Embed Size (px)

Citation preview

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

Subject BUSINESS ECONOMICS

Paper No and Title 4: Principles of Business Finance and Accounting

Module No and Title 29: Cash Credit Systems

Module Tag BSE_P4_M29

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

TABLE OF CONTENTS

1. Learning Outcome

2. Introduction

3. What is Cash Credit System?

4. Features of Cash Credit system

5. Drawbacks of cash Credit system

6. Credit Limit

7. Security of Cash Credit Account

8. Interest on Cash Credit Account

9. Drawing Power

10. Difference between Cash Credit and Bank Overdraft

11. Regulation of Bank Finance: A historical Perspective

12. Summary

13. References

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

1. Learning Outcomes

After going through this module you will be able to learn about the:

Learn cash credit systems, its features and its drawbacks.

Learn about credit limit, security and interest charged on cash credit account.

Learn about drawing power and its calculation.

Learn about the difference between cash credit and overdraft.

Learn about the historical perspective of regulations of bank finance.

2. Introduction

Banks finance has been always the most preferred source of working capital requirements.

Overdraft, bills discounting and working capital loan, and cash credits are the various forms of

working capital finance. Working capital needs of any firm are determined as per the norms. These

norms are based on the recommendations of Tandon Committee (1974) and Chore Committee

(1979).

3. What is Cash Credit System?

A cash credit facility provides short term loan to a corporate house. Cash credit is a loan account

which helps the corporate to arrange working capital requirements. Cash credit is a flexible lending

system which allows the borrower to withdraw the funds as per his requirements. Bank stipulates

the cash credit limit for the customer. Customer can withdraw money up to this credit limit. Cash

credit account is a running account (i.e. payable on demand) with cheque book facility, just like

current account.

Excess of total current assets over total current liabilities is known as Net Working Capital of a

firm. Operating cycle of a firm determines its working capital requirement. Operating cycle is a

time gap between procurement of raw materials and realization of sales into cash. The requirement

of fund depends upon the length of operating cycle. Larger the operating period, larger will be the

requirement of funds. Cash credit account supports the smooth functioning of working capital cycle

by providing the sufficient funds at the time of need. As per the working capital requirement bank

decides the credit limit of the customer.

4. Features of Cash Credit Systems

Features of cash credit system which makes it highly acceptable by the customers are as follows:

1. Cash credit account is a very flexible account. Borrower can draw upon his cash credit

account number of times as and when need arises. There is no stipulation on the number of

transaction. Transaction should not cross the “drawing limit” of the borrower.

2. Borrower can repay frequently in cash credit account, when he is having surplus money.

3. Interest is paid on the total amount of credit utilized by the borrower and not on the total

credit limit approved.

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

4. Technically, cash credit is a short term loan secured by the current asset, such as inventory

and receivables. This loan is repayable on demand. But in practice, cash credit acts as a

continuous borrowing account, which is renewed annually or half yearly depending upon

the performance of the borrower.

5. Drawbacks of Cash Credit Systems

Apart from the above desirable features for the borrower, cash credit system has certain drawback

from the point of view of banks. The drawbacks are as follows:

1. At any particular time, bank has no control over the actual level of cash credit advances.

Bank can only control the total amount of cash credit limits. Borrowers decide the actual

utilization of these credit limits.

2. Whenever borrower is having surplus cash he can credit this surplus cash to his cash credit

account. This reduces the outstanding balance in the cash credit account and save the

borrower from paying interest cost to the bank and ultimately reducing bank’s interest

income.

3. The credit limit was fixed on the basis of security available in the account, sometimes it

created the problem of double finance.

4. Most of the times banks oversell the credit, because a major portion of credit limits

authorized by banks remained unutilized.

5. The operating mechanism of cash credit system makes a challenging task for the banks to

have effective control over the end-usage of the credit. If a borrower maintains a certain

level of inventory and receivables, then his cash credit account will be fairly active. In this

situation bank cannot demand the customer to repay the loan, and customer uses the credit

allowed to him as a permanent source of finance.

6. Cash Credit system favors established and big borrowers, as they tend to hold big level of

inventories hence their credit limit is also high. This leaves very small room for giving

credit to small and new borrowers.

6. Credit Limit

Credit limit is the maximum amount that borrower can draw from his cash credit account. If the

value of stock is high, even then also borrower is allowed to withdraw only up to his sanctioned

credit limit.

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

7. Security of Cash Credit Account

There are two ways under which securities can be held by the bank. These are:

1. Pledge: Under pledge the possession of goods is with the bank. Bank links the drawings

in the account with the actual movement of goods from and to the possession with the bank.

In case borrower fails to pay the borrowed amount, bank can recover the money by selling

the goods pledged.

2. Hypothecation: Under hypothecation goods are in the possession of borrower and bank

creates a floating charge on the goods. An agreement binds the borrower to give possession

of goods to the bank, whenever bank requires the borrower to do so. Borrower has to submit

monthly statements of stock, receivables etc. Drawings from the cash credit account are

based on the stock statements submitted by borrower.

8. Interest on Cash Credit Account

Interest on cash credit account is charged every month. Interest is charged on the amount withdrawn

by the borrower and not on the total credit limit. Borrower transacts many entries of debit and credit

everyday through cash credit account. Interest calculation is never a problem. Even with many

transactions, only day end balance is charged for interest. Computerization of banks has made this

task even much easier.

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

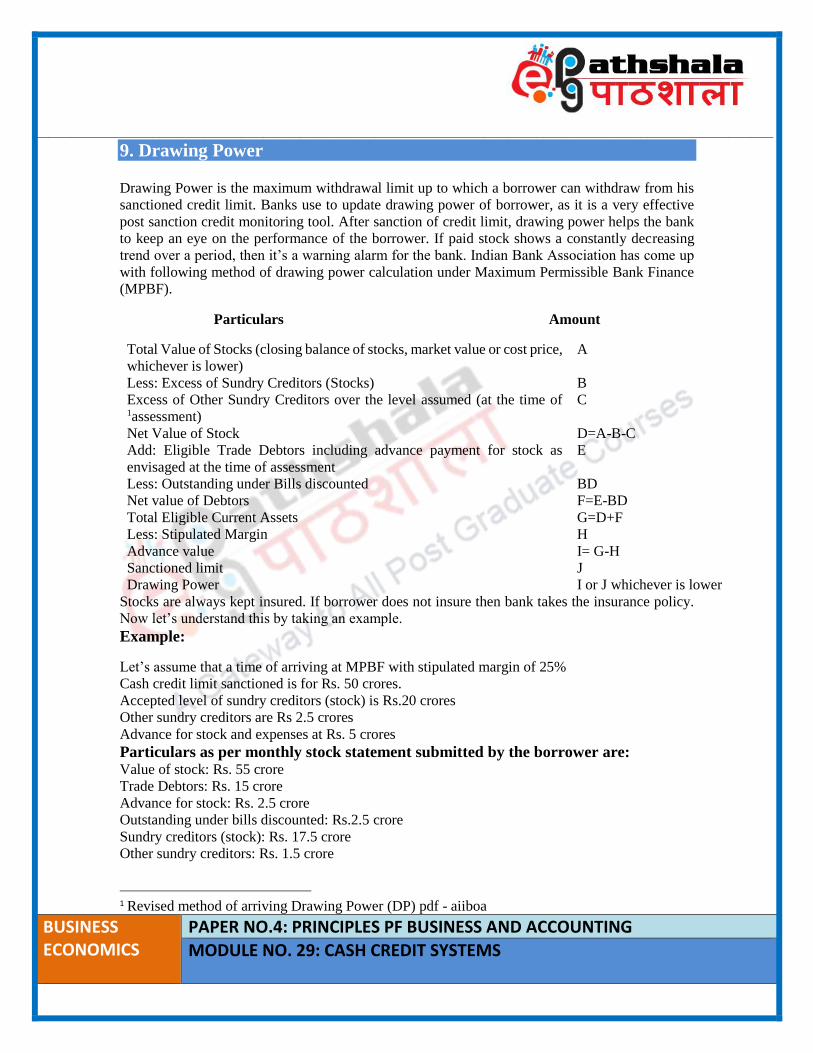

9. Drawing Power

Drawing Power is the maximum withdrawal limit up to which a borrower can withdraw from his

sanctioned credit limit. Banks use to update drawing power of borrower, as it is a very effective

post sanction credit monitoring tool. After sanction of credit limit, drawing power helps the bank

to keep an eye on the performance of the borrower. If paid stock shows a constantly decreasing

trend over a period, then it’s a warning alarm for the bank. Indian Bank Association has come up

with following method of drawing power calculation under Maximum Permissible Bank Finance

(MPBF).

Particulars Amount

Total Value of Stocks (closing balance of stocks, market value or cost price,

whichever is lower)

A

Less: Excess of Sundry Creditors (Stocks)

Excess of Other Sundry Creditors over the level assumed (at the time of 1assessment)

B

C

Net Value of Stock D=A-B-C

Add: Eligible Trade Debtors including advance payment for stock as

envisaged at the time of assessment

E

Less: Outstanding under Bills discounted BD

Net value of Debtors F=E-BD

Total Eligible Current Assets G=D+F

Less: Stipulated Margin H

Advance value I= G-H

Sanctioned limit J

Drawing Power I or J whichever is lower

Stocks are always kept insured. If borrower does not insure then bank takes the insurance policy.

Now let’s understand this by taking an example.

Example:

Let’s assume that a time of arriving at MPBF with stipulated margin of 25%

Cash credit limit sanctioned is for Rs. 50 crores.

Accepted level of sundry creditors (stock) is Rs.20 crores

Other sundry creditors are Rs 2.5 crores

Advance for stock and expenses at Rs. 5 crores

Particulars as per monthly stock statement submitted by the borrower are: Value of stock: Rs. 55 crore

Trade Debtors: Rs. 15 crore

Advance for stock: Rs. 2.5 crore

Outstanding under bills discounted: Rs.2.5 crore

Sundry creditors (stock): Rs. 17.5 crore

Other sundry creditors: Rs. 1.5 crore

1 Revised method of arriving Drawing Power (DP) pdf - aiiboa

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

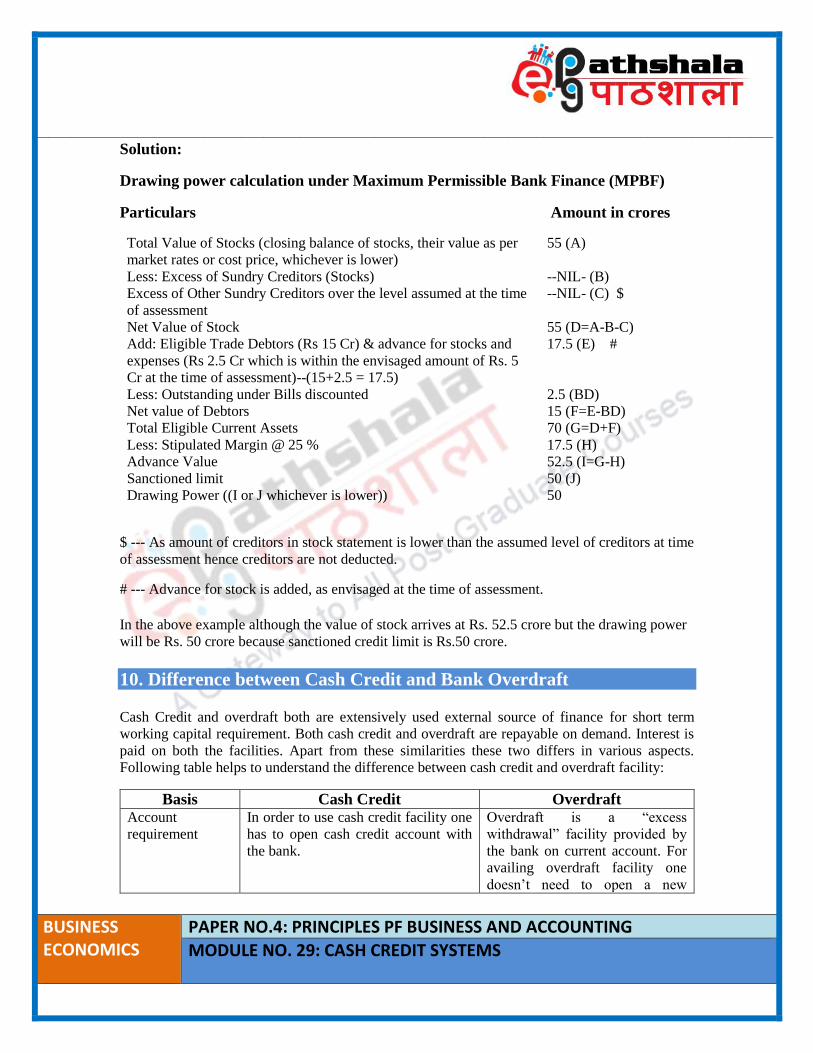

Solution:

Drawing power calculation under Maximum Permissible Bank Finance (MPBF)

Particulars Amount in crores

Total Value of Stocks (closing balance of stocks, their value as per

market rates or cost price, whichever is lower)

55 (A)

Less: Excess of Sundry Creditors (Stocks)

Excess of Other Sundry Creditors over the level assumed at the time

of assessment

--NIL- (B)

--NIL- (C) $

Net Value of Stock 55 (D=A-B-C)

Add: Eligible Trade Debtors (Rs 15 Cr) & advance for stocks and

expenses (Rs 2.5 Cr which is within the envisaged amount of Rs. 5

Cr at the time of assessment)--(15+2.5 = 17.5)

17.5 (E) #

Less: Outstanding under Bills discounted 2.5 (BD)

Net value of Debtors 15 (F=E-BD)

Total Eligible Current Assets 70 (G=D+F)

Less: Stipulated Margin @ 25 % 17.5 (H)

Advance Value 52.5 (I=G-H)

Sanctioned limit 50 (J)

Drawing Power ((I or J whichever is lower)) 50

$ --- As amount of creditors in stock statement is lower than the assumed level of creditors at time

of assessment hence creditors are not deducted.

# --- Advance for stock is added, as envisaged at the time of assessment.

In the above example although the value of stock arrives at Rs. 52.5 crore but the drawing power

will be Rs. 50 crore because sanctioned credit limit is Rs.50 crore.

10. Difference between Cash Credit and Bank Overdraft

Cash Credit and overdraft both are extensively used external source of finance for short term

working capital requirement. Both cash credit and overdraft are repayable on demand. Interest is

paid on both the facilities. Apart from these similarities these two differs in various aspects.

Following table helps to understand the difference between cash credit and overdraft facility:

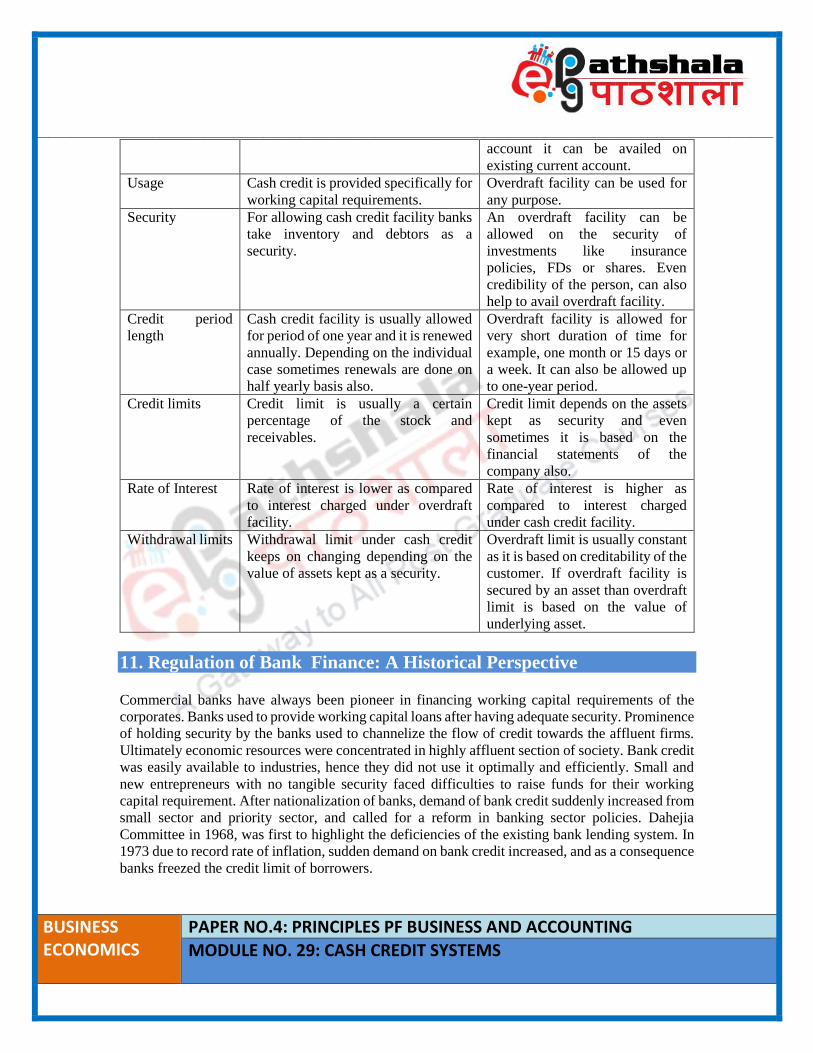

Basis Cash Credit Overdraft Account

requirement

In order to use cash credit facility one

has to open cash credit account with

the bank.

Overdraft is a “excess

withdrawal” facility provided by

the bank on current account. For

availing overdraft facility one

doesn’t need to open a new

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

account it can be availed on

existing current account.

Usage Cash credit is provided specifically for

working capital requirements.

Overdraft facility can be used for

any purpose.

Security For allowing cash credit facility banks

take inventory and debtors as a

security.

An overdraft facility can be

allowed on the security of

investments like insurance

policies, FDs or shares. Even

credibility of the person, can also

help to avail overdraft facility.

Credit period

length

Cash credit facility is usually allowed

for period of one year and it is renewed

annually. Depending on the individual

case sometimes renewals are done on

half yearly basis also.

Overdraft facility is allowed for

very short duration of time for

example, one month or 15 days or

a week. It can also be allowed up

to one-year period.

Credit limits Credit limit is usually a certain

percentage of the stock and

receivables.

Credit limit depends on the assets

kept as security and even

sometimes it is based on the

financial statements of the

company also.

Rate of Interest Rate of interest is lower as compared

to interest charged under overdraft

facility.

Rate of interest is higher as

compared to interest charged

under cash credit facility.

Withdrawal limits Withdrawal limit under cash credit

keeps on changing depending on the

value of assets kept as a security.

Overdraft limit is usually constant

as it is based on creditability of the

customer. If overdraft facility is

secured by an asset than overdraft

limit is based on the value of

underlying asset.

11. Regulation of Bank Finance: A Historical Perspective

Commercial banks have always been pioneer in financing working capital requirements of the

corporates. Banks used to provide working capital loans after having adequate security. Prominence

of holding security by the banks used to channelize the flow of credit towards the affluent firms.

Ultimately economic resources were concentrated in highly affluent section of society. Bank credit

was easily available to industries, hence they did not use it optimally and efficiently. Small and

new entrepreneurs with no tangible security faced difficulties to raise funds for their working

capital requirement. After nationalization of banks, demand of bank credit suddenly increased from

small sector and priority sector, and called for a reform in banking sector policies. Dahejia

Committee in 1968, was first to highlight the deficiencies of the existing bank lending system. In

1973 due to record rate of inflation, sudden demand on bank credit increased, and as a consequence

banks freezed the credit limit of borrowers.

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

Tandon Committee: In July 1974, Reserve Bank of India constituted a committee with Shri

Prakash Tandon as chairman to frame necessary guidelines on bank credit. Tandon committee

recommended the following notions: 2

1. Operating Plan: Committee recommended that every borrower should draw up an

operating plan for the whole year and provide this plan to the bank. This will help the bank

to estimate the borrower’s credit requirement in the coming year. This will enable bank to

perform credit planning process more efficiently.

2. Production based financing: Banks should make their financing production based. It

simply means that banks should finance only borrower’s genuine production needs.

Borrower should try to maintain a reasonably good level of stock and receivables and

manage them efficiently. Flabby inventories should be avoided. Flabby inventories consist

of raw materials, finished goods and other stores held due to faulty distribution and poor

working capital management.

3. Partial bank Finance: Banks will provide only reasonable part of working capital and

remaining working capital will be arranged by the borrower internally or externally.

4. Receivables norms: Receivables which are in tune with the firm and industry practices

should be financed by the banker.

5. Information System: There must be an information flow from borrower to the bank.

Information flow will serve both, operational purpose as well as supervision purpose of

follow up credit. Information should be provided by giving operating statements, quarterly

budget and funds flow statements. Annual projected figures help in genuine credit appraisal

and quarterly figures when submitted continuously helps the bank in regular follow up of

the credit.

These norms tried to bring uniformity among the banks in financing the working capital

requirement. Tandon committee suggested norms for 15 industries, highly seasonal industries like

sugar and heavy industries were not included in it. These norms were applied uniformly to all

industrial borrowers, even including small scale industries. Norm suggested by the Tandon

committee represented the maximum limit of credit, which any bank should not cross in any

circumstances. Committee allowed deviations only in circumstances like, power cuts, transport

delays and strikes etc. and these deviations were allowed only for short period of time. And as soon

as conditions are back to normal, once again norms should be followed.

Lending norms: Committee also recommended the lending norms for banks. According to these

norms firstly, every borrower should maintain a reasonable level of current asset secondly, a part

of working capital requirement must be financed from long term funds consisting of owners fund

and term borrowings.

Maximum Permissible Bank Finance (MPBF): Following three methods of determining the

permissible level of bank borrowing were suggested by the Tandon committee:

2 Pandey, I. M. (2006) 6th edition, Financial Management, Working Capital Finance, Chapter 31.

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

1. First method: Under this first method bank finances 75 percent, and borrower contributes

25 percent of working capital gap. Current asset minus current liabilities excluding

borrowings from bank is known as working capital gap. This method gives a minimum

current ratio of 1:1.

2. Second Method: Under this method borrower should finance 25 percent of all current

assets from owned funds and long-term liabilities and balance is financed by bank. This

method ensures a current ratio of 1.33:1.

3. Third Method: As per this third method hard core current asset must be financed by the

borrower. Apart from this, borrower should also provide 25 percent of the remaining

current assets and remaining working capital gap is financed by bank.

Tandon committee also suggested that banks should determine new cash credit limit based on

quarterly budgeting and reporting system. Committee also recommended that there should be

difference in interest rates on loans and cash credit account.

Tandon committee report is landmark in banking, it changed the outlook of both the bankers and

the borrowers. Most of the recommendations of Tandon committee were accepted by Reserve Bank

of India, except third method.

The Chore Committee: To review the system of cash credit Reserve Bank of India constituted

a working group in April 1979 under the chairmanship of Mr. K. B. Chore. The term of reference

for the group was:

1) To review the existing cash credit system,

2) Suggest any modifications in the system,

3) Alternative type of credit facilities, which will promote greater credit discipline and this,

will relate credit limits to production activities.

4) To make any further recommendations on any other related issue, if ‘Group’ considers

relevant to the subject.

12. Summary

Cash credit is a flexible lending system which allows the borrower to withdraw the funds

as per his requirements. Cash credit account is a running account (i.e. payable on demand)

with cheque book facility, just like current account.

Cash credit account is a very flexible account. Borrower can draw upon his cash credit

account number of times as and when need arises. Interest is paid on the total amount of

credit utilized. Interest on cash credit account is charged every month. This loan is

repayable on demand.

There are few drawbacks of cash credit system. At any particular time, bank has no control

over the actual level of cash credit advances. The credit limit was fixed on the basis of

security available in the account, sometimes it created the problem of double finance. Most

of the times banks oversell the credit.

____________________________________________________________________________________________________

BUSINESS ECONOMICS

PAPER NO.4: PRINCIPLES PF BUSINESS AND ACCOUNTING

MODULE NO. 29: CASH CREDIT SYSTEMS

Credit limit is the maximum amount that borrower can draw from his cash credit account.

There are two ways under which securities can be held by the bank- pledge and

hypothecation.

Drawing Power is the maximum withdrawal limit up to which a borrower can withdraw

from his sanctioned credit limit. After sanction of credit limit, drawing power helps the

bank to keep an eye on the performance of the borrower.

Cash Credit and overdraft both are extensively used external source of finance for short

term working capital requirement. Both cash credit and overdraft are repayable on demand.

Interest is paid on both the facilities. But still there is lots of difference between the two.

Overdraft is a “excess withdrawal” facility provided by the bank on current account.

After nationalization of banks, demand of bank credit suddenly increased from small sector

and priority sector, and called for a reform in banking sector lending policies. Dahejia

Committee in 1968, was first to highlight the deficiencies of the existing bank lending

system. After this in July 1974, Reserve Bank of India constituted a committee with Shri

Prakash Tandon as chairman to frame necessary guidelines on bank credit. To review the

system of cash credit Reserve Bank of India constituted a working group in April 1979

under the chairmanship of Mr. K. B. Chore.

13. References

http://www.efinancemanagement.com/working-capital-financing/difference-

between-overdraft-and-cash-credit (assessed on 6 Feb 2016)

http://www.yourarticlelibrary.com/banking/cash-credit-system-in-banking-features-

and-drawbacks/40815/ (assessed on 6 Feb 2016)

Revised method of arriving Drawing Power (DP) pdf - aiiboa downloaded from

www.aiiboa.in/promotion/circular/CIR-14-15/ADV_138.pdf on 6 Feb 2016

Pandey, I. M. (2006) 6th edition, Financial Management, Working Capital Finance,

Chapter 31