Embed Size (px)

Citation preview

www.ggu.edu

Cost Center, Profit Center, Balance Scorecard

Professor: Ananth Avva, CPA CFA CMA

www.ggu.edu6-2

Performance measurement against: Strategic business Units, Cost Centers, and profit centers

Role of variable costing and full costing in evaluating profit centers

Balanced scorecard in strategic performance measurement

Learning Objectives

www.ggu.edu6-3

Performance Measurement & Control

Performance measurement is the process by which managers at all levels gain information about the performance of tasks within the firm and judge that performance against pre-established criteria as set out in budgets, plans, and goals

• Top management, middle management, and operating-level personnel should be evaluated

Management control refers to the evaluation by upper-level managers of the performance of mid-level managers

www.ggu.edu6-4

Performance Measurement & Control

Operational control means the evaluation of operating-level employees by mid-level managers

Management control focuses on higher-level managers and long-term strategic issues (a broader objective), while operational control focuses on detailed short-term performance

Operational control is a management-by-exception approach while management control is more consistent with the management-by-objectives approach

www.ggu.edu6-5

Performance Measurement & Control

18-5

Managem

ent ControlO

perational Control

Financial

Management

Operations

Management

Marketing

Management

Plant A Plant BRegion BRegion A

Chief Executive

Employee

1

Employee

2

Employee

3

Employee

4

www.ggu.edu6-6

Management by Objectives Areas of responsibility are often called strategic business units

(SBUs)

An SBU consists of a well-defined set of controllable operating activities over which the SBU manager is responsible

Motivate managers to exert a high level of effort to achieve the goals set by top management

Provide the right incentive for managers to make decisions consistent with the goals set by top management (that is, to align managers’ efforts with the desired strategic goals)

Determine fairly the rewards earned by managers for their efforts and skill and the effectiveness of their decision making

www.ggu.edu6-7

Management by Objectives Areas of responsibility are often called strategic business units

(SBUs)

An SBU consists of a well-defined set of controllable operating activities over which the SBU manager is responsible

Motivate managers to exert a high level of effort to achieve the goals set by top management

Provide the right incentive for managers to make decisions consistent with the goals set by top management (that is, to align managers’ efforts with the desired strategic goals)

Determine fairly the rewards earned by managers for their efforts and skill and the effectiveness of their decision making

www.ggu.edu6-8

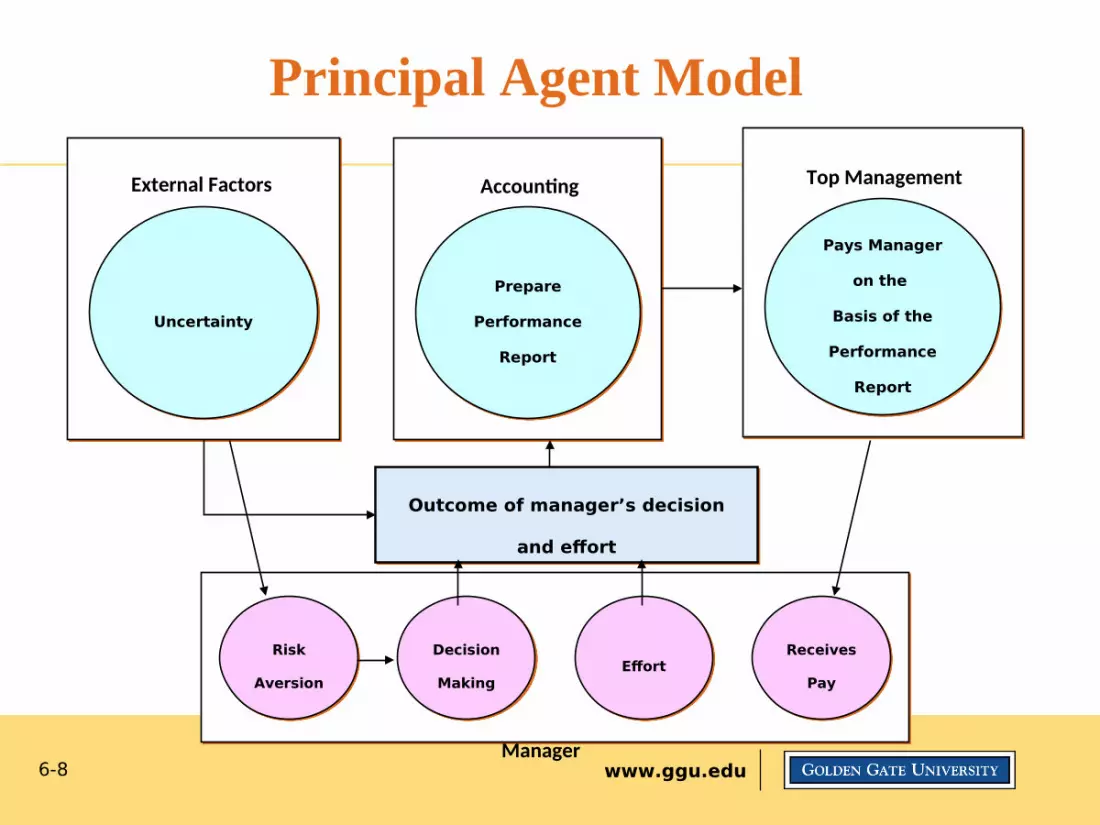

Principal Agent Model

Outcome of manager’s decision

and effort

Risk

Aversion

Decision

MakingEffort

Receives

Pay

Uncertainty

External Factors

Prepare

Performance

Report

Accounting

Pays Manager

on the

Basis of the

Performance

Report

Top Management

Manager

www.ggu.edu6-9

Strategic Performance Management

•Cost Centers are a firm’s production or support departments that are charged with the responsibility of providing the best quality product or service at the lowest cost (examples: a plant’s assembly department, data-processing department, and its shipping and receiving department)

•Revenue Centers focus on the selling function and are defined either by product line or by geographic area

•Profit Centers: when an SBU both generates revenues and incurs the major portion of the cost for producing these revenues, it is considered a profit center

• Investment Centers include assets employed by the SBU as well as profits in the performance evaluation

www.ggu.edu6-10

Strategic Performance Management

The choice of a profit, cost, or revenue center depends on the nature of the production and selling environment in the firm:

• Products that have little need for coordination between the manufacturing and selling functions are good candidates for cost and revenue centers

• For products that require close coordination between these functions, profit centers would be the preferred option

www.ggu.edu6-11

Cost Centers

Direct manufacturing and manufacturing support departments are often evaluated as cost centers since these managers have significant direct control over costs but little control over revenues or decision-making for investment in facilities

Several strategic issues arise when implementing cost centers:

• Cost shifting occurs when a department replaces its controllable costs with noncontrollable costs (e.g., variable costs to fixed costs)

• Budgetary slack can be good as it reduces risk aversion, but too much slack can result in reduced employee effort

www.ggu.edu6-12

Implementation

Discretionary-Cost Approach

Costs are mainly fixed, uncontrollableFirms use an input-oriented planning focusOutputs are ill-definedThe focus is on planning

Engineered-Cost Approach

Costs are mainly variable, controllableFirms use an output-oriented evaluation focusOutputs are well-definedThe focus is on evaluation

www.ggu.edu6-13

G&A Cost Centers

These departments have the same two methods to choose from, but the proper choice may change over time:

–For example, if cost reduction is a key objective, the human resources department might be treated as an engineered-cost center

–Later, it might be changed to a discretionary-cost center to motivate managers to focus on the achievement of long-term goals

www.ggu.edu

G&A Cost Centers

Total Cost

4,800

3,600

2,400

1,200

Cost Driver

(number of applications)

100 200 300 400

Cost Variance

250

Cost behavior in

administrative

support centers

is often a

step cost

Engineered Cost

www.ggu.edu6-15

Implementation Considerations

Many firms are choosing to outsource manufacturing, customer service, engineering, and other services

When using a cost center, how should the firm allocate the jointly incurred costs of service departments to the

departments using the service?

An allocation method should be chosen based on its ability to motivate managers, encourage goal congruence, and

provide a basis for fair evaluation of the managers’ performance

Dual allocation is a cost-allocation method that separates fixed and variable costs; variable costs are

directly traced to user departments, and fixed costs are allocated on some logical basis

Indirect costs should be traced to cost Centers using activity-based costing (ABC)

www.ggu.edu6-16

Revenue Centers

Revenue drivers in manufacturing firms are the factors that affect sales volume,

such as price changes, promotions, discounts, customer service, changes in

product features, delivery dates, and other value-added factors

Revenue drivers in service firms focus on the quality of the service

www.ggu.edu6-17

Marketing Departments

Marketing departments can be either a revenue or a cost Center:

• The revenue center responsibility stems from the fact that the marketing department manages the revenue-generating process and produces revenue reports for evaluation

• This department can also be a cost center as it incurs two types of costs, order-getting (advertising and promotion) and order-filling (warehousing, packing, and shipping) costs

www.ggu.edu6-18

Profit Centers

The profit center manager’s goal is to earn profits

Three strategic issues cause firms to choose profit Centers rather than cost or revenue Centers:

• Profit Centers provide the incentive for the desired coordination among marketing, production, and support functions

• Profit Centers motivate service department managers to consider their product as marketable to outside customers

• Profit Centers motivate managers to develop new ways to earn a profit from their products and services

www.ggu.edu6-19

Strategy Drives Structure

Manufacturing

Plant

Warehouse

Sales

Manufacturing

Plant

Profit

Center

Profit

Center

Sales

Cost Center Revenue Center

Cost Leadership Strategy

Differentiation Strategy

www.ggu.edu6-20

Contribution Income Statement

• A common form of profit center evaluation is the contribution income statement, which is based on the contribution margin

• Contribution by Profit Center (CPC) measures all costs traceable to, and therefore controllable by, the individual profit center, including traceable fixed costs

www.ggu.edu6-21

Controllable & NonControllable FC

• Controllable fixed costs are fixed costs that the profit center manager can influence in approximately a year or less, such as advertising, data processing, and management consulting expenses

• Noncontrollable fixed costs are those that are not controllable within a year’s time, such as depreciation and taxes

www.ggu.edu6-22

Profit Center Measure

Subtracting controllable fixed costs from the contribution margin results in the center’s controllable margin

The contribution margin income statement can also be used to help determine whether a profit center should be dropped or retained

One complication in the preparation of this statement is that some costs that are not traceable at a detailed level are traceable at a higher level

www.ggu.edu6-23

Contribution Margin IS

The Contribution Income Statement shows the CPC for both Divisions is positive, and when Division B is

partitioned into its three product lines, Products 1 and 2 are shown as profitable, while Product 3 has a CPC loss

of $70.

www.ggu.edu6-24

Profit Center Measure

Subtracting controllable fixed costs from the contribution margin results in the center’s controllable margin

The contribution margin income statement can also be used to help determine whether a profit center should be dropped or retained

One complication in the preparation of this statement is that some costs that are not traceable at a detailed level are traceable at a higher level

www.ggu.edu6-25

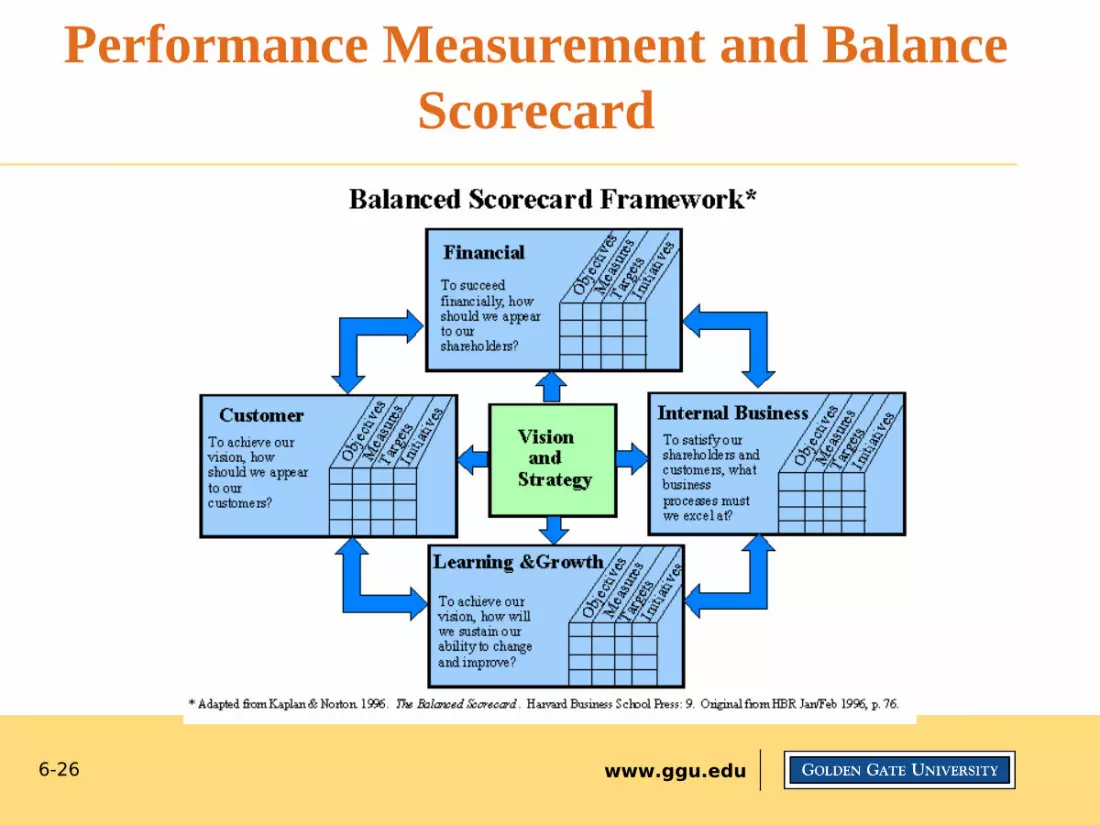

Performance Measurement and Balance Scorecard

The BSC measures SBU performance in four key perspectives:

• Customer satisfaction• Financial performance• Internal business processes• Learning and innovation

Cost, revenue, and profit Centers focus on the financial dimension

www.ggu.edu6-26

Performance Measurement and Balance Scorecard

www.ggu.edu6-27

Performance Measurement and Balance Scorecard

www.ggu.edu6-28

Performance Measurement and Balance Scorecard

So why doesn’t everyone do this?- Measurement challenges- Alignment challenges- Short-sighted- Doesn’t quiet explain how?