Embed Size (px)

Citation preview

1

STUDYMATERIAL

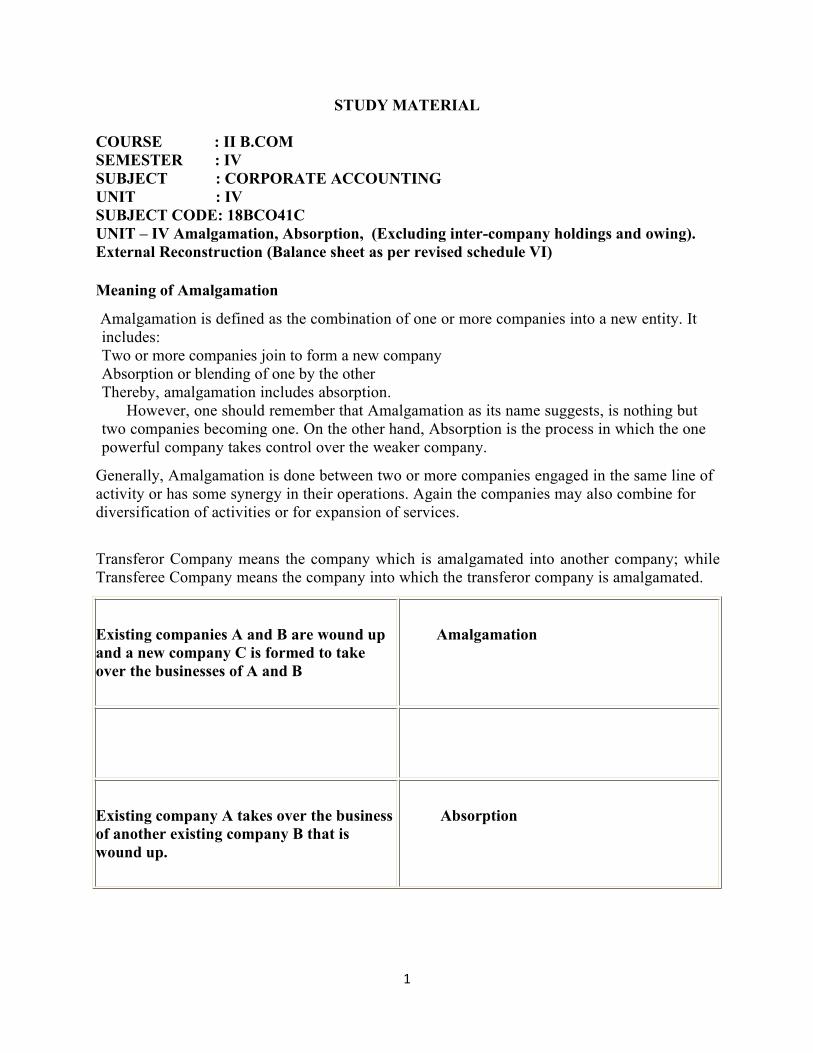

COURSE : II B.COMSEMESTER : IVSUBJECT : CORPORATE ACCOUNTINGUNIT : IVSUBJECT CODE: 18BCO41CUNIT – IV Amalgamation, Absorption, (Excluding inter-company holdings and owing).External Reconstruction (Balance sheet as per revised schedule VI)

Meaning of Amalgamation

Amalgamation is defined as the combination of one or more companies into a new entity. Itincludes:Two or more companies join to form a new companyAbsorption or blending of one by the otherThereby, amalgamation includes absorption.

However, one should remember that Amalgamation as its name suggests, is nothing buttwo companies becoming one. On the other hand, Absorption is the process in which the onepowerful company takes control over the weaker company.

Generally, Amalgamation is done between two or more companies engaged in the same line ofactivity or has some synergy in their operations. Again the companies may also combine fordiversification of activities or for expansion of services.

Transferor Company means the company which is amalgamated into another company; whileTransferee Company means the company into which the transferor company is amalgamated.

Existing companies A and B are wound upand a new company C is formed to takeover the businesses of A and B

Amalgamation

Existing company A takes over the businessof another existing company B that iswound up.

Absorption

2

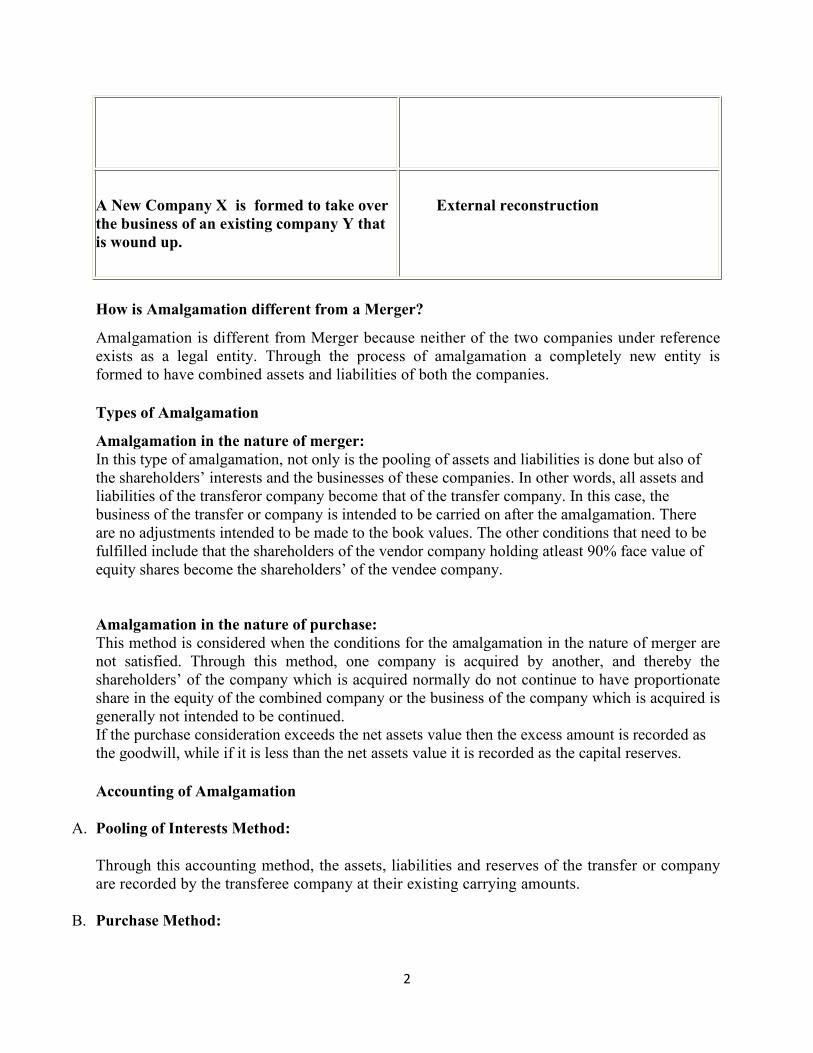

A New Company X is formed to take overthe business of an existing company Y thatis wound up.

External reconstruction

How is Amalgamation different from a Merger?

Amalgamation is different from Merger because neither of the two companies under referenceexists as a legal entity. Through the process of amalgamation a completely new entity isformed to have combined assets and liabilities of both the companies.

Types of Amalgamation

Amalgamation in the nature of merger:In this type of amalgamation, not only is the pooling of assets and liabilities is done but also ofthe shareholders’ interests and the businesses of these companies. In other words, all assets andliabilities of the transferor company become that of the transfer company. In this case, thebusiness of the transfer or company is intended to be carried on after the amalgamation. Thereare no adjustments intended to be made to the book values. The other conditions that need to befulfilled include that the shareholders of the vendor company holding atleast 90% face value ofequity shares become the shareholders’ of the vendee company.

Amalgamation in the nature of purchase:This method is considered when the conditions for the amalgamation in the nature of merger arenot satisfied. Through this method, one company is acquired by another, and thereby theshareholders’ of the company which is acquired normally do not continue to have proportionateshare in the equity of the combined company or the business of the company which is acquired isgenerally not intended to be continued.If the purchase consideration exceeds the net assets value then the excess amount is recorded asthe goodwill, while if it is less than the net assets value it is recorded as the capital reserves.

Accounting of Amalgamation

A. Pooling of Interests Method:

Through this accounting method, the assets, liabilities and reserves of the transfer or companyare recorded by the transferee company at their existing carrying amounts.

B. Purchase Method:

3

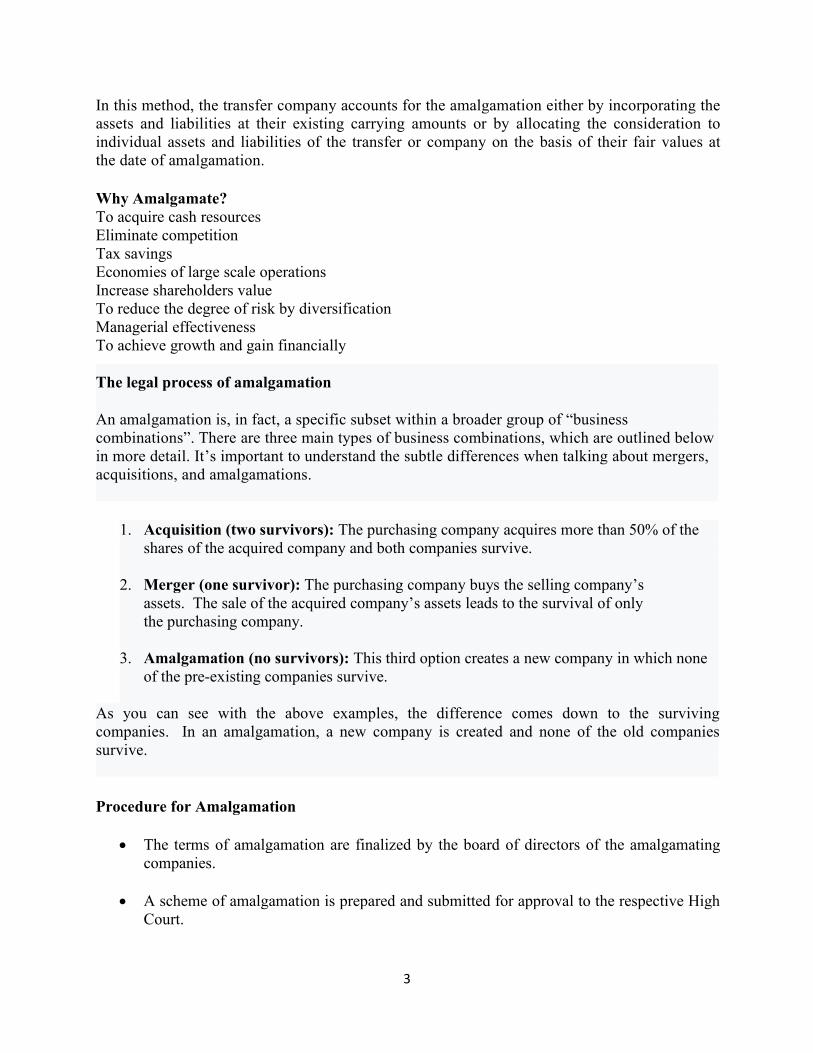

In this method, the transfer company accounts for the amalgamation either by incorporating theassets and liabilities at their existing carrying amounts or by allocating the consideration toindividual assets and liabilities of the transfer or company on the basis of their fair values atthe date of amalgamation.

Why Amalgamate?To acquire cash resourcesEliminate competitionTax savingsEconomies of large scale operationsIncrease shareholders valueTo reduce the degree of risk by diversificationManagerial effectivenessTo achieve growth and gain financially

The legal process of amalgamation

An amalgamation is, in fact, a specific subset within a broader group of “businesscombinations”. There are three main types of business combinations, which are outlined belowin more detail. It’s important to understand the subtle differences when talking about mergers,acquisitions, and amalgamations.

1. Acquisition (two survivors): The purchasing company acquires more than 50% of theshares of the acquired company and both companies survive.

2. Merger (one survivor): The purchasing company buys the selling company’sassets. The sale of the acquired company’s assets leads to the survival of onlythe purchasing company.

3. Amalgamation (no survivors): This third option creates a new company in which noneof the pre-existing companies survive.

As you can see with the above examples, the difference comes down to the survivingcompanies. In an amalgamation, a new company is created and none of the old companiessurvive.

Procedure for Amalgamation

The terms of amalgamation are finalized by the board of directors of the amalgamatingcompanies.

A scheme of amalgamation is prepared and submitted for approval to the respective HighCourt.

4

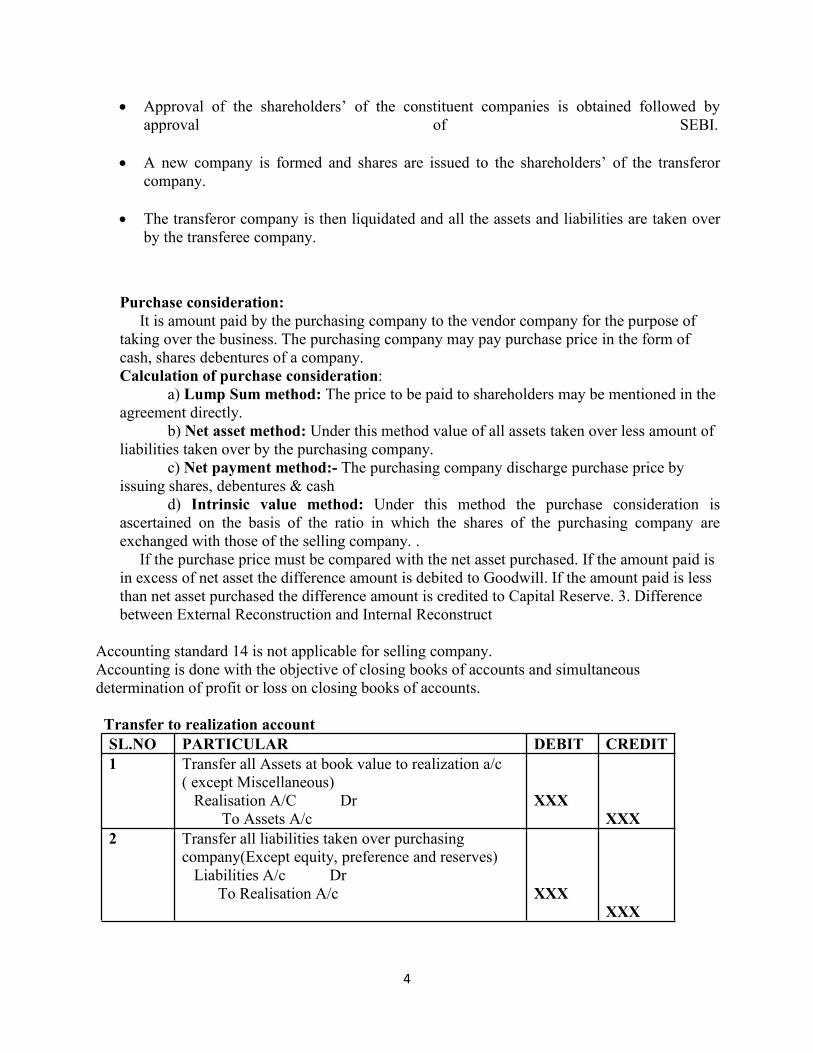

Approval of the shareholders’ of the constituent companies is obtained followed byapproval of SEBI.

A new company is formed and shares are issued to the shareholders’ of the transferorcompany.

The transferor company is then liquidated and all the assets and liabilities are taken overby the transferee company.

Purchase consideration:It is amount paid by the purchasing company to the vendor company for the purpose of

taking over the business. The purchasing company may pay purchase price in the form ofcash, shares debentures of a company.Calculation of purchase consideration:

a) Lump Sum method: The price to be paid to shareholders may be mentioned in theagreement directly.

b) Net asset method: Under this method value of all assets taken over less amount ofliabilities taken over by the purchasing company.

c) Net payment method:- The purchasing company discharge purchase price byissuing shares, debentures & cash

d) Intrinsic value method: Under this method the purchase consideration isascertained on the basis of the ratio in which the shares of the purchasing company areexchanged with those of the selling company. .

If the purchase price must be compared with the net asset purchased. If the amount paid isin excess of net asset the difference amount is debited to Goodwill. If the amount paid is lessthan net asset purchased the difference amount is credited to Capital Reserve. 3. Differencebetween External Reconstruction and Internal Reconstruct

Accounting standard 14 is not applicable for selling company.Accounting is done with the objective of closing books of accounts and simultaneousdetermination of profit or loss on closing books of accounts.

Transfer to realization accountSL.NO PARTICULAR DEBIT CREDIT1 Transfer all Assets at book value to realization a/c

( except Miscellaneous)Realisation A/C Dr

To Assets A/cXXX

XXX2 Transfer all liabilities taken over purchasing

company(Except equity, preference and reserves)Liabilities A/c Dr

To Realisation A/c XXXXXX

5

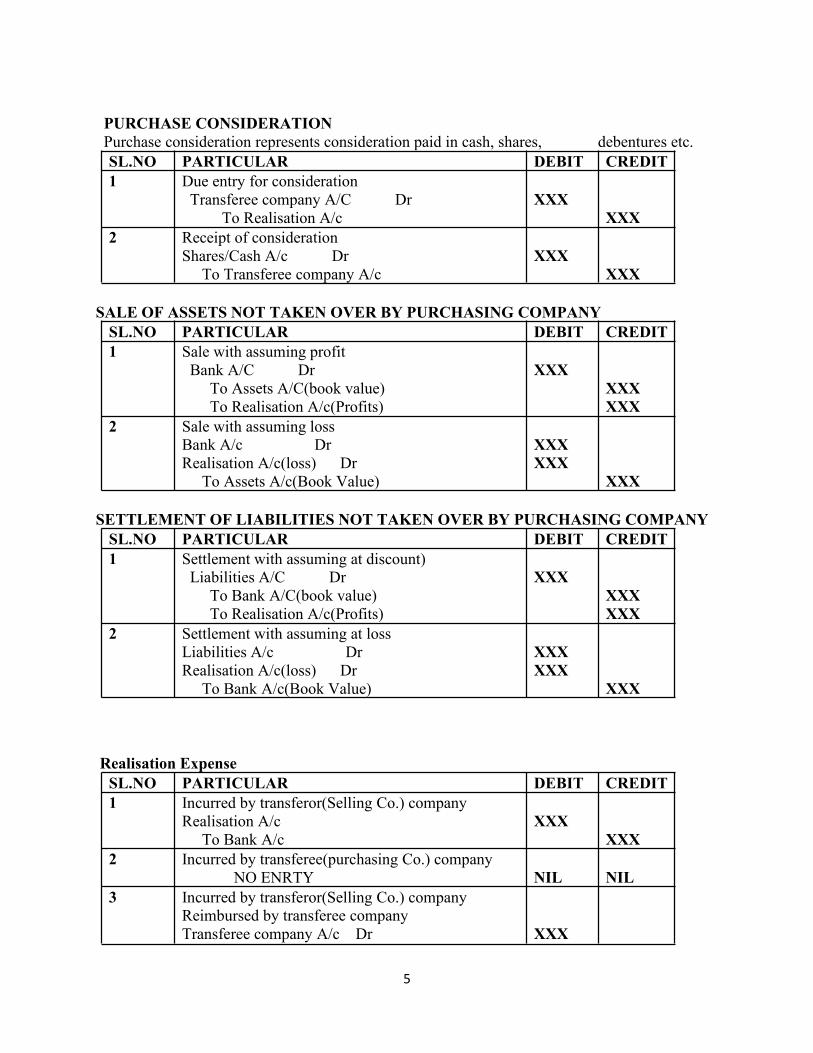

PURCHASE CONSIDERATIONPurchase consideration represents consideration paid in cash, shares, debentures etc.SL.NO PARTICULAR DEBIT CREDIT1 Due entry for consideration

Transferee company A/C DrTo Realisation A/c

XXXXXX

2 Receipt of considerationShares/Cash A/c Dr

To Transferee company A/cXXX

XXX

SALE OF ASSETS NOT TAKEN OVER BY PURCHASING COMPANYSL.NO PARTICULAR DEBIT CREDIT1 Sale with assuming profit

Bank A/C DrTo Assets A/C(book value)To Realisation A/c(Profits)

XXXXXXXXX

2 Sale with assuming lossBank A/c DrRealisation A/c(loss) Dr

To Assets A/c(Book Value)

XXXXXX

XXX

SETTLEMENT OF LIABILITIES NOT TAKEN OVER BY PURCHASING COMPANYSL.NO PARTICULAR DEBIT CREDIT1 Settlement with assuming at discount)

Liabilities A/C DrTo Bank A/C(book value)To Realisation A/c(Profits)

XXXXXXXXX

2 Settlement with assuming at lossLiabilities A/c DrRealisation A/c(loss) Dr

To Bank A/c(Book Value)

XXXXXX

XXX

Realisation ExpenseSL.NO PARTICULAR DEBIT CREDIT1 Incurred by transferor(Selling Co.) company

Realisation A/cTo Bank A/c

XXXXXX

2 Incurred by transferee(purchasing Co.) companyNO ENRTY NIL NIL

3 Incurred by transferor(Selling Co.) companyReimbursed by transferee companyTransferee company A/c Dr XXX

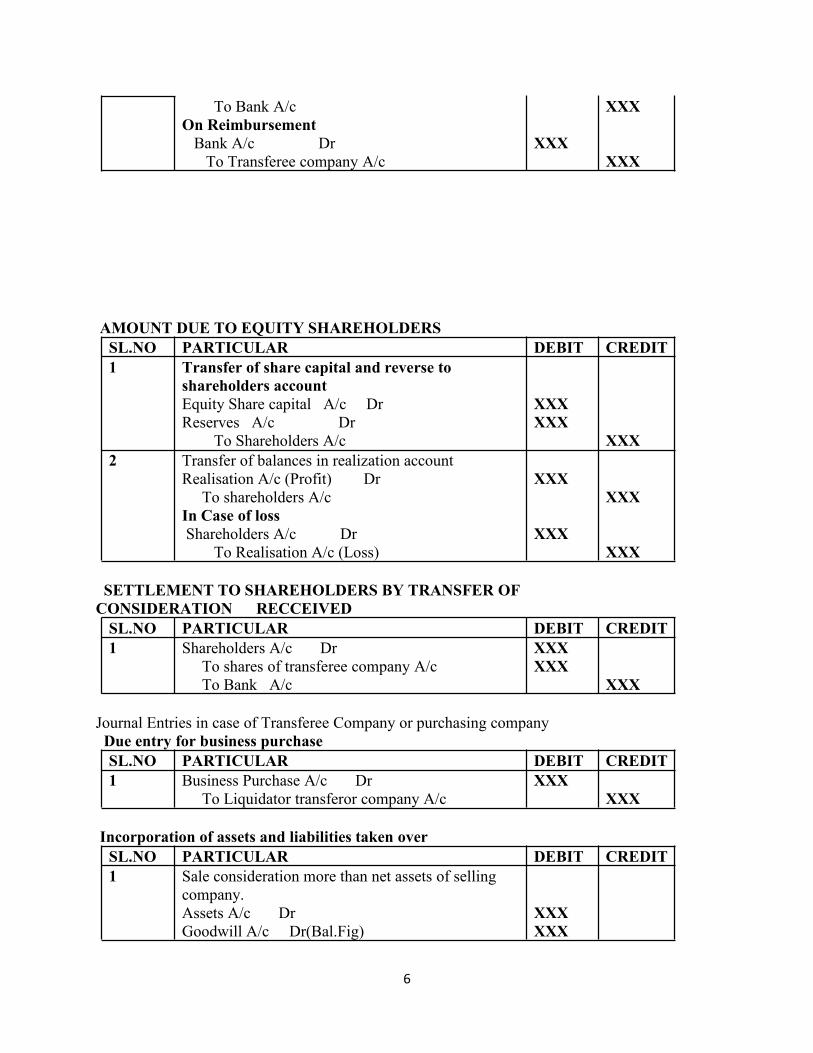

6

To Bank A/cOn ReimbursementBank A/c DrTo Transferee company A/c

XXX

XXX

XXX

AMOUNT DUE TO EQUITY SHAREHOLDERSSL.NO PARTICULAR DEBIT CREDIT1 Transfer of share capital and reverse to

shareholders accountEquity Share capital A/c DrReserves A/c Dr

To Shareholders A/c

XXXXXX

XXX2 Transfer of balances in realization account

Realisation A/c (Profit) DrTo shareholders A/c

In Case of lossShareholders A/c Dr

To Realisation A/c (Loss)

XXX

XXX

XXX

XXX

SETTLEMENT TO SHAREHOLDERS BY TRANSFER OFCONSIDERATION RECCEIVEDSL.NO PARTICULAR DEBIT CREDIT1 Shareholders A/c Dr

To shares of transferee company A/cTo Bank A/c

XXXXXX

XXX

Journal Entries in case of Transferee Company or purchasing companyDue entry for business purchaseSL.NO PARTICULAR DEBIT CREDIT1 Business Purchase A/c Dr

To Liquidator transferor company A/cXXX

XXX

Incorporation of assets and liabilities taken overSL.NO PARTICULAR DEBIT CREDIT1 Sale consideration more than net assets of selling

company.Assets A/c DrGoodwill A/c Dr(Bal.Fig)

XXXXXX

7

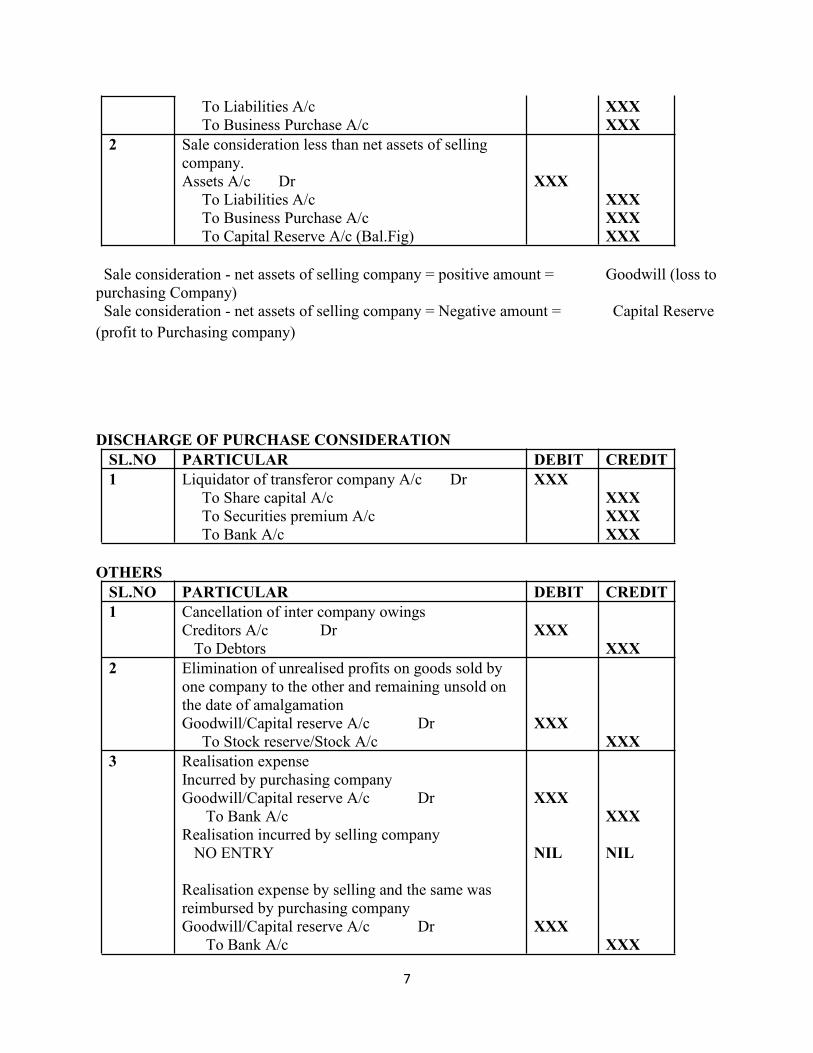

To Liabilities A/cTo Business Purchase A/c

XXXXXX

2 Sale consideration less than net assets of sellingcompany.Assets A/c Dr

To Liabilities A/cTo Business Purchase A/cTo Capital Reserve A/c (Bal.Fig)

XXXXXXXXXXXX

Sale consideration - net assets of selling company = positive amount = Goodwill (loss topurchasing Company)Sale consideration - net assets of selling company = Negative amount = Capital Reserve(profit to Purchasing company)

DISCHARGE OF PURCHASE CONSIDERATIONSL.NO PARTICULAR DEBIT CREDIT1 Liquidator of transferor company A/c Dr

To Share capital A/cTo Securities premium A/cTo Bank A/c

XXXXXXXXXXXX

OTHERSSL.NO PARTICULAR DEBIT CREDIT1 Cancellation of inter company owings

Creditors A/c DrTo Debtors

XXXXXX

2 Elimination of unrealised profits on goods sold byone company to the other and remaining unsold onthe date of amalgamationGoodwill/Capital reserve A/c Dr

To Stock reserve/Stock A/cXXX

XXX3 Realisation expense

Incurred by purchasing companyGoodwill/Capital reserve A/c Dr

To Bank A/cRealisation incurred by selling companyNO ENTRY

Realisation expense by selling and the same wasreimbursed by purchasing companyGoodwill/Capital reserve A/c Dr

To Bank A/c

XXX

NIL

XXX

XXX

NIL

XXX

8

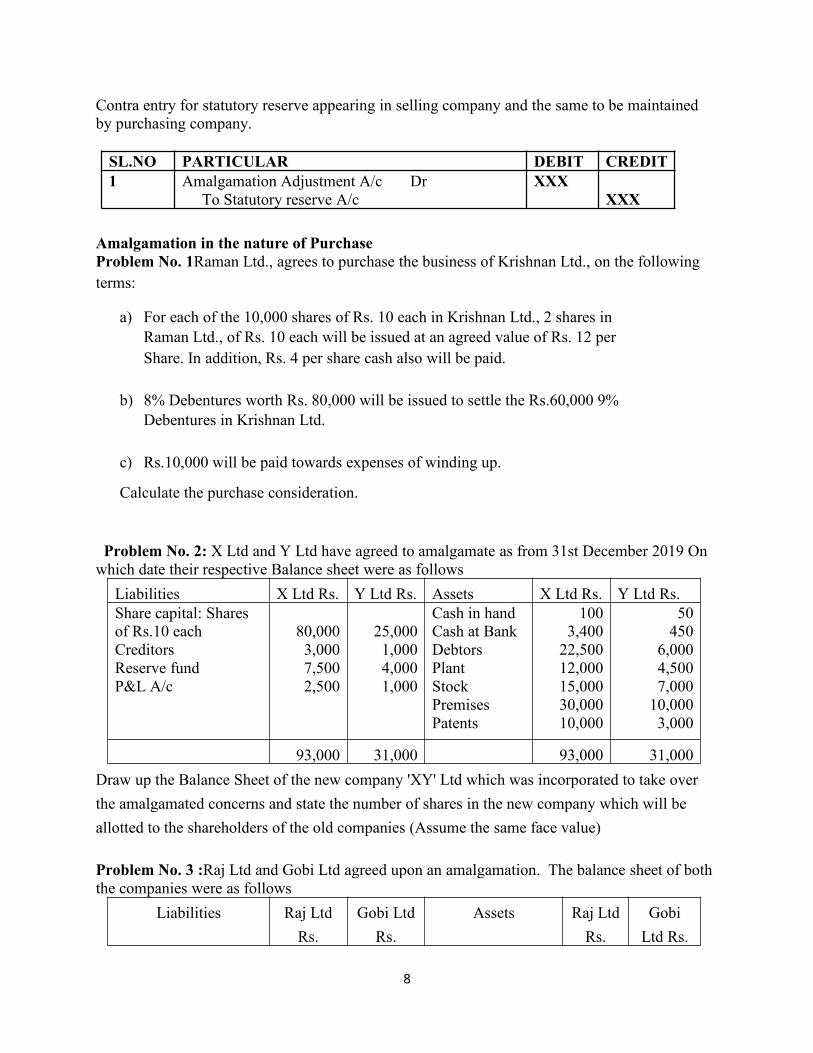

Contra entry for statutory reserve appearing in selling company and the same to be maintainedby purchasing company.

SL.NO PARTICULAR DEBIT CREDIT1 Amalgamation Adjustment A/c Dr

To Statutory reserve A/cXXX

XXX

Amalgamation in the nature of PurchaseProblem No. 1Raman Ltd., agrees to purchase the business of Krishnan Ltd., on the followingterms:

a) For each of the 10,000 shares of Rs. 10 each in Krishnan Ltd., 2 shares inRaman Ltd., of Rs. 10 each will be issued at an agreed value of Rs. 12 perShare. In addition, Rs. 4 per share cash also will be paid.

b) 8% Debentures worth Rs. 80,000 will be issued to settle the Rs.60,000 9%Debentures in Krishnan Ltd.

c) Rs.10,000 will be paid towards expenses of winding up.

Calculate the purchase consideration.

Problem No. 2: X Ltd and Y Ltd have agreed to amalgamate as from 31st December 2019 Onwhich date their respective Balance sheet were as follows

Liabilities X Ltd Rs. Y Ltd Rs. Assets X Ltd Rs. Y Ltd Rs.Share capital: Sharesof Rs.10 eachCreditorsReserve fundP&L A/c

80,0003,0007,5002,500

25,0001,0004,0001,000

Cash in handCash at BankDebtorsPlantStockPremisesPatents

1003,40022,50012,00015,00030,00010,000

50450

6,0004,5007,00010,0003,000

93,000 31,000 93,000 31,000Draw up the Balance Sheet of the new company 'XY' Ltd which was incorporated to take overthe amalgamated concerns and state the number of shares in the new company which will beallotted to the shareholders of the old companies (Assume the same face value)

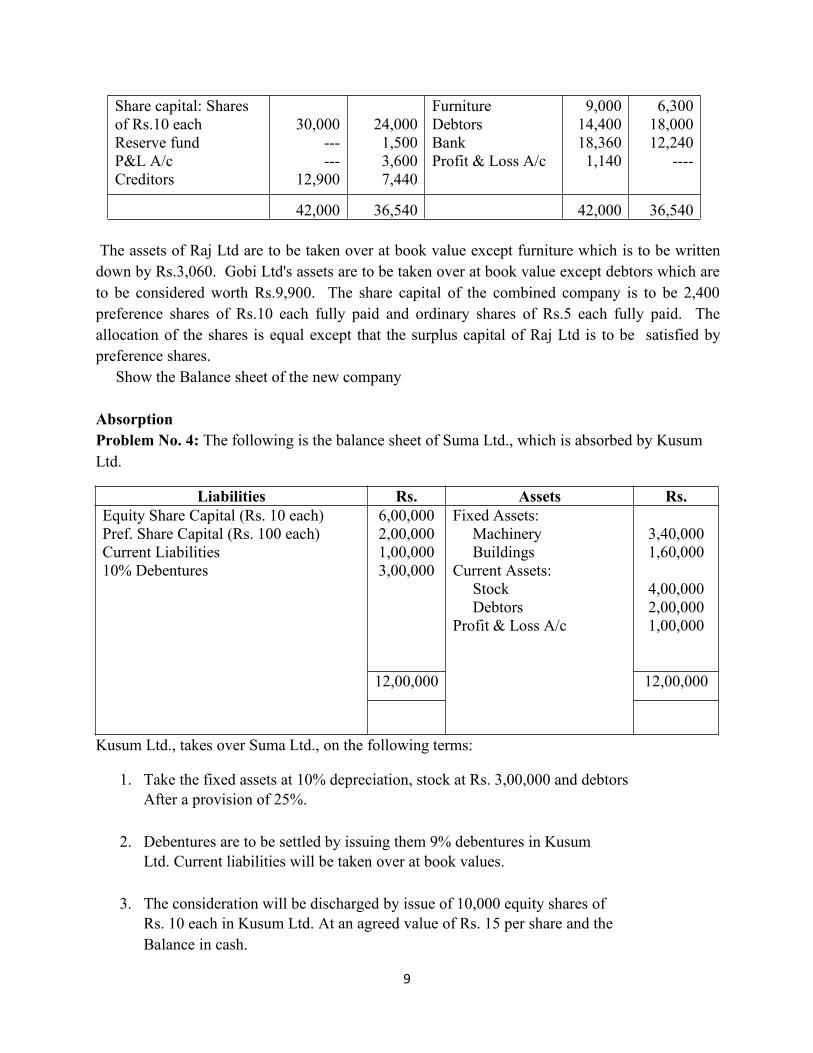

Problem No. 3 :Raj Ltd and Gobi Ltd agreed upon an amalgamation. The balance sheet of boththe companies were as follows

Liabilities Raj LtdRs.

Gobi LtdRs.

Assets Raj LtdRs.

GobiLtd Rs.

9

Share capital: Sharesof Rs.10 eachReserve fundP&L A/cCreditors

30,000------

12,900

24,0001,5003,6007,440

FurnitureDebtorsBankProfit & Loss A/c

9,00014,40018,3601,140

6,30018,00012,240

----

42,000 36,540 42,000 36,540

The assets of Raj Ltd are to be taken over at book value except furniture which is to be writtendown by Rs.3,060. Gobi Ltd's assets are to be taken over at book value except debtors which areto be considered worth Rs.9,900. The share capital of the combined company is to be 2,400preference shares of Rs.10 each fully paid and ordinary shares of Rs.5 each fully paid. Theallocation of the shares is equal except that the surplus capital of Raj Ltd is to be satisfied bypreference shares.

Show the Balance sheet of the new company

AbsorptionProblem No. 4: The following is the balance sheet of Suma Ltd., which is absorbed by KusumLtd.

Liabilities Rs. Assets Rs.Equity Share Capital (Rs. 10 each)Pref. Share Capital (Rs. 100 each)Current Liabilities10% Debentures

6,00,0002,00,0001,00,0003,00,000

Fixed Assets:MachineryBuildings

Current Assets:StockDebtors

Profit & Loss A/c

3,40,0001,60,000

4,00,0002,00,0001,00,000

12,00,000 12,00,000

Kusum Ltd., takes over Suma Ltd., on the following terms:

1. Take the fixed assets at 10% depreciation, stock at Rs. 3,00,000 and debtorsAfter a provision of 25%.

2. Debentures are to be settled by issuing them 9% debentures in KusumLtd. Current liabilities will be taken over at book values.

3. The consideration will be discharged by issue of 10,000 equity shares ofRs. 10 each in Kusum Ltd. At an agreed value of Rs. 15 per share and theBalance in cash.

10

4. Expenses of liquidation of Rs. 20,000 will be reimbursed by Kusum Ltd.

You are required to give (a) journal entries to close the books of Suma Ltd.

(b) Journal entries to record the acquisition assuming it is in the nature of purchase.

Problem No. 5:Spring Field Ltd.is absorbed by Sports Field Ltd., the consideration being:

1) The taking over of the trade liabilities of Rs. 40,000;

2) The payment of cost of absorption of Rs. 15,000;

3) The repayment of ‘B’ debentures of Spring Field Ltd. Of Rs. 2,00,000 at par;

4) The discharge of ‘A’ debentures of Rs. 3,00,000 in the Vendor Co. at aPremium of 10% by the issue of 8% debentures in Sports Field Ltd. at par;

5) A payment of Rs. 20 per share in cash and the exchange of 4 fully paidRs. 10 shares in Sports Field Ltd. at a market price of Rs. 15 per share forEvery Rs. 50 share in Spring Field Ltd. which were 40,000 in number.

You are required to find out the purchase consideration.

Problem No:6 Ram & Co Ltd. is absorbed by Krishnan & Co Ltd. the consideration being

1) Assumption of the liabilities,

2) The discharge of the debentures at a premium of 7.5% by issue of 7.5% debentures inKrishnan & Co Ltd.

3) A cash payment of Rs. 100 per share and the exchange of 12 shares of Rs. 20 each inthe Krishnan & Co Ltd. at an agreed value of Rs. 25 per share for every share in Ram& Co Ltd.

4) The liquidation expenses of Rs. 8,000 to be borne by Ram & Co Ltd. Show thenecessary journal entries in the books of both the companies.

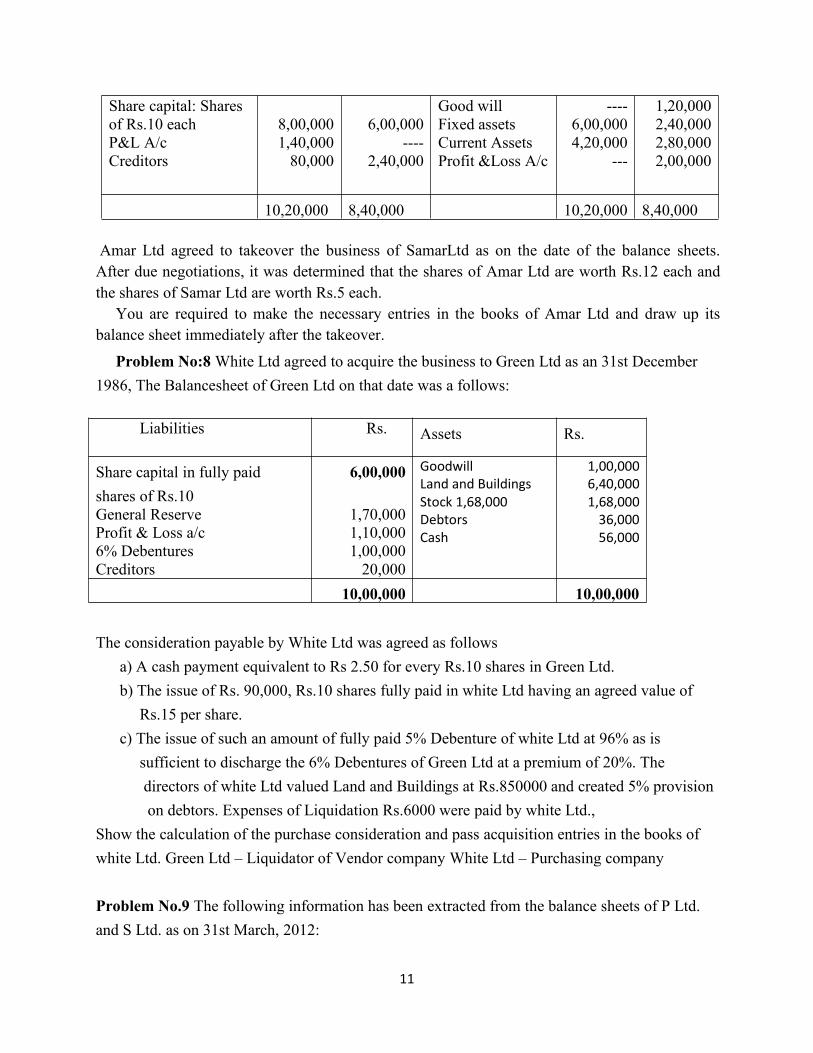

Problem No:7 The following are the summarized Balance sheets of Amar Ltd and Samar Led ason 31st March 2019:

Liabilities Amar LtdRs.

SammarLtd Rs.

Assets Amar LtdRs.

SammarLtd Rs.

11

Share capital: Sharesof Rs.10 eachP&L A/cCreditors

8,00,0001,40,00080,000

6,00,000----

2,40,000

Good willFixed assetsCurrent AssetsProfit &Loss A/c

----6,00,0004,20,000

---

1,20,0002,40,0002,80,0002,00,000

10,20,000 8,40,000 10,20,000 8,40,000

Amar Ltd agreed to takeover the business of SamarLtd as on the date of the balance sheets.After due negotiations, it was determined that the shares of Amar Ltd are worth Rs.12 each andthe shares of Samar Ltd are worth Rs.5 each.

You are required to make the necessary entries in the books of Amar Ltd and draw up itsbalance sheet immediately after the takeover.

Problem No:8White Ltd agreed to acquire the business to Green Ltd as an 31st December1986, The Balancesheet of Green Ltd on that date was a follows:

Liabilities Rs. Assets Rs.

Share capital in fully paidshares of Rs.10General ReserveProfit & Loss a/c6% DebenturesCreditors

6,00,000

1,70,0001,10,0001,00,00020,000

GoodwillLand and BuildingsStock 1,68,000DebtorsCash

1,00,0006,40,0001,68,00036,00056,000

10,00,000 10,00,000

The consideration payable by White Ltd was agreed as followsa) A cash payment equivalent to Rs 2.50 for every Rs.10 shares in Green Ltd.b) The issue of Rs. 90,000, Rs.10 shares fully paid in white Ltd having an agreed value of

Rs.15 per share.c) The issue of such an amount of fully paid 5% Debenture of white Ltd at 96% as is

sufficient to discharge the 6% Debentures of Green Ltd at a premium of 20%. Thedirectors of white Ltd valued Land and Buildings at Rs.850000 and created 5% provisionon debtors. Expenses of Liquidation Rs.6000 were paid by white Ltd.,

Show the calculation of the purchase consideration and pass acquisition entries in the books ofwhite Ltd. Green Ltd – Liquidator of Vendor company White Ltd – Purchasing company

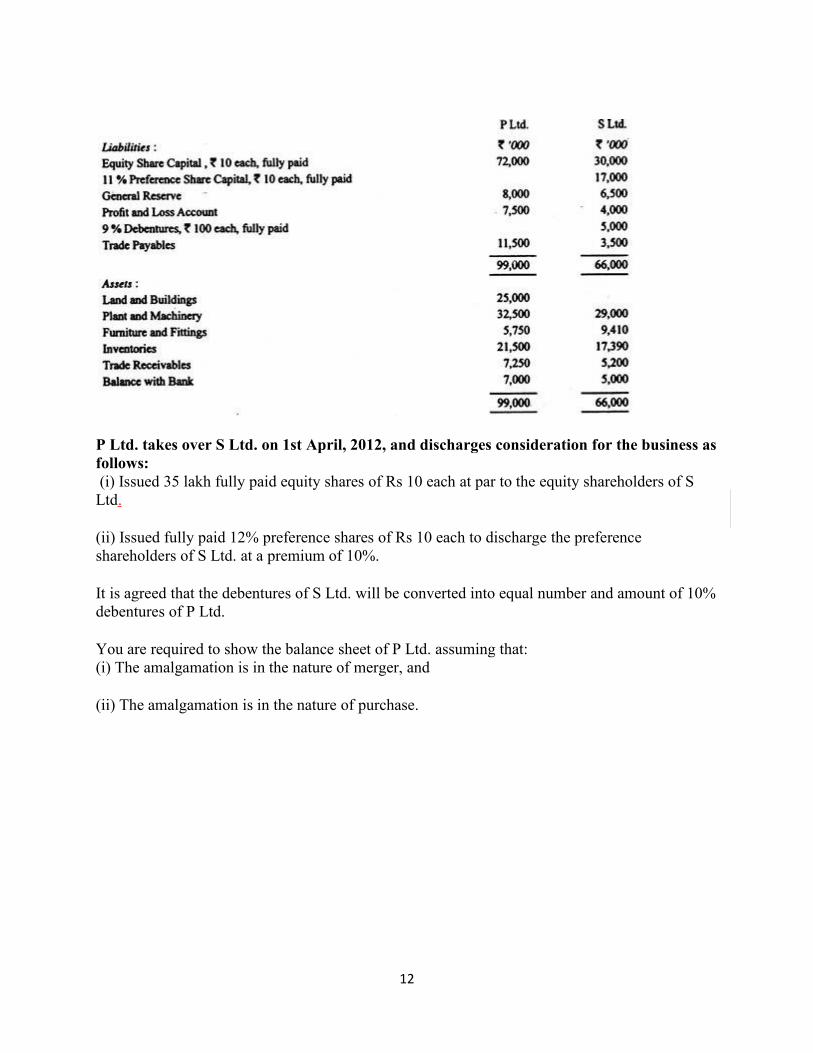

Problem No.9 The following information has been extracted from the balance sheets of P Ltd.and S Ltd. as on 31st March, 2012:

12

P Ltd. takes over S Ltd. on 1st April, 2012, and discharges consideration for the business asfollows:(i) Issued 35 lakh fully paid equity shares of Rs 10 each at par to the equity shareholders of SLtd.

(ii) Issued fully paid 12% preference shares of Rs 10 each to discharge the preferenceshareholders of S Ltd. at a premium of 10%.

It is agreed that the debentures of S Ltd. will be converted into equal number and amount of 10%debentures of P Ltd.

You are required to show the balance sheet of P Ltd. assuming that:(i) The amalgamation is in the nature of merger, and

(ii) The amalgamation is in the nature of purchase.

13

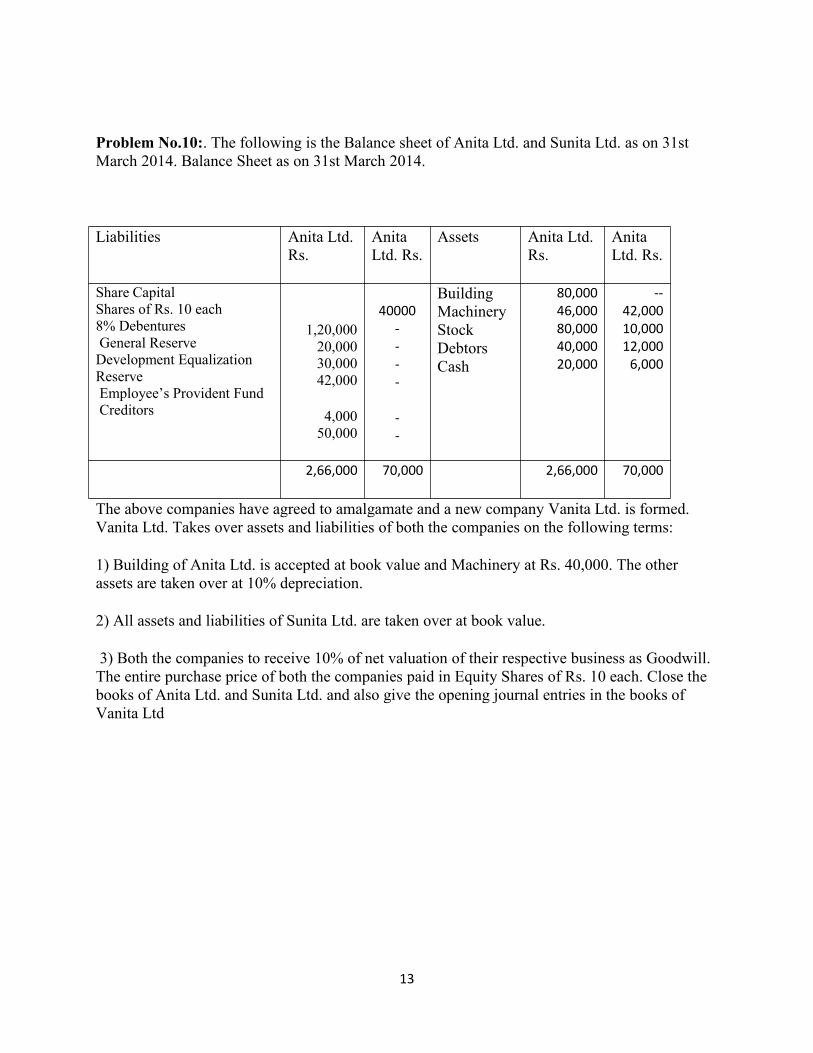

Problem No.10:. The following is the Balance sheet of Anita Ltd. and Sunita Ltd. as on 31stMarch 2014. Balance Sheet as on 31st March 2014.

Liabilities Anita Ltd.Rs.

AnitaLtd. Rs.

Assets Anita Ltd.Rs.

AnitaLtd. Rs.

Share CapitalShares of Rs. 10 each8% DebenturesGeneral ReserveDevelopment EqualizationReserveEmployee’s Provident FundCreditors

1,20,00020,00030,00042,000

4,00050,000

40000----

--

BuildingMachineryStockDebtorsCash

80,00046,00080,00040,00020,000

--42,00010,00012,0006,000

2,66,000 70,000 2,66,000 70,000

The above companies have agreed to amalgamate and a new company Vanita Ltd. is formed.Vanita Ltd. Takes over assets and liabilities of both the companies on the following terms:

1) Building of Anita Ltd. is accepted at book value and Machinery at Rs. 40,000. The otherassets are taken over at 10% depreciation.

2) All assets and liabilities of Sunita Ltd. are taken over at book value.

3) Both the companies to receive 10% of net valuation of their respective business as Goodwill.The entire purchase price of both the companies paid in Equity Shares of Rs. 10 each. Close thebooks of Anita Ltd. and Sunita Ltd. and also give the opening journal entries in the books ofVanita Ltd

14

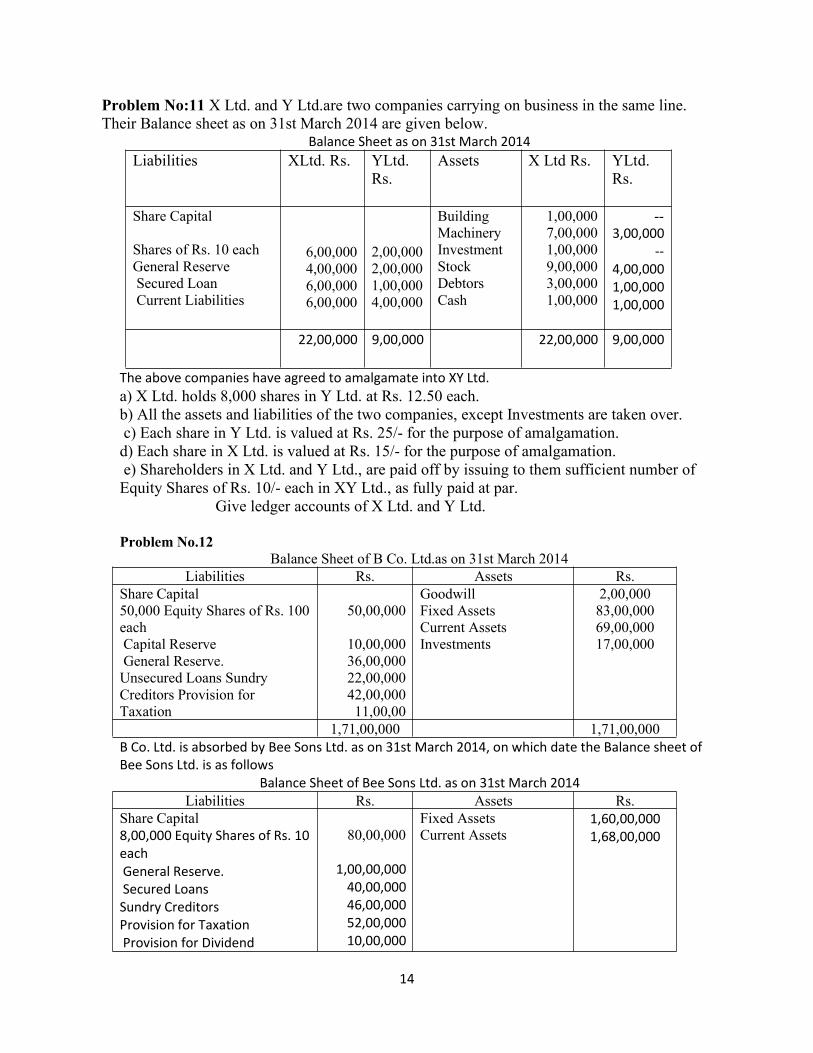

Problem No:11 X Ltd. and Y Ltd.are two companies carrying on business in the same line.Their Balance sheet as on 31st March 2014 are given below.

Balance Sheet as on 31st March 2014Liabilities XLtd. Rs. YLtd.

Rs.Assets X Ltd Rs. YLtd.

Rs.

Share Capital

Shares of Rs. 10 eachGeneral ReserveSecured LoanCurrent Liabilities

6,00,0004,00,0006,00,0006,00,000

2,00,0002,00,0001,00,0004,00,000

BuildingMachineryInvestmentStockDebtorsCash

1,00,0007,00,0001,00,0009,00,0003,00,0001,00,000

--3,00,000

--4,00,0001,00,0001,00,000

22,00,000 9,00,000 22,00,000 9,00,000

The above companies have agreed to amalgamate into XY Ltd.a) X Ltd. holds 8,000 shares in Y Ltd. at Rs. 12.50 each.b) All the assets and liabilities of the two companies, except Investments are taken over.c) Each share in Y Ltd. is valued at Rs. 25/- for the purpose of amalgamation.d) Each share in X Ltd. is valued at Rs. 15/- for the purpose of amalgamation.e) Shareholders in X Ltd. and Y Ltd., are paid off by issuing to them sufficient number ofEquity Shares of Rs. 10/- each in XY Ltd., as fully paid at par.

Give ledger accounts of X Ltd. and Y Ltd.

Problem No.12Balance Sheet of B Co. Ltd.as on 31st March 2014

Liabilities Rs. Assets Rs.Share Capital50,000 Equity Shares of Rs. 100eachCapital ReserveGeneral Reserve.Unsecured Loans SundryCreditors Provision forTaxation

50,00,000

10,00,00036,00,00022,00,00042,00,00011,00,00

GoodwillFixed AssetsCurrent AssetsInvestments

2,00,00083,00,00069,00,00017,00,000

1,71,00,000 1,71,00,000B Co. Ltd. is absorbed by Bee Sons Ltd. as on 31st March 2014, on which date the Balance sheet ofBee Sons Ltd. is as follows

Balance Sheet of Bee Sons Ltd. as on 31st March 2014Liabilities Rs. Assets Rs.

Share Capital8,00,000 Equity Shares of Rs. 10eachGeneral Reserve.Secured LoansSundry CreditorsProvision for TaxationProvision for Dividend

80,00,000

1,00,00,00040,00,00046,00,00052,00,00010,00,000

Fixed AssetsCurrent Assets

1,60,00,0001,68,00,000

15

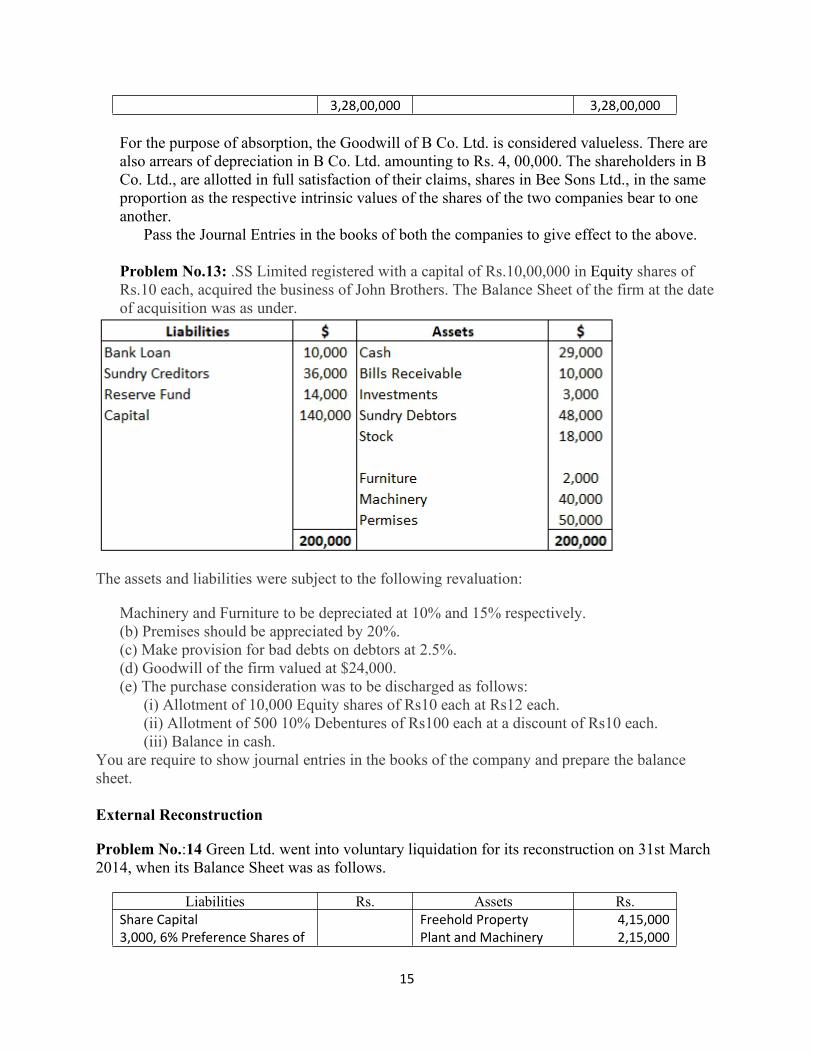

3,28,00,000 3,28,00,000

For the purpose of absorption, the Goodwill of B Co. Ltd. is considered valueless. There arealso arrears of depreciation in B Co. Ltd. amounting to Rs. 4, 00,000. The shareholders in BCo. Ltd., are allotted in full satisfaction of their claims, shares in Bee Sons Ltd., in the sameproportion as the respective intrinsic values of the shares of the two companies bear to oneanother.

Pass the Journal Entries in the books of both the companies to give effect to the above.

Problem No.13: .SS Limited registered with a capital of Rs.10,00,000 in Equity shares ofRs.10 each, acquired the business of John Brothers. The Balance Sheet of the firm at the dateof acquisition was as under.

The assets and liabilities were subject to the following revaluation:

Machinery and Furniture to be depreciated at 10% and 15% respectively.(b) Premises should be appreciated by 20%.(c) Make provision for bad debts on debtors at 2.5%.(d) Goodwill of the firm valued at $24,000.(e) The purchase consideration was to be discharged as follows:

(i) Allotment of 10,000 Equity shares of Rs10 each at Rs12 each.(ii) Allotment of 500 10% Debentures of Rs100 each at a discount of Rs10 each.(iii) Balance in cash.

You are require to show journal entries in the books of the company and prepare the balancesheet.

External Reconstruction

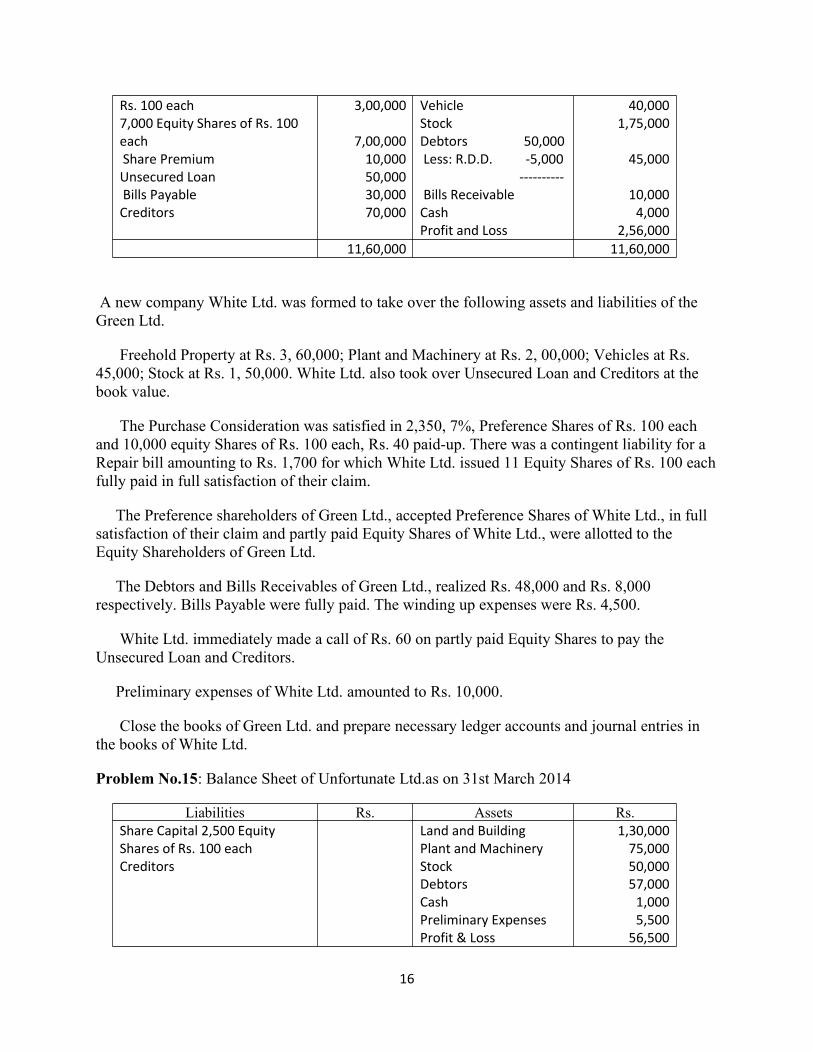

Problem No.:14 Green Ltd. went into voluntary liquidation for its reconstruction on 31st March2014, when its Balance Sheet was as follows.

Liabilities Rs. Assets Rs.Share Capital3,000, 6% Preference Shares of

Freehold PropertyPlant and Machinery

4,15,0002,15,000

16

Rs. 100 each7,000 Equity Shares of Rs. 100eachShare PremiumUnsecured LoanBills PayableCreditors

3,00,000

7,00,00010,00050,00030,00070,000

VehicleStockDebtors 50,000Less: R.D.D. -5,000

----------Bills ReceivableCashProfit and Loss

40,0001,75,000

45,000

10,0004,000

2,56,00011,60,000 11,60,000

A new company White Ltd. was formed to take over the following assets and liabilities of theGreen Ltd.

Freehold Property at Rs. 3, 60,000; Plant and Machinery at Rs. 2, 00,000; Vehicles at Rs.45,000; Stock at Rs. 1, 50,000. White Ltd. also took over Unsecured Loan and Creditors at thebook value.

The Purchase Consideration was satisfied in 2,350, 7%, Preference Shares of Rs. 100 eachand 10,000 equity Shares of Rs. 100 each, Rs. 40 paid-up. There was a contingent liability for aRepair bill amounting to Rs. 1,700 for which White Ltd. issued 11 Equity Shares of Rs. 100 eachfully paid in full satisfaction of their claim.

The Preference shareholders of Green Ltd., accepted Preference Shares of White Ltd., in fullsatisfaction of their claim and partly paid Equity Shares of White Ltd., were allotted to theEquity Shareholders of Green Ltd.

The Debtors and Bills Receivables of Green Ltd., realized Rs. 48,000 and Rs. 8,000respectively. Bills Payable were fully paid. The winding up expenses were Rs. 4,500.

White Ltd. immediately made a call of Rs. 60 on partly paid Equity Shares to pay theUnsecured Loan and Creditors.

Preliminary expenses of White Ltd. amounted to Rs. 10,000.

Close the books of Green Ltd. and prepare necessary ledger accounts and journal entries inthe books of White Ltd.

Problem No.15: Balance Sheet of Unfortunate Ltd.as on 31st March 2014

Liabilities Rs. Assets Rs.Share Capital 2,500 EquityShares of Rs. 100 eachCreditors

Land and BuildingPlant and MachineryStockDebtorsCashPreliminary ExpensesProfit & Loss

1,30,00075,00050,00057,0001,0005,500

56,500

17

11,60,000 11,60,000The shareholders of the company resolved to take the company into voluntary liquidation and toform Fortunate Ltd., a new company with an authorised share capital of Rs. 10 lakhs to take overthe business on the following terms:--

a) Preferential Creditors of Rs. 15,000 are to be paid in full.

b) Unsecured Creditors to receive 50 paisa in a rupee in full settlement of their claims or atpar value in 7% Debentures of Fortunate Ltd.

c) 2,500 Equity Shares of Rs. 100 each, Rs. 60 paid, to be distributed pro-rata to existingshareholders.

Half the Unsecured Creditors opted to be paid in Cash, and the funds for this purpose were foundby calling up the balance of Rs. 40 per share. Cost of liquidation amounted to Rs. 3,500 was paidby Fortunate Ltd. to Unfortunate Ltd.

Compute the Purchase Consideration and prepare the Balance Sheet of the new companyassuming that all assets are taken over at book value except Building, which is also taken over.

----------------------------------------------------------------