Embed Size (px)

Citation preview

Equity Analysis and Valuation of Texas Roadhouse

Taylor Edwards [email protected]

Slade Solcher [email protected]

Kason Wood [email protected]

Blake Rasmussen [email protected]

2

Table of Contents

EXECUTIVE SUMMARY 6

INDUSTRY ANALYSIS 7 ACCOUNTING ANALYSIS 10 FINANCIAL ANALYSIS 11 VALUATION ANALYSIS 14

COMPANY OVERVIEW 16

INDUSTRY OVERVIEW 17

FIVE FORCES MODEL 21

RIVALRY AMONG EXISTING FIRMS 22 INDUSTRY GROWTH RATE 22 CONCENTRATION 25 DIFFERENTIATION 27 SWITCHING COSTS 27 LEARNING AND SCALE ECONOMIES 28 FIXED – VARIABLE COSTS 30 EXCESS CAPACITY 31 EXIT BARRIERS 33 CONCLUSION 33 THREAT OF NEW ENTRANTS 34 ECONOMIES OF SCALE 34 FIRST MOVER ADVANTAGE 35 ACCESS TO CHANNELS OF DISTRIBUTION AND RELATIONSHIPS 38 LEGAL BARRIERS 38 CONCLUSION 39 THREAT OF SUBSTITUTES 40 RELATIVE PRICE PERFORMANCE 41 BARGAINING POWER OF CUSTOMERS 41 DIFFERENTIATION 41 PRICE SENSITIVITY 42 NUMBER OF CUSTOMERS 43 CONCLUSION 44 BARGAINING POWER OF SUPPLIERS 44 SWITCHING COSTS 45 DIFFERENTIATION 45 IMPORTANCE OF PRODUCT FOR COSTS AND QUALITY 46 NUMBER OF SUPPLIERS 46 CONCLUSION 47 COST LEADERSHIP 48 ECONOMIES OF SCALE 48 EFFICIENT PRODUCTION 49 RESEARCH AND DEVELOPMENT AND BRAND ADVERTISING 50 DIFFERENTIATION 51 SUPERIOR PRODUCT QUALITY 51 SUPERIOR PRODUCT VARIETY 52

3

INVESTMENT IN BRAND IMAGE 53 CONCLUSION 54

COMPETITIVE ADVANTAGE ANALYSIS 55

COST LEADERSHIP 55 PRODUCT DIFFERENTIATION 56

INTRODUCTION TO ACCOUNTING ANALYSIS 57

KEY ACCOUNTING POLICIES 57

TYPE ONE ACCOUNTING POLICIES 58 ECONOMIES OF SCALE 58 PRODUCT QUALITY 60 BRAND IMAGE 61 TYPE TWO ACCOUNTING POLICIES 61 OPERATING LEASES 62 GOODWILL 62

ASSESS DEGREE OF POTENTIAL ACCOUNTING FLEXIBILITY 63

OPERATING/CAPITAL LEASES 64 GOODWILL 64 CONCLUSION 65

EVALUATION OF ACTUAL ACCOUNTING STRATEGY 66

PENSION PLAN 66 RESEARCH AND DEVELOPMENT 66 GOODWILL 66 OPERATING AND CAPITAL LEASING 68 CONCLUSION 69

QUALITY OF DISCLOSURE 70

QUALITATIVE MEASURES OF ACCOUNTING QUALITY 70 ECONOMIES OF SCALE 70 GOODWILL 71 OPERATING AND CAPITAL LEASING 71 QUANTITATIVE MEASURES OF ACCOUNTING QUALITY 72

IDENTIFYING POTENTIAL RED FLAGS 72

GOODWILL 72 OPERATING LEASES 72 GOODWILL 77 FINANCIAL STATEMENTS 78 BALANCE SHEET 79 INCOME STATEMENT 84 CONCLUSION 87

INTRODUCTION TO FINANCIAL ANALYSIS 88

4

RATIO ANALYSIS 88

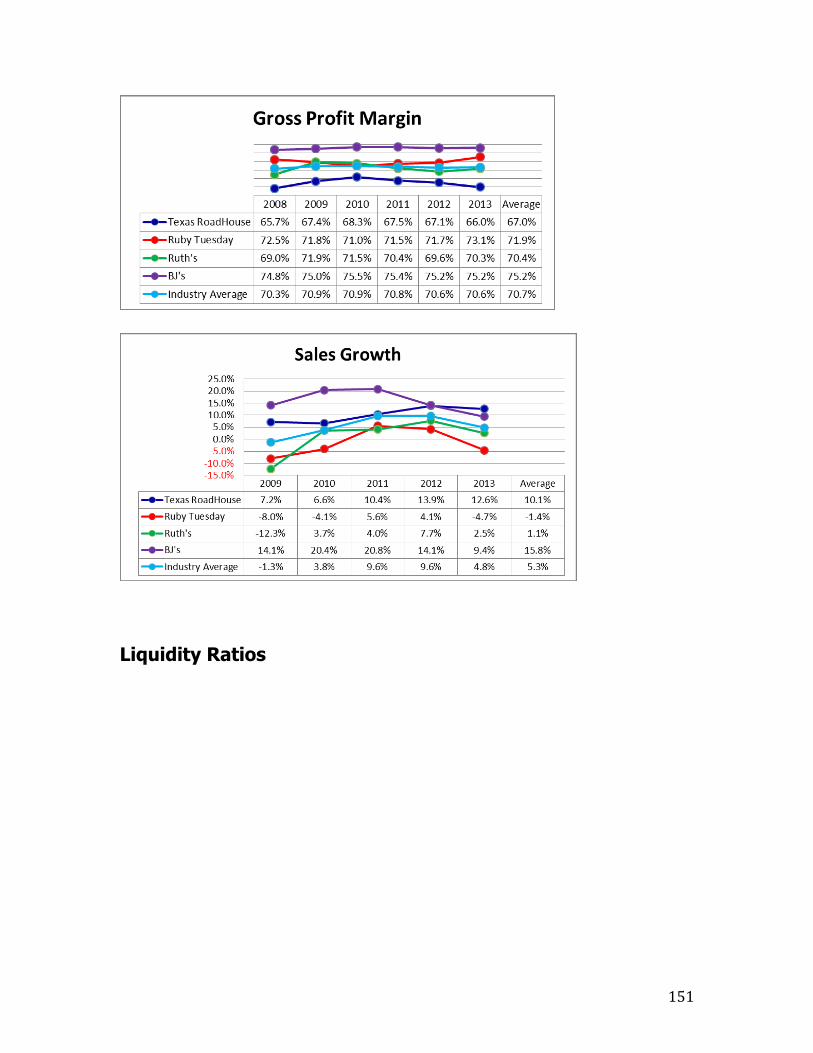

LIQUIDITY RATIOS 88 CURRENT RATIO 89 QUICK RATIO 90 INVENTORY TURNOVER 91 ACCOUNTS RECEIVABLE TURNOVER 92 ACCOUNTS RECEIVABLE DAYS 93 CASH TO CASH CYCLE 94 WORKING CAPITAL TURNOVER 95 CONCLUSION 96 PROFITABILITY RATIOS 96 SALES GROWTH 97 GROSS PROFIT MARGIN 98 OPERATING PROFIT MARGIN 99 NET PROFIT MARGIN 100 RETURN ON ASSET 102 RETURN ON EQUITY 103 CONCLUSION 104

CAPITAL STRUCTURE RATIOS 104

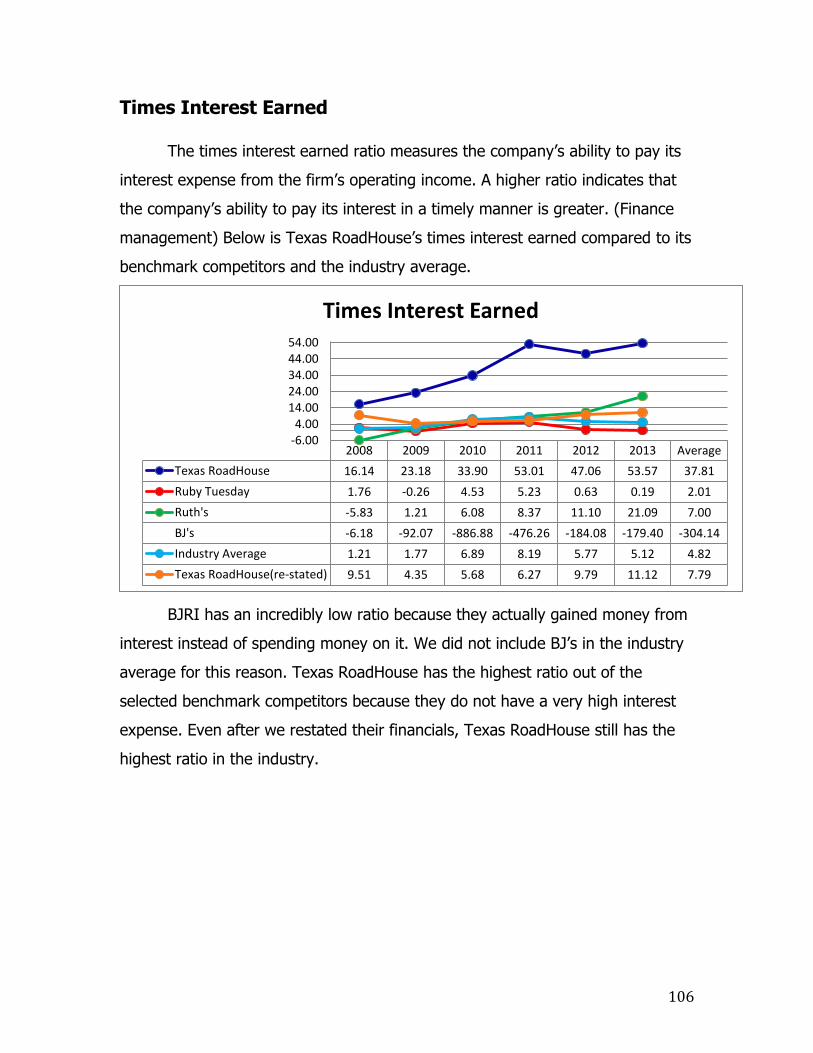

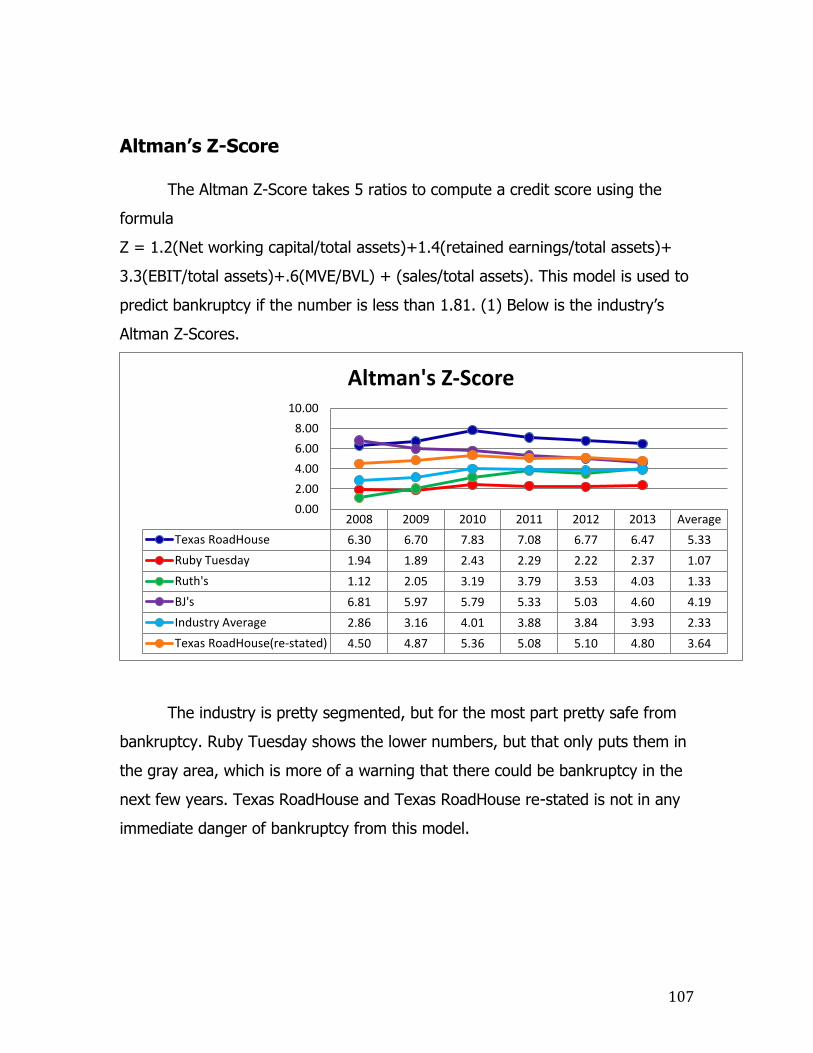

DEBT TO EQUITY 105 TIMES INTEREST EARNED 106 ALTMAN’S Z-SCORE 107 INTERNAL GROWTH RATE 108 SUSTAINABLE GROWTH RATE 109 CONCLUSION 110

FINANCIAL FORECASTING 110

INCOME STATEMENT 110 DIVIDENDS FORECASTING 114 BALANCE SHEET 114 STATEMENT OF CASH FLOWS 118

COST OF CAPITAL ESTIMATION 120

COST OF DEBT 120 COST OF EQUITY 121 BACKDOOR COST OF EQUITY 124 WEIGHTED AVERAGE COST OF CAPITAL (WACC) 124

METHOD OF COMPARABLES 127

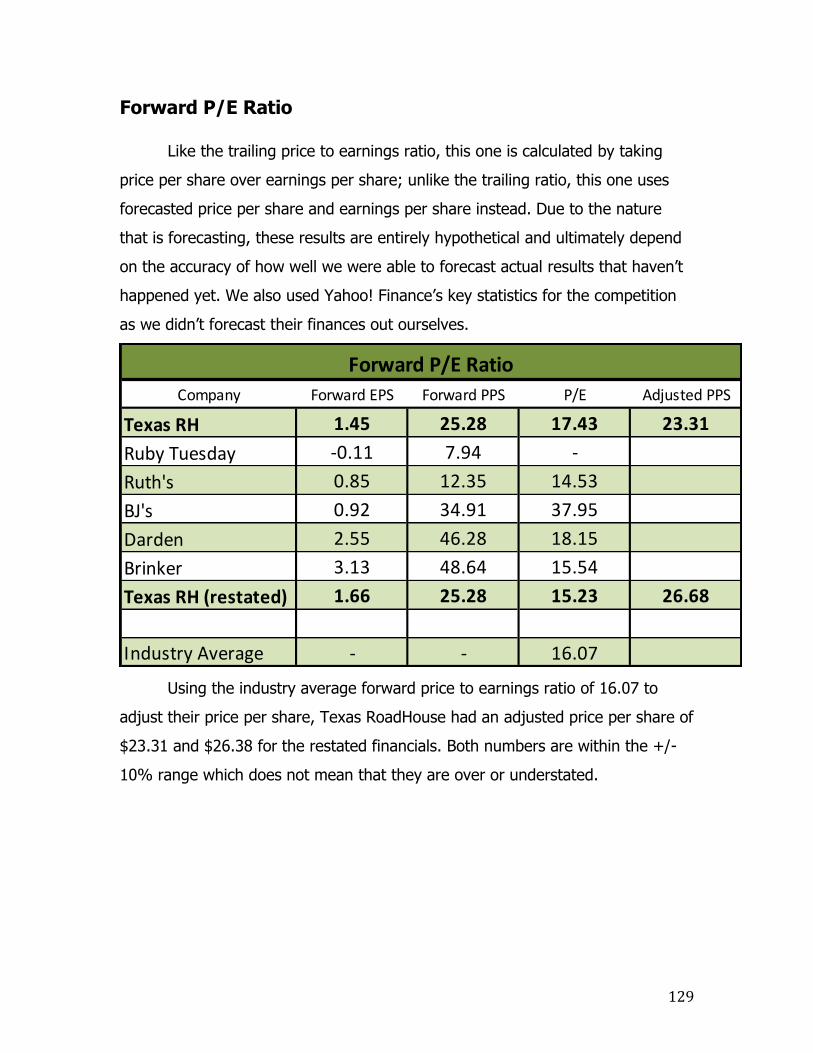

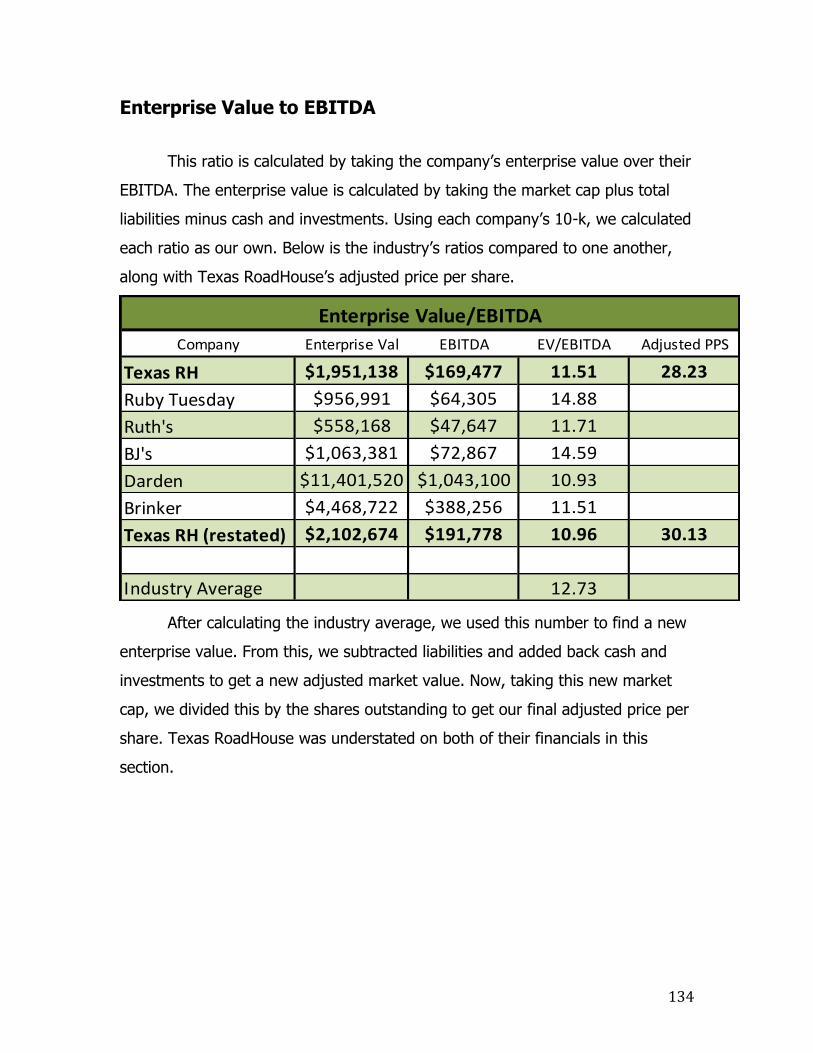

TRAILING P/E RATIO 128 FORWARD P/E RATIO 129 PRICE TO BOOK RATIO 130 DIVIDENDS TO PRICE RATIO 131 PRICE EARNINGS GROWTH RATIO 132 PRICE TO EBITDA 133 ENTERPRISE VALUE TO EBITDA 134 CONCLUSION 135

5

INTRINSIC VALUATION MODEL 135

DISCOUNTED DIVIDENDS MODEL 136 DISCOUNTED FREE CASH FLOWS MODEL 137 AS STATED RESIDUAL INCOME MODEL 140 LONG RUN RESIDUAL INCOME MODEL 142 AS STATED LONG-RUN RESIDUAL INCOME MODELS 143 RESTATED LONG-RUN RESIDUAL INCOME MODELS 145

SOURCES 147

APPENDIX 148

CAPITAL STRUCTURES RATIOS 148 PROFITABILITY RATIOS 149 LIQUIDITY RATIOS 151 METHOD OF COMPARABLES 154 COST OF DEBT AND EQUITY MODELS 157 GROWTH RATE GRAPHS 158 REGRESSIONS 159 1 YEAR REGRESSIONS 161 7 YEAR REGRESSIONS 164 INTRINSIC VALUATION MODELS 169

6

Executive Summary

Analyst Recommendation: SELL (OVERVALUED)

TXRH - NYSE (6/1/2014) Altman Z-Scores

52 Week Range $22.87 - $29.07 2009 2010 2011 2012 2013

Revenue 1.59 Billion Initial Scores 23.18 33.9 53.01 47.06 53.57

Market Capitalization 1.83 Billion Revised Scores 4.35 5.68 6.27 9.79 11.12

Shares Outstanding 69.17 Million

Financial Based Valuations

As Stated Restated As Stated Restated

Book Value Per Share 0.001 Trailing P/E 22.05 25.76

Return on Equity 15.60% 17.40% Forward P/E 23.31 26.68

Return on Assets 10.53% 10.1% Dividends to Price 30.17 30.17

PEG Ratio 15.45 22.46

Cost of Capital Price to Book 53.51 54.52

Estimated Adj. R^2 Beta Size Adj Ke Price to EBITDA 21.28 24.08

3 month 5.11% 0.42 7.68% EV/EBITDA 28.23 30.13

1 Year 5.11% 0.42 7.68%

2 Year 5.12% 0.42 7.69% Intrinsic Valuations

7 Year 5.18% 0.42 7.70% As Stated Restated

10 Year 5.14% 0.42 7.69% Discounted Dividends $20.18 N/A

Free Cash Flows $10.51 N/A

As Stated Restated Residual Income $17.16 $18.18

Backdoor Ke 10.4% Long Run Residual Income $12.99 $13.91

WACC(BT) 8.80% 9.73%

Published Beta 0.88

Lower Bound

Center Value Upper Bound

Ke 0.92% 5.90% 10.88%

Size Adjusted Ke 2.72% 7.70% 12.68%

WACC(BT) 8.31% 9.73% 11.15%

7

TXRH Historical Stock Prices

TXRH, BJRI, RT, RUTH Historical Prices

Industry Analysis

Texas Roadhouse is an upscale casual dining restaurant that operates in

the United States and 3 foreign countries. They compete with other restaurants

such as Ruby Tuesday, BJ’s Brewhouse, and Ruth’s Hospitality Group. Because

these companies have similar strategies and corporate structures, we have

chosen to use them as a sample of the restaurant industry Texas Roadhouse

competes in. Overall, the restaurant industry is growing, with sales expected to

8

reach 683.4 Billion in 2014. Firms in the upscale casual industry use economics

of scale, relationships with distributers of raw goods, and processes to increase

efficiency to compete on a price basis with other restaurants. In order to

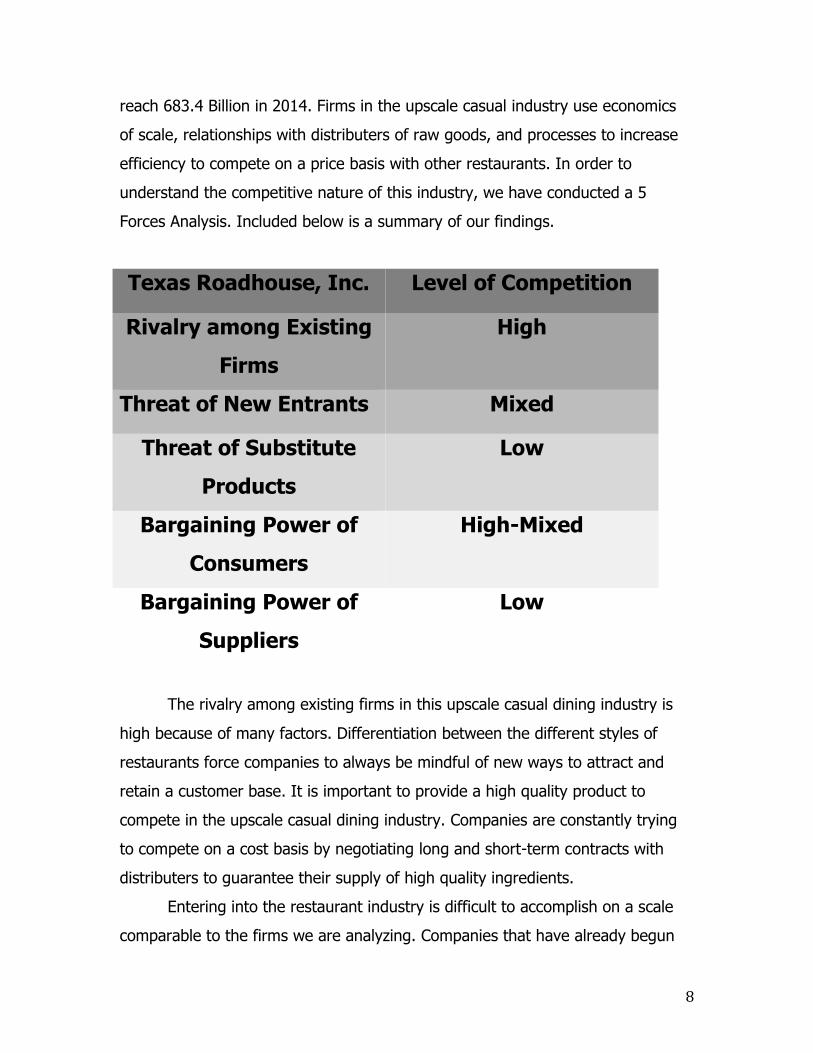

understand the competitive nature of this industry, we have conducted a 5

Forces Analysis. Included below is a summary of our findings.

Texas Roadhouse, Inc. Level of Competition

Rivalry among Existing

Firms

High

Threat of New Entrants Mixed

Threat of Substitute

Products

Low

Bargaining Power of

Consumers

High-Mixed

Bargaining Power of

Suppliers

Low

The rivalry among existing firms in this upscale casual dining industry is

high because of many factors. Differentiation between the different styles of

restaurants force companies to always be mindful of new ways to attract and

retain a customer base. It is important to provide a high quality product to

compete in the upscale casual dining industry. Companies are constantly trying

to compete on a cost basis by negotiating long and short-term contracts with

distributers to guarantee their supply of high quality ingredients.

Entering into the restaurant industry is difficult to accomplish on a scale

comparable to the firms we are analyzing. Companies that have already begun

9

operations at the level of these firms have a distinct cost advantage because of

economies of scale. This allows companies that are buying ingredients in huge

quantities to demand prices from suppliers that smaller businesses cannot

obtain. Also, new entrants are faced with the difficult process of negotiating

channels of distribution, while existing firms have these contracts in place. In

addition to this cost disadvantage, new entrants generally do not have the

opportunity to obtain a “first mover advantage” because of the sheer size of the

industry they are trying to enter. This is due to the small amount of room for

innovation in the restaurant industry. Finally, new entrants must be ready to deal

with the heavy regulation of the industry. Food safety, alcohol regulations, and

employee regulations can be costly to these start-ups.

The threat of substitute products in the restaurant industry is low. While it

may be more cost efficient for households to eat at home, many will simply

choose the ease of dining out over preparing meals at home.

The consumer base for the restaurant industry has significant bargaining

power over the companies we are analyzing. Customers have many options and

will choose to take their business elsewhere if a company is not meeting high

standards in quality at a bargain price.

Companies in this industry have bargaining power over their suppliers.

The companies we are analyzing all have a core group of suppliers that provide a

majority of their raw goods, but they also have a secondary network of suppliers

in place in the event of a shortage. The wide range of options to supply goods

allows firms in the restaurant industry to demand low prices from their suppliers.

Overall the restaurant industry is very competitive. By researching

disclosures by the firms in our sample industry, we have determined several Key

Success Factors for these companies. These KSFs are efficiency (cost

leadership), differentiation from other companies through superior quality and

variety, and brand image.

10

Accounting Analysis

In addition to looking at the nature of the restaurant industry, we have

also analyzed the accounting practices of Texas Roadhouse. This is necessary

because the degree of flexibility allowed in reporting by GAAP can lead a

company’s financial statements to be misleading. Firms that do not have a

credible amount of disclosure can be difficult to value because investors are

unable to see where value is being created. By evaluating their disclosure

regarding Type 1 (related to the KSFs identified above) and Type 2 (potentially

distortive) accounting policies, we have determined which areas of Texas

Roadhouses corporate structure could be misleading.

Type 1 policies, for Texas Roadhouse, cover disclosures regarding

economies of scale, product quality, and brand image. We have analyzed Texas

Roadhouse’s disclosures about their KSFs and found that they disclose

information at or above the level of the other companies in our sample industry.

Texas Roadhouse’s Type 2 accounting policies include disclosure about

their operating/capital lease structure, and goodwill. These items in their

financials are accounted for with a high degree of flexibility and were identified

as potential red flags.

Texas Roadhouse categorizes a majority of their leases as operating

leases. Because the off the book nature of these leases changes the structure of

Texas Roadhouse’s financials, we have capitalized them and provided restated

financial statements later in this report, allowing for a more accurate view of the

financial standing of the company.

Goodwill is an asset that is usually improperly impaired, causing

companies to overstate their assets and understate their expenses. We have

determined that Texas Roadhouse has not properly impaired their goodwill, so

we have also restated this on the restated financial statements provided.

Through our analysis, we have determined that Texas Roadhouse’s

disclosure in not extensive enough to provide accurate information for a

11

valuation. Because of this, we will restate the financials for this company to

account for the potential red flags we have identified.

Financial Analysis

After conducting the analysis of Texas Roadhouse’s accounting policies,

we began our financial analysis. The first step in the process was to use ratio

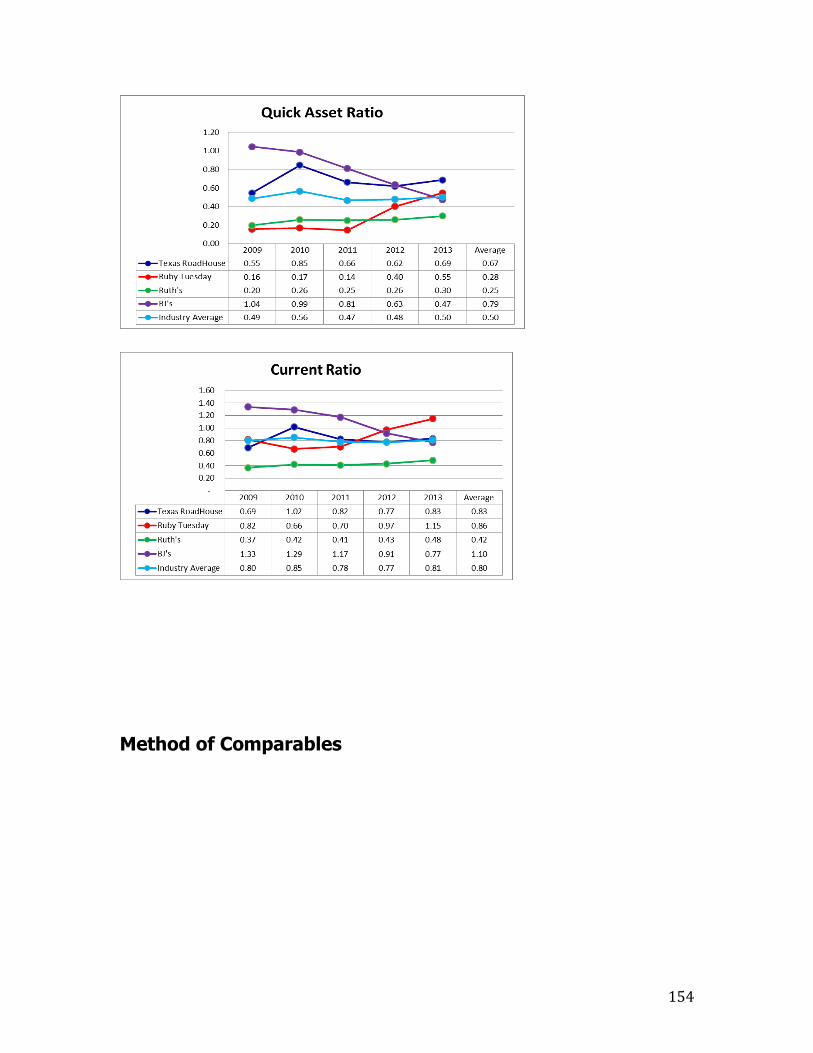

analysis to gain a better understanding of Texas Roadhouse’s liquidity, capital

structure, and profitability. The liquidity ratios we used are the current ratio,

quick ratio, inventory turnover, accounts receivable turnover, accounts receivable

days, cash to cash cycle, and working capital turnover. These ratios show a

firm’s ability to pay their short-term obligations, so a higher level of liquidity is

considered to show a better short-term financial standing. Below, Texas

Roadhouse is compared relative to the ratios for the other firms in our sample

industry.

12

After the liquidity ratios, we analyzed Texas Roadhouse’s profitability by

looking at sales growth, gross profit margin, operating profit margin, net profit

margin, asset turnover, return on assets, and return on equity. These ratios

show the ability of Texas Roadhouse to transform sales revenue to profit. In the

ratio analysis section of this report, we show Texas Roadhouse relative to the

other sample firms we selected. After looking at the profitability ratios, we can

conclude that Texas Roadhouse is performing at or above the level of the other

firms in our sample industry.

Analyzing the capital structure ratios for Texas Roadhouse allows us to

see how Texas Roadhouse finances their operating and investing activities. The

ratios we used are debt to equity, times interest earned, and Altman’s Z-score.

Banks and investors use Altman’s Z-score to determine a company’s likelihood of

declaring bankruptcy. Compared to the other benchmark companies, Texas

Roadhouse shows no real concerns in their capital structure ratios. Even after

financial re-statements, this company still competes on a number basis fairly well

against the competition.

13

After conducting the ratio analysis, we were able to forecast Texas

Roadhouse’s financial statements for the next 10 years. Although no forecast can

be perfect, we believe that our forecast is reasonably accurate. After determining

the forward trend of the sales growth rate by looking at the trend for Texas

Roadhouse and considering the different factors influencing the industry, we

forecasted the rest of the income statement using ratio analysis and taking past

performance into consideration. For balance sheet purposes, we used the asset

turnover ratio to calculate asset values relative to sales. Because we are valuing

the equity of Texas Roadhouse, little weight was given to the liabilities and the

remainder of our focus for the balance sheet was spent on accurately forecasting

equity. We also forecasted the statement of cash flows, but this is a very volatile

and hard to predict financial statement. Therefore, this forecast can be expected

to be less accurate than the income statement and balance sheet. All of our

forecasts took into account the restatement of Texas Roadhouse’s goodwill and

operating leases.

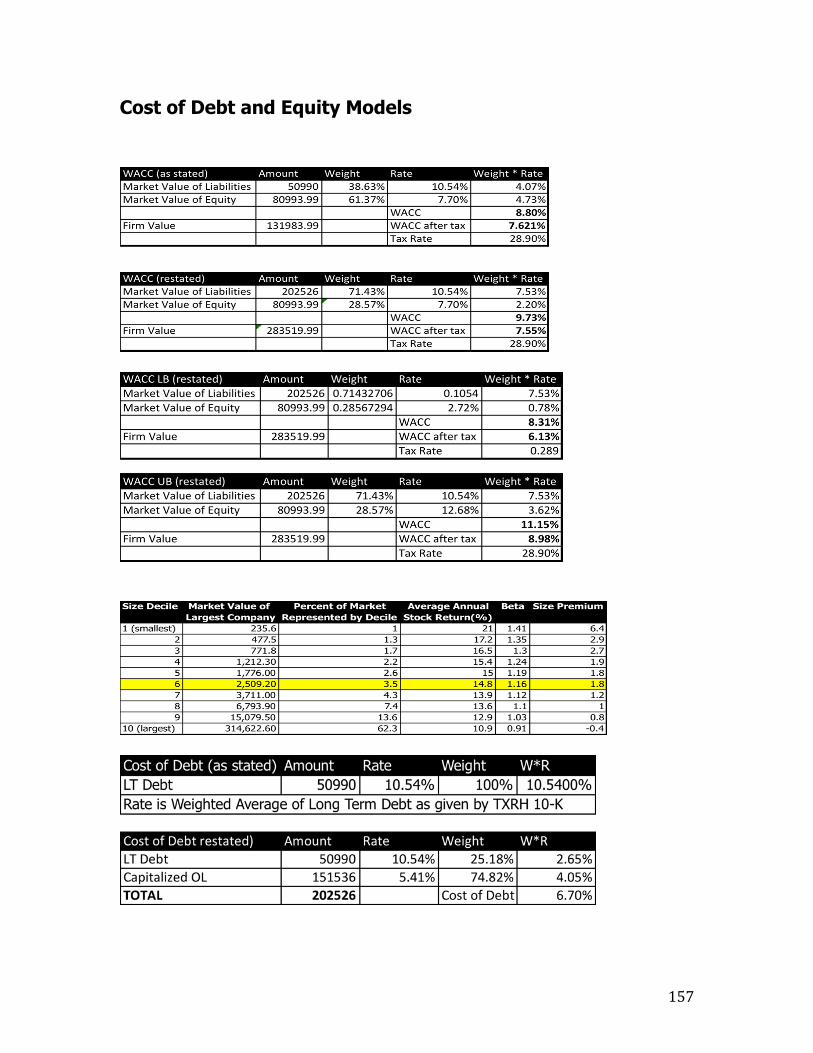

The final step of our financial analysis was to calculate Texas Roadhouse’s

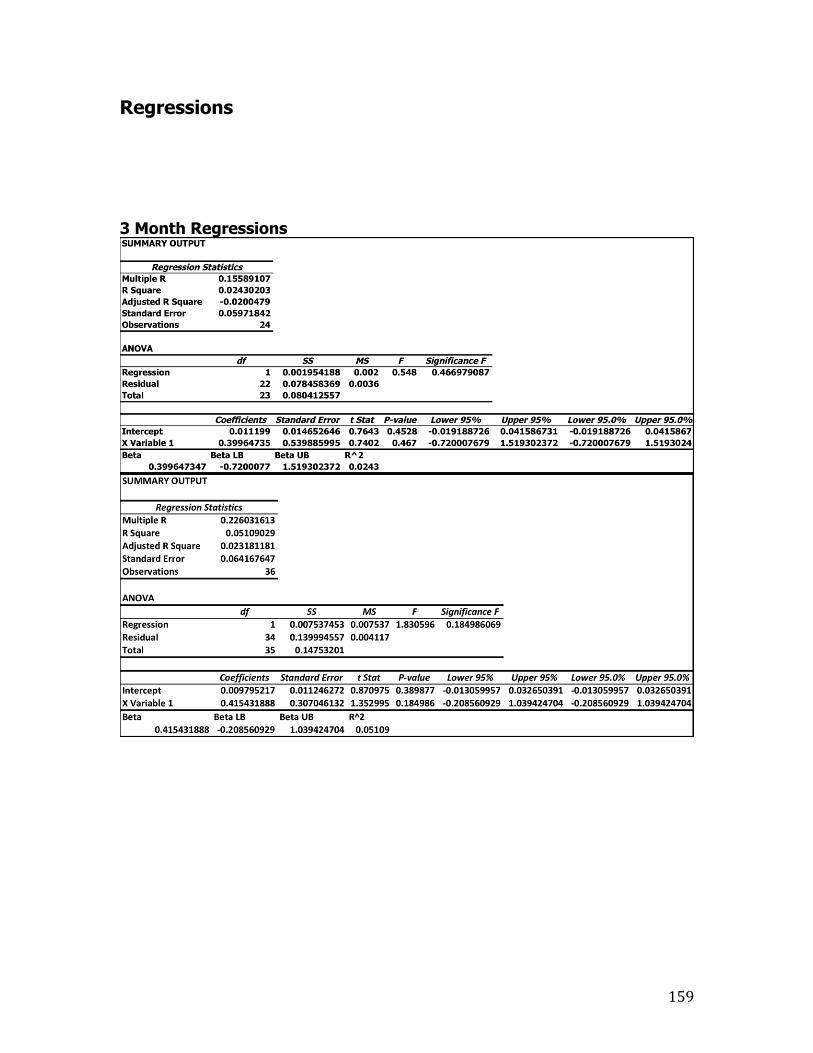

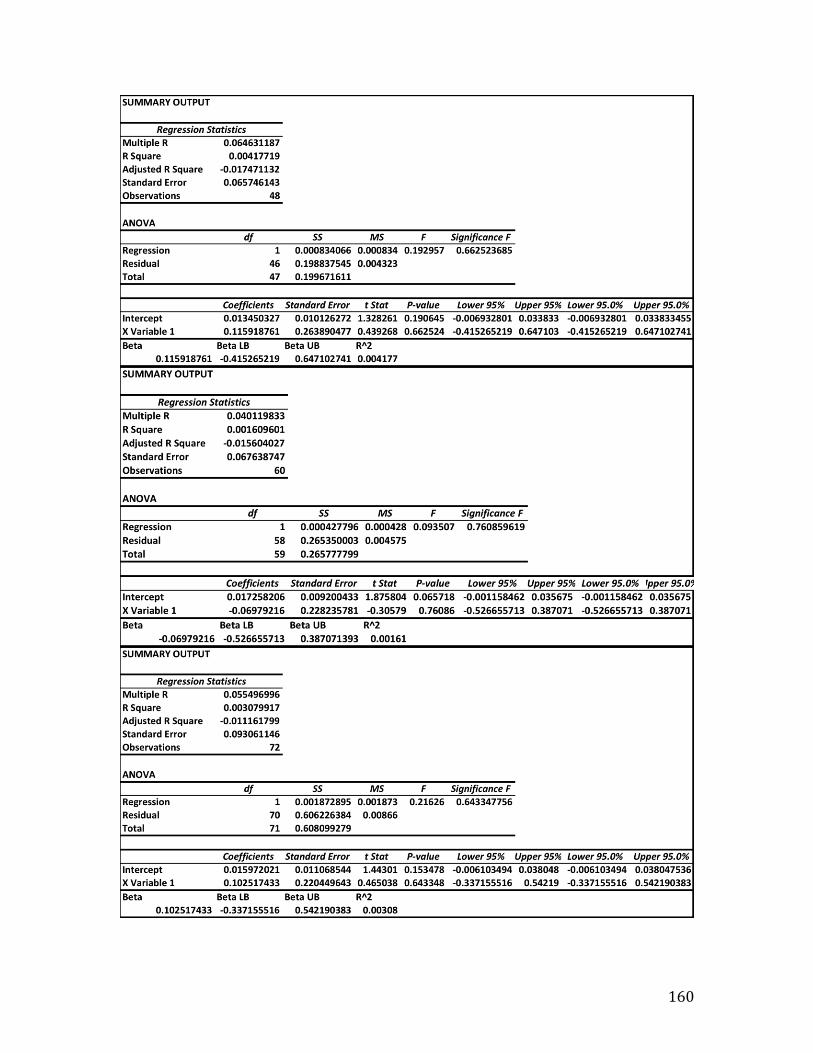

cost of capital. Through regression analysis, we were able to estimate a beta for

Texas Roadhouse at different points on the yield curve and at different points in

time. We chose the beta with the highest R2 statistic (a measure of statistical

relevance), which was the 7 year, 36 month regression. Using a beta of .417, we

14

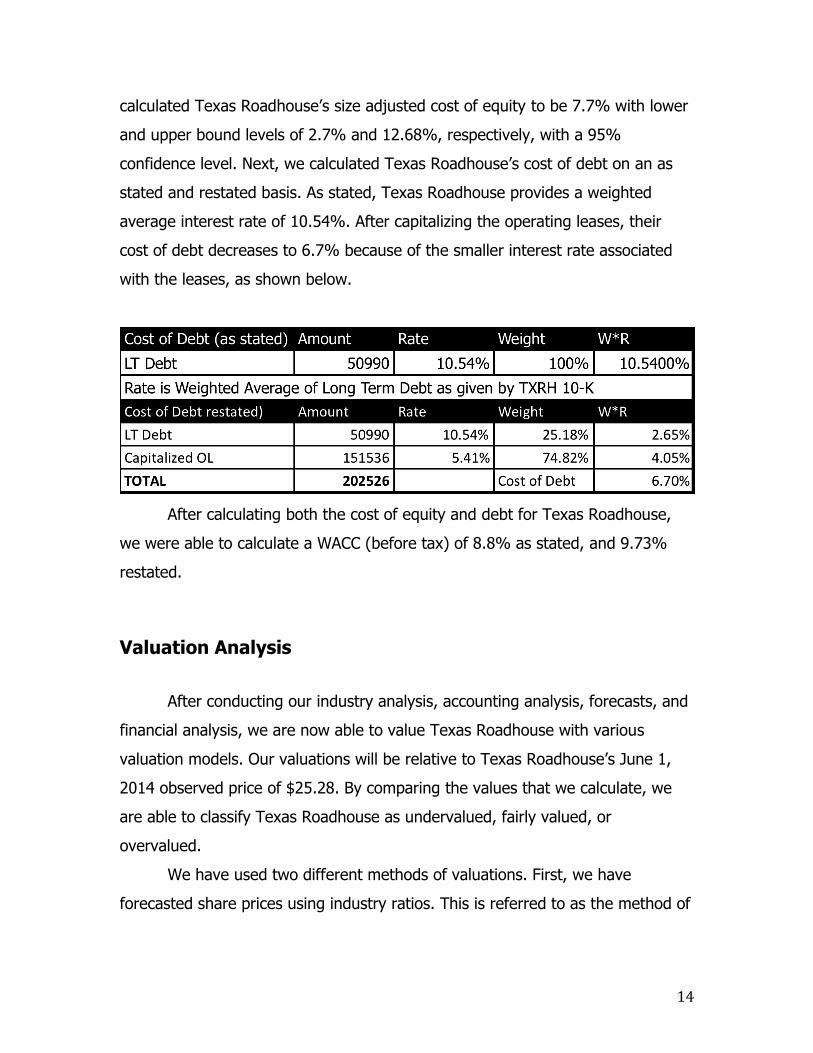

calculated Texas Roadhouse’s size adjusted cost of equity to be 7.7% with lower

and upper bound levels of 2.7% and 12.68%, respectively, with a 95%

confidence level. Next, we calculated Texas Roadhouse’s cost of debt on an as

stated and restated basis. As stated, Texas Roadhouse provides a weighted

average interest rate of 10.54%. After capitalizing the operating leases, their

cost of debt decreases to 6.7% because of the smaller interest rate associated

with the leases, as shown below.

After calculating both the cost of equity and debt for Texas Roadhouse,

we were able to calculate a WACC (before tax) of 8.8% as stated, and 9.73%

restated.

Valuation Analysis

After conducting our industry analysis, accounting analysis, forecasts, and

financial analysis, we are now able to value Texas Roadhouse with various

valuation models. Our valuations will be relative to Texas Roadhouse’s June 1,

2014 observed price of $25.28. By comparing the values that we calculate, we

are able to classify Texas Roadhouse as undervalued, fairly valued, or

overvalued.

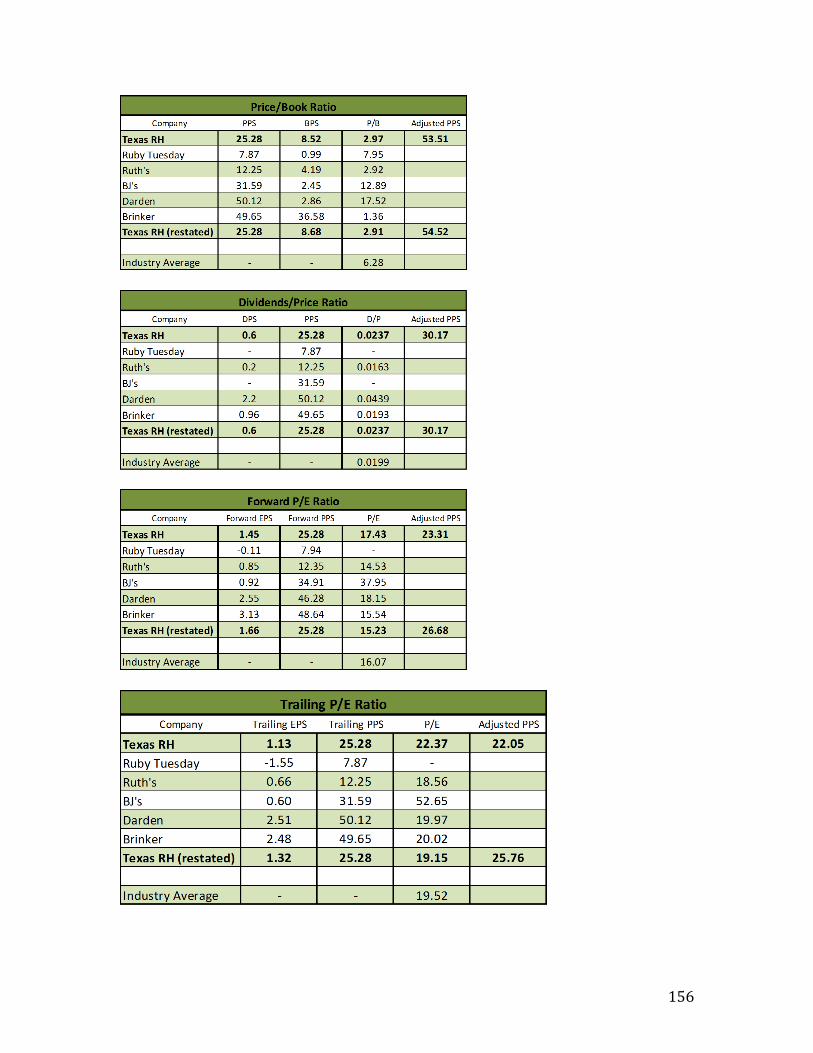

We have used two different methods of valuations. First, we have

forecasted share prices using industry ratios. This is referred to as the method of

15

comparables. Because of the simple nature of ratio analysis as a valuation tool,

this method does not carry as much weight as our intrinsic valuation method.

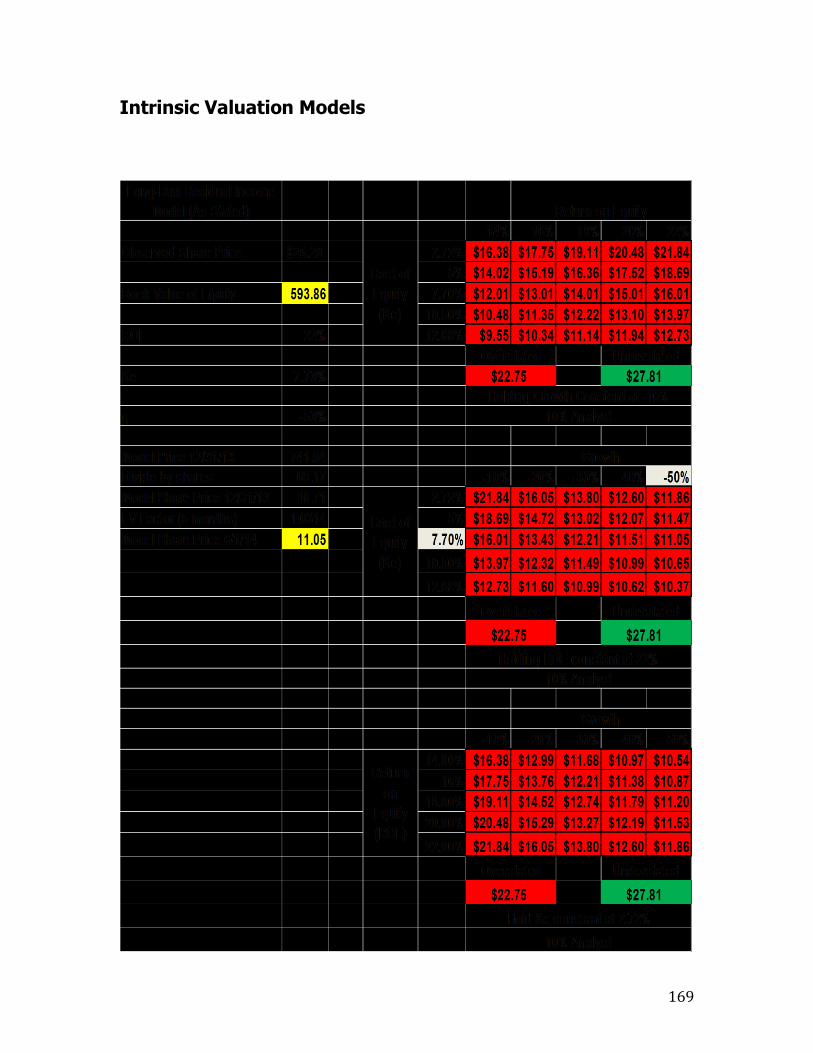

The intrinsic value methods used to value Texas Roadhouse use the

forecasted financials we have calculated and provide a value of the company

based on internal information, rather than industry standards. The models we

have used to value Texas Roadhouse are the discounted dividend model, free

cash flow model, residual income model, and the long run residual income

model. Compared to the industry ratio analysis valuation method, intrinsic value

models are significantly more reliable. Our valuation places the most weight on

discounted dividend model, residual income model, and long run residual income

model because of the unreliable nature of forecasted cash flows. By using these

models and allowing a 10% cushion of fair value, we are able to come to the

conclusion that Texas Roadhouse is overvalued.

16

Company Overview

Opening in Clarksville, Indiana in 1993, Texas Roadhouse is designed to

offer a casual dinning experience to “hometown consumers seeking high quality,

affordable meals served with friendly, attentive service”(2). The company

currently operates in 48 states and 3 foreign countries with 346 Corporately

owned restaurants with an additional 74 franchises (2). Texas Roadhouse is a full

service restaurant known for its specialty seasoned and aged steaks, which are

hand-cut daily on site and cooked to order on an open gas-fired grill.

Additionally, TXRH offers guests a selection of ribs, fish, seafood, chicken, pork

chops, pulled pork ad vegetable plates, hamburgers, salads, and sandwiches (2).

A kids menu is available for children 12 & under. Lastly, guests are offered an

unlimited supply of roasted in-shell peanuts and yeast rolls which are made from

scratch (2). This variety of a menu is a critical asset to TXRH because consumers

have a variety of choices, which appeases big groups and families, as well as the

female demographic.

Entrée’s range from $8.99 - $24.99, with at least 15 meals priced under

$10.00 (2). Main items include the specialty and seasoned steaks including

6,8,11, and 16 oz. Sirloins; 10, 12, and 16 oz. Rib-eyes; 6 and 8 oz. Filets; New

York Strip; Prime Rib; and our Porterhouse T-Bone (2). These items are TXRH

showcase items in which the restaurant regularly pushes to sale. TXRH has

maintained a consistent menu over time with about 60 entrees and 90 total

menu items. Extensive studies on operational and economic implications are

conducted and considered in feedback when selecting new, and removing old,

items from the menu.

Most of TXRH restaurants feature a full bar with an extensive selection of

draft and bottle beer, major liquor brands, and specialty margaritas. Managing

partners are encouraged to stock local brewery’s and distillers in their inventory.

TXRH doesn’t push the bar atmosphere but instead a family friendly

17

environment, and consequently, alcohol sales accounted for only 11% of sales in

2013(2).

Site Selection is a volatile characteristic in which TXRH spends significant

time and resources in the evaluation process of selecting sites for future

restaurants. Evaluation key points include market demographics, population

density, household income levels, as well as site specific traits such as visibility,

accessibility, traffic generators, proximity to other retail activities, traffic counts,

and parking (2). By spending significant resources towards the selection of sites

for potential TXRH sites, the company sets the restaurant up for success by

placing locations in high traffic areas of towns where visibility, accessibility, and

customer volume is high.

To succeed in the highly competitive restaurant industry against

competitors such as BJ’s, Ruby Tuesdays, and Ruth’s Steakhouse, TXRH strives

to provide an exceptional quality product with a casual, but attentive, dining

experience.

Industry Overview

TXRH is in the fast growing, but highly competitive restaurant industry,

which is expected to reach 683.4 Billion in industry sales in 2014. This 3.6%

growth since last year is only expected to continue throughout the foreseeable

future. With over 990,000 restaurant locations in the United States, the

restaurant industry employs over 13.5 Million workers, which is about 10% of the

entire workforce in the U.S.. Specifically, Texas ranks number 2 in fastest

restaurant job growth rate projections for the next decade at 15.3%. (9) This

industry has almost tripled since 1990, and will continue to be a dominant source

of employment and GDP in the future.

18

Below is a graph of the restaurant industry sales over the past 4 decades,

a performance index from 04/2013 – 04/2014, and a growth analysis for 2014

19

20

The Restaurant Performance Index is a monthly index that tracks the

health and the overall outlook for the U.S. restaurant industry. The RPI consists

of 2 different components including the Current Situation Index and the

Expectations Index. The Current Situation Index measures the current trends in

4 industry indicators (same-store sales, traffic, labor and capital market

expenditures). The Expectation Index Measures restaurant operators’ six-month

outlook in 4 industry indicators (same-store sales, employees, capital

expenditures, and business conditions)

The companies that we have chosen to represent the overall market are

Ruby Tuesday’s, BJ’s Restaurant and Brewhouse, and Ruth’s hospitality group.

21

Five Forces Model

The five forces model is a tool for estimating profitability of a firm by

using “five forces” to interpret the intensity of competition (1). This model is a

step towards valuing a firm’s worth and determining if that firm’s stock prices are

set at the right price. The five forces that drive this model are rivalry among

existing firms, Threat of new entrants, threat of substitute products, bargaining

power of consumers, and bargaining power of suppliers. These five elements will

allow us to gather a strong understanding of the industry’s weaknesses and

strengths, while also explaining the industry’s profitability as a whole. There are

three levels of competition that can exist in an industry: high competition, low

competition, or mixed competition. All parts of the five forces model is

categorized into high, low, or mixed competition in order to understand whether

your industry is a cost leadership or differentiated industry.

Texas Roadhouse, Inc. Level of Competition

Rivalry among Existing

Firms

High

Threat of New Entrants Mixed

Threat of Substitute

Products

Low

Bargaining Power of

Consumers

High-Mixed

Bargaining Power of

Supplies

Low

22

Rivalry among Existing Firms

Rivalry among firms in the restaurant industry exists because of changes

of demand and supply in the market. When demand is high, firms in the

restaurant industry avoid competing against each other, but when demand is low

competition over customers occurs and consequently the firms must adapt their

promotions, deals, and lowering their overall prices on goods.

The companies that we decided to use to represent the overall market are

Ruby Tuesday’s, BJ’s Restaurant and Brewhouse, and Ruth’s Hospitality Group,

along with the company we are valuing, Texas Roadhouse. We chose these

companies to represent the overall market mainly because of their common

ground in market share, niche type, profit margin, and growth rate. The

important components that we will analyze to gain an understanding of the

rivalry in the restaurant industry are growth rate, concentration, differentiation,

switching costs, scale of economy/learning curve, fixed-variable costs, excess

capacity, and exit barriers.

Industry Growth Rate Industry growth rate is something that averages the growth of all the

companies in a certain industry, like the restaurant industry for example. To

maintain growth in the restaurant industry many companies have adapted their

menus, prices, overall demeanor, etc. to the consumer demand. For example,

Texas Roadhouse spends extreme amounts of time training their managers and

partners to be able to run their franchises and restaurants in a way that

increases Texas Roadhouse’s competitive advantage and ability to grow as a

company. Another example of attempt to maintain growth by companies in the

restaurant industry is Ruby Tuesday’s initiative to increase their brand value by

changing menu items to reach a larger segment of customers while also

23

attempting to reduce the debt on their balance sheet by refinancing and

extending some of their contracts on property.

Depending on whether industry growth rate is high or low market share

becomes a very important component as well, causing competitors to either steal

share from other competing companies or grow internally. The companies in the

restaurant industry steal market share from each other consistently over time by

obtaining ideal business locations, which are difficult to find. All of the companies

we chose to represent the restaurant industry are franchising companies, which

allow them to sell their branding to an individual or group, for fees, royalties, and

increased growth.

Franchising can be a very important tool to help with a company’s growth

while leaving the care of the facility itself to another individual. This year will be

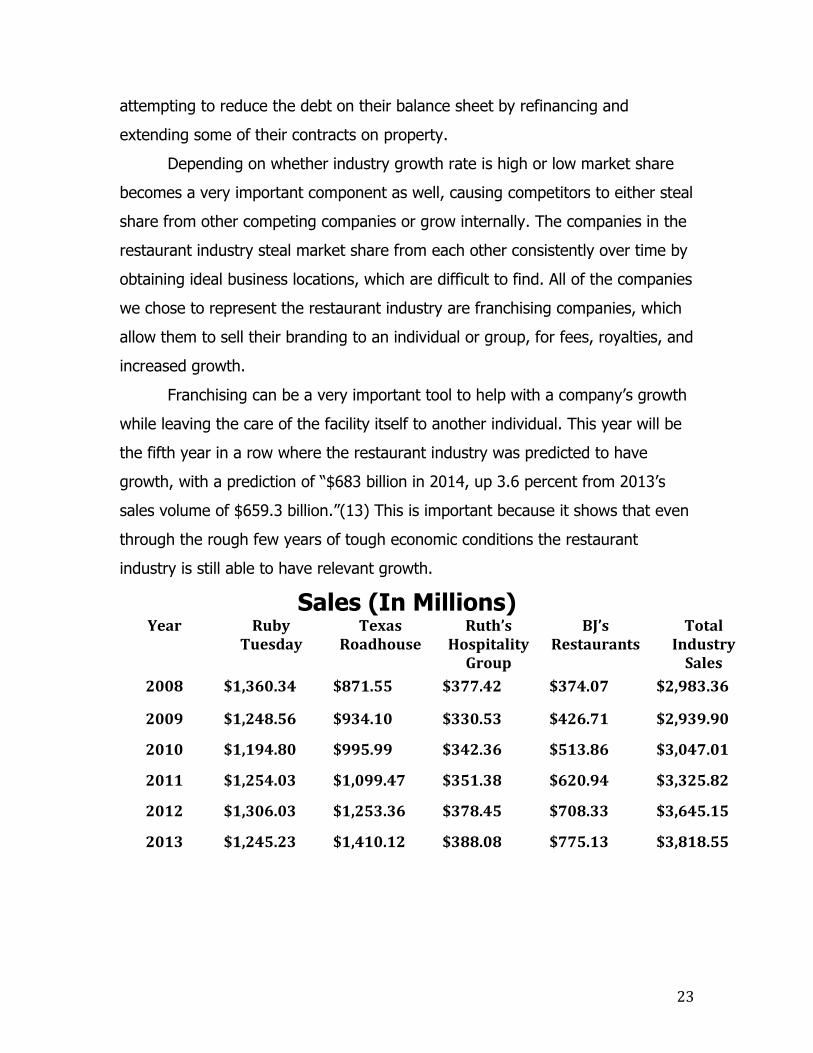

the fifth year in a row where the restaurant industry was predicted to have

growth, with a prediction of “$683 billion in 2014, up 3.6 percent from 2013’s

sales volume of $659.3 billion.”(13) This is important because it shows that even

through the rough few years of tough economic conditions the restaurant

industry is still able to have relevant growth.

Sales (In Millions) Year Ruby

Tuesday Texas

Roadhouse Ruth’s

Hospitality Group

BJ’s Restaurants

Total Industry

Sales

2008 $1,360.34 $871.55 $377.42 $374.07 $2,983.36

2009 $1,248.56 $934.10 $330.53 $426.71 $2,939.90

2010 $1,194.80 $995.99 $342.36 $513.86 $3,047.01

2011 $1,254.03 $1,099.47 $351.38 $620.94 $3,325.82

2012 $1,306.03 $1,253.36 $378.45 $708.33 $3,645.15

2013 $1,245.23 $1,410.12 $388.08 $775.13 $3,818.55

24

Annual Percent Change in Sales

When comparing the sample firms, the graph shows which firms have

higher potential for continued growth, like Texas Roadhouse, and which

companies are hitting a mature stage in their time line where growth is at a

plateau, like Ruby Tuesday. Even though there is continued growth throughout

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2008 2009 2010 2011 2012 2013

Ruby Tuesday

Texas Roadhouse, Inc.

Ruth's Hospitality Group, Inc.

Bj's Restaurants, Inc.

Ruby Tuesday Texas Roadhouse, Inc. Ruth's Hospitality Group, Inc. Bj's Restaurants, Inc. Total Industry Sales

2009 -8.21% 7.18% -12.42% 14.07% -1.46%

2010 -4.31% 6.63% 3.58% 20.42% 3.64%

2011 4.96% 10.39% 2.63% 20.84% 9.15%

2012 4.15% 13.91% 7.70% 14.07% 9.60%

2013 -4.66% 12.60% 2.55% 9.43% 4.76%

25

the years for the sample as a whole, the growth rate seems to have decreased

over the past two year. We believe Texas Roadhouse’s increased revenue has

been attributed to by the constant increase in number of stores, which has been

around an average of 25 each year, and the additional sales from existing

franchise owners. (2) Ruby Tuesday’s stunted growth is caused by the difficulty

of continuing to put up more restaurants to maintain a continuing stream of

growth in sales and the extinguishing of already owned properties over the past

couple of years.

The lack of growth from Ruby Tuesday and Ruth’s compared to BJ’s and

Texas Roadhouse is also because of the difference of casual dining market

compared to upper scale casual dining market. The difference in sales between

casual and upper scale casual restaurants has increased over the past years

because of the consumer idea of finding a better bargain.

Concentration The restaurant industry is a very competitive and intense setting for most

businesses, where new competition is always a strong possibility and battles over

possible new business sites and customers is constant. The restaurant industry

itself has some very large players such as Ruby Tuesday, who have over 700

restaurants active throughout the world. (3) These large players cause many

attempts by new firms to enter the restaurant industry to fall short and fail, so

even though it is somewhat easy to enter the industry itself the large players in

the industry tend to create a high failure rate of new restaurant companies.

Keeping new competitors out of the industry requires the willingness to

undercut on prices even when not undercutting on any quality of product, so

price competition is still pretty stiff even though the industry is run by big players

for the most part. Even with the big players controlling most of the market,

smaller companies every once in a while establish themselves in an effective

manner allowing them to maintain themselves in the industry. These new firms

26

can pose a threat to the existing firm’s market share and give customers another

choice when it comes to the already very competitive restaurant industry. Below

is a graph of the market share of each firm in the sample used to represent the

industry.

Market Share (Sales)

In terms of market share of the sample Ruby Tuesday and Texas

Roadhouse contain most of the market share, where Ruby Tuesday is losing

share and Texas Roadhouse is gaining share. The main reason for both Ruby

Tuesday and Texas Roadhouse having more market share than Bj’s and Ruth’s is

because of their larger number of restaurants.

As the years progress Texas Roadhouse’s gains of market share are

contributed to by the increase of restaurants being opened yearly, while the

discontinuing of restaurants contributes to the loss of market share by Ruby

Tuesday. Ruth’s, being an intensely more upscale causal restaurant, has a harder

time gathering market share because they put so much more money into the

preparation of their restaurants. BJ’s, being like Texas Roadhouse, has a steady

growth rate from putting up new restaurants at an average rate of 14

restaurants per year. (5) As demonstrated by the recent information, market

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

2009 2010 2011 2012 2013

Ruby Tuesday

Texas Roadhouse, Inc.

Ruth's Hospitality Group, Inc.

Bj's Restaurants, Inc.

27

share is strongly influenced by the increase of new locations for the acting firm.

A firm intending to increase their concentration is completely influenced by

increasing locations and market share.

Differentiation In an industry, product differentiation can become a key part of expansion

and competitive advantage. Product differentiation is the ability of a firm to

differentiate their good and services from the rest of the firms in the same

market as them, in most cases, either based on price, quality, atmosphere, or

services. When a firm has little product difference the consumers it targets have

an option to go other firms with like products instead. Firms like Ruth’s

Hospitality Group depend on their more upscale food choices, whereas BJ’s

Brewhouse instead spends most of its resources giving its’ customers an

enjoyable service experience while still providing a relaxing and casual social

environment. (5, 4) Another example of differentiation is the way Texas

Roadhouse has its menu reviewed each year and adjusts it to customer opinions,

but also still only maintaining 60 menu items. (2) The intensity of the

competition in the restaurant industry causes product differentiation to be

important for a firm to attain leverage over their competitors, and a lack of it can

be detrimental to their success.

Switching Costs

Switching costs represent the cost of a company to go from one industry

to another industry. In the restaurant industry, if a company wants to switch

from one specific industry to a completely different industry they would have to

sell off almost all of their assets and have them completely replaced. All of the

cooking machinery, kitchens, dining areas, and other industry machinery cannot,

in most cases, be used for any other industry, so switching costs for the

28

restaurant industry can be very costly. It would be much cheaper for a company

to switch to another area in the same industry. An example would be, if a

company in the restaurant industry makes a switch to another section of the

restaurant industry such as a switch from serving in a casual setting to serving in

an upper casual setting. Since it is so expensive to switch out of the industry, the

industry itself becomes more competitive because no one can easily leave the

industry in a cost-worthy manner. The biggest risks for companies in this specific

industry is the dilution of available customers over the increasing number of

competitors and the ability of competitors to be able to switch into specific

industry niche markets in a cost conservative manner.

Learning and Scale Economies Learning and scale economies play an important part to almost every

industry because of the ability these two economies have in lowering production

costs over all. The learning economy boosts this competitive advantage inside

the restaurant industry by utilizing methods that allow for reduced waste with

resources, empowering employees, and overall increasing productivity to lower

costs. Meanwhile, when there are economies of scale, increasing the size of the

operation decreases the minimum average cost (8). In other words, the larger

the size of the production, the lower the average cost per unit will be.

Our benchmark companies utilize mainly intensive training for

management and team members as a means to increase the learning economies

in this industry. Training times can range anywhere from 7-17 weeks (2)(4)and

most of the firms have either third party training or specialized programs their

personnel can go through. Just from Ruby Tuesday’s most recent 10-K, we can

see they have at least three major training centers located around their HQ

because they believe “[their] emphasis on training and retaining high quality

restaurant managers is critical to [their] long-term success.” (2)Texas

29

RoadHouse is also willing to pay 550k on the average store on pre-opening

costs, which is consisted of mainly training and recruiting costs.

Because this industry does not revolve around low-skilled jobs that the

fast food industry needs, it makes sense that firm’s would need to invest time

and money in increasing the learning economy from training employees. Each

staff member is now an important asset that adds value, so we can conclude

that competition will arise in firms competing for quality workers.

In this industry, scale economies come into play by the amount of

restaurants each firm has opened and the total assets they have. The following

graph shows the assets of our selected key companies along with the industry

total.

We see here that the industry is growing slowly over the years, so this

means the individual firms are getting larger on average. Because the industry is

growing larger, the companies are able to open more stores which allow them to

grow even larger, provided they keep profits per store up. Below is another

graph that shows the number of stores each firm in the industry own for the past

five years.

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

2007 2008 2009 2010 2011 2012 2013

Total Assets

Texas RoadHouse

Ruth's Hospitality Group

BJ's Restaurants

RubyTuesday

Industry Assets

30

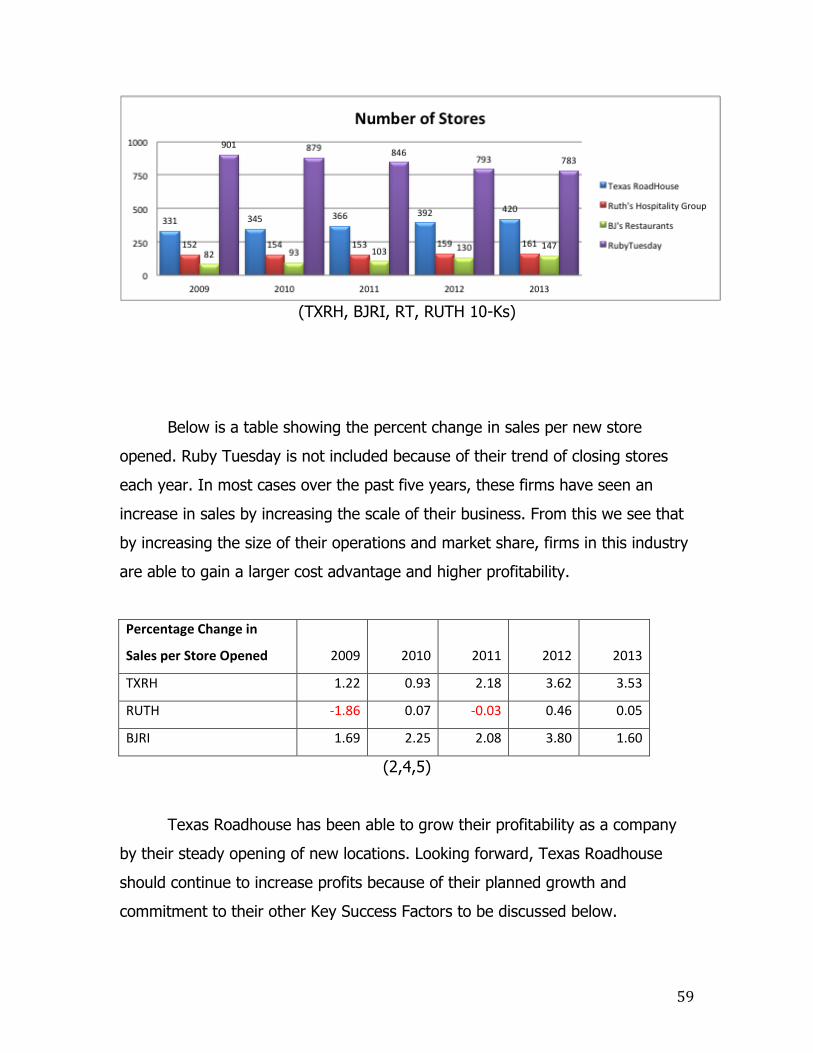

Looking at the above graph, all but Ruby Tuesday did well as far as

opening up new restaurants. Ruby Tuesday had to close a few stores due to

losing a lot of consumer base after the financial crises of 2008 and have been

trying to find new methods to get them back. In 2013, BJ’s sales increased over

$16 million, and they attribute that increase primarily due to the opening of 17

new restaurants during the year. They also stated that if [they] do not

successfully expand [their] restaurant operations, [their] growth rate and results

of operations would be adversely affected. So expanding all operations in this

industry is key to increasing sales.

Fixed – Variable Costs

Fixed to variable costs can show how volatile a firm might be. If a firm

has a high fixed to variable cost ratio, then that means that an increase in sales

would allow the firm to be able to have far more profit in that period as opposed

to having a lower ratio due to a greater reduction in cost per unit. However, a

decrease in sales with a high fixed-variable cost ratio would mean that the cost

per unit shoots up and the firm will struggle with covering the losses if it isn’t

able to cut fixed costs.

331 345 366 392 420

152 154 153 159 161 82 93 103 130 147

901 879 846 793 783

0

250

500

750

1000

2009 2010 2011 2012 2013

Number of Stores

Texas RoadHouse

Ruth's Hospitality Group

BJ's Restaurants

RubyTuesday

31

In this industry, the firms all have a high fixed-variable cost ratio as

shown below.

The firms here show almost a 3:1 ratio of fixed costs to variable costs

which would indicate that a slight increase to sales would allow this industry to

have incredible profits; however, this would also cause the firms to increase

competition because if too many mistakes were made, profits would plummet.

Selling, general, and administrative expenses, net increased $18.4 million

(15.3%) from the prior year for Ruby Tuesday (3) which contributed to higher

fixed costs and then sales also decreased 4.6% that period, causing the fixed-

variable ratio to increase and Ruby Tuesday took a 39 million dollar loss last

year.

We can easily see that this ratio could either make or break a firm for the

year, so our conclusion is that because there is so much risk in having a higher

fixed-variable cost, this will cause price wars amongst the industry. Firms that

are able to either sell more or cut down on fixed costs will come out on top, but

there is intense competition.

Excess Capacity

Excess capacity refers to the extra space in something that hasn’t yet

been filled. In the business world this can be a very dangerous thing, because if

there is something not being used, it’s costing the firm money. Companies might

cut costs to fill that excess capacity if the customer demand in the industry isn’t

as large as what could be produced. (1)

Fixed/Variable Ratio 2009 2010 2011 2012 2013

Texas RoadHouse 1.77 1.82 1.76 1.72 1.65

Ruth's Hospitality 2.47 2.26 2.15 2.08 2.08

BJ's Restaurants 2.82 2.84 2.79 2.80 2.92

Ruby Tuesday 2.60 2.25 2.27 2.45 2.65

32

In the restaurant industry where firms don’t make a lot of mass products

to fill orders whenever they want, excess capacity comes in other forms.

Whenever there is a lull in customer traffic into a restaurant, there is a lot of

potential production that isn’t being taken advantage of because there simply

aren’t enough customers, especially if the location doesn’t have many people

living around it. For this reason, the industry won’t order more food than it

absolutely needs because there is a good chance it will have too much than the

general population demands. In order to maximize operating efficiencies

between purchase and usage, each restaurant’s Executive Kitchen Manager

determines daily usage requirements for food ingredients, products and supplies

for their restaurant. (5)

A good measurement of the excess capacity we used is the sales per

square foot ratio, and compared this to the same measurement from previous

years. This describes how efficient the area of the entire restaurant floor for all

of the industry is. The more dollars there is per square foot, the less excess

capacity. Below is our table showing the ratio from each of our benchmark firms.

Sales/Square Foot 2009 2010 2011 2012 2013

Texas RoadHouse $397.47 $406.61 $423.10 $449.97 $472.88

Ruth's Hospitality $228.90 $234.01 $241.75 $250.54 $253.73

BJ's Restaurants $626.96 $665.71 $726.33 $656.46 $635.30

Ruby Tuesday $275.05 $269.83 $296.46 $329.39 $318.07

We see there is positive growth inside this industry as the years progress

in regards to getting rid of excess capacity. Each firm is able to utilize more and

more of their space, which lowers the competition just a little bit. However, the

rate of increase isn’t very high and is comparable to the current inflation rate of

2% (14). So in actuality, there hasn’t been much growth at all and competition

for more customers will stay high as the industry fights to rid its excess capacity.

33

Exit Barriers

Exit barriers keep firms from getting out of an industry due to the high

costs that might be required to leave. Exit barriers are high when the assets are

specialized or if there are regulations which make exit costly. (1) In some cases

in an industry, it might be hard to essentially liquidate to get out because of

highly specialized equipment or material. Most companies won’t find a use for

these kinds of things unless the industry is highly competitive. If a firm can’t get

out, its only option is to compete with others more to stay alive.

In the restaurant industry, however, the overall cost to exit would be low.

This overall is a highly competitive environment to where selling off the few

specialized assets wouldn’t pose too much of a problem, and the property itself

could be easily gutted and remodeled for any other business that wants to move

in. Therefore, we conclude that because of the low cost for the exit barriers, this

would not add too much more competition to the mix since it wouldn’t be too

hard to leave the industry.

Conclusion

For the rivalry among existing firms, we conclude that competition is

extremely high. Differentiation, switching cost, the fixed-variable cost ratio,

concentration, learning and scale economies, and excess capacity all add to the

intensity of the competition. Because of the high competition, there is little room

for mistakes as just a few could cause the firms to lose a lot of competitive

advantage and go under.

34

Threat of New Entrants

The threat of new entrants into the industry analyzes the potential

barriers to entry for firms seeking to begin operations on the scale of other firms

in the industry. Many factors play into the threat of new entrants including

economies of scale, first mover advantage, relationships with channels of

distribution, and legal barriers(1). Existing firms in the industry must keep these

potential new entrants in mind when making business decisions regarding their

ability to compete. If firms find that there are few barriers to enter a market,

they must work to maintain their market share and prevent a loss of profitability

to new firms.

Economies of Scale

An economy of scale occurs when a proportionate savings in cost is

generated by an increase in production. Economies of scale can apply to both

fixed and variable costs can be affected by the size of a firm entering the

industry(1). Firms looking to enter an industry must be able to begin operations

at the same level as their competition. As seen in the charts that follow, the

firms selected as a representative of the restaurant industry have between 147

and 783 stores currently open. In addition to this, the trend with the restaurants

(with the exception of Ruby Tuesday) is to continue opening stores and

extending the scale of their business.(2,3,4,5) New entrants to the industry will

be subject to a distinct cost advantage, at least at start up in comparison to the

large firms they hope to compete with. To effectively compete at the level of the

firms in our sample industry, new entrants must be able to effectively match the

scale of their competitors while also matching the quality of food and service

their customers desire.

35

In our sample of the restaurant industry, Texas Roadhouse is the second

largest firm in terms of stores in business at 420 company and franchise stores,

behind Ruby Tuesday at 783 company and franchise stores.(2,3) Ruth’s

Hospitality and BJ’s Restaurants Inc. are approximately the same size, but BJ’s

does not have any franchisee stores at this time.(5,4)

Because these firms operate on such a large scale, they have a cost

advantage achieved by their ability to buy in large quantities and establish long

and short-term relationships with their suppliers.

Restaurant Additions 2009 2010 2011 2012 2013

Texas RoadHouse 17 14 21 26 28

Ruth's Hospitality Group 15 2 -1 6 2

BJ's Restaurants 12 11 10 27 17

RubyTuesday -44 -22 -33 -53 -10

First Mover Advantage

The first movers in an industry have the advantage of being able to set

trends for the entire industry, have a cost advantage while other firms adjust to

the new trends, and even potentially create barriers to enter into the new area of

the market.(1)

A first mover advantage can be attained in the restaurant industry by site

selection. Below is the location breakdown for Texas Roadhouse. Texas

36

Roadhouse plans to continue expansion domestically and has franchising

contracts in place to develop restaurants in the Middle East.(2) Currently, Ruby

Tuesday is the only other firm in our sample industry conducting international

operations with 44 international franchises.(3) By having an international

presence, Ruby Tuesday and Texas Roadhouse have achieved a first mover

advantage and have the ability to set the trends for the restaurant industries in

those areas.

Similarly, new entrants have the ability to gain a first mover advantage by

following these strategies or by moving into new areas domestically.

37

38

Access to Channels of Distribution and Relationships

New entrants into an industry can be deterred by the difficulty and cost of

distribution. Existing competitors usually have contracts in place with distributors,

which can limit the options for a new entrant.(1)

In our sample industry, Texas Roadhouse, Ruby Tuesday and Ruth’s

Hospitality Group rely on two to three core suppliers to meet their needs

company wide.(2,3,4) BJ’s has an agreement with “a large consortium of large,

regional food distributors” in lieu of the type of agreements in place with the

other three firms.(5) Texas Roadhouse also has local agreements to purchase

products such as dairy and select produce in the interest of freshness.(2) Texas

Roadhouse and Ruth’s Hospitality Group also have a chain of secondary suppliers

in the event there is a shortage or failure to deliver with their primary

suppliers.(2,4)

Restaurants such as those included in our sample industry use their size

to negotiate better prices from their suppliers. They also have to take into

account the quality, freshness, and large-scale availability of the products to

insure their products consistently meet the standards set by the firms and their

customers. By negotiating long and short-term deals with suppliers, restaurants

in this industry work to maintain positive relationships with distribution sources.

These relationships ease the future negation process and are beneficial for firms,

distribution sources, and consumers.

Because of the difficulty of locating and negotiating distribution channels, new

entrants to the industry may be unable to begin business on a scale large

enough to compete with the firms in our sample industry and those like them.

Legal Barriers

Legal barriers to entry are regulations or legal ramifications that could

prevent potential new entrants to the industry.(1) The restaurant industry is

39

heavily regulated by federal, state, and local agencies. Restaurants are required

to obtain permits and licensing to cover food safety, alcohol service, regulations

such as OSHA, minimum wage requirements and alcohol service, which is the

most directly related to profits.(2,3,4,5)

Both Ruby Tuesday and Texas Roadhouse attribute approximately 11% of

yearly sales to alcoholic beverages (2,3), BJ’s attributes 22%(5), and Ruth’s

Hospitality Group does not disclose their alcoholic sales, although they do state

that wine makes up 61% of their beverage sales.(4) The regulation of alcohol

sales is stringent and approval to sell such beverages can be costly (Texas

Roadhouse accounts for up to $75,000 in alcohol permitting fees when opening a

new restaurant.)(2) Such an expense could pose serious limitations to firms

seeking to enter the market.

Even more regulated than alcohol sales, food safety is a top priority for

most regulations regarding the restaurant industry. While these are not as costly

pertaining to fees involved, properly training management and workers on how

to properly abide by the regulations can pose a significant cost as well.

Entrants to the industry wishing to compete at the same level as the firms

included in our sample industry as well as those like it will face significant

regulatory barriers to begin business operations. The cost of these regulations

and the level of difficulty involved in overcoming them may prove to be too much

for many potential entrants.

Conclusion

New entrants will find that in order to begin business operations at the

level of firms such as Texas Roadhouse, Ruby Tuesday, BJ’s, and Ruth’s

Hospitality Group, there are many barriers to entry. Existing competition has a

significant cost advantage because of the sheer size of their operations. Without

the benefits of lower cost, quality ingredients, new entrants may find it difficult

to compete with these firms.

40

Another difficulty facing new entrants to this industry is that there is

limited first mover advantage, leaving room for this advantage only in new

markets. In most cases, existing firms in an area have already been established

and have a reliable customer base, leaving little room for innovation and price

setting. In some cases, the attraction of a new business may help offset this

issue, but new entrants will find that their advantage as movers will not be

significant.

Distribution among existing firms is large scale and can cause limitations

for potential entrants. New entrants will have to negotiate contracts and try to

obtain cost advantages similar to those held firms already in business within the

industry because of their existing relationships. This will be the least difficult task

for new entrants, as there are many options for suppliers in the food service

industry.

The restaurant industry is heavily regulated. These regulations can be

difficult to adhere to, as well as expensive to undertake. If new entrants cannot

properly manage the heavily regulated aspects of the business, it will be very

difficult to become a major firm in this industry.

Overall, it is very difficult to grow to the size and market share of the

firms included in our sample of the industry and those like them. Many new

entrants would be more suited to being operations on a much smaller scale.

Firms that already have an established market share and customer base have a

significant advantage over new firms trying to enter the industry.

Threat of Substitutes

Threat of Substitutes is a risk the industry faces in its products or services.

Substitutes are not necessarily the same form as existing products, but

essentially perform the same function (1). Substitutes can come from a variety

of reasons including the utilization of technology that allow consumers to use

either less, or go completely without existing products (1).

41

Relative Price Performance

In the casual dining industry they’re 2 threats of substitutes, eating in,

and quick service restaurants. Both of these substitutions are of a completely

different, and lower price point in comparison to casual dining. Fast food

customers generally pay a price of $5 to $7 a meal, while cooking in cost people

on average $1.50 to $3.00 (16).

We believe this price differentiation is a low risk to casual dining

restaurants, in that, we believe that the experience in which is being offered by

the casual dining restaurants will overcome the price differentiation. We believe

that the ease of going out will outweigh the complications faced by eating in,

and that the experience of service and attentiveness will outweigh the cost

benefit of fast food.

Bargaining Power of Customers

The bargaining power of customers refers to the power that the consumer

has relative to price and options within the market. These pressures by the

consumer force restaurants to offer a unique experience at a great value. By

having a variety of choices and low switching cost, restaurants are at the mercy

of the consumer.

Differentiation

Differentiation refers to how close one product is to its competitors. For

example, in the television industry, there is little product differentiation between

the major competitors in the market. Each product, essentially, provides the

exact same service and function.

42

The casual dining industry is the complete opposite. Within the industry

there are unlimited different options to consumers not only in terms of types of

food, but also in preferential atmosphere. Sometimes, consumers can even walk

across the street and receive the exact same type of food, but with a different

Atmosphere.

Price Sensitivity

Consumers are always looking for a valuable experience at a great price.

Price sensitivity relates to how the consumer will act when prices are lowered or

raised. In the competitive restaurant industry, since there are very few switching

costs for consumers, restaurants must remain price competitive in order to keep

market share.

From High-end all the way down to a fast food drive through, the

consumer considers a variety of factors when deciding where to eat, rather than

just personal preference. Time and dress appropriateness are non-price sensitive

factors in deciding on the level of prestige that consumers care to entice in.

Consumers with a time constraint will move towards the casual to drive through

spectrum of eating out, while consumers with no time constraints and

appropriate attire will move towards the high-end to upper casual.

In order to compete with the extremely competitive casual dining

experience, along with the excessive amounts of steakhouse competition, TXRH

has competitively set prices against major competitors in the acceptable range in

terms of quality compared to price. TXRH offers a variety of price ranges for

entrees, which start at under $10 all the way up to $24.99(2), while Ruby

Tuesdays offers entrees from $7.49 to 19.49(4). BJ’s is also competitive in this

price range, with an average check of $11 to $17(5).

43

Number of Customers

One of the most critical parts of the restaurant industry is the number of

customers the restaurant serves. With an almost 100% customer base of people

who are willing to eat out, the competition to get these customers through the

door is immense. As the price of the meal goes down, the more customer base

the restaurant is going to have. Therefore, it is imperative to capture as much of

the market share as possible within the vast scale of casual dining restaurants

available to consumers.

Since the drop in traffic since 2008, the restaurant industry has slowly

started to grow back to its original normality. Traffic has increased by 8 percent

from 2012, but overall checks totals have only increased by 1 percent (11).

Economists predict this growth will maintain stable as the markets continue to

grow. Below is a graph of the change in customer traffic at Fast Casual and

Quick Service restaurants from 2009.

44

(8)

Conclusion Although the industry as a whole is growing, the power still remains with

the consumer. This price taking market must constantly offer consumers with a

valuable price or risk being easily replaced. The high competition in the industry

is the key factor, in that consumers can easily switch restaurants if it’s deemed

that the value being offered to them is more at a competitor.

Bargaining Power of Suppliers

The bargaining power of suppliers represents the ability of suppliers to

control the price and conditions of their contracts with firms that need materials

to do business. Suppliers tend to be powerful in this regard when there are few

companies in an industry and few substitute products for customers to choose

from. (9) In the restaurant industry there tends to be a lot of give and take when

45

it comes to suppliers, some restaurants have the ability to maintain the power in

their relationships with their suppliers, while others don’t have as much freedom

and maintain one or a few specific suppliers.

Switching Costs Switching costs, when applied between firm and supplier, is the cost of a

firm to switch from one supplier to another. Depending on the amount of

suppliers in an industry, the switching costs can be quite different. In the

restaurant industry there are a good amount of suppliers, but there are some

very big ones that maintain most of the market share in the restaurant supplying

industry, like Crisco. In most cases restaurants will make contracts with multiple

suppliers for different foods and materials in an attempt to gain the best deal.

Texas Roadhouse, Inc. gathers most of their meats from five different suppliers

under contracts, while most of its other materials are gathered locally to insure

freshness. (2) Ruby Tuesday has opt-out contracts with multiple suppliers and

secondary suppliers to insure their good are to the level that they designate at all

times. (3)

Differentiation

Product differentiation, when it comes to food material, is not much

different from supplier to supplier. Most suppliers have to compete with each

other on delivery time, price, and quality of service, which causes the restaurant

industry to have some power in their negotiations with the suppliers. This also

causes suppliers to maintain quality goods to be able to compete for business.

Restaurants like Texas Roadhouse, Ruby Tuesday, and Ruth’s all maintain

contracts with multiple suppliers for meats, dairy product, etc. in order to

maintain the quality of their products and keep the supplier prices at a

46

reasonable level. (3,1,4) Since restaurants have such a high expectation of

supplied goods even small differentiation is important.

Importance of Product for Costs and Quality

In the restaurant industry product cost and quality is very important for a

competing firm. For a firm to not have a product that is up to par with the given

standards can be very detrimental to their business and in some cases illegal.

This can be a problem for suppliers because of the consumer’s standards, “If any

major supplier or distributor is unable to meet our supply needs, we would

negotiate and enter into agreements with alternative providers to supply or

distribute products to our restaurants”, so suppliers have no room for error when

it comes to their goods quality and cost. (5) Restaurants have to attempt to get

quality products for the cheapest price possible, which can’t always happen in

most cases because of certain circumstances beyond anybody’s control. For

example, if a flood hit a farm in Texas and killed most of the crops prices would

raise from lack of supply in most cases. To avoid these problems most

restaurants join into short-term contracts with specific suppliers in order to lock

in specific prices.

Number of Suppliers There are many suppliers for the restaurant industry in the United States,

which causes a lot of competition for contracts between suppliers and firms.

Since there isn’t much difference from each supplier’s raw materials, most

suppliers have to compete with price and other competitive values like service.

The number of suppliers compared to the number of firms in the restaurant

industry is somewhat smaller than in other industries mainly because there are

large amounts of suppliers while at the same time there are also large amounts

of restaurant firms. Since switching costs are so low, restaurants are able to

47

look around when it comes to picking relevant suppliers to purchase materials

from. This causes suppliers to have a major disadvantage when it comes to

negotiating with the firms.

Conclusion By examining all of these factors, assessments can be made that the

bargaining power of suppliers in the restaurant industry is relatively weak as a

whole. Switching costs for firms is relatively low because of the large number of

suppliers for the restaurant industry. The differentiation of products from

supplier to supplier is largely similar, so price and service tends to determine

which supplier gets the business from the restaurant industry firms. The volume

of firms to suppliers is relatively even, which causes competition for reasonably

scarce consumers.

Classification of Industry

Based on our findings from the five forces model, we concluded that this

industry utilizes a mixed model of cost leadership and differentiation. However,

this industry is mainly focused on the cost leadership strategies rather than

differentiation, but does pick and choose a few differentiation techniques.

Analysis of Key Success Factors

Firms within any industry will either try to become a costing leader by

lowering costs whenever they can to beat out competitors prices, or by becoming

differentiated to the point where customers are easily able to see a clear

difference between the firms and attract people that way. We will see that in the

restaurant industry, firms use a mix of cost leadership strategies and

differentiation to try to maximize their sales each year.

48

Cost Leadership

Firms that achieve cost leadership focus on tight cost controls. (1) This

means that the firms that utilize a cost leadership strategy will try to cut down on

costs wherever they can. The restaurant industry is no exception to this idea.

They will compete with each other for this almost invaluable competitive

advantage by trying to minimize expenses across the board.

Economies of Scale Economies of scale we defined earlier is when a firm increases the size of

the operation, this ends up decreasing the minimum average cost (8) For an

industry focused on cost leadership, having a lower cost is extremely important,

and the economies of scale play an important part in aiding this.

In the restaurant industry, this comes into play once again by the amount

of stores the firm has open. The idea is that the bigger the firm, the more power

it will have to open up more stores, which in turn makes the firm bigger. Below

is a table that shows the number of new restaurants opened (closed) for the past

five years.

Restaurant Additions 2009 2010 2011 2012 2013

Texas RoadHouse 17 14 21 26 28

Ruth's Hospitality

Group 15 2 (1) 6 2

BJ's Restaurants 12 11 10 27 17

RubyTuesday (44) (22) (33) (53) (10)

49

Besides Ruby Tuesday, these firms opened quite a few new restaurants,

which significantly increased the size of them overall. The increase in size gives

them a huge competitive advantage over smaller companies, which allows them

to be able to expand even further, as long as the customer base is able to

support the firms.

Efficient Production

A firm that is able to have an efficient production is able to cut costs by

not having a very high waste, or by utilizing all the resources available to it,

whether that be time, money, or materials.

Firms in the restaurant industry have to be incredibly efficient because

food supplies can either be scarce, or go bad because some items are perishable.

Service can either take a lot of time per customer, or the lack of customers will

cause an overabundance of time due to a high excess capacity. There also have

to be wise investments that will ultimately create value to the firms, which goes

across the board for all industries, and is no exception here.

Because food is generally perishable unlike metals or plastics that other

industries might produce, wastes here can be very devastating and unintentional.

Because of the relatively short storage life of inventories, a minimum amount of

inventory is maintained at our restaurants. (3) Food also loses a lot of its weight

when it is washed, pruned of all defects, and cut into shape for consumption, so

firms have to hire highly qualified chefs and food handlers to not have as much

excess scraps. BJ’s has a theoretical food cost system and automated food prep

system to measure the amount of waste and their product yields, while

increasing kitchen efficiency. (5).

Time, depending on the amount of customers, can either be in extreme

excess or extreme shortage. When a restaurant is busy, customers will take

50

longer to serve because the waiting time is increased. Either there aren’t enough

seats available, or the staff is just overwhelmed and can’t serve everybody. Food

takes a long time to cook correctly, but if the customer is kept waiting too long,

they will clearly be unsatisfied and might get impatient, which will cause them to

down value everything else in the restaurant. Texas RoadHouse implements

some sort of process to reduce customer waiting times to combat this. (2)

Overall, an inefficient firm in this industry would not last very long. Firms

can’t afford to have much waste of anything because of the high fixed costs they

have to overcome each period. So if a firm can’t invest in itself to become more

efficient, it’s not worth investing in period.

Research and Development and Brand Advertising Having little to no research and development is key to a cost leadership

focused industry. R&D can be incredibly expensive, especially because non

specialized products are generally bought up. There isn’t too much benefit in

changing something that will sell anyways. As for brand advertising, firms

generally rely on their relationship of the public alone to promote themselves.

In this industry, most of the firms do not engage in research and

development, but instead conduct inexpensive studies. Ruby Tuesday for

example, [does] not engage in any material research and development activities.

However, [they] do engage in ongoing studies to assist with food and menu

development. (3) These types of activities help the firms to control costs and

lower overall expenses.

Brand advertising is something that all our benchmark companies engage

in, but expenses are generally very low (1-3% of total revenue) for each firm.

Most of the firms use other methods as a means to attract customers. Texas

RoadHouse utilizes public relations to generate "earned media" story placement

in local, regional and national media. (2) This means that most of Texas

RoadHouse’s advertising is done by the media for free.

51

With little to no research and development and very inexpensive

advertising campaigns, this segment shows us this industry is definitely using the

cost leadership idea here. This saves the restaurants millions of dollars each

year, and allows them to put money where they think would be a better

investment.

Differentiation

A firm that is trying to have a differentiation strategy must find ways to

become unique and stand out from their competitors. For differentiation to be

successful, a firm has to accomplish three things: First, it needs to identify one

or more attributes of a product or service that customer’s value. Second, it has

to position itself to meet the chosen customer need in a unique manner. Finally,

the firm has to achieve differentiation at a cost that is lower than the price the

customer is willing to pay for the differentiated product or service. (1)

Superior Product Quality Superior product quality is very important to any differentiating company.

Having a better product than the competitors adds a competitive advantage to

where customers would want what is better for the same price they could get

elsewhere. This comes at an extra cost as opposed to a cost leadership strategy,

but might be worth it to some industries.

In the restaurant industry, where customers go to sit down to enjoy a

meal, having a high quality product is very important. As opposed to fast food,

where customers expect to pay for something cheap just to sate their hunger,

people go to restaurants expecting so much better for a higher price because of

the environment a sit down restaurant has. For this reason, firms invest a lot in

creating the best product they can. Product quality is added by the quality of the

52

actual product itself, the service that comes with it, and how the entire thing is

presented.

Texas RoadHouse for example, hand-cuts all but one of [their] assortment

of steaks and make [their] sides from scratch. In other food industries, food is

shipped in frozen, then nuked in an microwave, oven, or fryer and is basically

served immediately straight from the package. Texas RoadHouse also has a

management level employee to inspect every entrée before it leaves the kitchen

to confirm it matches the guest's order and meets [their] standards for quality,

appearance and presentation. (2) Ruth’s Chris restaurants oversees a line check

system of quality control and must complete a quality assurance checklist

verifying the flavor, presentation and proper temperature of the food and

beverages. (4) BJ’s Executive Kitchen Manager is responsible for managing food

quality and preparation. These lead to the idea that every product must be

uniform, meaning that every meal must be the same so that customers receive

the same quality every time they order.

In this industry, having high quality food is essential to making sales. If

customers don’t feel like they are receiving the best quality for their money, then

they will simply go elsewhere. Therefore, it is wise to be willing to spend the

extra money on creating something superior to ultimately add value by having

yet another benefit to competitive advantage.

Superior Product Variety Most of the time in industries, creating more than one different types of

products can be incredibly expensive; however, in some industries, having more

variety will allow customers to feel like they are being treated more personally

and will be willing to pay a little bit more for some customization of their own.

Fortunately for the restaurant industry, adding more products to menus is

relatively inexpensive compared to adding entire new product lines in major

manufacturing industries. The excess costs come from training the employees

53

how to handle each and every product available to the customer, and the special

licensing costs that might be associated with the product itself like alcohol. Firms

like Ruth’s sells over 50 different items on their menus, and offer over 200

different selections of wine and even more selections of other alcoholic drinks.(4)

Texas RoadHouse also has well over 50 different customizable options on their

menu not including alcohol, and all four restaurants have an ever changing

menu. (2)

Although an expensive investment, BJ’s even has created its own brewery

that allows it to craft a wide variety of beer that you can’t buy anywhere else.

This has allowed BJ’s to add a 9% increase in sales for 2013 from their own

brewed beer alone. So because of this, we concluded that having a superior

product variety is incredibly value adding to this industry.

Investment in Brand Image Brand image is how the customers see the company and its product. This

is essentially the firm’s reputation in society and is aided by having uniformity

between stores. For the restaurant industry, this created by having the same

theme and atmosphere across all the stores in a firm. This adds value by

allowing the customer to feel a sense of the same quality and service they will

receive at any of the locations.

Substantially all Texas Roadhouse restaurants are of [their] prototype

design, reflecting a rustic southwestern lodge atmosphere, featuring an exterior

of rough-hewn cedar siding and corrugated metal. (2) Along with this, they have

jukeboxes and host line dancing inside their restaurants, and customers can

either wait in the lounge or go to the southwestern styled bar. (2) Restaurants

typically try to look and feel the same way wherever the customer might go.

They are willing to invest to try to achieve this idea of uniformity across the

board. According to a 2003 New York Times article, Ruby Tuesday budgets

$25,000 to $50,000 for up to 1,000 refurbished antiques it will use in a

54

restaurant, because when people go out, they want more than food; they want

visual stimulation. ''It is part of the entertainment of eating out,'' said Rick

Johnson. (15)

From this, we can conclude that restaurants value having a certain

ambiance about them, that the customers can relate to and associate themselves

with the brand image of the firm. This creates a certain immeasurable value that

causes the customer to want to return at a later date, increasing sales at each

store. If each restaurant can achieve uniformity with one another, then overall

sales will increase much more as customers travel and recognize something they

are already used to.

Conclusion In general, restaurants in this industry commonly use a mix between cost

leadership strategies, and differentiation strategies. Typically, these companies

will lean towards mainly the cost leadership side of business, but will have a little

influence from differentiation techniques.

Firms save a lot of money from the cost leadership side, mainly through

their efficient production to where wastes are kept at a minimum, and the entire