Embed Size (px)

Citation preview

MANAGEMENTACCOU-AL-TINGPUBLISHED BY THE NATIONAL ASSOCIATION OF ACCOUNTANTS/ JANUARY 1969

NNIFA NONNI

IMENER r MEMO,..

_ . .

A FALIV d L

111111111101NONNINONNI"44, 9 F-.

pa 9PPa

p -

I V

W 'h'

4 0 m n1101

ME t1

Uniform Cost Accounting Standards in Negotiated Defense Contracts /

A Conceptual Framework / Systems in a Growth Company / Variances

from Standard Cost / Investment of Excess Cash / Market Mix: The Key

to Profitability / Holding Gains and Losses / Clerical Work Control

Quick asa wink...and

ju st

as quiet*'The new Burroughs C 3000 Electronic Calculator.

Now we're bringing absolute silence to calculating. You see ournew Burroughs C 3000. But you never hear it.

It's fast. You never wait for a result. It performs the mostcomplex computation in milliseconds.

It's easy to use. On the simple, logical keyboard, you doyour problem just like you would say it.

It's light and compact. You can tuck it under your arm,carry it from desk to desk, or take it home with you.

It's Low -Cost.

And i t g ives you a unique combinati on of refinedfeatures:

• Large, Easy -to -Read Tube Display —with a glare- eliminatingshield.

• Two Independent Storage Memories—each having 16-digit 8- decimal storage capacity in plus or minus

balances.• Independent Constant Factor Memory—to simplify

repetitive figure handling.

• Calculator Mode Lights —for easy operation.• Independent Compute and Storage Decimal Selectors

— settable for computational exactness and decimalflexibility.

• Recall Key—that displays multiplier, divisor, constantfactor, etc., with decimal points, whenever desired.

• Adjustable Working Angle—to provide working com-fort.

• Integrated Circuitry— reduces a multiplicity of partsinto a few small, highly reliable, easy -to- service units.

We'd like you to see the Series C 3000 . . . fivemodels to choose from. For a demonstration ofthe one that best suits your needs and budget,call our local office or write Burroughs Cor-poration, Detroit, Michigan 48232.

Burroughs one

MANAGEMENT ACCOUNTINGPUBLISHED BY THE NATIONAL ASSOCIATION OF ACCOUNTANTS I JANUARY 1969

A CONCEPTUAL FRAMEWORK FOR ANALYZING AND EVALUATING 9MANAGERIAL DECISIONSBy K. Fred Skousen and Belverd E. Needles, Jr.

Based on an operational approach to problem solving, the decision evaluationmodel presented in this article is intended as a frame Of reference in develop-ing the information usable in management decisions.

MANAGEMENT SYSTEMS IN A GROWTH COMPANY 12By Carl J. Thomsen

There is a need for understanding of Management Systems in a fundamentalway —as the beginning of a management revolution.

MISUSE OF STANDARDS IN DECISION MAKING 14By Robert W. Rosen

It is minimum total cost, not minimum operating cost, which is of primaryconcern to the decision maker.

THE NAT URE AND IMPORTANCE OF VARIANCES FROM STANDARD 16COST OF PRODUCT IONBy Oswald Nielsen

Significance of a cost variance relates to such factors as size of gross margin,inventory turnover and change in magnitude, rather than the size of variancerelative to the standard cost itself.

UNIFORM COST ACCOUNTING STANDARDS IN NEGOT IATED 21DEFENSE CONTRACTSBy Elmer B. Staats

Toward better guidelines for the use of alternate methods in reporting the costof performance under negotiated contracts with improved comparability, re-liability and consistency.

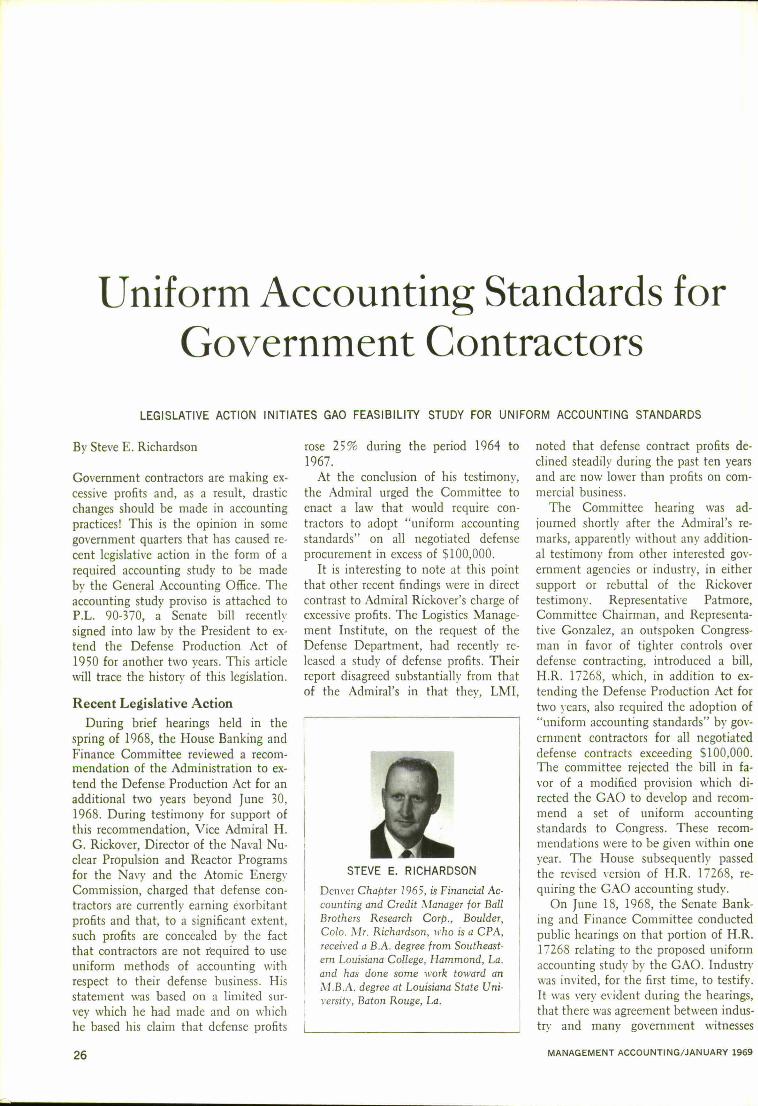

UNIFORM ACCOUNTING STANDARDS FOR GOVE RNMENT 26CONTRACTORSBy Steve E. Richardson

Uniform accounting standards —are they needed —and will they work? The au-thor traces the legislative action leading to the GAO Feasibility Study andsuggests that each of us examine this subject.

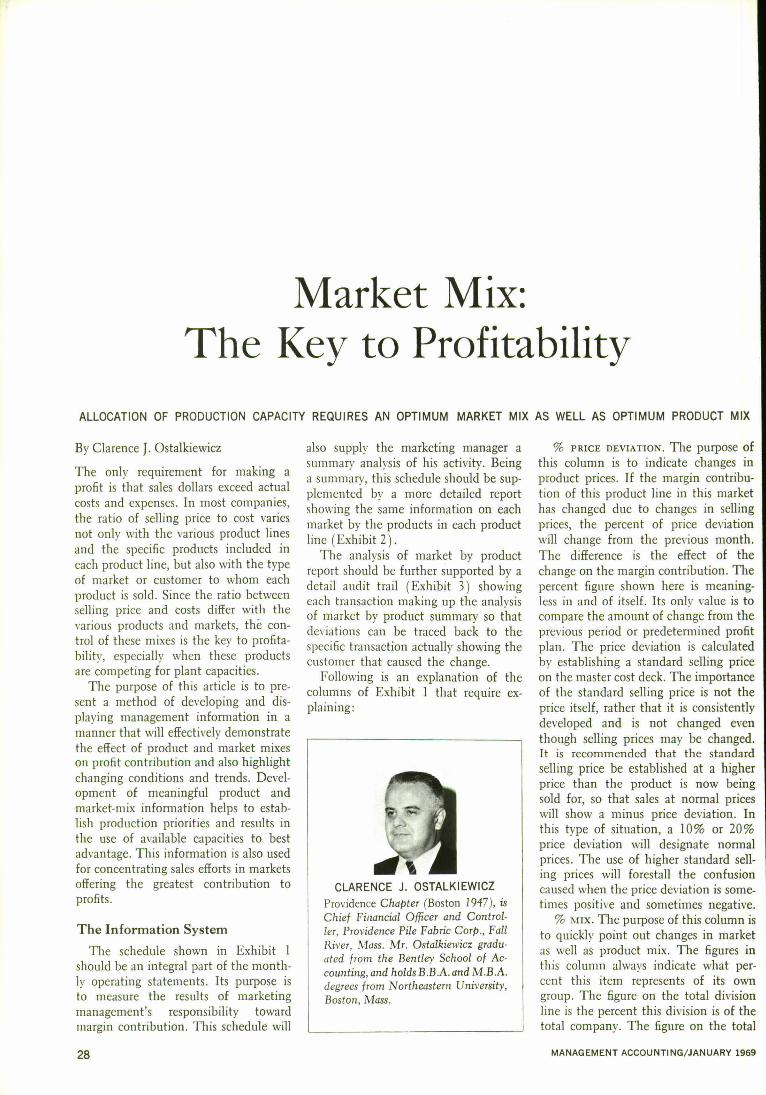

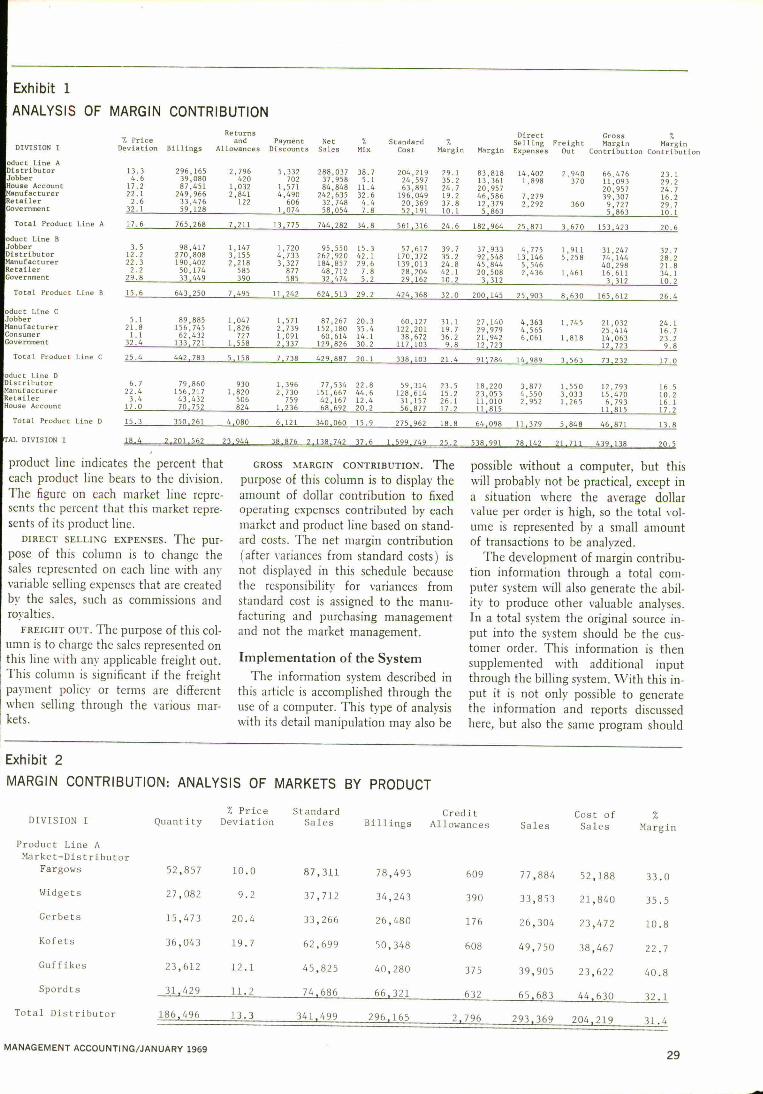

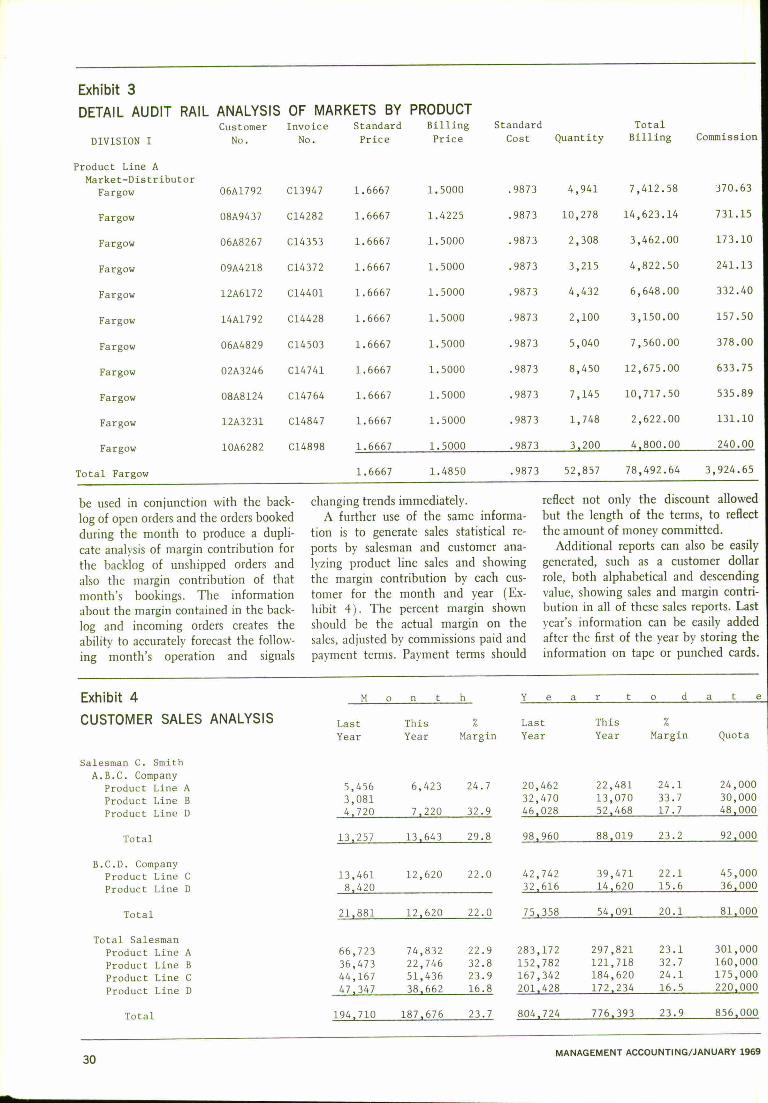

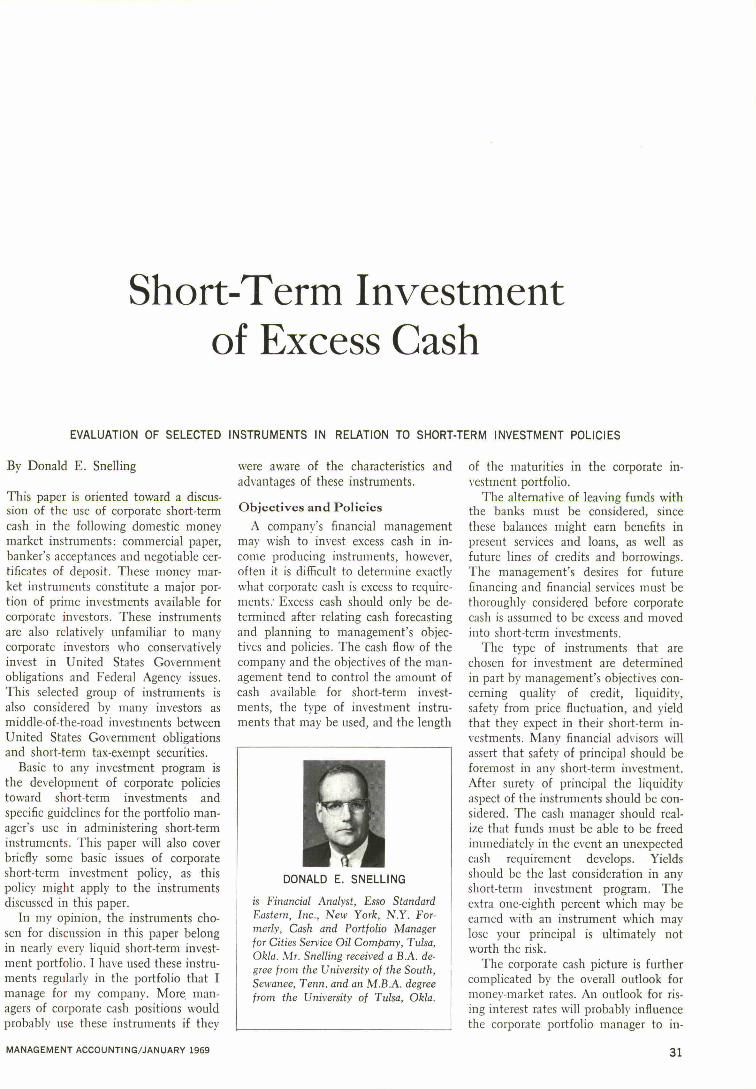

MARKET MIX: THE KEY TO PROFITABILITY 28By Clarence J. Ostalkiewicz

The information system presented here effectively demonstrates the effect ofproduct and market mixes on profit contribution. It also highlights changingconditions and trends.

MANAGEMENT ACCOUNTING /JANUARY 1969 1

2

SHORT -TERM INVESTMENT OF EXCESS CASH 31By Donald E. Snelling

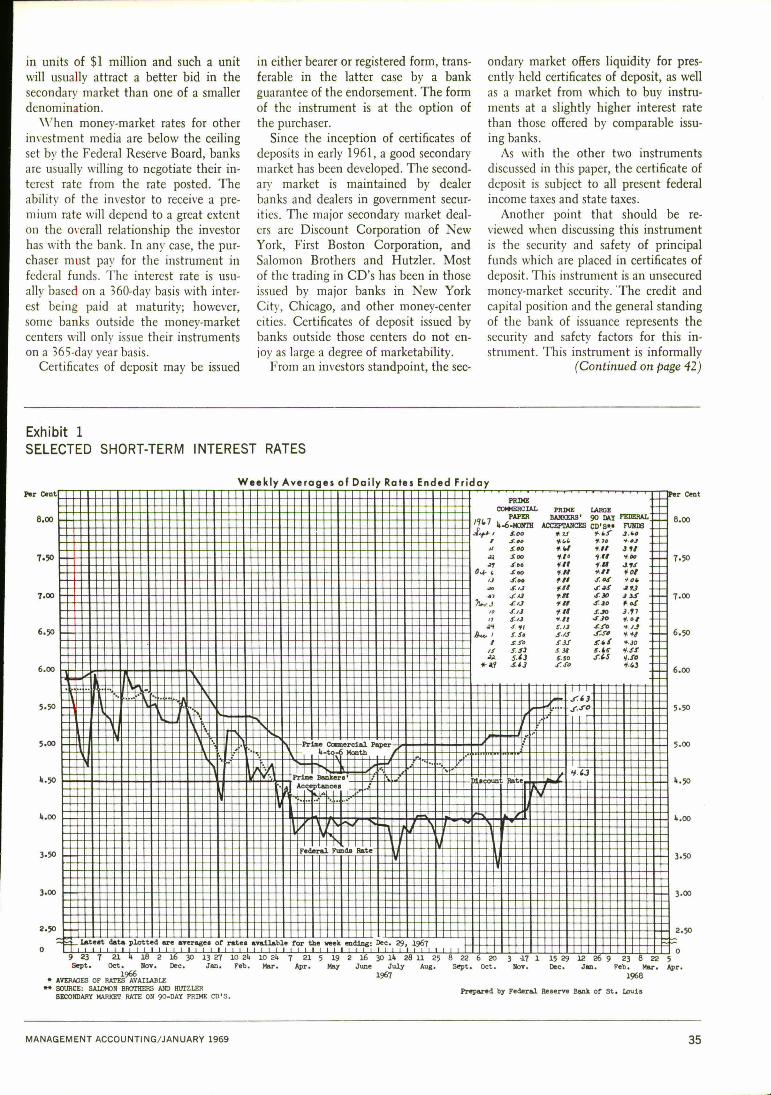

Commercial paper, bankers' acceptances and negotiable certificates of depositare the money market instruments discussed in the article. Some basic issuesof corporate short -term investment policy are also covered.

COMPUTER TIME - SHARING 36By Brandt R. Allen

This article is addressed to the manager. It describes how time - sharing works,why it seems useful, how other firms are now using it and how their usage islikely to change in the future.

ON RELIABILITY STRATEGY IN ELECTRONIC DATA PROCESSING 39By Donald R. Thomas

On -line information systems require sophisticated error detection and recoverymethods on a pre -audit basis.

CLERICAL WORK MEASUREMENT TECHNIQUES IN A CONTROL 43SYSTEMBy Charles D. Winslow

This review of the various techniques includes illustrative examples of their ap-plication. The discussion also covers the key elementsofthe related reporting.

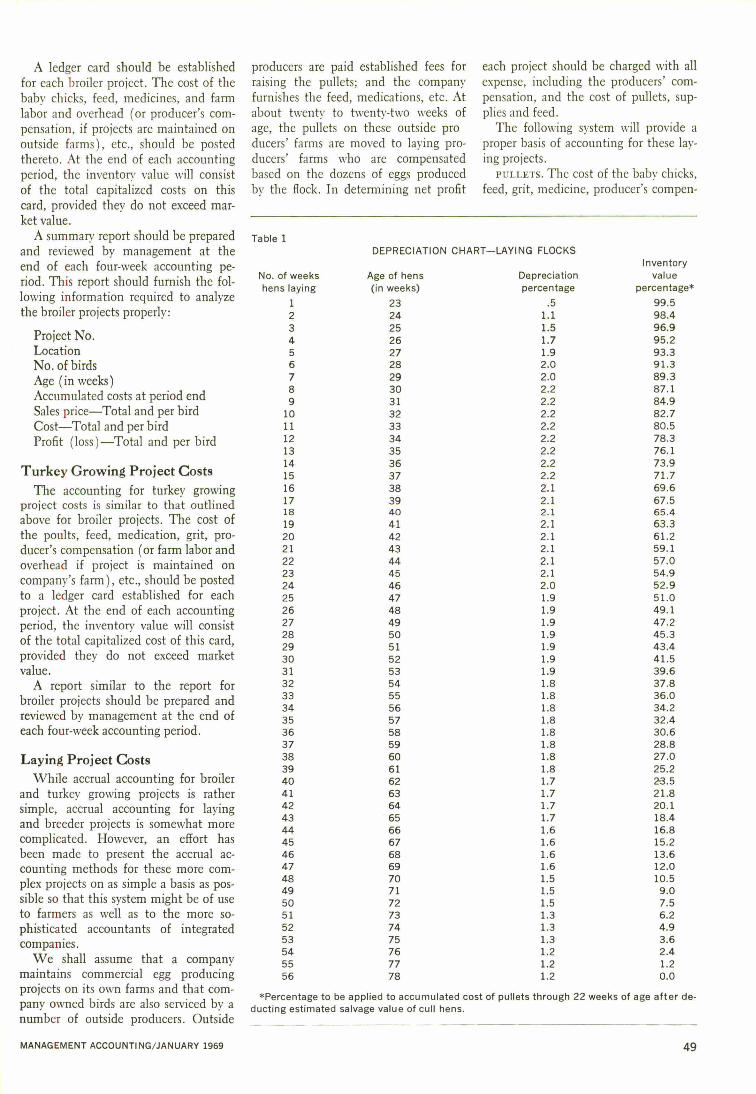

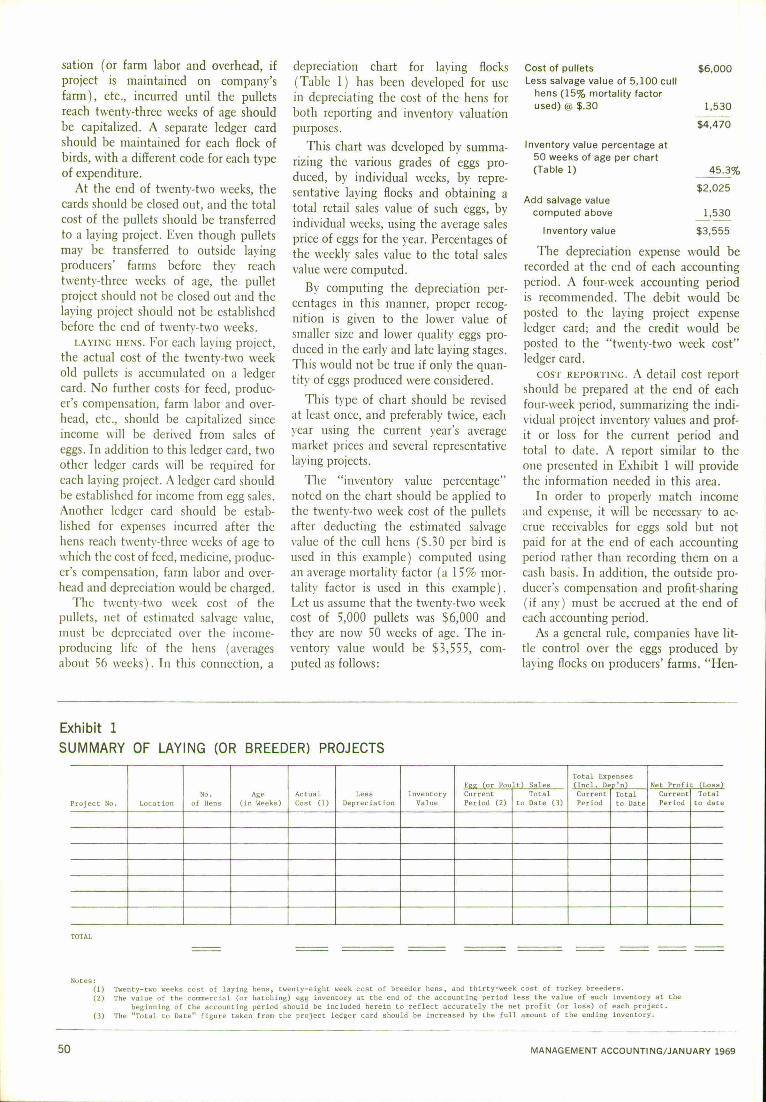

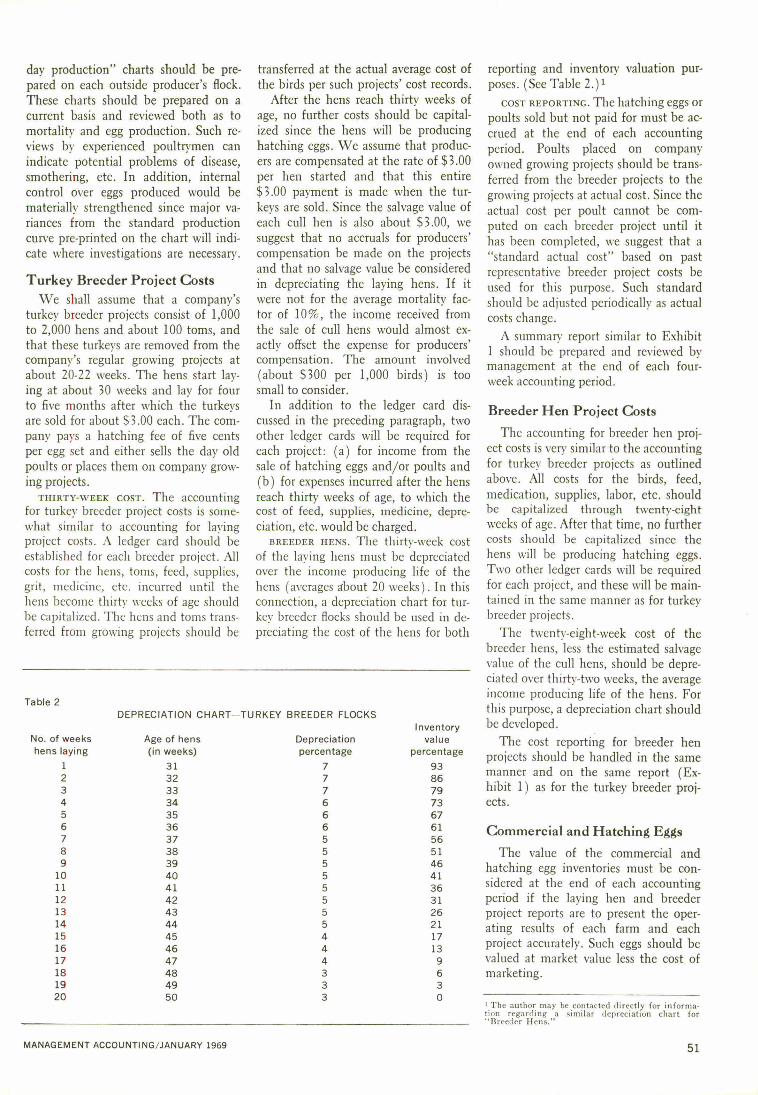

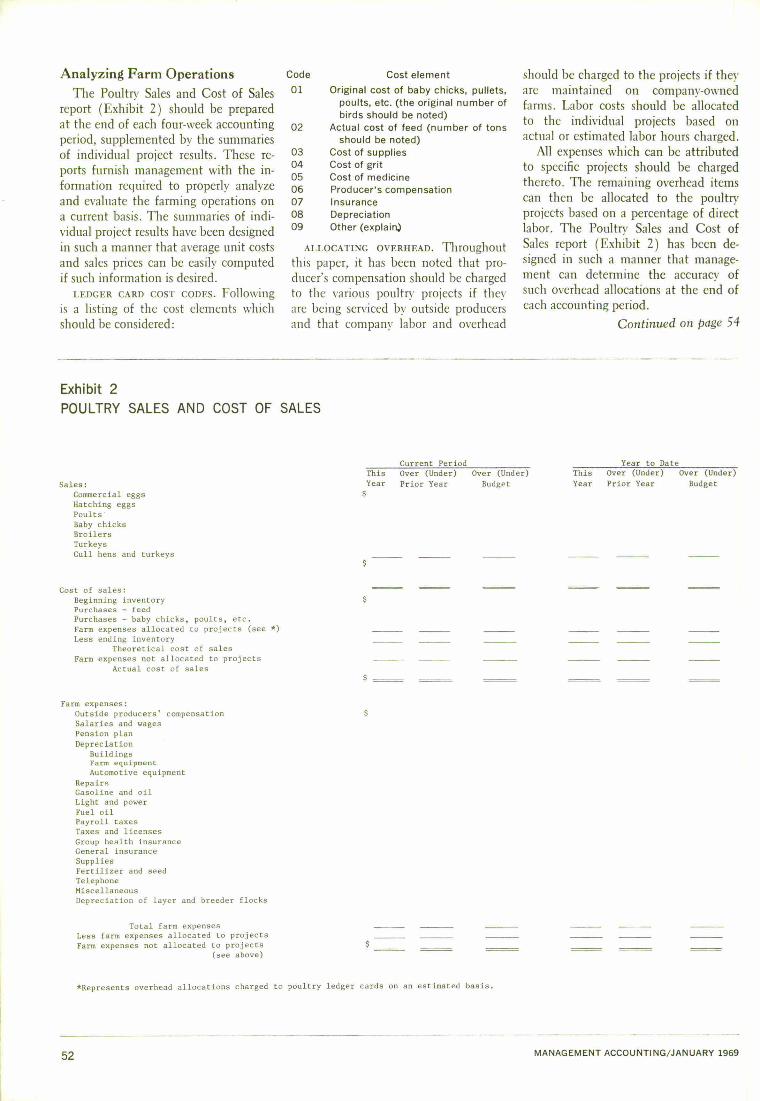

ACCOUNTING FOR POULTRY PROJECTS 48By Charles T. Smith, Jr.

Based on a study ofthe poultry operations ofan integrated feed manufactur-ing company, this article sets forth a simplified method of accounting.

MOTOR FREIGHT MANAGEMENT REPORTING 53By Jesse W. Atwood

Assignment of all costs and revenues on a responsibility basis.

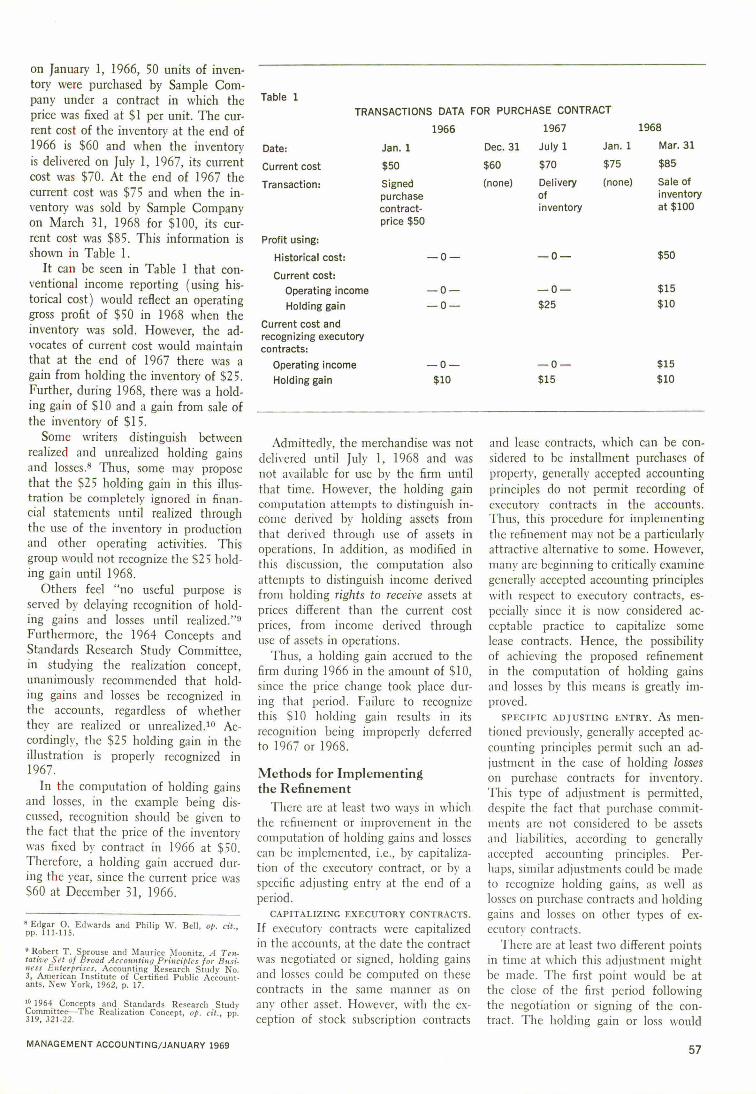

HOLDING GAINS AND LOSSES ON EXECUTORY CONTRACTS 55By Joseph F. Wojdak

A refinement or improvement in the computation of holding gains and lossesis possible by using current cost in valuing assets.

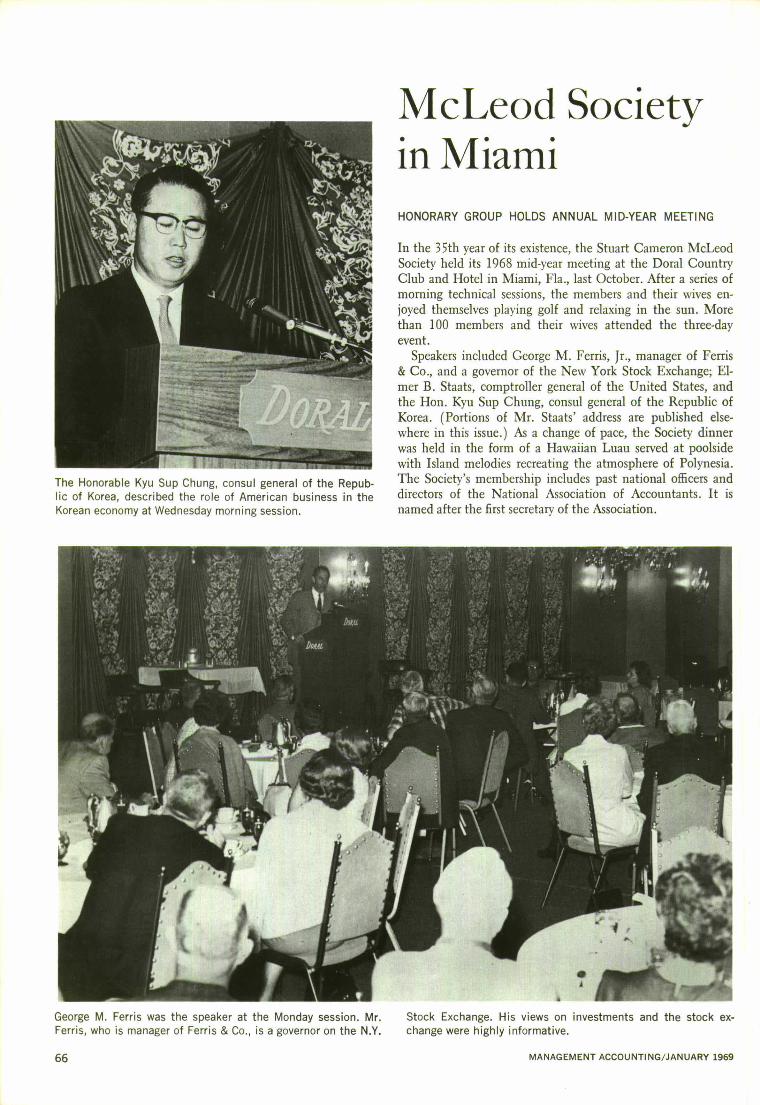

DIARY OF A PERIPATETIC SECRETARY 61Dr. McLeod's wry comments depict exciting era ofNAA growth.

HOW ETHICAL ARE BUSINESSMEN? 63Survey of 1800 businessmen indicates vast majority are more honest thantheir public image.

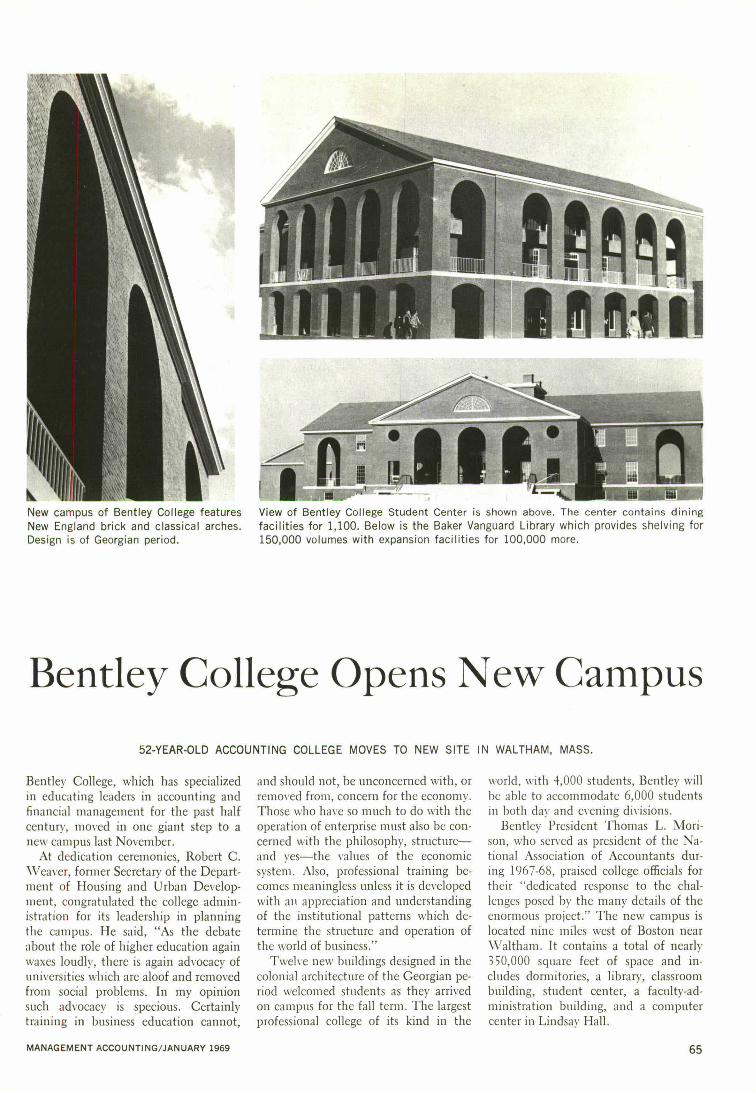

BENTLEY COLLEGE OPENS NEW CAMPUS 6552- year -old accounting college moves to new site in Waltham, Mass.

NEW INTEGRATED MANAGEMENT ACCOUNTING PROGRAM 68

DEPARTMENTS

DATA SHEET items of interest for businessmen 4READERS REACT letters to the editor 6RECENT PUBLICATIONS book review notes 59CLOSE UP focus on members in action 66CHAPTER/MEMBER NEWS all about chapters and members 70

Views expressed herein are authors' and do not represent Association policy unless so stated.

MANAGEMENT ACCOUNTING /J ANUARY 1969

M A N A G E M E N TACCOUNTINGVOL. L NO. 5 JANUARY 1969

Published monthly, for members only, by theNATIONAL ASSOCIATION

OF ACCOUNTANTS505 Park Avenue, New York, N.Y. 10022

EXECUTIVE DIRECTORRawn Brinkley

PUBLISHERDonald M. Woodard

EDITORStephen Landekich

ASSISTANT EDITORAlbert Cohen

FEATURE EDITORRobert F. Randall

EDITORIAL ASSISTANTDebbie Rienzi

PRODUCTION MANAGERErwin S. Koval

CIRCULATION MANAGERMichael R. Cloney

Advertising Representative: Mead Irwin As-sociates, 520 Fifth Ave., New York, N.Y.10036, (212) 986 -9781.

Associate advertising representatives: E. W.Carlson, Union Trust Bldg., Pittsburgh, Pa.15219, (412) 471 -1410; James K. Millhouse,919 N. Michigan Ave., Chicago, Iil. 60611,(312) 642 -6625; Thomas P. Galavan, Gala -van, Hatfield 6 Kittle, Inc., 2322 W. 3rd St.,Los Angeles, Calif. 90057, (213) 385 -3991;Edward Spasek, Galavan, Hatfield er Kittle,Inc., 681 Market St., Suite 798, San Fran-cisco, Calif. 94105, (415) 718 -5815.

Second class postage paid at New York, N.Y.To ensure uninterrupted mail service, pleasenotify us immediately of any change ofaddress. Send present address label and newaddress, including Zip number, to MemberRelations Department. Allow six weeks forchange. Price $1.25 per copy; $10.00 peryear. Subscriptions available only to NAAmembers and to college -level accountingstudents.

Copyright © 1969 by theNational Association of Accountants

MANAGEMENT ACCOUNTING /JANUARY 1969

CommentOnce in a while we take a step forward by improving our publication in termsof its general appearance, format and layout. The most recent change, inSeptember 1968, was preceded by our first major improvement, implementedin September 1965. It was then, three years ago, that we adopted our presentname and introduced this page.

This stepwise upward movement is closely related to our progress in contentquality. As a matter of fact, it is our continuously rising standards in terms ofcontents that prompts us to bring up the appearance to a correspondinglevel. Though less dramatic, perhaps hardly appreciable at times, our efforttoward better article quality is our constant concern. For we assume that anart icle attracts and holds the reader 's at tention primarily by virtue of its use-fulness. While we are in this vein, let us briefly review our latest volume, usingthe topical index as our basis, as we did in the earlier comments on the sametheme.

Each year, we list and topically classify the articles that have appeared in thetwelve issues of the respective volume. Our latest annual topical index waspublished as Section 4 of the August 1968 issue. As usual, the index also includedother technical publications (research studies and monographs) issued by NAAduring the same one -year period.

Volume XLIX (September 1967— August 1968) of our publication contains119 articles, 40 letters to the editor and 137 book review notes. Each article islisted in the topical index under one or more subject headings. Articles referringto a particular industry are also listed under the respective industry headings.

There are 264 entries in the latest index -204 entries under 47 subjectheadings and 61 entries under 33 industry headings. A summary breakdownof the list ings under subject headings is given below:

1. General topics— accounting, financial statements, cost accounting, etc. -45entries (23 %).

2. Topics related to balance -sheet and income - statement items —fixed assets,profits, inventories, etc.-33 entries (16%).

3. Major management accounting techniques —data processing techniques,statistical and mathematical methods, return on investment, direct costing,budgeting, etc. -84 entries (41 % ) .

4. Major purposes served by these techniques— management, productionplanning and control, financial control, pricing, mergers, et c. -37 entries(18 %).

5. Various minor topics -5 entries (2%).

These categories are arbitrarily established, but they are consistent withthose used in previous years' comments. A comparison with the preceding year(see Comment in the October 1967 issue) shows an increase of 10 entries ongeneral topics, with no significant change in other areas. The detail comparison,however, reveals a few interesting changes in terms of articles on individualtopics (the numbers in parentheses refer to Vol. XLVIII): 8 (0) on cash flow,3 (0) on production measurement, 4 (1) on mergers, 11 (6) on return oninvestment, 12 (7) on statistical and mathematical methods, 18 (22) on dataprocessing, 2 (6) on taxes, etc. Some of these changes probably indicate eitherthe problem areas of immediate concern in the respective year (cash flow,capital expenditures) or a trend toward newly developing techniques coupledwith somewhat decreasing interest in the familiar ones.

Data S h e e t JANUARY 1969

AICPA Board CommentsOn SEC Pr oposed RulesCommenting on the proposed regulationsof the Securities & Exchange Commissionto require fuller financial disclosure bysegments of a business, the AccountingPrinciples Board of AICPA declared itself"very much concerned." The Board said itsupported fuller disclosure but suggestedthe SEC should delay new rules untilresearch in this area has been completed.In particular, the Board pointed out thatproblems involved in reporting on segmentassets were so significant that it advisedsuch disclosure should not be imposednow. Many Board members also thought the107o rule for reporting segments too low.The Board noted that it expects to make a"definitive pronouncement" in the futureon the need for, and extent of, disclosureof supplemental information by diversifiedcompanies, based on its analysis ofvoluntary disclosure efforts and theconclusions of current research activitiesand further study.

NAM Oppose s Rule sThe National Assn. of Manufacturers alsoopposed the SEC proposed amendments,citing some of the same reasons made byleading accounting organizations. The NAMconcluded that "Issuance of the amendmentsin their present form could lead toundesirable consequences from the point ofview of the businessman, the investingcommunity and the general public." Theorganization urged delay in issuing theregulations.

Boar d on Earni ngs Per ShareThe AICPA has proposed that companies showtwo kinds of earnings - per -share figureson financial statements. Under theAccounting Board proposal each incomestatement would present primary earningsper share — earnings based on each shareof common stock — and, if residualsecurities exist, equivalent shares ofcommon stock attributable to residualsecurities. The Board also proposed thatearnings - per -share figures be included inthe financial statements which arecertified by independent auditors.

D. &B. Plans Data ServiceA computerized data service to providemarket profiles on three million of thenation's leading businesses is planned byDun & Bradstreet, Inc. The profile wouldinclude street and mailing address, lineof business, number of employees, salesvolume, credit rating, state, city andcounty geographical code and the year thebusiness was started. The service will bein operation in February 1969.

Study Anal yze s Ef fec ti ve Executi veThe most highly successful executives arethose who have specialized early andgeneralized at the graduate level,according to a new research study whoseresults were unveiled at the 37thInternational Conference of the FinancialExecutives Institute. The study,conducted by A. T. Kearney & Co.,management consultants, indicated thatless effective executives were more likelyto confine themselves to a "business"curriculum. The study also concluded thata sizeable portion of the $6 billion spentannually by American corporations fortraining appears to be wasted. FEI plansto publish the full report.

Course in Systems and Proc edur esA new 50- lesson home study course insystems and procedures is now being madeavailable from North American Instituteof Systems and Procedures. Furtherinformation on the course, which i ssponsored and copyrighted by the Systemsand Procedures Assn., may be obtained fromNorth American Institute of Systems andProcedures, Dept. M.A., 4401 Birch St.,Newport Beach, Calif. 92660.

Ac c ount i ng Sys te m for Smal l B ank sA realistic accrual accounting system canand should be developed for smallerbanks contends the Bank AdministrationInstitute which has just issued a manual,"Realistic Accounting and Reporting inthe Smaller Bank." "It seems the time hascome when the financial reporting ofbanks must portray assets, liabilities,and income and expenses in a current,realistic relationship," the manual says.

4 MANAGEMENT ACCOUNTING /JANUARY 1969

Over 10,100 successful CPA candidateshave been coached by

International Accountants Society, Inc.

Byron Menides,President of IAS, says:

"If you don't pass your CPA examinationafter our CPA Coaching Course,we 11 coach you free until you do!"

Aty CPA will tell you it takes more than accountingknowledge and experience to pass the CPA examination.

You must know the quick, correct way to apply your knowl-edge, under examination room conditions.

How you budget your exam time, for example —how youapproach each problem or question — how you decide,quickly, the exact requirements for the solution — constructan acceptable presentation — extract relevant data — and useaccounting terms acceptable to the examiners.

That's where the International Accountants Society canhelp you. As of May 1, 1967, 10,176 former IAS students whohad obtained all or a part of their accounting trainingthrough IAS had passed CPA examinations. Our CPA Coach-ing Course is proven so effective we can make this agree-ment with you:

"If any IAS CPA COACHING COURSE enrolleefails to pass the CPA examination in any stateafter meeting all the legal requirements of thestate as to residence, experience, preliminary edu-cation, etc., IAS will CONTINUE COACHINGWITHOUT ADDITIONAL COST unti l the en.rollee is successful."

The IAS CPA Coaching Course is designed for busy ac-countants. You train at home in your spare time, at your ownpace. Most important, every lesson is examined and gradedby one of our faculty of CPA's, who knows exactly the prob-lems you'll face in your CPA examination.

If you need refresher training in certain areas, IAS willsupply, at no extra cost, up to 30 additional elective assign-ments, complete with model answers, for brush up study.

Approved under the new GI Bill

The IAS CPA Coaching Course as well as the full IASaccounting curriculum is approved under the GI Bill. Youstart any time you please —there are no classes, no fixed en.rollment periods. So, you can make maximum use of thetime available, starting as soon as you enroll and continuingright up to the examination dates.

Send today for free report

To get the complete story on how you (or some memberof your staff) can benefit from the proven IAS CPA Coach.ing Course, just fi ll out and mail the coupon below. Noobligation.

r ---------------------------

I Interna tiona l Accountants Society, Inc.A Home Study School Since 1903Dept. 8907, 209 W. Jackson Blvd.Chicago, Illinois 60606Alt: Director of CPA CoachingPlease send me your new report on the IAS CPA CoachiugCourse. I understand there is no obligation.

I ,.I name ..........................................:...................:... ...............................

Address............................................................... ...............................

Cit y................... .............................. ........ ....... ......................... ..........I

St ate.................................. ................................Zip...........................

Employed by

Approved under the new GI Bill. Check here if entitled to GI Bill benefits.Accredited Member, National Home Study Council.

Readers React

Passive IncomeTo the Editor:

As aptly pointed out by Michael R.Skigen & Eugene K. Snyder in the arti-cle "It Pays to Pay: Accepting Section531 Penalties May Be Sound Econom-ics" ( August 1968) , the additional taxmay not be as bad as one might thinkin view of the available alternatives.However, I think the authors shouldhave gone one step further and pointedout one of the dangers a closely heldcompany may run up against when itdoes accept the penalty tax under Sec-tion 531 and decides to invest the avail-

Stat Tab's answerto an over - workedbilling department:

able cash in marketable securities.The closely held company must keep

in mind the potential personal holdingcompany problems when it elects to in-vest excess funds in investments thatproduce so- called passive income. SinceSection 542 (a) (1) was amended withrespect to taxable years beginning afterDecember 31, 1963, many closely heldcompanies found themselves with per-sonal holding company problems. Thelaw was amended to reduce the grossincome requirements of a personal hold-ing company from 80% to 60 % . Thispassive type income generated by in-

The AutomatedAccounts ReceivableSystem.

/ ,

i► -

SfAiTAB

vestments could result in a manufactur-ing or sales company becoming a per-sonal holding company.

The tax on undistributed personalholding company income is 70 % , orequal to the top individual tax bracket.It is true that a company cannot be sub-ject to both the personal holding com-pany tax and the penalty tax underSection 531, however the difference liesin the application of both taxes by theInternal Revenue Service.

Whether a company is l iable for thepenalty tax under Section 531 is usuallythe result of litigation, however the de-

You'd expect a program like thisto come from Stat Tab. It's fast,accurate, economical and informa-tive. Your statements are accuratelyprepared —on time —each month.In addit ion, you receive: An AgedAccounts Receivable Report; AnActivity Card, listing the 12 monthactivity of each account; Manage-ment Reports that analyze eachaccount, and Flexibili ty... allowingyou to make changes whenever youwant. Stat Tab's been answeringproblems since 1936, our Auto-mated Accounts Receivable Systemcould be the answer for you. Forinformation, contact:

DATA SERVICE CENTERSA Division of Statistical Tabulating Corporation_ The Answer Company.

National Headquarters: 104 South Michigan Avenue, Chicago, Illinois 60603 • (312) 332 -2484Since 1936. Offices in principal cities coast-to-coast-

MANAGEMENT ACCOUNTING /J ANUARY 1969

termination of the personal holdingcompany tax is generally based upon thefacts in each situation. In other words,it is much easier for the Internal Reve-nue Service to make the personal hold-ing company tax stick than it is forthem to prove that a company has ac-cumulated earnings beyond a reasonableneed.

The tax under the personal holdingcompany regulations is not much of analternative to the penalty tax for accu-mulated earnings.

R. S. McCoy, Jr.Tax Manager

Price Waterhouse & Co.

Columbus, O h i o

Tread Cautiously

To the Editor:

Mathematical modeling described inthe May 1968 issue by Alex E. Den -haan in the article, "Dynamic BusinessModels —A Tool to Meet New Business

Make Profits for Your Companyand More Money for Yourself!... ENROLL in NOrlhAmeftan'SMewNOME STUDY COURSEinsystems & ProcedureSponsored by SYSTEMS 8PROCEDURES Association -

I:41f1I e1North American Correspondente Schools has guided athousands of ambitiousmen and women to successthrough its ac credited s —

Home- Study C ourses inmany fie lds.

NOW NOR TH AMER ICAN AN NOUNCES itsnew 50- lesson Course in Systems & Procedures. Writtenand edited with the help of acknowledged leaders in thesystems and procedures field and sponsored by the Sys.tems & Procedures Association, this is a complete, compre.hensive, authentic and up -to-date correspondence course on For Training Re Trainingsystems and procedures. INDUSTRY PERSONNEL...If you would like to "preview" North American's Coursethe Course without obligation, ins tems and proceduress designed for those nowjust mail the coupon for FREE In Systems Departmentsfact-filled CAREER OPPOR- who want to broaden,T U N I T Y BOOKLE T, plus fu ll brush up on or "fill indetails on the North American gaps" in their knowledgeInstitute of Systems and Pro. of the subject... for com-cedures. There's no cost orobli- panies —both large andgation —now or ever. No sales- small —who desire to trainman will call. Mail the coupon their own personnel intoday, systems and procedures

.and for beginners whodesire a knowledge of

SPECIAL DISCOUNTS systems and procedures._1 AVAILABLE for

Multiple Enrollments from the some Company

NORTH AMERICAN INSTITUTE OF SYSTEMS& PROCEDURESDept. 3681, 4401 Birch Street, Newport, California 92660

MANAGEMENT ACCOUNTING /J ANUARY 1969

Challenges" is truly a great assist inmanagement planning and decisionmaking. Our experience certainly en-dorses the two payoff stages of dynamicmodels. However, before we entice theuninitiated to plunge into this bed ofroses, we better warn that there are somevery sharp thorns.

Most models will be composed of anumber of smaller models covering man-ufacturing, research, market, marketshare, etc. The structuring of these canbe very time - consuming and expensive.If one plunges in to make a fine struc-tured model of a large job on his firsttry lie will probably fail as he gets miredin the multitude of details.

I would heartily recommend that anynovice start by modeling an existingbusiness where the various segments ofthe model can be tested and validatedagainst historical data. A rough modelof the business which can be createdrapidly can be utilized to seek out theimportant segments of the business. Asthese are defined, the finer structuredmodels can be built and data collectedfor them in the areas which have thesensitivity. However, again let me urge

NEWCOMPUTER?Protect

Your

Investment

... AdoptProfessionalDocumentationTechniques —NOW !

that at each stage the models be testedand validated against historical data.

V. C. QuarlesAssistant Control Manager

Explosives DepartmentE. I. du Pont de Nemours 6 Co.

Wilmington, Del.

Chapter Assistance to CollegesTo the Editor:

Your article, "Consultants to Acade-mia," is more timely than you mightrealize. Please add the Cedar RapidsChapter to your list of cooperating chap-ters. Since mid -1967, the chapter hasbeen providing assistance to Area TenCommunity College in its developmentof accounting programs.

Speaking as one who must be provid-ing a relevant education for studentsentering the accounting field, I feelNAA chapter participation in curricu-lum development is necessary andgreatly appreciated.

Edward L. BurrellAccounting Coordinator

Area Ten Community CollegeCedar Rapids, Iowa

DOCU -PAK is a complete set of documentation standards and procedures for theS/360, H /200 and other configurations. DOCU -PAK is being used today by Federaland State government agencies, "Fortune" 500 companies and small business con-cerns.DOCU -PAK is priced at $245., a fraction of the cost of developing your own procedures

S Y N E R G E T I C S C O R P O R A T I O N

Quality Analysis and ProgrammingNorthwest Industrial Park

Burlington, Massachusetts 01803Telephone: (617) 272 -3450-3450

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -SYNERGETICS CORPORATION: I am in terested in l earn i ng how DOCU -PAK can develop businessapp l i ca t i ons , t rai n pers onne l and doc um ent s ys tems . P leas e s end :—Free b roc hure des c r i b i ng DOCU -PAK—A DOCU -PAK for 10 -day on- approva l exam ina t ion

Fl

ADDR

CITY

(P leas e p r i n t a l l i n fo rm at i on)

PT

unknown values place your business in a realm of uncertaintyThe increasing complexity of business operations requiresvaluation counsel for: federal, ad valorem and estate taxes;sale, merger, allocation of purchase price, insurance,condemnation, cost accounting, depreciation;and other corporate requirements involving knowledgeof tangible and intangible property value.

Consultants in Valuation since 1896. AP M E R I C A N

P P L I S A T

The American Appraisal Company, Milwaukee, Wisconsin 53201 U.S.A. • Canada • Philippines • Brazil • France • Italy • Spain

A Conceptual Framework forAnalyzing and Evaluating

Managerial DecisionsA FRAMEWORK FLEXIBLE ENOUGH TO COPE WITH A GREAT VARIETY OF PROBLEMS

By K. Fred Skousenand Belverd E. Needles, Jr

If we assume that management is in-creasingly faced with complex anddiverse decisions, then it follows thatsome frame of reference for viewingthese decisions might be helpful. Fur-ther, if we assume that the managementaccountant is to assist management insolving its wide range of problems bygathering, organizing, interpreting, andcommunicating relevant data for man-agerial decision - making purposes, it maybe contended that the managementaccountant needs a frame of referencefor developing and organizing this data.

j_

'AK. FRED SKOUSEN

is Assistant Professor of Accountingat the University of Minnesota, Min-neapolis, Minn. Professor Skousen, aCPA, holds a B.S. degree from Brig-ham Young University and M.A.S.and Ph.D. degrees from the Univer-sity of Illinois. He has published pre-viously in another accounting journal.

MANAGEMENT ACCOUNTING /JANUARY 1969

The purpose of this paper is topropose such a conceptual frameworkwhich may be useful for analyzing andevaluating managerial decisions. Ourintention is to have the framework aidin making original decisions as well asin evaluating the results of past decisionsonce they have been put into effect. Wecall the framework a Decision Evalua-tion Model (DEM) and base it on anoperational approach to solving prob-lems.

An "Operational Approach"

A framework which is useful for theabove purposes must be flexible enoughto cope with a great variety of problemsand circumstances. Not only are theyvaried, they are dynamic, continuallychanging. To provide the frameworkwith required flexibility, an operationalapproach is employed.

The operational approach is a logicaland scientific approach to problemsolving.' In essence "operationalism" 2

means that having established a specificpurpose, one can develop concepts andmeans to accomplish that purpose.Therefore, the key elements of theoperational approach are: (1) a specific

1 Ma n y o f F . S . C. No r th ru p 's b as ic id eas , d irec t edto ward business decision - making problems, a r e em-bo d ied in t h e ap p ro ach p ro pposed here. See F . S . C.No r th ru p , Th e Logic of t he Sci ences and t h e H u -man i t i es, MacM ill an , New Yo rk, 1947, Ch ap te r I .

2 Th is t e rm is des cribed in some de ta il in connec-tion with an opera tion al co n cept o f in co m e in No r-ton M. Bed fo rd 's book. I n come Determi nat ionTh eo r y : An A cc o u n t i n g Fr a me wo r k , Addison -Wes-ley , R ead in g, Mas s. , 1965, p p. 67 -70, 73.

objective and (2) relevant concepts andmeans to achieve the desired results.In an accounting sense this means de-velopment of useful data and methodsof analysis to accomplish the specificpurposes for which the information isto be used.

This approach to solving businessproblems recognizes that single, rigidconcepts and methods will not be ad-equate-for every purpose and situation,especially in an increasingly complexand changing business economy. In-

I

BELVERD E. NEEDLES, JR.

is Assistant Professor of Accounting atTexas Technological College, Schoolof Business Administration, Lubbock,Texas. He was formerly on the re-search staff of the American HospitalAssociation, Chicago, Ill. ProfessorNeedles is a CPA and holds BBA andMBA degrees from Texas Technologi-cal College. In February 1969 he willreceive his Ph.D. from the Universityof Illinois.

stead, concepts are considered relativeto the set of operations with which theyare connected. Thus, as P. W. Bridge -man states, the proper definition of aconcept is not in terms of its properties,but in terms of the operations withwhich it is associated.3 This provides forthe flexibility to adjust to a changingenvironment.

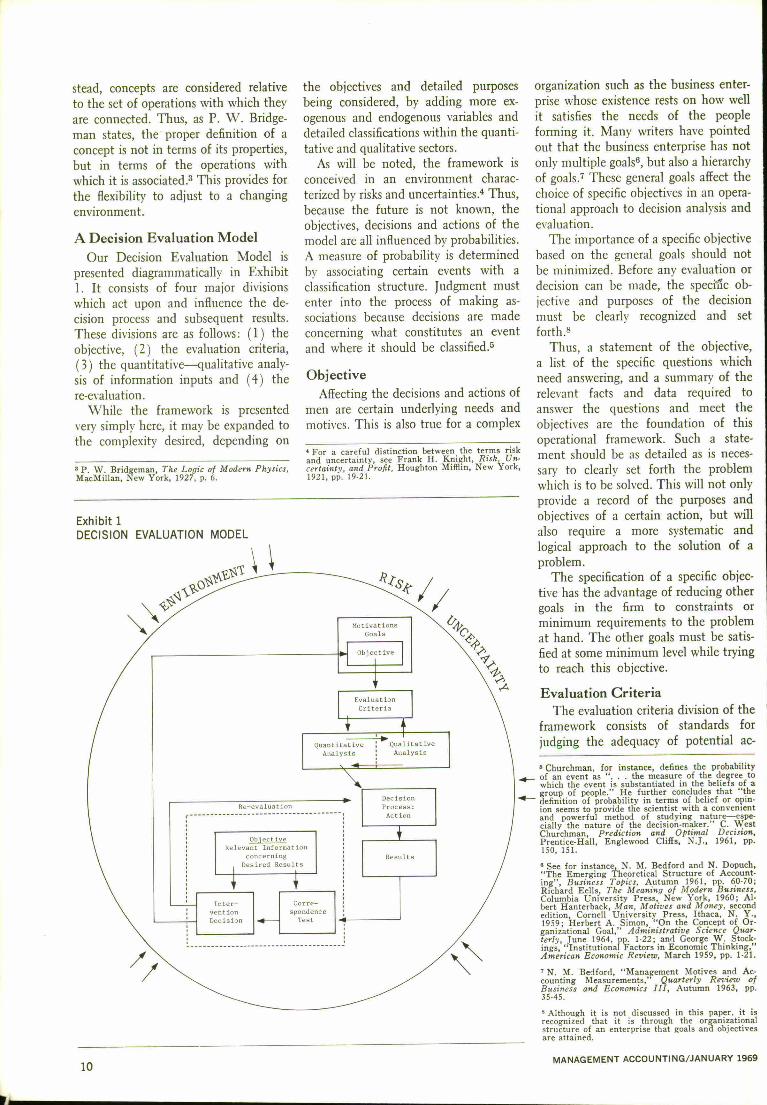

A Decision Evaluation Model

Our Decision Evaluation Model ispresented diagrammatically in Exhibit1. It consists of four major divisionswhich act upon and influence the de-cision process and subsequent results.These divisions are as follows: (1) theobjective, (2) the evaluation criteria,(3) the quantitative—qualitative analy-sis of information inputs and (4) there- evaluation.

While the framework is presentedvery simply here, it may be expanded tothe complexity desired, depending on

a P . W . Brid ge in an , Th e Lo g i c o f M o d e r n Ph y s ics ,Mac Mil lan , Ne w Yo r k , 1927, p . 6 .

Exhibit 1DECISION EVALUATION MODEL

10

the objectives and detailed purposesbeing considered, by adding more ex-ogenous and endogenous variables anddetailed classifications within the quanti-tative and qualitative sectors.

As will be noted, the framework isconceived in an environment charac-terized by risks and uncertainties.4 Thus,because the future is not known, theobjectives, decisions and actions of themodel are all influenced by probabilities.A measure of probability is determinedby associating certain events with aclassification structure. Judgment mustenter into the process of making as-sociations because decisions are madeconcerning what constitutes an eventand where it should be classified .5

ObjectiveAffecting the decisions and actions of

men are certain underlying needs andmotives. This is also true for a complex

4 Fo r a ca re fu l dist inc t io n between th e t e r m s r is kan d u n cer t a in ty , see F r a n k H . Kn igh t , R i s k Un -cer ta i nt y , a nd Pr o fi t , Ho u gh t o n Mi ff l in , N ew Fo r k,

1921, pp. 19 -21.

Mo t i v a t i o nsG o a l s

Objective

rG�♦A

Evaluat ioon W

C r i e r i s

Qu a n t i t a t i v e Qu a l i t a t i v eAnalysis , Analysis

De c i s i o nRe- evaluation Process:

r - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - Ac t i o n

Obje c t i v eRelevant Information

co nce r ni ng ResultsDesired Results

I n t e r - . -v e nt i o n - P -- • Decision

organization such as the business enter-prise whose existence rests on how wellit satisfies the needs of the peopleforming it. Many writers have pointedout that the business enterprise has notonly multiple goalse, but also a hierarchyof goals.' These general goals affect thechoice of specific objectives in an opera-tional approach to decision analysis andevaluation.

The importance of a specific objectivebased on the general goals should notbe minimized. Before any evaluation ordecision can be made, the specific ob-jective and purposes of the decisionmust be clearly recognized and setforth.8

Thus, a statement of the objective,a list of the specific questions whichneed answering, and a summary of therelevant facts and data required toanswer the questions and meet theobjectives are the foundation of thisoperational framework. Such a state-ment should be as detailed as is neces-sary to clearly set forth the problemwhich is to be solved. This will not onlyprovide a record of the purposes andobjectives of a certain action, but willalso require a more systematic andlogical approach to the solution of aproblem.

The specification of a specific objec-tive has the advantage of reducing othergoals in the firm to constraints orminimum requirements to the problemat hand. The other goals must be satis-fied at some minimum level while tryingto reach this objective.

Evaluation Criter iaThe evaluation criteria division of the

framework consists of standards forjudging the adequacy of potential ac-

8 Churchman, for instance, defines the probabilityf of an event as "... the measure of the degree to

gwhich the event is substantiated in thebeliefs of a~ definition ofoprobability in erms of be l ie f ot opin-

ionseems to provide the scientist with a convenientand powerful method of studying nature —espe-cially the nature of the decision - maker.' C. WestChurchman, Prediction and Optimal Decision,Prentice-Hall, Englewood Cliffs, N.J. , 1961, pp.150, 151.

See for instance N. M. Bedf ord and N. Dopuch,"The Emerging 'theoretical Structure of Account-ing' , Business Topics, Autumn 1961, pp 60 -70;Richard Eells, The Meaning of Modern Business,Columbia University Press, New York , 1960; Al-bert Hanterback, Man, Motives and Money, secondedition Cornell University Press, Ithaca, N. Y.,1959; herbe rt A. Simon, On the Concept of Or-ganizational Goal," Administrative Science Quar.terly,June 1964, pp 1.22; and George W. Stock.ings, " Institutional Factors in Economic Thinking,"

R American Economic Review, March 1959, pp. 1 -21.\

I N. M . Bed fo rd , " Management Mo t ives an d Ac-co u n tin g Meas u r em en t s , ' Qu a r t er ly Re v i ew ofBu s i nes s an d Eco n om ics I I I , Au tu m n 1963, pp.35 -45.

9 Alth o ugh it is not dis cu ss ed in th is paper, it isrecognized that it is through the organizationalstructure of an enterprise that goals and objectivesare attained.

MANAGEMENT ACCOUNTING /J ANUARY 1969

counting information. The developmentof a coordinated group of such criteriaor standards has been discussed recentlyin at least two studies, one issued by acommittee of the American AccountingAssociation9 and the other developed byHoward J. Snavely.10 The committeehas developed a set of four standards:relevance, verifiability, freedom frombias, and quantifiability. The standardof relevance is the primary criterionunder this scheme and requires that in-formation be directed toward a specificpurpose, that is, information should beassociated with the actions it is designedto facilitate or with the results it isdesired to produce.

The committee recommends that atrade -off might exist in the applicationof the standards: Adequate fulfillment

...does not require complete adherenceto any one or all of these standards un-der all circumstances. It is possible torealize them more fully in some casesthan in others. Further, it is basic to rec-ognize that different uses call for differ-ent degrees of adherence." 11

Snavely, on the other hand, has effec-tively argued that there should be ahierarchy of criteria, that is, somecriteria are more widely applicablethan others. He suggests that usefulnessis on the highest level of the hierarchybecause it is unrestricted in its appli-cability. This statement asserts that datamust be useful before it qualifies foraccounting information. To be useful,Snavely urges that data must meet allsecond level criteria which are "mutuallyexclusive and singularly powerful." 12

Thus, there can be no trade -off onthis level. He suggests that the reasonthe AAA's statement must accept thepossibility of a trade -off among thestandards is because the committee hasmixed second and third level criteria.

These important studies leave somequestions unanswered, such as, are thesecond level standards truly indepen-dent, must they be independent, whatis the place of verifiability and freedomfrom bias in accounting, are thereother standards, and can methods bedeveloped which will allow effectiveapplication of the standards? Answersto these and other questions may not be

A Statement of Basic Accounting Tkeor? Ameri-can Accounting Association, Evanston, Ilf., 1966,pp. 7 -13.

]U Howard ] Snavely,• "Accounting InformationCrite ria," The Accounting Review, April 1967, pp.223.232.11 A Statement..., op.cit., p. 8.19 Snavely, op. cit., p. 232.

immediately forthcoming, but researchshould continue in this area because ofthe important place that informationcriteria occupy in a decision evaluationmodel.

The evaluation criteria division of theframework serves a dual purpose. First,based on the specific objective, thecriteria are used as guides in selectingthe methods that will most likely pro-duce the information (both quantita-tive and qualitative) required for theparticular decision. The search for datais aided from its initiation. Effort can bedirected toward the best possibilities.Second, during the accumulation of dataand at its completion, data gatheredwithin the quantitative - qualitative phaseof the framework may be judged on thebasis of the criteria standards in order toensure that it meets them sufficientlyto be useful in the decision process.Certainly, accountants usually attemptthis type of evaluation on an informalbasis, both consciously and unconscious-ly, but a formal system of criteriaand a recognition of its role in thedecision framework should aid theentire process.

Quantitative—QualitativeAnalysis of Information Inputs

Exhibit 1 shows the important in-teraction between the quantitative andqualitative factors within the frame-work. The ideal is to quantify as manyof the qualitative factors as possible.While some subjective elements willalways be present in decision - making,the use of modern mathematical tech-niques and especially the use of com-puters makes it feasible to quantifymany factors which previously weremerely as given and treated as qualita-tive factors.

More specifically, the quantitativesector of the framework deals primarilywith objective facts and figures. It isconcerned with assignment of revenuesor products, divisions, or responsibilitycenters; with various cost classificationsand allocations; and with the mathe-matical and statistical methods of mak-ing revenue and cost analyses. On theother hand, the qualitative sector is con-cerned primarily with subjective factorswhich are difficult to express in quantita-tive terms. However, even here, subjec-tive probabilities should be used to givequantitative expression to qualitativefactors. The use of subjective probabili-ties, where it is feasible, gives properrecognition to past experience and

quantifies the assumptions made. Thus,it forces one to think more logically andanalytically. Better decisions are theproduct of such an analysis.

The Decision Process

In the final analysis then, managerialdecisions should be based on analysesand judgement of both quantitative andqualitative informational inputs whichhave been directed toward a specificobjective and have met certain evalua-tion criteria. After such decisions havebeen implemented and results gener-ated, there is need for re- evaluation ofthe process.

Re- evaluation

The re- evaluation process is centered,as is all the operational approach,around the objective which is in turnsubject to the constraints mentionedpreviously. This process, which consistsof two steps, has the advantage of beingable to use the previous analysis informa-tion and any subsequent informationthat may be relevant to the problem.

The first step is the correspondencetest which has the task of comparingthe results with the objective. It seemslikely that the results will be examinedon some statistical sampling basis. Thecorrespondence test can have two possi-ble outcomes. First, if no difference ora non - significant difference is the out-come, the re- evaluation process ends atthis point. Second, if a significant differ-ence is the outcome, this informationis forward to the next step.

The second step is the interventiondecision which is concerned withwhether or not to take action that willaffect the results in the future. This isa separate process from the correspond-ence test and may result in one of threepossible courses of action. First, theremay be a decision to take no action.For instance, the correspondence testmay reveal that the goal is being ex-ceeded or if the goal is not being met,it may be the result of reasons not with-in the control of this part of theorganization such as changes in con-straints arising from other goals withinthe firm. Second, there may be adecision to take action and change theoriginal decision, thus affecting theresults in the future. This decision isbased on the objective, the previous in-formation collected in making theoriginal decision, any additional infor-

(Continued on page 15)

MANAGEMENT ACCOUNTING /JANUARY 196911

Management Systems in aGrowth Company

A FRESH VIEW OF HOW TO ORGANIZE AND INTERRELATE MANAGERIAL ACTIONS

By Carl J. Thomsen

In current management literature thewords "Management Systems" and"Management Information Systems"appear frequently. Does this reflect onlya fad?

Is the current interest in Manage-ment Systems only a fad as was thepopularity of long -range planning in themanagement literature and managementseminars of the early 1950's? Top man-agers demanded an emphasis on long -range planning, and their subordinatesresponded with accumulations ofnumerical projections of billings andprofits which were reviewed at carefullyselected resorts in remote locations toassure concentration on .the long termwithout the distraction of meeting to-day's performance goals.

Then during the middle 50's,thoughtful managers became disen-chanted with their long -range planningefforts. They began to ask themselves,"Is this really long -range planning ?""Is it serving our purposes ?" And theanswers generally were "No." This dis-enchantment brought a lull in thepopularity of long -range planning. Dur-ing this lull, managers thought aboutlong -range planning in a more funda-mental way and evolved the approacheswhich are beginning to be used current-ly. The difference between the popu-larity of long -range planning in the early1950's and today is that now long -rangeplanning is looked upon as a fundamen-tal management process with emphasis

12

on how to accomplish goals rather thanmerely to express them.

There are some disturbing indicationsthat the current interest in Manage-ment Systems is like the interest in long -range planning of the early 1950's. Theincreased popularity of ManagementSystems in management literature andseminars is nearly fantastic. Anotherconcern leading one to the feeling thatinterest in Management Systems maycurrently be only a fad is the too fre-quent emphasis upon tools and tech-niques rather than upon the goals to beachieved. Also, there is too little interestin understanding of Management Sys-tems in a fundamental way.

Or, is the current interest in Man-

CARL J. THOMSEN

Senior Vice President in charge of Or-ganization and Management SystemsDevelopment Activity, Texas Instru-ments, Dallas, Tex. Mr. Thomsenjoined Texas Instruments in 1946 af-ter serving as an officer in the NavalReserve. He is active in the affairs ofRensselaer Polytechnic Institute fromwhich he graduated.

agement Systems the beginning of amanagement revolution? There are thosewho do feel that we are entering upona management revolution, althoughtheir names for it may differ.

The Management Revolution

The following will indicate whyreference is made to a managementrevolution rather than just a cybernetic,information, or industrial revolution.For this purpose, the author refers to oneof the basic organizational philosophiesof Texas Instruments. This companybelieves that the business must beProduct - Customer centered, and identi-fies as line functions those most closelyrelated to this Product - Customer center—the create, make and market func-tions. Creating identifies the develop-ment and design of products; makeidentifies production; and market —theidentification and anticipation of thecustomer's needs. These are the main-stream actions of a business. Activitiessuch as control, personnel, procurement,accounting, industrial engineering, aresupporting and performance- enhancingfunctions serving the three line or mainstream efforts of the business.

With create, make and market inmind, the first industrial revolution isrecognizable as concerned almost en-tirely with only one of the three; it wasa drastic departure from the past in theway actions were organized to makeproducts. Over nearly several hundredyears, mechanization —and in the lasttwo decades automation of production

MANAGEMENT ACCOUNTING /JANUARY 1969

—has progressed to the present exten-sive computer control of productionprocesses in some industries. Mechaniza-tion and automation though are onlyhigher degrees of structuring of actionsto make products.

Now though, one is beginning to seeautomation in the create function too.For example, a number of electroniccompanies —and TI is one — currentlyare developing their capability to designcomplete electronic circuits by com-puters. Computer programs identify thecomponents required, determine theiroptimum location in relation to oneanother and then run a maze of likelyinterconnecting paths to determine thebest one.

With growing automation in thecreate function and substantial increaseof automation in the make function, itis inevitable that one's interface withcustomers, the market function will besubstantially influenced too. One ex-ample of this is TI's Supply Companyhaving a communications terminallocated in some of its customers' plants,so that predescribed industrial supplyitems can be ordered.

Thus far the organization of actionsto create products, to make them andto market them has been emphasized.There is also concern with a signifi-cantly higher degree of structuring ofthe actions in the supporting and per-formance enhancing functions, such asaccounting and control, of businesses.This conglomeration and interrelationof the organization of actions in themainstream, supporting and perform-ance- enhancing functions of a businessis the Management System of that busi-ness. This leads to the definition ofManagement System as "How a man-ager organizes actions to use the re-sources of a business to accomplish itspurposes within a particular environ-ment." It is with this broadly definedManagement System that the manage-ment revolution is concerned. Its impactis broad.

Impact of the ManagementRevolution

Major impact of the managementrevolution is by the very nature of itsbreadth; that is, the opportunity formanagers to take an entirely fresh viewof how they organize all the actions andinterrelate them in a business to achievetheir objectives. This is the truly dis-tinguishing characteristic of the man-agement revolution, and it is much more

encompassing than merely information,cybernetics, or industrial revolutions.

How a particular manager organizesactions to accomplish his purposes isexpressed in these four forms:

1. In the first form, how he organizeshis own actions to use his inherentcapabilities — including his motivat-ing and innovating capabilities.

2. In the second form, with his depend-ence upon the abilities of other per-sonnel, how he organizes people. Itis expressed in the conventional man -to -man organization pattern withwhich all are well acquainted.

3. In the third form, the organizationof actions by systems and machinesis expressed. As the degree of struc-turing of actions becomes higher, itis more difficult to separate systemfrom machine because the machine(for instance, the computer) or-ganizes actions (in the form ofcomputer programs) .

4. And the fourth form of expressionis the organization of actions toobtain and apply information andknowledge from the environmentprescribing the arena within whichall other actions are being organized.

One can think of the particularbalance among these four expressionsof how actions are organized as repre-senting a particular manager's style ofmanaging. The management revolutionwill alter significantly the styles thathave been seen so far in business ex-perience.

GAINS. The effects of the impact of themanagement revolution upon Manage-ment Systems and style in terms ofgains and problems include:

1. Progress in the development ofmanagement systems will requirefirst that objectives and purposes forthose systems be clearly stated. Asa consequence, the actions of in-dividuals affected by new manage-ment systems should be moredirected. The consequent reductionin misdirected effort could providethe opportunity to make a sub-stantial gain from the relatively loweffectivity of present business enter-prise.

2. In a world where the needs forhighly skilled and professionallytrained individuals have exceededand portend to continue to exceedthe ability to supply them, the gapbetween the two could be narrowedas managers organize their own and

their subordinates' actions to ac-complish purposes more effectively.As advanced management systemsstructure more of the actions ofmanagers, they should become freeto apply their capabilities to con-ceiving new ideas to solve problems,and to realize opportunities in areaswhere they previously have had littletime. Perhaps this freedom andreapplication of managers' effortsmay result in higher growth ratesfor individual businesses and of theeconomy as a whole.Managers' new freedom and reap-plication of talents could give themthe satisfaction of using more oftheir inherent capabilities.

P R O B L E M S . Some of the problems are:

An aspiring manager ten andcertainly twenty years from nowwithout substantial training in Man-agement Systems, Management Sci-ences, and the use of computers, willnot realize his aspiration. A managertoday who aspires to higher manage-ment levels ten to twenty years fromnow and who has not received suchtraining will be replaced by thosewho have. There will be the inevita-ble strains of obsolete managers di-recting subordinate managers whoare better qualified in the science ofmanaging.With so much emphasis upon thetools and upon newly acquired tech-niques, there is the danger of ourlosing sight of the purposes whichthose tools and techniques shouldhelp one achieve. As defined earlier,management systems organize ac-tions to achieve purposes, and in-cidental thereto there is concern forthe organization of information andthe use of computers. Failure toappreciate that Management Sys-tems are how actions are organizedto accomplish purposes leads to amisplaced emphasis upon the tools,such as computers.The task of developing advancedManagement Systems will be oneof the most difficult undertaken in abusiness institution's history. Therewill be many false starts. There willbe the inevitable disenchantmentwith something which is new. Therewill be swings from wild enthusiasmto highly restricted efforts, but ef-fective advanced Management Sys-tems of a quality expressing the

(Continued on page 15)

MANAGEMENT ACCOUNTING /JANUARY 1969 13

Misuse of Standardsin Decision Making

VARIABILITY MAY BE AS SIGNIFICANT AS THE STANDARD ITSELF

By Rober t W. Rosen

Are standard costs and times really andconceptually valid for decision makingand control? It has already been dem-onstrated that least standard or actualcost is not an appropriate cri terion forselecting among alternative choiceswhen the most efficient resource hasless capacity than the amount of workto be done., Second, overattention to"cost" has generated the notion thatminimizing cost will maximize profits orrate of return. Where costs and revenue,or costs and inventory, are interrelated,as in the case of setting productionquotas, then minimizing cost is notalways coincident with maximum prof-i t s or ra t e of r e turn .

Basically, standards are averages. Onedifficulty which arose as a result of usingonly the average or standard is that ob-jective techniques could not be used todetermine whether an observed variancein actual cost was statistically signifi-cant. Consequently, rules of thumb,such as variance of $100 or 5 %, wereestablished to determine whether thevariance was significant, i.e., whetherfurther investigation was justified. Inshort, accountants usually disregard thedeviations about the standard which isthe very data needed to determinewhether a significant variance has oc-curred.

1 Robert W. Rosen " Accountant—Spare That Va-riance!," N.A.A . bulletin, November 1961, p. 91.

14

Use of Standards in DecisionMaking

The use of standards to select amongalternatives can lead to many pitfalls.Waiting line models provide interestingexamples. Deviations about the stand-ard (machine) time can cause the aver-age amount of in -bank inventory, aver-age waiting time, and carrying cost toincrease by 100% over what they wouldbe if no deviations existed.2 Similarly,the frequency and magnitude of stock -out or runout is much less for the caseof zero deviation.

In general then, operations withgreater deviations about average orstandard machine times incur extracosts in the form of greater in -bankinventories, stockout, or both. It is per-fectly possible, and very probable, thata machine which is faster and thereforehas a lower average time and cost may,by virtue of its variability, generategreater carrying and runout costs. As a

Y E . S . Bu ffa, Mo d er n Produ ct ion Mo n a me en t ,second ed it ion , J o h n W iley , New Yo rk , ,� anuary

1965, pp. 730 -734.

ROBERT W. ROSEN

is Visiting Professor, San Diego StateCollege, San Diego, Calif. ProfessorRosen holds a B.A. degree from ColbyCollege, Waterville, Me. and a Ph.D.degree f rom the University of Pitts-burgh. He is the author of a numberof articles which have appeared in ac-counting periodicals.

result, the total combined cost of usingsuch a machine could be significantlylarger than a slower machine withhigher operating cost but less variabilityin output. Hence, using the standardtime or cost only, which neglects thevariability about the standard, wouldlead to the wrong decision, i.e., a highertotal cost. Obviously, it is minimumtotal cost, not minimum operating cost,which is of primary concern to the deci-sion maker.

It would be tedious and unnecessaryto show in detail that deviations aboutthe computed standard must be con-sidered in choosing among alternativesand when preparing pro forma estimatesof the expected profit from a given setof proposa l s . T h u s , it is qu i t e possib le ,

for example, for sales to increase sub-stantially and for unit cost to remainconstant, while profits decrease. Suchresults might occur when the incremen-tal sales exhibit marked variability, lead-ing to larger inventories, more laborturnover, greater use of overtime, orsome combination of all of them.Standard cost, as currently employed,would not reflect these other costs andwould thus overstate the potentialprofit.

Similarly, one could demonstrate thata deliberate reduction or fall in salesaccompanied by a sufficient decrease invariability could yield larger profits eventhough standard or operating cost perunit remained constant. As a final ex-

MANAGEMENT ACCOUNTING /JANUARY 1969

ample, one can also show that it mightbe more profitable to buy from a vendorwho quotes a longer average deliveryperiod, but less variability, than onewhich delivers faster but with greatervariability about the average deliverytime.

Neglecting the variation or dispersion

Conceptual Framework(Continued from page 11)

mation available, and certain otherconsiderations. These other considera-tions are such things as the likelihoodof failure in the attempt to change, theextent and effects of disruption of theprocess that is now in operation, theeffects of a change on other parts of thefirm, time restrictions, and the relative

Management Systems

(Continued from page 13)

management revolution are not go-ing to be developed without acontinuing commitment of effort tothem. For this reason, it is hopedthat the possible tendency towardManagement Systems being first afad can be avoided. Perhaps theexperience with long -range planningin the 1950's can help to at leastminimize any period of disenchant-ment with Management Systemsdevelopment. It can be minimizedif those in business organizationsand those in educational institutionswill seek to express a science ofManagement Systems which can bereadily communicated. Withoutsuch an underlying body of logicand knowledge, it is only naturalto expect that concentration willcontinue on the "easier to under-stand" tools and some techniques.With individual systems being de-veloped as parts of networks ofsystems, the need will be for menwho can see a business as a whole.It was interesting to hear JamesWebb say in a dedication addressabout a year ago, "To see a manat all you must see the whole man."

about computed aggregates, averages,percentages or standards often resultsin suboptimal decisions, or worse. Whydoes this deficiency exist and continueto exist? Partly, the problem is thatconcepts useful for bookkeeping pur-poses have been misapplied to decisionmaking. A concept which is useful for

values of possible successes or failures.Third, the decision may be made tochange the objective due to changedconditions or to an unrealistic originalobjective.

The Objective Restated

The Decision Evaluation Model isnot a new technique for solving prob-lems, nor can it compensate for basicweaknesses in data or decision - making

This might be reworded, "In thefuture, to see a business at all wemust see the whole business." Toofew men have this ability.

5. Development of Management Sys-tems will bring together managerswho know their businesses, andsystem designers and managementscientists who have substantial pro-fessional competence in their fields.A communication problem betweenthese two exists currently and amajor problem will be to facilitatethis communication in the yearsto come.

6. This management revolution will becreating a new environment inwhich people will be working. It willbe an environment some will see asstructuring their actions far beyonda point where they retain theiridentity as individuals in a businessorganization. If the environmentcreated deserves this characteriza-tion, or if there even a widespreadfeeling that it should deserve it, theadvanced management system de-velopment efforts will have failed.To avoid such failures, it will benecessary for those whose actionsare being structured to participateto the maximum extent possible inthe development of advanced man-

the former may be quite misleading orincomplete for decision making.

Such deficiencies would diminish ifdevelopments in related fields, such asWaiting Line Theory, were studied todetermine the implications for data col-lection and reporting, or advising man-agement.

techniques. Rather, it is a structuredviewpoint, a frame of reference, for ana-lyzing decisions, both prospectively andretrospectively. The framework's opera-tional approach gives it a flexibilitywhich, it is hoped, will stimulate newthoughts concerning the many relation-ships involved in management decisionsand will aid, ultimately, in achieving itsgoal of reducing the uncertainty sur-rounding those decisions.

agement systems, the systems whichwill organize their actions. But thesesame systems— properly conceiveddesigned —will create opportunitiesfor managers and others to use theirinherent capabilities to a muchhigher degree than we have everknown. The opportunity of creatingsuch an environment is the fasci-nating challenge in management sys-tems development. The environ-ment created will be in sharp con-trast with business environments ofthe past, and that change char-acterizes the management revolu-tion.

Conclusions

This discussion began by questioningwhether the current interest in manage-ment systems was a faddish interest, orwas it at the beginning of a managementrevolution —and it could be both. Someof the current interest is undoubtedlyfaddish, and as a consequence theremay be a time of inevitable disenchant-ment with advanced management sys-tems development. Such a reaction maybe only a necessary early stage. Duringthis management revolution, all willhave much to learn —much to under-stand— before we realize and appreciateits benefits.

MANAGEMENT ACCOUNTING /J ANUARY 1969 15

The Nature and Importance ofVariances from Standard Cost

of Production*

TOWARD MORE CLEARLY DEFINED EXPRESSIONS OF WHAT MAKES A VARIANCE SIGNIFICANT

By Oswald Nielsen

Generally, it is assumed that analysisand treatment of variance is singularlyimportant in the operation of a stand-ard cost accounting system. It is furtherpresupposed that large variances mustbe recognized by some special processof analysis, proration, or presentation.Contrarily, small variances may be ig-nored because of the insignificant resultsto be expected from such treatment.

Whatever their merits, these assump-tions and procedures are based uponsuperficial considerations of the magni-tude of the variance figure itself. It isthe purpose here to explore the natureof such suppositions and appraise theirvalidity.

Recognizing that cost variances maybe either qualitative or quantitative, thisdiscussion will be concentrated on thequantitative factors, specifically address-ing itself to quantitative significance.First, those that are significantly in ex-cess of standard (unfavorable) will becovered. Those that are significantlyless than standard ( favorable) will betreated only incidentally here.'

I David H. Li makes a clear statement of the con-cept of favorable and unfavorable variances in hisAccou nt ing for Ma n ag emen t An a lys i s , Charles E.Merrill, Inc., Columbus, Ohio, 1964, p. 293.

The author is indebted to the firm of Webb &Webb, certified public accountants, for financialsupport to make this study possible. He also ac-knowledges valuable assistance from Barbara Man-chester Vendelin and Charles T. Horngren.

16

Quantitative vs. QualitativeAspects

In distributing "quantitative" and"qualitative" variances it may be helpfulto indicate the sense in which theseterms are used here. Quantitatively, avariance is presumed to be expressed asa certain number of dollars and cents(although it could just as well be statedin non - monetary quantities), regardlessof what the cause of the variance maybe. The qualitative significance of vari-ance is presumed to be associated with(a) those characteristics which havegiven rise to it or (b) the nature of the

OSWALD NIELSENSan Francisco Chapter (Minneapolis1944), Professor of Accounting, Stan-ford University, Graduate School ofBusiness, Stanford, Calif. ProfessorNielsen, a CPA, received a Ph.B. de-gree from the University of Chicagoand a Ph.D. degree from the Univer-sity of Minnesota.

impact of the variance on the operationto which it pertains.

Frequently the quantitative signifi-cance of variance is the one that receivesbasic treatment, while the qualitativesignificance of it often is ignored. Thefollowing discussion relates to the sig-nificance of variance, first from thequantitative aspect and then with anappraisal of the qualitative significanceof variance.

The treatment of quantities of vari-ance has its impact on the preparationof the traditional financial statements(whether distributed internally or ex-ternally) and on such other external re-porting as is done for income tax pur-poses. In outside reporting and state-ment presentation, the treatment ofvariance essentially involves overall con-siderations, in contrast to the segmentedtreatment required for internal controlpurposes. Any examination into thecomponents of a variance may disclosedetailed significance, even though theoverall total of variances is not neces-sarily significant. Conversely, an aggre-gation of small variances, insignificantindividually, may be significant. Hence,the managerial implications of the vari-ance and its treatment may be some-what different from what it would befrom the standpoint of overall reporting.

From the standpoint of overall state-ment presentation it is only if a variance

MANAGEMENT ACCOUNTING /JANUARY 1969

is significant quantitatively that it gainspractical significance qualitatively. Inthis sense, qualitative significance at-taches largely to the problem of whatmay be done about the variance, evento the extent of indicating the locus oforganizational responsibility for it. Theremay be qualitative significance to quan-titative small variances, such as "for theprinciple of the thing," which might ap-ply if there are moral or ethical consider-ations at issue. Any qualitative consider-ations will be limited to those aspectsthat rest with management, assumingthat there will be no idealistic qualitiesat stake.

Literature on the Subject

In the literature on variance analysisit is preponderantly assumed that onlya large variance ought to be scrutinized.This approach, thought of as an appli-cation of the "principle of exceptions"in cost control, implies that a small vari-ance does not deserve managerial consid-eration. It is for this alleged reason ofinsignificance that small variances mightwell be disposed of by direct charges tocost of sold goods, and thus allocated tothe period of incurrence. In this respect,variance is considered to be large orsmall in relation to the standard costfrom which it varies.

Some writers are disposed to handlevariances on the basis of whether theyare above or below standard costs. Intypifying this group, Clinton W. Ben -nett2 suggests that all variances of actualover standard cost might well be addedto cost of goods sold in the period inwhich they occur but that variances ofactual under standard should be appor-tioned between cost of goods sold andinventory. This essentially conservativeattitude ascribes to the process of valua-tion of inventory those figures that willreduce its value. Bennett relates this ar-gument to his discussion of the valua-tion of inventories at the lower of costor market. Obviously, this viewpoint em-phasizes the qualitative nature of thevariance, its directional quality ratherthan its absolute or relative magnitude.

Another approach involves treatmentof variance according to whether thereis external or internal responsibility forit. This treatment, as described by JohnC. Blocker,3 suggests that any variance

o Wyman P. Fiske and John A. Beckett, Editors,Industrial Accountants Handbook, Prentice -Hall,Inc., New York, 1954, p. 339.

John G. Blocker, "Mismatching of Costs andRevenues," The Accounting Review, January 1949,pp. 33.43.

of actual labor or overhead costs fromstandard might appropriately be chargedto cost of goods sold on the theory thatthe firm itself has responsibility for themagnitude of these supposedly internalcosts. This theory further assumes thatprice variances of materials result fromexternal forces operative in the marketand consequently justify the distributionof variance between cost of goods soldand inventory. These arguments are de-fective according to Blocker in that theydo not provide a logical basis for distinc-tion between variances properly charge-able to current periods and those whichmust be apportioned to future periodsthrough inclusion in the inventory valu-ation. If there is a flaw in the reasoningbehind this viewpoint, it stems fromfailure to distinguish clearly betweenforces which are external to the businessand those which emanate from withinthe business itself. It appears to evademany questions on the responsibility forprice, wage rate, quantity, efficiency, andgeneral overhead variances, such as ca-pacity and budget variances which maystem from complex forces.

The arguments just cited are inquiriesinto the responsibility for variances andin that respect have merit. But theirmerit does not extend to a determina-tion of the treatment of variance accord-ing to its significance in modern man-agement and reporting.

Although he looks upon variance asthe "prime product of standard costs,"William W. Voorhees4 reasons (in1950) to the effect that variances needto be expressed in both percentages andabsolute numbers because one may belarge while the other may not necessarilybe so. Outside of this realization, hegives no indication of the characteristicsof a variance which make it worthy orunworthy of consideration.

Shillinglaw5 summarizes the way inwhich variances might be disposed of ina three -part set of alternatives:1. to pro -rate variances between sold

and remaining inventory, presum-ably on the basis of the sale, (He in-dicates the result in this case to bethe same as if all cost analyses weredone after all information for theperiod under review had been avail-able at the time of the disposition ofthe variance.)

4 Lillian Doris, Editor, Corporate Treasurer's andController's Handbook, Prentice -Hall, Inc., NewJersey, 1950, pp. 198 -199.G Gordon Shillinglaw, Cost Accountingo; Analysisand Control, revised edition, Richard D. IrwinInc., Homewood, Ill., 1967, pp. 533.36.

2. to allocate variances to the periodof its occurrence, and

3. to carry period variances forward tobe offset by variances in opposite di-rections in subsequent periods.

These references to current literaturesuggest that much remains to be donetoward formulating more clearly definedexpressions of what makes a variancesignificant in modern reporting andanalysis. The following discussion en-compasses some of the factors whichbear upon the importance of variancein analysis and reporting.

Variance and Cost of Goods Sold

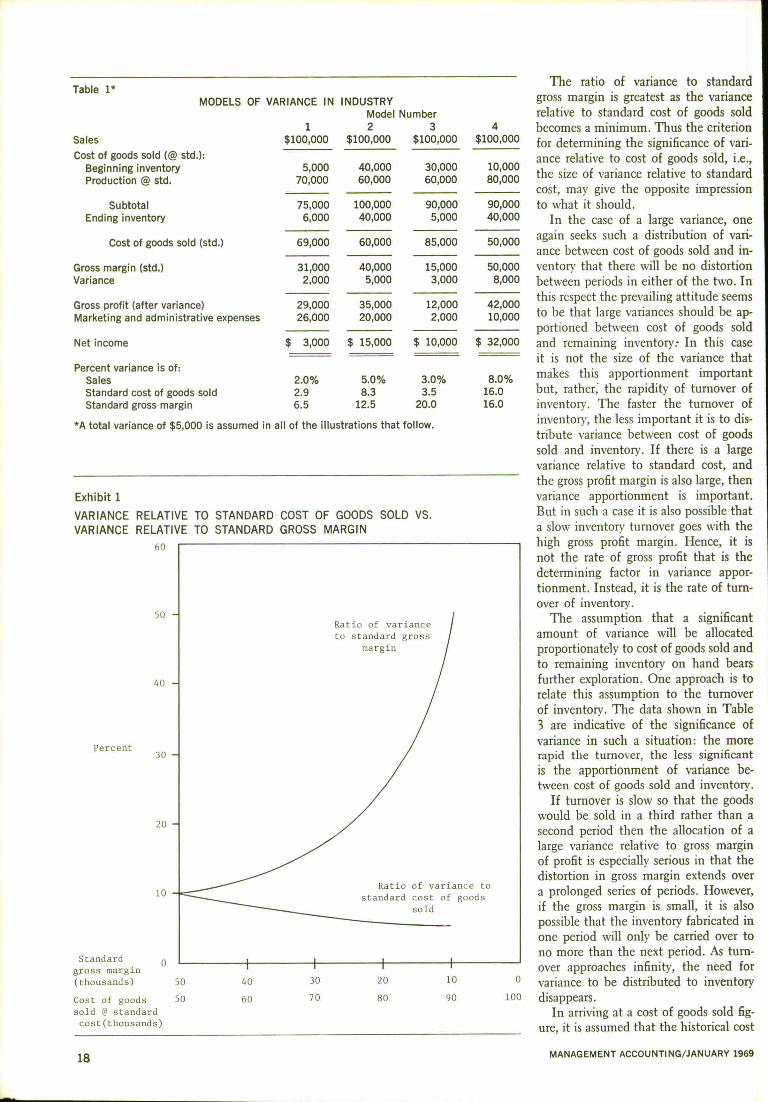

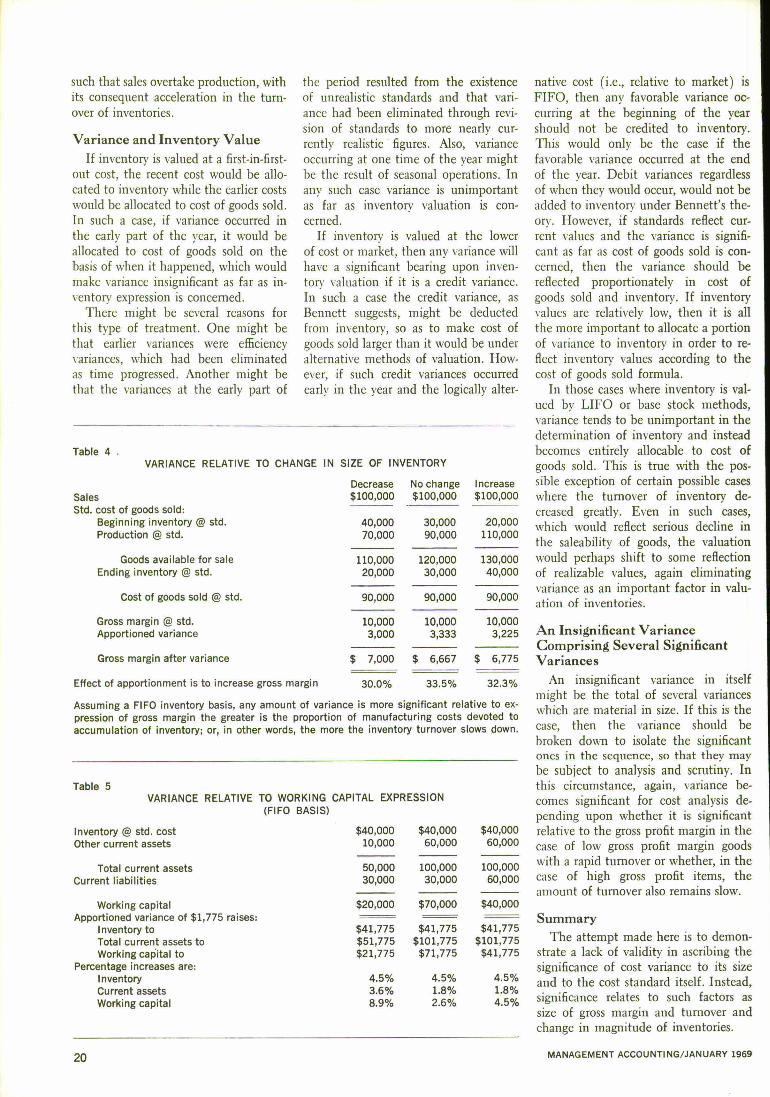

The importance of the disposal ofvariance as far as cost of goods sold isconcerned, is that of making propertemporal determination of cost of goodssold. The assumption that a small vari-ance relative to standard cost of manu-facture can be added to cost of goodssold for the year of occurrence withoutany distortion of net income from oneyear to another is probably true if thevariance is a small one relative to grossmargin as well. This is not true if thegoods enter into the market at a smallmargin of gross profit, for in such a casethe variance, although small relative tothe cost of goods sold, is large relativeto the margin of profit. In such a case,the factor which determines whetherthe variance is significant enough to beapportioned between cost of goods soldand inventory is the size of the variancerelative to the margin of gross profitrealizable on the production and sale ofthe goods and not on the size of thevariance relative to the standard cost ofproductions Table 1 suggests this.

A similar situation is shown in Exhibit1 and Table 2. It will be noticed herethat the ratio of a given amount of vari-ance to standard cost of goods sold isrelatively small, whereas the same vari-ance bears a ratio to standard gross mar-gin that increases at a rapidly accelerat-ing rate as the gross margin decreases.The variance declines in significancerelative to the standard cost as the latterbecomes a larger proportion of salesprice. As thus viewed, the rate of de-cline is slow. Conversely, that same vari-ance increases in significance relative tothe standard gross margin as it declinesrelative to sales price. It aproaches infin-ity as the percent of gross margin ap-proaches zero.

I The same approach has been taken concerning de.preciation. Although it might be insignificant rela-tive to sales it may be large relative to net income.

MANAGEMENT ACCOUNTING /J ANUARY 1969 17

Table 1*MODELS OF VARIANCE IN INDUSTRY

Model Number1 2 3 4

Sales $100,000 $100,000 $100,000 $100,000

Cost of goods sold (@ std.):Beginning inventory 5,000 40,000Production @ std. 70,000 60,000

Subtotal 75,000 100,000

Ending inventory 6,000 40,000

Cost of goods sold (std.) 69,000 60,000

Gross margin (std.) 31,000 40,000Variance 2,000 5,000

Gross profit (after variance) 29,000 35,000Marketing and administrative expenses 26,000 20,000

Net income $ 3,000 $ 15,000

30,000 10,00060,000 80,000

90,000 90,0005,000 40,000

85,000 50,000

15,000 50,0003,000 8,000

12,000 42,0002,000 10,000

$ 10,000 $ 32,000

Percent variance is of:Sales 2.0% 5.0% 3.0% 8.0%

Standard cost of goods sold 2.9 8.3 3.5 16.0

Standard gross margin 6.5 12.5 20.0 16.0

*A total variance of $5,000 is assumed in all of the illustrations that follow.

Exhibit 1VARIANCE RELATIVE TO STANDARD COST OF GOODS SOLD VS.VARIANCE RELATIVE TO STANDARD GROSS MARGIN

60

50

40

Percent30

20

10

Standard 0gross margin(thousands)

Cost of goodssold @ standardcost(thousands)

18

Ratio of varianceto standard gross

margin

Ratio of variance tostandard cost of goods

sold

50 40 30 20 10 0

50 60 70 80 90 100

The ratio of variance to standardgross margin is greatest as the variancerelative to standard cost of goods soldbecomes a minimum. Thus the criterionfor determining the significance of vari-ance relative to cost of goods sold, i.e.,the size of variance relative to standardcost, may give the opposite impressionto what it should.

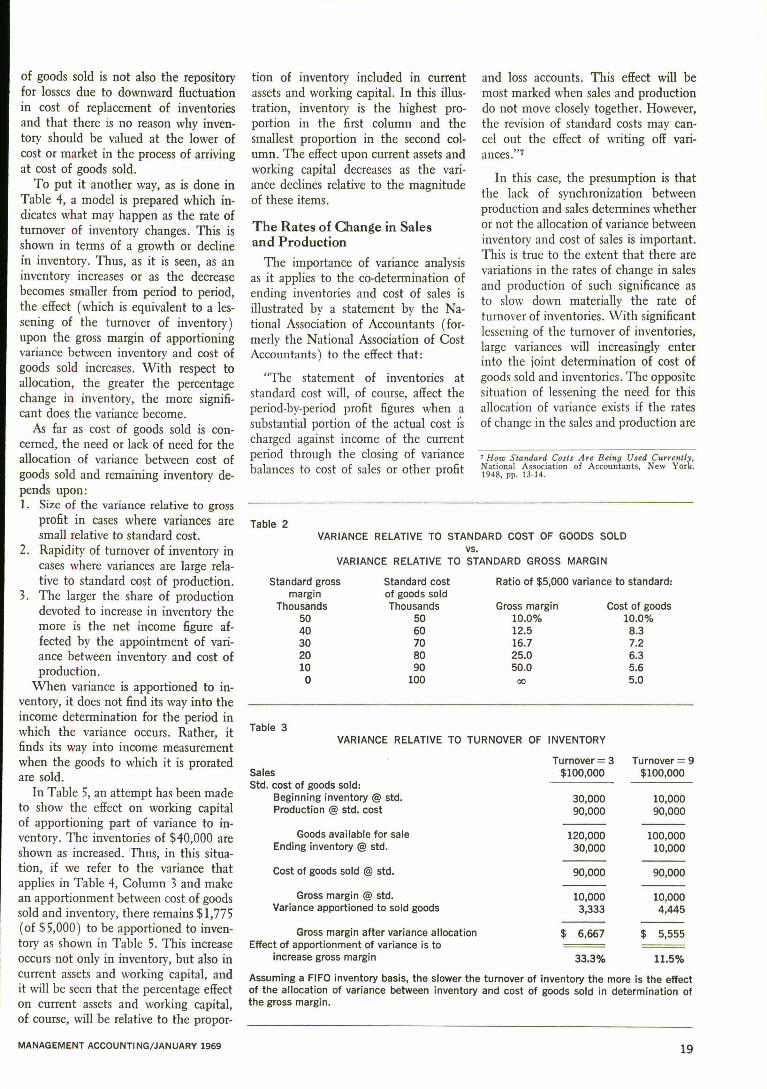

In the case of a large variance, oneagain seeks such a distribution of vari-ance between cost of goods sold and in-ventory that there will be no distortionbetween periods in either of the two. Inthis respect the prevailing attitude seemsto be that large variances should be ap-portioned between cost of goods soldand remaining inventory. In this caseit is not the size of the variance thatmakes this apportionment importantbut, rather; the rapidity of turnover ofinventory. The faster the turnover ofinventory, the less important it is to dis-tribute variance between cost of goodssold and inventory. If there is a largevariance relative to standard cost, andthe gross profit margin is also large, thenvariance apportionment is important.But in such a case it is also possible thata slow inventory turnover goes with thehigh gross profit margin. Hence, it isnot the rate of gross profit that is thedetermining factor in variance appor-tionment. Instead, it is the rate of turn-over of inventory.

The assumption that a significantamount of variance will be allocatedproportionately to cost of goods sold andto remaining inventory on hand bearsfurther exploration. One approach is torelate this assumption to the turnoverof inventory. The data shown in Table3 are indicative of the significance ofvariance in such a situation: the morerapid the turnover, the less significant

is the apportionment of variance be-tween cost of goods sold and inventory.

If turnover is slow so that the goodswould be sold in a third rather than asecond period then the allocation of alarge variance relative to gross marginof profit is especially serious in that thedistortion in gross margin extends overa prolonged series of periods. However,if the gross margin is small, it is alsopossible that the inventory fabricated inone period will only be carried over tono more than the next period. As turn-over approaches infinity, the need forvariance to be distributed to inventorydisappears.

In arriving at a cost of goods sold fig-ure, it is assumed that the historical cost

MANAGEMENT ACCOUNTING /JANUARY 1969

of goods sold is not also the repositoryfor losses due to downward fluctuationin cost of replacement of inventoriesand that there is no reason why inven-tory should be valued at the lower ofcost or market in the process of arrivingat cost of goods sold.

To put it another way, as is done inTable 4, a model is prepared which in-dicates what may happen as the rate ofturnover of inventory changes. This isshown in terms of a growth or declinein inventory. Thus, as it is seen, as aninventory increases or as the decreasebecomes smaller from period to period,the effect (which is equivalent to a les-sening of the turnover of inventory)upon the gross margin of apportioningvariance between inventory and cost ofgoods sold increases. With respect toallocation, the greater the percentagechange in inventory, the more signifi-cant does the variance become.

As far as cost of goods sold is con -cerned, the need or lack of need for theallocation of variance between cost ofgoods sold and remaining inventory de-pends upon:1. Size of the variance relative to gross

profit in cases where variances aresmall relative to standard cost.

2. Rapidity of turnover of inventory incases where variances are large rela-tive to standard cost of production.

3. The larger the share of productiondevoted to increase in inventory themore is the net income figure af-fected by the appointment of vari-ance between inventory and cost ofproduction.