Embed Size (px)

Citation preview

Foreign Entry Mode and Performance: The Moderating Effects of Environment

Howard S. Rasheed

University of South Florida

Second Revise and resubmit for: Journal of Small Business Management

Key words: Internationalization, foreign entry mode, environment, risk, and moderation. Topic: Internationalization, exporting, and small enterprises Author’s Note Howard S. Rasheed is an Assistant Professor of Management at the University of South Florida, College of Business Administration in Tampa Florida. His research interests include strategic and entrepreneurial management and electronic commerce. Address all correspondance to: Howard S. Rasheed, Ph.D., The University of South Florida College of Business, 4202 E. Fowler Ave. BSN3403, Tampa, FL, 33620; Tel: (813) 974-1727; Fax: (813) 974-1734; [email protected] Acknowledgements: The author would like to thank Drs. Gayle Baugh, Darla Domke-Damonte, Franz Lohrke, Winnifred Scott, and Craig Waring for their assistance.

1

Abstract

As the trend toward economic globalization increases, the internationalization of small and

medium sized enterprises (SMEs) has become an important topic. Research on the performance

outcomes of foreign market entry strategies has been primarily considered from the perspective

of the multinational corporations. In this paper hierarchical regression analyses were conducted

on archival data of 123 publicly held manufacturing SMEs based in the United States to test a

contingency model that hypothesizes more of the performance variance is explained when the

foreign market entry mode is strategically aligned with domestic and foreign environmental

factors. The results indicate that firms will have a higher rate of international revenue growth

using non-equity based (exporting) foreign market entry modes in growing domestic

environments. International revenue growth is higher for equity-based modes when foreign

market risks are high. The findings should provide managers of SMEs with contextual evidence

for making successful foreign market entry decisions.

2

Foreign Entry Mode and Performance: Moderating Effects of Environmental Factors

Growth through foreign market expansion has become an increasingly popular strategy,

as previously closed foreign markets open, and economies around the world globalize. Spurred

by technological advances in transportation and communications, smaller firms are now finding

it easier to expand internationally (Oviatt & McDougall, 1994). Research on international

expansion and foreign market entry is well established within the international market

diversification literature, but has primarily focused on multinational corporations (Stopford &

Wells, 1972; Daniels, Pitts, & Tretter, 1984; Galbraith & Kazanjian, 1986; Ghosal 1987; Kim,

Hwang, & Burgers, 1989; Habib & Victor; 1991). The internationalization trend for small and

medium-sized enterprises (SME) has prompted increased research interest in explaining the

factors that contribute to success, but sufficient theoretical framework is lacking (Lu & Beamish,

2001).

Many strategists have used contingency theory to explain how an organization maximizes

its alignment of strategy with its environment to achieve performance outcomes within a

domestic strategy context (Burns & Stalker, 1961; Christensen & Montgomery, 1981; Galbraith

& Kazanjian, 1986; Keats & Hitt, 1988; McArthur & Nystom, 1991; Goll & Rasheed, 1997;

Simerly & Li, 2000). The issue of strategic fit in an international context takes on additional

complexities due to the problems of control and coordination, confounded by the actions of

foreign market agents and the policies of foreign governments, particularly for SMEs (Lu &

Beamish, 2001). The theoretical precepts for a contingency model for SME international

expansion must therefore consider the unique issues associated with resource commitment, as

well as the relevant external factors associated with foreign markets.

One key stream of research has investigated the role that environmental factors play in an

3

SME’s international success. Research suggests that environmental factors in an SME’s home

market as well as obstacles or opportunities in their overseas market can affect its international

expansion (Madsen, 1988; Gripsrud, 1990). Most prior studies examining the effects of the

environment on SME foreign market entry have focused on exporting which does not require

foreign investment of assets (for example, Axinn, Savitt, Sinkula, and Thad, 1994). Others have

investigated how SMEs are increasingly using overseas joint ventures and wholly owned

subsidiaries that require higher commitments of resources than exporting, while reducing entry

and exit flexibility for the firm (Oviatt & McDougall, 1994; Baird, Lyles, and Orris, 1994).

Based on extant international market diversification theory and contingency theory, this

paper examines how performance outcomes vary between equity and non-equity entry modes

depending on the effects of domestic and foreign environmental factors. A review of the

literature will first establish a basis for hypothesis development. Second, the contingency model

will be tested and the results presented. Finally a discussion of the findings will provide

suggestions to managers for selecting the appropriate foreign entry mode, given their contextual

environments, as well as implications for future research.

Literature Review and Conceptual Framework

Foreign Market Entry Mode

Implementation of international market diversification strategy involves the development

of a comprehensive product/market plan that includes choosing a foreign market entry mode

(Root, 1987). Foreign market entry mode, is defined as institutional arrangements that allow

firms to use their product or service in a country exchange (Calof, 1993) or “an institutional

arrangement that makes possible the entry of a company’s products, technology, human skills,

management, or other resources into a foreign country” (Root, 1987; 5). In international market

diversification, institutional arrangements with firms of different national origin involve complex

4

factors such as host country risk and host government policy, which complicate the structural,

transactional, and resource dynamics of transnational activities (Ghosal, 1987).

Firms entering new foreign markets choose from a variety of different forms of entry,

ranging from licensing and franchising, through exporting (directly or through independent

channels), to foreign direct investment (joint ventures, acquisitions, mergers, and wholly owned

new ventures). Entry modes vary in the degree of control the firm has over invested tangible and

intangible resources, and the transactions costs associated with that resource commitment

(Anderson & Gatignon, 1986; Domke-Damonte, 2000). From another perspective, entry

involves two interdependent decisions—location and mode of control. Exporting is domestically

located and administratively controlled, foreign licensing is foreign located and contractually

controlled, and FDI is foreign located and administratively controlled. Transaction costs theory

views each choice of entry mode as an individual transaction that involves a tradeoff between

control and resource commitment (Anderson & Gatignon, 1986).

In terms of the performance implications of internationalization, evidence supports the

idea that foreign market entry, regardless of mode, significantly increases returns on sales and

assets (Daniels & Bracker, 1989). Other research has compared relative financial performance

between, and within modes. For example, Tang and Yu’s (1990) revenue maximization model

concluded that a wholly owned subsidiary is the optimal strategy because it generates the highest

level of economic profit and maximizes control of critical knowledge indefinitely. This

conclusion was based on a mathematical model that determined transfer prices in other entry

strategies are higher than marginal costs, making subsequent operations inefficient. Woodcock,

Beamish, & Makino (1994) found that new venture direct investment outperforms the joint

5

venture mode, which in turn, outperforms direct investments through acquisition. Their research

did not, however, investigate the variables that contribute to this performance variance.

Mosakowski (1988) provided evidence that, for service firms, joint ventures perform better than

internal arrangements and licensing; research and development (R&D) joint ventures perform

worse; sales joint ventures’ performance falls between the two; and licensing detracts from

performance when compared to using internal arrangements. This study did not adjust for

foreign risk, however.

Lu and Beamish (2001) argued that while both equity and non-equity based modes of

entry have the potential for increasing financial performance, exporting had a negative effect on

financial performance. Conversely, foreign direct investment had a curvilinear effect on

financial performance, such that firm performance declines with initial FDI activity and

improves with greater FDI activity. The authors suggested that the results were possibly a partial

reflection of the increase in the exchange rate of the yen during the period of the study, but did

not otherwise consider foreign risk. Lu and Beamish concluded that FDI is a more competitive

way than exporting for operating in international markets because the value of FDI was greater at

later stages.

The previously mentioned studies reflect the prevailing interest of performance at the

corporate financial level. Internationalization is a business level strategy and, as such, market

performance measures are an appropriate, but often overlooked, level of analysis (Bloodgood,

Sapienza and Almeida, 1996). To extend the literature on productivity based performance

models, this paper examines international performance from the perspective of revenue growth.

Domestic Environmental Factors

The moderating effects of environmental factors have been often used in performance

models relative to domestic strategies (Dess & Beard, 1984; Keats and Hitt, 1988; McArthur &

6

Nystrom, 1991; Goll & Rasheed, 1997; Pelham, 1999; Simerly & Li, 2000). In the context of

foreign market entry, Hill, Hwang, and Kim (1990) suggested that the choices for entry mode are

a tradeoff between preferences for control and resource commitments, based on environmental

variables. Although Luo (1999) found support for the moderating effects of environment on the

strategy-performance relationship for small businesses in China, the application of this

contingent performance model to foreign market entry is not well established.

In strategic management research, three types of domestic environmental factors have

been primary discussed—munificence (dynamism), volatility (turbulence), and complexity.

Environmental munificence is defined as the relative abundance of resources in the environment

and the capacity to support growth (Dess & Beard, 1984). Volatility is defined as the level of

turbulence or instability facing an environment and reflects change that is difficult to predict

(Keats & Hitt, 1988). Environmental complexity is defined as the heterogeneity and

concentration of environmental elements (Dess & Beard, 1984). Prior international studies have

primarily examined domestic munificence and volatility as contributing factors to success

(Kuzmicki & Kramer, 1994; Chen & Martin, 2001).

Keats and Hitt (1988) concluded that, generally, a munificent domestic environment can

present opportunities for expansion and enable a firm to generate slack resources in support of

growth. Kuzmicki and Kramer’s (1994) evidence that domestic industry munificence influences

the selection of foreign entry non-equity modes indicates that the effects of domestic industry

munificence on a firm’s rate of internationalization, depends on whether the entry mode requires

a commitment of equity resources. However, Chen & Martin (2001) argued that positive trends

in the domestic expansion of products, negatively affect foreign expansion. Since

internationalization involves inherent political and operational risk, firms in munificent

environments may be reluctant to take unnecessary equity risks associated with foreign market

entry if sufficient opportunities exist in the domestic markets (Chen & Martin, 2001). Therefore

the following hypothesis is offered:

7

Hypothesis 1: When domestic munificence is high, firms using non-equity modes will have higher rates of international revenue growth.

Research has linked volatility or turbulence as a moderator of the strategy-performance

relationship in domestic environments for large and small firms (Miles, Covin, & Heeley, 2000).

Although Contractor and Lorange (1988) proposed that volatile host markets increase the

likelihood of choosing a low resource mode, empirical research is limited on environmental

volatility as a moderator in an international context. Kim and Hwang (1992) suggested their lack

of findings regarding the effects of demand uncertainty on a firm’s foreign entry mode strategy

could be attributed to the mediating effects of resources. Since the mode of foreign entry is

partly based on the degree of resource commitment and control, the following is proposed: Hypothesis 2: When domestic volatility is high, firms using non-equity modes will have higher rates of international revenue growth.

Foreign Environmental Factors

The contingency model for determinants of foreign market entry performance includes

the risk effects of doing business in a foreign target market. Foreign transactional risks are

viewed in terms of the host country’s political and economic stability and the host country’s

policies and regulations related to transnational business activities. Risk factors related to

foreign transactions include general stability risk, ownership/control risk, operating risk, and

transfer risk. General stability risk refers to management’s uncertainty about the future viability

of the host country’s political system (Root, 1987). Ownership/control risk is defined as

management’s uncertainty about host government actions affecting the entrant’s ownership

position. Operations risk refers to the possibility of sanctions that could constrain an investor’s

operations in the host country. Transfer risk is defined as limitations on the entrant’s ability to

transfer capital out of the host country (Root, 1987). Agarwal and Ramaswami (1992)

considered the effects of foreign transaction risk from the perspective of investment and

8

contractual risk. Investment and contractual risk reflects the uncertainty over the continuation of

present economic and political conditions and government policies, which are critical to the

survival and profitability of a firm’s operations in that country.

The research relating risk and entry mode choice has varied. According to Agarwal &

Ramaswami (1992) host countries with greater probability of restrictive policies impede foreign

investment and encourage non-equity modes. On the other hand, firms with a proprietary

product or technology have a greater amount of leverage in countries characterized by high

investment risk and consequently may choose higher control modes. Contractor and Lorange

(1988) maintained that one of the strategic rationales for forming cooperative relationships over

wholly owned ventures was risk reduction. In their analysis of a variety of industries, they found

that the dominant consideration appears to be an accumulation of resources for the large

investment and the distribution of risk among partners. Cooperative ventures have the

advantage of lower capital investment risk, lower risk of return due to faster entry, and lower

political risk. Fatehi-Sedeh and Safizadeh (1988) proposed that certain social and political

events, such as elections, influenced the flow of direct foreign investment. Their conclusion

suggested a negative relationship between socio-political instability and the flow of foreign

direct investment, but did not incorporate a comprehensive measure of country risk as a

determinant. Similarly, Brouthers (1995) found that international risk increased entry mode

choices that shifted risk to other firms.

Research relating performance outcomes and risk in the context of internationalization

has been scarce. Geringer and Herbert (1991) found that the correlation between a concept

similar to foreign risk (culture) and some measures of sales performance depended on the degree

of cultural difference. Generally researchers have not incorporated a measure of foreign risk in

their models, however. Although the combined effects of risk and entry mode on performance

are unclear, based on the inverse relationship between equity-based entry modes and risk, as well

as between cultural differences and performance, this paper proposes that:

9

Hypothesis 3: When foreign market risk is high, firms using a non-equity mode will have a higher rate of international growth.

Methods

Sample

The organizations included in this research are U.S. based and publicly-held, SMEs,

whose United States Securities and Exchange Commission 10-k reports are summarized and

compiled in the Financial Disclosure data base produced by Disclosure, Inc. These reports

contain management information and financial data covering fiscal years 1988 through 1994.

The September 1991 edition of Financial Disclosure was used to identify companies that made

an entry mode selection prior to the period during which performance was measured (1992-

1994).

Additional criteria used for selecting a sample from this population included industry

sector and size. Manufacturing firms (SIC codes 2000-3999) were chosen because they

represent the industrial sector that could require a full compliment of resources and a full range

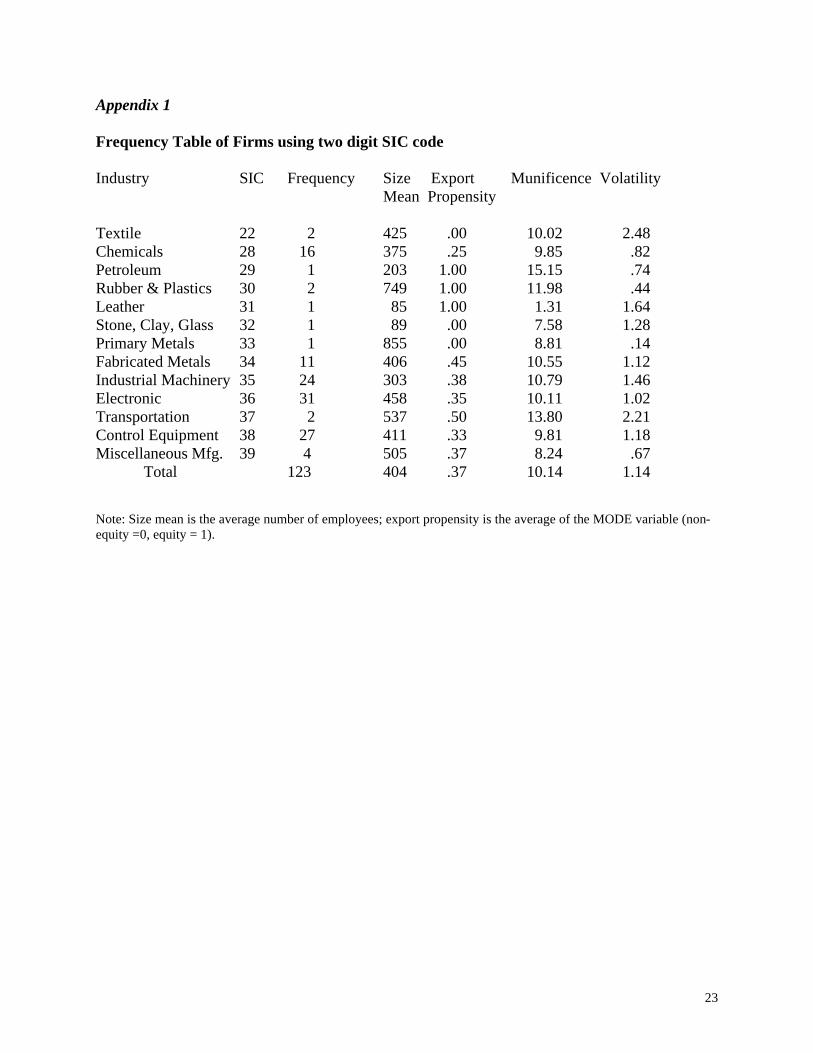

of entry modes in their expansion efforts (see Appendix 1 for list of two digit classifications and

their respective frequency, size, export propensity). In keeping with the size standards

established by the United States Small Business Administration for small manufacturing firms,

this research includes firms with less than 1000 employees (mean = 404). This SME size

distribution is consistent with previous descriptions of small and medium-sized firms

(Holzmuller & Kasper, 1991; Osteryoung, 1992; Calof, 1993; Julien, Joyals, & Deshaies, 1994).

Firms were also selected for this study based on whether current revenue from

international activity in the form of exporting, joint venture, and wholly-owned foreign

subsidiaries, is described in the management information text of the 10-k report summaries. The

financial and management text of the 10-k summaries of the firms meeting the aforementioned

criteria were further analyzed by this researcher and corroborated by an independent judge to

10

determine the primary mode used by each firm. Firms for which a primary mode could not be

established and firms for which international revenue figures for the three year fiscal period

ending in 1994 were unavailable were excluded from the sample. Inter-rater reliability test

revealed no significant difference in entry mode assessment (p<.05). Preliminary data indicated

the dependent variable was not normally distributed, therefore outliers beyond four standard

deviations were eliminated (Lomax, 1992). The results of segmenting the sample accordingly

yielded 123 firms whose records were of sufficient detail to be retained in the sample. The entry

mode distribution was dichotomized into non-equity (62 percent) and equity modes (38 percent).

Measurement Variables

Dependent Variable. The dependent variable, performance, has been measured in

strategic management literature by objective, profit-based, performance measures. Recent

research advocates productivity-based measurements (i.e. sales growth) as important

determinants of overall corporate performance (Nickell, 1996; Geroski, 1998). More

specifically, the success of internationalization has been calculated using objective measures of

sales growth (Bloodgood, Sapienza and Almeida, 1996). Although profit-oriented financial

measures of performance are preferred in many studies, these data are only available at the

aggregated corporate level. These data do not accurately isolate the influence of variables in an

international context and are not consistently segmented in corporate or business level financial

statements. Consequently, this research measures performance (INTPERF) based on the average

growth in international revenue over the most recent three-year period, 1992-1994, as reported in

Financial Disclosure database.

Independent Variables. Prior operationalizations have measured munificence in terms of

average growth in net sales and operating income in the dominant industry during the five-year

period prior to the foreign market entry, because a temporal approach lends credibility to the

nature of the contingency model (Keats & Hitt, 1988). Although Keats and Hitt used net sales

and operating income to measure environmental resources, Dess and Beard (1984) suggested that

11

industry sales are the primary factor in environmental munificence. This research uses a similar

approach, measuring the average growth in industry-wide total revenue (MUNIFICENCE)

between 1986 and 1990 for each primary Standard Industrial Classification (SIC) code as

reported in Financial Disclosure.

Keats & Hitt (1988) measured volatility by the degree of fluctuation in net sales and

operating income in the dominant industry during the five-year period prior to the performance

period. Similarly, this research calculates VOLATILE using the standard deviation of the

average change in revenue growth during the period 1986-1990.

Foreign market risk has been systematically evaluated and measured by a number of

private companies as a service for firms doing business internationally, as reviewed by

Krayenbuehl (1988). This study uses data from the “International Country Risk Guide” (ICRG),

a monthly newsletter that quantifies a monthly risk rating using factors consistent with the

determinants of risk identified in previous academic research (Cosset & Roy, 1991). ICRG bases

their rating on political, financial and economic risk variables (Krayenbuehl, 1988). The

political variable contributes 50 percent of the score and financial and economic indicators

represent 25 percent each. Political risk is determined using 13 indicators to measure political

leadership, law and order tradition, and quality of bureaucracy. Five factors are used to assess

financial risk such as loan default or unfavorable loan restructuring, losses from foreign

exchange controls, and repudiation of contracts by governments. Economic risk is determined

using six indicators to measure inflation, debt service ratio and international liquidity. This

research uses the composite political, financial and economic risk rating (RISK) from the

November 1988 ICRG (Krayenbuehl, 1988) for each target market. This time frame concurs

with the domestic environment measurement period, preceding the foreign market entry. In the

case of multiple countries of operation, the risk ratings are prorated based on the revenue

generated by country.

Following Erramilli & Rao (1990) foreign entry mode (MODE) is often measured as a

12

dichotomous variable, with “0” assigned to those foreign market entry decisions for which there

was low control (exporting), and “1” assigned to those foreign market entry decisions for which

there was integrated or independent control (joint ventures, and wholly-owned foreign

subsidiaries).

Control variables. Firm size, industrial sector, and firm resources have been considered

as contingency variables in prior international research. Variances in firm size are controlled for

by including the log of the number of employees (LOGEMP) in the model. Industry effects are

partially controlled for in this study since domestic environmental factor scores are calculated

separately for each two digit SIC codes as explained earlier. Resources are controlled for

because of the importance of resource commitment and control in foreign entry mode choice

(Hill, Hwang, & Kim, 1990; Agarwal & Ramaswami, 1992; Kim & Hwang, 1992). This

research measures financial resources by dividing the firm's long term debt to market value of

equity ratio by the average industry long term debt to market value of equity ratio within its two

digit SIC code (DEBT). This average measurement of a firm's comparative long-term liquidity

or debt capacity for a three-year period prior to entry mode choice is an indicator of the

availability of internal funds for international expansion (Chatterjee, 1990). Dividing by the

industry average corrects for industry effects. The log of DEBT was taken to limit the variance

in the distribution of the values and thereby minimize scaling problems among independent

variables.

Analysis

A hierarchical moderated regression variance was run for the main effects of entry mode

and environmental variables on performance, controlling for size and financial resources. The

13

product terms of entry mode with the three moderating environmental variables, respectively,

were subsequently added to the model to determine if there was a significant increase in the

predictability of the criterion variable (Jaccard, Turrisi, and Wan, 1990). The relationship is modeled in the following equation:

Eq. (1) Yi = B0 + B1X1 + BnXn + B1X1* BnXn + control variables + ε,

Where Yi represents average revenue growth (INTPERF), X1 represents entry mode (MODE),

Xn represents three external variables (MUNIFICENCE, VOLATILE, and RISK), and the

multiplicative factor represents the interaction between MODE and each of the external

variables. The control variables included in the model are size (LOGEMP) and resources

(LOGDEBT). In the hierarchical moderated regression model the predictor, moderator, and

control variables were entered in the first stage, and the interactive factors were added to the

model in the second stage (Cohen & Cohen, 1983). The incremental proportion of variance

explained by the interactive factors was tested. This study also tests the strength and form of the

interactive relationships by analyzing the direct effects of the moderator on the predictor variable

and dependent variable (McArthur & Nystrom, 1991).

Results

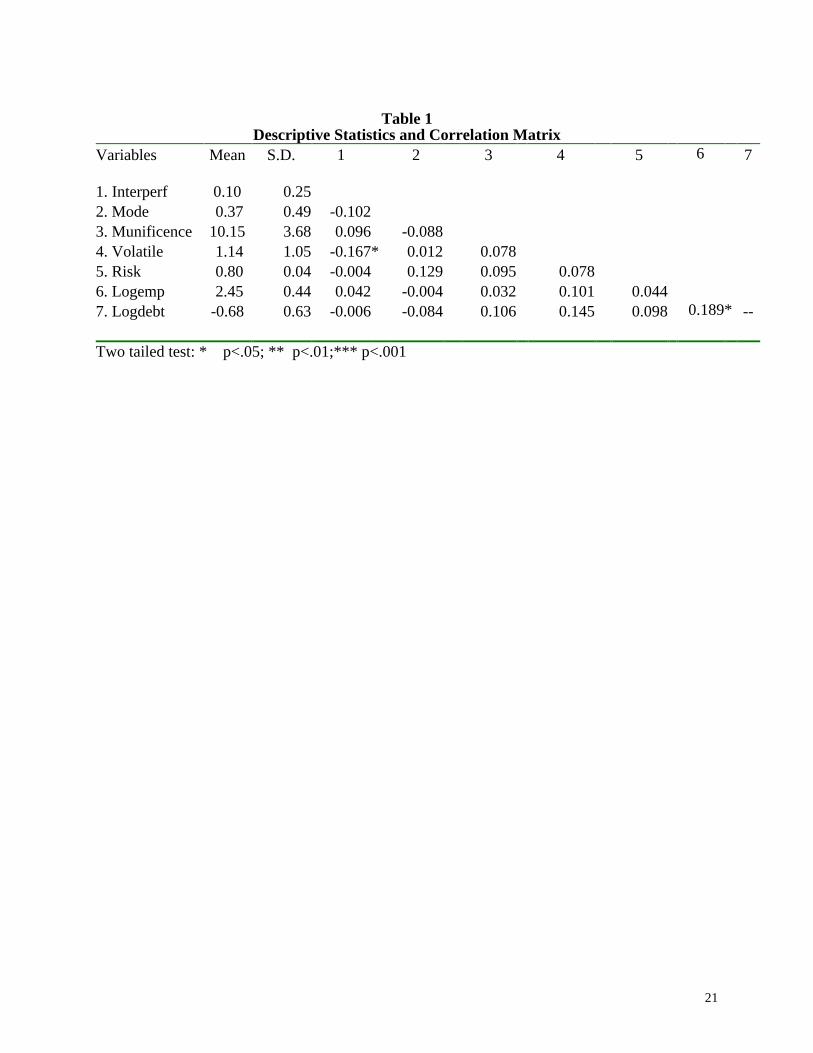

Descriptive statistics provided in Table 1 include product moment correlation (Pearson),

mean, and standard deviations. The correlations between the predictor, the moderator, and the

criterion variables are not significant or are very low and therefore, moderator effects should not

be unduly influenced by multicollinearity. Also, an analysis of the data indicated that none of

the variables exceeded an acceptable threshold (10.0) for variance inflations factors (VIF) also

indicating there are no problems with multicollinearty that would violate assumptions for the

general linear model (Lomax, 1992).

14

--------------------- Insert Table 1

---------------------

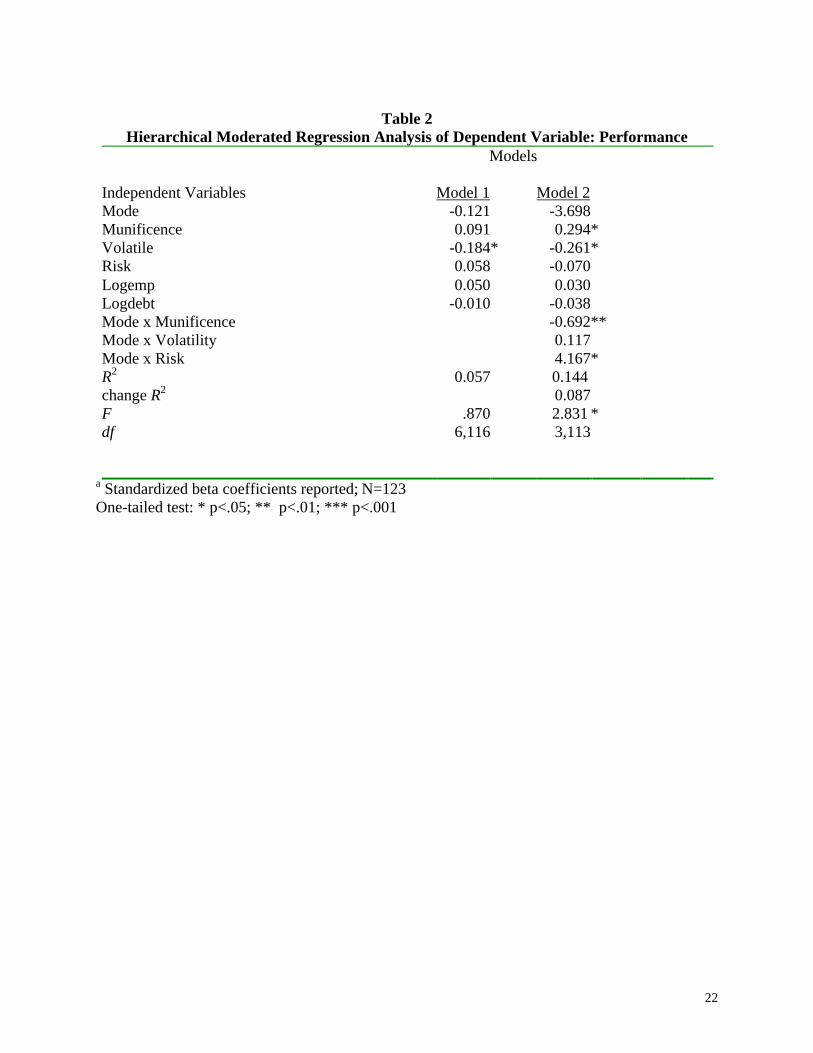

The moderated multiple regression results, presented in Table 2 determine the extent to

which moderating environmental variables interact with entry mode to predict performance. The

first model indicates there is a significant and negative main effect for VOLATILE only (p <.05).

--------------------- Insert Table 2

---------------------

The results of the second model indicate that the inclusion of the product terms improves

the amount of variance explained in performance significantly (R2 increases 8.7 percent, F=

2.831). More specifically, there is a significant interaction between MODE and

MUNIFICENCE (p< .05). The negative sign indicates that SMEs in more munificent industries

will have higher rates of international expansion when using non-equity modes, supporting

hypothesis 1. The main effects of volatility are negative and significant (p <.05), but the

interaction with entry mode is not . The results also indicate a significant interaction between

MODE and RISK (p < .05). Specifically, the positive sign indicates that SMEs in markets with

higher levels of foreign risk will have higher levels of international expansion when using equity

modes, contradicting the predicted sign of the product term proposed in hypothesis 3. Since

there are no significant relationships between the environmental variables and either mode or

performance, the model indicates that the significant environmental variables are homologizer

moderators (MacArthur & Nystrom, 1991). In other words, the magnitude of the entry mode-

performance relationship varies significantly for firms in different environmental conditions.

Considering the R2 of the model with main effects and product terms, the sample size (n=123) is

sufficient for achieving a power of .80 (alpha = 0.05) with a small effect size (ò.20), (Jaccard,

Turrisi, & Wan, 1990).

15

Discussion And Conclusion

The purpose of this research is to extend the contingency theory of strategic alignment to

the internationalization of small and medium sized enterprises (SME). Specifically, the

contingency model hypothesizes that the international rate of growth of SMEs depends on the

combined effects of environmental factors and entry mode. The general results confirm that

exporting firms have a higher rate of growth than equity modes when the domestic industry has

higher growth in prior periods. Firms using an equity-based mode have a higher rate of growth

than export modes when foreign risk is higher. Volatility does appear to have a significant and

negative main effect but not a significant interactive effect with entry mode. The results further

indicate that the full model with interactive terms accounts for a significantly (p<.05) greater

proportion of variance than the full model without interaction of each variable with MODE.

These findings further support the basic contingency theory that it is the interaction between

contingent environmental variables and foreign entry mode that has significant implications in

predicting the rate of international growth.

This study relates to prior research in a number of ways. The results support Kuzmicki

and Kramer’s (1994) contention that the effect of domestic munificence on international growth

is a function of resource commitment, as reflected in entry mode choice. In contrast to Lu and

Beamish’s (2001) findings that exporting has a negative impact on the financial performance of

SMEs, these results indicate that exporting can have a positive product/market performance

outcome for SMEs in faster growing industrial sectors. These findings also contrast Chen &

Martin’s (2001) conclusion that firms in fast growing domestic industries do not choose to grow

internationally. Instead, it is likely that exporting is still a viable option in munificent periods for

SMEs.

Contrary to the original hypothesis, the results suggest that SMEs will choose equity-

based modes in risky foreign environments to maximize international growth. In retrospect,

prior research has been contextually unclear regarding the relationship between risk and entry

16

mode choice and severely lacking empirical evidence on foreign performance implications.

Consequently, these results should serve as preliminary evidence that equity-based foreign entry

modes that provide resource control such as joint ventures and foreign direct investments can be

a viable alternative for international growth to minimize risk in foreign markets. Further

empirical investigation should focus on whether the firm’s equity investment involves a

proprietary product or technology as suggested by Agarwal and Ramaswam (1992). Similar to

Brouthers’ (1995) argument that differences in investment risk between joint ventures and

wholly-owned subsidiaries account for entry mode choice, this study indicates their combined

effects may also affect performance variances. However, future studies should also consider

differences in investment risk between the two types of equity-based entry modes. Finally, the

direct effects of volatility were hypothesized based on domestic research, suggesting an inverse

relationship to growth. Although the results indicate negative main effects, the non-significant

interactive effects suggest that foreign market entry may minimize these negative effects of

domestic volatility on international growth.

The results have to be interpreted within the context of some limitations. The type of

entry mode was identified based on a subjective analysis of management information from the

database, which is subject to interpretation error, despite high correlation between raters. Also,

the dichotomization of entry mode limits some of the distinctions that can be made between joint

ventures and wholly owned subsidiaries. Licensing mode of entry was eliminated because

licensing fees are not fully compatible with the financial reporting of the dependent variable,

revenue growth. Additionally, the lack of findings related to the interaction of volatility may be

due to the difficulty of changing strategies at the time of market entry, based on prevalent

external factors. Although strategic researchers prefer financial performance measures, using

corporate level data must take into account the relative contribution of international revenue on

profitability, which is not always ascertainable from archival data. Finally, using smaller and

privately held firms could complement the findings of this research.

17

In sum, this study provides managers with some evidence regarding how to maximize

performance by aligning entry mode strategy with external contextual circumstances.

Specifically, when times are good domestically, taking investment risks in a foreign market may

not be prudent. Likewise higher degrees of risk associated with the foreign market should

encourage modes of entry that provide for control of resources. References

Agarwal, S. and S. N. Ramaswami (1992). “Choice of Foreign Market Entry Mode: Impact of Ownership, Location and Internalization Factors,” Journal of International Business Strategy. 23(1), 1-27. Anderson, E. and H. Gatignon (1986). “Modes of Foreign Entry: A Transaction Cost Analysis and Propositions,” Journal of International Business Studies. 17, 1-26. Axinn, C. N., R. Savit, J. M. Sinkula, and S. V. Thach (1995). “Export Intention, Beliefs, and Behaviors in Smaller Industrial Firms,” Journal of Business Research. 32(1), 49-58. Baird, I., M. Lyles, and J. B. Orris (1994). “The Choice of International Strategies by Small Business, Journal of Small Business Management, 32(1), 48-59. Bloodgood, J. M., H. Sapienza & J. G. Almeida (1992). “The Internationalization of New High-Potential U.S. Ventures: Antecedents and Outcomes,” Entrepreneurship: Theory and Practice. 20(4), 61-76. Brouthers, K. D. (1995). “The Influence of International Risk on Entry Mode Strategy in the Computer Software Industry,” Management International Review. 35(1), 7-28. Burns, T. and G. M. Stalker (1961). The Management of Innovation. London: Tavistock. Calof, J. L. (1993). “The Impact of Size on Internationalization,” Journal of Small Business Management. 31(4), 60-69. Chatterjee, S. 1990. “Excess Resources, Utilization Costs, and Mode Entry,” Academy of Management Journal. 33:4, pp.780-800. Chen, R. and M. J. Martin (2001). “Foreign Expansion of Small Firms: The Impact of Domestic Alternatives and Prior Foreign Business Involvement,” Journal of Business Venturing, 16, 557-574.

18

Christensen, H. K. and C. A. Montgomery (1981). “Corporate economic performance: Diversification strategy versus market structure,” Strategic Management Journal, 2, 327-343. Cohen, J. and P. Cohen (1983). Applied Multiple Regression/correlation Analysis for the Behavioral Sciences. Hillsdale, NJ: Lawrence Erlbaum Associates. Contractor, F. and P. Lorange (eds.) (1988). Cooperative strategies in international business. Lexington, Mass.: Lexington Books. Cosset, J. and J. Roy (1991). “The determinants of country risk ratings,” Journal of International Business Studies, 22(1), 135-143. Daniels, J. D. and J. Bracker (1989). “Profit Performance: Do Foreign Operations Make a Difference?” Management International Review, 29(1), 46-56. Daniels, J. D., R. A. Pitts, and M. J. Tretter (1984). “Strategy and Structure of U.S. Multinationals: An Exploratory Study. Academy of Management Journal, 27(2), 292-307. Dess, G. G., and D. W. Beard (1984). “Dimensions of Organizational Task Environments,” Administrative Science Quarterly, 29(3), 52-73. Domke-Damonte, D. (2000). “Interactive effects of International Strategy and Throughput Technology on Entry Mode for Service Firms,” Management International Review, 40(1), 41-59. Erramilli, M. K. and C. P. Rao (1993). Service Firms International Entry-mode Choice: A Modified Transaction-cost Analysis Approach,” Journal of Marketing, 57(3), 19-38. Fatehi-Sedeh, K. and M. H. Safizadeh (1988). “Sociopolitical Events And Foreign Direct Investment,” Journal Of Management, 14(1), 93-108. Galbraith, J. R. and R. K. Kazanjian (1986). Strategy, implementation: Structure, systems and processes. St. Paul: West. Geringer, J. M. & L. Herbert. (1990). “Measuring Performance of International Joint Ventures,” Journal of International Business Studies, 12, 249-263. Geroski, P. A. (1998). “An Applied Econometrician’s View of Large Company Performance,” The Review of Industrial Organization, 13, 271-293. Ghosal, S. (1987). “Global Strategy: An Organizing Framework,” Strategic Management Journal, 8, 425-440. Goll, I. and A. Rasheed (1997). “ Rational Decision-Making And Firm Performance: The Moderating Role Of Environment,” Strategic Management Journal, 18, 583-591.

19

Gripsrud, G. (1990). “The Determinants of Export Decisions and Attitudes to a Distant Market: Norwegian Fishery Exports to Japan,” Journal of International Business Studies, 21(3), 469-486. Habib, M. M. and B. Victor (1991). “Strategy, Structure, and Performance of U.S. Manufacturing and Service MNCs: A Comparative Analysis,” Strategic Management Journal, 12, 589-60. Hill, C. W. L., P. Hwang, and W. C. Kim (1990). “An Eclectic Theory of the Choice of International Entry Mode,” Strategy Management Journal, 11, 117-128. Holzmuller, H. and H. Kasper (1991). “On a Theory of Export Performance: Personal and Organizational Determinants of Export Trade Activities Observed in Small and Medium-sized Firms,” Management International Review, 31, 45-70. Jaccard, J., R. Turrisi, and C. K. Wan (1990). Interaction Effects in Multiple Regression. Newbury Park, CA: Sage Publications. Julien, P., A. Joyal, and L. Deshaies (1994). “SMEs and International Competition: Free Trade Agreement or Globalization?” Journal of Small Business Management, 32(3), 52-64. Keats, B. and M. Hitt, (1988). “A Causal Model of Linkages Among Environmental Dimensions, Macro Organizational Characteristics, and Performance,” Academy of Management Journal, 31, 570-598. Kim, W. C. and P. Hwang (1992). “Global Strategy and Multinationals’ Entry Mode Choice,” Journal of International Business Studies, 23(1), 29-53. Kim W.C., Hwang, P. and W. P. Burgers (1989). “Global Diversification Strategy and Corporate Profit Performance,” Strategic Management Journal, 10(1), 45-57. Kogut, B. and H. Singh (1988). “The effect of national culture on the choice of entry mode,” Journal of International Business Studies. 19(3), 411-432. Krayenbuehl, T. (1988). Country Risk Assessment and Monitoring. New York: Woodhead-Faulkner. Kuzmicki, J. and T. Kramer (1994). “Non-equity strategic alliance formation: Environmental and industry influences, Southern Management Association Proceedings. Lomax, R. G. (1992). Statistical Concepts: A Second Course for Education and the Behavioral Sciences. White Plains, NY: Longman. Lu, J. and P. W. Beamish (2001). “The Internationalization and Performance of SMEs,” Strategic Management Journal, 22(6), 565-586.

20

Luo, Y. (1999). “The Structure-performance Relationship in a Transitional Economy: An Empirical Study of Multinational Alliances in China,” Journal of Business Research, 46(1), 15-31. Madsen, T. K. (1989). “Successful Export Marketing Management: Some Empirical Evidence,” International Marketing Review, 6(4), 41-58. McArthur, A. and P. Nystrom (1991). “Environmental Dyanmism, Complexity, And Munificence As Moderators Of Strategy-Performance Relationships,” Journal of Business Research, 23, 349-361. Miles, M. P., J. G. Covin, and M. B. Heeley (2000). “The Relationship between Environmental Dynamism and Small Firm Structure, Strategy, and Performance,” Journal of Marketing Theory and Practice, 8(2), 63-78. Mosakowski, E. (1988). “Structure, Strategy, and Performance of Entrepreneurial Firms: a Dynamic Analysis of the Computer Industry,” Unpublished dissertation, University of California, Berkely, CA. Nickell, S. J. (1996). “Competition and Corporate Performance,” Journal of Political Economy, 104(4), 724-746. Osteryoung, J. (1992). “Financial Ratios in Large Public and Small Private Firms,” Journal of Small Business Management, 30(3), 35-47. Oviatt B., and P. McDougall (1994). “Toward a Theory of International New Ventures,” Journal of International Business Studies. 25(1), 45-62. Pelham, A.E. (1999). “Influence of Environment, Strategy, and Market Orientation on Performance in Small Manufacturing Firms,” Journal of Business Research 45, 33-46. Root, F. R. (1987). Entry Strategies for International Markets. Lexington, MA: D.C. Heath. Simerly, R. and M. Li (2000). “Environmental Dynamism, Capital Structure And Performance: A Theoretical Integration And An Empirical Test,” Strategic Management Journal, 21, 31-49. Stopford, J.M. and L. T. Wells (1972). Managing the Multinational enterprise: Organization of the Firm and Ownership of the Subsidiaries. New York: Basic Books. Tang, J. and C. Espinal (1989). “A Model to Assess Country Risk,” Omega, 17(4), 363-369. Tang, M. and C. J. Yu (1990). “Foreign Market Entry: Production-related Strategies,” Management Science, 36(4), 476-489. Woodcock, C. P., Beamish, P. W., and S. Makino (1994). “Ownership-based Entry Mode Strategies and International Performance,” Journal of International Business Studies, 25(2), 253-273.

21

Table 1 Descriptive Statistics and Correlation Matrix

Variables Mean S.D. 1 2 3 4 5 6 7 1. Interperf 0.10 0.25

2. Mode 0.37 0.49 -0.102 3. Munificence 10.15 3.68 0.096 -0.088 4. Volatile 1.14 1.05 -0.167* 0.012 0.078 5. Risk 0.80 0.04 -0.004 0.129 0.095 0.078 6. Logemp 2.45 0.44 0.042 -0.004 0.032 0.101 0.044 7. Logdebt -0.68 0.63 -0.006 -0.084 0.106 0.145 0.098 0.189* -- Two tailed test: * p<.05; ** p<.01;*** p<.001

22

Table 2 Hierarchical Moderated Regression Analysis of Dependent Variable: Performance

Models Independent Variables Model 1 Model 2 Mode -0.121 -3.698 Munificence 0.091 0.294* Volatile -0.184* -0.261* Risk 0.058 -0.070 Logemp 0.050 0.030 Logdebt -0.010 -0.038 Mode x Munificence -0.692** Mode x Volatility 0.117 Mode x Risk 4.167* R2 0.057 0.144 change R2 0.087 F .870 2.831 * df 6,116 3,113

a Standardized beta coefficients reported; N=123 One-tailed test: * p<.05; ** p<.01; *** p<.001

23

Appendix 1 Frequency Table of Firms using two digit SIC code Industry SIC Frequency Size Export Munificence Volatility

Mean Propensity Textile 22 2 425 .00 10.02 2.48 Chemicals 28 16 375 .25 9.85 .82 Petroleum 29 1 203 1.00 15.15 .74 Rubber & Plastics 30 2 749 1.00 11.98 .44 Leather 31 1 85 1.00 1.31 1.64 Stone, Clay, Glass 32 1 89 .00 7.58 1.28 Primary Metals 33 1 855 .00 8.81 .14 Fabricated Metals 34 11 406 .45 10.55 1.12 Industrial Machinery 35 24 303 .38 10.79 1.46 Electronic 36 31 458 .35 10.11 1.02 Transportation 37 2 537 .50 13.80 2.21 Control Equipment 38 27 411 .33 9.81 1.18 Miscellaneous Mfg. 39 4 505 .37 8.24 .67 Total 123 404 .37 10.14 1.14 Note: Size mean is the average number of employees; export propensity is the average of the MODE variable (non-equity =0, equity = 1).