Embed Size (px)

Citation preview

FOTO CAPA

24 March 2016 Equity Research

Braz il ian Malls First Rule of Retailers’ Woes Is You Don’t Talk About

Retailers’ Woes

Nicole Hirakawa 55 11 3701 6307 [email protected]

Luis Stacchini 55 11 3701 6121 [email protected]

Vanessa Quiroga 52 55 5283 8939 [email protected]

After two years of weak sales performance (2016 to be no different) and significant inflationary pressure, several large retailers

are struggling. In this report, we investigate the financial health of the main retailers and malls’ exposure to mom & pop shops.

One-third of the largest retailers face some degree of financial hardship. We analyzed the largest mall retailers in the

segments of apparel, home appliances and miscellaneous (super-market, cosmetics and others). 6.5% of these retailers were

considered red flags, i.e. already filed for chapter 11 or are in serious financial distress. 25% of the surveyed universe was

considered yellow flag for having a substantial amount of protested bills by creditors or ND/EBITDA above 2.5x. All listed

companies have some exposure to these riskier retailers, 8%-10% of total store count.

If the largest chains are in financial difficulty, we wonder how the mom & pop shops are coping. These tier 5 retailers,

account for 30% of malls’ store count and are the most exposed to economic downturns for being less professionally managed

and having little or no access to capital. Multiplan and Iguatemi have the lowest exposure to mom & pop shops, which represent

22% and 27% of their store count, respectively, vs. ~32% for the other companies.

Micro to show its ugly face. After recent rally, we no longer see the malls as a reasonable way to play a potential political shift.

In 2016, we expect micro conditions to slowly become apparent while valuations don’t seem supportive. Vacancy and

delinquency risks are higher and key factor will be ability to replace retailers reducing store fleet and the ones that will go bust.

Lowering our estimates for 2016-17. In this spirit, we are factoring in a longer period until recovery, as retailers are in poor

financial shape. The higher occupancy costs and lower productivity (sales per sqm) vs. historical make us believe that future SSS

growth, when it comes, will serve to put retailers back on their feet, taking longer to translate in rent growth. In this scenario, we

favor Multiplan for its lower exposure to risky retailers and above average capacity to attract tenants – company increased the

number of top tier stores by 5% during 2Q15-1Q16.

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

2

24 March 2016

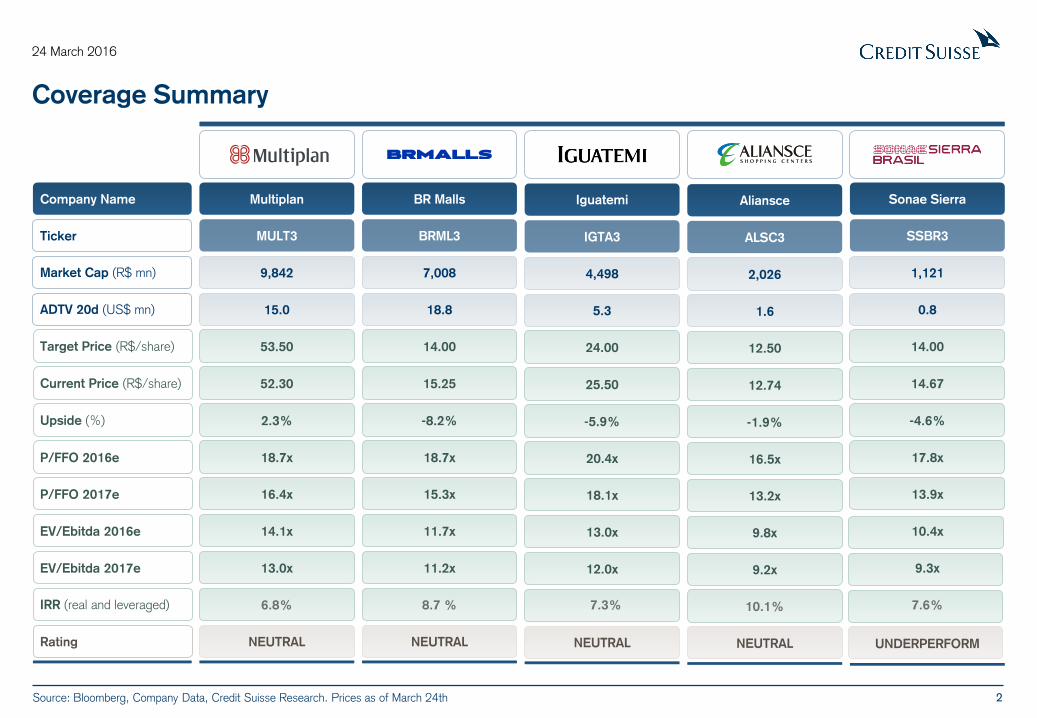

Coverage Summary

Company Name

Ticker

Market Cap (R$ mn)

ADTV 20d (US$ mn)

Target Price (R$/share)

Current Price (R$/share)

Upside (%)

Rating

P/FFO 2016e

P/FFO 2017e

EV/Ebitda 2016e

EV/Ebitda 2017e

IRR (real and leveraged)

Multiplan

MULT3

9,842

15.0

53.50

52.30

2.3%

18.7x

16.4x

14.1x

13.0x

6.8%

NEUTRAL

BR Malls

BRML3

7,008

18.8

14.00

15.25

-8.2%

18.7x

15.3x

11.7x

11.2x

8.7 %

NEUTRAL

Aliansce

ALSC3

2,026

1.6

12.50

12.74

-1.9%

16.5x

13.2x

9.8x

9.2x

10.1%

NEUTRAL

Sonae Sierra

SSBR3

1,121

0.8

14.00

14.67

-4.6%

17.8x

13.9x

10.4x

9.3x

7.6%

UNDERPERFORM

Iguatemi

IGTA3

4,498

5.3

24.00

25.50

-5.9%

20.4x

18.1x

13.0x

12.0x

7.3%

NEUTRAL

Source: Bloomberg, Company Data, Credit Suisse Research. Prices as of March 24th

3

24 March 2016

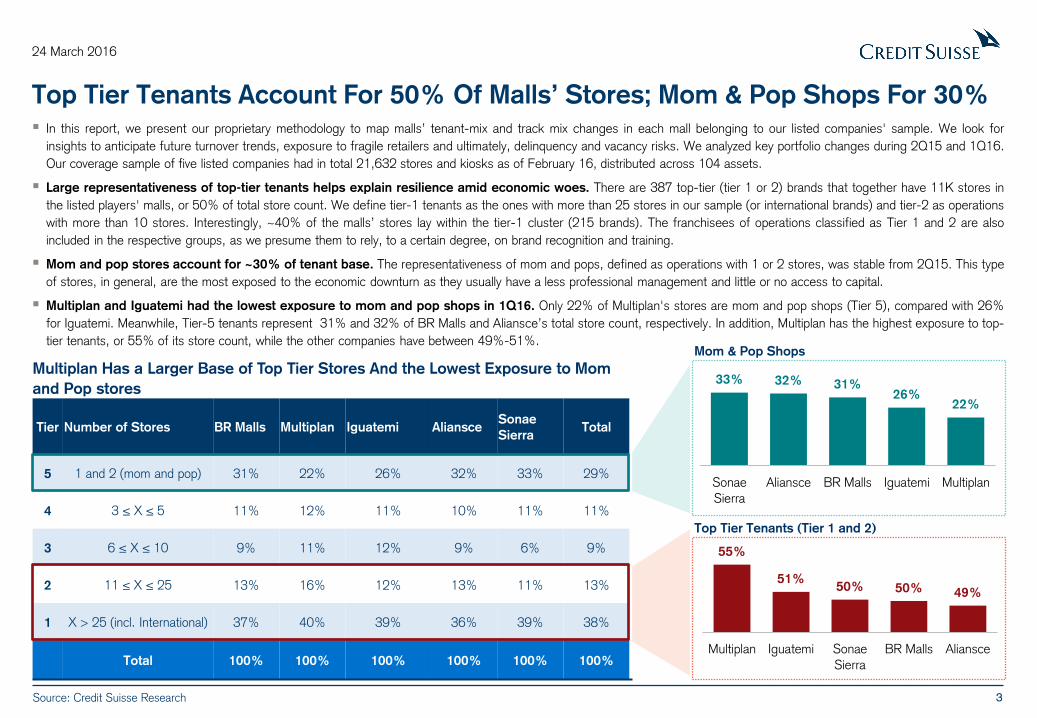

Top Tier Tenants Account For 50% Of Malls’ Stores; Mom & Pop Shops For 30%

In this report, we present our proprietary methodology to map malls’ tenant-mix and track mix changes in each mall belonging to our listed companies' sample. We look for

insights to anticipate future turnover trends, exposure to fragile retailers and ultimately, delinquency and vacancy risks. We analyzed key portfolio changes during 2Q15 and 1Q16.

Our coverage sample of five listed companies had in total 21,632 stores and kiosks as of February 16, distributed across 104 assets.

Large representativeness of top-tier tenants helps explain resilience amid economic woes. There are 387 top-tier (tier 1 or 2) brands that together have 11K stores in

the listed players' malls, or 50% of total store count. We define tier-1 tenants as the ones with more than 25 stores in our sample (or international brands) and tier-2 as operations

with more than 10 stores. Interestingly, ~40% of the malls’ stores lay within the tier-1 cluster (215 brands). The franchisees of operations classified as Tier 1 and 2 are also

included in the respective groups, as we presume them to rely, to a certain degree, on brand recognition and training.

Mom and pop stores account for ~30% of tenant base. The representativeness of mom and pops, defined as operations with 1 or 2 stores, was stable from 2Q15. This type

of stores, in general, are the most exposed to the economic downturn as they usually have a less professional management and little or no access to capital.

Multiplan and Iguatemi had the lowest exposure to mom and pop shops in 1Q16. Only 22% of Multiplan's stores are mom and pop shops (Tier 5), compared with 26%

for Iguatemi. Meanwhile, Tier-5 tenants represent 31% and 32% of BR Malls and Aliansce’s total store count, respectively. In addition, Multiplan has the highest exposure to top-

tier tenants, or 55% of its store count, while the other companies have between 49%-51%.

Source: Credit Suisse Research

Tier Number of Stores BR Malls Multiplan Iguatemi Aliansce Sonae

Sierra Total

5 1 and 2 (mom and pop) 31% 22% 26% 32% 33% 29%

4 3 ≤ X ≤ 5 11% 12% 11% 10% 11% 11%

3 6 ≤ X ≤ 10 9% 11% 12% 9% 6% 9%

2 11 ≤ X ≤ 25 13% 16% 12% 13% 11% 13%

1 X > 25 (incl. International) 37% 40% 39% 36% 39% 38%

Total 100% 100% 100% 100% 100% 100%

Multiplan Has a Larger Base of Top Tier Stores And the Lowest Exposure to Mom

and Pop stores

55%

51% 50% 50% 49%

Multiplan Iguatemi Sonae

Sierra

BR Malls Aliansce

33% 32% 31% 26%

22%

Sonae

Sierra

Aliansce BR Malls Iguatemi Multiplan

Mom & Pop Shops

Top Tier Tenants (Tier 1 and 2)

4

24 March 2016

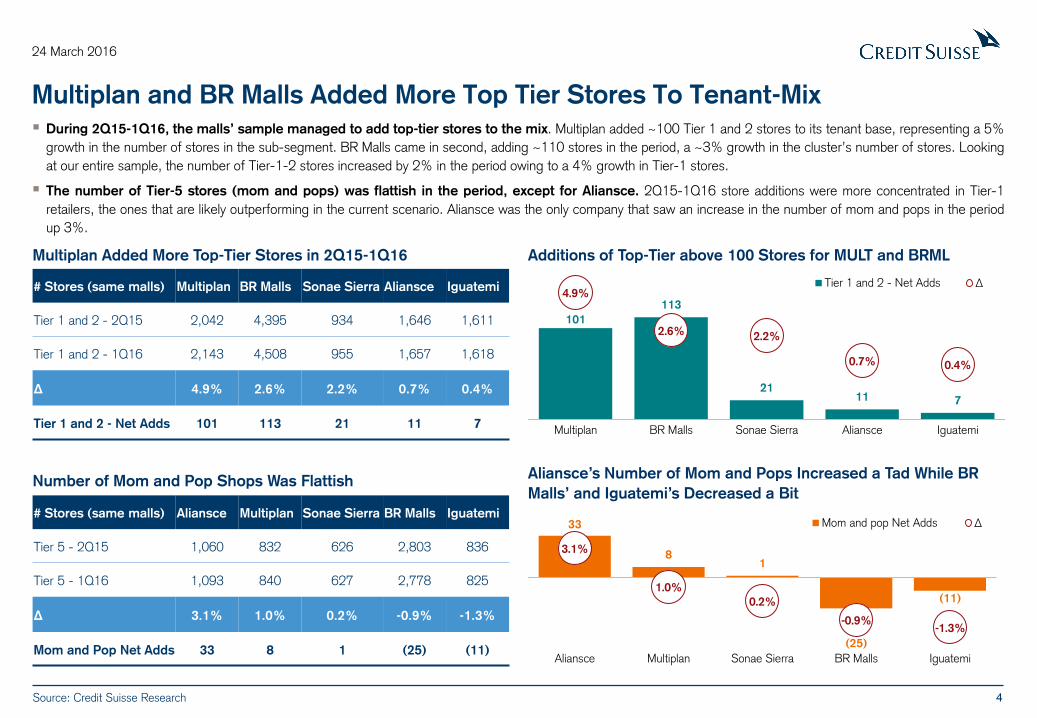

Multiplan and BR Malls Added More Top Tier Stores To Tenant-Mix

During 2Q15-1Q16, the malls’ sample managed to add top-tier stores to the mix. Multiplan added ~100 Tier 1 and 2 stores to its tenant base, representing a 5%

growth in the number of stores in the sub-segment. BR Malls came in second, adding ~110 stores in the period, a ~3% growth in the cluster’s number of stores. Looking

at our entire sample, the number of Tier-1-2 stores increased by 2% in the period owing to a 4% growth in Tier-1 stores.

The number of Tier-5 stores (mom and pops) was flattish in the period, except for Aliansce. 2Q15-1Q16 store additions were more concentrated in Tier-1

retailers, the ones that are likely outperforming in the current scenario. Aliansce was the only company that saw an increase in the number of mom and pops in the period

up 3%.

Source: Credit Suisse Research

Multiplan Added More Top-Tier Stores in 2Q15-1Q16

Number of Mom and Pop Shops Was Flattish

101

113

21 11 7

4.9%

2.6% 2.2%

0.7% 0.4%

Multiplan BR Malls Sonae Sierra Aliansce Iguatemi

Tier 1 and 2 - Net Adds ∆

33

8 1

(25)

(11)

3.1%

1.0%

0.2%

-0.9% -1.3%

Aliansce Multiplan Sonae Sierra BR Malls Iguatemi

Mom and pop Net Adds ∆

Aliansce’s Number of Mom and Pops Increased a Tad While BR

Malls’ and Iguatemi’s Decreased a Bit

# Stores (same malls) Multiplan BR Malls Sonae Sierra Aliansce Iguatemi

Tier 1 and 2 - 2Q15 2,042 4,395 934 1,646 1,611

Tier 1 and 2 - 1Q16 2,143 4,508 955 1,657 1,618

∆ 4.9% 2.6% 2.2% 0.7% 0.4%

Tier 1 and 2 - Net Adds 101 113 21 11 7

# Stores (same malls) Aliansce Multiplan Sonae Sierra BR Malls Iguatemi

Tier 5 - 2Q15 1,060 832 626 2,803 836

Tier 5 - 1Q16 1,093 840 627 2,778 825

∆ 3.1% 1.0% 0.2% -0.9% -1.3%

Mom and Pop Net Adds 33 8 1 (25) (11)

Additions of Top-Tier above 100 Stores for MULT and BRML

5

24 March 2016

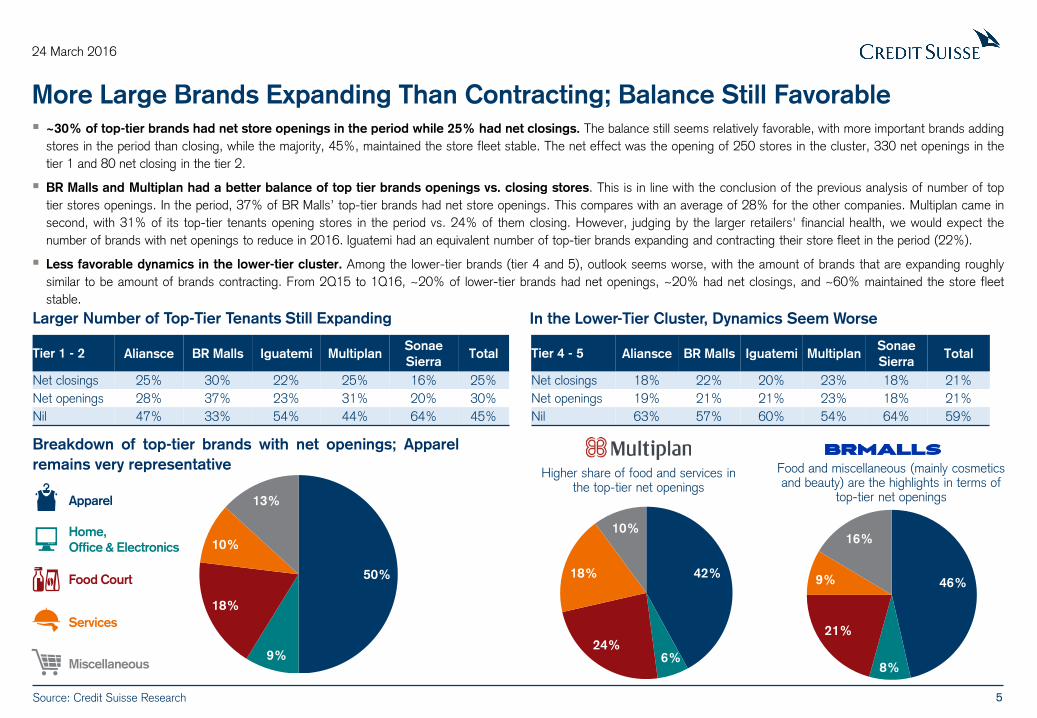

More Large Brands Expanding Than Contracting; Balance Still Favorable

~30% of top-tier brands had net store openings in the period while 25% had net closings. The balance still seems relatively favorable, with more important brands adding

stores in the period than closing, while the majority, 45%, maintained the store fleet stable. The net effect was the opening of 250 stores in the cluster, 330 net openings in the

tier 1 and 80 net closing in the tier 2.

BR Malls and Multiplan had a better balance of top tier brands openings vs. closing stores. This is in line with the conclusion of the previous analysis of number of top

tier stores openings. In the period, 37% of BR Malls’ top-tier brands had net store openings. This compares with an average of 28% for the other companies. Multiplan came in

second, with 31% of its top-tier tenants opening stores in the period vs. 24% of them closing. However, judging by the larger retailers' financial health, we would expect the

number of brands with net openings to reduce in 2016. Iguatemi had an equivalent number of top-tier brands expanding and contracting their store fleet in the period (22%).

Less favorable dynamics in the lower-tier cluster. Among the lower-tier brands (tier 4 and 5), outlook seems worse, with the amount of brands that are expanding roughly

similar to be amount of brands contracting. From 2Q15 to 1Q16, ~20% of lower-tier brands had net openings, ~20% had net closings, and ~60% maintained the store fleet

stable.

Tier 4 - 5 Aliansce BR Malls Iguatemi Multiplan Sonae

Sierra Total

Net closings 18% 22% 20% 23% 18% 21%

Net openings 19% 21% 21% 23% 18% 21%

Nil 63% 57% 60% 54% 64% 59%

Larger Number of Top-Tier Tenants Still Expanding In the Lower-Tier Cluster, Dynamics Seem Worse

Breakdown of top-tier brands with net openings; Apparel

remains very representative

42%

6% 24%

18%

10%

46%

8%

21%

9%

16%

Higher share of food and services in the top-tier net openings

Food and miscellaneous (mainly cosmetics and beauty) are the highlights in terms of

top-tier net openings

Tier 1 - 2 Aliansce BR Malls Iguatemi Multiplan Sonae

Sierra Total

Net closings 25% 30% 22% 25% 16% 25%

Net openings 28% 37% 23% 31% 20% 30%

Nil 47% 33% 54% 44% 64% 45%

Source: Credit Suisse Research

Apparel

Home,

Office & Electronics

Food Court

Services

Miscellaneous

50%

9%

18%

10%

13%

6

24 March 2016

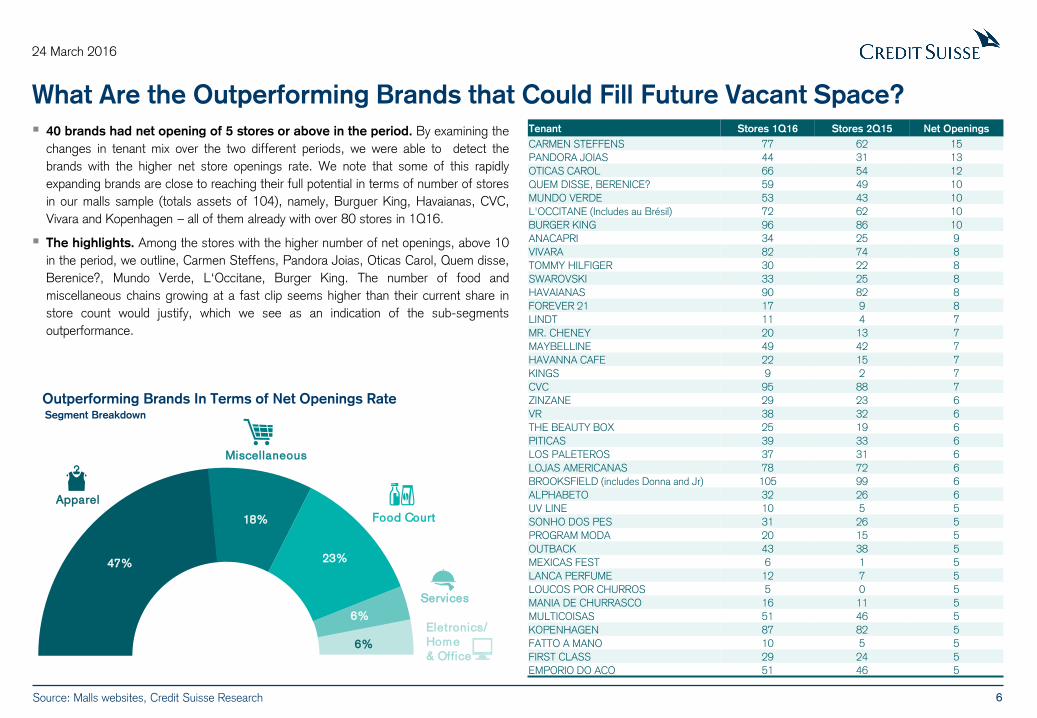

What Are the Outperforming Brands that Could Fill Future Vacant Space?

40 brands had net opening of 5 stores or above in the period. By examining the

changes in tenant mix over the two different periods, we were able to detect the

brands with the higher net store openings rate. We note that some of this rapidly

expanding brands are close to reaching their full potential in terms of number of stores

in our malls sample (totals assets of 104), namely, Burguer King, Havaianas, CVC,

Vivara and Kopenhagen – all of them already with over 80 stores in 1Q16.

The highlights. Among the stores with the higher number of net openings, above 10

in the period, we outline, Carmen Steffens, Pandora Joias, Oticas Carol, Quem disse,

Berenice?, Mundo Verde, L‘Occitane, Burger King. The number of food and

miscellaneous chains growing at a fast clip seems higher than their current share in

store count would justify, which we see as an indication of the sub-segments

outperformance.

Tenant Stores 1Q16 Stores 2Q15 Net Openings

CARMEN STEFFENS 77 62 15

PANDORA JOIAS 44 31 13

OTICAS CAROL 66 54 12

QUEM DISSE, BERENICE? 59 49 10

MUNDO VERDE 53 43 10

L'OCCITANE (Includes au Brésil) 72 62 10

BURGER KING 96 86 10

ANACAPRI 34 25 9

VIVARA 82 74 8

TOMMY HILFIGER 30 22 8

SWAROVSKI 33 25 8

HAVAIANAS 90 82 8

FOREVER 21 17 9 8

LINDT 11 4 7

MR. CHENEY 20 13 7

MAYBELLINE 49 42 7

HAVANNA CAFE 22 15 7

KINGS 9 2 7

CVC 95 88 7

ZINZANE 29 23 6

VR 38 32 6

THE BEAUTY BOX 25 19 6

PITICAS 39 33 6

LOS PALETEROS 37 31 6

LOJAS AMERICANAS 78 72 6

BROOKSFIELD (includes Donna and Jr) 105 99 6

ALPHABETO 32 26 6

UV LINE 10 5 5

SONHO DOS PES 31 26 5

PROGRAM MODA 20 15 5

OUTBACK 43 38 5

MEXICAS FEST 6 1 5

LANCA PERFUME 12 7 5

LOUCOS POR CHURROS 5 0 5

MANIA DE CHURRASCO 16 11 5

MULTICOISAS 51 46 5

KOPENHAGEN 87 82 5

FATTO A MANO 10 5 5

FIRST CLASS 29 24 5

EMPORIO DO ACO 51 46 5

Outperforming Brands In Terms of Net Openings Rate

Source: Malls websites, Credit Suisse Research

Apparel

Eletronics/

Home

& Office

Services

Food Court

47%

18%

23%

6%

6%

Miscellaneous

Segment Breakdown

7

24 March 2016

What Are the Main Brands Downsizing Their Store Fleet?

36 brands had net closings above or equal 4 during the period. 26 of them are

in the apparel segment, 6 food and 4 electronics segments. Among the brands with

the higher net closures, we highlight HP Store, Accessorize, M. Officer, Ponto Frio,

Camisaria Colombo, Arezzo, Dumond, Colcci, Handbook and Luigi Bertolli.

Significant representativeness of apparel stores among the brands reducing

store fleet, 63%. In addition, apparel accounted for 47% of the brands with the

higher net openings (aligned with its representativeness in our sample store count).

The higher rate of net closing among the apparel retailers, point to a marginal decline

in representativeness of the segment within the malls’ store mix going forward.

Tenant Stores 1Q16 Stores 2Q15 Net Openings

HP STORE 4 12 -8

ACCESSORIZE 15 22 -7

M. OFFICER 44 51 -7

MR. BEER 13 20 -7

PONTO FRIO 45 52 -7

ATHLETIC WAY 32 38 -6

CAMISARIA COLOMBO 51 57 -6

THE JEANS BOUTIQUE 3 9 -6

AREZZO 80 85 -5

EMME 16 21 -5

FERNI 5 10 -5

DUMOND 30 35 -5

FREDDO GELATERIA 18 23 -5

MR. KITSCH 15 20 -5

ANDARELLA 13 17 -4

BLUE MAN 4 8 -4

BY TENNIS 8 12 -4

COLCCI 34 38 -4

ESPACO FASHION 3 7 -4

FABRIZIO GIANNONE 6 10 -4

ETNA 4 8 -4

FOLIC 6 10 -4

HANDBOOK FASHION 20 24 -4

LUIGI BERTOLLI 29 33 -4

LIGA RETRO 10 14 -4

MR. PRETZELS 29 33 -4

LUPA LUPA 10 14 -4

MY SHOES 13 17 -4

PREMIATTO 9 13 -4

PRIMICIA 7 11 -4

SOFT TACOS 3 7 -4

SKY 7 11 -4

UNCLE K 7 11 -4

UNITED COLORS OF BENETTON 2 6 -4

VIVENDA DO CAMARAO 60 64 -4

VIA UNO 11 15 -4

Source: Malls websites, Credit Suisse Research

Apparel

Eletronics/

Home

& Office

Food Court 63% 18%

23%

6%

Miscellaneous

Underperforming Brands In Terms of Net Closings Rate Segment Breakdown

8

24 March 2016

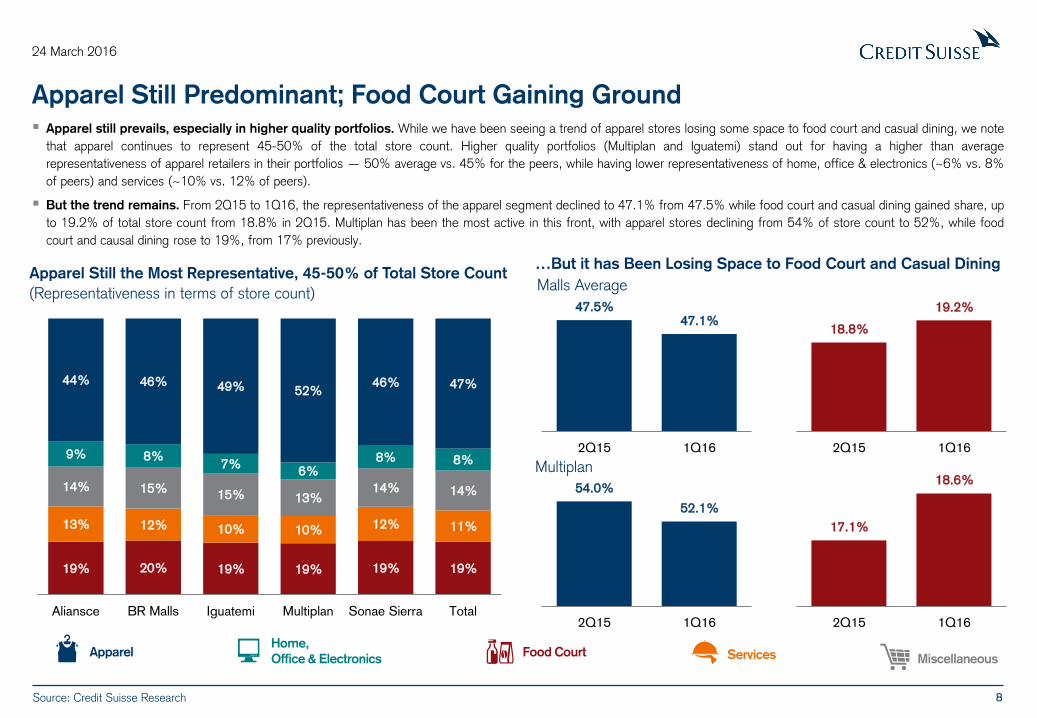

Apparel Still Predominant; Food Court Gaining Ground

Apparel still prevails, especially in higher quality portfolios. While we have been seeing a trend of apparel stores losing some space to food court and casual dining, we note

that apparel continues to represent 45-50% of the total store count. Higher quality portfolios (Multiplan and Iguatemi) stand out for having a higher than average

representativeness of apparel retailers in their portfolios — 50% average vs. 45% for the peers, while having lower representativeness of home, office & electronics (~6% vs. 8%

of peers) and services (~10% vs. 12% of peers).

But the trend remains. From 2Q15 to 1Q16, the representativeness of the apparel segment declined to 47.1% from 47.5% while food court and casual dining gained share, up

to 19.2% of total store count from 18.8% in 2Q15. Multiplan has been the most active in this front, with apparel stores declining from 54% of store count to 52%, while food

court and causal dining rose to 19%, from 17% previously.

Apparel Home,

Office & Electronics Food Court Services Miscellaneous

47.5% 47.1%

2Q15 1Q16

18.8%

19.2%

2Q15 1Q16

Apparel Still the Most Representative, 45-50% of Total Store Count

(Representativeness in terms of store count)

…But it has Been Losing Space to Food Court and Casual Dining

Malls Average

Multiplan

54.0%

52.1%

2Q15 1Q16

17.1%

18.6%

2Q15 1Q16

19% 20% 19% 19% 19% 19%

13% 12% 10% 10% 12% 11%

14% 15% 15% 13%

14% 14%

9% 8% 7%

6% 8% 8%

44% 46% 49% 52% 46% 47%

Aliansce BR Malls Iguatemi Multiplan Sonae Sierra Total

Source: Credit Suisse Research

9

24 March 2016

6,225

2,343

2,051

2,837

8,176

5,235

646

270

172

215

Tier 5 (1≤N≤2)

Tier 4 (3≤N≤5)

Tier 3 (6≤N≤10)

Tier 2 (10<N≤25)

Tier 1 (N>25)

Total Brands Total Stores

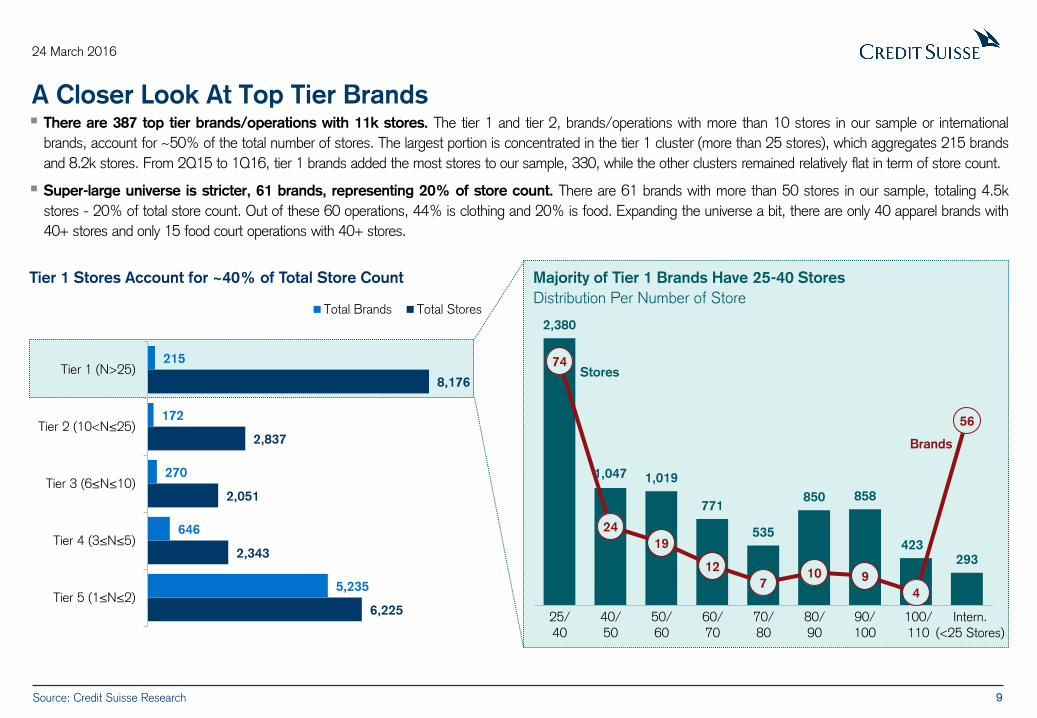

A Closer Look At Top Tier Brands There are 387 top tier brands/operations with 11k stores. The tier 1 and tier 2, brands/operations with more than 10 stores in our sample or international

brands, account for ~50% of the total number of stores. The largest portion is concentrated in the tier 1 cluster (more than 25 stores), which aggregates 215 brands

and 8.2k stores. From 2Q15 to 1Q16, tier 1 brands added the most stores to our sample, 330, while the other clusters remained relatively flat in term of store count.

Super-large universe is stricter, 61 brands, representing 20% of store count. There are 61 brands with more than 50 stores in our sample, totaling 4.5k

stores - 20% of total store count. Out of these 60 operations, 44% is clothing and 20% is food. Expanding the universe a bit, there are only 40 apparel brands with

40+ stores and only 15 food court operations with 40+ stores.

Tier 1 Stores Account for ~40% of Total Store Count Majority of Tier 1 Brands Have 25-40 Stores

2,380

1,047 1,019

771

535

850 858

423

293

74

24

19

12

7 10 9

4

56

25/

40

40/

50

50/

60

60/

70

70/

80

80/

90

90/

100

100/

110

Intern.

(<25 Stores)

Brands

Stores

Distribution Per Number of Store

Source: Credit Suisse Research

10

24 March 2016

-20%

-10%

0%

10%

20%

30%

40%

1Q

01

4Q

01

3Q

02

2Q

03

1Q

04

4Q

04

3Q

05

2Q

06

1Q

07

4Q

07

3Q

08

2Q

09

1Q

10

4Q

10

3Q

11

2Q

12

1Q

13

4Q

13

3Q

14

2Q

15

rea

l sa

les g

row

th y

oy

Apparel Home Appliances

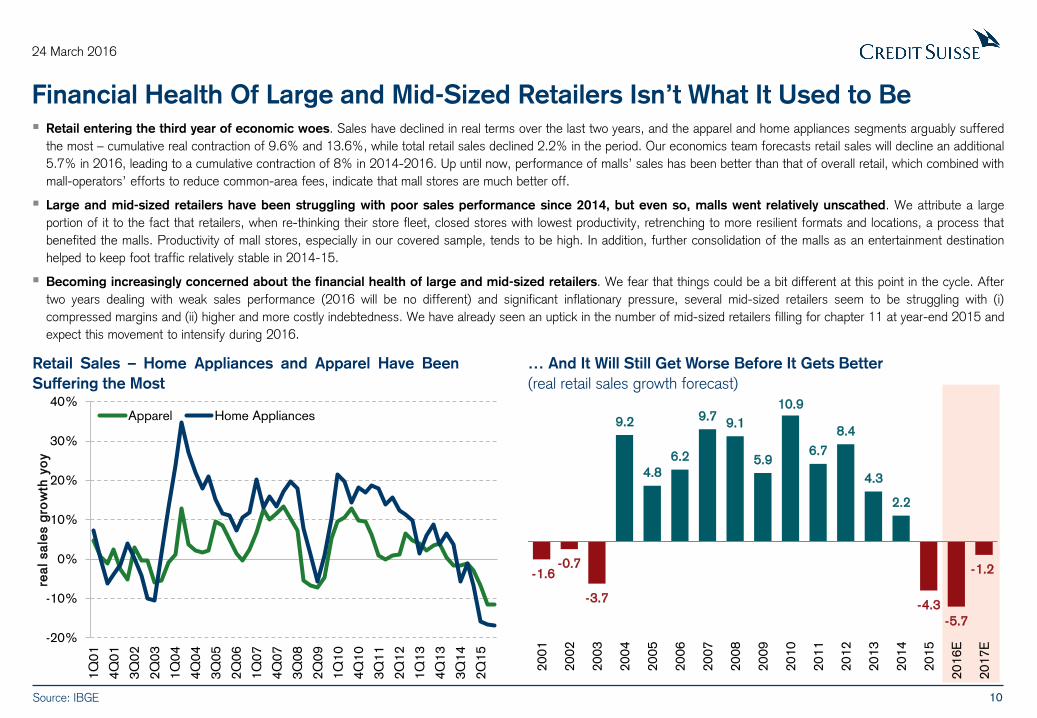

Financial Health Of Large and Mid-Sized Retailers Isn’t What It Used to Be

Retail entering the third year of economic woes. Sales have declined in real terms over the last two years, and the apparel and home appliances segments arguably suffered

the most – cumulative real contraction of 9.6% and 13.6%, while total retail sales declined 2.2% in the period. Our economics team forecasts retail sales will decline an additional

5.7% in 2016, leading to a cumulative contraction of 8% in 2014-2016. Up until now, performance of malls’ sales has been better than that of overall retail, which combined with

mall-operators’ efforts to reduce common-area fees, indicate that mall stores are much better off.

Large and mid-sized retailers have been struggling with poor sales performance since 2014, but even so, malls went relatively unscathed. We attribute a large

portion of it to the fact that retailers, when re-thinking their store fleet, closed stores with lowest productivity, retrenching to more resilient formats and locations, a process that

benefited the malls. Productivity of mall stores, especially in our covered sample, tends to be high. In addition, further consolidation of the malls as an entertainment destination

helped to keep foot traffic relatively stable in 2014-15.

Becoming increasingly concerned about the financial health of large and mid-sized retailers. We fear that things could be a bit different at this point in the cycle. After

two years dealing with weak sales performance (2016 will be no different) and significant inflationary pressure, several mid-sized retailers seem to be struggling with (i)

compressed margins and (ii) higher and more costly indebtedness. We have already seen an uptick in the number of mid-sized retailers filling for chapter 11 at year-end 2015 and

expect this movement to intensify during 2016.

Source: IBGE

Retail Sales – Home Appliances and Apparel Have Been

Suffering the Most

… And It Will Still Get Worse Before It Gets Better

(real retail sales growth forecast)

-1.6 -0.7

-3.7

9.2

4.8

6.2

9.7 9.1

5.9

10.9

6.7

8.4

4.3

2.2

-4.3

-5.7

-1.2

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16E

20

17E

11

24 March 2016

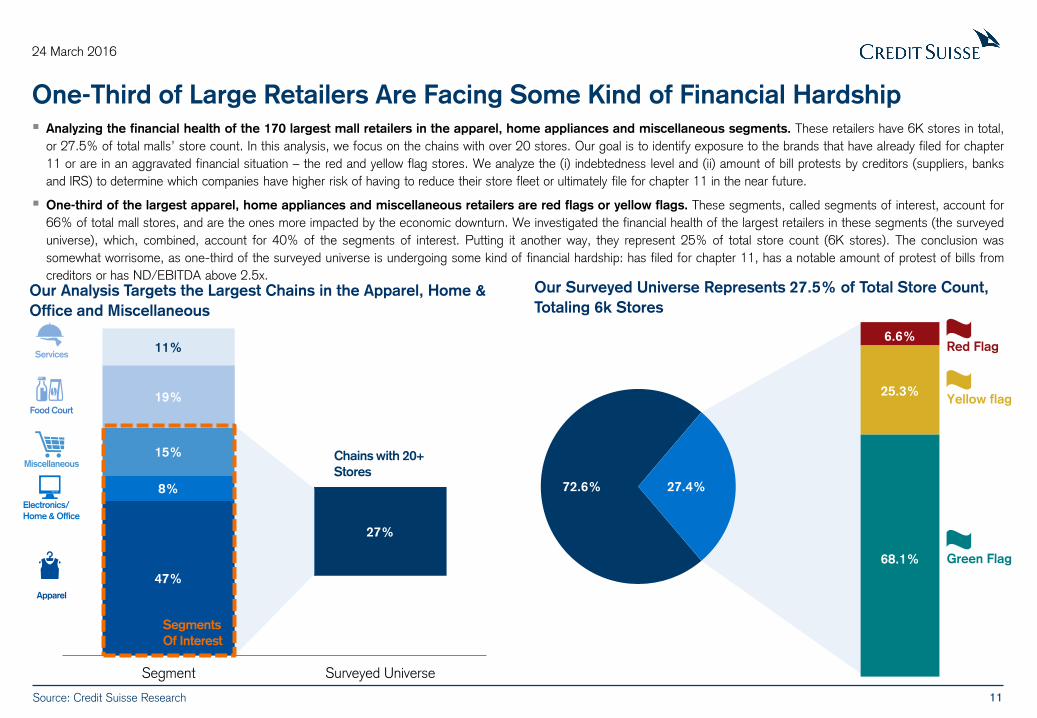

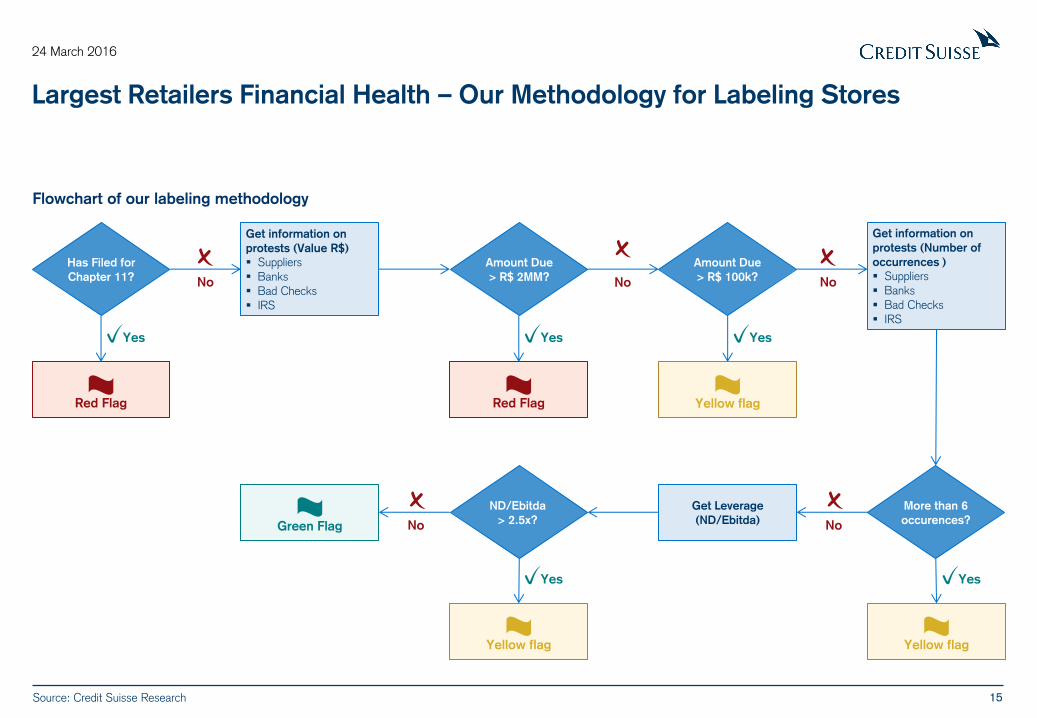

One-Third of Large Retailers Are Facing Some Kind of Financial Hardship

Analyzing the financial health of the 170 largest mall retailers in the apparel, home appliances and miscellaneous segments. These retailers have 6K stores in total,

or 27.5% of total malls’ store count. In this analysis, we focus on the chains with over 20 stores. Our goal is to identify exposure to the brands that have already filed for chapter

11 or are in an aggravated financial situation – the red and yellow flag stores. We analyze the (i) indebtedness level and (ii) amount of bill protests by creditors (suppliers, banks

and IRS) to determine which companies have higher risk of having to reduce their store fleet or ultimately file for chapter 11 in the near future.

One-third of the largest apparel, home appliances and miscellaneous retailers are red flags or yellow flags. These segments, called segments of interest, account for

66% of total mall stores, and are the ones more impacted by the economic downturn. We investigated the financial health of the largest retailers in these segments (the surveyed

universe), which, combined, account for 40% of the segments of interest. Putting it another way, they represent 25% of total store count (6K stores). The conclusion was

somewhat worrisome, as one-third of the surveyed universe is undergoing some kind of financial hardship: has filed for chapter 11, has a notable amount of protest of bills from

creditors or has ND/EBITDA above 2.5x.

Our Analysis Targets the Largest Chains in the Apparel, Home &

Office and Miscellaneous

Our Surveyed Universe Represents 27.5% of Total Store Count,

Totaling 6k Stores

Source: Credit Suisse Research

Red Flag

Yellow flag

Green Flag

6.6%

25.3%

68.1%

27.4% 72.6%

Apparel

Electronics/

Home & Office

Miscellaneous

Food Court

Services

47%

8%

15%

19%

11%

27%

Segment Surveyed Universe

Segments

Of Interest

Chains with 20+

Stores

12

24 March 2016

Red Flag,

6.7%

Yellow Flag,

24.6%

Other, 69%

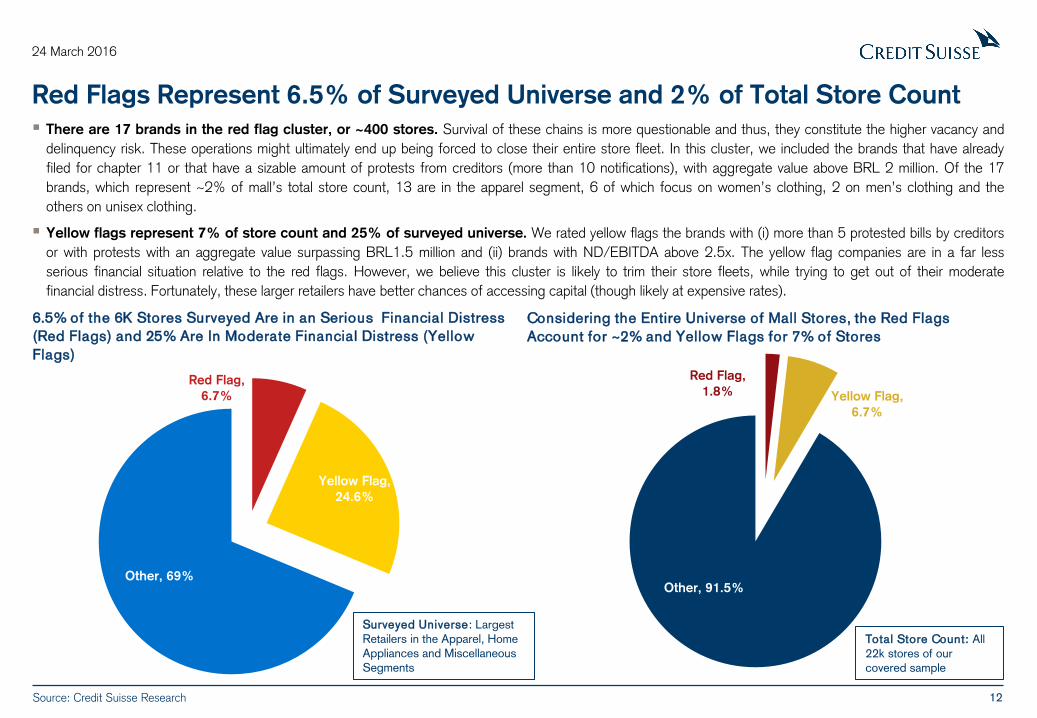

Red Flags Represent 6.5% of Surveyed Universe and 2% of Total Store Count

There are 17 brands in the red flag cluster, or ~400 stores. Survival of these chains is more questionable and thus, they constitute the higher vacancy and

delinquency risk. These operations might ultimately end up being forced to close their entire store fleet. In this cluster, we included the brands that have already

filed for chapter 11 or that have a sizable amount of protests from creditors (more than 10 notifications), with aggregate value above BRL 2 million. Of the 17

brands, which represent ~2% of mall’s total store count, 13 are in the apparel segment, 6 of which focus on women’s clothing, 2 on men’s clothing and the

others on unisex clothing.

Yellow flags represent 7% of store count and 25% of surveyed universe. We rated yellow flags the brands with (i) more than 5 protested bills by creditors

or with protests with an aggregate value surpassing BRL1.5 million and (ii) brands with ND/EBITDA above 2.5x. The yellow flag companies are in a far less

serious financial situation relative to the red flags. However, we believe this cluster is likely to trim their store fleets, while trying to get out of their moderate

financial distress. Fortunately, these larger retailers have better chances of accessing capital (though likely at expensive rates).

6.5% of the 6K Stores Surveyed Are in an Serious Financial Distress

(Red Flags) and 25% Are In Moderate Financial Distress (Yellow

Flags)

Considering the Entire Universe of Mall Stores, the Red Flags

Account for ~2% and Yellow Flags for 7% of Stores

Source: Credit Suisse Research

Red Flag,

1.8% Yellow Flag,

6.7%

Other, 91.5%

Surveyed Universe: Largest

Retailers in the Apparel, Home

Appliances and Miscellaneous

Segments

Total Store Count: All

22k stores of our

covered sample

13

24 March 2016

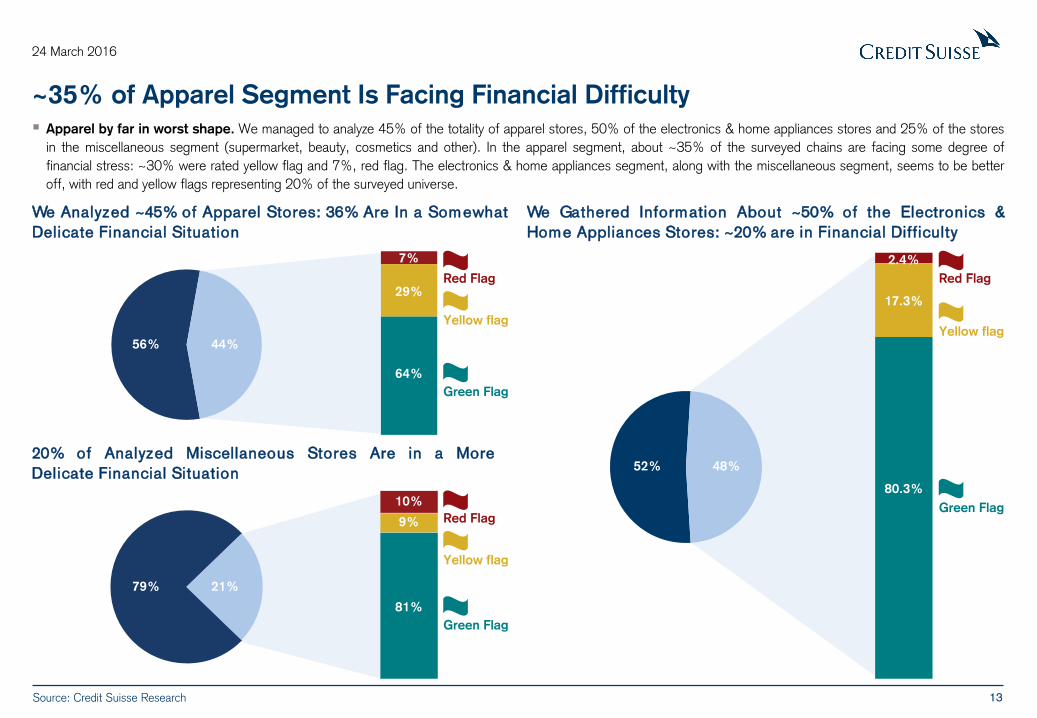

~35% of Apparel Segment Is Facing Financial Difficulty

Apparel by far in worst shape. We managed to analyze 45% of the totality of apparel stores, 50% of the electronics & home appliances stores and 25% of the stores

in the miscellaneous segment (supermarket, beauty, cosmetics and other). In the apparel segment, about ~35% of the surveyed chains are facing some degree of

financial stress: ~30% were rated yellow flag and 7%, red flag. The electronics & home appliances segment, along with the miscellaneous segment, seems to be better

off, with red and yellow flags representing 20% of the surveyed universe.

We Analyzed ~45% of Apparel Stores: 36% Are In a Somewhat

Delicate Financial Situation

We Gathered Information About ~50% of the Electronics &

Home Appliances Stores: ~20% are in Financial Difficulty

Source: Credit Suisse Research

20% of Analyzed Miscellaneous Stores Are in a More

Delicate Financial Situation

Red Flag

Yellow flag

Green Flag

Red Flag

Yellow flag

Green Flag

7%

29%

64%

10%

9%

81%

44%

21%

56%

79%

Red Flag

Yellow flag

Green Flag

2.4%

17.3%

80.3%

48% 52%

14

24 March 2016

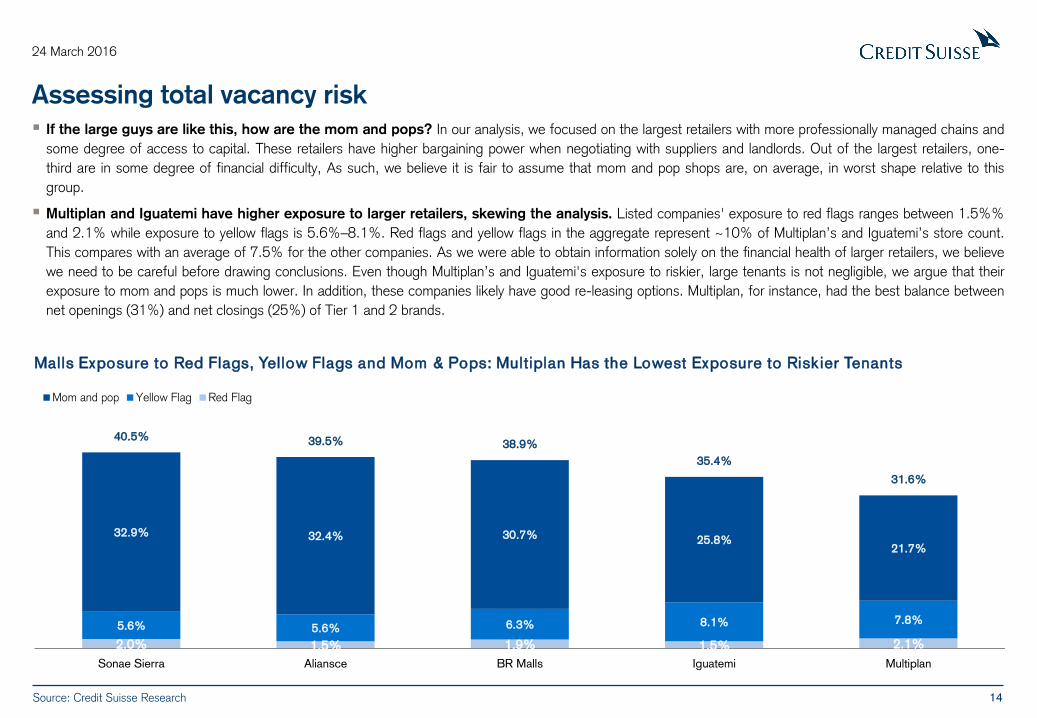

Assessing total vacancy risk

If the large guys are like this, how are the mom and pops? In our analysis, we focused on the largest retailers with more professionally managed chains and

some degree of access to capital. These retailers have higher bargaining power when negotiating with suppliers and landlords. Out of the largest retailers, one-

third are in some degree of financial difficulty, As such, we believe it is fair to assume that mom and pop shops are, on average, in worst shape relative to this

group.

Multiplan and Iguatemi have higher exposure to larger retailers, skewing the analysis. Listed companies' exposure to red flags ranges between 1.5%%

and 2.1% while exposure to yellow flags is 5.6%–8.1%. Red flags and yellow flags in the aggregate represent ~10% of Multiplan’s and Iguatemi’s store count.

This compares with an average of 7.5% for the other companies. As we were able to obtain information solely on the financial health of larger retailers, we believe

we need to be careful before drawing conclusions. Even though Multiplan’s and Iguatemi's exposure to riskier, large tenants is not negligible, we argue that their

exposure to mom and pops is much lower. In addition, these companies likely have good re-leasing options. Multiplan, for instance, had the best balance between

net openings (31%) and net closings (25%) of Tier 1 and 2 brands.

2.0% 1.5% 1.9% 1.5% 2.1%

5.6% 5.6% 6.3% 8.1% 7.8%

32.9% 32.4% 30.7% 25.8% 21.7%

40.5% 39.5% 38.9%

35.4%

31.6%

Sonae Sierra Aliansce BR Malls Iguatemi Multiplan

Mom and pop Yellow Flag Red Flag

Malls Exposure to Red Flags, Yellow Flags and Mom & Pops: Multiplan Has the Lowest Exposure to Riskier Tenants

Source: Credit Suisse Research

15

24 March 2016

Largest Retailers Financial Health – Our Methodology for Labeling Stores

Flowchart of our labeling methodology

Source: Credit Suisse Research

Get information on

protests (Value R$)

Suppliers Banks Bad Checks

IRS

Get information on

protests (Number of

occurrences )

Suppliers Banks

Bad Checks IRS

Get Leverage

(ND/Ebitda)

Red Flag Yellow flag

Green Flag

Yellow flag Yellow flag

Red Flag

Yes

No No

Yes Yes

No No

Yes Yes

No

Has Filed for

Chapter 11?

Amount Due

> R$ 2MM?

Amount Due

> R$ 100k?

ND/Ebitda

> 2.5x?

More than 6

occurences?

16

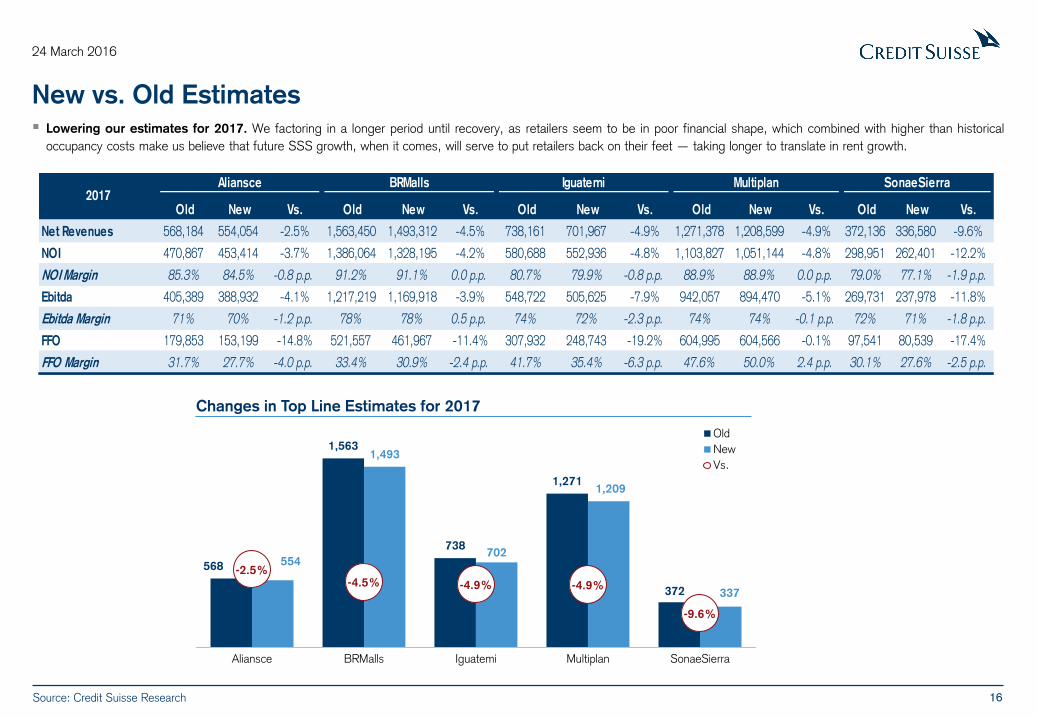

24 March 2016

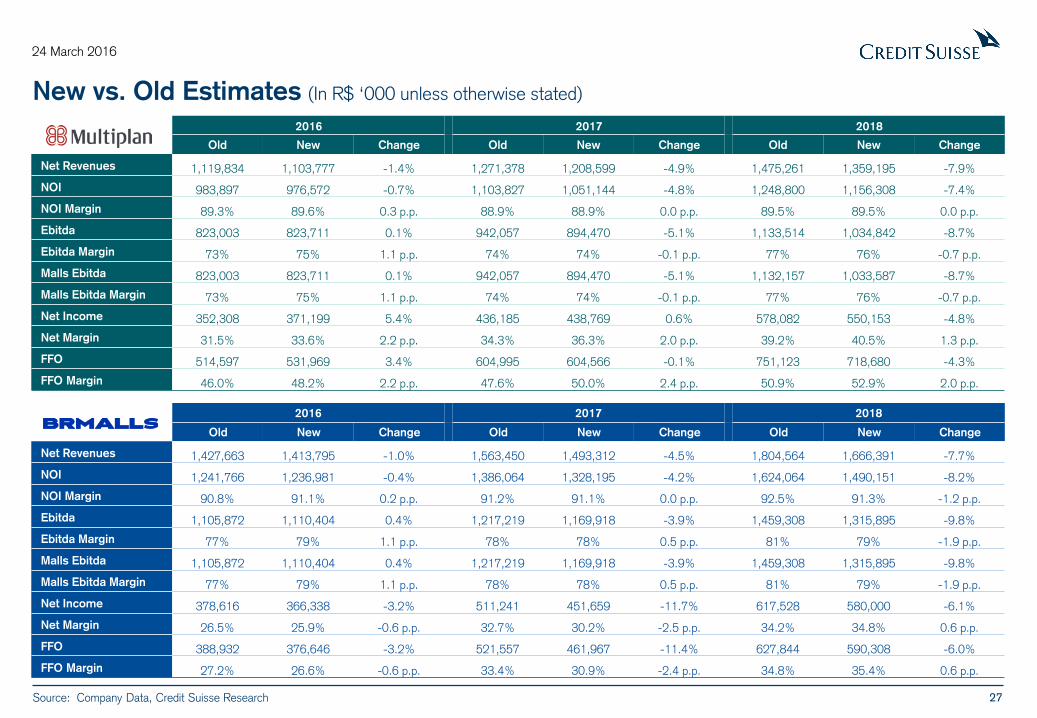

New vs. Old Estimates

Lowering our estimates for 2017. We factoring in a longer period until recovery, as retailers seem to be in poor financial shape, which combined with higher than historical

occupancy costs make us believe that future SSS growth, when it comes, will serve to put retailers back on their feet — taking longer to translate in rent growth.

Old New Vs. Old New Vs. Old New Vs. Old New Vs. Old New Vs.

Net Revenues 568,184 554,054 -2.5% 1,563,450 1,493,312 -4.5% 738,161 701,967 -4.9% 1,271,378 1,208,599 -4.9% 372,136 336,580 -9.6%

NOI 470,867 453,414 -3.7% 1,386,064 1,328,195 -4.2% 580,688 552,936 -4.8% 1,103,827 1,051,144 -4.8% 298,951 262,401 -12.2%

NOI Margin 85.3% 84.5% -0.8 p.p. 91.2% 91.1% 0.0 p.p. 80.7% 79.9% -0.8 p.p. 88.9% 88.9% 0.0 p.p. 79.0% 77.1% -1.9 p.p.

Ebitda 405,389 388,932 -4.1% 1,217,219 1,169,918 -3.9% 548,722 505,625 -7.9% 942,057 894,470 -5.1% 269,731 237,978 -11.8%

Ebitda Margin 71% 70% -1.2 p.p. 78% 78% 0.5 p.p. 74% 72% -2.3 p.p. 74% 74% -0.1 p.p. 72% 71% -1.8 p.p.

FFO 179,853 153,199 -14.8% 521,557 461,967 -11.4% 307,932 248,743 -19.2% 604,995 604,566 -0.1% 97,541 80,539 -17.4%

FFO Margin 31.7% 27.7% -4.0 p.p. 33.4% 30.9% -2.4 p.p. 41.7% 35.4% -6.3 p.p. 47.6% 50.0% 2.4 p.p. 30.1% 27.6% -2.5 p.p.

SonaeSierra2017

Aliansce BRMalls Iguatemi Multiplan

568

1,563

738

1,271

372

554

1,493

702

1,209

337

-2.5% -4.5% -4.9% -4.9%

-9.6%

Aliansce BRMalls Iguatemi Multiplan SonaeSierra

Old

New

Vs.

Changes in Top Line Estimates for 2017

Source: Credit Suisse Research

17

24 March 2016

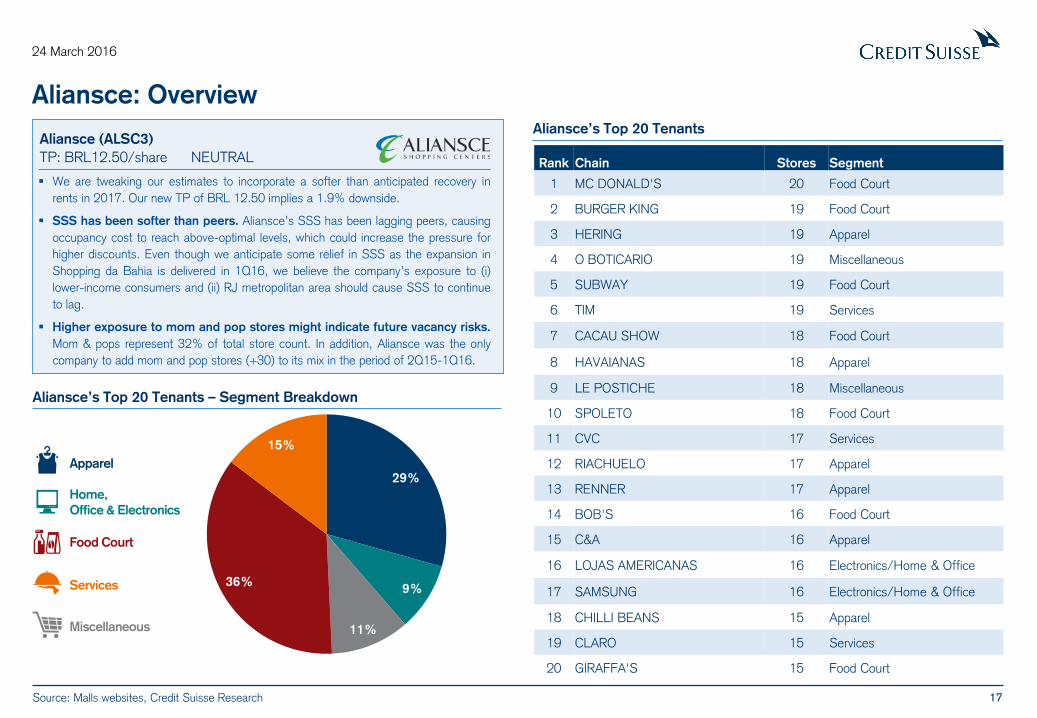

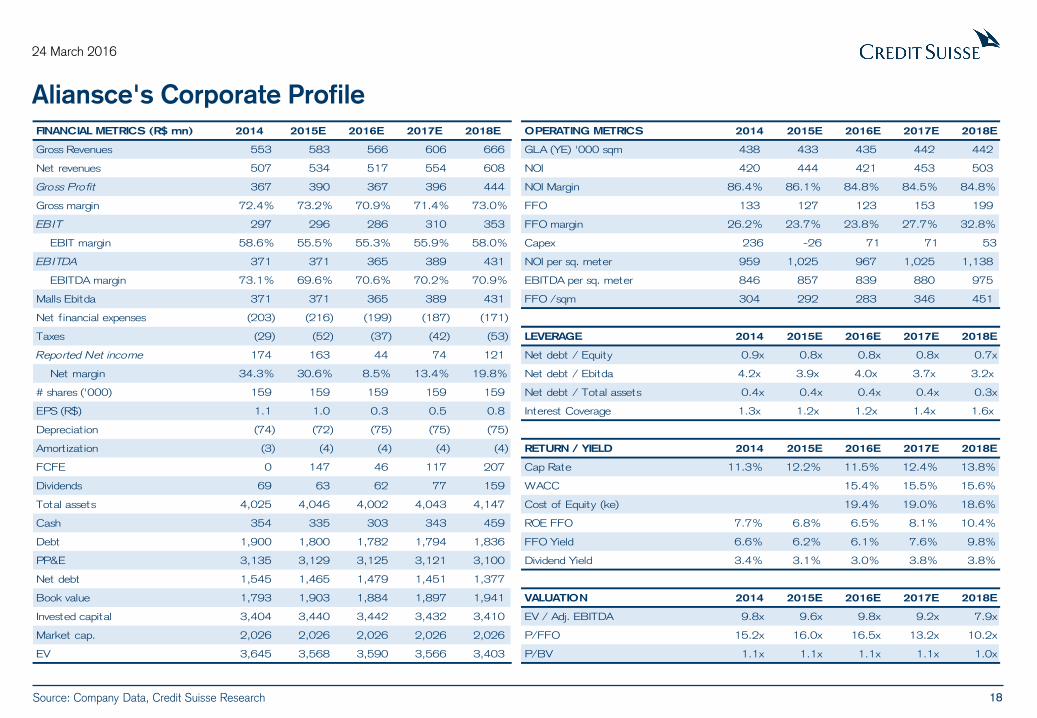

Aliansce: Overview

Source: Malls websites, Credit Suisse Research

We are tweaking our estimates to incorporate a softer than anticipated recovery in

rents in 2017. Our new TP of BRL 12.50 implies a 1.9% downside.

SSS has been softer than peers. Aliansce’s SSS has been lagging peers, causing

occupancy cost to reach above-optimal levels, which could increase the pressure for

higher discounts. Even though we anticipate some relief in SSS as the expansion in

Shopping da Bahia is delivered in 1Q16, we believe the company’s exposure to (i)

lower-income consumers and (ii) RJ metropolitan area should cause SSS to continue

to lag.

Higher exposure to mom and pop stores might indicate future vacancy risks.

Mom & pops represent 32% of total store count. In addition, Aliansce was the only

company to add mom and pop stores (+30) to its mix in the period of 2Q15-1Q16.

Aliansce’s Top 20 Tenants Aliansce (ALSC3)

TP: BRL12.50/share NEUTRAL Rank Chain Stores Segment

1 MC DONALD'S 20 Food Court

2 BURGER KING 19 Food Court

3 HERING 19 Apparel

4 O BOTICARIO 19 Miscellaneous

5 SUBWAY 19 Food Court

6 TIM 19 Services

7 CACAU SHOW 18 Food Court

8 HAVAIANAS 18 Apparel

9 LE POSTICHE 18 Miscellaneous

10 SPOLETO 18 Food Court

11 CVC 17 Services

12 RIACHUELO 17 Apparel

13 RENNER 17 Apparel

14 BOB'S 16 Food Court

15 C&A 16 Apparel

16 LOJAS AMERICANAS 16 Electronics/Home & Office

17 SAMSUNG 16 Electronics/Home & Office

18 CHILLI BEANS 15 Apparel

19 CLARO 15 Services

20 GIRAFFA'S 15 Food Court

29%

9%

11%

36%

15%

Apparel

Home,

Office & Electronics

Food Court

Services

Miscellaneous

Aliansce’s Top 20 Tenants – Segment Breakdown

18

24 March 2016

Aliansce's Corporate Profile

Source: Company Data, Credit Suisse Research

FINANCIAL METRICS (R$ mn) 2014 2015E 2016E 2017E 2018E OPERATING METRICS 2014 2015E 2016E 2017E 2018E

Gross Revenues 553 583 566 606 666 GLA (YE) '000 sqm 438 433 435 442 442

Net revenues 507 534 517 554 608 NOI 420 444 421 453 503

Gross Profit 367 390 367 396 444 NOI Margin 86.4% 86.1% 84.8% 84.5% 84.8%

Gross margin 72.4% 73.2% 70.9% 71.4% 73.0% FFO 133 127 123 153 199

EBIT 297 296 286 310 353 FFO margin 26.2% 23.7% 23.8% 27.7% 32.8%

EBIT margin 58.6% 55.5% 55.3% 55.9% 58.0% Capex 236 -26 71 71 53

EBITDA 371 371 365 389 431 NOI per sq. meter 959 1,025 967 1,025 1,138

EBITDA margin 73.1% 69.6% 70.6% 70.2% 70.9% EBITDA per sq. meter 846 857 839 880 975

Malls Ebitda 371 371 365 389 431 FFO /sqm 304 292 283 346 451

Net financial expenses (203) (216) (199) (187) (171)

Taxes (29) (52) (37) (42) (53) LEVERAGE 2014 2015E 2016E 2017E 2018E

Reported Net income 174 163 44 74 121 Net debt / Equity 0.9x 0.8x 0.8x 0.8x 0.7x

Net margin 34.3% 30.6% 8.5% 13.4% 19.8% Net debt / Ebitda 4.2x 3.9x 4.0x 3.7x 3.2x

# shares ('000) 159 159 159 159 159 Net debt / Total assets 0.4x 0.4x 0.4x 0.4x 0.3x

EPS (R$) 1.1 1.0 0.3 0.5 0.8 Interest Coverage 1.3x 1.2x 1.2x 1.4x 1.6x

Depreciat ion (74) (72) (75) (75) (75)

Amort izat ion (3) (4) (4) (4) (4) RETURN / YIELD 2014 2015E 2016E 2017E 2018E

FCFE 0 147 46 117 207 Cap Rate 11.3% 12.2% 11.5% 12.4% 13.8%

Dividends 69 63 62 77 159 WACC 15.4% 15.5% 15.6%

Total assets 4,025 4,046 4,002 4,043 4,147 Cost of Equity (ke) 19.4% 19.0% 18.6%

Cash 354 335 303 343 459 ROE FFO 7.7% 6.8% 6.5% 8.1% 10.4%

Debt 1,900 1,800 1,782 1,794 1,836 FFO Yield 6.6% 6.2% 6.1% 7.6% 9.8%

PP&E 3,135 3,129 3,125 3,121 3,100 Dividend Yield 3.4% 3.1% 3.0% 3.8% 3.8%

Net debt 1,545 1,465 1,479 1,451 1,377

Book value 1,793 1,903 1,884 1,897 1,941 VALUATION 2014 2015E 2016E 2017E 2018E

Invested capital 3,404 3,440 3,442 3,432 3,410 EV / Adj. EBITDA 9.8x 9.6x 9.8x 9.2x 7.9x

Market cap. 2,026 2,026 2,026 2,026 2,026 P/FFO 15.2x 16.0x 16.5x 13.2x 10.2x

EV 3,645 3,568 3,590 3,566 3,403 P/BV 1.1x 1.1x 1.1x 1.1x 1.0x

19

24 March 2016

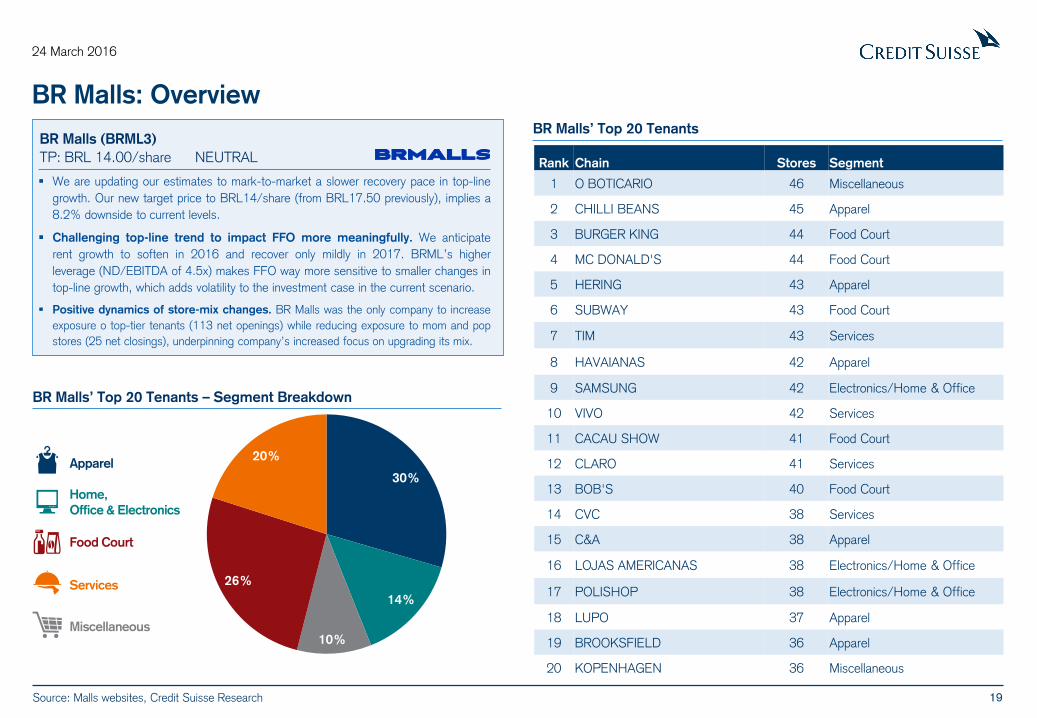

BR Malls: Overview

Source: Malls websites, Credit Suisse Research

We are updating our estimates to mark-to-market a slower recovery pace in top-line

growth. Our new target price to BRL14/share (from BRL17.50 previously), implies a

8.2% downside to current levels.

Challenging top-line trend to impact FFO more meaningfully. We anticipate

rent growth to soften in 2016 and recover only mildly in 2017. BRML’s higher

leverage (ND/EBITDA of 4.5x) makes FFO way more sensitive to smaller changes in

top-line growth, which adds volatility to the investment case in the current scenario.

Positive dynamics of store-mix changes. BR Malls was the only company to increase

exposure o top-tier tenants (113 net openings) while reducing exposure to mom and pop

stores (25 net closings), underpinning company’s increased focus on upgrading its mix.

BR Malls (BRML3)

TP: BRL 14.00/share NEUTRAL

BR Malls’ Top 20 Tenants

Rank Chain Stores Segment

1 O BOTICARIO 46 Miscellaneous

2 CHILLI BEANS 45 Apparel

3 BURGER KING 44 Food Court

4 MC DONALD'S 44 Food Court

5 HERING 43 Apparel

6 SUBWAY 43 Food Court

7 TIM 43 Services

8 HAVAIANAS 42 Apparel

9 SAMSUNG 42 Electronics/Home & Office

10 VIVO 42 Services

11 CACAU SHOW 41 Food Court

12 CLARO 41 Services

13 BOB'S 40 Food Court

14 CVC 38 Services

15 C&A 38 Apparel

16 LOJAS AMERICANAS 38 Electronics/Home & Office

17 POLISHOP 38 Electronics/Home & Office

18 LUPO 37 Apparel

19 BROOKSFIELD 36 Apparel

20 KOPENHAGEN 36 Miscellaneous

30%

14%

10%

26%

20% Apparel

Home,

Office & Electronics

Food Court

Services

Miscellaneous

BR Malls’ Top 20 Tenants – Segment Breakdown

20

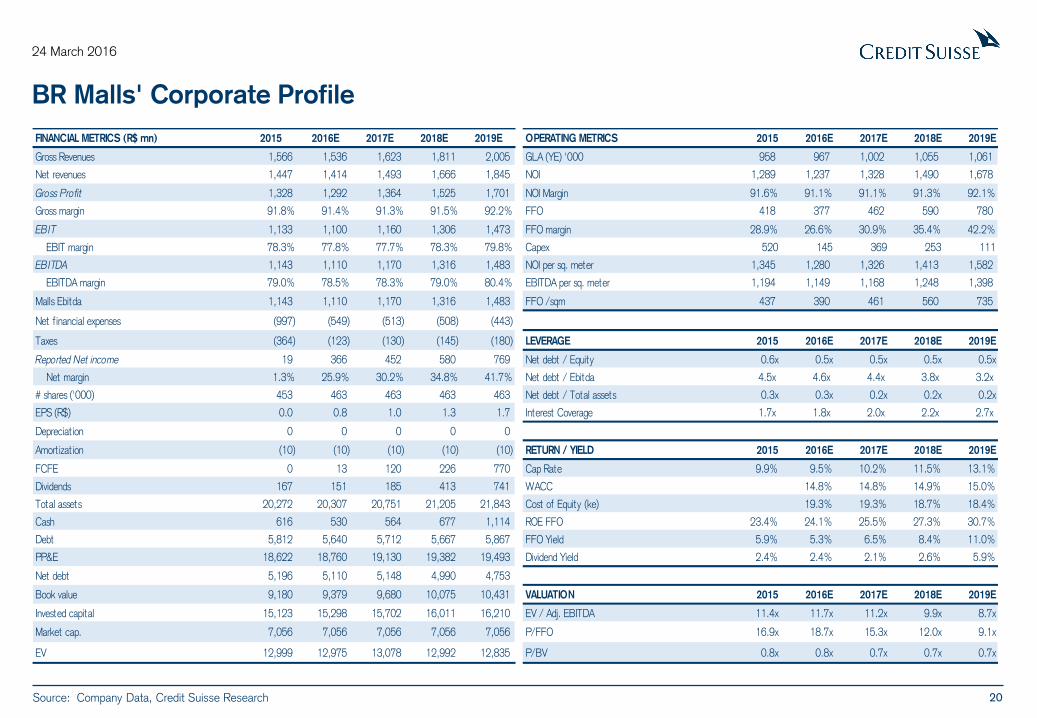

24 March 2016

BR Malls' Corporate Profile

Source: Company Data, Credit Suisse Research

FINANCIAL METRICS (R$ mn) 2015 2016E 2017E 2018E 2019E OPERATING METRICS 2015 2016E 2017E 2018E 2019E

Gross Revenues 1,566 1,536 1,623 1,811 2,005 GLA (YE) '000 958 967 1,002 1,055 1,061

Net revenues 1,447 1,414 1,493 1,666 1,845 NOI 1,289 1,237 1,328 1,490 1,678

Gross Profit 1,328 1,292 1,364 1,525 1,701 NOI Margin 91.6% 91.1% 91.1% 91.3% 92.1%

Gross margin 91.8% 91.4% 91.3% 91.5% 92.2% FFO 418 377 462 590 780

EBIT 1,133 1,100 1,160 1,306 1,473 FFO margin 28.9% 26.6% 30.9% 35.4% 42.2%

EBIT margin 78.3% 77.8% 77.7% 78.3% 79.8% Capex 520 145 369 253 111

EBITDA 1,143 1,110 1,170 1,316 1,483 NOI per sq. meter 1,345 1,280 1,326 1,413 1,582

EBITDA margin 79.0% 78.5% 78.3% 79.0% 80.4% EBITDA per sq. meter 1,194 1,149 1,168 1,248 1,398

Malls Ebitda 1,143 1,110 1,170 1,316 1,483 FFO /sqm 437 390 461 560 735

Net financial expenses (997) (549) (513) (508) (443)

Taxes (364) (123) (130) (145) (180) LEVERAGE 2015 2016E 2017E 2018E 2019E

Reported Net income 19 366 452 580 769 Net debt / Equity 0.6x 0.5x 0.5x 0.5x 0.5x

Net margin 1.3% 25.9% 30.2% 34.8% 41.7% Net debt / Ebitda 4.5x 4.6x 4.4x 3.8x 3.2x

# shares ('000) 453 463 463 463 463 Net debt / Total assets 0.3x 0.3x 0.2x 0.2x 0.2x

EPS (R$) 0.0 0.8 1.0 1.3 1.7 Interest Coverage 1.7x 1.8x 2.0x 2.2x 2.7x

Depreciat ion 0 0 0 0 0

Amort izat ion (10) (10) (10) (10) (10) RETURN / YIELD 2015 2016E 2017E 2018E 2019E

FCFE 0 13 120 226 770 Cap Rate 9.9% 9.5% 10.2% 11.5% 13.1%

Dividends 167 151 185 413 741 WACC 14.8% 14.8% 14.9% 15.0%

Total assets 20,272 20,307 20,751 21,205 21,843 Cost of Equity (ke) 19.3% 19.3% 18.7% 18.4%

Cash 616 530 564 677 1,114 ROE FFO 23.4% 24.1% 25.5% 27.3% 30.7%

Debt 5,812 5,640 5,712 5,667 5,867 FFO Yield 5.9% 5.3% 6.5% 8.4% 11.0%

PP&E 18,622 18,760 19,130 19,382 19,493 Dividend Yield 2.4% 2.4% 2.1% 2.6% 5.9%

Net debt 5,196 5,110 5,148 4,990 4,753

Book value 9,180 9,379 9,680 10,075 10,431 VALUATION 2015 2016E 2017E 2018E 2019E

Invested capital 15,123 15,298 15,702 16,011 16,210 EV / Adj. EBITDA 11.4x 11.7x 11.2x 9.9x 8.7x

Market cap. 7,056 7,056 7,056 7,056 7,056 P/FFO 16.9x 18.7x 15.3x 12.0x 9.1x

EV 12,999 12,975 13,078 12,992 12,835 P/BV 0.8x 0.8x 0.7x 0.7x 0.7x

21

24 March 2016

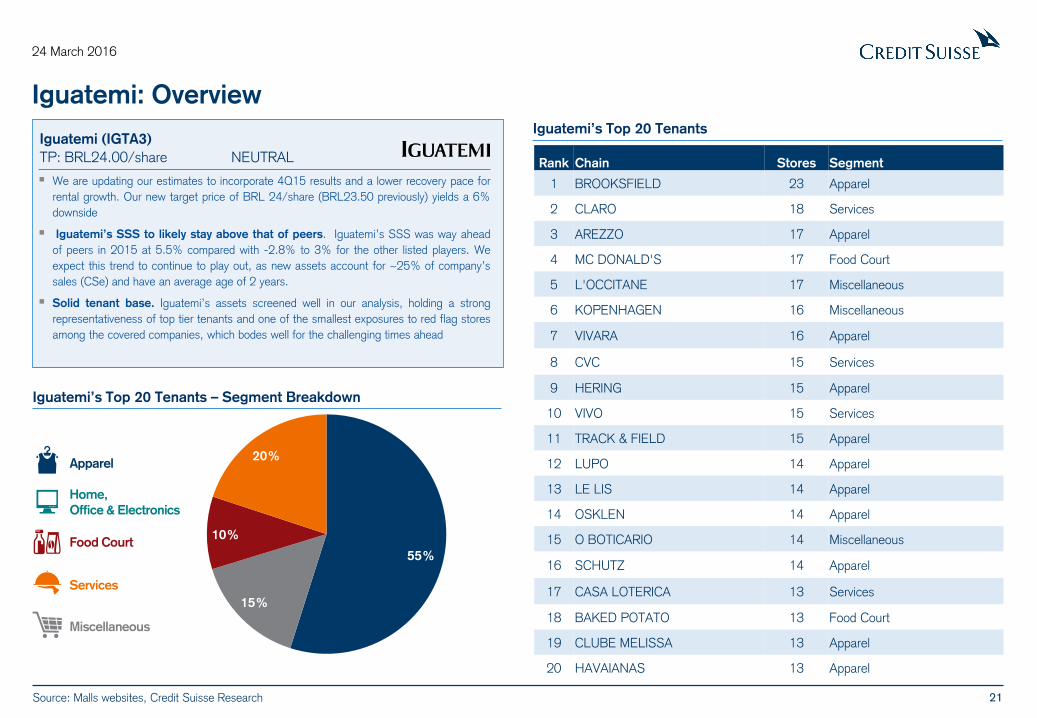

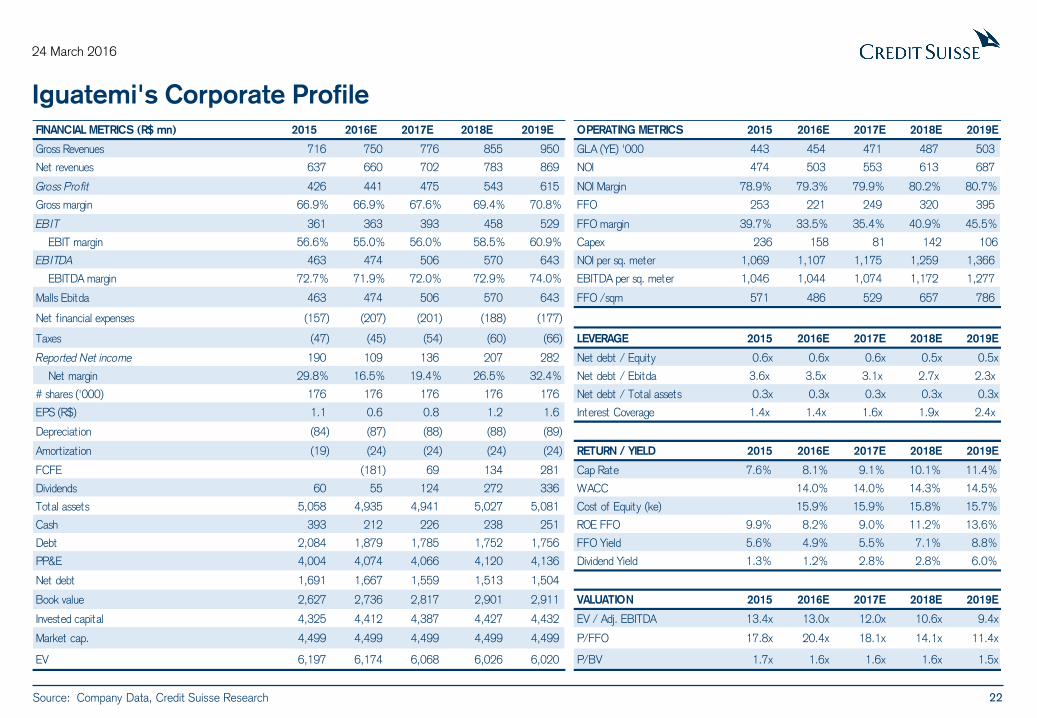

Iguatemi: Overview

We are updating our estimates to incorporate 4Q15 results and a lower recovery pace for

rental growth. Our new target price of BRL 24/share (BRL23.50 previously) yields a 6%

downside

Iguatemi’s SSS to likely stay above that of peers. Iguatemi’s SSS was way ahead

of peers in 2015 at 5.5% compared with -2.8% to 3% for the other listed players. We

expect this trend to continue to play out, as new assets account for ~25% of company’s

sales (CSe) and have an average age of 2 years.

Solid tenant base. Iguatemi’s assets screened well in our analysis, holding a strong

representativeness of top tier tenants and one of the smallest exposures to red flag stores

among the covered companies, which bodes well for the challenging times ahead

Iguatemi (IGTA3)

TP: BRL24.00/share NEUTRAL

Iguatemi’s Top 20 Tenants

Rank Chain Stores Segment

1 BROOKSFIELD 23 Apparel

2 CLARO 18 Services

3 AREZZO 17 Apparel

4 MC DONALD'S 17 Food Court

5 L'OCCITANE 17 Miscellaneous

6 KOPENHAGEN 16 Miscellaneous

7 VIVARA 16 Apparel

8 CVC 15 Services

9 HERING 15 Apparel

10 VIVO 15 Services

11 TRACK & FIELD 15 Apparel

12 LUPO 14 Apparel

13 LE LIS 14 Apparel

14 OSKLEN 14 Apparel

15 O BOTICARIO 14 Miscellaneous

16 SCHUTZ 14 Apparel

17 CASA LOTERICA 13 Services

18 BAKED POTATO 13 Food Court

19 CLUBE MELISSA 13 Apparel

20 HAVAIANAS 13 Apparel

55%

0%

15%

10%

20% Apparel

Home,

Office & Electronics

Food Court

Services

Miscellaneous

Iguatemi’s Top 20 Tenants – Segment Breakdown

Source: Malls websites, Credit Suisse Research

22

24 March 2016

Iguatemi's Corporate Profile

Source: Company Data, Credit Suisse Research

FINANCIAL METRICS (R$ mn) 2015 2016E 2017E 2018E 2019E OPERATING METRICS 2015 2016E 2017E 2018E 2019E

Gross Revenues 716 750 776 855 950 GLA (YE) '000 443 454 471 487 503

Net revenues 637 660 702 783 869 NOI 474 503 553 613 687

Gross Profit 426 441 475 543 615 NOI Margin 78.9% 79.3% 79.9% 80.2% 80.7%

Gross margin 66.9% 66.9% 67.6% 69.4% 70.8% FFO 253 221 249 320 395

EBIT 361 363 393 458 529 FFO margin 39.7% 33.5% 35.4% 40.9% 45.5%

EBIT margin 56.6% 55.0% 56.0% 58.5% 60.9% Capex 236 158 81 142 106

EBITDA 463 474 506 570 643 NOI per sq. meter 1,069 1,107 1,175 1,259 1,366

EBITDA margin 72.7% 71.9% 72.0% 72.9% 74.0% EBITDA per sq. meter 1,046 1,044 1,074 1,172 1,277

Malls Ebitda 463 474 506 570 643 FFO /sqm 571 486 529 657 786

Net financial expenses (157) (207) (201) (188) (177)

Taxes (47) (45) (54) (60) (66) LEVERAGE 2015 2016E 2017E 2018E 2019E

Reported Net income 190 109 136 207 282 Net debt / Equity 0.6x 0.6x 0.6x 0.5x 0.5x

Net margin 29.8% 16.5% 19.4% 26.5% 32.4% Net debt / Ebitda 3.6x 3.5x 3.1x 2.7x 2.3x

# shares ('000) 176 176 176 176 176 Net debt / Total assets 0.3x 0.3x 0.3x 0.3x 0.3x

EPS (R$) 1.1 0.6 0.8 1.2 1.6 Interest Coverage 1.4x 1.4x 1.6x 1.9x 2.4x

Depreciat ion (84) (87) (88) (88) (89)

Amort izat ion (19) (24) (24) (24) (24) RETURN / YIELD 2015 2016E 2017E 2018E 2019E

FCFE (181) 69 134 281 Cap Rate 7.6% 8.1% 9.1% 10.1% 11.4%

Dividends 60 55 124 272 336 WACC 14.0% 14.0% 14.3% 14.5%

Total assets 5,058 4,935 4,941 5,027 5,081 Cost of Equity (ke) 15.9% 15.9% 15.8% 15.7%

Cash 393 212 226 238 251 ROE FFO 9.9% 8.2% 9.0% 11.2% 13.6%

Debt 2,084 1,879 1,785 1,752 1,756 FFO Yield 5.6% 4.9% 5.5% 7.1% 8.8%

PP&E 4,004 4,074 4,066 4,120 4,136 Dividend Yield 1.3% 1.2% 2.8% 2.8% 6.0%

Net debt 1,691 1,667 1,559 1,513 1,504

Book value 2,627 2,736 2,817 2,901 2,911 VALUATION 2015 2016E 2017E 2018E 2019E

Invested capital 4,325 4,412 4,387 4,427 4,432 EV / Adj. EBITDA 13.4x 13.0x 12.0x 10.6x 9.4x

Market cap. 4,499 4,499 4,499 4,499 4,499 P/FFO 17.8x 20.4x 18.1x 14.1x 11.4x

EV 6,197 6,174 6,068 6,026 6,020 P/BV 1.7x 1.6x 1.6x 1.6x 1.5x

23

24 March 2016

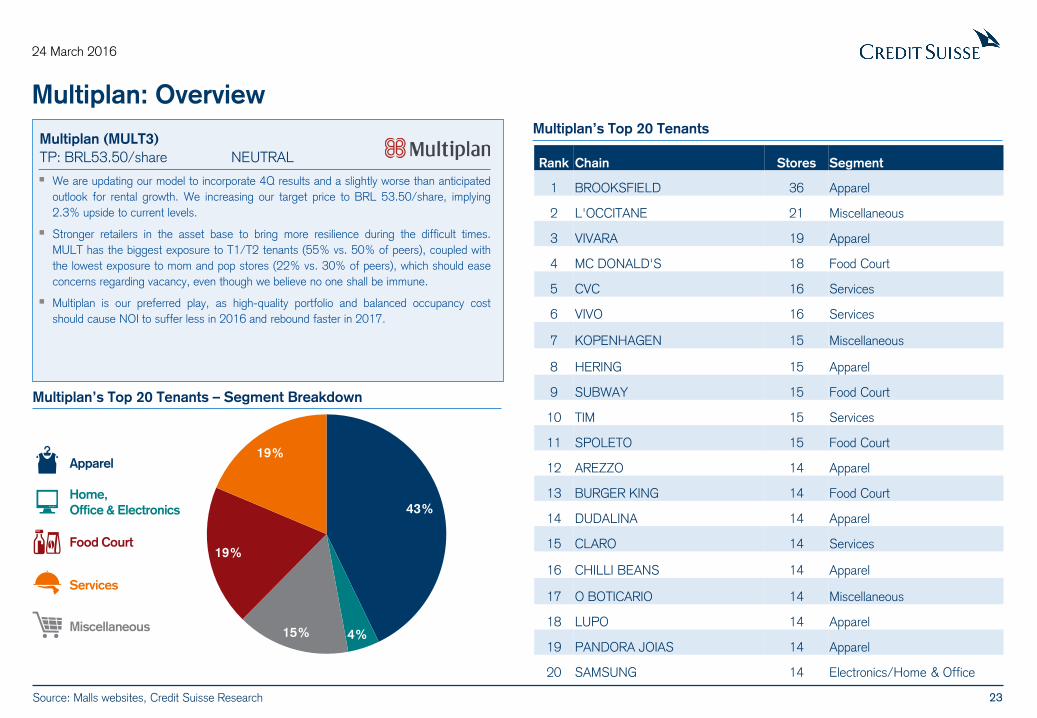

Multiplan: Overview

We are updating our model to incorporate 4Q results and a slightly worse than anticipated

outlook for rental growth. We increasing our target price to BRL 53.50/share, implying

2.3% upside to current levels.

Stronger retailers in the asset base to bring more resilience during the difficult times.

MULT has the biggest exposure to T1/T2 tenants (55% vs. 50% of peers), coupled with

the lowest exposure to mom and pop stores (22% vs. 30% of peers), which should ease

concerns regarding vacancy, even though we believe no one shall be immune.

Multiplan is our preferred play, as high-quality portfolio and balanced occupancy cost

should cause NOI to suffer less in 2016 and rebound faster in 2017.

Multiplan (MULT3)

TP: BRL53.50/share NEUTRAL

Multiplan’s Top 20 Tenants

Rank Chain Stores Segment

1 BROOKSFIELD 36 Apparel

2 L'OCCITANE 21 Miscellaneous

3 VIVARA 19 Apparel

4 MC DONALD'S 18 Food Court

5 CVC 16 Services

6 VIVO 16 Services

7 KOPENHAGEN 15 Miscellaneous

8 HERING 15 Apparel

9 SUBWAY 15 Food Court

10 TIM 15 Services

11 SPOLETO 15 Food Court

12 AREZZO 14 Apparel

13 BURGER KING 14 Food Court

14 DUDALINA 14 Apparel

15 CLARO 14 Services

16 CHILLI BEANS 14 Apparel

17 O BOTICARIO 14 Miscellaneous

18 LUPO 14 Apparel

19 PANDORA JOIAS 14 Apparel

20 SAMSUNG 14 Electronics/Home & Office

43%

4% 15%

19%

19% Apparel

Home,

Office & Electronics

Food Court

Services

Miscellaneous

Multiplan’s Top 20 Tenants – Segment Breakdown

Source: Malls websites, Credit Suisse Research

24

24 March 2016

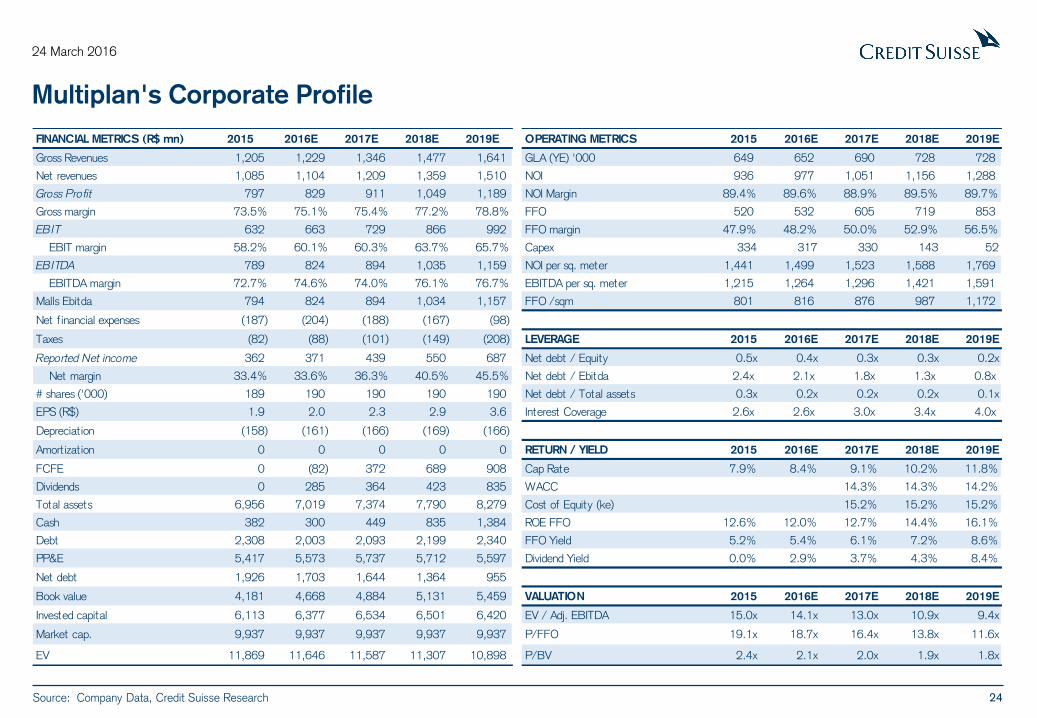

Multiplan's Corporate Profile

Source: Company Data, Credit Suisse Research

FINANCIAL METRICS (R$ mn) 2015 2016E 2017E 2018E 2019E OPERATING METRICS 2015 2016E 2017E 2018E 2019E

Gross Revenues 1,205 1,229 1,346 1,477 1,641 GLA (YE) '000 649 652 690 728 728

Net revenues 1,085 1,104 1,209 1,359 1,510 NOI 936 977 1,051 1,156 1,288

Gross Profit 797 829 911 1,049 1,189 NOI Margin 89.4% 89.6% 88.9% 89.5% 89.7%

Gross margin 73.5% 75.1% 75.4% 77.2% 78.8% FFO 520 532 605 719 853

EBIT 632 663 729 866 992 FFO margin 47.9% 48.2% 50.0% 52.9% 56.5%

EBIT margin 58.2% 60.1% 60.3% 63.7% 65.7% Capex 334 317 330 143 52

EBITDA 789 824 894 1,035 1,159 NOI per sq. meter 1,441 1,499 1,523 1,588 1,769

EBITDA margin 72.7% 74.6% 74.0% 76.1% 76.7% EBITDA per sq. meter 1,215 1,264 1,296 1,421 1,591

Malls Ebitda 794 824 894 1,034 1,157 FFO /sqm 801 816 876 987 1,172

Net financial expenses (187) (204) (188) (167) (98)

Taxes (82) (88) (101) (149) (208) LEVERAGE 2015 2016E 2017E 2018E 2019E

Reported Net income 362 371 439 550 687 Net debt / Equity 0.5x 0.4x 0.3x 0.3x 0.2x

Net margin 33.4% 33.6% 36.3% 40.5% 45.5% Net debt / Ebitda 2.4x 2.1x 1.8x 1.3x 0.8x

# shares ('000) 189 190 190 190 190 Net debt / Total assets 0.3x 0.2x 0.2x 0.2x 0.1x

EPS (R$) 1.9 2.0 2.3 2.9 3.6 Interest Coverage 2.6x 2.6x 3.0x 3.4x 4.0x

Depreciat ion (158) (161) (166) (169) (166)

Amort izat ion 0 0 0 0 0 RETURN / YIELD 2015 2016E 2017E 2018E 2019E

FCFE 0 (82) 372 689 908 Cap Rate 7.9% 8.4% 9.1% 10.2% 11.8%

Dividends 0 285 364 423 835 WACC 14.3% 14.3% 14.2%

Total assets 6,956 7,019 7,374 7,790 8,279 Cost of Equity (ke) 15.2% 15.2% 15.2%

Cash 382 300 449 835 1,384 ROE FFO 12.6% 12.0% 12.7% 14.4% 16.1%

Debt 2,308 2,003 2,093 2,199 2,340 FFO Yield 5.2% 5.4% 6.1% 7.2% 8.6%

PP&E 5,417 5,573 5,737 5,712 5,597 Dividend Yield 0.0% 2.9% 3.7% 4.3% 8.4%

Net debt 1,926 1,703 1,644 1,364 955

Book value 4,181 4,668 4,884 5,131 5,459 VALUATION 2015 2016E 2017E 2018E 2019E

Invested capital 6,113 6,377 6,534 6,501 6,420 EV / Adj. EBITDA 15.0x 14.1x 13.0x 10.9x 9.4x

Market cap. 9,937 9,937 9,937 9,937 9,937 P/FFO 19.1x 18.7x 16.4x 13.8x 11.6x

EV 11,869 11,646 11,587 11,307 10,898 P/BV 2.4x 2.1x 2.0x 1.9x 1.8x

25

24 March 2016

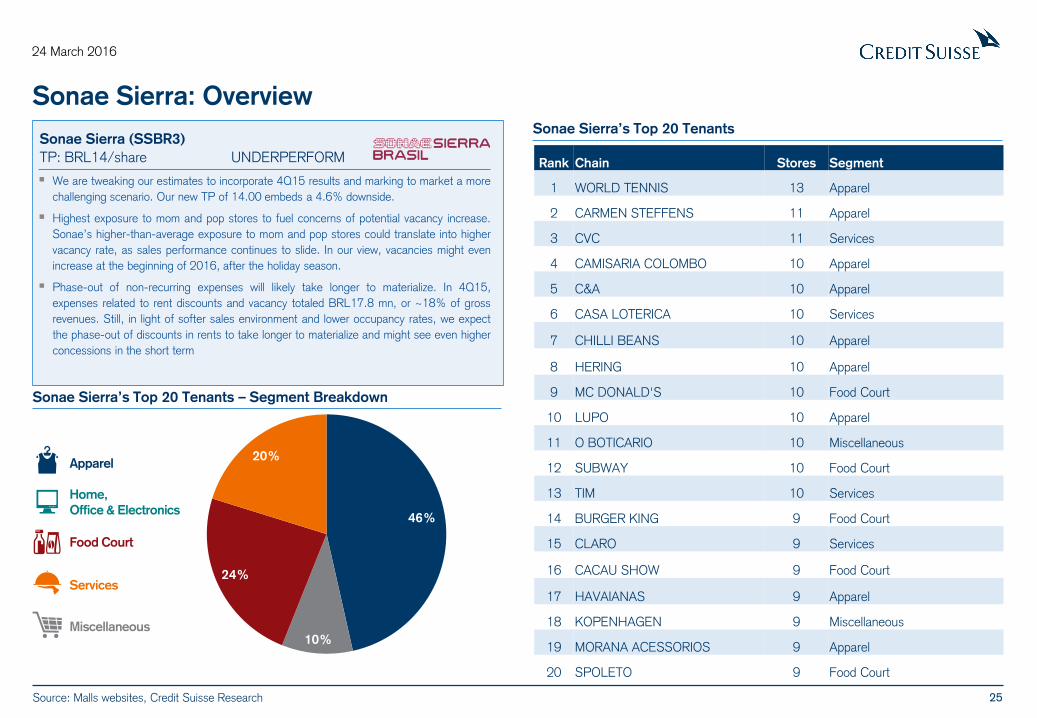

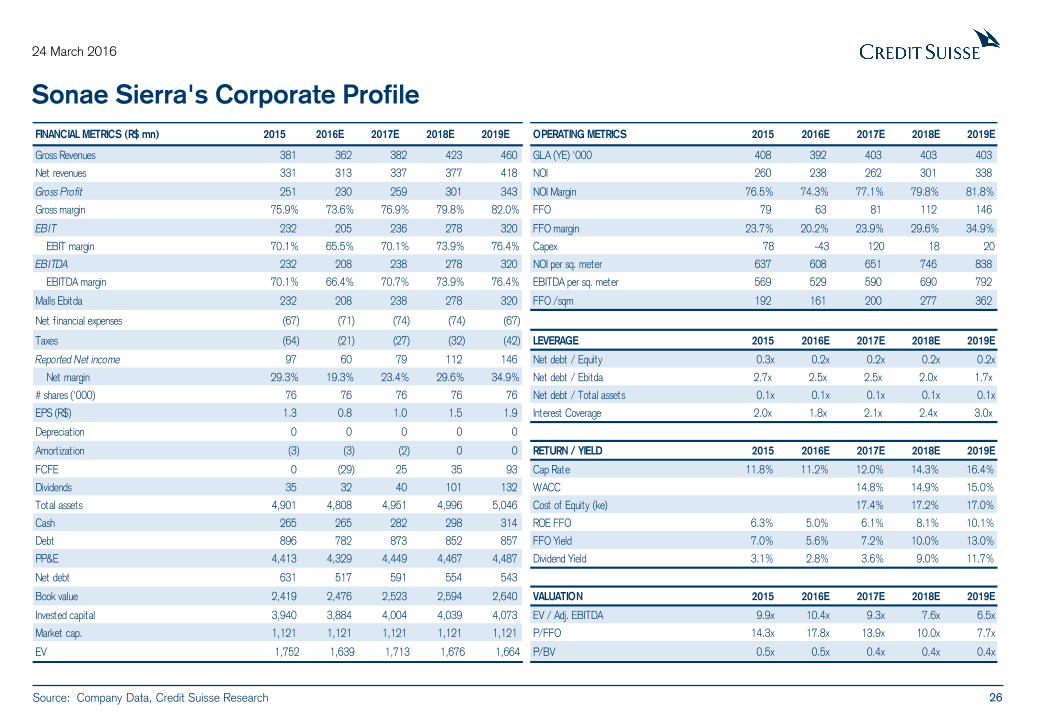

Sonae Sierra: Overview

We are tweaking our estimates to incorporate 4Q15 results and marking to market a more

challenging scenario. Our new TP of 14.00 embeds a 4.6% downside.

Highest exposure to mom and pop stores to fuel concerns of potential vacancy increase.

Sonae’s higher-than-average exposure to mom and pop stores could translate into higher

vacancy rate, as sales performance continues to slide. In our view, vacancies might even

increase at the beginning of 2016, after the holiday season.

Phase-out of non-recurring expenses will likely take longer to materialize. In 4Q15,

expenses related to rent discounts and vacancy totaled BRL17.8 mn, or ~18% of gross

revenues. Still, in light of softer sales environment and lower occupancy rates, we expect

the phase-out of discounts in rents to take longer to materialize and might see even higher

concessions in the short term

Sonae Sierra (SSBR3)

TP: BRL14/share UNDERPERFORM

Sonae Sierra’s Top 20 Tenants

Rank Chain Stores Segment

1 WORLD TENNIS 13 Apparel

2 CARMEN STEFFENS 11 Apparel

3 CVC 11 Services

4 CAMISARIA COLOMBO 10 Apparel

5 C&A 10 Apparel

6 CASA LOTERICA 10 Services

7 CHILLI BEANS 10 Apparel

8 HERING 10 Apparel

9 MC DONALD'S 10 Food Court

10 LUPO 10 Apparel

11 O BOTICARIO 10 Miscellaneous

12 SUBWAY 10 Food Court

13 TIM 10 Services

14 BURGER KING 9 Food Court

15 CLARO 9 Services

16 CACAU SHOW 9 Food Court

17 HAVAIANAS 9 Apparel

18 KOPENHAGEN 9 Miscellaneous

19 MORANA ACESSORIOS 9 Apparel

20 SPOLETO 9 Food Court

46%

0%

10%

24%

20% Apparel

Home,

Office & Electronics

Food Court

Services

Miscellaneous

Sonae Sierra’s Top 20 Tenants – Segment Breakdown

Source: Malls websites, Credit Suisse Research

26

24 March 2016

Sonae Sierra's Corporate Profile

Source: Company Data, Credit Suisse Research

FINANCIAL METRICS (R$ mn) 2015 2016E 2017E 2018E 2019E OPERATING METRICS 2015 2016E 2017E 2018E 2019E

Gross Revenues 381 362 382 423 460 GLA (YE) '000 408 392 403 403 403

Net revenues 331 313 337 377 418 NOI 260 238 262 301 338

Gross Profit 251 230 259 301 343 NOI Margin 76.5% 74.3% 77.1% 79.8% 81.8%

Gross margin 75.9% 73.6% 76.9% 79.8% 82.0% FFO 79 63 81 112 146

EBIT 232 205 236 278 320 FFO margin 23.7% 20.2% 23.9% 29.6% 34.9%

EBIT margin 70.1% 65.5% 70.1% 73.9% 76.4% Capex 78 -43 120 18 20

EBITDA 232 208 238 278 320 NOI per sq. meter 637 608 651 746 838

EBITDA margin 70.1% 66.4% 70.7% 73.9% 76.4% EBITDA per sq. meter 569 529 590 690 792

Malls Ebitda 232 208 238 278 320 FFO /sqm 192 161 200 277 362

Net financial expenses (67) (71) (74) (74) (67)

Taxes (64) (21) (27) (32) (42) LEVERAGE 2015 2016E 2017E 2018E 2019E

Reported Net income 97 60 79 112 146 Net debt / Equity 0.3x 0.2x 0.2x 0.2x 0.2x

Net margin 29.3% 19.3% 23.4% 29.6% 34.9% Net debt / Ebitda 2.7x 2.5x 2.5x 2.0x 1.7x

# shares ('000) 76 76 76 76 76 Net debt / Total assets 0.1x 0.1x 0.1x 0.1x 0.1x

EPS (R$) 1.3 0.8 1.0 1.5 1.9 Interest Coverage 2.0x 1.8x 2.1x 2.4x 3.0x

Depreciat ion 0 0 0 0 0

Amort izat ion (3) (3) (2) 0 0 RETURN / YIELD 2015 2016E 2017E 2018E 2019E

FCFE 0 (29) 25 35 93 Cap Rate 11.8% 11.2% 12.0% 14.3% 16.4%

Dividends 35 32 40 101 132 WACC 14.8% 14.9% 15.0%

Total assets 4,901 4,808 4,951 4,996 5,046 Cost of Equity (ke) 17.4% 17.2% 17.0%

Cash 265 265 282 298 314 ROE FFO 6.3% 5.0% 6.1% 8.1% 10.1%

Debt 896 782 873 852 857 FFO Yield 7.0% 5.6% 7.2% 10.0% 13.0%

PP&E 4,413 4,329 4,449 4,467 4,487 Dividend Yield 3.1% 2.8% 3.6% 9.0% 11.7%

Net debt 631 517 591 554 543

Book value 2,419 2,476 2,523 2,594 2,640 VALUATION 2015 2016E 2017E 2018E 2019E

Invested capital 3,940 3,884 4,004 4,039 4,073 EV / Adj. EBITDA 9.9x 10.4x 9.3x 7.6x 6.5x

Market cap. 1,121 1,121 1,121 1,121 1,121 P/FFO 14.3x 17.8x 13.9x 10.0x 7.7x

EV 1,752 1,639 1,713 1,676 1,664 P/BV 0.5x 0.5x 0.4x 0.4x 0.4x

27

24 March 2016

New vs. Old Estimates (In R$ ‘000 unless otherwise stated)

Source: Company Data, Credit Suisse Research

2016 2017 2018

Old New Change Old New Change Old New Change

Net Revenues 1,119,834 1,103,777 -1.4% 1,271,378 1,208,599 -4.9% 1,475,261 1,359,195 -7.9%

NOI 983,897 976,572 -0.7% 1,103,827 1,051,144 -4.8% 1,248,800 1,156,308 -7.4%

NOI Margin 89.3% 89.6% 0.3 p.p. 88.9% 88.9% 0.0 p.p. 89.5% 89.5% 0.0 p.p.

Ebitda 823,003 823,711 0.1% 942,057 894,470 -5.1% 1,133,514 1,034,842 -8.7%

Ebitda Margin 73% 75% 1.1 p.p. 74% 74% -0.1 p.p. 77% 76% -0.7 p.p.

Malls Ebitda 823,003 823,711 0.1% 942,057 894,470 -5.1% 1,132,157 1,033,587 -8.7%

Malls Ebitda Margin 73% 75% 1.1 p.p. 74% 74% -0.1 p.p. 77% 76% -0.7 p.p.

Net Income 352,308 371,199 5.4% 436,185 438,769 0.6% 578,082 550,153 -4.8%

Net Margin 31.5% 33.6% 2.2 p.p. 34.3% 36.3% 2.0 p.p. 39.2% 40.5% 1.3 p.p.

FFO 514,597 531,969 3.4% 604,995 604,566 -0.1% 751,123 718,680 -4.3%

FFO Margin 46.0% 48.2% 2.2 p.p. 47.6% 50.0% 2.4 p.p. 50.9% 52.9% 2.0 p.p.

2016 2017 2018

Old New Change Old New Change Old New Change

Net Revenues 1,427,663 1,413,795 -1.0% 1,563,450 1,493,312 -4.5% 1,804,564 1,666,391 -7.7%

NOI 1,241,766 1,236,981 -0.4% 1,386,064 1,328,195 -4.2% 1,624,064 1,490,151 -8.2%

NOI Margin 90.8% 91.1% 0.2 p.p. 91.2% 91.1% 0.0 p.p. 92.5% 91.3% -1.2 p.p.

Ebitda 1,105,872 1,110,404 0.4% 1,217,219 1,169,918 -3.9% 1,459,308 1,315,895 -9.8%

Ebitda Margin 77% 79% 1.1 p.p. 78% 78% 0.5 p.p. 81% 79% -1.9 p.p.

Malls Ebitda 1,105,872 1,110,404 0.4% 1,217,219 1,169,918 -3.9% 1,459,308 1,315,895 -9.8%

Malls Ebitda Margin 77% 79% 1.1 p.p. 78% 78% 0.5 p.p. 81% 79% -1.9 p.p.

Net Income 378,616 366,338 -3.2% 511,241 451,659 -11.7% 617,528 580,000 -6.1%

Net Margin 26.5% 25.9% -0.6 p.p. 32.7% 30.2% -2.5 p.p. 34.2% 34.8% 0.6 p.p.

FFO 388,932 376,646 -3.2% 521,557 461,967 -11.4% 627,844 590,308 -6.0%

FFO Margin 27.2% 26.6% -0.6 p.p. 33.4% 30.9% -2.4 p.p. 34.8% 35.4% 0.6 p.p.

28

24 March 2016

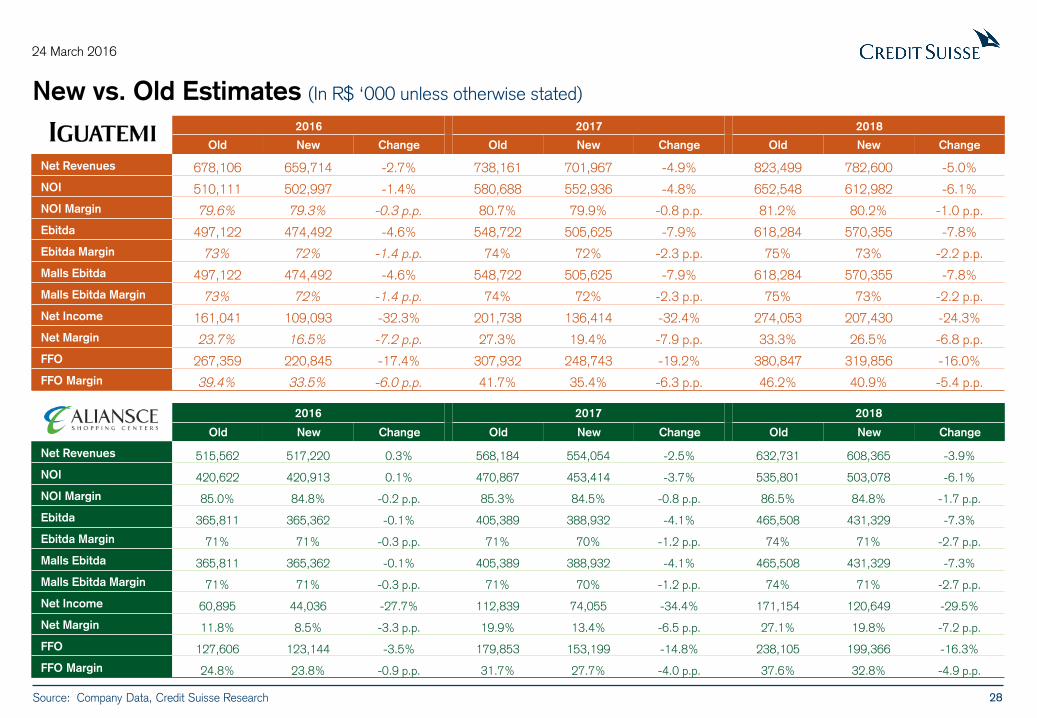

New vs. Old Estimates (In R$ ‘000 unless otherwise stated)

Source: Company Data, Credit Suisse Research

2016 2017 2018

Old New Change Old New Change Old New Change

Net Revenues 678,106 659,714 -2.7% 738,161 701,967 -4.9% 823,499 782,600 -5.0%

NOI 510,111 502,997 -1.4% 580,688 552,936 -4.8% 652,548 612,982 -6.1%

NOI Margin 79.6% 79.3% -0.3 p.p. 80.7% 79.9% -0.8 p.p. 81.2% 80.2% -1.0 p.p.

Ebitda 497,122 474,492 -4.6% 548,722 505,625 -7.9% 618,284 570,355 -7.8%

Ebitda Margin 73% 72% -1.4 p.p. 74% 72% -2.3 p.p. 75% 73% -2.2 p.p.

Malls Ebitda 497,122 474,492 -4.6% 548,722 505,625 -7.9% 618,284 570,355 -7.8%

Malls Ebitda Margin 73% 72% -1.4 p.p. 74% 72% -2.3 p.p. 75% 73% -2.2 p.p.

Net Income 161,041 109,093 -32.3% 201,738 136,414 -32.4% 274,053 207,430 -24.3%

Net Margin 23.7% 16.5% -7.2 p.p. 27.3% 19.4% -7.9 p.p. 33.3% 26.5% -6.8 p.p.

FFO 267,359 220,845 -17.4% 307,932 248,743 -19.2% 380,847 319,856 -16.0%

FFO Margin 39.4% 33.5% -6.0 p.p. 41.7% 35.4% -6.3 p.p. 46.2% 40.9% -5.4 p.p.

2016 2017 2018

Old New Change Old New Change Old New Change

Net Revenues 515,562 517,220 0.3% 568,184 554,054 -2.5% 632,731 608,365 -3.9%

NOI 420,622 420,913 0.1% 470,867 453,414 -3.7% 535,801 503,078 -6.1%

NOI Margin 85.0% 84.8% -0.2 p.p. 85.3% 84.5% -0.8 p.p. 86.5% 84.8% -1.7 p.p.

Ebitda 365,811 365,362 -0.1% 405,389 388,932 -4.1% 465,508 431,329 -7.3%

Ebitda Margin 71% 71% -0.3 p.p. 71% 70% -1.2 p.p. 74% 71% -2.7 p.p.

Malls Ebitda 365,811 365,362 -0.1% 405,389 388,932 -4.1% 465,508 431,329 -7.3%

Malls Ebitda Margin 71% 71% -0.3 p.p. 71% 70% -1.2 p.p. 74% 71% -2.7 p.p.

Net Income 60,895 44,036 -27.7% 112,839 74,055 -34.4% 171,154 120,649 -29.5%

Net Margin 11.8% 8.5% -3.3 p.p. 19.9% 13.4% -6.5 p.p. 27.1% 19.8% -7.2 p.p.

FFO 127,606 123,144 -3.5% 179,853 153,199 -14.8% 238,105 199,366 -16.3%

FFO Margin 24.8% 23.8% -0.9 p.p. 31.7% 27.7% -4.0 p.p. 37.6% 32.8% -4.9 p.p.

29

24 March 2016

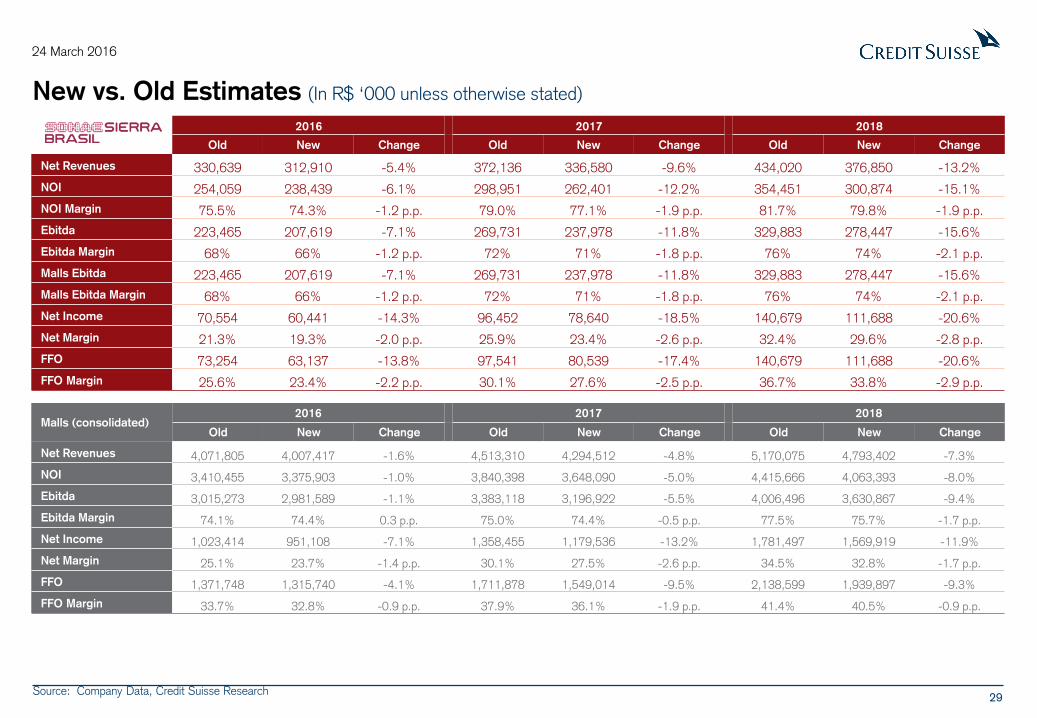

New vs. Old Estimates (In R$ ‘000 unless otherwise stated)

Source: Company Data, Credit Suisse Research

2016 2017 2018

Old New Change Old New Change Old New Change

Net Revenues 330,639 312,910 -5.4% 372,136 336,580 -9.6% 434,020 376,850 -13.2%

NOI 254,059 238,439 -6.1% 298,951 262,401 -12.2% 354,451 300,874 -15.1%

NOI Margin 75.5% 74.3% -1.2 p.p. 79.0% 77.1% -1.9 p.p. 81.7% 79.8% -1.9 p.p.

Ebitda 223,465 207,619 -7.1% 269,731 237,978 -11.8% 329,883 278,447 -15.6%

Ebitda Margin 68% 66% -1.2 p.p. 72% 71% -1.8 p.p. 76% 74% -2.1 p.p.

Malls Ebitda 223,465 207,619 -7.1% 269,731 237,978 -11.8% 329,883 278,447 -15.6%

Malls Ebitda Margin 68% 66% -1.2 p.p. 72% 71% -1.8 p.p. 76% 74% -2.1 p.p.

Net Income 70,554 60,441 -14.3% 96,452 78,640 -18.5% 140,679 111,688 -20.6%

Net Margin 21.3% 19.3% -2.0 p.p. 25.9% 23.4% -2.6 p.p. 32.4% 29.6% -2.8 p.p.

FFO 73,254 63,137 -13.8% 97,541 80,539 -17.4% 140,679 111,688 -20.6%

FFO Margin 25.6% 23.4% -2.2 p.p. 30.1% 27.6% -2.5 p.p. 36.7% 33.8% -2.9 p.p.

Malls (consolidated) 2016 2017 2018

Old New Change Old New Change Old New Change

Net Revenues 4,071,805 4,007,417 -1.6% 4,513,310 4,294,512 -4.8% 5,170,075 4,793,402 -7.3%

NOI 3,410,455 3,375,903 -1.0% 3,840,398 3,648,090 -5.0% 4,415,666 4,063,393 -8.0%

Ebitda 3,015,273 2,981,589 -1.1% 3,383,118 3,196,922 -5.5% 4,006,496 3,630,867 -9.4%

Ebitda Margin 74.1% 74.4% 0.3 p.p. 75.0% 74.4% -0.5 p.p. 77.5% 75.7% -1.7 p.p.

Net Income 1,023,414 951,108 -7.1% 1,358,455 1,179,536 -13.2% 1,781,497 1,569,919 -11.9%

Net Margin 25.1% 23.7% -1.4 p.p. 30.1% 27.5% -2.6 p.p. 34.5% 32.8% -1.7 p.p.

FFO 1,371,748 1,315,740 -4.1% 1,711,878 1,549,014 -9.5% 2,138,599 1,939,897 -9.3%

FFO Margin 33.7% 32.8% -0.9 p.p. 37.9% 36.1% -1.9 p.p. 41.4% 40.5% -0.9 p.p.

30

24 March 2016

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Companies Mentioned (Price as of 24-Mar-2016)

Aliansce Shopping Centers (ALSC3.SA, R$12.74, NEUTRAL, TP R$12.5) Alpargatas SA (ALPA4.SA, R$7.75) Arezzo Industria e Comercio SA (ARZZ3.SA, R$22.0) BR Malls Participacoes (BRML3.SA, R$15.25, NEUTRAL, TP R$14.0) Burger King Worldwide, Inc. (BKW.N, $35.5) CIA Hering S.A. (HGTX3.SA, R$15.06) CVC Brasil (CVCB3.SA, R$15.95) Guararapes Confe (GUAR3.SA, R$52.99) Hewlett Packard Enterprise (HPE.N, $17.57) Iguatemi (IGTA3.SA, R$25.5, NEUTRAL, TP R$24.0) Lindt & Sprungli (LISN.S, SFr68450.0) Lojas Americanas S.A. (LAME4.SA, R$21.14) Lojas Renner S.A. (LREN3.SA, R$21.5) McDonald's Corp (MCD.N, $123.29) Multiplan Empreendimentos. Imobiliarios S/A (MULT3.SA, R$52.3, NEUTRAL, TP R$53.5) Restoque Comércio e Confecções de Roupas S.A. (LLIS3.SA, R$5.21) Samsung Elec (SMSN.BA, $366.5) Sonae Sierra Brasil (SSBR3.SA, R$14.67, UNDERPERFORM, TP R$14.0) TIM Participacoes (TIMP3.SA, R$8.2) Via Varejo S.A (VVAR11.SA, R$5.9)

Disclosure Appendix

Important Global Disclosures

Nicole Hirakawa, Luis Stacchini and Vanessa Quiroga, CFA each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

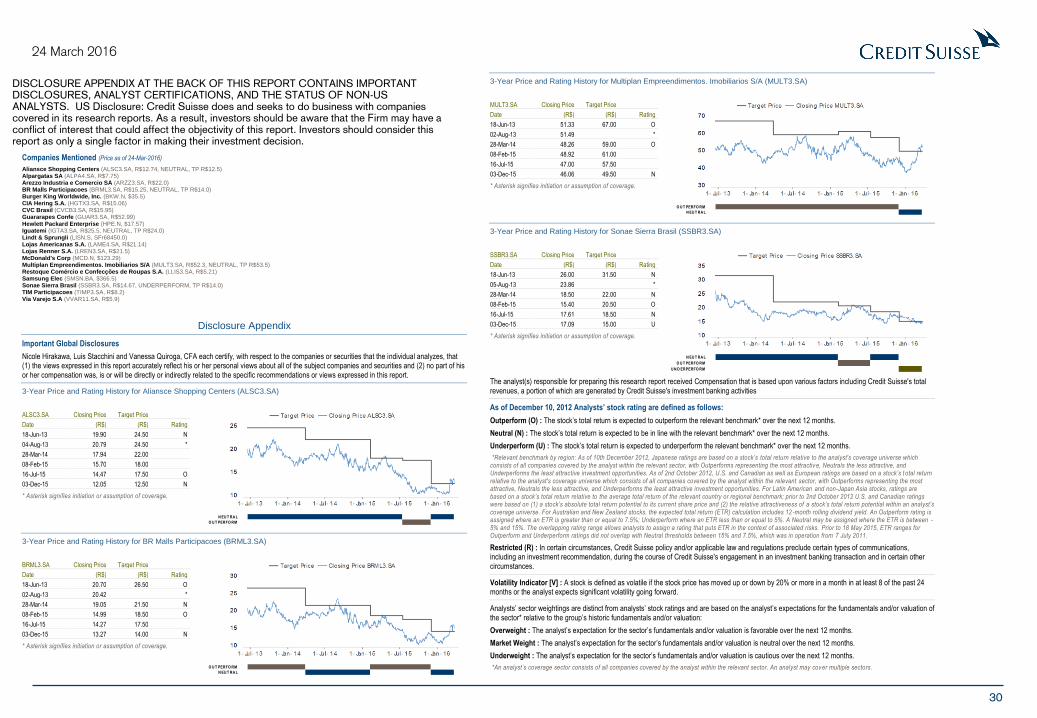

3-Year Price and Rating History for Aliansce Shopping Centers (ALSC3.SA)

ALSC3.SA Closing Price Target Price

Date (R$) (R$) Rating

18-Jun-13 19.90 24.50 N

04-Aug-13 20.79 24.50 *

28-Mar-14 17.94 22.00

08-Feb-15 15.70 18.00

16-Jul-15 14.47 17.50 O

03-Dec-15 12.05 12.50 N

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

O U T PERFO RM

3-Year Price and Rating History for BR Malls Participacoes (BRML3.SA)

BRML3.SA Closing Price Target Price

Date (R$) (R$) Rating

18-Jun-13 20.70 26.50 O

02-Aug-13 20.42 *

28-Mar-14 19.05 21.50 N

08-Feb-15 14.99 18.50 O

16-Jul-15 14.27 17.50

03-Dec-15 13.27 14.00 N

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

3-Year Price and Rating History for Multiplan Empreendimentos. Imobiliarios S/A (MULT3.SA)

MULT3.SA Closing Price Target Price

Date (R$) (R$) Rating

18-Jun-13 51.33 67.00 O

02-Aug-13 51.49 *

28-Mar-14 48.26 59.00 O

08-Feb-15 48.92 61.00

16-Jul-15 47.00 57.50

03-Dec-15 46.06 49.50 N

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

3-Year Price and Rating History for Sonae Sierra Brasil (SSBR3.SA)

SSBR3.SA Closing Price Target Price

Date (R$) (R$) Rating

18-Jun-13 26.00 31.50 N

05-Aug-13 23.86 *

28-Mar-14 18.50 22.00 N

08-Feb-15 15.40 20.50 O

16-Jul-15 17.61 18.50 N

03-Dec-15 17.09 15.00 U

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

O U T PERFO RM

U N D ERPERFO RM

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark* over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractiv e, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s t otal return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin American and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, the expected total return (ETR) calculation includes 12 -month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform where an ETR less than or equal to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

31

24 March 2016

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 57% (39% banking clients)

Neutral/Hold* 31% (29% banking clients)

Underperform/Sell* 11% (45% banking clients)

Restricted 1%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, an d Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdings, and other indivi dual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Aliansce Shopping Centers (ALSC3.SA)

Method: Our blended NAV (50% weight) and DCF (50% weight) price target of BRL 12.50 for ALSC3 assumes a 16.3% WACC and implies a target P/FFO multiple of 16.1x for 2016. Our rating of NEUTRAL is based on the company's valuation and the stock's expected return relative to country's benchmark over the next 12 months.

Risk: Factors that could impede achievement of our BRL 12.50 target price and change the rating of NEUTRAL for ALSC3 shares include: (1) Competition from new players driving yields downwards; (2) increase in the basic interest rate, (3) deterioration in consuption could lead to lower earnings given sector's leverage on the retail industry performance.

Target Price and Rating Valuation Methodology and Risks: (12 months) for BR Malls Participacoes (BRML3.SA)

Method: Our target price of R$14/share for BRML3 shares is based on a blended discounted cash flow to firm method (50% weight) using a 15.2%% WACC and a target NAV multiple (50% weight). At our R$14 TP, BR Malls would be trading at a P/FFO of 18x for 2016. Our rating of NEUTRAL is based on the company's valuation and the stock's expected return relative to country's benchmark over the next 12 months.

Risk: Risks to our R$14 target price and rating of NEUTRAL for BRML3 are (1) Competition from new players driving yields downwards; (2) increase in the basic interest rate; (3) deterioration in consumption could lead to lower earnings given the sector's leverage on the retail industry performance

Target Price and Rating Valuation Methodology and Risks: (12 months) for Iguatemi (IGTA3.SA)

Method: Our target price of R$24/share for IGTA3 shares is based on our blended discounted cash flow to firm method using a 14.2% WACC (50% weight) and a target NAV multiple (50% weight). At our TP of R$23/share , Iguatemi would be trading at a P/FFO (price/funds from operations) of 19x for 2016. Our rating of NEUTRAL is based on the company's valuation and the stock's expected return relative to country's benchmark over the next 12 months.

Risk: Factors that could impede achievement of our R$24 target price and change the rating of NEUTRAL for IGTA3 shares include: (1) competition from new players driving yields downwards; (2) increase in the basic interest rate; (3) deterioration in consumption could lead to lower earnings given the sector's leverage on the retail industry performance.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Multiplan Empreendimentos. Imobiliarios S/A (MULT3.SA)

Method: Our target price of R$53.5/share for MULT3 shares is based on our blended discounted cash flow to firm (FCFF) using a 13.8% WACC (50% weight) and a target NAV multiple (50% weight). At our R$53.5/share TP, Multiplan would be trading at R$19.1x P/FFO (price/funds from operations) for 2016. Our rating of NEUTRAL is based on the company's valuation and the stock's expected return relative to country's benchmark over the next 12 months.

Risk: Factors that could impede achievement of our R$53.5 target price and change the rating of NEUTRAL for MULT3 shares include: (1) competition from new players driving yields downwards; (2) increase in the real interest rates of the economy and (3) Deterioration in consumption could lead to lower NOIs given the sector's leverage on the retail industry performance

Target Price and Rating Valuation Methodology and Risks: (12 months) for Sonae Sierra Brasil (SSBR3.SA)

Method: Our target price of R$14/share for SSBR3 shares is based on our blended discounted cash flow to firm method using a 14.9% WACC (50% weight) and a target NAV multiple (50% weight) . At our R$14 TP, Sonae Sierra would be trading at 16.9x P/FFO 2016. Our rating of UNDERPERFORM is based on the company's valuation and the stock's expected return relative to country's benchmark over the next 12 months.

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 57% (39% banking clients)

Neutral/Hold* 31% (29% banking clients)

Underperform/Sell* 11% (45% banking clients)

Restricted 1%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, an d Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdings, and other indivi dual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Aliansce Shopping Centers (ALSC3.SA)

Method: Our blended NAV (50% weight) and DCF (50% weight) price target of BRL 12.50 for ALSC3 assumes a 16.3% WACC and implies a target P/FFO multiple of 16.1x for 2016. Our rating of NEUTRAL is based on the company's valuation and the stock's expected return relative to country's benchmark over the next 12 months.

Risk: Factors that could impede achievement of our BRL 12.50 target price and change the rating of NEUTRAL for ALSC3 shares include: (1) Competition from new players driving yields downwards; (2) increase in the basic interest rate, (3) deterioration in consuption could lead to lower earnings given sector's leverage on the retail industry performance.

Target Price and Rating Valuation Methodology and Risks: (12 months) for BR Malls Participacoes (BRML3.SA)

Method: Our target price of R$14/share for BRML3 shares is based on a blended discounted cash flow to firm method (50% weight) using a 15.2%% WACC and a target NAV multiple (50% weight). At our R$14 TP, BR Malls would be trading at a P/FFO of 18x for 2016. Our rating of NEUTRAL is based on the company's valuation and the stock's expected return relative to country's benchmark over the next 12 months.

Risk: Risks to our R$14 target price and rating of NEUTRAL for BRML3 are (1) Competition from new players driving yields downwards; (2) increase in the basic interest rate; (3) deterioration in consumption could lead to lower earnings given the sector's leverage on the retail industry performance

Target Price and Rating Valuation Methodology and Risks: (12 months) for Iguatemi (IGTA3.SA)

Method: Our target price of R$24/share for IGTA3 shares is based on our blended discounted cash flow to firm method using a 14.2% WACC (50% weight) and a target NAV multiple (50% weight). At our TP of R$23/share , Iguatemi would be trading at a P/FFO (price/funds from operations) of 19x for 2016. Our rating of NEUTRAL is based on the company's valuation and the stock's expected return relative to country's benchmark over the next 12 months.

Risk: Factors that could impede achievement of our R$24 target price and change the rating of NEUTRAL for IGTA3 shares include: (1) competition from new players driving yields downwards; (2) increase in the basic interest rate; (3) deterioration in consumption could lead to lower earnings given the sector's leverage on the retail industry performance.

Target Price and Rating Valuation Methodology and Risks: (12 months) for Multiplan Empreendimentos. Imobiliarios S/A (MULT3.SA)

Method: Our target price of R$53.5/share for MULT3 shares is based on our blended discounted cash flow to firm (FCFF) using a 13.8% WACC (50% weight) and a target NAV multiple (50% weight). At our R$53.5/share TP, Multiplan would be trading at R$19.1x P/FFO (price/funds from operations) for 2016. Our rating of NEUTRAL is based on the company's valuation and the stock's expected return relative to country's benchmark over the next 12 months.

Risk: Factors that could impede achievement of our R$53.5 target price and change the rating of NEUTRAL for MULT3 shares include: (1) competition from new players driving yields downwards; (2) increase in the real interest rates of the economy and (3) Deterioration in consumption could lead to lower NOIs given the sector's leverage on the retail industry performance

Target Price and Rating Valuation Methodology and Risks: (12 months) for Sonae Sierra Brasil (SSBR3.SA)

Method: Our target price of R$14/share for SSBR3 shares is based on our blended discounted cash flow to firm method using a 14.9% WACC (50% weight) and a target NAV multiple (50% weight) . At our R$14 TP, Sonae Sierra would be trading at 16.9x P/FFO 2016. Our rating of UNDERPERFORM is based on the company's valuation and the stock's expected return relative to country's benchmark over the next 12 months.