Embed Size (px)

Citation preview

Contents

Acknowledgements

Preface

Executive Summary

Work Experience

Retail Processing Centre

Treasury Back Office

Finance Department

Financial Analysis

Acknowledgements

I personally feel grateful to be given the opportunity to complete a

two-week internship period at the ICICI Bank Ltd. Colombo Branch. It has

been an honor to work at multi-national bank with a network of 3100

branches and 10481 ATMs spread out globally. I would express my

gratitude to the Country Head, Mr. Biju Jacob who personally welcomed

me prior to my internship term and warmly accepted my request for a

placement as an intern at the bank. I am also deeply thankful to Ms.

Nadeeka Samaranayake, the country Operations Head for assisting me in

making arrangements with other workers at the bank and Ms. Dulamini

Jayawardhana, the HR Manager for introducing me to several other people

at the branch and guiding me on different issues that I faced during the

work. I would also like to pay my thanks to Ms. Kristina as she made me

familiar with procedures followed at the RPC and Mr. Sohan in the Trade

Department for explaining me the trade cycle steps that are the work norm

at the department. I feel indebted to Mr. Madhava Hettiarachi for

discussing with me the working fundamentals at the Treasury Back Office

at a full depth and fully answering my questions on the various doubts and

misconceptions that I had regarding the Treasury. I am also deeply grateful

to Mr. Chanaka at the Finance Department as he told me at a length about

the daily, weekly, monthly and yearly working practices that are conducted

at the department apart from detailing the various methods to analyze

financials of a given company.

Yours,

Osama Mahmood

(AS-Level)

Preface

Internship is an integral part of an educational life as a student gets the

valued opportunity to learn by practically applying his knowledge and skills

which has gained through the books and classrooms by years of study. As a

person experiences the working procedures of a particular organization it

turns up extra learning potential and prepares the mind for a clearer grasp

of concepts when further education/knowledge is sought in the relevant

field i.e. Banking.

With the working experience of two weeks at the ICICI Bank Ltd I feel

equipped with the confidence to pursue my education in commercial field

as skills that I gained at the bank would help me in bringing up brighter

ideas during my education at the University and enable me to quote

examples from the latest Banking practices. Moreover, the work experience

would be an advantage to the Bank that employs me in the future as it

would get an employee who is already well-acquainted with the basic

practices in various departments of a bank.

Executive Summary

The two-week work at the ICICI Sri Lanka has been particularly enriching

and educational. The report elaborates the working practices learnt at the

RPC, Treasury, Finance and Trade departments at the internship. It is

followed by a Financial analysis of the bank coupled with a few suggestions

from the point-of-view of an intern.

The work experience section would list out basics of the mentioned depts.

and the Financial Analysis section would discuss the Financial performance

of the Bank in the past few years at an International scope.

Work Experience

Retail Processing Centre

The RPC deals with Cash and cash transactions and importantly, clearing. Clearing denotes all activities from the time a commitment is made for a transaction until it is settled. Clearing of payments is necessary to turn the promise of payment (for example, in the form of a cheque or electronic payment request) into actual movement of money from one bank to another.

In trading, clearing is necessary because the speed of trades is much faster than the cycle time for completing the underlying transaction. It involves the management of post-trading, pre-settlement credit exposures to ensure that trades are settled in accordance with market rules, even if a buyer or seller should become insolvent prior to settlement. Processes included in clearing are reporting/monitoring, risk margining, netting of trades to single positions, tax handling, and failure handling.

Tuesday, 13 Aug 2013

Practically, clearing is one of the simplest and most logical processes in a bank done on a daily basis. The need arises when a customer turns up at the branch handing over a cheque of a different bank than ICICI. These cheques are collected by the Clearing department and the first step of the clearing process involves scanning these cheques through a scanner. Thereafter, only the softcopy of the cheque routes whereas the physical cheques rests in a fire-proof cabinet at the Clearing Department, as per regulations. A several number of cheque batches are made in a day following a maker-checker process where a person first passes entries into the system from the cheque image and the other confirms it by one-by-one matching each and every cheque entry.

A cut-off time is set at 11 00 am, which implies that any check processed after the time would be cleared on the following day. After all the check entries are recorded in the soft form a CD would be composed which would be then collected by an agent from LankaClear Ltd at around 3 00 pm.

The online interbank system used to settle the transactions is called SLIPS

of which ICICI is a participant. Sri Lanka Interbank Payment System

(SLIPS) is an online interbank electronic fund transfer system catering

mainly for low-value payments (up to Rs 5 million). Electronic Funds

Transfer (EFT) is a movement of funds from one account to another

without the corresponding piece of paper to authorize or prove that the

transfer had occurred. Thus, crediting and debiting of accounts are handled

more promptly and accurately without the need to write cheques, pay

orders or vouchers. Moving electronic records rather than paper results in

payments being processed much efficiently with advanced security features

and audit trails.

During the first I went through the SLIPS manual which laid out the

guidelines and regulations governing the settlement of transactions in the

banking system. The manual detailed solutions to various problems and

risks that might arise during the clearing function and designated

responsibilities to various working units such as the participant bank,

clearing house, clearing agent and the bank representative to SLIPS.

Wednesday, 14 Aug 2013

During the second day at the RPC I was handed a manual “Global

Remittances Manual”. As ICICI is India’s largest private bank it serves the

needs of Indians throughout the world at their doorstep. Reputedly, India

receives more remittances every year than any other country in the world.

Therefore remittance sending to India is one of the most feasible products

in the bank’s portfolio. The programme used to transfer funds to India is

schemed as “Money2India”. The product facilitates quickest transfer of

funds to India and is widely popular among the Indian customers of the

bank who send money to their country on monthly basis.

The manual lists out guidelines governing the transfer of funds to India,

eligibility of the remitter maximum limits and other regulations by the

Central Bank such as retaining at least 10% of the income in Sri Lanka.

The core banking system in use at the ICICI is Finacle. Finacle is a core

banking software package developed by Infosys, designed to address retail

banking, wealth management, CRM, Islamic banking and treasury

requirements of retail, corporate and universal banks. Finacle is used in 168

banks across 81 countries.

Data received by the bank from the LankaClear Ltd is verified, sought for

any discrepancies such as wrong name/account number and then entered

into the personal accounts via Finacle. At the day end a summary of the

financial transactions at the RPC are to be compiled and reported to the

Treasury.

Treasury Back Office

The treasury department of a bank is responsible for balancing and

managing the daily cash flow and liquidity of funds within the bank. The

department also handles the bank's investments in securities, foreign

exchange, asset/liability management and cash instruments.

Thursday & Friday, 15 & 16 Aug 2013

The Treasury Back Office is specifically required to support the Front Office

which is hitting live deals in the open money markets. Middle office serves

as an intermediary between the Front and the Back Office. However, in the

case of ICICI the Middle Office (TMOG) is located in India connected

through the online banking systems with the Back Office. This confronts

the department with several challenges as work is slowed down due

collaboration issues. Nonetheless, overseas location might have its own

cost-saving and economies of scale advantages.

The treasury department is basically concerned with earning a surplus over

the bank’s funds so that a return is made after the interest deductions to the

customers and savers. It is therefore often termed that a job in treasury is

the most stress-full and challenging, nevertheless, the most rewarding job

in the bank.

Some tasks needed to be done on a daily basis in the department include

reconciling the day-end treasury balance with the data received from the

TMOG. This reconciliation is to be done before 4 30 pm which is the closing

time for the system and therefore if any differences in the balances are

found they have to be quickly probed in settled. With this, as clear, a

permanent record of entries into the Finacle is to be duly maintained using

the information received from other departments such as RPC, Finance and

Trade on a daily basis.

As per the CBSL revised regulations, a new system of Statutory Reserve

Ratio has been enforced by 1 May 2013. The previous system requires banks

to have a cash equivalent reserve with the central bank of 6% of the total

liabilities, updated on a weekly basis. Under the new system the updating

would be done on a bi-monthly basis. SRR calculated during the first half of

a month (1st to 15th date) will be applicable to the first half of the following

month while the SRR calculated for the second half (16th to last date) would

apply to the second half of the following month. Hence the maintenance of

the ratio would done on a daily basis by tracking the liquidity level at the

end of each day while the updating has to carried out before 22nd of month

for the first half while 7th of the next month for the second half ( As per

CBSL requirements).

During my work at the Treasury I was recommended a manual on the

Currency dealings in the exchange market. The manual interestingly laid

out the way deals are done at the live market. It also instructed the ethics

and morals to be kept in mind while making the deals explained certain

tricks to get better deals. For example, in the market dealings it is never to

be specified whether the Asker’s intention is to buy or sell the currency.

Therefore the question raised in the Reuters’s system would be “Spot

USD/LKR please?”. Hence the Quoter would quote two different rates such

as “43/53”. It may seem confusing but things have been made simple. It is

the common market knowledge that the on-going USD/LKR rate is 131.2,

hence the quote means that quoter is willing to buy USD at LKR 131.243

and will sell it at LKR 131.253. The difference between the two quotes is

generally called the “spread” which serves as a profit margin for the quoter.

Deals done on the exchange market generally have their own jargon. There

different derivatives such as call, put etc. and time duration of currency

dealings classified as Tom (tomorrow), Spot (Day after tomorrow) and

TomSpot (Day after Spot). Hence the correct use of the market language is

to be made in order to deal effectively with the participants.

A major drawback faced by the Treasury Office at ICICI is that deals with

many banks are not permitted moreover, there a few banks upon which all

the Treasury dealings are concentrated. This lemmatizes the profiteering

scope of the Treasury and therefore exposes the bank to liquidity risks.

Each day a major portion of the bank’s Treasury funds is loaned out to the

CBS as a Reverse Repo upon which only a 7% interest is payable as per the

CBS rules and regulations. If dealings with other banks are allowed, then a

higher mark-up would be earned on the call-money lending.

The Bank’s DBU and FCBU, both act as uniquely disjoint units. Hence if

FCBU/DBU is under the minimum limit at the closing of a particular date

then the coverage will have to be borrowed from DBU/FCBU at an interest

charged.

Finance Department

The Finance Department (FIN) is responsible for the mobilization and

administration of the Bank's financial resources, both the assets and

liabilities, and for the management of the Bank's liquidity, accounting and

financial records, and the relations with financial markets and

intermediaries. FIN is divided in the Treasury Division and Accounting

Division. Hence it is often termed as the ‘heart’ of a bank since cash-flow is

deemed as blood-flow for a bank.

Tuesday, 20 Aug 2013

On the very first day I was familiarized with the Detailed Balance Sheet,

Profit and Loss Account and the Cash-flow Statement of the Bank. A task

was delegated to me which required me to segregate account holders on the

basis of the currency denominated in their accounts. It is necessary to have

a separate record for each and every currency account and then tally the

total with the reserves which are listed in the Detailed Balance Sheet since

such pieces of information are often sought by the internal and the external

auditors for scrutinizing. Major denominations of currency in the ICICI are

LKR, USD, EUR and GPB.

I also got the opportunity to read the 2012-13 annual report of the bank.

Detailed financial derivations are elaborated under the “Financial Analysis”

section.

Wednesday, 21 Aug 2013

Finance is not mere a game of numbers but it also requires constant

improvement through regular review and comparison. A Variance Analysis

of Expenses is done where expenses of one time period such a month are

compared to that of the previous month and reasons underlying and

considerable variations are reported, both, favorable and non-favorable.

The latter are done clearly to prevent any mistakes, that are made. in the

future while the former is done to seek the reasons behind the

improvements and give them extra focus to exploit them.

The task was practically done on an excel sheet by calculating variance

percentage of all the expenses over the June and the July month. Any

considerable change in the amount of the expense such as > 10% requires

probing by entering the account number in the General Ledger through the

Finacle and seeking out details underlying the variations and reporting

them in short words. Hence, this facilitates better financial analysis as

many reasons backing the variations in financial figures are unveiled and

explained.

A weekly task at the Finance department is to send a weekly report to the

CBS that details out the Minimum and Maximum rates offered by the bank

to any organization during the week. Hence the data of all the corporate

and personal customers of the bank is obtained, organized, strictly verified

and then properly sorted to get the maximum and minimum rates charged

by the bank. The verification process is done through one-by-one ticking

out of customers and their respective rates based on information provided

by other departments and previous week’s report. This also follows a

maker-checker system as the report produced will be then verified by the

Head of Finance and authorized by the Treasury Front Office before final

uploading to the CBS.

Another interesting book handed over was the “Earnest & Young Good

Bank” which specifies the qualities and tips over producing coherent and

appealing banking financial reports.

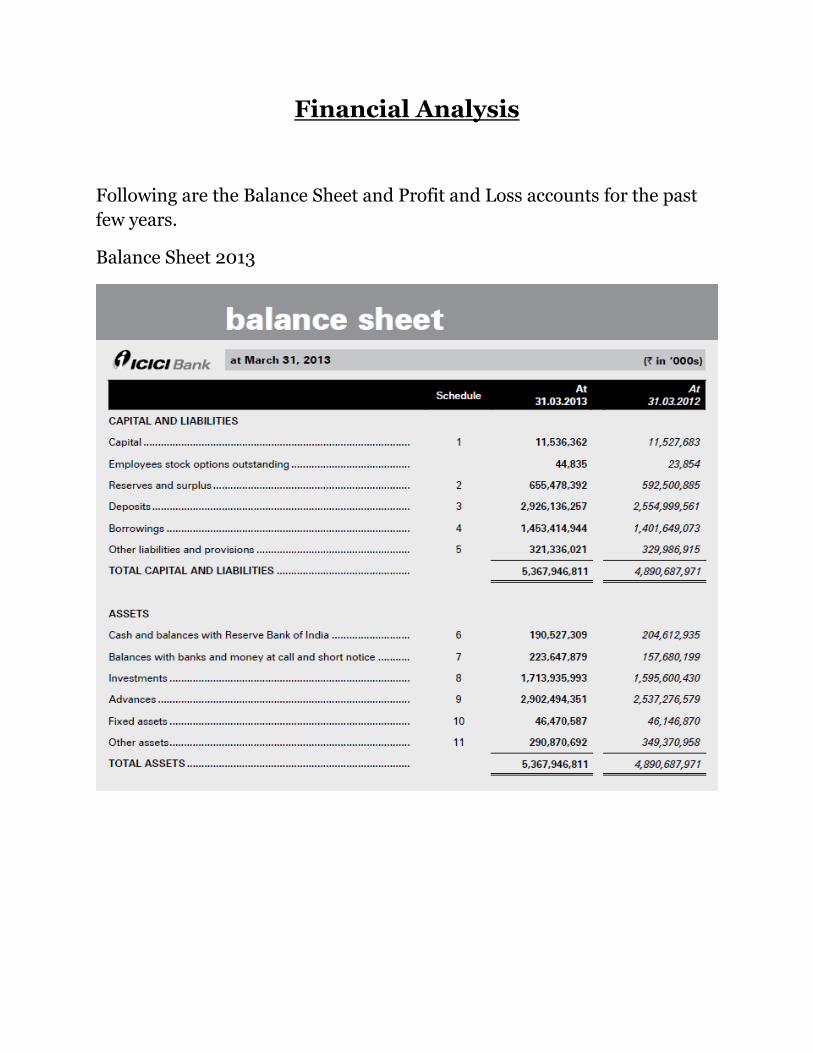

Financial Analysis

Following are the Balance Sheet and Profit and Loss accounts for the past

few years.

Balance Sheet 2013

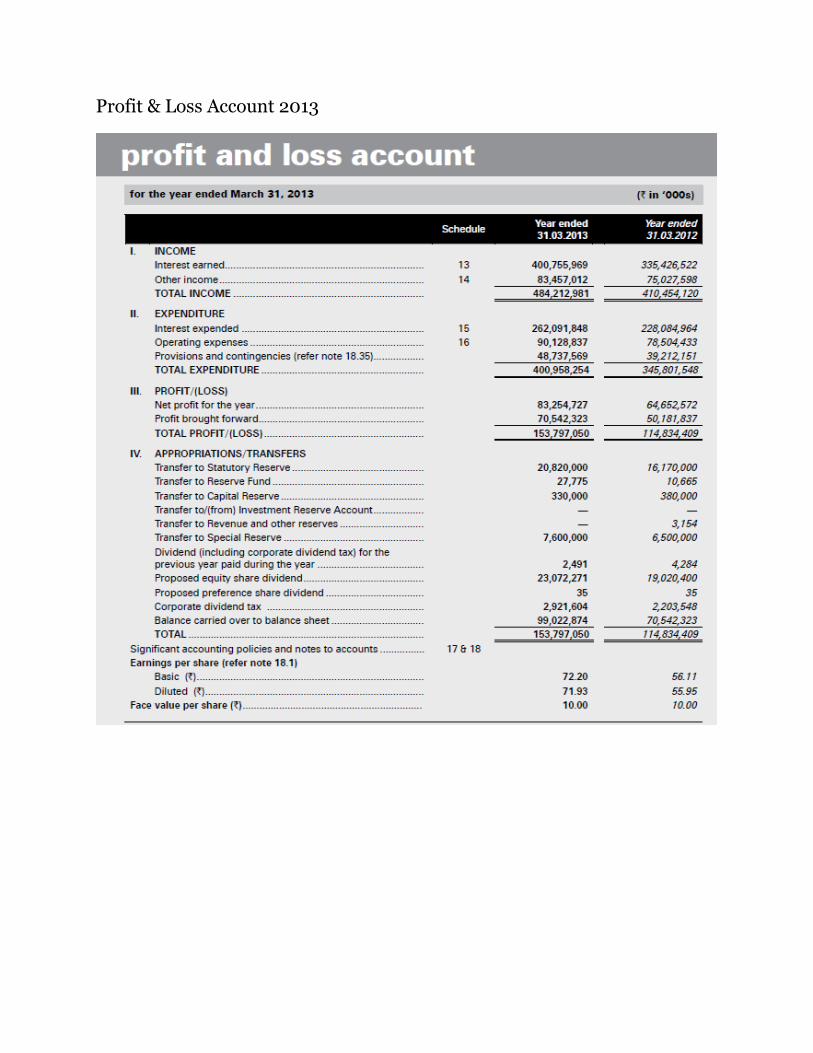

Profit & Loss Account 2013

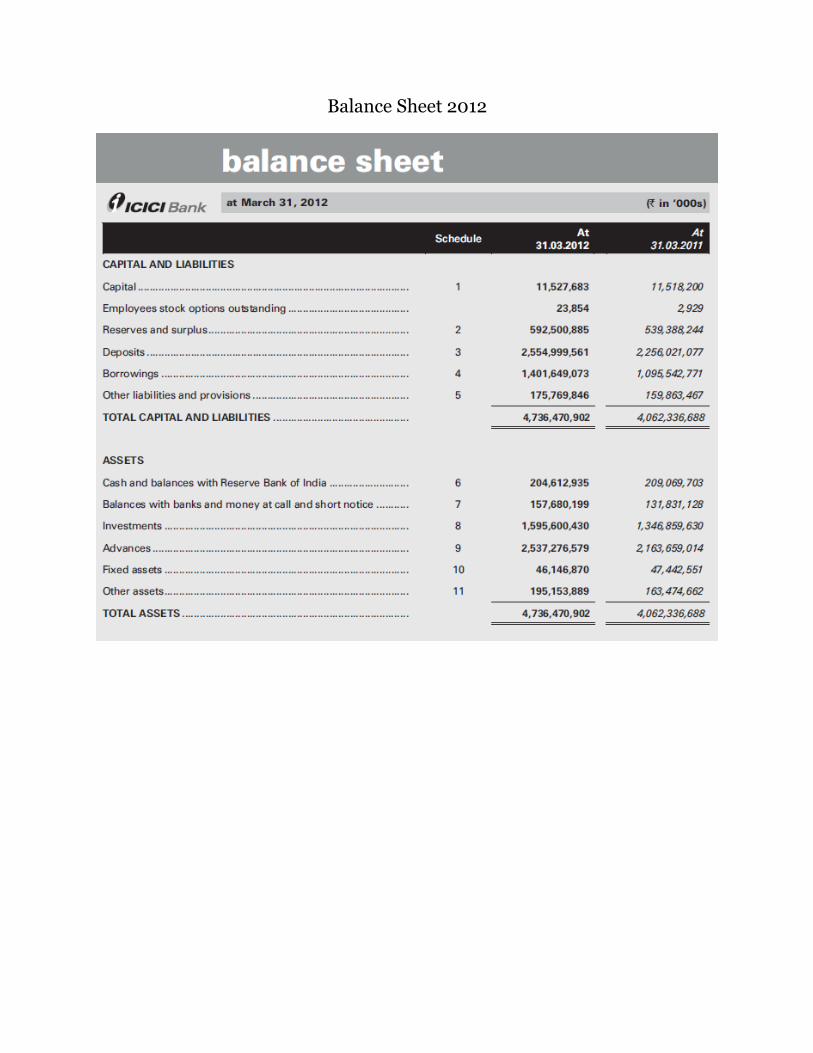

Balance Sheet 2012

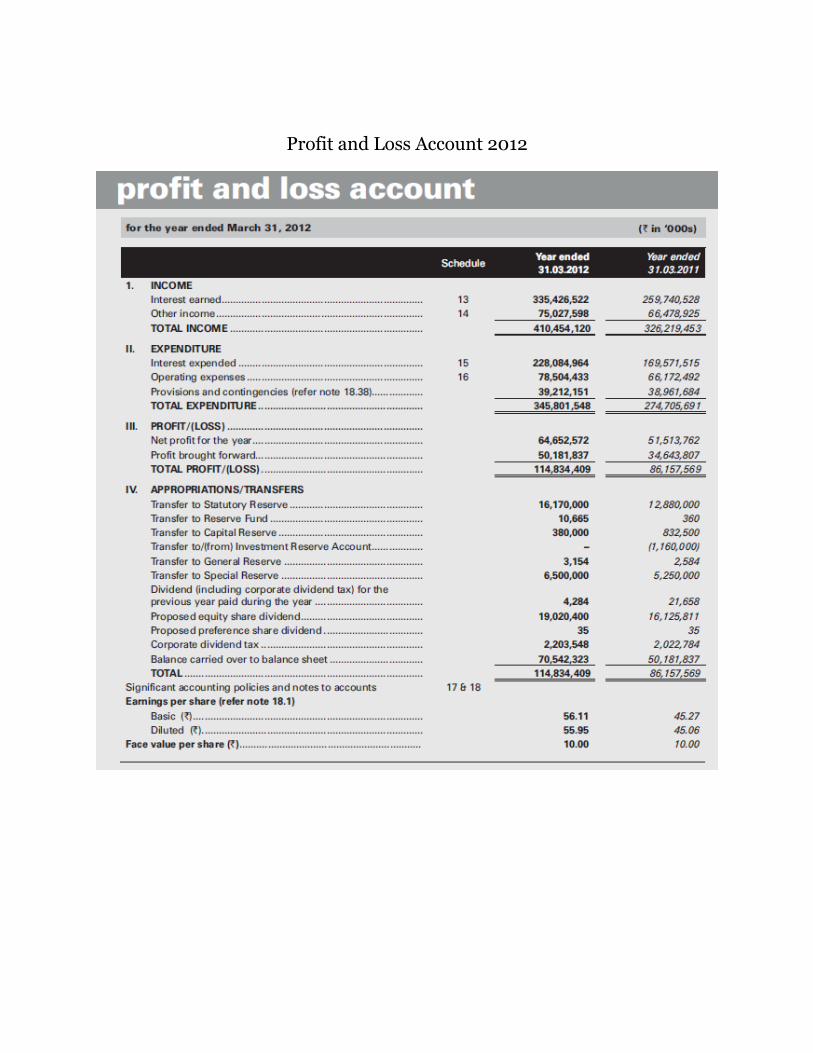

Profit and Loss Account 2012

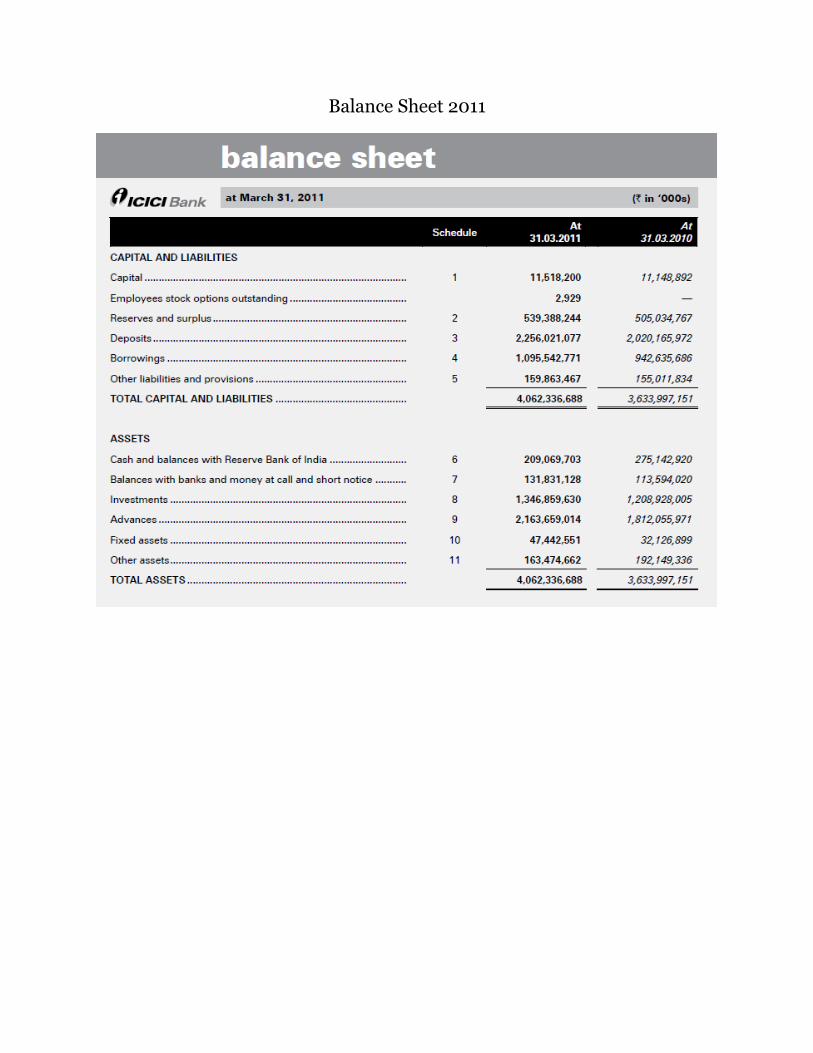

Balance Sheet 2011

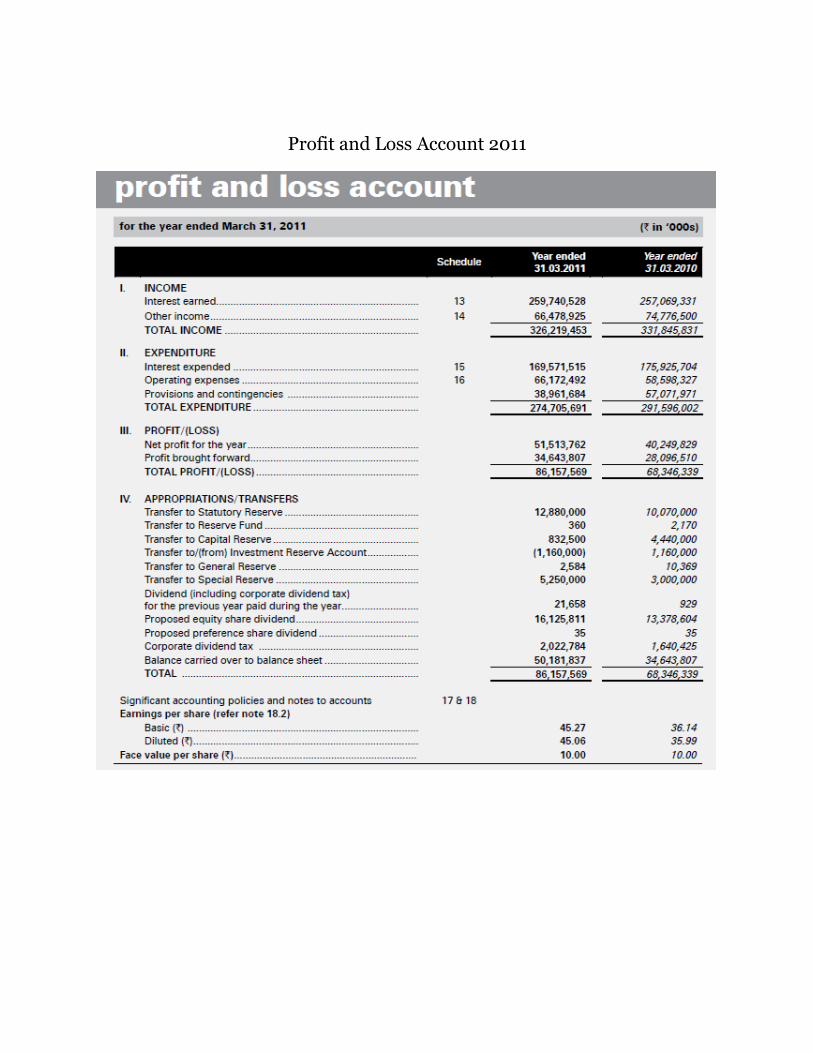

Profit and Loss Account 2011

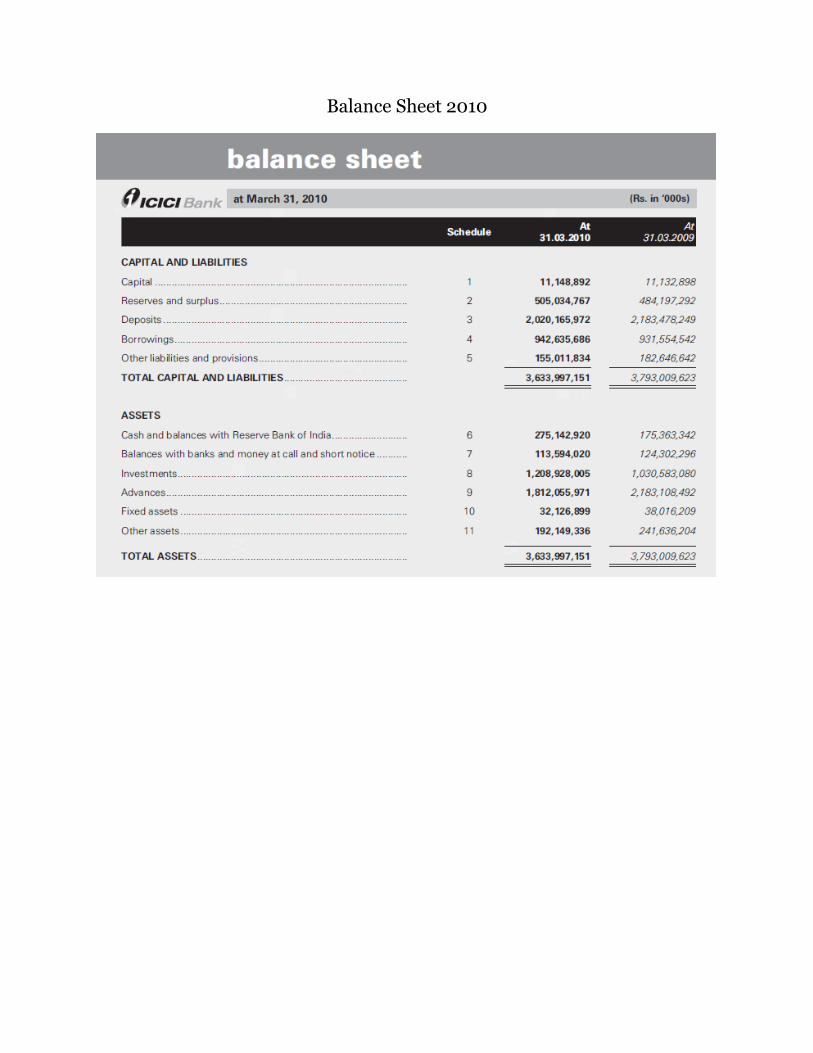

Balance Sheet 2010

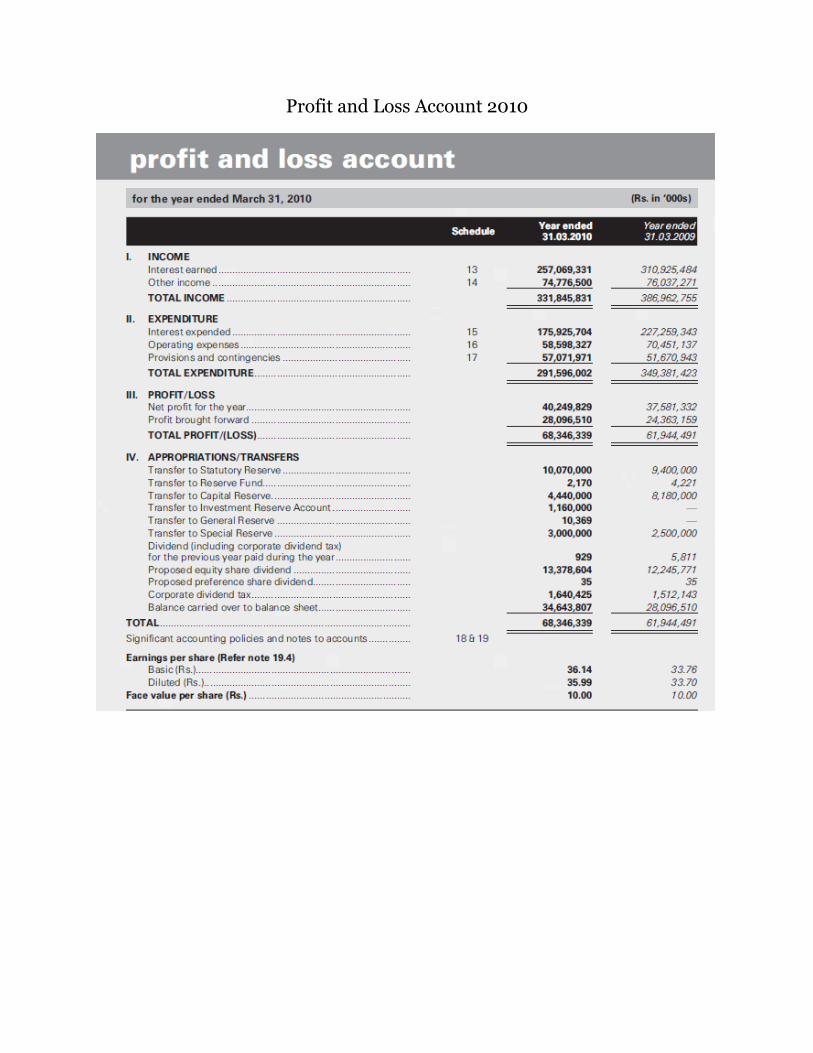

Profit and Loss Account 2010

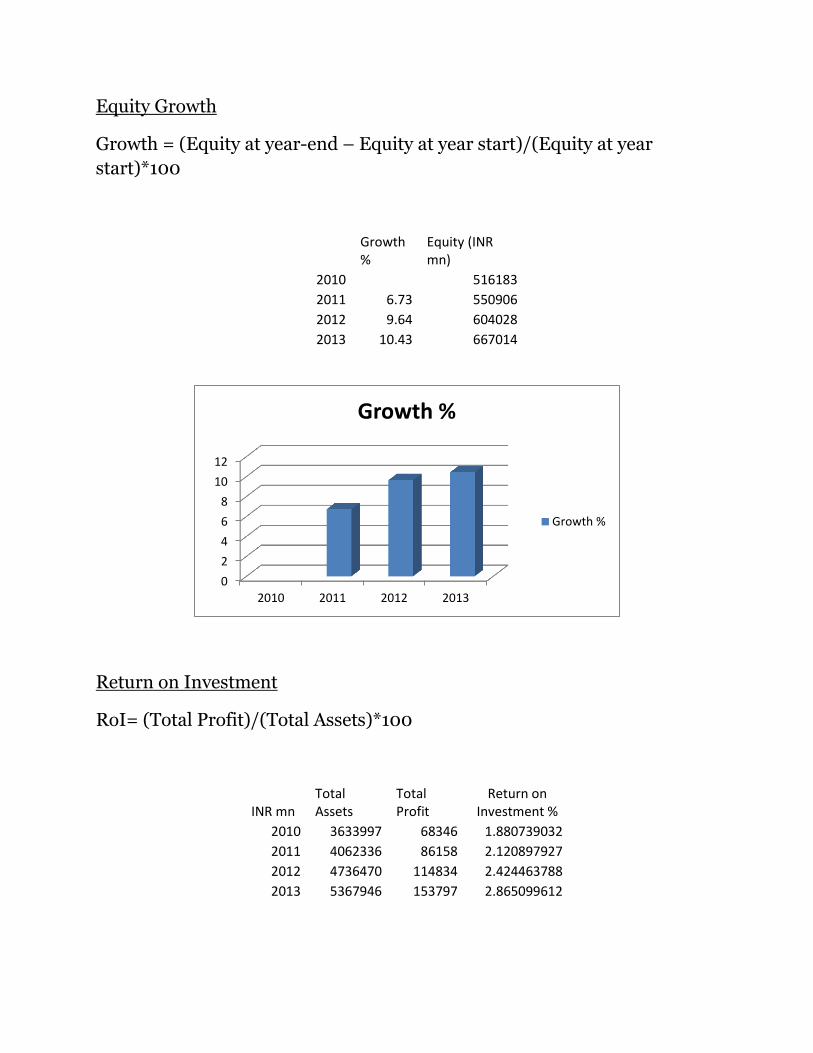

Equity Growth

Growth = (Equity at year-end – Equity at year start)/(Equity at year

start)*100

Growth %

Equity (INR mn)

2010

516183

2011 6.73 550906

2012 9.64 604028

2013 10.43 667014

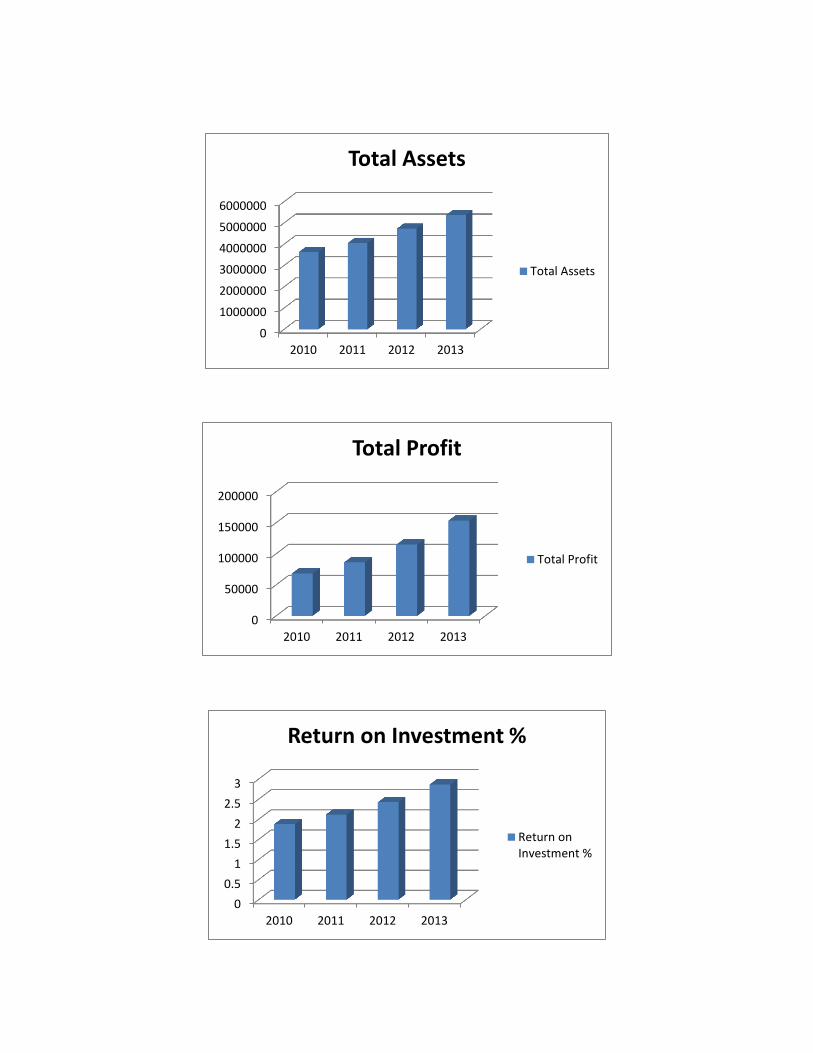

Return on Investment

RoI= (Total Profit)/(Total Assets)*100

INR mn Total Assets

Total Profit

Return on Investment %

2010 3633997 68346 1.880739032

2011 4062336 86158 2.120897927

2012 4736470 114834 2.424463788

2013 5367946 153797 2.865099612

0

2

4

6

8

10

12

2010 2011 2012 2013

Growth %

Growth %

0

1000000

2000000

3000000

4000000

5000000

6000000

2010 2011 2012 2013

Total Assets

Total Assets

0

50000

100000

150000

200000

2010 2011 2012 2013

Total Profit

Total Profit

0

0.5

1

1.5

2

2.5

3

2010 2011 2012 2013

Return on Investment %

Return onInvestment %

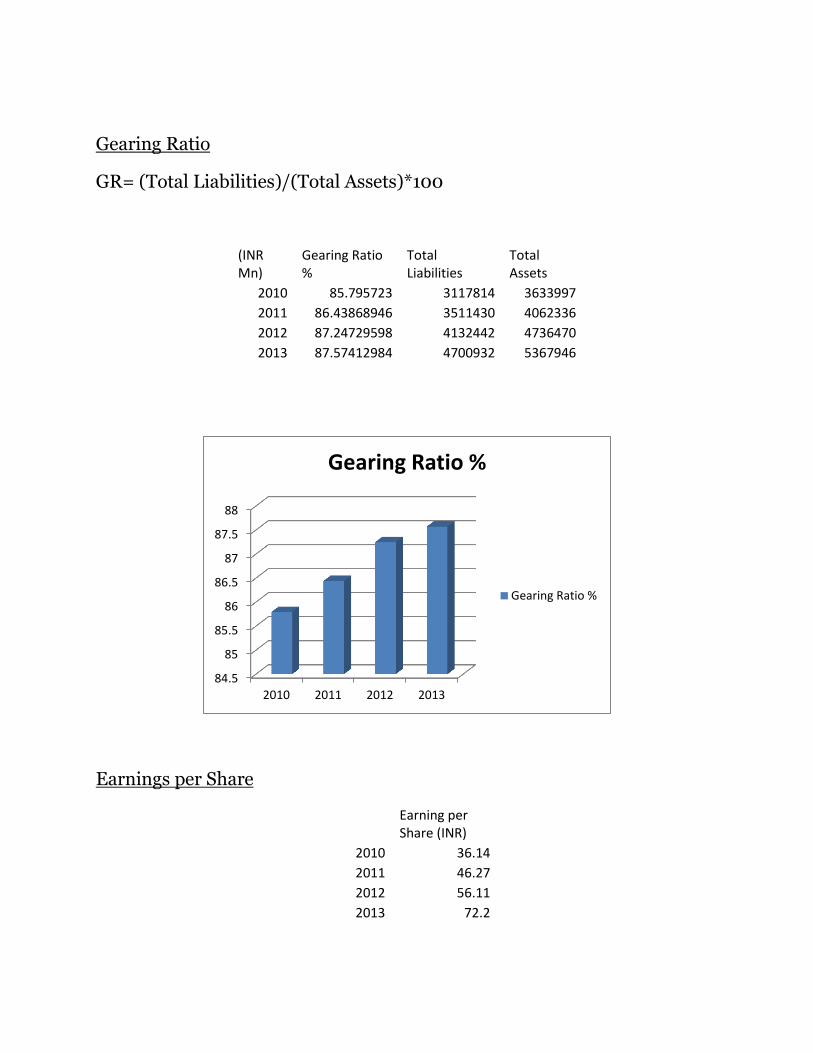

Gearing Ratio

GR= (Total Liabilities)/(Total Assets)*100

(INR Mn)

Gearing Ratio %

Total Liabilities

Total Assets

2010 85.795723 3117814 3633997

2011 86.43868946 3511430 4062336

2012 87.24729598 4132442 4736470

2013 87.57412984 4700932 5367946

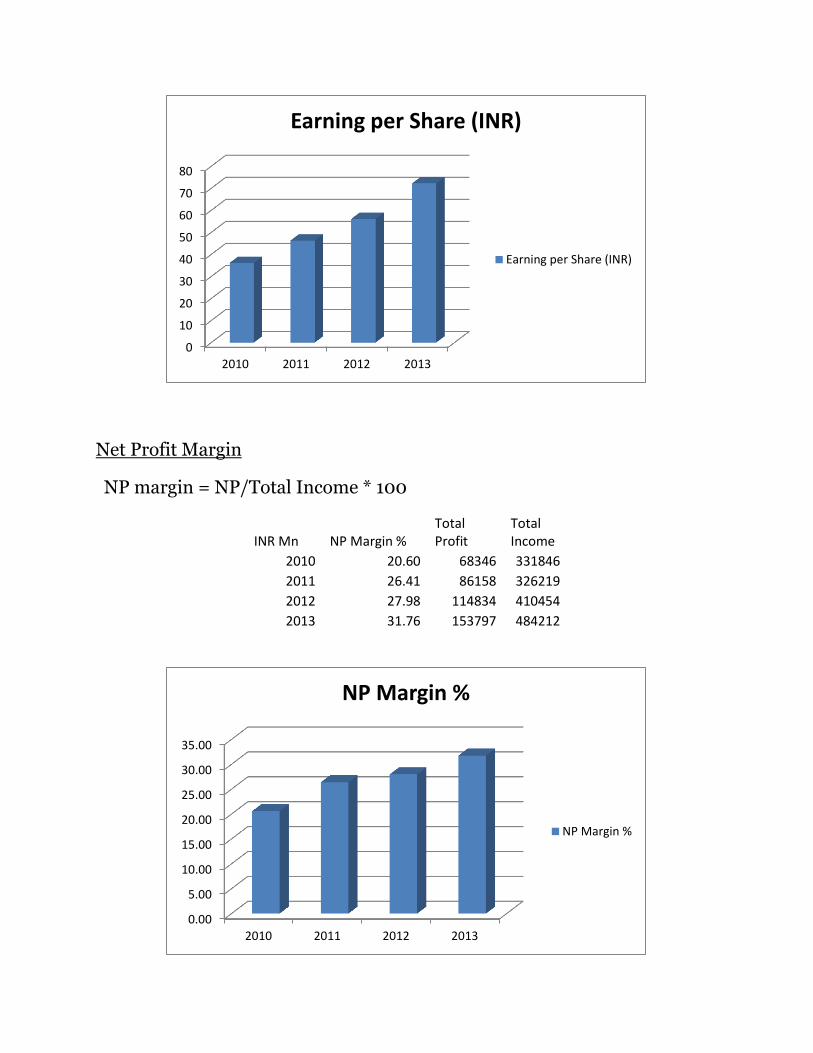

Earnings per Share

Earning per Share (INR)

2010 36.14

2011 46.27

2012 56.11

2013 72.2

84.5

85

85.5

86

86.5

87

87.5

88

2010 2011 2012 2013

Gearing Ratio %

Gearing Ratio %

Net Profit Margin

NP margin = NP/Total Income * 100

INR Mn NP Margin % Total Profit

Total Income

2010 20.60 68346 331846

2011 26.41 86158 326219

2012 27.98 114834 410454

2013 31.76 153797 484212

0

10

20

30

40

50

60

70

80

2010 2011 2012 2013

Earning per Share (INR)

Earning per Share (INR)

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

2010 2011 2012 2013

NP Margin %

NP Margin %

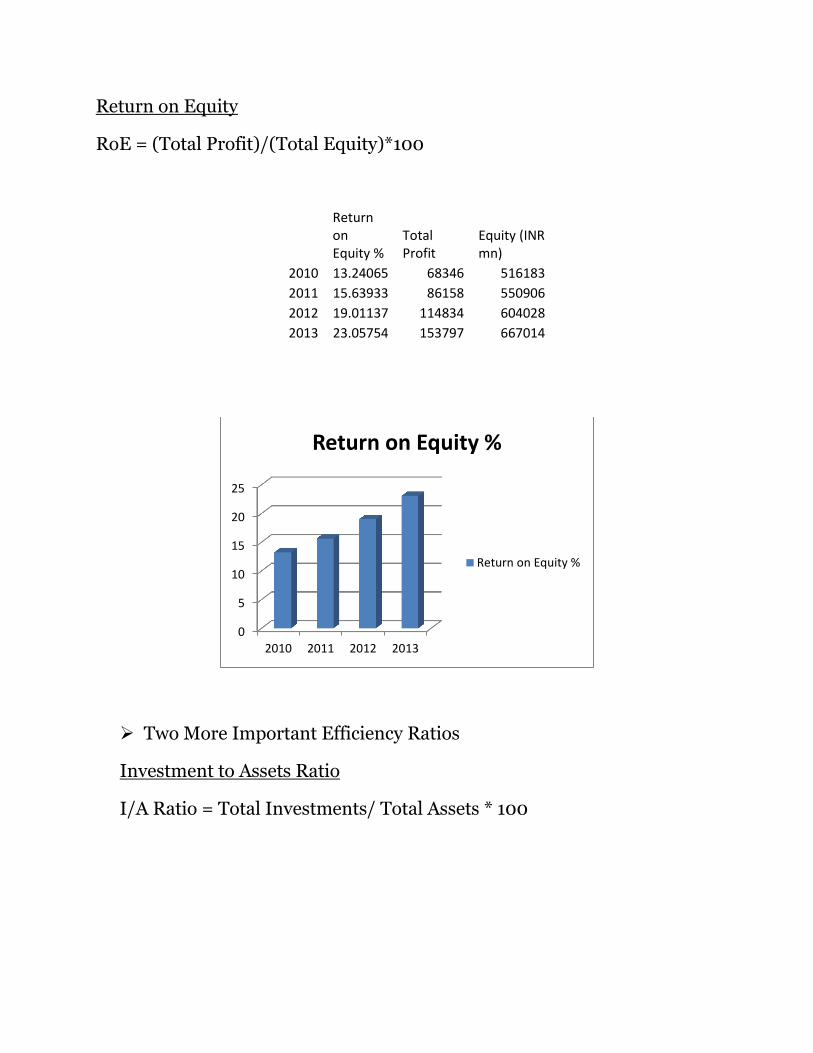

Return on Equity

RoE = (Total Profit)/(Total Equity)*100

Return on Equity %

Total Profit

Equity (INR mn)

2010 13.24065 68346 516183

2011 15.63933 86158 550906

2012 19.01137 114834 604028

2013 23.05754 153797 667014

Two More Important Efficiency Ratios

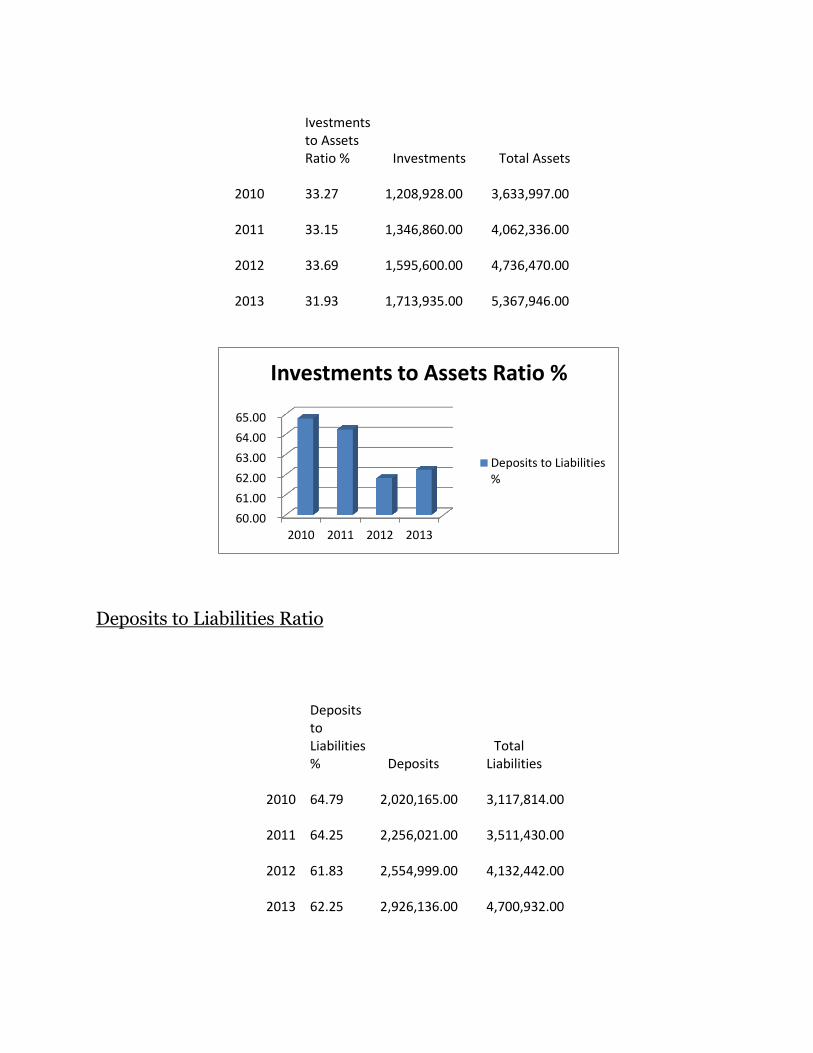

Investment to Assets Ratio

I/A Ratio = Total Investments/ Total Assets * 100

0

5

10

15

20

25

2010 2011 2012 2013

Return on Equity %

Return on Equity %

Ivestments to Assets Ratio % Investments Total Assets

2010

33.27

1,208,928.00

3,633,997.00

2011

33.15

1,346,860.00

4,062,336.00

2012

33.69

1,595,600.00

4,736,470.00

2013

31.93

1,713,935.00

5,367,946.00

Deposits to Liabilities Ratio

Deposits to Liabilities % Deposits

Total Liabilities

2010 64.79

2,020,165.00

3,117,814.00

2011 64.25

2,256,021.00

3,511,430.00

2012 61.83

2,554,999.00

4,132,442.00

2013 62.25

2,926,136.00

4,700,932.00

60.00

61.00

62.00

63.00

64.00

65.00

2010 2011 2012 2013

Investments to Assets Ratio %

Deposits to Liabilities%

@@@@@@@@@@

60.00

60.50

61.00

61.50

62.00

62.50

63.00

63.50

64.00

64.50

65.00

2010 2011 2012 2013

Deposits to Liabilities %

Deposits to Liabilities %