Embed Size (px)

Citation preview

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION™

Client-Driven Solutions, Insights, and Access

13 June 2013

Asia Pacific

Equity Research

Investment Strategy

Jump-Start STRATEGY

Jump-Start aims to provide you with a summary of the week that was and helps you prepare

for the week ahead with a results calendar, economic forecasts and valuation summaries.

TIPS—Buying opportunity or mean reversion? With the TIPs falling by at least 15% in USD

terms from their recent highs, investors may consider this a buying opportunity. But, Sakthi Siva

argues, it is not a buying opportunity and instead mean reversion is starting. The P/B gap

between the three most undervalued markets (China, Korea, Hong Kong) and the three most

overvalued (TIPs) is the biggest since 2007. In 2007, the gap between the two cheapest and two

most overvalued narrowed from a low of -54% to -37% within six months. Thus, the gap could

narrow from the current -57%. Sakthi believes the recent rise in bond yields, currency weakness

and lower EPS revisions could act as catalysts for this mean reversion. Of the three most

undervalued markets, Korea looks the most attractive with P/B close to the last two troughs,

underowned by foreign investors, and yen and EPS revisions stabilising. Full reports

China coal—Finding a floor: It is déjà vu of 2Q12, according to Trina Chen—weak demand,

strong hydro and rising imports. Trina estimates it would take a demand growth acceleration of 6-

7% from the current level for the coastal coal market to move back to balance; optimistic, based

on the macro outlook. Nevertheless, she believes the spot coal price in China has mostly floored,

given 15-30% of production is already at loss in our estimates, due to low calorific value, or high

cost. Our stress test suggests ROE versus P/B is more attractive for Shenhua, but negative for

Yanzhou, Yitai and MMC. Our top picks are: Shenhua for thermal and Fushan for met coal. We

downgrade both Chinacoal and Yitai to NEUTRAL (from Outperform). Full report.

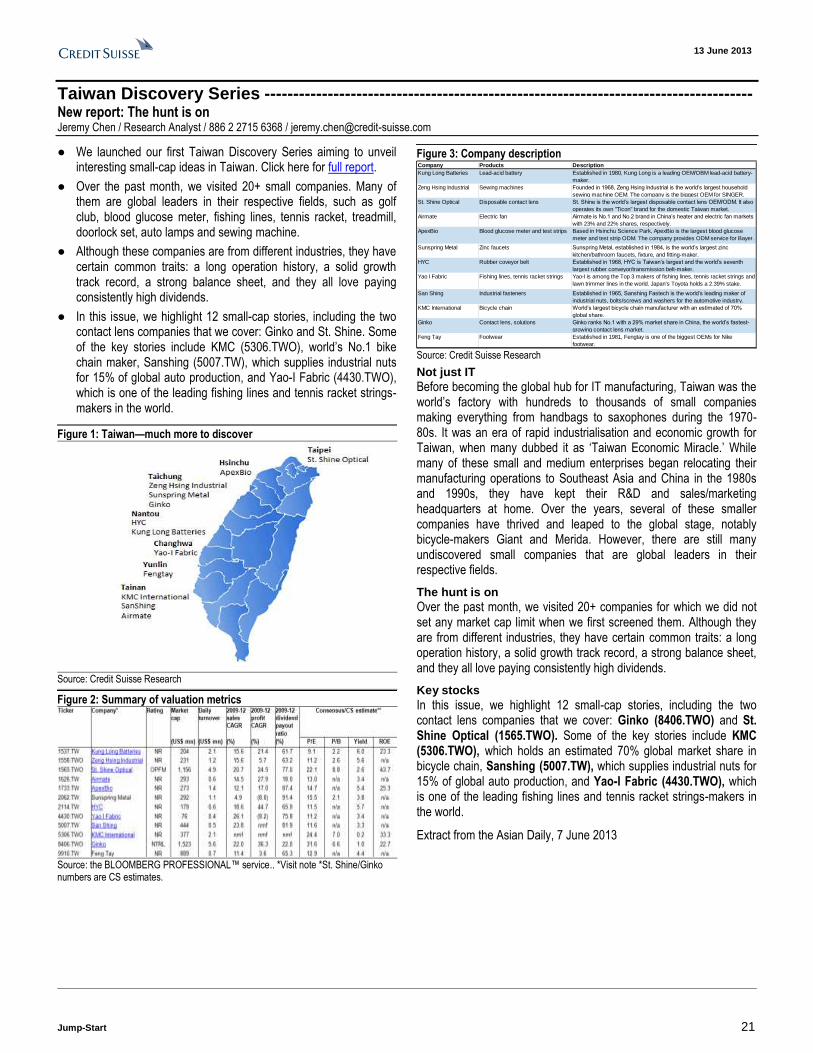

Taiwan Discovery Series—The hunt is on: Our first Taiwan Discovery Series aims to unveil

interesting small-cap ideas in Taiwan. Last month, we visited 20+ small companies, many global

leaders in their respective fields. Although from different industries, they have certain common

traits: long operation history, solid growth track record, strong balance sheet, and consistently

high dividends. Here, we highlight 12 small-cap stories, including two companies we cover: Ginko

and St. Shine. Key stories: KMC (world’s No.1 bike chain maker); Sanshing (supplies industrial

nuts for 15% of global auto production); and Yao-I Fabric (leading fishing line and tennis racket

string-maker globally). Full report

Must-read recently published reports

1) APAC E-Commerce Primer – An evolutionary force (28/5)

Karim P. Salamatian

E-commerce in emerging Asia is an integral evolutionary force behind consumption and retail sales growth; China will emerge as the largest e-commerce market globally by 2013

2) India Market Strategy – INR: Currency crisis? Unlikely for now (22/4)

Neelkanth Mishra

Neelkanth Mishra argues that at least the pressure on INR is changing. Medium-term risks aside, a “crisis” is not imminent

3) Research Institute – Credit Suisse Global Investment Returns Yearbook 2013

Andrew Garthwaite

CS examines how stocks and bonds perform in a world of resurgency in investor risk appetite and might soon see inflation expectations rise.

4) Asia Emerging Consumer Survey 2013: Confidence revival (23/1)

Karim P. Salamatian

Asian consumers show the strongest confidence momentum. Superior return potential in discretionary, brand-driven ideas

5) China Market Strategy: The worst is probably over (16/10)

Vincent Chan

Economy may have bottomed out. Valuations back to 2008 levels. Add beta.

6) APAC: Consumption S curve: Winners & losers as Asian consumers evolve (6/8)

Karim P. Salamatian

A unique report as it is perhaps the first time that country-by-country S curves for consumption have been constructed.

Research Analyst

Jahanzeb Naseer

852 2101 6554

Credit Suisse forthcoming events

Hong Kong

China/Hong Kong Emerging Corporate Day

Date 19 June, Hong Kong

Coverage Analyst Kenny Lau

CESC Ltd (CESC.BO)

Date 24 June, Hong Kong

Coverage Analyst Amish Shah

APAC Transport Corporate Day

Date 26 June, Hong Kong

Coverage Analyst Timothy Ross

21 Vianet Group Inc (VNET.O)

Date 11-12 July, Hong Kong

Coverage Analyst Colin McCallum

Singapore

Skyworth Digital (0751.HK)

Date 03-05 July, Singapore

Coverage Analyst Kenny Lau

21 Vianet Group Inc (VNET.O)

Date 10 July, Hong Kong

Coverage Analyst Colin McCallum

US

HDFC Bank (HDBK.BO)

Date 17-21 June, US

Coverage Analyst Ashish Gupta

Charoen Pokphand Foods Public (CPF.BK)

Date 9-15 July, US

Coverage Analyst Chai Techakumpuch

Europe

Reserve Bank of India

Date 14 June, London

Coverage Analyst Ashish Gupta

China Life Taiwan (2823.TW)

Date 17-21 June, Europe

Coverage Analyst Chung Hsu

Wharf Holdings (004.HK)

Date 17-21 June, Europe

Coverage Analyst Cusson Leung

Skyworth Digital (0751.HK)

Date 08-12 July, London

Coverage Analyst Kenny Lau

Others

Credit Suisse Asian Technology Conference

Date 11-13 September, Taiwan

Coverage Analyst Manish Nigam

Asian Investment Conference 2014

Date 24-28 March, Hong Kong

Contact [email protected] or your usual sales representative

13 u

ne 2

013

Ju

mp

-Sta

rt 2

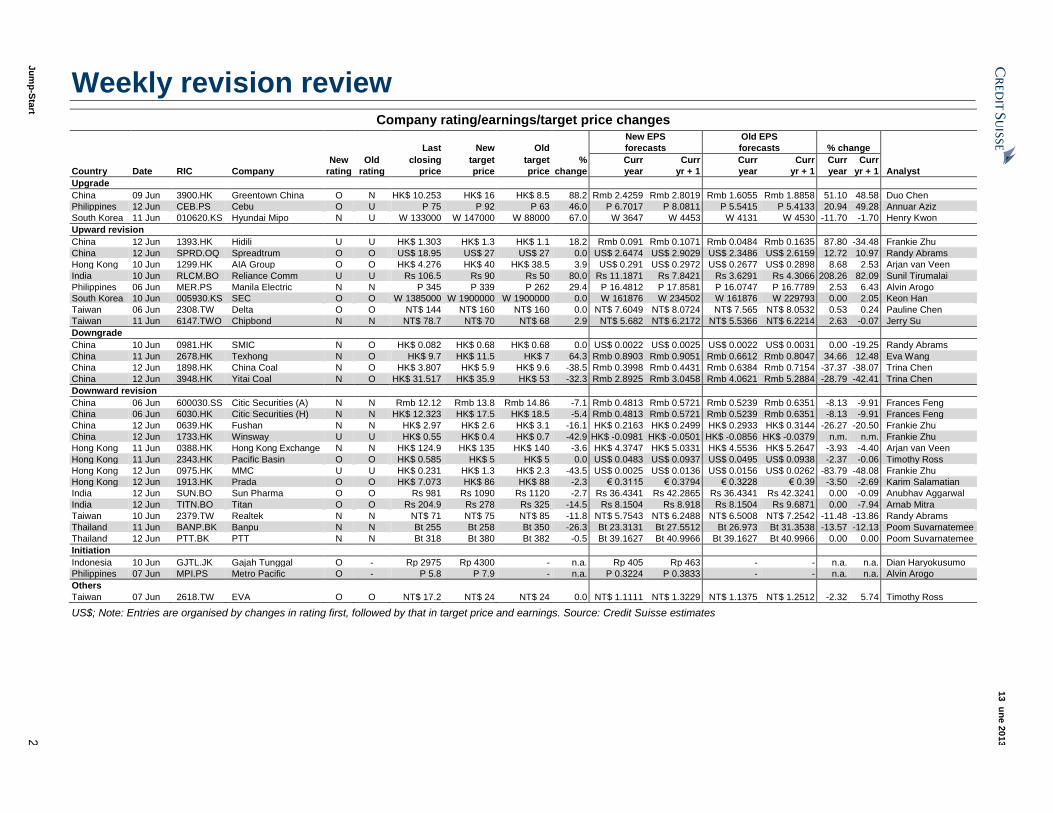

Weekly revision review

Company rating/earnings/target price changes New EPS Old EPS

Last New Old forecasts forecasts % change

New Old closing target target % Curr Curr Curr Curr Curr Curr

Country Date RIC Company rating rating price price price change year yr + 1 year yr + 1 year yr + 1 Analyst

Upgrade

China 09 Jun 3900.HK Greentown China O N HK$ 10.253 HK$ 16 HK$ 8.5 88.2 Rmb 2.4259 Rmb 2.8019 Rmb 1.6055 Rmb 1.8858 51.10 48.58 Duo Chen

Philippines 12 Jun CEB.PS Cebu O U P 75 P 92 P 63 46.0 P 6.7017 P 8.0811 P 5.5415 P 5.4133 20.94 49.28 Annuar Aziz

South Korea 11 Jun 010620.KS Hyundai Mipo N U W 133000 W 147000 W 88000 67.0 W 3647 W 4453 W 4131 W 4530 -11.70 -1.70 Henry Kwon

Upward revision

China 12 Jun 1393.HK Hidili U U HK$ 1.303 HK$ 1.3 HK$ 1.1 18.2 Rmb 0.091 Rmb 0.1071 Rmb 0.0484 Rmb 0.1635 87.80 -34.48 Frankie Zhu

China 12 Jun SPRD.OQ Spreadtrum O O US$ 18.95 US$ 27 US$ 27 0.0 US$ 2.6474 US$ 2.9029 US$ 2.3486 US$ 2.6159 12.72 10.97 Randy Abrams

Hong Kong 10 Jun 1299.HK AIA Group O O HK$ 4.276 HK$ 40 HK$ 38.5 3.9 US$ 0.291 US$ 0.2972 US$ 0.2677 US$ 0.2898 8.68 2.53 Arjan van Veen

India 10 Jun RLCM.BO Reliance Comm U U Rs 106.5 Rs 90 Rs 50 80.0 Rs 11.1871 Rs 7.8421 Rs 3.6291 Rs 4.3066 208.26 82.09 Sunil Tirumalai

Philippines 06 Jun MER.PS Manila Electric N N P 345 P 339 P 262 29.4 P 16.4812 P 17.8581 P 16.0747 P 16.7789 2.53 6.43 Alvin Arogo

South Korea 10 Jun 005930.KS SEC O O W 1385000 W 1900000 W 1900000 0.0 W 161876 W 234502 W 161876 W 229793 0.00 2.05 Keon Han

Taiwan 06 Jun 2308.TW Delta O O NT$ 144 NT$ 160 NT$ 160 0.0 NT$ 7.6049 NT$ 8.0724 NT$ 7.565 NT$ 8.0532 0.53 0.24 Pauline Chen

Taiwan 11 Jun 6147.TWO Chipbond N N NT$ 78.7 NT$ 70 NT$ 68 2.9 NT$ 5.682 NT$ 6.2172 NT$ 5.5366 NT$ 6.2214 2.63 -0.07 Jerry Su

Downgrade

China 10 Jun 0981.HK SMIC N O HK$ 0.082 HK$ 0.68 HK$ 0.68 0.0 US$ 0.0022 US$ 0.0025 US$ 0.0022 US$ 0.0031 0.00 -19.25 Randy Abrams

China 11 Jun 2678.HK Texhong N O HK$ 9.7 HK$ 11.5 HK$ 7 64.3 Rmb 0.8903 Rmb 0.9051 Rmb 0.6612 Rmb 0.8047 34.66 12.48 Eva Wang

China 12 Jun 1898.HK China Coal N O HK$ 3.807 HK$ 5.9 HK$ 9.6 -38.5 Rmb 0.3998 Rmb 0.4431 Rmb 0.6384 Rmb 0.7154 -37.37 -38.07 Trina Chen

China 12 Jun 3948.HK Yitai Coal N O HK$ 31.517 HK$ 35.9 HK$ 53 -32.3 Rmb 2.8925 Rmb 3.0458 Rmb 4.0621 Rmb 5.2884 -28.79 -42.41 Trina Chen

Downward revision

China 06 Jun 600030.SS Citic Securities (A) N N Rmb 12.12 Rmb 13.8 Rmb 14.86 -7.1 Rmb 0.4813 Rmb 0.5721 Rmb 0.5239 Rmb 0.6351 -8.13 -9.91 Frances Feng

China 06 Jun 6030.HK Citic Securities (H) N N HK$ 12.323 HK$ 17.5 HK$ 18.5 -5.4 Rmb 0.4813 Rmb 0.5721 Rmb 0.5239 Rmb 0.6351 -8.13 -9.91 Frances Feng

China 12 Jun 0639.HK Fushan N N HK$ 2.97 HK$ 2.6 HK$ 3.1 -16.1 HK$ 0.2163 HK$ 0.2499 HK$ 0.2933 HK$ 0.3144 -26.27 -20.50 Frankie Zhu

China 12 Jun 1733.HK Winsway U U HK$ 0.55 HK$ 0.4 HK$ 0.7 -42.9 HK$ -0.0981 HK$ -0.0501 HK$ -0.0856 HK$ -0.0379 n.m. n.m. Frankie Zhu

Hong Kong 11 Jun 0388.HK Hong Kong Exchange N N HK$ 124.9 HK$ 135 HK$ 140 -3.6 HK$ 4.3747 HK$ 5.0331 HK$ 4.5536 HK$ 5.2647 -3.93 -4.40 Arjan van Veen

Hong Kong 11 Jun 2343.HK Pacific Basin O O HK$ 0.585 HK$ 5 HK$ 5 0.0 US$ 0.0483 US$ 0.0937 US$ 0.0495 US$ 0.0938 -2.37 -0.06 Timothy Ross

Hong Kong 12 Jun 0975.HK MMC U U HK$ 0.231 HK$ 1.3 HK$ 2.3 -43.5 US$ 0.0025 US$ 0.0136 US$ 0.0156 US$ 0.0262 -83.79 -48.08 Frankie Zhu

Hong Kong 12 Jun 1913.HK Prada O O HK$ 7.073 HK$ 86 HK$ 88 -2.3 € 0.3115 € 0.3794 € 0.3228 € 0.39 -3.50 -2.69 Karim Salamatian

India 12 Jun SUN.BO Sun Pharma O O Rs 981 Rs 1090 Rs 1120 -2.7 Rs 36.4341 Rs 42.2865 Rs 36.4341 Rs 42.3241 0.00 -0.09 Anubhav Aggarwal

India 12 Jun TITN.BO Titan O O Rs 204.9 Rs 278 Rs 325 -14.5 Rs 8.1504 Rs 8.918 Rs 8.1504 Rs 9.6871 0.00 -7.94 Arnab Mitra

Taiwan 10 Jun 2379.TW Realtek N N NT$ 71 NT$ 75 NT$ 85 -11.8 NT$ 5.7543 NT$ 6.2488 NT$ 6.5008 NT$ 7.2542 -11.48 -13.86 Randy Abrams

Thailand 11 Jun BANP.BK Banpu N N Bt 255 Bt 258 Bt 350 -26.3 Bt 23.3131 Bt 27.5512 Bt 26.973 Bt 31.3538 -13.57 -12.13 Poom Suvarnatemee

Thailand 12 Jun PTT.BK PTT N N Bt 318 Bt 380 Bt 382 -0.5 Bt 39.1627 Bt 40.9966 Bt 39.1627 Bt 40.9966 0.00 0.00 Poom Suvarnatemee

Initiation

Indonesia 10 Jun GJTL.JK Gajah Tunggal O - Rp 2975 Rp 4300 - n.a. Rp 405 Rp 463 - - n.a. n.a. Dian Haryokusumo

Philippines 07 Jun MPI.PS Metro Pacific O - P 5.8 P 7.9 - n.a. P 0.3224 P 0.3833 - - n.a. n.a. Alvin Arogo

Others

Taiwan 07 Jun 2618.TW EVA O O NT$ 17.2 NT$ 24 NT$ 24 0.0 NT$ 1.1111 NT$ 1.3229 NT$ 1.1375 NT$ 1.2512 -2.32 5.74 Timothy Ross

US$; Note: Entries are organised by changes in rating first, followed by that in target price and earnings. Source: Credit Suisse estimates

13 June 2013

Jump-Start 3

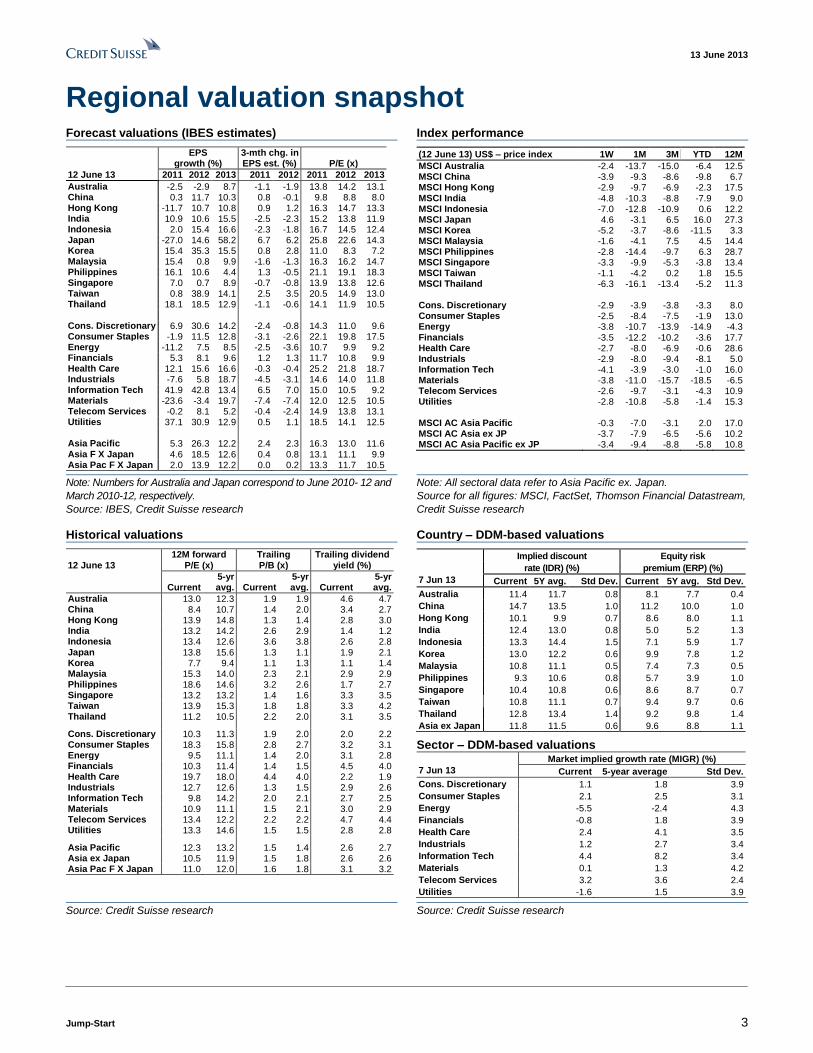

Regional valuation snapshot Forecast valuations (IBES estimates) Index performance

EPS 3-mth chg. in growth (%) EPS est. (%) P/E (x)

12 June 13 2011 2012 2013 2011 2012 2011 2012 2013

Australia -2.5 -2.9 8.7 -1.1 -1.9 13.8 14.2 13.1 China 0.3 11.7 10.3 0.8 -0.1 9.8 8.8 8.0 Hong Kong -11.7 10.7 10.8 0.9 1.2 16.3 14.7 13.3 India 10.9 10.6 15.5 -2.5 -2.3 15.2 13.8 11.9 Indonesia 2.0 15.4 16.6 -2.3 -1.8 16.7 14.5 12.4 Japan -27.0 14.6 58.2 6.7 6.2 25.8 22.6 14.3 Korea 15.4 35.3 15.5 0.8 2.8 11.0 8.3 7.2 Malaysia 15.4 0.8 9.9 -1.6 -1.3 16.3 16.2 14.7 Philippines 16.1 10.6 4.4 1.3 -0.5 21.1 19.1 18.3 Singapore 7.0 0.7 8.9 -0.7 -0.8 13.9 13.8 12.6 Taiwan 0.8 38.9 14.1 2.5 3.5 20.5 14.9 13.0 Thailand 18.1 18.5 12.9 -1.1 -0.6 14.1 11.9 10.5 Cons. Discretionary 6.9 30.6 14.2 -2.4 -0.8 14.3 11.0 9.6 Consumer Staples -1.9 11.5 12.8 -3.1 -2.6 22.1 19.8 17.5 Energy -11.2 7.5 8.5 -2.5 -3.6 10.7 9.9 9.2 Financials 5.3 8.1 9.6 1.2 1.3 11.7 10.8 9.9 Health Care 12.1 15.6 16.6 -0.3 -0.4 25.2 21.8 18.7 Industrials -7.6 5.8 18.7 -4.5 -3.1 14.6 14.0 11.8 Information Tech 41.9 42.8 13.4 6.5 7.0 15.0 10.5 9.2 Materials -23.6 -3.4 19.7 -7.4 -7.4 12.0 12.5 10.5 Telecom Services -0.2 8.1 5.2 -0.4 -2.4 14.9 13.8 13.1 Utilities 37.1 30.9 12.9 0.5 1.1 18.5 14.1 12.5 Asia Pacific 5.3 26.3 12.2 2.4 2.3 16.3 13.0 11.6 Asia F X Japan 4.6 18.5 12.6 0.4 0.8 13.1 11.1 9.9 Asia Pac F X Japan 2.0 13.9 12.2 0.0 0.2 13.3 11.7 10.5

(12 June 13) US$ – price index 1W 1M 3M YTD 12M

MSCI Australia -2.4 -13.7 -15.0 -6.4 12.5 MSCI China -3.9 -9.3 -8.6 -9.8 6.7 MSCI Hong Kong -2.9 -9.7 -6.9 -2.3 17.5 MSCI India -4.8 -10.3 -8.8 -7.9 9.0 MSCI Indonesia -7.0 -12.8 -10.9 0.6 12.2 MSCI Japan 4.6 -3.1 6.5 16.0 27.3 MSCI Korea -5.2 -3.7 -8.6 -11.5 3.3 MSCI Malaysia -1.6 -4.1 7.5 4.5 14.4 MSCI Philippines -2.8 -14.4 -9.7 6.3 28.7 MSCI Singapore -3.3 -9.9 -5.3 -3.8 13.4 MSCI Taiwan -1.1 -4.2 0.2 1.8 15.5 MSCI Thailand -6.3 -16.1 -13.4 -5.2 11.3 Cons. Discretionary -2.9 -3.9 -3.8 -3.3 8.0 Consumer Staples -2.5 -8.4 -7.5 -1.9 13.0 Energy -3.8 -10.7 -13.9 -14.9 -4.3 Financials -3.5 -12.2 -10.2 -3.6 17.7 Health Care -2.7 -8.0 -6.9 -0.6 28.6 Industrials -2.9 -8.0 -9.4 -8.1 5.0 Information Tech -4.1 -3.9 -3.0 -1.0 16.0 Materials -3.8 -11.0 -15.7 -18.5 -6.5 Telecom Services -2.6 -9.7 -3.1 -4.3 10.9 Utilities -2.8 -10.8 -5.8 -1.4 15.3 MSCI AC Asia Pacific -0.3 -7.0 -3.1 2.0 17.0 MSCI AC Asia ex JP -3.7 -7.9 -6.5 -5.6 10.2 MSCI AC Asia Pacific ex JP -3.4 -9.4 -8.8 -5.8 10.8

Note: Numbers for Australia and Japan correspond to June 2010- 12 and

March 2010-12, respectively.

Source: IBES, Credit Suisse research

Note: All sectoral data refer to Asia Pacific ex. Japan.

Source for all figures: MSCI, FactSet, Thomson Financial Datastream,

Credit Suisse research

Historical valuations Country – DDM-based valuations

12 June 13

12M forward P/E (x)

Trailing P/B (x)

Trailing dividend yield (%)

Current 5-yr avg. Current

5-yr avg. Current

5-yr avg.

Australia 13.0 12.3 1.9 1.9 4.6 4.7 China 8.4 10.7 1.4 2.0 3.4 2.7 Hong Kong 13.9 14.8 1.3 1.4 2.8 3.0 India 13.2 14.2 2.6 2.9 1.4 1.2 Indonesia 13.4 12.6 3.6 3.8 2.6 2.8 Japan 13.8 15.6 1.3 1.1 1.9 2.1 Korea 7.7 9.4 1.1 1.3 1.1 1.4 Malaysia 15.3 14.0 2.3 2.1 2.9 2.9 Philippines 18.6 14.6 3.2 2.6 1.7 2.7 Singapore 13.2 13.2 1.4 1.6 3.3 3.5 Taiwan 13.9 15.3 1.8 1.8 3.3 4.2 Thailand 11.2 10.5 2.2 2.0 3.1 3.5 Cons. Discretionary 10.3 11.3 1.9 2.0 2.0 2.2 Consumer Staples 18.3 15.8 2.8 2.7 3.2 3.1 Energy 9.5 11.1 1.4 2.0 3.1 2.8 Financials 10.3 11.4 1.4 1.5 4.5 4.0 Health Care 19.7 18.0 4.4 4.0 2.2 1.9 Industrials 12.7 12.6 1.3 1.5 2.9 2.6 Information Tech 9.8 14.2 2.0 2.1 2.7 2.5 Materials 10.9 11.1 1.5 2.1 3.0 2.9 Telecom Services 13.4 12.2 2.2 2.2 4.7 4.4 Utilities 13.3 14.6 1.5 1.5 2.8 2.8 Asia Pacific 12.3 13.2 1.5 1.4 2.6 2.7 Asia ex Japan 10.5 11.9 1.5 1.8 2.6 2.6 Asia Pac F X Japan 11.0 12.0 1.6 1.8 3.1 3.2

Implied discount Equity risk

rate (IDR) (%) premium (ERP) (%)

7 Jun 13 Current 5Y avg. Std Dev. Current 5Y avg. Std Dev.

Australia 11.4 11.7 0.8 8.1 7.7 0.4

China 14.7 13.5 1.0 11.2 10.0 1.0

Hong Kong 10.1 9.9 0.7 8.6 8.0 1.1

India 12.4 13.0 0.8 5.0 5.2 1.3

Indonesia 13.3 14.4 1.5 7.1 5.9 1.7

Korea 13.0 12.2 0.6 9.9 7.8 1.2

Malaysia 10.8 11.1 0.5 7.4 7.3 0.5

Philippines 9.3 10.6 0.8 5.7 3.9 1.0

Singapore 10.4 10.8 0.6 8.6 8.7 0.7

Taiwan 10.8 11.1 0.7 9.4 9.7 0.6

Thailand 12.8 13.4 1.4 9.2 9.8 1.4

Asia ex Japan 11.8 11.5 0.6 9.6 8.8 1.1

Sector – DDM-based valuations Market implied growth rate (MIGR) (%)

7 Jun 13 Current 5-year average Std Dev.

Cons. Discretionary 1.1 1.8 3.9

Consumer Staples 2.1 2.5 3.1

Energy -5.5 -2.4 4.3

Financials -0.8 1.8 3.9

Health Care 2.4 4.1 3.5

Industrials 1.2 2.7 3.4

Information Tech 4.4 8.2 3.4

Materials 0.1 1.3 4.2

Telecom Services 3.2 3.6 2.4

Utilities -1.6 1.5 3.9

Source: Credit Suisse research Source: Credit Suisse research

13 June 2013

Jump-Start 4

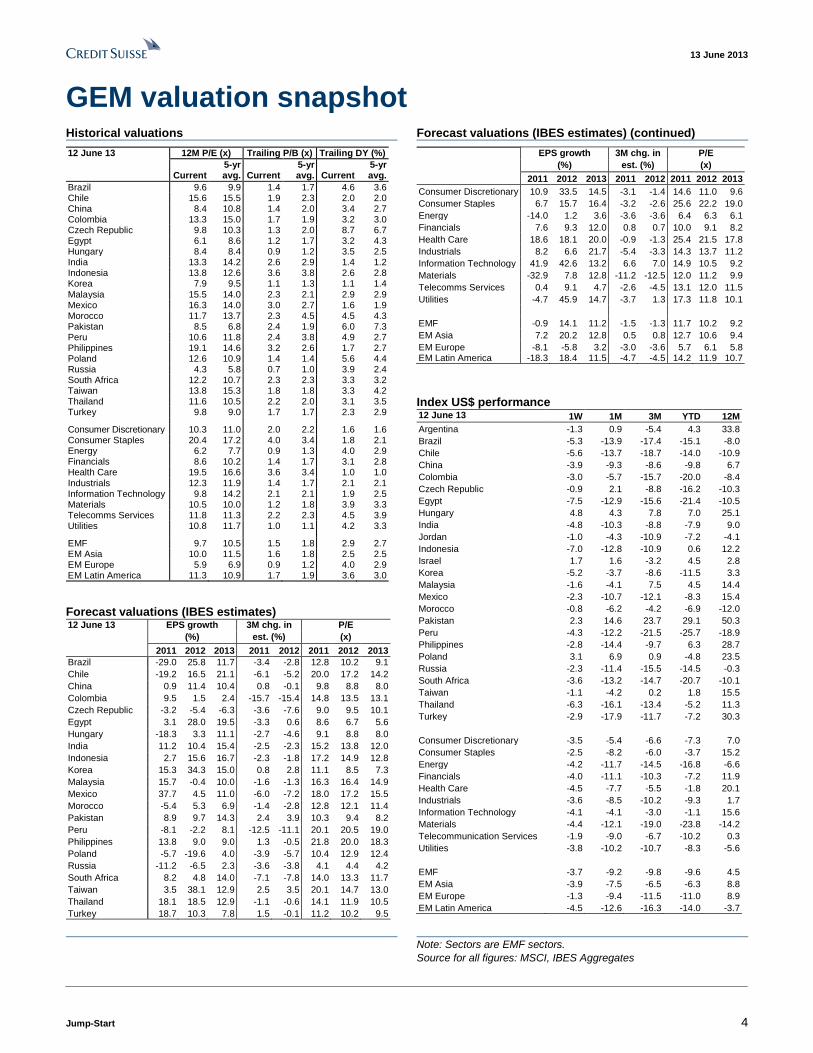

GEM valuation snapshot Historical valuations Forecast valuations (IBES estimates) (continued)

12 June 13 12M P/E (x) Trailing P/B (x) Trailing DY (%)

Current 5-yr

avg. Current 5-yr avg. Current

5-yr avg.

Brazil 9.6 9.9 1.4 1.7 4.6 3.6 Chile 15.6 15.5 1.9 2.3 2.0 2.0 China 8.4 10.8 1.4 2.0 3.4 2.7 Colombia 13.3 15.0 1.7 1.9 3.2 3.0 Czech Republic 9.8 10.3 1.3 2.0 8.7 6.7 Egypt 6.1 8.6 1.2 1.7 3.2 4.3 Hungary 8.4 8.4 0.9 1.2 3.5 2.5 India 13.3 14.2 2.6 2.9 1.4 1.2 Indonesia 13.8 12.6 3.6 3.8 2.6 2.8 Korea 7.9 9.5 1.1 1.3 1.1 1.4

Malaysia 15.5 14.0 2.3 2.1 2.9 2.9 Mexico 16.3 14.0 3.0 2.7 1.6 1.9 Morocco 11.7 13.7 2.3 4.5 4.5 4.3 Pakistan 8.5 6.8 2.4 1.9 6.0 7.3 Peru 10.6 11.8 2.4 3.8 4.9 2.7 Philippines 19.1 14.6 3.2 2.6 1.7 2.7 Poland 12.6 10.9 1.4 1.4 5.6 4.4 Russia 4.3 5.8 0.7 1.0 3.9 2.4 South Africa 12.2 10.7 2.3 2.3 3.3 3.2 Taiwan 13.8 15.3 1.8 1.8 3.3 4.2 Thailand 11.6 10.5 2.2 2.0 3.1 3.5 Turkey 9.8 9.0 1.7 1.7 2.3 2.9 Consumer Discretionary 10.3 11.0 2.0 2.2 1.6 1.6 Consumer Staples 20.4 17.2 4.0 3.4 1.8 2.1 Energy 6.2 7.7 0.9 1.3 4.0 2.9 Financials 8.6 10.2 1.4 1.7 3.1 2.8 Health Care 19.5 16.6 3.6 3.4 1.0 1.0 Industrials 12.3 11.9 1.4 1.7 2.1 2.1 Information Technology 9.8 14.2 2.1 2.1 1.9 2.5 Materials 10.5 10.0 1.2 1.8 3.9 3.3 Telecomms Services 11.8 11.3 2.2 2.3 4.5 3.9 Utilities 10.8 11.7 1.0 1.1 4.2 3.3 EMF 9.7 10.5 1.5 1.8 2.9 2.7 EM Asia 10.0 11.5 1.6 1.8 2.5 2.5 EM Europe 5.9 6.9 0.9 1.2 4.0 2.9 EM Latin America 11.3 10.9 1.7 1.9 3.6 3.0

Forecast valuations (IBES estimates) 12 June 13 EPS growth 3M chg. in P/E

(%) est. (%) (x)

2011 2012 2013 2011 2012 2011 2012 2013

Brazil -29.0 25.8 11.7 -3.4 -2.8 12.8 10.2 9.1

Chile -19.2 16.5 21.1 -6.1 -5.2 20.0 17.2 14.2

China 0.9 11.4 10.4 0.8 -0.1 9.8 8.8 8.0

Colombia 9.5 1.5 2.4 -15.7 -15.4 14.8 13.5 13.1

Czech Republic -3.2 -5.4 -6.3 -3.6 -7.6 9.0 9.5 10.1

Egypt 3.1 28.0 19.5 -3.3 0.6 8.6 6.7 5.6

Hungary -18.3 3.3 11.1 -2.7 -4.6 9.1 8.8 8.0

India 11.2 10.4 15.4 -2.5 -2.3 15.2 13.8 12.0

Indonesia 2.7 15.6 16.7 -2.3 -1.8 17.2 14.9 12.8

Korea 15.3 34.3 15.0 0.8 2.8 11.1 8.5 7.3

Malaysia 15.7 -0.4 10.0 -1.6 -1.3 16.3 16.4 14.9

Mexico 37.7 4.5 11.0 -6.0 -7.2 18.0 17.2 15.5

Morocco -5.4 5.3 6.9 -1.4 -2.8 12.8 12.1 11.4

Pakistan 8.9 9.7 14.3 2.4 3.9 10.3 9.4 8.2

Peru -8.1 -2.2 8.1 -12.5 -11.1 20.1 20.5 19.0

Philippines 13.8 9.0 9.0 1.3 -0.5 21.8 20.0 18.3

Poland -5.7 -19.6 4.0 -3.9 -5.7 10.4 12.9 12.4

Russia -11.2 -6.5 2.3 -3.6 -3.8 4.1 4.4 4.2

South Africa 8.2 4.8 14.0 -7.1 -7.8 14.0 13.3 11.7

Taiwan 3.5 38.1 12.9 2.5 3.5 20.1 14.7 13.0

Thailand 18.1 18.5 12.9 -1.1 -0.6 14.1 11.9 10.5

Turkey 18.7 10.3 7.8 1.5 -0.1 11.2 10.2 9.5

EPS growth 3M chg. in P/E

(%) est. (%) (x)

2011 2012 2013 2011 2012 2011 2012 2013

Consumer Discretionary 10.9 33.5 14.5 -3.1 -1.4 14.6 11.0 9.6

Consumer Staples 6.7 15.7 16.4 -3.2 -2.6 25.6 22.2 19.0

Energy -14.0 1.2 3.6 -3.6 -3.6 6.4 6.3 6.1

Financials 7.6 9.3 12.0 0.8 0.7 10.0 9.1 8.2

Health Care 18.6 18.1 20.0 -0.9 -1.3 25.4 21.5 17.8

Industrials 8.2 6.6 21.7 -5.4 -3.3 14.3 13.7 11.2

Information Technology 41.9 42.6 13.2 6.6 7.0 14.9 10.5 9.2

Materials -32.9 7.8 12.8 -11.2 -12.5 12.0 11.2 9.9

Telecomms Services 0.4 9.1 4.7 -2.6 -4.5 13.1 12.0 11.5

Utilities -4.7 45.9 14.7 -3.7 1.3 17.3 11.8 10.1

EMF -0.9 14.1 11.2 -1.5 -1.3 11.7 10.2 9.2

EM Asia 7.2 20.2 12.8 0.5 0.8 12.7 10.6 9.4

EM Europe -8.1 -5.8 3.2 -3.0 -3.6 5.7 6.1 5.8 EM Latin America -18.3 18.4 11.5 -4.7 -4.5 14.2 11.9 10.7

Index US$ performance 12 June 13 1W 1M 3M YTD 12M

Argentina -1.3 0.9 -5.4 4.3 33.8

Brazil -5.3 -13.9 -17.4 -15.1 -8.0

Chile -5.6 -13.7 -18.7 -14.0 -10.9

China -3.9 -9.3 -8.6 -9.8 6.7

Colombia -3.0 -5.7 -15.7 -20.0 -8.4

Czech Republic -0.9 2.1 -8.8 -16.2 -10.3

Egypt -7.5 -12.9 -15.6 -21.4 -10.5

Hungary 4.8 4.3 7.8 7.0 25.1

India -4.8 -10.3 -8.8 -7.9 9.0

Jordan -1.0 -4.3 -10.9 -7.2 -4.1

Indonesia -7.0 -12.8 -10.9 0.6 12.2

Israel 1.7 1.6 -3.2 4.5 2.8

Korea -5.2 -3.7 -8.6 -11.5 3.3

Malaysia -1.6 -4.1 7.5 4.5 14.4

Mexico -2.3 -10.7 -12.1 -8.3 15.4

Morocco -0.8 -6.2 -4.2 -6.9 -12.0

Pakistan 2.3 14.6 23.7 29.1 50.3

Peru -4.3 -12.2 -21.5 -25.7 -18.9

Philippines -2.8 -14.4 -9.7 6.3 28.7

Poland 3.1 6.9 0.9 -4.8 23.5

Russia -2.3 -11.4 -15.5 -14.5 -0.3

South Africa -3.6 -13.2 -14.7 -20.7 -10.1

Taiwan -1.1 -4.2 0.2 1.8 15.5

Thailand -6.3 -16.1 -13.4 -5.2 11.3

Turkey -2.9 -17.9 -11.7 -7.2 30.3

Consumer Discretionary -3.5 -5.4 -6.6 -7.3 7.0

Consumer Staples -2.5 -8.2 -6.0 -3.7 15.2

Energy -4.2 -11.7 -14.5 -16.8 -6.6

Financials -4.0 -11.1 -10.3 -7.2 11.9

Health Care -4.5 -7.7 -5.5 -1.8 20.1

Industrials -3.6 -8.5 -10.2 -9.3 1.7

Information Technology -4.1 -4.1 -3.0 -1.1 15.6

Materials -4.4 -12.1 -19.0 -23.8 -14.2

Telecommunication Services -1.9 -9.0 -6.7 -10.2 0.3

Utilities -3.8 -10.2 -10.7 -8.3 -5.6

EMF -3.7 -9.2 -9.8 -9.6 4.5

EM Asia -3.9 -7.5 -6.5 -6.3 8.8

EM Europe -1.3 -9.4 -11.5 -11.0 8.9

EM Latin America -4.5 -12.6 -16.3 -14.0 -3.7

Note: Sectors are EMF sectors.

Source for all figures: MSCI, IBES Aggregates

13 June 2013

Jump-Start 5

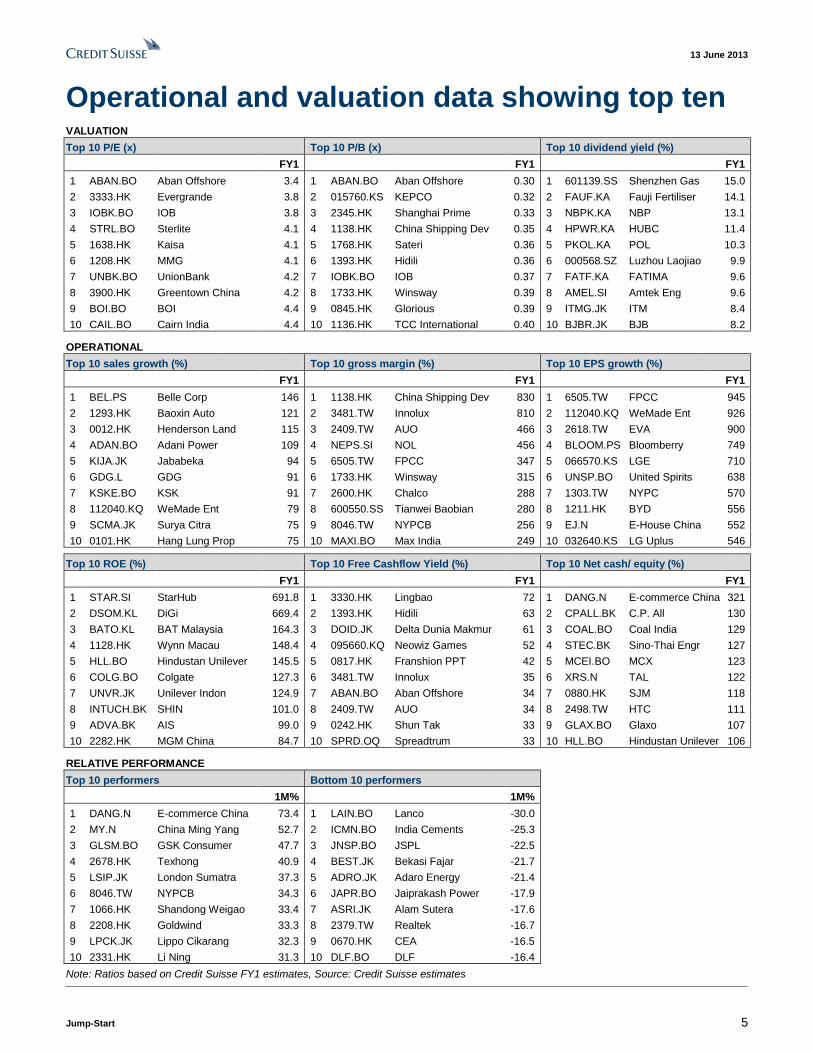

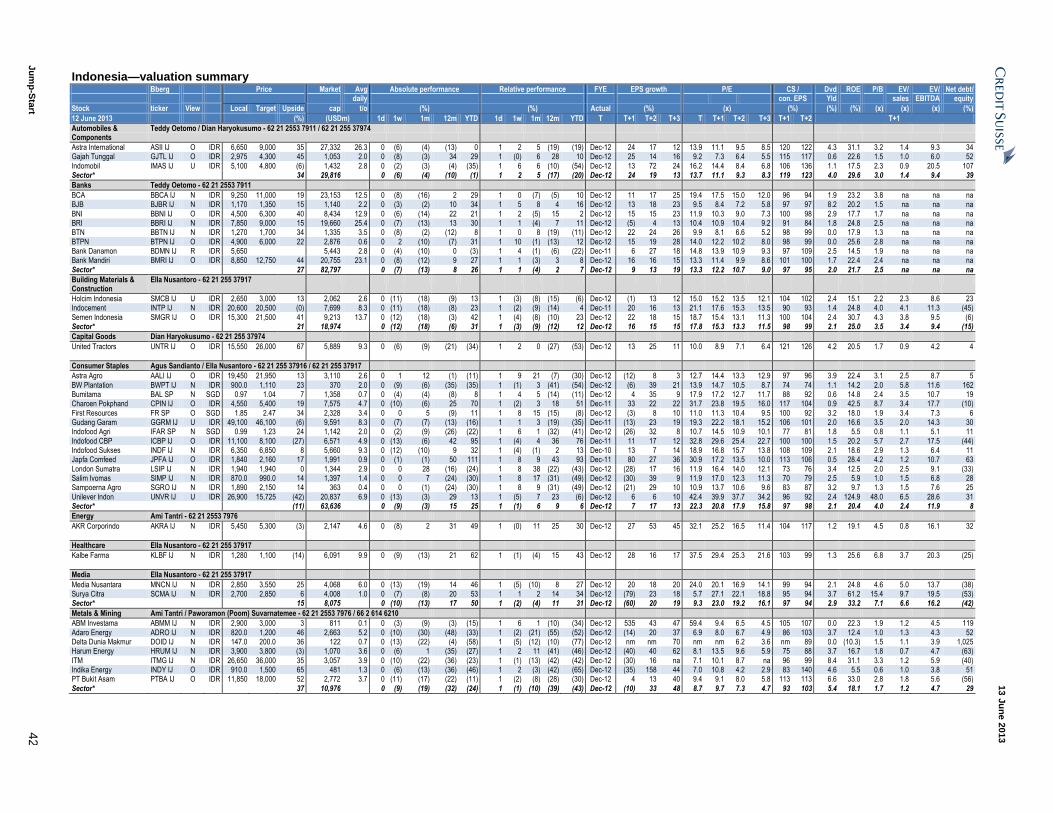

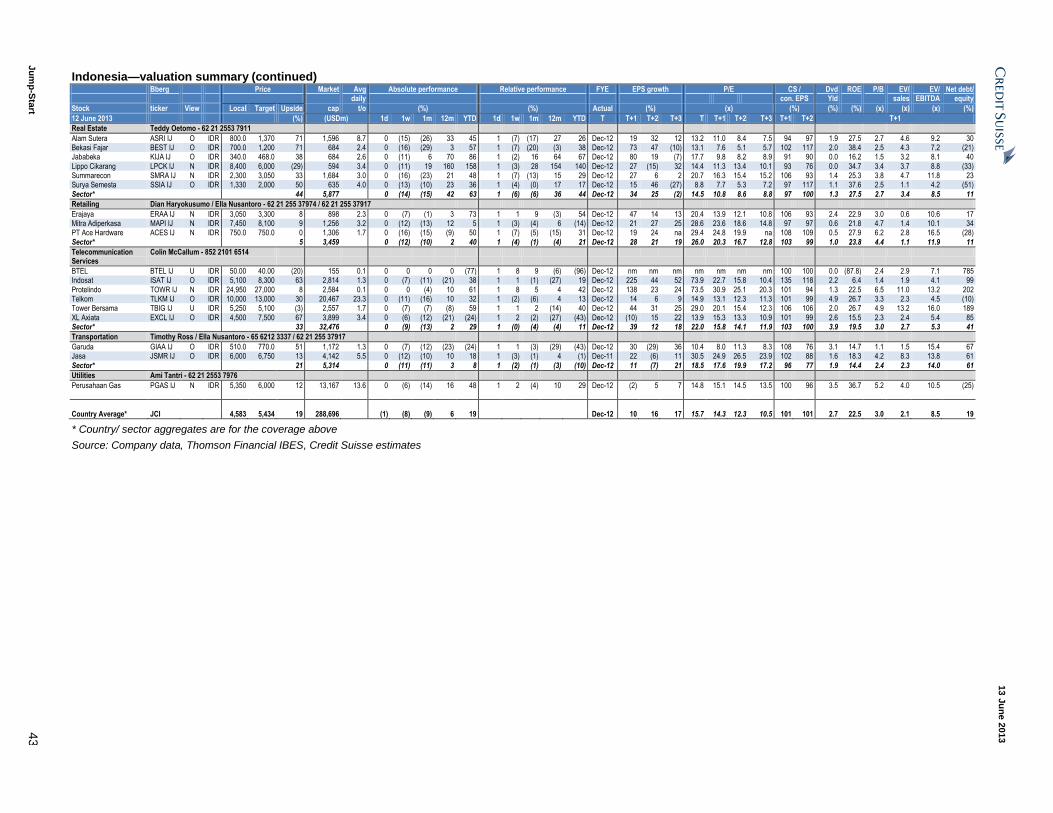

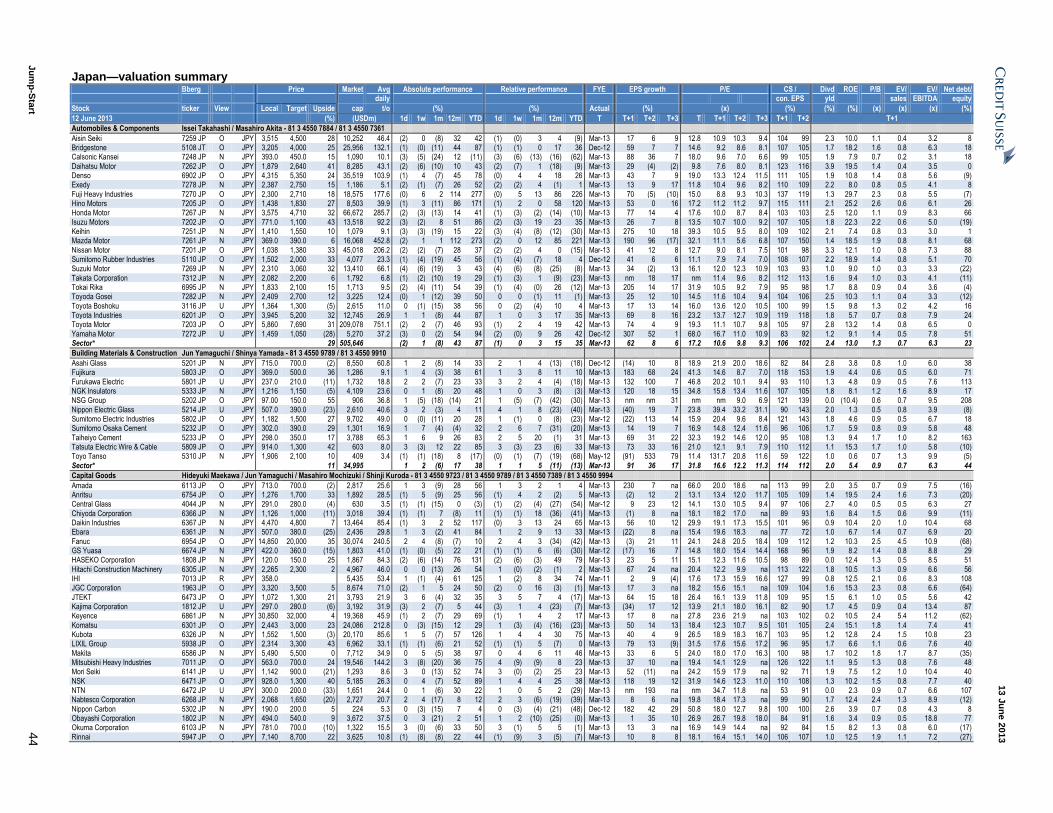

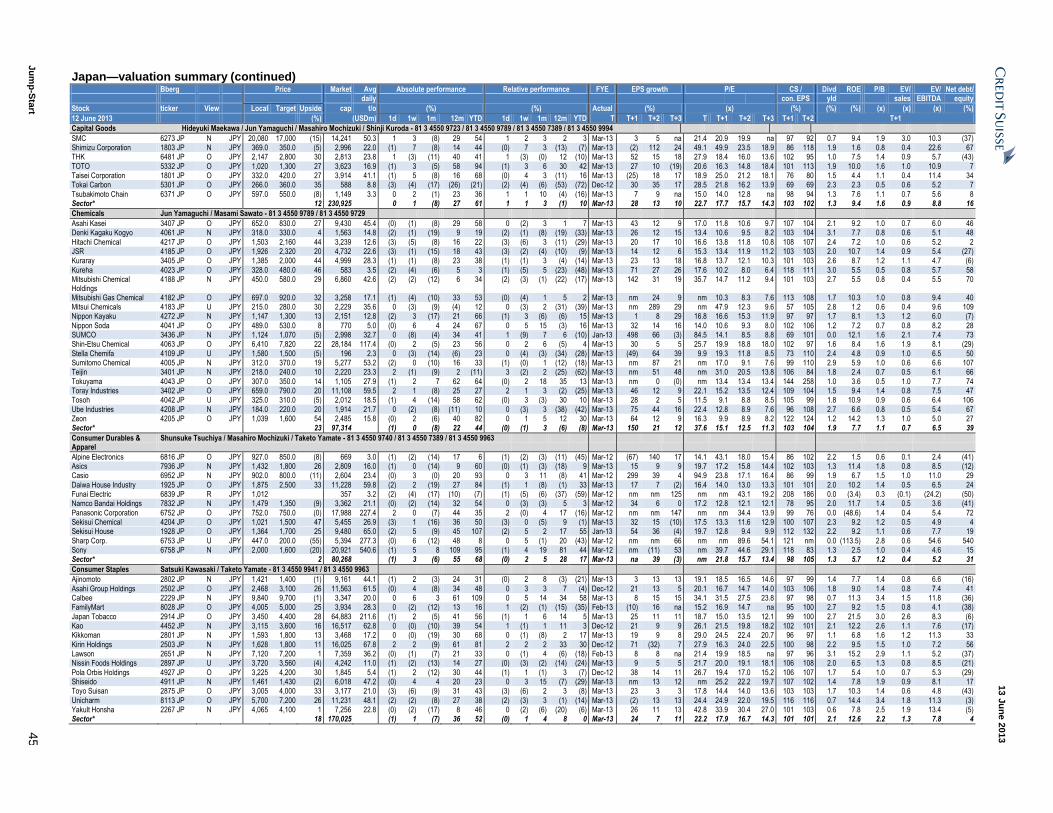

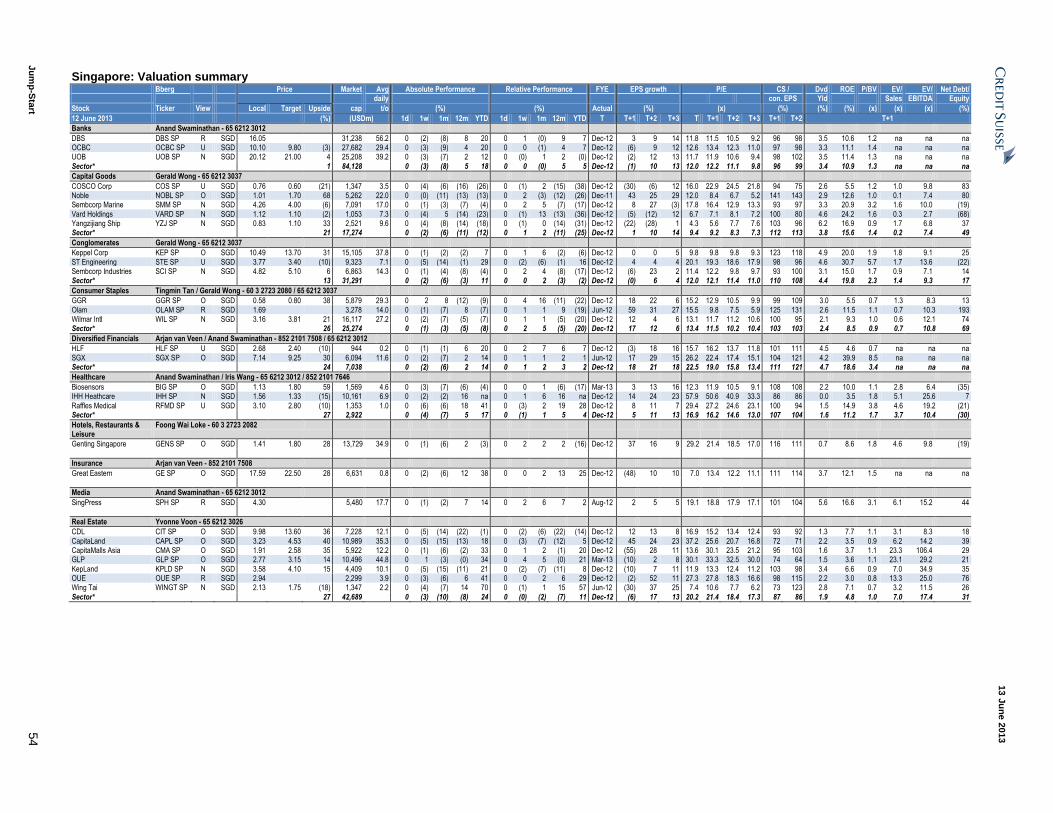

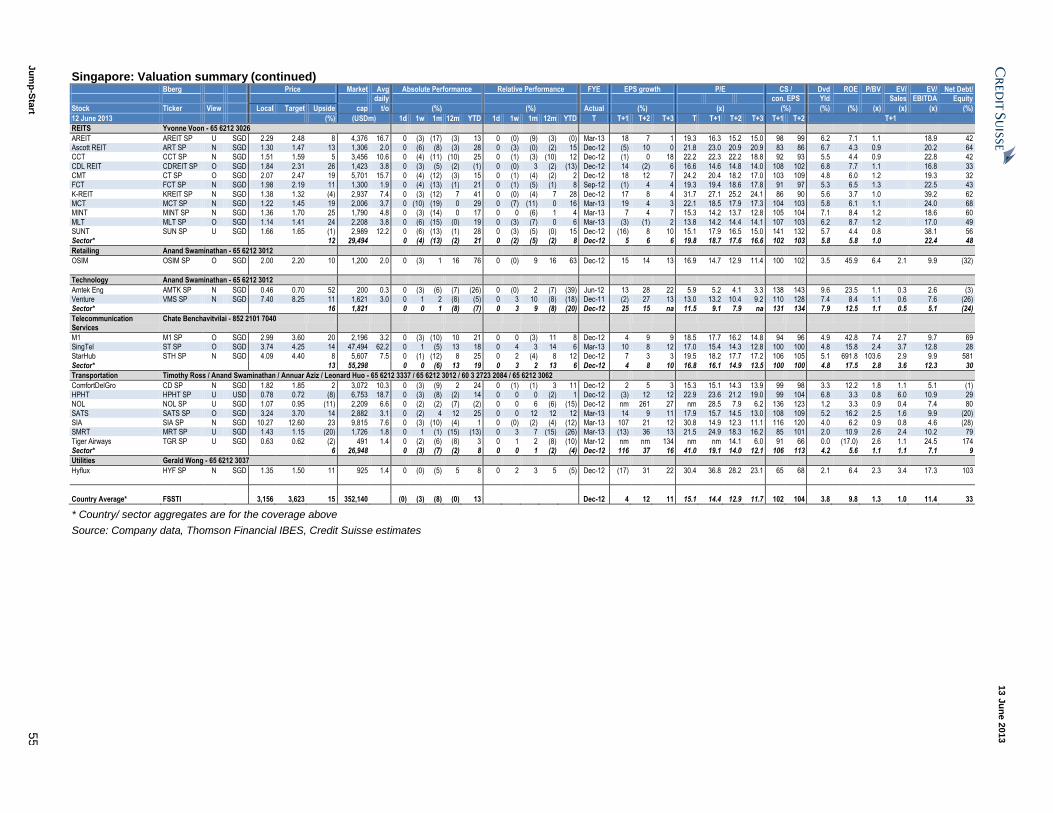

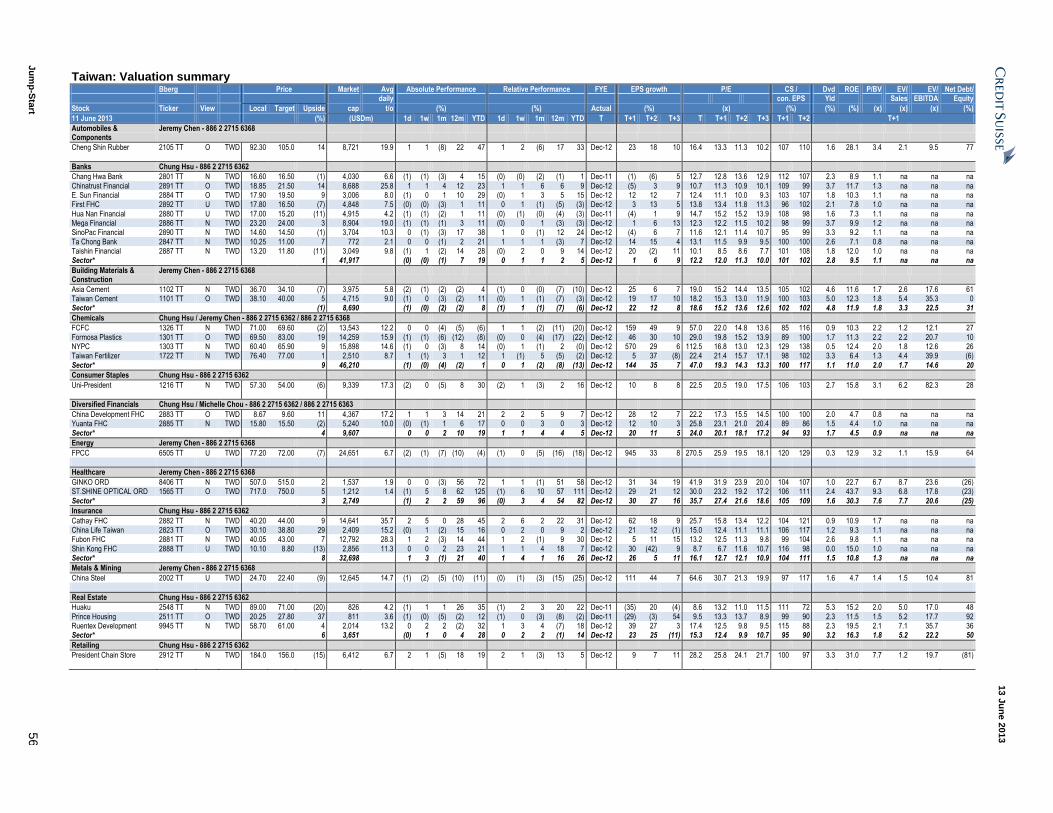

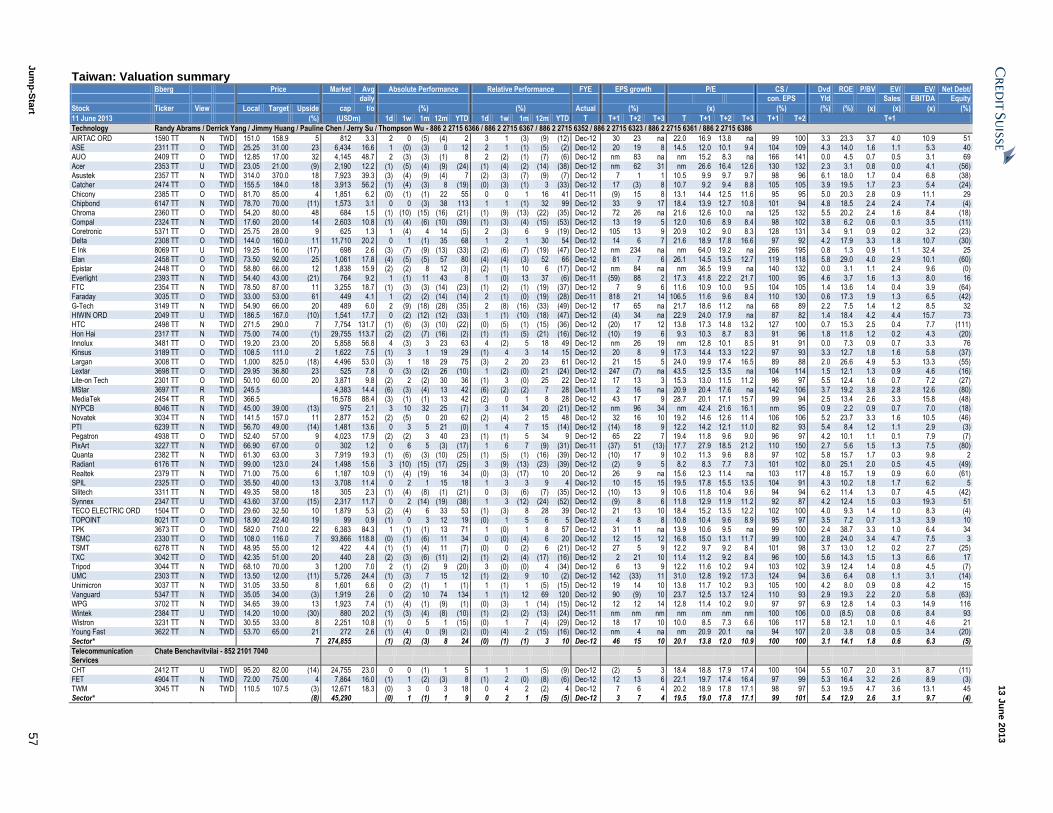

Operational and valuation data showing top ten VALUATION

Top 10 P/E (x) Top 10 P/B (x) Top 10 dividend yield (%)

FY1 FY1 FY1

1 ABAN.BO Aban Offshore 3.4 1 ABAN.BO Aban Offshore 0.30 1 601139.SS Shenzhen Gas 15.0

2 3333.HK Evergrande 3.8 2 015760.KS KEPCO 0.32 2 FAUF.KA Fauji Fertiliser 14.1

3 IOBK.BO IOB 3.8 3 2345.HK Shanghai Prime 0.33 3 NBPK.KA NBP 13.1

4 STRL.BO Sterlite 4.1 4 1138.HK China Shipping Dev 0.35 4 HPWR.KA HUBC 11.4

5 1638.HK Kaisa 4.1 5 1768.HK Sateri 0.36 5 PKOL.KA POL 10.3

6 1208.HK MMG 4.1 6 1393.HK Hidili 0.36 6 000568.SZ Luzhou Laojiao 9.9

7 UNBK.BO UnionBank 4.2 7 IOBK.BO IOB 0.37 7 FATF.KA FATIMA 9.6

8 3900.HK Greentown China 4.2 8 1733.HK Winsway 0.39 8 AMEL.SI Amtek Eng 9.6

9 BOI.BO BOI 4.4 9 0845.HK Glorious 0.39 9 ITMG.JK ITM 8.4

10 CAIL.BO Cairn India 4.4 10 1136.HK TCC International 0.40 10 BJBR.JK BJB 8.2

OPERATIONAL

Top 10 sales growth (%) Top 10 gross margin (%) Top 10 EPS growth (%)

FY1 FY1 FY1

1 BEL.PS Belle Corp 146 1 1138.HK China Shipping Dev 830 1 6505.TW FPCC 945

2 1293.HK Baoxin Auto 121 2 3481.TW Innolux 810 2 112040.KQ WeMade Ent 926

3 0012.HK Henderson Land 115 3 2409.TW AUO 466 3 2618.TW EVA 900

4 ADAN.BO Adani Power 109 4 NEPS.SI NOL 456 4 BLOOM.PS Bloomberry 749

5 KIJA.JK Jababeka 94 5 6505.TW FPCC 347 5 066570.KS LGE 710

6 GDG.L GDG 91 6 1733.HK Winsway 315 6 UNSP.BO United Spirits 638

7 KSKE.BO KSK 91 7 2600.HK Chalco 288 7 1303.TW NYPC 570

8 112040.KQ WeMade Ent 79 8 600550.SS Tianwei Baobian 280 8 1211.HK BYD 556

9 SCMA.JK Surya Citra 75 9 8046.TW NYPCB 256 9 EJ.N E-House China 552

10 0101.HK Hang Lung Prop 75 10 MAXI.BO Max India 249 10 032640.KS LG Uplus 546

Top 10 ROE (%) Top 10 Free Cashflow Yield (%) Top 10 Net cash/ equity (%)

FY1 FY1 FY1

1 STAR.SI StarHub 691.8 1 3330.HK Lingbao 72 1 DANG.N E-commerce China 321

2 DSOM.KL DiGi 669.4 2 1393.HK Hidili 63 2 CPALL.BK C.P. All 130

3 BATO.KL BAT Malaysia 164.3 3 DOID.JK Delta Dunia Makmur 61 3 COAL.BO Coal India 129

4 1128.HK Wynn Macau 148.4 4 095660.KQ Neowiz Games 52 4 STEC.BK Sino-Thai Engr 127

5 HLL.BO Hindustan Unilever 145.5 5 0817.HK Franshion PPT 42 5 MCEI.BO MCX 123

6 COLG.BO Colgate 127.3 6 3481.TW Innolux 35 6 XRS.N TAL 122

7 UNVR.JK Unilever Indon 124.9 7 ABAN.BO Aban Offshore 34 7 0880.HK SJM 118

8 INTUCH.BK SHIN 101.0 8 2409.TW AUO 34 8 2498.TW HTC 111

9 ADVA.BK AIS 99.0 9 0242.HK Shun Tak 33 9 GLAX.BO Glaxo 107

10 2282.HK MGM China 84.7 10 SPRD.OQ Spreadtrum 33 10 HLL.BO Hindustan Unilever 106

RELATIVE PERFORMANCE

Top 10 performers Bottom 10 performers

1M% 1M%

1 DANG.N E-commerce China 73.4 1 LAIN.BO Lanco -30.0

2 MY.N China Ming Yang 52.7 2 ICMN.BO India Cements -25.3

3 GLSM.BO GSK Consumer 47.7 3 JNSP.BO JSPL -22.5

4 2678.HK Texhong 40.9 4 BEST.JK Bekasi Fajar -21.7

5 LSIP.JK London Sumatra 37.3 5 ADRO.JK Adaro Energy -21.4

6 8046.TW NYPCB 34.3 6 JAPR.BO Jaiprakash Power -17.9

7 1066.HK Shandong Weigao 33.4 7 ASRI.JK Alam Sutera -17.6

8 2208.HK Goldwind 33.3 8 2379.TW Realtek -16.7

9 LPCK.JK Lippo Cikarang 32.3 9 0670.HK CEA -16.5

10 2331.HK Li Ning 31.3 10 DLF.BO DLF -16.4

Note: Ratios based on Credit Suisse FY1 estimates, Source: Credit Suisse estimates

13 June 2013

Jump-Start 6

Credit Suisse macroeconomic forecasts

13 June 2013

Jump-Start 7

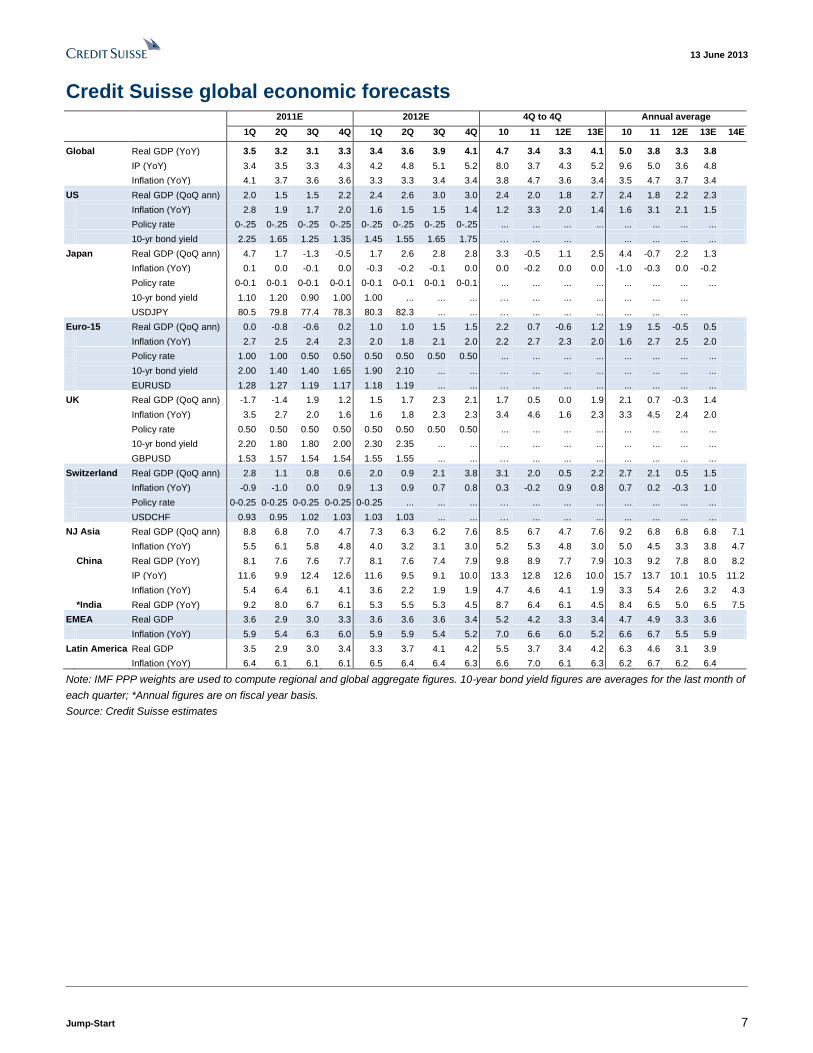

Credit Suisse global economic forecasts

2011E 2012E 4Q to 4Q Annual average

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 10 11 12E 13E 10 11 12E 13E 14E

Global Real GDP (YoY) 3.5 3.2 3.1 3.3 3.4 3.6 3.9 4.1 4.7 3.4 3.3 4.1 5.0 3.8 3.3 3.8 IP (YoY) 3.4 3.5 3.3 4.3 4.2 4.8 5.1 5.2 8.0 3.7 4.3 5.2 9.6 5.0 3.6 4.8 Inflation (YoY) 4.1 3.7 3.6 3.6 3.3 3.3 3.4 3.4 3.8 4.7 3.6 3.4 3.5 4.7 3.7 3.4

US Real GDP (QoQ ann) 2.0 1.5 1.5 2.2 2.4 2.6 3.0 3.0 2.4 2.0 1.8 2.7 2.4 1.8 2.2 2.3 Inflation (YoY) 2.8 1.9 1.7 2.0 1.6 1.5 1.5 1.4 1.2 3.3 2.0 1.4 1.6 3.1 2.1 1.5 Policy rate 0-.25 0-.25 0-.25 0-.25 0-.25 0-.25 0-.25 0-.25 ... ... ... ... ... ... ... ... 10-yr bond yield 2.25 1.65 1.25 1.35 1.45 1.55 1.65 1.75 … ... ... ... ... ... ...

Japan Real GDP (QoQ ann) 4.7 1.7 -1.3 -0.5 1.7 2.6 2.8 2.8 3.3 -0.5 1.1 2.5 4.4 -0.7 2.2 1.3 Inflation (YoY) 0.1 0.0 -0.1 0.0 -0.3 -0.2 -0.1 0.0 0.0 -0.2 0.0 0.0 -1.0 -0.3 0.0 -0.2 Policy rate 0-0.1 0-0.1 0-0.1 0-0.1 0-0.1 0-0.1 0-0.1 0-0.1 ... ... ... ... ... ... ... ... 10-yr bond yield 1.10 1.20 0.90 1.00 1.00 ... ... ... … ... ... ... ... ... ... USDJPY 80.5 79.8 77.4 78.3 80.3 82.3 ... ... … ... ... ... ... ... ...

Euro-15 Real GDP (QoQ ann) 0.0 -0.8 -0.6 0.2 1.0 1.0 1.5 1.5 2.2 0.7 -0.6 1.2 1.9 1.5 -0.5 0.5 Inflation (YoY) 2.7 2.5 2.4 2.3 2.0 1.8 2.1 2.0 2.2 2.7 2.3 2.0 1.6 2.7 2.5 2.0 Policy rate 1.00 1.00 0.50 0.50 0.50 0.50 0.50 0.50 ... ... ... ... ... ... ... ... 10-yr bond yield 2.00 1.40 1.40 1.65 1.90 2.10 ... ... … ... ... ... ... ... ... ... EURUSD 1.28 1.27 1.19 1.17 1.18 1.19 ... ... … ... ... ... ... ... ... ...

UK Real GDP (QoQ ann) -1.7 -1.4 1.9 1.2 1.5 1.7 2.3 2.1 1.7 0.5 0.0 1.9 2.1 0.7 -0.3 1.4 Inflation (YoY) 3.5 2.7 2.0 1.6 1.6 1.8 2.3 2.3 3.4 4.6 1.6 2.3 3.3 4.5 2.4 2.0 Policy rate 0.50 0.50 0.50 0.50 0.50 0.50 0.50 0.50 ... ... ... ... ... ... ... ... 10-yr bond yield 2.20 1.80 1.80 2.00 2.30 2.35 ... ... … ... ... ... ... ... ... ... GBPUSD 1.53 1.57 1.54 1.54 1.55 1.55 ... ... … ... ... ... ... ... ... ...

Switzerland Real GDP (QoQ ann) 2.8 1.1 0.8 0.6 2.0 0.9 2.1 3.8 3.1 2.0 0.5 2.2 2.7 2.1 0.5 1.5 Inflation (YoY) -0.9 -1.0 0.0 0.9 1.3 0.9 0.7 0.8 0.3 -0.2 0.9 0.8 0.7 0.2 -0.3 1.0 Policy rate 0-0.25 0-0.25 0-0.25 0-0.25 0-0.25 ... ... ... … ... ... ... ... ... ... ... USDCHF 0.93 0.95 1.02 1.03 1.03 1.03 ... ... … ... ... ... ... ... ... ...

NJ Asia Real GDP (QoQ ann) 8.8 6.8 7.0 4.7 7.3 6.3 6.2 7.6 8.5 6.7 4.7 7.6 9.2 6.8 6.8 6.8 7.1

Inflation (YoY) 5.5 6.1 5.8 4.8 4.0 3.2 3.1 3.0 5.2 5.3 4.8 3.0 5.0 4.5 3.3 3.8 4.7 China Real GDP (YoY) 8.1 7.6 7.6 7.7 8.1 7.6 7.4 7.9 9.8 8.9 7.7 7.9 10.3 9.2 7.8 8.0 8.2 IP (YoY) 11.6 9.9 12.4 12.6 11.6 9.5 9.1 10.0 13.3 12.8 12.6 10.0 15.7 13.7 10.1 10.5 11.2 Inflation (YoY) 5.4 6.4 6.1 4.1 3.6 2.2 1.9 1.9 4.7 4.6 4.1 1.9 3.3 5.4 2.6 3.2 4.3 *India Real GDP (YoY) 9.2 8.0 6.7 6.1 5.3 5.5 5.3 4.5 8.7 6.4 6.1 4.5 8.4 6.5 5.0 6.5 7.5

EMEA Real GDP 3.6 2.9 3.0 3.3 3.6 3.6 3.6 3.4 5.2 4.2 3.3 3.4 4.7 4.9 3.3 3.6 Inflation (YoY) 5.9 5.4 6.3 6.0 5.9 5.9 5.4 5.2 7.0 6.6 6.0 5.2 6.6 6.7 5.5 5.9

Latin America Real GDP 3.5 2.9 3.0 3.4 3.3 3.7 4.1 4.2 5.5 3.7 3.4 4.2 6.3 4.6 3.1 3.9 Inflation (YoY) 6.4 6.1 6.1 6.1 6.5 6.4 6.4 6.3 6.6 7.0 6.1 6.3 6.2 6.7 6.2 6.4

Note: IMF PPP weights are used to compute regional and global aggregate figures. 10-year bond yield figures are averages for the last month of

each quarter; *Annual figures are on fiscal year basis.

Source: Credit Suisse estimates

13 June 2013

Jump-Start 8

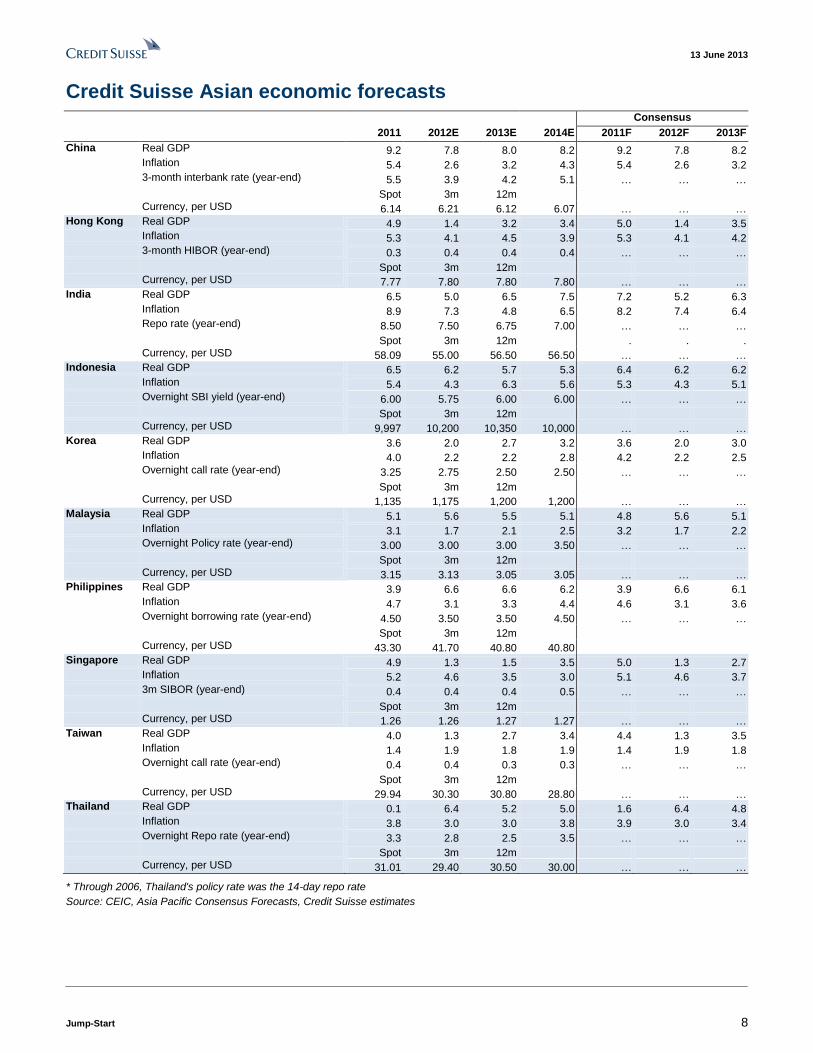

Credit Suisse Asian economic forecasts Consensus

2011 2012E 2013E 2014E 2011F 2012F 2013F

China Real GDP 9.2 7.8 8.0 8.2 9.2 7.8 8.2 Inflation 5.4 2.6 3.2 4.3 5.4 2.6 3.2 3-month interbank rate (year-end) 5.5 3.9 4.2 5.1 … … … Spot 3m 12m Currency, per USD 6.14 6.21 6.12 6.07 … … … Hong Kong Real GDP 4.9 1.4 3.2 3.4 5.0 1.4 3.5 Inflation 5.3 4.1 4.5 3.9 5.3 4.1 4.2 3-month HIBOR (year-end) 0.3 0.4 0.4 0.4 … … … Spot 3m 12m Currency, per USD 7.77 7.80 7.80 7.80 … … … India Real GDP 6.5 5.0 6.5 7.5 7.2 5.2 6.3 Inflation 8.9 7.3 4.8 6.5 8.2 7.4 6.4 Repo rate (year-end) 8.50 7.50 6.75 7.00 … … … Spot 3m 12m . . . Currency, per USD 58.09 55.00 56.50 56.50 … … … Indonesia Real GDP 6.5 6.2 5.7 5.3 6.4 6.2 6.2 Inflation 5.4 4.3 6.3 5.6 5.3 4.3 5.1 Overnight SBI yield (year-end) 6.00 5.75 6.00 6.00 … … … Spot 3m 12m Currency, per USD 9,997 10,200 10,350 10,000 … … … Korea Real GDP 3.6 2.0 2.7 3.2 3.6 2.0 3.0 Inflation 4.0 2.2 2.2 2.8 4.2 2.2 2.5 Overnight call rate (year-end) 3.25 2.75 2.50 2.50 … … … Spot 3m 12m Currency, per USD 1,135 1,175 1,200 1,200 … … … Malaysia Real GDP 5.1 5.6 5.5 5.1 4.8 5.6 5.1 Inflation 3.1 1.7 2.1 2.5 3.2 1.7 2.2 Overnight Policy rate (year-end) 3.00 3.00 3.00 3.50 … … … Spot 3m 12m Currency, per USD 3.15 3.13 3.05 3.05 … … … Philippines Real GDP 3.9 6.6 6.6 6.2 3.9 6.6 6.1 Inflation 4.7 3.1 3.3 4.4 4.6 3.1 3.6 Overnight borrowing rate (year-end) 4.50 3.50 3.50 4.50 … … … Spot 3m 12m Currency, per USD 43.30 41.70 40.80 40.80 Singapore Real GDP 4.9 1.3 1.5 3.5 5.0 1.3 2.7 Inflation 5.2 4.6 3.5 3.0 5.1 4.6 3.7 3m SIBOR (year-end) 0.4 0.4 0.4 0.5 … … … Spot 3m 12m Currency, per USD 1.26 1.26 1.27 1.27 … … … Taiwan Real GDP 4.0 1.3 2.7 3.4 4.4 1.3 3.5 Inflation 1.4 1.9 1.8 1.9 1.4 1.9 1.8 Overnight call rate (year-end) 0.4 0.4 0.3 0.3 … … … Spot 3m 12m Currency, per USD 29.94 30.30 30.80 28.80 … … … Thailand Real GDP 0.1 6.4 5.2 5.0 1.6 6.4 4.8 Inflation 3.8 3.0 3.0 3.8 3.9 3.0 3.4 Overnight Repo rate (year-end) 3.3 2.8 2.5 3.5 … … … Spot 3m 12m Currency, per USD 31.01 29.40 30.50 30.00 … … …

* Through 2006, Thailand's policy rate was the 14-day repo rate

Source: CEIC, Asia Pacific Consensus Forecasts, Credit Suisse estimates

13 June 2013

Jump-Start 9

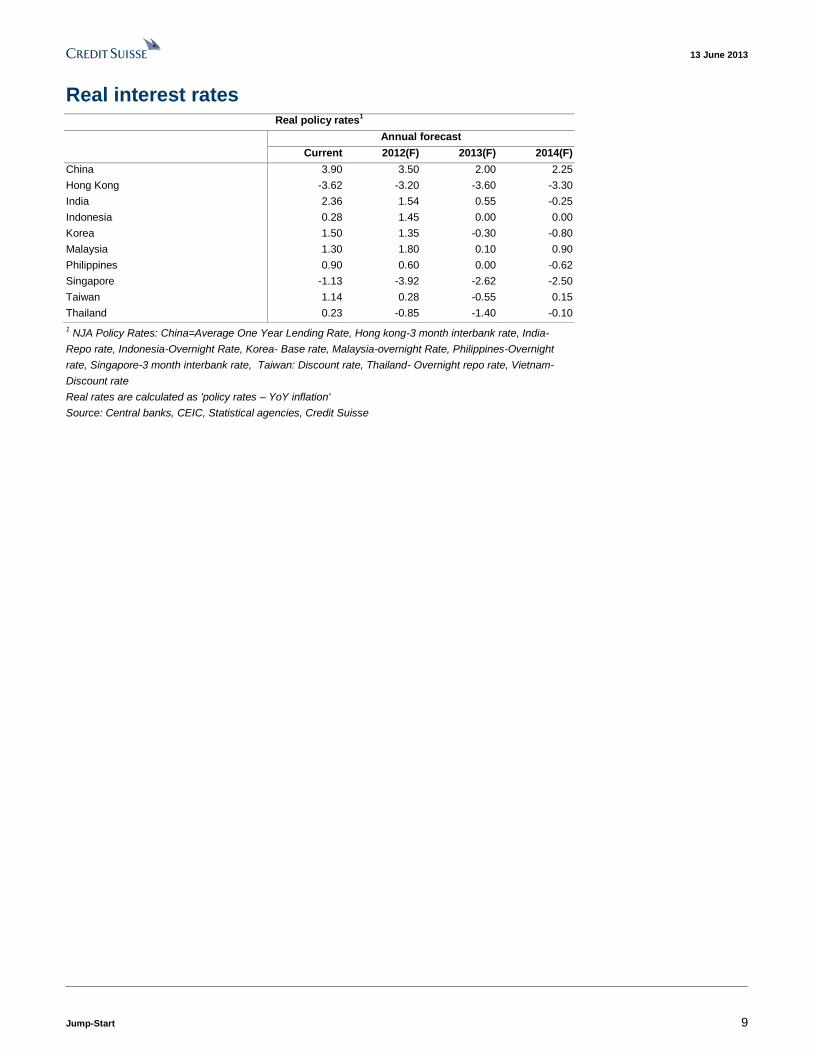

Real interest rates Real policy rates

1

Annual forecast

Current 2012(F) 2013(F) 2014(F)

China 3.90 3.50 2.00 2.25

Hong Kong -3.62 -3.20 -3.60 -3.30

India 2.36 1.54 0.55 -0.25

Indonesia 0.28 1.45 0.00 0.00

Korea 1.50 1.35 -0.30 -0.80

Malaysia 1.30 1.80 0.10 0.90

Philippines 0.90 0.60 0.00 -0.62

Singapore -1.13 -3.92 -2.62 -2.50

Taiwan 1.14 0.28 -0.55 0.15

Thailand 0.23 -0.85 -1.40 -0.10

1 NJA Policy Rates: China=Average One Year Lending Rate, Hong kong-3 month interbank rate, India-

Repo rate, Indonesia-Overnight Rate, Korea- Base rate, Malaysia-overnight Rate, Philippines-Overnight

rate, Singapore-3 month interbank rate, Taiwan: Discount rate, Thailand- Overnight repo rate, Vietnam-

Discount rate

Real rates are calculated as 'policy rates – YoY inflation'

Source: Central banks, CEIC, Statistical agencies, Credit Suisse

13 June 2013

Jump-Start 10

Top stories from Credit Suisse research last week

13 June 2013

Jump-Start 11

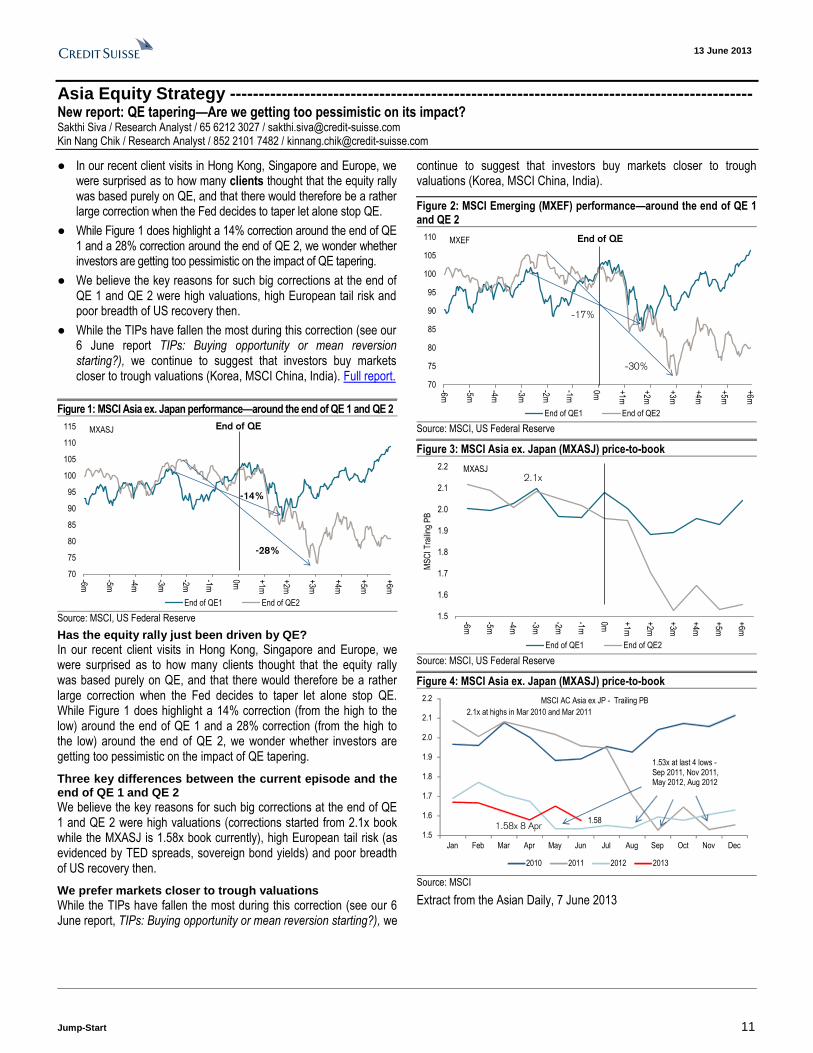

Asia Equity Strategy ------------------------------------------------------------------------------------------- New report: QE tapering—Are we getting too pessimistic on its impact? Sakthi Siva / Research Analyst / 65 6212 3027 / [email protected] Kin Nang Chik / Research Analyst / 852 2101 7482 / [email protected]

● In our recent client visits in Hong Kong, Singapore and Europe, we were surprised as to how many clients thought that the equity rally was based purely on QE, and that there would therefore be a rather large correction when the Fed decides to taper let alone stop QE.

● While Figure 1 does highlight a 14% correction around the end of QE 1 and a 28% correction around the end of QE 2, we wonder whether investors are getting too pessimistic on the impact of QE tapering.

● We believe the key reasons for such big corrections at the end of QE 1 and QE 2 were high valuations, high European tail risk and poor breadth of US recovery then.

● While the TIPs have fallen the most during this correction (see our 6 June report TIPs: Buying opportunity or mean reversion starting?), we continue to suggest that investors buy markets closer to trough valuations (Korea, MSCI China, India). Full report.

Figure 1: MSCI Asia ex. Japan performance—around the end of QE 1 and QE 2

70

75

80

85

90

95

100

105

110

115

-6m

-5m

-4m

-3m

-2m

-1m

0m +1m

+2m

+3m

+4m

+5m

+6m

MXASJ

End of QE1 End of QE2

-14%

-28%

End of QE

Source: MSCI, US Federal Reserve

Has the equity rally just been driven by QE?

In our recent client visits in Hong Kong, Singapore and Europe, we were surprised as to how many clients thought that the equity rally was based purely on QE, and that there would therefore be a rather large correction when the Fed decides to taper let alone stop QE. While Figure 1 does highlight a 14% correction (from the high to the low) around the end of QE 1 and a 28% correction (from the high to the low) around the end of QE 2, we wonder whether investors are getting too pessimistic on the impact of QE tapering.

Three key differences between the current episode and the end of QE 1 and QE 2

We believe the key reasons for such big corrections at the end of QE 1 and QE 2 were high valuations (corrections started from 2.1x book while the MXASJ is 1.58x book currently), high European tail risk (as evidenced by TED spreads, sovereign bond yields) and poor breadth of US recovery then.

We prefer markets closer to trough valuations

While the TIPs have fallen the most during this correction (see our 6 June report, TIPs: Buying opportunity or mean reversion starting?), we

continue to suggest that investors buy markets closer to trough valuations (Korea, MSCI China, India).

Figure 2: MSCI Emerging (MXEF) performance—around the end of QE 1 and QE 2

70

75

80

85

90

95

100

105

110

-6m

-5m

-4m

-3m

-2m

-1m

0m +1m

+2m

+3m

+4m

+5m

+6m

MXEF

End of QE1 End of QE2

-30%

-17%

End of QE

Source: MSCI, US Federal Reserve

Figure 3: MSCI Asia ex. Japan (MXASJ) price-to-book

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

-6m

-5m

-4m

-3m

-2m

-1m

0m +1m

+2m

+3m

+4m

+5m

+6m

MS

CI T

raili

ng P

B

MXASJ

End of QE1 End of QE2

2.1x

Source: MSCI, US Federal Reserve

Figure 4: MSCI Asia ex. Japan (MXASJ) price-to-book

1.58

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MSCI AC Asia ex JP - Trailing PB

2010 2011 2012 2013

1.53x at last 4 lows -Sep 2011, Nov 2011, May 2012, Aug 2012

2.1x at highs in Mar 2010 and Mar 2011

1.58x 8 Apr

Source: MSCI

Extract from the Asian Daily, 7 June 2013

13 June 2013

Jump-Start 12

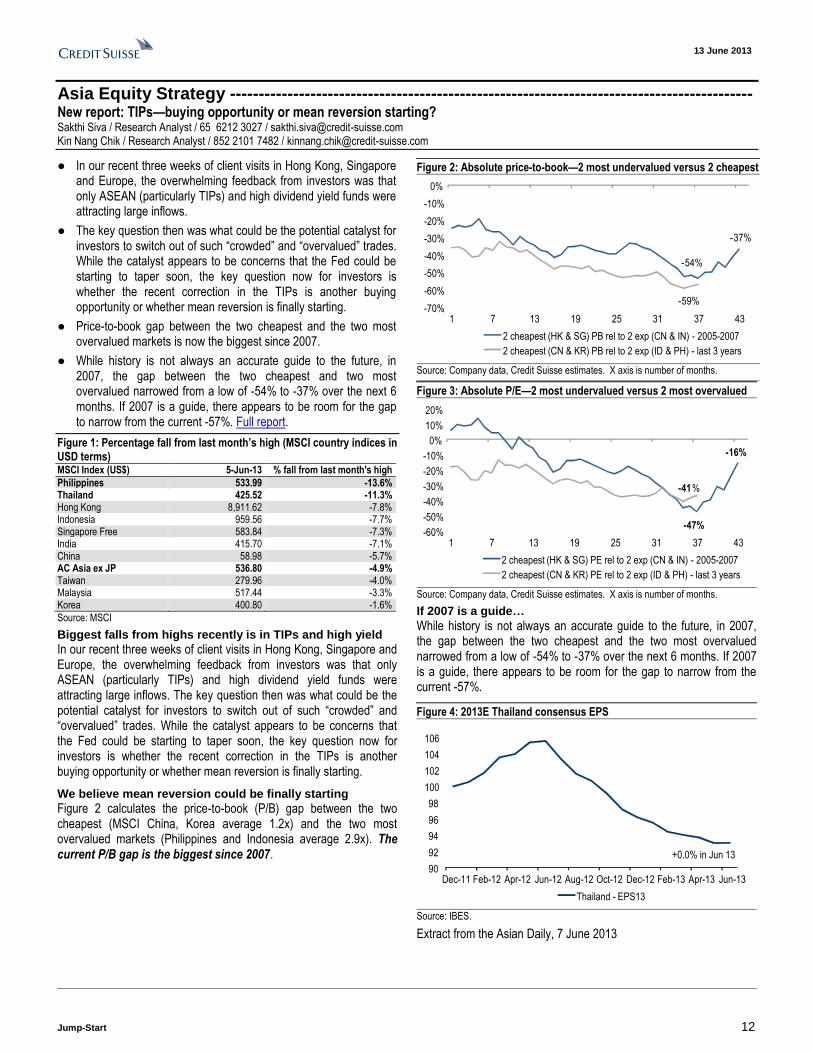

Asia Equity Strategy ------------------------------------------------------------------------------------------- New report: TIPs—buying opportunity or mean reversion starting? Sakthi Siva / Research Analyst / 65 6212 3027 / [email protected] Kin Nang Chik / Research Analyst / 852 2101 7482 / [email protected]

● In our recent three weeks of client visits in Hong Kong, Singapore and Europe, the overwhelming feedback from investors was that only ASEAN (particularly TIPs) and high dividend yield funds were attracting large inflows.

● The key question then was what could be the potential catalyst for investors to switch out of such “crowded” and “overvalued” trades. While the catalyst appears to be concerns that the Fed could be starting to taper soon, the key question now for investors is whether the recent correction in the TIPs is another buying opportunity or whether mean reversion is finally starting.

● Price-to-book gap between the two cheapest and the two most overvalued markets is now the biggest since 2007.

● While history is not always an accurate guide to the future, in 2007, the gap between the two cheapest and two most overvalued narrowed from a low of -54% to -37% over the next 6 months. If 2007 is a guide, there appears to be room for the gap to narrow from the current -57%. Full report.

Figure 1: Percentage fall from last month’s high (MSCI country indices in USD terms) MSCI Index (US$) 5-Jun-13 % fall from last month's high

Philippines 533.99 -13.6% Thailand 425.52 -11.3% Hong Kong 8,911.62 -7.8% Indonesia 959.56 -7.7% Singapore Free 583.84 -7.3% India 415.70 -7.1% China 58.98 -5.7% AC Asia ex JP 536.80 -4.9% Taiwan 279.96 -4.0% Malaysia 517.44 -3.3% Korea 400.80 -1.6%

Source: MSCI

Biggest falls from highs recently is in TIPs and high yield

In our recent three weeks of client visits in Hong Kong, Singapore and Europe, the overwhelming feedback from investors was that only ASEAN (particularly TIPs) and high dividend yield funds were attracting large inflows. The key question then was what could be the potential catalyst for investors to switch out of such “crowded” and “overvalued” trades. While the catalyst appears to be concerns that the Fed could be starting to taper soon, the key question now for investors is whether the recent correction in the TIPs is another buying opportunity or whether mean reversion is finally starting.

We believe mean reversion could be finally starting

Figure 2 calculates the price-to-book (P/B) gap between the two cheapest (MSCI China, Korea average 1.2x) and the two most overvalued markets (Philippines and Indonesia average 2.9x). The current P/B gap is the biggest since 2007.

Figure 2: Absolute price-to-book—2 most undervalued versus 2 cheapest

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

1 7 13 19 25 31 37 43

2 cheapest (HK & SG) PB rel to 2 exp (CN & IN) - 2005-2007

2 cheapest (CN & KR) PB rel to 2 exp (ID & PH) - last 3 years

-59%

-54%

-37%

Source: Company data, Credit Suisse estimates. X axis is number of months.

Figure 3: Absolute P/E—2 most undervalued versus 2 most overvalued

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

1 7 13 19 25 31 37 43

2 cheapest (HK & SG) PE rel to 2 exp (CN & IN) - 2005-2007

2 cheapest (CN & KR) PE rel to 2 exp (ID & PH) - last 3 years

-47%

-16%

-41%

Source: Company data, Credit Suisse estimates. X axis is number of months.

If 2007 is a guide…

While history is not always an accurate guide to the future, in 2007, the gap between the two cheapest and the two most overvalued narrowed from a low of -54% to -37% over the next 6 months. If 2007 is a guide, there appears to be room for the gap to narrow from the current -57%.

Figure 4: 2013E Thailand consensus EPS

90

92

94

96

98

100

102

104

106

Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12 Dec-12 Feb-13 Apr-13 Jun-13

Thailand - EPS13

+0.0% in Jun 13

Source: IBES.

Extract from the Asian Daily, 7 June 2013

13 June 2013

Jump-Start 13

Asia Equity Strategy ------------------------------------------------------------------------------------------- New report: TIPs—buying opportunity or mean reversion? Part 2 Sakthi Siva / Research Analyst / 65 6212 3027 / [email protected] Kin Nang Chik / Research Analyst / 852 2101 7482 / [email protected]

● TIPs – not yet a buying opportunity. With the TIPs falling by at least 15% in USD terms from their recent highs, investors may consider this a buying opportunity. But as discussed previously in our 6 June report, we believe it is not yet a buying opportunity and instead believe mean reversion is starting.

● Figure 1 highlights that the price to book gap between the three most undervalued markets (MSCI China, Korea, MSCI Hong Kong) and the three most overvalued markets (TIPs) is the biggest since 2007.

● Bond yields, currency, EPS revisions potential catalysts. We believe the recent rise in bond yields, currency weakness and EPS revisions that are no longer superior to the region could act as catalysts for this mean reversion.

● Korea the most attractive of the 3 most undervalued markets. Of the three most undervalued markets of MSCI China, Korea and MSCI Hong Kong, Korea looks the most attractive with price-to-book close to the last two troughs, underowned by foreign investors, and yen and EPS revisions stabilising. Full report.

Figure 1: Absolute price-to-book—3 cheapest versus 3 most overvalued

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

1 7 13 19 25 31 37 43

3 cheapest PB rel to 3 exp - 2005-2007 3 cheapest PB rel to 3 exp - last 3 years

-56%

-9%

-59%

Note: X axis is number of months. Source: Company data, Credit Suisse estimates

TIPs – buying opportunity or mean reversion? Part 2

TIPs – not yet a buying opportunity. With the TIPs falling by at least 15% in USD terms from their recent highs, investors may consider this a buying opportunity. But as discussed previously in our 6 June report, we believe it is not yet a buying opportunity and instead believe mean reversion is starting. Figure 1 highlights that the price to book gap between the three most undervalued markets (MSCI China, Korea, MSCI Hong Kong) and the three most overvalued markets (TIPs) is the biggest since 2007.

Bond yields, currency, EPS revisions potential catalysts. We believe the recent rise in bond yields (see Figures 2 and 3), currency weakness (two of the three TIPs have current account deficits, see Figure 4) and EPS revisions that are no longer superior to the region could act as catalysts for this mean reversion. For Thailand, we again highlight 11 consecutive months of downgrades to 2013E consensus EPS, and that those downgrades are more broad-based than just Energy.

Korea the most attractive of the 3 most undervalued markets. Of the three most undervalued markets of MSCI China, Korea and MSCI Hong Kong, Korea looks the most attractive with price-to-book close to the last two troughs, underowned by foreign investors, and Yen and EPS revisions stabilising.

Figure 2: Indonesia 10-year bond yield

5.0

5.2

5.4

5.6

5.8

6.0

6.2

6.4

6.6

6.8

Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13

Indonesia Govt Bond 10 yr (%)

Low 5.1%

6.67%

Source: the BLOOMBERG PROFESSIONAL™ service.

Figure 3: Thai 10-year bond yield

3.2

3.3

3.4

3.5

3.6

3.7

3.8

Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13

Thailand Govt Bond 10 yr (%)

Low 3.3%

3.7%

Source: the BLOOMBERG PROFESSIONAL™ service.

Figure 4: Thailand—current account deficit as a % of GDP

-10

-5

0

5

10

15

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013E

Thailand - current account as a % of GDP

-0.2%

Source: CEIC, Datastream, Credit Suisse estimates

Extract from the Asian Daily, 13 June 2013

13 June 2013

Jump-Start 14

Asia Technology Strategy ------------------------------------------------------------------------------------ New report: Mid-year review—One-eyed man in the land of the blind Manish Nigam / Research Analyst / 852 2101 7067 / [email protected]

● Last week, CS tech team visited several companies alongside the annual Computex show in Taipei. In our full note published today, we review our tech strategy in view of what we learnt last week and what has happened YTD. In summary, we remain modestly bullish about tech sector’s performance for the rest of the year.

● The outlook for the sector has remained mixed throughout the last eight quarters or so—a period over which tech has been the best performing sector. This time again, demand dynamics for tech remain largely mixed with hopes centred on some existing categories and expectations for some new launches.

● Earnings have been upgraded YTD but we expect a pause in that momentum until 2Q results are announced and we are closer to the seasonally strong months. Performance, as has been the case for the past few years around summer, is likely to remain challenging until then, particularly given the YTD outperformance.

● However, using this weakness to identify earnings growers could prove to be the successful strategy again, in our view, as has been the case for the past two years. Our top ideas include Samsung Electronics, SK Hynix, TSMC, ASE, TPK, Lenovo and HCL Tech.

Figure 1: MSCI AxJ sector performance – since 30 June 2011 (%)

(9)

(28)

(38)

(25)

(11)

4 3

(7)

10 9 8

-40

-30

-20

-10

0

10

20

NJA

En

erg

y

Ma

teria

ls

Indu

stri

als

Con

s. D

isc

Co

ns

Sta

ple

s

Hea

lth C

are

Fin

an

cia

ls

Te

ch

Te

lcos

Util

ities

(%)

Performance since 30-Jun-11

Source: MSCI, Factset

Our view on performance. Despite the sharp fall in Samsung Elec’s share price in the past few days, tech has still managed to outperform the market and more importantly most other cyclicals by 2-9 pp in 2Q13 so far. This outperformance has further added to tech’s consistent outperformance against both the overall region and cyclical sectors that started from mid-2011. Given that the sector’s performance over the past two years has been tied to the earnings momentum, our view, that the upgrade momentum is likely to see a pause until 2Q results, means that the sector’s performance could be challenging until then (see our full report for more details). We expect the upgrade momentum to likely resume going into August as we get more clarity about the launch schedule for Apple and Wintel products and we see a reconfirmation of margins from 2Q13 results. In any case, the sector has had a mid-year correction – sometime between April and August – for each of the past four years and this year may be no different. The magnitude of that correction will, of course, depend on what happens in broader markets, but our view is that the sector is unlikely to be under-performing even during this period given the supportive valuations versus earnings profile.

Figure 2: MSCI AxJ Tech – 2Q corrections

100

150

200

250

300

Jan-09 May-09 Sep-09 Jan-10 May-10 Sep-10 Jan-11 May-11 Sep-11 Jan-12 May-12 Sep-12 Jan-13 May-13

June-9%

Apr-May-18% May-Aug

-28%

May-Jun-16%

Source: MSCI, the BLOOMBERG PROFESSIONAL™ service.

Figure 3: MSCI AxJ Tech – 2013 and 2014 street EPS estimates (US$)

22

24

26

28

30

32

34

Feb-12 Apr-12 Jun-12 Aug-12 Oct-12 Dec-12 Feb-13 Apr-13

2014 EPS 2013 EPS

Source: MSCI, IBES, Datastream

Our view on the demand outlook: Wintel and Apple hold key to 2H. We were in Taiwan last week and met with several tech companies alongside the annual Computex show. We summarise our views on the demand and product dynamics in major end-markets impacting Asian tech. More details are in the full report.

A. Smartphones and tablets: Proliferation of devices continues. (1) No order cuts yet for upstream in early 3Q despite the slight build of inventory further downstream in the low-cost space. (2) Worries about an imminent slowdown in the high-end smartphone space are off the mark. (3) The 10”-sized tablet market seems to be under a significant challenge. (4) Apple will end up refreshing almost its entire hardware portfolio (and adding at least one new product) by November.

B. Wintel camp: Significant innovation but still trying to convince customers. (1) Several new chips and platforms launched at Computex. (2) Wintel eco-system is throwing most of its weight behind 2-in-1 or the hybrid tablet-cum-notebook devices. (3) We have been an early buyer of the mid-sized convertible devices theme so we believe in this story. However, challenges remain around price point, consumer education and availability. (4) We are quite convinced that touch interface is the way to go for almost all portable tech devices.

C. TVs: No major product cycle, but nothing sinister either. (1) News flow around China TV units likely to remain tough from August-September, though, most on the street should be aware of that. (2) A push for 4Kx2K products in China this Golden Week is likely.

Extract from the Asian Daily, 13 June 2013

13 June 2013

Jump-Start 15

Samsung Electronics ------------------------------------------------------- Maintain OUTPERFORM New report: Sanity checks on insane price action EPS: ◄► TP: ◄► Keon Han / Research Analyst / 822 3707 3740 / [email protected] Ray Kim / Research Analyst / 822 3707 3776 / [email protected]

● We conclude Friday’s sharp sell-off was overdone and in hindsight it should prove to be another buying opportunity in the long run. We believe a lack of quantifiable metrics for GS4 sales and the unknown fear factor of what the expectation adjustment means led to the sharp sell-off. We attempt to provide some rational numbers behind GS4.

● We look from various angles of what adjustments for slower GS4 means and how investors are pricing in Samsung’s handset business currently. To us, nothing justifies a decline of W14 trn in market cap—particularly due to few million units of GS4.

● Analysis: (1) Quantifiable adjustment that could impact earnings is W1.8 trn (4% of OP); (2) Current stock price values its handsets at 10% OPM, not its current 22%; and (3) valuation support is strong on both a historical and relative basis.

● More than a one product pony. Our thesis has been on handset mix improvement and sustainability of handset margins, which is unchanged. Smartphone volumes are tracking up 8% QoQ and blended ASP are rising at 9% QoQ on better product blend. Handset OPM is tracking about 22%, similar to 1Q13, ensuring ~9% QoQ OP growth for telecom division in 2Q13. Samsung Electronics is a CS NJA focus list stock. Full report.

Click here for detailed financials

Sanity check #1

We did a bottom-up build-up to get at theoretical revenue and OP generated by GS4 based on best available market understanding because no accurate data on price and profitability is available. Methodology: GS4 ASP assumption: $400 unit; GS4-only OPM: theoretically 30%, but 25% OPM simulation provided; 2013 GS4 shipment: 75 mn for consensus expectations, dropping to 60 mn as likely. Both extreme expectations and further adjustment o 55 mn was also simulated. Base case conclusion: Handsets represent about 69% of the company’s total OP. GS4 represents about 32% of all handset

OP and 22% of total company OP. Theoretical required OP adjustment for expectations change from 75-to-60 mn (15 mn delta) GS4 sales is about W1.9 trn in OP - 6% adjustment to total handset OP and 4% to total company OP. An expectations adjustment down to 55 mn GS4 would be about W2.6 trn OP—9% adjustment to handset op and 6% adjustment to total OP. An average cut of 5% in earnings at the worst case (if that since this assumes decline in sales and not being replaced by other products)—about W2 trn—driving down market capitalisation of W13 trn—equal to the entire market of LG Electronics (W12.4 trn), seems overdone in our opinion. While it is GS4 story at the moment, our thesis on the stock has consistently been on mix.

Sanity Check #2

While it is true that handsets represent 56% of the total company revenues and 69% of the company’s profits, other core business such as DRAM, NAND, System LSI, OLED, TVs, Home Appliances also have some intrinsic value attached to them. By isolating all of the non-handset revenues and earnings contribution, we can derive at handset business implied value. Methodology: All of Samsung’s non-handset business global comps have both double digit forward and trailing P/E multiples, if profitable. We think Samsung is one of the leaders in each of the categories, so ascribing 9x P/E on non-handset business to not demanding. As of Friday’s closing share price non-handset business at 9.0x P/E represents an implied W666K of W1.43 mn share price. By deduction, implied share price for the handset business is W761K, which implies 4.7x P/E. Of the handset universe, AAPL, HTC and LGE has 10x-to-16x P/E range. AAPL, Samsung’s, most likely comparable from a competitive standpoint is about 10.3x. Conclusion: If AAPL’s P/E is applied to Samsung’s handset earnings, Samsung’s implied EPS on the handset business is about W73,900 per share - or W10.9 trn in implied handset net income. Backing in effective tax rate, we implied OP is W13.8 trn. On estimated Handset revenues for 2013 of W134 trn, the current share price is stating that Samsung’s handset OPM is 10.3%. Clearly this is mispriced, as 1Q13 OPM was 22%, and even in a worst case scenario Samsung’s handset OPM is not likely to fall to 10%, even in 2014.

Sanity Check #3

Valuation support. Even highly anticipating the success of G4, Samsung’s stock price has not moved much, and is actually down YTD on Friday’s price action. Samsung’s 2013 estimated P/E is 6.1x. On a forward basis, it is 5.8x, and if not factoring in any growth the trailing P/E is 7.0x, substantially cheaper than most of its global peers. Even on trailing P/E basis, assuming no growth, the average since 2001 was 10.2x. It is currently trading at low-end of the range. Clearly, the low-multiples could be attributable to the very low dividend yield of 0.5%. However, we think it is just a matter of time before the cash balance is released to increase the dividends. Samsung’s cash-build is simply too strong to maintain.

Date Old rating New rating Old TP New TP

6 Feb, 2013 OUTPERFORM OUTPERFORM W1,720,000 W1,900,000

27 Nov, 2012 OUTPERFORM OUTPERFORM W1,700,000 W1,720,000

Extract from the Asian Daily, 10 June 2013

Bbg/RIC 005930 KS / 005930.KS Rating (prev. rating) O (O) Shares outstanding (mn) 147.30 Daily trad vol - 6m avg (mn) 0.3 Daily trad val - 6m avg (US$ mn) 343.9 Free float (%) 75.6 Major shareholders Samsung Life, 7.3%

Price (07 Jun 13 , W) 1,427,000 TP (prev. TP W) 1,900,000 (1,900,000) Est. pot. % chg. to TP 33 52-wk range (W) 1576000 - 1091000 Mkt cap (W/US$ bn) 210,196.2/ 188.2

Performance 1M 3M 12M

Absolute (%) (4.1) (4.8) 12.8 Relative (%) (2.4) (0.7) 8.7

Year 12/10A 12/11A 12/12E 12/13E 12/14E

Revenue (W bn) 154,630 165,002 201,103 240,531 268,255 EBITDA (W bn) 30,700 30,810 45,783 61,007 66,269 Net profit (W bn) 16,147 13,735 23,844 34,542 37,699 EPS (W) 109,617 93,243 161,876 234,502 255,932 - Change from prev. EPS (%) n.a. n.a. 0 0 0 - Consensus EPS (W) n.a. n.a. 153,950 215,743 237,885 EPS growth (%) 65.4 (14.9) 73.6 44.9 9.1 P/E (x) 13.0 15.3 8.8 6.1 5.6 Dividend yield (%) 0.8 0.4 0.6 0.7 1.2 EV/EBITDA (x) 6.9 6.8 4.5 3.1 2.4 P/B (x) 2.3 2.0 1.7 1.3 1.1 ROE (%) 19.4 14.2 20.9 24.4 21.4 Net debt(cash)/equity (%) 1.1 (0.2) (3.2) (15.2) (25.4)

Note 1: Samsung Electronics manufactures and exports a wide range of consumer and industrial electronic equipment and products such as memory chips, TFT-LCD, personal computers, peripherals, monitors, televisions, and home appliances.

13 June 2013

Jump-Start 16

Samsung Electronics ------------------------------------------------------- Maintain OUTPERFORM New report: Tweaking up earnings on better DRAM EPS: ▲ TP: ◄► Keon Han / Research Analyst / 82 2 3707 3740 / [email protected] Ray Kim / Research Analyst / 82 2 3707 3776 / [email protected]

● We tweak up 2013 and 2014 earnings by 2% on better DRAM forecast. On improved DRAM pricing and strong smartphone product cycle, Samsung’s 2Q13 OP is tracking W10.6 tn, up 21% QoQ. Seasonal products such as TVs and Appliance are also improving.

● Most of the earnings increase is driven by DRAMs. While Samsung is the most dominant DRAM producer, it caters more to the specialty DRAM segment, which is not seeing the price surge similar to PC DRAMs. But we think Samsung remains the most profitable DRAM maker with 31% DRAM OPM in 2Q13 based on technology lead.

● Total handset volumes are tracking no growth in volume on a QoQ basis. But smartphone volumes are up 8% and blended ASP is rising 9% QoQ on better product blend with estimated OPM of 22%—similar to 1Q13.

● We maintain our OUTPERFORM rating and TP based on the average of 2012/13 P/B, applying a target multiple of 1.85x, the average of the last ten years and the top-end of the post-2007 P/B range. Samsung Electronics is a CS NJA focus list stock. Full report.

Click here for detailed financials

Mid-quarter check slightly better

We tweak up 2013 and 2014 earnings by 2% mostly on our more optimistic global DRAM forecast. On much improved DRAM pricing, we believe Samsung’s 2Q13 OP is tracking in-line with consensus of W10.6 tn. Samsung’s overall core OP is rising 21% QoQ, benefiting from strong smartphone product cycle and memory semiconductor pick-up. Seasonally, TV OPM will likely return to mid-single digit levels on new product cycle and richer UHD TV mix where the company is seeing faster demand pick-up as the affordability ratio is improving. Home appliances’ profitability is also improving on seasonal products

such as A/C. Most other divisions are tracking in-line. We maintain our OUTPERFORM rating.

DRAM much stronger

Most of our upward earnings revision is driven by DRAM products. We maintain our positive view on the DRAM industry and believe the industry will continue to experience tight supply conditions throughout 2014, helping to stabilise blended DRAM ASP and expand OPM on better cost cuts. Samsung is the most diversified DRAM producer globally, dominating in the Mobile Server, PC, Graphics and Consumer DRAM segments. However, because it is more focused on the Mobile DRAM segment due to high internal demand requirements to support its smartphone and tablet PC programme, Samsung is proportionately less reliant on PC DRAMs. Also, while it remains the largest DRAM producer globally, DRAMs accounts for less than 10% of total earnings for the company due to the diversified nature of the overall business and the dominance of smartphones as the main profit contributor. Therefore, it does not fully benefit as much from the recent price surge in PC DRAMs. Still, we think Samsung remains the most profitable DRAM company with 31% DRAM OPM forecast for 2Q13 based on technology lead.

Total handset volume weaker, smartphones stronger

Total handset volumes are tracking no growth in volume on a QoQ basis compared with our earlier projection of a 5% QoQ increase. But we estimate smartphone volumes are up 8% QoQ and blended ASP is rising sharply at a 9% QoQ rate on a much better product blend. Handset OPM is tracking about 22%, similar to 1Q13, ensuring about 9% QoQ OP growth for the Telecom division. Change toward richer smartphone mix is occurring at a faster rate as feature phone volumes are declining at a more rapid rate. As a result, we lower our total handset estimate to 476 mn units from 494 mn units for 2013, while smartphone volumes are slightly tweaked down to 331 mn units from 333 mn. Total OP contribution from handsets remains W30 tn for the year on better blended ASP assumptions.

Tweaking earnings up

We raise 2013/2014 EPS by 2% each on stronger DRAM. Most other divisions are tracking in-line. We maintain our OUTPERFORM rating and TP based on the average of 2012/13 P/B, applying a target multiple of 1.85x, the average of the last ten years and the top-end of the post-2007 P/B range. Samsung Electronics is a CS NJA focus list

Rating history (005930.KS) Date Old rating New rating Old TP New TP

6 Feb, 2013 OUTPERFORM OUTPERFORM W1,720,000 W1,900,000

27 Nov, 2012 OUTPERFORM OUTPERFORM W1,700,000 W1,720,000

Extract from the Asian Daily, 7 June 2013

Bbg/RIC 005930 KS / 005930.KS Rating (prev. rating) O (O) Shares outstanding (mn) 147.30 Daily trad vol - 6m avg (mn) 0.3 Daily trad val - 6m avg (US$ mn) 334.4 Free float (%) 75.6 Major shareholders Samsung Life, 7.3%

Price (05 Jun 13, W) 1,521,000 TP (prev. TP W) 1,900,000 (1,900,000) Est. pot. % chg. to TP 25 52-wk range (W) 1576000 - 1091000 Mkt cap (W/US$ bn) 224,042.3/ 200.3

Performance 1M 3M 12M

Absolute (%) 1.9 1.5 26.4 Relative (%) 1.6 3.8 17.7

Year 12/10A 12/11A 12/12E 12/13E 12/14E

Revenue (W bn) 154,630 165,002 201,103 240,531 268,255 EBITDA (W bn) 30,700 30,810 45,783 61,007 66,269 Net profit (W bn) 16,147 13,735 23,844 34,542 37,699 EPS (W) 109,617 93,243 161,876 234,502 255,932 - Change from prev. EPS (%) n.a. n.a. 0 2 2 - Consensus EPS (W) n.a. n.a. 153,950 215,301 238,194 EPS growth (%) 65.4 (14.9) 73.6 44.9 9.1 P/E (x) 13.9 16.3 9.4 6.5 5.9 Dividend yield (%) 0.7 0.4 0.6 0.6 1.1 EV/EBITDA (x) 7.3 7.3 4.8 3.3 2.7 P/B (x) 2.5 2.2 1.8 1.4 1.2 ROE (%) 19.4 14.2 20.9 24.4 21.4 Net debt (cash)/equity (%) 1.1 (0.2) (3.2) (15.2) (25.4)

Note 1: Samsung Electronics manufactures and exports a wide range of consumer and industrial electronic equipment and products such as memory chips, TFT-LCD, personal computers, peripherals, monitors, televisions, and home appliances.

13 June 2013

Jump-Start 17

Metro Pacific Investments --------------------------- Initiating Coverage with OUTPERFORM New report: Hospitals biz deserves a second look Alvin Arogo / Research Analyst / 63 2 858 7716 / [email protected] Gab Roque / Research Analyst / 63 2 858 7756 / [email protected]

● We initiate coverage on Metro Pacific with an OUTPERFORM rating and a P7.90 SOTP-based target price, implying a 35% potential upside. Its investments are in utilities, toll roads and hospitals. We forecast that hospitals will contribute 11% to its 2014E net profit but see a bigger NAV contribution of 20%.

● Mainly driven by our assumption for an 18% CAGR in its number of beds, we forecast hospitals’ net income contribution will witness a 47% CAGR from 2013E to 2015E. This is higher than the 22% p.a. average of the two fastest-growing healthcare stocks in NJA.

● Consolidated cash flow and net profit is on solid ground, in our view, as 80% of its NAV comes from utilities and toll roads, which provide a combination of earnings visibility and growth.

● Despite 32% year-to-date share price increase, we believe that there is scope for further gains as the stock’s 2014E P/E of 15.3x is below its past five-year average level of 17.7x. Our SOTP valuation also suggests that ex-hospitals, MPI’s fair value is P6.40 or just 9% above its current share price. Full report.

Click here for detailed financials

Initiate with OUTPERFORM; 35% potential upside

We initiate coverage on Metro Pacific with an OUTPERFORM rating and a P7.90 target price, implying 35% potential upside. Our target price is SOTP-based and translates to an implied 2014E P/E of 20.6x and P/B of 2.0x (sector average of 18.0x and 2.2x, respectively). The company focuses on water, power, toll roads and hospitals. We forecast that hospitals will contribute 11% to 2014E net profit but we estimate that its NAV contribution is more substantial at 20%.

Multi-year growth potential for hospitals

Metro Pacific manages and operates various privately held hospitals and we forecast its total beds will increase by 18% CAGR to 3,000 by 2015. This would be the main driver for the 47% CAGR in its net income contribution, in our view. This is higher than the 22% p.a.

average of the two fastest-growing healthcare stocks in NJA. Over the long term, we believe growth will be driven by the potential for higher per capita healthcare spending and capacity investments, as these have a high positive correlation with improvements in GDP per capita.

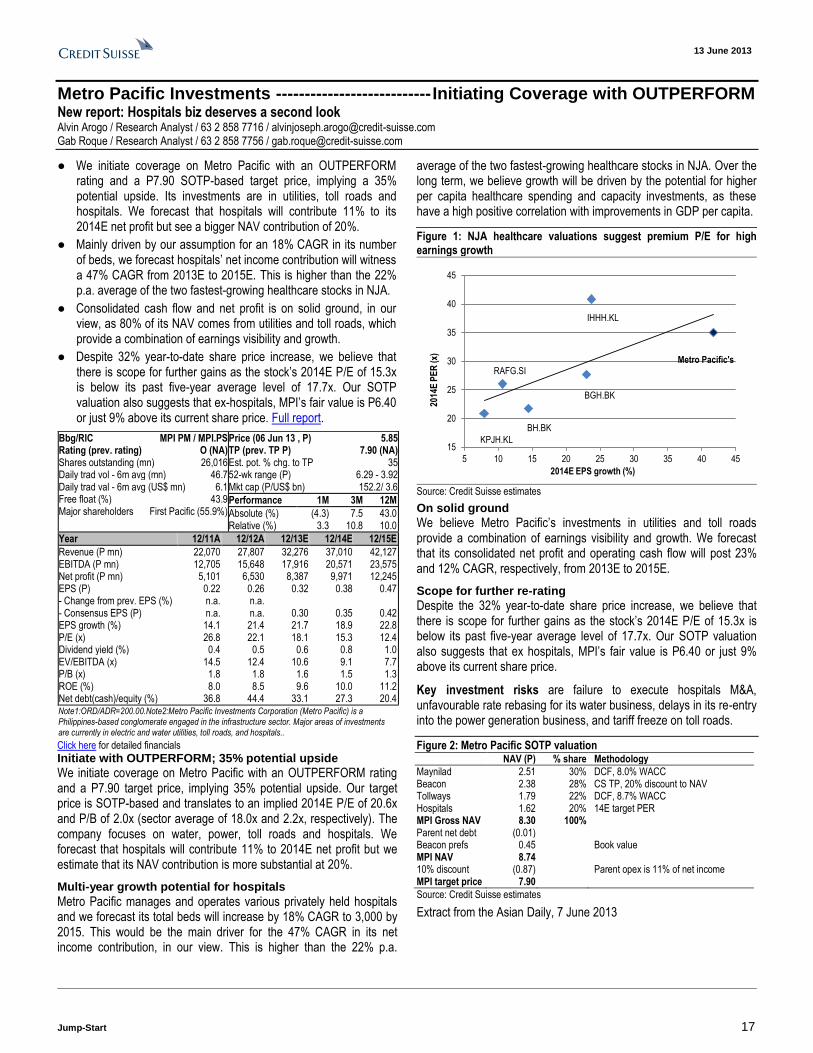

Figure 1: NJA healthcare valuations suggest premium P/E for high earnings growth

15

20

25

30

35

40

45

5 10 15 20 25 30 35 40 45

2014E EPS growth (%)

2014

E P

ER

(x) Metro Pacific's

IHHH.KL

BGH.BK

BH.BK

RAFG.SI

KPJH.KL

Source: Credit Suisse estimates

On solid ground

We believe Metro Pacific’s investments in utilities and toll roads provide a combination of earnings visibility and growth. We forecast that its consolidated net profit and operating cash flow will post 23% and 12% CAGR, respectively, from 2013E to 2015E.

Scope for further re-rating

Despite the 32% year-to-date share price increase, we believe that there is scope for further gains as the stock’s 2014E P/E of 15.3x is below its past five-year average level of 17.7x. Our SOTP valuation also suggests that ex hospitals, MPI’s fair value is P6.40 or just 9% above its current share price.

Key investment risks are failure to execute hospitals M&A, unfavourable rate rebasing for its water business, delays in its re-entry into the power generation business, and tariff freeze on toll roads.

Figure 2: Metro Pacific SOTP valuation NAV (P) % share Methodology

Maynilad 2.51 30% DCF, 8.0% WACC Beacon 2.38 28% CS TP, 20% discount to NAV Tollways 1.79 22% DCF, 8.7% WACC Hospitals 1.62 20% 14E target PER MPI Gross NAV 8.30 100% Parent net debt (0.01) Beacon prefs 0.45 Book value MPI NAV 8.74 10% discount (0.87) Parent opex is 11% of net income MPI target price 7.90

Source: Credit Suisse estimates

Extract from the Asian Daily, 7 June 2013

Bbg/RIC MPI PM / MPI.PS Rating (prev. rating) O (NA) Shares outstanding (mn) 26,016 Daily trad vol - 6m avg (mn) 46.7 Daily trad val - 6m avg (US$ mn) 6.1 Free float (%) 43.9 Major shareholders First Pacific (55.9%)

Price (06 Jun 13 , P) 5.85 TP (prev. TP P) 7.90 (NA) Est. pot. % chg. to TP 35 52-wk range (P) 6.29 - 3.92 Mkt cap (P/US$ bn) 152.2/ 3.6

Performance 1M 3M 12M

Absolute (%) (4.3) 7.5 43.0 Relative (%) 3.3 10.8 10.0

Year 12/11A 12/12A 12/13E 12/14E 12/15E

Revenue (P mn) 22,070 27,807 32,276 37,010 42,127 EBITDA (P mn) 12,705 15,648 17,916 20,571 23,575 Net profit (P mn) 5,101 6,530 8,387 9,971 12,245 EPS (P) 0.22 0.26 0.32 0.38 0.47 - Change from prev. EPS (%) n.a. n.a. - Consensus EPS (P) n.a. n.a. 0.30 0.35 0.42 EPS growth (%) 14.1 21.4 21.7 18.9 22.8 P/E (x) 26.8 22.1 18.1 15.3 12.4 Dividend yield (%) 0.4 0.5 0.6 0.8 1.0 EV/EBITDA (x) 14.5 12.4 10.6 9.1 7.7 P/B (x) 1.8 1.8 1.6 1.5 1.3 ROE (%) 8.0 8.5 9.6 10.0 11.2 Net debt(cash)/equity (%) 36.8 44.4 33.1 27.3 20.4

Note1:ORD/ADR=200.00.Note2:Metro Pacific Investments Corporation (Metro Pacific) is a Philippines-based conglomerate engaged in the infrastructure sector. Major areas of investments are currently in electric and water utilities, toll roads, and hospitals..

13 June 2013

Jump-Start 18

Gajah Tunggal -------------------------------------------- Initiating Coverage with OUTPERFORM New report: Full of grip Dian Haryokusumo / Research Analyst / 62 21 255 37974 / [email protected]

● We initiate coverage on Gajah Tunggal (GT) with an OUTPERFORM rating and a target price of Rp4,300. It is the largest integrated SEA tyre manufacturer with own production of synthetic rubber and tyre cords. Click here for the full report.

● For radial tyre, GT has 24% market share in replacement market. We expect this to improve to 27% by FY15 through better penetration into OEM tyre by: (1) being the biggest tyre supplier for Suzuki Ertiga (the new breakthrough low-end MPV after Toyota Avanza and Daihatsu Xenia), and (2) supplying the potential low cost green car (LCGC) market.

● GT to continue to dominate 2W and bias (heavy duty) tyres. Over 70% of revenue came from replacement, a high-margin business. GT has been the biggest tyre supplier for Yamaha / Suzuki motorcycles.

● Undemanding valuation. The stock is trading at 8.0x FY13E P/E, 13% discount to regional tyre peers, 33% discount to Indo auto. The stock is also a play on domestic consumption, benefitting from rising middle-high income population, where it is trading at a steep discount of around 76% to Indonesian consumer stocks.

Click here for detailed financials

Initiate coverage with an OUTPERFORM rating

Gajah Tunggal (GT) is the largest integrated SEA tyre manufacturer with own production of synthetic rubber and tyre cords. We believe Indonesia’s tyre industry would benefit from growing auto industry, where we started to see an inflection point in 4W population, growing at 11% CAGR over FY13–15E. GT’s valuation is undemanding, trading at 8.0x FY13E P/E, 13% discount to regional tyre peers, 33% discount to Indonesia auto. The stock is also a play on domestic consumption, benefitting from rising middle-high income population, where it is trading at a steep discount of around 76% to Indonesian consumer stocks.

Improvement in the replacement market by better penetrating into OEM business

Domestic replacement tyre contributing more than 50% of GT’s total tyre revenue. For radial tyre, GT has 24% market share in the replacement market. We expect this market share to improve to 27% by FY15 through better penetration into OEM tyre by: (1) being the biggest tyre supplier for Suzuki Ertiga (the new breakthrough low-end MPV after Toyota Avanza and Daihatsu Xenia), (2) supplying the potential LCGC market. We expect domestic radial tyre revenue to grow at 28% CAGR.

Continues to dominate 2W and bias (heavy duty) tyres

More than 70% of each 2W and bias tyre revenue is generated from replacements, a high-margin business. GT has been the biggest tyre supplier for Yamaha and Suzuki motorcycles. We expect the combined revenue to witness a 14% CAGR over FY13–15, with 2W tyres being the primary growth driver.

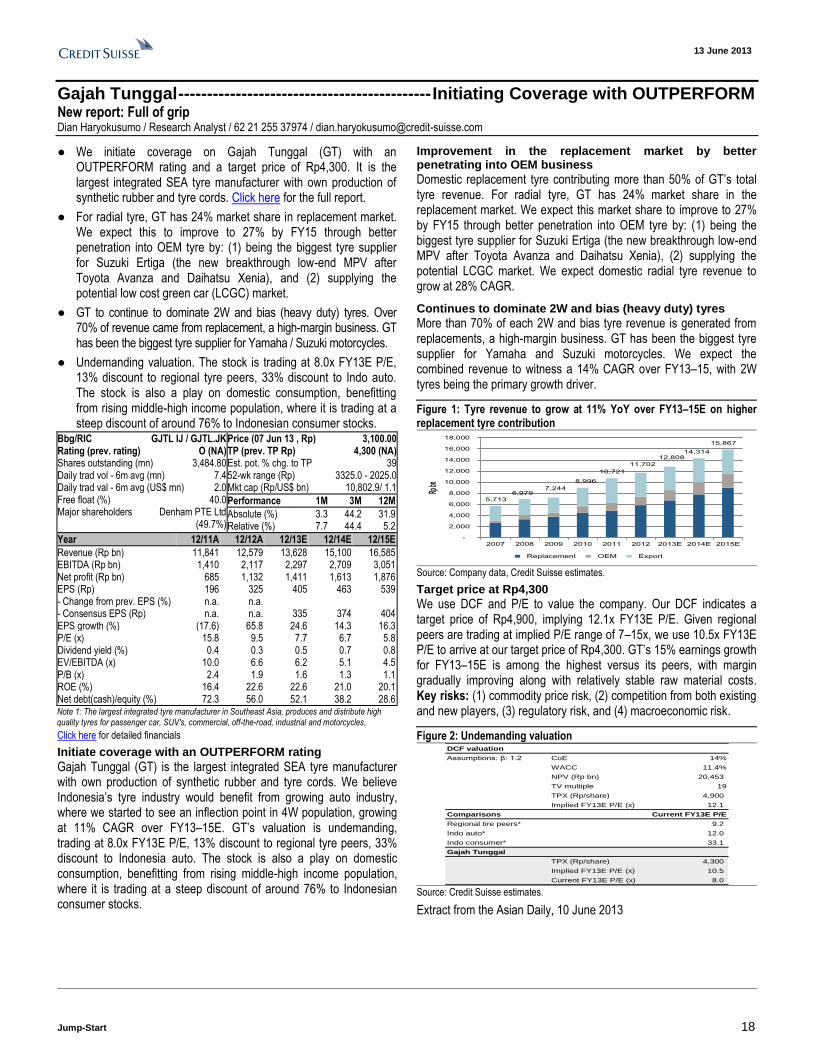

Figure 1: Tyre revenue to grow at 11% YoY over FY13–15E on higher replacement tyre contribution

5,713

6,979 7,244

8,996

10,721

11,702

12,808 14,314

15,867

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2007 2008 2009 2010 2011 2012 2013E 2014E 2015E

Rp bn

Replacement OEM Export

Source: Company data, Credit Suisse estimates.

Target price at Rp4,300

We use DCF and P/E to value the company. Our DCF indicates a target price of Rp4,900, implying 12.1x FY13E P/E. Given regional peers are trading at implied P/E range of 7–15x, we use 10.5x FY13E P/E to arrive at our target price of Rp4,300. GT’s 15% earnings growth for FY13–15E is among the highest versus its peers, with margin gradually improving along with relatively stable raw material costs. Key risks: (1) commodity price risk, (2) competition from both existing and new players, (3) regulatory risk, and (4) macroeconomic risk.

Figure 2: Undemanding valuation DCF valuation

Assumptions: β: 1.2 CoE 14%

WACC 11.4%

NPV (Rp bn) 20,453

TV multiple 19

TPX (Rp/share) 4,900

Implied FY13E P/E (x) 12.1

Comparisons Current FY13E P/E

Regional tire peers* 9.2

Indo auto* 12.0

Indo consumer* 33.1

Gajah Tunggal

TPX (Rp/share) 4,300

Implied FY13E P/E (x) 10.5

Current FY13E P/E (x) 8.0 Source: Credit Suisse estimates.

Extract from the Asian Daily, 10 June 2013

Bbg/RIC GJTL IJ / GJTL.JK Rating (prev. rating) O (NA) Shares outstanding (mn) 3,484.80 Daily trad vol - 6m avg (mn) 7.4 Daily trad val - 6m avg (US$ mn) 2.0 Free float (%) 40.0 Major shareholders Denham PTE Ltd

(49.7%)

Price (07 Jun 13 , Rp) 3,100.00 TP (prev. TP Rp) 4,300 (NA) Est. pot. % chg. to TP 39 52-wk range (Rp) 3325.0 - 2025.0 Mkt cap (Rp/US$ bn) 10,802.9/ 1.1

Performance 1M 3M 12M

Absolute (%) 3.3 44.2 31.9 Relative (%) 7.7 44.4 5.2

Year 12/11A 12/12A 12/13E 12/14E 12/15E

Revenue (Rp bn) 11,841 12,579 13,628 15,100 16,585 EBITDA (Rp bn) 1,410 2,117 2,297 2,709 3,051 Net profit (Rp bn) 685 1,132 1,411 1,613 1,876 EPS (Rp) 196 325 405 463 539 - Change from prev. EPS (%) n.a. n.a. - Consensus EPS (Rp) n.a. n.a. 335 374 404 EPS growth (%) (17.6) 65.8 24.6 14.3 16.3 P/E (x) 15.8 9.5 7.7 6.7 5.8 Dividend yield (%) 0.4 0.3 0.5 0.7 0.8 EV/EBITDA (x) 10.0 6.6 6.2 5.1 4.5 P/B (x) 2.4 1.9 1.6 1.3 1.1 ROE (%) 16.4 22.6 22.6 21.0 20.1 Net debt(cash)/equity (%) 72.3 56.0 52.1 38.2 28.6

Note 1: The largest integrated tyre manufacturer in Southeast Asia, produces and distribute high quality tyres for passenger car, SUV's, commercial, off-the-road, industrial and motorcycles.

13 June 2013

Jump-Start 19

China Coal Sector ----------------------------------------------------------------------------------------------- New report: Finding floor Trina Chen / Research Analyst / 852 2101 7031 / [email protected] Frankie Zhu / Research Analyst / 852 2101 7426 / [email protected]

● It is Déjà vu of 2Q12—weak demand, strong hydro and rising imports. We estimate it would take a demand growth acceleration of 6-7% from the current level for the coastal coal market to move back to balance: optimistic based on macro outlook. Full report

● Nevertheless, we believe the spot coal price in China has mostly floored, given 15-30% of the production is already at loss in our estimates, due to low calorific value, or high cost.

● While coal price may stay flat for longer, earnings risk is on the downside in the coming months, driven by short-fall in ASP partly due to discount of mid-ranged CV coal, potential miss in cost targets (Yanzhou and Chinacoal), coupled with operational leverage. Our stress test suggests ROE versus P/B is more attractive for Shenhua, but negative for Yanzhou, Yitai and MMC.

● Our top picks are Shenhua (maintain OUTPERFORM) for thermal and Fushan (maintain NEUTRAL) for met coal. We downgrade Chinacoal to NEUTRAL (from Outperform) with a revised target of HK$5.9 (from $9.6), and Yitai to NEUTRAL from Outperform with a revised TP of HK$35.9. Maintain UNDERPERFORM on Yanzhou.

Figure 1: Coverage summary—China coal sector Company Ticker Shr Ratings Target Earnings chg P/E P/B EV/EBITDA

Price as of Jun 11 Price New Old New Old 13E 14E 13E 14E 13E 14E 13E 14E

Shenhua 1088.HK 24.6 O O 34.9 39.7 -9% -16% 8.8 7.8 1.4 1.2 5.4 4.6

Chinacoal 1898.HK 4.8 N O 5.9 9.6 -37% -38% 9.7 8.8 0.6 0.6 8.0 7.1

Yanzhou 1171.HK 7.6 U U 6.6 6.6 -21% -21% 14.6 11.6 0.7 0.6 10.4 7.4

Yitai 3948.HK 39.9 N O 35.9 53.0 -29% -42% 11.1 10.6 2.3 2.0 7.9 7.6

Fushan 0639.HK 3.0 N N 2.6 3.1 -26% -21% 13.7 11.9 0.8 0.8 4.7 3.9

Hidili 1393.HK 1.7 U U 1.3 1.1 n.a. -34% n.a. 12.4 0.4 0.4 16.4 10.1

MMC 0975.HK 1.8 U U 1.3 2.3 -84% -48% 91.0 16.9 1.1 1.0 13.9 8.9

Winsway 1733.HK 0.6 U U 0.4 0.7 15% 32% n.a. n.a. 0.4 0.4 10.7 7.6 Source: Company data, Credit Suisse estimates.

Figure 2: P/B versus ROE (base case and stress test case)

1.4

0.6 0.7

2.3

0.8

0.4

1.1

0.4

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

-10%

-5%

0%

5%

10%

15%

20%

25%

Shenhua Chinacoal Yanzhou Yitai Fushan Hidili MMC Winsway

Base case Stress test case (spot coal price soften by another Rmb50/t) P/B

2013E ROE (recurring) (%) P/B (x)

Source: Company data, Credit Suisse estimates.

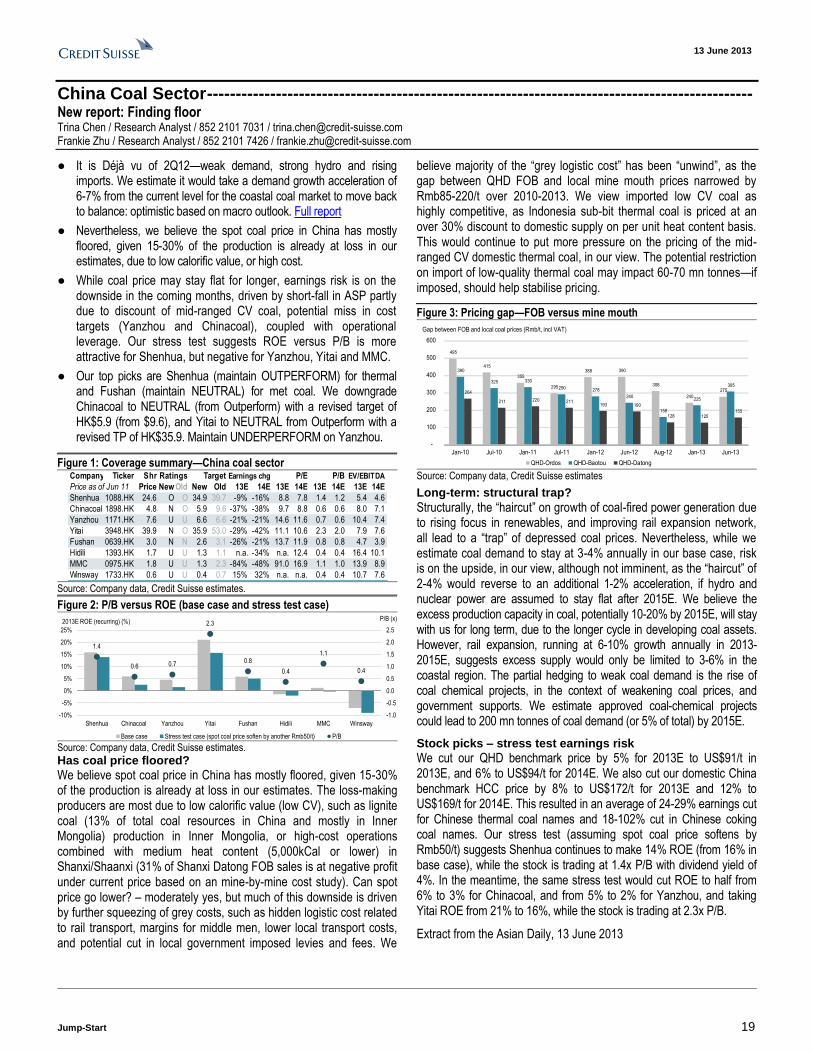

Has coal price floored?

We believe spot coal price in China has mostly floored, given 15-30% of the production is already at loss in our estimates. The loss-making producers are most due to low calorific value (low CV), such as lignite coal (13% of total coal resources in China and mostly in Inner Mongolia) production in Inner Mongolia, or high-cost operations combined with medium heat content (5,000kCal or lower) in Shanxi/Shaanxi (31% of Shanxi Datong FOB sales is at negative profit under current price based on an mine-by-mine cost study). Can spot price go lower? – moderately yes, but much of this downside is driven by further squeezing of grey costs, such as hidden logistic cost related to rail transport, margins for middle men, lower local transport costs, and potential cut in local government imposed levies and fees. We

believe majority of the “grey logistic cost” has been “unwind”, as the gap between QHD FOB and local mine mouth prices narrowed by Rmb85-220/t over 2010-2013. We view imported low CV coal as highly competitive, as Indonesia sub-bit thermal coal is priced at an over 30% discount to domestic supply on per unit heat content basis. This would continue to put more pressure on the pricing of the mid-ranged CV domestic thermal coal, in our view. The potential restriction on import of low-quality thermal coal may impact 60-70 mn tonnes—if imposed, should help stabilise pricing.

Figure 3: Pricing gap—FOB versus mine mouth

495

415

355

295

388 390

308

240

275

390

325 330

290 278

240

158

225

305

264

211 220 211 193 190

128 125 155

-

100

200

300

400

500

600

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jun-12 Aug-12 Jan-13 Jun-13

QHD-Ordos QHD-Baotou QHD-Datong

Gap between FOB and local coal prices (Rmb/t, incl VAT)

Source: Company data, Credit Suisse estimates

Long-term: structural trap?