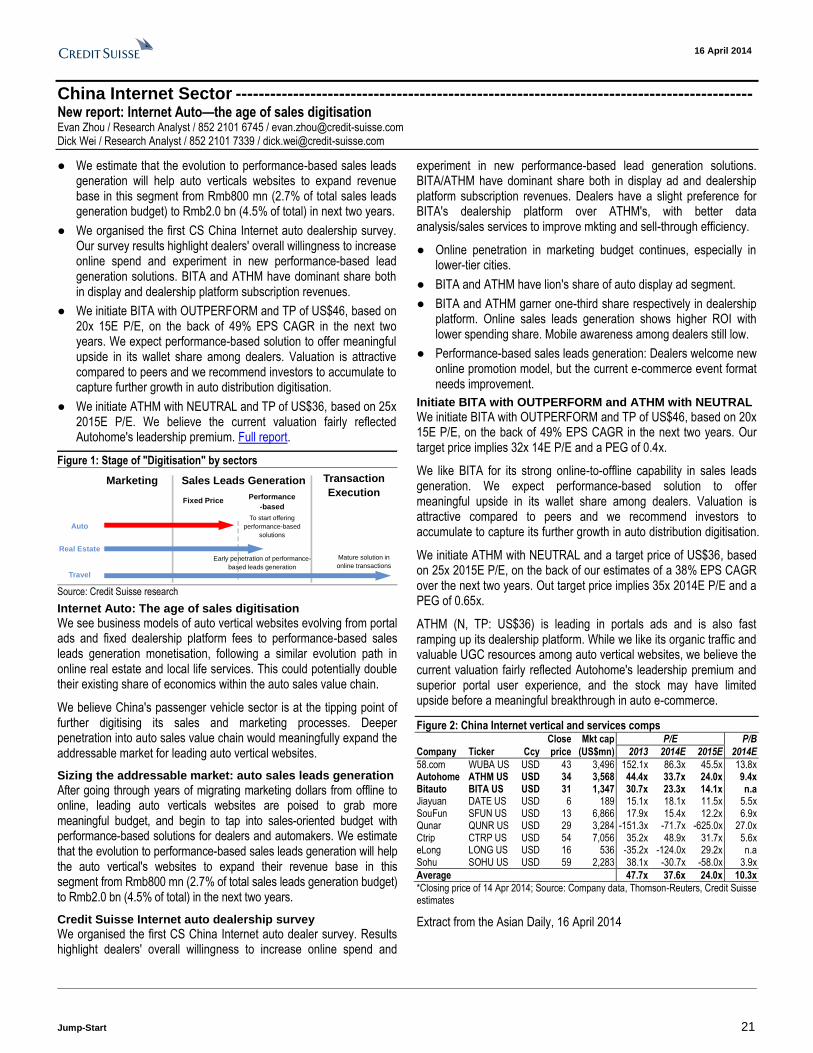

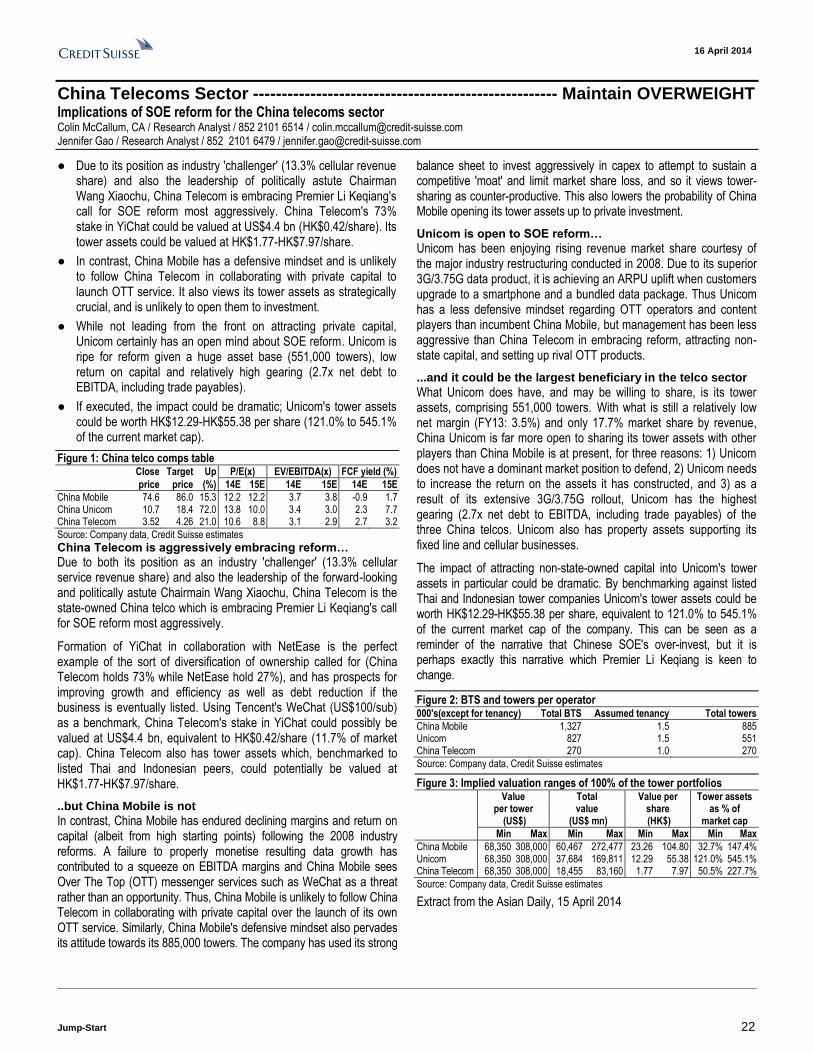

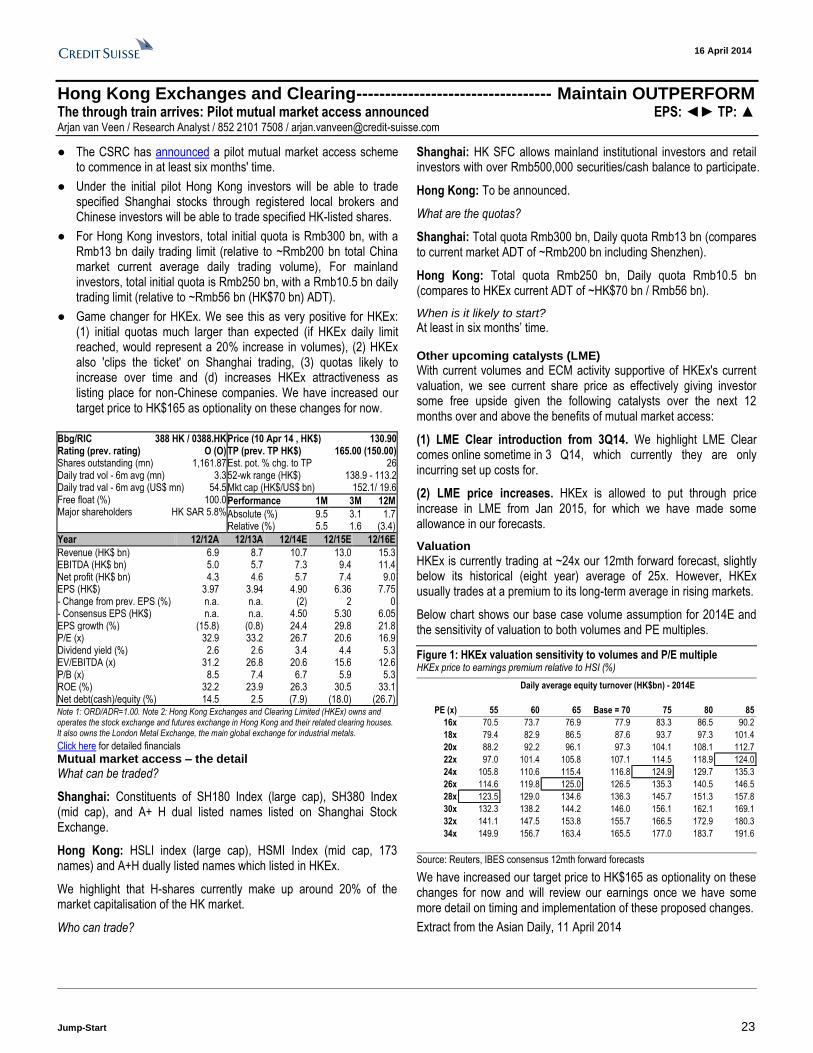

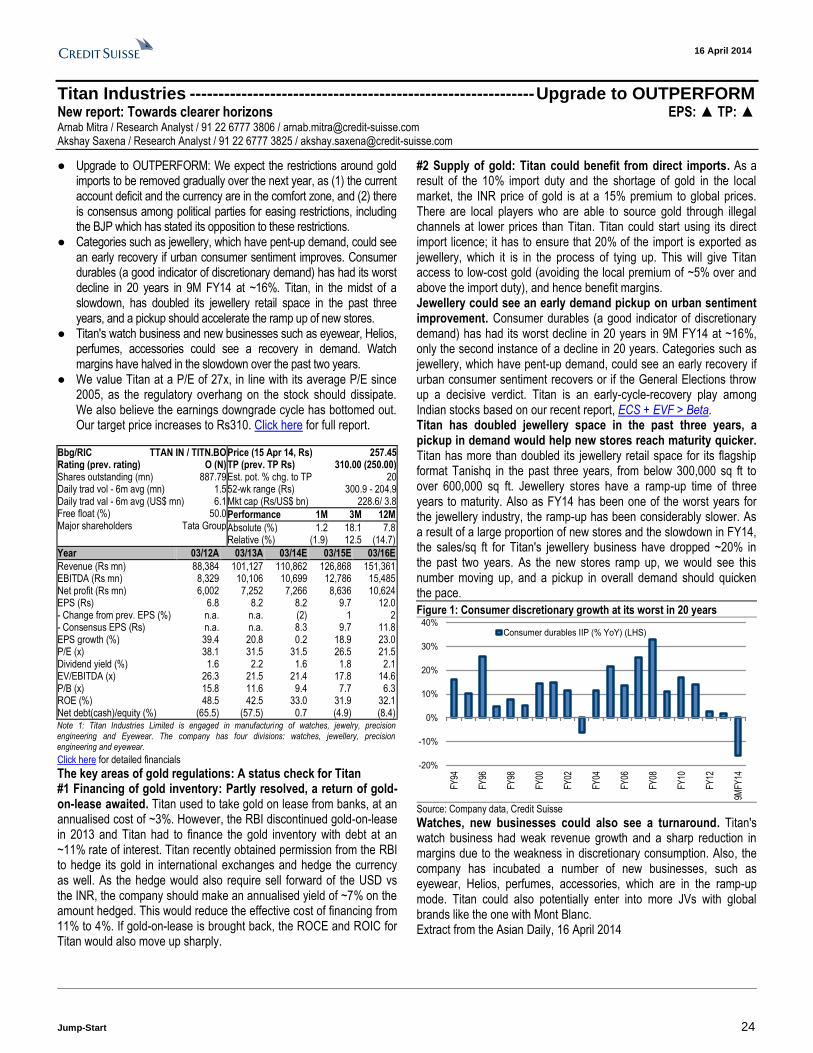

Embed Size (px)

Citation preview

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION™

Client-Driven Solutions, Insights, and Access

16 April 2014

Asia Pacific

Equity Research

Investment Strategy

Jump-Start STRATEGY

Jump-Start aims to provide you with a summary of the week that was and helps you prepare

for the week ahead with a results calendar, economic forecasts and valuation summaries.

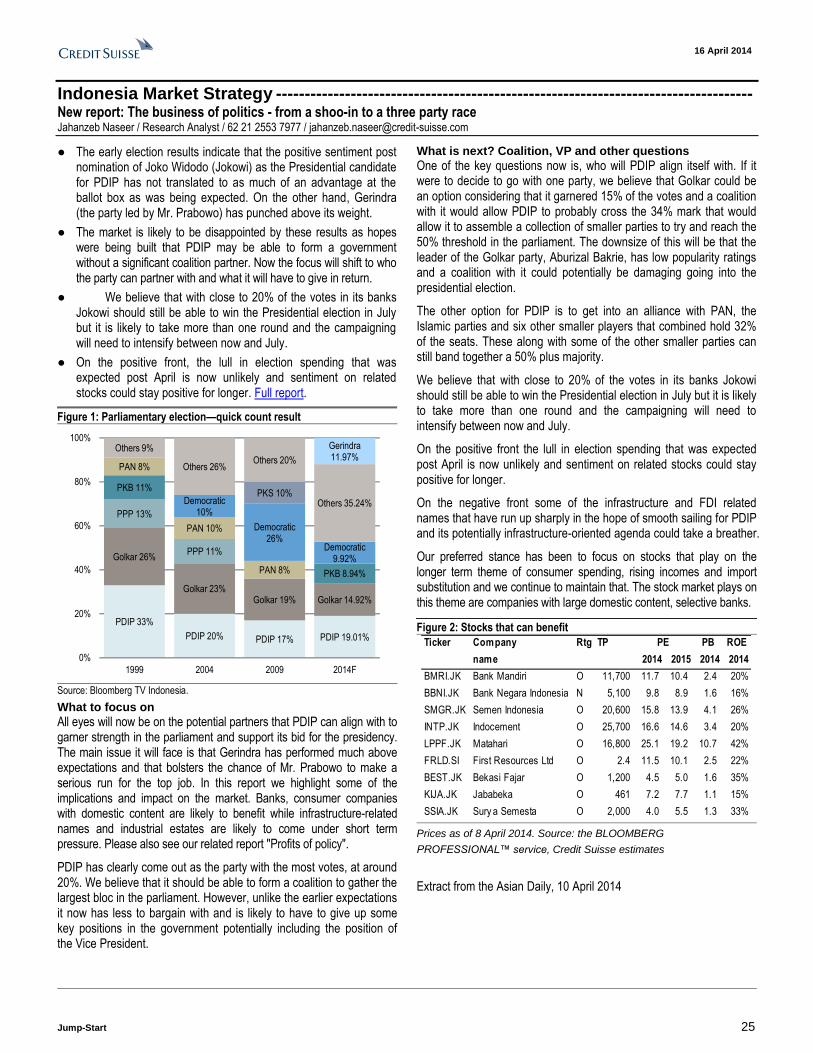

China Market Strategy – SOE : Real or "cut-and-paste" reform? China had undergone a

major round of SOE reform in the late 1990s, with almost 60,000 industrial SOEs closed and

30 mn state workers laid off. Operating efficiency improved significantly, but still lagged the

non-SOEs. Improving operating efficiency through a more diversified ownership is the core

principle of the new SOE reform, write Vincent Chan and team. We evaluated the possible

reform plans of 11 major non-financial listed SOEs, and the banking sector. The possible

telecom (China Telecom & Unicom) sector reforms look most interesting to us. While chance

may not be high, the macro impact of the reform of Chalco and Beijing Enterprise could be the

biggest. (click here)

CS NJA Focus List. We are relaunching the Credit Suisse Asia ex Japan Focus List. These

are 14 of our highest conviction ideas from around the region. The list is not supposed to be a

balanced portfolio, but simply our strongest bottom-up ideas. We intend to limit the stock count

to <20. The final selection of stocks appears to have a quality and a GARP bias. Overall, the

simple average EPS growth on offer for the list is 16%/21% (2014E/15E) with an average P/E

of 14x/11x (2014E/15E) and a simple average ROE of 16.3% for 2014E. Overall, HK/China at

the country level and tech at the sector level constitute a large proportion of the list. The Focus

List will be monitored regularly with changes to the list being made simultaneously with the

change in view on any of the selected stocks, or when we find any new idea compelling

enough for an inclusion to the list. (Click here)

Must-read recently published reports

1) Credit Suisse Asia ex Japan Focus List – Our best ideas (16/4)

Manish Nigam Felix Rusli

These are 14 of our highest conviction ideas from around the region. The list is not supposed to be a balanced portfolio, but simply our strongest bottom-up ideas. While we did not start off with any specific themes in mind, the current Focus List seems to have a quality and a GARP (growth at a reasonable price) bias.

2) China Market Strategy – SOE: Real or 'cut-and-paste' reform?(15/4)

Vincent Chan Improving operating efficiency through a more diversified ownership is the core principle of the new SOE reform. We evaluated the possible reform plans of 11 major non-financial listed SOEs, and the banking sector. The possible telecom (China Telecom & Unicom) sector reforms look most interesting to us.

3) Asia Telecoms Sector – Killer app: OTT voice (13/3)

Colin McCallum OTT threat level rises given the global scale of OTT communities together with the level of stickiness and critical mass OTT apps have created market-by-market. Bundling is the best response.

4) China Power Equipment Sector – Let the wind blow! (3/3)

Edmond Huang We see multi-year investment opportunities in the wind-related business given: (1) resilient demand driven by supportive government policies; (2) alleviated oversupply and improving pricing discipline, and (3) decent profitability recovery.

5) India Steel Sector – Industry-wide high debt hurts discipline (28/2)

Neelkanth Mishra Indian steel companies reach ~5x debt/EBITDA. Market seems unaware of how widespread this is, affecting at least 2/3rd of capacity. Even on forward 12M EBITDA, the ratio is similar despite our current forecasts building in stable EBITDA/t. Debt/EBITDA may rise as competition brings down EBITDA/t.

Research Analyst

Manish Nigam

852 2101 7067

Credit Suisse forthcoming events

Hong Kong / China

China State Construction International Holdings (3311.HK)

Date 29 April, Shenzhen

Analyst Baiding Rong

China Environmental Conference

Date 19-20 May, Hong Kong

Analyst Trina Chen

Singapore

Woori Finance Holdings (053000.KS)

Date 15-17 April, Singapore

Analyst Gil Kim

Sinopac Holdings (2890.TW)

Date 21-24 April, Singapore

Analyst Chung Hsu

Energy Development Corporation (EDC.PS)

Date 28-29 April, Singapore

Analyst Alvin Arogo

Westports Holdings Berhad (WPHB.KL)

Date 05 May, Singapore

Analyst Timothy Ross

Singapore Airlines (SIAL.SI) Post-results

Date 15 May, Singapore

Analyst Timothy Ross

China Property Corporate Day

Date 02 July, Singapore

Analyst Jinsong Du

US

Pacific Basin Shipping Ltd (2343.HK)

Date 12-16 May, US

Analyst Timothy Ross

China Corporate Day in US

Date 24-26 June, US

Analyst Vincent Chan

Others

China Industrial/Auto Conference

Date 2H May

15th Annual Asian Technology Conference

Date 10-12 September, Taipei

Analyst Manish Nigam

Contact [email protected] or your usual sales representative

16 A

pril 2

014

Ju

mp

-Sta

rt 2

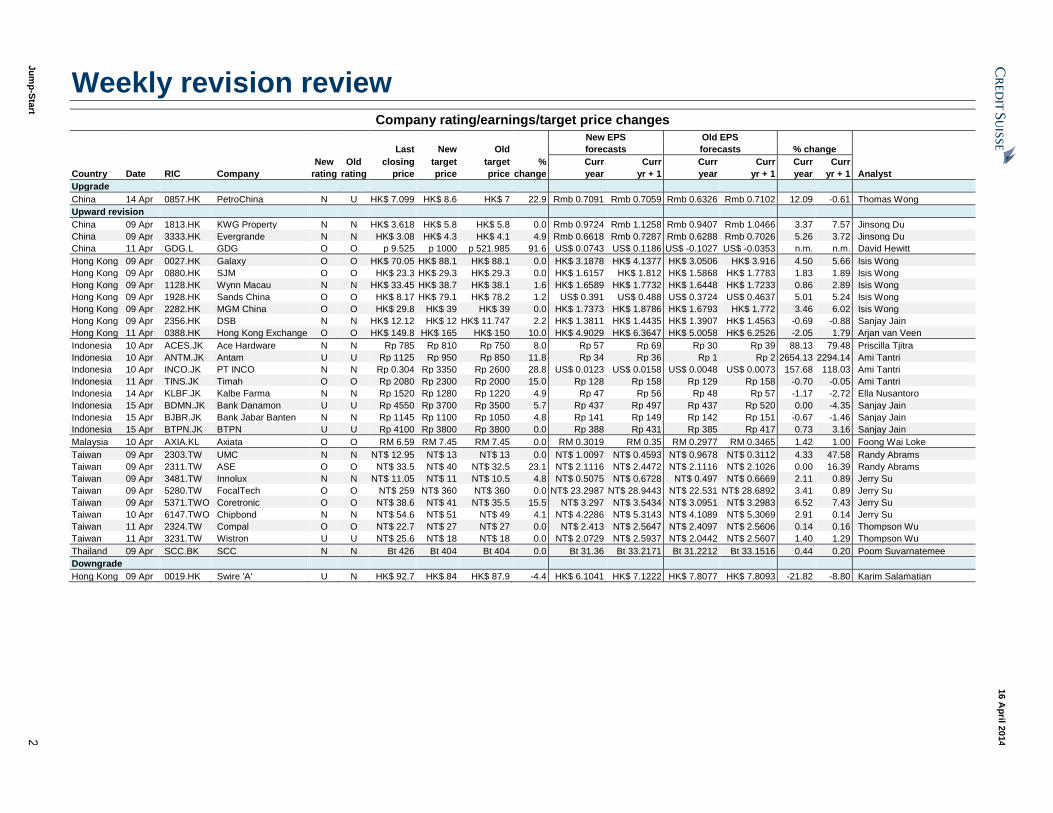

Weekly revision review

Company rating/earnings/target price changes

New EPS Old EPS

Last New Old forecasts forecasts % change

New Old closing target target % Curr Curr Curr Curr Curr Curr

Country Date RIC Company rating rating price price price change year yr + 1 year yr + 1 year yr + 1 Analyst

Upgrade

China 14 Apr 0857.HK PetroChina N U HK$ 7.099 HK$ 8.6 HK$ 7 22.9 Rmb 0.7091 Rmb 0.7059 Rmb 0.6326 Rmb 0.7102 12.09 -0.61 Thomas Wong

Upward revision

China 09 Apr 1813.HK KWG Property N N HK$ 3.618 HK$ 5.8 HK$ 5.8 0.0 Rmb 0.9724 Rmb 1.1258 Rmb 0.9407 Rmb 1.0466 3.37 7.57 Jinsong Du

China 09 Apr 3333.HK Evergrande N N HK$ 3.08 HK$ 4.3 HK$ 4.1 4.9 Rmb 0.6618 Rmb 0.7287 Rmb 0.6288 Rmb 0.7026 5.26 3.72 Jinsong Du

China 11 Apr GDG.L GDG O O p 9.525 p 1000 p 521.985 91.6 US$ 0.0743 US$ 0.1186 US$ -0.1027 US$ -0.0353 n.m. n.m. David Hewitt

Hong Kong 09 Apr 0027.HK Galaxy O O HK$ 70.05 HK$ 88.1 HK$ 88.1 0.0 HK$ 3.1878 HK$ 4.1377 HK$ 3.0506 HK$ 3.916 4.50 5.66 Isis Wong

Hong Kong 09 Apr 0880.HK SJM O O HK$ 23.3 HK$ 29.3 HK$ 29.3 0.0 HK$ 1.6157 HK$ 1.812 HK$ 1.5868 HK$ 1.7783 1.83 1.89 Isis Wong

Hong Kong 09 Apr 1128.HK Wynn Macau N N HK$ 33.45 HK$ 38.7 HK$ 38.1 1.6 HK$ 1.6589 HK$ 1.7732 HK$ 1.6448 HK$ 1.7233 0.86 2.89 Isis Wong

Hong Kong 09 Apr 1928.HK Sands China O O HK$ 8.17 HK$ 79.1 HK$ 78.2 1.2 US$ 0.391 US$ 0.488 US$ 0.3724 US$ 0.4637 5.01 5.24 Isis Wong

Hong Kong 09 Apr 2282.HK MGM China O O HK$ 29.8 HK$ 39 HK$ 39 0.0 HK$ 1.7373 HK$ 1.8786 HK$ 1.6793 HK$ 1.772 3.46 6.02 Isis Wong

Hong Kong 09 Apr 2356.HK DSB N N HK$ 12.12 HK$ 12 HK$ 11.747 2.2 HK$ 1.3811 HK$ 1.4435 HK$ 1.3907 HK$ 1.4563 -0.69 -0.88 Sanjay Jain

Hong Kong 11 Apr 0388.HK Hong Kong Exchange O O HK$ 149.8 HK$ 165 HK$ 150 10.0 HK$ 4.9029 HK$ 6.3647 HK$ 5.0058 HK$ 6.2526 -2.05 1.79 Arjan van Veen

Indonesia 10 Apr ACES.JK Ace Hardware N N Rp 785 Rp 810 Rp 750 8.0 Rp 57 Rp 69 Rp 30 Rp 39 88.13 79.48 Priscilla Tjitra

Indonesia 10 Apr ANTM.JK Antam U U Rp 1125 Rp 950 Rp 850 11.8 Rp 34 Rp 36 Rp 1 Rp 2 2654.13 2294.14 Ami Tantri

Indonesia 10 Apr INCO.JK PT INCO N N Rp 0.304 Rp 3350 Rp 2600 28.8 US$ 0.0123 US$ 0.0158 US$ 0.0048 US$ 0.0073 157.68 118.03 Ami Tantri

Indonesia 11 Apr TINS.JK Timah O O Rp 2080 Rp 2300 Rp 2000 15.0 Rp 128 Rp 158 Rp 129 Rp 158 -0.70 -0.05 Ami Tantri

Indonesia 14 Apr KLBF.JK Kalbe Farma N N Rp 1520 Rp 1280 Rp 1220 4.9 Rp 47 Rp 56 Rp 48 Rp 57 -1.17 -2.72 Ella Nusantoro

Indonesia 15 Apr BDMN.JK Bank Danamon U U Rp 4550 Rp 3700 Rp 3500 5.7 Rp 437 Rp 497 Rp 437 Rp 520 0.00 -4.35 Sanjay Jain

Indonesia 15 Apr BJBR.JK Bank Jabar Banten N N Rp 1145 Rp 1100 Rp 1050 4.8 Rp 141 Rp 149 Rp 142 Rp 151 -0.67 -1.46 Sanjay Jain

Indonesia 15 Apr BTPN.JK BTPN U U Rp 4100 Rp 3800 Rp 3800 0.0 Rp 388 Rp 431 Rp 385 Rp 417 0.73 3.16 Sanjay Jain

Malaysia 10 Apr AXIA.KL Axiata O O RM 6.59 RM 7.45 RM 7.45 0.0 RM 0.3019 RM 0.35 RM 0.2977 RM 0.3465 1.42 1.00 Foong Wai Loke

Taiwan 09 Apr 2303.TW UMC N N NT$ 12.95 NT$ 13 NT$ 13 0.0 NT$ 1.0097 NT$ 0.4593 NT$ 0.9678 NT$ 0.3112 4.33 47.58 Randy Abrams

Taiwan 09 Apr 2311.TW ASE O O NT$ 33.5 NT$ 40 NT$ 32.5 23.1 NT$ 2.1116 NT$ 2.4472 NT$ 2.1116 NT$ 2.1026 0.00 16.39 Randy Abrams

Taiwan 09 Apr 3481.TW Innolux N N NT$ 11.05 NT$ 11 NT$ 10.5 4.8 NT$ 0.5075 NT$ 0.6728 NT$ 0.497 NT$ 0.6669 2.11 0.89 Jerry Su

Taiwan 09 Apr 5280.TW FocalTech O O NT$ 259 NT$ 360 NT$ 360 0.0 NT$ 23.2987 NT$ 28.9443 NT$ 22.531 NT$ 28.6892 3.41 0.89 Jerry Su

Taiwan 09 Apr 5371.TWO Coretronic O O NT$ 38.6 NT$ 41 NT$ 35.5 15.5 NT$ 3.297 NT$ 3.5434 NT$ 3.0951 NT$ 3.2983 6.52 7.43 Jerry Su

Taiwan 10 Apr 6147.TWO Chipbond N N NT$ 54.6 NT$ 51 NT$ 49 4.1 NT$ 4.2286 NT$ 5.3143 NT$ 4.1089 NT$ 5.3069 2.91 0.14 Jerry Su

Taiwan 11 Apr 2324.TW Compal O O NT$ 22.7 NT$ 27 NT$ 27 0.0 NT$ 2.413 NT$ 2.5647 NT$ 2.4097 NT$ 2.5606 0.14 0.16 Thompson Wu

Taiwan 11 Apr 3231.TW Wistron U U NT$ 25.6 NT$ 18 NT$ 18 0.0 NT$ 2.0729 NT$ 2.5937 NT$ 2.0442 NT$ 2.5607 1.40 1.29 Thompson Wu

Thailand 09 Apr SCC.BK SCC N N Bt 426 Bt 404 Bt 404 0.0 Bt 31.36 Bt 33.2171 Bt 31.2212 Bt 33.1516 0.44 0.20 Poom Suvarnatemee

Downgrade

Hong Kong 09 Apr 0019.HK Swire 'A' U N HK$ 92.7 HK$ 84 HK$ 87.9 -4.4 HK$ 6.1041 HK$ 7.1222 HK$ 7.8077 HK$ 7.8093 -21.82 -8.80 Karim Salamatian

16 A

pril 2

014

Ju

mp

-Sta

rt 3

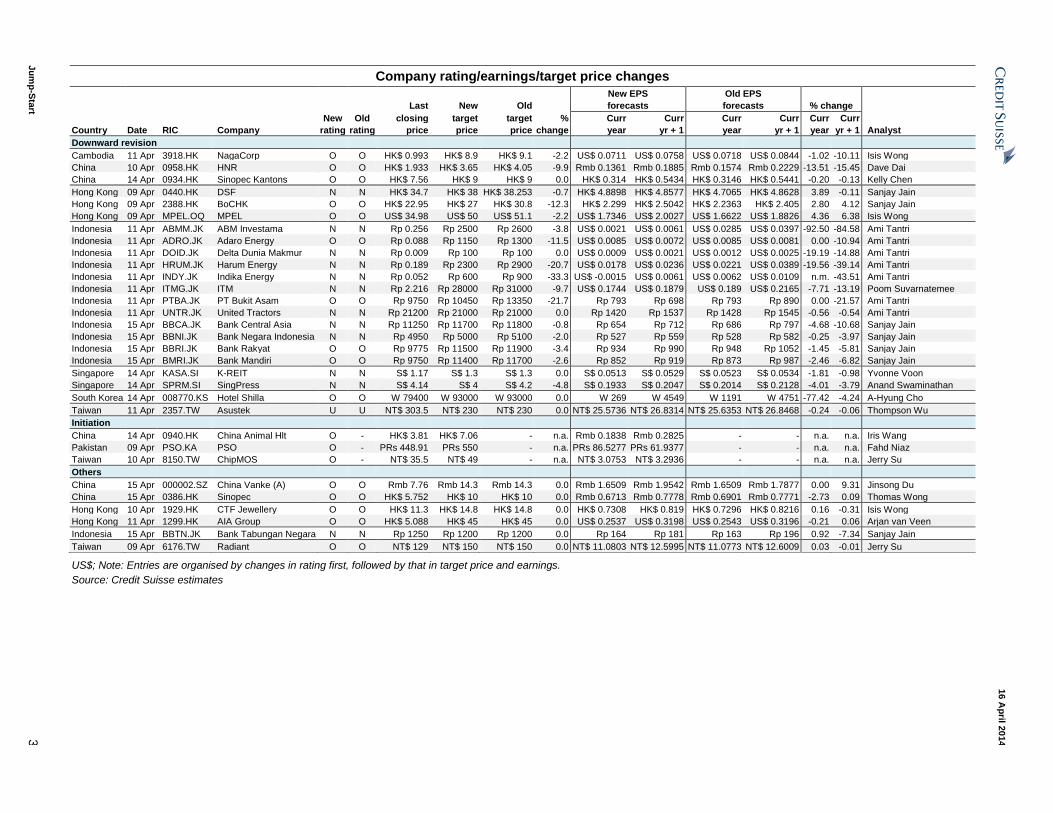

Company rating/earnings/target price changes

New EPS Old EPS

Last New Old forecasts forecasts % change

New Old closing target target % Curr Curr Curr Curr Curr Curr

Country Date RIC Company rating rating price price price change year yr + 1 year yr + 1 year yr + 1 Analyst

Downward revision

Cambodia 11 Apr 3918.HK NagaCorp O O HK$ 0.993 HK$ 8.9 HK$ 9.1 -2.2 US$ 0.0711 US$ 0.0758 US$ 0.0718 US$ 0.0844 -1.02 -10.11 Isis Wong

China 10 Apr 0958.HK HNR O O HK$ 1.933 HK$ 3.65 HK$ 4.05 -9.9 Rmb 0.1361 Rmb 0.1885 Rmb 0.1574 Rmb 0.2229 -13.51 -15.45 Dave Dai

China 14 Apr 0934.HK Sinopec Kantons O O HK$ 7.56 HK$ 9 HK$ 9 0.0 HK$ 0.314 HK$ 0.5434 HK$ 0.3146 HK$ 0.5441 -0.20 -0.13 Kelly Chen

Hong Kong 09 Apr 0440.HK DSF N N HK$ 34.7 HK$ 38 HK$ 38.253 -0.7 HK$ 4.8898 HK$ 4.8577 HK$ 4.7065 HK$ 4.8628 3.89 -0.11 Sanjay Jain

Hong Kong 09 Apr 2388.HK BoCHK O O HK$ 22.95 HK$ 27 HK$ 30.8 -12.3 HK$ 2.299 HK$ 2.5042 HK$ 2.2363 HK$ 2.405 2.80 4.12 Sanjay Jain

Hong Kong 09 Apr MPEL.OQ MPEL O O US$ 34.98 US$ 50 US$ 51.1 -2.2 US$ 1.7346 US$ 2.0027 US$ 1.6622 US$ 1.8826 4.36 6.38 Isis Wong

Indonesia 11 Apr ABMM.JK ABM Investama N N Rp 0.256 Rp 2500 Rp 2600 -3.8 US$ 0.0021 US$ 0.0061 US$ 0.0285 US$ 0.0397 -92.50 -84.58 Ami Tantri

Indonesia 11 Apr ADRO.JK Adaro Energy O O Rp 0.088 Rp 1150 Rp 1300 -11.5 US$ 0.0085 US$ 0.0072 US$ 0.0085 US$ 0.0081 0.00 -10.94 Ami Tantri

Indonesia 11 Apr DOID.JK Delta Dunia Makmur N N Rp 0.009 Rp 100 Rp 100 0.0 US$ 0.0009 US$ 0.0021 US$ 0.0012 US$ 0.0025 -19.19 -14.88 Ami Tantri

Indonesia 11 Apr HRUM.JK Harum Energy N N Rp 0.189 Rp 2300 Rp 2900 -20.7 US$ 0.0178 US$ 0.0236 US$ 0.0221 US$ 0.0389 -19.56 -39.14 Ami Tantri

Indonesia 11 Apr INDY.JK Indika Energy N N Rp 0.052 Rp 600 Rp 900 -33.3 US$ -0.0015 US$ 0.0061 US$ 0.0062 US$ 0.0109 n.m. -43.51 Ami Tantri

Indonesia 11 Apr ITMG.JK ITM N N Rp 2.216 Rp 28000 Rp 31000 -9.7 US$ 0.1744 US$ 0.1879 US$ 0.189 US$ 0.2165 -7.71 -13.19 Poom Suvarnatemee

Indonesia 11 Apr PTBA.JK PT Bukit Asam O O Rp 9750 Rp 10450 Rp 13350 -21.7 Rp 793 Rp 698 Rp 793 Rp 890 0.00 -21.57 Ami Tantri

Indonesia 11 Apr UNTR.JK United Tractors N N Rp 21200 Rp 21000 Rp 21000 0.0 Rp 1420 Rp 1537 Rp 1428 Rp 1545 -0.56 -0.54 Ami Tantri

Indonesia 15 Apr BBCA.JK Bank Central Asia N N Rp 11250 Rp 11700 Rp 11800 -0.8 Rp 654 Rp 712 Rp 686 Rp 797 -4.68 -10.68 Sanjay Jain

Indonesia 15 Apr BBNI.JK Bank Negara Indonesia N N Rp 4950 Rp 5000 Rp 5100 -2.0 Rp 527 Rp 559 Rp 528 Rp 582 -0.25 -3.97 Sanjay Jain

Indonesia 15 Apr BBRI.JK Bank Rakyat O O Rp 9775 Rp 11500 Rp 11900 -3.4 Rp 934 Rp 990 Rp 948 Rp 1052 -1.45 -5.81 Sanjay Jain

Indonesia 15 Apr BMRI.JK Bank Mandiri O O Rp 9750 Rp 11400 Rp 11700 -2.6 Rp 852 Rp 919 Rp 873 Rp 987 -2.46 -6.82 Sanjay Jain

Singapore 14 Apr KASA.SI K-REIT N N S$ 1.17 S$ 1.3 S$ 1.3 0.0 S$ 0.0513 S$ 0.0529 S$ 0.0523 S$ 0.0534 -1.81 -0.98 Yvonne Voon

Singapore 14 Apr SPRM.SI SingPress N N S$ 4.14 S$ 4 S$ 4.2 -4.8 S$ 0.1933 S$ 0.2047 S$ 0.2014 S$ 0.2128 -4.01 -3.79 Anand Swaminathan

South Korea 14 Apr 008770.KS Hotel Shilla O O W 79400 W 93000 W 93000 0.0 W 269 W 4549 W 1191 W 4751 -77.42 -4.24 A-Hyung Cho

Taiwan 11 Apr 2357.TW Asustek U U NT$ 303.5 NT$ 230 NT$ 230 0.0 NT$ 25.5736 NT$ 26.8314 NT$ 25.6353 NT$ 26.8468 -0.24 -0.06 Thompson Wu

Initiation

China 14 Apr 0940.HK China Animal Hlt O - HK$ 3.81 HK$ 7.06 - n.a. Rmb 0.1838 Rmb 0.2825 - - n.a. n.a. Iris Wang

Pakistan 09 Apr PSO.KA PSO O - PRs 448.91 PRs 550 - n.a. PRs 86.5277 PRs 61.9377 - - n.a. n.a. Fahd Niaz

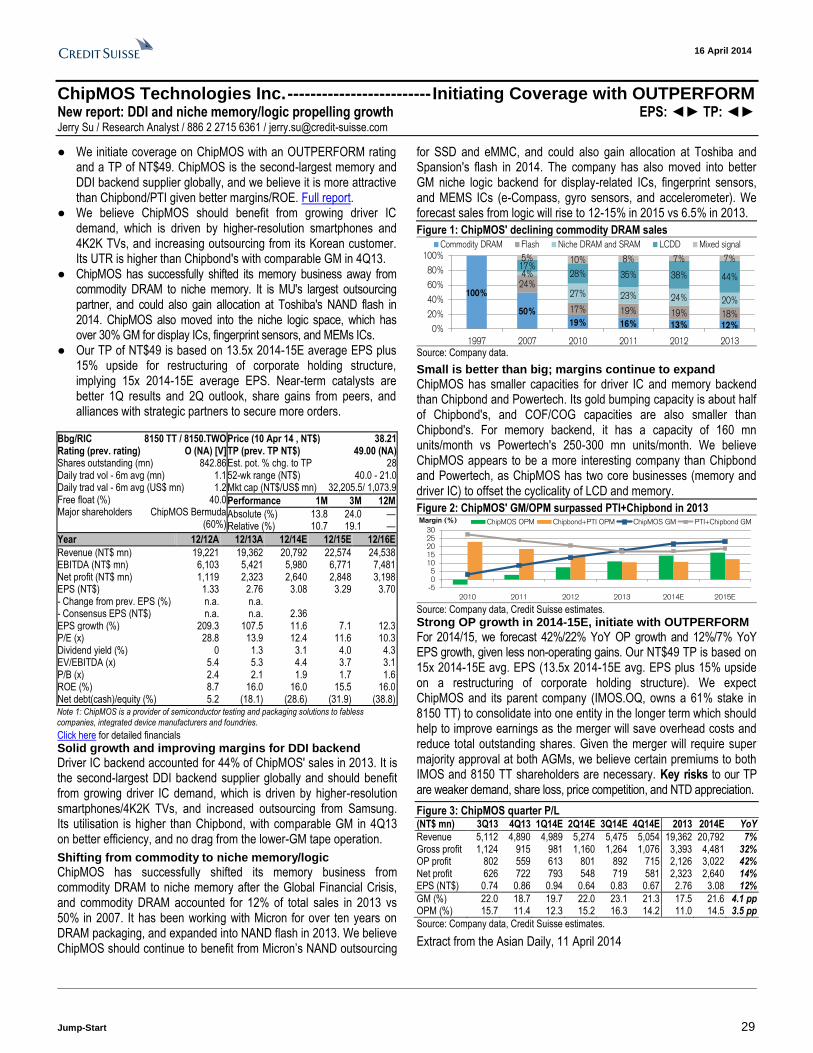

Taiwan 10 Apr 8150.TW ChipMOS O - NT$ 35.5 NT$ 49 - n.a. NT$ 3.0753 NT$ 3.2936 - - n.a. n.a. Jerry Su

Others

China 15 Apr 000002.SZ China Vanke (A) O O Rmb 7.76 Rmb 14.3 Rmb 14.3 0.0 Rmb 1.6509 Rmb 1.9542 Rmb 1.6509 Rmb 1.7877 0.00 9.31 Jinsong Du

China 15 Apr 0386.HK Sinopec O O HK$ 5.752 HK$ 10 HK$ 10 0.0 Rmb 0.6713 Rmb 0.7778 Rmb 0.6901 Rmb 0.7771 -2.73 0.09 Thomas Wong

Hong Kong 10 Apr 1929.HK CTF Jewellery O O HK$ 11.3 HK$ 14.8 HK$ 14.8 0.0 HK$ 0.7308 HK$ 0.819 HK$ 0.7296 HK$ 0.8216 0.16 -0.31 Isis Wong

Hong Kong 11 Apr 1299.HK AIA Group O O HK$ 5.088 HK$ 45 HK$ 45 0.0 US$ 0.2537 US$ 0.3198 US$ 0.2543 US$ 0.3196 -0.21 0.06 Arjan van Veen

Indonesia 15 Apr BBTN.JK Bank Tabungan Negara N N Rp 1250 Rp 1200 Rp 1200 0.0 Rp 164 Rp 181 Rp 163 Rp 196 0.92 -7.34 Sanjay Jain

Taiwan 09 Apr 6176.TW Radiant O O NT$ 129 NT$ 150 NT$ 150 0.0 NT$ 11.0803 NT$ 12.5995 NT$ 11.0773 NT$ 12.6009 0.03 -0.01 Jerry Su

US$; Note: Entries are organised by changes in rating first, followed by that in target price and earnings.

Source: Credit Suisse estimates

16 April 2014

Jump-Start 4

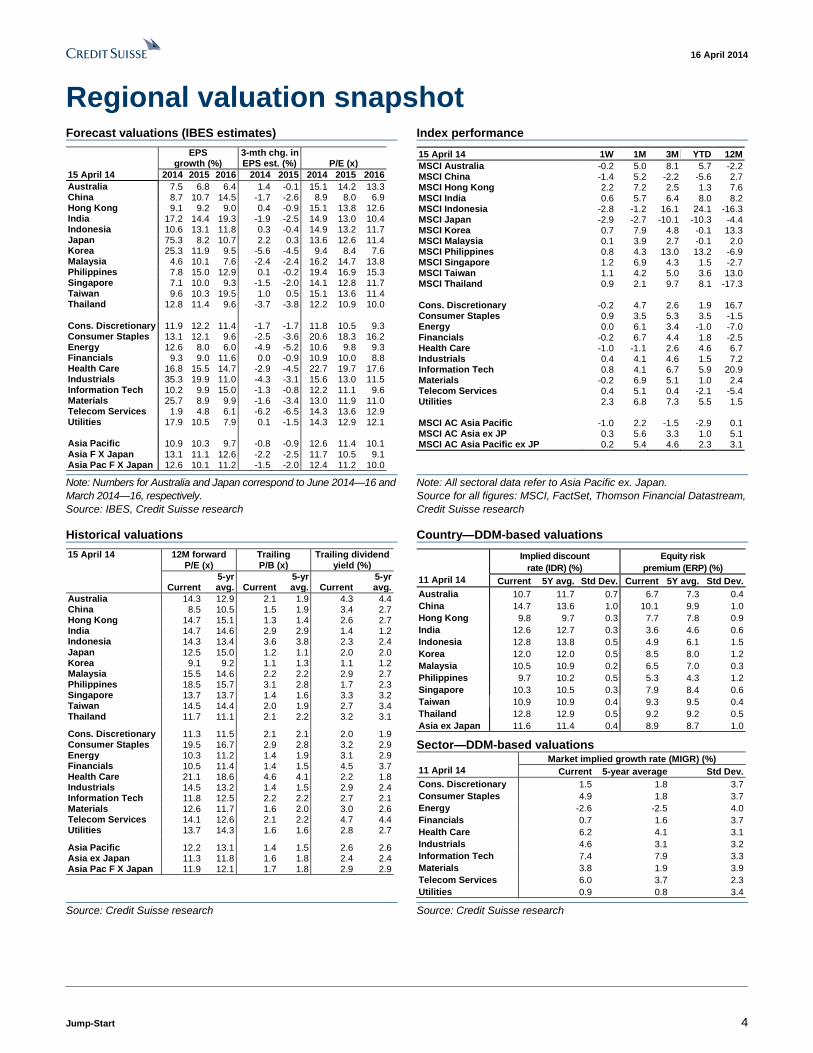

Regional valuation snapshot Forecast valuations (IBES estimates) Index performance

EPS 3-mth chg. in growth (%) EPS est. (%) P/E (x)

15 April 14 2014 2015 2016 2014 2015 2014 2015 2016

Australia 7.5 6.8 6.4 1.4 -0.1 15.1 14.2 13.3 China 8.7 10.7 14.5 -1.7 -2.6 8.9 8.0 6.9 Hong Kong 9.1 9.2 9.0 0.4 -0.9 15.1 13.8 12.6 India 17.2 14.4 19.3 -1.9 -2.5 14.9 13.0 10.4 Indonesia 10.6 13.1 11.8 0.3 -0.4 14.9 13.2 11.7 Japan 75.3 8.2 10.7 2.2 0.3 13.6 12.6 11.4 Korea 25.3 11.9 9.5 -5.6 -4.5 9.4 8.4 7.6 Malaysia 4.6 10.1 7.6 -2.4 -2.4 16.2 14.7 13.8 Philippines 7.8 15.0 12.9 0.1 -0.2 19.4 16.9 15.3 Singapore 7.1 10.0 9.3 -1.5 -2.0 14.1 12.8 11.7 Taiwan 9.6 10.3 19.5 1.0 0.5 15.1 13.6 11.4 Thailand 12.8 11.4 9.6 -3.7 -3.8 12.2 10.9 10.0 Cons. Discretionary 11.9 12.2 11.4 -1.7 -1.7 11.8 10.5 9.3 Consumer Staples 13.1 12.1 9.6 -2.5 -3.6 20.6 18.3 16.2 Energy 12.6 8.0 6.0 -4.9 -5.2 10.6 9.8 9.3 Financials 9.3 9.0 11.6 0.0 -0.9 10.9 10.0 8.8 Health Care 16.8 15.5 14.7 -2.9 -4.5 22.7 19.7 17.6 Industrials 35.3 19.9 11.0 -4.3 -3.1 15.6 13.0 11.5 Information Tech 10.2 9.9 15.0 -1.3 -0.8 12.2 11.1 9.6 Materials 25.7 8.9 9.9 -1.6 -3.4 13.0 11.9 11.0 Telecom Services 1.9 4.8 6.1 -6.2 -6.5 14.3 13.6 12.9 Utilities 17.9 10.5 7.9 0.1 -1.5 14.3 12.9 12.1 Asia Pacific 10.9 10.3 9.7 -0.8 -0.9 12.6 11.4 10.1 Asia F X Japan 13.1 11.1 12.6 -2.2 -2.5 11.7 10.5 9.1 Asia Pac F X Japan 12.6 10.1 11.2 -1.5 -2.0 12.4 11.2 10.0

15 April 14 1W 1M 3M YTD 12M

MSCI Australia -0.2 5.0 8.1 5.7 -2.2 MSCI China -1.4 5.2 -2.2 -5.6 2.7 MSCI Hong Kong 2.2 7.2 2.5 1.3 7.6 MSCI India 0.6 5.7 6.4 8.0 8.2 MSCI Indonesia -2.8 -1.2 16.1 24.1 -16.3 MSCI Japan -2.9 -2.7 -10.1 -10.3 -4.4 MSCI Korea 0.7 7.9 4.8 -0.1 13.3 MSCI Malaysia 0.1 3.9 2.7 -0.1 2.0 MSCI Philippines 0.8 4.3 13.0 13.2 -6.9 MSCI Singapore 1.2 6.9 4.3 1.5 -2.7 MSCI Taiwan 1.1 4.2 5.0 3.6 13.0 MSCI Thailand 0.9 2.1 9.7 8.1 -17.3 Cons. Discretionary -0.2 4.7 2.6 1.9 16.7 Consumer Staples 0.9 3.5 5.3 3.5 -1.5 Energy 0.0 6.1 3.4 -1.0 -7.0 Financials -0.2 6.7 4.4 1.8 -2.5 Health Care -1.0 -1.1 2.6 4.6 6.7 Industrials 0.4 4.1 4.6 1.5 7.2 Information Tech 0.8 4.1 6.7 5.9 20.9 Materials -0.2 6.9 5.1 1.0 2.4 Telecom Services 0.4 5.1 0.4 -2.1 -5.4 Utilities 2.3 6.8 7.3 5.5 1.5 MSCI AC Asia Pacific -1.0 2.2 -1.5 -2.9 0.1 MSCI AC Asia ex JP 0.3 5.6 3.3 1.0 5.1 MSCI AC Asia Pacific ex JP 0.2 5.4 4.6 2.3 3.1

Note: Numbers for Australia and Japan correspond to June 2014—16 and

March 2014—16, respectively.

Source: IBES, Credit Suisse research

Note: All sectoral data refer to Asia Pacific ex. Japan.

Source for all figures: MSCI, FactSet, Thomson Financial Datastream,

Credit Suisse research

Historical valuations Country—DDM-based valuations

15 April 14 12M forward P/E (x)

Trailing P/B (x)

Trailing dividend yield (%)

Current 5-yr avg. Current

5-yr avg. Current

5-yr avg.

Australia 14.3 12.9 2.1 1.9 4.3 4.4 China 8.5 10.5 1.5 1.9 3.4 2.7 Hong Kong 14.7 15.1 1.3 1.4 2.6 2.7 India 14.7 14.6 2.9 2.9 1.4 1.2 Indonesia 14.3 13.4 3.6 3.8 2.3 2.4 Japan 12.5 15.0 1.2 1.1 2.0 2.0 Korea 9.1 9.2 1.1 1.3 1.1 1.2 Malaysia 15.5 14.6 2.2 2.2 2.9 2.7 Philippines 18.5 15.7 3.1 2.8 1.7 2.3 Singapore 13.7 13.7 1.4 1.6 3.3 3.2 Taiwan 14.5 14.4 2.0 1.9 2.7 3.4 Thailand 11.7 11.1 2.1 2.2 3.2 3.1 Cons. Discretionary 11.3 11.5 2.1 2.1 2.0 1.9 Consumer Staples 19.5 16.7 2.9 2.8 3.2 2.9 Energy 10.3 11.2 1.4 1.9 3.1 2.9 Financials 10.5 11.4 1.4 1.5 4.5 3.7 Health Care 21.1 18.6 4.6 4.1 2.2 1.8 Industrials 14.5 13.2 1.4 1.5 2.9 2.4 Information Tech 11.8 12.5 2.2 2.2 2.7 2.1 Materials 12.6 11.7 1.6 2.0 3.0 2.6 Telecom Services 14.1 12.6 2.1 2.2 4.7 4.4 Utilities 13.7 14.3 1.6 1.6 2.8 2.7 Asia Pacific 12.2 13.1 1.4 1.5 2.6 2.6 Asia ex Japan 11.3 11.8 1.6 1.8 2.4 2.4 Asia Pac F X Japan 11.9 12.1 1.7 1.8 2.9 2.9

Implied discount Equity risk

rate (IDR) (%) premium (ERP) (%)

11 April 14 Current 5Y avg. Std Dev. Current 5Y avg. Std Dev.

Australia 10.7 11.7 0.7 6.7 7.3 0.4

China 14.7 13.6 1.0 10.1 9.9 1.0

Hong Kong 9.8 9.7 0.3 7.7 7.8 0.9

India 12.6 12.7 0.3 3.6 4.6 0.6

Indonesia 12.8 13.8 0.5 4.9 6.1 1.5

Korea 12.0 12.0 0.5 8.5 8.0 1.2

Malaysia 10.5 10.9 0.2 6.5 7.0 0.3

Philippines 9.7 10.2 0.5 5.3 4.3 1.2

Singapore 10.3 10.5 0.3 7.9 8.4 0.6

Taiwan 10.9 10.9 0.4 9.3 9.5 0.4

Thailand 12.8 12.9 0.5 9.2 9.2 0.5

Asia ex Japan 11.6 11.4 0.4 8.9 8.7 1.0

Sector—DDM-based valuations Market implied growth rate (MIGR) (%)

11 April 14 Current 5-year average Std Dev.

Cons. Discretionary 1.5 1.8 3.7

Consumer Staples 4.9 1.8 3.7

Energy -2.6 -2.5 4.0

Financials 0.7 1.6 3.7

Health Care 6.2 4.1 3.1

Industrials 4.6 3.1 3.2

Information Tech 7.4 7.9 3.3

Materials 3.8 1.9 3.9

Telecom Services 6.0 3.7 2.3

Utilities 0.9 0.8 3.4

Source: Credit Suisse research Source: Credit Suisse research

16 April 2014

Jump-Start 5

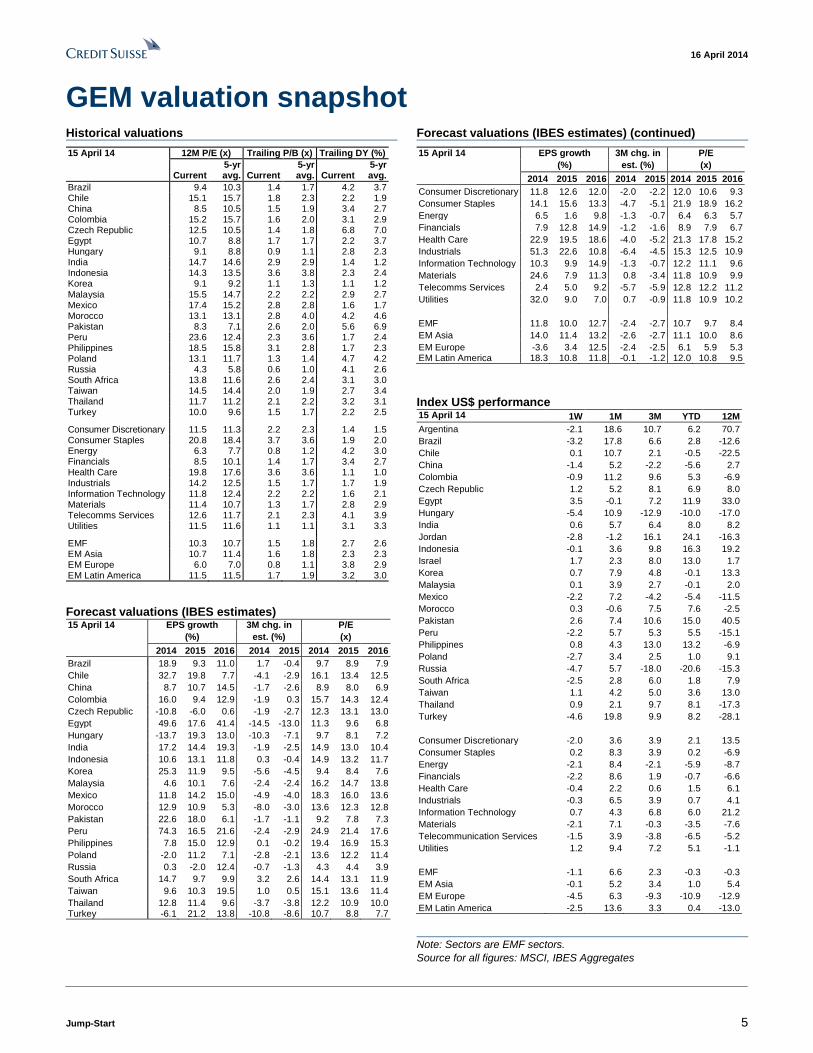

GEM valuation snapshot Historical valuations Forecast valuations (IBES estimates) (continued)

15 April 14 12M P/E (x) Trailing P/B (x) Trailing DY (%)

Current 5-yr

avg. Current 5-yr avg. Current

5-yr avg.

Brazil 9.4 10.3 1.4 1.7 4.2 3.7 Chile 15.1 15.7 1.8 2.3 2.2 1.9 China 8.5 10.5 1.5 1.9 3.4 2.7 Colombia 15.2 15.7 1.6 2.0 3.1 2.9 Czech Republic 12.5 10.5 1.4 1.8 6.8 7.0 Egypt 10.7 8.8 1.7 1.7 2.2 3.7 Hungary 9.1 8.8 0.9 1.1 2.8 2.3 India 14.7 14.6 2.9 2.9 1.4 1.2 Indonesia 14.3 13.5 3.6 3.8 2.3 2.4 Korea 9.1 9.2 1.1 1.3 1.1 1.2

Malaysia 15.5 14.7 2.2 2.2 2.9 2.7 Mexico 17.4 15.2 2.8 2.8 1.6 1.7 Morocco 13.1 13.1 2.8 4.0 4.2 4.6 Pakistan 8.3 7.1 2.6 2.0 5.6 6.9 Peru 23.6 12.4 2.3 3.6 1.7 2.4 Philippines 18.5 15.8 3.1 2.8 1.7 2.3 Poland 13.1 11.7 1.3 1.4 4.7 4.2 Russia 4.3 5.8 0.6 1.0 4.1 2.6 South Africa 13.8 11.6 2.6 2.4 3.1 3.0 Taiwan 14.5 14.4 2.0 1.9 2.7 3.4 Thailand 11.7 11.2 2.1 2.2 3.2 3.1 Turkey 10.0 9.6 1.5 1.7 2.2 2.5 Consumer Discretionary 11.5 11.3 2.2 2.3 1.4 1.5 Consumer Staples 20.8 18.4 3.7 3.6 1.9 2.0 Energy 6.3 7.7 0.8 1.2 4.2 3.0 Financials 8.5 10.1 1.4 1.7 3.4 2.7 Health Care 19.8 17.6 3.6 3.6 1.1 1.0 Industrials 14.2 12.5 1.5 1.7 1.7 1.9 Information Technology 11.8 12.4 2.2 2.2 1.6 2.1 Materials 11.4 10.7 1.3 1.7 2.8 2.9 Telecomms Services 12.6 11.7 2.1 2.3 4.1 3.9 Utilities 11.5 11.6 1.1 1.1 3.1 3.3 EMF 10.3 10.7 1.5 1.8 2.7 2.6 EM Asia 10.7 11.4 1.6 1.8 2.3 2.3 EM Europe 6.0 7.0 0.8 1.1 3.8 2.9 EM Latin America 11.5 11.5 1.7 1.9 3.2 3.0

Forecast valuations (IBES estimates) 15 April 14 EPS growth 3M chg. in P/E

(%) est. (%) (x)

2014 2015 2016 2014 2015 2014 2015 2016

Brazil 18.9 9.3 11.0 1.7 -0.4 9.7 8.9 7.9

Chile 32.7 19.8 7.7 -4.1 -2.9 16.1 13.4 12.5

China 8.7 10.7 14.5 -1.7 -2.6 8.9 8.0 6.9

Colombia 16.0 9.4 12.9 -1.9 0.3 15.7 14.3 12.4

Czech Republic -10.8 -6.0 0.6 -1.9 -2.7 12.3 13.1 13.0

Egypt 49.6 17.6 41.4 -14.5 -13.0 11.3 9.6 6.8

Hungary -13.7 19.3 13.0 -10.3 -7.1 9.7 8.1 7.2

India 17.2 14.4 19.3 -1.9 -2.5 14.9 13.0 10.4

Indonesia 10.6 13.1 11.8 0.3 -0.4 14.9 13.2 11.7

Korea 25.3 11.9 9.5 -5.6 -4.5 9.4 8.4 7.6

Malaysia 4.6 10.1 7.6 -2.4 -2.4 16.2 14.7 13.8

Mexico 11.8 14.2 15.0 -4.9 -4.0 18.3 16.0 13.6

Morocco 12.9 10.9 5.3 -8.0 -3.0 13.6 12.3 12.8

Pakistan 22.6 18.0 6.1 -1.7 -1.1 9.2 7.8 7.3

Peru 74.3 16.5 21.6 -2.4 -2.9 24.9 21.4 17.6

Philippines 7.8 15.0 12.9 0.1 -0.2 19.4 16.9 15.3

Poland -2.0 11.2 7.1 -2.8 -2.1 13.6 12.2 11.4

Russia 0.3 -2.0 12.4 -0.7 -1.3 4.3 4.4 3.9

South Africa 14.7 9.7 9.9 3.2 2.6 14.4 13.1 11.9

Taiwan 9.6 10.3 19.5 1.0 0.5 15.1 13.6 11.4

Thailand 12.8 11.4 9.6 -3.7 -3.8 12.2 10.9 10.0 Turkey -6.1 21.2 13.8 -10.8 -8.6 10.7 8.8 7.7

15 April 14 EPS growth 3M chg. in P/E

(%) est. (%) (x)

2014 2015 2016 2014 2015 2014 2015 2016

Consumer Discretionary 11.8 12.6 12.0 -2.0 -2.2 12.0 10.6 9.3

Consumer Staples 14.1 15.6 13.3 -4.7 -5.1 21.9 18.9 16.2

Energy 6.5 1.6 9.8 -1.3 -0.7 6.4 6.3 5.7

Financials 7.9 12.8 14.9 -1.2 -1.6 8.9 7.9 6.7

Health Care 22.9 19.5 18.6 -4.0 -5.2 21.3 17.8 15.2

Industrials 51.3 22.6 10.8 -6.4 -4.5 15.3 12.5 10.9

Information Technology 10.3 9.9 14.9 -1.3 -0.7 12.2 11.1 9.6

Materials 24.6 7.9 11.3 0.8 -3.4 11.8 10.9 9.9

Telecomms Services 2.4 5.0 9.2 -5.7 -5.9 12.8 12.2 11.2

Utilities 32.0 9.0 7.0 0.7 -0.9 11.8 10.9 10.2

EMF 11.8 10.0 12.7 -2.4 -2.7 10.7 9.7 8.4

EM Asia 14.0 11.4 13.2 -2.6 -2.7 11.1 10.0 8.6

EM Europe -3.6 3.4 12.5 -2.4 -2.5 6.1 5.9 5.3 EM Latin America 18.3 10.8 11.8 -0.1 -1.2 12.0 10.8 9.5

Index US$ performance 15 April 14 1W 1M 3M YTD 12M

Argentina -2.1 18.6 10.7 6.2 70.7

Brazil -3.2 17.8 6.6 2.8 -12.6

Chile 0.1 10.7 2.1 -0.5 -22.5

China -1.4 5.2 -2.2 -5.6 2.7

Colombia -0.9 11.2 9.6 5.3 -6.9

Czech Republic 1.2 5.2 8.1 6.9 8.0

Egypt 3.5 -0.1 7.2 11.9 33.0

Hungary -5.4 10.9 -12.9 -10.0 -17.0

India 0.6 5.7 6.4 8.0 8.2

Jordan -2.8 -1.2 16.1 24.1 -16.3

Indonesia -0.1 3.6 9.8 16.3 19.2

Israel 1.7 2.3 8.0 13.0 1.7

Korea 0.7 7.9 4.8 -0.1 13.3

Malaysia 0.1 3.9 2.7 -0.1 2.0

Mexico -2.2 7.2 -4.2 -5.4 -11.5

Morocco 0.3 -0.6 7.5 7.6 -2.5

Pakistan 2.6 7.4 10.6 15.0 40.5

Peru -2.2 5.7 5.3 5.5 -15.1

Philippines 0.8 4.3 13.0 13.2 -6.9

Poland -2.7 3.4 2.5 1.0 9.1

Russia -4.7 5.7 -18.0 -20.6 -15.3

South Africa -2.5 2.8 6.0 1.8 7.9

Taiwan 1.1 4.2 5.0 3.6 13.0

Thailand 0.9 2.1 9.7 8.1 -17.3

Turkey -4.6 19.8 9.9 8.2 -28.1

Consumer Discretionary -2.0 3.6 3.9 2.1 13.5

Consumer Staples 0.2 8.3 3.9 0.2 -6.9

Energy -2.1 8.4 -2.1 -5.9 -8.7

Financials -2.2 8.6 1.9 -0.7 -6.6

Health Care -0.4 2.2 0.6 1.5 6.1

Industrials -0.3 6.5 3.9 0.7 4.1

Information Technology 0.7 4.3 6.8 6.0 21.2

Materials -2.1 7.1 -0.3 -3.5 -7.6

Telecommunication Services -1.5 3.9 -3.8 -6.5 -5.2

Utilities 1.2 9.4 7.2 5.1 -1.1

EMF -1.1 6.6 2.3 -0.3 -0.3

EM Asia -0.1 5.2 3.4 1.0 5.4

EM Europe -4.5 6.3 -9.3 -10.9 -12.9

EM Latin America -2.5 13.6 3.3 0.4 -13.0

Note: Sectors are EMF sectors.

Source for all figures: MSCI, IBES Aggregates

16 April 2014

Jump-Start 6

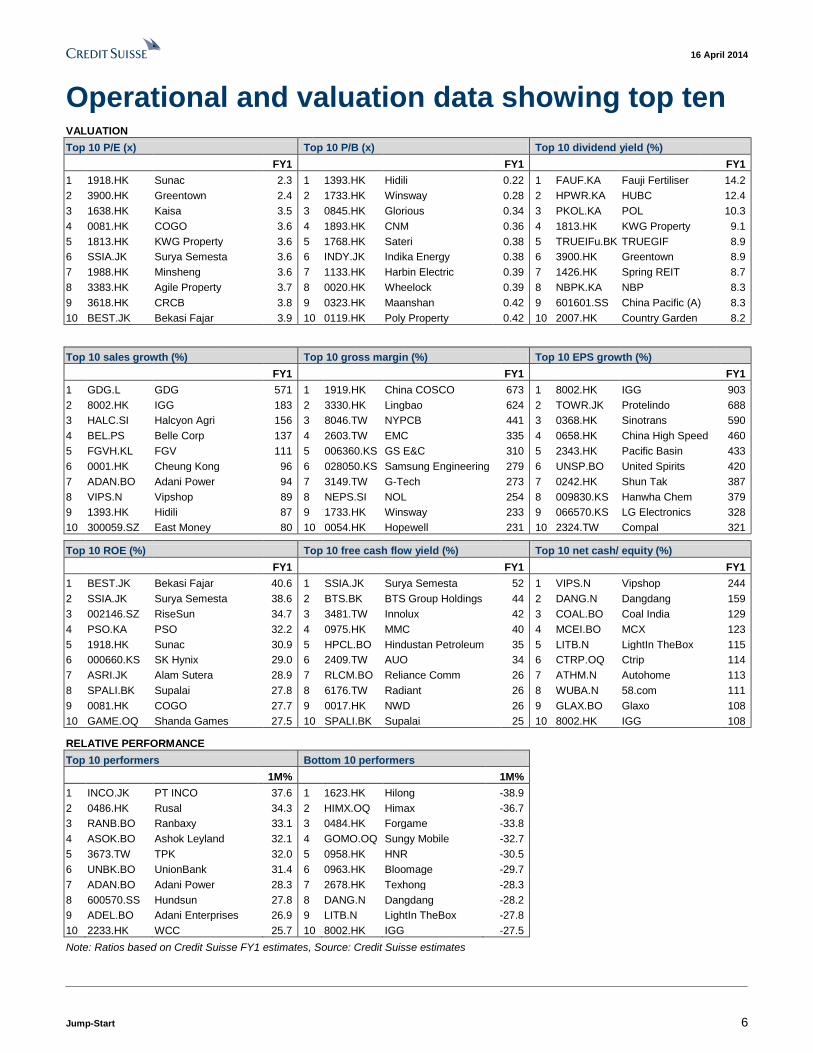

Operational and valuation data showing top ten VALUATION

Top 10 P/E (x) Top 10 P/B (x) Top 10 dividend yield (%)

FY1 FY1 FY1

1 1918.HK Sunac 2.3 1 1393.HK Hidili 0.22 1 FAUF.KA Fauji Fertiliser 14.2

2 3900.HK Greentown 2.4 2 1733.HK Winsway 0.28 2 HPWR.KA HUBC 12.4

3 1638.HK Kaisa 3.5 3 0845.HK Glorious 0.34 3 PKOL.KA POL 10.3

4 0081.HK COGO 3.6 4 1893.HK CNM 0.36 4 1813.HK KWG Property 9.1

5 1813.HK KWG Property 3.6 5 1768.HK Sateri 0.38 5 TRUEIFu.BK TRUEGIF 8.9

6 SSIA.JK Surya Semesta 3.6 6 INDY.JK Indika Energy 0.38 6 3900.HK Greentown 8.9

7 1988.HK Minsheng 3.6 7 1133.HK Harbin Electric 0.39 7 1426.HK Spring REIT 8.7

8 3383.HK Agile Property 3.7 8 0020.HK Wheelock 0.39 8 NBPK.KA NBP 8.3

9 3618.HK CRCB 3.8 9 0323.HK Maanshan 0.42 9 601601.SS China Pacific (A) 8.3

10 BEST.JK Bekasi Fajar 3.9 10 0119.HK Poly Property 0.42 10 2007.HK Country Garden 8.2

Top 10 sales growth (%) Top 10 gross margin (%) Top 10 EPS growth (%)

FY1 FY1 FY1

1 GDG.L GDG 571 1 1919.HK China COSCO 673 1 8002.HK IGG 903

2 8002.HK IGG 183 2 3330.HK Lingbao 624 2 TOWR.JK Protelindo 688

3 HALC.SI Halcyon Agri 156 3 8046.TW NYPCB 441 3 0368.HK Sinotrans 590

4 BEL.PS Belle Corp 137 4 2603.TW EMC 335 4 0658.HK China High Speed 460

5 FGVH.KL FGV 111 5 006360.KS GS E&C 310 5 2343.HK Pacific Basin 433

6 0001.HK Cheung Kong 96 6 028050.KS Samsung Engineering 279 6 UNSP.BO United Spirits 420

7 ADAN.BO Adani Power 94 7 3149.TW G-Tech 273 7 0242.HK Shun Tak 387

8 VIPS.N Vipshop 89 8 NEPS.SI NOL 254 8 009830.KS Hanwha Chem 379

9 1393.HK Hidili 87 9 1733.HK Winsway 233 9 066570.KS LG Electronics 328

10 300059.SZ East Money 80 10 0054.HK Hopewell 231 10 2324.TW Compal 321

Top 10 ROE (%) Top 10 free cash flow yield (%) Top 10 net cash/ equity (%)

FY1 FY1 FY1

1 BEST.JK Bekasi Fajar 40.6 1 SSIA.JK Surya Semesta 52 1 VIPS.N Vipshop 244

2 SSIA.JK Surya Semesta 38.6 2 BTS.BK BTS Group Holdings 44 2 DANG.N Dangdang 159

3 002146.SZ RiseSun 34.7 3 3481.TW Innolux 42 3 COAL.BO Coal India 129

4 PSO.KA PSO 32.2 4 0975.HK MMC 40 4 MCEI.BO MCX 123

5 1918.HK Sunac 30.9 5 HPCL.BO Hindustan Petroleum 35 5 LITB.N LightIn TheBox 115

6 000660.KS SK Hynix 29.0 6 2409.TW AUO 34 6 CTRP.OQ Ctrip 114

7 ASRI.JK Alam Sutera 28.9 7 RLCM.BO Reliance Comm 26 7 ATHM.N Autohome 113

8 SPALI.BK Supalai 27.8 8 6176.TW Radiant 26 8 WUBA.N 58.com 111

9 0081.HK COGO 27.7 9 0017.HK NWD 26 9 GLAX.BO Glaxo 108

10 GAME.OQ Shanda Games 27.5 10 SPALI.BK Supalai 25 10 8002.HK IGG 108

RELATIVE PERFORMANCE

Top 10 performers Bottom 10 performers

1M% 1M%

1 INCO.JK PT INCO 37.6 1 1623.HK Hilong -38.9

2 0486.HK Rusal 34.3 2 HIMX.OQ Himax -36.7

3 RANB.BO Ranbaxy 33.1 3 0484.HK Forgame -33.8

4 ASOK.BO Ashok Leyland 32.1 4 GOMO.OQ Sungy Mobile -32.7

5 3673.TW TPK 32.0 5 0958.HK HNR -30.5

6 UNBK.BO UnionBank 31.4 6 0963.HK Bloomage -29.7

7 ADAN.BO Adani Power 28.3 7 2678.HK Texhong -28.3

8 600570.SS Hundsun 27.8 8 DANG.N Dangdang -28.2

9 ADEL.BO Adani Enterprises 26.9 9 LITB.N LightIn TheBox -27.8

10 2233.HK WCC 25.7 10 8002.HK IGG -27.5

Note: Ratios based on Credit Suisse FY1 estimates, Source: Credit Suisse estimates

16 April 2014

Jump-Start 7

Credit Suisse macroeconomic forecasts

16 April 2014

Jump-Start 8

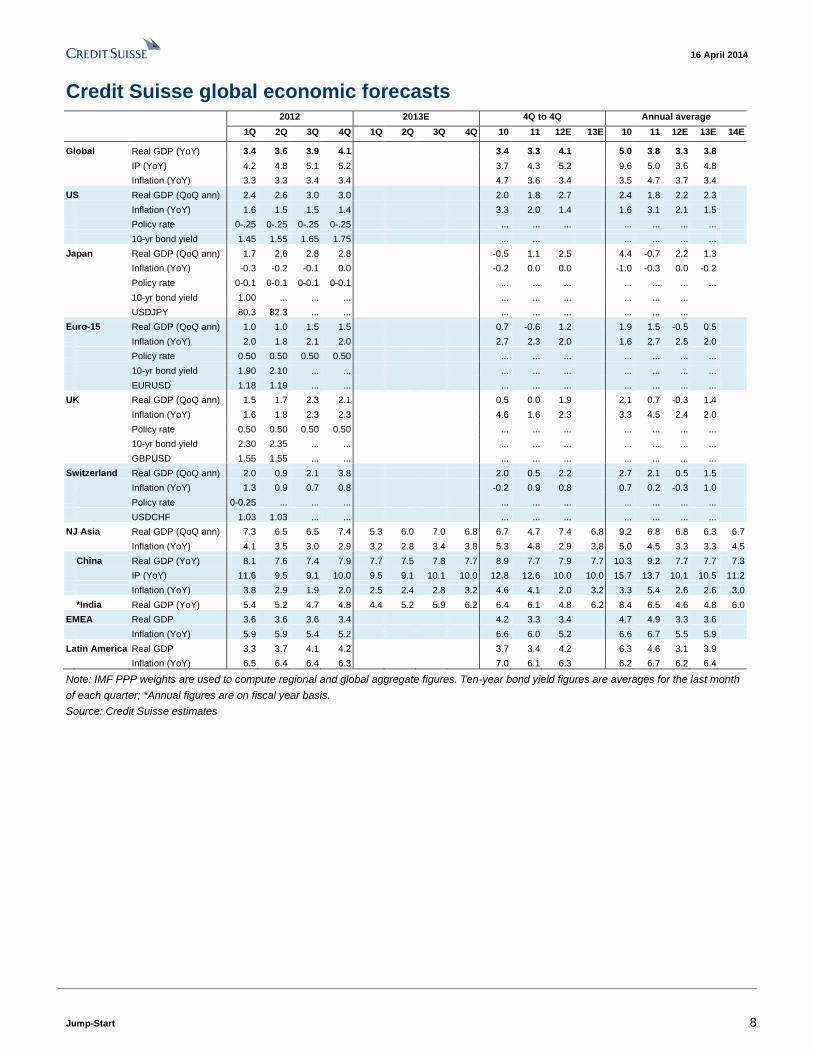

Credit Suisse global economic forecasts

2012 2013E 4Q to 4Q Annual average

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 10 11 12E 13E 10 11 12E 13E 14E

Global Real GDP (YoY) 3.4 3.6 3.9 4.1 3.4 3.3 4.1 5.0 3.8 3.3 3.8 IP (YoY) 4.2 4.8 5.1 5.2 3.7 4.3 5.2 9.6 5.0 3.6 4.8 Inflation (YoY) 3.3 3.3 3.4 3.4 4.7 3.6 3.4 3.5 4.7 3.7 3.4

US Real GDP (QoQ ann) 2.4 2.6 3.0 3.0 2.0 1.8 2.7 2.4 1.8 2.2 2.3 Inflation (YoY) 1.6 1.5 1.5 1.4 3.3 2.0 1.4 1.6 3.1 2.1 1.5 Policy rate 0-.25 0-.25 0-.25 0-.25 ... ... ... ... ... ... ... 10-yr bond yield 1.45 1.55 1.65 1.75 ... ... ... ... ... ...

Japan Real GDP (QoQ ann) 1.7 2.6 2.8 2.8 -0.5 1.1 2.5 4.4 -0.7 2.2 1.3 Inflation (YoY) -0.3 -0.2 -0.1 0.0 -0.2 0.0 0.0 -1.0 -0.3 0.0 -0.2 Policy rate 0-0.1 0-0.1 0-0.1 0-0.1 ... ... ... ... ... ... ... 10-yr bond yield 1.00 ... ... ... ... ... ... ... ... ... USDJPY 80.3 82.3 ... ... ... ... ... ... ... ...

Euro-15 Real GDP (QoQ ann) 1.0 1.0 1.5 1.5 0.7 -0.6 1.2 1.9 1.5 -0.5 0.5 Inflation (YoY) 2.0 1.8 2.1 2.0 2.7 2.3 2.0 1.6 2.7 2.5 2.0 Policy rate 0.50 0.50 0.50 0.50 ... ... ... ... ... ... ... 10-yr bond yield 1.90 2.10 ... ... ... ... ... ... ... ... ... EURUSD 1.18 1.19 ... ... ... ... ... ... ... ... ...

UK Real GDP (QoQ ann) 1.5 1.7 2.3 2.1 0.5 0.0 1.9 2.1 0.7 -0.3 1.4 Inflation (YoY) 1.6 1.8 2.3 2.3 4.6 1.6 2.3 3.3 4.5 2.4 2.0 Policy rate 0.50 0.50 0.50 0.50 ... ... ... ... ... ... ... 10-yr bond yield 2.30 2.35 ... ... ... ... ... ... ... ... ... GBPUSD 1.55 1.55 ... ... ... ... ... ... ... ... ...

Switzerland Real GDP (QoQ ann) 2.0 0.9 2.1 3.8 2.0 0.5 2.2 2.7 2.1 0.5 1.5 Inflation (YoY) 1.3 0.9 0.7 0.8 -0.2 0.9 0.8 0.7 0.2 -0.3 1.0 Policy rate 0-0.25 ... ... ... ... ... ... ... ... ... ... USDCHF 1.03 1.03 ... ... ... ... ... ... ... ... ...

NJ Asia Real GDP (QoQ ann) 7.3 6.5 6.5 7.4 5.3 6.0 7.0 6.8 6.7 4.7 7.4 6.8 9.2 6.8 6.8 6.3 6.7

Inflation (YoY) 4.1 3.5 3.0 2.9 3.2 2.8 3.4 3.8 5.3 4.8 2.9 3.8 5.0 4.5 3.3 3.3 4.5 China Real GDP (YoY) 8.1 7.6 7.4 7.9 7.7 7.5 7.8 7.7 8.9 7.7 7.9 7.7 10.3 9.2 7.7 7.7 7.3 IP (YoY) 11.6 9.5 9.1 10.0 9.5 9.1 10.1 10.0 12.8 12.6 10.0 10.0 15.7 13.7 10.1 10.5 11.2 Inflation (YoY) 3.8 2.9 1.9 2.0 2.5 2.4 2.8 3.2 4.6 4.1 2.0 3.2 3.3 5.4 2.6 2.6 3.0 *India Real GDP (YoY) 5.4 5.2 4.7 4.8 4.4 5.2 5.9 6.2 6.4 6.1 4.8 6.2 8.4 6.5 4.6 4.8 6.0

EMEA Real GDP 3.6 3.6 3.6 3.4 4.2 3.3 3.4 4.7 4.9 3.3 3.6 Inflation (YoY) 5.9 5.9 5.4 5.2 6.6 6.0 5.2 6.6 6.7 5.5 5.9

Latin America Real GDP 3.3 3.7 4.1 4.2 3.7 3.4 4.2 6.3 4.6 3.1 3.9 Inflation (YoY) 6.5 6.4 6.4 6.3 7.0 6.1 6.3 6.2 6.7 6.2 6.4

Note: IMF PPP weights are used to compute regional and global aggregate figures. Ten-year bond yield figures are averages for the last month

of each quarter; *Annual figures are on fiscal year basis.

Source: Credit Suisse estimates

16 April 2014

Jump-Start 9

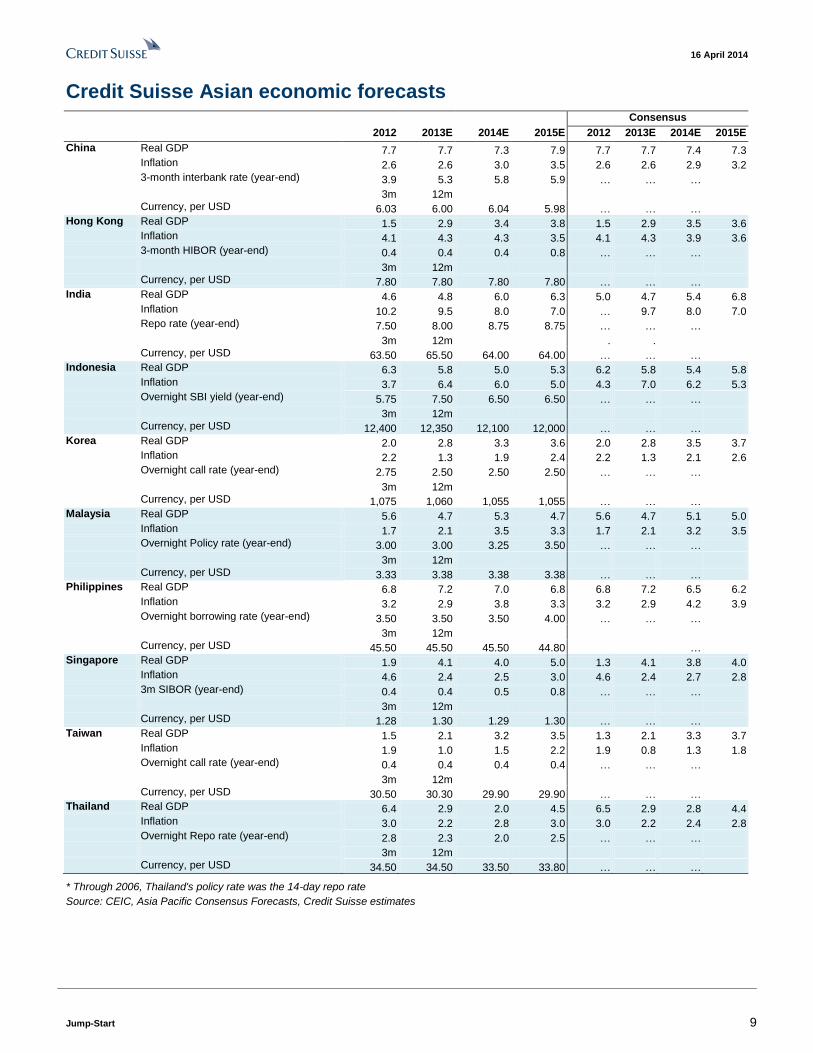

Credit Suisse Asian economic forecasts Consensus

2012 2013E 2014E 2015E 2012 2013E 2014E 2015E

China Real GDP 7.7 7.7 7.3 7.9 7.7 7.7 7.4 7.3 Inflation 2.6 2.6 3.0 3.5 2.6 2.6 2.9 3.2 3-month interbank rate (year-end) 3.9 5.3 5.8 5.9 … … … 3m 12m Currency, per USD 6.03 6.00 6.04 5.98 … … … Hong Kong Real GDP 1.5 2.9 3.4 3.8 1.5 2.9 3.5 3.6 Inflation 4.1 4.3 4.3 3.5 4.1 4.3 3.9 3.6 3-month HIBOR (year-end) 0.4 0.4 0.4 0.8 … … … 3m 12m Currency, per USD 7.80 7.80 7.80 7.80 … … … India Real GDP 4.6 4.8 6.0 6.3 5.0 4.7 5.4 6.8 Inflation 10.2 9.5 8.0 7.0 … 9.7 8.0 7.0 Repo rate (year-end) 7.50 8.00 8.75 8.75 … … … 3m 12m . . Currency, per USD 63.50 65.50 64.00 64.00 … … … Indonesia Real GDP 6.3 5.8 5.0 5.3 6.2 5.8 5.4 5.8 Inflation 3.7 6.4 6.0 5.0 4.3 7.0 6.2 5.3 Overnight SBI yield (year-end) 5.75 7.50 6.50 6.50 … … … 3m 12m Currency, per USD 12,400 12,350 12,100 12,000 … … … Korea Real GDP 2.0 2.8 3.3 3.6 2.0 2.8 3.5 3.7 Inflation 2.2 1.3 1.9 2.4 2.2 1.3 2.1 2.6 Overnight call rate (year-end) 2.75 2.50 2.50 2.50 … … … 3m 12m Currency, per USD 1,075 1,060 1,055 1,055 … … … Malaysia Real GDP 5.6 4.7 5.3 4.7 5.6 4.7 5.1 5.0 Inflation 1.7 2.1 3.5 3.3 1.7 2.1 3.2 3.5 Overnight Policy rate (year-end) 3.00 3.00 3.25 3.50 … … … 3m 12m Currency, per USD 3.33 3.38 3.38 3.38 … … … Philippines Real GDP 6.8 7.2 7.0 6.8 6.8 7.2 6.5 6.2 Inflation 3.2 2.9 3.8 3.3 3.2 2.9 4.2 3.9 Overnight borrowing rate (year-end) 3.50 3.50 3.50 4.00 … … … 3m 12m Currency, per USD 45.50 45.50 45.50 44.80 … Singapore Real GDP 1.9 4.1 4.0 5.0 1.3 4.1 3.8 4.0 Inflation 4.6 2.4 2.5 3.0 4.6 2.4 2.7 2.8 3m SIBOR (year-end) 0.4 0.4 0.5 0.8 … … … 3m 12m Currency, per USD 1.28 1.30 1.29 1.30 … … … Taiwan Real GDP 1.5 2.1 3.2 3.5 1.3 2.1 3.3 3.7 Inflation 1.9 1.0 1.5 2.2 1.9 0.8 1.3 1.8 Overnight call rate (year-end) 0.4 0.4 0.4 0.4 … … … 3m 12m Currency, per USD 30.50 30.30 29.90 29.90 … … … Thailand Real GDP 6.4 2.9 2.0 4.5 6.5 2.9 2.8 4.4 Inflation 3.0 2.2 2.8 3.0 3.0 2.2 2.4 2.8 Overnight Repo rate (year-end) 2.8 2.3 2.0 2.5 … … … 3m 12m Currency, per USD 34.50 34.50 33.50 33.80 … … …

* Through 2006, Thailand's policy rate was the 14-day repo rate

Source: CEIC, Asia Pacific Consensus Forecasts, Credit Suisse estimates

16 April 2014

Jump-Start 10

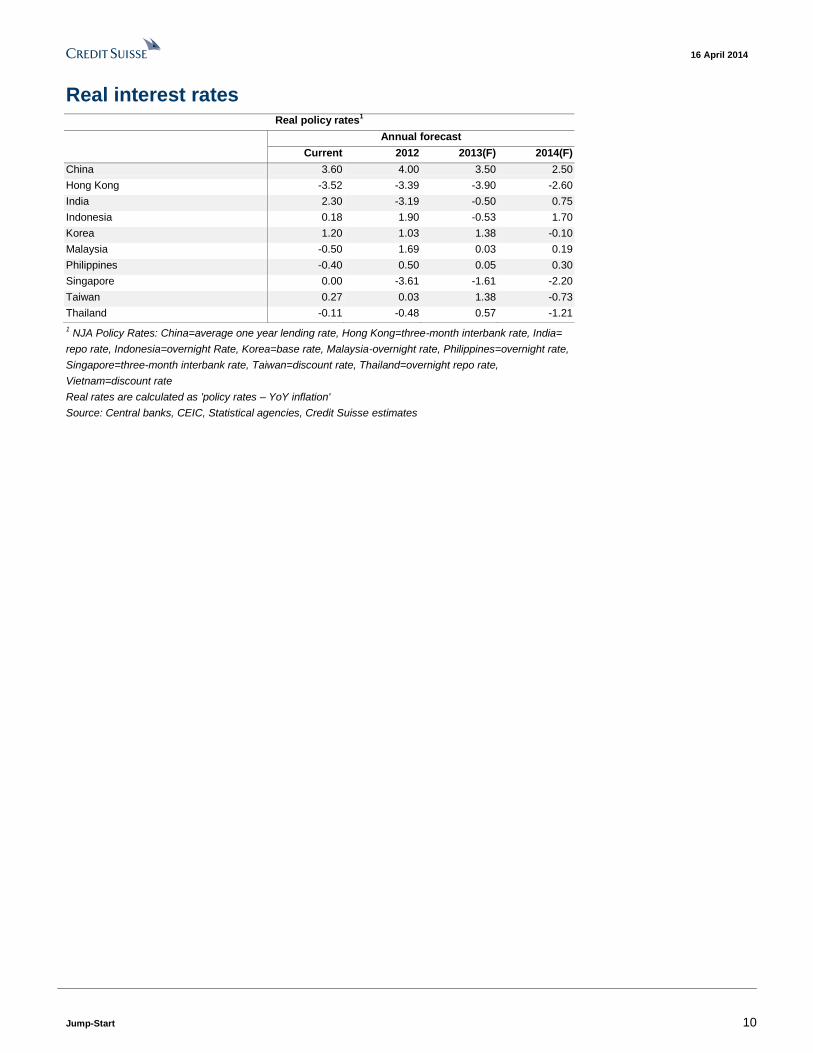

Real interest rates Real policy rates

1

Annual forecast

Current 2012 2013(F) 2014(F)

China 3.60 4.00 3.50 2.50

Hong Kong -3.52 -3.39 -3.90 -2.60

India 2.30 -3.19 -0.50 0.75

Indonesia 0.18 1.90 -0.53 1.70

Korea 1.20 1.03 1.38 -0.10

Malaysia -0.50 1.69 0.03 0.19

Philippines -0.40 0.50 0.05 0.30

Singapore 0.00 -3.61 -1.61 -2.20

Taiwan 0.27 0.03 1.38 -0.73

Thailand -0.11 -0.48 0.57 -1.21

1 NJA Policy Rates: China=average one year lending rate, Hong Kong=three-month interbank rate, India=

repo rate, Indonesia=overnight Rate, Korea=base rate, Malaysia-overnight rate, Philippines=overnight rate,

Singapore=three-month interbank rate, Taiwan=discount rate, Thailand=overnight repo rate,

Vietnam=discount rate

Real rates are calculated as 'policy rates – YoY inflation'

Source: Central banks, CEIC, Statistical agencies, Credit Suisse estimates

16 April 2014

Jump-Start 11

Top stories from Credit Suisse research last week

16 April 2014

Jump-Start 12

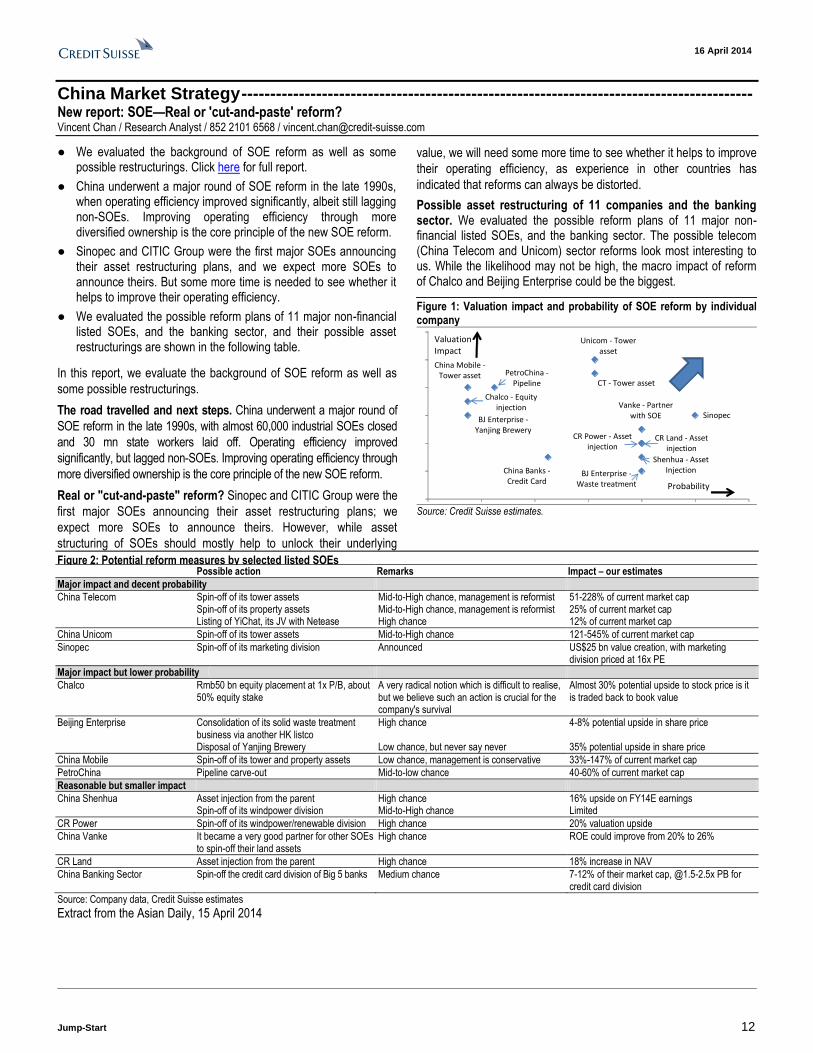

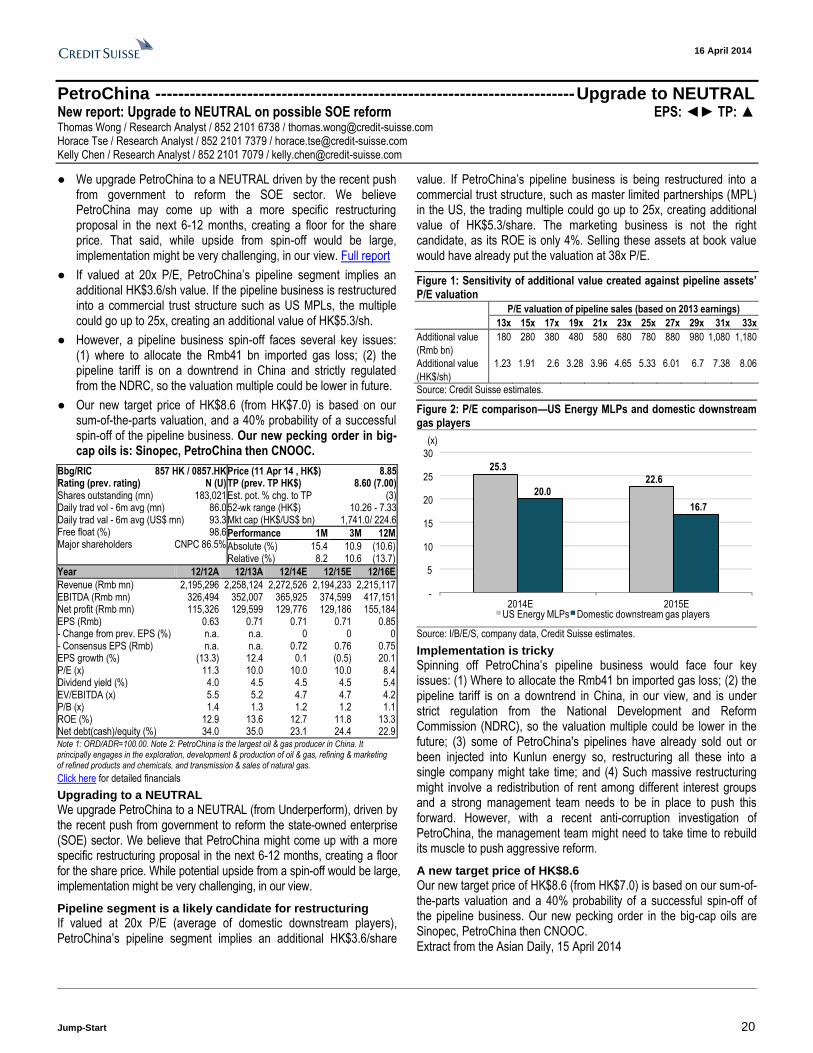

China Market Strategy ----------------------------------------------------------------------------------------- New report: SOE—Real or 'cut-and-paste' reform? Vincent Chan / Research Analyst / 852 2101 6568 / [email protected]

● We evaluated the background of SOE reform as well as some possible restructurings. Click here for full report.

● China underwent a major round of SOE reform in the late 1990s, when operating efficiency improved significantly, albeit still lagging non-SOEs. Improving operating efficiency through more diversified ownership is the core principle of the new SOE reform.

● Sinopec and CITIC Group were the first major SOEs announcing their asset restructuring plans, and we expect more SOEs to announce theirs. But some more time is needed to see whether it helps to improve their operating efficiency.

● We evaluated the possible reform plans of 11 major non-financial listed SOEs, and the banking sector, and their possible asset restructurings are shown in the following table.

In this report, we evaluate the background of SOE reform as well as

some possible restructurings.

The road travelled and next steps. China underwent a major round of

SOE reform in the late 1990s, with almost 60,000 industrial SOEs closed

and 30 mn state workers laid off. Operating efficiency improved

significantly, but lagged non-SOEs. Improving operating efficiency through

more diversified ownership is the core principle of the new SOE reform.

Real or "cut-and-paste" reform? Sinopec and CITIC Group were the

first major SOEs announcing their asset restructuring plans; we

expect more SOEs to announce theirs. However, while asset

structuring of SOEs should mostly help to unlock their underlying

value, we will need some more time to see whether it helps to improve

their operating efficiency, as experience in other countries has

indicated that reforms can always be distorted.

Possible asset restructuring of 11 companies and the banking sector. We evaluated the possible reform plans of 11 major non-financial listed SOEs, and the banking sector. The possible telecom (China Telecom and Unicom) sector reforms look most interesting to us. While the likelihood may not be high, the macro impact of reform of Chalco and Beijing Enterprise could be the biggest.

Figure 1: Valuation impact and probability of SOE reform by individual company

Shenhua - Asset Injection

Chalco - Equity injection

CR Power - Asset injection

BJ Enterprise -Waste treatment

BJ Enterprise -Yanjing Brewery

China Mobile -Tower asset

CT - Tower asset

Unicom - Tower asset

Vanke - Partner with SOE

CR Land - Asset injection

Sinopec

PetroChina -Pipeline

China Banks -Credit Card

Valuation Impact

Probability

Source: Credit Suisse estimates.

Figure 2: Potential reform measures by selected listed SOEs Possible action Remarks Impact – our estimates

Major impact and decent probability

China Telecom Spin-off of its tower assets Mid-to-High chance, management is reformist 51-228% of current market cap Spin-off of its property assets Mid-to-High chance, management is reformist 25% of current market cap Listing of YiChat, its JV with Netease High chance 12% of current market cap

China Unicom Spin-off of its tower assets Mid-to-High chance 121-545% of current market cap

Sinopec Spin-off of its marketing division Announced US$25 bn value creation, with marketing division priced at 16x PE

Major impact but lower probability

Chalco Rmb50 bn equity placement at 1x P/B, about 50% equity stake

A very radical notion which is difficult to realise, but we believe such an action is crucial for the company's survival

Almost 30% potential upside to stock price is it is traded back to book value

Beijing Enterprise Consolidation of its solid waste treatment business via another HK listco

High chance 4-8% potential upside in share price

Disposal of Yanjing Brewery Low chance, but never say never 35% potential upside in share price

China Mobile Spin-off of its tower and property assets Low chance, management is conservative 33%-147% of current market cap

PetroChina Pipeline carve-out Mid-to-low chance 40-60% of current market cap

Reasonable but smaller impact

China Shenhua Asset injection from the parent High chance 16% upside on FY14E earnings Spin-off of its windpower division Mid-to-High chance Limited

CR Power Spin-off of its windpower/renewable division High chance 20% valuation upside

China Vanke It became a very good partner for other SOEs to spin-off their land assets

High chance ROE could improve from 20% to 26%

CR Land Asset injection from the parent High chance 18% increase in NAV

China Banking Sector Spin-off the credit card division of Big 5 banks Medium chance 7-12% of their market cap, @1.5-2.5x PB for credit card division

Source: Company data, Credit Suisse estimates

Extract from the Asian Daily, 15 April 2014

16 April 2014

Jump-Start 13

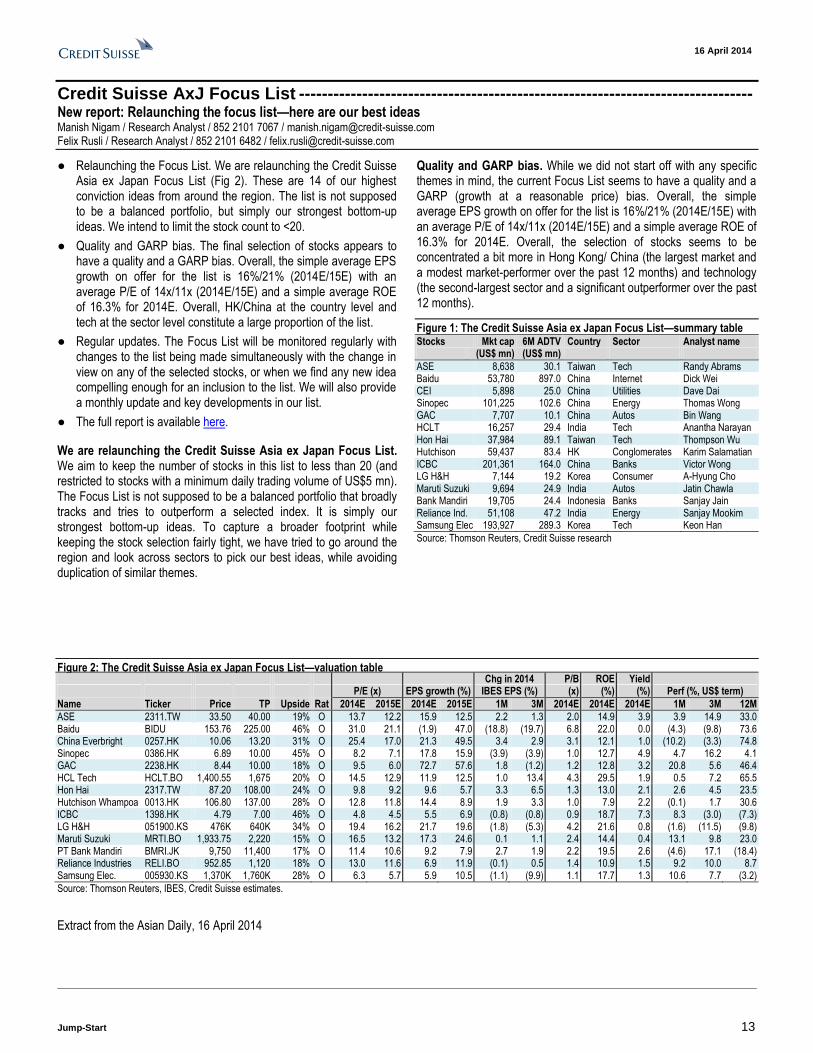

Credit Suisse AxJ Focus List ------------------------------------------------------------------------------- New report: Relaunching the focus list—here are our best ideas Manish Nigam / Research Analyst / 852 2101 7067 / [email protected] Felix Rusli / Research Analyst / 852 2101 6482 / [email protected]

● Relaunching the Focus List. We are relaunching the Credit Suisse Asia ex Japan Focus List (Fig 2). These are 14 of our highest conviction ideas from around the region. The list is not supposed to be a balanced portfolio, but simply our strongest bottom-up ideas. We intend to limit the stock count to <20.

● Quality and GARP bias. The final selection of stocks appears to have a quality and a GARP bias. Overall, the simple average EPS growth on offer for the list is 16%/21% (2014E/15E) with an average P/E of 14x/11x (2014E/15E) and a simple average ROE of 16.3% for 2014E. Overall, HK/China at the country level and tech at the sector level constitute a large proportion of the list.

● Regular updates. The Focus List will be monitored regularly with changes to the list being made simultaneously with the change in view on any of the selected stocks, or when we find any new idea compelling enough for an inclusion to the list. We will also provide a monthly update and key developments in our list.

● The full report is available here.

We are relaunching the Credit Suisse Asia ex Japan Focus List. We aim to keep the number of stocks in this list to less than 20 (and restricted to stocks with a minimum daily trading volume of US$5 mn). The Focus List is not supposed to be a balanced portfolio that broadly tracks and tries to outperform a selected index. It is simply our strongest bottom-up ideas. To capture a broader footprint while keeping the stock selection fairly tight, we have tried to go around the region and look across sectors to pick our best ideas, while avoiding duplication of similar themes.

Quality and GARP bias. While we did not start off with any specific themes in mind, the current Focus List seems to have a quality and a GARP (growth at a reasonable price) bias. Overall, the simple average EPS growth on offer for the list is 16%/21% (2014E/15E) with an average P/E of 14x/11x (2014E/15E) and a simple average ROE of 16.3% for 2014E. Overall, the selection of stocks seems to be concentrated a bit more in Hong Kong/ China (the largest market and a modest market-performer over the past 12 months) and technology (the second-largest sector and a significant outperformer over the past 12 months).

Figure 1: The Credit Suisse Asia ex Japan Focus List—summary table Stocks Mkt cap 6M ADTV Country Sector Analyst name (US$ mn) (US$ mn)

ASE 8,638 30.1 Taiwan Tech Randy Abrams Baidu 53,780 897.0 China Internet Dick Wei CEI 5,898 25.0 China Utilities Dave Dai Sinopec 101,225 102.6 China Energy Thomas Wong GAC 7,707 10.1 China Autos Bin Wang HCLT 16,257 29.4 India Tech Anantha Narayan Hon Hai 37,984 89.1 Taiwan Tech Thompson Wu Hutchison 59,437 83.4 HK Conglomerates Karim Salamatian ICBC 201,361 164.0 China Banks Victor Wong LG H&H 7,144 19.2 Korea Consumer A-Hyung Cho Maruti Suzuki 9,694 24.9 India Autos Jatin Chawla Bank Mandiri 19,705 24.4 Indonesia Banks Sanjay Jain Reliance Ind. 51,108 47.2 India Energy Sanjay Mookim Samsung Elec 193,927 289.3 Korea Tech Keon Han

Source: Thomson Reuters, Credit Suisse research

Figure 2: The Credit Suisse Asia ex Japan Focus List—valuation table Chg in 2014 P/B ROE Yield P/E (x) EPS growth (%) IBES EPS (%) (x) (%) (%) Perf (%, US$ term)

Name Ticker Price TP Upside Rat 2014E 2015E 2014E 2015E 1M 3M 2014E 2014E 2014E 1M 3M 12M

ASE 2311.TW 33.50 40.00 19% O 13.7 12.2 15.9 12.5 2.2 1.3 2.0 14.9 3.9 3.9 14.9 33.0 Baidu BIDU 153.76 225.00 46% O 31.0 21.1 (1.9) 47.0 (18.8) (19.7) 6.8 22.0 0.0 (4.3) (9.8) 73.6 China Everbright 0257.HK 10.06 13.20 31% O 25.4 17.0 21.3 49.5 3.4 2.9 3.1 12.1 1.0 (10.2) (3.3) 74.8 Sinopec 0386.HK 6.89 10.00 45% O 8.2 7.1 17.8 15.9 (3.9) (3.9) 1.0 12.7 4.9 4.7 16.2 4.1 GAC 2238.HK 8.44 10.00 18% O 9.5 6.0 72.7 57.6 1.8 (1.2) 1.2 12.8 3.2 20.8 5.6 46.4 HCL Tech HCLT.BO 1,400.55 1,675 20% O 14.5 12.9 11.9 12.5 1.0 13.4 4.3 29.5 1.9 0.5 7.2 65.5 Hon Hai 2317.TW 87.20 108.00 24% O 9.8 9.2 9.6 5.7 3.3 6.5 1.3 13.0 2.1 2.6 4.5 23.5 Hutchison Whampoa 0013.HK 106.80 137.00 28% O 12.8 11.8 14.4 8.9 1.9 3.3 1.0 7.9 2.2 (0.1) 1.7 30.6 ICBC 1398.HK 4.79 7.00 46% O 4.8 4.5 5.5 6.9 (0.8) (0.8) 0.9 18.7 7.3 8.3 (3.0) (7.3) LG H&H 051900.KS 476K 640K 34% O 19.4 16.2 21.7 19.6 (1.8) (5.3) 4.2 21.6 0.8 (1.6) (11.5) (9.8) Maruti Suzuki MRTI.BO 1,933.75 2,220 15% O 16.5 13.2 17.3 24.6 0.1 1.1 2.4 14.4 0.4 13.1 9.8 23.0 PT Bank Mandiri BMRI.JK 9,750 11,400 17% O 11.4 10.6 9.2 7.9 2.7 1.9 2.2 19.5 2.6 (4.6) 17.1 (18.4) Reliance Industries RELI.BO 952.85 1,120 18% O 13.0 11.6 6.9 11.9 (0.1) 0.5 1.4 10.9 1.5 9.2 10.0 8.7 Samsung Elec. 005930.KS 1,370K 1,760K 28% O 6.3 5.7 5.9 10.5 (1.1) (9.9) 1.1 17.7 1.3 10.6 7.7 (3.2)

Source: Thomson Reuters, IBES, Credit Suisse estimates.

Extract from the Asian Daily, 16 April 2014

16 April 2014

Jump-Start 14

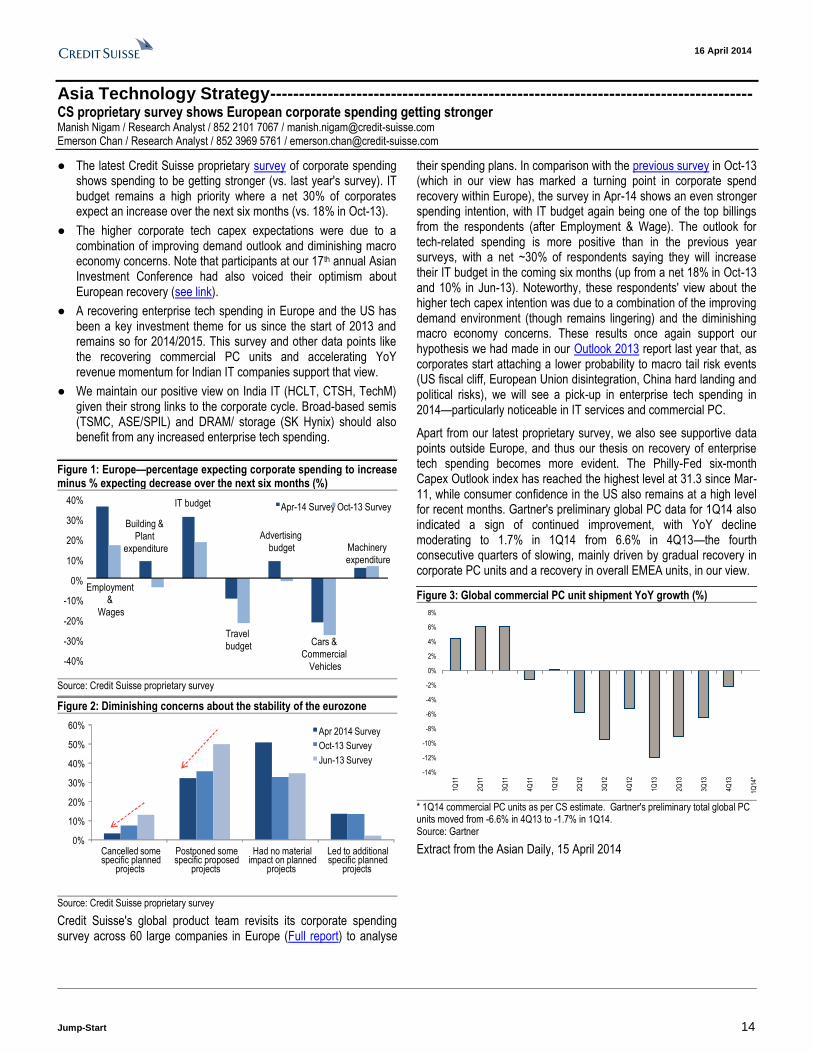

Asia Technology Strategy ------------------------------------------------------------------------------------ CS proprietary survey shows European corporate spending getting stronger Manish Nigam / Research Analyst / 852 2101 7067 / [email protected] Emerson Chan / Research Analyst / 852 3969 5761 / [email protected]

● The latest Credit Suisse proprietary survey of corporate spending shows spending to be getting stronger (vs. last year's survey). IT budget remains a high priority where a net 30% of corporates expect an increase over the next six months (vs. 18% in Oct-13).

● The higher corporate tech capex expectations were due to a combination of improving demand outlook and diminishing macro economy concerns. Note that participants at our 17th annual Asian Investment Conference had also voiced their optimism about European recovery (see link).

● A recovering enterprise tech spending in Europe and the US has been a key investment theme for us since the start of 2013 and remains so for 2014/2015. This survey and other data points like the recovering commercial PC units and accelerating YoY revenue momentum for Indian IT companies support that view.

● We maintain our positive view on India IT (HCLT, CTSH, TechM) given their strong links to the corporate cycle. Broad-based semis (TSMC, ASE/SPIL) and DRAM/ storage (SK Hynix) should also benefit from any increased enterprise tech spending.

Figure 1: Europe—percentage expecting corporate spending to increase minus % expecting decrease over the next six months (%)

Employment

&

Wages

Building &

Plant

expenditure

IT budget

Travel

budget

Advertising

budget

Cars &

Commercial

Vehicles

Machinery

expenditure

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%Apr-14 Survey Oct-13 Survey

Source: Credit Suisse proprietary survey

Figure 2: Diminishing concerns about the stability of the eurozone

0%

10%

20%

30%

40%

50%

60%

Cancelled somespecific planned

projects

Postponed somespecific proposed

projects

Had no materialimpact on planned

projects

Led to additionalspecific planned

projects

Apr 2014 Survey

Oct-13 Survey

Jun-13 Survey

Source: Credit Suisse proprietary survey

Credit Suisse's global product team revisits its corporate spending survey across 60 large companies in Europe (Full report) to analyse

their spending plans. In comparison with the previous survey in Oct-13 (which in our view has marked a turning point in corporate spend recovery within Europe), the survey in Apr-14 shows an even stronger spending intention, with IT budget again being one of the top billings from the respondents (after Employment & Wage). The outlook for tech-related spending is more positive than in the previous year surveys, with a net ~30% of respondents saying they will increase their IT budget in the coming six months (up from a net 18% in Oct-13 and 10% in Jun-13). Noteworthy, these respondents' view about the higher tech capex intention was due to a combination of the improving demand environment (though remains lingering) and the diminishing macro economy concerns. These results once again support our hypothesis we had made in our Outlook 2013 report last year that, as corporates start attaching a lower probability to macro tail risk events (US fiscal cliff, European Union disintegration, China hard landing and political risks), we will see a pick-up in enterprise tech spending in 2014—particularly noticeable in IT services and commercial PC.

Apart from our latest proprietary survey, we also see supportive data points outside Europe, and thus our thesis on recovery of enterprise tech spending becomes more evident. The Philly-Fed six-month Capex Outlook index has reached the highest level at 31.3 since Mar-11, while consumer confidence in the US also remains at a high level for recent months. Gartner's preliminary global PC data for 1Q14 also indicated a sign of continued improvement, with YoY decline moderating to 1.7% in 1Q14 from 6.6% in 4Q13—the fourth consecutive quarters of slowing, mainly driven by gradual recovery in corporate PC units and a recovery in overall EMEA units, in our view.

Figure 3: Global commercial PC unit shipment YoY growth (%)

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

*

* 1Q14 commercial PC units as per CS estimate. Gartner's preliminary total global PC units moved from -6.6% in 4Q13 to -1.7% in 1Q14. Source: Gartner

Extract from the Asian Daily, 15 April 2014

16 April 2014

Jump-Start 15

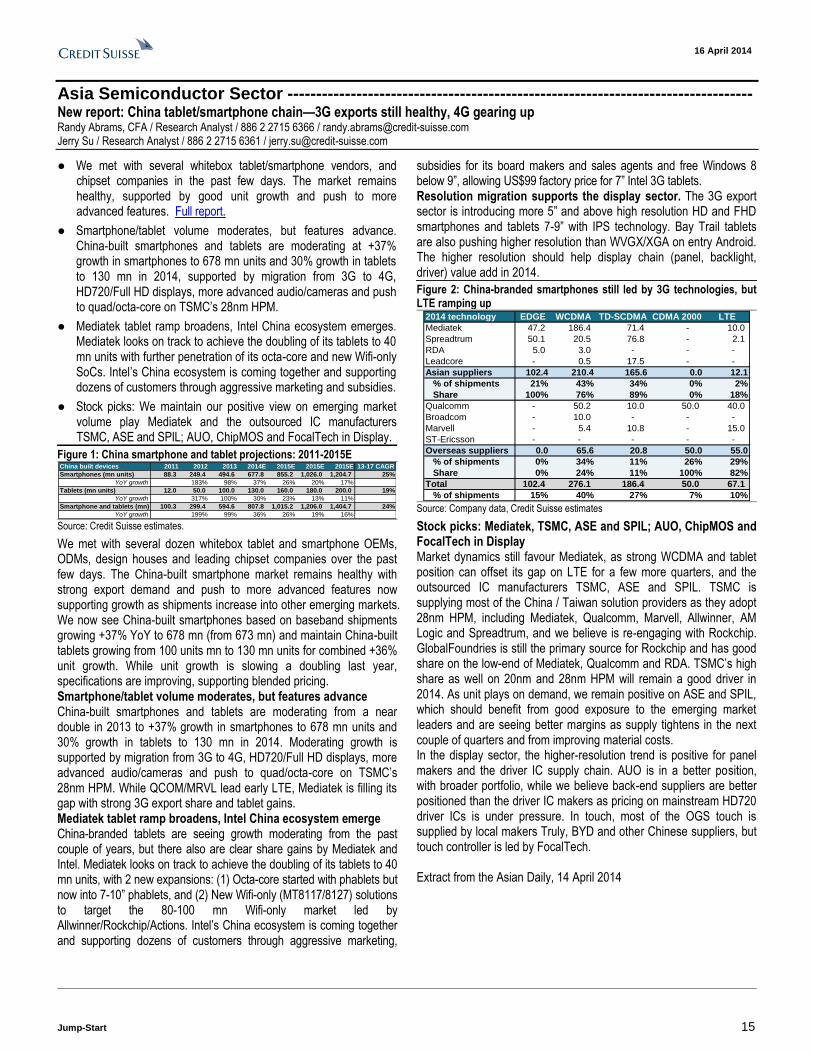

Asia Semiconductor Sector --------------------------------------------------------------------------------- New report: China tablet/smartphone chain—3G exports still healthy, 4G gearing up Randy Abrams, CFA / Research Analyst / 886 2 2715 6366 / [email protected] Jerry Su / Research Analyst / 886 2 2715 6361 / [email protected]

● We met with several whitebox tablet/smartphone vendors, and chipset companies in the past few days. The market remains healthy, supported by good unit growth and push to more advanced features. Full report.

● Smartphone/tablet volume moderates, but features advance. China-built smartphones and tablets are moderating at +37% growth in smartphones to 678 mn units and 30% growth in tablets to 130 mn in 2014, supported by migration from 3G to 4G, HD720/Full HD displays, more advanced audio/cameras and push to quad/octa-core on TSMC’s 28nm HPM.

● Mediatek tablet ramp broadens, Intel China ecosystem emerges. Mediatek looks on track to achieve the doubling of its tablets to 40 mn units with further penetration of its octa-core and new Wifi-only SoCs. Intel’s China ecosystem is coming together and supporting dozens of customers through aggressive marketing and subsidies.

● Stock picks: We maintain our positive view on emerging market volume play Mediatek and the outsourced IC manufacturers TSMC, ASE and SPIL; AUO, ChipMOS and FocalTech in Display.

Figure 1: China smartphone and tablet projections: 2011-2015E China built devices 2011 2012 2013 2014E 2015E 2015E 2015E 13-17 CAGR

Smartphones (mn units) 88.3 249.4 494.6 677.8 855.2 1,026.0 1,204.7 25%

YoY growth 183% 98% 37% 26% 20% 17%

Tablets (mn units) 12.0 50.0 100.0 130.0 160.0 180.0 200.0 19%

YoY growth 317% 100% 30% 23% 13% 11%

Smartphone and tablets (mn) 100.3 299.4 594.6 807.8 1,015.2 1,206.0 1,404.7 24%

YoY growth 199% 99% 36% 26% 19% 16% Source: Credit Suisse estimates.

We met with several dozen whitebox tablet and smartphone OEMs, ODMs, design houses and leading chipset companies over the past few days. The China-built smartphone market remains healthy with strong export demand and push to more advanced features now supporting growth as shipments increase into other emerging markets. We now see China-built smartphones based on baseband shipments growing +37% YoY to 678 mn (from 673 mn) and maintain China-built tablets growing from 100 units mn to 130 mn units for combined +36% unit growth. While unit growth is slowing a doubling last year, specifications are improving, supporting blended pricing. Smartphone/tablet volume moderates, but features advance China-built smartphones and tablets are moderating from a near double in 2013 to +37% growth in smartphones to 678 mn units and 30% growth in tablets to 130 mn in 2014. Moderating growth is supported by migration from 3G to 4G, HD720/Full HD displays, more advanced audio/cameras and push to quad/octa-core on TSMC’s 28nm HPM. While QCOM/MRVL lead early LTE, Mediatek is filling its gap with strong 3G export share and tablet gains. Mediatek tablet ramp broadens, Intel China ecosystem emerge China-branded tablets are seeing growth moderating from the past couple of years, but there also are clear share gains by Mediatek and Intel. Mediatek looks on track to achieve the doubling of its tablets to 40 mn units, with 2 new expansions: (1) Octa-core started with phablets but now into 7-10” phablets, and (2) New Wifi-only (MT8117/8127) solutions to target the 80-100 mn Wifi-only market led by Allwinner/Rockchip/Actions. Intel’s China ecosystem is coming together and supporting dozens of customers through aggressive marketing,

subsidies for its board makers and sales agents and free Windows 8 below 9”, allowing US$99 factory price for 7” Intel 3G tablets. Resolution migration supports the display sector. The 3G export sector is introducing more 5” and above high resolution HD and FHD smartphones and tablets 7-9” with IPS technology. Bay Trail tablets are also pushing higher resolution than WVGX/XGA on entry Android. The higher resolution should help display chain (panel, backlight, driver) value add in 2014.

Figure 2: China-branded smartphones still led by 3G technologies, but LTE ramping up

2014 technology EDGE WCDMA TD-SCDMA CDMA 2000 LTE

Mediatek 47.2 186.4 71.4 - 10.0

Spreadtrum 50.1 20.5 76.8 - 2.1

RDA 5.0 3.0 - - -

Leadcore - 0.5 17.5 - -

Asian suppliers 102.4 210.4 165.6 0.0 12.1

% of shipments 21% 43% 34% 0% 2%

Share 100% 76% 89% 0% 18%

Qualcomm - 50.2 10.0 50.0 40.0

Broadcom - 10.0 - - -

Marvell - 5.4 10.8 - 15.0

ST-Ericsson - - - - -

Overseas suppliers 0.0 65.6 20.8 50.0 55.0

% of shipments 0% 34% 11% 26% 29%

Share 0% 24% 11% 100% 82%

Total 102.4 276.1 186.4 50.0 67.1

% of shipments 15% 40% 27% 7% 10% Source: Company data, Credit Suisse estimates

Stock picks: Mediatek, TSMC, ASE and SPIL; AUO, ChipMOS and FocalTech in Display Market dynamics still favour Mediatek, as strong WCDMA and tablet position can offset its gap on LTE for a few more quarters, and the outsourced IC manufacturers TSMC, ASE and SPIL. TSMC is supplying most of the China / Taiwan solution providers as they adopt 28nm HPM, including Mediatek, Qualcomm, Marvell, Allwinner, AM Logic and Spreadtrum, and we believe is re-engaging with Rockchip. GlobalFoundries is still the primary source for Rockchip and has good share on the low-end of Mediatek, Qualcomm and RDA. TSMC’s high share as well on 20nm and 28nm HPM will remain a good driver in 2014. As unit plays on demand, we remain positive on ASE and SPIL, which should benefit from good exposure to the emerging market leaders and are seeing better margins as supply tightens in the next couple of quarters and from improving material costs. In the display sector, the higher-resolution trend is positive for panel makers and the driver IC supply chain. AUO is in a better position, with broader portfolio, while we believe back-end suppliers are better positioned than the driver IC makers as pricing on mainstream HD720 driver ICs is under pressure. In touch, most of the OGS touch is supplied by local makers Truly, BYD and other Chinese suppliers, but touch controller is led by FocalTech. Extract from the Asian Daily, 14 April 2014

16 April 2014

Jump-Start 16

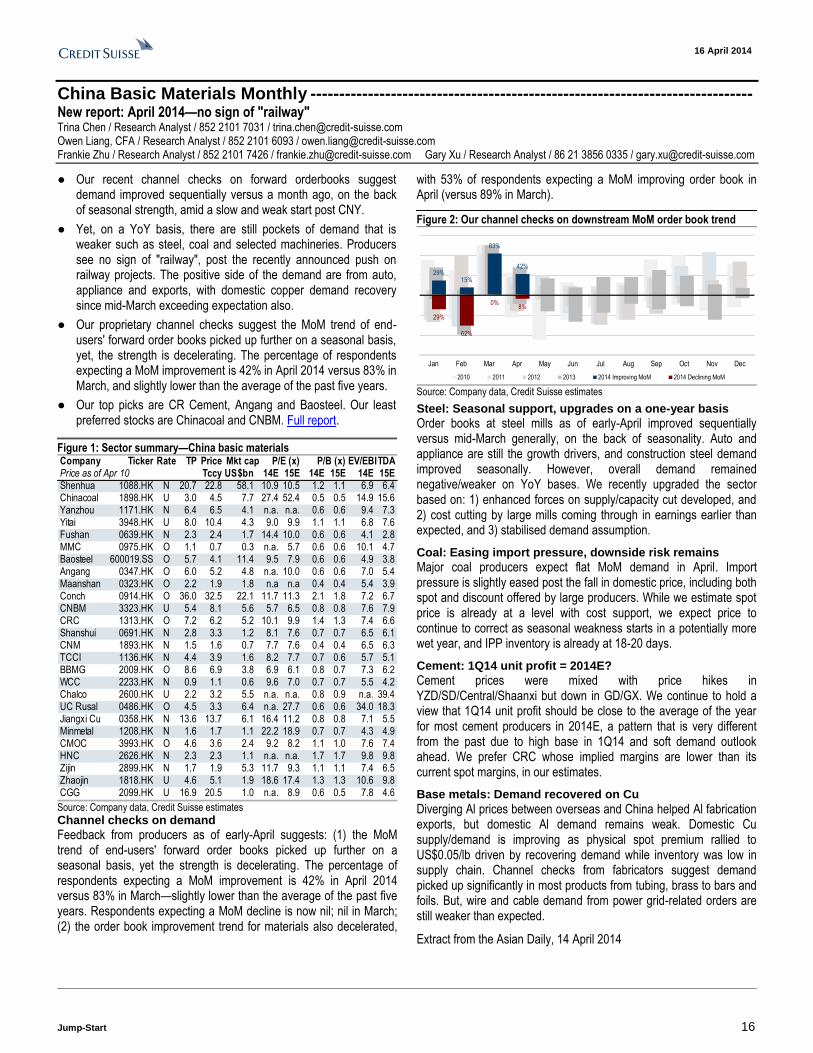

China Basic Materials Monthly ----------------------------------------------------------------------------- New report: April 2014—no sign of "railway" Trina Chen / Research Analyst / 852 2101 7031 / [email protected] Owen Liang, CFA / Research Analyst / 852 2101 6093 / [email protected] Frankie Zhu / Research Analyst / 852 2101 7426 / [email protected] Gary Xu / Research Analyst / 86 21 3856 0335 / [email protected]

● Our recent channel checks on forward orderbooks suggest demand improved sequentially versus a month ago, on the back of seasonal strength, amid a slow and weak start post CNY.

● Yet, on a YoY basis, there are still pockets of demand that is weaker such as steel, coal and selected machineries. Producers see no sign of "railway", post the recently announced push on railway projects. The positive side of the demand are from auto, appliance and exports, with domestic copper demand recovery since mid-March exceeding expectation also.

● Our proprietary channel checks suggest the MoM trend of end-users' forward order books picked up further on a seasonal basis, yet, the strength is decelerating. The percentage of respondents expecting a MoM improvement is 42% in April 2014 versus 83% in March, and slightly lower than the average of the past five years.

● Our top picks are CR Cement, Angang and Baosteel. Our least preferred stocks are Chinacoal and CNBM. Full report.

Figure 1: Sector summary—China basic materials Company Ticker Rate TP Price Mkt cap P/E (x) P/B (x) EV/EBITDAPrice as of Apr 10 Tccy US$bn 14E 15E 14E 15E 14E 15EShenhua 1088.HK N 20.7 22.8 58.1 10.9 10.5 1.2 1.1 6.9 6.4Chinacoal 1898.HK U 3.0 4.5 7.7 27.4 52.4 0.5 0.5 14.9 15.6Yanzhou 1171.HK N 6.4 6.5 4.1 n.a. n.a. 0.6 0.6 9.4 7.3Yitai 3948.HK U 8.0 10.4 4.3 9.0 9.9 1.1 1.1 6.8 7.6Fushan 0639.HK N 2.3 2.4 1.7 14.4 10.0 0.6 0.6 4.1 2.8MMC 0975.HK O 1.1 0.7 0.3 n.a. 5.7 0.6 0.6 10.1 4.7Baosteel 600019.SS O 5.7 4.1 11.4 9.5 7.9 0.6 0.6 4.9 3.8Angang 0347.HK O 6.0 5.2 4.8 n.a. 10.0 0.6 0.6 7.0 5.4Maanshan 0323.HK O 2.2 1.9 1.8 n.a n.a 0.4 0.4 5.4 3.9Conch 0914.HK O 36.0 32.5 22.1 11.7 11.3 2.1 1.8 7.2 6.7CNBM 3323.HK U 5.4 8.1 5.6 5.7 6.5 0.8 0.8 7.6 7.9CRC 1313.HK O 7.2 6.2 5.2 10.1 9.9 1.4 1.3 7.4 6.6Shanshui 0691.HK N 2.8 3.3 1.2 8.1 7.6 0.7 0.7 6.5 6.1CNM 1893.HK N 1.5 1.6 0.7 7.7 7.6 0.4 0.4 6.5 6.3TCCI 1136.HK N 4.4 3.9 1.6 8.2 7.7 0.7 0.6 5.7 5.1BBMG 2009.HK O 8.6 6.9 3.8 6.9 6.1 0.8 0.7 7.3 6.2WCC 2233.HK N 0.9 1.1 0.6 9.6 7.0 0.7 0.7 5.5 4.2Chalco 2600.HK U 2.2 3.2 5.5 n.a. n.a. 0.8 0.9 n.a. 39.4UC Rusal 0486.HK O 4.5 3.3 6.4 n.a. 27.7 0.6 0.6 34.0 18.3Jiangxi Cu 0358.HK N 13.6 13.7 6.1 16.4 11.2 0.8 0.8 7.1 5.5Minmetal 1208.HK N 1.6 1.7 1.1 22.2 18.9 0.7 0.7 4.3 4.9CMOC 3993.HK O 4.6 3.6 2.4 9.2 8.2 1.1 1.0 7.6 7.4HNC 2626.HK N 2.3 2.3 1.1 n.a. n.a. 1.7 1.7 9.8 9.8Zijin 2899.HK N 1.7 1.9 5.3 11.7 9.3 1.1 1.1 7.4 6.5Zhaojin 1818.HK U 4.6 5.1 1.9 18.6 17.4 1.3 1.3 10.6 9.8CGG 2099.HK U 16.9 20.5 1.0 n.a. 8.9 0.6 0.5 7.8 4.6

Source: Company data, Credit Suisse estimates

Channel checks on demand

Feedback from producers as of early-April suggests: (1) the MoM trend of end-users' forward order books picked up further on a seasonal basis, yet the strength is decelerating. The percentage of respondents expecting a MoM improvement is 42% in April 2014 versus 83% in March—slightly lower than the average of the past five years. Respondents expecting a MoM decline is now nil; nil in March; (2) the order book improvement trend for materials also decelerated,

with 53% of respondents expecting a MoM improving order book in April (versus 89% in March).

Figure 2: Our channel checks on downstream MoM order book trend

29%15%

83%

42%

29%

62%

0%8%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2010 2011 2012 2013 2014 Improving MoM 2014 Declining MoM

Source: Company data, Credit Suisse estimates

Steel: Seasonal support, upgrades on a one-year basis

Order books at steel mills as of early-April improved sequentially versus mid-March generally, on the back of seasonality. Auto and appliance are still the growth drivers, and construction steel demand improved seasonally. However, overall demand remained negative/weaker on YoY bases. We recently upgraded the sector based on: 1) enhanced forces on supply/capacity cut developed, and 2) cost cutting by large mills coming through in earnings earlier than expected, and 3) stabilised demand assumption.

Coal: Easing import pressure, downside risk remains

Major coal producers expect flat MoM demand in April. Import pressure is slightly eased post the fall in domestic price, including both spot and discount offered by large producers. While we estimate spot price is already at a level with cost support, we expect price to continue to correct as seasonal weakness starts in a potentially more wet year, and IPP inventory is already at 18-20 days.

Cement: 1Q14 unit profit = 2014E?

Cement prices were mixed with price hikes in YZD/SD/Central/Shaanxi but down in GD/GX. We continue to hold a view that 1Q14 unit profit should be close to the average of the year for most cement producers in 2014E, a pattern that is very different from the past due to high base in 1Q14 and soft demand outlook ahead. We prefer CRC whose implied margins are lower than its current spot margins, in our estimates.

Base metals: Demand recovered on Cu

Diverging Al prices between overseas and China helped Al fabrication exports, but domestic Al demand remains weak. Domestic Cu supply/demand is improving as physical spot premium rallied to US$0.05/lb driven by recovering demand while inventory was low in supply chain. Channel checks from fabricators suggest demand picked up significantly in most products from tubing, brass to bars and foils. But, wire and cable demand from power grid-related orders are still weaker than expected.

Extract from the Asian Daily, 14 April 2014

16 April 2014

Jump-Start 17

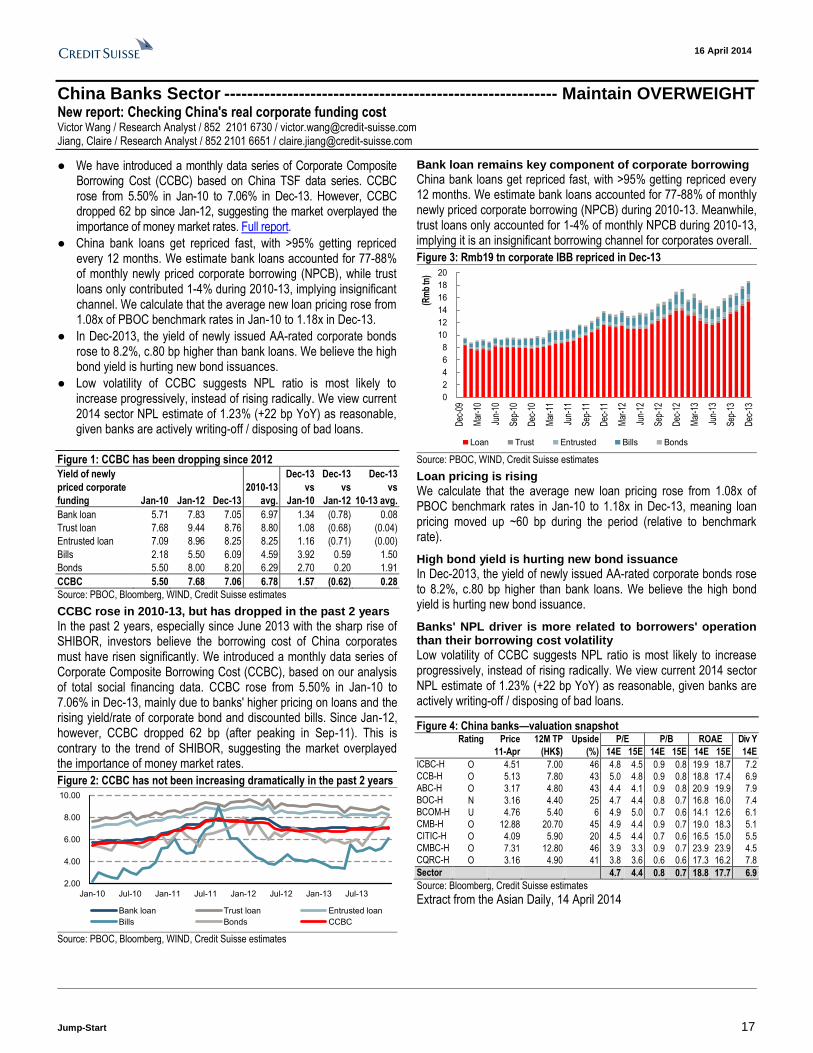

China Banks Sector ---------------------------------------------------------- Maintain OVERWEIGHT New report: Checking China's real corporate funding cost Victor Wang / Research Analyst / 852 2101 6730 / [email protected] Jiang, Claire / Research Analyst / 852 2101 6651 / [email protected]

● We have introduced a monthly data series of Corporate Composite Borrowing Cost (CCBC) based on China TSF data series. CCBC rose from 5.50% in Jan-10 to 7.06% in Dec-13. However, CCBC dropped 62 bp since Jan-12, suggesting the market overplayed the importance of money market rates. Full report.

● China bank loans get repriced fast, with >95% getting repriced every 12 months. We estimate bank loans accounted for 77-88% of monthly newly priced corporate borrowing (NPCB), while trust loans only contributed 1-4% during 2010-13, implying insignificant channel. We calculate that the average new loan pricing rose from 1.08x of PBOC benchmark rates in Jan-10 to 1.18x in Dec-13.

● In Dec-2013, the yield of newly issued AA-rated corporate bonds rose to 8.2%, c.80 bp higher than bank loans. We believe the high bond yield is hurting new bond issuances.

● Low volatility of CCBC suggests NPL ratio is most likely to increase progressively, instead of rising radically. We view current 2014 sector NPL estimate of 1.23% (+22 bp YoY) as reasonable, given banks are actively writing-off / disposing of bad loans.

Figure 1: CCBC has been dropping since 2012

Yield of newly Dec-13 Dec-13 Dec-13

priced corporate 2010-13 vs vs vs

funding Jan-10 Jan-12 Dec-13 avg. Jan-10 Jan-12 10-13 avg.

Bank loan 5.71 7.83 7.05 6.97 1.34 (0.78) 0.08

Trust loan 7.68 9.44 8.76 8.80 1.08 (0.68) (0.04)

Entrusted loan 7.09 8.96 8.25 8.25 1.16 (0.71) (0.00)

Bills 2.18 5.50 6.09 4.59 3.92 0.59 1.50

Bonds 5.50 8.00 8.20 6.29 2.70 0.20 1.91

CCBC 5.50 7.68 7.06 6.78 1.57 (0.62) 0.28

Source: PBOC, Bloomberg, WIND, Credit Suisse estimates

CCBC rose in 2010-13, but has dropped in the past 2 years

In the past 2 years, especially since June 2013 with the sharp rise of SHIBOR, investors believe the borrowing cost of China corporates must have risen significantly. We introduced a monthly data series of Corporate Composite Borrowing Cost (CCBC), based on our analysis of total social financing data. CCBC rose from 5.50% in Jan-10 to 7.06% in Dec-13, mainly due to banks' higher pricing on loans and the rising yield/rate of corporate bond and discounted bills. Since Jan-12, however, CCBC dropped 62 bp (after peaking in Sep-11). This is contrary to the trend of SHIBOR, suggesting the market overplayed the importance of money market rates.

Figure 2: CCBC has not been increasing dramatically in the past 2 years

2.00

4.00

6.00

8.00

10.00

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13

Bank loan Trust loan Entrusted loan

Bills Bonds CCBC

Source: PBOC, Bloomberg, WIND, Credit Suisse estimates

Bank loan remains key component of corporate borrowing

China bank loans get repriced fast, with >95% getting repriced every 12 months. We estimate bank loans accounted for 77-88% of monthly newly priced corporate borrowing (NPCB) during 2010-13. Meanwhile, trust loans only accounted for 1-4% of monthly NPCB during 2010-13, implying it is an insignificant borrowing channel for corporates overall.

Figure 3: Rmb19 tn corporate IBB repriced in Dec-13

0

2

4

6

8

10

12

14

16

18

20

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

(Rm

b tn

)

Loan Trust Entrusted Bills Bonds

Source: PBOC, WIND, Credit Suisse estimates

Loan pricing is rising

We calculate that the average new loan pricing rose from 1.08x of PBOC benchmark rates in Jan-10 to 1.18x in Dec-13, meaning loan pricing moved up ~60 bp during the period (relative to benchmark rate).

High bond yield is hurting new bond issuance

In Dec-2013, the yield of newly issued AA-rated corporate bonds rose to 8.2%, c.80 bp higher than bank loans. We believe the high bond yield is hurting new bond issuance.

Banks' NPL driver is more related to borrowers' operation than their borrowing cost volatility

Low volatility of CCBC suggests NPL ratio is most likely to increase progressively, instead of rising radically. We view current 2014 sector NPL estimate of 1.23% (+22 bp YoY) as reasonable, given banks are actively writing-off / disposing of bad loans.

Figure 4: China banks—valuation snapshot Rating Price 12M TP Upside P/E P/B ROAE Div Y

11-Apr (HK$) (%) 14E 15E 14E 15E 14E 15E 14E

ICBC-H O 4.51 7.00 46 4.8 4.5 0.9 0.8 19.9 18.7 7.2 CCB-H O 5.13 7.80 43 5.0 4.8 0.9 0.8 18.8 17.4 6.9 ABC-H O 3.17 4.80 43 4.4 4.1 0.9 0.8 20.9 19.9 7.9 BOC-H N 3.16 4.40 25 4.7 4.4 0.8 0.7 16.8 16.0 7.4 BCOM-H U 4.76 5.40 6 4.9 5.0 0.7 0.6 14.1 12.6 6.1 CMB-H O 12.88 20.70 45 4.9 4.4 0.9 0.7 19.0 18.3 5.1 CITIC-H O 4.09 5.90 20 4.5 4.4 0.7 0.6 16.5 15.0 5.5 CMBC-H O 7.31 12.80 46 3.9 3.3 0.9 0.7 23.9 23.9 4.5 CQRC-H O 3.16 4.90 41 3.8 3.6 0.6 0.6 17.3 16.2 7.8

Sector 4.7 4.4 0.8 0.7 18.8 17.7 6.9

Source: Bloomberg, Credit Suisse estimates

Extract from the Asian Daily, 14 April 2014

16 April 2014

Jump-Start 18

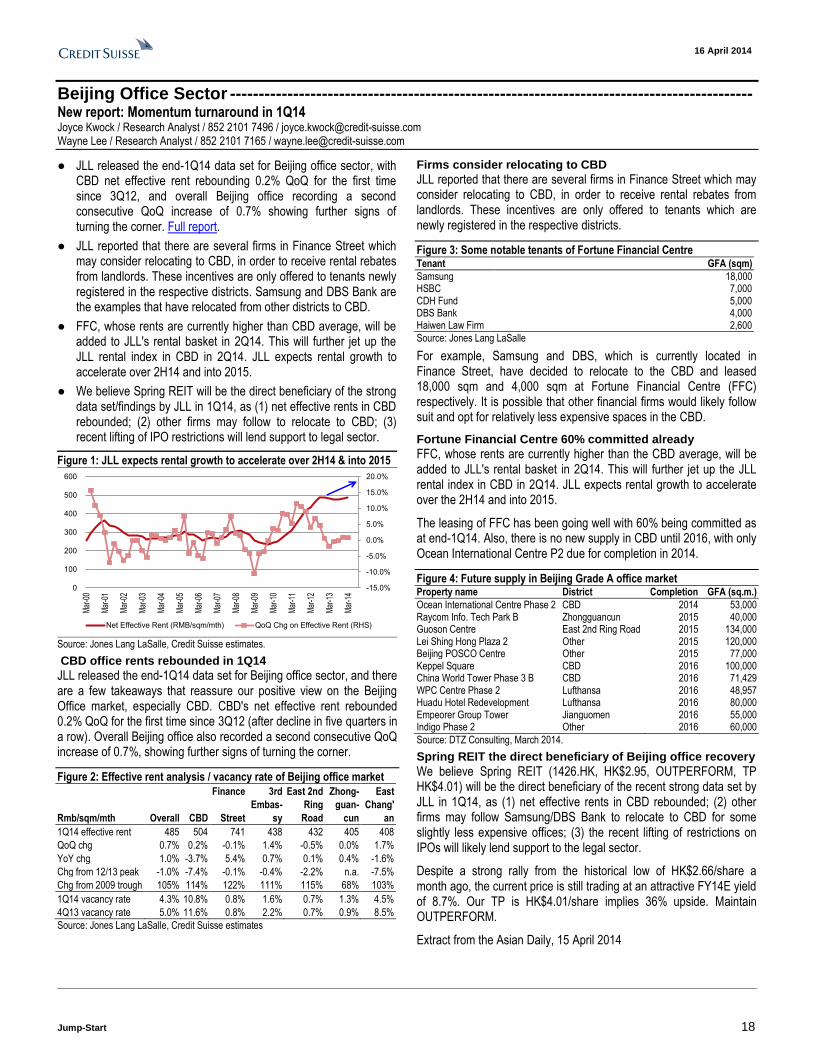

Beijing Office Sector ------------------------------------------------------------------------------------------- New report: Momentum turnaround in 1Q14 Joyce Kwock / Research Analyst / 852 2101 7496 / [email protected] Wayne Lee / Research Analyst / 852 2101 7165 / [email protected]

● JLL released the end-1Q14 data set for Beijing office sector, with CBD net effective rent rebounding 0.2% QoQ for the first time since 3Q12, and overall Beijing office recording a second consecutive QoQ increase of 0.7% showing further signs of turning the corner. Full report.

● JLL reported that there are several firms in Finance Street which may consider relocating to CBD, in order to receive rental rebates from landlords. These incentives are only offered to tenants newly registered in the respective districts. Samsung and DBS Bank are the examples that have relocated from other districts to CBD.

● FFC, whose rents are currently higher than CBD average, will be added to JLL's rental basket in 2Q14. This will further jet up the JLL rental index in CBD in 2Q14. JLL expects rental growth to accelerate over 2H14 and into 2015.

● We believe Spring REIT will be the direct beneficiary of the strong data set/findings by JLL in 1Q14, as (1) net effective rents in CBD rebounded; (2) other firms may follow to relocate to CBD; (3) recent lifting of IPO restrictions will lend support to legal sector.

Figure 1: JLL expects rental growth to accelerate over 2H14 & into 2015

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

0

100

200

300

400

500

600

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Net Effective Rent (RMB/sqm/mth) QoQ Chg on Effective Rent (RHS)

Source: Jones Lang LaSalle, Credit Suisse estimates.

CBD office rents rebounded in 1Q14

JLL released the end-1Q14 data set for Beijing office sector, and there are a few takeaways that reassure our positive view on the Beijing Office market, especially CBD. CBD's net effective rent rebounded 0.2% QoQ for the first time since 3Q12 (after decline in five quarters in a row). Overall Beijing office also recorded a second consecutive QoQ increase of 0.7%, showing further signs of turning the corner.

Figure 2: Effective rent analysis / vacancy rate of Beijing office market

Finance 3rd East 2nd Zhong- East

Embas- Ring guan- Chang'

Rmb/sqm/mth Overall CBD Street sy Road cun an

1Q14 effective rent 485 504 741 438 432 405 408

QoQ chg 0.7% 0.2% -0.1% 1.4% -0.5% 0.0% 1.7%

YoY chg 1.0% -3.7% 5.4% 0.7% 0.1% 0.4% -1.6%

Chg from 12/13 peak -1.0% -7.4% -0.1% -0.4% -2.2% n.a. -7.5%

Chg from 2009 trough 105% 114% 122% 111% 115% 68% 103%

1Q14 vacancy rate 4.3% 10.8% 0.8% 1.6% 0.7% 1.3% 4.5%

4Q13 vacancy rate 5.0% 11.6% 0.8% 2.2% 0.7% 0.9% 8.5%

Source: Jones Lang LaSalle, Credit Suisse estimates

Firms consider relocating to CBD

JLL reported that there are several firms in Finance Street which may consider relocating to CBD, in order to receive rental rebates from landlords. These incentives are only offered to tenants which are newly registered in the respective districts.

Figure 3: Some notable tenants of Fortune Financial Centre Tenant GFA (sqm)

Samsung 18,000 HSBC 7,000 CDH Fund 5,000 DBS Bank 4,000 Haiwen Law Firm 2,600

Source: Jones Lang LaSalle

For example, Samsung and DBS, which is currently located in Finance Street, have decided to relocate to the CBD and leased 18,000 sqm and 4,000 sqm at Fortune Financial Centre (FFC) respectively. It is possible that other financial firms would likely follow suit and opt for relatively less expensive spaces in the CBD.

Fortune Financial Centre 60% committed already

FFC, whose rents are currently higher than the CBD average, will be added to JLL's rental basket in 2Q14. This will further jet up the JLL rental index in CBD in 2Q14. JLL expects rental growth to accelerate over the 2H14 and into 2015.

The leasing of FFC has been going well with 60% being committed as at end-1Q14. Also, there is no new supply in CBD until 2016, with only Ocean International Centre P2 due for completion in 2014.

Figure 4: Future supply in Beijing Grade A office market Property name District Completion GFA (sq.m.)

Ocean International Centre Phase 2 CBD 2014 53,000 Raycom Info. Tech Park B Zhongguancun 2015 40,000 Guoson Centre East 2nd Ring Road 2015 134,000 Lei Shing Hong Plaza 2 Other 2015 120,000 Beijing POSCO Centre Other 2015 77,000 Keppel Square CBD 2016 100,000 China World Tower Phase 3 B CBD 2016 71,429 WPC Centre Phase 2 Lufthansa 2016 48,957 Huadu Hotel Redevelopment Lufthansa 2016 80,000 Empeorer Group Tower Jianguomen 2016 55,000 Indigo Phase 2 Other 2016 60,000

Source: DTZ Consulting, March 2014.

Spring REIT the direct beneficiary of Beijing office recovery

We believe Spring REIT (1426.HK, HK$2.95, OUTPERFORM, TP HK$4.01) will be the direct beneficiary of the recent strong data set by JLL in 1Q14, as (1) net effective rents in CBD rebounded; (2) other firms may follow Samsung/DBS Bank to relocate to CBD for some slightly less expensive offices; (3) the recent lifting of restrictions on IPOs will likely lend support to the legal sector.

Despite a strong rally from the historical low of HK$2.66/share a month ago, the current price is still trading at an attractive FY14E yield of 8.7%. Our TP is HK$4.01/share implies 36% upside. Maintain OUTPERFORM.

Extract from the Asian Daily, 15 April 2014

16 April 2014

Jump-Start 19

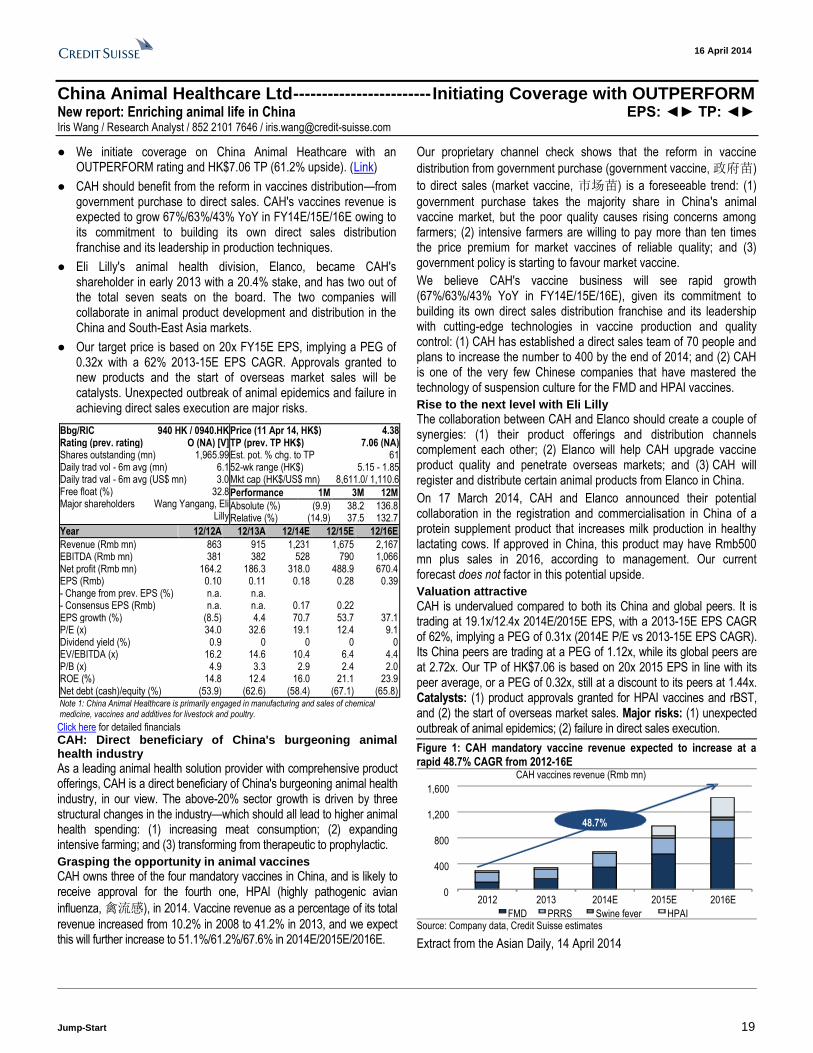

China Animal Healthcare Ltd ------------------------ Initiating Coverage with OUTPERFORM New report: Enriching animal life in China EPS: ◄► TP: ◄► Iris Wang / Research Analyst / 852 2101 7646 / [email protected]

● We initiate coverage on China Animal Heathcare with an OUTPERFORM rating and HK$7.06 TP (61.2% upside). (Link)

● CAH should benefit from the reform in vaccines distribution—from government purchase to direct sales. CAH's vaccines revenue is expected to grow 67%/63%/43% YoY in FY14E/15E/16E owing to its commitment to building its own direct sales distribution franchise and its leadership in production techniques.

● Eli Lilly's animal health division, Elanco, became CAH's shareholder in early 2013 with a 20.4% stake, and has two out of the total seven seats on the board. The two companies will collaborate in animal product development and distribution in the China and South-East Asia markets.

● Our target price is based on 20x FY15E EPS, implying a PEG of 0.32x with a 62% 2013-15E EPS CAGR. Approvals granted to new products and the start of overseas market sales will be catalysts. Unexpected outbreak of animal epidemics and failure in achieving direct sales execution are major risks.

Click here for detailed financials

CAH: Direct beneficiary of China's burgeoning animal health industry

As a leading animal health solution provider with comprehensive product offerings, CAH is a direct beneficiary of China's burgeoning animal health industry, in our view. The above-20% sector growth is driven by three structural changes in the industry—which should all lead to higher animal health spending: (1) increasing meat consumption; (2) expanding intensive farming; and (3) transforming from therapeutic to prophylactic.

Grasping the opportunity in animal vaccines

CAH owns three of the four mandatory vaccines in China, and is likely to receive approval for the fourth one, HPAI (highly pathogenic avian

influenza, 禽流感), in 2014. Vaccine revenue as a percentage of its total

revenue increased from 10.2% in 2008 to 41.2% in 2013, and we expect this will further increase to 51.1%/61.2%/67.6% in 2014E/2015E/2016E.

Our proprietary channel check shows that the reform in vaccine

distribution from government purchase (government vaccine, 政府苗)

to direct sales (market vaccine, 市场苗) is a foreseeable trend: (1)

government purchase takes the majority share in China's animal vaccine market, but the poor quality causes rising concerns among farmers; (2) intensive farmers are willing to pay more than ten times the price premium for market vaccines of reliable quality; and (3) government policy is starting to favour market vaccine.

We believe CAH's vaccine business will see rapid growth (67%/63%/43% YoY in FY14E/15E/16E), given its commitment to building its own direct sales distribution franchise and its leadership with cutting-edge technologies in vaccine production and quality control: (1) CAH has established a direct sales team of 70 people and plans to increase the number to 400 by the end of 2014; and (2) CAH is one of the very few Chinese companies that have mastered the technology of suspension culture for the FMD and HPAI vaccines.

Rise to the next level with Eli Lilly

The collaboration between CAH and Elanco should create a couple of synergies: (1) their product offerings and distribution channels complement each other; (2) Elanco will help CAH upgrade vaccine product quality and penetrate overseas markets; and (3) CAH will register and distribute certain animal products from Elanco in China.

On 17 March 2014, CAH and Elanco announced their potential collaboration in the registration and commercialisation in China of a protein supplement product that increases milk production in healthy lactating cows. If approved in China, this product may have Rmb500 mn plus sales in 2016, according to management. Our current forecast does not factor in this potential upside.

Valuation attractive

CAH is undervalued compared to both its China and global peers. It is trading at 19.1x/12.4x 2014E/2015E EPS, with a 2013-15E EPS CAGR of 62%, implying a PEG of 0.31x (2014E P/E vs 2013-15E EPS CAGR). Its China peers are trading at a PEG of 1.12x, while its global peers are at 2.72x. Our TP of HK$7.06 is based on 20x 2015 EPS in line with its peer average, or a PEG of 0.32x, still at a discount to its peers at 1.44x. Catalysts: (1) product approvals granted for HPAI vaccines and rBST, and (2) the start of overseas market sales. Major risks: (1) unexpected outbreak of animal epidemics; (2) failure in direct sales execution.

Figure 1: CAH mandatory vaccine revenue expected to increase at a rapid 48.7% CAGR from 2012-16E

0

400

800

1,200

1,600

2012 2013 2014E 2015E 2016E

CAH vaccines revenue (Rmb mn)

FMD PRRS Swine fever HPAI

48.7%

Source: Company data, Credit Suisse estimates

Extract from the Asian Daily, 14 April 2014