Embed Size (px)

Citation preview

Full Terms & Conditions of access and use can be found athttp://www.tandfonline.com/action/journalInformation?journalCode=raec20

Download by: [Queensland University of Technology] Date: 12 January 2016, At: 18:23

Applied Economics

ISSN: 0003-6846 (Print) 1466-4283 (Online) Journal homepage: http://www.tandfonline.com/loi/raec20

Bank reforms and efficiency in Vietnamese banks:evidence based on SFA and DEA

Thanh Pham Thien Nguyen, Son Hong Nghiem, Eduardo Roca & ParmendraSharma

To cite this article: Thanh Pham Thien Nguyen, Son Hong Nghiem, Eduardo Roca & ParmendraSharma (2016): Bank reforms and efficiency in Vietnamese banks: evidence based on SFA andDEA, Applied Economics, DOI: 10.1080/00036846.2015.1130788

To link to this article: http://dx.doi.org/10.1080/00036846.2015.1130788

View supplementary material

Published online: 12 Jan 2016.

Submit your article to this journal

View related articles

View Crossmark data

Bank reforms and efficiency in Vietnamese banks: evidence based on SFA andDEAThanh Pham Thien Nguyena,b, Son Hong Nghiemc, Eduardo Rocab and Parmendra Sharmab

aBanking Faculty, University of Economics HCMC, Ho Chi Minh City, Vietnam; bDepartment of Accounting, Finance and Economics, GriffithUniversity, Brisbane, QLD, Australia; cInstitute of Health and Biomedical Innovation (IHBI), Queensland University of Technology, KelvinGrove, QLD, Australia

ABSTRACTThis study examines the cost efficiency of Vietnamese banks from 2000 to 2014 in the first stage,and the selection and dynamic effects of two governance reforms, foreign partial acquisition andlisting on the stock exchange, on the efficiency in the second stage. Empirical results from thetwo-stage Stochastic Frontier Analysis (SFA) are highly consistent with those from the two-stageData Envelopment Analysis (DEA) . Specifically, the first-stage efficiency estimation indicates thatthe cost efficiency shows a slightly upward trend over the period 2000–2014, with the costefficiency score being 0.93 and state-owned banks outperforming joint-stock banks (JSBs). Themixed process seemingly unrelated regression estimator which controls the potential endogene-ity of public listing and foreign acquisition in the second stage shows that selection effects occurin the Vietnamese banking system: banks selected by the strategic foreign investors for partialacquisition and banks selected for public listing are more cost-efficient than those not selected.The short-term and long-term dynamic effects of foreign partial acquisition are documented: thecost efficiency of the Vietnamese banks post-partial acquisition is lower than prior-partial acquisi-tion, and it experiences a decreasing trend since partial acquisition. However, the short-term andlong-term dynamic effects of public listing are not evidenced: the cost efficiency of the banksafter public listing is not statistically different from that before public listing, and it also reveals anunclear trend since public listing.

KEYWORDSBank efficiency; reforms;listing; foreign partialacquisition; ownership;Vietnam

JEL CLASSIFICATIONG21; G28; C30

I. Introduction

The performance of the banking sector has alwaysbeen of particular interest to policy makers andresearchers worldwide since banks are vital for acountry’s growth and development prospects. Thatinterest appears to have been intensified in the lasttwo decades since the banking systems around theworld suffered from the 1997–1998 Asian financialcrisis and the 2007–2008 global financial crisis.Various significant reforms have been implementedin the banking systems, with the goal to improvebank efficiency and stability. However, the effec-tiveness of the combination of banking reforms,which is captured by the trend in bank performanceover time, varies from one country to another. Forexample, the cost efficiency of Thai banks(Chunhachinda and Li 2010) and Indian banks(Sahoo and Mandal 2011) has experienced anupward trend, while that of Chinese banks (Ariff

and Can 2008) and Filipino banks (Dacanay III2011) showed a downward trend.

The literature concerning the selection anddynamic effects of the two governance reforms –foreign partial acquisition and listing on the stockexchange – on bank performance is limited.Selection effect captures the difference in performancebetween banks selected for foreign partial acquisitionor public listing and those not selected. Short-termdynamic effect relates to the difference in perfor-mance before and after having foreign partial acquisi-tion or public listing while long-term dynamic effectpertains to how the effect changes as time passes sincehaving foreign partial acquisition or public listing.Generally, foreign partial acquisition may result inperformance improvement since foreign strategicinvestors may bring state-of-the-arts technology andhuman capital to domestic banks that are encum-bered by the legacies of the centrally planned era.

Supplemental data for this article can be accessed here.CONTACT Thanh Pham Thien Nguyen [email protected]

APPLIED ECONOMICS, 2016http://dx.doi.org/10.1080/00036846.2015.1130788

© 2016 Taylor & Francis

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

Listing on the stock exchange may also lead to theperformance enhancement as market discipline canexert considerable pressure on banks to adopt cost-reducing practices. Nonetheless, the limited literatureconcerning these two governance reforms providescontradictory evidence. For instance, the selectioneffects of foreign partial acquisition and listing onthe stock exchange are found in Chinese banks,while their dynamic effects are statistically insignif-icant in both the short and long term (Lin and Zhang2009). In contrast, the selection effects and short-termand long-term dynamic effects of these two reformsare found in banks in South East Asia (Williams andNguyen 2005).

The effects of reforms on the performance ofVietnamese banks are interesting for examinationfor the following reasons. Vietnam is a rising eco-nomic star in Asia. It is now widely considered to bethe next ‘dragon’ in Asia. Within the ASEAN region,Vietnam is easily the leader or one of the leaders interms of economic performance (Chaponnière, Cling,and Zhou 2007; Abbott & Tarp 2012; Pomfret 2013).The Vietnamese banking system is the main pillar forthe Vietnamese financial system as the Vietnamesestock market has been set up in 2001. TheVietnamese banking system has experienced signifi-cant reforms towards deregulation since the 1990s.These reforms involved reducing state ownership,relaxing restrictions on the activity, entry and openingbranches of foreign banks, encouraging foreign insti-tutional ownership in a local bank, stimulating banksto list on the stock exchange and raising bank capital.Of these reforms, there are two which lead to govern-ance changes in the Vietnamese banking system: (i)raising the stake limit for a strategic foreign institu-tional investor at a local bank1 to attract partial for-eign acquisition, and (ii) encouraging banks to list onthe stock exchange. Despite several studies examiningthe performance of Vietnamese banks, to the best ofour knowledge, none has investigated the effects ofthese two governance reforms on the performance ofVietnamese banks. We address this important knowl-edge gap. In this study, we examine the trend in costefficiency in Vietnamese banks over the period 2000–2014 to evaluate the effectiveness of the combinationof banking reforms in Vietnam, and investigate the

selection and dynamic effects of the two governancereforms, foreign partial acquisition and listing on thestock exchange, on the cost efficiency of Vietnamesebanks.

Efficiency can be measured by either parametricapproaches or non-parametric approaches, withStochastic Frontier Analysis (SFA) being the mostpopular for the former and Data EnvelopmentAnalysis (DEA) being the most common for thelatter. Although there have been very few studiescomparing the outcomes between DEA and SFA,these studies produce mixed evidence. For example,the average efficiency scores obtained by DEA andSFA are similar in studies by Huang and Wang(2002) and Weill (2004), but dissimilar in studiesby Dong, Hamilton, and Tippett (2014) and Deliset al. (2009). The consistency in efficiency scorerankings obtained by SFA and DEA are moderatein the study by Dong, Hamilton, and Tippett (2014),but low in the studies by Huang and Wang (2002)and Weill (2004). The efficiency distribution and theinefficiency source are remarkably similar in a studyby Wadud and White (2000). As one can havegreater confidence when making policy decisions ifpolicy implications from different methods are con-sistent, this study employs both the SFA and DEA toestimate the cost efficiency of Vietnamese banks, andthen investigate the effects of governance reforms onthe cost efficiency of these banks from 1995 to 2011.

This article makes several contributions to theliterature. First, this is the first study onVietnamese banks that take into account the effectsof individual reforms on bank efficiency by focusingon the selection effect and the dynamic effect offoreign acquisition and public listing using themost updated dataset (2000–2014). Second, weexamine and control for the potential endogeneityof foreign acquisition and public listing on bankefficiency using a conditional mixed process see-mingly unrelated regression. Third, to the knowl-edge of the authors, this is also the first study onVietnamese banks’ efficiency which tests for therobustness of efficiency analysis by using both DEAand SFA.

This study has six sections, including this intro-ductory section. Section II provides a background of

1Vietnam allowed the maximum stake of a foreign strategic investor in a local bank of 15% from 2007, while the cap for total foreign holdings at any localbank was 30%. At the proposal of the central bank, this ownership of a foreign strategic investor can be raised up to 20% by Prime Minister’s decision(Decree No. 69/2007/NĐ-CP).

2 T. P. T. NGUYEN ET AL.

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

the Vietnamese banking system and key reformswhich have been occurred. Section III reviews therelated literature. Section IV presents the methodol-ogy and dataset. Empirical results are shown inSection V and the conclusion is drawn in Section VI.

II. The Vietnamese banking system and keyreforms

In this section, we briefly outline the key reformsthat have substantially transformed Vietnam’s bank-ing sector since the 1990s, from a predominantlystate-controlled to an increasingly market-orientedsector, remarkably, with visible foreign presence. Butfirst, a brief background on the structure of thebanking sector.

In 2014, Vietnam’s banking sector comprised of 4major and 1 minor state-owned commercial banks(SOCBs), 35 joint-stock banks (JSBs), 50 foreignbank branches, 4 joint-venture banks, and 2 devel-opment and policy banks, making up 96 in total,seemingly, a disproportionately large number for apopulation of 90 million (Nguyen, Roca, and Sharma2014). The large number of banks has been duemainly to an influx of foreign branch banks, a con-sequence of the reform program, they numberedonly eight in 1993; the number of SOCBs and JSBshave remained steady over the years. Another posi-tive consequence of the reform programs appear tobe a conspicuous decline in the concentration ratiofrom around 80% in early 2000s to around 50% in2014. Further, the market share of deposits alsochanged over the years, for example the share ofJCBs improved from just over 11% in 2000 to over51% by 2014, the largest market share at the time.During the same period, the market share of SOCBsdeclined from 78% to 40%.

Beginning in 1986, Vietnam has aspired to trans-form its long-standing centrally planned economy toa market-oriented economy, with a distinctively big-ger role for the private sector (Orden et al. 2007). Inthe process, consequently, a crucial transformationwith respect to the banking sector has been a movefrom a one-tier system, where the central bank wasalso a commercial bank, to a two-tier system separ-ating the role and functions of the central bank fromcommercial banking in 1988. Subsequently, from1990 onwards, the Vietnamese government has con-spicuously and purposely implemented reform

policies directed towards deregulation, with theobjective mainly of improving the efficiency andstability of the banking system. Towards this end,three key reform programs are discussed below.

The first reform program involved allowing for-eign ownership in local banks. Decree No. 69/2007/NĐ-CP paved the way for a foreign strategic institu-tional investor to purchase up to a maximum of 15%shares in a local bank from 2007, with total foreignholdings at any local bank capped at 30%. At thePrime Minister’s discretion the ownership of a for-eign strategic investor could be increased to 20%.This decree provided the necessary legal frameworkto entice foreign financial institutions to partiallyacquire Vietnamese local banks. As a result, thenumber of local banks with foreign strategic institu-tional investors holding at least a 5% stake (i.e. withforeign partial acquisition) has grown considerablyfrom just one in 2002 to 13 by 2014. Among others,expectedly, this strategy has provided opportunitiesfor local banks to develop new banking products,and to improve their managerial and technologicalcapacities.

The second key reforms relate to the privatizationof state-owned banks and the encouragement andsupport for the listing of all local banks on theVietnamese stock exchange. Government NoticeNo. 03/TB-VPCP indicates that the state intendedto reduce its ownership in banks by 49% by 2010. By2010, two of the five wholly state-owned banks hadbeen successfully privatized and listed on the stockexchange. Moreover, the number of local bankslisted on the stock exchange had increased fromtwo in 2006 to nine by 2014.

The Basel Accord on international bank capitalstandards has been shown to effectively mitigate ris-kiness in banks and improve efficiencies. In 2007,more than 100 countries worldwide had adoptedBasel I norms, and 95 countries intended to adoptBasel II, in some form, by 2015 (Sarma and Nikaidō2007). In line with this, a third key reform thatVietnam has embarked relates to the bolstering ofits banks’ capitalization. The central bank employstwo tools for measuring banks’ capital adequacy inVietnam: a minimum nominal amount of capital anda minimum capital adequacy ratio (a ratio of totalcapital to risk weighted assets). According to DecreeNo. 141/2006/NĐ-CP, all commercial banks musthold at least VND 3 trillion in capital in 2008, up

APPLIED ECONOMICS 3

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

from the prior minimum of VND 70 billion.However, of the 44 domestic commercial banks oper-ating in the Vietnamese banking system (5 state-owned banks, 4 joint-venture banks and 35 JSBs),only 20 meet the capital requirement by deadline.Therefore, the government extended this deadline to31 December 2011. Circular No. 13/2010/TT-NHNN,the central bank raised the minimum capital ade-quacy ratio to 9% in 2010 from 8% in 2005. Thiscapital raising leads to a change in capital ratio (ratioof total equity to total assets) in the Vietnamesebanks.

As previously stated, in this article, we focus onthe first two reforms – partial foreign acquisition oflocal banks and the listing of banks in theVietnamese stock markets as these two reformshave led to governance changes within banks. Bankreforms in Vietnam have been motivated byVietnam’s growing participation in internationalagreements and ongoing efforts to adopt interna-tional banking standards (FRBSF 2011). Thesereforms have made local banks operate in a morechallenging environment as foreign banks’ presencesignificantly increases and prudential ratios areenacted. For example, local banks have to competewith foreign banks which have better operatingexperience, capital capacity, banking technologyand corporate governance. They also have to meetsubstantially capital raising requirement in both legalcapital amount and capital adequacy ratio. Theexplanation is that banks’ capital grows after havingforeign partial acquisition, which may then expandtheir market power, and then enhance public’s con-fidence in these banks.

Foreign strategic shareholders can also transferadvanced corporate governance and modern bank-ing technology to local banks. In addition, publiclisting provides great opportunities for banks tohave new shareholders, supporting the success ofbanks’ equity rising. Market disciplines from publiclisting also force bank management to adopt cost-reducing practices. These two reforms appear tohave brought the most significant changes in corpo-rate governance in Vietnamese banks (Son, ThanhTu, and Hoang Yen 2014). However, it has beenshown in the literature that the effectiveness ofthese two reforms depends on the context of eachcountry, the method and organization of implement-ing these reforms. Also, reforming the banking

system would be much more difficult in developingcountries like Vietnam due to the lack of regulations,technology and institutional capacity which areneeded to reform the system (Son, Thanh Tu, andHoang Yen 2014). Therefore, our study, whichinvestigates the effects of the two reforms, foreignpartial acquisition and public listing, on the costefficiency of Vietnamese banks, provides significantpolicy implication for policy makers and bank man-agers in initiating strategy to strengthen the effi-ciency and stability of Vietnamese banks.

III. Related literature review

This section begins with an overview of the studiesconcerning the performance of Vietnamese banks,and then proceeds to the literature concerning theeffects of governance reforms on the performance ofinternational banks.

Existing banking studies covering Vietnaminclude four studies concerning economic efficiency:Vu and Turnell (2010), Gardener, Molyneux, andNguyen-Linh (2011), Nahm and Vu (2013) andNguyen, Roca, and Sharma (2014). Vu and Turnell(2010) applied a Bayesian stochastic frontierapproach and found that the Vietnamese bankingindustry faced a slight decrease in cost efficiencybetween 2000 and 2006, and that there was no effi-ciency differences between state-owned banks andJSBs. Gardener, Molyneux, and Nguyen-Linh(2011) employed a two-stage DEA approach toexplore the efficiency determinants of banks in fiveSouth East Asian countries (Indonesia, Malaysia, thePhilippines, Thailand and Vietnam). They reportedthat state-owned banks were more cost-efficient thanprivate banks. Cost efficiency was found to beaffected positively by capital ratio and economicgrowth, but negatively by size. Vu and Nahm(2013) explored the determinants of profit efficiencyof Vietnamese banks from 2000 to 2006 using a two-stage DEA approach. They found that profit effi-ciency decreased in the first half, but increased inthe second half of the study period, with moreprofit-efficient state-owned banks than JSBs. Theyalso reported that profit efficiency was driven posi-tively by size and GDP growth, and negatively bynon-performing loan ratio, capital ratio and infla-tion. Nguyen, Roca, and Sharma (2014) investigatedthe efficiency of Vietnamese banks over the 1995–

4 T. P. T. NGUYEN ET AL.

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

2011 period using a DEA Window Analysis. Theyfound that cost and profit efficiencies were 0.90 and0.75, respectively, and the efficiency of Vietnamesebanks displayed an upward trend over the analysisperiod. They also found that state-owned banks weremore efficient than JSBs in both cost and profitaspects.

It can be seen that studies on Vietnamese banksfocus on examining the efficiency level, efficiencytrend, efficiency gap between state-owned banksand JSBs, and efficiency effects of capital ratio. Themost common finding of these studies is that state-owned banks outperform JSBs. The findings on theremaining examined issues are contradictory. Onepossible reason is that few previous studies test forthe robustness of their results using different choicesof inputs/outputs and methodologies. Furthermore,no previous studies examine the effects of the twogovernance reforms, foreign partial acquisition andpublic listing, on the efficiency of Vietnamese banks.

The literature concerning the selection anddynamic effects of foreign partial acquisition andlisting on the stock exchange on the performanceof international banks is limited, and provides con-tradictory evidence as well. Specifically, Williamsand Nguyen (2005) employed a two-stage SFA toestimate efficiency scores and then investigated theselection and dynamic effects of reformingprograms, including foreign acquisition and privati-zation, on the efficiency of banks in South East Asia(Indonesia, Korea, Malaysia, Philippines andThailand) between 1990 and 2003. The authorsfound that, for profit efficiency, regarding the selec-tion effects, banks with foreign partial acquisitionwere more profit-efficient than banks without for-eign partial acquisition, while there was no profitefficiency difference between listed and non-listedbanks. Regarding the dynamic effects, they reportedthat foreign partial acquisition lowered profit effi-ciency in the short term, but enhanced profit effi-ciency in the long term, whereas listing policy hadno significant effect on profit efficiency in the shortterm, but brought efficiency gains in the long term.A different picture emerged from cost efficiency;banks with foreign partial acquisition or listedbanks were less cost-efficient than banks withoutforeign partial acquisition or non-listed banks,respectively. The effect of foreign partial acquisitionon cost efficiency was positive in the short term, but

negative in the long term, whilst listing strategyconveyed no cost efficiency advantage in both theshort and long term.

Lin and Zhang (2009) used four indicators –return on equity (ROE), return on assets (ROA),ratio of cost to income and ratio of non-performingloans to gross loans – to capture the performance ofChinese banks from 1997 to 2004, and then exam-ined the effects of reforms on the performance ofthese banks. They observed the existence of theselection effects in Chinese banks. In particular,banks with partial foreign acquisitions outperformedbanks without partial foreign acquisitions, and bankslisted on the stock exchange also performed betterthan non-listed banks. However, there was insuffi-cient evidence of the dynamic effects of foreignpartial acquisition and listing on the stock exchangeon the performance of Chinese banks in both theshort and long terms.

Jiang, Yao, and Feng (2013) employed a two-stageSFA to evaluate the efficiency effects of reforms inChinese banks from 1995 to 2010. The selectioneffects were documented in such a way that bankslisted on the Chinese stock exchange were more costand profit-efficient than non-listed banks; bankswith foreign partial acquisition were more profit-efficient than banks without partial foreign acquisi-tion. For the dynamic effects of foreign partial acqui-sition and listing on the stock exchange, theseauthors found that foreign partial acquisition led toefficiency losses in the short term, but efficiencygains in the long term; listing on the stock exchangeimproved cost efficiency in the short term, but thecost efficiency gains were not sustained in the longterm, while there were profit efficiency gains frompublic listing in both the short and long terms.

Burki and Ahmad (2010) investigated the effectsof governance reforms on the cost efficiency ofbanks in Pakistan from 1991 to 2005. Using theone-stage SFA approach, these authors found thatthere were insignificant selection effects of privatiza-tion, but a significant negative selection effect ofdomestic merger and acquisition (M&A).Compared to pre-privatization, the cost efficiencyof banks post-privatization was lower (significantshort-term dynamic effect). However, the cost effi-ciency of banks revealed an unclear trend sinceprivatization (insignificant long-term dynamiceffect). M&A had insignificant short-term and

APPLIED ECONOMICS 5

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

long-term dynamic effects on the cost efficiency ofbanks in Pakistan.

Perera, Skully, and Wickramanayake (2007)employed the two-stage SFA to obtain efficiencyscores of banks in Bangladesh, India, Pakistan andSri Lanka from 1997 to 2004, and then explored theselection effects of public listing in these banks. Theyreported that listed banks operated more efficientlythan non-listed banks, which is inconsistent with thefindings on Indian banks of Bhaumik and Dimova(2004) that there was no difference in performance(measured by ROA) between them. Choi and Hasan(2005) investigated the effects of foreign ownershipon bank performance in Korea. Using ROA to mea-sure performance, they found that there was a sta-tistically strong positive relationship between thepercentage of foreign ownership in a local bankand bank performance.

Overall, the literature on international banks indi-cates that there is a dearth of research regarding theselection and dynamic effects of foreign partialacquisition and public listing on bank performance.Furthermore, the findings from the reviewed studiesvary from one country to another and even from onestudy to another for the same country which couldbe due to differences in the employed efficiencyestimation methods and analysis periods and thedistinct characteristics of different banking systems.However, these reviewed banking studies commonlyfind the occurrence of selection effects in relation topartial foreign ownership and public listing – that isforeign investors carefully select the relatively moreefficient banks for partial acquisition and the gov-ernment cherry-pick the better performing banks togo public (i.e. foreign acquisition and public listingvariables can be endogenous). To the best of ourknowledge, there are no previous studies that exam-ine the potential endogeneity of variables such aspublic listing and foreign acquisition when examin-ing the effects of these factors on bank efficiency.

IV. Methodology

Efficiency estimation

In this section, we briefly describe the two efficiencyestimation techniques: SFA and DEA. We capture theperformance of Vietnamese banks by cost efficiency,which reflects how close a bank’s cost is to what a best-

practice bank’s cost would be given certain outputamounts and input prices, since it is one of the besteconomic foundations for analysing bank perfor-mance (Berger and Mester 1997; Williams 2004).

Stochastic frontier analysis (SFA)

SFA, proposed by Aigner et al. (1977) and Meeusenand Van den Broeck (1977), is a parametric techniquethat decomposes the residuals from an estimated costfrontier into a stochastic error term and an ineffi-ciency term. In this study, we adopt the translog(transcendental logarithmic) form which is the mostcommonly used functional form in the bank efficiencyliterature. We use the time trend (t) to representtechnological changes and apply the SFA estimationprocedures proposed by Battese and Coelli (1995).This study follows the intermediation approach forthe production of banking services, pioneered bySealey and Lindley (1977), which treats a bank as anintermediary using personnel and physical capital toconvert deposits into earning assets. Accordingly, thisstudy involves two outputs – net loans (Y1) and otherearning assets (Y2) – and three inputs – total funding(X1), fixed assets (X2) and personnel (X3) – as in thestudies by Gaganis and Pasiouras (2013), Duygun,Sena, and Shaban (2013), Lensink, Meesters, andNaaborg (2008) and many others. The prices of inputsX1–3 are financial capital price (W1), physical capitalprice (W2) and labour price (W3), respectively.

The translog stochastic cost frontier to estimatecost efficiency for the panel data is as follows:

lnTCit¼ α0þX2m¼1

αmlnYitmþ12

X2m¼1

X2

k¼1

αmklnYitmlnYitk

þX3n¼1

βnlnWitnþ12

X3n¼1

X3

l¼1

βnllnWitnlnWitl

þ12

X2m¼1

X3n¼1

βmnlnYitmlnWitnþγ1tþ12γ2t

2

þX2m¼1

γ2þm t lnYitmþX3n¼1

γ4þnt lnWitn

þðvitþuitÞ(1)

where the subscript i denotes the cross-sectionaldimension across banks, subscript t denotes the time

6 T. P. T. NGUYEN ET AL.

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

dimension. Parameters α, β, δ and γ of the costfunction capture the unknown technology of thebanking system and are estimated by maximum like-lihood method. TC is the observed total cost, whichconsists of interest expenses, other operatingexpenses and personnel expenses. The compositeerror term includes the random noise vit, which isassumed to follow a normal distribution, and thecost inefficiency uit, which is assumed to follow atruncated distribution.

By exploiting the linear homogeneity condition,Equation (1) can be transformed into a cost functionby normalizing the dependent variable and all inputprices by the price of input 3 (W3) as follows:

lnðTCit=Wit3Þ ¼ α0 þX2

m¼1αmlnYitm

þ 12

X2

m¼1

X2

k¼1αmklnYitmlnYitk

þX2

n¼1βnlnððWitn=Wit3Þ

þ 12

X2

n¼1

X2

l¼1βnllnðWitn=Wit3ÞlnðWitl=Wit3Þ

þ 12

X2

m¼1

X2

n¼1δmnlnYitmlnðWitn=Wit3Þ

þ γ1t þ12γ2t

2 þX2

m¼1γ2þmt lnYitm

þX2

n¼1γ4þnt lnðWitn=Wit3Þ þ vit þ uit

(2)

The individual cost efficiency scores are calculatedas CEit = exp(–uit). CE will range from 0 to 1, withgreater score indicating greater efficiency.

Data envelopment analysis (DEA)DEA, developed by Charnes, Cooper, and Rhodes(1978), is a non-parametric technique which usesthe linear programming technique to construct aset of best practices or frontier observations. Thevariable returns to scale cost minimization DEAmodel for estimating the cost efficiency of bank jfor period t is as follows (time subscript t isdropped for brevity):

MinXm

WjmXjm (3)

Subject to Xjm �Xi

Ximλi"m

Yjs �Xi

Yisλi"s

Xni¼1

λi ¼ 1

λ � 0

Where j = 1, 2, 3,. . ., n is the number of the bankswhich use a vector of m inputs Xi ¼ Xi1; . . . ;Ximð Þfor which they pay prices Wi ¼ Wi1; . . . ;Wimð Þ toproduce a vector of s outputs Yi ¼ Yi1; . . . ;Yisð Þ; λ isthe vector of input and output weights.

The solution to this model is the optimal inputdemand vector X�

j ¼ X�j1 . . . . . . ;X

�jm

� �, which mini-

mizes costs for bank j with the given input prices W,and is obtained from a linear combination of banksthat produces at least as much output as bank j does,using the same or less amount of input. The costefficiency of bank j (CEj) is calculated by the ratiobetween the optimal cost and the actual cost asfollows:

CEj ¼C�j

Cj¼

PmWjmX�

jmPmWjmXjm

(4)

The inputs and outputs employed in Equation (3)are the same as in Equation (1).

Efficiency effects of reforms

Once the cost efficiency of Vietnamese banks iscalculated, our next step is to regress these effi-ciency scores against a vector of explanatory vari-ables. Berger et al. (2005) developed a method thatsimultaneously examines the selection and dynamiceffects of governance changes on bank perfor-mance. This method has been employed in recentefficiency studies, such as Jiang, Yao, and Feng(2013), Lin and Zhang (2009) and Jiang, Yao, andZhang (2009). Our study follows this method toexamine the selection and dynamic effects of thetwo governance reforms, foreign partial acquisitionand public listing, on the cost efficiency of banks inVietnam as follows:

APPLIED ECONOMICS 7

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

Efficiency ¼ β1�Selection� Foreign Partial Acquisition

þ β2�Selection � Public Listing

þ β3�Short-term dynamic

� Foreign Partial Acquisition

þ β4�Short-termdynamic

� Public Listing

þ β5�Long-term dynamic

� Foreign Partial Acquisition

þ β6�Long-term dynamic

� Public Listingþ β7�Time

þ β8�10�Control Variablesþ Constant

þ Error Terms

(5)

One possible issue in estimating Equation (5) is thatforeign acquisition and public listing may be endo-genous. One source of endogeneity is omitted vari-able bias. In particular, the error terms in Equation(5) may include a vector of unobserved characteris-tics of individual banks (i.e. business culture, man-agement style) that affect both cost efficiency and theprobability of public listing and foreign acquisition.Thus, applying standard regressions to estimateEquation (5) may produce biased results.

We mitigate the potential endogeneity of PublicListing and Foreign Partial Acquisition variables inEquation (5) using a conditional mixed process see-mingly unrelated regression approach introduced byRoodman (2009). In particular, we estimate Equation(5) with two additional equations for two potentialendogenous variables:

Foreign partial acquisition ¼ f ðZ; εÞ (6)

Public listing ¼ gðX; ηÞ (7)

where f() and g() are link functions with relevantfunctional forms (probit regression in this case); Zand X are vectors of covariates, which may includesome variables in Equation (5); and ε and η are errorterms, which may include unobserved characteristicsof banks as the error term of Equation (5). Wecombine Equations (5)–(7) into a system of see-mingly unrelated equations and estimate this systemsimultaneously. Parameters in this system can beconsistently estimated equation by equation, but asimultaneous estimation that takes into account thefull covariance structure is, in general, more effi-cient. The correlation coefficients of error termsacross these three equations is denoted as ρs, andthe non-zero variance of the unobserved bank char-acteristics that may cause the error terms to becorrelated is denoted as δ2, the significance of δ2

and ρs can play the role of a test for endogeneity ofPublic Listing and Foreign Partial Acquisition vari-ables in Equation 5.

All independent variables are defined in Table 1.Selection dummy variables (‘Selection – ForeignPartial Acquisition’ and ‘Selection – Public Listing’)detect whether banks which are selected by foreignstrategic investors for partial acquisition and bankswhich are selected by the government for listing onthe stock exchange are more efficient than theircounterparts. Dynamic governance indicators in theshort term (‘Short-term dynamic – Foreign PartialAcquisition’ and ‘Short-term dynamic – PublicListing’) capture the short-run efficiency effects ofgovernance reforms, while dynamic governanceindicators in the long term (‘Long-term dynamic –Foreign Partial Acquisition’ and ‘Long-term

Table 1. Definition of variables in the model for the efficiency effects of reforms.Governance reform variablesSelection governance indicatorsSelection – Partial Foreign Acquisition Equals 1 for banks with foreign partial acquisition and 0 otherwiseSelection – Public Listing Equals 1 for listed banks and 0 otherwise

Dynamic governance indicators – short termShort-term dynamic – Partial Foreign Acquisition Equals 1 after foreign partial acquisition, 0 before acquisition and all other banksShort-term dynamic – Public Listing Equals 1 after listing banks on stock exchange, 0 before listing and all other banks

Dynamic governance indicators – long termLong-term dynamic – Partial Foreign Acquisition Number of years since partial foreign acquisition, 0 before partial acquisition and all other banksLong-term dynamic – Public Listing Number of years since listing on stock exchange, 0 before listing and all other banks

Control variablesTime Equals 1 in year 2000, 2 in year 2001 and so onState-owned bank Equals 1 for state-owned banks and 1 for joint-stock banksEquity to Total Assets Ratio of total equity to total assetsGDP growth Annual GDP growth rate

8 T. P. T. NGUYEN ET AL.

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

dynamic – Public Listing’) identify how the effectschange as time passes since the governance changes.Variable ‘Time’ explores the trend in cost efficiencyover the analysis period. Control variables includedummy bank ownership type variable (‘State-ownedbank’), bank capital (‘Capital ratio’) and annual GDPgrowth rate (‘GDP growth’).

The reviewed literature provides a clue as regardsthe occurrence of positive selection effects of foreignacquisition and public listing on bank performance.Therefore, it is expected that there are positive selec-tion effects of foreign partial acquisition and publiclisting on the cost efficiency of Vietnamese banks(i.e. β1 and β2 are expected to be positive). Onepossible explanation is that foreign investors arecareful when investing in banks in emerging mar-kets, and so they are likely to prefer banks that areable to keep costs under control. Moreover, since theVietnamese stock market started operation in 2000,the Vietnamese government tends to select betterbanks for public listing in order to attract privateinvestors, avoid failure of the banking reform anddevelop the stock market. Furthermore, the effects offoreign partial acquisition and public listing on thecost efficiency are expected to occur in the long termrather than in the short term (i.e. β5,6 are expected tobe positive), since it usually takes some time for theforeign shareholders and market discipline to exertsignificant influence on management behaviour. Stillfurther, despite the deregulating process, theVietnamese banking system is still a regulated sys-tem, and state-owned banks may receive favourabletreatment from the government. Therefore, state-owned banks are expected to be more cost-efficientthan JSBs.

Data

The data used in this study are collected fromInternational Bank Credit Analysis Ltd (Fitch-IBCA).

All data are cropped at the 0.5 and 99.5 percentilesto minimize the impacts of outliers on the efficiencyestimation. As a result, an unbalanced panel consistingof 32 banks over the period 2000–2014 is constructed;of which, there are 5 state-owned banks and 27 JSBs,13 banks partially acquired by the foreign strategicinvestors (banks which have foreign strategic institu-tional investors holding at least 5% of the chartercapital) and 9 banks listed on the stock exchange.The total number of observations in the sample is360, with 73 observations from state-owned banks,287 observations from JSBs, 156 observations frombanks with foreign partial acquisition and 118 obser-vations from listed banks (see Supplementary data).The average duration of being partially acquired byforeign institutions is 4.75 years and that of publiclisting is 3.8 years. The banks included in this datasetaccount for more than 85% of the deposits of theVietnamese banking system, with the brief descriptivestatistics of input and output variables for estimatingcost efficiency presented in Table 2. It can be seen thatover the period 2000–2014, Vietnamese banks rely onthe lending activities (data on outputs 1–2); the aver-age deposit interest rate is approximately 6.2% peryear; the average capital ratio is 10.93% and the aver-age GDP growth rate in Vietnam is 6.28% per year.

V. Empirical results

Operational efficiency

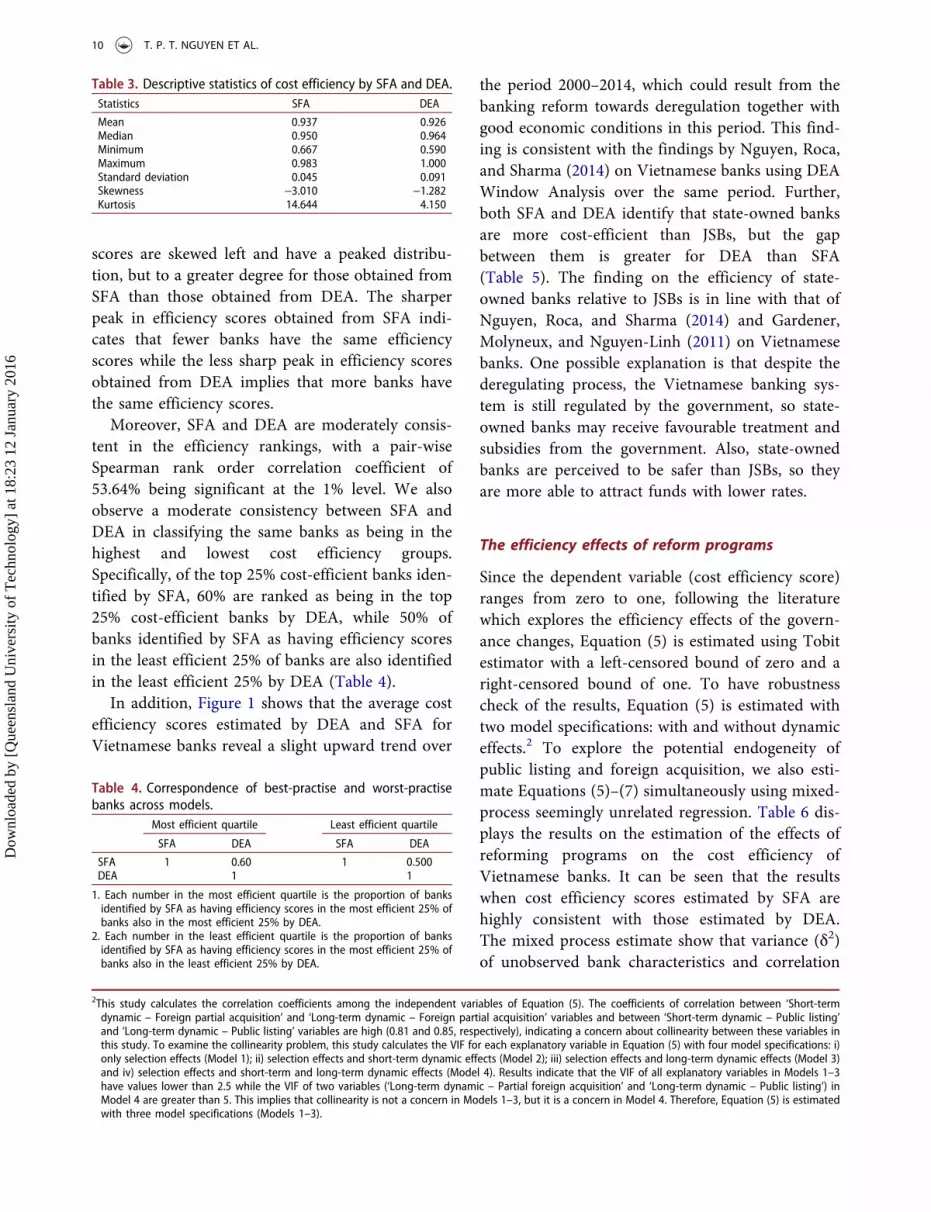

Table 3 shows descriptive statistics of cost efficiencyscores estimated by SFA and DEA. It can be seenthat SFA and DEA yield similar average efficiency(0.93), implying that the average Vietnamese bankcould reduce its costs by 7% by adopting the bestpractice. However, the efficiency scores estimated byDEA exhibit greater variability than those estimatedby SFA. Moreover, negative values for skewness andpositive values for kurtosis indicate that efficiency

Table 2. Descriptive statistics of variables used in the efficiency estimation.Variables Descriptions Mean

TC (total cost) The sum of interest expenses, other operating expenses and personnel expenses (thousand $US) 2978.54 (4471.61)Y1 (output 1) Net loans measured by gross loans minus reserves for impaired loans (thousand $US) 24979.66 (40,695.18)Y2 (output 2) Other earning assets measured by security investments and non-security investments (thousand $US) 13479.32 (16,789.16)W1 (price of input 1) Financial capital price calculated by the ratio of interest expenses to total funding 0.062 (0.026)W2 (price of input 2) Physical capital price computed by the ratio of other operating expenses to fixed assets 1.337 (1.486)W3 (price of input 3) Labour price which is proxied by the ratio of personnel expenses to total assets 0.007 (0.007)Equity to total assets Capital ratio measured by the ratio of total equity to total assets (%) 10.931 (7.971)GDP growth Annual GDP growth rate (%) 6.289 (0.755)

Standard deviation in parentheses.

APPLIED ECONOMICS 9

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

scores are skewed left and have a peaked distribu-tion, but to a greater degree for those obtained fromSFA than those obtained from DEA. The sharperpeak in efficiency scores obtained from SFA indi-cates that fewer banks have the same efficiencyscores while the less sharp peak in efficiency scoresobtained from DEA implies that more banks havethe same efficiency scores.

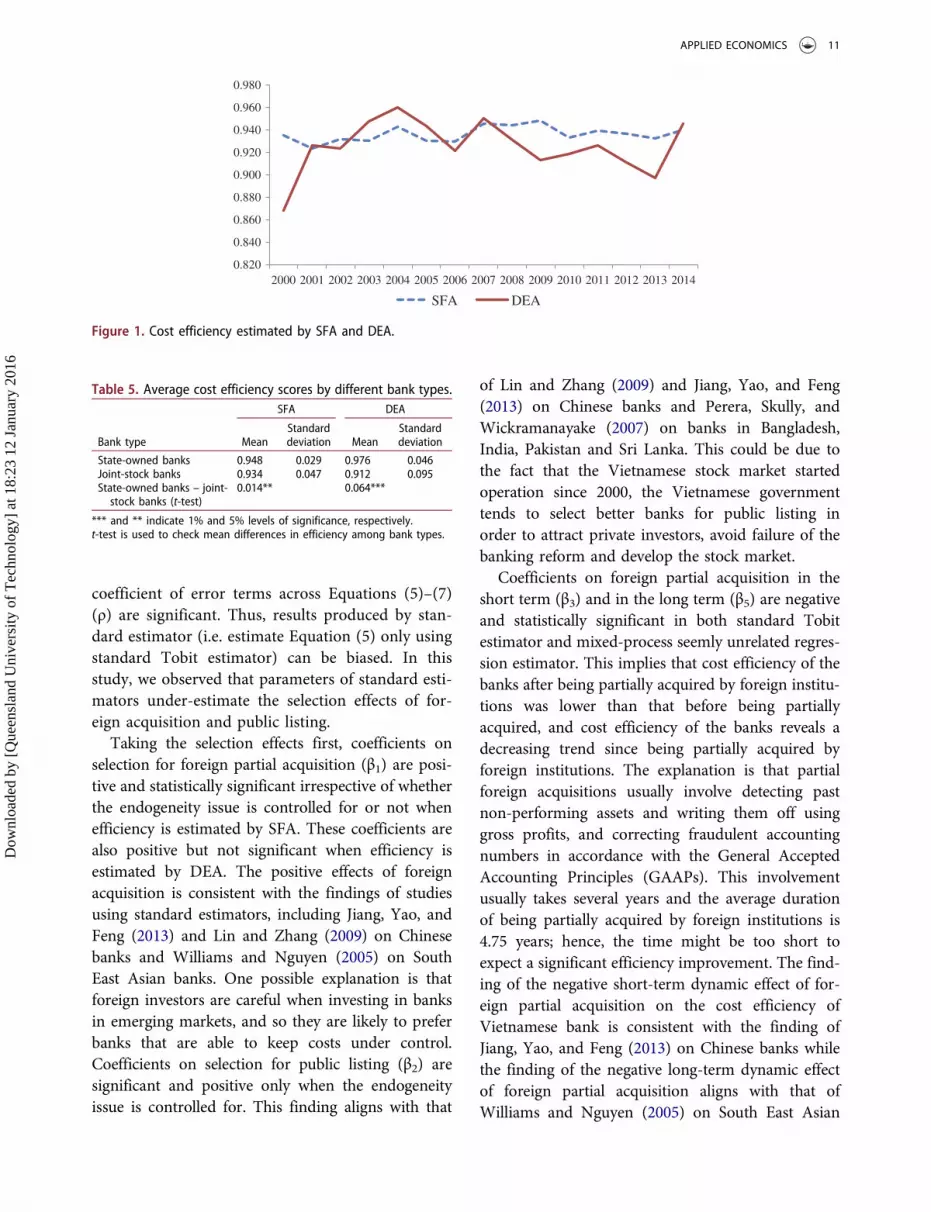

Moreover, SFA and DEA are moderately consis-tent in the efficiency rankings, with a pair-wiseSpearman rank order correlation coefficient of53.64% being significant at the 1% level. We alsoobserve a moderate consistency between SFA andDEA in classifying the same banks as being in thehighest and lowest cost efficiency groups.Specifically, of the top 25% cost-efficient banks iden-tified by SFA, 60% are ranked as being in the top25% cost-efficient banks by DEA, while 50% ofbanks identified by SFA as having efficiency scoresin the least efficient 25% of banks are also identifiedin the least efficient 25% by DEA (Table 4).

In addition, Figure 1 shows that the average costefficiency scores estimated by DEA and SFA forVietnamese banks reveal a slight upward trend over

the period 2000–2014, which could result from thebanking reform towards deregulation together withgood economic conditions in this period. This find-ing is consistent with the findings by Nguyen, Roca,and Sharma (2014) on Vietnamese banks using DEAWindow Analysis over the same period. Further,both SFA and DEA identify that state-owned banksare more cost-efficient than JSBs, but the gapbetween them is greater for DEA than SFA(Table 5). The finding on the efficiency of state-owned banks relative to JSBs is in line with that ofNguyen, Roca, and Sharma (2014) and Gardener,Molyneux, and Nguyen-Linh (2011) on Vietnamesebanks. One possible explanation is that despite thederegulating process, the Vietnamese banking sys-tem is still regulated by the government, so state-owned banks may receive favourable treatment andsubsidies from the government. Also, state-ownedbanks are perceived to be safer than JSBs, so theyare more able to attract funds with lower rates.

The efficiency effects of reform programs

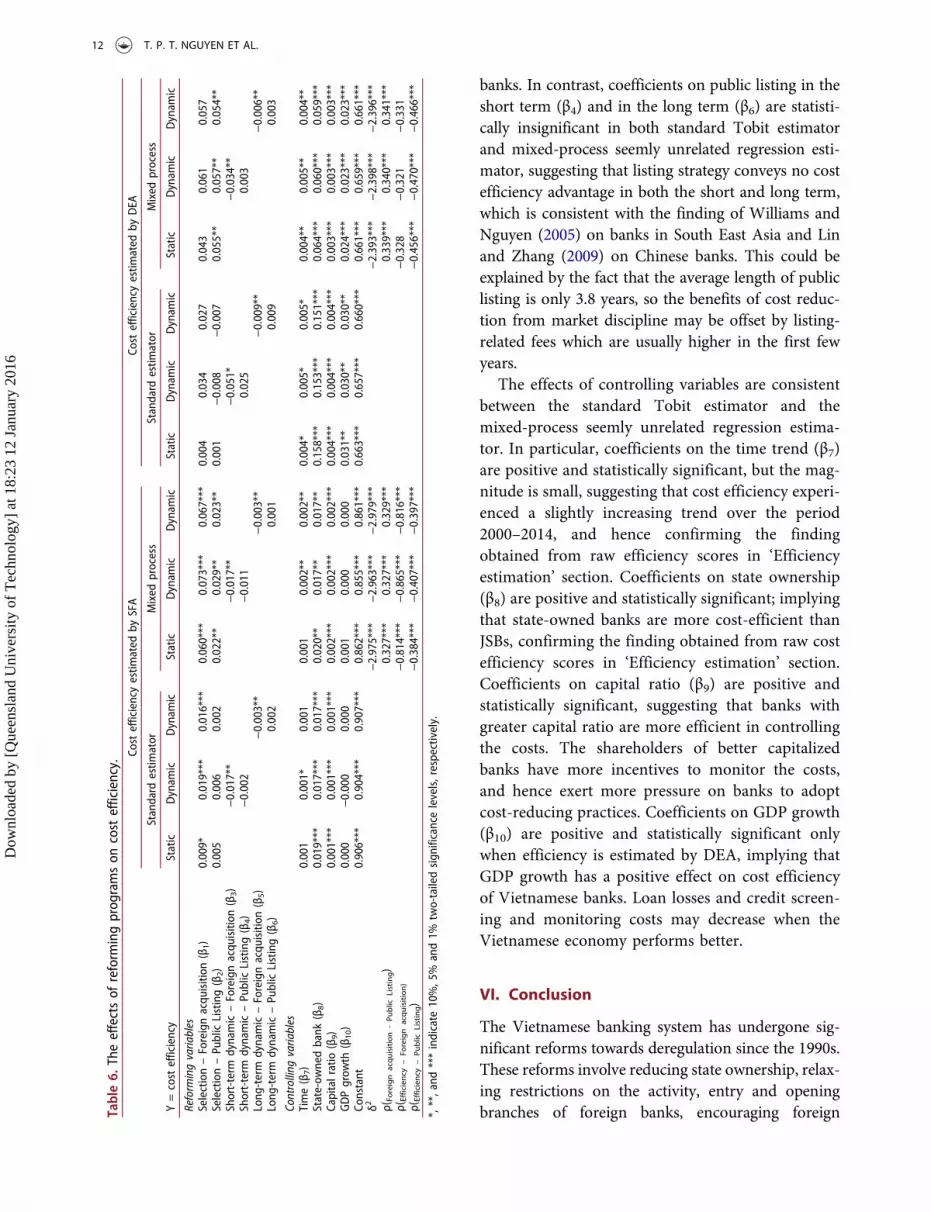

Since the dependent variable (cost efficiency score)ranges from zero to one, following the literaturewhich explores the efficiency effects of the govern-ance changes, Equation (5) is estimated using Tobitestimator with a left-censored bound of zero and aright-censored bound of one. To have robustnesscheck of the results, Equation (5) is estimated withtwo model specifications: with and without dynamiceffects.2 To explore the potential endogeneity ofpublic listing and foreign acquisition, we also esti-mate Equations (5)–(7) simultaneously using mixed-process seemingly unrelated regression. Table 6 dis-plays the results on the estimation of the effects ofreforming programs on the cost efficiency ofVietnamese banks. It can be seen that the resultswhen cost efficiency scores estimated by SFA arehighly consistent with those estimated by DEA.The mixed process estimate show that variance (δ2)of unobserved bank characteristics and correlation

Table 3. Descriptive statistics of cost efficiency by SFA and DEA.Statistics SFA DEA

Mean 0.937 0.926Median 0.950 0.964Minimum 0.667 0.590Maximum 0.983 1.000Standard deviation 0.045 0.091Skewness −3.010 −1.282Kurtosis 14.644 4.150

Table 4. Correspondence of best-practise and worst-practisebanks across models.

Most efficient quartile Least efficient quartile

SFA DEA SFA DEA

SFA 1 0.60 1 0.500DEA 1 1

1. Each number in the most efficient quartile is the proportion of banksidentified by SFA as having efficiency scores in the most efficient 25% ofbanks also in the most efficient 25% by DEA.

2. Each number in the least efficient quartile is the proportion of banksidentified by SFA as having efficiency scores in the most efficient 25% ofbanks also in the least efficient 25% by DEA.

2This study calculates the correlation coefficients among the independent variables of Equation (5). The coefficients of correlation between ‘Short-termdynamic – Foreign partial acquisition’ and ‘Long-term dynamic – Foreign partial acquisition’ variables and between ‘Short-term dynamic – Public listing’and ‘Long-term dynamic – Public listing’ variables are high (0.81 and 0.85, respectively), indicating a concern about collinearity between these variables inthis study. To examine the collinearity problem, this study calculates the VIF for each explanatory variable in Equation (5) with four model specifications: i)only selection effects (Model 1); ii) selection effects and short-term dynamic effects (Model 2); iii) selection effects and long-term dynamic effects (Model 3)and iv) selection effects and short-term and long-term dynamic effects (Model 4). Results indicate that the VIF of all explanatory variables in Models 1–3have values lower than 2.5 while the VIF of two variables (‘Long-term dynamic – Partial foreign acquisition’ and ‘Long-term dynamic – Public listing’) inModel 4 are greater than 5. This implies that collinearity is not a concern in Models 1–3, but it is a concern in Model 4. Therefore, Equation (5) is estimatedwith three model specifications (Models 1–3).

10 T. P. T. NGUYEN ET AL.

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

coefficient of error terms across Equations (5)–(7)(ρ) are significant. Thus, results produced by stan-dard estimator (i.e. estimate Equation (5) only usingstandard Tobit estimator) can be biased. In thisstudy, we observed that parameters of standard esti-mators under-estimate the selection effects of for-eign acquisition and public listing.

Taking the selection effects first, coefficients onselection for foreign partial acquisition (β1) are posi-tive and statistically significant irrespective of whetherthe endogeneity issue is controlled for or not whenefficiency is estimated by SFA. These coefficients arealso positive but not significant when efficiency isestimated by DEA. The positive effects of foreignacquisition is consistent with the findings of studiesusing standard estimators, including Jiang, Yao, andFeng (2013) and Lin and Zhang (2009) on Chinesebanks and Williams and Nguyen (2005) on SouthEast Asian banks. One possible explanation is thatforeign investors are careful when investing in banksin emerging markets, and so they are likely to preferbanks that are able to keep costs under control.Coefficients on selection for public listing (β2) aresignificant and positive only when the endogeneityissue is controlled for. This finding aligns with that

of Lin and Zhang (2009) and Jiang, Yao, and Feng(2013) on Chinese banks and Perera, Skully, andWickramanayake (2007) on banks in Bangladesh,India, Pakistan and Sri Lanka. This could be due tothe fact that the Vietnamese stock market startedoperation since 2000, the Vietnamese governmenttends to select better banks for public listing inorder to attract private investors, avoid failure of thebanking reform and develop the stock market.

Coefficients on foreign partial acquisition in theshort term (β3) and in the long term (β5) are negativeand statistically significant in both standard Tobitestimator and mixed-process seemly unrelated regres-sion estimator. This implies that cost efficiency of thebanks after being partially acquired by foreign institu-tions was lower than that before being partiallyacquired, and cost efficiency of the banks reveals adecreasing trend since being partially acquired byforeign institutions. The explanation is that partialforeign acquisitions usually involve detecting pastnon-performing assets and writing them off usinggross profits, and correcting fraudulent accountingnumbers in accordance with the General AcceptedAccounting Principles (GAAPs). This involvementusually takes several years and the average durationof being partially acquired by foreign institutions is4.75 years; hence, the time might be too short toexpect a significant efficiency improvement. The find-ing of the negative short-term dynamic effect of for-eign partial acquisition on the cost efficiency ofVietnamese bank is consistent with the finding ofJiang, Yao, and Feng (2013) on Chinese banks whilethe finding of the negative long-term dynamic effectof foreign partial acquisition aligns with that ofWilliams and Nguyen (2005) on South East Asian

0.820

0.840

0.860

0.880

0.900

0.920

0.940

0.960

0.980

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

SFA DEA

Figure 1. Cost efficiency estimated by SFA and DEA.

Table 5. Average cost efficiency scores by different bank types.

Bank type

SFA DEA

MeanStandarddeviation Mean

Standarddeviation

State-owned banks 0.948 0.029 0.976 0.046Joint-stock banks 0.934 0.047 0.912 0.095State-owned banks – joint-stock banks (t-test)

0.014** 0.064***

*** and ** indicate 1% and 5% levels of significance, respectively.t-test is used to check mean differences in efficiency among bank types.

APPLIED ECONOMICS 11

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

banks. In contrast, coefficients on public listing in theshort term (β4) and in the long term (β6) are statisti-cally insignificant in both standard Tobit estimatorand mixed-process seemly unrelated regression esti-mator, suggesting that listing strategy conveys no costefficiency advantage in both the short and long term,which is consistent with the finding of Williams andNguyen (2005) on banks in South East Asia and Linand Zhang (2009) on Chinese banks. This could beexplained by the fact that the average length of publiclisting is only 3.8 years, so the benefits of cost reduc-tion from market discipline may be offset by listing-related fees which are usually higher in the first fewyears.

The effects of controlling variables are consistentbetween the standard Tobit estimator and themixed-process seemly unrelated regression estima-tor. In particular, coefficients on the time trend (β7)are positive and statistically significant, but the mag-nitude is small, suggesting that cost efficiency experi-enced a slightly increasing trend over the period2000–2014, and hence confirming the findingobtained from raw efficiency scores in ‘Efficiencyestimation’ section. Coefficients on state ownership(β8) are positive and statistically significant; implyingthat state-owned banks are more cost-efficient thanJSBs, confirming the finding obtained from raw costefficiency scores in ‘Efficiency estimation’ section.Coefficients on capital ratio (β9) are positive andstatistically significant, suggesting that banks withgreater capital ratio are more efficient in controllingthe costs. The shareholders of better capitalizedbanks have more incentives to monitor the costs,and hence exert more pressure on banks to adoptcost-reducing practices. Coefficients on GDP growth(β10) are positive and statistically significant onlywhen efficiency is estimated by DEA, implying thatGDP growth has a positive effect on cost efficiencyof Vietnamese banks. Loan losses and credit screen-ing and monitoring costs may decrease when theVietnamese economy performs better.

VI. Conclusion

The Vietnamese banking system has undergone sig-nificant reforms towards deregulation since the 1990s.These reforms involve reducing state ownership, relax-ing restrictions on the activity, entry and openingbranches of foreign banks, encouraging foreignTa

ble6.

Theeffectsof

reform

ingprog

ramson

cost

efficiency.

Cost

efficiencyestim

ated

bySFA

Cost

efficiencyestim

ated

byDEA

Standard

estim

ator

Mixed

process

Standard

estim

ator

Mixed

process

Y=costefficiency

Static

Dynam

icDynam

icStatic

Dynam

icDynam

icStatic

Dynam

icDynam

icStatic

Dynam

icDynam

ic

Reform

ingvariables

Selection–Foreignacqu

isition

(β1)

0.009*

0.019***

0.016***

0.060***

0.073***

0.067***

0.004

0.034

0.027

0.043

0.061

0.057

Selection–PublicListing(β

2)0.005

0.006

0.002

0.022**

0.029**

0.023**

0.001

−0.008

−0.007

0.055**

0.057**

0.054**

Short-term

dynamic–Foreignacqu

isition

(β3)

−0.017**

−0.017**

−0.051*

−0.034**

Short-term

dynamic–PublicListing(β

4)−0.002

−0.011

0.025

0.003

Long

-term

dynamic–Foreignacqu

isition

(β5)

−0.003**

−0.003**

−0.009**

−0.006**

Long

-term

dynamic–PublicListing(β

6)0.002

0.001

0.009

0.003

Controlling

variables

Time(β

7)0.001

0.001*

0.001

0.001

0.002**

0.002**

0.004*

0.005*

0.005*

0.004**

0.005**

0.004**

State-ow

nedbank

(β8)

0.019***

0.017***

0.017***

0.020**

0.017**

0.017**

0.158***

0.153***

0.151***

0.064***

0.060***

0.059***

Capitalratio

(β9)

0.001***

0.001***

0.001***

0.002***

0.002***

0.002***

0.004***

0.004***

0.004***

0.003***

0.003***

0.003***

GDPgrow

th(β

10)

0.000

−0.000

0.000

0.001

0.000

0.000

0.031**

0.030**

0.030**

0.024***

0.023***

0.023***

Constant

0.906***

0.904***

0.907***

0.862***

0.855***

0.861***

0.663***

0.657***

0.660***

0.661***

0.659***

0.661***

δ2−2.975***

−2.963***

−2.979***

−2.393***

−2.398***

−2.396***

ρ( Foreignacquisition-Public

Listing)

0.327***

0.327***

0.329***

0.339***

0.340***

0.341***

ρ( Efficiency

–Foreignacquisition)

−0.814***

−0.865***

−0.816***

−0.328

−0.321

−0.331

ρ( Efficiency

–Public

Listing)

−0.384***

−0.407***

−0.397***

−0.456***

−0.470***

−0.466***

*,**,and

***indicate

10%,5

%and1%

two-tailedsign

ificancelevels,respectively.

12 T. P. T. NGUYEN ET AL.

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

institutional ownership in a local bank, stimulatingbanks to list on the stock exchange and raising bankcapital. Of which, there are two reforms which lead togovernance changes in the Vietnamese banking sys-tem, foreign partial acquisition and listing on the stockexchange. Therefore, this study attempted to: i) exam-ine the cost efficiency of Vietnamese banks over theperiod 2000–2014 to evaluate the effectiveness of thecombination of banking reforms in Vietnam; ii) inves-tigate the selection and dynamic effects of foreignpartial acquisition and listing on the stock exchangeon the cost efficiency of Vietnamese banks. Moreover,as policy makers can have greater confidence whenmaking policy decisions if policy implications fromdifferent methods are consistent, this study also checkswhether the two-stage SFA and the two-stage DEAyield the same results.

Using a dataset which consists of 32 Vietnamesebanks between 2000 and 2014, we observe that thetwo-stage SFA and two-stage DEA produce consis-tent results. Specifically, the first-stage efficiencyestimation indicates that the cost efficiency shows aslightly upward trend over the period 2000–2014,with the cost efficiency score being 0.93 and state-owned banks outperforming JSBs. The mixed pro-cess seemingly unrelated regression estimator whichcontrols the potential endogeneity of public listingand foreign acquisition in the second stage showsthat selection effects occur in the Vietnamese bank-ing system: banks selected by the strategic foreigninvestors for partial acquisition and banks selectedfor public listing are more cost-efficient than thosenot selected. The short-term and long-term dynamiceffects of foreign partial acquisition are documented:the cost efficiency of the Vietnamese banks post-partial acquisition is lower than prior-partial acqui-sition, and it experiences a decreasing trend sincepartial acquisition. However, the short-term andlong-term dynamic effects of public listing are notevidenced: the cost efficiency of the banks afterpublic listing is not statistically different from thatbefore public listing, and it also reveals an uncleartrend since public listing. Lastly, capital ratio andGDP growth has a positive effect on the cost effi-ciency of Vietnamese banks.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

Abbott, P., and F. Tarp. 2012. “Globalization Crises, Tradeand Development in Vietnam.” Journal of InternationalCommerce, Economics and Policy 3: 1–23. doi:10.1142/S1793993312400066.

Aigner, D., C. A. K. Lovell, and P. Schmidt. 1977.“Formulation and Estimation of Stochastic FrontierProduction Function Models.” Journal of Econometrics 6:21–37. doi:10.1016/0304-4076(77)90052-5.

Ariff,M., and L. Can. 2008. “Cost and Profit Efficiency of ChineseBanks: A Non-Parametric Analysis.” China Economic Review19: 260–273. doi:10.1016/j.chieco.2007.04.001.

Battese, G. E., and T. J. Coelli. 1995. “A Model for TechnicalInefficiency Effects in a Stochastic Frontier ProductionFunction for Panel Data.” Empirical Economics 20: 325–332. doi:10.1007/BF01205442.

Berger, A. N., G. R. G. Clarke, R. Cull, L. Klapper, and G. F.Udell. 2005. “Corporate Governance and BankPerformance: A Joint Analysis of the Static, Selection,and Dynamic Effects of Domestic, Foreign, and StateOwnership.” Journal of Banking & Finance 29: 2179–2221. doi:10.1016/j.jbankfin.2005.03.013.

Berger, A. N., and L. J. Mester. 1997. “Inside the Black Box:What Explains Differences in the Efficiencies of FinancialInstitutions?” Journal of Banking & Finance 21: 895–947.doi:10.1016/S0378-4266(97)00010-1.

Bhaumik, S. K., and R. Dimova. 2004. “How Important IsOwnership in a Market with Level Playing Field?: TheIndian Banking Sector Revisited.” Journal of ComparativeEconomics 32: 165–180. doi:10.1016/j.jce.2003.12.001.

Burki, A. A., and S. Ahmad. 2010. “Bank GovernanceChanges in Pakistan: Is There a Performance Effect?”Journal of Economics and Business 62: 129–146.doi:10.1016/j.jeconbus.2009.08.002.

Chaponnière, J.-R., J.-P. Cling, and B. Zhou. 2007. “Vietnamfollowing in China’s Footsteps: The Third Wave ofEmerging Asian Economies.” WIDER Conference onSouthern Engines of Global Growth: China, India, Braziland South Africa, Helsinki, September 7–8.

Charnes, A., W. W. Cooper, and E. Rhodes. 1978.“Measuring the Efficiency of Decision Making Units.”European Journal of Operational Research 2: 429–444.doi:10.1016/0377-2217(78)90138-8.

Choi, S., and I. Hasan. 2005. “Ownership, Governance, andBank Performance: Korean Experience.” FinancialMarkets, Institutions & Instruments 14: 215–242.doi:10.1111/fmii.2005.14.issue-4.

Chunhachinda, P., and L. Li. 2010. “Efficiency of ThaiCommercial Banks: Pre-Vs. Post-1997 Financial Crisis.”Review of Pacific Basin Financial Markets and Policies 13:417–447. doi:10.1142/S0219091510002013.

Dacanay, S. J. O., III. 2011. “The Evolution of Cost and ProfitEfficiency of Philippine Commercial Banks.” PhilippineReview of Economics 47: 109–146.

Delis, M. D., A. Koutsomanoli-Fillipaki, C. K. Staikouras,and G. Katerina. 2009. “Evaluating Cost and Profit

APPLIED ECONOMICS 13

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16

Efficiency: A Comparison of Parametric andNonparametric Methodologies.” Applied FinancialEconomics 19: 191–202. doi:10.1080/09603100801935370.

Dong, Y., R. Hamilton, and M. Tippett. 2014. “CostEfficiency of the Chinese Banking Sector: A Comparisonof Stochastic Frontier Analysis and Data EnvelopmentAnalysis.” Economic Modelling 36: 298–308. doi:10.1016/j.econmod.2013.09.042.

Duygun, M., V. Sena, and M. Shaban. 2013. “SchumpeterianCompetition and Efficiency among Commercial Banks.”Journal of Banking & Finance 37: 5176–5185. doi:10.1016/j.jbankfin.2013.07.003.

FRBSF. 2011. Banking Reform in Vietnam. San Francisco,CA: Asia Focus Country Analysis Unit, Federal ReserveBank of San Francisco.

Gaganis, C., and F. Pasiouras. 2013. “Financial SupervisionRegimes and Bank Efficiency: International Evidence.”Journal of Banking & Finance 37: 5463–5475.doi:10.1016/j.jbankfin.2013.04.026.

Gardener, E., P. Molyneux, and H. Nguyen-Linh. 2011.“Determinants of Efficiency in South East AsianBanking.” The Service Industries Journal 31: 2693–2719.doi:10.1080/02642069.2010.512659.

Huang, T.-H., and M.-H. Wang. 2002. “Comparison ofEconomic Efficiency Estimation Methods:Parametric and Non-Parametric Techniques.” TheManchester School 70: 682–709. doi:10.1111/manc.2002.70.issue-5.

Jiang, C., S. Yao, and G. Feng. 2013. “Bank Ownership,Privatization, and Performance: Evidence from aTransition Country.” Journal of Banking & Finance 37:3364–3372. doi:10.1016/j.jbankfin.2013.05.009.

Jiang, C., S. Yao, and Z. Zhang. 2009. “The Effects ofGovernance Changes on Bank Efficiency in China: AStochastic Distance Function Approach.” China EconomicReview 20: 717–731. doi:10.1016/j.chieco.2009.05.005.

Lensink, R., A. Meesters, and I. Naaborg. 2008. “BankEfficiency and Foreign Ownership: Do Good InstitutionsMatter?” Journal of Banking & Finance 32: 834–844.doi:10.1016/j.jbankfin.2007.06.001.

Lin, X., and Y. Zhang. 2009. “Bank Ownership Reform andBank Performance in China.” Journal of Banking &Finance 33: 20–29. doi:10.1016/j.jbankfin.2006.11.022.

Meeusen, W., and J. Van den Broeck. 1977. “EfficiencyEstimation from Cobb-Douglas Production Functionswith Composed Error.” International Economic Review18: 435–444. doi:10.2307/2525757.

Nahm, D., and H. Vu. 2013. “Profit Efficiency andProductivity of Vietnamese Banks: A New IndexApproach.” Journal of Applied Finance & Banking 3: 45–65.

Nguyen, T. P. T., E. Roca, and P. Sharma. 2014. “HowEfficient Is the Banking System of Asia’s NextEconomic Dragon? Evidence from Rolling DEAWindows.” Applied Economics 46: 2665–2684.doi:10.1080/00036846.2014.909578.

Orden, D., F. Cheng, H. Nguyen, U. Grote, M. Thomas, K.Mullen, and D. Sun. 2007. “Agricultural Producer SupportEstimates for Developing Countries: Measurement Issuesand Evidence from India, Indonesia, China, andVietnam.” IFPRI Research Report 152. Washington, DC:International Food Policy Research Institute.

Perera, S., M. Skully, and J. Wickramanayake. 2007. “CostEfficiency in South Asian Banking: The Impact of BankSize, State Ownership and Stock Exchange Listings.”International Review of Finance 7: 35–60. doi:10.1111/j.1468-2443.2007.00067.x.

Pomfret, R. 2013. “ASEAN’s New Frontiers: Integrating theNewest Members into the ASEAN EconomicCommunity.” Asian Economic Policy Review 8: 25–41.doi:10.1111/aepr.12000.

Roodman, D. 2009. “Fitting Fully Observed Recursive MixedProcess Model with CMP.” The Stata Journal 11: 159–206.

Sahoo, B. K., and A. Mandal. 2011. “Examining thePerformance of Banks in India: Post Transition Period.”The IUP Journal of Bank Management 10: 7–31.

Sarma, M., and Y. Nikaidō. 2007.” Capital Adequacy Regimein India: An Overview.” Working Paper No. 196. NewDelhi: Indian Council for Research on InternationalEconomic Relations.

Sealey, C. W., and J. T. Lindley. 1977. “Inputs, Outputs, and aTheory of Production and Cost at Depository FinancialInstitutions.” The Journal of Finance 32: 1251–1266.doi:10.1111/j.1540-6261.1977.tb03324.x.

Son, N. H., T. Thanh Tu, and T. T. Hoang Yen. 2014. “BankRestructuring–International Perspectives and VietnamPractices.” Accounting and Finance Research 3: 36–50.doi:10.5430/afr.v3n2p36.

Vu, H., and D. Nahm. 2013. “The Determinants of ProfitEfficiency of Banks in Vietnam.” Journal of the Asia PacificEconomy 18: 615–631. doi:10.1080/13547860.2013.803847.

Vu, H. T., and S. Turnell. 2010. “Cost Efficiency of the BankingSector in Vietnam: A Bayesian Stochastic Frontier Approachwith Regularity Constraints.” Asian Economic Journal 24:115–139. doi:10.1111/j.1467-8381.2010.02035.x.

Wadud, A., and B. White. 2000. “Farm Household Efficiencyin Bangladesh: A Comparison of Stochastic Frontier andDEA Methods.” Applied Economics 32: 1665–1673.doi:10.1080/000368400421011.

Weill, L. 2004. “Measuring Cost Efficiency in EuropeanBanking: A Comparison of Frontier Techniques.” Journalof Productivity Analysis 21: 133–152. doi:10.1023/B:PROD.0000016869.09423.0c.

Williams, J. 2004. “Determining Management Behaviour inEuropean Banking.” Journal of Banking & Finance 28:2427–2460. doi:10.1016/j.jbankfin.2003.09.010.

Williams, J., and N. Nguyen. 2005. “Financial Liberalisation,Crisis, and Restructuring: A Comparative Study of BankPerformance and Bank Governance in South East Asia.”Journal of Banking & Finance 29: 2119–2154. doi:10.1016/j.jbankfin.2005.03.011.

14 T. P. T. NGUYEN ET AL.

Dow

nloa

ded

by [

Que

ensl

and

Uni

vers

ity o

f T

echn

olog

y] a

t 18:

23 1

2 Ja

nuar

y 20

16