Embed Size (px)

Citation preview

BRAND VALUATION SERIES

TELECOMS/ENTERTAINMENT

+30%FINANCIAL

+26%

AUTOMOBILES

+23%

FOOD, DRINKS & ALCOHOL

+5%

OTHER

+10%

TOP50 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

1617

1819

2021

2223

2425

262728293031323334353637383940

4142

4344

4546

4748

4950

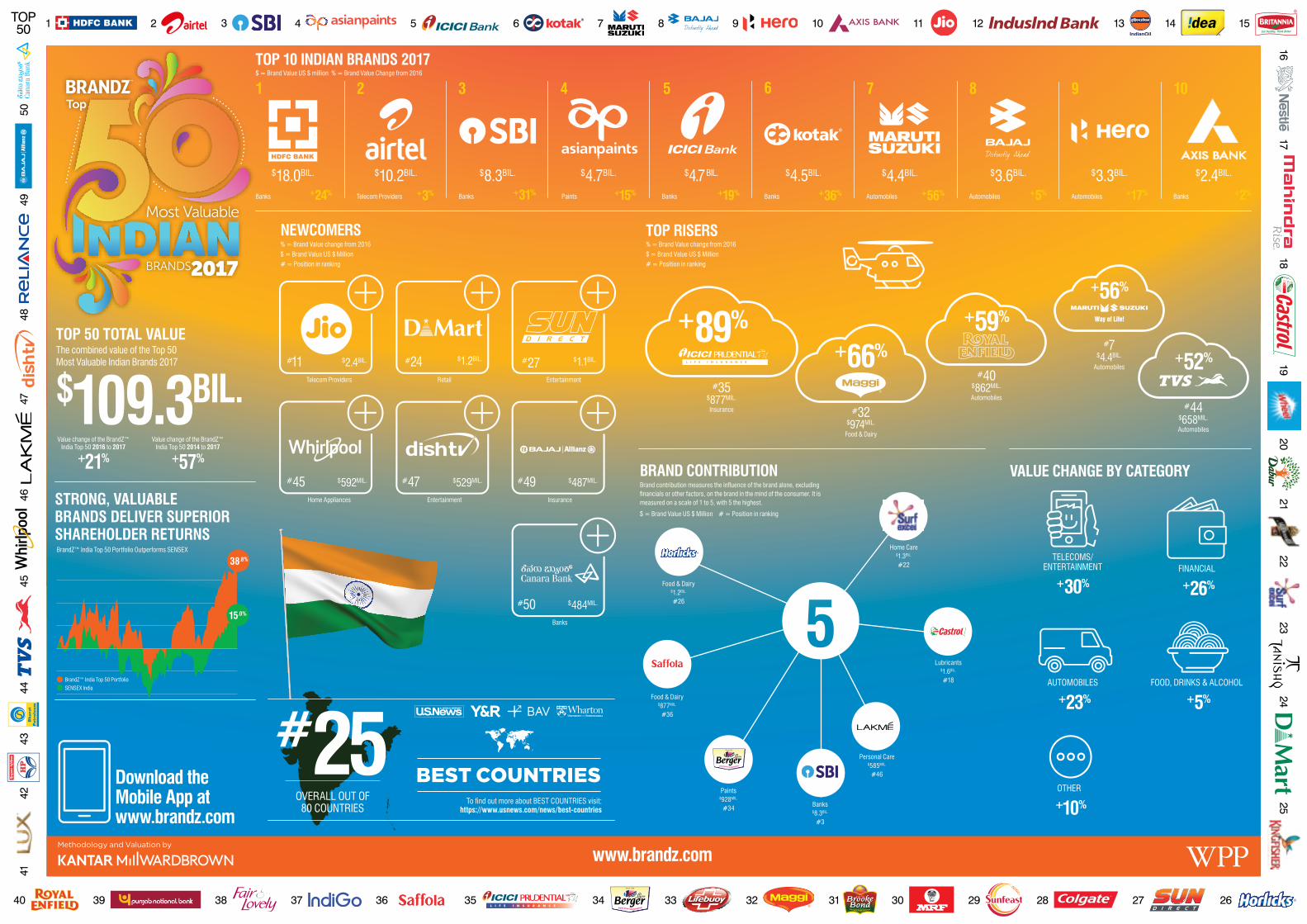

$109.3BIL.

+21% +57%

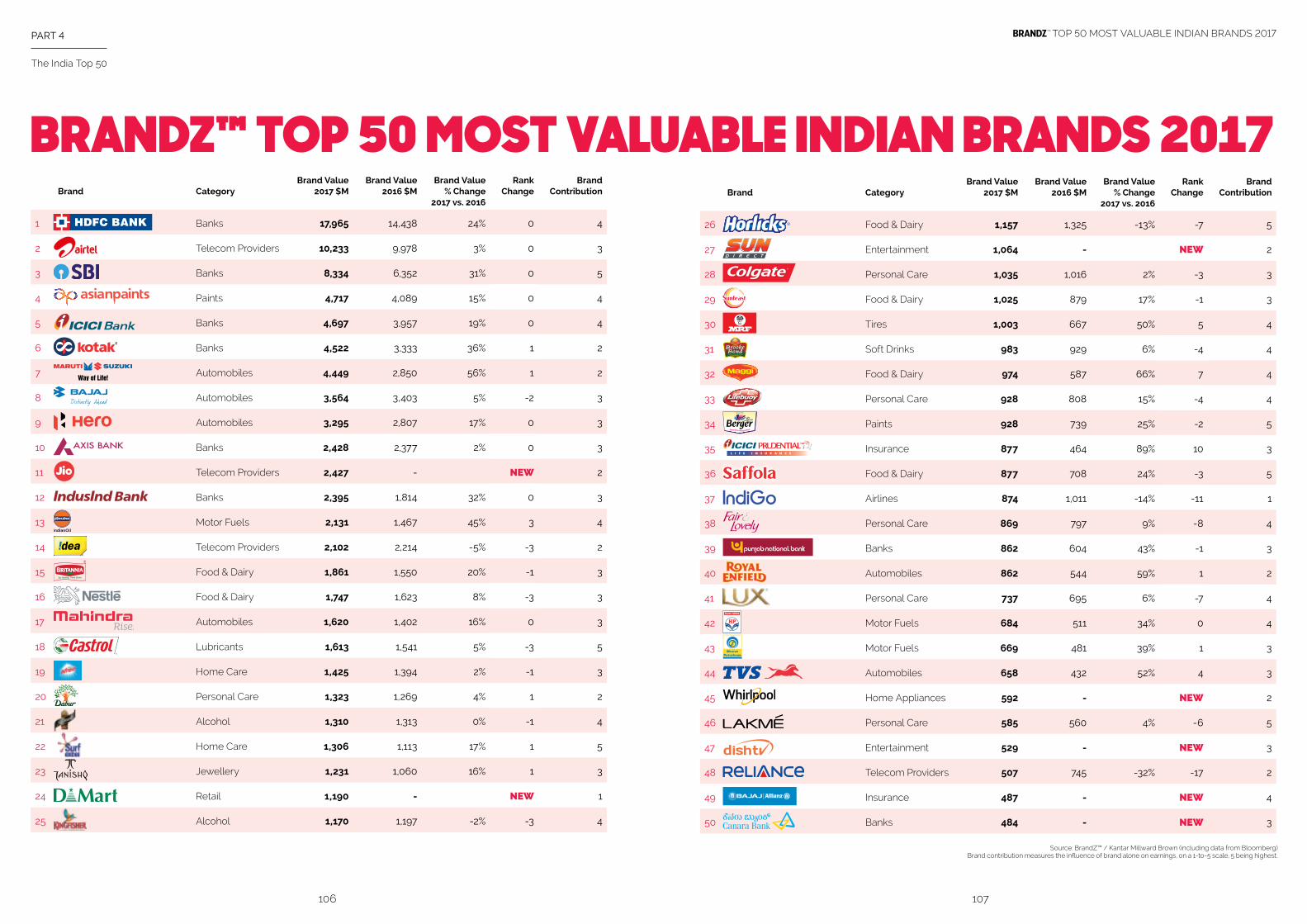

TOP 50 TOTAL VALUEThe combined value of the Top 50 Most Valuable Indian Brands 2017

Value change of the BrandZ™ India Top 50 2016 to 2017

Value change of the BrandZ™ India Top 50 2014 to 2017

TOP 10 INDIAN BRANDS 2017

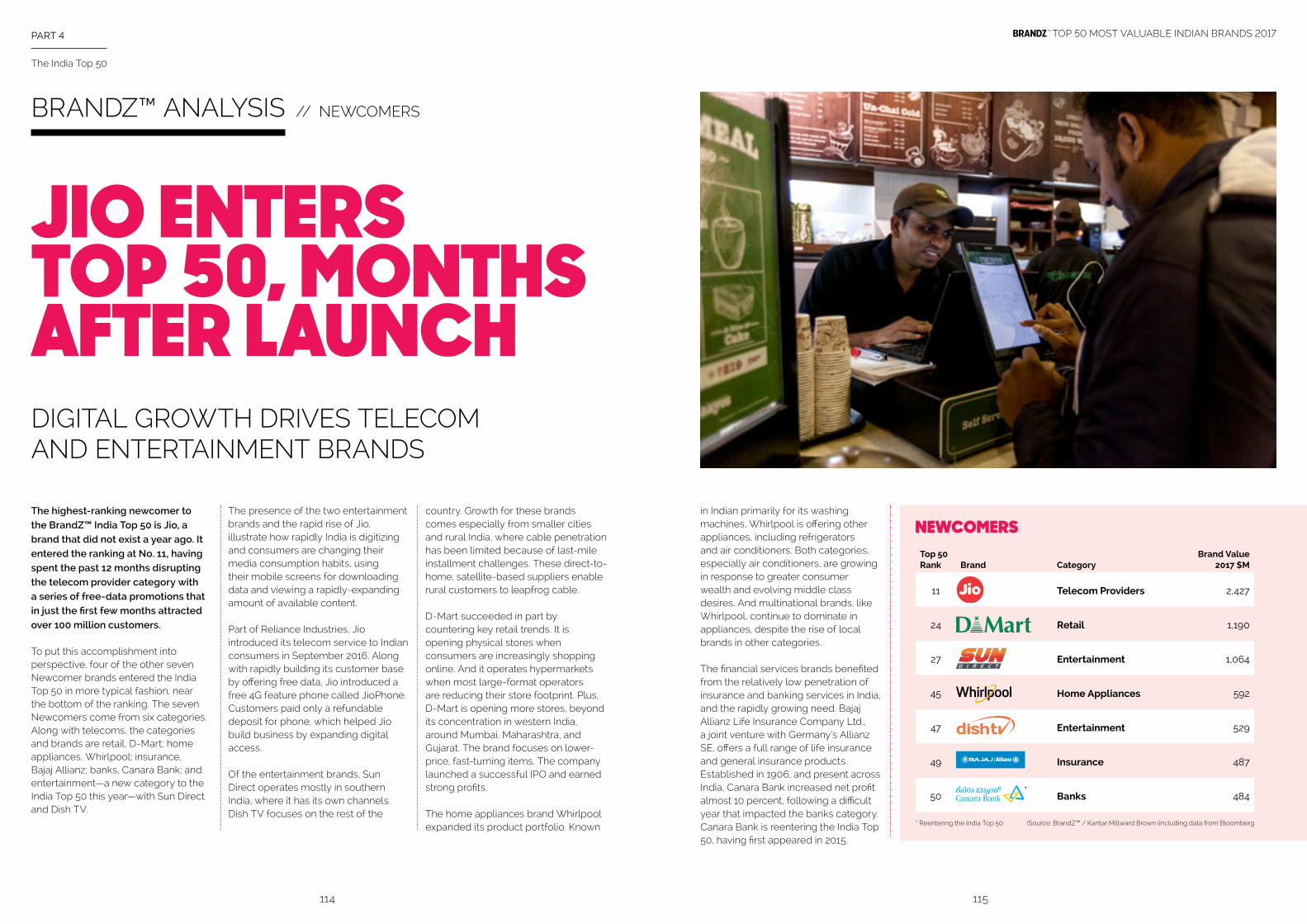

NEWCOMERS

$ = Brand Value US $ million % = Brand Value Change from 2016

% = Brand Value change from 2016

$ = Brand Value US $ Million

# = Position in ranking

+31%Banks

3

$8.3BIL.

+15%Paints

4

$4.7BIL.

STRONG, VALUABLE BRANDS DELIVER SUPERIOR SHAREHOLDER RETURNSBrandZ™ India Top 50 Portfolio Outperforms SENSEX

BrandZ™ India Top 50 Portfolio

38.8%

15.0%

SENSEX India

$2.4BIL.

$592MIL. $529MIL. $487MIL.

$484MIL.

$1.2BIL. $1.1BIL. #11

#45 #47 #49

#50

#24 #27Telecom Providers

Home Appliances Entertainment Insurance

Banks

Retail Entertainment

BRAND CONTRIBUTIONBrand contribution measures the influence of the brand alone, excluding financials or other factors, on the brand in the mind of the consumer. It is measured on a scale of 1 to 5, with 5 the highest.

$ = Brand Value US $ Million # = Position in ranking

TOP RISERS% = Brand Value change from 2016

$ = Brand Value US $ Million

# = Position in ranking

+19%Banks

5

$4.7 BIL.

+36%Banks

6

$4.5BIL.

+56%Automobiles

7

$4.4BIL.

+5%Automobiles

8

$3.6BIL.

+17%Automobiles

9

$3.3BIL.

+2%Banks

10

$2.4BIL.

+89%

$877MIL.

#35Insurance

+66%

$974MIL.

#32Food & Dairy

+59%

$862MIL.

#40Automobiles

+56%

$4.4BIL.

#7Automobiles

+52%

$658MIL.

#44Automobiles

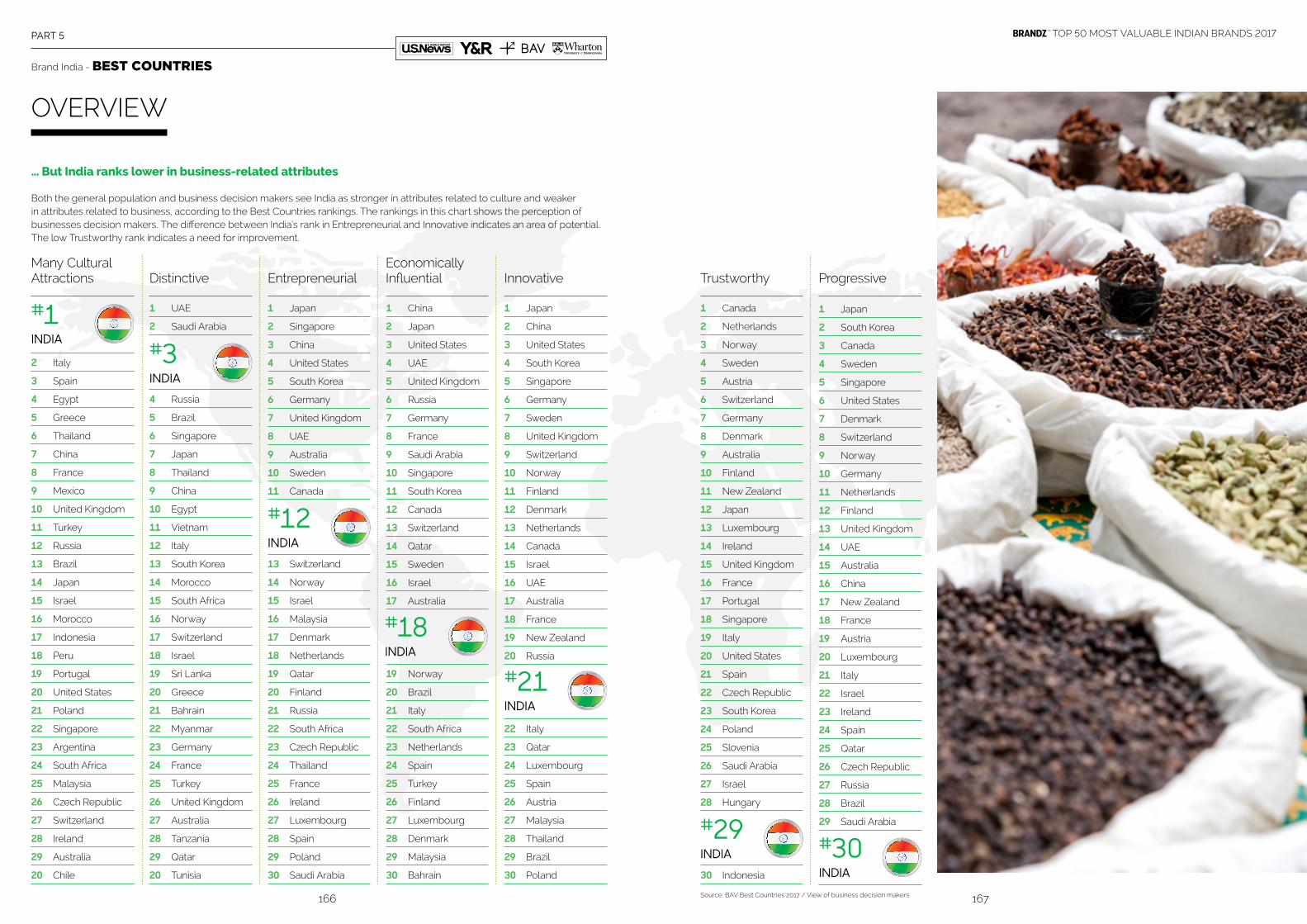

To find out more about BEST COUNTRIES visit: https://www.usnews.com/news/best-countries

OVERALL OUT OF 80 COUNTRIES

#25Download the Mobile App at www.brandz.com

Banks

$18.0BIL.

+24%

1 2

+3%Telecom Providers

$10.2BIL.

Home Care$1.3BIL.

#22

Personal Care$585MIL.

#46

Lubricants$1.6BIL.

#18

Banks$8.3BIL.

#3

Paints$928MIL.

#34

Food & Dairy$877MIL.

#36

Food & Dairy$1.2BIL.

#26

www.brandz.com

VALUE CHANGE BY CATEGORY

03

Thought Leadership

86 Valuation by Amarjeet Thakur, Mirum

88 New India by Arnab Bhowmik, Kantar Millward Brown - Firefly Practice

90 Unicorns by Sonya Misquitta and Amanda Mendes, Grey

92 Brand Vulnerability by Hareesh Tibrewala, Mirum

94 Advertising by Milind Pathak, Madhouse

96 Future-Ready Brands by Shaziya Khan, J. Walter Thompson

98 Social Responsibility by Sunil R. Shetty, Contract

100 Apps by Varun Jain, Kantar Millward Brown

02

Market Knowledge & Intelligence

40 Key Facts and Figures

44 Disruption

46 Consumers

64 Urban-Rural

66 Digital

76 Media

78 OUR INSIGHTS

05

Brand India

158 Best Countries

162 Overview

168 Methodology

170 Soft Power

174 India & China

176 Cultural Rankings

06

Brand Building Best Practices

186 Complexity by Aditya Kilpady, Contract

190 Storytelling by Anvar Ailkhan, J. Walter Thompson

194 Spending by Dia Kirpalani, Contract

198 Loyalty by Divya Khanna, J. Walter Thompson

202 Social Media by Karthik Nagarajan, GroupM

204 Startups by Parul Budhiraja, Contract

208 Social Context by Sanjana Mathur, Landor

210 Trust by Siddhant Lahiri, Rediffusion Y&R

214 OUR INSIGHTS

07

Resources

220 BrandZ™ Brand Valuation Methodology

224 BrandZ™ Reports, Apps, and Powered by BrandZ™

228 WPP Resources

230 WPP Company Contributors

235 WPP in India

236 WPP Company Brand Building Experts

238 BrandZ™ India Top 50 Team

240 BrandZ™ Contact Details

241 BrandZ™ Mobile

04

The India Top 50

106 The India Top 50 Ranking

108 BrandZ™ Analysis

Top Risers

Newcomers

Brand Contribution

120 Vitality Quotient

Overview

India Top 50

Brand Value

Brand Value Growth

Resilience

Love

136 C-Suite Interviews

Suparna Mitra Chief Marketing Officer, Titan Company Ltd.

Ajay Kakar, Chief Marketing Officer, Aditya Birla Capital Ltd.

Siddharth Banerjee, Executive Vice President, Marketing, Vodafone India

150 OUR INSIGHTS

01

Introduction

14 Overview

20 BrandZ™ India Top 50 Portfolio

24 Key Findings

28 Cross-Category Trends

32 Takeaways

36 OUR INSIGHTS

8 Welcome David Roth, CEO,

The Store WPP, EMEA & Asia

CONTENTS

WELCOME

BRANDS NEED KNOWLEDGE AND INSIGHT TO KEEP PACE

TOP 50 GROWS 21 PERCENTIN RAPIDLY CHANGING INDIA

←

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

David RothCEO, The Store WPP, EMEA and [email protected]: davidrothlondonBlog: www.davidroth.com

India is changing rapidly, with GDP

defying expectations and growing

faster than all other major economies,

despite several recent disruptions—

demonetization and the goods and

services tax (GST)—aimed at driving

the economy even faster. This speed

presents brands with a dilemma:

move too cautiously and miss

opportunities; or move too quickly

and make avoidable mistakes.

We see this momentum in the BrandZ™ Top 50 Most Valuable Indian Brands 2017, which appreciated 21 percent this year, and 57 percent over the past three years, outpacing the value growth of both the China Top 50 and the Global Top 50. Similarly, the BrandZ™ India Top 50 Portfolio rose 38.8 percent over the past three years, more than twice the rate of SENSEX, the Indian stock market index, which increased just 15.0 percent—demonstrating how valuable brands deliver superior stockholder returns.

This dynamism is also apparent in the churn of the India Top 50 and the emergence of new Indian brands. Only 38 brands that were in our 2014 BrandZ™ India Top 50 remain in the 2017 India Top 50. A brand needed to grow 48 percent just to retain its rank. Rising in the ranking required a brand to increase its value 106 percent, around

twice the growth rate of the India Top 50 overall.

Brands that remain in the India Top 50 are significantly healthier than Indian brands overall, based on their Vitality Quotient (VQ), our new BrandZ™ measurement of brand health. In fact, the health of the India Top 50 brands is comparable to the health of the Global Top 50, the most valuable and powerful brands in the world.

Which brings up the question of how the world views India, a vital topic at this point in India’s rise to global player. Business decision makers rank India low on some business dimensions, like transparency, but they rank India No. 2 in the Movers category of up-and-coming economies. This is one of many findings from Y&R’s BAV Best Countries study, which we present here for the first time in a special section called Brand India.

The consumers driving all this change and growth no longer live only in Mumbai, Delhi, Chennai, or some other major metro. They live throughout India, in cities of all sizes and in rural areas, too. Marketers need to think about Multiple India’s—an India where people want to be the best they can be—wherever they live and whatever their background.

In these fast-changing, complicated circumstances, what should marketers do to identify opportunities and avoid mistakes? To start, I suggest reading this report—closely. It is an example of what we at WPP call “horizontality”—informing clients with our extensive experience creating and building valuable brands, based on knowledge and insights from our presence in 112 countries. We’ve been in India for over 85 years.

Knowledge, Intelligence, and Insights

We take a 360-degree view that includes market research, media management, futures, advertising, digital, promotion, public relations, public affairs, shopper marketing, content creation, and activation. We begin with WPP’s proprietary BrandZ™ database, which includes information from over 3 million consumers about their attitudes about (and relationships with) 120,000 brands in 414 categories across 51 country markets. All that produces more than 4.6 billion data points.

98

Throughout this report you’ll find the knowledge, intelligence, and insights necessary to keep up with brand developments in fast-changing India, and scattered throughout these pages you’ll also find prescriptive action points for building valuable brands, provided by some of the most cutting-edge thinkers and practitioners from WPP companies in India. Here are just a few highlights to think about as you get into the details:

VALUE The Indian notion of value is changing. The change is evident in fast moving consumer goods (FMCG), where consumers increasingly prefer brands that specifically meet Indian preferences. That’s often a local Indian brand, but brands owned by multinationals are responding. Ultimately, it’s not about provenance, but the right combination of a locally relevant product and a fair price.

SPENDINGIn a vast country of 1.3 billion people, 22 official languages, and multiple cultural roots, the market is remarkably segmented. Our research has identified a sub-segment of FMCG shoppers that we call “Elites,” people who spend more on FMCG than other wealthy consumers. It’s an important opportunity—one of many.

TRUST Indian consumers today are less likely to accept a brand message before verifying it with online research. Still, one of this year’s important stories was the rebound of Maggi, the instant noodle brand that lost consumer trust during a food safety crisis a few years ago, and regained trust by fixing its problems and leveraging its substantial brand equity.

One of our key WPP strengths—and a benefit for our clients—is that when we say we cover the world of brands, that’s exactly what we mean. We have assembled an extensive library of brand reports and I invite to you access them with our compliments at BrandZ.com. Here are just some of the reports you will find there: the BrandZ™ Top 100 Most Valuable Global Brands; the BrandZ™ Top 100 Most Valuable Chinese Brands; the BrandZ™ Top 50 Most Valuable Latin American Brands; and the BrandZ™ Top 50 Most Valuable Indonesian Brands. In addition, I recommend these recently published titles: Spotlight on Cuba, Spotlight on Myanmar, Spotlight on Mongolia, and Leaders in the Hot Seat: Behind the brands that shape lives and build value.

We have the data, knowledge, experience, insight, determination, and single-minded purpose to help you

create and build valuable brands. To learn more about how to harness our passion to work for your brand, please contact any of the WPP companies that contributed expertise to this report. Turn to the resource section at the end of this report for summaries of each company and the contact details of key executives. Or feel free to contact me directly.

Sincerely,

David [email protected]: davidrothlondon

WELCOME

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

1110

INTRODUCTION

GROWTH MOMENTUM INDICATES POWER OF HEALTHY BRANDS

INDIA TOP 50 BRAND VALUE RISES 21% DESPITE MARKET DISRUPTIONS

The BrandZ™ Top 50 Most Valuable

Indian Brands 2017 increased 21

percent to $109.3 billion, in a year

marked by serious disruptions,

particularly from government

initiatives to reform the economy.

Following a 2 percent decline a year

ago, the ranking resumed its positive

momentum, with value up 57 percent

since 2014, when the Top 50 brand

value totaled $69.6 billion.

The India Top 50 outpaced both the BrandZ™ Global Top 50 and China Top 50, which grew 32 percent and 46 percent in value over the same period. The composition of the Top 50 shifted over three years with 38 local Indian brands in the Top 50 compared with 35 in 2014, while Indian brands owned by multinationals declined from 15 to 12.

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

1514

OVERVIEW

The strong brand value increase reflected consumer optimism, with some regional variations, and a strong performance by financial brands, which comprise 39 percent of Top 50 value. Banks rebounded from bad-debt problems. ICICI Prudential, an insurance brand, led in value appreciation, increasing 89 percent. HDFC Bank retained the No. 1 rank in the BrandZ™ India Top 50, rising 24 percent in value, following a 15 percent increase a year ago.

The BrandZ™ Top 50 value increase also echoed the robust appreciation of the Indian stock exchange, which soared to record levels. The BrandZ™ Top 50 Portfolio of stocks continued to outperform SENSEX India, a weighted index of 30 stocks on the Bombay Stock Exchange. The BrandZ™ India Top 50

Portfolio rose 38.8 percent over the past three years, more than twice the rate of SENSEX, which increased just 15.0 percent, demonstrating how valuable brands deliver superior stock holder returns. In addition:

All but five Top 50 brands increased in value, and growth crossed categories, led by a 30 percent increase in telecom providers/entertainment, followed by financial, up 26 percent, and automobiles, with a 23 percent increase.

Six of the seven Newcomers are local Indian brands. And two Newcomers—Sun Direct and Dish TV—inaugurate the entertainment category in the India Top 50, reflecting changing consumer viewing habits and greater variety of content.

PART 1

Introduction

Brands invested more in digital media, which led all media segments in percentage rise in spending. TV remained strong, however, and India was the only major market where investment in traditional media continued to grow.

The India Top 50 exhibited strong brand health, as measured by a new BrandZ™ metric called Vitality Quotient (VQ), which assesses brand health based on five indicators—Brand Purpose, Innovation, Communications, Brand Experience, and Love. The India Top 50 scored 110, identical to the Global Top 50, on an index where 100 is average.

Growth despite disruptions

Brand value increased despite successive market disruptions,

some strategically implemented by the government of Prime Minister Narendra Modi to improve conditions for doing business in India, and realize the government’s vision for a New India with greater stature abroad and economic equality at home.

With demonetization, implemented in November 2016, the government banned certain cash currency to reduce the underground economy, increase tax revenues, and accelerate the shift to digitization and mobile wallets. On July 1, India implemented a national goods and services tax (GST), a type of VAT intended to simplify a complicated combination of state and local taxes and add transparency.

The shock of demonetization impacted brands in different ways, depending

on how dependent the category was on cash transactions. Fast moving consumer goods (FMCG) brands focused on short-term tactics to build revenue. In contrast, mobile wallets and some other financial services brands benefited immediately from demonetization.

Disruption also erupted more narrowly, impacting certain categories, like telecoms, where Jio, a brand less than a year old, offered free data, which quickly won the brand over 100 million customers, but also fomented a price war. Jio entered the BrandZ™ India Top 50—at No. 11.

←

In FMCG, Patanjali continued to broaden from its original focus on Ayurvedic wellness products into an extensive FMCG range that challenged the multinationals. Patanjali turned up the communications volume and more aggressively called out the multinationals for not being as authentic.

Hindustan Unilever Ltd. and Colgate-Palmolive India Ltd. responded by introducing new brands of Ayurvedic products. Because of their ability to communicate “Indianness,” Indian FMCG brands owned by multinationals outscored local Indian FMCG brands—including Patanjali—in VQ, the new BrandZ™ measurement of brand health, and in all five VQ components.

Brand India

Other disruptions resulted from India’s global integration. In today’s wired world, news of overseas shocks—Brexit and the US election—reached India instantaneously and had an impact on consumer confidence, especially in IT centers like Bengaluru, where people

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

1716

OVERVIEW

PART 1

Introduction

worried whether the America First declarations of the Trump administration would limit business growth in India and opportunities to study or work in the US.

In addition, the populism of Brexit and the Trump election reverberated in India. As happened in other parts of the world, populism sometimes produced ugly bigotry, but other populist expressions were about Indian national pride. And the sharpest distinction between populism abroad and in India was that Indians did not reject globalization. They embraced it. Globalization has been good for India.

Conversely, these developments influenced how the rest of the world views India. Business decision makers ranked India low on some dimensions that are important for doing business, like transparency, according to the latest Best Countries research of Y&R’s BAV Group. But business decision makers also expressed high regard for India as culturally significant, innovative, and on the move. They ranked India No. 2 in the Movers category of up-and-coming economies, above China and Japan.

The India Top 50 resumed its positive momentum, with value up 57 percent since 2014. The India Top 50 outpaced both the BrandZ™ Global Top 50 and China Top 50, which grew 32 percent and 46 percent in value over the same period.

India Top 50 outpaces Global and China rankings

Source: BrandZ™ / Kantar Millward Brown (including data from Bloomberg)

$100BIL.

$50BIL.

$0

2014 $69.6BIL.

2015 $92.2BIL.

2016 $90.5BIL.

2017 $109.3BIL.

Brand Value Increase over

3 years

+33%

+21%

+57%

+46%

+32%

-2%

BUT TELECOMS/ENTERTAINMENT LEADS IN VALUE GROWTH

VALUE IS CONCENTRATEDIN FINANCIAL CATEGORIES

The value of the BrandZ™ India

Top 50 is concentrated in financial

brands—banks, which are primarily

state-owned, and insurance

companies. But the Top 50 brands are

evenly distributed among five broad

categories: financial; automotive,

including automobiles, lubricants,

motor oil, and tires; telecom providers

and entertainment; food, drinks, and

alcohol; and other.

The telecom providers and entertainment categories led in value growth, increasing 30 percent. Advertising and data price promotions, led by the Jio brand, and the availability of inexpensive mobile handsets, drove telecom demand. Digitization, and a growing range of content, boosted the entertainment category, which is new to the BrandZ™ India Top 50 this year.

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

1918

OVERVIEW

The financial category grew 26 percent, as banks rebounded from loan performance problems. Automobiles followed, rising 23 percent in value, because of a combination of factors, including: consumer confidence, favorable interest rates, and insightful marketing that responded to customer desire for products that offered style and performance as well as price.

Food, drinks, and alcohol lagged primarily because of demonetization, the government initiative to curtail the underground economy, increase tax revenue, and accelerate digitization. Implemented in November, demonetization removed key cash currency from circulation. Fast moving consumer goods (FMCG), which rely on cash currency, took several months to recover.

The food and drink brands and automobiles scored highest in new BrandZ™ metric, called Vitality Quotient (VQ), a measurement of brand health. The telecoms and entertainment brands also scored well. Brands in the financial category have room to improve in the five indicators that make up the composite VQ score: Brand Purpose, Innovation, Communications, Brand Experience, and Love.

These VQ finding have important consequences for brands across all categories. Brands with high VQ scores usually are Meaningful (consumers feel an affinity for them and believe the brands meet their needs in relevant ways) and Different (consumer see the brands as distinctive and trend- setting). Meaningfully Different brands appreciate faster in value and are more likely to grow market share and command a premium.

PART 1

Introduction

// BRANDZ™ ANALYSIS

The value of the India Top 50 is concentrated in the financial category, comprised of banks, which are primarily state-owned, and insurance companies. Brands are distributed more evenly among categories.

The telecom providers and entertainment categories led in value growth, increasing 30 percent. Financial followed, rising 26 percent in value, as banks rebounded from loanperformance problems.

A new BrandZ™ metric of brand health, called Value Quotient (VQ), found that brands in the financial category could be healthier. Despite their financial value, financial brands score around 100, which is average, on each of the five brand health indicators that make up the composite VQ score. Stronger brand health should make financial brands more resilient during periods of market volatility.

Automotive includes automobiles, lubricants, motor oil, and tires

Value is concentrated in the financial category…

… But telecoms/entertainment lead in value growth…

… And the financial category lags in brand health

FINANCIAL

39%

10 Brands

AUTOMOTIVE

19%

11 Brands

TELECOMS / ENTERTAINMENT

16%

6 Brands

FOOD, DRINKS & ALCOHOL

10%

9 Brands

OTHER

16%

14 Brands

Source: BrandZ™ / Kantar Millward Brown

Source: BrandZ™ / Kantar Millward BrownAverage VQ score = 100Source: BrandZ™ / Kantar Millward Brown

0

30%

20%

10%

30%

% Value Change

26% 23%

10%

5%

Brand Purpose 102 108 117 117 113

Innovation 98 104 112 111 109

Communications 100 106 115 118 113

Brand Experience 100 106 114 117 113

Love 99 104 111 114 112

Score 100 106 114 115 112

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

2120

BRANDZ™ INDIA TOP 50 PORTFOLIO OUTPERFORMS SENSEX

STRONG VALUABLE BRANDS DELIVER SUPERIOR SHAREHOLDER RETURNS

A stock portfolio of the BrandZ™

Top 50 Most Valuable Indian brands

increased 38.8 percent in value

between August 2014 and July 2017,

while over the same three-year period,

India’s SENSEX, a weighted index

of 30 stocks on the Bombay Stock

Exchange, increased 15.0 percent.

BRANDZ™ INDIA TOP 50 PORTFOLIO

PART 1

Introduction

The BrandZ™ Top 50 Portfolio outperformed SENSEX, even as India’s stock exchange reached record highs in 2017. And the BrandZ™ Top 50 Portfolio never declined as severely as SENSEX during periods of economic stress in 2015.

This performance by the BrandZ™ India Top 50 Portfolio demonstrates the critical ability of valuable brands to navigate volatility and generate superior returns for shareholders. High-value

brands also help drive sales volume, command premium pricing, and expand market share.

To quantify the impact of high-value brands, $100 invested in 2014, in the BrandZ™ India Top 50 Portfolio, would have grown to around $139. However, $100 invested at the same time in SENSEX stocks would be worth only $115. The ROI for the investor is over 20 percent greater with the BrandZ™ Top 50 Portfolio.

A stock portfolio of the BrandZ™ Top 50 Most Valuable Indian Brands increased 38.8 percent over three years, when India’s SENSEX increased 15.0 percent. The BrandZ™ India Top 50 Portfolio successfully navigated volatility and delivered superior shareholder value.

BrandZ™ India Top 50 Portfolio vs. SENSEX India(August 2014 to July 2017)

0%

10%

20%

30%

-10%

-20%

BrandZ™ India Top 50

Portfolio

38.8%

SENSEX India

15%

Source: BrandZ™ / Kantar Millward Brown (including data from Bloomberg)

. . . O N T H E W I N G S O F T E C H A N D C U LT U R E .

B R A N D I N D I A C I R C L E S T H E G L O B E . . .

SUBSTANTIAL VALUE GROWTH DEFINES THE RANKING

COMPETITION CREATES TOP 50 BRAND CHURN

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

2524

KEY FINDINGS

PART 1

Introduction

BRANDS NEEDED SUBSTANTIAL VALUE GROWTH TO REMAIN IN THE TOP 50

Only 38 brands that appeared in the 2014 BrandZ™ India Top 50, just three years ago, remain in the BrandZ™ Top 50 2017. Of the remaining brands, those that held their rank increased value 48 percent, on average. Brands that failed to increase value by at least 18 percent dropped in rank. Brands that rose in rank increased value 106 percent, on average, almost double the overall Top 50 value growth rate of 57 percent.

MEANINGFUL DIFFERENCE WAS THE KEY TO SUBSTANTIAL BRAND VALUE GROWTH

Brands in the India Top 50 that are high in Meaningful (consumers feel an affinity for them and believe the brands meet their needs in relevant ways) and Different (consumer see the brands as distinctive and trend setting) totaled $45.6 billion in value, more than twice the $21.8 billion total value of brands with low Meaningful Difference

BRANDS THAT GREW VALUE SUBSTANTIALLY HAD HIGH BRAND CONTRIBUTION AND BRAND POWER

India Top 50 brands that grew substantially in value between 2014 and 2017 had high Brand Contribution and high Brand Power. These brands grew value at twice the rate of brands with low Brand Contribution and low Brand Power. Brand Contribution represents the value of a brand itself—the intangible asset that exists in the minds of consumers. Brand Power is the BrandZ™ metric of brand equity.

0

50%

100%

% Increase in Brand Value

Brand Contribution measures the impact of brand alone on financial value, on a scale of 1 to 5, 5 highest. Brand Power scores are based on an index where 100 is average (India top 50 2017). The % $ value change is based on the India Top 50 2014 to 2017.

+18%

Declined in ranking

+48%

Held their position

+57%

India Top 50

+106%

Improved in ranking

Source: BrandZ™ / Kantar Millward BrownSource: BrandZ™ / Kantar Millward Brown

$0

$50 BIL.

$21.8BIL.

LOW on Meaningful Difference

$45.6BIL.

HIGH on Meaningful Difference

+109%

Source: BrandZ™ / Kantar Millward Brown

50

20

10

30

40

0

Brand Contribution HIGH (4,5)

Brand Power317

+38%Brand Contribution

MEDIUM (3)

Brand Power175

+23%

Brand Contribution LOW (1,2)

Brand Power124

+18%

←

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

2726

KEY FINDINGS

PART 1

Introduction

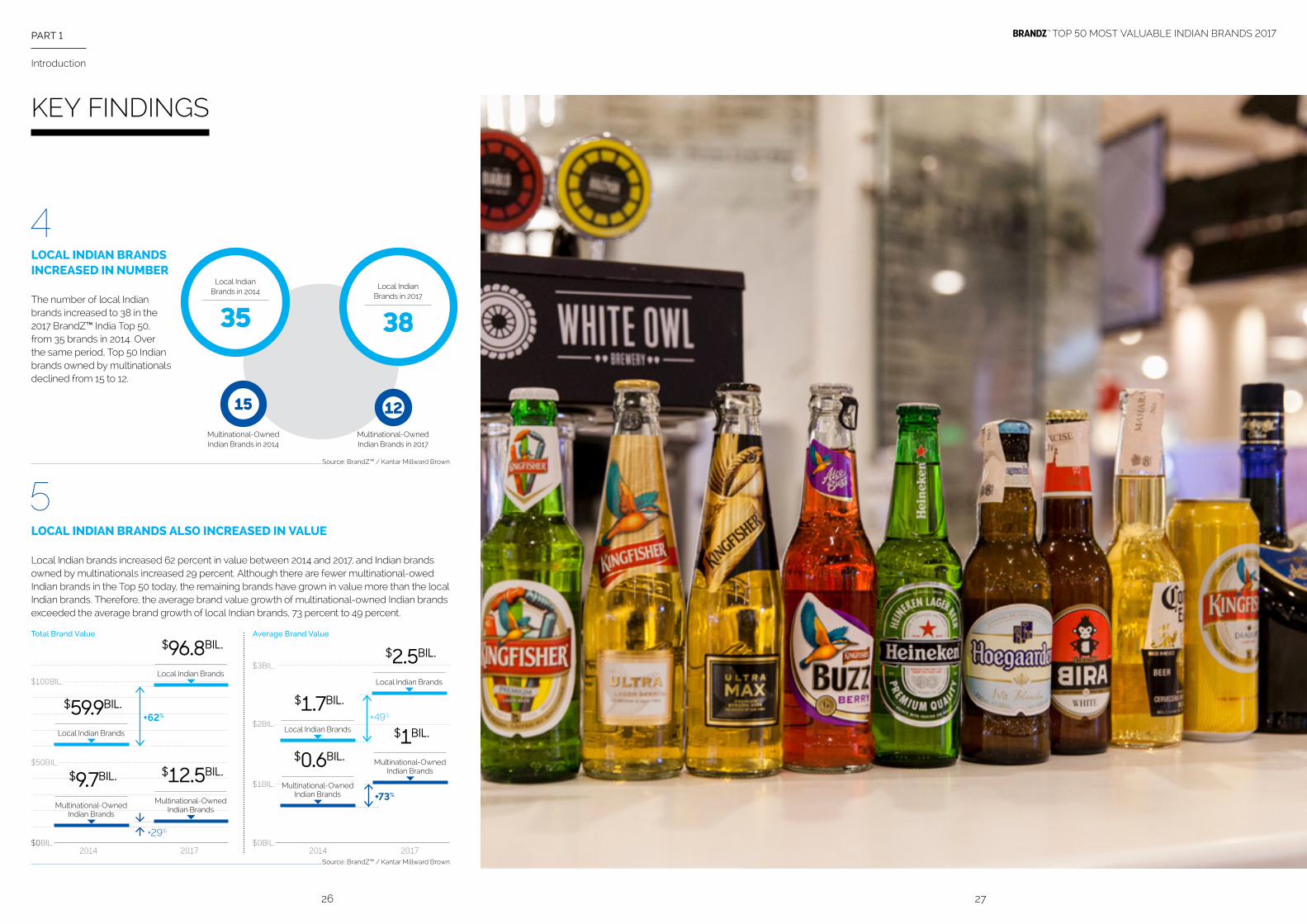

LOCAL INDIAN BRANDS INCREASED IN NUMBER

The number of local Indian brands increased to 38 in the 2017 BrandZ™ India Top 50, from 35 brands in 2014. Over the same period, Top 50 Indian brands owned by multinationals declined from 15 to 12.

LOCAL INDIAN BRANDS ALSO INCREASED IN VALUE

Local Indian brands increased 62 percent in value between 2014 and 2017, and Indian brands owned by multinationals increased 29 percent. Although there are fewer multinational-owed Indian brands in the Top 50 today, the remaining brands have grown in value more than the local Indian brands. Therefore, the average brand value growth of multinational-owned Indian brands exceeded the average brand growth of local Indian brands, 73 percent to 49 percent.

Source: BrandZ™ / Kantar Millward Brown

Source: BrandZ™ / Kantar Millward Brown

35Local Indian

Brands in 2014

15 12Multinational-Owned Indian Brands in 2014

Multinational-Owned Indian Brands in 2017

38Local Indian

Brands in 2017

$100BIL.

$3BIL.

$2BIL.

$1BIL.

$50BIL.

2014 20142017 2017$0$0BIL. $0BIL.

$9.7BIL.

Multinational-Owned Indian Brands

$0.6BIL.

Multinational-Owned Indian Brands

$59.9BIL.

Local Indian Brands

$1.7BIL.

Local Indian Brands

$2.5BIL.

Local Indian Brands

$12.5BIL.

Multinational-Owned Indian Brands

$1BIL.

Multinational-Owned Indian Brands

$96.8BIL.

Local Indian Brands

+29%

+73%

+62% +49%

Total Brand Value Average Brand Value

SOCIAL AND ECONOMICFORCES ARE RESHAPING THE INDIAN MARKET

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

2928

CROSS-CATEGORY TRENDS

PART 1

Introduction

←

While most brands avoided taking a political stand, they aligned with aspects of the government’s national-building agenda that are most brand-relevant. Dettol, a soap brand, campaigned for improved sanitation and hygiene. Sports brands, including some cricket teams, supported government attempts to improve the status of women by having the athletes display the names of their mothers or daughters on their uniforms. The free data offer by Jio gained the new brand over 100 million new customers in its first few months, and simultaneously helped advance the government’s Digital India initiative. Meanwhile, the Ayurvedic and fast moving consumer goods (FMCG) brand, Patanjali, intensified its nationalistic message by suggesting that its Indian provenance made the brand more authentic than the brands of multinationals.

Digitization drove access, enabling people even in the smallest villages to have smartphones and engage in e-commerce and online banking. But greater access did not always result in greater inclusion. That requires understanding people, helping them benefit from new opportunities, and communicating in the appropriate language and tone. Ultimately, brands can benefit. Amazon, for example, is positioning itself as an online store for India’s dreams, and many of those dreamers reside in small towns and villages.

Connected with the rise in nationalism is a soothing nostalgia countertrend to the many changes jolting India’s tradition-based society. These changes include greater equality for women, which redefines

gender roles, and increased mobility, which strains strong family ties. The most obvious expression of nostalgia is the interest in Ayurvedic products, a phenomenon also driven by nationalism, concern about health and wellness, and the search for

products deemed trustworthy.

Paper Boat, a local soft drink brand, based its business proposition around nostalgia. Using the strapline “drinks and memories,” Paper Boat markets flavors

that Indians associate with an earlier and simpler time. The nostalgia wave is also evident in the changing attitudes and behavior of young people. While they adopt the latest technology and trends emanating from the West, more young Indians are returning to live with their families and embrace traditional life.

NATIONALISM

ACCESS AND INCLUSION

NOSTALGIA

BRANDS FIND PURPOSE IN THE NATIONAL VISION

DIGITAL EXPANDS ACCESS, BUT NOT

ALWAYS INCLUSION

A COUNTERTREND OPENS MARKETING

OPPORTUNITIES

Another global trend has reached India—distrust. Rather than rely only on brand communications—or even word-of-

mouth—Indians, particularly in cities, are more likely to research online to corroborate brand claims. Having been disappointed by some brands, they

do not want to be disappointed again. Brands need to earn the trust of Indian consumers. And brands need to communicate in ways that inspire trust. Reaching young people requires projecting authenticity, for example. Idealized celebrity brand ambassadors or overly

romanticized commercials will resonate less than messages presented with a sense of realism.

The urban-rural divide is less useful now as a marketing framework for several reasons. First, the urban-rural gaps

are narrowing, in income, education, and other dimensions. Second, the notion of Multiple Indias more

closely captures the reality of one country combining many differences in geography, language, and culture. Third, all of India is changing. And rural Indians do not match

the conventional stereotypes. Increasingly, they do not aspire to be just country versions of urban people. According to research by Kantar IMRB, rural Indians want to retain their rural identities, while improving themselves and their communities. These changes affect all brand activities, including product development, communication, and distribution.

TRUST

MULTIPLE INDIAS

BRAND MESSAGES MEET CONSUMER

SKEPTICISM

URBAN-RURAL DOES NOT DEFINE INDIA

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

3130

CROSS-CATEGORY TRENDS

PART 1

Introduction

Consumer confidence is generally strong, but how strong varies by geography, according to the Shopper Barometer of Kantar IMRB. In most urban areas consumers felt more confident and spent more. But confidence sagged in areas known for IT, like Bengaluru, because a startup slowdown impacted employment and the Trump administration America First declarations raised concerns about working or studying in the US. These findings suggest that brands face great opportunity in India, but maximum success requires identifying and adjusting for local fluctuations in spending.

CONFIDENCEOPTIMISM IS STRONG BUT

VARIES REGIONALLY

The rich are getting richer, and some of the poor are still left behind, as people pursue the dream of a New India, but progress at different speeds. Within the SEC classifications of household spending hierarchy, Kantar Worldpanel identified a group it called “Elites.” Adding a few more household characteristics, such as car ownership, revealed a group that spends more on FMCG than other households in top SEC classifications. For brands across categories it is useful to know who these people are and how they spend. It is also useful to understand the less affluent, and to help them become more capable consumers.

WEALTHTHE DREAM IS

CLOSER TO SOME THAN OTHERS

VITAL ACTIONS FOR BUILDINGVALUABLE BRANDSIN TODAY’S INDIA

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

3332

TAKEAWAYS

PART 1

Introduction

The rise of Indian nationalism does not mean that Indian consumers automatically prefer brands with Indian provenance, but it does mean that they prefer brands that respect their culture, understand their preferences, and communicate in the appropriate language and tone. A brand does not need to be Indian to act Indian.

As India enhances its global profile, the impression of Brand India rises and consumers outside India potentially become

more receptive to Indian products across categories. Continue to be entrepreneurial, but

match entrepreneurship with greater innovation.

Indians are now inundated with brands that have a product or service to sell, and are

reaching them all the time on multiple screens. Being different and being heard requires presenting the message in an emotionally

compelling way that helps cultivate a relationship that is more than transactional.

It is not just about price anymore. Indian consumers want the same things that affluent consumers worldwide seek, which

is, depending on the category, quality products with style and design, or trustworthy products with healthy ingredients. If there is

a difference in India, it is that Indian consumers remain price conscious. They seek value, but value now includes more considerations.

Skepticism is on the rise. Consumers are likely to search the internet to test the veracity of brand messages. Build trust by acting with consistency. Deliver on all brand claims. And when the brand

comes up short, admit to a mistake before it is broadcast all over social media.

The urban-rural divide is an outdated binary concept. Successful brands understand that there are many Indias, and these distinctions can be geographic, cultural, or economic. Economically, as the middle class expands, some people rise to the top, to an elite status, while others are left behind. Brands selling to those who have succeeded need to remember those still struggling. It demonstrates leadership.

BE INDIAN

BE A LEADER

BE EMOTIONALMEET DESIRE WITH AFFORDABILITY

BUILD TRUST

EMBRACE MULTIPLE INDIAS

←

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

3534

TAKEAWAYS

PART 1

Introduction

Digital India is not simply a government slogan. Throughout India people are spending more time on their smartphones—for entertainment, e-commerce, or banking. Astute digital strategies and tactics are prerequisites for brand success. Brands need to be present on multiple screens, and that often includes TV. As in most markets, digital is growing faster

than any other medium, but as is often the case, India is distinctive. It is the only major media market where

spending on print continues to grow.

The India Top 50 Brands with high Meaningful Difference are twice as valuable as brands with low Meaningful Difference, which is a BrandZ™ measurement of whether consumers view a brand as Meaningful (meeting my needs in relevant ways) and Different (distinctive and trendsetting). Consumers typically describe Meaningfully Different brands as trustworthy and caring.

GAIN A DIGITAL EDGE

CULTIVATE MEANINGFUL DIFFERENCE

37

PART 1

Introduction

36

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

OUR INSIGHTS

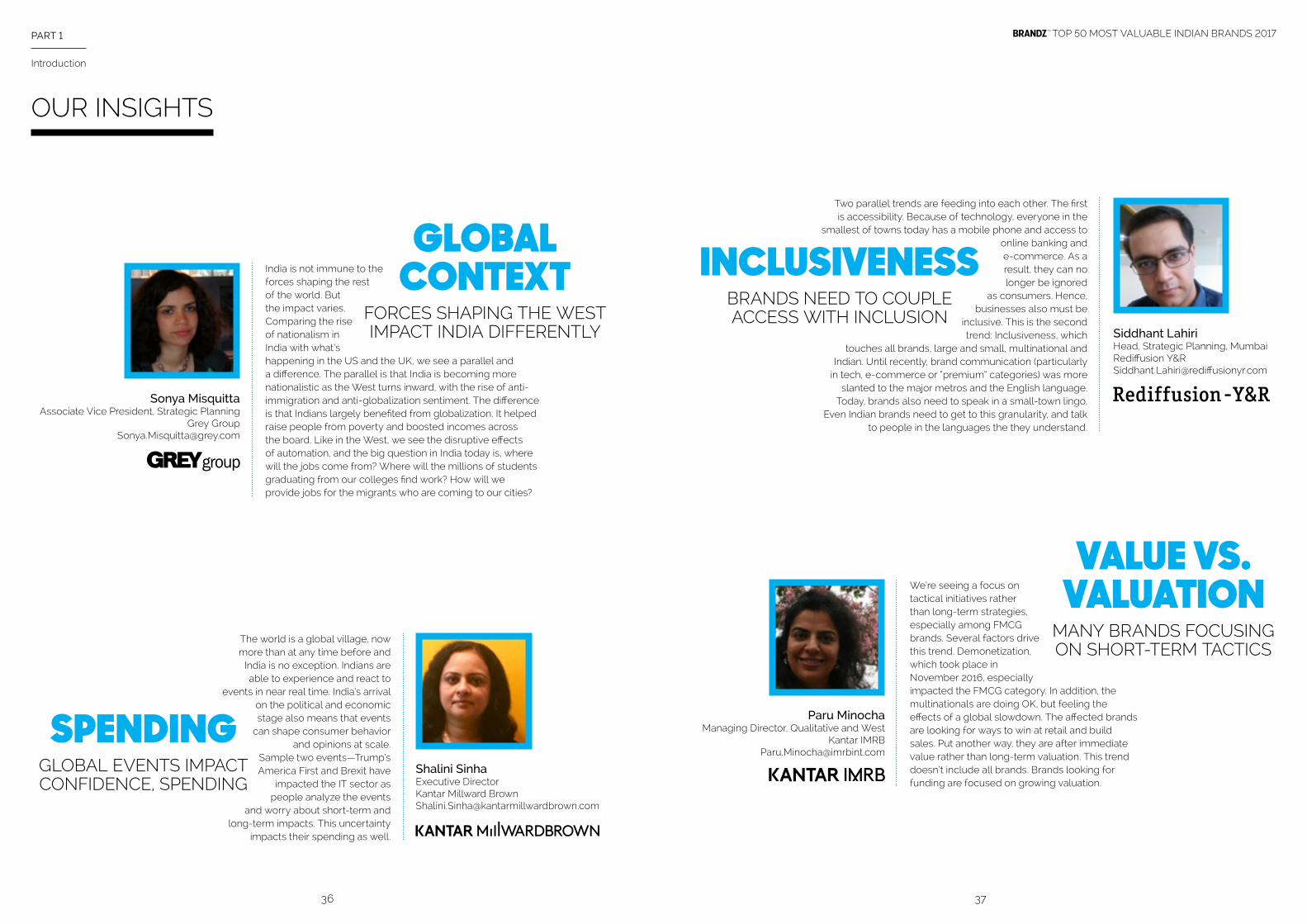

India is not immune to the forces shaping the rest of the world. But the impact varies. Comparing the rise of nationalism in India with what’s happening in the US and the UK, we see a parallel and a difference. The parallel is that India is becoming more nationalistic as the West turns inward, with the rise of anti-immigration and anti-globalization sentiment. The difference is that Indians largely benefited from globalization. It helped raise people from poverty and boosted incomes across the board. Like in the West, we see the disruptive effects of automation, and the big question in India today is, where will the jobs come from? Where will the millions of students graduating from our colleges find work? How will we provide jobs for the migrants who are coming to our cities?

Sonya MisquittaAssociate Vice President, Strategic Planning

Grey [email protected]

GLOBAL CONTEXT

FORCES SHAPING THE WESTIMPACT INDIA DIFFERENTLY

The world is a global village, now more than at any time before and

India is no exception. Indians are able to experience and react to

events in near real time. India’s arrival on the political and economic stage also means that events

can shape consumer behavior and opinions at scale.

Sample two events—Trump’s America First and Brexit have

impacted the IT sector as people analyze the events

and worry about short-term and long-term impacts. This uncertainty

impacts their spending as well.

Shalini Sinha Executive DirectorKantar Millward [email protected]

SPENDINGGLOBAL EVENTS IMPACTCONFIDENCE, SPENDING

Two parallel trends are feeding into each other. The first is accessibility. Because of technology, everyone in the

smallest of towns today has a mobile phone and access to online banking and e-commerce. As a result, they can no longer be ignored

as consumers. Hence, businesses also must be

inclusive. This is the second trend: Inclusiveness, which

touches all brands, large and small, multinational and Indian. Until recently, brand communication (particularly

in tech, e-commerce or “premium” categories) was more slanted to the major metros and the English language.

Today, brands also need to speak in a small-town lingo. Even Indian brands need to get to this granularity, and talk

to people in the languages the they understand.

Siddhant Lahiri Head, Strategic Planning, MumbaiRediffusion Y&[email protected]

INCLUSIVENESSBRANDS NEED TO COUPLEACCESS WITH INCLUSION

We’re seeing a focus on tactical initiatives rather than long-term strategies, especially among FMCG brands. Several factors drive this trend. Demonetization, which took place in November 2016, especially impacted the FMCG category. In addition, the multinationals are doing OK, but feeling the effects of a global slowdown. The affected brands are looking for ways to win at retail and build sales. Put another way, they are after immediate value rather than long-term valuation. This trend doesn’t include all brands. Brands looking for funding are focused on growing valuation.

Paru Minocha Managing Director, Qualitative and West

Kantar [email protected]

VALUE VS. VALUATION

MANY BRANDS FOCUSINGON SHORT-TERM TACTICS

MARKETKNOWLEDGE & INTELLIGENCE

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

4140

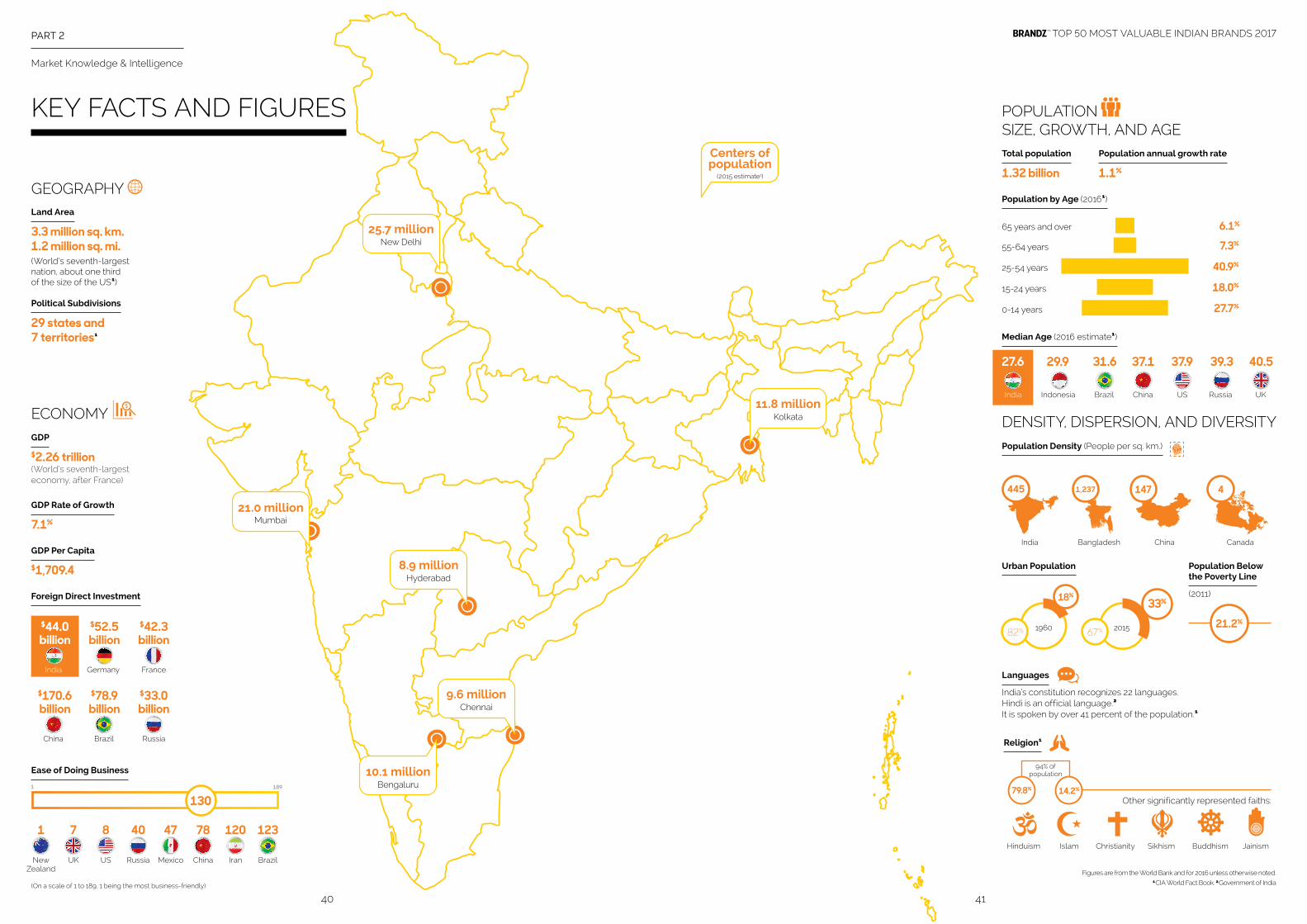

KEY FACTS AND FIGURES

PART 2

Market Knowledge & Intelligence

Centers of population

(2015 estimate1)

New Delhi25.7 million

Mumbai

Hyderabad

Chennai

Bengaluru

8.9 million

21.0 million

9.6 million

10.1 million

Kolkata11.8 million

GEOGRAPHYLand Area

3.3 million sq. km. 1.2 million sq. mi. (World’s seventh-largest nation, about one third of the size of the US1)

Political Subdivisions

29 states and 7 territories1

Figures are from the World Bank and for 2016 unless otherwise noted. 1 CIA World Fact Book. 2 Government of India

POPULATIONSIZE, GROWTH, AND AGETotal population

1.32 billion

Religion1

Hinduism Islam

79.8%

21.2%

14.2%

Other significantly represented faiths:

Christianity Sikhism Buddhism Jainism

DENSITY, DISPERSION, AND DIVERSITYPopulation Density (People per sq. km.)

Languages

India’s constitution recognizes 22 languages. Hindi is an official language.2 It is spoken by over 41 percent of the population.1

Urban Population Population Below the Poverty Line

(2011)

Population annual growth rate

1.1%

Population by Age (20161)

65 years and over 6.1%

15-24 years 18.0%

25-54 years 40.9%

27.7% 0-14 years

55-64 years 7.3%

India

India Bangladesh

Brazil ChinaIndonesia US Russia UK

Median Age (2016 estimate1)

27.6 31.6 37.129.9 37.9 39.3 40.5

445 147 4

China Canada

1,237

1960

18%

82% 2015

33%

67%

94% of population

ECONOMYGDP

$2.26 trillion (World’s seventh-largest economy, after France)

GDP Rate of Growth

7.1%

GDP Per Capita

$1,709.4

Foreign Direct Investment

Ease of Doing Business

$44.0 billion

$52.5 billion

$42.3 billion

$170.6 billion

$78.9 billion

$33.0 billion

India France

China

New Zealand

Russia Mexico China Iran BrazilUK US

Brazil Russia

Germany

1 189

(On a scale of 1 to 189, 1 being the most business-friendly)

130

1 7 8 40 47 78 120 123

. . .T H E V I S I O N O F A N E W I N D I A .

R E S O L U T E E N T R E P R E N E U R S A N I M AT E . . .

FMCG SLOWS, BUT TELECOM GROWS

KEY GOVERNMENT INITIATIVESIMPACT SPENDING

The BrandZ™ India Top 50 grew a

robust 21 percent in brand value and

India’s GDP continued to expand at

an annual rate of around 7 percent,

greater than all other major economies.

And these developments happened

despite—or possibility because of—

disruption, much of it generated by

Indian government initiatives to be a

leader in the global economy and build

a more equitable society.

With demonetization, implemented in November 2016, the government removed certain cash currency from the market to reduce the underground economy, increase tax revenues, and accelerate the shift to digitalization and mobile wallets. Demonetization initially slowed categories dependent on cash transactions, such as luxury, leisure, and especially FMCG.

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

4544

DISRUPTION

Most affected categories rebounded quickly, however, as people adjusted to paying with a mix of cash and digital wallets. Mobile wallet transactions increased by a factor of 20 to 206 billion rupees ($3.2 billion) in 2016, compared with 10 billion rupees ($157 million) in 2013, according to Kantar IMRB.

On July 1, India implemented a national goods and services tax (GST), a type of VAT intended to simplify a complicated combination of state and local taxes, add transparency, and make it easier to transact business in India. Other government initiatives also impacted categories.

Make in India, a government initiative started in 2014, opened India to more foreign investment and competition, as it attempted to elevate India into a

center of global manufacturing and design. Chinese handset brands, which cut costs by manufacturing in India, now dominate the Indian market.

The government’s Digital India initiative, in place for two years, disrupted the telecom category, as illustrated by the Jio brand. Introduced less than a year ago, the brand entered the BrandZ™ India Top 50 at No. 11 based on its ability to challenge the category pricing by offering free data.

Similarly, Swachh Bharat Abhiyan (Clean India Mission), initiated in 2014 to improve sanitation, particularly toilet habits, stimulated sales of household cleaning products. Sales of bathroom cleaners, floor cleaners, and liquid hand wash rose noticeably over the past several years.

Because of the dependence on cash transactions, consumption of FMCG products declined after demonetization, in November 2016, and slowly recovered through the first quarter of 2017.

Swachh Bharat Abhiyan (Clean India Mission), an initiative to improve sanitation, particularly toilet habits, stimulated sales of household cleaning products.

Year-on-year change in FMCG consumption

The percentages represent the moving average total (MAT), the 12-month average of sales increases through the month indicated.

Demonetization slows FMCG growth...

… But an initiative to improve sanitation drives sales

Source: Kantar Worldpanel Source: Kantar Worldpanel

5%

0%

-5%

OCT. 2016

0.4%

APR. 2017

3.9%

MAR. 2017

0.6%

DEC. 2016

-2.4%

FEB. 2017

-1.4%

JAN. 2017

0.1%

Toilet / Bathroom Cleaners

Before Swachh Bharat

After Swachh Bharat

18.7%

18.6%

20.6%

26.1%

Floor Cleaners

Before Swachh Bharat

After Swachh Bharat

8.5%

8.7%

9.5%

11.2%

Liquid Hand Wash

Before Swachh Bharat

After Swachh Bharat

4.2%

4.8%

5.8%

7.3%

October 2013 October 2014 October 2015 October 2016NOV. 2016

-4.2%

PART 2

Market Knowledge & Intelligence

SHOPPERS SEEK AUTHENTICITY AND VALUE

CONFIDENCE REMAINS STEADY DESPITE YEAR OF DISRUPTIONS

Indian consumers exhibited

confidence, but sentiment varied by

income and geography, depending

on the impact of local disruptions and

global events. And even as the gaps

between rich and poor, and urban and

rural narrowed, the extremes became

more exaggerated.

India consumers endured a year of successive domestic, government-induce shocks intended to reform the financial system and increase national revenue. Introduced virtually overnight in November, demonetization eliminated certain paper currency to encourage a shift from cash to digital transactions. A national goods and services tax (GST), implemented in July, replaced a complicated system of state and local levies. These disruptions impacted spending.

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

4746

CONSUMERS // OVERVIEW

Shocks from abroad, like Brexit and the Trump election, resonated quickly because of broad internet access, and stirred anxieties. The American First policies of the Trump administration disturbed consumers working in India’s vast IT sector, for example, resulting in regional variations in spending, according to the Kantar IMRB Shopper Barometer. (Please see page 48).

India also experienced its own version of populism with a nationalist movement that embraced Indian heritage, but without rejecting globalization, which has impacted India in positive ways. While most Indians avoided the more extreme expressions of nationalism, they expressed a desire for products and brands that best understood their particularly Indian sensibilities and tastes. This inclination drove a rise in local brands, put pressure on multinationals, especially in fast moving consumer goods (FMCG) and personal care, and fostered a nostalgia trend.

The accelerated interest in local brands is best illustrated by the rise of Patanjali, which in the decade since it launched has expanded from a narrow focus on Ayurvedic products to a wide FMCG range that challenges established multinationals. Current research by Kantar Millward Brown quantifies the disruptive impact of emerging Indian brands, particularly Patanjali, in FMCG.

In its analysis of Brand Power, the BrandZ™metric of brand equity, in the India Top 50 2017, Kantar Millward Brown discovered that Patanjali increased 64 percentage points, while multinationals grew by less than half that rate, and Indian FMCG brands declined. New Kantar Worldpanel research explains Patanjali’s impact in detail. The Kantar Worldpanel research also identifies an emerging classification of “Elite” consumers who spend significantly more on FMCG than other relatively wealthy households. (Please see page 50). ←

Trust and “Indianness”

In this context of disruptive events, greater access to online information, and a desire for authenticity, consumers scrutinized brands more closely. In the past, when consumers received a brand message they were likely to believe it. Today, they are more likely to ask questions and search the internet for answers.

Living in a communal society, Indians consumers typically have shared information before making a purchase. Today, social media has replaced—or at least greatly supplements—word-of-mouth. The circle of influencers is much wider, and includes bloggers,

especially for urban and other educated consumers who are active online.

To get into the consumer’s consideration set, brands need to earn the trust of Indians who have been impacted by the overall global decline in trust and disappointed by some trusted Indian brands. Indian consumers want to trust. Many were patient with the inconveniences of demonetization because it symbolized the possibility of reducing corruption and elevating the importance of honesty and trust, according to Kantar IMRB.

Once Indian consumers trust a brand, they primarily look for the best offer of value for money. But a brand’s “Indianness” has also become an

important determinant in brand selection. Being made in India is especially relevant in categories such as health and wellness and Ayurveda, where Indian heritage implies high levels of quality and distinctiveness.

Patanjali is the most prominent example of brand that emphasizes “Indianness.” Recently, Patajali has more aggressively promoted its “Indianness” as proof of authenticity when compared with multinational brands. Other brands that promote their Indian provenance include Dabur, a brand of Ayurvedic and wellness products, and Forest Essentials, a premium brand that has reinterpreted and updated Ayurvedic and other Indian personal care and beauty traditions.

PART 2

Market Knowledge & Intelligence

The consumer desire for brands that authentically capture Indian tastes and heritage has pressured the multinationals and many have responded. Hindustan Unilever, a consumer products giant present in India since 1933, has introduced a new brand of Ayurvedic products, called Ayush, and intends to leverage its extensive distribution system, which reaches even the most remote parts of India.

Colgate has introduced a toothpaste with Ayurvedic properties. In its recovery from recent food safety issues, Maggi, a Nestlé brand, benefited from a reservoir of brand equity built up over time. Maggi rose 66 percent in brand value this year, making it one of the Top Risers in the BrandZ™ India Top 50.

Brands owned by multinationals continue to dominate in certain categories, like durable goods, primarily because they are creating products with benefits designed for the Indian

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

4948

CONSUMERS // OVERVIEW

market. And, in most categories, Indian consumers are likely to make purchase decisions based on product, price, and service—rather than provenance.

Reaching consumers

Reaching today’s more knowledgeable and skeptical Indian consumers requires communicating with real-life, relatable situations. Young people, particularly, are unimpressed with celebrity brand ambassadors who project an unattainable level of perfection. Expansive romantic stories may work for Bollywood movies, but they generally are less effective for selling products.

The detergent powder Ghari appealed emotionally in a commercial aired during the Muslim holiday of Eid-ul-Fitr, a time of purification at the end of Ramadan. The commercial showed friends reconciling differences and gathered for an Eid feast, and it treated the theme of cleansing in spiritual terms, using an Indian word that means wash away.

To differentiate and strengthen their emotional engagement with consumers, many brands connect with relevant progressive social issues, in an expression of nationalism aimed at supporting India’s development. A campaign from the jewelry brand Tanishq promotes empowerment of women. Parachute, a body lotion brand, also advocates for the empowerment of women, with the strapline, “Be confident in your own skin.”

Indian consumers respond to brands that go beyond their transactional relationship with consumers and create an emotional bond, according to Kantar IMRB. When consumers felt stressed immediately after demonetization, brands had an opportunity to respond in empathetic and relevant ways, but few brands met the challenge, Kantar IMRB found. In rapidly transforming India, however, demonetization is only one of many disruptions and brand opportunities.

PART 2

Market Knowledge & Intelligence

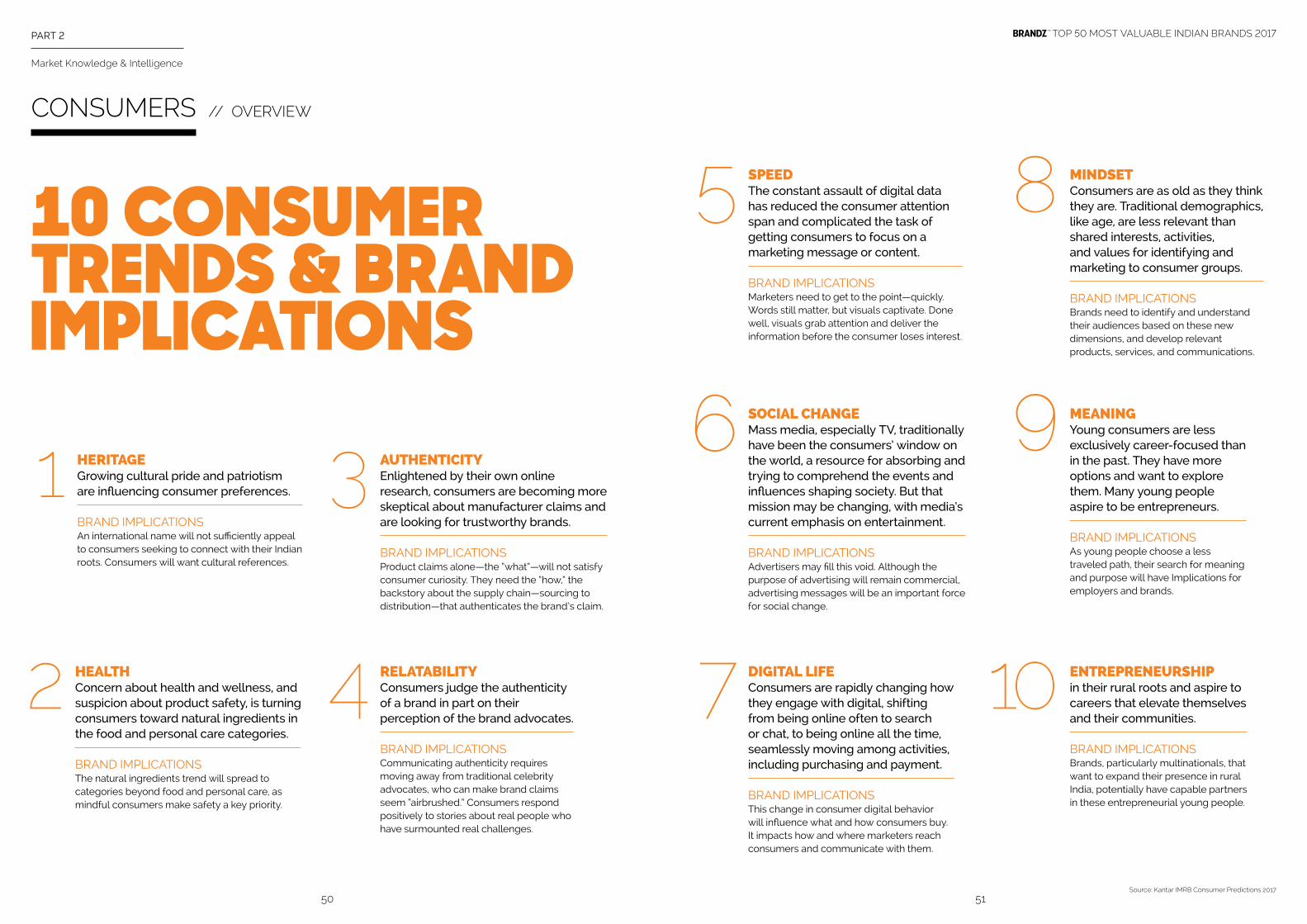

10 CONSUMER TRENDS & BRAND IMPLICATIONS

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

5150

CONSUMERS // OVERVIEW

HERITAGE Growing cultural pride and patriotism are influencing consumer preferences.

BRAND IMPLICATIONSAn international name will not sufficiently appeal to consumers seeking to connect with their Indian roots. Consumers will want cultural references.

SPEED The constant assault of digital data has reduced the consumer attention span and complicated the task of getting consumers to focus on a marketing message or content.

BRAND IMPLICATIONSMarketers need to get to the point—quickly. Words still matter, but visuals captivate. Done well, visuals grab attention and deliver the information before the consumer loses interest.

AUTHENTICITY Enlightened by their own online research, consumers are becoming more skeptical about manufacturer claims and are looking for trustworthy brands.

BRAND IMPLICATIONSProduct claims alone—the “what”—will not satisfy consumer curiosity. They need the “how,” the backstory about the supply chain—sourcing to distribution—that authenticates the brand’s claim.

MINDSET Consumers are as old as they think they are. Traditional demographics, like age, are less relevant than shared interests, activities, and values for identifying and marketing to consumer groups.

BRAND IMPLICATIONSBrands need to identify and understand their audiences based on these new dimensions, and develop relevant products, services, and communications.

HEALTH Concern about health and wellness, and suspicion about product safety, is turning consumers toward natural ingredients in the food and personal care categories.

BRAND IMPLICATIONSThe natural ingredients trend will spread to categories beyond food and personal care, as mindful consumers make safety a key priority.

RELATABILITY Consumers judge the authenticity of a brand in part on their perception of the brand advocates.

BRAND IMPLICATIONSCommunicating authenticity requires moving away from traditional celebrity advocates, who can make brand claims seem “airbrushed.” Consumers respond positively to stories about real people who have surmounted real challenges.

1

5

3

8

2 DIGITAL LIFE Consumers are rapidly changing how they engage with digital, shifting from being online often to search or chat, to being online all the time, seamlessly moving among activities, including purchasing and payment.

BRAND IMPLICATIONSThis change in consumer digital behavior will influence what and how consumers buy. It impacts how and where marketers reach consumers and communicate with them.

ENTREPRENEURSHIP in their rural roots and aspire to careers that elevate themselves and their communities.

BRAND IMPLICATIONSBrands, particularly multinationals, that want to expand their presence in rural India, potentially have capable partners in these entrepreneurial young people.

7 104

SOCIAL CHANGE Mass media, especially TV, traditionally have been the consumers’ window on the world, a resource for absorbing and trying to comprehend the events and influences shaping society. But that mission may be changing, with media’s current emphasis on entertainment.

BRAND IMPLICATIONSAdvertisers may fill this void. Although the purpose of advertising will remain commercial, advertising messages will be an important force for social change.

MEANING Young consumers are less exclusively career-focused than in the past. They have more options and want to explore them. Many young people aspire to be entrepreneurs.

BRAND IMPLICATIONSAs young people choose a less traveled path, their search for meaning and purpose will have Implications for employers and brands.

6 9

Source: Kantar IMRB Consumer Predictions 2017

PART 2

Market Knowledge & Intelligence

BUT CONFIDENCE VARIES BY INCOME, CITY, AND CATEGORY

METRO SHOPPERSINCREASE SPENDING

Indian consumers are sending mixed

signals, according to the Shopper

Barometer report by Kantar IMRB.

Spending is up compared with a year

ago for wealthier metro shoppers, but

so is the number of less affluent middle

class shoppers who say they are less

confident about their financial situation.

The research, conducted during the first quarter of 2017, looked at shopper mood among the middle class in eight major cities: Mumbai, Kolkata, Delhi, Chennai, Bengaluru, Hyderabad, Ahmedabad, and Pune. It revealed that consumer confidence and spending varied widely by income level and city, and these factors impacted categories unevenly.

RICH FEELING RICHER 44 percent of wealthier urban consumers felt better off financially, compared with only 29 percent of the less affluent.

MOOD DRIVES SPENDING 61 percent of urban shoppers increased spending compared with

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

5352

CONSUMERS // SHOPPER BAROMETER

a year ago, and they primarily were wealthier members of the middle class.

VARIES BY CITY Confidence and spending declined in Delhi, Bengaluru, and Kolkata, in part because the softening of startup business affected local economies dependent on the technology sector.

Some categories seemed immune to the more cautious consumer mood. More consumers planned to eat out or spend money on fashion or telecommunications, despite a rise in the consumer price index (CPI) in those categories. In contrast, people planned to spend less on household items, spas and personal grooming.

Changing consumer priorities are also expected to affect car sales, as only 15 percent of consumers said they are “very likely” to buy a four-wheel vehicle in the next couple of months, while 29 percent said they planned to travel on a holiday within India.

Consumers expressed less interest in buying cars and more in going on a holiday trip in India or spending on health and fitness.

% Shoppers ‘Very Likely’ to buy in the next couple of months.

Consumer mood affects spending priorities

Source: Kantar IMRB Consumer Predictions 2017

Four-Wheel Vehicle

15%

Tw0-Wheel Vehicle

20%

Holiday Abroad

22%

Health & Fitness Product or Service

25%

Holiday in India

29%

Property Investment

17%

PART 2

Market Knowledge & Intelligence

THEY SPEND MORE ON FMCG THAN OTHERS

RESEARCH IDENTIFIESNEW “ELITE” HOUSEHOLDS

Indian marketers rely on a Socio-

Economic Classification (SEC) system

to place households into a hierarchy

that helps organize the market and

facilitate planning. Households

belong in one of five classifications (A

to E plus subgroups) determined by

the education level of the household

head and the number of durable

products owned.

A new report by WPP’s Kantar Worldpanel concludes that the expansion of wealth in India is outpacing the recently-revised SEC system. The report—Crystal Gazing: Did you see this coming? — identifies a group of households with a significantly greater spending profile than highest SEC classification—A1.

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

5554

CONSUMERS // ELITES

The A1 households own least nine durable products and the head has more than a college education. In a comparison of FMCG purchase occasions and average FMCG categories purchased per trip, the report found no difference between A1 households and other relatively wealthy households that own somewhat fewer durable products and where the head may be less educated.

However, by adding a few more criteria to the A1 classification (owning a car and computer, and traveling abroad), the report identified a sub-classification of wealthy Indian households differentiated by its higher spending—an A1+ group. Labeled “Elites” by Kantar Worldpanel, these households spend significantly more on FMCG than other relatively wealthy Indian households.

The FMCG spending of “Elite” households is significantly greater than the spending of other relatively wealthy households.

Penetration is significantly greater for “Elite” households compared with A1 households across many FMCG subcategories.

“Elite” households spend more on FMCG…

… And “Elite” penetration is greater across FMCG

ELITE

72

ELITE

6

ELITE

66

SEC A1

69

SEC A1

5

SEC A1

50

SEC A2/A3

69

SEC A2/A3

5

SEC A2/A3

41

PURCHASE OCCASIONS:

AVERAGE CATEGORIES BOUGHT PER TRIP:

RUPEES SPENT PER KG OF FMCG PRODUCT:

Source: Kantar Worldpanel

Sunscreen Anti-aging Soup Honey Face Wash Hand Wash Milk / Food & Drinks

Butter / Cheese

0%

50%

100%

Source: Kantar Worldpanel

SEC A1

Elite

PART 2

Market Knowledge & Intelligence

BRAND FOUND IN 100 MILLION INDIAN HOUSEHOLDS

PATANJALI BRAND INCREASES REACH ACROSS INDIA

In India, the brand Patanjali is

synonymous with disruption. Patanjali

began around a decade ago when

a Yoga guru named Baba Ramdev

started a company devoted to

Ayurvedic healing. Since then, the

brand has expanded into a broad

range of FMCG products and has

opened retail outlets, marketed

relentlessly, and challenged

multinationals.

The Patanjali Group, which includes the brand’s Ayurvedic and FMCG businesses, along with a charitable trust, reported revenue of $1.6 billion for the year ending March 2017, a 111 percent

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

5756

CONSUMERS // PATANJALI

year-on-year increase, following a 150 percent rise a year earlier. The brand is available at 47,000 points of sale.

Baba Ramdev inspired and capitalized on the current Indian consumer interest in Ayurveda and brands that seem to authentically understand Indian needs. Patanjali’s growth also corresponds with a surge in Indian nationalism.

All these factors contributed to the Patanjali brand’s extraordinary growth—but they did not guarantee it. The other unquantifiable factor is the charisma and drive of Baba Ramdev, for whom brand building seems to be not only a business imperative, but, more fundamentally, a mission.

Patanjali brand FMCG products reach 53 percent of urban households and 28 percent of rural households, up sharply from a year ago.

Patanjali customers come back for more. The customer retention rate for toothpaste is 80 percent, for example, up from 65 percent a year ago.

Patanjali reach rises sharply across India…

… And customers are returning

0% 0%

50% 50%

Source: Kantar Worldpanel

Source: Kantar Worldpanel

New research by Kantar Worldpanel, a WPP company, reveals the brand’s scale in new ways that help appreciate its impact. The Patanjali brand is in over 100 million Indian households. And those households typically have Patanjali products in 3 categories compared with 1.8 categories just three years ago.

The brand reach increased dramatically in the past year. Patanjali FMCG products now reach 53 percent of urban households, compared with 31 percent in 2016. In rural India, Patanjali doubled its reach to 28 percent, in just one year. And customers come back for more. The customer retention rate for toothpaste is 80 percent, for example, up from 65 percent a year ago.

Patanjali reach in FMCG. The percentages represent the moving average total (MAT), the 12-month average percent sales increase.

Patanjali Retention Rate. The percentages represent the moving average total (MAT), the 12-month average of retention rate increases through the month indicated.

Urban Household Reach Rural Household Reach

MAT 2017 Overall Household ReachMAT 2016 Overall Household Reach

MAT 2016

14%

MAT 2017

26%

Food & Beverages

MAT 2016

3%

MAT 2017

7%

Food & Beverages

MAT 2016

24%

MAT 2017

45%

Personal Care

MAT 2016

11%

MAT 2017

24%

Personal Care

MAT 2016

9%

MAT 2017

17%

Household Care

MAT 2016

2%

MAT 2017

5%

Household Care

53%

28%31%

13%

0%

50%

100%MAT March 2016 vs. 2015

MAT March 2017 vs. 2016

53%64%

52%58% 65%

80%

Soap Bars Shampoo Toothpaste

PART 2

Market Knowledge & Intelligence

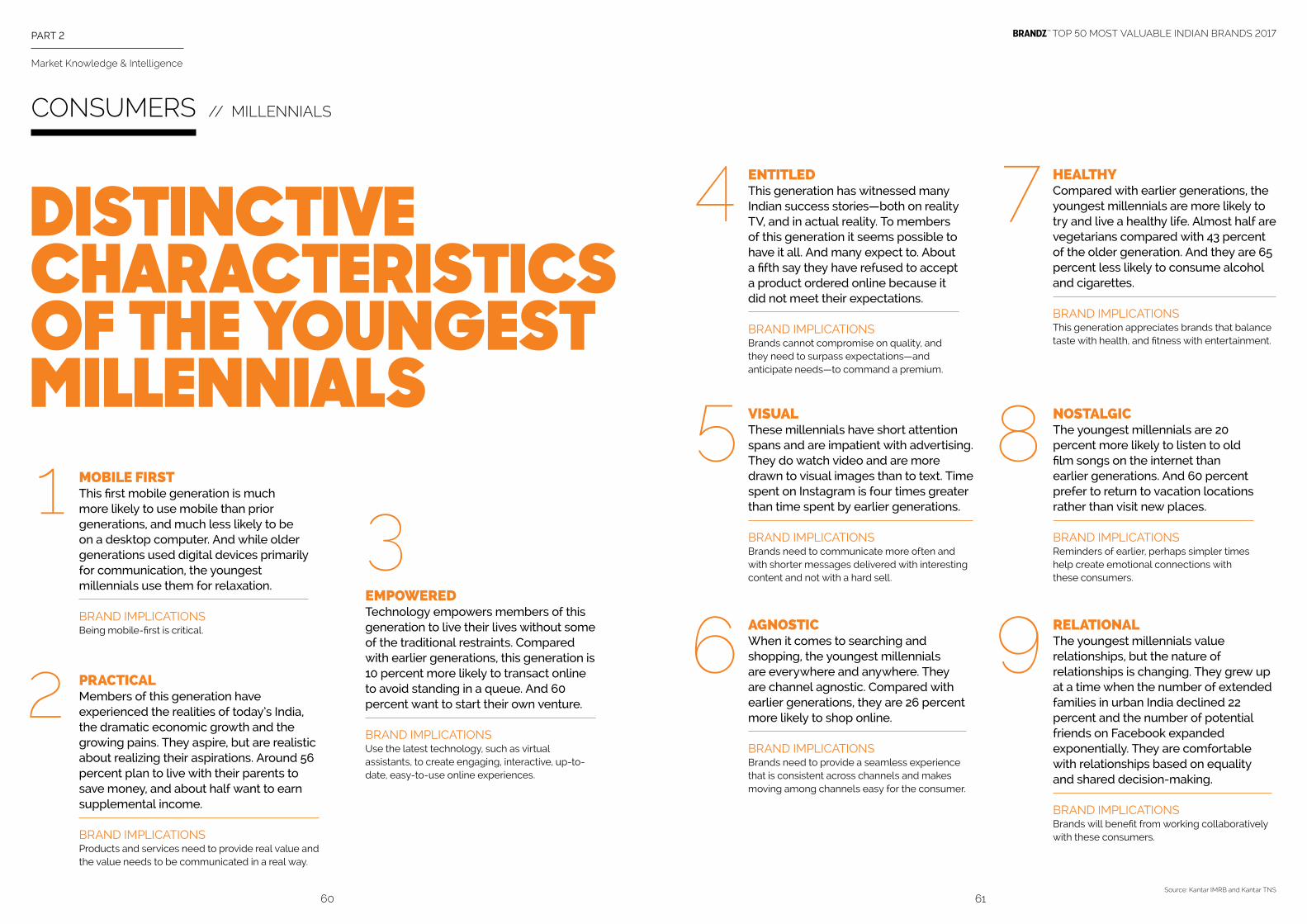

YOUNGEST MILLENNIALS ARE NEWEST CONSUMERS

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

5958

CONSUMERS // MILLENNIALS

The term millennial describes a

generation born between 1981 and

2001. People born at the start and the

end of that two-decade period differ

in life experience and attitudes. And

those differences inform their behavior

as consumers.

The youngest millennials, born between 1997 and 2001, are now 16-to-20 years old. They not only are coming of age, but they also comprise 28 million consumers in India. And, according to studies by Kantar IMRB and TNS, they are influential:

One-third have their own source of personal income;

One-quarter live on their own or with friends;

Almost one-third of those living with their parents are the main shoppers for the household; and

Over one-third of those living with their parents influence household purchasing decisions.

In many ways, these younger millennials are similar in their attitudes to older generations. They are equally hardworking, collaborative, responsible, and loyal, which also identify distinctive characteristics that are important for marketers and brand builders.

PART 2

Market Knowledge & Intelligence

DISTINCTIVE CHARACTERISTICSOF THE YOUNGEST MILLENNIALS

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

6160

CONSUMERS // MILLENNIALS

MOBILE FIRST This first mobile generation is much more likely to use mobile than prior generations, and much less likely to be on a desktop computer. And while older generations used digital devices primarily for communication, the youngest millennials use them for relaxation.

BRAND IMPLICATIONSBeing mobile-first is critical.

ENTITLED This generation has witnessed many Indian success stories—both on reality TV, and in actual reality. To members of this generation it seems possible to have it all. And many expect to. About a fifth say they have refused to accept a product ordered online because it did not meet their expectations.

BRAND IMPLICATIONSBrands cannot compromise on quality, and they need to surpass expectations—and anticipate needs—to command a premium.

EMPOWERED Technology empowers members of this generation to live their lives without some of the traditional restraints. Compared with earlier generations, this generation is 10 percent more likely to transact online to avoid standing in a queue. And 60 percent want to start their own venture.

BRAND IMPLICATIONSUse the latest technology, such as virtual assistants, to create engaging, interactive, up-to-date, easy-to-use online experiences.

NOSTALGIC The youngest millennials are 20 percent more likely to listen to old film songs on the internet than earlier generations. And 60 percent prefer to return to vacation locations rather than visit new places.

BRAND IMPLICATIONSReminders of earlier, perhaps simpler times help create emotional connections with these consumers.

PRACTICAL Members of this generation have experienced the realities of today’s India, the dramatic economic growth and the growing pains. They aspire, but are realistic about realizing their aspirations. Around 56 percent plan to live with their parents to save money, and about half want to earn supplemental income.

BRAND IMPLICATIONSProducts and services need to provide real value and the value needs to be communicated in a real way.

HEALTHY Compared with earlier generations, the youngest millennials are more likely to try and live a healthy life. Almost half are vegetarians compared with 43 percent of the older generation. And they are 65 percent less likely to consume alcohol and cigarettes.

BRAND IMPLICATIONSThis generation appreciates brands that balance taste with health, and fitness with entertainment.

AGNOSTIC When it comes to searching and shopping, the youngest millennials are everywhere and anywhere. They are channel agnostic. Compared with earlier generations, they are 26 percent more likely to shop online.

BRAND IMPLICATIONSBrands need to provide a seamless experience that is consistent across channels and makes moving among channels easy for the consumer.

VISUAL These millennials have short attention spans and are impatient with advertising. They do watch video and are more drawn to visual images than to text. Time spent on Instagram is four times greater than time spent by earlier generations.

BRAND IMPLICATIONSBrands need to communicate more often and with shorter messages delivered with interesting content and not with a hard sell.

RELATIONAL The youngest millennials value relationships, but the nature of relationships is changing. They grew up at a time when the number of extended families in urban India declined 22 percent and the number of potential friends on Facebook expanded exponentially. They are comfortable with relationships based on equality and shared decision-making.

BRAND IMPLICATIONSBrands will benefit from working collaboratively with these consumers.

Source: Kantar IMRB and Kantar TNS

PART 2

Market Knowledge & Intelligence

. . .W I T H P E R M A N E N C E A N D P O S S I B I L I T Y .

L A N D A N D P E O P L E E N R I C H I N D I A . . .

MARKETERS NEED TO ABANDON OUTDATED ASSUMPTIONS

RURAL INDIA IS RISING,IN UNEXPECTED WAYS

With growing internet penetration

and wide access to smartphones,

brand marketers may have assumed

that any urban-rural gap in mentality

would begin to narrow; rural people

would start to resemble their urban

peers, and not the other way around.

Those assumptions may be flawed.

Rural Indians do not aspire to be more like urban Indians; they want to be who they are. They want to create a “more confident, progressive, and economically sustainable rural India,” according to a recent WPP Kantar IMRB report called, Revenge of a Scarecrow: Seizing the winds of change in rural India.

The report asserts that marketers have based their assumptions about people

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

6564

URBAN-RURAL // NEW ASSUMPTIONS

in rural India on faulty stereotypes, and have missed the core cultural insight animating rural Indians: They can make collective progress without sacrificing their roots. Farmers are reinventing themselves as businessmen; women are expanding their roles; and young people are embracing their rural roots, rather than trying to escape them.

“Today’s farmer is aware, optimistic, and ambitious,” the report finds. It describes today’s rural farmer as a leader who is devoted both to his land and to the people he empowers to help develop it. Meanwhile, rural women are quietly pursuing education and seeking opportunities outside formerly restricted roles, but while keeping the aspects of their changing identity in harmony.

Rural youth have “gained colossal confidence in their abilities and are unwilling to embrace the city as an escape route,” according to the report. Young rural Indians are optimistic and entrepreneurial, but they express their ambitions in collectivistic rather than individualistic ways. And this balance is expressed in the rural family, where children are nurtured in a “culture of knowledge,” that places the collective welfare above “individualistic gains.”

To succeed in rural India, marketers need to reject outdated assumptions and embrace the new reality of rural India, according to the report, which recommends that marketers apply these five core rural values:

POWER OF INNOCENCE

Communicate the brand message simply and honestly—and with humility.

PLASTICITY

Be spontaneous and courageous in the way the brand interacts.

PASSION

Empathize with people’s needs and wants, and encourage their odyssey.

PERSEVERANCE

Express commitment to rural India and the aspirations of its people, and be diligent in fulfilling that commitment.

PARTNERSHIP

Create partnerships with local entrepreneurs, listen to their advice and adopt their suggestions.

PART 2

Market Knowledge & Intelligence

TOP 50 MOST VALUABLE INDIAN BRANDS 2017

6766

DIGITAL // OVERVIEW

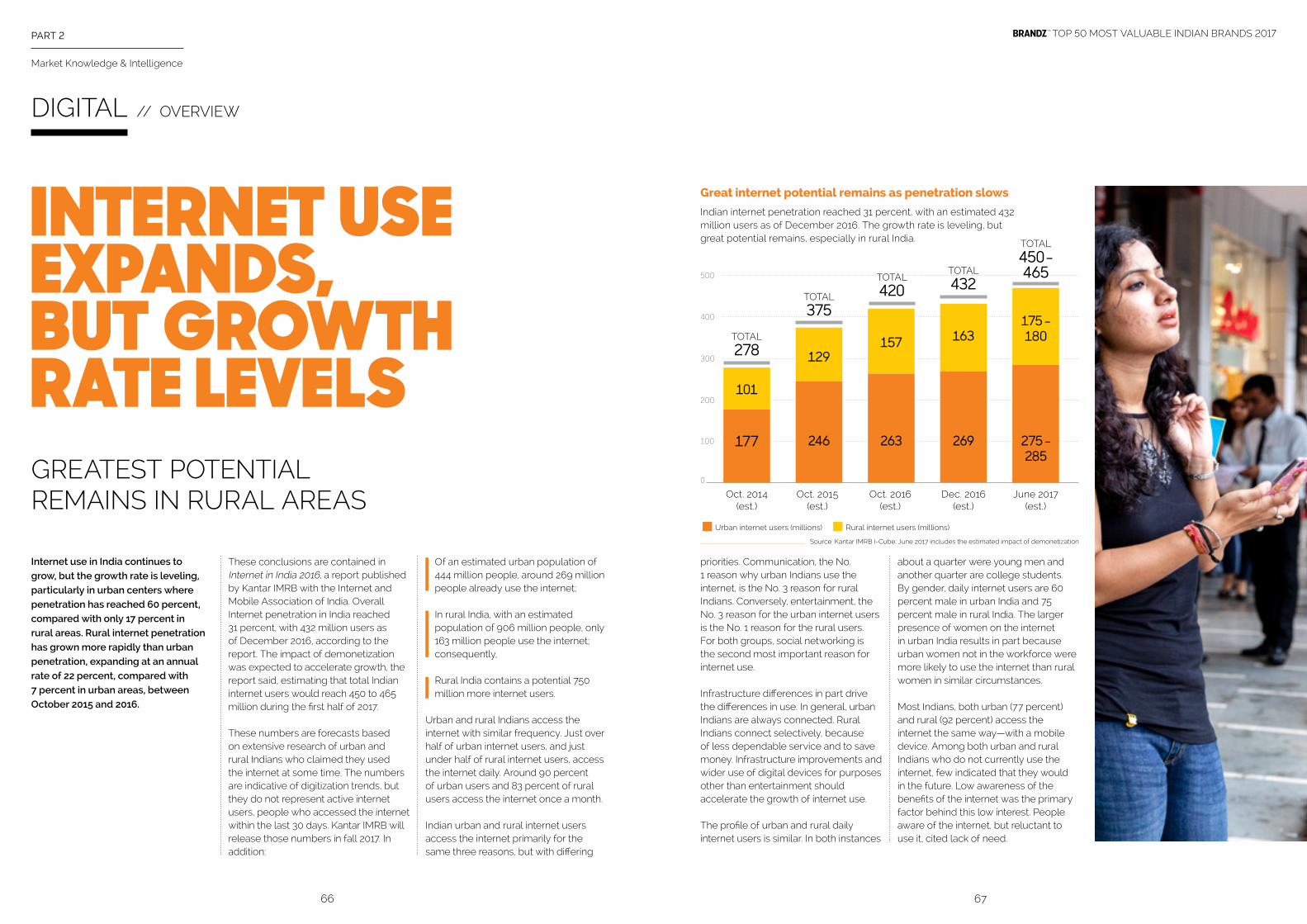

Internet use in India continues to

grow, but the growth rate is leveling,

particularly in urban centers where

penetration has reached 60 percent,

compared with only 17 percent in

rural areas. Rural internet penetration

has grown more rapidly than urban

penetration, expanding at an annual

rate of 22 percent, compared with

7 percent in urban areas, between

October 2015 and 2016.

These conclusions are contained in Internet in India 2016, a report published by Kantar IMRB with the Internet and Mobile Association of India. Overall Internet penetration in India reached 31 percent, with 432 million users as of December 2016, according to the report. The impact of demonetization was expected to accelerate growth, the report said, estimating that total Indian internet users would reach 450 to 465 million during the first half of 2017.

These numbers are forecasts based on extensive research of urban and rural Indians who claimed they used the internet at some time. The numbers are indicative of digitization trends, but they do not represent active internet users, people who accessed the internet within the last 30 days. Kantar IMRB will release those numbers in fall 2017. In addition:

GREATEST POTENTIAL REMAINS IN RURAL AREAS

INTERNET USE EXPANDS,BUT GROWTH RATE LEVELS

Of an estimated urban population of 444 million people, around 269 million people already use the internet;

In rural India, with an estimated population of 906 million people, only 163 million people use the internet; consequently,

Rural India contains a potential 750 million more internet users.

Urban and rural Indians access the internet with similar frequency. Just over half of urban internet users, and just under half of rural internet users, access the internet daily. Around 90 percent of urban users and 83 percent of rural users access the internet once a month.

Indian urban and rural internet users access the internet primarily for the same three reasons, but with differing

priorities. Communication, the No. 1 reason why urban Indians use the internet, is the No. 3 reason for rural Indians. Conversely, entertainment, the No. 3 reason for the urban internet users is the No. 1 reason for the rural users. For both groups, social networking is the second most important reason for internet use.