Embed Size (px)

Citation preview

CORPORATEFINANCE

ffirs 13 January 2012; 9:6:55

CFA Institute is the premier association for investment professionals around the world, withover 101,000 members in 134 countries. Since 1963 the organization has developed andadministered the renowned Chartered Financial Analysts Program. With a rich history ofleading the investment profession, CFA Institute has set the highest standards in ethics,education, and professional excellence within the global investment community, and is theforemost authority on investment profession conduct and practice.

Each book in the CFA Institute Investment Series is geared toward industry practi-tioners along with graduate-level finance students and covers the most important topics inthe industry. The authors of these cutting-edge books are themselves industry professionalsand academics and bring their wealth of knowledge and expertise to this series.

ffirs 13 January 2012; 9:6:55

CORPORATEFINANCE

A Practical Approach

Second Edition

Michelle R. Clayman, CFA

Martin S. Fridson, CFA

George H. Troughton, CFA

John Wiley & Sons, Inc.

ffirs 13 January 2012; 9:6:56

Copyright r 2012 by CFA Institute. All rights reserved.

Published by John Wiley & Sons, Inc., Hoboken, New JerseyPublished simultaneously in Canada

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or byany means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted underSection 107 or 108 of the 1976 United States Copyright Act, without either the prior written permission of thePublisher, or authorization through payment of the appropriate per-copy fee to the Copyright Clearance Center, Inc.,222 Rosewood Drive, Danvers, MA 01923, (978) 750-8400, fax (978) 646-8600, or on the web at www.copyright.com. Requests to the Publisher for permission should be addressed to the Permissions Department, JohnWiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748-6011, fax (201) 748-6008, or online athttp://www.wiley.com/go/permission.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts in preparingthis book, they make no representations or warranties with respect to the accuracy or completeness of the contents ofthis book and specifically disclaim any implied warranties of merchantability or fitness for a particular purpose. Nowarranty may be created or extended by sales representatives or written sales materials. The advice and strategiescontained herein may not be suitable for your situation. You should consult with a professional where appropriate.Neither the publisher nor author shall be liable for any loss of profit or any other commercial damages, including butnot limited to special, incidental, consequential, or other damages.

For general information on our other products and services or for technical support, please contact our CustomerCare Department within the United States at (800) 762-2974, outside the United States at (317) 572-3993 orfax (317) 572-4002.

Wiley also publishes its books in a variety of electronic formats. Some content that appears in print may not beavailable in electronic formats. For more information about Wiley products, visit our web site at www.wiley.com.

Library of Congress Cataloging-in-Publication Data:

Corporate finance : a practical approach / [edited by] Michelle R. Clayman, Martin S. Fridson,George H. Troughton. — 2nd ed.

p. cm. — (CFA Institute investment series ; 42)Includes index.ISBN 978-1-118-10537-5 (cloth); ISBN 978-1-118-21729-0 (ebk);ISBN 978-1-118-21730-6 (ebk); ISBN 978-1-118-21731-3 (ebk)1. Corporations—Finance. I. Clayman,Michelle R. II. Fridson,Martin S. III. Troughton,GeorgeH.

HG4026.C67 2012658.15—dc23

2011039258Printed in the United States of America

10 9 8 7 6 5 4 3 2 1

ffirs 13 January 2012; 9:6:56

CONTENTS

Foreword xiAcknowledgments xvAbout the CFA Institute Investment Series xvii

CHAPTER 1Corporate Governance 1

Learning Outcomes 11. Introduction 12. Corporate Governance: Objectives and Guiding Principles 23. Forms of Business and Conflicts of Interest 3

3.1. Sole Proprietorships 43.2. Partnerships 53.3. Corporations 5

4. Specific Sources of Conflict: Agency Relationships 64.1. Manager–Shareholder Conflicts 64.2. Director–Shareholder Conflicts 10

5. Corporate Governance Evaluation 105.1. The Board of Directors 115.2. Examples of Codes of Corporate Governance 24

6. Environmental, Social, and Governance Factors 377. Valuation Implications of Corporate Governance 398. Summary 40

Problems 42

CHAPTER 2Capital Budgeting 47

Learning Outcomes 471. Introduction 482. The Capital Budgeting Process 493. Basic Principles of Capital Budgeting 504. Investment Decision Criteria 52

4.1. Net Present Value 524.2. Internal Rate of Return 534.3. Payback Period 554.4. Discounted Payback Period 574.5. Average Accounting Rate of Return 584.6. Profitability Index 584.7. NPV Profile 59

ftoc 13 January 2012; 9:9:50

v

4.8. Ranking Conflicts between NPV and IRR 614.9. The Multiple IRR Problem and the No IRR Problem 654.10. Popularity and Usage of the Capital Budgeting Methods 68

5. Cash Flow Projections 705.1. Table Format with Cash Flows Collected by Year 705.2. Table Format with Cash Flows Collected by Type 725.3. Equation Format for Organizing Cash Flows 72

6. More on Cash Flow Projections 746.1. Straight-Line and Accelerated Depreciation Methods 746.2. Cash Flows for a Replacement Project 776.3. Spreadsheet Modeling 796.4. Effects of Inflation on Capital Budgeting Analysis 81

7. Project Analysis and Evaluation 827.1. Mutually Exclusive Projects with Unequal Lives 827.2. Capital Rationing 847.3. Risk Analysis of Capital Investments—Standalone Methods 867.4. Risk Analysis of Capital Investments—Market Risk Methods 927.5. Real Options 957.6. Common Capital Budgeting Pitfalls 99

8. Other Income Measures and Valuation Models 1018.1. The Basic Capital Budgeting Model 1018.2. Economic and Accounting Income 1028.3. Economic Profit, Residual Income, and Claims Valuation 106

9. Summary 110Problems 113

CHAPTER 3Cost of Capital 127

Learning Outcomes 1271. Introduction 1282. Cost of Capital 128

2.1. Taxes and the Cost of Capital 1292.2. Weights of the Weighted Average 1312.3. Applying the Cost of Capital to Capital Budgeting and

Security Valuation 1333. Costs of the Different Sources of Capital 135

3.1. Cost of Debt 1353.2. Cost of Preferred Stock 1383.3. Cost of Common Equity 140

4. Topics in Cost of Capital Estimation 1464.1. Estimating Beta and Determining a Project Beta 1464.2. Country Risk 1534.3. Marginal Cost of Capital Schedule 1544.4. Flotation Costs 1574.5. What Do CFOs Do? 160

5. Summary 160Problems 163

ftoc 13 January 2012; 9:9:50

vi Contents

CHAPTER 4Measures of Leverage 171

Learning Outcomes 1711. Introduction 1712. Leverage 1723. Business Risk and Financial Risk 173

3.1. Business Risk and Its Components 1743.2. Sales Risk 1743.3. Operating Risk 1763.4. Financial Risk 1823.5. Total Leverage 1843.6. Breakeven Points and Operating Breakeven Points 1893.7. The Risks of Creditors and Owners 191

4. Summary 194Problems 194

CHAPTER 5Capital Structure 199

Learning Outcomes 1991. Introduction 1992. The Capital Structure Decision 200

2.1. Proposition I without Taxes: Capital Structure Irrelevance 2012.2. Proposition II without Taxes: Higher Financial Leverage

Raises the Cost of Equity 2032.3. Taxes, the Cost of Capital, and the Value of the Company 2052.4. Costs of Financial Distress 2102.5. Agency Costs 2112.6. Costs of Asymmetric Information 2122.7. The Optimal Capital Structure According to the Static

Trade-Off Theory 2133. Practical Issues in Capital Structure Policy 216

3.1. Debt Ratings 2163.2. Evaluating Capital Structure Policy 2173.3. Leverage in an International Setting 218

4. Summary 222Problems 223

CHAPTER 6Dividends and Share Repurchases: Basics 229

Learning Outcomes 2291. Introduction 2292. Dividends: Forms 230

2.1. Regular Cash Dividends 2312.2. Extra or Special (Irregular) Dividends 2322.3. Liquidating Dividends 234

ftoc 13 January 2012; 9:9:50

Contents vii

2.4. Stock Dividends 2342.5. Stock Splits 236

3. Dividends: Payment Chronology 2383.1. Declaration Date 2383.2. Ex-Dividend Date 2383.3. Holder-of-Record Date 2393.4. Payment Date 2393.5. Interval between Key Dates in the Dividend Payment Chronology 239

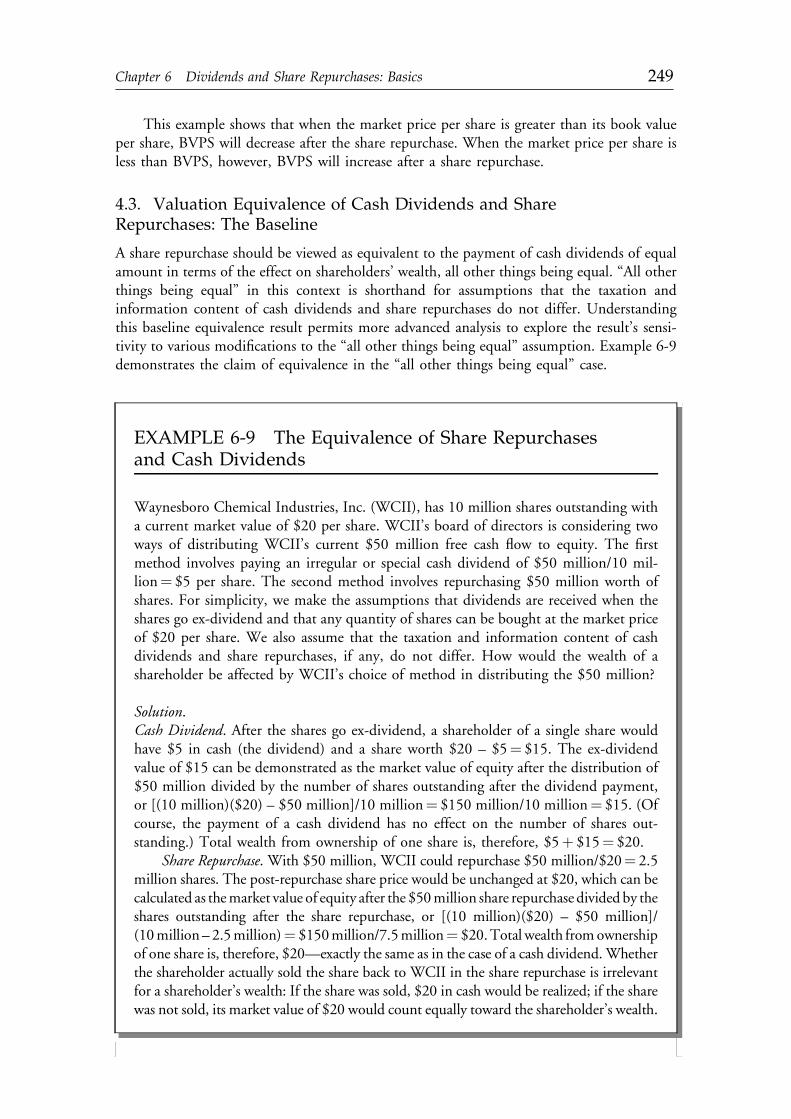

4. Share Repurchases 2414.1. Share Repurchase Methods 2434.2. Financial Statement Effects of Repurchases 2454.3. Valuation Equivalence of Cash Dividends and

Share Repurchases: The Baseline 2495. Concluding Remarks 2506. Summary 251

Problems 252

CHAPTER 7Dividends and Share Repurchases: Analysis 257

Learning Outcomes 2571. Introduction 2582. Dividend Policy and Company Value: Theory 258

2.1. Dividend Policy Does Not Matter 2582.2. Dividend Policy Matters: The Bird-in-the-Hand Argument 2602.3. Dividend Policy Matters: The Tax Argument 2602.4. Other Theoretical Issues 2612.5. Dividend Theory: Summary 271

3. Factors Affecting Dividend Policy 2713.1. Investment Opportunities 2723.2. The Expected Volatility of Future Earnings 2723.3. Financial Flexibility 2733.4. Tax Considerations 2733.5. Flotation Costs 2763.6. Contractual and Legal Restrictions 2773.7. Factors Affecting Dividend Policy: Summary 278

4. Payout Policies 2794.1. Types of Dividend Policies 2794.2. The Dividend versus Share Repurchase Decision 2854.3. Global Trends in Payout Policy 291

5. Analysis of Dividend Safety 2936. Summary 297

Problems 298

CHAPTER 8Working Capital Management 303

Learning Outcomes 3031. Introduction 304

ftoc 13 January 2012; 9:9:51

viii Contents

2. Managing and Measuring Liquidity 3052.1. Defining Liquidity Management 3052.2. Measuring Liquidity 307

3. Managing the Cash Position 3123.1. Forecasting Short-Term Cash Flows 3133.2. Monitoring Cash Uses and Levels 315

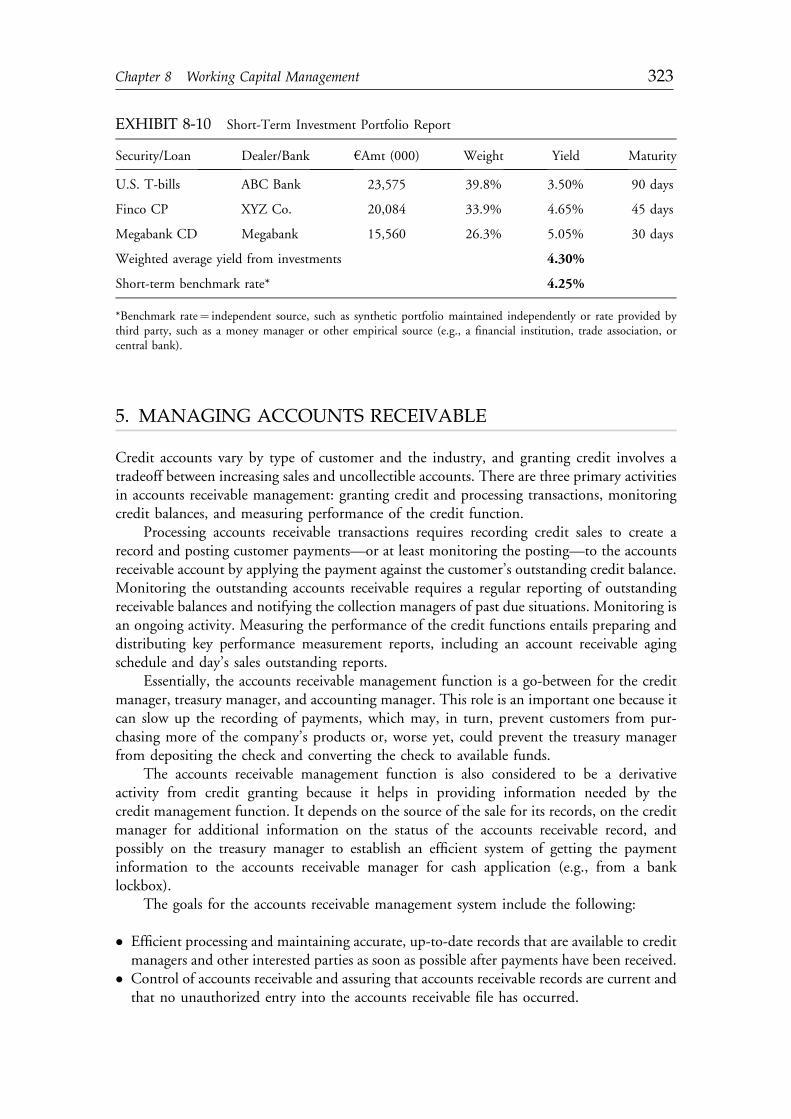

4. Investing Short-Term Funds 3164.1. Short-Term Investment Instruments 3164.2. Strategies 3204.3. Evaluating Short-Term Funds Management 322

5. Managing Accounts Receivable 3235.1. Key Elements of the Trade Credit Granting Process 3245.2. Managing Customers’ Receipts 3265.3. Evaluating Accounts Receivable Management 328

6. Managing Inventory 3306.1. Approaches to Managing Levels of Inventory 3316.2. Inventory Costs 3326.3. Evaluating Inventory Management 332

7. Managing Accounts Payable 3347.1. The Economics of Taking a Trade Discount 3357.2. Managing Cash Disbursements 3367.3. Evaluating Accounts Payable Management 337

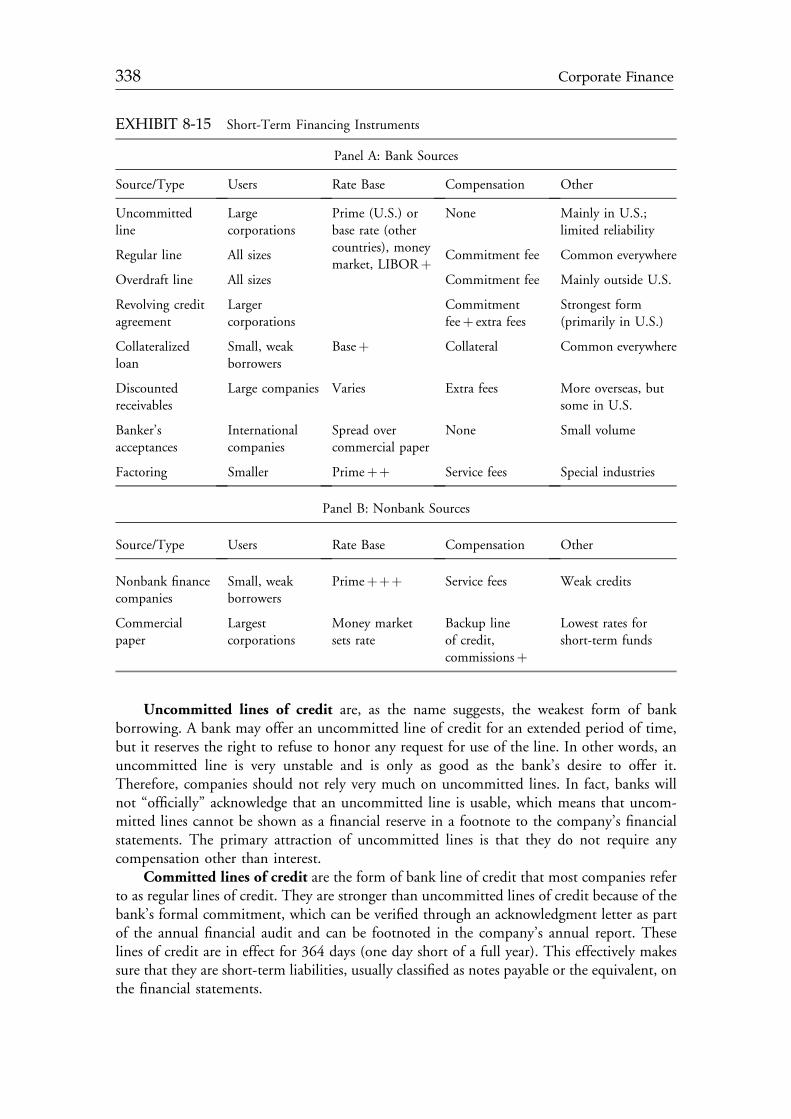

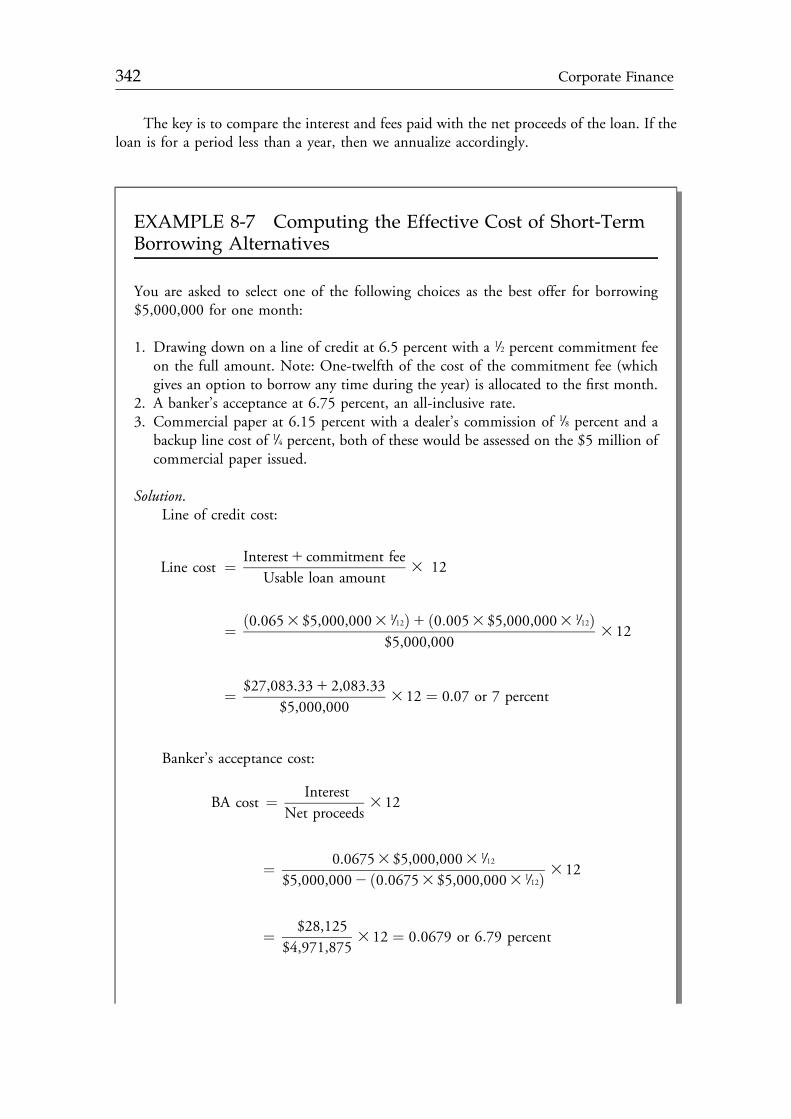

8. Managing Short-Term Financing 3378.1. Sources of Short-Term Financing 3378.2. Short-Term Borrowing Approaches 3398.3. Asset-Based Loans 3408.4. Computing the Costs of Borrowing 341

9. Summary 343Problems 344

CHAPTER 9Financial Statement Analysis 347

Learning Outcomes 3471. Introduction 3472. Common-Size Analysis 348

2.1. Vertical Common-Size Analysis 3502.2. Horizontal Common-Size Analysis 353

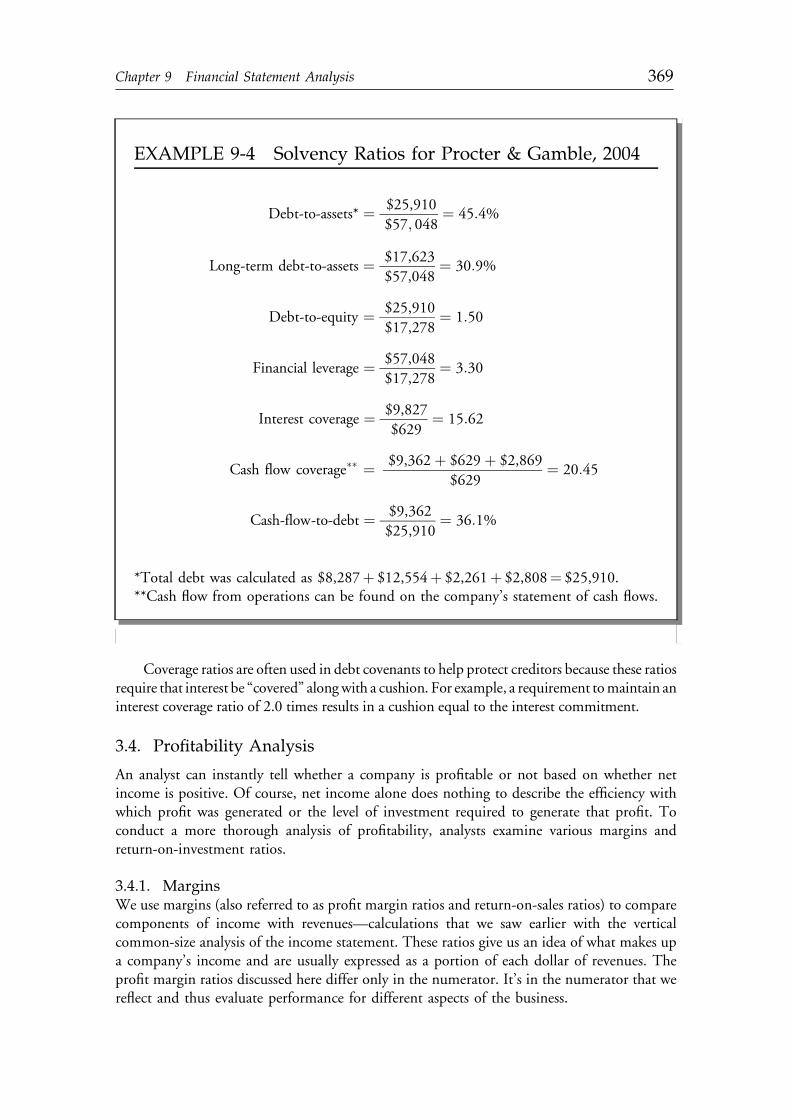

3. Financial Ratio Analysis 3563.1. Activity Ratios 3573.2. Liquidity Analysis 3633.3. Solvency Analysis 3653.4. Profitability Analysis 3693.5. Other Ratios 3833.6. Effective Use of Ratio Analysis 386

4. Pro Forma Analysis 3924.1. Estimating the Sales-Driven Relations 3954.2. Estimating the Fixed Burdens 396

ftoc 13 January 2012; 9:9:51

Contents ix

4.3. Forecasting Revenues 3974.4. Constructing Pro Forma Statements 397

5. Summary 401Problems 402

CHAPTER 10Mergers and Acquisitions 407

Learning Outcomes 4071. Introduction 4082. Mergers and Acquisitions: Definitions and Classifications 4103. Motives for Merger 413

3.1. Synergy 4133.2. Growth 4133.3. Increasing Market Power 4143.4. Acquiring Unique Capabilities and Resources 4143.5. Diversification 4143.6. Bootstrapping Earnings 4153.7. Managers’ Personal Incentives 4163.8. Tax Considerations 4163.9. Unlocking Hidden Value 4163.10. Cross-Border Motivations 417

4. Transaction Characteristics 4184.1. Form of Acquisition 4194.2. Method of Payment 4204.3. Mind-Set of Target Management 422

5. Takeovers 4245.1. Pre-Offer Takeover Defense Mechanisms 4245.2. Post-Offer Takeover Defense Mechanisms 426

6. Regulation 4296.1. Antitrust 4306.2. Securities Laws 433

7. Merger Analysis 4347.1. Target Company Valuation 4347.2. Bid Evaluation 446

8. Who Benefits from Mergers? 4509. Corporate Restructuring 45110. Summary 452

Problems 454

Glossary 463References 475About the Authors 481About the CFA Program 487Index 489

ftoc 13 January 2012; 9:9:51

x Contents

FOREWORD

I am honored to introduce this second edition of Corporate Finance: A Practical Approach,which promises to be an important and comprehensive discourse on corporate financialmanagement. The significant additions in this edition and revisions to the first edition buildon the topic areas introduced in 2008. Furthermore, they bring much-needed practicaldimensions to the complex and dynamic aspects of corporate finance.

Certainly, the global financial landscape has changed dramatically since the release ofthe first edition of this work. The economic drama and financial carnage injected into themarketplace starting in late 2007 have penetrated the very core of financial thought andpractice and have challenged long-standing economic beliefs and relationships. The effects oncorporate governance, capital structure, and budgeting caused by this extreme market vola-tility and economic upheaval have moved corporate treasurers and chief financial officers tothe front lines in their companies’ continuing pursuits of profitability and financial security.Only those institutions that can quickly adapt their financial management and corporatestructure to this “new normal” will survive well into the future. The chapters in this editionhave been revised to take into consideration some of the profound changes that have affectedthis new global financial setting. Yet, it is refreshing to note that no matter what economicenvironment exists in the future, sound, traditional financial management practices willalways be essential to the long-term success of any entity.

The authors of these chapters are leading industry practitioners and recognized academicthought leaders. Their unique perspectives and thorough understanding of their respectivetopic areas are invaluable in providing readers with a factual exposition of the subject matter.In addition, their commonsense approach of highlighting important learning outcomes andincorporating practical problem-solving tools gives readers techniques they can apply in real-world financial settings.

Like the original text, this edition is assembled from readings used in the CFA Pro-gram curriculum. The CFA Program is a comprehensive, self-directed, distance learningprogram administered by CFA Institute. Since the early 1960s, the attainment of the CFAdesignation has been viewed as a significant achievement in the realm of finance and investmentmanagement. Those who enter the CFA Program sit for three consecutive and rigorousexaminations that cover a broad range of important financial topics, including accounting,quantitative methods, equity and fixed-income analysis, portfolio management, and ethics.Most who enter this program already possess a strong record of achievement in the financialindustry, as well as advanced business degrees, but welcome the additional focus and com-prehensive curriculum of this designation program. I am fortunate to have earned the CFAcharter and am proud to serve on the Board of Governors of CFA Institute.

fbetw 13 January 2012; 9:5:34

xi

WHY THIS TEXT IS IMPORTANT

Competing in the global financial arena has been a far more daunting challenge during thisdecade than in earlier periods. The scarcity of credit and risk capital following the globalfinancial challenges of the past few years, along with the evolution of emerging economies asformidable players on the world financial stage, demands that businesses operate at utmostefficiency. Optimal financial management and peak operating effectiveness are prerequisitesnot only for success but also for survival. And in order to successfully commit risk capital,companies must incorporate disciplined, systematic capital-budgeting techniques so as toallocate capital to only those projects with optimal returns. Furthermore, companies must beable to understand the life spans of projects, effectively anticipate cash flow needs, andaccurately forecast lean periods in their liquidity to avoid potentially devastating shocks totheir financial and market health. Also critical in this new financial environment is the abilityto properly analyze the effects of inflation, disinflation, foreign currency shocks, and regu-latory risk on existing projects, as well as the ability to recognize capital-budgeting biases anderrors. This book offers comprehensive insights into avoiding these common pitfalls.

In particular, the chapter on capital budgeting is instrumental in instilling in the readerthe discipline to anticipate extraneous influences on capital planning. Another critical sectionof the book concerns forecasting and evaluating the weighted average cost of capital that anentity faces. Recent as well as long-term financial history has taught everyone the importanceof properly analyzing this crucial financial component. The degree of assumed leverage, taxbenefits and implications of using debt over other forms of capitalization, the cost of debtversus common and preferred equity, and the impact of changes in debt ratings—all areessential areas of knowledge for company leaders. The ability to use the cost of capital as aneffective discipline in organizational budgeting is yet another key component of continuedfinancial stability.

In addition to the tools and techniques for measuring the cost of capital, the appropriateuse of financial leverage is an important topic in this text. Clearly, increased leverageheightens the level of earnings volatility and, ultimately, the cost of equity and the overall riskattached to any company. Properly understanding the prudent use of financial leverage as anearnings-enhancement vehicle is essential. Furthermore, examining the degree of operatingleverage and the impact of cost structure on production is a vital component of measuringand evaluating the operating efficiency of any organization. And last but not least, anincredibly large part of ultimately determining the financial competitiveness of a company issuccessfully anticipating and accounting for the effect of taxes.

A key element of attracting investors and maintaining adequate sources of capital is fullyunderstanding how an entity manages its own equity in the context of dividends and sharerepurchases. In addition, I cannot overstate the advantages of having a technical grasp of theeffects on financial statements of altering dividend policy or engaging in share buybacks orsecondary offerings, nor can I overemphasize the commensurate impacts on a company’seffective cost of capital and overall financial flexibility. In this environment of heightenedinvestor focus on liquidity and financial health, effective working capital management is anecessity. The text walks the reader through the important steps in successfully monitoring anoptimal cash balance, contains a primer on short-term investment instruments, and delvesinto accounts receivable and inventory management. It also examines the benefits of short-term borrowing versus cash disbursements and other accounts payable strategies.

fbetw 13 January 2012; 9:5:34

xii Foreword

Finally, the critical steps in a merger and acquisition strategy are defined and analyzed.This segment of the text highlights the effects of the successful use of these approaches onfirm competitiveness, scale, and market power and addresses the potential pitfalls of inte-gration and cost management. Finally, this section examines the impact of taxes and regu-latory challenges on a potentially successful business combination tactic, as well as discussingwhen an acquisition posture makes sense.

WHAT HAS CHANGED SINCE THE FIRST EDITION

This second edition provides the reader with comprehensive updates on all topics, especiallywhere new techniques or technologies have emerged, and gears the learning outcomes,descriptions, and end-of-chapter exercises to the new economic realities of this decade. Thesections on dividend policy, share repurchases, and capital structure have also been revisedand reconstructed. These chapters contain significantly new content as well as updatedexercises.

No book can provide a practitioner or student with a no-fail recipe for comprehensivesuccess in financial management, and most entities have discovered that challenges andimpacts generally appear from unexpected sources and directions. The authors have tried tocreate a substantial taxonomy of corporate financial topics with real-world, commonsenseapplications as well as rigorous problems and exercises that allow readers to test their com-prehension of the subjects covered.

This book will become an important resource for a wide array of individuals. Some mayask whether the intricacies of capital budgeting, corporate liquidity, and dividend policy areof interest to a cross section of practitioners, but as many have discovered over the past fiveyears, ignoring the key building blocks of an optimal corporate financial structure and a lean,competitive, and well-capitalized organization can be perilous. Today’s corporate landscape,with all its volatility and high barriers to entry, requires that most members of a corporateentity be well schooled in the fundamentals of financial management. Organizations todaymust deal with formidable foreign competition, an older workforce, and significant capitalinvestments in order to achieve critical scale. A sound understanding of the capital man-agement techniques needed to maintain competitiveness and innovation is a necessity.Students will use this book either as a resource to gain a broad understanding of corporatefinancial practice or as a useful reference tool for quickly comprehending specific areas of thefinancial domain.

The long-term performance of all organizations is based on sound decision making bytheir constituents, whose decisions have wide-ranging implications for the future soundnessof their companies. I hope this book will prove to be a valuable resource for present andfuture members of these organizations.

Matthew Scanlan, CFAPresident and CEO

Renaissance Institutional Management LLCCFA Institute Board of Governors

fbetw 13 January 2012; 9:5:34

Foreword xiii

fbetw 13 January 2012; 9:5:34

ACKNOWLEDGMENTS

We would like to thank the many individuals who played important roles in producingthis book.

The standards and orientation of the second edition are a continuation of those set forthe first edition. Robert R. Johnson, CFA, former senior managing director of CFA Institute,supported the creation of custom curriculum readings in this area and their revision. DennisW. McLeavey, CFA, initiated the project during his term as head of Curriculum Develop-ment. Christopher B. Wiese, CFA, oversaw final organization, writing, and editing of the firstedition for the CFA curriculum.

First edition manuscript reviewers were Jean-Francois Bureau, CFA, Sean D. Carr,Rosita P. Chang, CFA, Jacques R. Gagne, CFA, Gene C. Lai, Asjeet S. Lamba, CFA, PimanLimpaphayom, CFA, and Zhiyi Song, CFA. Chapter authors Pamela P. Drake, CFA, andJohn D. Stowe, CFA, provided notable assistance at critical junctures. We thank all of theabove for their excellent and detailed work.

For this second edition, Gregory Noronha, CFA, was added to the author lineup.Second edition manuscript reviewers were Evan Ashcraft, CFA, David K. Chan, CFA, LeeDunham, CFA, Philip Fanara, CFA, Usman Hayat, CFA, William Jacobson, CFA, FrankLaatsch, CFA, Murli Rajan, CFA, Knut Reinertz, CFA, Sanjiv Sabherwal, Sandeep Singh,CFA, Frank Smudde, CFA, and Peter Stimes, CFA. Jerald E. Pinto, CFA, director, Cur-riculum Projects, had primary responsibility for the delivery of the revised chapters.

flast 13 January 2012; 9:8:54

xv

flast 13 January 2012; 9:8:54

ABOUT THE CFA INSTITUTEINVESTMENT SERIES

CFA Institute is pleased to provide you with the CFA Institute Investment Series, whichcovers major areas in the field of investments. We provide this best-in-class series for the samereason we have been chartering investment professionals for more than 45 years: to lead theinvestment profession globally by setting the highest standards of ethics, education, andprofessional excellence.

The books in the CFA Institute Investment Series contain practical, globally relevantmaterial. They are intended both for those contemplating entry into the extremely com-petitive field of investment management as well as for those seeking a means of keepingtheir knowledge fresh and up to date. This series was designed to be user friendly andhighly relevant.

We hope you find this series helpful in your efforts to grow your investment knowledge,whether you are a relatively new entrant or an experienced veteran ethically bound to keep upto date in the ever-changing market environment. As a long-term, committed participant inthe investment profession and a not-for-profit global membership association, CFA Instituteis pleased to provide you with this opportunity.

THE TEXTS

One of the most prominent texts over the years in the investment management industry hasbeen Maginn and Tuttle’s Managing Investment Portfolios: A Dynamic Process. The thirdedition updates key concepts from the 1990 second edition. Some of the more experiencedmembers of our community own the prior two editions and will add the third edition to theirlibraries. Not only does this seminal work take the concepts from the other readings and putthem in a portfolio context, but it also updates the concepts of alternative investments,performance presentation standards, portfolio execution, and, very importantly, individualinvestor portfolio management. Focusing attention away from institutional portfolios andtoward the individual investor makes this edition an important and timely work.

Quantitative Investment Analysis focuses on some key tools that are needed by today’sprofessional investor. In addition to classic time value of money, discounted cash flowapplications, and probability material, there are two aspects that can be of value over tra-ditional thinking.

The first involves the chapters dealing with correlation and regression that ultimatelyfigure into the formation of hypotheses for purposes of testing. This gets to a critical skill thatchallenges many professionals: the ability to distinguish useful information from the over-whelming quantity of available data. For most investment researchers and managers, their

flast 13 January 2012; 9:8:54

xvii

analysis is not solely the result of newly created data and tests that they perform. Rather, theysynthesize and analyze primary research done by others. Without a rigorous manner by whichto explore research, you cannot understand good research or have a basis on which to evaluateless rigorous research.

Second, the last chapter of Quantitative Investment Analysis covers portfolio concepts andtakes the reader beyond the traditional capital asset pricing model (CAPM) type of tools andinto the more practical world of multifactor models and arbitrage pricing theory.

Fixed Income Analysis has been at the forefront of new concepts in recent years, and thisparticular text offers some of the most recent material for the seasoned professional who is nota fixed-income specialist. The application of option and derivative technology to the once-staid province of fixed income has helped contribute to an explosion of thought in this area.Professionals have been challenged to stay up to speed with credit derivatives, swaptions,collateralized mortgage securities, mortgage-backed securities, and other vehicles, and thisexplosion of products has strained the world’s financial markets and tested central banks toprovide sufficient oversight. Armed with a thorough grasp of the new exposures, the pro-fessional investor is much better able to anticipate and understand the challenges our centralbankers and markets face.

International Financial Statement Analysis is designed to address the ever-increasingneed for investment professionals and students to think about financial statement analysisfrom a global perspective. The text is a practically oriented introduction to financial state-ment analysis that is distinguished by its combination of a true international orientation, astructured presentation style, and abundant illustrations and tools covering concepts asthey are introduced in the text. The authors cover this discipline comprehensively andwith an eye to ensuring the reader’s success at all levels in the complex world of financialstatement analysis.

Equity Asset Valuation is a particularly cogent and important resource for anyone involvedin estimating the value of securities and understanding security pricing. A well-informedprofessional knows that the common forms of equity valuation—dividend discount modeling,free cash flow modeling, price/earnings modeling, and residual income modeling—can all bereconciled with one another under certain assumptions. With a deep understanding of theunderlying assumptions, the professional investor can better understand what other investorsassume when calculating their valuation estimates. This text has a global orientation, includingemerging markets. The second edition provides new coverage of private company valuationand expanded coverage of required rate of return estimation.

Investments: Principles of Portfolio and Equity Analysis provides an accessible yet rigorousintroduction to portfolio and equity analysis. Portfolio planning and portfolio managementare presented within a context of up-to-date, global coverage of security markets, trading, andmarket-related concepts and products. The essentials of equity analysis and valuation areexplained in detail and profusely illustrated. The book includes coverage of practitioner-important but often neglected topics, such as industry analysis. Throughout, the focus is onthe practical application of key concepts with examples drawn from both emerging anddeveloped markets. Each chapter affords the reader many opportunities to self-check his orher understanding of topics. In contrast to other texts, the chapters are collaborations ofrespected senior investment practitioners and leading business school teachers from aroundthe globe. By virtue of its well-rounded, expert, and global perspectives, the book should beof interest to anyone who is looking for an introduction to portfolio and equity analysis.

The New Wealth Management: The Financial Advisor’s Guide to Managing and InvestingClient Assets is an updated version of Harold Evensky’s mainstay reference guide for wealth

flast 13 January 2012; 9:8:54

xviii About the CFA Institute Investment Series

managers. Harold Evensky, Stephen Horan, and Thomas Robinson have updated the coretext of the 1997 first edition and added an abundance of new material to fully reflect today’sinvestment challenges. The text provides authoritative coverage across the full spectrum ofwealth management and serves as a comprehensive guide for financial advisors. The bookexpertly blends investment theory and real-world applications and is written in the samethorough but highly accessible style as the first edition.

Corporate Finance: A Practical Approach is a solid foundation for those looking to achievelasting business growth. In today’s competitive business environment, companies must findinnovative ways to enable rapid and sustainable growth. This text equips readers with thefoundational knowledge and tools for making smart business decisions and formulatingstrategies to maximize company value. It covers everything from managing relationshipsbetween stakeholders to evaluating merger and acquisition bids, as well as the companiesbehind them. The second edition of the book preserves the hallmark conciseness of the firstedition while expanding coverage of dividend policy, share repurchases, and capital structure.

Through extensive use of real-world examples, readers will gain critical perspective intointerpreting corporate financial data, evaluating projects, and allocating funds in ways thatincrease corporate value. Readers will gain insights into the tools and strategies used inmodern corporate financial management.

flast 13 January 2012; 9:8:54

About the CFA Institute Investment Series xix

flast 13 January 2012; 9:8:54

CHAPTER 1CORPORATE GOVERNANCE

Rebecca T. McEnally, CFANew Bern, North Carolina, U.S.A.

Kenneth KimBuffalo, New York, U.S.A.

LEARNING OUTCOMES

After completing this chapter, you will be able to do the following:

! Explain corporate governance, describe the objectives and core attributes of an effectivecorporate governance system, and evaluate whether a company’s corporate governance hasthose attributes.

! Compare major business forms and describe the conflicts of interest associated with each.! Explain conflicts that arise in agency relationships, including manager-shareholder conflicts

and director-shareholder conflicts.! Describe responsibilities of the board of directors and explain qualifications and core

competencies that an investment analyst should look for in the board of directors.! Explain effective corporate governance practice as it relates to the board of directors, and

evaluate the strengths and weaknesses of a company’s corporate governance practice.! Describe elements of a company’s statement of corporate governance policies that

investment analysts should assess.! Explain the valuation implications of corporate governance.

1. INTRODUCTION

The modern corporation is a very efficient and effective means of raising capital, obtainingneeded resources, and generating products and services. These and other advantages havecaused the corporate form of business to become the dominant one in many countries. Thecorporate form, in contrast to other business forms, frequently involves the separation ofownership and control of the assets of the business. The ownership of the modern, publiccorporation is typically diffuse; it has many owners, most with proportionally small stakes in

1

c01 13 January 2012; 9:5:40

the company, who are distant from, and often play no role in, corporate decisions. Profes-sional managers control and deploy the assets of the corporation. This separation of own-ership (shareholders) and control (managers) may result in a number of conflicts of interestbetween managers and shareholders. Conflicts of interest can also arise that affect creditors aswell as other stakeholders such as employees and suppliers. In order to remove or at leastminimize such conflicts of interest, corporate governance structures have been developed andimplemented in corporations. Specifically, corporate governance is the system of principles,policies, procedures, and clearly defined responsibilities and accountabilities used by stake-holders to overcome the conflicts of interest inherent in the corporate form.

The failure of a company to establish an effective system of corporate governancerepresents a major operational risk to the company and its investors.1 Corporate governancedeficiencies may even imperil the continued existence of a company. Consequently, tounderstand the risks inherent in an investment in a company, it is essential to understand thequality of the company’s corporate governance practices. It is also necessary to continuallymonitor a company’s practices, because changes in management, the composition of its boardof directors, the company’s competitive and market conditions, or mergers and acquisitions,can affect them in important ways.

A series of major corporate collapses in North America, Europe, and Asia, nearly all ofwhich involved the failure or direct override by managers of corporate governance systems,have made it clear that strong corporate governance structures are essential to the efficient andeffective functioning of companies and the financial markets in which they operate. Investorslost great amounts of money in the failed companies. The collapses weakened the trust andconfidence essential to the efficient functioning of financial markets worldwide.

Legislators and regulators responded to the erosion of trust by introducing strong newregulatory frameworks. These measures are intended to restore the faith of investors incompanies and the markets, and, very importantly, to help prevent future collapses. Never-theless, the new regulations did not address all outstanding corporate governance problemsand were not uniform across capital markets. Thus, we may expect corporate governance-related laws and regulations to further evolve.

The chapter is organized as follows: Section 2 presents the objectives of corporate gov-ernance systems and the key attributes of effective ones. Section 3 addresses forms of businessand conflicts of interest, and Section 4 discusses two major sources of governance problems.In Section 5 we discuss standards and principles of corporate governance, providing threerepresentative sets of principles from current practice. Section 6 addresses environmental,social, and governance factors. Section 7 touches on the valuation implications of the qualityof corporate governance, and Section 8 summarizes the chapter.

2. CORPORATE GOVERNANCE: OBJECTIVESAND GUIDING PRINCIPLES

The modern corporation is subject to a variety of conflicts of interest. This fact leads to thefollowing two major objectives of corporate governance:

1An operational risk is the risk of loss from failures in a company’s systems and procedures or fromexternal events.

2 Corporate Finance

c01 13 January 2012; 9:5:40

1. To eliminate or mitigate conflicts of interest, particularly those between managers andshareholders.

2. To ensure that the assets of the company are used efficiently and productively and in thebest interests of its investors and other stakeholders.

How then can a company go about achieving those objectives? The first point is that itshould have a set of principles and procedures sufficiently comprehensive to be called acorporate governance system. No single system of effective corporate governance applies to allfirms in all industries worldwide. Different industries and economic systems, legal and reg-ulatory environments, and cultural differences may affect the characteristics of an effectivecorporate governance system for a particular company. However, there are certain char-acteristics that are common to all sound corporate governance structures. The core attributesof an effective corporate governance system are:

! Delineation of the rights of shareholders and other core stakeholders.! Clearly defined manager and director governance responsibilities to stakeholders.! Identifiable and measurable accountabilities for the performance of the responsibilities.! Fairness and equitable treatment in all dealings betweenmanagers, directors, and shareholders.! Complete transparency and accuracy in disclosures regarding operations, performance, risk,

and financial position.

These core attributes form the foundation for systems of good governance, as well as forthe individual principles embodied in such systems. Investors and analysts should determinewhether companies in which they may be interested have these core attributes.

3. FORMS OF BUSINESS AND CONFLICTS OF INTEREST

The goal of for-profit businesses in any society is simple and straightforward: to maximizetheir owners’ wealth. This can be achieved through strategies that result in long-term growthin sales and profits. However, pursuing wealth maximization involves taking risks. A businessitself is risky for a variety of reasons. For example, there may be demand uncertainty for itsproducts and/or services, economic uncertainty, and competitive pressures. Financial risk ispresent when a business must use debt to finance operations. Thus, continued access tosufficient capital is an important consideration and risk for businesses. These risks, andthe inherent conflicts of interests in businesses, increase the need for strong corporategovernance.

A firm’s ability to obtain capital and to control risk is perhaps most influenced by themanner in which it is organized. Three of the predominant forms of business globallyare the sole proprietorship, the partnership, and the corporation. Hybrids of these threeprimary business forms also exist, but we do not discuss them here because they are simplycombinations of the three main business forms. With regard to the three primary businessforms, each has different advantages and disadvantages. We will discuss each of them, theconflicts of interest that can arise in each, and the relative need for strong corporate gover-nance associated with each form. However, a summary of the characteristics is provided inExhibit 1-1.

Chapter 1 Corporate Governance 3

c01 13 January 2012; 9:5:40

EXHIBIT 1-1 Comparison of Characteristics of Business Forms

Characteristic Sole Proprietorship Partnership Corporation

Ownership Sole owner Multiple owners Unlimited ownership

Legal requirementsand regulation

Few; entity easilyformed

Few; entity easilyformed

Numerous legalrequirements

Legal distinction betweenowner and business

None None Legal separation betweenowners and business

Liability Unlimited Unlimited but sharedamong partners

Limited

Ability to raise capital Very limited Limited Nearly unlimited

Transferability ofownership

Nontransferable(except by sale ofentire business)

Nontransferable Easily transferable

Owner expertise inbusiness

Essential Essential Unnecessary

3.1. Sole Proprietorships

The sole proprietorship is a business owned and operated by a single person. The owner ofthe local cleaner, restaurant, beauty salon, or fruit stand is typically a sole proprietor.Generally, there are few, if any, legal formalities involved in establishing a sole proprietorshipand they are relatively easy to start. In many jurisdictions, there are few, if any, legal dis-tinctions between the sole proprietor and the business. For example, tax liabilities and relatedfiling requirements for sole proprietorships are frequently set at the level of the sole pro-prietor. Legitimate business expenses are simply deducted from the sole proprietor’s taxableincome.

Sole proprietorships are the most numerous form of business worldwide, representing,for example, approximately 70 percent of all businesses in the United States, by number.2

However, because they are usually small-scale operations, they represent the smallest amountof market capitalization in many markets. Indeed, the difficulties of the sole proprietor inraising large amounts of capital, coupled with unlimited liability and lack of transferability ofownership, are serious impediments to the growth of a sole proprietorship.

From the point of view of corporate governance, the sole proprietorship presents fewerrisks than the corporation because the manager and the owner are one and the same. Indeed,the major corporate governance risks are those faced by creditors and suppliers of goods andservices to the business. These stakeholders are in a position to be able to demand the typesand quality of information that they need to evaluate risks before lending money to thebusiness or providing goods and services to it. In addition, because they typically maintaindirect, recurring business relations with the companies, they are better able to monitor thecondition and risks of the business, and to control their own exposure to risk. Consequently,we will not consider sole proprietorships further in this chapter.

2Megginson (1997), 40.

4 Corporate Finance

c01 13 January 2012; 9:5:40

3.2. Partnerships

A partnership, which is composed of more than one owner/manager, is similar to a soleproprietorship. For the most part, partnerships share many of the same advantages anddisadvantages as the sole proprietorship. Two obvious advantages of a partnership over a soleproprietorship are the pooling together of financial capital of the partners and the sharing ofbusiness risk among them. However, even these advantages may not be as important as thepooling together of service-oriented expertise and skill, especially for larger partnerships.Some very large international partnerships operate in such fields as real estate, law, investmentbanking, architecture, engineering, advertising, and accounting. Note also that larger part-nerships may enjoy competitive and economy-of-scale benefits over sole proprietorships.

Partners typically overcome conflicts of interest internally by engaging in partnershipcontracts specifying the rights and responsibilities of each partner. Conflicts of interestwith those entities outside the partnership are similar to those for the sole proprietorship andare dealt with in the same way. Hence, we will not consider these conflicts further in thischapter.

3.3. Corporations

Corporations represent less than 20 percent of all businesses in the United States but generateapproximately 90 percent of the country’s business revenue.3 The percentage is lowerelsewhere, but growing. The corporation is a legal entity, and has rights similar to those of aperson. For example, a corporation is permitted to enter into contracts. The chief officers ofthe corporation, the executives or top managers, act as agents for the firm and are legallyentitled to authorize corporate activities and to enter into contracts on behalf of the business.

There are several important and striking advantages of the corporate form of business.First, corporations can raise very large amounts of capital by issuing either stocks or bonds tothe investing public. A corporation can grant ownership stakes, common stock, to individualinvestors in exchange for cash or other assets. Similarly, it can borrow money, for example,bonds or other debt from individual or institutional investors, in exchange for interest pay-ments and a promise to pay back the principal of the loan. Shareholders are the owners of thecorporation, and any profits that the corporation generates accrue to the shareholders.

A second advantage is that corporate owners need not be experts in the industry ormanagement of the business, unlike the owners of sole proprietorships and partnerships wherebusiness expertise is essential to success. Any individual with sufficient money can own stock.This has benefits to both the business and the owners. The business can seek capital frommillions of investors, not only in domestic markets but worldwide.

Among the most important advantages of the corporate form is that stock ownership iseasily transferable. Transferability of shares allows corporations to have unlimited life. A finaland extremely important advantage is that shareholders have limited liability. That is, theycan lose only the money they have invested, nothing more.

The corporate form of business has a number of disadvantages, however. For example,because many corporations have thousands or even millions of nonmanager owners, they aresubject to more regulation than are partnerships or sole proprietorships. While regulationserves to protect shareholders, it can also be costly to shareholders as well. For example, thecorporation must hire accountants and lawyers to deal with accounting and other legal

3Megginson (1997).

Chapter 1 Corporate Governance 5

c01 13 January 2012; 9:5:40

documents to comply with regulations. Perhaps the most significant disadvantage with thecorporation (and the one most critical to corporate governance) is the difficulty that share-holders have in monitoring management and the firm’s operations. As a sole proprietor of asmall business, the owner will be able to directly oversee such day-to-day business concerns asinventory levels, product quality, expenses, and employees. However, it is impossible for ashareholder of a large corporation such as General Motors or International Business Machinesto monitor business activities and personnel, and to exert any control rights over the firm. Infact, a shareholder of a large firm may not even feel like an owner in the usual sense, especiallybecause corporations are owned by so many other shareholders, and because most owners of alarge public corporation hold only a relatively small stake in it.

Agency relationships arise when someone, an agent, acts on behalf of another person,the principal. In a corporation, managers are the agents who act on behalf of the owners, theshareholders. If a corporation has in place a diligent management team that works in the bestinterests of its shareholders and other stakeholders, then the problem of passive shareholdersand bondholders becomes a nonissue. In real life, unfortunately, management may not alwayswork in the stakeholders’ best interests. Managers may be tempted to see to their own well-being and wealth at the expense of their shareholders and others to whom they owe a fiduciaryduty. This is known as an agency problem, or the principal–agent problem. The money ofshareholders, the principals, is used and managed by agents, the managers, who promise thatthe firm will pursue wealth-maximizing business activities. However, there are potentialproblems with these relationships, which we will discuss next.

4. SPECIFIC SOURCES OF CONFLICT:AGENCY RELATIONSHIPS

Conflicts among the various constituencies in corporations have the potential to cause pro-blems in the relationships among managers, directors, shareholders, creditors, employees, andsuppliers. However, we will concentrate here on the relationships between (1) managers andshareholders, and (2) directors and shareholders. These two relationships are the primaryfocus of most systems of corporate governance. However, to the extent that strong corporategovernance structures are in place and effective in companies, the agency conflicts amongother stakeholders are mitigated as well. For example, managers are responsible for maxi-mizing the wealth of the shareholders and minimizing waste (including excessive compen-sation and perquisite consumption). To the extent that managers do so, the interests ofemployees and suppliers are more likely to be met because the probability increases thatsufficient funds will be available for payment of salaries and benefits, as well as for goods andservices. In this section, we will describe these agency relationships, discuss the problemsinherent in each, and will illustrate these agency problems with real-world examples. Anunderstanding of the nature of the conflicts in each relationship is essential to a full under-standing of the importance of the provisions in codes of corporate governance.

4.1. Manager–Shareholder Conflicts

From the point of view of investors, the manager–shareholder relationship is the most criticalone. It is important to recognize that firms and their managers, the shareholders’ agents,obtain operating and investing capital from the shareholders, the owners, in two ways. First,although shareholders have a 100 percent claim on the firm’s net income, the undistributed

6 Corporate Finance

c01 13 January 2012; 9:5:40

net income (the earnings remaining after the payment of dividends) is reinvested in thecompany. We normally term this reinvested income retained earnings. Second, the firm canissue stock to obtain the capital, either through an initial public offering (IPO) if the firm iscurrently privately owned, or through a seasoned equity offering (SEO) if the firm already hasshares outstanding. By whatever means the firm obtains equity capital, shareholders entrustmanagement to use the funds efficiently and effectively to generate profits and maximizeinvestors’ wealth.

However, although the manager is responsible for advancing the shareholder’s bestinterests, this may not happen. For example, management may use funds to try to expand thesize of the business to increase their job security, power, and salaries without consideration ofthe shareholders’ interests. In addition, managers may also grant themselves numerous andexpensive perquisites, which are treated as ordinary business expenses. Managers enjoy thesebenefits, and shareholders bear the costs. This is a serious agency problem and, unfortunately,there are a number of recent real-world examples of their occurrence in corporations.

Managers also may make other business decisions, such as investing in highly risky ven-tures, that benefit themselves but that may not serve the company’s investors well. For example,managers who hold substantial amounts of executive stock options will receive large benefitsif risky ventures pay off, but will not suffer losses if the ventures fail. By contrast, managerswhose wealth is closely tied to the company and who are therefore not well diversified maychoose to not invest in projects with a positive expected net present value because of excessiverisk aversion. The checks and balances in effective corporate governance systems are designedto reduce the probability of such practices.

The cases of Enron (bankruptcy filing: 2001, in the United States) and Tyco (resignation ofCEO: 2002, in the United States) make clear that in the absence of the checks and balancesof strong and effective corporate governance systems, investors and others cannot necessarilyrely uponmanagers to serve as stewards of the resources entrusted to them. Example 1-1, dealingwith Enron, illustrates the problems that can ensue from a lack of commitment to a corporategovernance system. Example 1-2, dealing with Tyco, illustrates a case in which there wereinadequate checks and balances to the power of a CEO.

EXAMPLE 1-1 Corporate Governance Failure (1)

Enron was one of the world’s largest energy, commodities, and services companies.However, it is better known today as a classic example of how the conflicts of interestbetween shareholders and managers can harm even major corporations and theirshareholders. Enron executives, with the approval of members of the board of directors,overrode provisions in Enron’s code of ethics and corporate governance system thatforbade any practices involving self-dealing by executives. Specifically, Enron’s chieffinancial officer set up off-shore partnerships in which he served as general partner. Asan Enron executive, he was able to make deals with these partnerships on behalf ofEnron. As a general partner of the partnerships, he received the enormous fees that thedeals generated.4

4See Powers, Troubh, and Winokur (2002).

Chapter 1 Corporate Governance 7

c01 13 January 2012; 9:5:40

The role of complete transparency in sound corporate governance, including under-standable and accurate financial statements, cannot be overestimated. Without full infor-mation, investors and other stakeholders are unable to evaluate the company’s financialposition and riskiness, whether the condition is improving or deteriorating, and whetherinsiders are aggrandizing themselves, or making poor business decisions, to the detriment oflong-term investors.

The partnerships served other useful purposes. For example, they made it possibleto hide billions of dollars in Enron debt off of the company’s balance sheet, andgenerated artificial profits for Enron. Thus, disclosure of the company’s rapidly dete-riorating financial condition was delayed, preventing investors and creditors fromobtaining information critical to the valuation and riskiness of their securities. At thesame time, Enron executives were selling their own stock in the company.

These egregious breaches of good governance harmed both Enron’s outsideshareholders and their creditors. The bonds were becoming riskier but the creditorswere not informed of the deteriorating prospects. The exorbitant fees the executivespaid themselves came out of the shareholders’ earnings, earnings that were alreadyoverstated by the artificial profits. Investors did not receive full information about theproblems in the company until well after the collapse and the company’s bankruptcyfiling, by which time their stock had lost essentially all of its value.

Most, if not all, of the core attributes of good governance were violated by Enron’smanagers, but especially the responsibility to deal fairly with all stakeholders, includinginvestors and creditors, and to provide full transparency of all material information on atimely basis.

EXAMPLE 1-2 Corporate Governance Failure (2)

Tyco provides another well-known example of a corporate governance failure. TheCEO of Tyco used corporate funds to buy home decorating items, including a $17,000traveling toilette box, a $445 pincushion, and a $15,000 umbrella stand. He alsoborrowed money from the company’s employee loan program to buy $270 million-worth of yachts, art, jewelry, and vacation estates. Then, in his capacity as CEO, heforgave the loan. All told, the CEO may have looted the firm, and thereby its share-holders, of over $600 million.5

It is instructive that in court proceedings in the Tyco case, the CEO and hisrepresentatives have not argued that he did not do these things, but rather that it wasnot illegal for him to do so. Tyco is a striking example of excessive perquisite con-sumption by a CEO.

5Maremont and Cohen (2002), A1.

8 Corporate Finance

c01 13 January 2012; 9:5:41

Two additional cases illustrate how false, misleading, or incomplete corporate disclosuremay harm investors and other stakeholders.

The severity of the agency problems of the companies discussed in Examples 1-1 through1-4 does not represent the norm, although the potential for serious conflicts of interestbetween shareholders and managers is inherent in the modern corporation. Strong corporategovernance systems provide mechanisms for monitoring managers’ activities, rewarding goodperformance and disciplining those in a position of responsibility for the company to makesure they act in the interests of the company’s stakeholders.

EXAMPLE 1-3 Corporate Governance Failure (3)

The Italian firm, Parmalat, was one of the world’s largest dairy foods suppliers. Thefounders and top executives of Parmalat were accused of fictitiously reporting theexistence of a $4.9 billion bank account so that the company’s enormous liabilitieswould appear less daunting.6 By hiding the true financial condition of the firm, theexecutives were able to continue borrowing. The fraud perpetrated by Parmalat’s largestshareholders and executives hurt Parmalat’s creditors as well as the shareholders. Par-malat eventually defaulted on a $185 million bond payment in November 2003 andthe company collapsed shortly thereafter.

EXAMPLE 1-4 Corporate Governance Failure (4)

During the late 1990s, Adelphia, the fifth-largest provider of cable entertainment in theUnited States, and the company’s founders embarked on an aggressive acquisitioncampaign to increase the size of the company. During this time, the size of Adelphia’sdebt more than tripled from $3.5 billion to $12.6 billion. However, the founders alsoarranged a $2.3 billion personal loan, which Adelphia guaranteed, but this arrangementwas not fully disclosed to Adelphia’s other stakeholders.7 In addition, it is alleged thatfictitious transactions were recorded to boost accounting profits.8 These actions byAdelphia’s owners were harmful to all of Adelphia’s nonfounder stakeholders, includinginvestors and creditors. The company collapsed in bankruptcy in 2002.

6Edmondson (2004).7Nofsinger and Kim (2003), 60–61.8Markon and Frank (2002), A3.

Chapter 1 Corporate Governance 9

c01 13 January 2012; 9:5:41

4.2. Director–Shareholder Conflicts

Corporate governance systems rely on a system of checks and balances between the managersand investors in which the board of directors plays a critical role. The purpose of boards ofdirectors in modern corporations is to provide an intermediary between managers and theowners, the shareholders. Members of the board of directors serve as agents for the owners,the shareholders, a mechanism designed to represent the investors and to ensure that theirinterests are being well served. This intermediary generally is responsible for monitoring theactivities of managers, approving strategies and policies, and making certain that these serveinvestors’ interests. The board is also responsible for approving mergers and acquisitions,approving audit contracts and reviewing the audit and financial statements, setting managers’compensation including any incentive or performance awards, and disciplining or replacingpoorly performing managers.

The conflict between directors and shareholders arises when directors come to identifywith the managers’ interests rather than those of the shareholders. This can occur when theboard is not independent, for example, or when the members of the board have business orpersonal relationships with the managers that bias their judgment or compromise their dutiesto the shareholders. If members of the board have consulting agreements with the company,serve as major lenders to the firm, are members of the manager’s family, or are from thecircle of close friends, their objectivity may be called into question. Many corporations havebeen found to have inter-linked boards. For example, one or more senior managers fromone firm may serve as directors in the companies of their own board members, frequentlyon compensation committees. Another ever-present problem is the frequently overly generouscompensation paid to directors for their services. Excessive compensation may incline directorsto accommodate the wishes of management rather than attend to the concerns of investors.

All of the examples cited in this section involve compliant or less than independent boardmembers. In Section 5, we formulate the most important points to check in evaluating acompany’s corporate governance system.

5. CORPORATE GOVERNANCE EVALUATION

An essential component of the analysis of a company and its risk is a review of the quality ofits corporate governance system. This evaluation requires an assessment of issues relating tothe board of directors, managers, and shareholders. Ultimately, the long-term performance ofa company is dependent upon the quality of managers’ decisions and their commitment toapplying sound management practice. However, as one group concerned with the issuesobserves, “by analyzing the state of corporate governance for a given company, an analyst orshareholder may ascertain whether the company is governed in a manner that produces bettermanagement practices, promotes higher returns on shareholder capital, or if there is a gov-ernance and/or management problem which may impair company performance.”9

In the following sections we provide a set of guidelines for evaluating the quality ofcorporate governance in a company. We reiterate that there is no single system of governancethat is appropriate for all companies in all industries worldwide. However, this core set ofglobal best practices is being applied in financial markets in Europe, Asia, and North America.They represent a standard by which corporate practices may be evaluated.

9New York Society of Securities Analysts (2003).

10 Corporate Finance

c01 13 January 2012; 9:5:41

The information and corporate disclosure available in a specific jurisdiction will varywidely. However, most large financial markets and, increasingly, smaller ones require asubstantial amount of information be provided about companies’ governance structures andpractices. In addition, a few regulatory jurisdictions will require a subset of the criteria weshall give as part of registration, exchange listing, or other requirements.

The analyst should begin by carefully reviewing the requirements in effect for thecompany. Information is generally available in the company’s required filings with reg-ulators. For example, in the United States, such information is provided in the 10-K report,the annual report, and the Proxy Statement (SEC Form DEF 14A). All of these are filedwith the U.S. Securities and Exchange Commission (U.S. SEC), are available on the U.S.SEC website, usually are available on the company’s website, and are provided by thecompany to current investors as well as on request. In Europe, the company’s annual reportprovides some information. However, in an increasing number of EU countries, companiesare required to provide a report on corporate governance. This report typically will provideinformation on board activities and decisions, whether the company has abided by itsrelevant national code, and explain why it departed from the code, if it has. In addition,the announcement of the company’s annual general meeting should disclose the issues on theagenda that are subject to shareholder vote. The specific sources of information will differ byjurisdiction and company.

5.1. The Board of Directors

Boards of directors are a critical part of the system of checks and balances that lie at the heartof corporate governance systems. Board members, both individually and as a group, have theresponsibility to:

! Establish corporate values and governance structures for the company to ensure that thebusiness is conducted in an ethical, competent, fair, and professional manner.

! Ensure that all legal and regulatory requirements are met and complied with fully and in atimely fashion.

! Establish long-term strategic objectives for the company with a goal of ensuring that thebest interests of shareholders come first and that the company’s obligations to others aremet in a timely and complete manner.

! Establish clear lines of responsibility and a strong system of accountability and performancemeasurement in all phases of a company’s operations.

! Hire the chief executive officer, determine the compensation package, and periodicallyevaluate the officer’s performance.

! Ensure that management has supplied the board with sufficient information for it to befully informed and prepared to make the decisions that are its responsibility, and to be ableto adequately monitor and oversee the company’s management.

! Meet frequently enough to adequately perform its duties, and meet in extraordinary sessionas required by events.

! Acquire adequate training so that members are able to adequately perform their duties.

Depending upon the nature of the company and the industries within which the com-pany operates, these responsibilities will vary; however, these general obligations are commonto all companies.

Chapter 1 Corporate Governance 11

c01 13 January 2012; 9:5:41

In summarizing the duties and needs of boards of directors, The Corporate Governance ofListed Companies: A Manual for Investors10 states:

Board members owe a duty to make decisions based on what ultimately is best for thelong-term interests of shareowners. In order to do this effectively, board membersneed a combination of three things: independence, experience and resources.

First, a board should be composed of at least a majority of independentboard members with the autonomy to act independently from management. Boardmembers should bring with them a commitment to take an unbiased approach inmaking decisions that will benefit the company and long-term shareowners, rather thansimply voting with management. Second, board members who have appropriateexperience and expertise relevant to the Company’s business are best able to evaluatewhat is in the best interests of shareowners. Depending on the nature of the business,thismay require specialized expertise by at least some boardmembers.Third, there needto be internal mechanisms to support the independent work of the board, including theauthority to hire outside consultants without management’s intervention or approval.This mechanism alone provides the board with the ability to obtain expert help inspecialized areas, to circumvent potential areas of conflict with management, and topreserve the integrity of the board’s independent oversight function. [Emphasis added]

In the following sections we detail the attributes of the board that an investor orinvestment analyst must assess.

5.1.1. Board Composition and IndependenceThe board of directors of a corporation is established for the primary purpose of serving thebest interests of the outside shareholders in the company. Other stakeholders includingemployees, creditors, and suppliers are usually in a more powerful position to oversee theirinterests in the company than are shareholders. The millions of outside investors cannot,individually or collectively, monitor, oversee, and approve management’s strategies andpolicies, performance, and compensation and consumption of perquisites.

The objectives of the board are to see that company assets are used in the best long-terminterests of shareholders and that management strategies, plans, policies, and practices aredesigned to achieve this objective. In a recent amendment to the Investment Company Act of1940 rules, the U.S. SEC argues that a board must be “an independent force in [company]affairs rather than a passive affiliate of management. Its independent directors must bring tothe boardroom a high degree of rigor and skeptical objectivity to the evaluation of [company]managements and its plans and proposals, particularly when evaluating conflicts of interest.”11

Similarly, the Corporate Governance Handbook12 observes:

Board independence is essential to a sound governance structure. Without inde-pendence there can be little accountability. In the words of Professor Jeffrey Son-nenfeld of Yale University, “The highest performing companies have extremelycontentious boards that regard dissent as an obligation and that treat no subject asundiscussable.”

10The Corporate Governance of Listed Companies: A Manual for Investors (2005), 11.11Amendments to Rules Governing the Investment Company Act of 1940, 17 CFR Part 270 (July 2004): 3.12New York Society of Securities Analysts (2003), 3.

12 Corporate Finance

c01 13 January 2012; 9:5:41

Clearly, for members who are appointed to the board to be in a position to best performtheir fiduciary responsibilities to shareholders, at a minimum a majority of the members mustbe independent of management. However, global best practice now recommends that at leastthree-quarters of the board members should be independent.

Some experts in corporate governance have argued that all members of the board shouldbe independent, eliminating the possibility of any senior executives serving on the board.Those who hold this position argue that the presence of managers in board deliberations maywork to the detriment of the best interests of investors and other shareholders by intimidatingthe board or otherwise limiting debate and full discussion of important matters. Others arguethat with appropriate additional safeguards, such potential problems can be overcome to thebenefit of all stakeholders.

Independence is difficult to evaluate. Factors that often indicate a lack of independenceinclude:

! Former employment with the company, including founders, executives, or other employees.! Business relationships, for example, prior or current service as outside counsel, auditors, or

consultants, or business interests involving contractual commitments and obligations.! Personal relationships, whether familial, friendship, or other affiliations.! Interlocking directorships, a director of another company whose independence might be

impaired by the relationship with the other board or company, particularly if the directorserves on interlocking compensation committees.

! Ongoing banking or other creditor relationships.

Information on the business and other relationships of board members as well asnominees for the board may be obtained from regulatory filings in most jurisdictions. Forexample, in the United States, such information is required to be provided in the ProxyStatement, SEC Form DEF 14A, sent to shareholders and filed with the SEC prior to share-holder meetings.

5.1.2. Independent Chairman of the BoardMany, if not most, corporate boards now permit a senior executive of a corporation to serve asthe chairman of the board of directors. However, corporate governance experts do not regardsuch an arrangement to be in the best interests of the shareholders of the company. As theU.S. SEC observes,

This practice may contribute to the [company’s] ability to dominate the actions ofthe board of directors. The chairman of a . . . board can largely control the board’sagenda, which may include matters not welcomed by the [company’s manage-ment] . . . Perhaps more important, the chairman of the board can have a sub-stantial influence on the . . . boardroom’s culture. The boardroom culture canfoster (or suppress) the type of meaningful dialogue between . . . management andindependent directors that is critical for healthy . . . governance. It can support (ordiminish) the role of the independent directors in the continuous, active engagementof . . . management necessary for them to fulfill their duties. A boardroom cultureconducive to decisions favoring the long-term interest of . . . shareholders may bemore likely to prevail when the chairman does not have the conflicts of interestinherent in his role as an executive of the [company]. Moreover, a . . . board may be

Chapter 1 Corporate Governance 13

c01 13 January 2012; 9:5:41

more effective when negotiating with the [company] over matters such as the[compensation] if it were not at the same time led by an executive of the [company]with whom it is negotiating.13

Not all market participants agree with this view. Many corporate managers argue thatit is essential for efficient and effective board functioning that the chairman be the seniorexecutive in the company. They base their arguments on the proposition that only suchan executive has the knowledge and experience necessary to provide needed informationto the board on questions on strategy, policy, and the operational functioning of thecompany. Critics of this position counter that it is incumbent upon corporate manage-ment to provide all such necessary information to the board. Indeed, many argue that thisobligation is the sole reason that one or more corporate managers serve as members of theboard.

Whether the company has separate positions for the chief executive and chairman of theboard can be determined readily from regulatory filings of the company. If the positions arenot separate, an investor may doubt that the board is operating efficiently and effectively in itsmonitoring and oversight of corporate operations, and that decisions made are necessarily inthe best interests of investors and other stakeholders.

Tradition and practice in many countries prescribes a so-called “unitary” board system,a single board of directors. However, some countries, notably Germany, have developed aformal system whose intent is to overcome such difficulties as lack of independence of boardmembers and lack of independence of the chairman of the board from company manage-ment. The latter approach requires a tiered hierarchy of boards, a management boardresponsible for overseeing management’s strategy, planning, and similar functions, and anindependent supervisory board charged with monitoring and reviewing decisions of themanagement board, and making decisions in which conflicts of interest in the managementboard may impair their independence, for example, in determining managerial compensation.

Clearly, independence of the chairman of the board does not guarantee that the boardwill function properly. However, independence should be regarded as a necessary condition,even if it is not a sufficient one.

5.1.3. Qualifications of DirectorsIn addition to independence, directors need to bring sufficient skill and experience to theposition to ensure that they will be able to fulfill their fiduciary responsibilities to investorsand other stakeholders. Information on directors’ prior business experience and other bio-graphical material, including current and past business affiliations, can generally be found inregulatory filings.

Boards of directors require a variety of skills and experience in order to function prop-erly. These skills will vary by industry although such core skills as knowledge of finance,accounting, and legal matters are required by all boards. Evaluation of the members shouldinclude an assessment of whether needed skills are available among the board members.Among the qualifications and core competencies that an investor should look for in the boardas a group, and in individual members or candidates for the board, are:

13Amendments to Rules Governing the Investment Company Act of 1940 (2004): 4.

14 Corporate Finance

c01 13 January 2012; 9:5:41

! Independence (see factors to consider in Section 5.1.1 above).! Relevant expertise in the industry, including the principal technologies used in the business

and in financial operations, legal matters, accounting and auditing; and managerial con-siderations such as the success of companies with which the director has been associated inthe past.

! Indications of ethical soundness, including public statements or writings of the director,problems in companies with which the director has been associated in the past such as legalor other regulatory violations involving ethical lapses.

! Experience in strategic planning and risk management.! Other board experience with companies regarded as having sound governance practices and

that are effective stewards of investors’ capital as compared to serving management’sinterests.

! Dedication and commitment to serving the board and investors’ interests. Board memberswith such qualities will not serve on more than a few boards, have an excellent record ofattendance at board meetings, and will limit other business commitments that require largeamounts of time.

! Commitment to the needs of investors as shown, for example, by significant personalinvestments in this or other companies for which he or she serves as a director, and by anabsence of conflicts of interest.