directly measure these anticipated future cash flows. In such situations, current and past cash flow performance can be used as a surrogate for anticipated future cash flow, on the assumption that investor expectations are formed on the basis of the level of previous firm performance (Weston, 1963). For creditors, a large positive anticipated cash flow suggests a high probability of receiving payment from a firm.

SALES was chosen as the measure of firm size, though other standard measures, including total number of employees, were substituted in the estimated models with no substantive impact on the reported results.

Research in Japan (Ouchi, 1981; Hashimoto, 1979; Pascal and Athos, 1981) suggests that a commitment to lifetime employment is the most common way in which employees are compensated for accepting the riskier income stream associated with profit sharing bonus compensation. Lifetime employment means that once employees begin working for the Japanese firms, they wili not be laid- off. This has the effect of reducing the risk of unemployment to almost zero. With profit sharing bonuses and lifetime employment, employees accept higher risk that their compensation in any given period will be lower, but they have low risk that they will have no income for some periods. The variable SERVICE was included in the model as a measure of the extent to which lifetime employment is practiced in a firm.

Analyses and Results

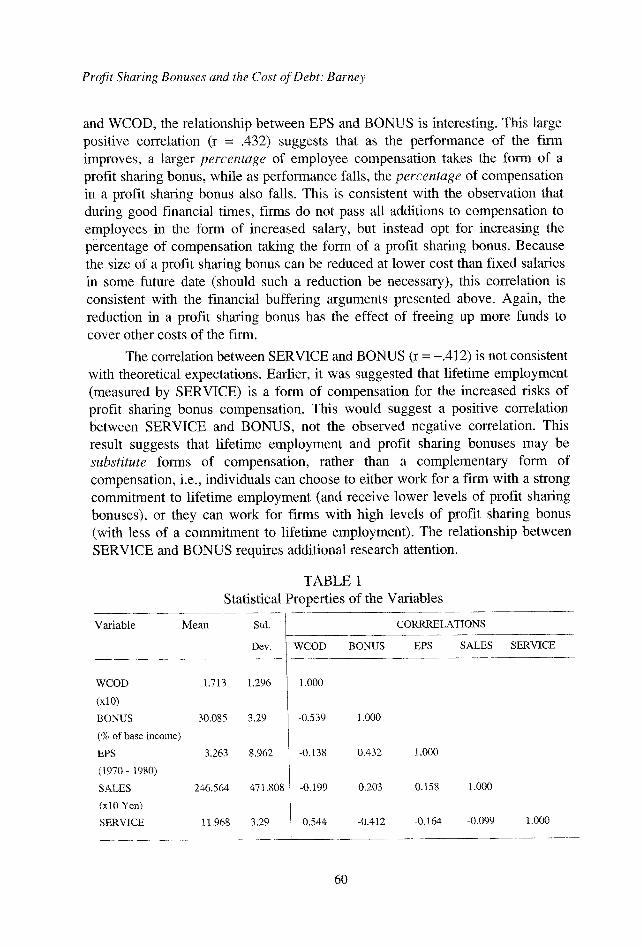

Means, standard deviations, and correlations of all the variables included in the model are reported in Table 1. Some of the correlations in this table are suggestive. Beyond the large negative correlation (r = .539) between BONUS

59

Profit Sharing Bonuses and the Cost of Debt." Barney

and WCOD, the relationship between EPS and BONUS is interesting. This large positive correlation (r = .432) suggests that as the performance of the firm improves, a larger percentage of employee compensation takes the form of a profit sharing bonus, while as performance falls, the percentage of compensation in a profit sharing bonus also falls. This is consistent with the observation that during good financial times, firms do not pass all additions to compensation to employees in the form of increased salary, but instead opt for increasing the percentage of compensation taking the form of a profit sharing bonus. Because the size of a profit sharing bonus can be reduced at lower cost than fixed salaries in some future date (should such a reduction be necessary), this correlation is consistent with the financial buffering arguments presented above. Again, the reduction in a profit sharing bonus has the effect of freeing up more funds to cover other costs of the firm.

The correlation between SERVICE and BONUS (r = -.412) is not consistent with theoretical expectations. Earlier, it was suggested that lifetime employment (measured by SERVICE) is a form of compensation for the increased risks of profit sharing bonus compensation. This would suggest a positive correlation between SERVICE and BONUS, not the observed negative correlation. This result suggests that lifetime employment and profit sharing bonuses may be substitute forms of compensation, rather than a complementary form of compensation, i.e., individuals can choose to either work for a firm with a strong commitment to lifetime employment (and receive lower levels of profit sharing bonuses), or they can work for firms with high levels of profit sharing bonus (with less of a commitment to lifetime employment). The relationship between SERVICE and BONUS requires additional research attention.

TABLE 1 Statistical Properties of the Variables

Variable Mean Std.

Dev.

WCOD 1.713 1.296

(xl0) BONUS 30.085 3.29

CORRRELATIONS

WCOD BONUS EPS SALES SERVICE

1.000

1.000

-0.539

(% of base income)

EPS 3.263 8.962

(1970- 1980)

SALES 246.564 471.808

(xl0 Yen)

SERVICE 11.968 3.29

-0.138 0.432 1.000

-0.1.99 0.203 0.158 1.000

0.544 -0.412 -0.164 -0.099 1.000

60

ASIA PACIFIC JOURNAL OF MANAGEMENT VOL. 7, NO. 1

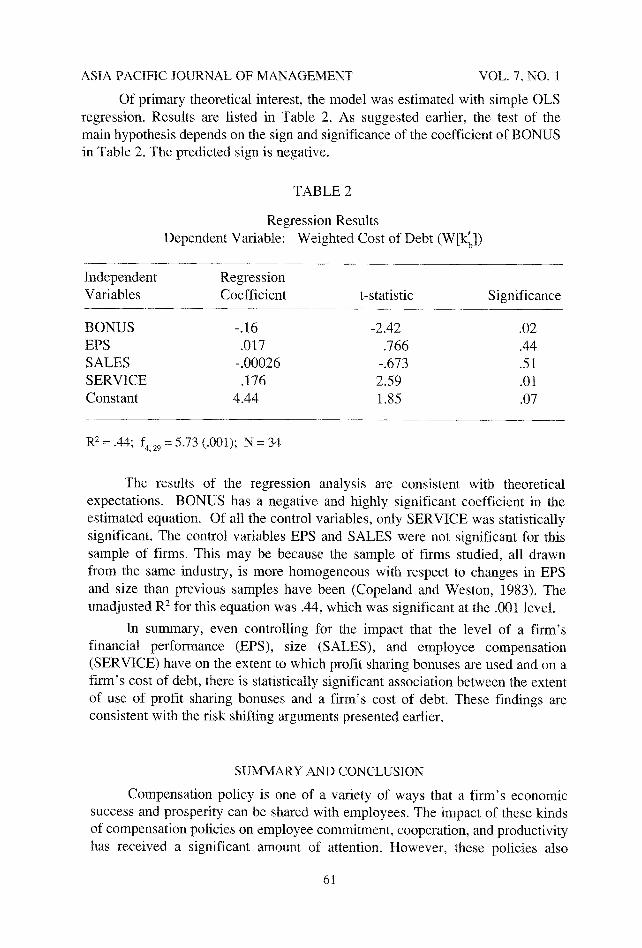

Of primary theoretical interest, the model was estimated with simple OLS regression. Results are listed in Table 2. As suggested earlier, the test of the main hypothesis depends on the sign and significance of the coefficient of BONUS in Table 2. The predicted sign is negative.

TABLE 2

Regression Results Dependent Variable: Weighted Cost of Debt (W[k{o])

Independent Regression Variables Coefficient t-statistic Significance

BONUS -.16 -2.42 .02 EPS .017 .766 .44 SALES -.00026 -.673 .51 SERVICE .176 2.59 .01 Constant 4.44 1.85 .07

R 2 = .44; f<29 = 5.73 (.001); N = 34

The results of the regression analysis are consistent with theoretical expectations. BONUS has a negative and highly significant coefficient in the estimated equation. Of all the control variables, only SERVICE was statistically significant. The control variables EPS and SALES were not significant for this sample of firms. This may be because the sample of firms studied, all drawn from the same industry, is more homogeneous with respect to changes in EPS and size than previous samples have been (Copeland and Weston, 1983). The unadjusted R z for this equation was .44, which was significant at the .001 level.

In summary, even controlling for the impact that the level of a firm's financial performance (EPS), size (SALES), and employee compensation (SERVICE) have on the extent to which profit sharing bonuses are used and on a firm's cost of debt, there is statistically significant association between the extent of use of profit sharing bonuses and a firm's cost of debt. These findings are consistent with the risk shifting arguments presented earlier.

SUMMARY AND CONCLUSION

Compensation policy is one of a variety of ways that a firm's economic success and prosperity can be shared with employees. The impact of these kinds of compensation policies on employee commitment, cooperation, and productivity has received a significant amount of attention. However, these policies also

61

Profit Sharing Bonuses and the Cost of Debt: Barney

affect relations between a firm and its other stakeholders. In this paper, the impact of profit sharing bonuses on relations between a firm and its debt holders was examined. It was argued that, because a profit sharing bonus shifts risks from debt holders to employees, this form of compensation has the effect of reducing a firm's cost of debt. The results reported here suggest that the extent of use of profit sharing bonuses is negatively correlated with the cost of debt, at least among the kinds of firms that have been examined. This result holds, even controlling for any beneficial impact that profit sharing bonuses might, or might not, have for a firm's performance and growth.

This analysis suggests yet another reason why firms might want to consider implementing a compensation scheme that shares some of their economic success with employees: the cost of capital implications of these compensation schemes. The cost of capital is a major component of a firm's cost of doing business. Actions that reduce this cost can improve a firm's performance. While only profit sharing bonuses and the cost of debt have been examined here, it may well be the case that other compensation plans that allow employees to share in a firm's prosperity also have cost of capital implications. Work on these other compensation policies should continue (Barney, 1988).

ENDNOTES

1. A profit sharing bonus plan is any compensation plan where employees are paid a sum of money in addition to base salary. Though these plans differ in detail, it is usually the case that bonuses are distributed once or twice a year, and the size of bonuses vary as a function of either the performance of an entire firm (or division) and/or as a function of the performance of a particular employee.

2. The argumems developed here apply to investors that have long-term debt interest in a firm, and to investors that have a series of short-term debt interests in a firm. Notice that these arguments focus directly on the business risks associated with investing in a firm and not the agency risk of such investments (Jensen and Meckling, 1976).

3. The impact of other compensation schemes (e.g., employee stock ownership) on the cost of debt have been investigated elsewhere (Barney, 1988). The extent to which these are substitutes for profit sharing bonus compensation schemes is not examined in this paper in detail.

4. As Ouchi (1981) has suggested, employees may not develop a common commitment to improve firm performance if bonuses are distributed exclusively on the basis of individual performance.

5. Though the number of firms in this sample is relatively small, it is consistent with sample sizes of previous research on profit sharing bonus and related compensation plans (Metzger, 1978; Howard, 1979; Conte and Tannenbaum, 1978). Moreover, because the firms in this sample are all relatively large, and because profit sharing

62

ASIA PACIFIC JOURNAL OF MANAGEMENT VOL. 7, NO. 1

bonuses are paid to virtually all employees in these firms (Ouchi, 1981), the total number of employees included in the bonus plans studied is over 300,000.

REFERENCES

Azapiadis, C. and Stiglitz, J. E. (1983), "Implicit Contracts and Fixed Price Equilibria,"QuarterIy Journal of Economics, 148, pp. 1-22.

Ballon, R. J., Tomita, I. and Usami, H. (1976), Financial Reporting in Japan. Tokyo: Kodansha.

Barney, J. B. (1988), "Agency Theory, Employee Stock Ownership, and the Cost of Equity, "UnpuNished, Department of Management, Texas A & M University.

Conte, M. and Tannenbaum, A. S. (1978), "Employee Owned Companies: Is the Difference Measurable?" Monthly Labour Review.

Copeland, T. and Weston, J. F. (1982), Financial Theory and Corporate Policy, Reading, Mass: Addison-Wesley.

Fama, E. F. (1970), "Efficient Capital Markets: A Review of Theory and Empirical Work," Journal of Finance, May, pp. 383-417.

and Jensen, M. C. (1983), "Separation of Ownership and Control," Journal of Economics, 26, pp. 301-325.

Frost, C. F., Wakeley, J. H., and Ruh, R. A. (1974), The Scanlon Plan for Organization Development: Identity, Participation, and Equity, Lansing: Michigan State University Press.

Gordon, R. J. (1982), "Why U. S. Wage and Employment Behavior Differs From That in Britain and Japan," The Economic Journal, 82, pp. 929-964.

Hannan, M.T. and Freeman, J. (1977), "The Population Ecology of Organizations," American Journal of Sociology, 82, pp. 929-964.

Hashimoto, M. (1979), "Bonus Payments, On-the-Job Training, and Lifetime Employment in Japan," Journal of Political Economy, 87(5), pp. 1086-1104.

Henderson, B. (1979), Henderson on Corporate Strategy, New York: Mentor.

Hirshliefer, J. (1980), Price Theory and Applications, 2rid ed., Englewood Cliffs, N J: Prentice-Hall.

Howard, B. B. (1979), A Study of the Financial Significance of Profit Sharing, 1958-1977, Chicago: Profit Sharing Council.

Jensen, M. C. and Meckling, W. H. (1976), "Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure," Journal of Financial Economics, 3(4), pp. 305-360.

63

Profit Sharing Bonuses and the Cost of Debt: Barney

Kidney, J. (1986), Financial Performance and the Reputation of Management Teams. Unpublished Dissertation, Graduate School of Management, UCLA.

Lambert, R. and Larcker, D. (1985), "Executive Compensation, Corporate Decision Making and Shareholder Wealth: A Review of the Evidence," Midland Corporate Finance Journal, 2, pp. 6-22.

Latta, G. W. (t981), Profit Sharing, Employee Stock Ownership, and Savings and Asset Formation in the Western World, Philadelphia: Wharton School, Industrial Research Unit.

Lawter, E. E. (1981), Pay and Organization Development, Reading, MS: Addison- Wesley.

Metzger, B. C. (1978), Profit Sharing in 38 Large Companies, Evanston, IL: Profit Sharing Research Foundation.

Noyee, R. (1980), Statement Presented Before the Subcommittee on International Finance of the Committee on Banking, Housing, and Urban Affairs, United States Senate (January 15, 1980).

Ouchi, W. G. (1981), Theory Z, Reading, MS: Addison-Wesley.

(1984), The M Form Society, Reading, MS: Addison-Wesley.

Pascal, R. T. and Athos, A. G. (1981). The Art of Japanese Management, New York: Simon and Schuster.

Porter, M. E. (1980), Competitive Strategy, New York: Free Press.

(1985), Competitive Advantage, New York: Free Press.

Ross, S. A. (1977), "The Determination of Financial Structure: The Incentive Signaling Approach," Bell Journal of Economics, 8, pp. 23-40.

Spence, A. M. (1974), Market Signaling: Informational Transfer in Hiring and Related Screening Processes, Cambridge: Harvard.

Tichy, N. (1983), Management of Strategic Change: Technical, Political, and Cultural Dynamics, New York: Wiley.

Weston, J. F. (1963), "A Test of Cost of Capital Propositions," The Southern Economic Journal, 30(2), pp. 105-112.

64