Embed Size (px)

Citation preview

Economic Analysis for Lawyers

butler 3e 00 fmt 7/24/14 11:38 AM Page i

Carolina Academic PressLaw Advisory Board

❦

Gary J. Simson, ChairmanDean, Mercer University School of Law

Raj BhalaUniversity of Kansas School of Law

Davison M. DouglasDean, William and Mary Law School

Paul FinkelmanAlbany Law School

Robert M. JarvisShepard Broad Law CenterNova Southeastern University

Vincent R. JohnsonSt. Mary’s University School of Law

Peter NicolasUniversity of Washington School of Law

Michael A. OlivasUniversity of Houston Law Center

Kenneth L. PortWilliam Mitchell College of Law

H. Jefferson PowellDuke University School of Law

Michael P. ScharfCase Western Reserve University School of Law

Michael Hunter SchwartzDean, William H. Bowen School of LawUniversity of Arkansas at Little Rock

Peter M. ShaneMichael E. Moritz College of Law

The Ohio State University

butler 3e 00 fmt 7/24/14 11:38 AM Page ii

Economic Analysis for Lawyers

third edition

Henry N. ButlerGeorge Mason University Foundation Professor of Law and

Executive Director, Law & Economics Center, George Mason University School of Law

Christopher R. DrahozalJohn M. Rounds Professor of Law,

University of Kansas School of Law

Joanna ShepherdProfessor of Law,

Emory University School of Law

Carolina Academic PressDurham, North Carolina

butler 3e 00 fmt 7/24/14 11:38 AM Page iii

Copyright © 1998, 2006, 2014Henry N. Butler, Christopher R. Drahozal, and Joanna Shepherd

All Rights Reserved

ISBN: 978-1-59460-997-8 LCCN: 2014943567

Carolina Academic Press700 Kent Street

Durham, NC 27701Telephone (919) 489-7486

Fax (919) 493-5668www.cap-press.com

Printed in the United States of America

butler 3e 00 fmt 7/24/14 11:38 AM Page iv

To Paige–H.N.B.

To Julia–C.R.D.

To Ted and Sophie–J.S.

butler 3e 00 fmt 7/24/14 11:38 AM Page v

butler 3e 00 fmt 7/24/14 11:38 AM Page vi

Contents

Table of Cases xviiPreface to the Third Edition xxiPreface to the Second Edition xxiiiPreface to the First Edition xxv

Chapter I · The Economics Perspective: Incentives Matter 3Austan Goolsbee, Where the Buses Run on Time 3

A. Economic Behavior 51. Opportunity Costs, Economic Choices, and the Margin 52. Assumptions About Human Behavior 6

Michael C. Jensen and William H. Meckling, The Nature of Man 6Notes and Questions 10

3. Assumptions about Firm Behavior 12Matsushita Elec. Indus. Co. v. Zenith Radio Corp. 12

Notes and Questions 15B. Property Rights and Exchange in a Free Market Economy 17

1. An Overview of the Efficient Property Rights System 182. Enforcement of Property Rights 19

Guido Calabresi & A. Douglas Melamed, Property Rules, Liability Rules, and Inalienability: One View of the Cathedral 20Notes and Questions 21

3. Poorly Defined Property Rights 21Garrett Hardin, The Tragedy of the Commons 21

Notes and Questions 22Wronski v. Sun Oil Co. 22

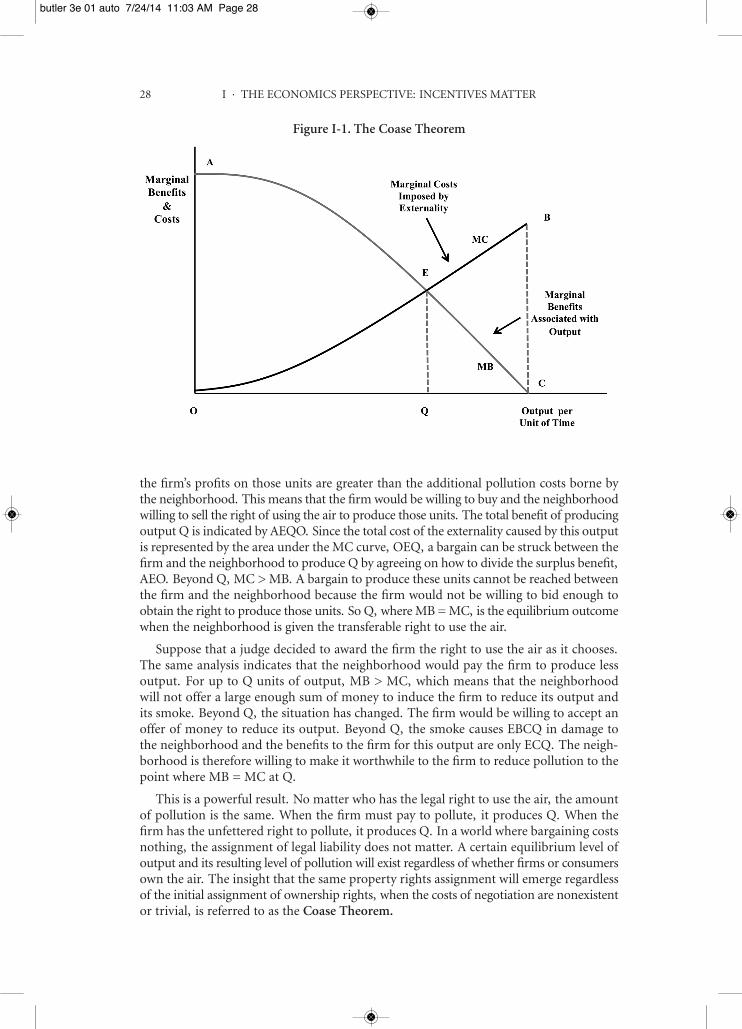

Notes and Questions 244. Public Goods 265. Externalities, Property Rights, and the Coase Theorem 27

Miller v. Schoene 29Fontainebleau Hotel Corp. v. Forty-Five Twenty-Five, Inc. 30

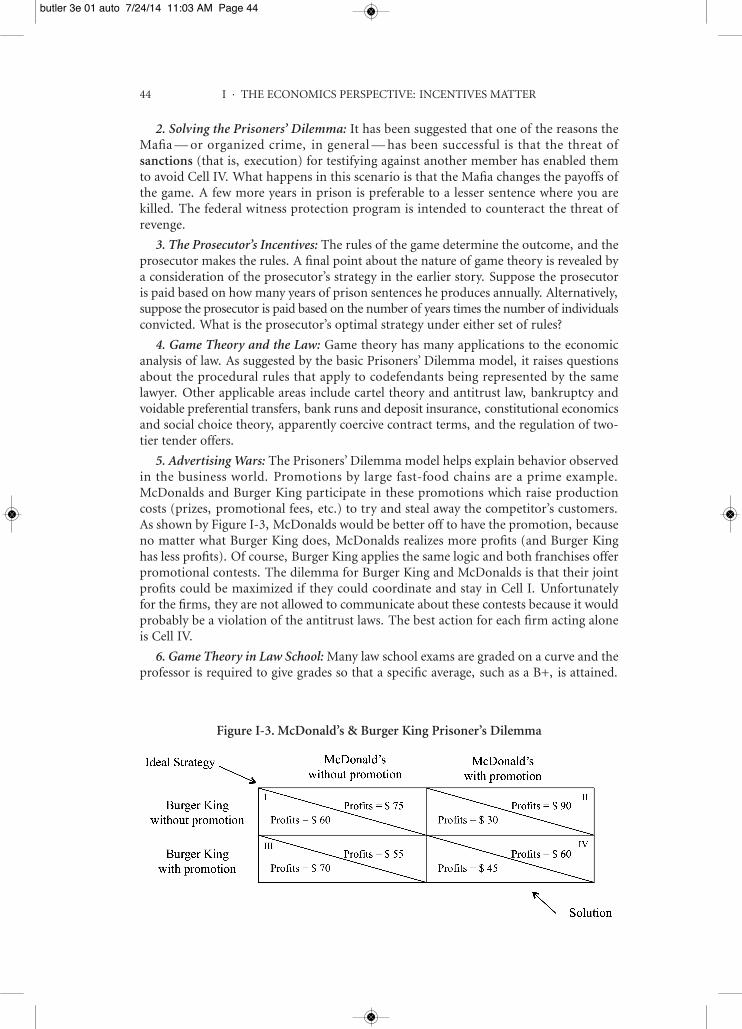

Notes and Questions 31C. Legal Analysis and the Art of Economics 33

Eldred v. Ashcroft 33Notes and Questions 37

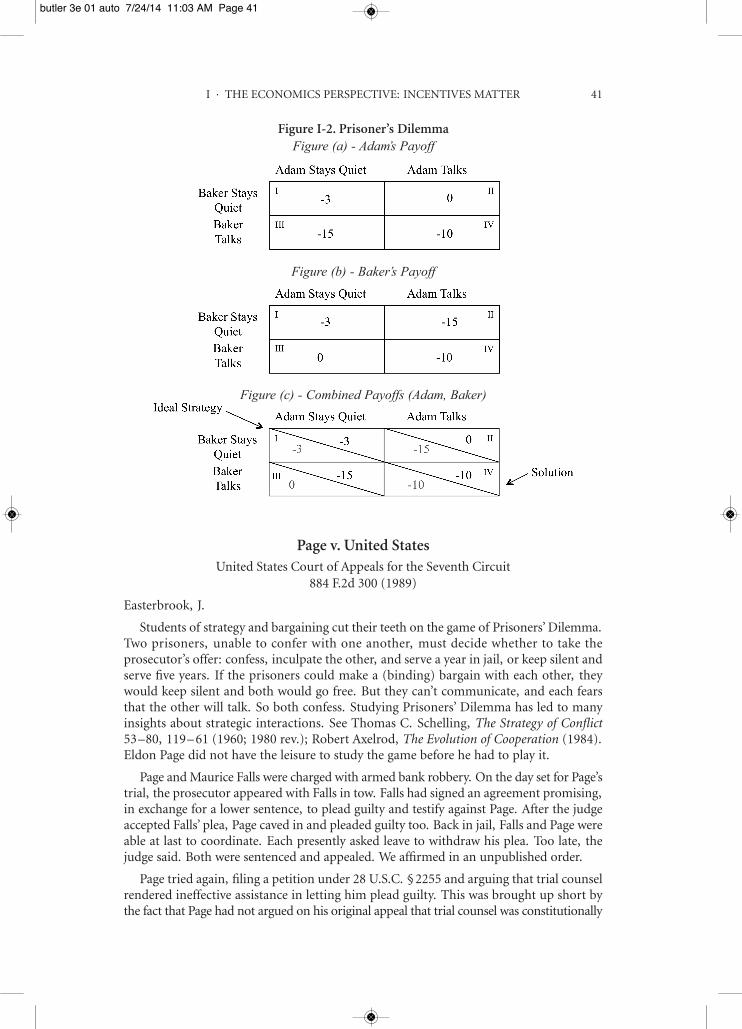

D. Game Theory 39Page v. United States 41

Notes and Questions 43

vii

butler 3e 00 fmt 7/24/14 11:38 AM Page vii

viii CONTENTS

E. Positive versus Normative Economic Analysis 451. Positive Economic Analysis and Scientific Methodology 45

In Re Aluminum Phosphide Antitrust Litigation 46Notes and Questions 50

2. Efficiency and Other Normative Goals 51

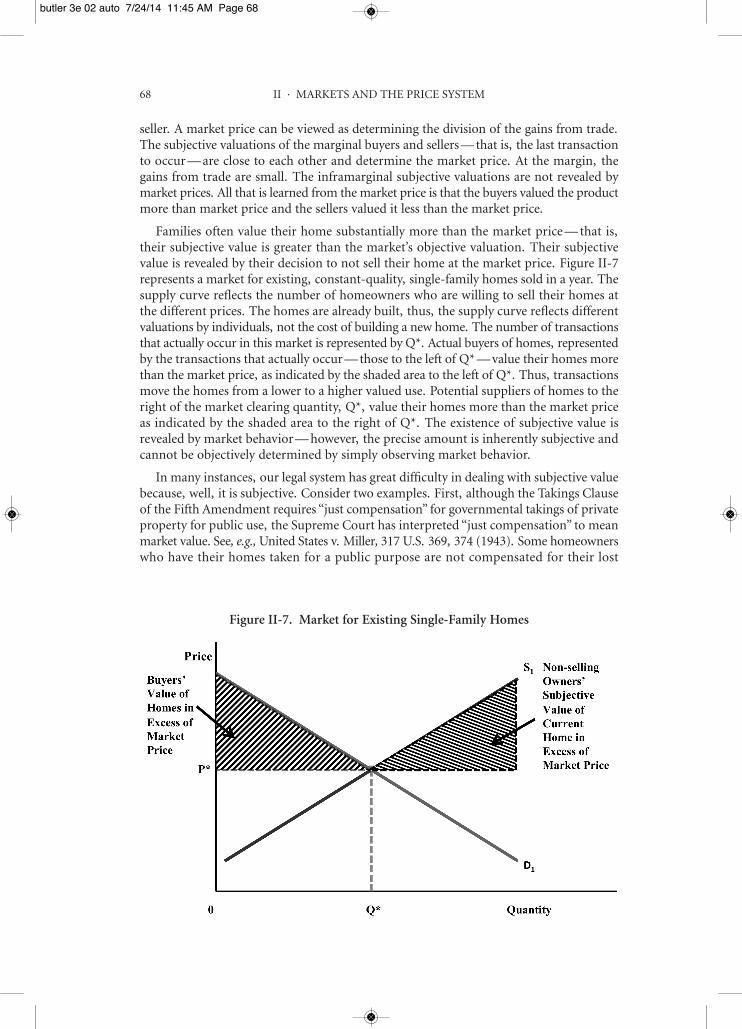

Chapter II · Markets and the Price System 55A. The Law of Demand 56

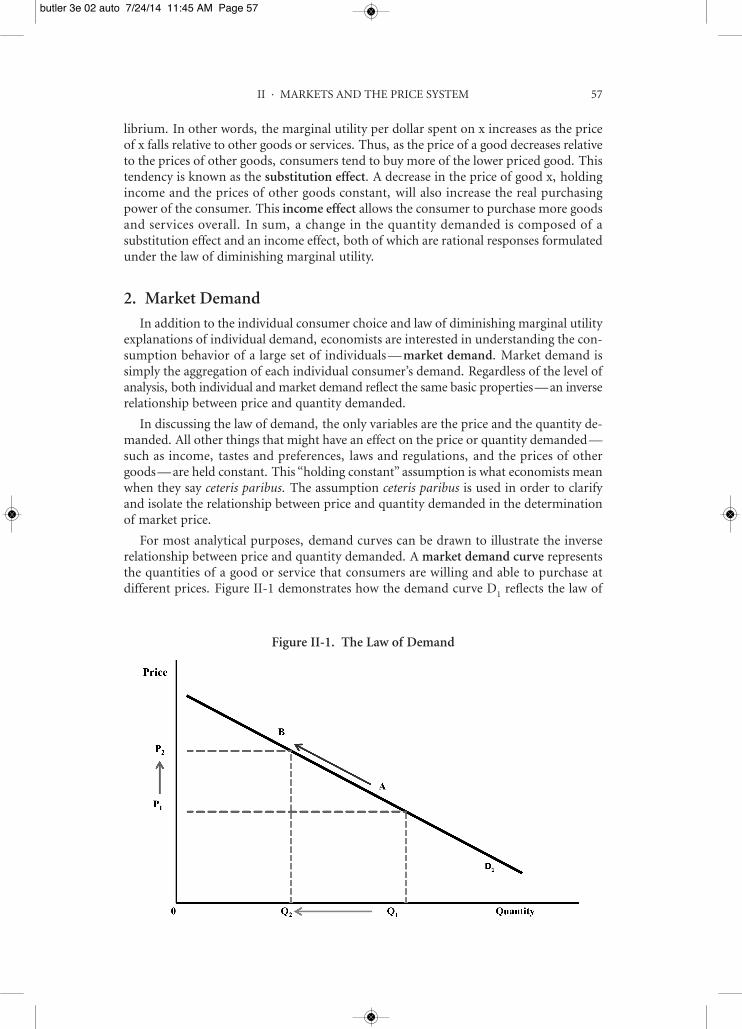

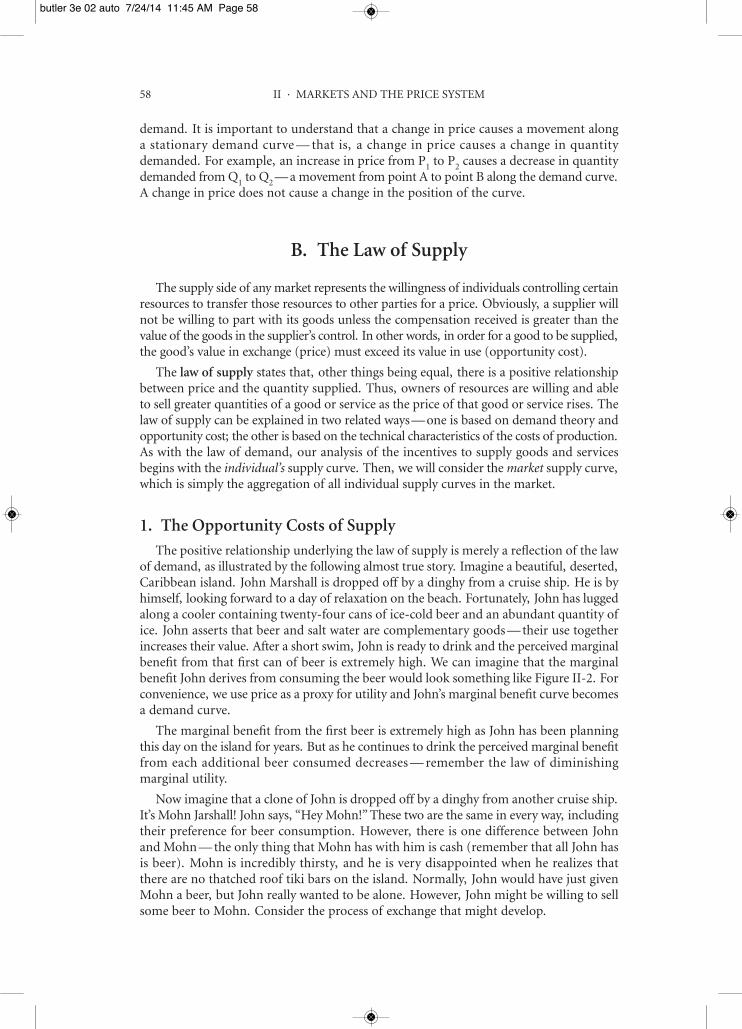

1. Consumer Choice 562. Market Demand 57

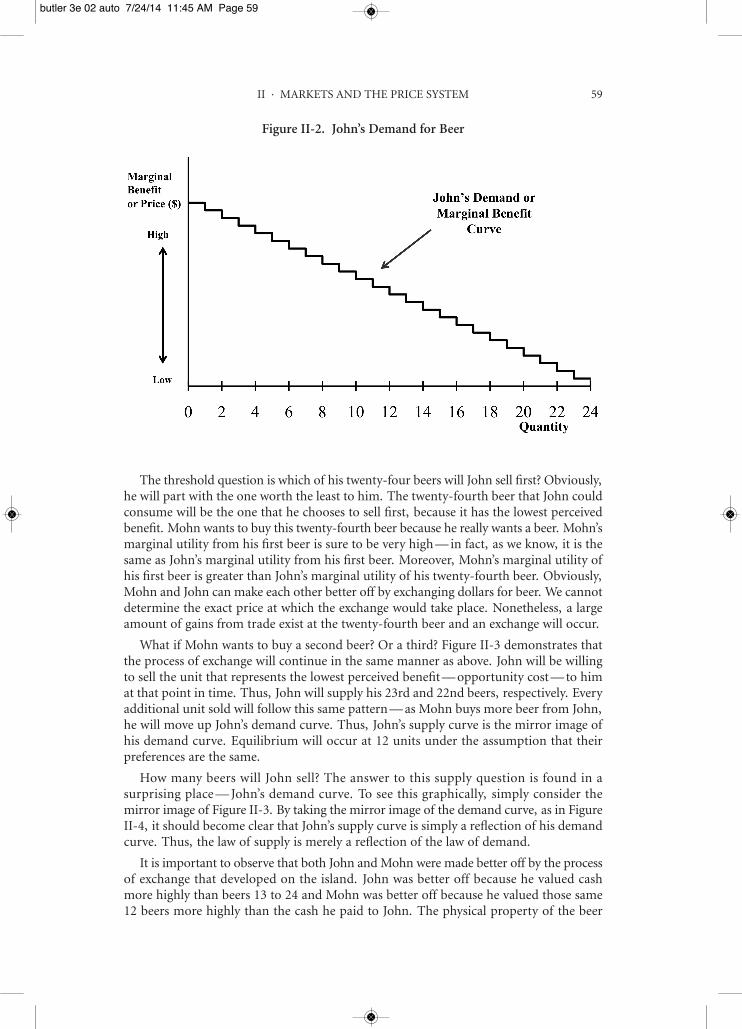

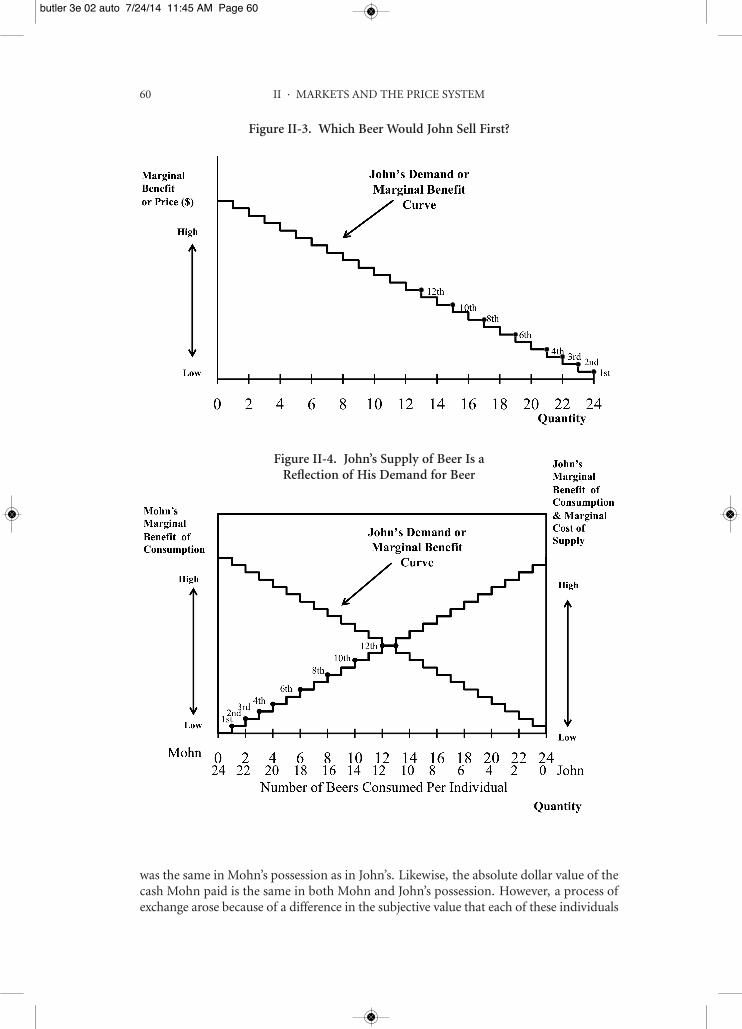

B. The Law of Supply 581. The Opportunity Costs of Supply 582. Supply and Costs of Production 61

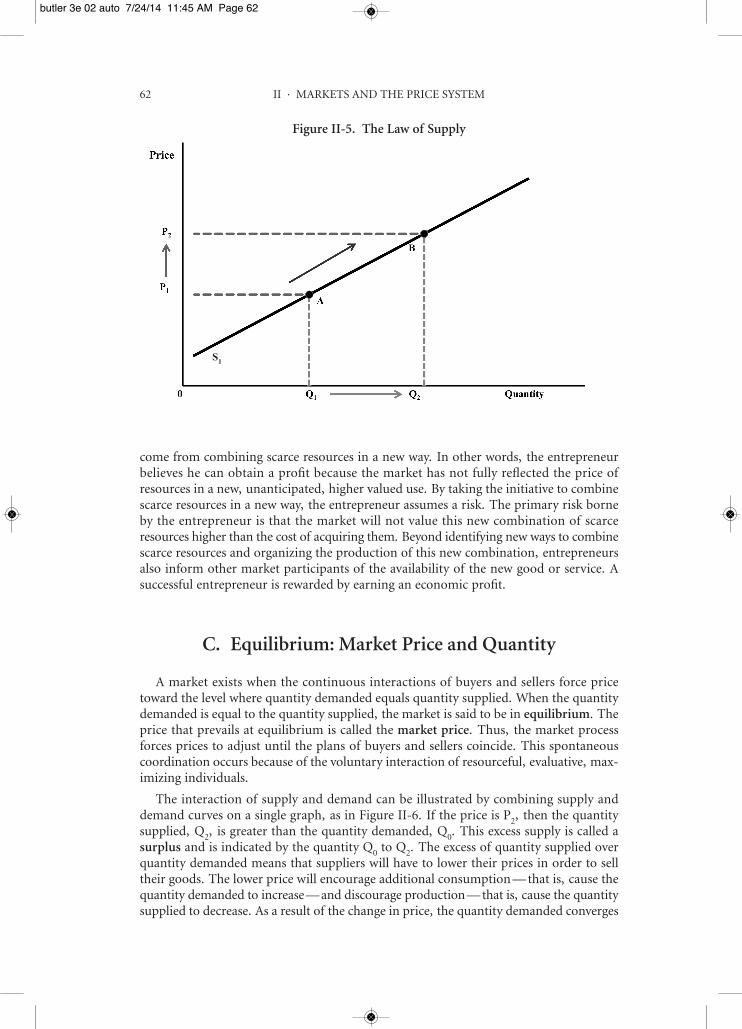

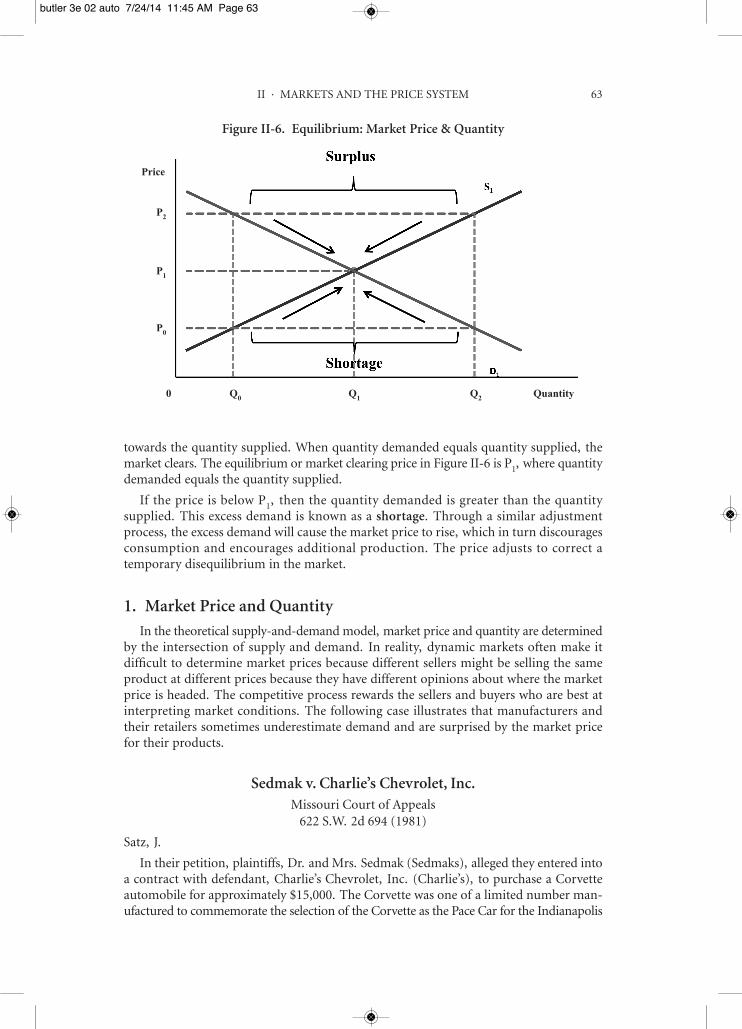

C. Equilibrium: Market Price and Quantity 621. Market Price and Quantity 63

Sedmak v. Charlie’s Chevrolet, Inc. 63Notes and Questions 65

2. Market Prices and Subjective Value 67Peevyhouse v. Garland Coal & Mining Co. 69

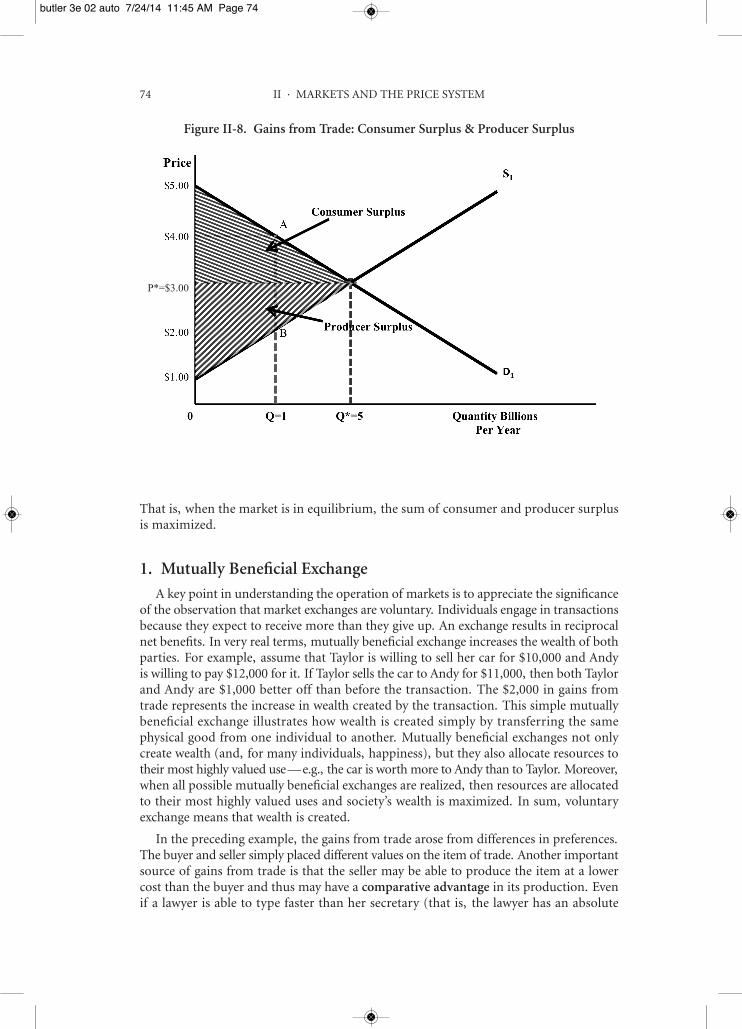

Notes and Questions 72D. Gains From Trade: Consumer Surplus and Producer Surplus 73

1. Mutually Beneficial Exchange 742. Individual Self-Interest, Free Markets, and Social Welfare:

The Invisible Hand 75Adam Smith, An Inquiry into the Nature and Causes of the Wealth

of Nations 76Leonard E. Read, I, Pencil: My Family Tree as Told to Leonard E. Read 76

Notes and Questions 783. Unequal Bargaining Power and the Limits of Mutually Beneficial

Exchange 80a. Unconscionability 80

Williams v. Walker Thomas Furniture Co. 80Williams v. Walker Thomas Furniture Co. II 81

Notes and Questions 83b. Modification and the Pre-Existing Duty Rule 86

Alaska Packers’ Association v. Domenico 86Notes and Questions 87

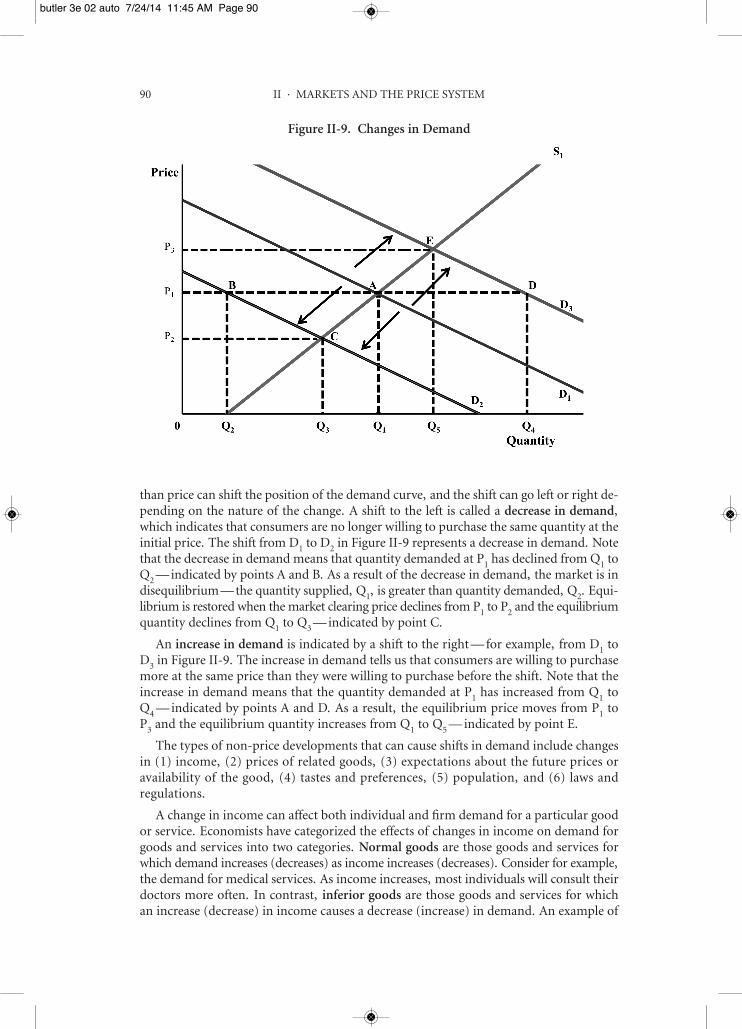

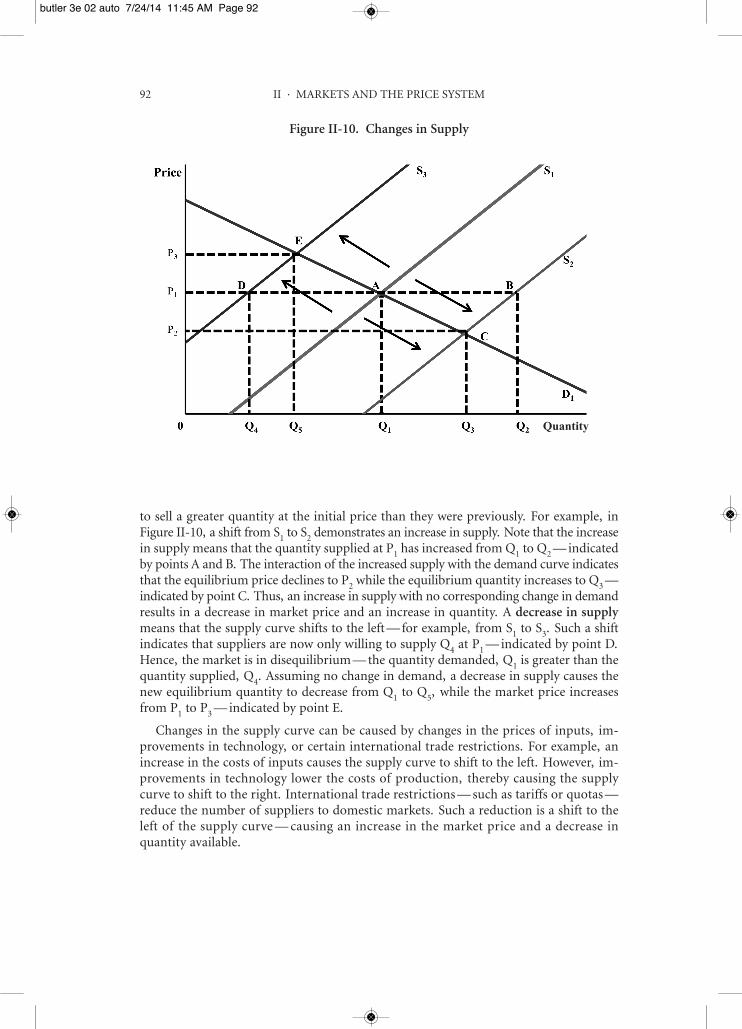

E. Changes in Demand and Supply 891. Changes in Demand 892. Changes in Supply 91

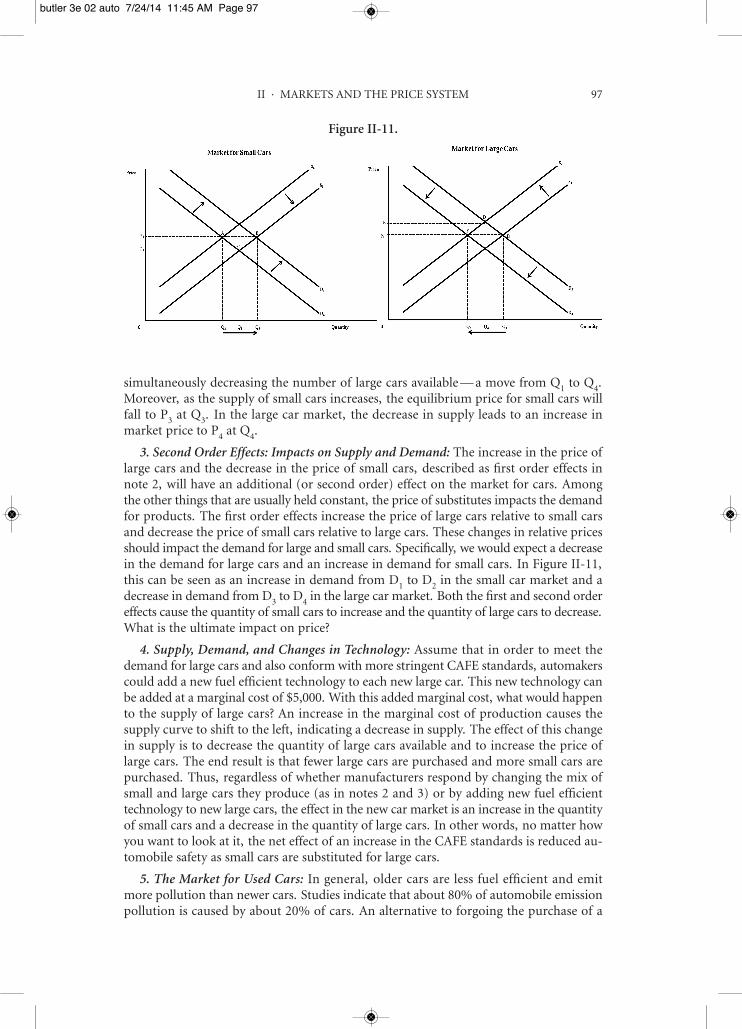

Competitive Enterprise Institute v. National Highway Traffic Safety Admin. 93Notes and Questions 96

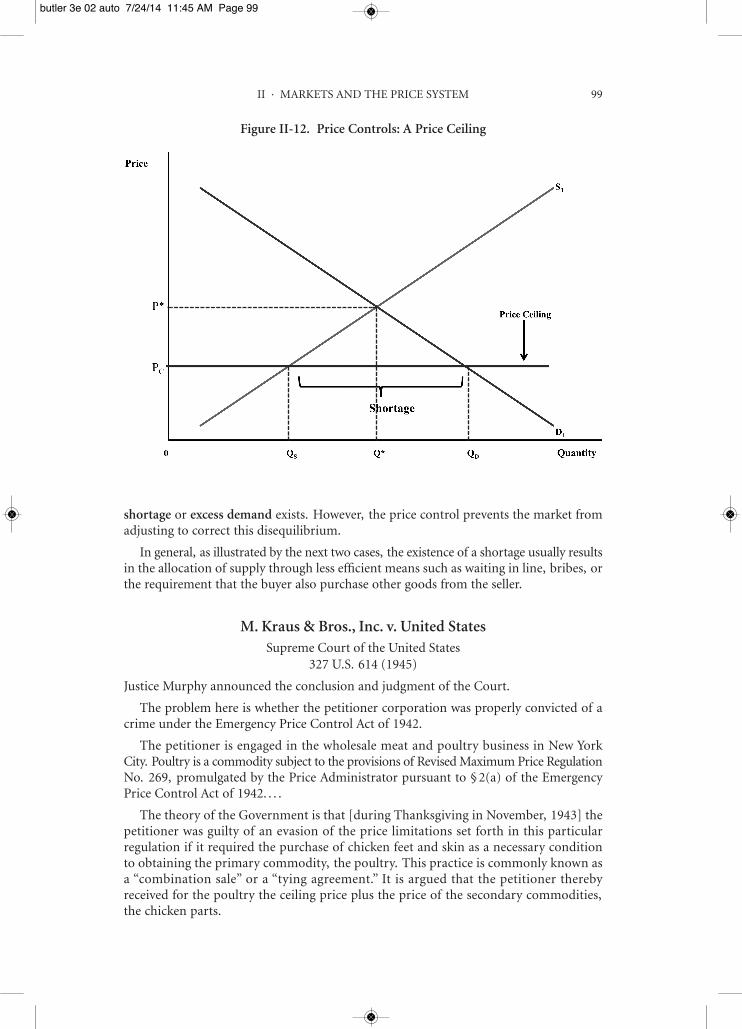

F. Price Controls 981. Price Ceilings 98

M. Kraus & Bros., Inc. v. United States 99Notes and Questions 102

Jones v. Star Credit Corp. 104Notes and Questions 106

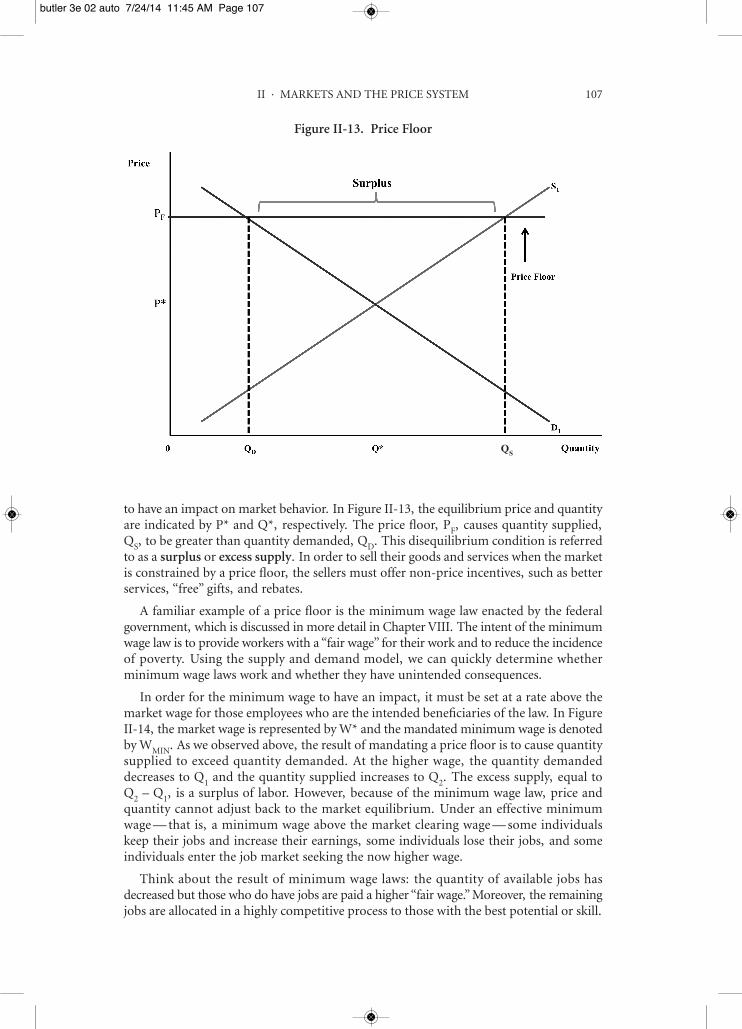

2. Price Floors 106

butler 3e 00 fmt 7/24/14 11:38 AM Page viii

CONTENTS ix

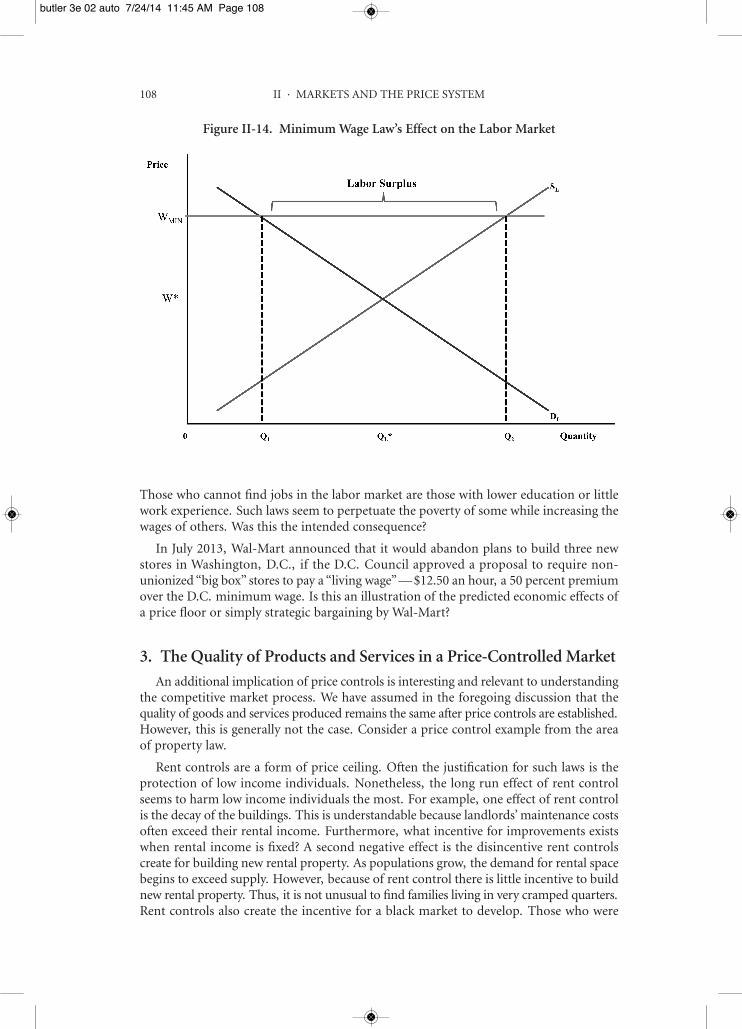

3. The Quality of Products and Services in a Price-Controlled Market 108G. Elasticity: The Responsiveness of Supply and Demand to a Price Change 109

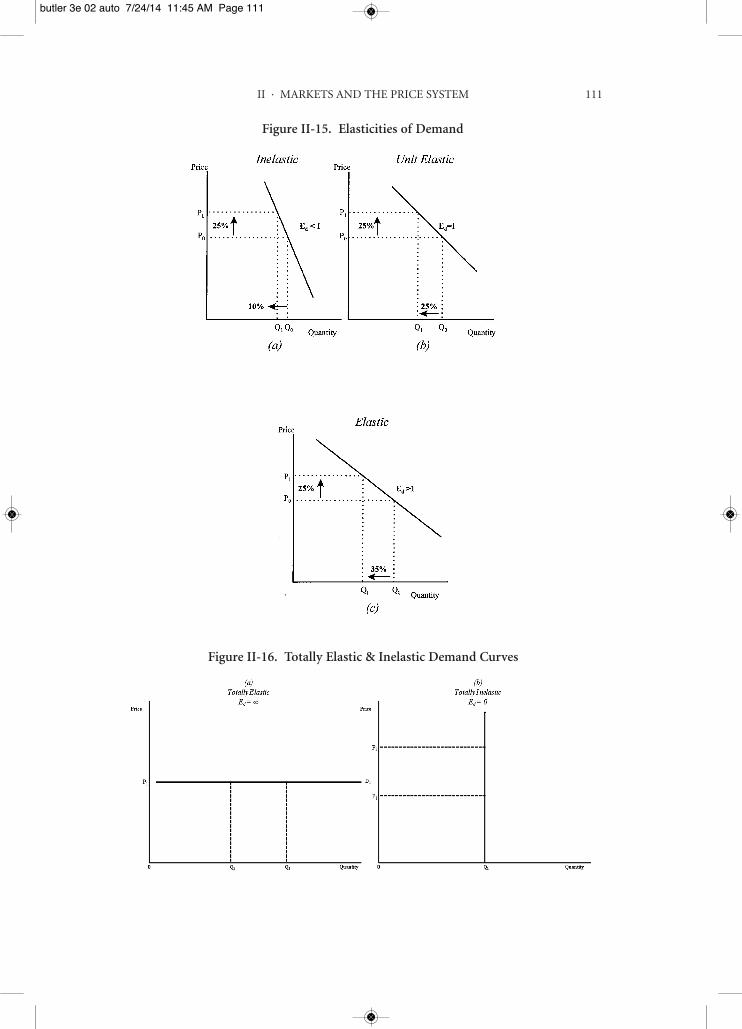

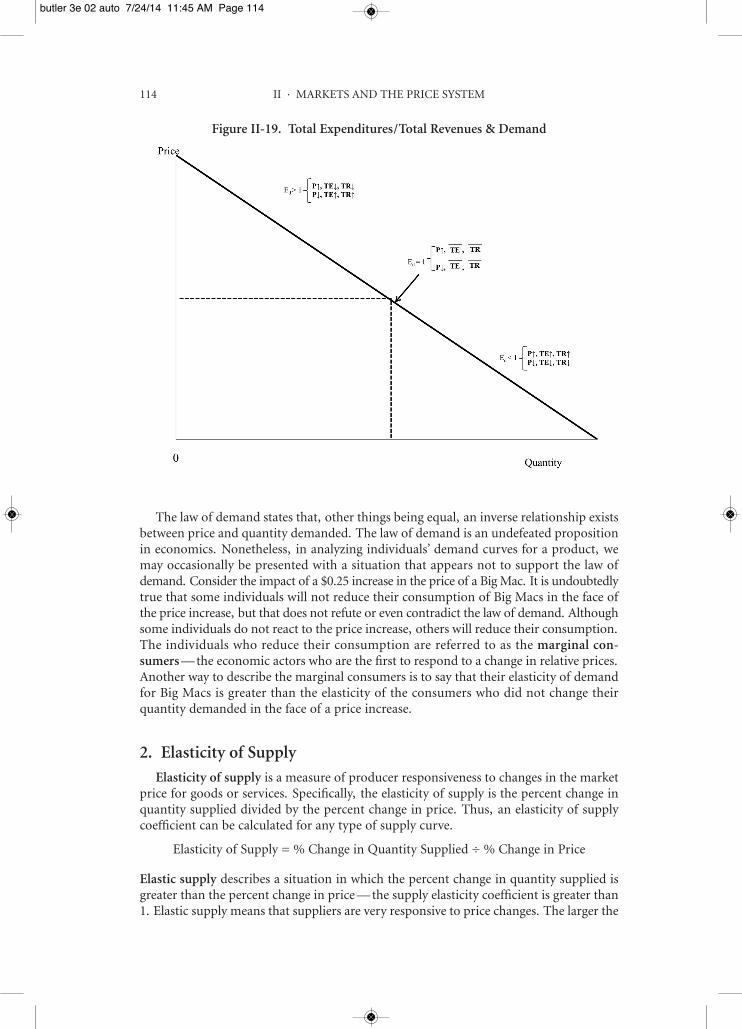

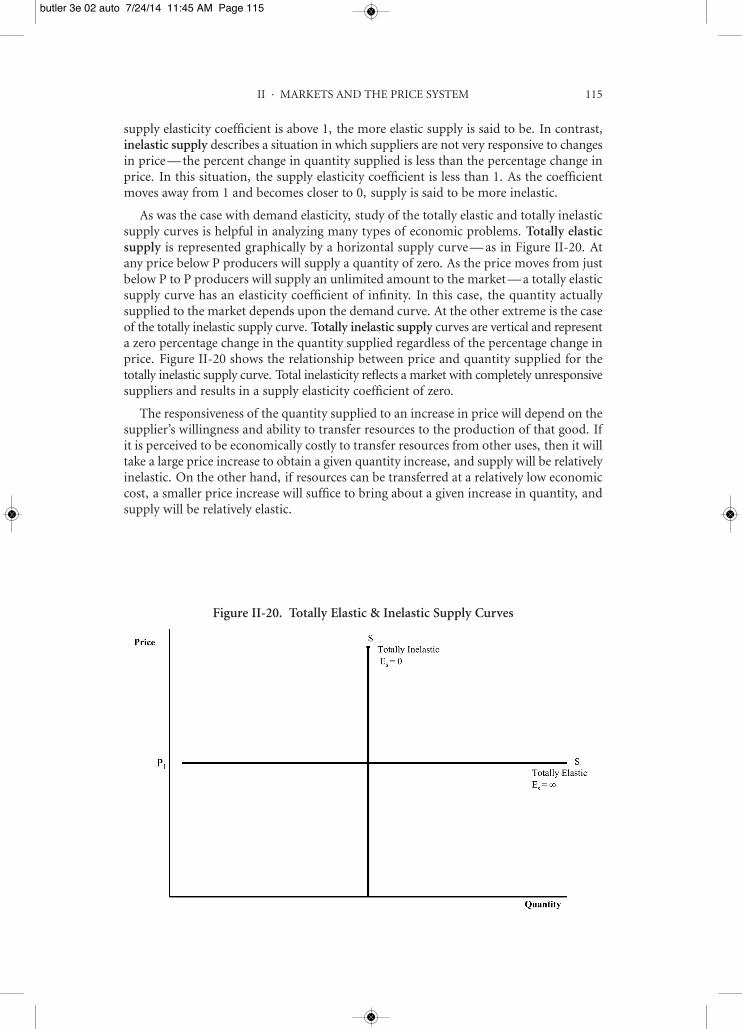

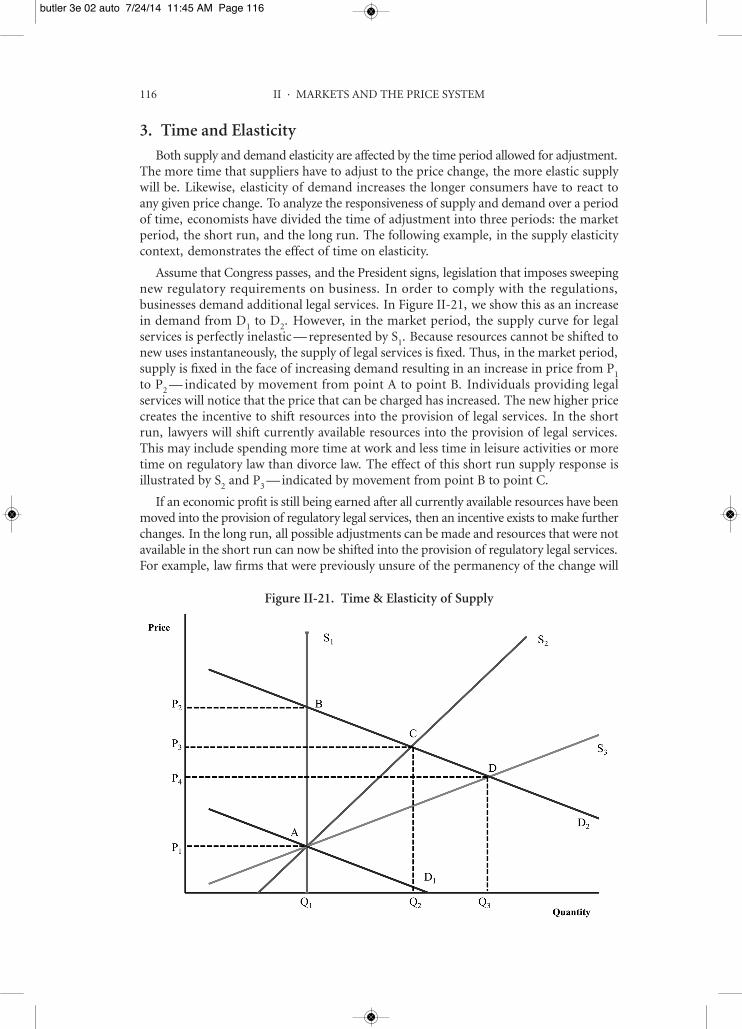

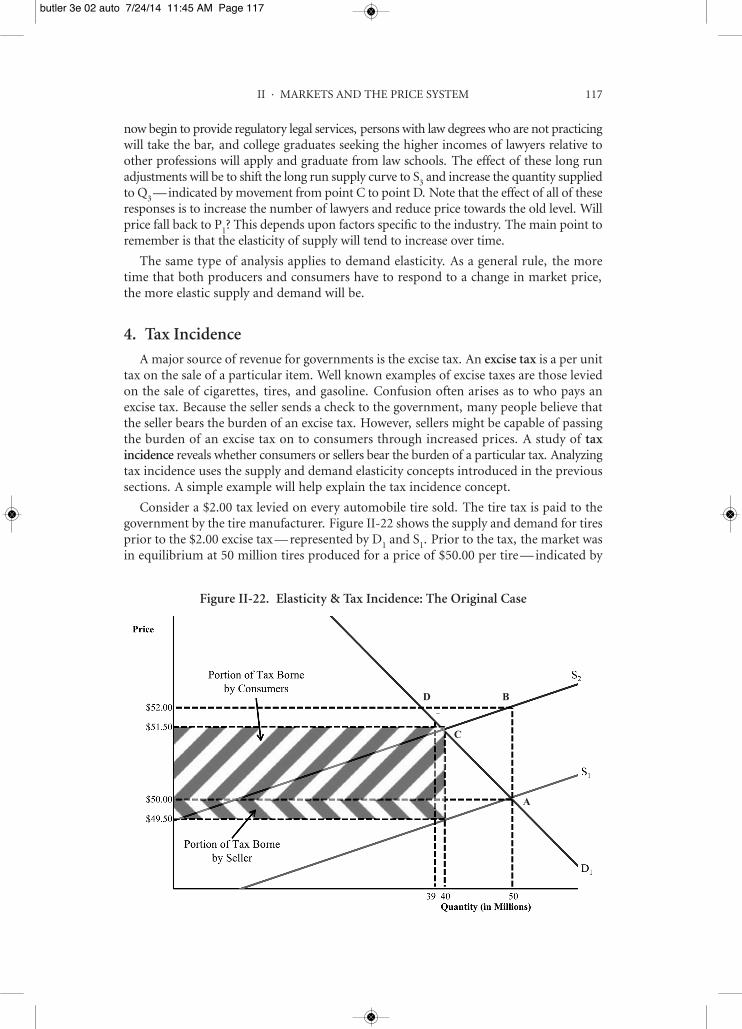

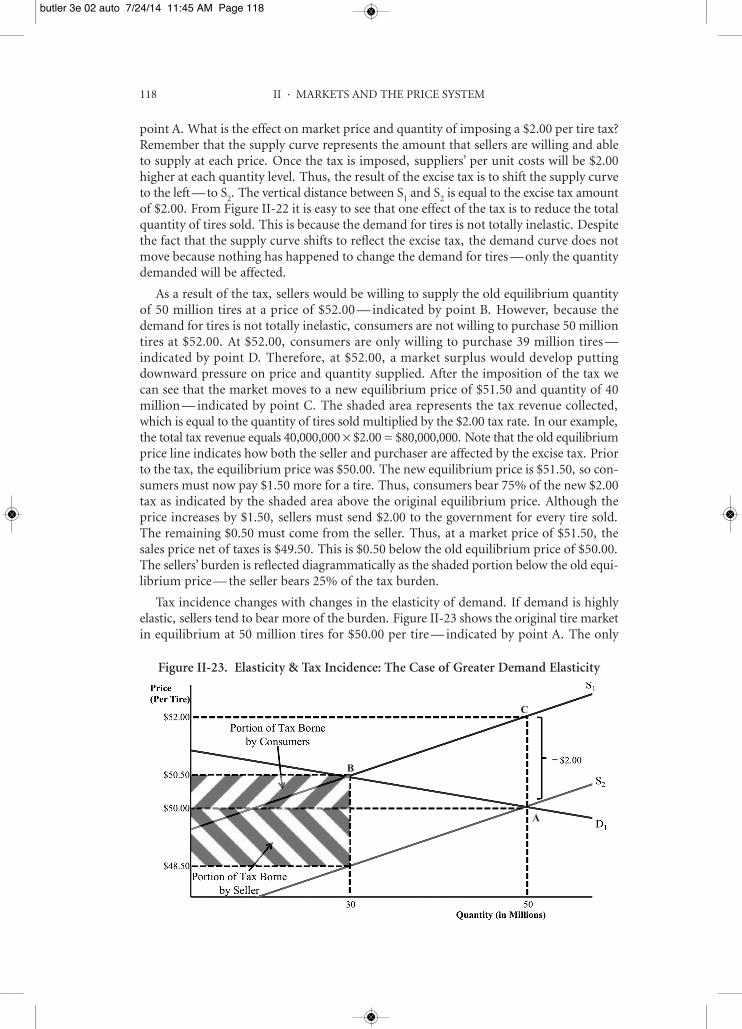

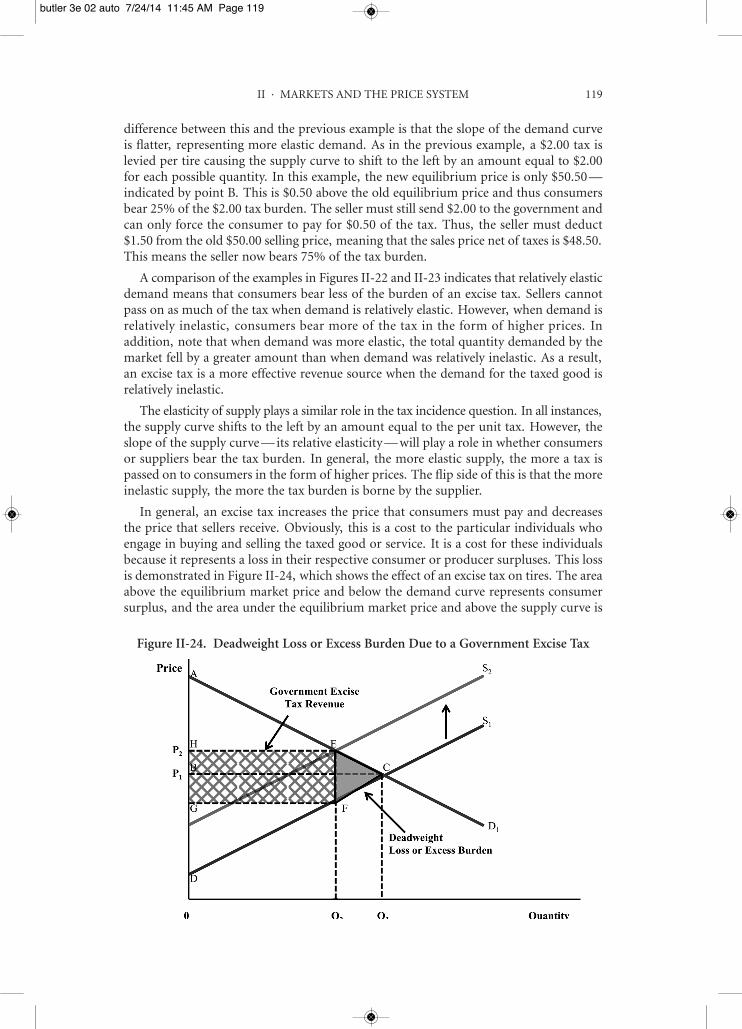

1. Elasticity of Demand 1092. Elasticity of Supply 1143. Time and Elasticity 1164. Tax Incidence 117

H. The Role of Prices 120Friedreich von Hayek, The Use of Knowledge in Society 120

Notes and Questions 122

Chapter III · The Legislative Process and the Courts 125A. Normative Grounds for Government Intervention 125

1. Market Failures 126a. Information Problems 126b. Externalities 127c. Monopoly 128d. Public Goods 129

2. Distributional Issues 129B. Public Choice Economics 130

Fred S. McChesney, Money for Nothing: Politicians, Rent Extraction, and Political Extortion 131Notes and Questions 134

City of Columbia v. Omni Outdoor Advertising, Inc. 137Notes and Questions 140

West Lynn Creamery, Inc. v. Healy 142Notes and Questions 146

C. The Economics of the Court System 1471. Public Choice and the Courts 147

Republican Party of Minnesota v. White 148Notes and Questions 155

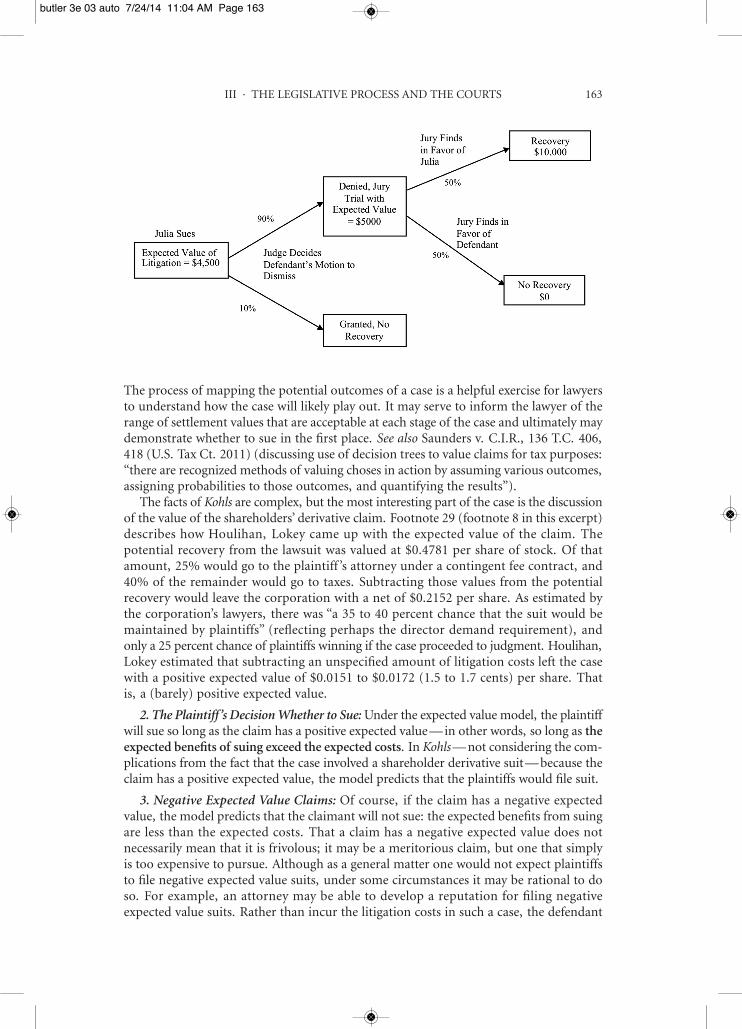

2. Suit and Settlement 158Kohls v. Duthie 159

Notes and Questions 1623. The Economics of Court Procedures 167

a. Discovery 167Hagemeyer North America, Inc. v. Gateway Data Sciences Corp. 168

Notes and Questions 171b. Class Actions 172

In re: Bridgestone/Firestone, Inc. 173Notes and Questions 175

Lane v. Facebook, Inc. 176Notes and Questions 181

4. Arbitration 182Carbajal v. H&R Block Tax Services, Inc. 182

Notes and Questions 183

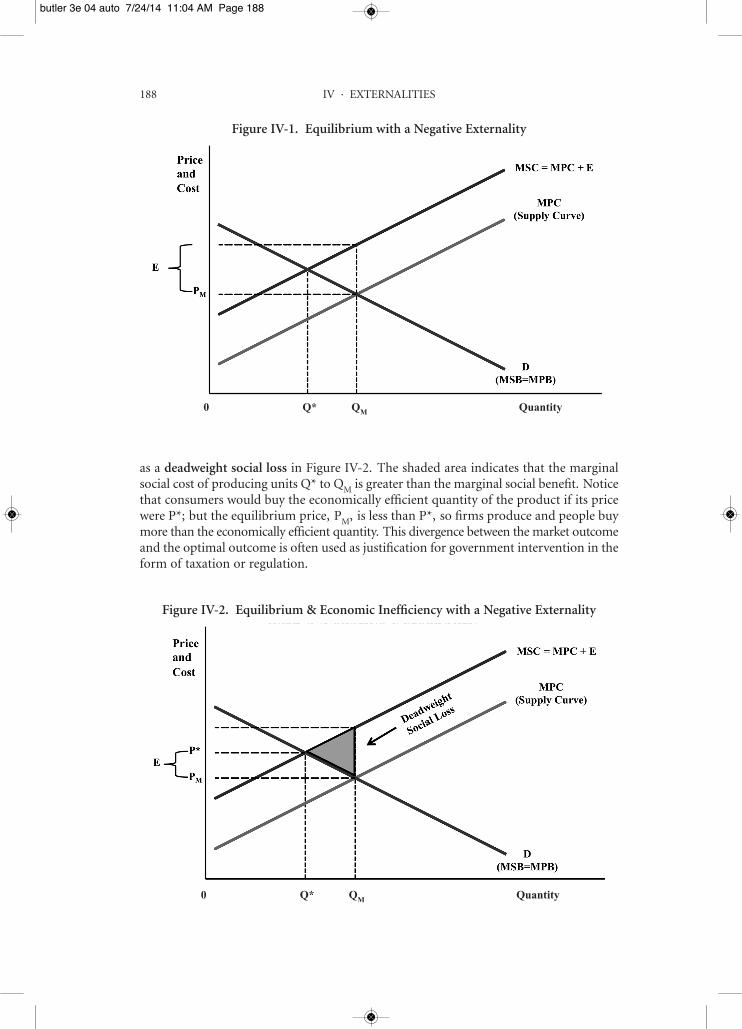

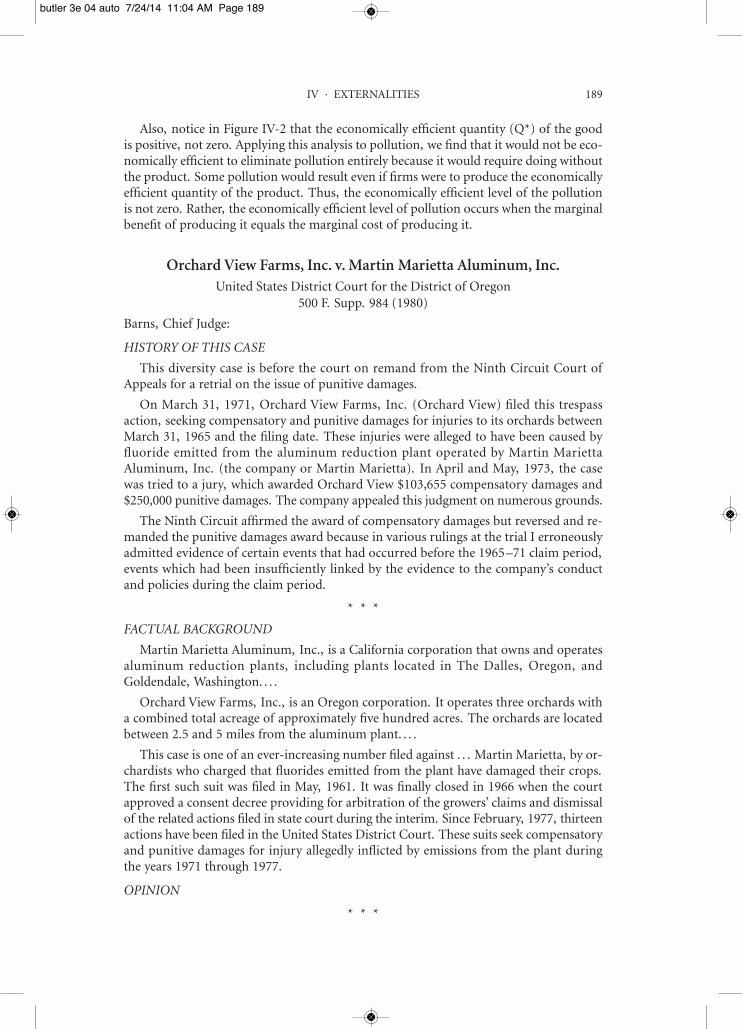

Chapter IV · Externalities 185A. Externalities 185

1. Negative Externalities 187Orchard View Farms, Inc. v. Martin Marietta Aluminum, Inc. 189

butler 3e 00 fmt 7/24/14 11:38 AM Page ix

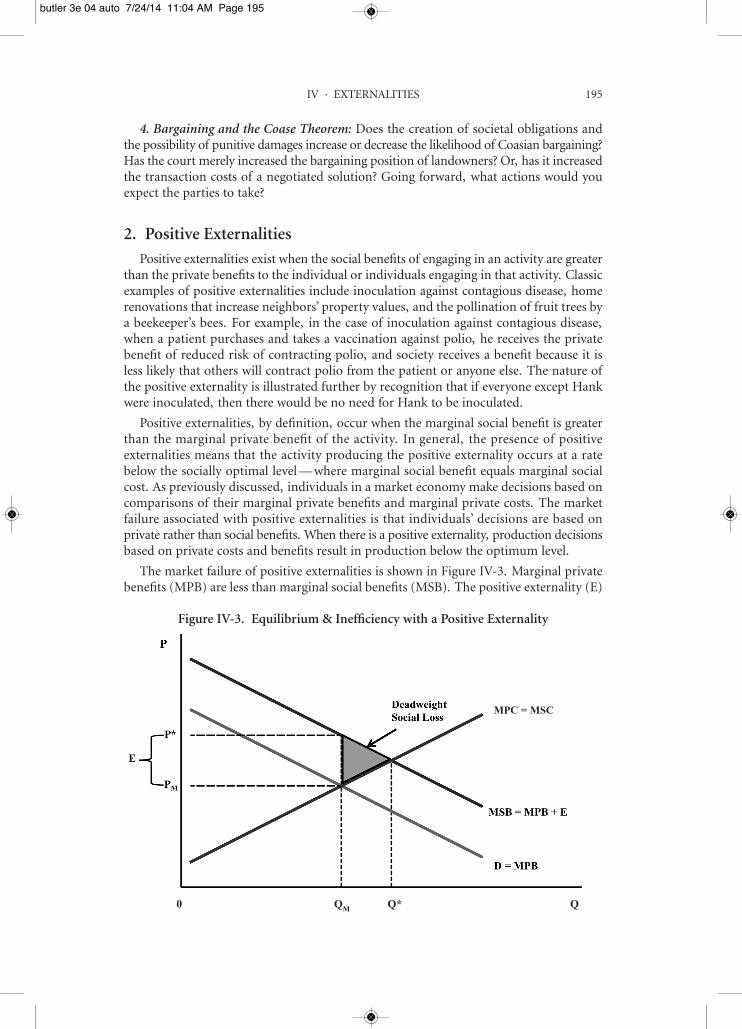

Notes and Questions 1942. Positive Externalities 195

B. Dealing with Externalities 1961. The Assignment and Enforcement of Property Rights 197

a. Bargaining and the Coase Theorem 198Prah v. Maretti 198

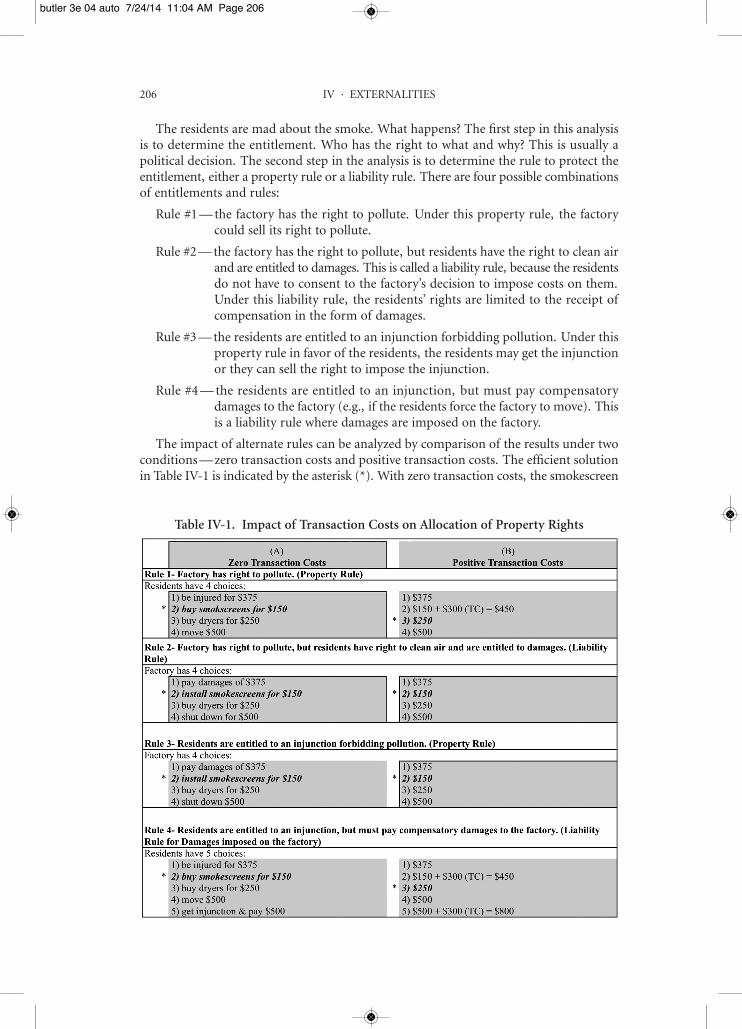

Notes and Questions 205b. Transaction Costs 205

Boomer v. Atlantic Cement Co., Inc. 207Notes and Questions 211

Spur Industries, Inc. v. Del E. Webb Development Co. 213Notes and Questions 217

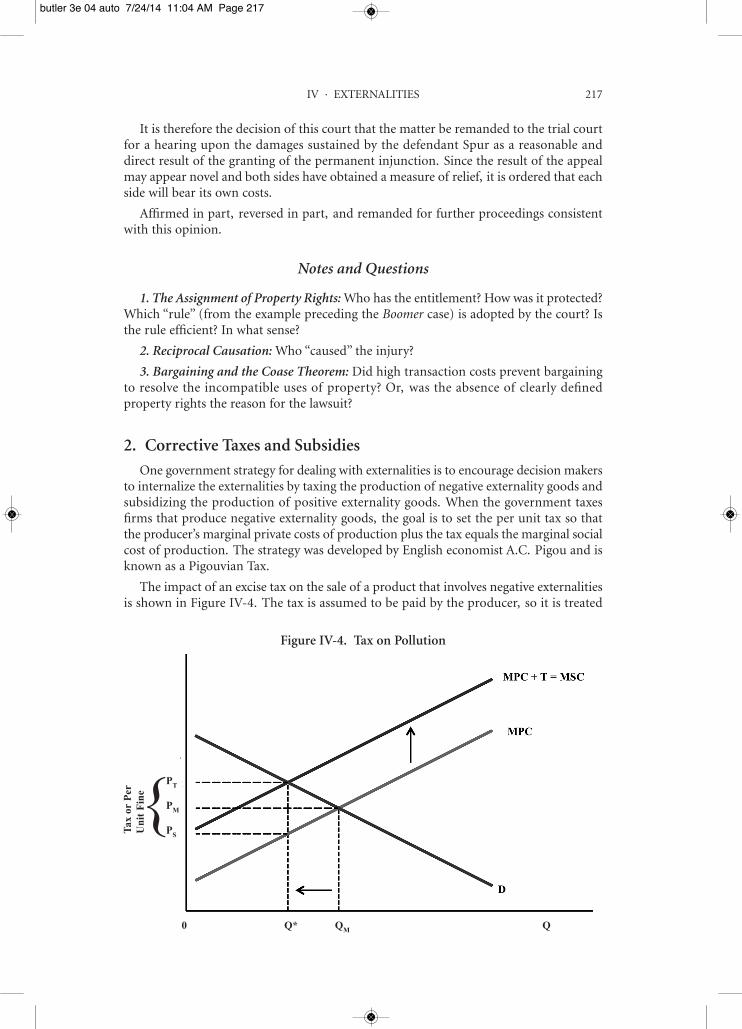

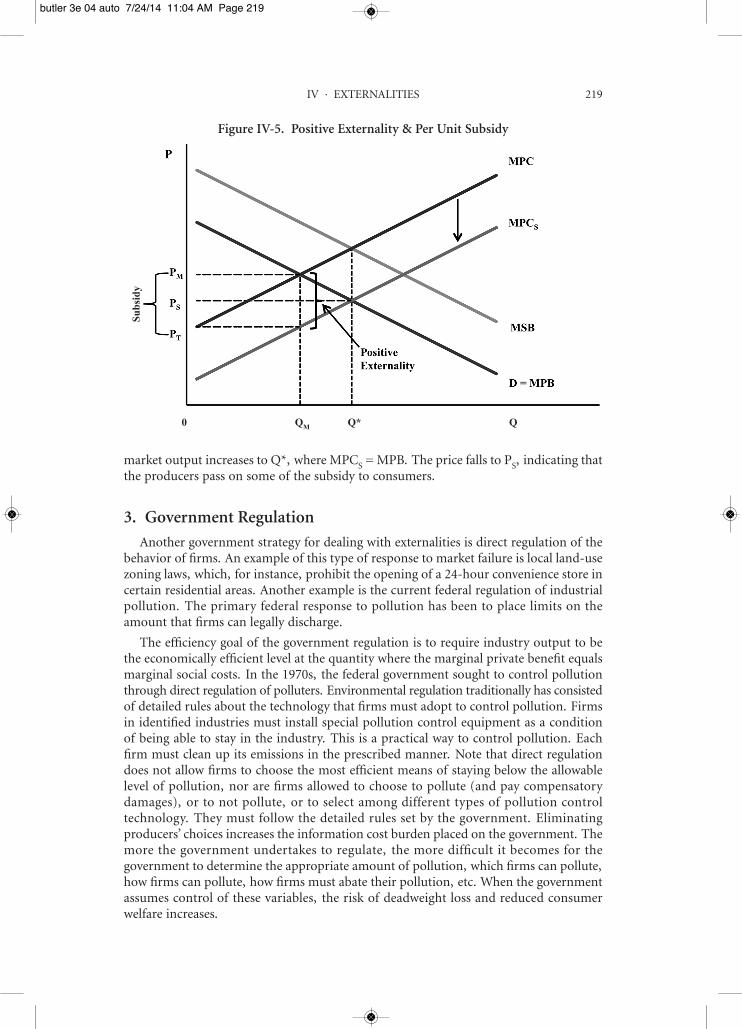

2. Corrective Taxes and Subsidies 2173. Government Regulation 219

a. Direct Regulation Versus Corrective Taxes 220b. Selling Rights to Pollute 220

C. Market Failures and Government Failures 222Terry L. Anderson, Markets and the Environment: Friends or Foes? 223

Notes and Questions 229

Chapter V · Information Costs and Transaction Costs 231A. Asymmetric Information and Market Responses 233

1. The Market for “Lemons” 2332. Adverse Selection and Insurance Contracts 2343. Reputational Bonds and Other Market Mechanisms for Disclosing

Information About Quality 234Benjamin Klein & Keith Leffler, The Role of Market Forces in

Assuring Contractual Performance 235Notes and Questions 239

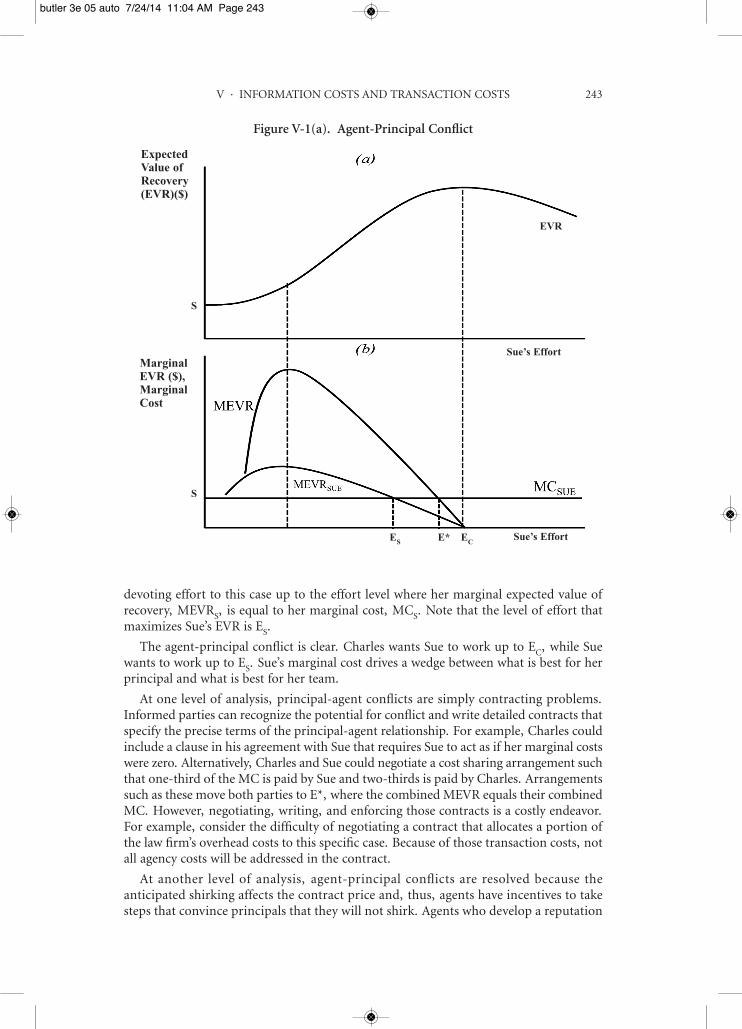

B. Monitoring Contractual Performance: Agent-Principal Contracting 241C. Opportunism: Market and Contractual Solutions 244

1. Firm-Specific Investments and the Appropriation of Quasi-Rents 246Lake River Corp. v. Carborundum Co. 247

Notes and Questions 2502. Franchising 254

Corenswet, Inc. v. Amana Refrigeration, Inc. 255Benjamin Klein, Transaction Cost Determinants of “Unfair”

Contractual Arrangements 259Notes and Questions 263

D. Corporate Governance 2661. Shareholder Voting and Rationally Ignorant Shareholders 2672. Agency Costs and Owner/Manager Conflicts 2683. The Contractual Theory of the Corporation 269

a. The Market for Corporate Control 270Notes on the Market for Corporate Control 271

b. Product Market Competition 272c. Capital Market Competition and Capital Structure 272d. Corporate Performance and Executive Compensation 273

Kamin v. American Express Co. 274

x CONTENTS

butler 3e 00 fmt 7/24/14 11:38 AM Page x

Notes and Questions 276e. Markets for Managers 277f. The Board of Directors 277g. Ownership Structure 278h. Corporate Law and Fiduciary Duties 278

Jordan v. Duff and Phelps, Inc. 279Notes and Questions 285

i. Corporate Federalism 286Questions on Corporate Federalism 287

j. Corporate Federalization 287Notes and Questions on Corporate Federalization 288

Chapter VI · Risk 291A. Economics of Uncertainty and Risk 291

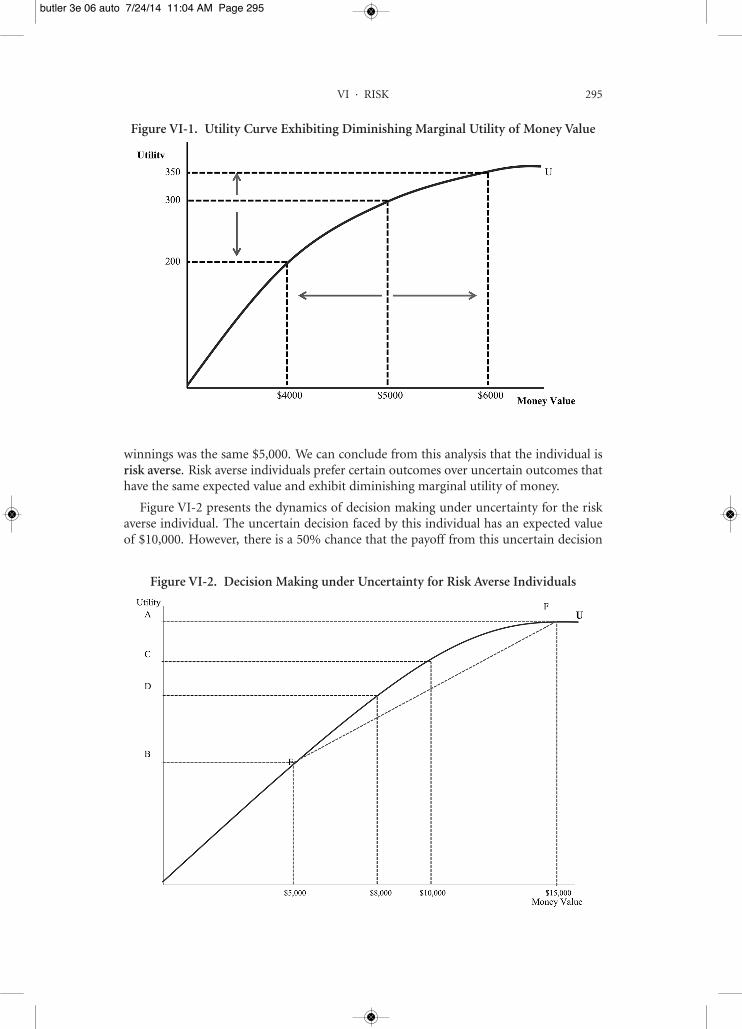

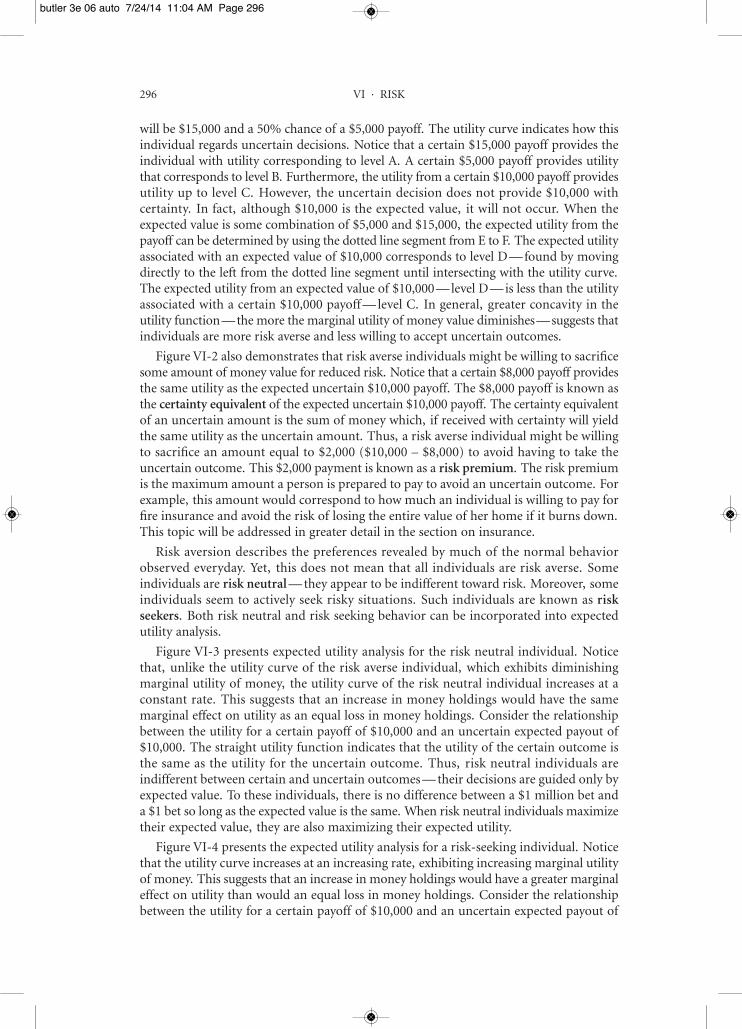

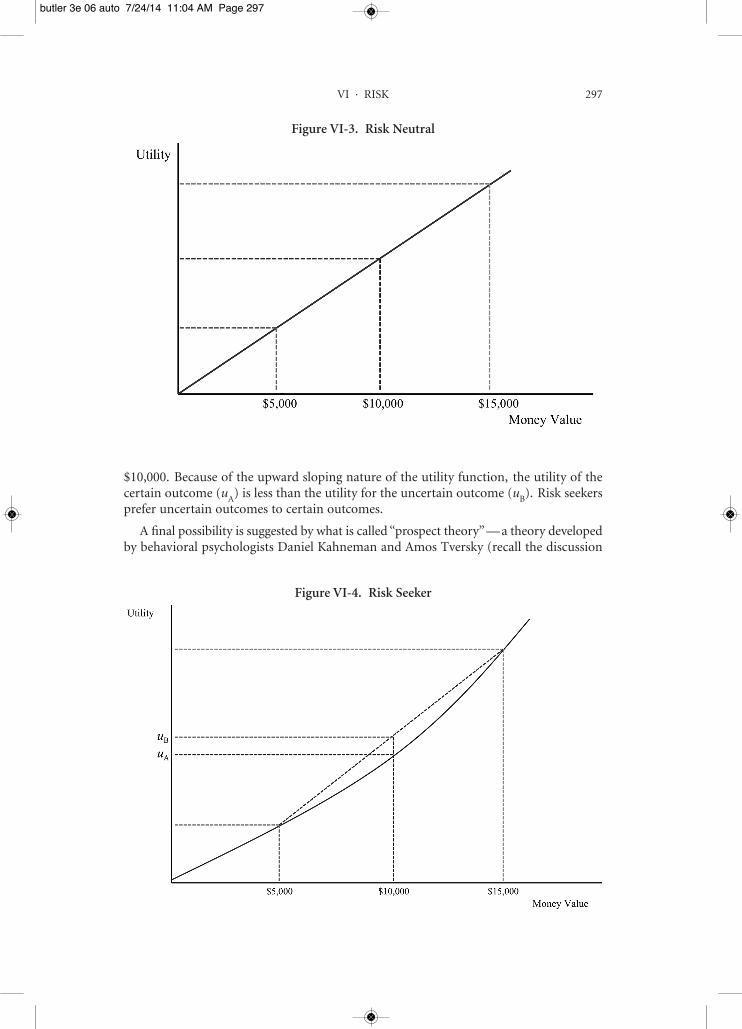

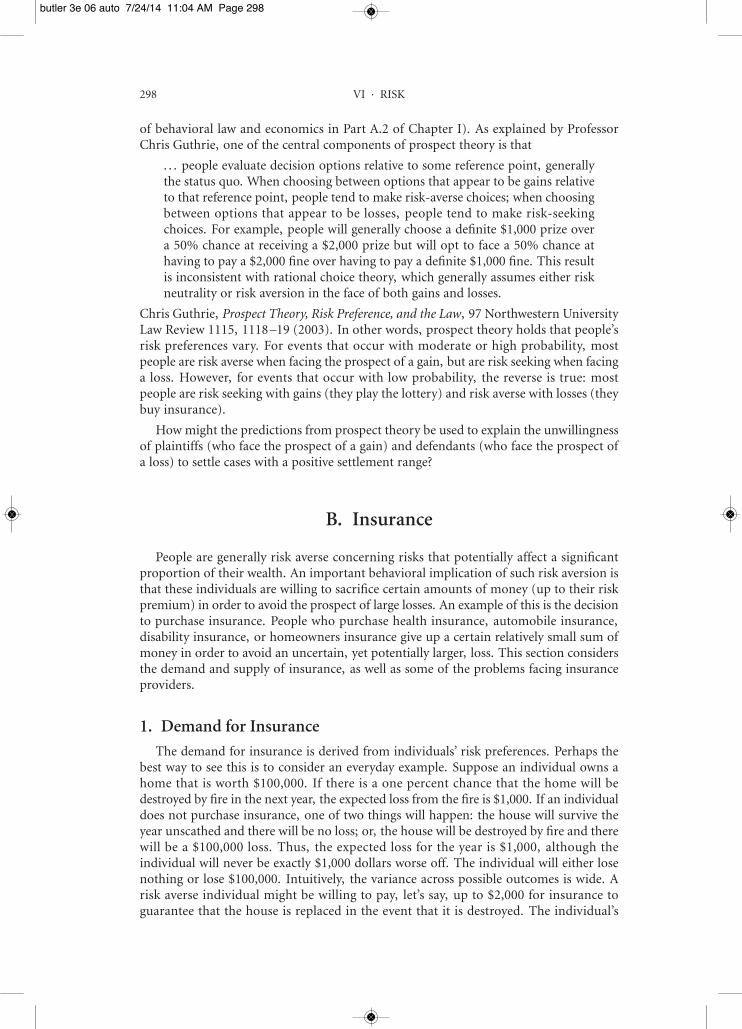

1. Basic Probability Theory 2912. Expected Value and Variance 2923. Expected Utility and Risk Preference 294

B. Insurance 2981. Demand for Insurance 2982. Supply of Insurance 299

a. Adverse Selection 299Hall v. Continental Casualty Co. 300

Notes and Questions 302b. Moral Hazard 304

Atwater Creamery Co. v. Western National Mutual Insurance Co. 304Notes and Questions 308

c. Insurer’s Duty to Settle 308Mowry v. Badger State Mutual Casualty Co. 308

Notes and Questions 3133. Self-Insurance 314

C. Risk and Market Prices 3141. Financial Products 314

Richard A. Posner, The Rights of Creditors of Affiliated Corporations 3152. Products and Services: Risk Allocation and Contract Law 316

a. Assumption of Risk 316Avram Wisna v. New York University 317

Notes and Questions 319b. The Bargaining Principle and Least-Cost Risk Avoider 319c. The Allocation of Risk — Impracticability and Mistake 319

Eastern Air Lines v. Gulf Oil Corp. 320Notes and Questions 321

Wilkin v. 1st Source Bank 322Notes and Questions 324

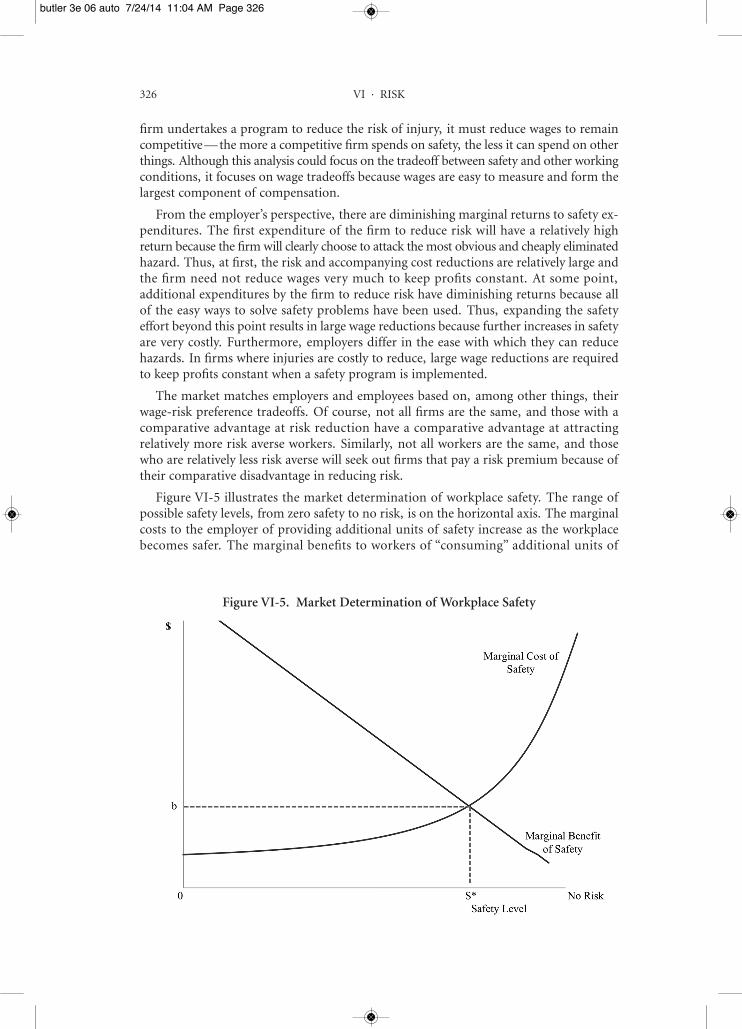

3. Compensating Wage Differentials and Market Levels of Safety 3254. Information, Risk, and Price Adjustments 327

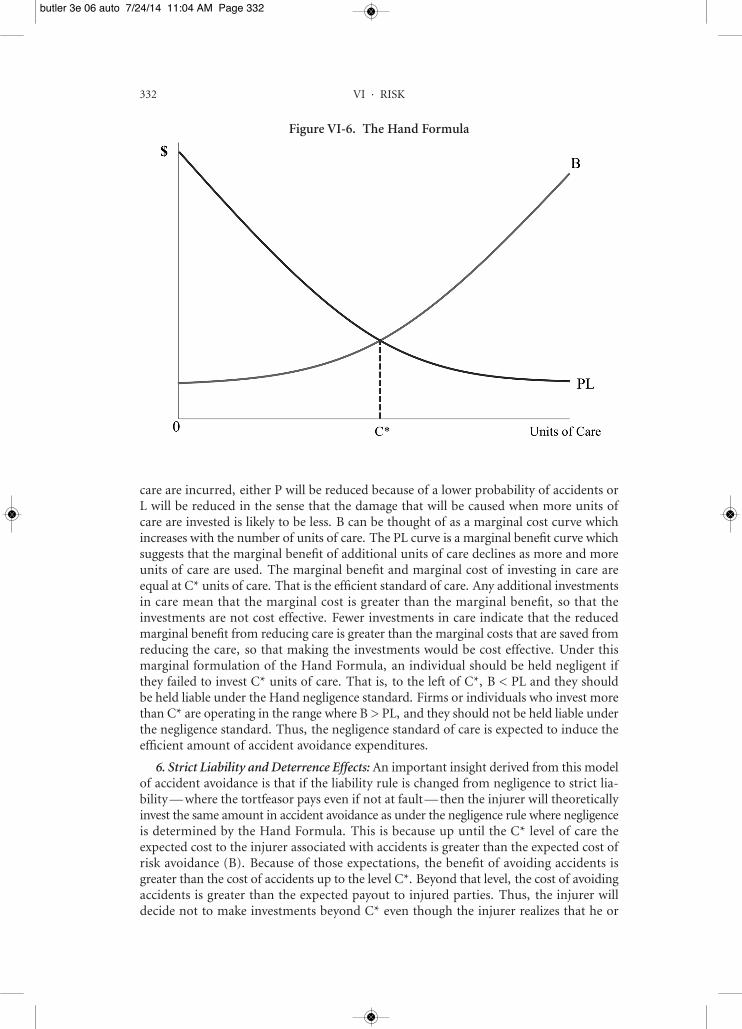

D. Tort Law 3271. Behavior Modification and Minimizing the Costs of Accidents 327

United States v. Carroll Towing Co. 328Notes and Questions 330

CONTENTS xi

butler 3e 00 fmt 7/24/14 11:38 AM Page xi

xii CONTENTS

2. Loss Spreading and Insurance 335Greenman v. Yuba Power Products, Inc. 335

Notes and Questions 337George Priest, The Current Insurance Crisis and Modern Tort Law 339

Notes and Questions 3453. Allocative Efficiency 347

Doe v. Miles Laboratories, Inc. 348Notes and Questions 351

4. Tort Damages and Incentives 351a. Compensatory Damages 351b. Punitive Damages 351Mathias v. Accor Economy Lodging, Inc. 352

Notes and Questions 356c. The Collateral Source Rule 358Helfend v. Southern California Rapid Transit District 359

Notes and Questions 361E. Risk Regulation 362

1. Cost-Benefit Analysis 362UAW v. Occupational Safety & Health Administration 363

Notes and Questions 3672. Measuring Risk: All Risks Are Relative 372

Corrosion Proof Fittings v. Environmental Protection Agency 372Notes and Questions 378

3. Risk versus Risk 380Competitive Enterprise Institute v. NHTSA 381

4. Risk Regulation Priorities 3815. Political Economy of Health and Safety Regulation 382

Chapter VII · The Economics of Crime and Punishment 383A. The Economics of Criminal Behavior 383

1. The Rational Choice Model 383Gary Becker, Crime and Punishment: An Economic Approach 384

2. The Benefits and Costs from Crime 384a. The Stigma of Criminal Activity 386b. The Criminal’s Discount Rate 386c. The Economic Theory of Recidivism 386d. Economics versus Criminology 386e. Are Criminals Really Rational? 387

Ian Urbina and Sean D. Hammill, As Economy Dips, Arrests for Shoplifting Soar 387Notes and Questions 389

B. Empirical Studies of the Economic Model of Crime 3901. Police 3912. Imprisonment 3913. Capital Punishment 3914. Gun Laws 3915. Income 3926. Income Inequality 3927. Unemployment 392

Notes and Questions 393

butler 3e 00 fmt 7/24/14 11:38 AM Page xii

C. The Economics of Law Enforcement 393United States v. United States Gypsum Co. 394

Notes and Questions 3981. Certainty versus Severity 399

United States v. Rajat K. Gupta 400Notes and Questions 401

2. Fines versus Imprisonment 402Tate v. Short 402

Notes and Questions 4043. Extensions of the Basic Model 404

Richard A. Posner, An Economic Theory of the Criminal Law 404a. Risk Preferences 407b. Marginal Deterrence 408c. Repeat Offenders 409

Ewing v. California 409Notes and Questions 412

d. Discount Rates 412United States v. Craig 412

Notes and Questions 414D. Crime in the U.S. 414

Steven D. Levitt, Understanding Why Crime Fell in the 1990s: Four Factors That Explain the Decline and Six That Do Not 414

Notes and Questions 420

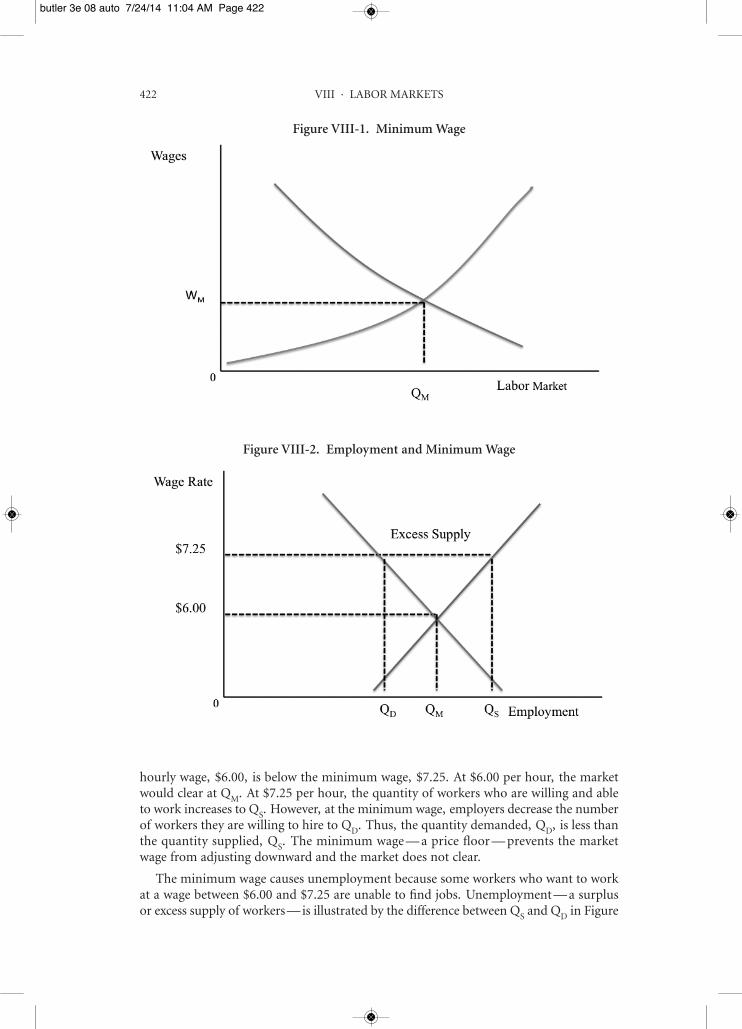

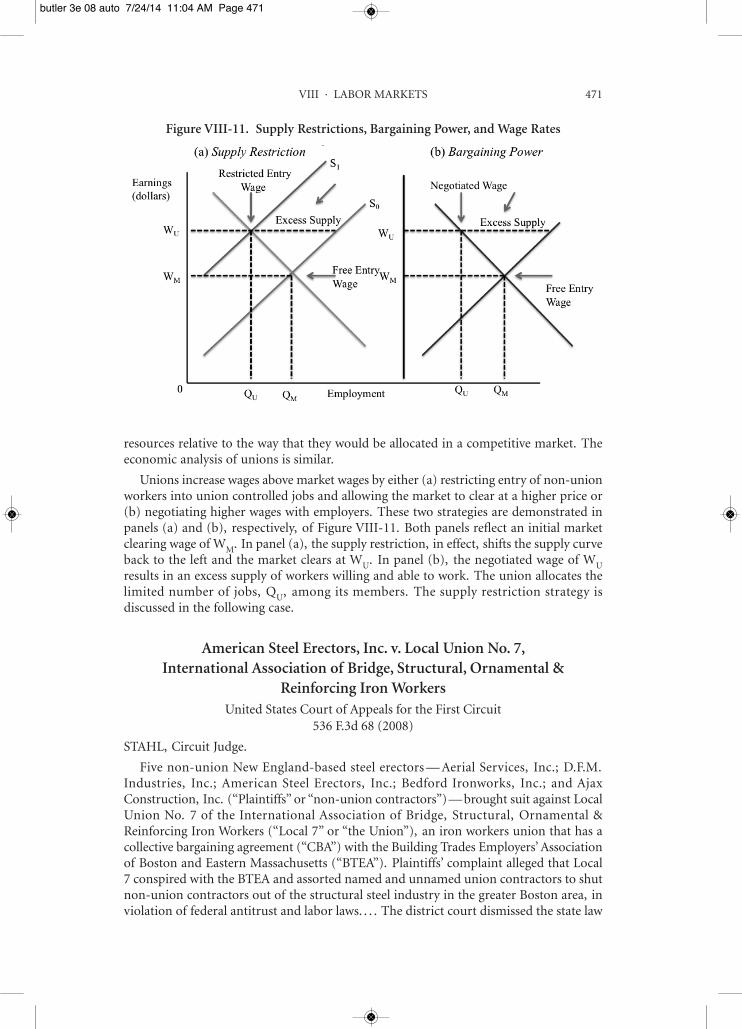

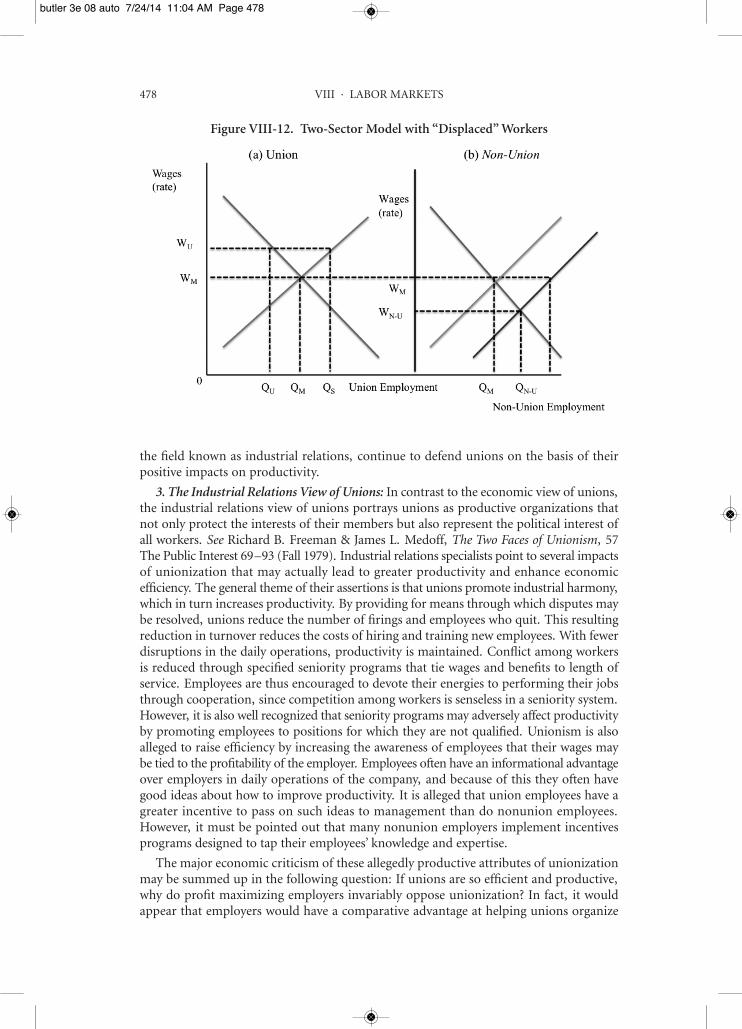

Chapter VIII · Labor Markets 421A. Supply and Demand Analysis: An Overview 421

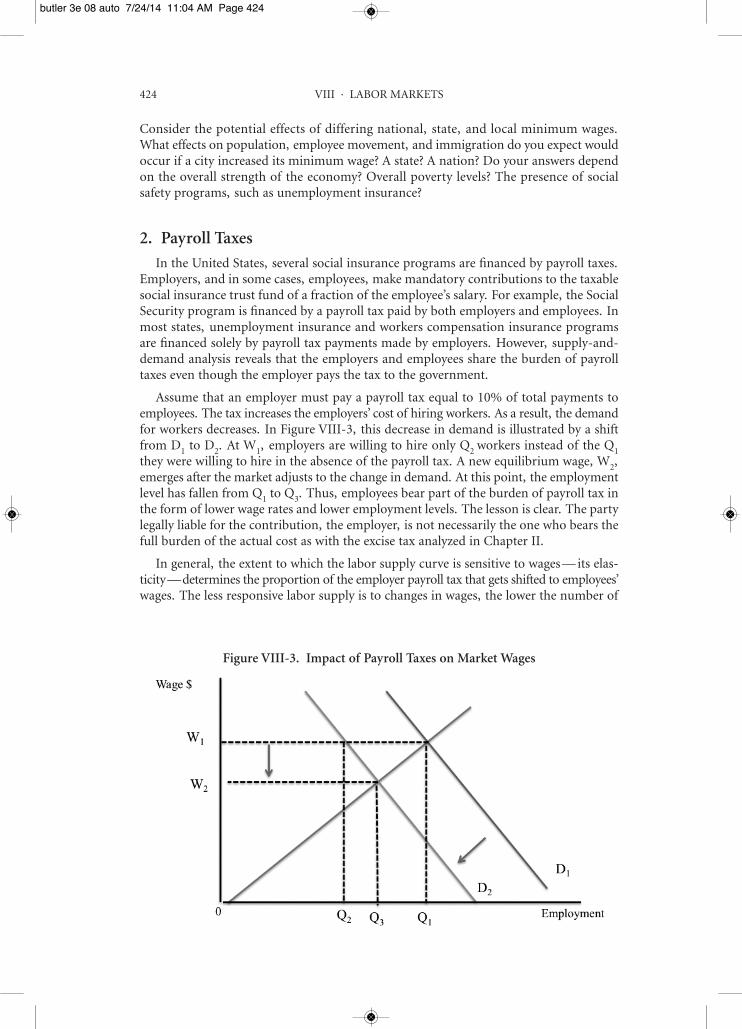

1. The Minimum Wage 4212. Payroll Taxes 4243. Fringe Benefits 425

B. Employers’ Behavior 4251. The Demand for Labor 4262. Employer Investments 431

a. Hiring 431Columbus Medical Services, LLC v. Thomas 432

Notes and Questions 439b. Training 439

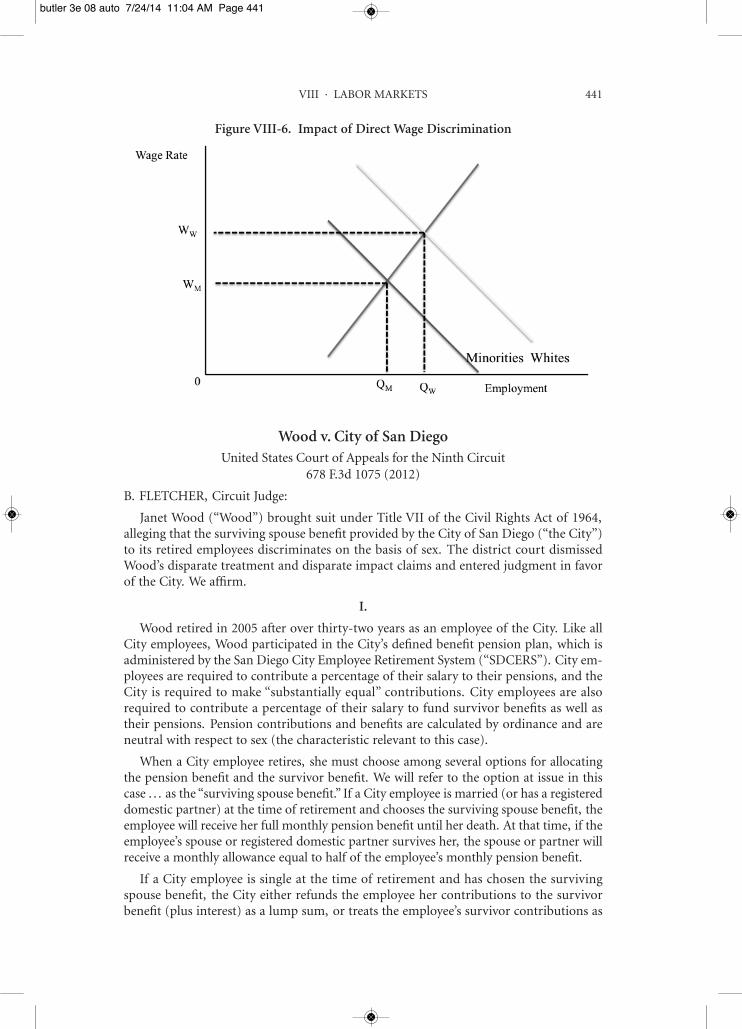

3. Discrimination 440Wood v. City of San Diego 441

Notes and Questions 4464. Employment At Will 450

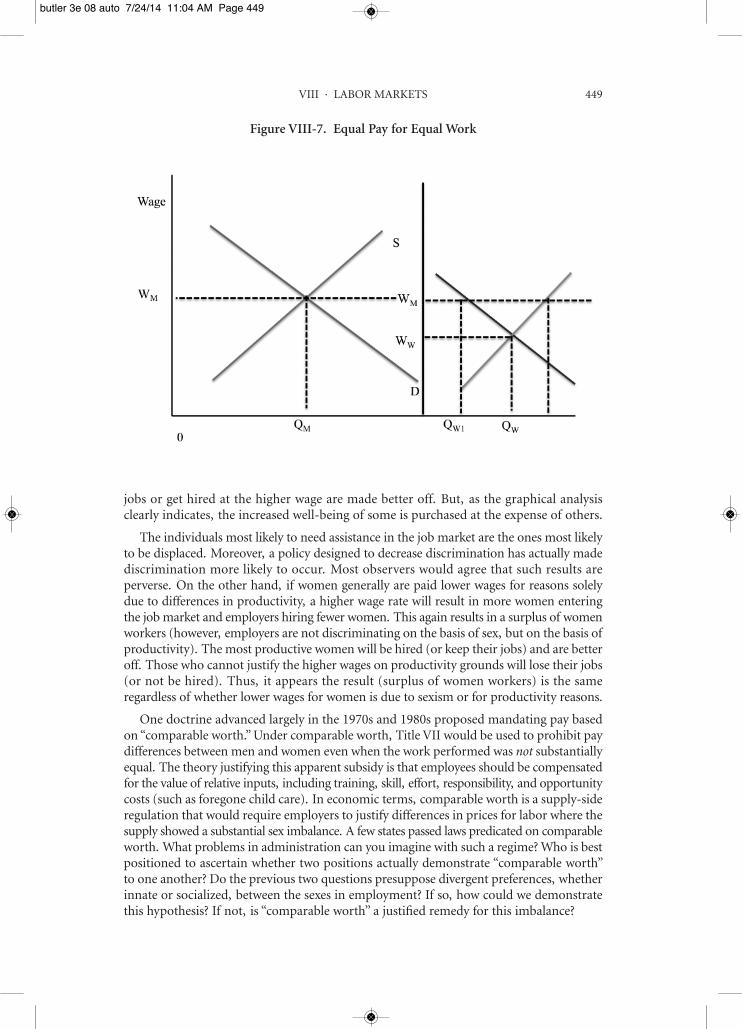

Garcia v. Kankakee County Housing Authority 450Notes and Questions 452

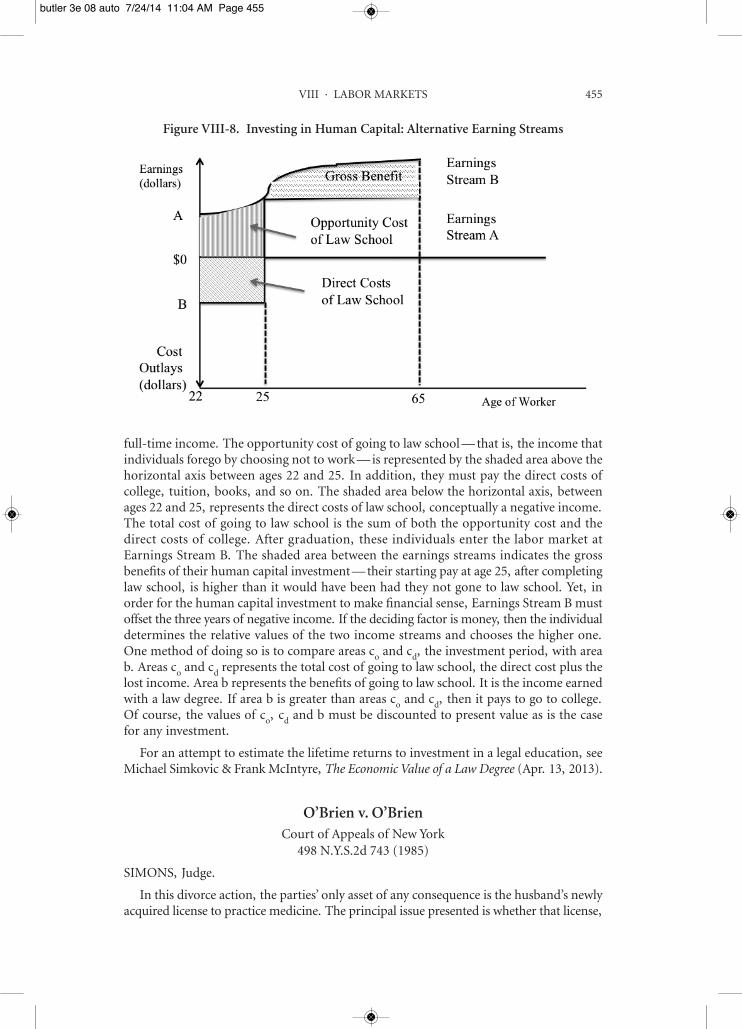

C. Employees’ Behavior: The Supply of Labor 4531. Human Capital Investments 454

O’Brien v. O’Brien 455Notes and Questions 461

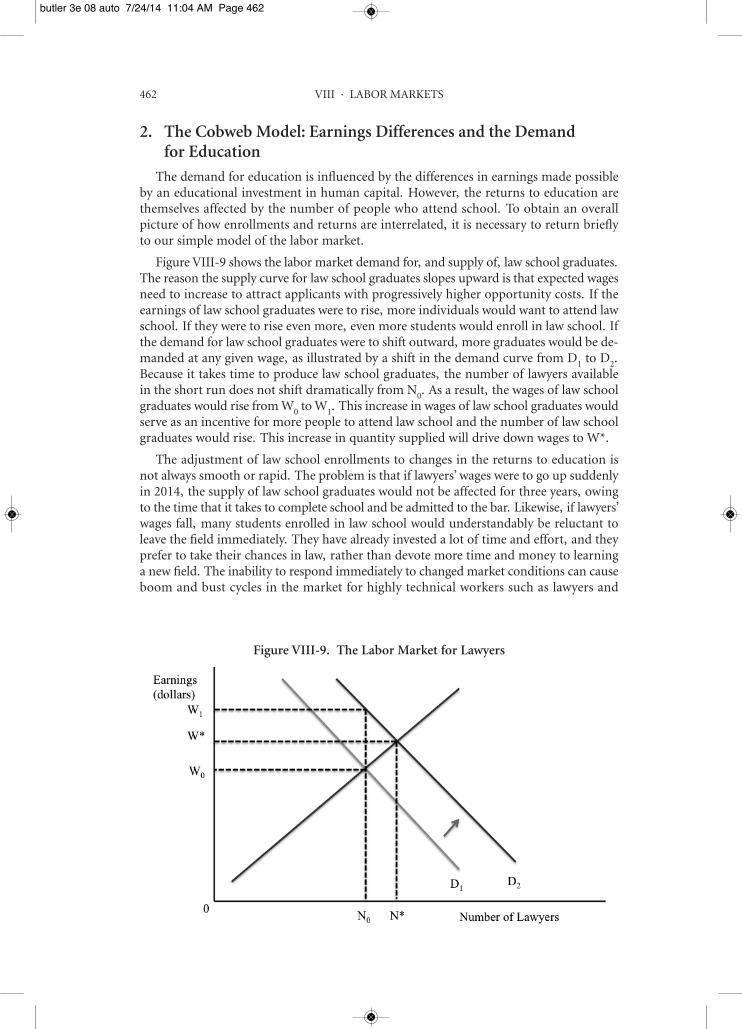

2. The Cobweb Model: Earnings Differences and the Demand for Education 462

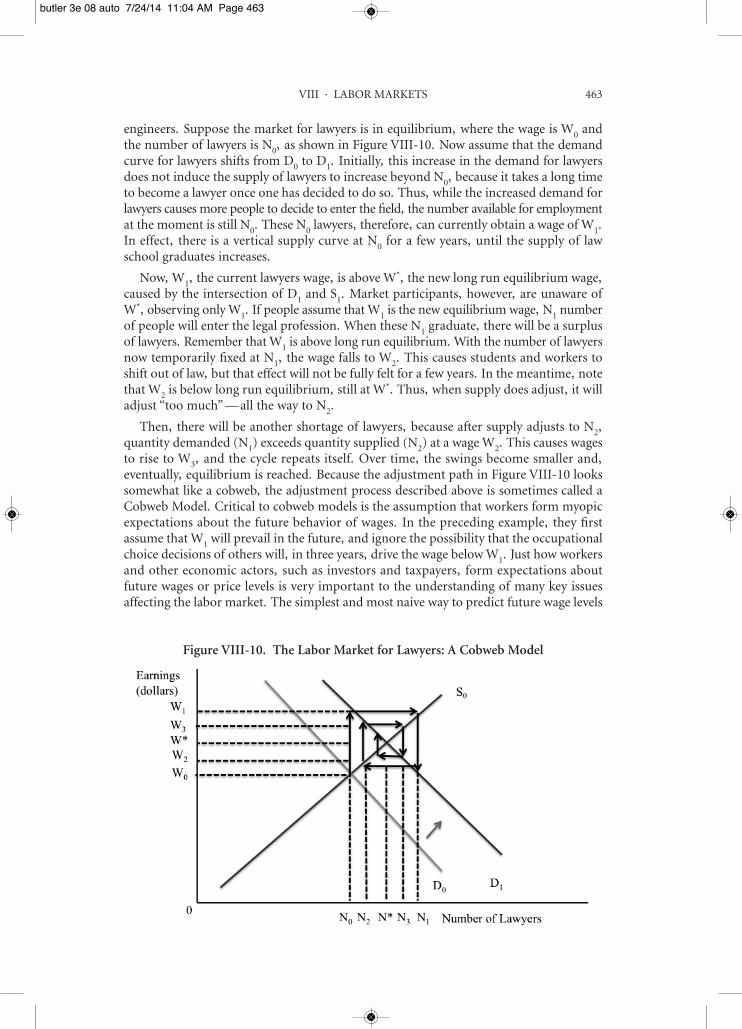

3. Occupational Choice and Compensating Wage Differentials 464

CONTENTS xiii

butler 3e 00 fmt 7/24/14 11:38 AM Page xiii

4. Occupational Licensing 466In Re: Doering 466

Notes and Questions 469D. Labor Unions and Collective Bargaining 470

American Steel Erectors, Inc. v. Local Union No. 7, International Association of Bridge, Structural, Ornamental & Reinforcing Iron Workers 471Notes and Questions 477

Chapter IX · Market Structure and Antitrust 481A. Costs & Production 481

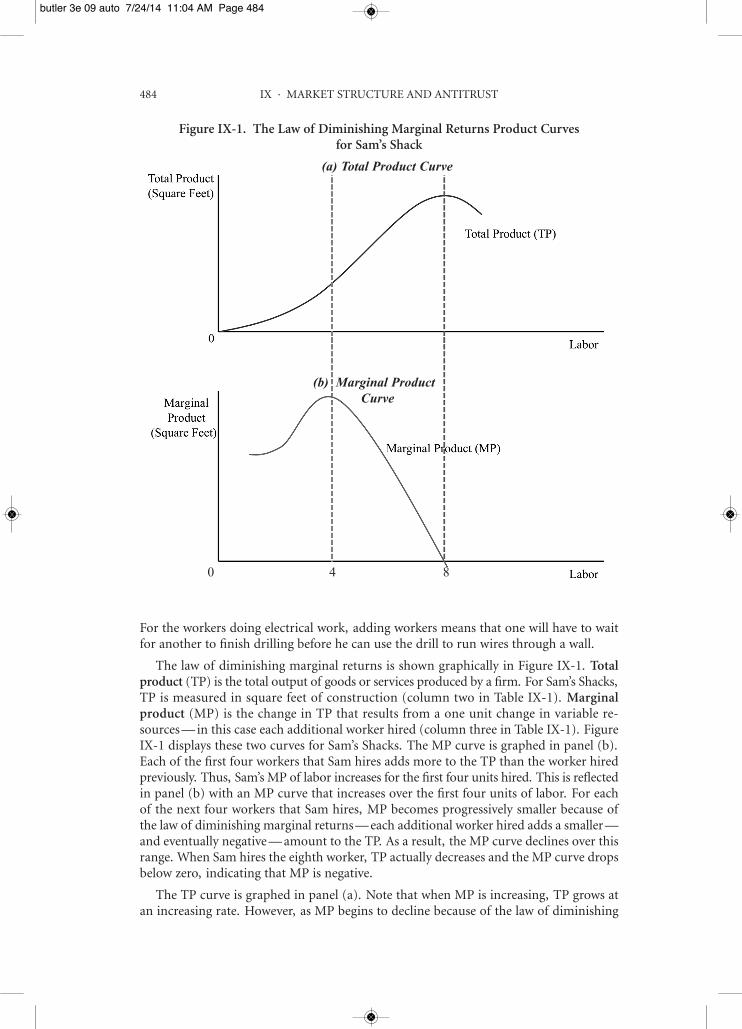

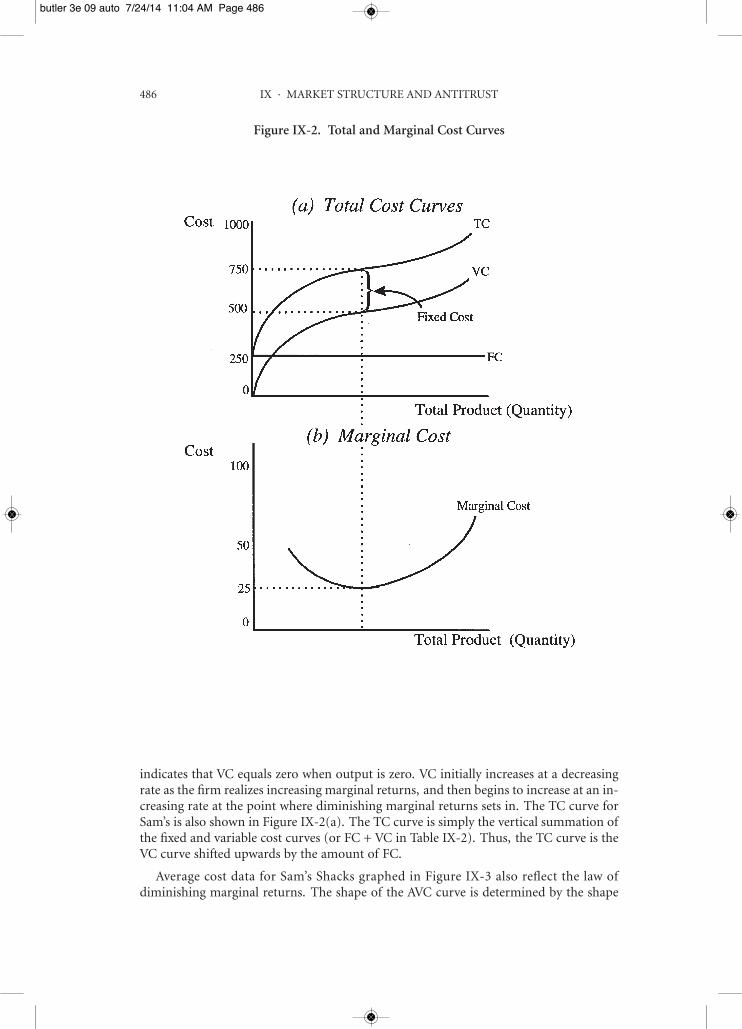

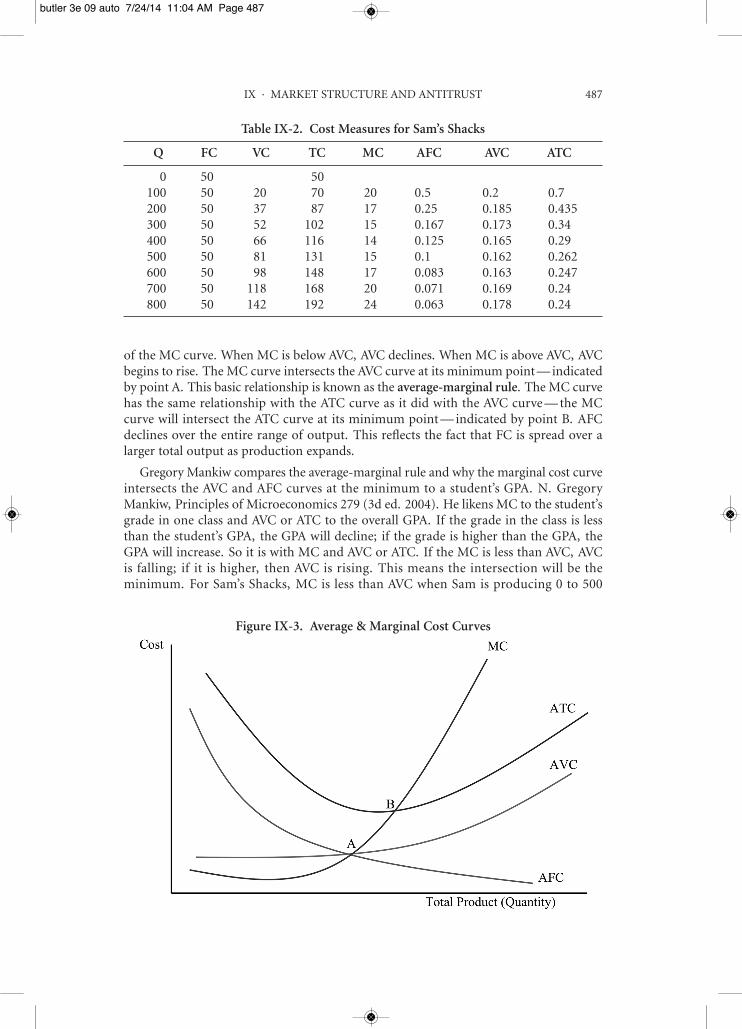

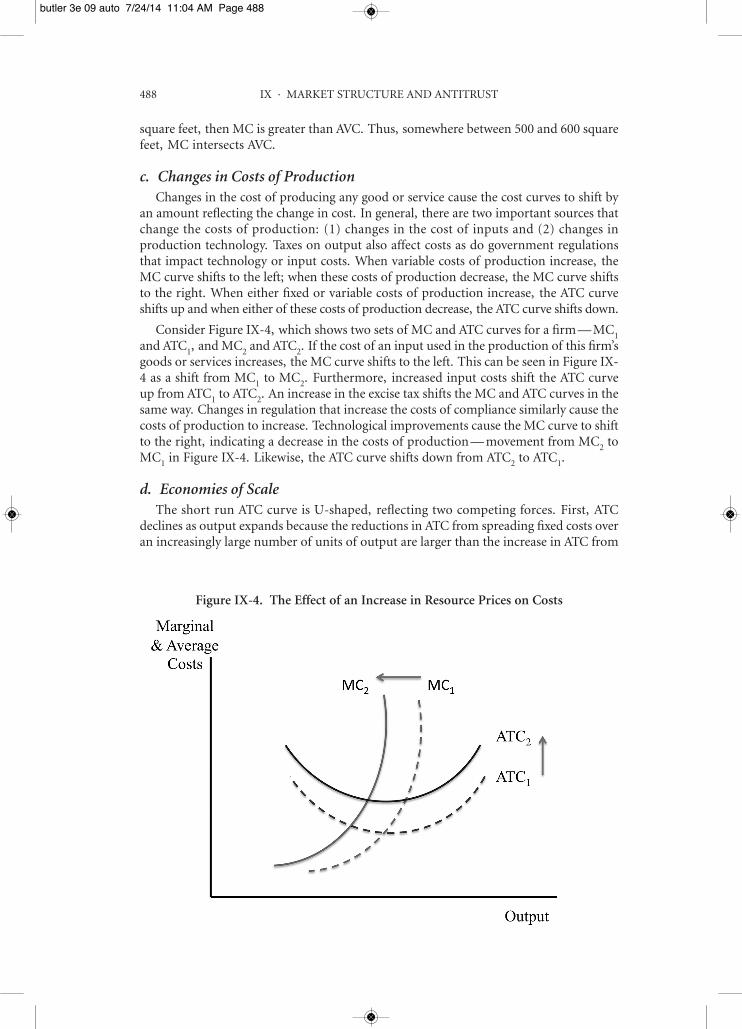

1. Short-Run Production 481a. The Law of Diminishing Marginal Returns 482b. Short-Run Costs 485c. Changes in Costs of Production 488d. Economies of Scale 488

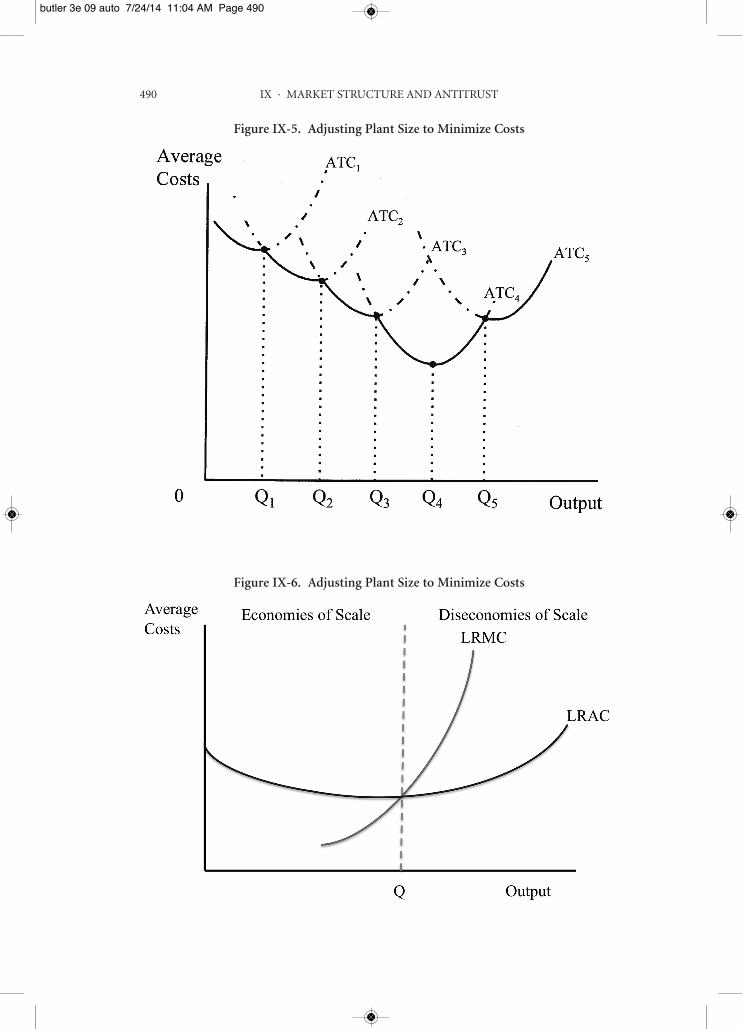

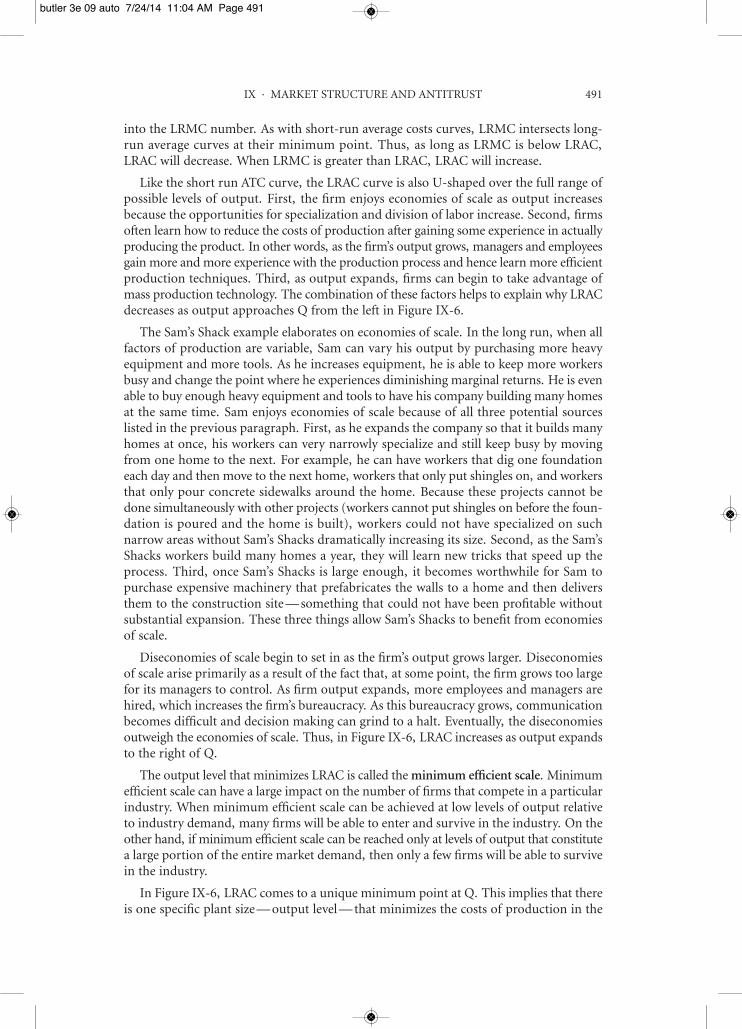

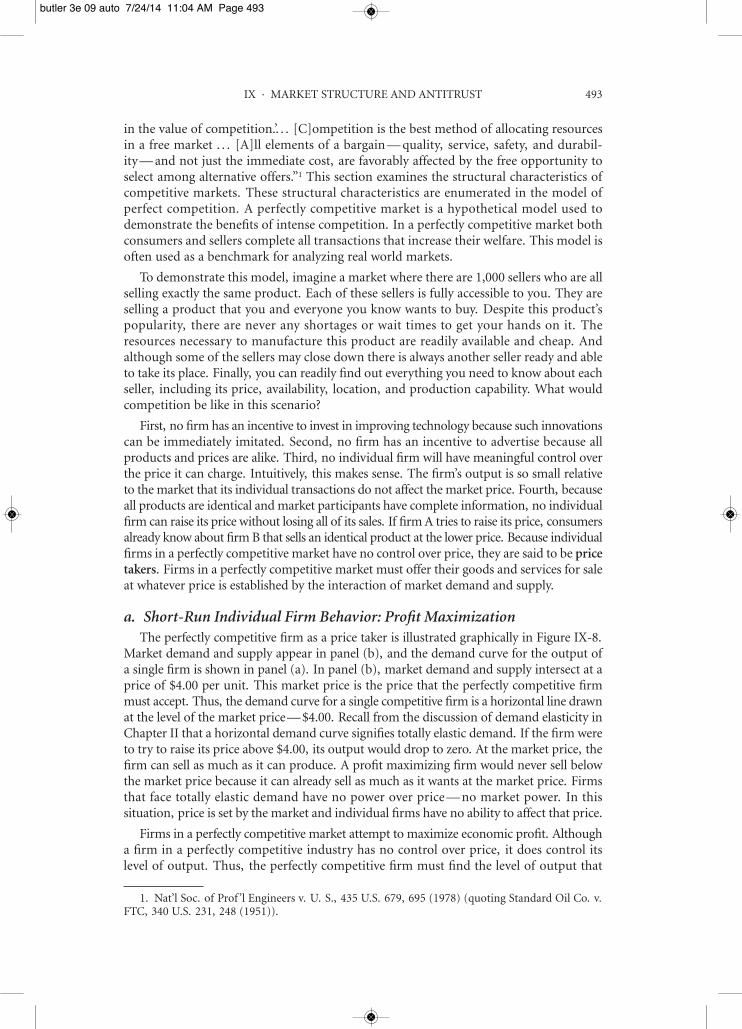

2. Long-Run Production 489B. Market Structures 492

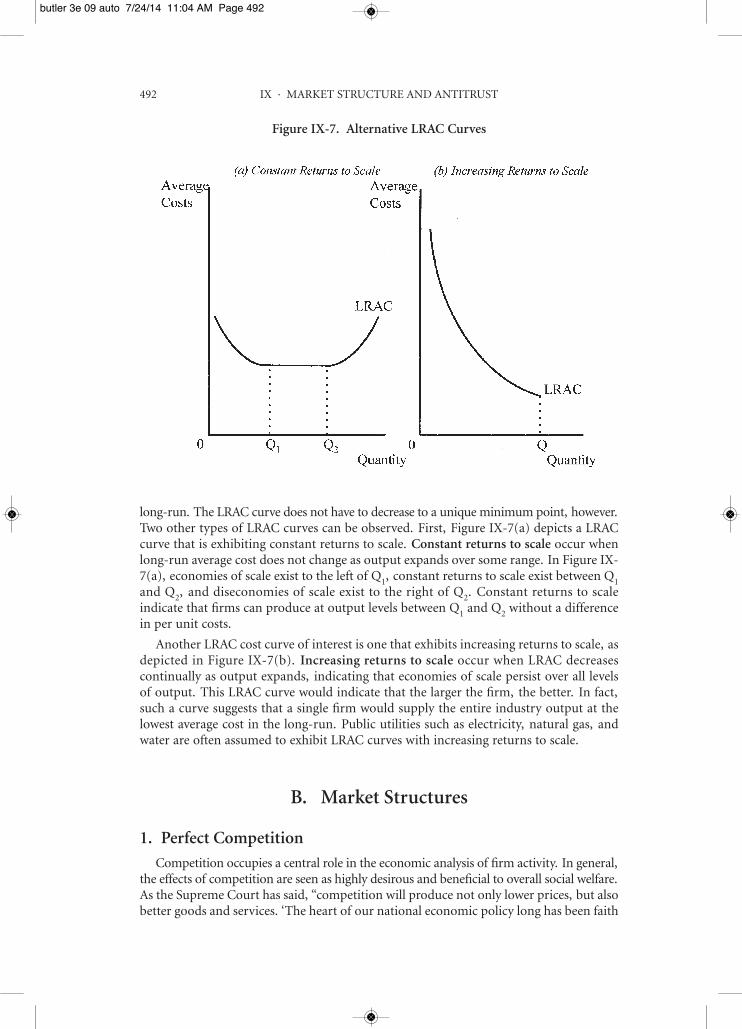

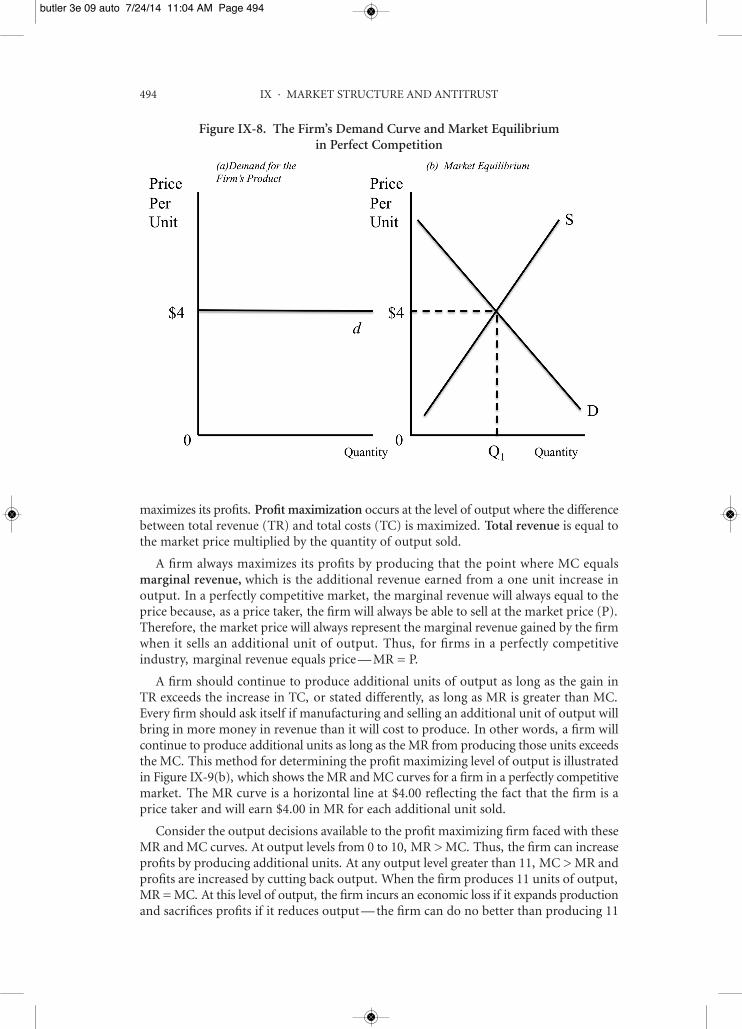

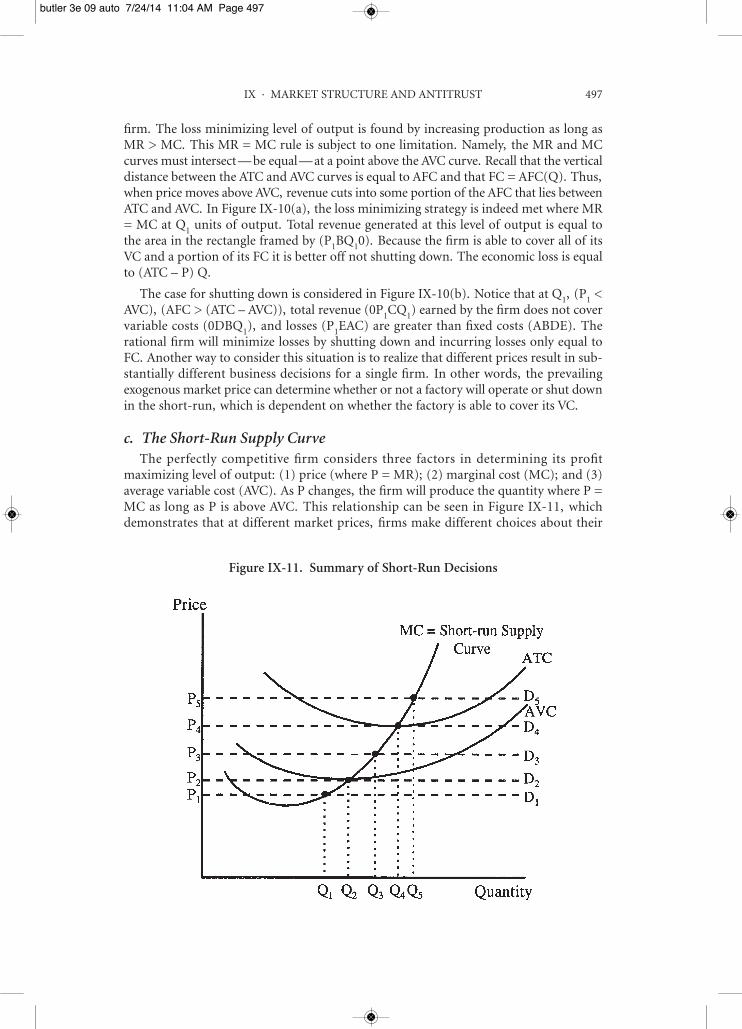

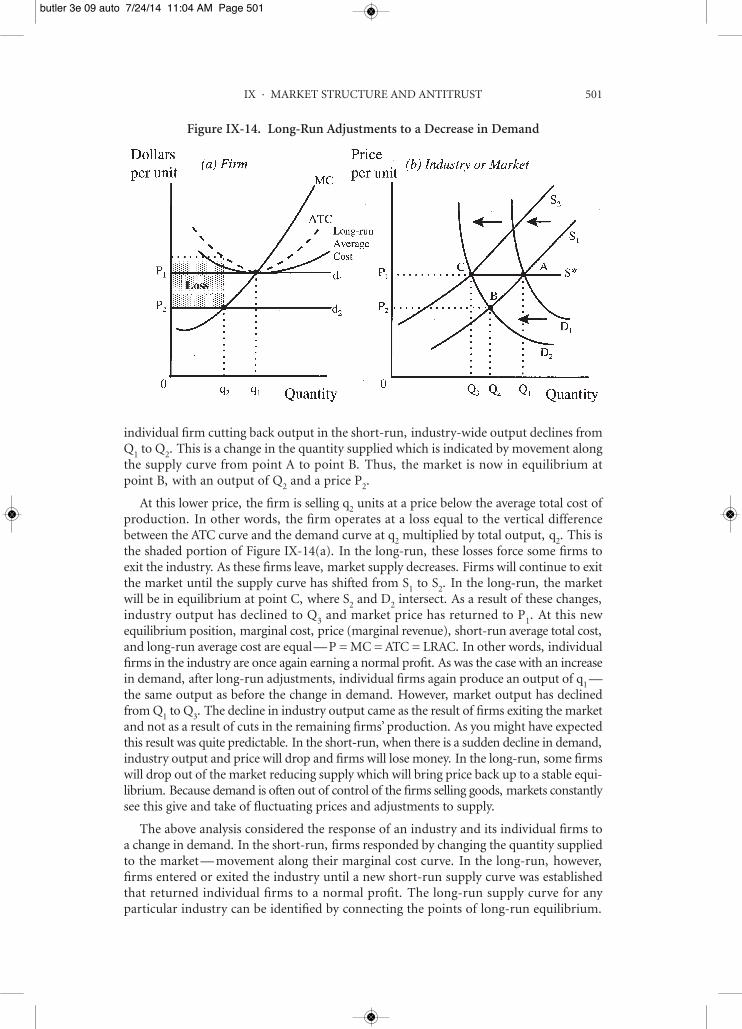

1. Perfect Competition 492a. Short-Run Individual Firm Behavior: Profit Maximization 493b. Loss Minimization: The Shut-Down Decision 496c. The Short-Run Supply Curve 497d. Long-Run Firm Behavior: Industry Supply 498e. The Economic Benefits of Competition 502

2. Monopoly 503a. Profit Maximizing Price and Quantity 503b. Barriers to Entry 508

United States v. Microsoft Corp. 508Notes and Questions 512

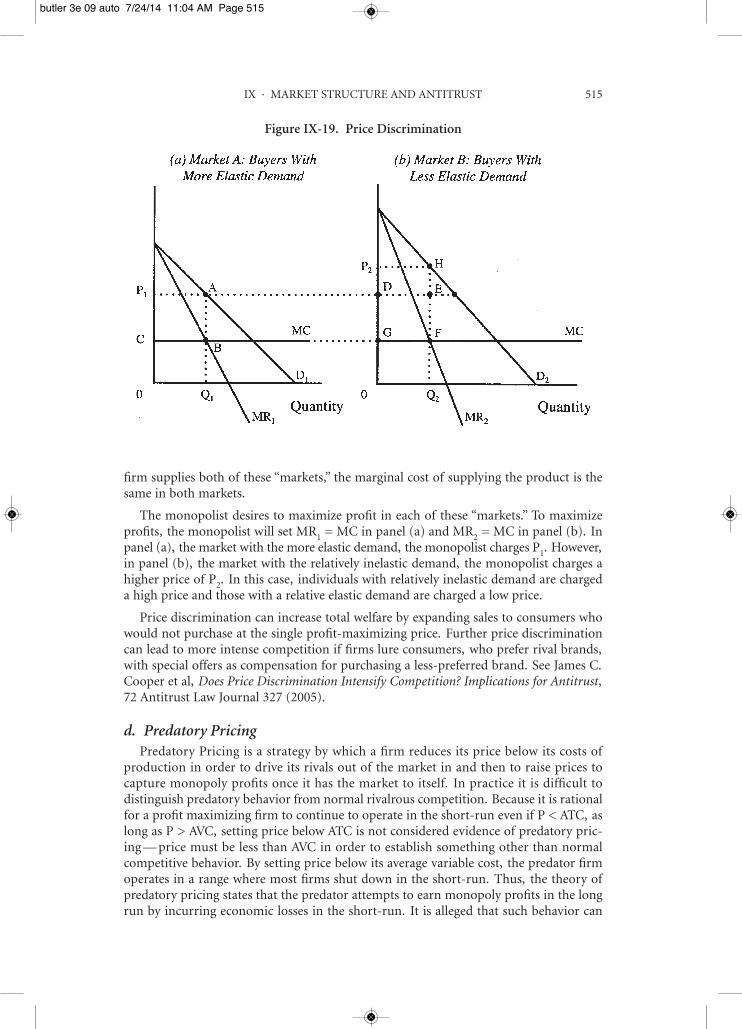

c. Price Discrimination 513d. Predatory Pricing 515

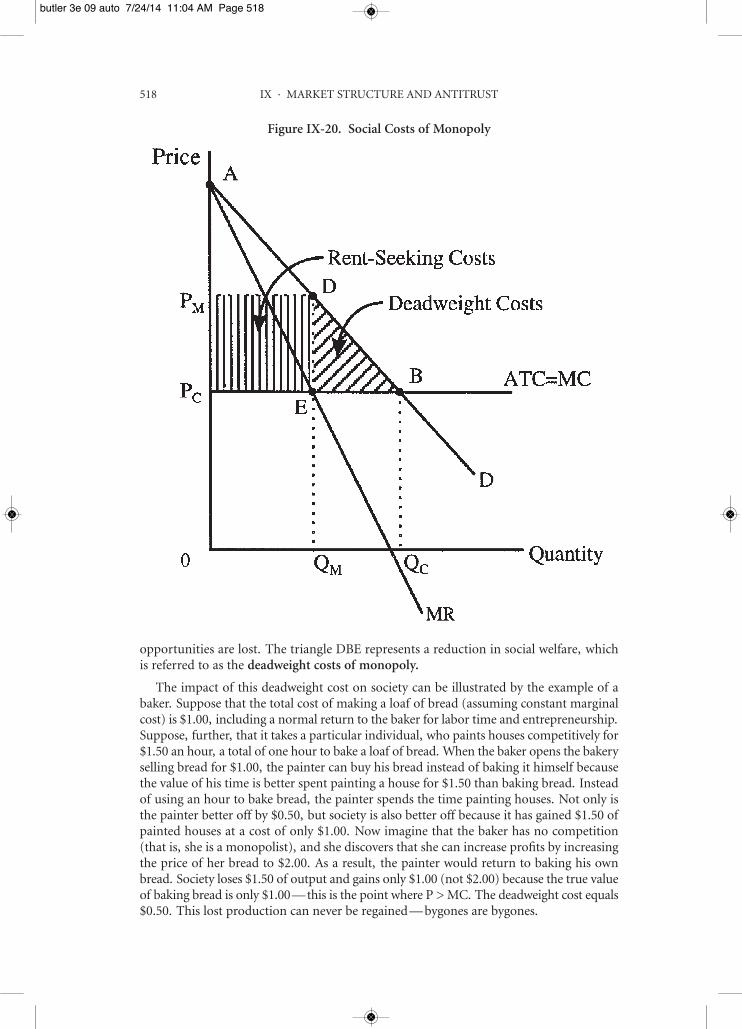

Matsushita Elec. Indus. Co. v. Zenith Radio Corp. 516e. The Social Costs of Monopoly 517

Verizon Communications Inc. v. Law Offices of Curtis V. Trinko, LLP 520Notes and Questions 521

3. More Realistic Models of Competition: Differentiated Products Markets & Oligopoly 523a. Competition with Differentiated Products 524

Leegin Creative Leather Products, Inc. v. PSKS, Inc. 526Notes and Questions 531

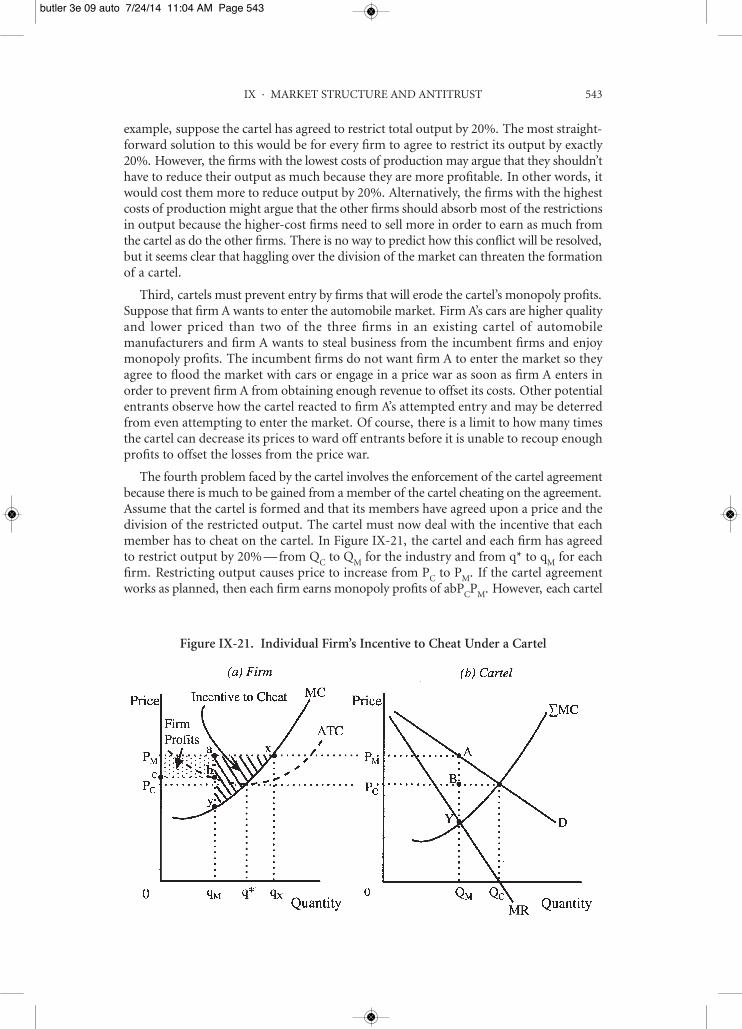

b. Oligopoly 537Bell Atlantic Corporation v. Twombly 538Palmer v. BRG of Georgia 540

Notes and Questions 542John M. Connor, Global Cartels Redux: The Amino Acid Lysine

Antitrust Litigation 545Notes and Questions 547

Broadcast Music, Inc. v. Columbia Broadcasting System, Inc. 554Notes and Questions 562

xiv CONTENTS

butler 3e 00 fmt 7/24/14 11:38 AM Page xiv

Chapter X · Principles of Valuation 565A. Prejudgment Interest 565

Gorenstein Enterprises, Inc. v. Quality Care-USA, Inc. 566Notes and Questions 567

United Telecommunications, Inc. v. American Television and Communications Corp. 568

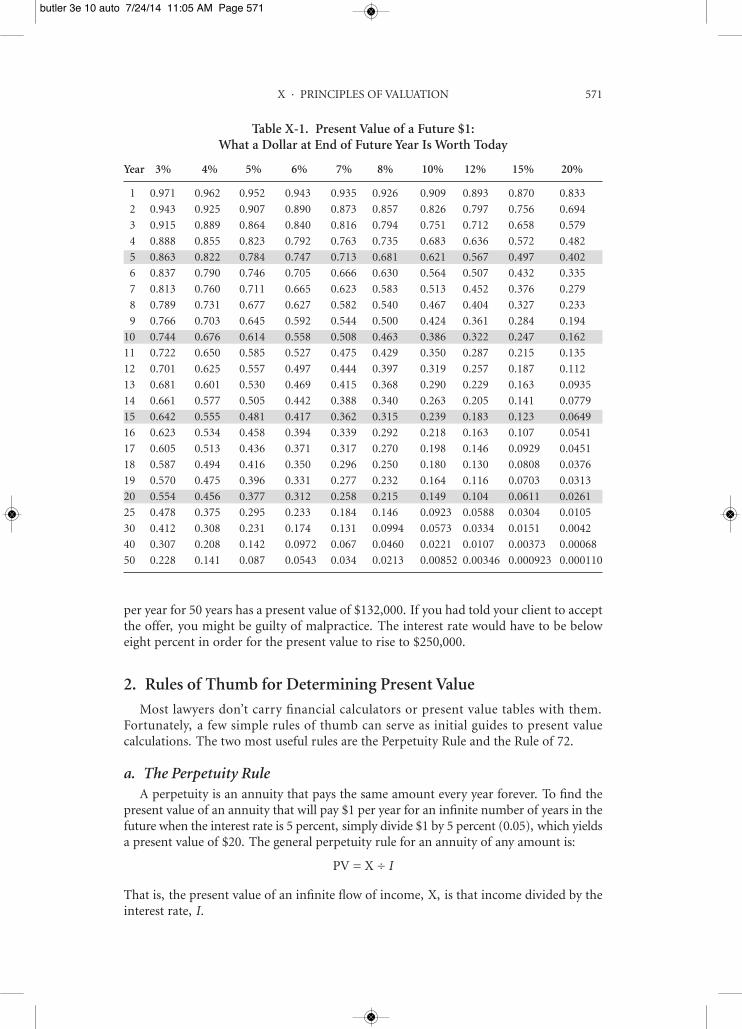

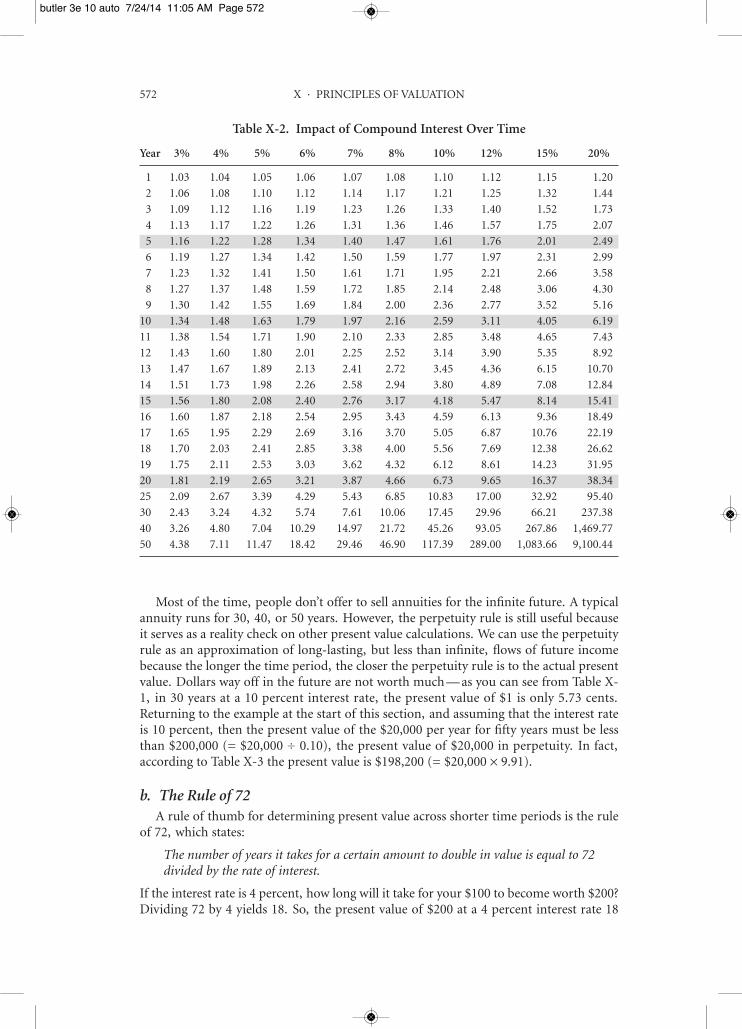

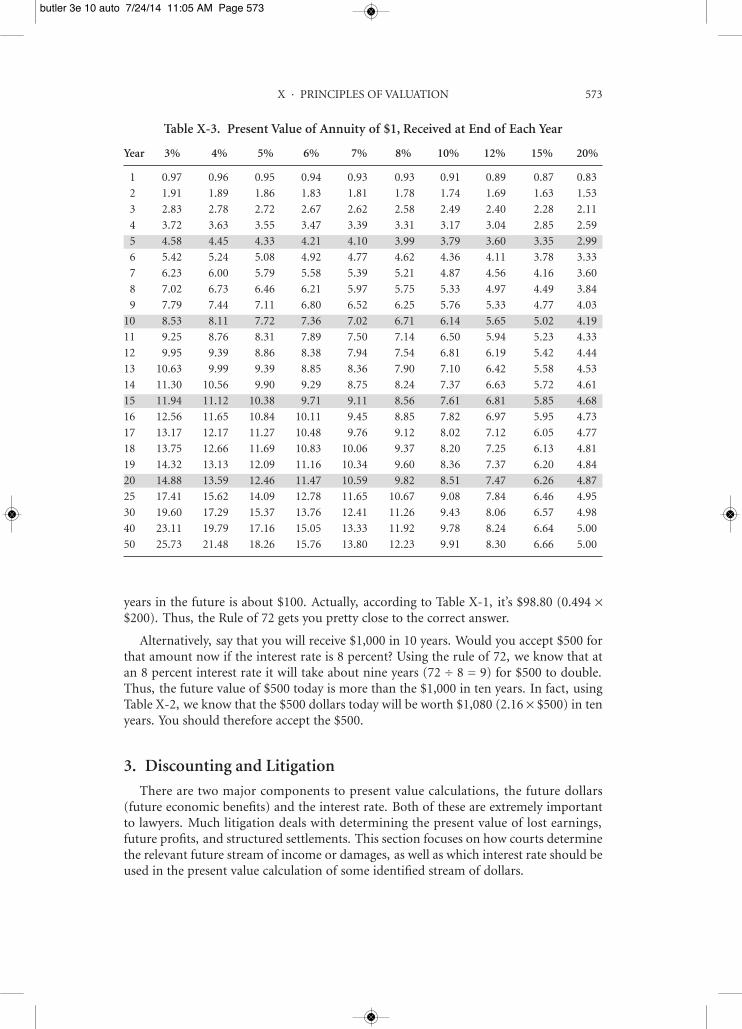

B. Discounted Present Value 5691. The Present Value Formula 5702. Rules of Thumb for Determining Present Value 571

a. The Perpetuity Rule 571b. The Rule of 72 572

3. Discounting and Litigation 573a. Determining the Relevant Future Stream of Economic Benefits 574

Haugan v. Haugan 574Notes and Questions 577

Diocese of Buffalo v. State of New York 578Notes and Questions 581

b. Determining the Proper Interest Rate 582Trevino v. United States 582

Notes and Questions 585c. Pulling It All Together 586

O’Shea v. Riverway Towing Co. 587Notes and Questions 591

C. The Value of Life 5911. Economic Value of Life 592

Cappello v. Duncan Aircraft Sales of Florida 592Notes and Questions 593

Kip Viscusi, The Value of Life 5952. The Hedonic Value of Life 596

Mercado v. Ahmed 597Notes and Questions 600

D. Valuation of Close Corporations 6011. Discounted Future Returns Approach 603

Kleinwort Benson, Ltd. v. Silgan Corp. 604Notes and Questions 608

2. Approaches Using Current or Historical Data 610Central Trust Co. v. United States 612

Notes and Questions 620

Glossary 621Index 641

CONTENTS xv

butler 3e 00 fmt 7/24/14 11:38 AM Page xv

butler 3e 00 fmt 7/24/14 11:38 AM Page xvi

xvii

Table of Cases

Alaska Packers’ Association v.Domenico, 86–89

Alleghany Corp. v. Kirby, 181Amanda Acquisition Corp. v. Universal

Foods Corp., 287American Steel Erectors, Inc. v. LocalUnion No. 7, International Associa-tion of Bridge, Structural, Orna-mental & Reinforcing Iron Workers,471–77

Amino Acid Lysine Antitrust Litigation,545–59

Arizona Governing Committee for TaxDeferred Annuity & Deferred Com-pensation Plans v. Norris, 443, 445

Atwater Creamery Co. v. Western Na-tional Mutual Insurance Co.,304–08

Bell Atlantic Corp. v. Twombly, 538–40Boomer v. Atlantic Cement Co. Inc.,

207–13Broadcast Music, Inc. v. ColumbiaBroadcasting System Inc., 554–62

Cappello v. Duncan Aircraft Sales ofFlorida, 592–93

Carbajal v. H&R Block Tax Services, Inc.,182–83

Central Trust Co v. United States, 612–20City of Columbia v. Omni Outdoor Ad-vertising, Inc., 137–40

City of Los Angeles, Department ofWater & Power v. Manhart, 443–47

Columbus Medical Services, LLC v.Thomas, 432–39

Competitive Enterprise Institute v. Na-tional Highway Safety Admin.,93–96, 381, 591

Connell Constr. Co. v. Plumbers Local100, 475, 477

Consultants & Designers, Inc. v. ButlerServ. Group, Inc., 436–38

Continental T.V., Inc. v. GTE Sylvania,Inc., 244, 532–33

Corenswet, Inc. v. Amana Refrigeration,Inc., 255–58, 264

Corrosion Proof Fittings v. Environmen-tal Protection Agency, 372–78

Craigmiles v. Giles, 141–42Daubert v. Merrell Dow Pharmaceuti-

cals, Inc., 47, 49–51, 601Diocese of Buffalo v. State of New York,

578–81Doe v. Miles Laboratory, Inc., 348–51Eastern Air Lines v. Gulf Oil Corp.,

320–21Eastern Railroad Presidents Conference

v. Noerr Motor Freight, Inc.,139–41, 520

Eldred v. Ashcroft, 33–39Escola v. Coca Cola Bottling Co., 337Ewing v. California, 409–12Fontainebleau Hotel Corp. v. Forty-FiveTwenty-Five, Inc., 30–33, 201–02,205

Garcia v. Kankakee County Housing Au-thority, 450–52

Goldfarb v. Virginia State Bar, 470,551–52

Gorenstein Enterprises, Inc. v. QualityCare-USA, Inc., 566–67

Greenman v. Yuba Power Products, Inc.,335–37, 339, 340

Hagemeyer North America, Inc. v. Gate-way Data Sciences Corp., 168–72

butler 3e 00 fmt 7/24/14 11:38 AM Page xvii

Hall v. Continental Casualty Co.,300–02

Hasty v. Rent-A-Driver, Inc., 435, 438Haugan v. Haugan, 461, 574–77, 578,

586Helfend v. Southern California RapidTransit District, 359–61

Henningsen v. Bloomfield Motors,84–86

Hickman v. Taylor, 167In Re Aluminum Phosphide AntitrustLitigation, 46–51

In Re: Doering, 466–69In re Rhone-Poulenc Rorer, Inc., 175–76In re: Bridgestone/Firestone, Inc.,

173–75Jones v. Star Credit Corp., 84, 104–06Jordan v. Duff and Phelps, Inc., 279–85Joy v. North, 286Kamilewicz v. Bank of Boston, 181Kamin v. American Express Co., 274–76Kleinwort Benson, Ltd. v. Silgan Corp.,

604–10Kohls v. Duthie, 159–63Lake River Corp. v. Carborundum Co.,

247–52Lane v. Facebook, Inc., 176–81Leegin Creative Leather Products, Inc. v.PSKS, Inc., 526–36, 550

Liggett Co. v. Lee, 287Lochner v. New York, 142M. Kraus & Bros., Inc. v. United States,

99–104Mathias v. Accor Economy Lodging, Inc.,

352–56Matsushita Elec. Indus. Co. v. ZenithRadio Corp., 12-15, 516, 521

McPeek v. Ashcroft, 169–71Mercado v. Ahmed, 597–601Miller v. Schoene, 29Morris v. Schoonfield, 403Mowry v. Badger State Mutual CasualtyCo., 308–13

North Carolina Board of Dental Examin-ers v. Federal Trade Commission,470

O’Brien v. O’Brien, 455–61O’Shea v. Riverway Towing Co., 587–91

Orchard View Farms, Inc. v. Martin Ma-rietta Aluminum, Inc., 189–94

Page v. United States, 41–43Palmer v. BRG of Georgia, 540–42Parker v. Brown, 138–41Peevyhouse v. Garland Coal & MiningCo., 69–72

Perkins v. F.I.E. Corp., 347Perma Life Mufflers, Inc. v. International

Parts Corp., 264Power v. Harris, 142Prah v. Maretti, 198–204ProCD, Inc. v. Zeidenberg, 513–14Republican Party of Minnesota v. White,

148–55Reynolds Metals Co. v. Lampert, 190,

194Richman v. Charter Arms Corp., 346Roe v. Wade, 419Rowe Entm’t, Inc. v. William Morris

Agency, Inc., 169–71Schiller & Schmidt, Inc. v. Nordisco

Corp., 51Sedmak v. Charlie’s Chevrolet, Inc.,

63–67Shepard v. Superior Court, 338–39Sherwood v. Walker, 323–24Spur Industries, Inc. v. Del E. Webb De-velopment Co., 213–17

State Oil Co. v. Khan, 528, 533–34Tate v. Short, 402–04Trevino v. United States, 582–86UAW v. Occupational Safety & HealthAdministration, 363–67, 594

United States v. Andreas, 548–49United States v. Apple, Inc., 549–50United States v. Carroll Towing Co.,

328–30, 365United States v. Craig, 412–14United States v. Hutcheson, 473–74United States v. Microsoft Corp.,

508–13, 521United States v. Miller, 68United States v. Rajat K. Gupta, 400–01United States v. Socony-Vacuum Oil,

541, 559United States v. Topco Associates Inc.,

521, 541–42, 556, 563

xviii TABLE OF CASES

butler 3e 00 fmt 7/24/14 11:38 AM Page xviii

TABLE OF CASES xix

United States v. United States GypsumCo., 394–98

United Telecommunications, Inc. v.American Television and Communi-cations Corp., 568–69

Vande Zande v. State of Wisconsin De-partment of Administration, 447–48

Vantage Tech., LLC v. Cross, 435–36Verizon Communications Inc. v. Law Of-fices of Curtis V. Trinko, LLP,520–21

Weinberger v. UOP, Inc., 609

West Lynn Creamery, Inc. v. Healy,142–46, 147

Wilkin v. 1st Source Bank, 322–24Williams v. Walker Thomas FurnitureCo., 80–81, 105, 264

Williams v. Walker Thomas FurnitureCo. II, 81–83, 84

Wood v. City of San Diego, 441–47Wronski v. Sun Oil Co., 22–24Wyoming v. Oklahoma, 146Zubulake v. U.B.S. Warburg, LLC, 169,

170

butler 3e 00 fmt 7/24/14 11:38 AM Page xix

butler 3e 00 fmt 7/24/14 11:38 AM Page xx

Preface to the Third Edition

This is a microeconomics book that relies on numerous examples from the law andpublic policy to illustrate practical economic concepts in action. As explained in the priorprefaces, the first three chapters are foundational and should be taught first. The basicnarrative is to explain how ideal markets operate, the consequences of interfering withmarket price adjustments, a consideration of “market failures” as a justification forgovernment intervention in markets, and then the harsh reality that governmentinterventions are often as imperfect as the markets they aspire to correct.

After the first three chapters, subsequent chapters can be taught in whatever orderworks best. In essence, chapters IV through X are free standing. This third edition includestwo new chapters— Chapter VII on Crime and Punishment and Chapter VIII on LaborMarkets. These chapters were added in response to suggestions by many of the hundredsof judges who have attended the Economics Institute for Judges offered by the Law &Economics Center at George Mason University School of Law.

We acknowledge the valuable suggestions of professors who adopted the second edition.In particular, Bruce Johnsen and James Cooper have provided detailed suggestions andCooper helped revise Chapter IX on Market Structure and Antitrust. Several researchassistants helped update examples and cases. The George Mason team consisted of NateHarris, Matt Wheatley, Mark Weiss, Allen Gibby, Sam Banks, Maurio Fiore, ChristopherMufarriage, Jason Greaves, Mark Ericson, and Taylor Hoverman. The Emory teamconsisted of Robin Caskey, Steve Ferketic, Kasia Hebda, Sarah O’Donohue, Caitlin Pardue,and Luka Stanic.

Henry N. ButlerArlington, Virginia

Christopher R. DrahozalLawrence, Kansas

Joanna ShepherdAtlanta, Georgia

xxi

butler 3e 00 fmt 7/24/14 11:38 AM Page xxi

butler 3e 00 fmt 7/24/14 11:38 AM Page xxii

xxiii

Preface to the Second Edition

This second edition continues to reflect our belief in the value of the building blockapproach to teaching economics to lawyers and law students, and in the usefulness of casesas a supplement to that approach. Our use of the first edition in class, and the feedback fromour students, has reinforced those beliefs. Our goal in preparing this second edition has beento reorganize and streamline the materials in response to comments from professors, lawstudents, and judges, while staying true to the pedagogical approach of the first edition.

The first three chapters remain the core materials and should be covered first. Thosechapters cover much of the same ground as in the first edition, but with a somewhatdifferent organization. Chapter 1 introduces the economics approach, examining suchtopics as the economist’s assumptions about human and firm behavior and the fundamentalconcepts of opportunity cost and property rights. Among the new material in the chapteris a note summarizing some of the recent scholarship on behavioral law and economics.Chapter 2 develops the basic supply-and-demand model in a variety of market and legalsettings. Chapter 3 examines the economics of government regulation (and governmentfailure— i.e., public choice economics), and includes a new section on the economics ofthe court system.

The remaining chapters may be covered in whatever order the instructor prefers. As withthe first edition, the organization is by economic concept rather than by substantive legalarea. Chapter 4 discusses externalities and legal responses to externalities. Chapter 5 combinestwo chapters from the first edition (on the economics of information and on organizationaleconomics) into a single chapter dealing with information costs and transaction costs. Theremaining three chapters have been updated but largely follow the same structure as theircounterparts in the first edition. Chapter 6 discusses risk, Chapter 7 deals with competitionand monopoly, and Chapter 8 addresses valuation issues.

By design, this edition is substantially shorter than the first edition. We have accomplishedthis both by excluding some topics covered in the first edition, and by a careful editingof the cases to focus on the key aspects (both legal and factual) of the case. The result,we hope, is that reading assignments will be of a more manageable size but without anysignificant loss of substance. There remains ample material for a one semester course inlaw and economics.

Thanks to our families for their support and patience with us during this revision. Inaddition, we very much appreciate the research assistance of Eric Hatchett, Matt Koenigsdorf,and Sean McGivern, and financial support from the University of Kansas School of Law.

Henry N. ButlerOrange, California

Christopher R. DrahozalLawrence, Kansas

butler 3e 00 fmt 7/24/14 11:38 AM Page xxiii

butler 3e 00 fmt 7/24/14 11:38 AM Page xxiv

xxv

Preface to the First Edition

This casebook is designed to help law students and lawyers learn the principles of mi-croeconomics. A quick review of the table of contents reveals that economics conceptsprovide the organizational structure of the book. Instead of organizing around substantiveareas of the law, it follows the building block approach used in most successful principlesof economics textbooks. This proven approach to teaching economics differs from otherlaw-and-economics casebooks that tend to focus on applications of economics to legalissues rather than teaching economics. After fifteen years of teaching economics— oftento law students, law school professors, lawyers, and judges— I am convinced of the ped-agogical advantages of this approach. For the many law professors who share this viewand have been forced to supplement principles of economics textbooks with cases, Ibelieve that this casebook offers a more convenient and coherent alternative.

My involvement with this casebook started as an effort to revise the first edition ofQuantitative Methods for Lawyers by Professor Steven M. Crafton and Margaret F. Brinigof George Mason University School of Law. Their ambitious effort to create a casebookintroduction to economics, finance, accounting, statistics, and econometrics has metwith considerable success as judged by adoptions at numerous leading law schools. Nev-ertheless, my interest in these materials quickly turned to concentrating on a moretraditional approach to teaching economics. The result is a very different type of casebookthan Crafton and Brinig’s initial effort. Keith Sipe, the publisher of Carolina AcademicPress, has encouraged me to incorporate some materials from the first edition ofQuantitative Methods for Lawyers and I have done so in numerous areas of this casebook.It is our hope that many of the materials presented here will be incorporated in the secondedition of Quantitative Methods for Lawyers by Crafton and Butler. The materials remaina “work in progress.” I encourage you to send your comments, criticisms, and suggestionsfor improvements of subsequent editions.

This casebook is not intended to be an encyclopedic treatise on either the principlesof economics or the economic analysis of law. Some topics typically covered in a principlestextbook are not found here; similarly, numerous legal issues susceptible to economicanalysis are not covered. Nevertheless, there is plenty of material for a typical one-semestercourse. I encourage you to work through the first five chapters and then choose chaptersaccording to your interests. Figures are available in PowerPoint. Many of the edited casespresented here are longer than one would expect if they were excerpted in a specializedcasebook on their particular area of the law. The pedagogical reason for this is that I wasconcerned that first or second year law students needed to have more information aboutthe particular substantive law (especially in some regulatory cases) in order to understandthe economic issues. I have attempted to ease this pain by minimizing and shorteningmany case citations in the cases presented.

butler 3e 00 fmt 7/24/14 11:38 AM Page xxv

xxvi PREFACE TO THE FIRST EDITION

Numerous individuals have helped me complete this book. I am especially grateful totwo individuals. Geoffrey Lysaught, a J.D./Ph.D. in finance student at the University ofKansas, has been involved in every aspect of the project. He was especially helpful on thefinance and risk issues covered in Chapters IV, IX, and XI. Christopher Drahozal, acolleague in the School of Law, provided detailed comments and suggestions on the entiremanuscript. Geoff and Chris, thank you! I also acknowledge the valuable contributionsof research assistants Gary Eastman, Matt Hoy, and Alok Srivastava. The Smith RichardsonFoundation provided essential financial support at the start of this project.

I have used earlier drafts of these materials in my Law and Economics classes as wellas in the Economics Institutes for State Judges offered by the University of Kansas Law andOrganizational Economics Center (LOEC). Comments from law students, professors inthe Economics Institutes for State Judges (Barry Baysinger, Keith Chauvin, and MauriceJoy of Kansas; Terry L. Anderson of PERC and the Hoover Institution; and W. Kip Viscusiof Harvard Law School), and judges have improved the final product. I would like tooffer my thanks to three judges— Victor T. Barrera of California, Richard T. Jessen ofMinnesota, and Donald S. Owens of Michigan— who took great pride in their ability tospot typos. Accordingly, any remaining typos are their responsibility.

Finally, I wish to express my sincerest gratitude and appreciation to Cathy Lysaughtand Missy Amlong at the LOEC for their loyal and tireless assistance. They “hung in there”during the long and tedious process of compiling these materials.

Henry N. ButlerLawrence, Kansas

butler 3e 00 fmt 7/24/14 11:38 AM Page xxvi

Economic Analysis for Lawyers

butler 3e 01 auto 7/24/14 11:03 AM Page 1

butler 3e 01 auto 7/24/14 11:03 AM Page 2

3

1. Microeconomics is also referred to as price theory. It is important to note that there is muchmore agreement among economists about certain principles of microeconomic theory than there isabout macroeconomic theory and policy. See Dan Fuller & Doris Geide-Stevenson, Consensus AmongEconomists: Revisited, 34 Journal of Economic Education 369 (2003) (reporting results of survey ofeconomists).

Chapter I

The Economics Perspective: Incentives Matter

Economics is an analytical discipline and a practical science. Its aim is to provide a setof tools to understand, analyze, and, sometimes, solve problems. Just as a physicist musttake into account the effects of gravity, so too must a lawyer understand the effects ofeconomic forces. In a very real sense, economic forces are the gravity of the social world—often invisible, but omnipresent. As imposing as this view of economics may sound, thiscasebook presupposes no prior exposure to economics— it concentrates on the few foun-dational concepts and analytical tools necessary for the lawyer to take advantage of theeconomics perspective.

Economics is the study of the rational behavior of individuals when choices are limitedor constrained in relation to human desires. This broad definition should serve to dispeltwo common myths about economics. First, economics is not simply about money— itis about how incentives influence behavior. In fact, the crucial point of economics is thatincentives matter. Second, economics is concerned with more than just economy-wide,macroeconomic phenomena such as inflation, unemployment, trade deficits, and businesscycles. It also includes microeconomics, which uses individual decision-makers andindividual markets as the basic units of analysis. In this casebook, the principles of mi-croeconomics are introduced by analyzing the impact of changes in various legal ruleson the behavior of economic actors.1 Changes in laws and regulations affect incentives,and incentives matter!

Where the Buses Run on TimeAustan Goolsbee

Slate.com (March 16, 2006)

On a summer afternoon, the drive home from the University of Chicago to the northside of the city must be one of the most beautiful commutes in the world. On the lefton Lake Shore Drive you pass Grant Park, some of the world’s first skyscrapers, and theSears Tower. On the right is the intense blue of Lake Michigan. But for all the beauty,

butler 3e 01 auto 7/24/14 11:03 AM Page 3

4 I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER

the traffic can be hell. So, if you drive the route every day, you learn the shortcuts. Youknow that if it backs up from the Buckingham Fountain all the way to McCormick Place,you’re better off taking the surface streets and getting back onto Lake Shore Drive a fewmiles north.

A lot of buses, however, wait in the traffic jams. I have always wondered about that:Why don’t the bus drivers use the shortcuts? Surely they know about them— they drivethe same route every day, and they probably avoid the traffic when they drive their owncars. Buses don’t stop on Lake Shore Drive, so they wouldn’t strand anyone by detouringaround the congestion. And when buses get delayed in heavy traffic, it wreaks havoc onthe scheduled service. Instead of arriving once every 10 minutes, three buses come in atthe same time after half an hour. That sort of bunching is the least efficient way to run apublic transportation system. So, why not take the surface streets if that would keep theschedule properly spaced and on time?

You might think at first that the problem is that the drivers aren’t paid enough to strategize.But Chicago bus drivers are the seventh-highest paid in the nation; full-timers earned morethan $23 an hour, according to a November 2004 survey. The problem may have to do notwith how much they are paid, but how they are paid. At least, that’s the implication of anew study of Chilean bus drivers by Ryan Johnson and David Reiley of the University ofArizona and Juan Carlos Muñoz of Pontificia Universidad Católica de Chile.

Companies in Chile pay bus drivers one of two ways: either by the hour or by thepassenger. Paying by the passenger leads to significantly shorter delays. Give them incentives,and drivers start acting like regular people do. They take shortcuts when the traffic is bad.They take shorter meal breaks and bathroom breaks. They want to get on the road andpick up more passengers as quickly as they can. In short, their productivity increases.

They also create new markets. At the bus stops in Chile, people known as sapos (frogs)literally hop on and off the buses that arrive, gathering information on how many peopleare traveling and telling the driver how many people were on the previous bus and howmany minutes ago it sat at the station. Drivers pay the sapos for the information becauseit helps them improve their performance.

Not everything about incentive pay is perfect, of course. When bus drivers start movingfrom place to place more quickly, they get in more accidents (just like the rest of us).Some passengers also complain that the rides make them nauseated because the driversstomp on the gas as soon as the last passenger gets on the bus. Yet when given the choice,people overwhelmingly choose the bus companies that get them where they’re going ontime. More than 95 percent of the routes in Santiago use incentive pay.

Perhaps we should have known that incentive pay could increase bus driver productivity.After all, the taxis in Chicago take the shortcuts on Lake Shore Drive to avoid the trafficthat buses just sit in. Since taxi drivers earn money for every trip they make, they wantto get you home as quickly as possible so they can pick up somebody else.

* * *

—————

This chapter introduces the economics perspective by describing several fundamentalconcepts and assumptions. In Section A, economists’ assumptions about human behaviorand firm behavior as well as the key concepts of scarcity, opportunity costs, and marginalanalysis are developed. In Section B, the importance of private property rights to afunctioning market economy is explored. Section C contrasts the ex ante (forward-looking) perspective of economics with the ex post (backward-looking) perspective

butler 3e 01 auto 7/24/14 11:03 AM Page 4

I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER 5

typical of legal analysis. Section D presents game theory as an explanation for mucheconomic behavior. Finally, Section E compares positive economic analysis, whichdescribes the world as it is, with normative economic analysis, which describes theworld as it should be.

A. Economic Behavior

The concept of scarcity is fundamental to the study of economics. Scarcitymeans thatour behavior is constrained because we live in a world of limited resources and unlimiteddesires. Scarcity is thus a relative concept in that it indicates we cannot satisfy every desire.The fact that there is an “abundance” of a particular resource does not mean that there isnot scarcity; it simply means that at current prices everyone who wants to control a certainamount of that resource can do so by paying the market price. Scarcity implies thatindividuals, families, governments, businesses, and other economic actors must makechoices or trade-offs among competing uses of limited resources.

Economic actors are assumed to maximize their well-being subject to constraints. Inthis section, assumptions about what guides decision making by individuals and firmsare developed.

1. Opportunity Costs, Economic Choices, and the Margin

There are only twenty-four hours in a day, and any decision to engage in one activityentails a decision to forego some other activity. People must choose how to spend theirtime, and choice requires a sacrifice. This sacrifice illustrates the fundamental economicconcept of opportunity cost. In general, the opportunity cost of using a resource in aparticular manner is defined as the value of the next best alternative use of that resource.For example, your time— a valuable resource— can be used in several different ways:sleeping, studying, partying, vacationing, exercising, working, eating, watching television,and so forth. The opportunity cost to you of reading this material is the next best alternativeuse of your time. Similarly, the opportunity cost of working as a lawyer is the next bestalternative career you may have chosen.

The classic phrase that illustrates the concept of opportunity cost is “There ain’t nosuch thing as a free lunch,” or “TANSTAAFL.” Someone else may pay for your lunch,but you gave up some other activity in order to go to lunch. Another way to think ofthe concept of opportunity cost is to recognize that “whenever you have a choice, thereis a cost.”

Choices or trade-offs, however, are rarely between extremes. For example, individualsare rarely faced with the choice between a twelve-course feast or going hungry; moreoften, individuals confront choices of a smaller magnitude— say, between steak and ham-burger. Economists assert that economic actors make choices “at the margin,” where themargin refers to the impact of a small change in one variable on another variable. Forexample, if the price (cost) of a product increases relative to the prices of other products,then people “at the margin” will substitute the now lower cost product for the higher costproduct. Raise the price of Toyotas and some people will buy fewer Toyotas and more(say) Nissans. Raise the price of heating oil, and even people who “need” it will substituteother products (e.g., sweaters and blankets) to keep warm. In general, the margin refers

butler 3e 01 auto 7/24/14 11:03 AM Page 5

6 I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER

* We use the word “man” here in its use as a non-gender-specific reference to human beings. Wehave attempted to make the language less gender-specific because the models being discussed describe

to the difference in cost, benefit, or some other measure (e.g., profit, revenue, etc.) betweenthe existing situation and a proposed change.

Suppose, for example, that you attempt to purchase a bag of pretzels by inserting fiftycents into a vending machine and pushing the appropriate buttons. Your actions demonstratethat your expected marginal benefit from the bag of pretzels is greater than fifty cents.Unfortunately, you failed to notice (prior to selecting the pretzels) that the next slot for apretzel bag was empty, and you did not receive anything for your fifty cents. You are veryconfident that a bag of pretzels will be dispensed if you pay another fifty cents. Your friendsays you are crazy to pay $1.00 for a bag of pretzels, but you reply that on the margin thenext bag costs fifty cents and that the marginal benefit to you of a bag of pretzels is stillmore than fifty cents. You buy the pretzels, but your friend gives you a hard time forpaying so much. You then explain to him that the first fifty cents was in the past, and therewas nothing that could be done about it. The first fifty cents was a sunk cost, and sunkcosts do not affect your future decisions because you make decisions on the margin.

The basic marginal analysis decision-making rule is that if the marginal benefit of anactivity is greater than the marginal cost of that activity, then do it! It is important toappreciate the individual basis of decision making because many costs and benefits aresubjective in the sense that they differ from individual to individual. Thus, an observeris often left to infer relative costs and benefits from observed behavior. All economicanalysis is concerned with consequences “at the margin.” Thus, one would expect that achange in a legal rule that affects a cost or benefit— that is, affects incentives— will havemeasurable (at least in principle) effects at the margin.

2. Assumptions About Human Behavior

Economists employ certain abstractions and assumptions to help predict the behavioralconsequences of changes in the constraints faced by individuals, businesses, and othereconomic actors. One of the most important assumptions is that individuals behave ra-tionally— that is, they seek to maximize their “self-interest.” The self-interest assumptiondoes not mean that individuals are cold, harsh calculators; rather it means that theirbehavior is consistent with a model of rational choice. Self-interest also does not implythat individuals are necessarily selfish; rational decision makers may benefit— that is,receive satisfaction— from making others happy. The significance of the self-interest as-sumption is that it allows economists to anticipate changes in individual behavior inresponse to changes in economic variables. These variables include activities that are notexplicitly within a market activity, such as marriage, crime, and driving. The rationalmaximizer responds to changes in incentives in a predictable manner.

The Nature of Man*Michael C. Jensen and William H. Meckling

7 Journal of Applied Corporate Finance 4–19 (Summer 1994)

* * *

The usefulness of any model of human nature depends on its ability to explain a widerange of social phenomena; the test of such a model is the degree to which it is consistent

butler 3e 01 auto 7/24/14 11:03 AM Page 6

I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER 7

the behavior of both sexes. We have been unable to find a genderless term for use in the title whichhas the same desired impact.

with observed human behavior. A model that explains behavior only in one smallgeographical area, or only for a short period in history, or only for people engaged incertain pursuits is not very useful. For this reason we must use a limited number of generaltraits to characterize human behavior. Greater detail limits the explanatory ability of amodel because individual people differ so greatly. We want a set of characteristics thatcaptures the essence of human nature, but no more.

While this may sound abstract and complex, it is neither. Each of us has in mind anduses models of human nature every day. We all understand, for example, that people arewilling to make trade-offs among things that they want. Our spouses, partners, children,friends, business associates, or perfect strangers can be induced to make substitutions ofall kinds. We offer to go out to dinner Saturday night instead of the concert tonight. Weoffer to substitute a bicycle for a stereo as a birthday gift. We allow an employee to gohome early today if the time is made up next week.

If our model specified that individuals were never willing to substitute some amountof a good for some amounts of other goods, it would quickly run aground on inconsistentevidence. It could not explain much of the human behavior we observe. While it maysound silly to characterize individuals as unwilling to make substitutions, that view ofhuman behavior is not far from models that are widely accepted and used by many socialscientists (for example, Maslow’s hierarchy of human needs and sociologists’ modelsportraying individuals as cultural role players or social victims).

* * *

RESOURCEFUL, EVALUATIVE, MAXIMIZING MODEL: REMM

. . . While the term is new, the concept is not. REMM is the product of over 200 yearsof research and debate in economics, the other social sciences, and philosophy. As a result,REMM is now defined in very precise terms, but we offer here only a bare-bones summaryof the concept. Many specifics can be added to enrich its descriptive content withoutsacrificing the basic foundation provided here.

Postulate I. Every individual cares; he or she is an evaluator.

(a) The individual cares about almost everything: knowledge, independence, the plightof others, the environment, honor, interpersonal relationships, status, peer approval,group norms, culture, wealth, rules of conduct, the weather, music, art, and so on.

(b) REMM is always willing to make trade-offs and substitutions. Each individual isalways willing to give up some sufficiently small amount of any particular good (oranges,water, air, housing, honesty, or safety) for some sufficiently large quantity of other goods.Furthermore, valuation is relative in the sense that the value of a unit of any particulargood decreases as the individual enjoys more of it relative to other goods.

(c) Individual preferences are transitive— that is, if A is preferred to B, and B is preferredto C, then A is preferred to C.

* * *

Postulate II. Each individual’s wants are unlimited.

(a) If we designate those things that REMM values positively as “goods,” then he orshe prefers more goods to less. Goods can be anything from art objects to ethical norms.

butler 3e 01 auto 7/24/14 11:03 AM Page 7

8 I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER

(b) REMM cannot be satiated. He or she always wants more of some things, be theymaterial goods such as art, sculpture, castles, and pyramids; or intangible goods such assolitude, companionship, honesty, respect, love, fame, and immortality.

Postulate III. Each individual is a maximizer.

He or she acts so as to enjoy the highest level of value possible. Individuals are alwaysconstrained in satisfying their wants. Wealth, time, and the laws of nature are all importantconstraints that affect the opportunities available to any individual. Individuals are alsoconstrained by the limits of their own knowledge about various goods and opportunities;and their choices of goods or courses of action will reflect the costs of acquiring theknowledge or information necessary to evaluate those choices.

The notion of an opportunity set provides the limit on the level of value attainable byany individual. The opportunity set is usually regarded as something that is given andexternal to the individual. Economists tend to represent it as a wealth or income constraintand a set of prices at which the individual can buy goods. But the notion of an individual’sopportunity set can be generalized to include the set of activities he or she can performduring a 24-hour day or in a lifetime.

Postulate IV. The individual is resourceful.

Individuals are creative. They are able to conceive of changes in their environment,foresee the consequences thereof, and respond by creating new opportunities.

Although an individual’s opportunity set is limited at any instant in time by his or herknowledge and the state of the world, that limitation is not immutable. Human beingsare not only capable of learning about new opportunities, they also engage in resourceful,creative activities that expand their opportunities in various ways.

The kind of highly mechanical behavior posited by economists— that is, assigningprobabilities and expected values to various actions and choosing the action with thehighest expected value— is formally consistent with the evaluating, maximizing modeldefined in Postulates I through III. But such behavior falls short of the human capabilitiesposited by REMM; it says nothing about the individual’s ingenuity and creativity.

REMMs AT WORK

One way of capturing the notion of resourcefulness is to think about the effects ofnewly imposed constraints on human behavior. These constraints might be new operatingpolicies in a corporation or new laws imposed by governments. No matter how much ex-perience we have with the response of people to changes in their environment, we tendto overestimate the impact of a new law or policy intended to constrain human behavior.Moreover, the constraint or law will almost always generate behavior which was neverimagined by its sponsors. Why? Because of the sponsors’ failure to recognize the creativityof REMMs. REMMs’ response to a new constraint is to begin searching for substitutesfor what is now constrained, a search that is not restricted to existing alternatives. REMMswill invent alternatives that did not previously exist.

An excellent illustration of how humans function as REMMs is the popular responseto the 1974 federal imposition of a 55-mile-per-hour speed limit in all states underpenalty of loss of federal transportation and highway moneys. The primary reasonoffered for this law was the conservation of gasoline and diesel fuel (for simplicity, weignore the benefits associated with the smaller number of accidents that occur at slowerspeeds).

butler 3e 01 auto 7/24/14 11:03 AM Page 8

I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER 9

2. REMM is not meant to describe the behavior of any particular individual. To do so requiresmore complete specification of the preferences, values, emotions, and talents of each person. Moreover,individuals respond very differently to factors such as stress, tension, and fear, and, in so doing, oftenviolate the predictions of the REMM model. For purposes of organizational and public policy, manyof these violations of REMM “cancel out” in the aggregate across large groups of people and overtime— but by no means all. For a discussion of a Pain Avoidance Model (PAM) that complementsREMM by accommodating systematically non-rational behavior, see Michael C. Jensen, “Economics,Organizations, and Non-Rational Behavior,” Economic Inquiry (1995).

The major cost associated with slower driving is lost time. At a maximum speed of 55mph instead of 70 mph, trips take longer. Those who argue that lost time is not importantmust recognize that an hour of time consumed is just as irreplaceable as— and generallymore valuable than— the gallon of gasoline consumed. On these grounds, the law createdinefficiencies, and the behavior of drivers is consistent with that conclusion. . . . Peopleresponded in REMM-like fashion to this newly imposed constraint in a number of ways.One was to reduce their automobile, bus, and truck travel, and, in some cases, to shiftto travel by other means such as airplanes and trains. Another response was to defy thelaw by driving at speeds exceeding the 55 mph maximum. Violating the speed limit, ofcourse, exposes offenders to potential costs in the form of fines, higher insurance rates,and possible loss of driver’s licenses. This, in turn, provides incentives for REMMs tosearch out ways to reduce such costs. The result has been an entire new industry, and therapid growth of an already existing one. Citizen’s Band radios (CBs), which had beenused primarily by truckers, suddenly became widely used by passenger car drivers andalmost all truckers. . . . CB radios have been largely replaced by radar detectors that warndrivers of the presence of police radar. These devices have become so common that policehave taken countermeasures, such as investing in more expensive and sophisticated radarunits that are less susceptible to detection. Manufacturers of radar detectors retaliated bymanufacturing increasingly sophisticated units.

The message is clear: people who drive value their time at more than [the savings infuel costs from the lower speed limit]. When the 55 mph maximum speed limit wasimposed, few would have predicted the ensuing chain of events. One seemingly modestconstraint on REMMs has created a new electronic industry designed to avoid the constraint.And such behavior shows itself again and again in a variety of contexts— for example,in taxpayers’ continuous search for, and discovery of, “loopholes” in income tax laws; thedevelopment of so-called clubs with private liquor stock in areas where serving liquor atpublic bars is prohibited; the ability of General Dynamics’ CEO George Anders and hismanagement team, when put under a lucrative incentive compensation plan tied to share-holder value, to quadruple the market value of the company even as the defense industrywas facing sharp cutbacks; and the growth in the number of hotel courtesy cars and gypsycabs in cities where taxi-cab licensing results in monopoly fares.

These examples are typical of behavior consistent with the REMM model, but not, aswe shall see, with other models that prevail in the social sciences. The failure of the othermodels is important because the individual stands in relation to organizations as the atomis to mass. From small groups to entire societies, organizations are composed of individuals.If we are to have a science of such organizations, it will have to be founded on buildingblocks that capture as simply as possible the most important traits of humans. Althoughclearly not a complete description of human behavior, REMM is the model of humanbehavior that best meets this criterion.2

* * *

butler 3e 01 auto 7/24/14 11:03 AM Page 9

10 I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER

Notes and Questions

1. The Self-Interest Assumption and the Critics’ “Straw Man”: Economics is oftencriticized based on the mistaken impression that economists assume that economic de-cision-makers are only interested in money. To the contrary, economists recognize thatindividuals gain utility from any variety of activities and any number of sources— notjust money. People enjoy looking at art, obtain satisfaction from their jobs over and abovethe salaries they earn, and feel good when helping others. Clearly, properly understood,the self-interest assumption does not mean that individuals are cold, “Dickensian” Scrooges,totally selfish and uncaring in their choices.

2. Transitive Preferences: An important assumption about economic behavior is thateconomic actors’ preferences are transitive (that is, if A is preferred to B, and B is preferredto C, then A is preferred to C), at least over short periods of time. Suppose a woman goesinto a restaurant and is informed that the only three entrees are chicken, lobster, andsteak. She orders chicken, but the waiter returns and tells her that they are out of chicken.She replies, “I’ll settle for the lobster.” However, the waiter returns again and says, “I madea mistake, it turns out that we do have chicken after all. Would you prefer chicken insteadof lobster?” To which she replies: “No, I’d like the steak.” Such behavior violates thetransitive preferences assumption.

3. Uncertainty and Risk Aversion: Individuals often make decisions when they are notcertain of the outcome. Such uncertainty introduces risk into the decision making process.Economists assume that most individuals are risk averse. When given a choice betweena certain value, say $1,000, and an uncertain outcome of a coin toss— heads you win$2,000, and tails you get $0— a risk averse individual will prefer the certain amount evenif the expected payoff from the coin toss is also $1,000. [The expected value of the cointoss is the weighted average of the possible payoffs. So, in this example, the expectedvalue is (.5 x $2,000) + (.5 x $0) = $1,000.00.] The concept of risk aversion is the basisfor many important insights in economics, finance, and law. Chapter VI, “Risk,” exploresthis important assumption about economic decision making in great detail.

4. Beware of Unintended Consequences: Many laws and regulations are intended tocorrect perceived problems with the market allocation of goods and services. It is importantin designing laws and regulations to consider how rational economic actors are likely torespond to new constraints on their behavior. Consider, for example, the Superfund re-quirement that contaminated soil at toxic waste sites be sterilized. This requirement meansthat companies looking for new industrial sites steer away from Superfund sites for fearof being held liable for cleaning up someone else’s pollution (the Superfund law calls forjoint and several liability of anyone who has ever owned the site). As a result, companiestend to locate in areas where the soil is not contaminated, and we end up with two dirtylots instead of one. “Brownfield” is the name that has been given to this unintended buttotally predictable result.

5. Bounded Rationality: The assumption that individuals are rational maximizers is,of course, an oversimplification. We don’t always seek to maximize our utility, and weall certainly have our irrational moments. But that is the idea of a model— it is a simplifiedversion of reality that generates predictions about behavior. The validity of a model isdetermined by the accuracy of its predictions— on which the economic model doesextremely well. The fact that individuals sometimes act irrationally merely adds noise tothe model, so long as the irrational behavior is essentially random. But if the irrationalityis systematic, such that individuals consistently behave in a particular (non-rational) way,it may be possible to develop a model that generates better predictions about behavior.

butler 3e 01 auto 7/24/14 11:03 AM Page 10

I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER 11

Footnote 5 to the Jensen and Meckling article describes one attempted model of non-rational behavior, what Jensen calls the Pain Avoidance Model. The growing field ofbehavioral law and economics is a broader attempt to identify such systematic irrationalities,which may result in predictions that differ from the more traditional law-and-economicsmodel. Cass Sunstein provides some highlights:

The idea of bounded rationality includes several different points. The firstinvolves the kind of cognitive errors that can come from biases in judgment andfrom efforts to economize on decision costs (“heuristics”). Biases fall in variouscategories; they include hindsight bias, optimistic bias, and extremeness aversion.Efforts to economize on decision costs are responsible for rules of thumb, orheuristics. Rules of thumb— as in the process of deciding on appropriate numbers(for many things, including real estate prices or pain-and-suffering awards) bychoosing an “anchor” and then making adjustments— reduce the costs of makingdecisions, but they may not be fully rational. . . .

A second form of bounded rationality comes from framing effects. People’sreaction to a choice may depend on how it is described; hence identical, but dif-ferently worded, problems can elicit quite different responses. Consider clientsdeciding whether to settle or to go to trial. If they are told that, of 100 litigants,90 who go to trial win, they may be far more likely to go to trial than if they aretold that of 100 litigants, 10 who go to trial lose. . . .

Some aspects of bounded rationality are modeled by prospect theory, whichis intended as a more accurate description of behavior than expected utilitytheory. For purposes of law, the first key feature of prospect theory, departingfrom expected utility theory, is that people are loss averse, that is, they dislikelosses more than they like corresponding gains. . . . The second key finding is thatpeople care a great deal about certainty (thus people would prefer a reductionof risk from 0.1 to 0.0 to a reduction of 0.3 to 0.1). . . . An important implicationis that people are risk seeking for losses (they would choose an 80% chance tolose $4,000 over a certain loss of $3,000) and risk averse for gains (they wouldprefer a certain gain of $3,000 over an 80% chance to gain $4,500).

Cass R. Sunstein, Behavioral Law and Economics: A Progress Report, 1 American Law &Economics Review 115, 123–24 (1999).

Most of the research to date on behavioral law and economics is based on experiments,which obviously raises questions about how well the experimental results transfer tothe real world. Judge Richard Posner identifies an important limitation of experimentalresearch:

Selection effects suggest that the experimental and real-world environmentswill differ systematically. The experimental subjects are chosen more or less randomly;but people are not randomly sorted to jobs and other activities. People who cannotcalculate probabilities will either avoid gambling, if they know their cognitiveweakness, or, if they do not, will soon be wiped out and thus be forced to discontinuegambling. People who are unusually “fair” will avoid (or, again, be forced out of)roughhouse activities— including highly competitive businesses, trial lawyering,and the academic rat race. Hyperbolic discounters will avoid the financial servicesindustry. These selection effects will not work perfectly, but they are likely to drivea big wedge between experimental and real-world consequences of irrationality.

Richard A. Posner, Rational Choice, Behavioral Economics, and the Law, 50 Stanford LawReview 1551, 1570–71 (1998). In essence, Posner’s argument is that markets will correct

butler 3e 01 auto 7/24/14 11:03 AM Page 11

12 I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER

for much of the non-rational behavior that individuals may exhibit, even if it is systematicrather than random. As a result, the traditional law-and-economics model is far frombeing supplanted.

3. Assumptions about Firm Behavior

A corollary of the self-interest assumption for individual behavior is the assumptionthat business firms attempt to maximize economic profit. Economic profit is defined asthe total revenues received from selling a product or service minus the total costs ofproducing the product or service, including the opportunity costs.

Matsushita Elec. Indus. Co. v. Zenith Radio Corp.Supreme Court of the United States

475 U.S. 574 (1986)

POWELL, J.

* * *Petitioners, defendants below, are 21 corporations that manufacture or sell “consumer

electronic products” (CEPs)— for the most part, television sets. Petitioners include bothJapanese manufacturers of CEPs and American firms, controlled by Japanese parents,that sell the Japanese-manufactured products. Respondents, plaintiffs below, are ZenithRadio Corporation (Zenith) and National Union Electric Corporation (NUE). Zenith isan American firm that manufactures and sells television sets. NUE is the corporate successorto Emerson Radio Company, an American firm that manufactured and sold televisionsets until 1970, when it withdrew from the market after sustaining substantial losses.Zenith and NUE began this lawsuit in 1974, claiming that petitioners had illegally conspiredto drive American firms from the American CEP market. According to respondents, thegist of this conspiracy was a “ ‘scheme to raise, fix and maintain artificially high prices fortelevision receivers sold by [petitioners] in Japan and, at the same time, to fix and maintainlow prices for television receivers exported to and sold in the United States.’ ” These “lowprices” were allegedly at levels that produced substantial losses for petitioners. . . .

* * *. . . The thrust of respondents’ argument is that petitioners used their monopoly profits

from the Japanese market to fund a concerted campaign to price predatorily and therebydrive respondents and other American manufacturers of CEPs out of business. Once suc-cessful, according to respondents, petitioners would cartelize the American CEP market,restricting output and raising prices above the level that fair competition would produce.The resulting monopoly profits, respondents contend, would more than compensate pe-titioners for the losses they incurred through years of pricing below market level.

* * *. . . According to petitioners, the alleged conspiracy is one that is economically irrational

and practically infeasible. Consequently, petitioners contend, they had no motive toengage in the alleged predatory pricing conspiracy; indeed, they had a strong motive notto conspire in the manner respondents allege. Petitioners argue that, in light of the absenceof any apparent motive and the ambiguous nature of the evidence of conspiracy, no trierof fact reasonably could find that the conspiracy with which petitioners are chargedactually existed. This argument requires us to consider the nature of the alleged conspiracyand the practical obstacles to its implementation.

butler 3e 01 auto 7/24/14 11:03 AM Page 12

I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER 13

IVA

A predatory pricing conspiracy is by nature speculative. Any agreement to price belowthe competitive level requires the conspirators to forgo profits that free competition wouldoffer them. The forgone profits may be considered an investment in the future. For theinvestment to be rational, the conspirators must have a reasonable expectation of recovering,in the form of later monopoly profits, more than the losses suffered. As then-ProfessorBork, discussing predatory pricing by a single firm, explained:

“Any realistic theory of predation recognizes that the predator as well as hisvictims will incur losses during the fighting, but such a theory supposes it maybe a rational calculation for the predator to view the losses as an investment infuture monopoly profits (where rivals are to be killed) or in future undisturbedprofits (where rivals are to be disciplined). The future flow of profits, appropriatelydiscounted, must then exceed the present size of the losses.” R. Bork, The AntitrustParadox 145 (1978).

As this explanation shows, the success of such schemes is inherently uncertain: the short-run loss is definite, but the long-run gain depends on successfully neutralizing thecompetition. Moreover, it is not enough simply to achieve monopoly power, as monopolypricing may breed quick entry by new competitors eager to share in the excess profits.The success of any predatory scheme depends on maintainingmonopoly power for longenough both to recoup the predator’s losses and to harvest some additional gain. Absentsome assurance that the hoped-for monopoly will materialize, and that it can be sustainedfor a significant period of time, “[the] predator must make a substantial investment withno assurance that it will pay off.” For this reason, there is a consensus among commentatorsthat predatory pricing schemes are rarely tried, and even more rarely successful.

These observations apply even to predatory pricing by a single firm seeking monopolypower. In this case, respondents allege that a large number of firms have conspired over aperiod of many years to charge below-market prices in order to stifle competition. Such aconspiracy is incalculably more difficult to execute than an analogous plan undertaken bya single predator. The conspirators must allocate the losses to be sustained during the con-spiracy’s operation, and must also allocate any gains to be realized from its success. Preciselybecause success is speculative and depends on a willingness to endure losses for an indefiniteperiod, each conspirator has a strong incentive to cheat, letting its partners suffer the lossesnecessary to destroy the competition while sharing in any gains if the conspiracy succeeds.The necessary allocation is therefore difficult to accomplish. Yet if conspirators cheat toany substantial extent, the conspiracy must fail, because its success depends on depressingthe market price for all buyers of CEPs. If there are too few goods at the artificially lowprice to satisfy demand, the would-be victims of the conspiracy can continue to sell at the“real” market price, and the conspirators suffer losses to little purpose.

Finally, if predatory pricing conspiracies are generally unlikely to occur, they areespecially so where, as here, the prospects of attaining monopoly power seem slight. Inorder to recoup their losses, petitioners must obtain enough market power to set higherthan competitive prices, and then must sustain those prices long enough to earn in excessprofits what they earlier gave up in below-cost prices. Two decades after their conspiracyis alleged to have commenced, petitioners appear to be far from achieving this goal: thetwo largest shares of the retail market in television sets are held by RCA and respondentZenith, not by any of petitioners. Moreover, those shares, which together approximate40% of sales, did not decline appreciably during the 1970’s. Petitioners’ collective share

butler 3e 01 auto 7/24/14 11:03 AM Page 13

14 I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER

3. Respondents offer no reason to suppose that entry into the relevant market is especially difficult,yet without barriers to entry it would presumably be impossible to maintain supra competitive pricesfor an extended time. Judge Easterbrook, commenting on this case in a law review article, offers thefollowing sensible assessment:

. . . There are no barriers to entry into electronics, as the proliferation of computer andaudio firms shows. The competition would come from resurgent United States firms, fromother foreign firms (Korea and many other nations make TV sets), and from defendantsthemselves. In order to recoup, the Japanese firms would need to suppress competitionamong themselves. On plaintiffs’ theory, the cartel would need to last at least thirty years,far longer than any in history, even when cartels were not illegal. None should be sanguineabout the prospects of such a cartel, given each firm’s incentive to shave price and expandits share of sales. The predation recoupment story therefore does not make sense, and weare left with the more plausible inference that the Japanese firms did not sell below cost inthe first place. They were just engaged in hard competition.

Easterbrook, The Limits of Antitrust, 63 Texas L. Rev. 1, 26–27 (1984) (footnotes omitted).

rose rapidly during this period, from one-fifth or less of the relevant markets to close to50%. Neither the District Court nor the Court of Appeals found, however, that petitioners’share presently allows them to charge monopoly prices; to the contrary, respondentscontend that the conspiracy is ongoing— that petitioners are still artificially depressingthe market price in order to drive Zenith out of the market. The data in the record stronglysuggest that goal is yet far distant.3

The alleged conspiracy’s failure to achieve its ends in the two decades of its assertedoperation is strong evidence that the conspiracy does not in fact exist. Since the losses insuch a conspiracy accrue before the gains, they must be “repaid” with interest. And becausethe alleged losses have accrued over the course of two decades, the conspirators couldwell require a correspondingly long time to recoup. Maintaining supra competitive pricesin turn depends on the continued cooperation of the conspirators, on the inability ofother would-be competitors to enter the market, and (not incidentally) on the conspirators’ability to escape antitrust liability for their minimum price-fixing cartel. Each of thesefactors weighs more heavily as the time needed to recoup losses grows. If the losses havebeen substantial— as would likely be necessary in order to drive out the competition—petitioners would most likely have to sustain their cartel for years simply to break even.

Nor does the possibility that petitioners have obtained supra competitive profits in theJapanese market change this calculation. Whether or not petitioners have the means tosustain substantial losses in this country over a long period of time, they have no motiveto sustain such losses absent some strong likelihood that the alleged conspiracy in thiscountry will eventually pay off. The courts below found no evidence of any such success,and— as indicated above— the facts actually are to the contrary: RCA and Zenith, notany of the petitioners, continue to hold the largest share of the American retail market incolor television sets. More important, there is nothing to suggest any relationship betweenpetitioners’ profits in Japan and the amount petitioners could expect to gain from aconspiracy to monopolize the American market. In the absence of any such evidence, thepossible existence of supra competitive profits in Japan simply cannot overcome theeconomic obstacles to the ultimate success of this alleged predatory conspiracy.

* * *

. . . [P]etitioners had no motive to enter into the alleged conspiracy. To the contrary,as presumably rational businesses, petitioners had every incentive not to engage in theconduct with which they are charged, for its likely effect would be to generate losses forpetitioners with no corresponding gains. . . .

butler 3e 01 auto 7/24/14 11:03 AM Page 14

I · THE ECONOMICS PERSPECTIVE: INCENTIVES MATTER 15

* * *