Embed Size (px)

Citation preview

VALUATIONTECHNIQUES

ffirs 12 September 2012; 17:36:29

CFA Institute Investment Perspectives Series is a thematically organized compilation ofhigh-quality content developed to address the needs of serious investment professionals. Thecontent builds on issues accepted by the profession in the CFA Institute Global Body ofInvestment Knowledge and explores less established concepts on the frontiers of investmentknowledge. These books tap into a vast store of knowledge of prominent thought leaders whohave focused their energies on solving complex problems facing the financial community.

CFA Institute is a global community of investment professionals dedicated to driving industry-wide adoption of the highest ethical and analytical standards. Through our programs,conferences, credentialing, and publications, CFA Institute leads industry thinking, helpingmembers of the investment community deepen their expertise. We believe that fair and effectivefinancial markets led by competent and ethically-centered professionals stimulate economicgrowth. Together—with our 110,000 members from around the world, including 100,000CFA charterholders—we are shaping an investment industry that serves the greater good.

www.cfainstitute.org

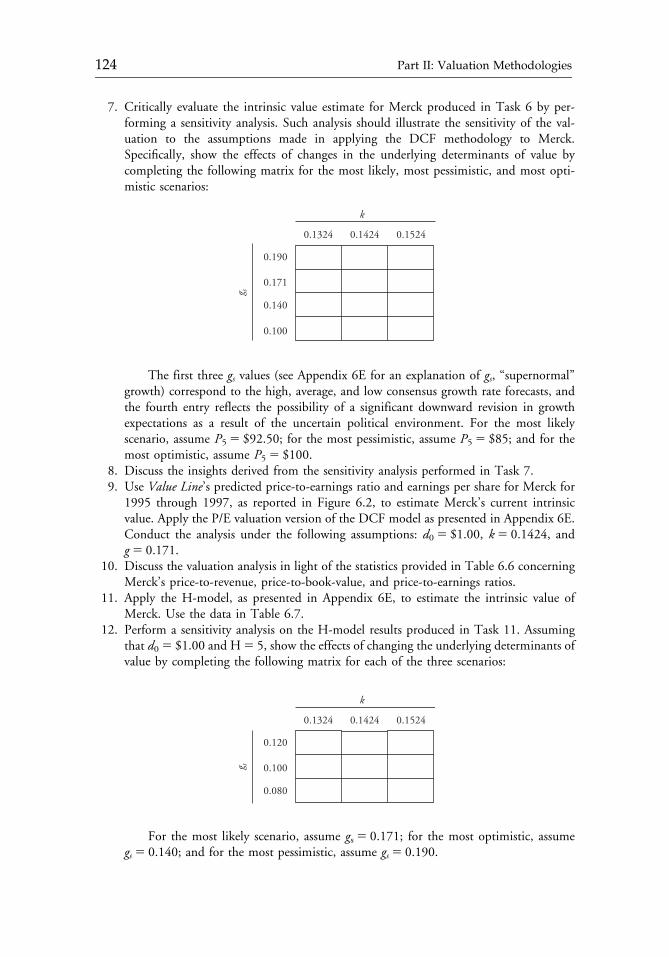

Research Foundation of CFA Institute is a not-for-profit organization established topromote the development and dissemination of relevant research for investment practitionersworldwide. Since 1965, the Research Foundation has emphasized research of practical value toinvestment professionals, while exploring new and challenging topics that provide a uniqueperspective in the rapidly evolving profession of investment management. To carry out itswork, the Research Foundation funds and publishes new research, supports the creation ofliterature reviews, sponsors workshops and seminars, and delivers online multimedia content.Recent efforts from the Research Foundation have addressed a wide array of topics, rangingfrom risk management to the equity risk premium.

www.cfainstitute.org/foundation

ffirs 12 September 2012; 17:36:29

VALUATIONTECHNIQUES

Discounted Cash Flow, Earnings Quality,Measures of Value Added, and Real Options

David T. Larrabee, CFAJason A. Voss, CFA

John Wiley & Sons, Inc.

ffirs 12 September 2012; 17:36:29

Cover Design: Loretta LeivaCover Photograph: ª Simon Belcher / Alamy

Copyright ª 2013 by CFA Institute. All rights reserved.

Published by John Wiley & Sons, Inc., Hoboken, New Jersey.Published simultaneously in Canada.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form orby any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except aspermitted under Section 107 or 108 of the 1976 United States Copyright Act, without either the priorwritten permission of the Publisher, or authorization through payment of the appropriate per-copy fee tothe Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers, MA 01923, (978) 750-8400,fax (978) 646-8600, or on the Web at www.copyright.com. Requests to the Publisher for permissionshould be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street,Hoboken, NJ 07030, (201) 748-6011, fax (201) 748-6008, or online at http://www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts inpreparing this book, they make no representations or warranties with respect to the accuracy orcompleteness of the contents of this book and specifically disclaim any implied warranties ofmerchantability or fitness for a particular purpose. No warranty may be created or extended by salesrepresentatives or written sales materials. The advice and strategies contained herein may not be suitablefor your situation. You should consult with a professional where appropriate. Neither the publisher norauthor shall be liable for any loss of profit or any other commercial damages, including but not limited tospecial, incidental, consequential, or other damages.

For general information on our other products and services or for technical support, please contact ourCustomer Care Department within the United States at (800) 762-2974, outside the United States at(317) 572-3993 or fax (317) 572-4002.

Wiley publishes in a variety of print and electronic formats and by print-on-demand. Some materialincluded with standard print versions of this book may not be included in e-books or in print-on-demand. If this book refers to media such as a CD or DVD that is not included in the version youpurchased, you may download this material at http://booksupport.wiley.com. For more informationabout Wiley products, visit www.wiley.com.

Library of Congress Cataloging-in-Publication Data:

Larrabee, David T.Valuation techniques : discounted cash flow, earnings quality, measures of value added, and

real options / David T. Larrabee and Jason A. Voss.p. cm. — (CFA Institute investment perspectives series)

Includes index.ISBN 978-1-118-39743-5 (cloth); ISBN 978-1-118-41760-7 (ebk);ISBN 978-1-118-42179-6 (ebk); ISBN 978-1-118-45017-8 (ebk)1. Corporations—Valuation. 2. Investment analysis. I. Voss, Jason Apollo. II. Title.

HG4028.V3L346 2013332.63 0221—dc23

2012022595

Printed in the United States of America

10 9 8 7 6 5 4 3 2 1

ffirs 12 September 2012; 17:36:29

CONTENTS

Foreword ix

Introduction 1

PART I: VALUATION PERSPECTIVES:THEN AND NOW 3

CHAPTER 1Two Illustrative Approaches to Formula Valuationsof Common Stocks 5Benjamin GrahamReprinted from the Financial Analysts Journal (November 1957):11�15.

CHAPTER 2Seeking a Margin of Safety and Valuation 17Matthew B. McLennan, CFAReprinted from CFA Institute Conference Proceedings Quarterly (June 2011):27�34.

PART II: VALUATION METHODOLOGIES 29

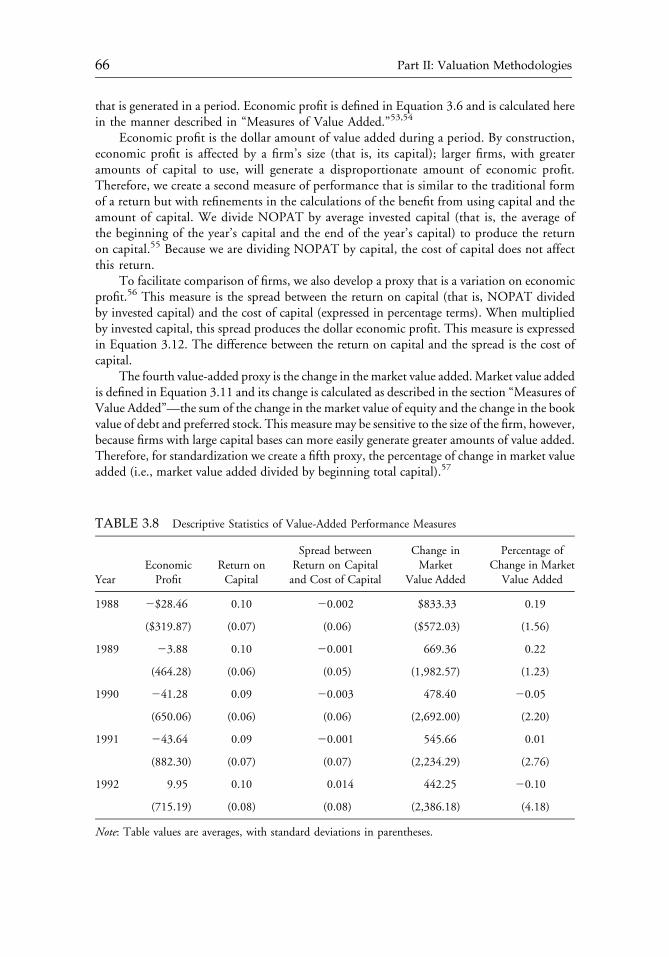

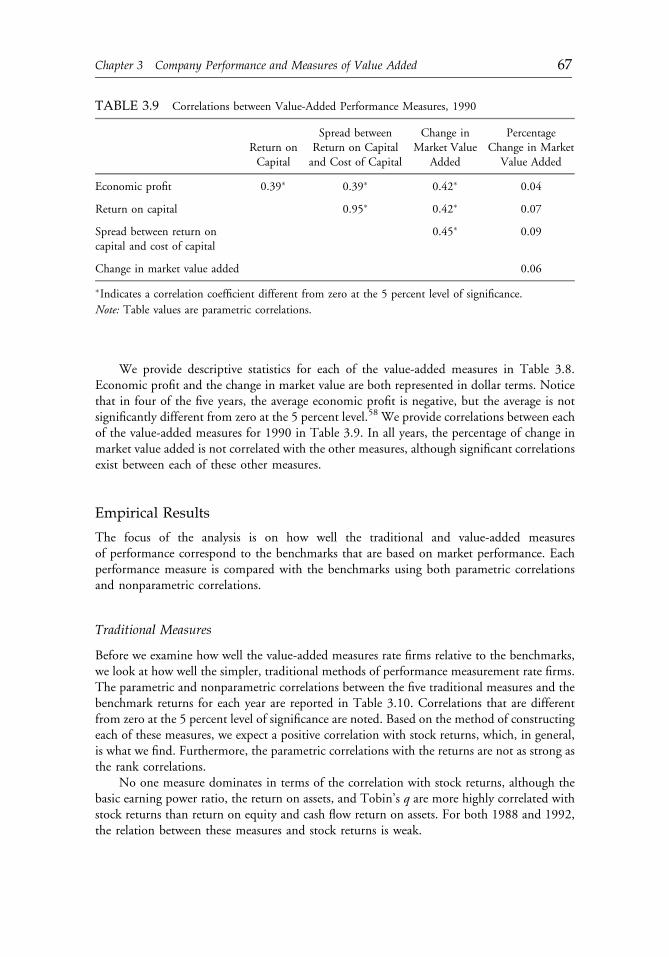

CHAPTER 3Company Performance and Measures of Value Added 31Pamela P. Peterson, CFA, and David R. PetersonReprinted from the Research Foundation of CFA Institute (December 1996).

CHAPTER 4The Affordable Dividend Approach to Equity Valuation 93Alfred RappaportReprinted from the Financial Analysts Journal (July/August 1986):52�58.

CHAPTER 5Discounted-Cash-Flow Approach to Valuation 105Gregory A. Gilbert, CFAReprinted from ICFA Continuing Education Series (1990):23�30.

ftoc 12 September 2012; 13:6:20

v

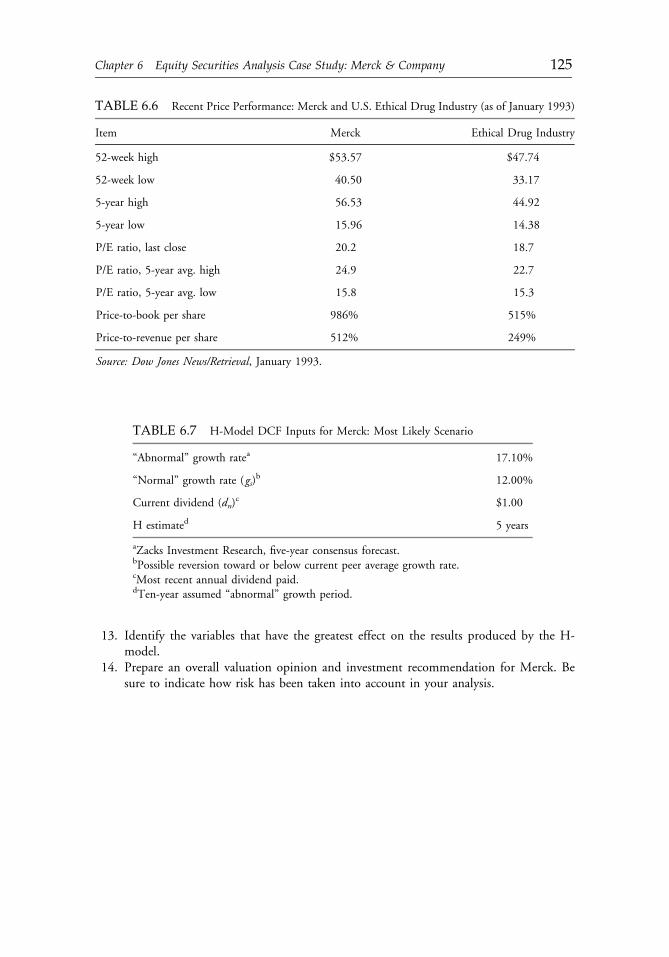

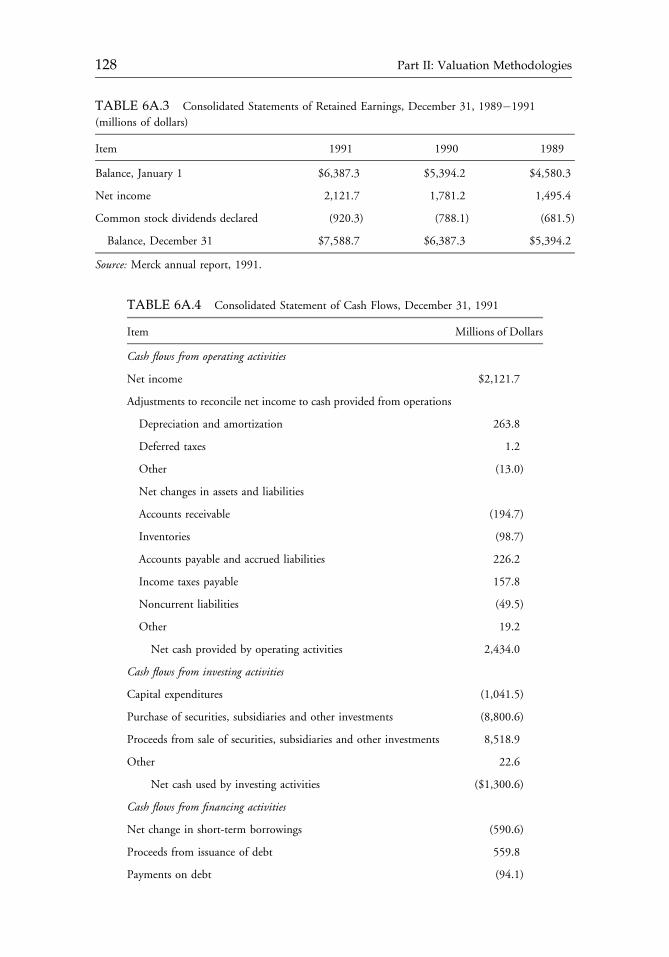

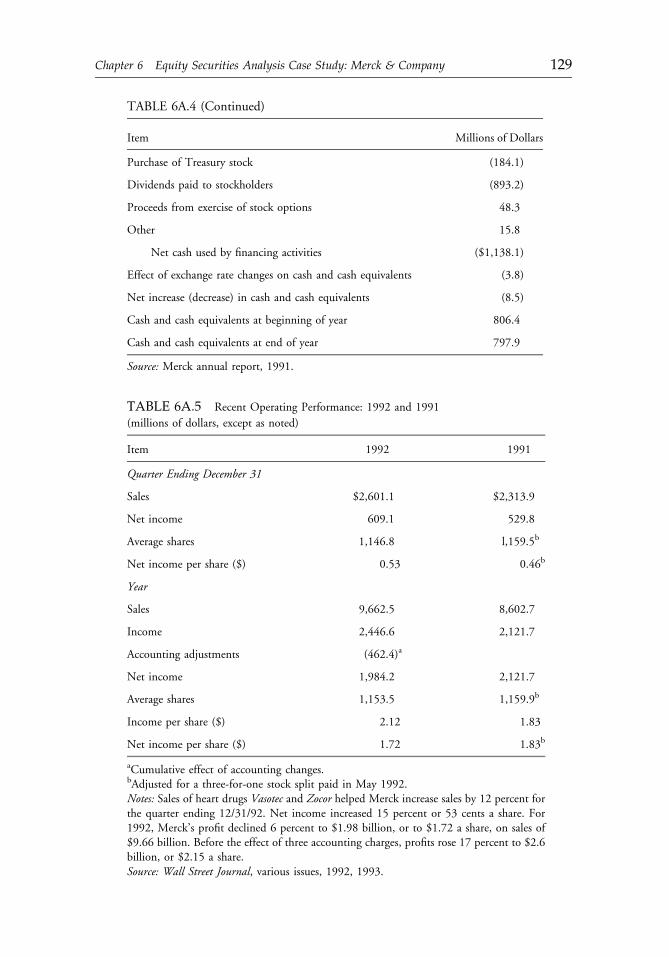

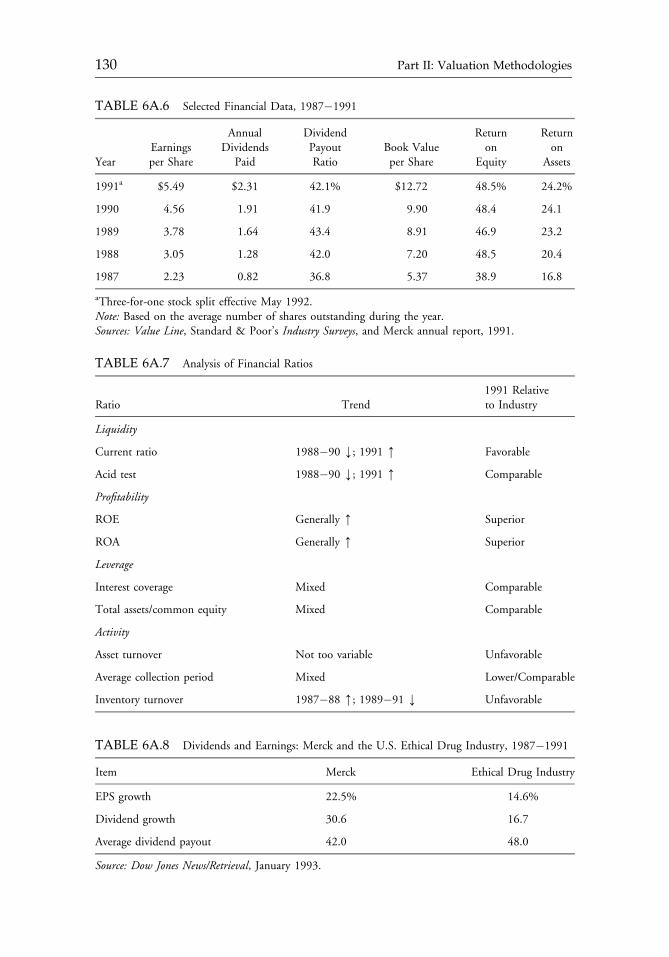

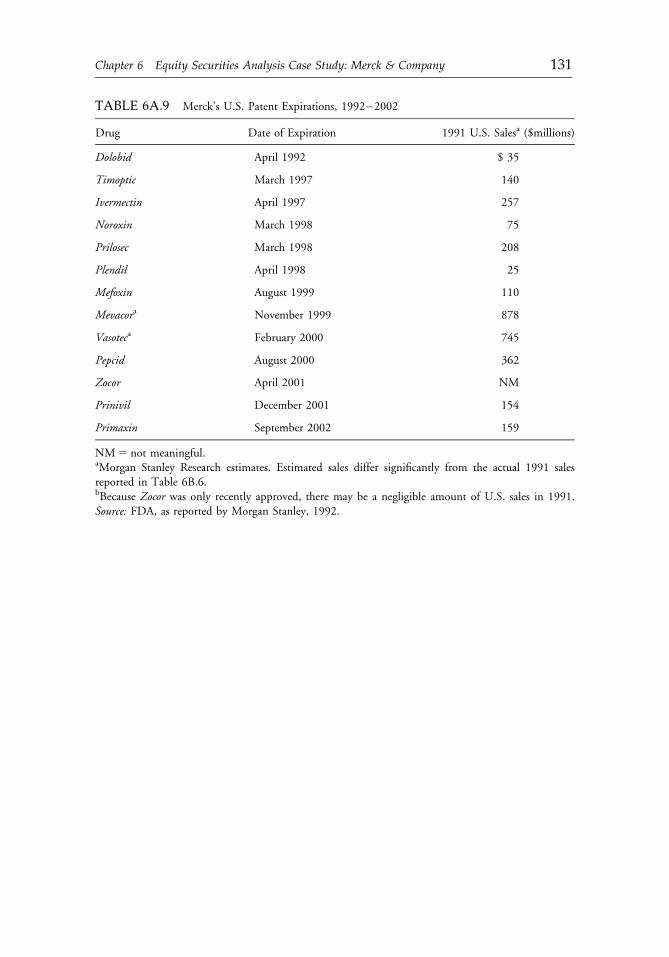

CHAPTER 6Equity Securities Analysis Case Study: Merck & Company 115Randall S. Billingsley, CFAReprinted from AIMR Conference Proceedings: Equity Securities Analysisand Evaluation (December 1993):63�95.

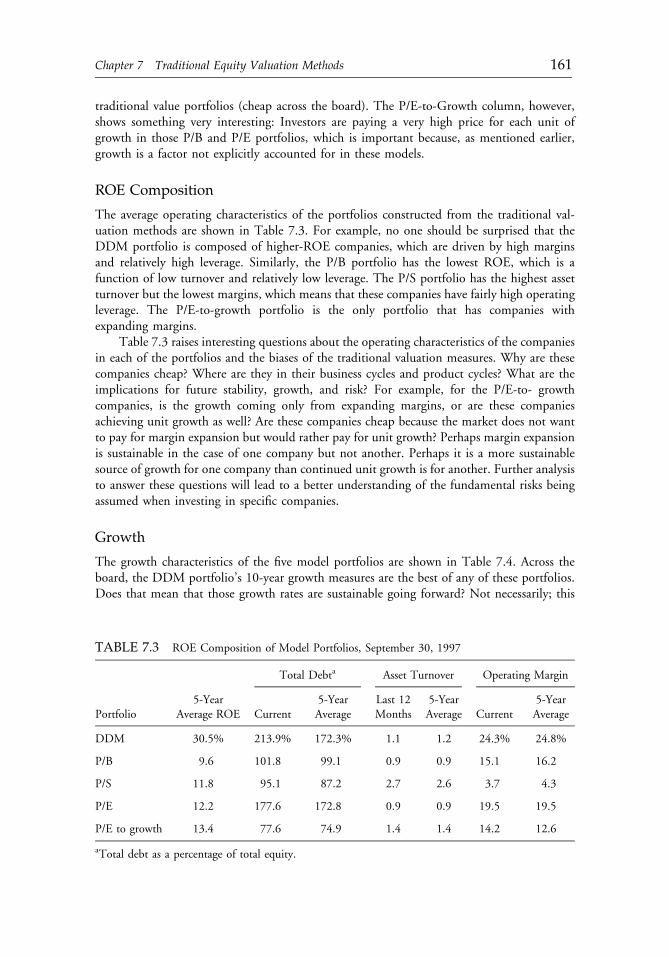

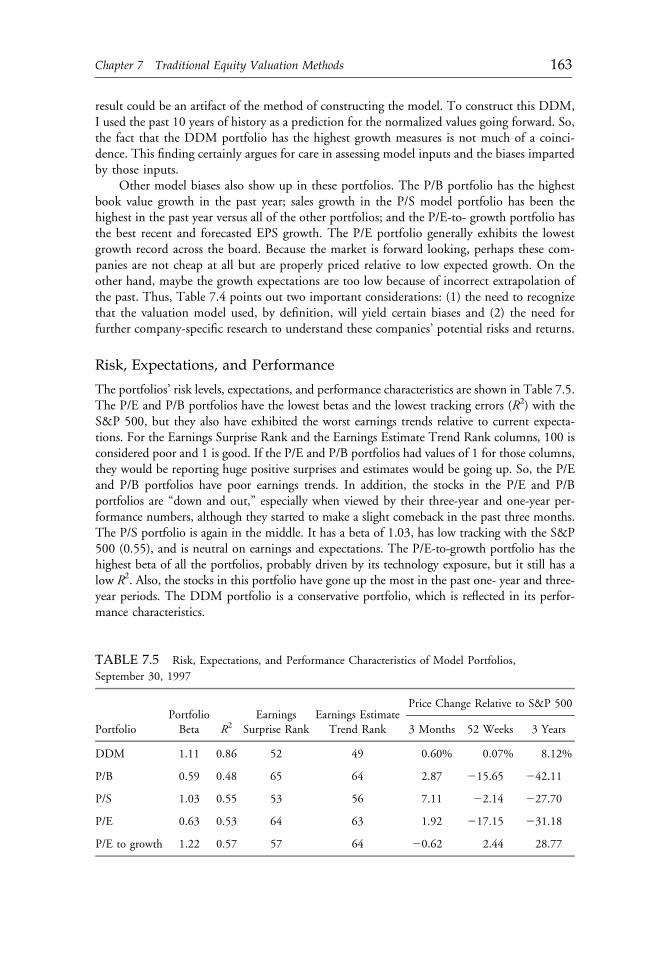

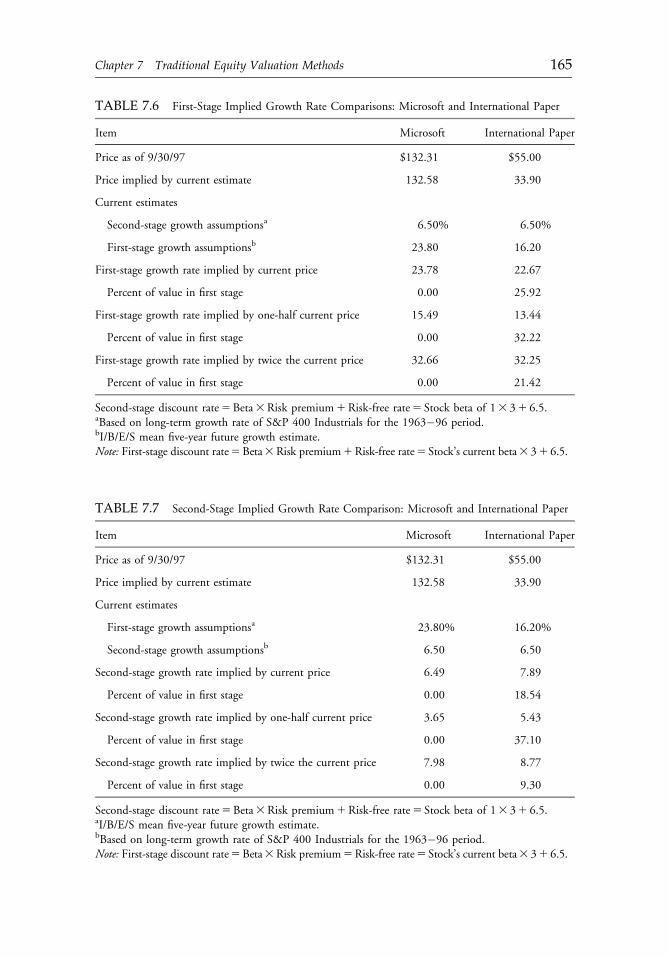

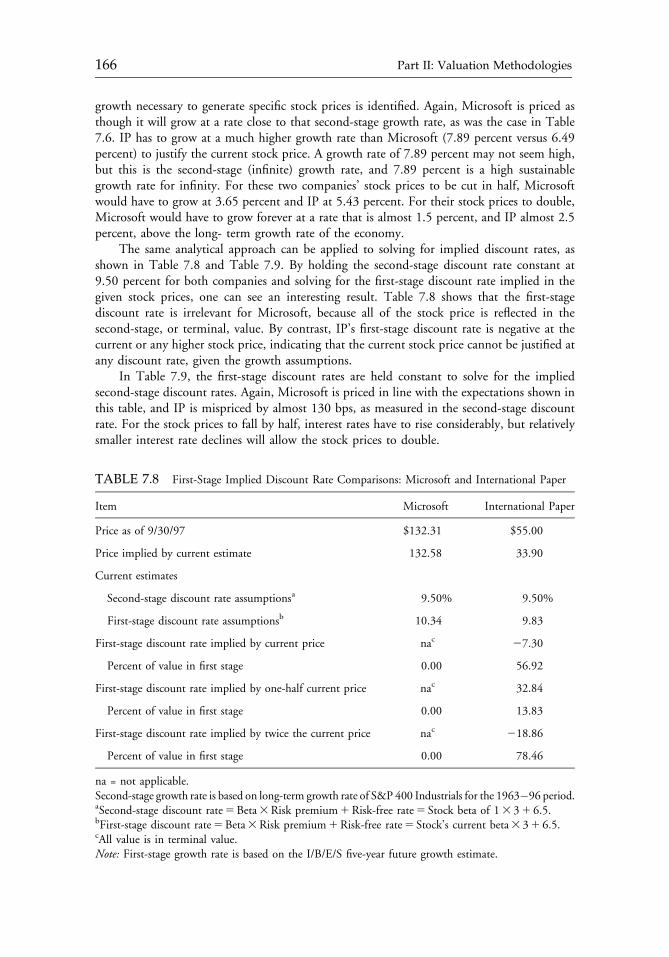

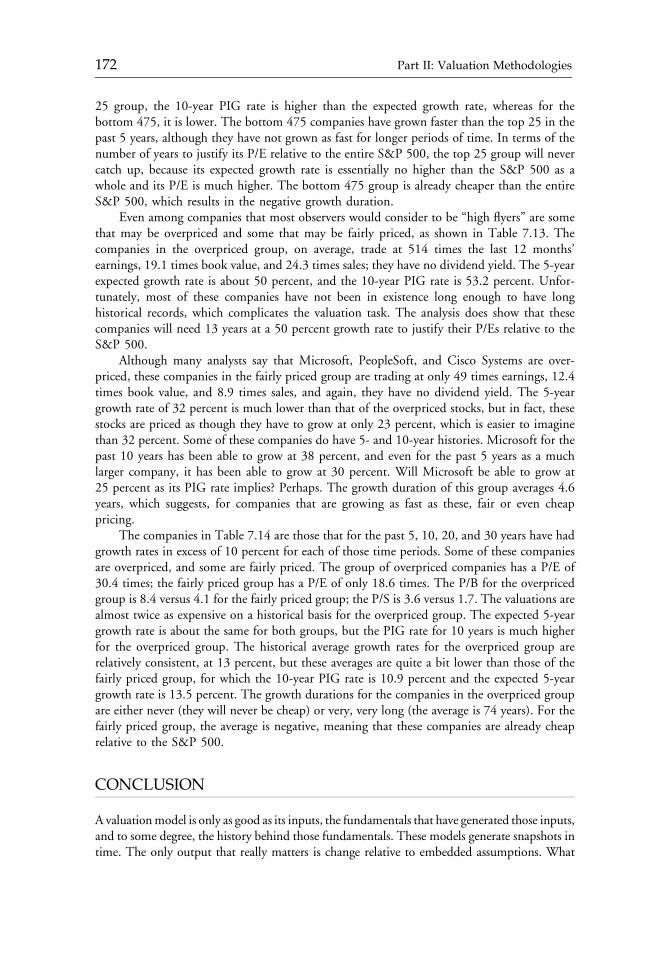

CHAPTER 7Traditional Equity Valuation Methods 155Thomas A. Martin, Jr., CFAReprinted from AIMR Conference Proceedings (May 1998):21�35.

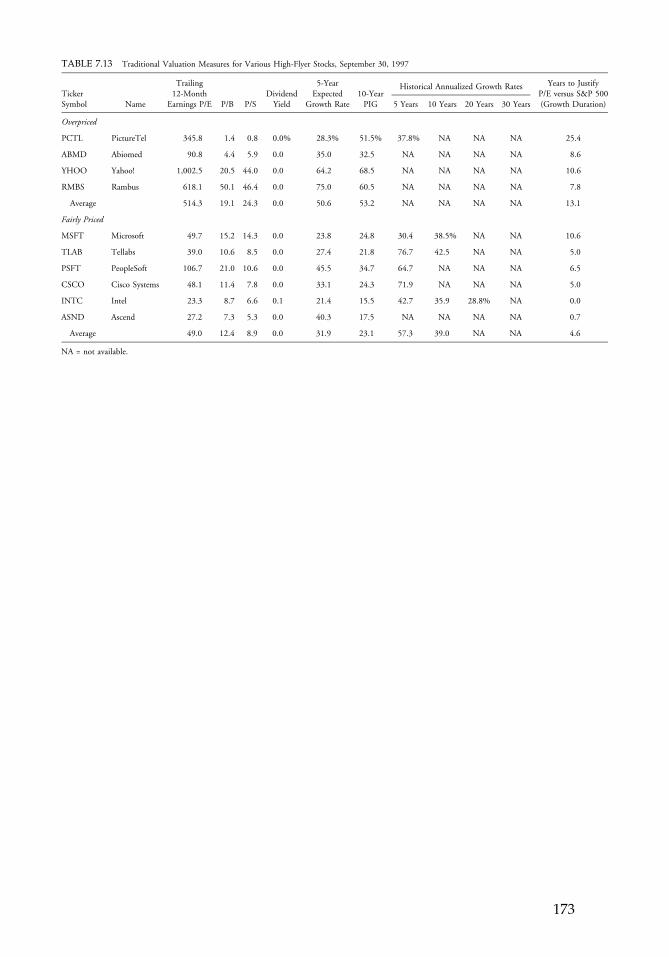

CHAPTER 8A Simple Valuation Model and Growth Expectations 177Morris G. DanielsonReprinted from the Financial Analysts Journal (May/June 1998):50�57.

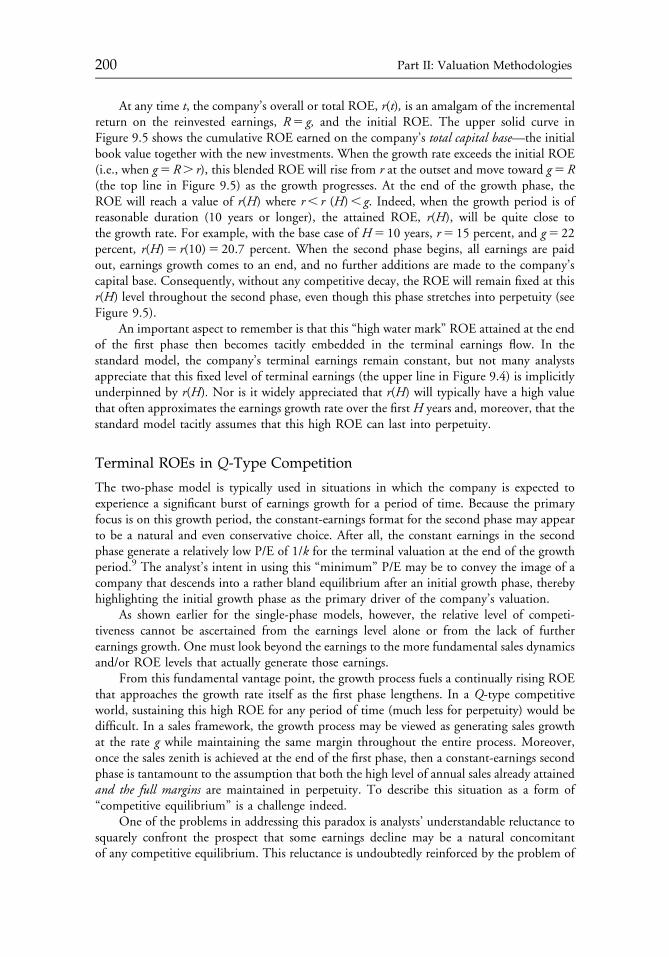

CHAPTER 9Franchise Valuation under Q-Type Competition 189Martin L. LeibowitzReprinted from the Financial Analysts Journal (November/December 1998):62�74.

CHAPTER 10Value Enhancement and Cash-Driven Valuation Models 209Aswath DamodaranReprinted from AIMR Conference Proceedings: Practical Issues in Equity Analysis(February 2000):4�17.

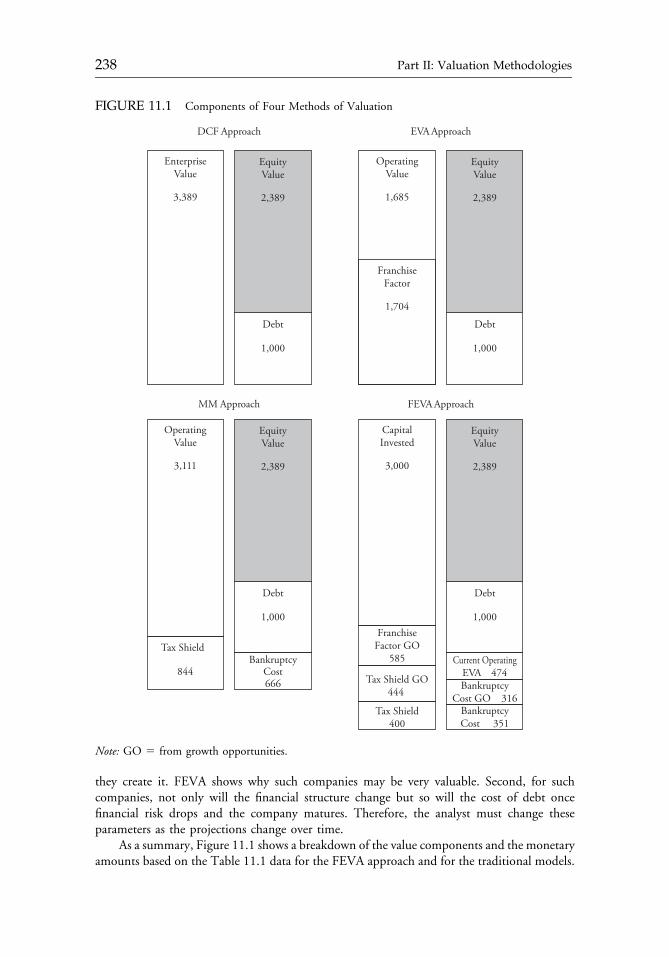

CHAPTER 11FEVA: A Financial and Economic Approach to Valuation 229Xavier Adsera and Pere VinolasReprinted from the Financial Analysts Journal (March/April 2003):80�87.

CHAPTER 12Choosing the Right Valuation Approach 243Charles M.C. LeeReprinted from AIMR Conference Proceedings: Equity Valuation in a GlobalContext (April 2003):4�14.

CHAPTER 13Choosing the Right Valuation Approach 259Robert Parrino, CFAReprinted from CFA Institute Conference Proceedings: Analyzing, Researching,and Valuing Equity Investments (June 2005):15�28.

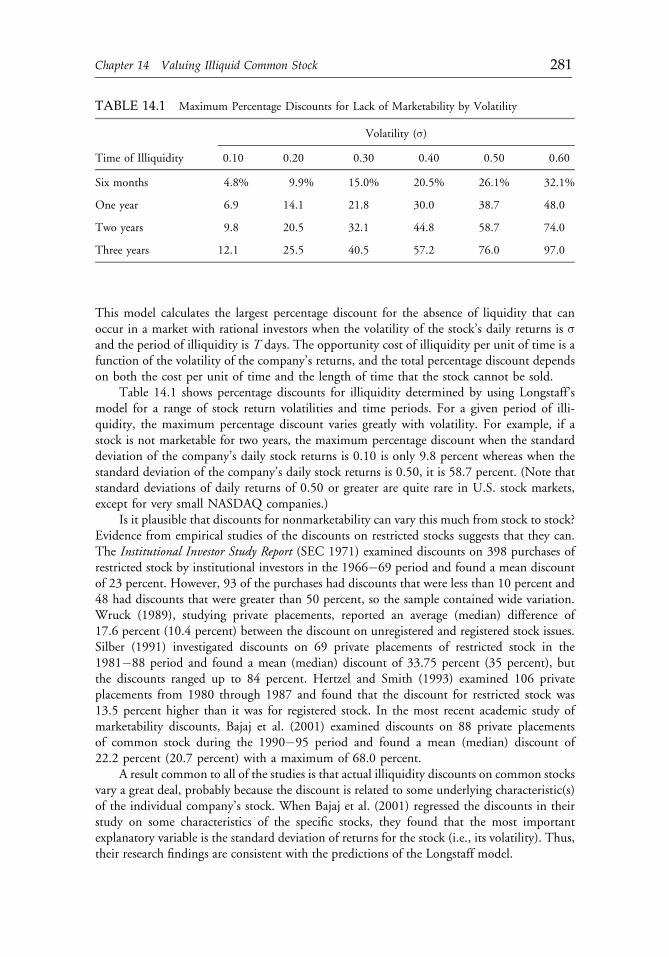

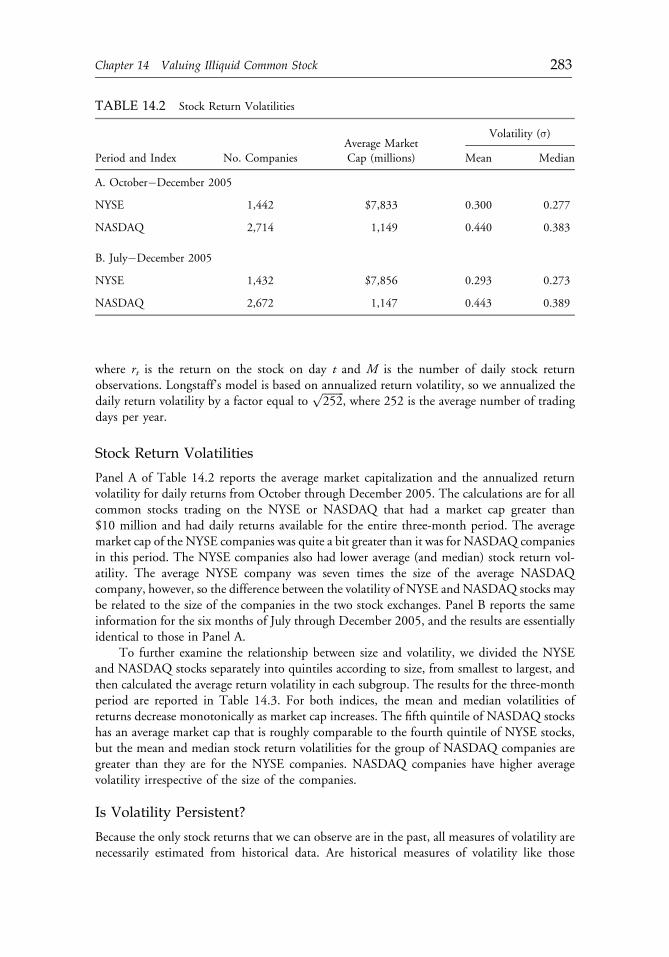

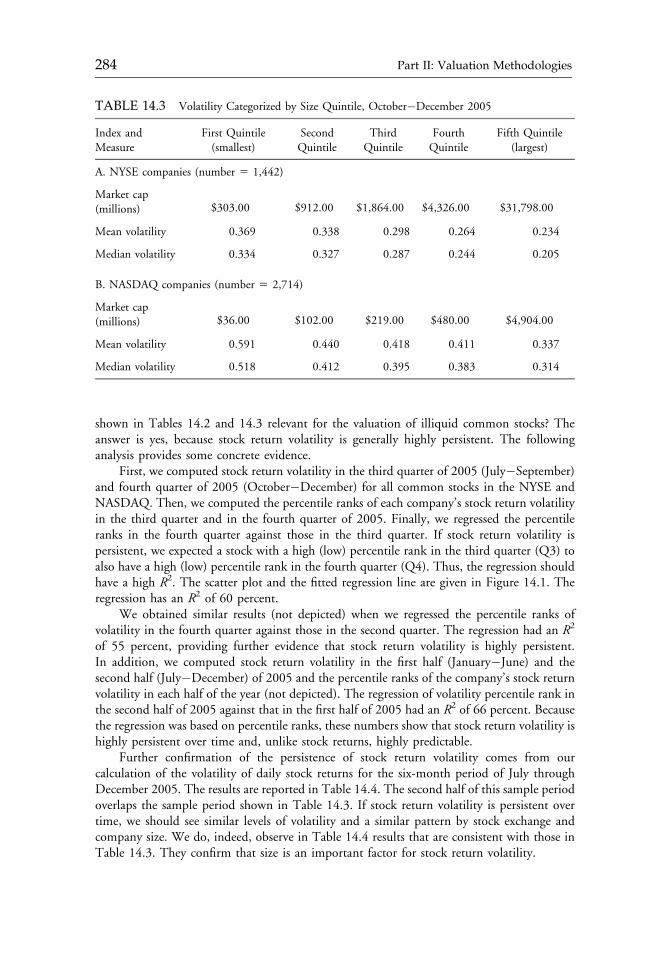

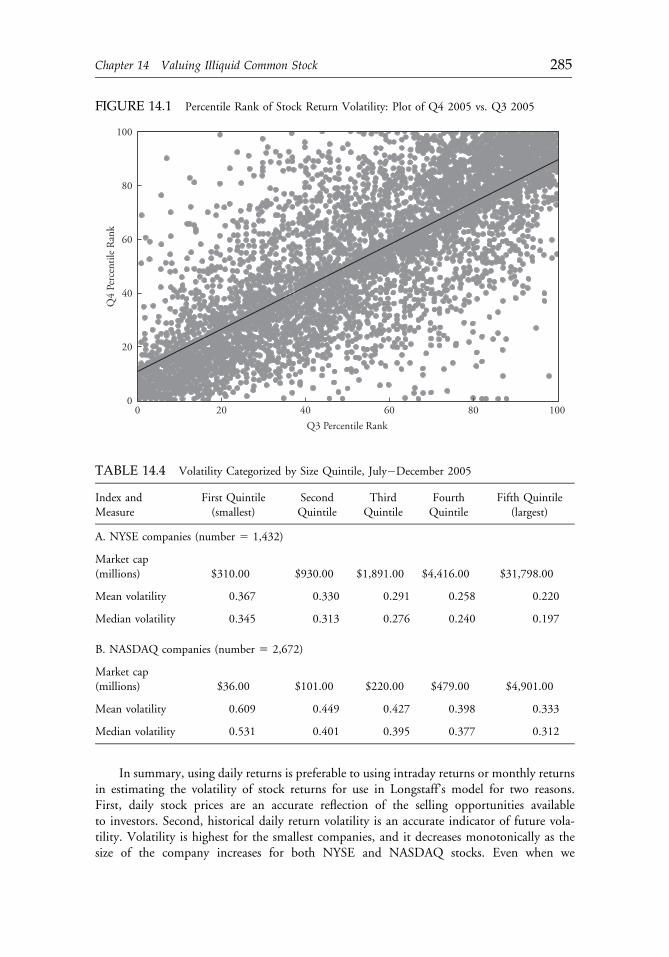

CHAPTER 14Valuing Illiquid Common Stock 279Edward A. Dyl and George J. JiangReprinted from the Financial Analysts Journal (July/August 2008):40�47.

ftoc 12 September 2012; 13:6:21

vi Contents

PART III: EARNINGS ANDCASH FLOW ANALYSIS 291

CHAPTER 15Earnings: Measurement, Disclosure, and the Impacton Equity Valuation 293D. Eric Hirst and Patrick E. HopkinsReprinted from the Research Foundation of CFA Institute (August 2000).

CHAPTER 16Cash Flow Analysis and Equity Valuation 349James A. OhlsonReprinted from AIMR Conference Proceedings: Equity Research and ValuationTechniques (May 1998):36�43.

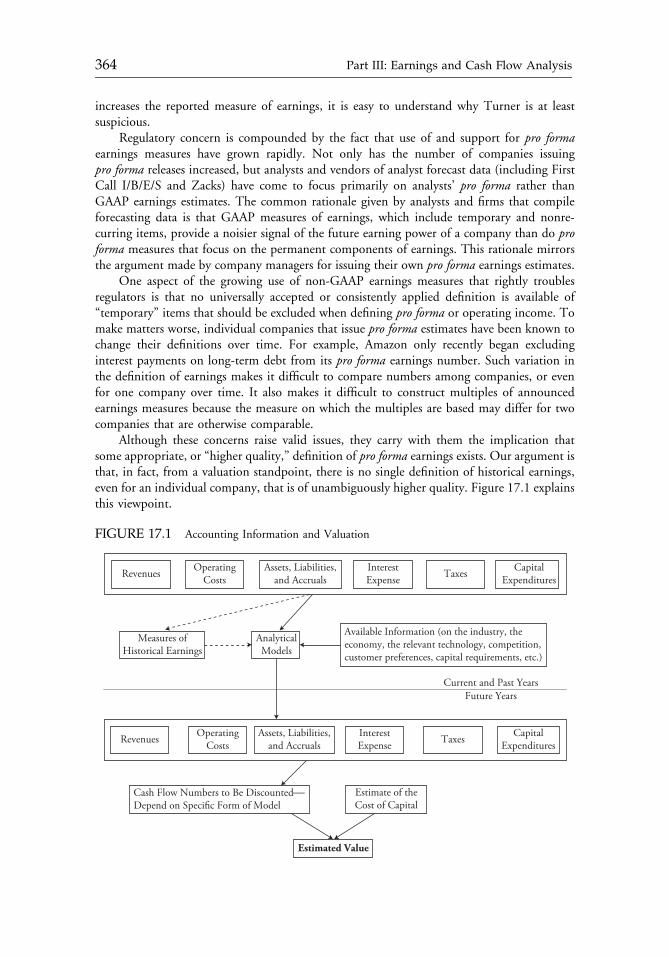

CHAPTER 17Accounting Valuation: Is Earnings Quality an Issue? 361Bradford Cornell and Wayne R. LandsmanReprinted from the Financial Analysts Journal (November/December 2003):20�28.

CHAPTER 18Earnings Quality Analysis and Equity Valuation 375Richard G. SloanReprinted from CFA Institute Conference Proceedings Quarterly (September 2006):52�60.

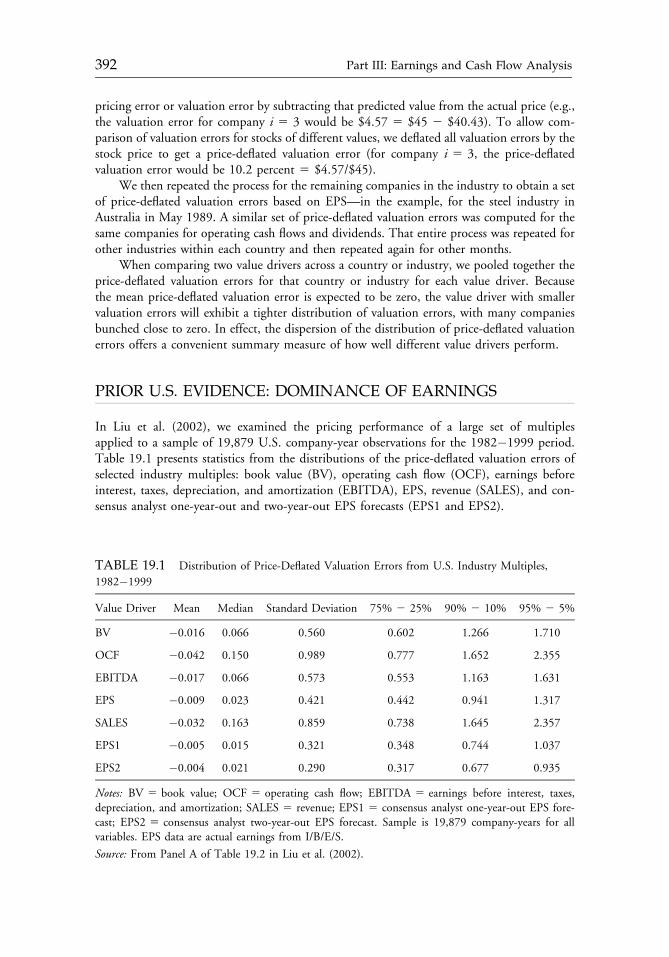

CHAPTER 19Is Cash Flow King in Valuations? 389Jing Liu, Doron Nissim, and Jacob ThomasReprinted from the Financial Analysts Journal (March/April 2007):56�68.

PART IV: OPTION VALUATION 407

CHAPTER 20Employee Stock Options and Equity Valuation 409Mark LangReprinted from the Research Foundation of CFA Institute (July 2004).

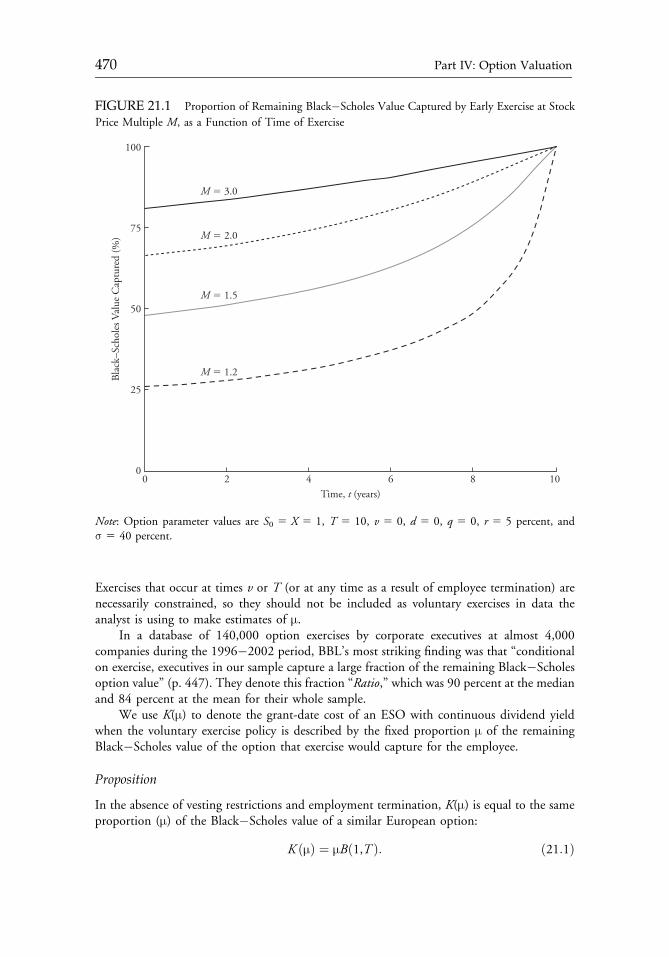

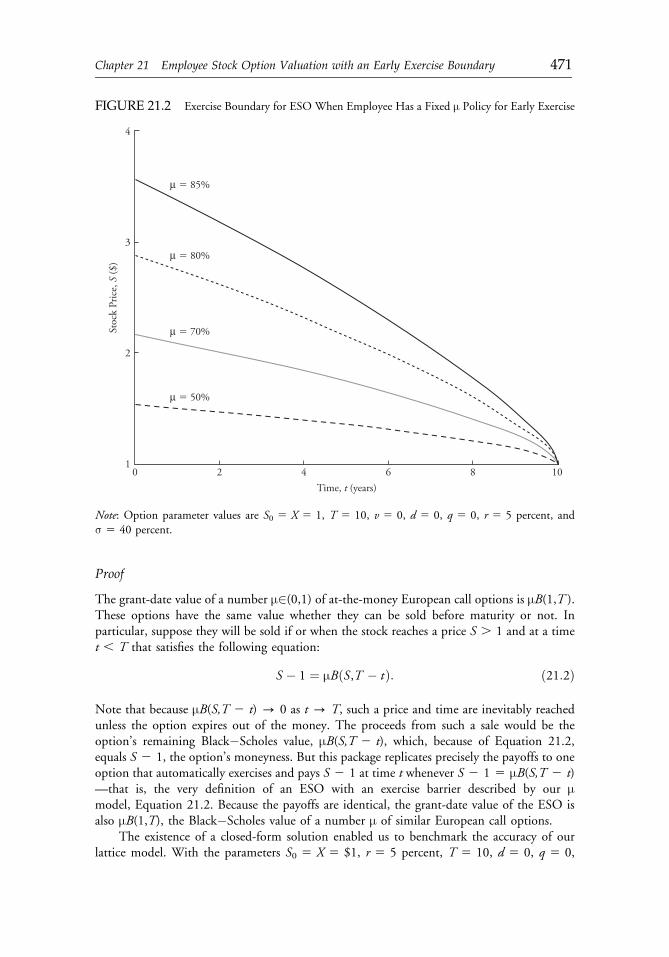

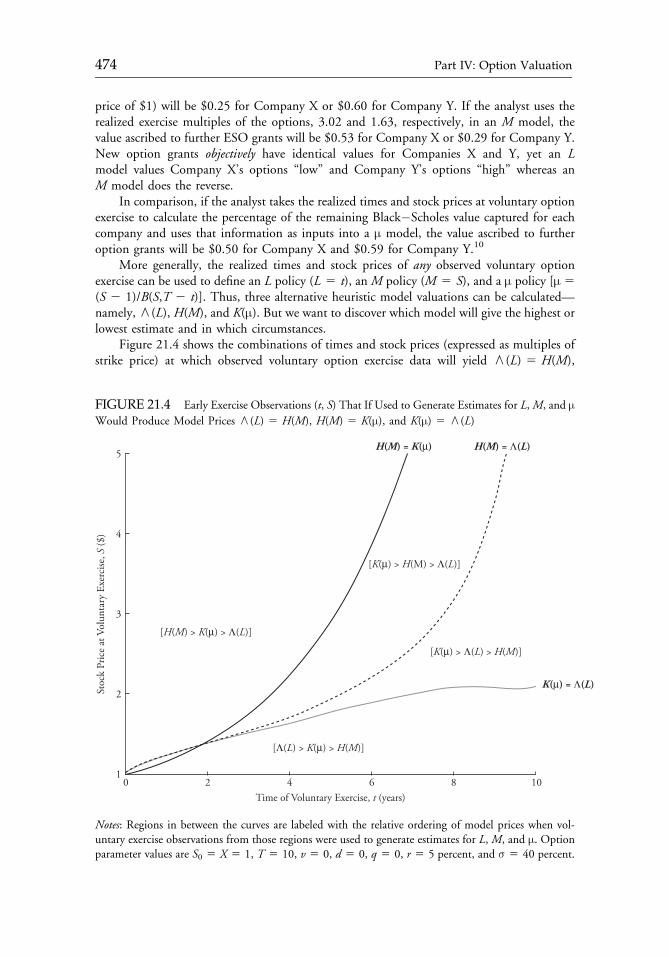

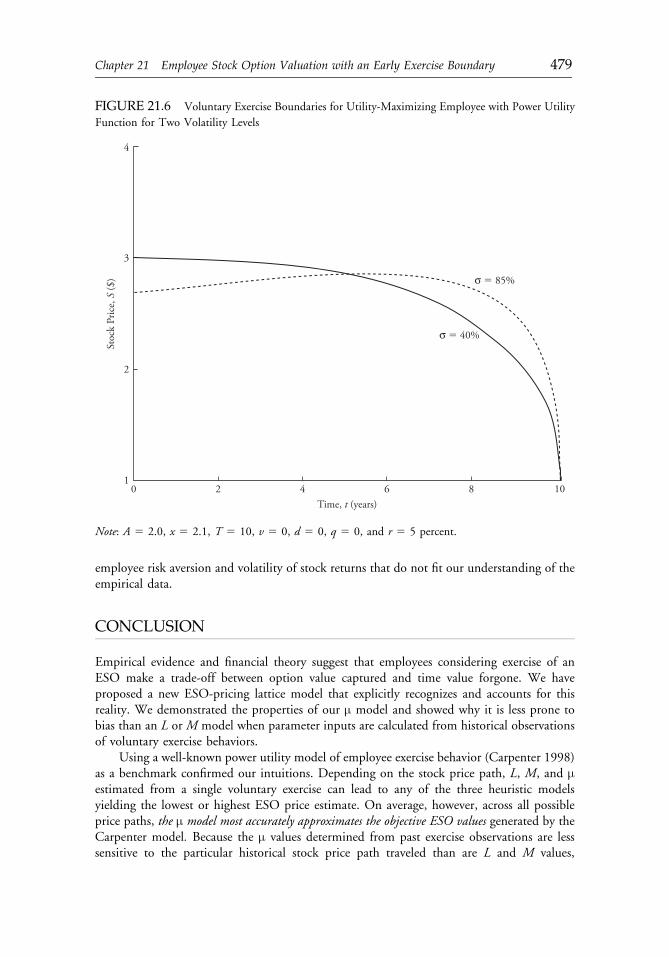

CHAPTER 21Employee Stock Option Valuation with an EarlyExercise Boundary 465Neil Brisley and Chris K. AndersonReprinted from the Financial Analysts Journal (September/October 2008):88�100.

ftoc 12 September 2012; 13:6:21

Contents vii

PART V: REAL OPTIONS VALUATION 483

CHAPTER 22Real Options and Investment Valuation 485Don M. Chance, CFA, and Pamela P. Peterson, CFAReprinted from the Research Foundation of CFA Institute (July 2002).

CHAPTER 23Real-Options Valuation for a Biotechnology Company 573David Kellogg and John M. CharnesReprinted from the Financial Analysts Journal (May/June 2000):76�84.

About the Contributors 587

Index 589

ftoc 12 September 2012; 13:6:21

viii Contents

FOREWORD

From peak to trough, Enron’s share price declined 99.98%, or from around $90 per share tojust $0.02, in only 12 months. Near its pinnacle valuation, rallying cries could be heard fromthe company’s management that Enron’s already inflated stock price was sure to go evenhigher. Unfortunately, most investors and analysts followed the tune of the Enron piper,paying no heed to the company’s true state when close scrutiny might have revealed hiddencracks in its foundation. Too few analysts questioned Enron’s valuation, and those who didwere often met with derision from employers, peers, and even Enron’s management.Groupthink pervaded Enron’s valuation, and investors and employees paid dearly.

How was Enron’s fraud eventually uncovered? Daniel Scotto, an analyst at BNP Paribas,was one of the first investment professionals to sound the alarm bells. After conducting athorough analysis of Enron that included an estimation of its value, Scotto said Enronsecurities “should be sold at all costs and sold now” in a 2001 research report. As has been thecase so often in the capital markets, valuation proved to be an essential investment tool topoint toward fraud.

Reporting shortly after the Enron scandal broke, Rebecca Smith, in her article headlined“Ex-Analyst at BNP Paribas Warned His Clients in August about Enron” in the 29 January2002 edition of the Wall Street Journal, stated:

Mr. Scotto’s experience highlights one of the oldest pressure points on Wall Streetinvolving financial analysts, who traditionally act as a filter between investors and thefinancial markets. During the past decade, Wall Street securities firms increasinglyhave pushed their research analysts to actively trumpet stocks and bonds, notimpartially analyze them.

When conducting financial analysis, the challenge is always to discern the truth about afirm or a security. Analysts have tools at their disposal for detecting reality and unearthingpotential misrepresentations. Among these tools are financial statement analysis, assessmentof management, and measures of absolute and relative value. By using these tools carefullyand objectively, the analyst can point to gaps in disclosure, inconsistencies, and mispricingopportunities. From time to time, the careful analyst can even identify possible mis-representations that can signal serious management failings.

Detailed, objective valuation serves as a powerful tool for establishing a case for the meritsof an investment. A holistic approach to valuation serves not just as a check on the economicworth of a prospective investment but also as an examination of the sustainability of thatprice. The ongoing application of these tools is just as important as the initial decision toinvest. Too many investors expend all their energy on the “buy” decision and do not reserveany for the consideration of the evolution of value over a holding period.

flast 12 September 2012; 13:9:16

ix

The publication of this book coincides with the 50th anniversary of the CFA Program. Italso comes at a time when trust in the financial industry and investment professionals isprofoundly challenged. As we take steps to rebuild trust, the tens of thousands of diligent andethical investment professionals who do their own analyses deserve thanks for upholding highstandards of practice.

Trust is built on reliability, transparency, and stewardship. Without public trust, theinvestment profession will stagnate and wither. At CFA Institute, we call on investment pro-fessionals to act to restore trust. We have broadened our mission—to lead the investmentprofession globally by promoting the highest standards of ethics, education, and professionalexcellence—to recognize our responsibility to serve society as a whole. Our mission guides us tolead and educate in the broad sense. This book on investment valuation is an expression of theCFA Institute mission. I hope its breadth, rigor, and relevance will educate and inspire readers.

JOHN ROGERS, CFAPresident and CEOCFA Institute

flast 12 September 2012; 13:9:16

x Foreword

VALUATIONTECHNIQUES

flast 12 September 2012; 13:9:16

flast 12 September 2012; 13:9:16

INTRODUCTION

Valuation is the cornerstone for the edifice we call “security analysis.” The pioneering work indeveloping a rigorous theory for valuation was published in 1938 as The Theory of InvestmentValue by John Burr Williams. For reasons that I have never been able to understand, it wasnot until 1959, when Myron J. Gordon published his paper “Dividends, Earnings, and StockPrices” in the Review of Economics and Statistics (where the now well-known Gordon modelwas put forth), that attention was finally directed to the seminal work of Williams’s 1938piece. Perhaps it was the highly quantitative nature (for its time) of the original Williamswork that deterred earlier interest; after all, in the early days finance and investments werelargely descriptive fields of endeavor and devoid of quantitative analysis other than that relatedto accounting statements. Benjamin Graham and David Dodd published their first edition ofSecurity Analysis in 1934, and the valuation work in that text was accounting based and didnot contain the necessary theoretical underpinnings that Williams and then Gordon laterdeveloped. Security Analysis (ultimately six editions have been published) was considered thedefinitive work for investors until the late 1960s, when attention began to turn to moreadvanced methodologies that were consistent with an understanding of the theory of valua-tion. Graham himself was somewhat skeptical of Williams’s valuation theory, saying in his1939 review (Journal of Political Economy, April 1939) that if investors can be persuaded totake a saner attitude toward stocks by Williams’s “higher algebra,” then he (Graham) wouldvote for it despite the hit-or-miss character embedded in the model’s assumptions.

Perhaps indirectly related, but of decided importance, to the development of valuationmethodologies for security analysis were two papers that concentrated on portfolio analysis.Harry Markowitz published his now famous article “Portfolio Selection” (Journal of Finance,March 1952) that focused attention on the proper understanding of stock price variability anddiversification. Bill Sharpe published his own path-breaking article, “A Simplified Model forPortfolio Analysis” (Management Science, January 1963), which built upon the earlier work ofMarkowitz and extended the understanding of equilibrium in security pricing. Both of thesepapers, although slow to be accepted in the practitioner’s toolkit until the 1970s, make a largecontribution to our understanding of “risk premiums” for valuation models. Similarly,Martin Leibowitz, in his 1972 book with Sidney Homer titled Inside the Yield Book, broughtvaluation techniques into clear perspective for fixed-income investors and also provided freshinsight into the importance of discount rates used in common stock valuation models.

This compendium of valuation methodologies put together by Jason Voss, CFA, andDavid Larrabee, CFA, draws from publications sponsored by CFA Institute and its pre-decessors over many years and provides a robust review of the important literature that hasevolved in the valuation field. Each of the pieces offers structure and insight into the

cintro 12 September 2012; 14:37:6

1

complexities of valuation modeling and, in its own way, points to the joint importance ofmodel design and input to the model’s variables. Models in and of themselves are critical inproviding us with a framework for thought as it pertains to security pricing. They anchor us tothe appropriate variables, their interaction with each other, and the resulting pricing sensi-tivities. But in the quest for making the models practical and useful to investors, the modelsthemselves have become a necessary yet insufficient condition for success. Model inputs viathe defined variables are the deciding factor, and it is here that the investor can distinguishhimself or herself from the crowd. Unlike Graham and Dodd with their emphasis on his-torical accounting data, today’s successful investor needs to understand the uncertainties ofthe future and how the input variables will develop ex ante rather than simply taking theex post observations. This can be a daunting task.

The economist Frank Knight in his book Risk, Uncertainty and Profit (1921) made afamous distinction that many in the investment profession seem to have forgotten but wouldbe well served to remember. Knight pointed out that risk is a condition in which the out-comes are unknown but the probabilities are known with certainty. Throwing dice is an easyexample of this risk case. Uncertainty, as Knight points out, is different from risk because theprobabilities are not known with exactness and the outcomes are similarly not known. Thisnotion of uncertainty is what we in the investment world are constantly grappling with in ourmodels. We need to always remind ourselves that our probabilities are subjective, notobjective, and flow from our analysis in establishing the ex ante input variables. Investors livein a world of uncertainty, not risk as defined by Knight, which is why the task is so daunting.

Valuation methodologies will continue to evolve with the passage of time and, correctlyapplied, will enable investors to cope more successfully with the inevitable uncertaintiesembedded in financial markets. The articles contained in this book should serve as aninvaluable resource for understanding the contributions made by CFA Institute to this field.

GARY P. BRINSON, CFA

cintro 12 September 2012; 14:37:6

2 Introduction

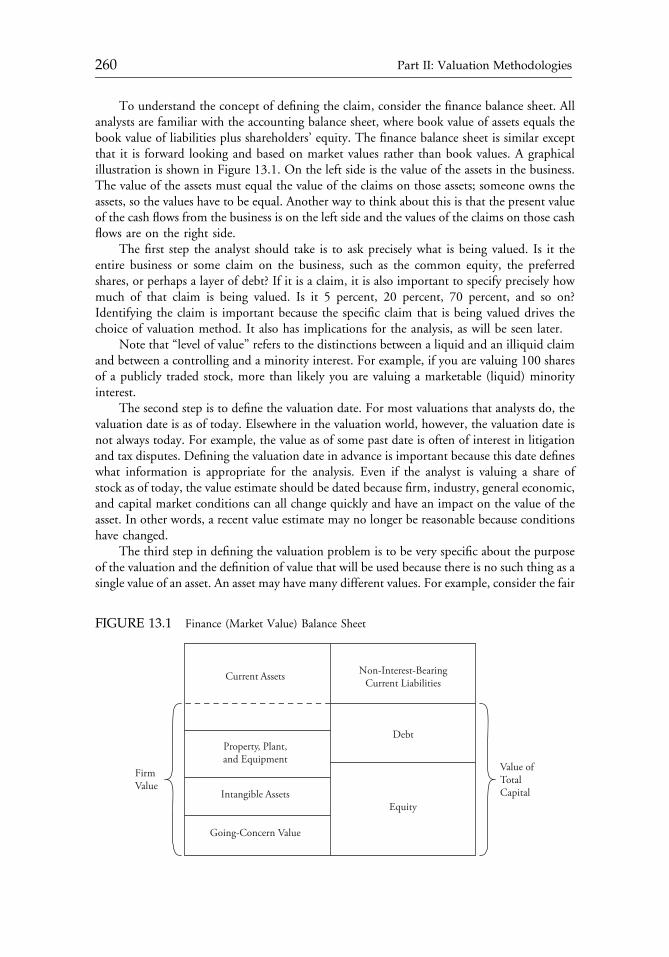

PART IVALUATION

PERSPECTIVES:THEN AND NOW

Chapter 1 Two Illustrative Approaches to Formula Valuations of Common Stocks 5

Chapter 2 Seeking a Margin of Safety and Valuation 17

c01 12 September 2012; 13:13:34

3

c01 12 September 2012; 13:13:34

CHAPTER 1TWO ILLUSTRATIVE

APPROACHESTO FORMULA VALUATIONS

OF COMMON STOCKS

Benjamin Graham

Two common-stock valuation approaches are examined in detail. The first approachconsiders company profitability, earnings growth and stability, and dividend payout.It derives an independent value of a stock that is then compared with the market price.In contrast, the second approach starts with the market price of a stock and calculatesthe rate of future growth implied by the market. From the expected growth rate, futureearnings can be derived, as well as the implicit earnings multiplier in the currentmarket price. Both approaches demonstrate that the market often has future growthexpectations that cannot be derived from companies’ past performance.

Of the various basic approaches to common-stock valuation, the most widely accepted is thatwhich estimates the average earnings and dividends for a period of years in the future andcapitalizes these elements at an appropriate rate. This statement is reasonably definite in form,but its application permits of the widest range of techniques and assumptions, including plainguesswork. The analyst has first a broad choice as to the future period he will consider; thenthe earnings and dividends for the period must be estimated, and finally a capitalization rateselected in accordance with his judgment or his prejudices. We may observe here that sincethere is no a priori rule governing the number of years to which the valuer should lookforward in the future, it is almost inevitable that in bull markets investors and analysts willtend to see far and hopefully ahead, whereas at other times they will not be so disposed to

Reprinted from the Financial Analysts Journal (November 1957):11�15. When this article was origi-nally published, Benjamin Graham was a visiting professor of finance at the University of SouthernCalifornia, Los Angeles.

c01 12 September 2012; 13:13:34

5

“heed the rumble of a distant drum.” Hence arises a high degree of built-in instability in themarket valuation of growth stocks, so much so that one might assert with some justice thatthe more dynamic the company the more inherently speculative and fluctuating may be themarket history of its shares.1

When it comes to estimating future earnings few analysts are willing to venture forth,Columbus-like, on completely uncharted seas. They prefer to start with known quantities—e.g., current or past earnings—and process these in some fashion to reach an estimate forthe future. As a consequence, in security analysis the past is always being thrown out of thewindow of theory and coming in again through the back door of practice. It would be a sorryjoke on our profession if all the elaborate data on past operations, so industriously collectedand so minutely analyzed, should prove in the end to be quite unrelated to the real deter-minants of the value—the earnings and dividends of the future.

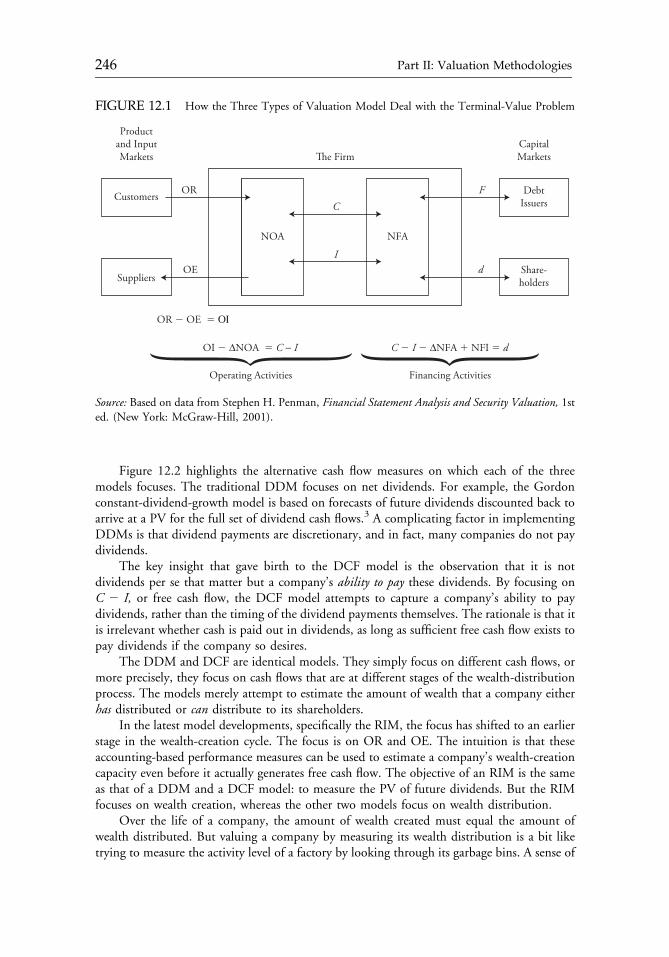

Undoubtedly there are situations, not few perhaps, where this proves to be the rueful fact.But in most cases the relationship between past and future proves significant enough to justifythe analyst’s preoccupation with the statistical record. In fact the daily work of our practi-tioner consists largely of an effort to construct a plausible picture of a company’s future fromhis study of its past performance, the latter phrase inevitably suggesting similar intensivestudies carried on by devotees of a very different discipline. The better the analyst he is, theless he confines himself to the published figures and the more he adds to these from his specialstudy of the company’s management, its policies, and its possibilities.

The student of security analysis, in the classroom or at home, tends to have a specialpreoccupation with the past record as distinct from an independent judgment of the com-pany’s future. He can be taught and can learn to analyze the former, but he lacks a suitableequipment to attempt the latter. What he seeks, typically, is some persuasive method bywhich a company’s earnings record—including such aspects as the average, the trend orgrowth, stability, etc.—plus some examination of the current balance sheet, can be trans-muted first into a projection of future earnings and dividends, and secondly into a valuationbased on such projection.

A closer look at this desired process will reveal immediately that the future earnings anddividends need not be computed separately to produce the final value. Take the simplestpresentation:

1. Past earnings times X equal future earnings.2. Future earnings times Y equal Present Value.

This operation immediately foreshortens to:

3. Past Earnings times XY equal Present Value.

It is the XY factor, or multiplier of past earnings, that my students would dearly love tolearn about and to calculate. When I tell them that there is no dependable method of findingthis multiplier they tend to be incredulous or to ask, “What good is security analysis then?”They feel that if the right weight is given to all the relevant factors in the past record, at least areasonably good present valuation of a common stock can be produced, one that will takeprobable future earnings into account and can be used as a guide to determine the attrac-tiveness or the reverse of the issue at its current market price.

In this article I propose to explain two approaches of this kind which have been developedin a Seminar on Common-Stock Valuation. I believe the first will illustrate reasonably well howformula operations of this kind may be worked out and applied. Ours is an endeavor toestablish a comparative value in 1957 for each of the 30 stocks in the Dow-Jones Industrial

c01 12 September 2012; 13:13:35

6 Part I: Valuation Perspectives: Then and Now

Average, related to a base valuation of 400 and 500, respectively, for the composite or group.(The 400 figure represented the approximate “Central Value” of the Dow-Jones Average, asfound separately by a whole series of formula methods derived from historical relationships. The500 figure represented about the average market level for the preceding twelve months.)

As will be seen, the valuations of each component issue take into account the four“quality elements” of profitability, growth, stability and dividend pay-out, applying them asmultipliers to the average earnings for 1947�1956. In addition, and entirely separately, aweight of 20% is given to the net asset value.

The second approach is essentially the reverse of that just described. Whereas the firstmethod attempts to derive an independent value to be compared with the market price, thesecond starts with the market price and calculates therefrom the rate of future growthexpected by the market. From that figure we readily derive the earnings expected for thefuture period, in our case 1957�1966, and hence the multiplier for such future earningsimplicit in the current market price.

The place for detailed comment on these calculations is after they have been developedand presented. But it may be well to express the gist of my conclusions at this point, viz.:

1. Our own “formula valuations” for the individual stocks, and probably any others of thesame general type, have little if any utility in themselves. It would be silly to assert thatStock A is “worth” only half its market price, or Stock B twice its market price, becausethese figures result from our valuation formula.

2. On the other hand, they may be suggestive and useful as composite reflections of the pastrecord, taken by itself. They may even be said to represent what the value would be,assuming that the future were merely a continuation of past performances.

3. The analyst is thus presented with a “discrepancy” of definite magnitude, between for-mula “value” and the price, which it becomes his task to deal with in terms of his superiorknowledge and judgment. The actual size of these discrepancies, and the attitude that maypossibly be taken respecting them, are discussed below.

Similarly, the approach which starts from the market price, and derives an implied“growth factor” and an implied multiplier therefrom, may have utility in concentratingthe analyst’s attention on just what the market seems to be expecting from each stock in thefuture, in comparison or contrast with what it actually accomplished in the past. Here againhis knowledge and judgment are called upon either to accept or reject the apparentassumptions of the marketplace.

Method 1. A Formula Valuation Based Solely on Past Performance in Relation to theDow-Jones Industrial Average as a Group.

The assumptions underlying this method are the following:

1. Each component issue of the Dow-Jones Industrial Average may be valued in relation to abase value of the average as a whole by a comparison of the statistical records.

2. The data to be considered are the following:a. Profitability—as measured by the rate of return on invested capital. (For convenience

this was computed only for the year 1956.)b. Growth of per-share earnings—as shown by two measurements: 1947�56 earnings vs.

1947 earnings, and 1956 earnings vs. 1947�56 earnings.

c01 12 September 2012; 13:13:35

Chapter 1 Two Illustrative Approaches to Formula Valuations of Common Stocks 7

(It would have been more logical to have used the 1954�56 average instead of thesingle year 1956, but the change would have little effect on the final valuations.)

c. Stability—as measured by the greatest shrinkage of profits in the periods 1937�1938and 1947�1956.(The calculation is based on the percentage of earnings retained in the period ofmaximum shrinkage.)

d. Pay-out—as measured by the ratio of 1956 dividends to 1956 earnings. In the fewcases where the 1956 earnings were below the 1947�56 average we substituted thelatter for the former, to get a more realistic figure of current pay-out.

These criteria demonstrate the quality of the company’s earnings (and dividend policy)and thus may control the multiplier to be applied to the earnings. The figure found undereach heading is divided by the corresponding figure for the Dow-Jones group as a whole, togive the company’s relative performance. The four relatives were then combined on the basisof equal weights to give a final “quality index” of the company as against the overall quality ofthe group.

The rate of earnings on invested capital is perhaps the most logical measure of the successand quality of an enterprise. It tells how productive are the dollars invested in the business. Instudies made in the relatively “normal” market of 1953 I found a surprisingly good corre-lation between the profitability rate and the price-earnings ratio, after introducing a majoradjustment for the dividend payout and a minor (moderating) adjustment for net asset value.

It is not necessary to emphasize the importance of the growth factor to stock-marketpeople. They are likely to ask rather why we have not taken it as the major determinant ofquality and multipliers. There is little doubt that the expected future growth is in fact themajor influence upon current price-earnings ratios, and this truth is fully recognized in oursecond approach, which deals with growth expectations as reflected in market prices. But thecorrelation between market multipliers and past growth is by no means close.

Some interesting figures worked out by Ralph A. Bing show this clearly.2 Dow Chemical,with per-share earnings growth of 31% (1955 vs. 1948) had in August 1956 a price-earningsratio of 47.3 times 1955 earnings. Bethlehem Steel, with corresponding growth of 93%, had amultiplier of only 9.1. The spread between the two relationships is thus as wide as fourteen toone. Other ratios in Mr. Bing’s table show similar wide disparities between past growth andcurrent multipliers.

It is here that the stability factor asserts its importance. The companies with highmultipliers may not have had the best growth in 1948�55, but most of them had greater thanaverage stability of earnings over the past two decades.

These considerations led us to adopt the simple arithmetical course of assigning equalweight to past growth, past stability, and current profitability in working out the qualitycoefficient for each company. The dividend payout is not strictly a measure of quality ofearning power, though in the typical case investors probably regard it in some such fashion.Its importance in most instances is undeniable, and it is both convenient and plausible to giveit equal weight and similar treatment with each of the other factors just discussed.

Finally we depart from the usual Wall Street attitude and assign a weight of 20% in thefinal valuation to the net assets per share. It is true that in the typical case the asset value hasno perceptible influence on current market price. But it may have some long-run effect onfuture market price, and thus it has a claim to be considered seriously in any independentvaluation of a company. As is well known, asset values invariably play some part, sometimes a

c01 12 September 2012; 13:13:35

8 Part I: Valuation Perspectives: Then and Now

fairly important one, in the many varieties of legal valuations of common stocks, which growout of tax cases, merger litigation, and the like. The basic justification for considering assetvalue in this process, even though it may be ignored in the current market price, lies in thepossibility of its showing its weight later, through competitive developments, changes inmanagement or its policies, merger or sale eventuality, etc.

The above discussion will explain, perhaps not very satisfactorily, why the four factorsentering into the quality rating and the fifth factor of asset value were finally assigned equalweight of 20% each.

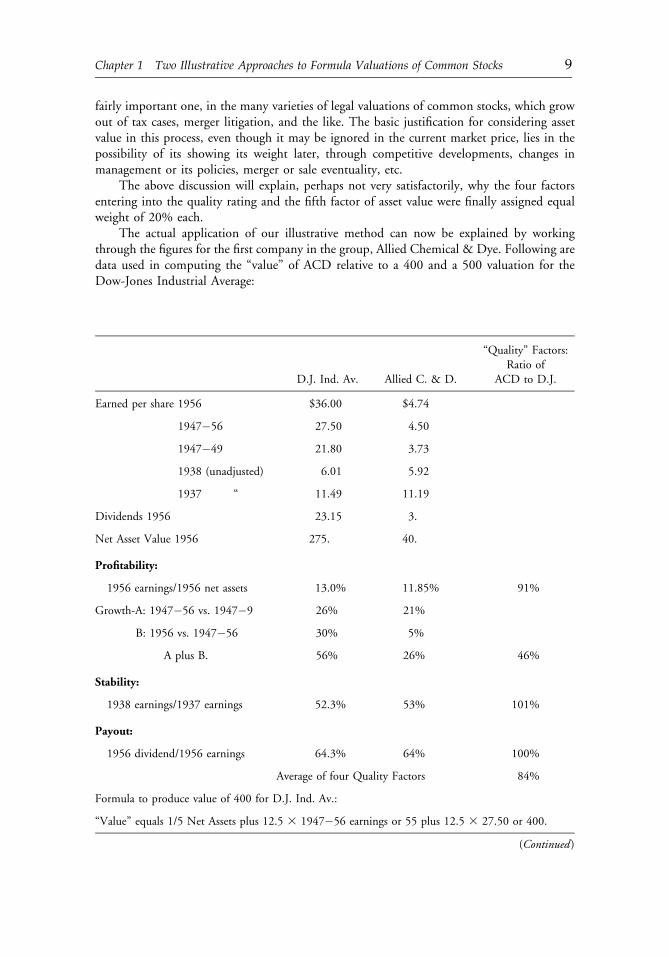

The actual application of our illustrative method can now be explained by workingthrough the figures for the first company in the group, Allied Chemical & Dye. Following aredata used in computing the “value” of ACD relative to a 400 and a 500 valuation for theDow-Jones Industrial Average:

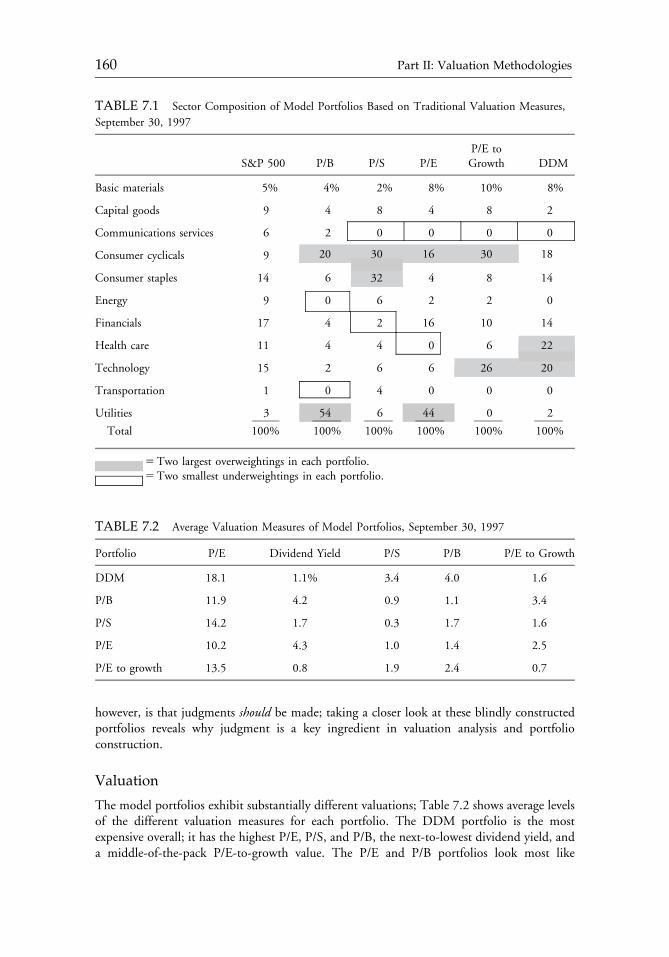

D.J. Ind. Av. Allied C. & D.

“Quality” Factors:Ratio of

ACD to D.J.

Earned per share 1956 $36.00 $4.74

1947�56 27.50 4.50

1947�49 21.80 3.73

1938 (unadjusted) 6.01 5.92

1937 “ 11.49 11.19

Dividends 1956 23.15 3.

Net Asset Value 1956 275. 40.

Profitability:

1956 earnings/1956 net assets 13.0% 11.85% 91%

Growth-A: 1947�56 vs. 1947�9 26% 21%

B: 1956 vs. 1947�56 30% 5%

A plus B. 56% 26% 46%

Stability:

1938 earnings/1937 earnings 52.3% 53% 101%

Payout:

1956 dividend/1956 earnings 64.3% 64% 100%

Average of four Quality Factors 84%

Formula to produce value of 400 for D.J. Ind. Av.:

“Value” equals 1/5 Net Assets plus 12.5 3 1947�56 earnings or 55 plus 12.5 3 27.50 or 400.

(Continued)

c01 12 September 2012; 13:13:35

Chapter 1 Two Illustrative Approaches to Formula Valuations of Common Stocks 9

Corresponding “Valuation” of Allied Chem. & Dye, (including Quality Factor of 84%):

Value equals 1/5 3 40 plus .84 3 12.5 3 4.50 or 55.

Formula to produce value of 500 for D.J. Ind. Av.:

Value equals 1/5 Net Assets plus 16.2 3 1947�56 earnings or 500.

Corresponding “Valuation” of Allied Chem. & Dye:

Value equals 1/5 3 40 plus .84 3 16.2 3 4.50 or 69.

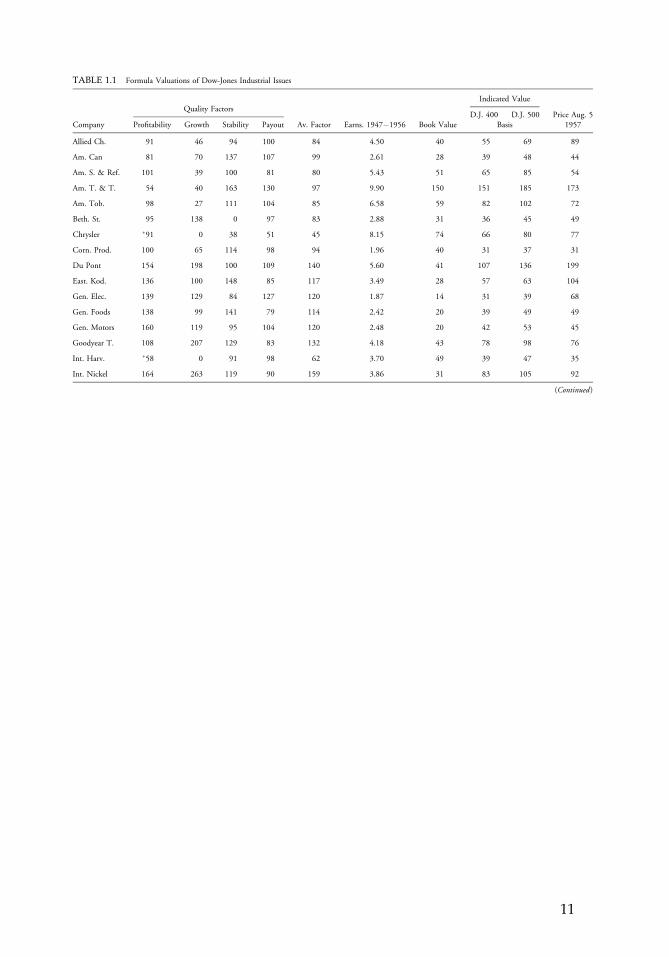

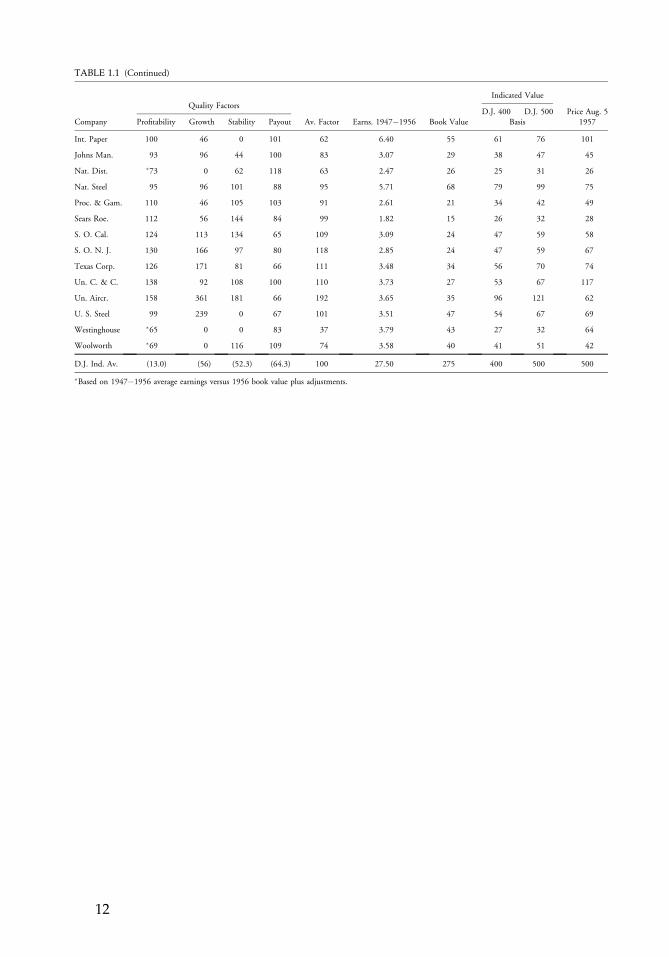

In Table 1.1 we supply the “valuation” reached by this method for each of the 30 stocksin the Dow Jones Industrial Average. Our table includes the various quality factors, theaverage earnings, and the asset values used to arrive at our final figures.

In about half the cases these “valuations” differ quite widely from the prices ruling onAugust 5 last, on which date the D. J. Average actually sold at 500. Seven issues were selling at20% or more above their formula value, and an equal number at 20% or more below suchvalue. At the extremes we find Westinghouse selling at a 100% “premium,” and UnitedAircraft at about a 50% “discount.” The extent of these disparities naturally suggests that ourmethod is technically a poor one, and that more plausible valuations could be reached—i.e.,ones more congruous with market prices—if a better choice were made of the factors andweights entering into the method.

A number of tests were applied to our results to see if they could be “improved” by someplausible changes in the technique. To give these in any detail would prolong this reportunnecessarily. Suffice it to say that they were unproductive. If the asset-value factor had beenexcluded, a very slight change would have resulted in favor of the issues which were selling atthe highest premium over their formula value. On the other hand, if major emphasis had beenplaced on the factor of past growth, some of our apparently undervalued issues would havebeen given still larger formula values; for Table 1.1 shows that more of the spectacular growthpercentages occur in this group than in the other—e.g., United Aircraft, International Nickel,and Goodyear.

It is quite evident from Table 1.1 that the stock market fixes its valuation of a givencommon stock on the basis not of its past statistical performance but rather of its expected futureperformance, which may differ significantly from its past behavior. The market is, of course,fully justified in seeking to make this independent appraisal of the future, and for that reasonany automatic rejection of themarket’s verdict because it differs from a formula valuation wouldbe the height of folly. We cannot avoid the observation, however, that the independentappraisals made in the stock market are themselves far from infallible, as is shown in part by therapid changes to which they are subject. It is possible, in fact, that they may be on the whole a nomore dependable guide to what the future will produce than the “values” reached by ourmechanical processing of past data, with all the latter’s obvious shortcomings.

Let us turn now to our second mathematical approach, which concerns itself with futuregrowth, or future earnings, as they appear to be predicted by the market price itself. We startwith the theory that the market price of a representative stock, such as any one in the Dow-Jones group, reflects the earnings to be expected in a future period, times a multiplier which isin turn based on the percentage of future growth. Thus an issue for which more than averagegrowth is expected will have this fact shown to a double degree, or “squared,” in its marketprice—first in the higher figure taken for future earnings, and second in the higher multiplierapplied to those higher earnings.

c01 12 September 2012; 13:13:35

10 Part I: Valuation Perspectives: Then and Now

TABLE 1.1 Formula Valuations of Dow-Jones Industrial Issues

Indicated ValueQuality Factors

D.J. 400 D.J. 500 Price Aug. 5Company Profitability Growth Stability Payout Av. Factor Earns. 1947�1956 Book Value Basis 1957

Allied Ch. 91 46 94 100 84 4.50 40 55 69 89

Am. Can 81 70 137 107 99 2.61 28 39 48 44

Am. S. & Ref. 101 39 100 81 80 5.43 51 65 85 54

Am. T. & T. 54 40 163 130 97 9.90 150 151 185 173

Am. Tob. 98 27 111 104 85 6.58 59 82 102 72

Beth. St. 95 138 0 97 83 2.88 31 36 45 49

Chrysler �91 0 38 51 45 8.15 74 66 80 77

Corn. Prod. 100 65 114 98 94 1.96 40 31 37 31

Du Pont 154 198 100 109 140 5.60 41 107 136 199

East. Kod. 136 100 148 85 117 3.49 28 57 63 104

Gen. Elec. 139 129 84 127 120 1.87 14 31 39 68

Gen. Foods 138 99 141 79 114 2.42 20 39 49 49

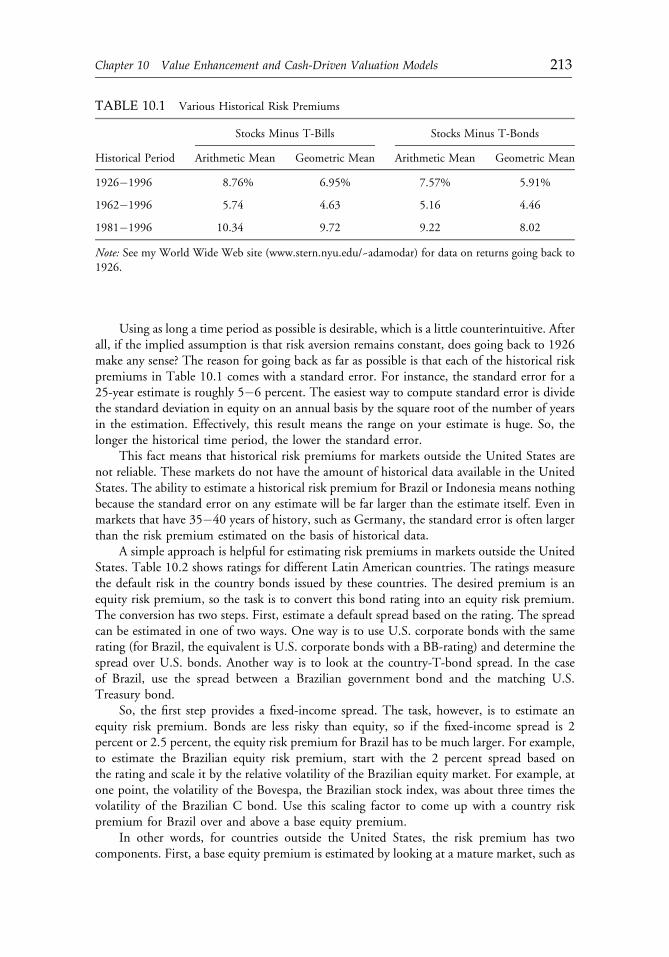

Gen. Motors 160 119 95 104 120 2.48 20 42 53 45

Goodyear T. 108 207 129 83 132 4.18 43 78 98 76

Int. Harv. �58 0 91 98 62 3.70 49 39 47 35

Int. Nickel 164 263 119 90 159 3.86 31 83 105 92

(Continued)

c01 12 September 2012; 13:13:36

11

TABLE 1.1 (Continued)

Indicated ValueQuality Factors

D.J. 400 D.J. 500 Price Aug. 5Company Profitability Growth Stability Payout Av. Factor Earns. 1947�1956 Book Value Basis 1957

Int. Paper 100 46 0 101 62 6.40 55 61 76 101

Johns Man. 93 96 44 100 83 3.07 29 38 47 45

Nat. Dist. �73 0 62 118 63 2.47 26 25 31 26

Nat. Steel 95 96 101 88 95 5.71 68 79 99 75

Proc. & Gam. 110 46 105 103 91 2.61 21 34 42 49

Sears Roe. 112 56 144 84 99 1.82 15 26 32 28

S. O. Cal. 124 113 134 65 109 3.09 24 47 59 58

S. O. N. J. 130 166 97 80 118 2.85 24 47 59 67

Texas Corp. 126 171 81 66 111 3.48 34 56 70 74

Un. C. & C. 138 92 108 100 110 3.73 27 53 67 117

Un. Aircr. 158 361 181 66 192 3.65 35 96 121 62

U. S. Steel 99 239 0 67 101 3.51 47 54 67 69

Westinghouse �65 0 0 83 37 3.79 43 27 32 64

Woolworth �69 0 116 109 74 3.58 40 41 51 42

D.J. Ind. Av. (13.0) (56) (52.3) (64.3) 100 27.50 275 400 500 500

�Based on 1947�1956 average earnings versus 1956 book value plus adjustments.

c01 12 September 2012; 13:13:36

12

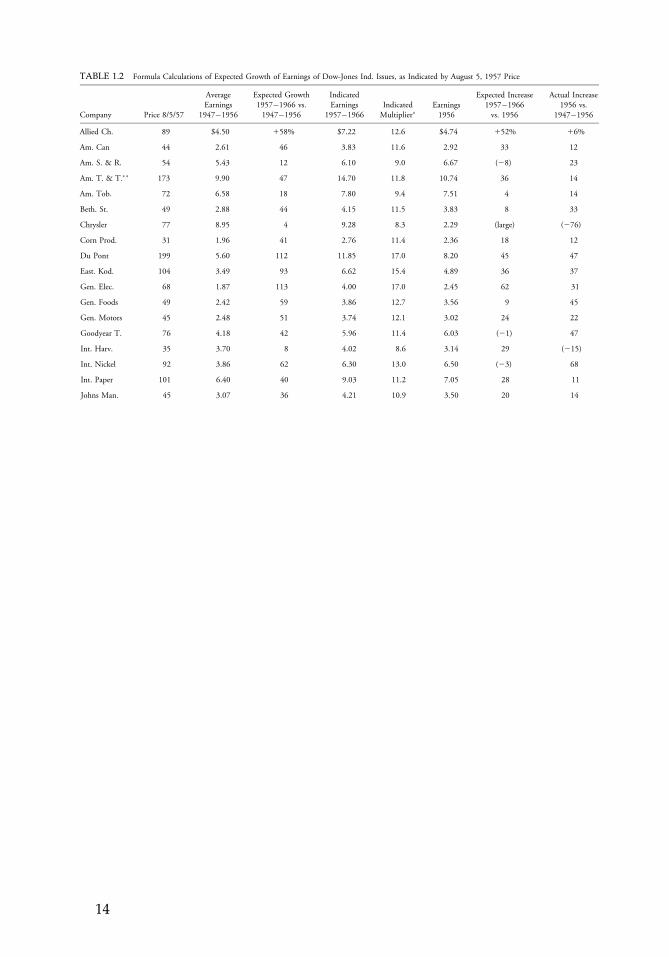

We shall measure growth by comparing the expected 1957�66 earnings with the actualfigures for 1947�56. Our basic formula says, somewhat arbitrarily, that where no growth isexpected the current price will be 8 times both 1947�56 earnings and the expected 1957�66earnings. If growth G is expected, expressed as the ratio of 1957�66 to 1947�56 earnings,then the price reflects such next decade earnings multiplied by 8 times G.

From these assumptions we obtain the simple formula:

Price equals ðE3GÞ3 ð83GÞ, or 8G2 3E,

where E is the per-share earnings for 1947�56:

To find G, the expected rate of future growth, we have only to divide the current price by8 times 1947�56 earnings, and take the square root.

When this is done for the Dow-Jones Average as a whole, using its August 5, 1957, priceof 500, we get a value of 1.5 for G—indicating an expected growth of 50% for 1957�66earnings vs. the 1947�56 actuality. This anticipates an average of $41 in the next decade, asagainst $27.50 for the previous 10 years and about $36 in 1956. This estimate appearsreasonable to the writer in relation to the 500 level. (In fact, he started with this estimate andworked back from it to get the basic multiplier of 8 to be applied to issues with no expectedgrowth.) The price of 500 for the D. J. Average would represent in turn a multiplier of 8 31.5, or 12, to be applied to the expected future earnings of $41. (Incidentally, on theseassumptions the average current formula value of about 400 for the Dow-Jones Averagewould reflect expectations of a decade-to-decade growth of 35%, average earnings of $37.1 for1957�66, and a current multiplier of 10.8 for such future earnings.)

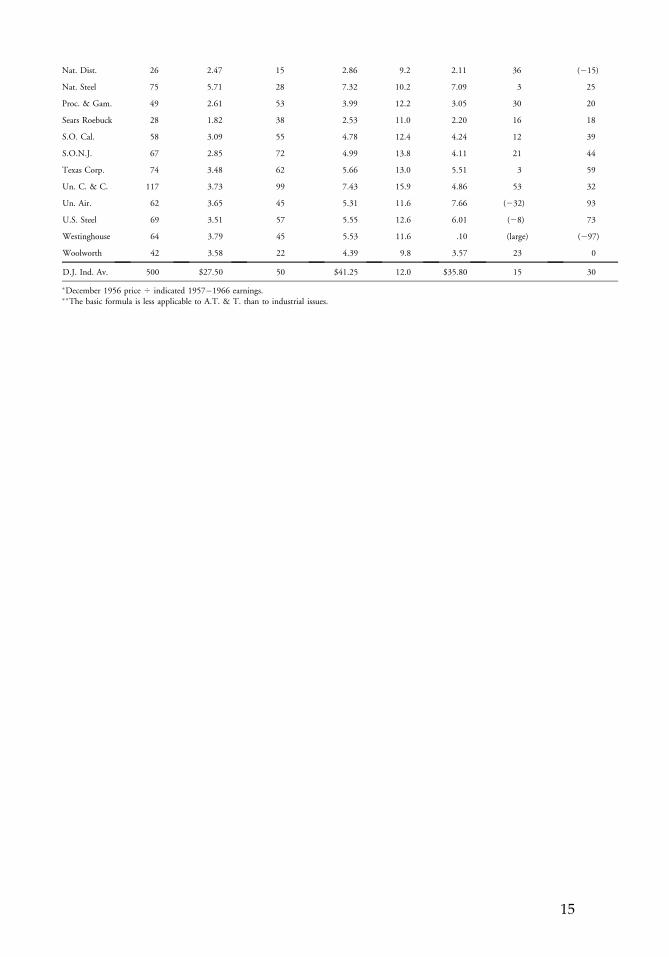

In Table 1.2 we set forth the results of applying this second approach to the 30 Dow-Jones issues. (The figures for Am. Tel. & Tel. might well be ignored, since utility issuesshould take a different basic formula.) The main interest in the table lies in the disparities itindicates between the expected future growth, implicit in the market prices, and the actualgrowth during the past decade. Ten of the companies (plus ATT) sold at prices anticipating atleast twice the Dow-Jones Average rate of growth, comparing 1957�66 with 1956. Of theseonly two, Du Pont and General Electric, had actually shown distinctly better than averagegrowth in the last 10 years. Conversely, eight of the companies were indicating less than halfthe average expected rate of growth, including five for which actual declines from 1956 levelswere apparently predicted. Yet of these eight companies, no less than five had actually shownfar greater than average growth in the past decade.

This leads us to our final observations, which tie our two tables together. The 10companies previously mentioned, for which unusually rapid growth is anticipated, includesseven of those shown in Table 1.1 as selling significantly above their formula valuation. Again,the eight for which subnormal or no growth is expected include six which were sellingsubstantially below their formula valuations.

We conclude that a large part of the discrepancies between carefully calculated formulavalues and the market prices can be traced to the growth factor, not because the formulasunderplay its importance, but rather because the market often has concepts of future earningschanges which cannot be derived from the companies’ past performance. The reasons for themarket’s breaking with the past are often abundantly clear. Investors do not believe, forexample, that United Aircraft will duplicate its brilliant record of 1947�1956, because theyconsider that a company with the United States Department of Defense as its chief customeris inherently vulnerable. They have the opposite view with regard to Westinghouse. They feel

c01 12 September 2012; 13:13:37

Chapter 1 Two Illustrative Approaches to Formula Valuations of Common Stocks 13

TABLE 1.2 Formula Calculations of Expected Growth of Earnings of Dow-Jones Ind. Issues, as Indicated by August 5, 1957 Price

Company Price 8/5/57

AverageEarnings

1947�1956

Expected Growth1957�1966 vs.1947�1956

IndicatedEarnings

1957�1966IndicatedMultiplier�

Earnings1956

Expected Increase1957�1966vs. 1956

Actual Increase1956 vs.

1947�1956

Allied Ch. 89 $4.50 158% $7.22 12.6 $4.74 152% 16%

Am. Can 44 2.61 46 3.83 11.6 2.92 33 12

Am. S. & R. 54 5.43 12 6.10 9.0 6.67 (28) 23

Am. T. & T.�� 173 9.90 47 14.70 11.8 10.74 36 14

Am. Tob. 72 6.58 18 7.80 9.4 7.51 4 14

Beth. St. 49 2.88 44 4.15 11.5 3.83 8 33

Chrysler 77 8.95 4 9.28 8.3 2.29 (large) (276)

Corn Prod. 31 1.96 41 2.76 11.4 2.36 18 12

Du Pont 199 5.60 112 11.85 17.0 8.20 45 47

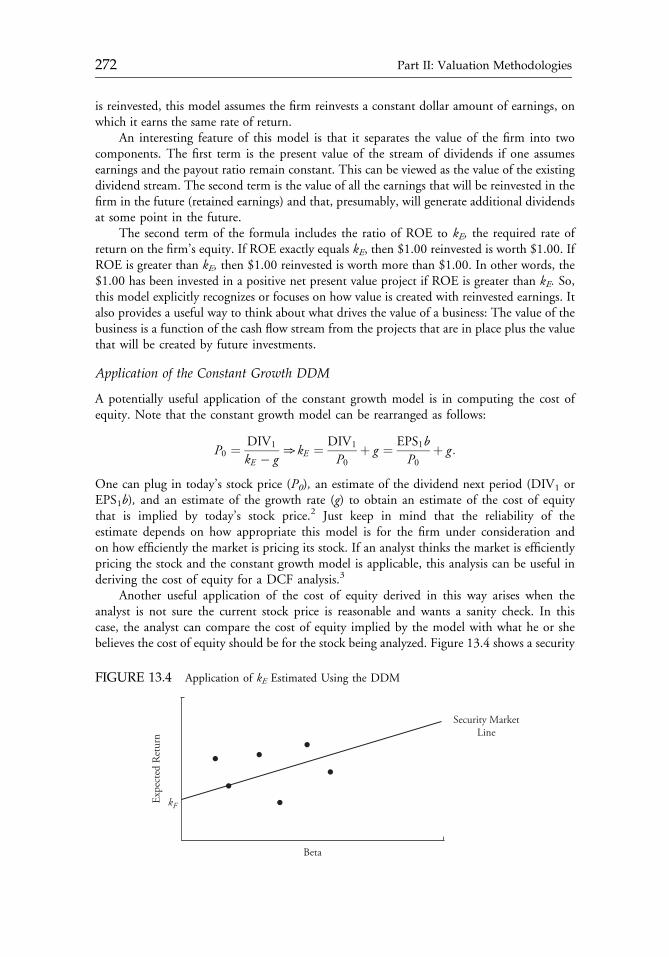

East. Kod. 104 3.49 93 6.62 15.4 4.89 36 37

Gen. Elec. 68 1.87 113 4.00 17.0 2.45 62 31

Gen. Foods 49 2.42 59 3.86 12.7 3.56 9 45

Gen. Motors 45 2.48 51 3.74 12.1 3.02 24 22

Goodyear T. 76 4.18 42 5.96 11.4 6.03 (21) 47

Int. Harv. 35 3.70 8 4.02 8.6 3.14 29 (215)

Int. Nickel 92 3.86 62 6.30 13.0 6.50 (23) 68

Int. Paper 101 6.40 40 9.03 11.2 7.05 28 11

Johns Man. 45 3.07 36 4.21 10.9 3.50 20 14

c01 12 September 2012; 13:13:37

14

Nat. Dist. 26 2.47 15 2.86 9.2 2.11 36 (215)

Nat. Steel 75 5.71 28 7.32 10.2 7.09 3 25

Proc. & Gam. 49 2.61 53 3.99 12.2 3.05 30 20

Sears Roebuck 28 1.82 38 2.53 11.0 2.20 16 18

S.O. Cal. 58 3.09 55 4.78 12.4 4.24 12 39

S.O.N.J. 67 2.85 72 4.99 13.8 4.11 21 44

Texas Corp. 74 3.48 62 5.66 13.0 5.51 3 59

Un. C. & C. 117 3.73 99 7.43 15.9 4.86 53 32

Un. Air. 62 3.65 45 5.31 11.6 7.66 (232) 93

U.S. Steel 69 3.51 57 5.55 12.6 6.01 (28) 73

Westinghouse 64 3.79 45 5.53 11.6 .10 (large) (297)

Woolworth 42 3.58 22 4.39 9.8 3.57 23 0

D.J. Ind. Av. 500 $27.50 50 $41.25 12.0 $35.80 15 30

�December 1956 price 4 indicated 1957�1966 earnings.��The basic formula is less applicable to A.T. & T. than to industrial issues.

c01 12 September 2012; 13:13:37

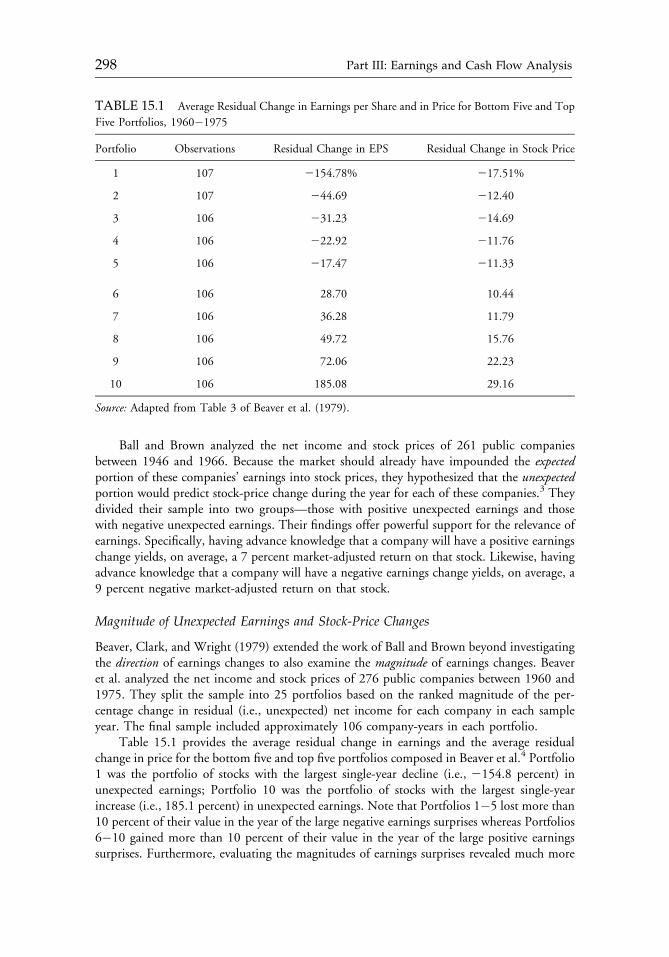

15

its relatively mediocre showing in recent years was the result of temporary factors, and that theelectric manufacturing industry is inherently so growth-assured that a major supplier such asWestinghouse is bound to prosper in the future.

These cases are clear cut enough, but other divergencies shown in our table are not soeasy to understand or to accept. There is a difference between these two verbs. The marketmay be right in its general feeling about a company’s future, but the price tag it sets on thatfuture may be quite unreasonable in either direction.

It is here that many analysts will find their challenge. They may not be satisfied merely tofind out what the market is doing and thinking, and then to explain it to everyone’s satis-faction. They may prefer to exercise an independent judgment—one not controlled by thedaily verdict of the marketplace, but ready at times to take definite issue with it. For this kindof activity one or more valuation processes, of the general type we have been illustrating, mayserve a useful purpose. They give a concrete and elaborated picture of the past record, whichthe analyst may use as a point of departure for his individual exploration and discoveries inthe field of investment values.

NOTES

1. On this point the philosophically inclined are referred to the recent article of DavidDurand on “Growth Stocks and the Petersburg Paradox,” in the September 1957 issue ofthe Journal of Finance. His conclusion is “that the growth-stock problem offers no greathope of a satisfactory solution.”

2. “Can We Improve Methods of Appraising Growth Stocks?” by R. A. Bing, Commercialand Financial Chronicle, Sept. 13, 1956; table on p. 24.

c01 12 September 2012; 13:13:37

16 Part I: Valuation Perspectives: Then and Now

CHAPTER 2SEEKING A MARGIN OF

SAFETY AND VALUATION

Matthew B. McLennan, CFA

The foremost goal of investing is to avoid the permanent impairment of capital,which we believe can be done primarily by investing in companies that provide amargin of safety. Cash and gold also play unique but significant roles in ourportfolios that are designed to preserve real wealth.

Nearly two decades ago, my wife and I visited a Buddhist temple on the west coast of Japan.As we walked into the monastery, we were approached by a monk with a piece of paper in hishand. My Western mind-set assumed that he was handing me a nondisclosure agreement or arelease of liability, but instead he was holding a sign, written in Japanese, that said if we wereto go into the temple, we had to do so with an open mind.

An open mind is also an essential element in the concept of margin of safety. A margin ofsafety is more about mind-set than it is about any specific algorithm, model, or set of preciseinputs. It is about temperament. In my presentation, I describe the mind-set that we haveembraced at First Eagle for defining and applying the concept of a margin of safety to helppreserve value over time for our clients.

TWO BASIC INVESTMENT GOALS

The most important element in adopting the right mind-set is to have a clear and sensible goal.But a lot of confusion exists in today’s investment industry about what an investor’s goals shouldactually be. The popular focus is on relative returns, tracking error, and similar measures, but

Reprinted from CFA Institute Conference Proceedings Quarterly (June 2011):27�34. This presentationcomes from the CFA Institute Security Analysis and the Search for Value conference held in Chicago on17�18 November 2010 in partnership with the CFA Society of Chicago. When this article was orig-inally published, Matthew B. McLennan, CFA, was a portfolio manager at First Eagle InvestmentManagement, LLC.

c02 12 September 2012; 13:19:18

17

such a focus obfuscates one simple truth—the first and most important goal of investing is toavoid the permanent impairment of capital. If people give an investment manager their hard-earned savings, the manager should first seek to not erode the real value of those savings. Themanager should also want to grow the purchasing power of those savings over time.

THE PRICE OF MONEY IS FAKE

Democracy and deflation are like oil and water. Virtually no popular appetite exists fordeflation. The consequence is that policymakers are doing “whatever it takes” to stabilize theprice outlook after the deflationary pulse of the global financial crisis, and the result is thatthe price of money today is actually fake. What do we mean by the term fake?

Short-term real interest rates are negative and meaningfully so. Fiscal deficits aimed atsustaining or smoothing aggregate demand are creating a burgeoning supply of governmentbonds. Governments are intervening directly in the long end of the bond market throughquantitative easing and long-dated sovereign liquidity facilities. Even bank debt during thecrisis was guaranteed. Central banks are adhering to exchange pegs, despite the fact thatfundamentals do not warrant the exchange pegs and are thus producing vast amounts ofreserve accumulation or the need for complicated bailout facilities to ease the required realadjustments.

In some ways, nature’s currency, gold, is an alternative store of value to the paper cur-rency conundrum because it cannot be printed, it is scarce, and its supply is not subject to apolitical process. But the challenge investors face is that gold has been symmetrically re-ratedupward in value as the quality of man-made money has deteriorated. There is no free lunch.

The primary goal of avoiding permanent impairment of capital is difficult to achieve inthe current environment because no risk-free instrument exists to help preserve capital in realterms with low credit or valuation risk. Thus, in a reflexive response, investors have begun toinvest heavily in longer-term fixed income for some incremental yield, despite low absoluteyields. Return envy has also led them to think about owning real assets that have growthpotential. Such thematic thinking has driven many investors to invest in the fully valuedemerging markets because they believe it is a sector that offers the real return and growth theyseek to compensate them for low yields in their fixed-income holdings. The problem is thatthis approach may not necessarily be the right way to find a margin of safety and to preservecapital. Both thematic decisions ignore individual security risks and the full valuation of bothlong-duration fixed income and emerging market equities, both of which require substantialfaith to be placed in policymakers, who have recently made mistakes.

THE FUTURE IS UNCERTAIN

At First Eagle, the core of our mind-set is not only a clear goal to preserve capital but also arecognition that it is necessary to have the humility to accept uncertainty, as well as to notplace excessive faith in the prescience of policymakers. We do not try to predict the next hugethematic growth trend. Let me illustrate why we internalize this philosophy by using theexample of a period in history that shares some parallels with today and in which emergingmarket bond investing was immensely popular, as it is today, because people had excessive

c02 12 September 2012; 13:19:19

18 Part I: Valuation Perspectives: Then and Now

confidence in the global financial architecture. The period I am referring to was, similar totoday, preceded by two decades of unprecedented global growth. As a result of this growth,it was a period of changing relativities in terms of the geopolitical backdrop—one super-power was peaking, another was in decline, and a third was on the rise. Inflation was low andstable and was believed to have been conquered. Global monetary orthodoxy reigned. Onlya year before the beginning of this period, the stock market had also lost 40 percent of itsvalue in a liquidity-induced panic caused by investment trust companies investing long andborrowing short. These are some interesting parallels.

The period I am describing is 1908�1911. An investor who had been investing for acouple of decades prior to that time would have experienced, before 1908, a fairly stable worldin which asset values did not appear to be out of balance. That investor may also have had avery precise sense of how to deploy capital in that world, but clearly that sense would soon beproven wrong.

A further warning that not all was certain after the 1907 market panic occurred when theTitanic, the unsinkable ship, sunk on its 1912 maiden voyage. Man cannot control nature.In 1914, an unfortunate assassination in the Balkans led to a domino-like chain reactionamong a complex set of geopolitical alliances that precipitated World War I. Man cannoteven guarantee rational behavior. Once the war broke out, the New York Stock Exchange,despite being on the other side of the Atlantic Ocean, closed for more than four months. Afterthe war, between 1918 and 1920, the Spanish flu pandemic wiped out nearly 5 percent of theworld’s population. The hyperinflation of the Weimar Republic, which broke the fabric of theGerman political economy and ultimately led to the rise of Hitler and World War II,materialized in 1921�1922, and was followed by a severe depression. One can only wonderwhat the economic and market prognosticators were predicting with seeming precision in1913. The lesson this historical comparison teaches is that the future is intrinsically uncertain.The crystal ball is foggy at best. The first step to becoming a sound investor is being honestwith oneself. The experience of one generation may be very different from the experience ofthe generations that both precede it and follow it.

But acknowledging that the future is murky is a very difficult thing for investors to do.Investors and managers alike tend to want to preserve their sense of ego. The sense of actuallybeing able to predict the future is an ego preservation device. At First Eagle, however, webelieve that in order to implement a margin of safety approach, it is fundamental toacknowledge that the future cannot be predicted with certainty. Only then does one demand amargin of safety at all times.

DEALING WITH MACRO RISK

Investors have several ways to attempt to control the macro risk in their portfolios: eschew thewrong systemic framework, hold liquid cash and gold, or hedge with options. Ironically, inmodern capital theory, the taught response to an assertion that the future is uncertain is forinvestors to be “fully invested” in the “market portfolio.” But if the goal is to preserve capitalin real terms, then investors should be willing to not own certain parts of the market port-folio—for example, those parts where property rights may not be respected, or where thegovernment is the leading shareholder with a primary goal to maximize employment and notcash flow, or where valuations are excessive, or where imprudent management behavior iscreating impairment risks.

c02 12 September 2012; 13:19:19

Chapter 2 Seeking a Margin of Safety and Valuation 19

Being fully invested at all times is also not a precondition for success. Some investorsargue that if cash has a low real return, a portfolio should never hold any cash because itcreates a drag on performance. Cash can be a residual of our investment approach. Becauseour goal is absolute—to find great businesses with good prices or good businesses with greatprices—if the markets become ebullient, as they were in 1999 and 2007, and we cannot findsufficient opportunities, then we wait. The cash builds in the portfolios. It is not a market-timing call. It is about having the flexibility and patience to commit to an absolute set ofstandards for underwriting across time. The return on the cash is not only its stated return butalso the option to deploy it in times of distress when liquidity is not otherwise available.

We like to commit capital when an absence of market liquidity exists. Consequently,some of our lowest cash levels ever occurred in March 2009. The reason was not because wewere calling the market bottom but because, as structural business buyers, we committedcapital when a wider margin of safety opened. Having a time-varying level of cash in aportfolio is actually an important part of dealing with uncertainty and enables equanimity inunderwriting standards.

We also hold gold in our portfolios. We view the value of gold as being inversely relatedto systemic confidence and positively related to political efforts to inflate the money supply.The reason for this relationship is that the supply of gold is exogenously determined bynature, not politics. All the gold ever mined remains in existence; the supply is thus not afunction of any one year of mining output but rather the cumulative stock of all of the goldever mined. The supply of gold barely moves by more than 1 percent based on the miningoutput in any given year. Historically, the relative stability of gold’s supply has meant thatgold’s value has varied inversely with confidence in a man-made economic system becausethe supply of man-made money usually becomes less predictable in economic distress. In theUnited States during the late 1920s, late 1960s, and late 1990s, when people believed thatthe economic system was strong, markets boomed, confidence was high, and gold wasinexpensive relative to the price of equities and personal incomes. But when the economicsystem frayed in the 1930s, 1980s, and most recently in 2008�2009, gold re-rated upwardsubstantially versus the price of equities and personal incomes.

Hence, gold is used at First Eagle as a source of ballast in our portfolios and has typicallybeen about 10 percent of the overall portfolio. We believe that if the allocation were 15percent or higher, it would start to become a directional view on gold, which is a situation wewant to avoid, given that we know we cannot predict future systemic confidence with pre-cision and we recognize that gold can suffer a generation of poor returns when, and if, sys-temic faith is restored. Yet, we also would not typically want it below 5 percent of the overallportfolio because it would not provide material ballast.

Another strategy for coping with macro risk is hedging with options. Hedging a portfoliowith options, however, requires paying very close attention to the cost of the potential hedgebecause it is time-definite. Investors often adopt tail-hedging strategies when implied volatilityis high and when asset values are cheap, such as after a major market correction. But ifinvestors use a fundamental approach to value options, we believe it becomes possible toidentify periods of time when options are expensive or cheap in fundamental terms. The timeto buy tail insurance is when asset values are high and implied volatility is low. Yet, mostpeople seem to do the opposite, which is an example of the rear-vision investing that webelieve is going on in the world today. Finally, the purchase of options often involves anassessment of counterparty risk. To the extent that an investor is trying to hedge for a tailevent, what matters is what the counterparty risk will be in the tail state of the world ratherthan in the current state of the world.

c02 12 September 2012; 13:19:19

20 Part I: Valuation Perspectives: Then and Now

OWNING AN ENTERPRISE PRESERVESPURCHASING POWER

To preserve purchasing power, investors need to not only avoid permanent impairment ofcapital but also to keep pace with the continual growth of human potential. Investing ina business enterprise allows investors to participate in humanity’s capacity to continueimproving.

The growth in human potential can be measured by numerous improvements over time:the mechanics of trade over roads, rails, and ports; the faster diffusion of ideas, from the speedof a horse to the speed of microprocessors and routers; the potential for greater energyproductivity harnessing solar, wind, and nuclear power versus burning timber, coal, and oil;the increased life expectancy through biotechnology and public health initiatives; and thebroadening of property rights.

Preserving purchasing power in real terms is not only about participating in the marchof man but also about keeping pace with a monetary stock that is growing steadily. In aworld of inflation-targeting orthodoxy, modest deflation is not deemed an acceptable out-come. The central banks of advanced economies are practicing some unconventional mon-etary “therapy” to try to sustain a rising monetary stock. For example, the U.S. FederalReserve is trying to put a floor under U.S. inflation, a policy that is producing commensu-rately greater inflationary pressures in the emerging markets, which are U.S. dollar reservecurrency accumulators. As a result, Brazil, Russia, India, and China (the BRIC) have arguablybecome the monetary epicenters of the world. The annual growth rate for M2 (the amount ofmoney in circulation) in most of these economies has been averaging more than 15 percent,which eclipses the credit growth rate in the United States during the last decade by nearlythreefold.

Owning a business is akin to owning the source of productivity. If investors own busi-nesses that generate real cash flow, then that cash flow over time will also scale with the level ofnominal activity and capital may be preserved. The result is that investors will come full circleto the first goal of investing: preserving capital, albeit paradoxically through the “risky”ownership of an enterprise.

SEEK A MARGIN OF SAFETY

The strategic need to be an owner of an enterprise while fundamentally accepting that theworld is an uncertain place means investors must demand a margin of safety on eachinvestment that they make. The best way to create a margin of safety is from the bottom up,by analyzing risk security by security.

Karl Popper, who was a leading figure in the field of scientific methodology, said in hisbook Objective Knowledge that “the main difference between Einstein and an amoeba is thatEinstein consciously seeks for error elimination.”1 It sounds trite, but it is a very profoundrealization. Many investors are simply trying to identify the next great wave of new-erainvestment, such as BRIC recently or technology in the late 1990s, and they try to catch thatparticular wave only to get dumped. We believe a better approach to investing is to attempt tomake the least number of bad choices at the individual security level. To invest with themind-set of Einstein is not to try and call the market’s “ups and downs” but rather toavoid errors.

c02 12 September 2012; 13:19:19

Chapter 2 Seeking a Margin of Safety and Valuation 21

From a bottom-up standpoint, investors should try to avoid the four following paths topermanent destruction of capital: overpayment for a business, business model substitutionrisk, vulnerability from the wrong capital structure, and management dilution. A lot of valuemanagers were wrong in 2008 because they had a unidimensional sense of a margin of safetythat was centered solely on price. Price is an important component of a margin of safety, but amultifaceted approach that incorporates the business model, capital structure, and manage-ment integrity is preferable.

Valuation

Businesses can be parsed into two broad categories: commodity businesses and franchisebusinesses.

A commodity business does not have a competitive advantage. Its intrinsic value isbasically its sustainable earnings power divided by its cost of capital. In growing its capital stock,it does not create value because it is only earning its cost of capital. If its capital stock shrinks,however, it will produce more free cash flow than earnings because it will release surplus capitaland not need as much to invest in the future. In the absence of product substitution ormanagement stupidity, the valuation exercise for a commodity business is relatively straight-forward; it is essentially about identifying the sustainable earnings power and the nominalcost of capital.

A franchise business has some competitive advantage that enables it to generate very highincremental returns on capital. It is like a royalty on a slice of the global economy. On the onehand, however, its growth requires limited capital and thereby creates substantial value. Onthe other hand, if it loses relevance and shrinks, no meaningful capital is released and valueerodes, and there is no shield against this fade. Valuing a franchise business, therefore, requiresthe discriminating investor to disentangle the concepts of an objective margin of safety and asubjective margin of safety because, counterintuitively, the range of intrinsic value outcomes isbroader for a franchise business than a commodity business. The subjective margin of safetyis based on the investor’s view of the franchise relevance and prospects for the future. Theobjective margin of safety is based on entry price. The value of a franchise business, for thosewithout a biased sense of how the company will evolve in relevance, should conservativelyassume no real growth but allow for pricing power to pass through the effects of inflation. Thenuance here relative to valuing a commodity business is that for a commodity business,inflation produces lower free cash flow than earnings because the maintenance capitalexpenditures will exceed historical book depreciation. In fact, the capital stock will have togrow by the amount of the inflation, thereby offsetting all the benefits of that growth. Thus,for a commodity business that is growing, use a nominal discount rate to discount earnings.In the case of a franchise business, however, take the business’s earnings power divided by thereal cost of capital to estimate intrinsic value. We use “real,” not “nominal,” cost of capitalbecause inflation passes through a franchise’s earnings stream without much capital drag—earnings are basically free cash flow irrespective of the level of inflation. In a normal cost ofcapital environment, the average commodity business is worth a low double-digit multipleof earnings (in the low teens) and the great franchise business, assuming no real growth, is wortha higher multiple of earnings (in the high teens). Assuming an unleveraged capital structure, thisvalue translates to high single-digit earnings before interest and taxes (EBIT) multiples forcommodity businesses and lower- to mid-teens EBIT multiples for franchise businesses.

Because of the wide range of outcomes, franchise investing requires not only an objectivemargin in price but also a subjective margin of safety in the analysis of franchise fade. We only

c02 12 September 2012; 13:19:19

22 Part I: Valuation Perspectives: Then and Now

buy franchise businesses that are priced for fade—that is, trading at a multiple lower than theinverse of their real cost of capital—and we try, while acknowledging the limits of our crystalball, to focus on those that have the potential to endure or grow in relevance.

In simple terms, whether buying a commodity business at a discount to intrinsic value ora franchise priced for fade, typically we are buying businesses at single-digit multiples ofEBIT. Investing in equities that are priced for fade creates an error-tolerant system. If abusiness does not produce the expected results, a margin of safety exists in the price. Takingthe concept one step further, if investors have already selected from the lower part of theequity universe that is priced for fade, it is possible to reduce the percentage of companies thatwill actually fade by focusing on the subjective margin of safety. The objective price is bal-anced against the subjective fade. Unfortunately, fade cannot be completely eliminated.

The ironclad rule of the universe—entropy—makes it self-evident that nothing willreplicate itself into perpetuity and that all forms of order are local and transient. The same lineof thinking exists in evolutionary theory. The concepts of fade and entropy mean investorsneed to think carefully about business model erosion.

Business Model Erosion

Investors are taught to think of businesses as perpetuities, and the typical dividend discountmodel projects 3�4 percent growth into perpetuity. Instead, investors should assumethat every business is on a path to some form of irrelevance. The only unknown is howlong the current earnings power can be sustained or increased in a transient fashion. Ratherthan assume perpetuity, investors should ponder the intrinsic duration of an earningspower stream.

For a commodity business, the basis of earnings power duration is asset life, assetreplacement value, and the cost-curve positioning of the business relative to competitors. Theearnings power in a commodity business is shielded by the replacement value of its long-livedassets. For a franchise business, the basis of earnings power duration is a specific and sus-tainable competitive advantage. The focus of our analysis is on identifying local scaleadvantages and the degree of customer captivity.

So, investors should begin their investment selection process within the universe ofequities that are priced for fade and then identify the subset of businesses they want to invest inthat are less likely to experience fade. If the business is commodity-like in nature, it must havelong-life asset value protection. If the business is franchise-like in nature, it must have intan-gible asset protection through the strength of its local market position and customer captivity.

Focus on Assets, Not on Residual Equity

Another area to consider, in keeping with the concept of a margin of safety, is seeking amaterial discount to the intrinsic value of a company’s assets. Equity should be viewed asa residual claim on a business. Equity has value only after debtholders, pension claimants,contingent litigants, and minority interests are satisfied. At First Eagle, we prefer to buy assetsat 70 cents on the dollar based on capitalizing EBIT, not post-tax earnings. On the basis ofthat asset value, we decide what price we are willing to pay for the equity, taking into accountthe company’s capital structure and other sources of contingent leakage.

A good example of the importance of distinguishing asset value from equity value is howan investor would obtain a margin of safety on a wholesale-funded bank that does not have alot of non-balance-sheet income. A bank typically has about 10 percent of its assets in equity

c02 12 September 2012; 13:19:19

Chapter 2 Seeking a Margin of Safety and Valuation 23

with the remainder in deposit- and debtholder liabilities. If the bank does not have a retaildeposit franchise, then most of the 90 percent nonequity liabilities will be some form of debtissued at market prices. Thus, no matter what investors pay for a wholesale bank’s equity, theyare paying at least 90 cents on the dollar for its assets. The equity sliver exists only after theother claimants are paid. It is thus hard to obtain a margin of safety on the assets deemed to beacceptable unless there is some form of below-market deposit funding that creates incrementalvalue or some other source of material intrinsic value based on fee-earning businesses inde-pendent of the balance sheet lending activity.

The margin of safety does not have to exist in the price paid for a company’s stock but inthe price paid for its assets. For equityholders, the asset value may be there in the long term,but this does not help them if the assets transition to the hands of the senior secured debt-holders in a short-term funding crisis. There is no point in owning assets that have somematerial probability of being taken away. Consequently, investors need to pay a lot ofattention to the quality of the capital structure.

Management

The management of an enterprise is also very important. For a typical equity that trades at 10times gross cash flow (i.e., earnings plus depreciation), the management team will redeployapproximately 10 percent of the face value of an investor’s investment every year. The realityis even more dramatic when mergers and acquisitions (M&A) via new security issuance areincluded. Over a long holding period, such as more than five years, the management teamcould easily redeploy 50 percent of the gross cash flow in market capitalization in mainte-nance capital expenditures, discretionary capital investments, security repurchases, and M&Aactivities. It is important to thus determine what amount of gross cash flow an investor willreceive back as dividends and whether management’s retained capital deployment is accretiveor dilutive in nature.

Investors should demand a larger valuation margin of safety in companies with thefollowing management mistakes: (1) implementing poor pricing strategies, such as gougingthe customer on price for short-term earnings power or engaging in destructive pricing warsdespite an oligopolistic market structure; (2) engaging in fad-driven business migration, suchas diversifying away from an advantaged local position or stretching to engage in “globali-zation” or product diversification; (3) showing financial imprudence, such as adding largeamounts of leverage or putting balance sheet growth ahead of secular market trends; and(4) practicing myopia, or “milking” the business.

Perhaps one of the best indicators of management prudence is free cash flow generation.Management teams that are focused on generating free cash flow relative to earnings typically aremaking conservative accounting choices, growing within the speed limit of their business, andmaking reasoned business decisions. Seek managers who are prudent owners/entrepreneursfocused on sustaining culture and thoughtfully distributing or retiring capital, and avoidexpeditionary management teams that are aggressive, new-era thinkers willing to bet the ranchon dilutive terms to feed their ambition.

FLEXIBILITY TO LOOK DIFFERENT

Combining all elements of the margin of safety is more important than believing you have acrystal ball. The successful turning points in First Eagle’s investment track record have oftenbeen acts of omission: being out of Japan in the late 1980s, being largely out of technology in

c02 12 September 2012; 13:19:19

24 Part I: Valuation Perspectives: Then and Now

the late 1990s, and being largely out of financials in 2007 and 2008. As I said earlier, we donot have a crystal ball; we simply could not find enough businesses during those times in thosemarket environments that embodied the valuation margin of safety and had the sustainableearnings power, conservative management behavior, and conservative balance sheet evolutionthat we demand. Our peripheral vision for macro capital preservation was the sum total of aset of prudent micro acts of omission.

Almost by definition, a passive approach to investing (i.e., mimicking an index) leads tooverweighting the sectors that experience the bubbles because it is in those sectors that thegreatest expectations for complacency exist in the system. Most managers seek a low trackingerror against a benchmark. The whole notion of minimizing risk by minimizing tracking erroris a logical non sequitur. The goal of avoiding permanent impairment of capital means thatsometimes investors need to stay away from sectors that embody the wrong set of expecta-tions, even if they are the biggest sectors of the market. Most investment managers are notstructured to flexibly implement such an approach.

At First Eagle, we view the market as if it were a piece of marble. The goal of errorminimization in structuring a portfolio is similar to chipping away the unwanted pieces ofmarble to let the statue emerge from within. We do not own the whole block of marblejust for the sake of owning it. The point of a margin of safety approach is not to ask, Dowe overweight Japan versus the United States? Do we own one sector versus another?Rather, the point is to find clusters of investments that we believe make sense from amargin of safety perspective and thus help in attaining the goal of preserving capital inreal terms.