Embed Size (px)

Citation preview

Faculty of Public Accountign and Administration

Mr. Marco Arguiropulos

Student. Abdón Isai Rivera González

Group. 3Ai

ID. 1634292

Autonomous University of Nuevo León

International Business Program Auditing

Learning Project Integrator

Faculty of Public Accountign and Administration

Autonomous University of Nuevo León

International Business Program

Learning Project Integrator

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of financial Statements Of July 2013Index

ReferencesJournal Entries

T-AccountsTrial Balance

Integral Income StatementSCHOE

Balance SheetPlan the audit

ABCDEFG

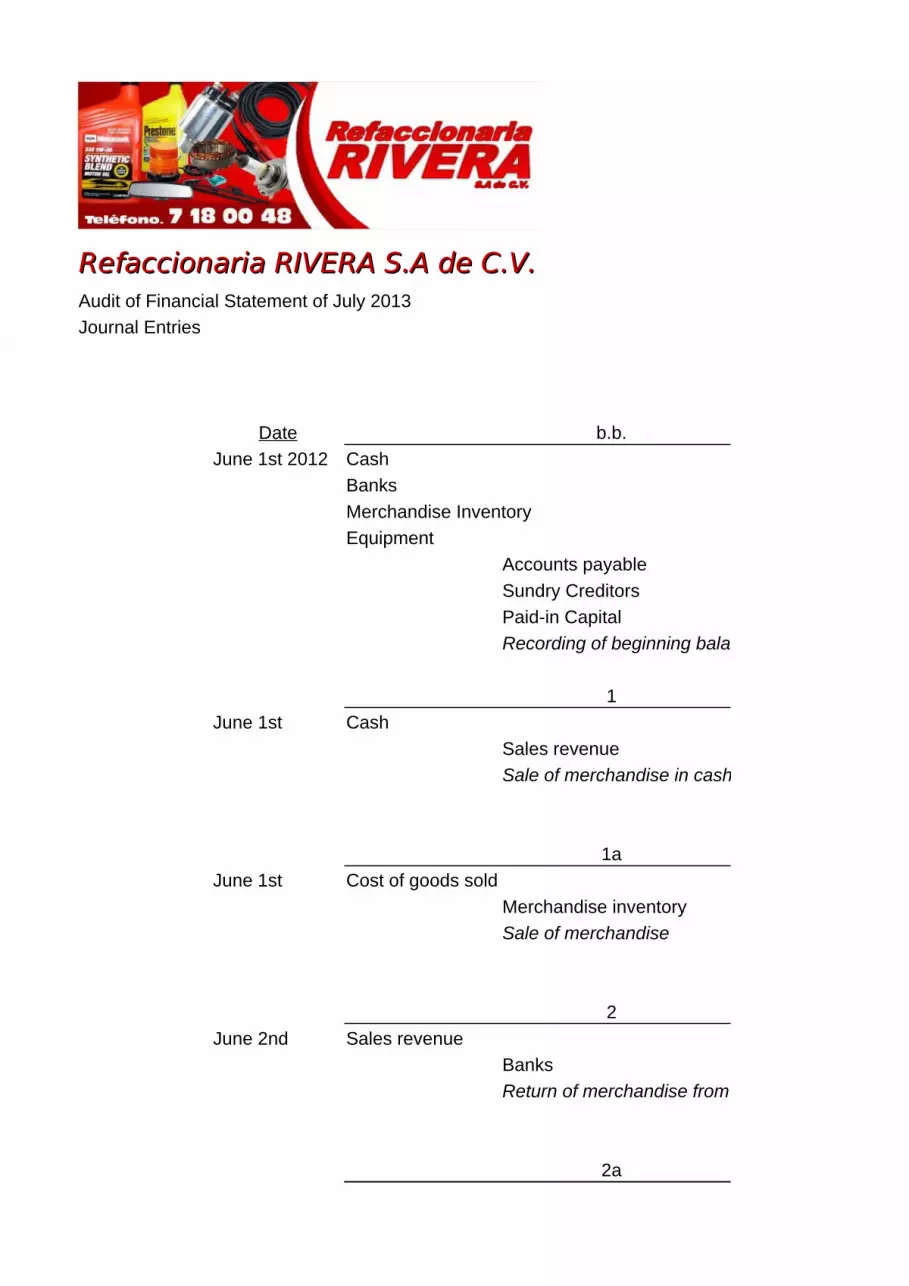

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013Journal Entries

Date b.b.June 1st 2012 Cash

BanksMerchandise InventoryEquipment

Accounts payableSundry CreditorsPaid-in CapitalRecording of beginning balances

1June 1st Cash

Sales revenueSale of merchandise in cash

1aJune 1st Cost of goods sold

Merchandise inventorySale of merchandise

2June 2nd Sales revenue

BanksReturn of merchandise from a sale

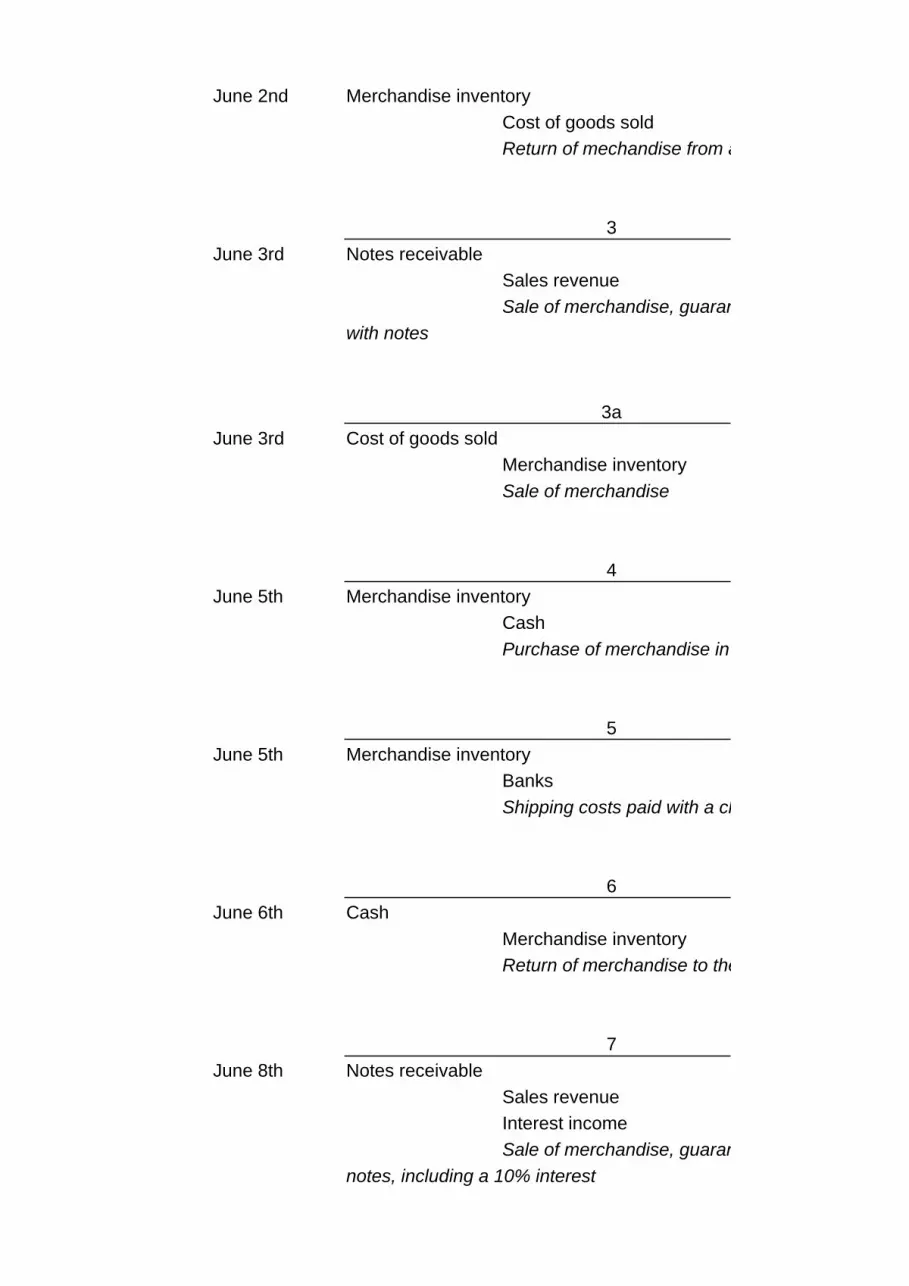

2a

June 2nd Merchandise inventoryCost of goods soldReturn of mechandise from a sale

3June 3rd Notes receivable

Sales revenueSale of merchandise, guaranteed

with notes

3aJune 3rd Cost of goods sold

Merchandise inventorySale of merchandise

4June 5th Merchandise inventory

CashPurchase of merchandise in cash

5June 5th Merchandise inventory

BanksShipping costs paid with a check

6June 6th Cash

Merchandise inventoryReturn of merchandise to the supplier

7June 8th Notes receivable

Sales revenueInterest incomeSale of merchandise, guaranteed with

notes, including a 10% interest

7aJune 8th Cost of goods sold

Merchandise inventorySale of merchandise

8June 10th Equipment

CashSundry creditorsPurchase of equipment, 50% on credit

9June 11th Merchandise inventory

Interest expenseBanksNotes payablePurchase of merchandise, 50% guaranteed

with a note, including a 10% interest10

June 12th Computer equipmentCashNotes payablePurchase of computer equipment, 50%

guaranteed with a note11

June 15th CashSales revenue

Sales revenueSale of merchandise, including a 10%

discount11a

June 15th Cost of goods soldMerchandise inventorySale of merchandise

12June 15th Accounts receivable

Sales revenueSale of merchandise on credit

12aJune 15th Cost of goods sold

Merchandise inventorySale of merchandise

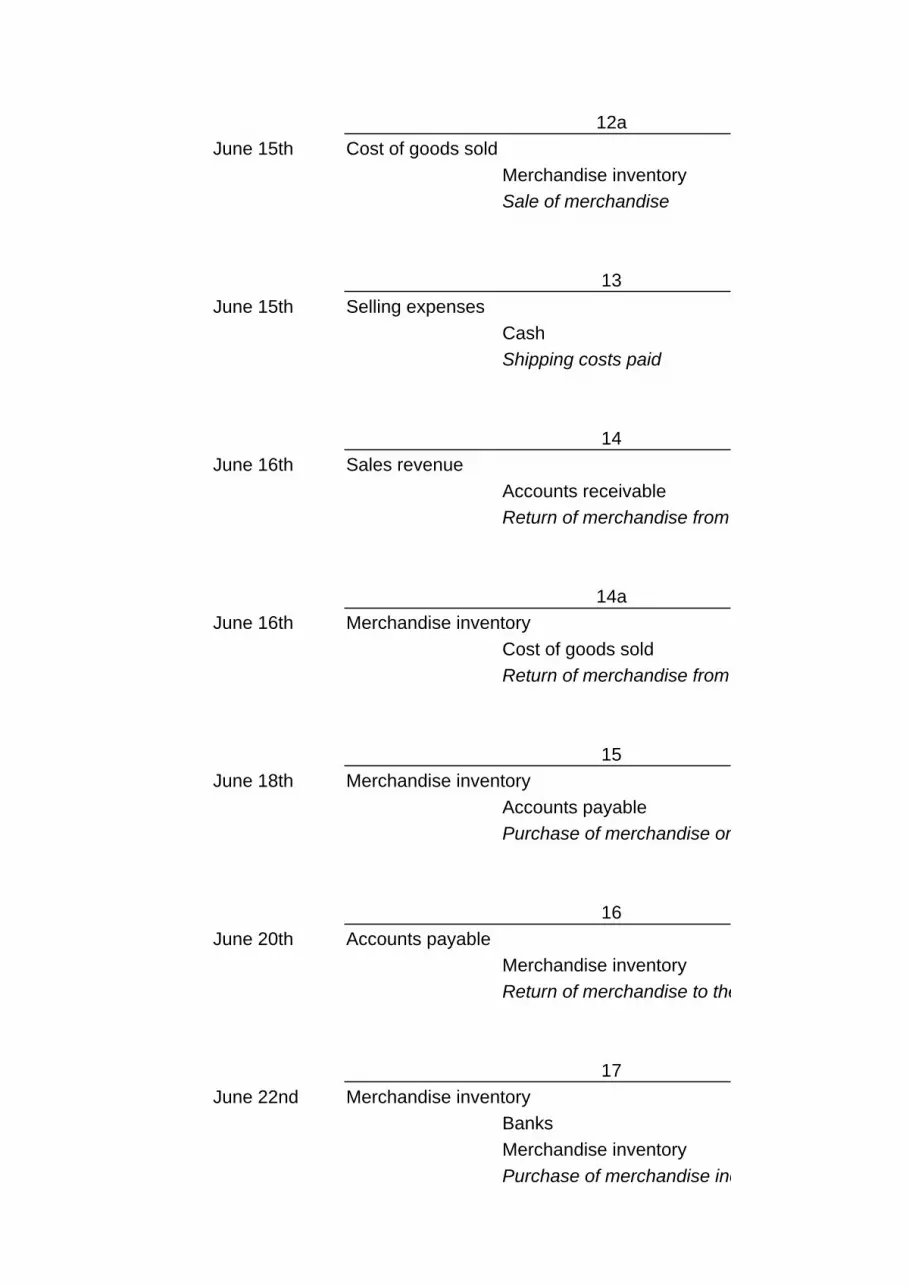

13June 15th Selling expenses

CashShipping costs paid

14June 16th Sales revenue

Accounts receivableReturn of merchandise from a sale on credit

14aJune 16th Merchandise inventory

Cost of goods soldReturn of merchandise from a sale

15June 18th Merchandise inventory

Accounts payablePurchase of merchandise on credit

16June 20th Accounts payable

Merchandise inventoryReturn of merchandise to the supplier

17June 22nd Merchandise inventory

BanksMerchandise inventoryPurchase of merchandise including a 10%

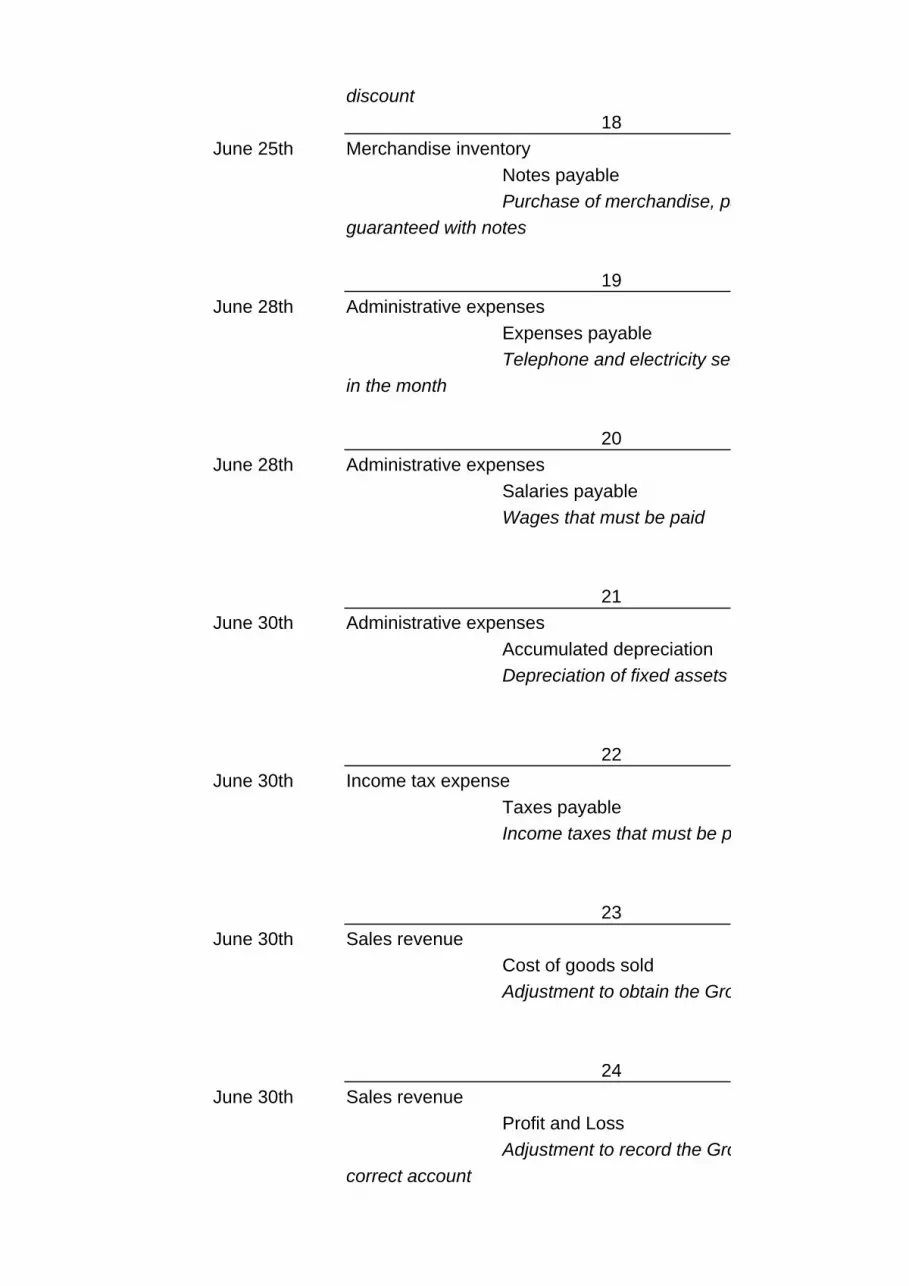

discount18

June 25th Merchandise inventoryNotes payablePurchase of merchandise, payment

guaranteed with notes

19June 28th Administrative expenses

Expenses payableTelephone and electricity services accrued

in the month

20June 28th Administrative expenses

Salaries payableWages that must be paid

21June 30th Administrative expenses

Accumulated depreciationDepreciation of fixed assets in the month

22June 30th Income tax expense

Taxes payableIncome taxes that must be paid

23June 30th Sales revenue

Cost of goods soldAdjustment to obtain the Gross Profit

24June 30th Sales revenue

Profit and LossAdjustment to record the Gross Profit in the

correct account

Equal amounts

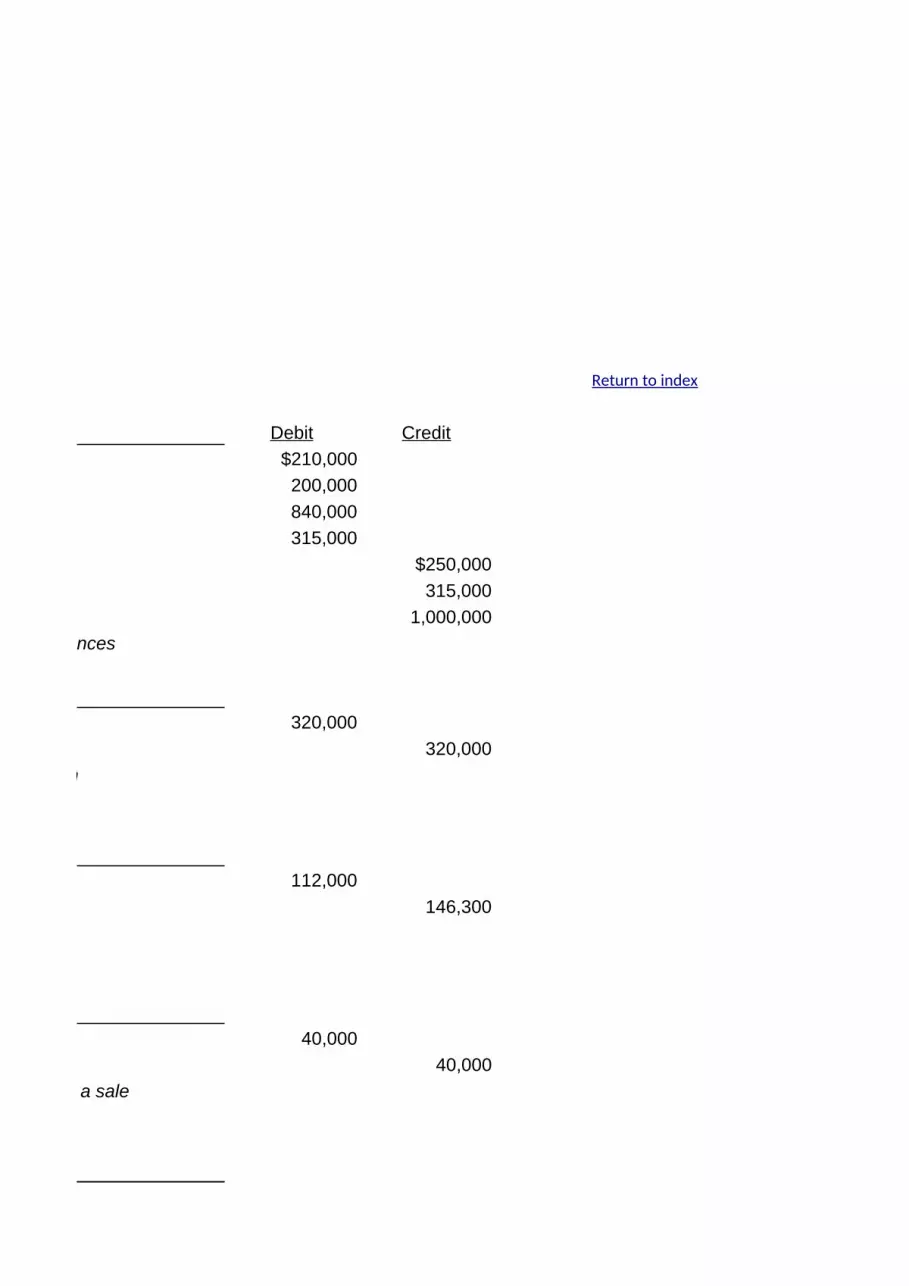

b.b. Debit Credit$210,000200,000840,000315,000

$250,000315,000

1,000,000Recording of beginning balances

1320,000

320,000Sale of merchandise in cash

1a112,000

146,300

240,000

40,000Return of merchandise from a sale

2a

Return to index

14,00029,750

Return of mechandise from a sale

3200,000

200,000Sale of merchandise, guaranteed

3a63,000

63,000

4100,000

100,000Purchase of merchandise in cash

55,000

5,000Shipping costs paid with a check

610,000

10,000Return of merchandise to the supplier

7330,000

300,00030,000

Sale of merchandise, guaranteed with

7a118,000

118,000

8200,734

100,367100,367

Purchase of equipment, 50% on credit

9260,000

13,000130,000143,000

Purchase of merchandise, 50% guaranteed

1048,000

24,00024,000

Purchase of computer equipment, 50%

11256,914

28,546285,460

Sale of merchandise, including a 10%

11a92,300

92,300

12102,000

102,000Sale of merchandise on credit

12a30,000

30,000

1310,000

10,000

146,000

6,000Return of merchandise from a sale on credit

14a1,764

1,764Return of merchandise from a sale

1550,000

50,000Purchase of merchandise on credit

1620,000

20,000Return of merchandise to the supplier

1790,000

81,0009,000

Purchase of merchandise including a 10%

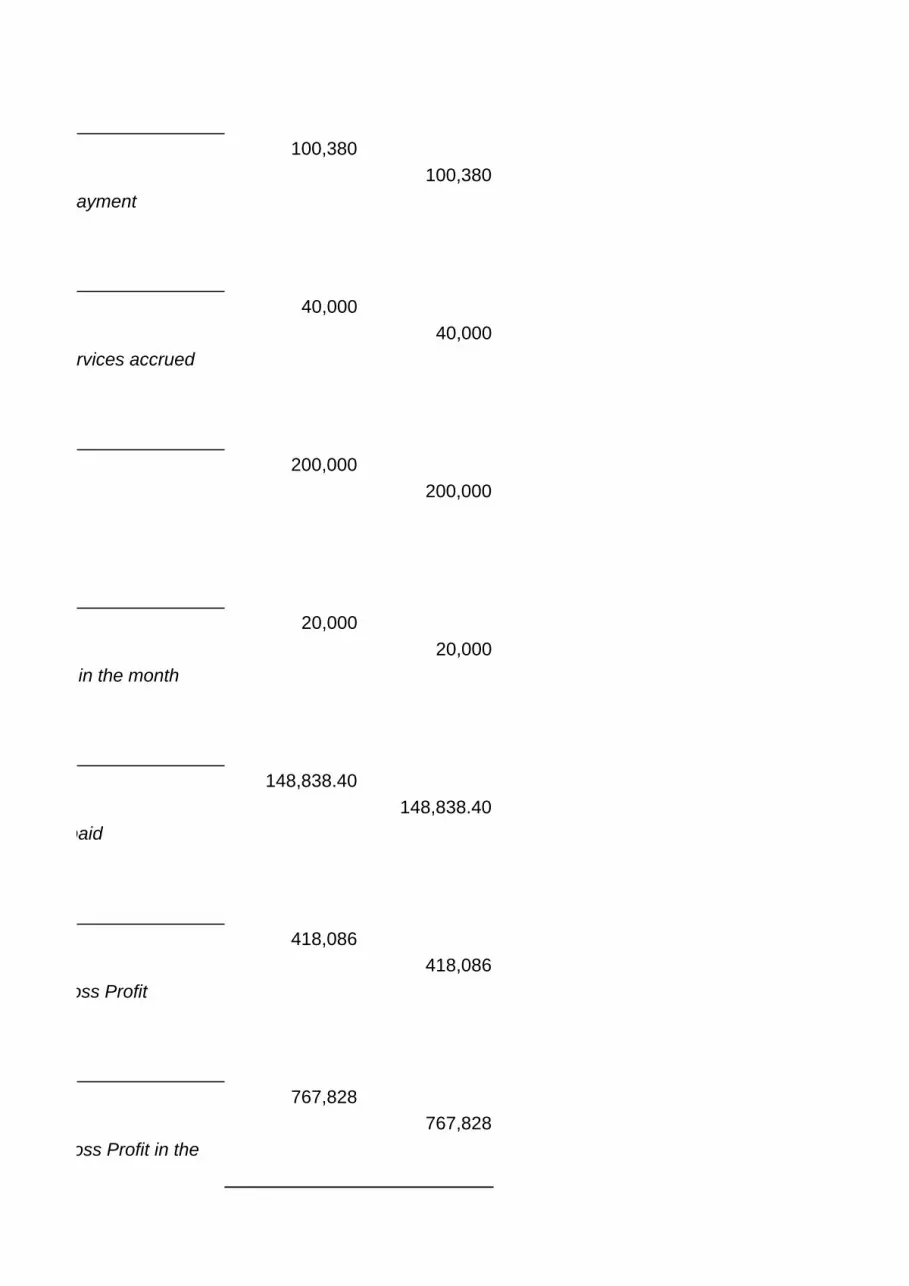

18100,380

100,380Purchase of merchandise, payment

$50,050.00

1940,000

40,000Telephone and electricity services accrued

20200,000

200,000

2120,000

20,000Depreciation of fixed assets in the month

22148,838.40

148,838.40Income taxes that must be paid

23418,086

418,086Adjustment to obtain the Gross Profit

24767,828

767,828Adjustment to record the Gross Profit in the

$5,831,440.40 $5,831,440.40

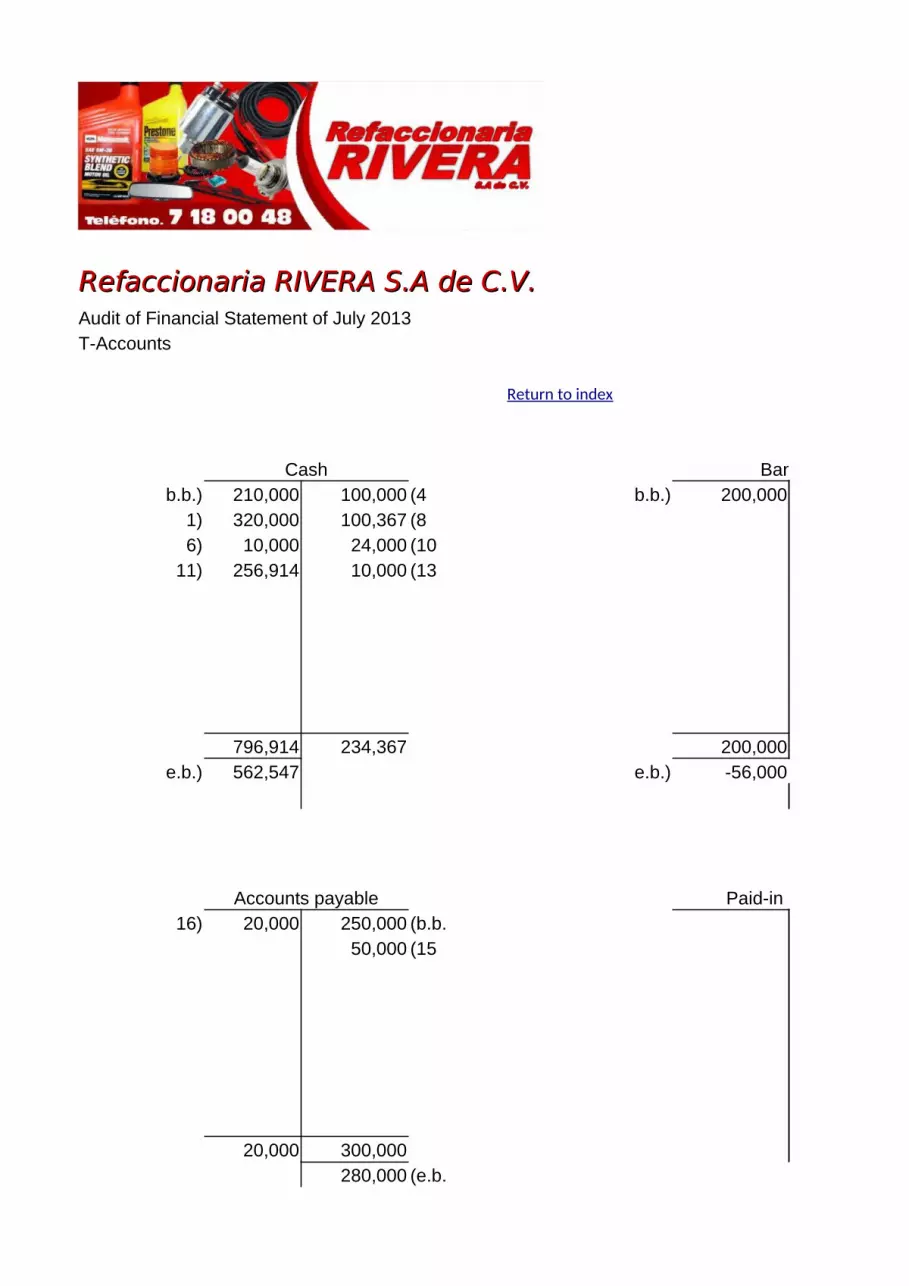

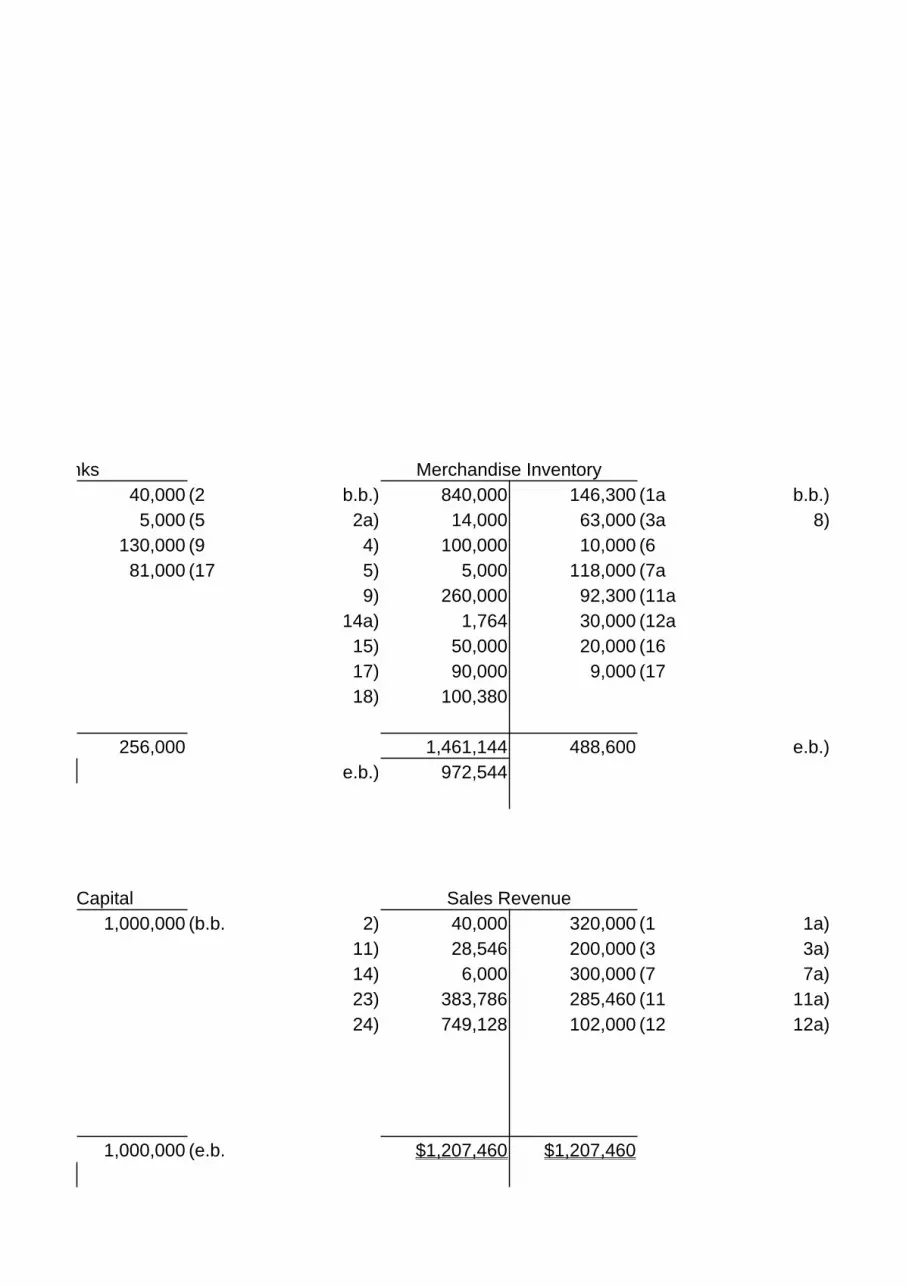

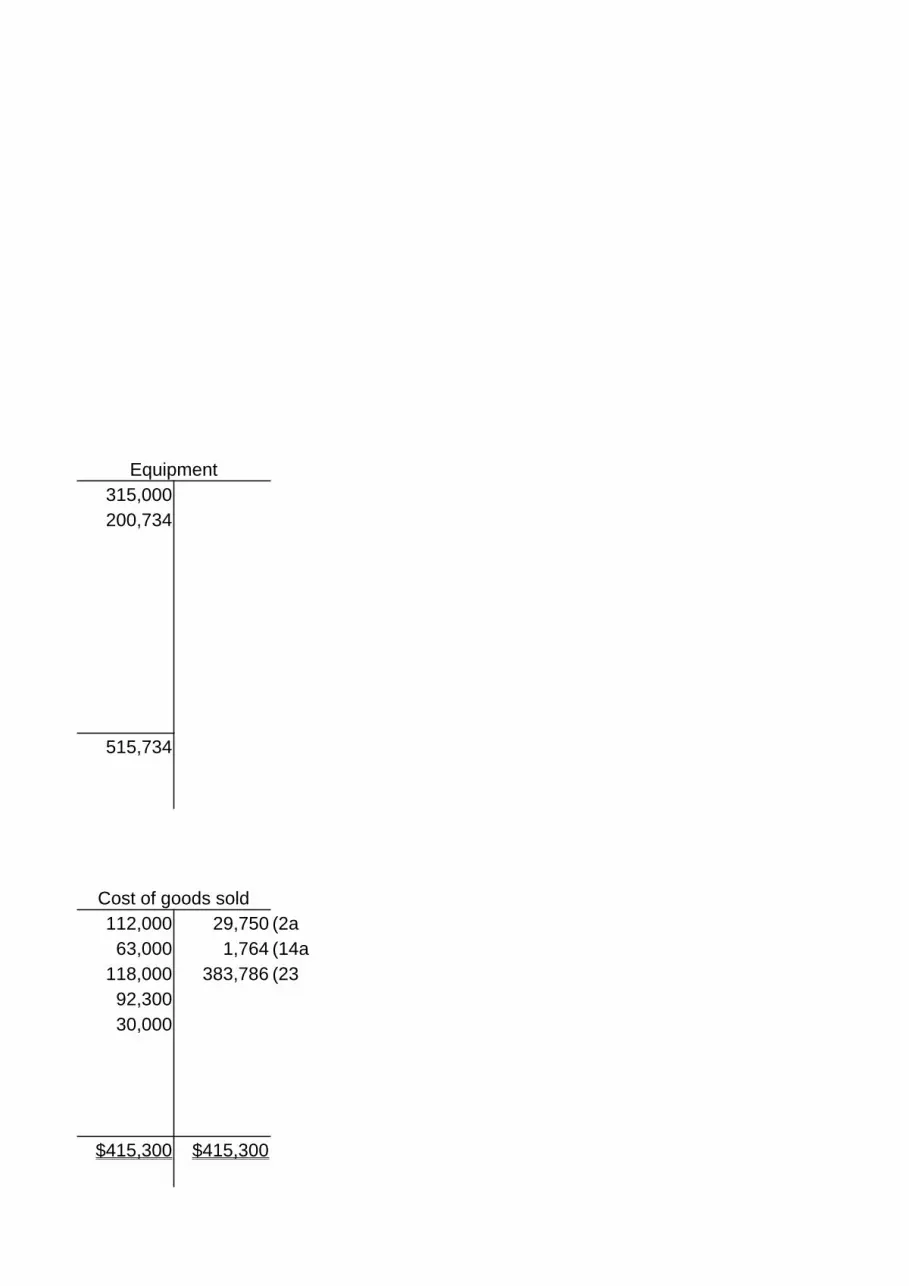

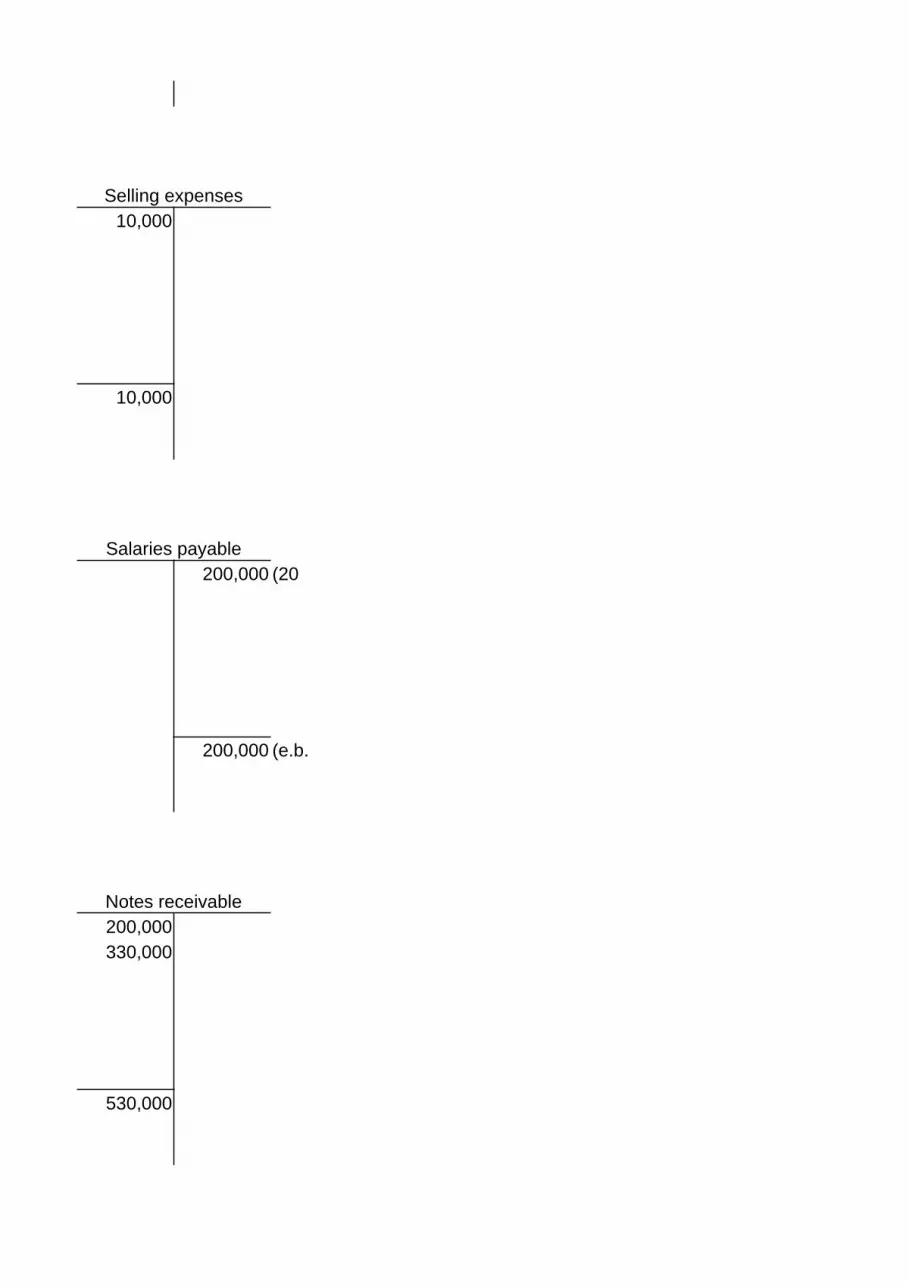

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013T-Accounts

Cash Banksb.b.) 210,000 100,000 (4 b.b.) 200,000

1) 320,000 100,367 (86) 10,000 24,000 (10

11) 256,914 10,000 (13

796,914 234,367 200,000e.b.) 562,547 e.b.) -56,000

Accounts payable Paid-in Capital16) 20,000 250,000 (b.b.

50,000 (15

20,000 300,000280,000 (e.b.

Return to index

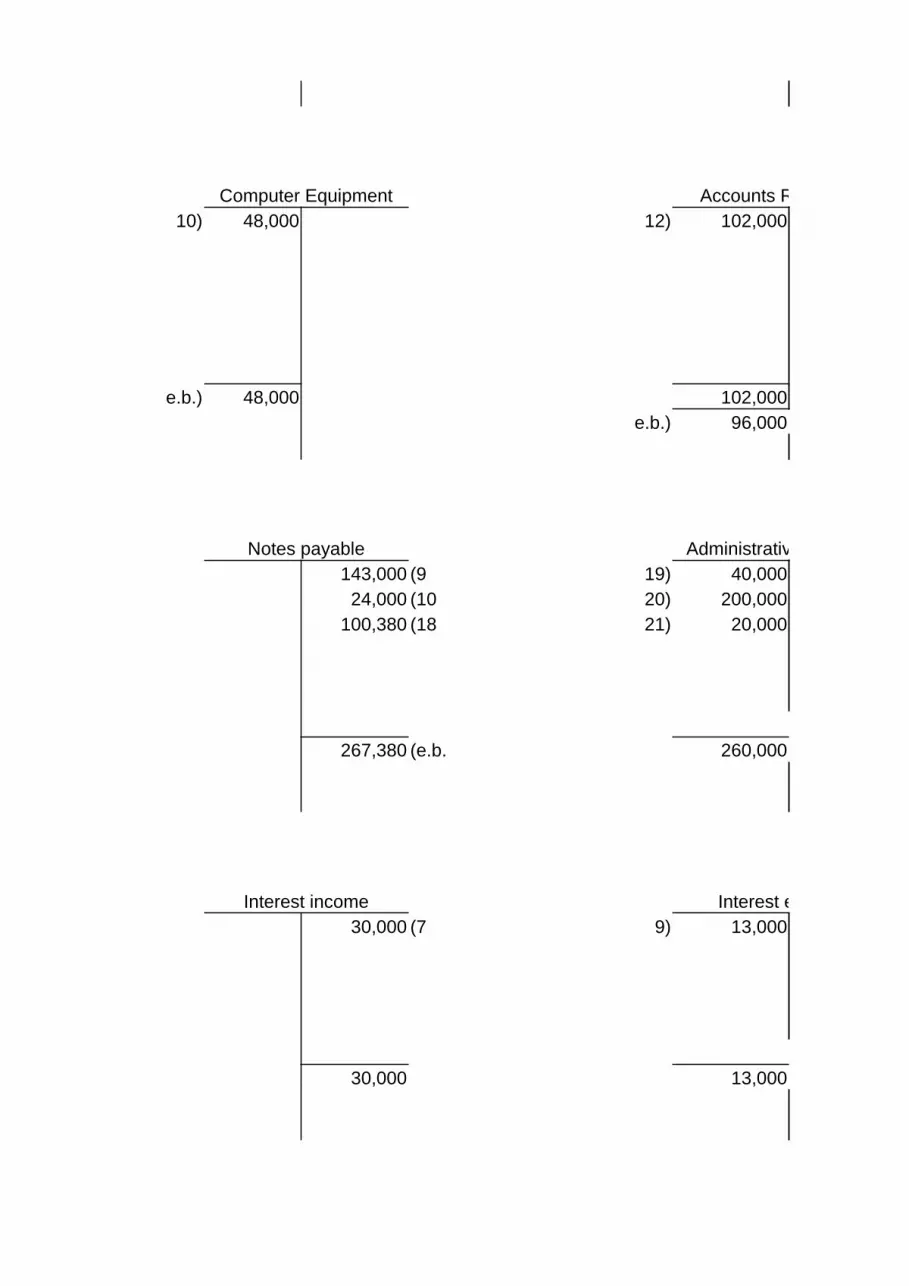

Computer Equipment Accounts Receivable10) 48,000 12) 102,000

e.b.) 48,000 102,000e.b.) 96,000

Notes payable Administrative expenses143,000 (9 19) 40,000

24,000 (10 20) 200,000100,380 (18 21) 20,000

267,380 (e.b. 260,000

Interest income Interest expense30,000 (7 9) 13,000

30,000 13,000

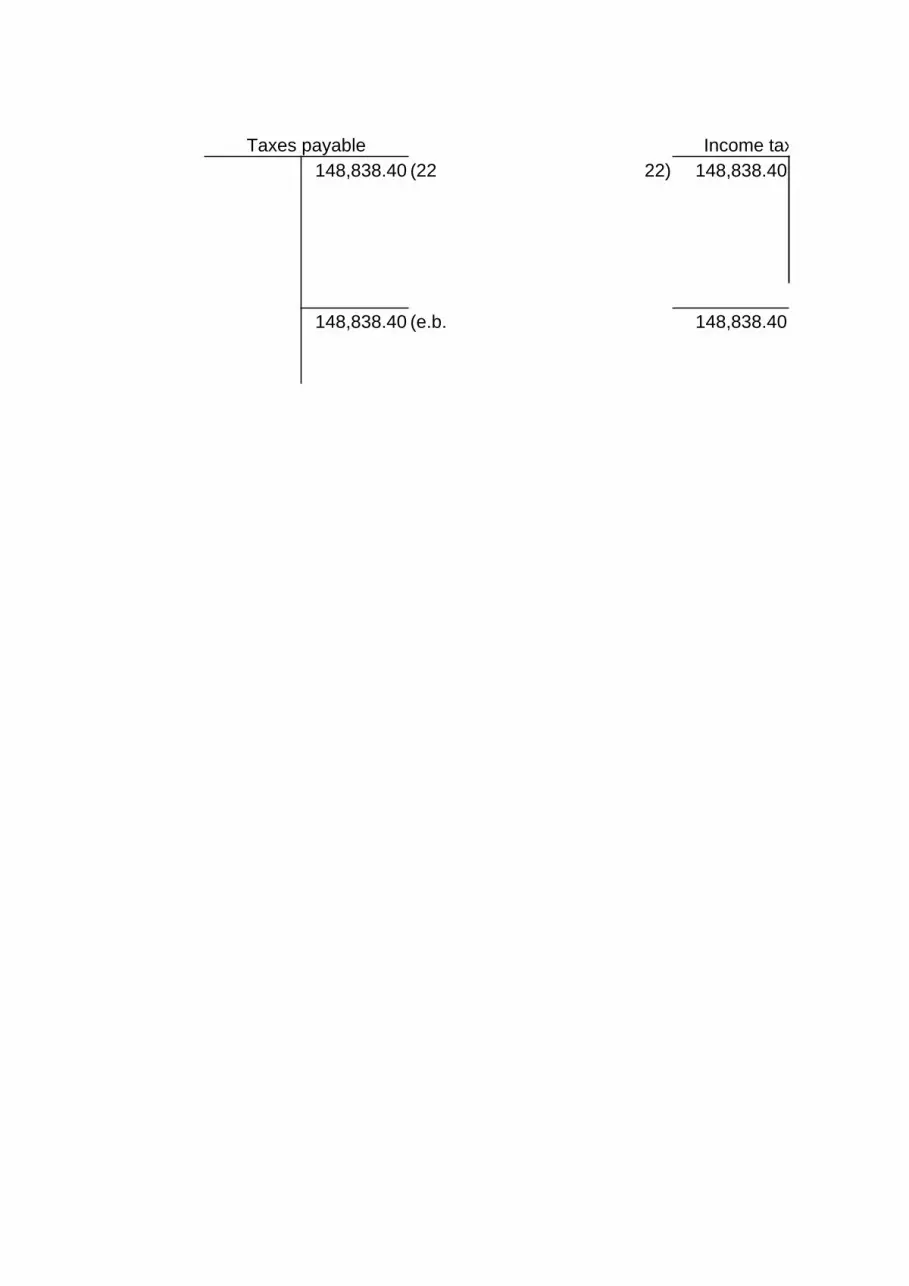

Taxes payable Income tax expense148,838.40 (22 22) 148,838.40

148,838.40 (e.b. 148,838.40

Banks Merchandise Inventory40,000 (2 b.b.) 840,000 146,300 (1a b.b.)

5,000 (5 2a) 14,000 63,000 (3a 8)130,000 (9 4) 100,000 10,000 (6

81,000 (17 5) 5,000 118,000 (7a9) 260,000 92,300 (11a

14a) 1,764 30,000 (12a15) 50,000 20,000 (1617) 90,000 9,000 (1718) 100,380

256,000 1,461,144 488,600 e.b.)e.b.) 972,544

Paid-in Capital Sales Revenue1,000,000 (b.b. 2) 40,000 320,000 (1 1a)

11) 28,546 200,000 (3 3a)14) 6,000 300,000 (7 7a)23) 383,786 285,460 (11 11a)24) 749,128 102,000 (12 12a)

1,000,000 (e.b. $1,207,460 $1,207,460

Accounts Receivable Sundry Creditors6,000 (14 315,000 (b.b. 13)

100,367 (8

6,000 415,367 (e.b.

Administrative expenses Expenses payable40,000 (19

40,000 (e.b.

Interest expense Accummulated depreciation20,000 (21 3)

7)

20,000 (e.b.e.b.)

Income tax expense Profit and Loss749,128 (24

Equipment315,000200,734

515,734

Cost of goods sold112,000 29,750 (2a

63,000 1,764 (14a118,000 383,786 (23

92,30030,000

$415,300 $415,300

Selling expenses10,000

10,000

Salaries payable200,000 (20

200,000 (e.b.

Notes receivable200,000330,000

530,000

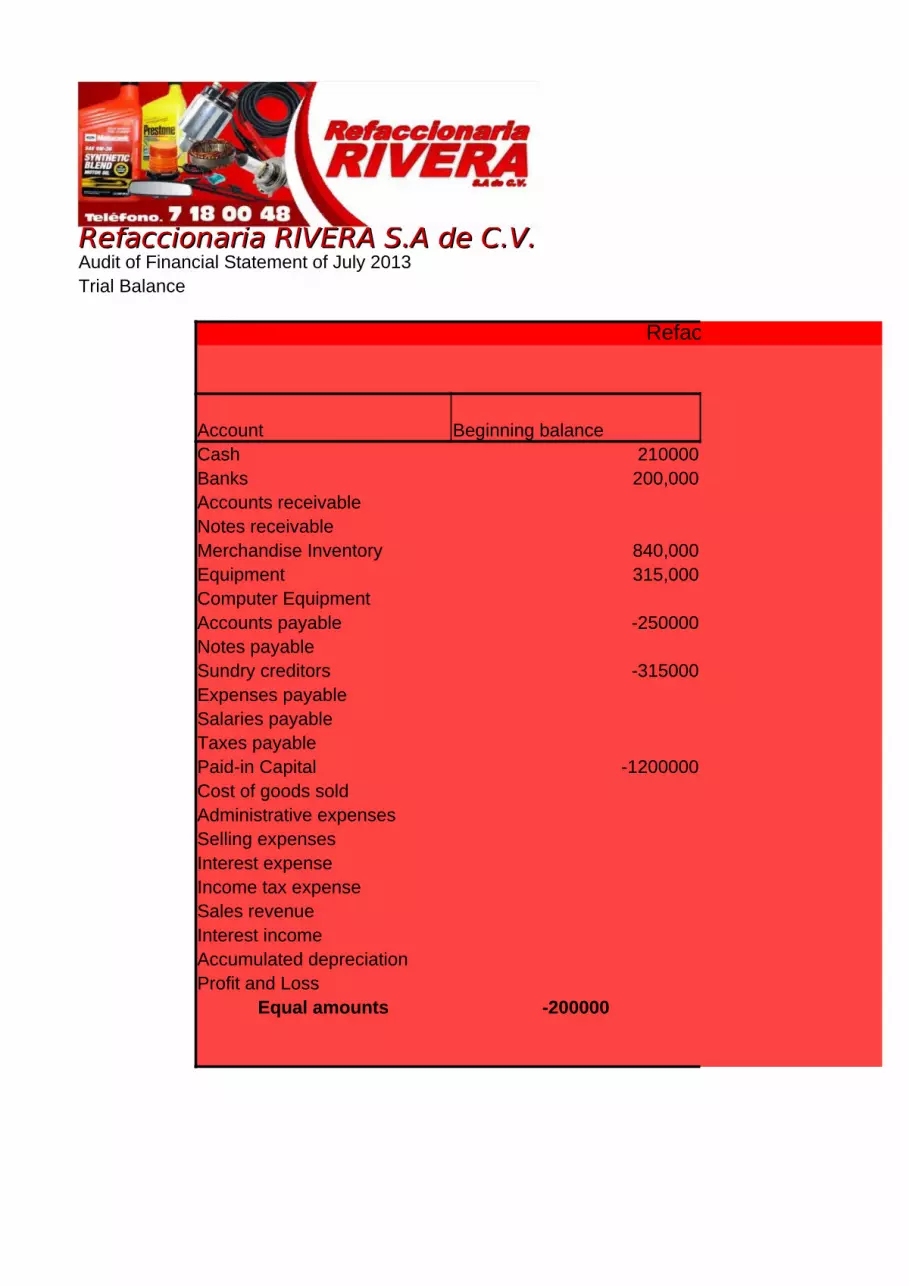

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013Trial Balance

Refaccionaria RIVERA S.A de C.V.Trial balance

For the month of June 2012

Account Beginning balanceCash 210000Banks 200,000Accounts receivableNotes receivableMerchandise Inventory 840,000Equipment 315,000Computer EquipmentAccounts payable -250000Notes payableSundry creditors -315000Expenses payableSalaries payableTaxes payablePaid-in Capital -1200000Cost of goods soldAdministrative expensesSelling expensesInterest expenseIncome tax expenseSales revenueInterest incomeAccumulated depreciationProfit and Loss

Equal amounts -200000

Refaccionaria RIVERA S.A de C.V.Trial balance

For the month of June 2012Account Activity Ending balances

Debit Credit Debit Credit$796,914 $234,367 $772,547

200,000 256,000 144,000102,000 6,000 96,000530,000 530,000

1,461,144 488,600 1,812,544515,734 830,734

48,000 48,00020,000 300,000 530,000

267,380 267,380415,367 730,367

40,000 40,000200,000 200,000

148,838.40 148,838.401,000,000 2,200,000

415,300 415,300260,000 260,000

10,000 10,00013,000 13,000

148,838.40 148,838.401,207,460 1,207,460

30,000 $200,000.00 30,000$50,050.00 20,000 -30,050

749,128 749,128$5,778,440.40 $5,778,440.40 $4,865,663.40 $4,865,663.40

Return to index

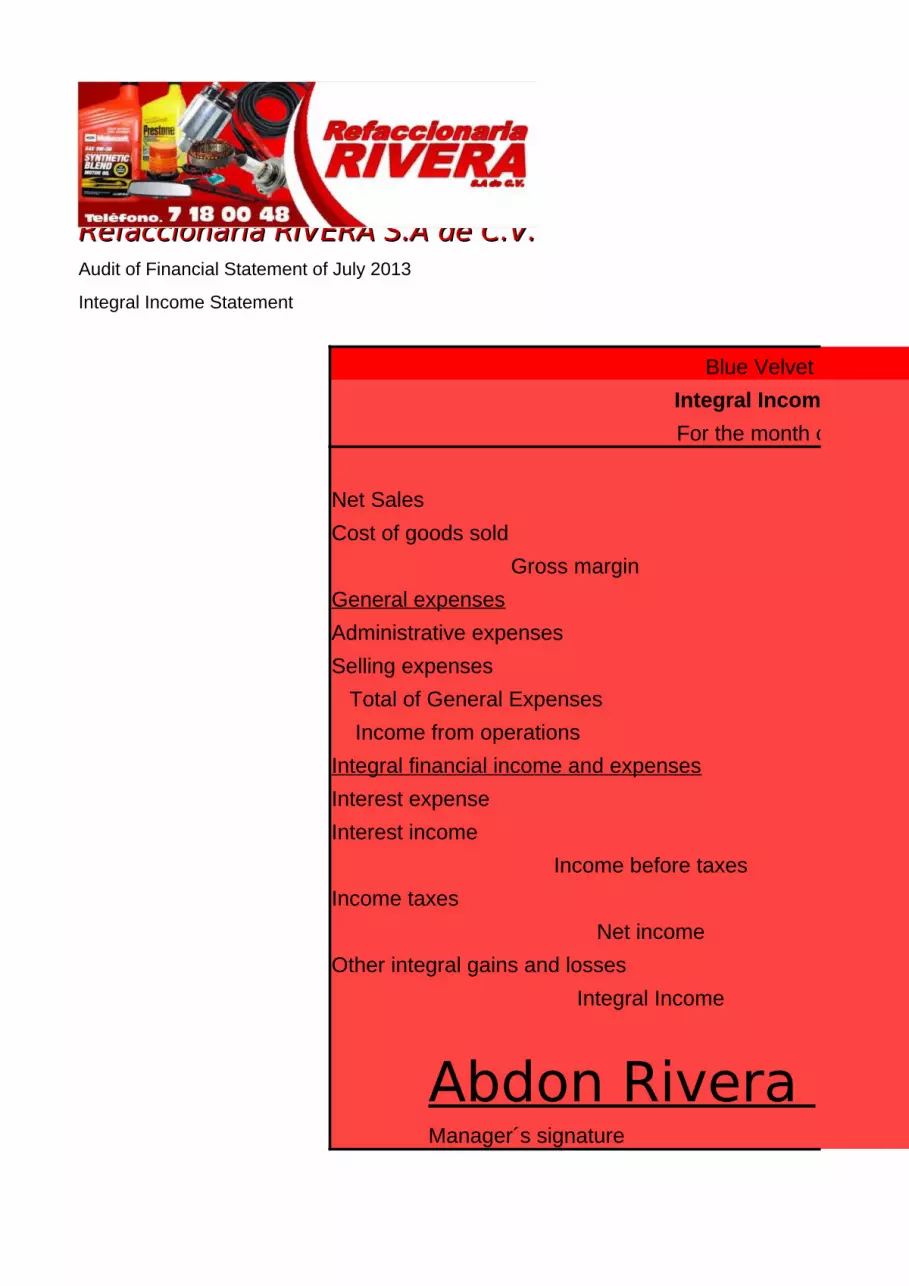

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013

Integral Income Statement

Blue Velvet CompanyIntegral Income StatementFor the month of June 2012

Net SalesCost of goods sold

Gross marginGeneral expensesAdministrative expensesSelling expenses Total of General Expenses Income from operationsIntegral financial income and expensesInterest expenseInterest income

Income before taxesIncome taxes

Net incomeOther integral gains and losses

Integral Income

Abdon Rivera Manager´s signature

Blue Velvet CompanyIntegral Income StatementFor the month of June 2012

$1,132,914383,786

$749,128

$260,00010,000

$270,000$479,128

$13,00030,000 $17,000

Income before taxes $496,128$148,838.40

Net income $347,289.60$0

Integral Income $347,289.60

Miguel E RdzAccountant´s signature

Return to index

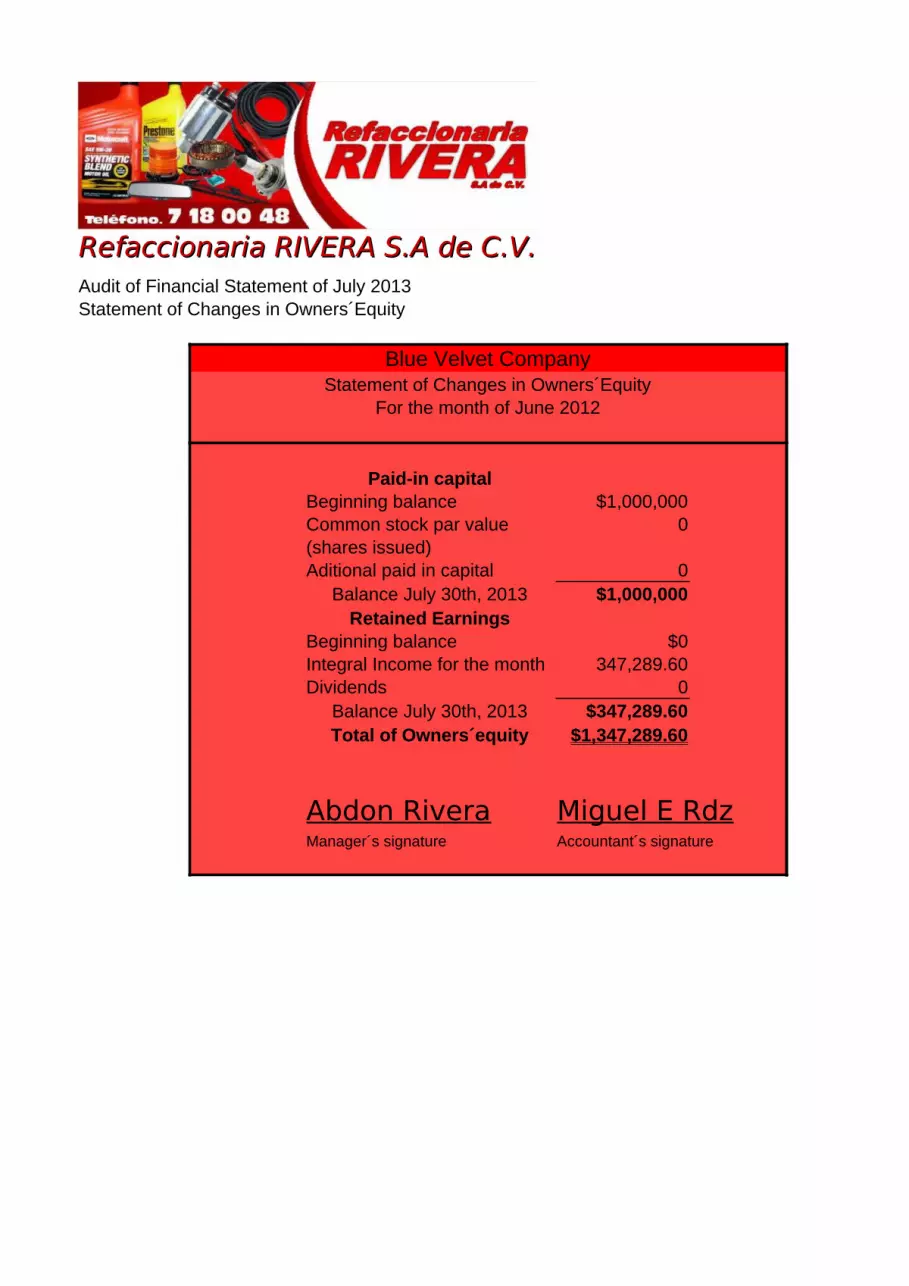

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013Statement of Changes in Owners´Equity

Blue Velvet CompanyStatement of Changes in Owners´Equity

For the month of June 2012

Paid-in capitalBeginning balance $1,000,000Common stock par value 0(shares issued)Aditional paid in capital 0

Balance July 30th, 2013 $1,000,000Retained Earnings

Beginning balance $0Integral Income for the month 347,289.60Dividends 0

Balance July 30th, 2013 $347,289.60Total of Owners´equity $1,347,289.60

Abdon Rivera Miguel E RdzManager´s signature Accountant´s signature

Return to index

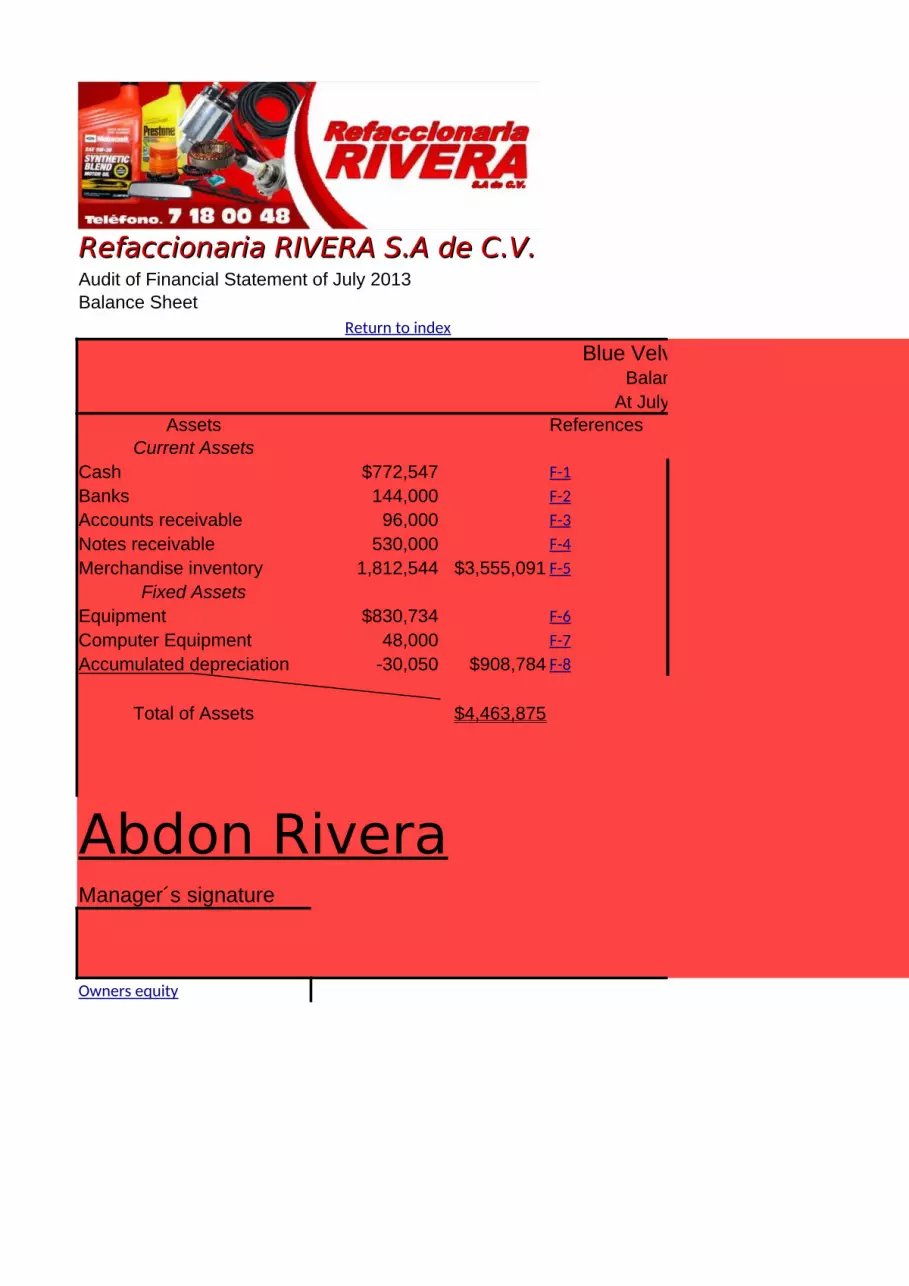

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013Balance Sheet

Blue Velvet CompanyBalance Sheet

At July 30th 2013Assets References

Current Assets $200,000Cash $772,547Banks 144,000Accounts receivable 96,000Notes receivable 530,000Merchandise inventory 1,812,544 $3,555,091

Fixed AssetsEquipment $830,734Computer Equipment 48,000Accumulated depreciation -30,050 $908,784

Total of Assets $4,463,875

Abdon RiveraManager´s signature

Return to index

F-1F-2F-3F-4F-5

F-6F-7F-8

Owners equity

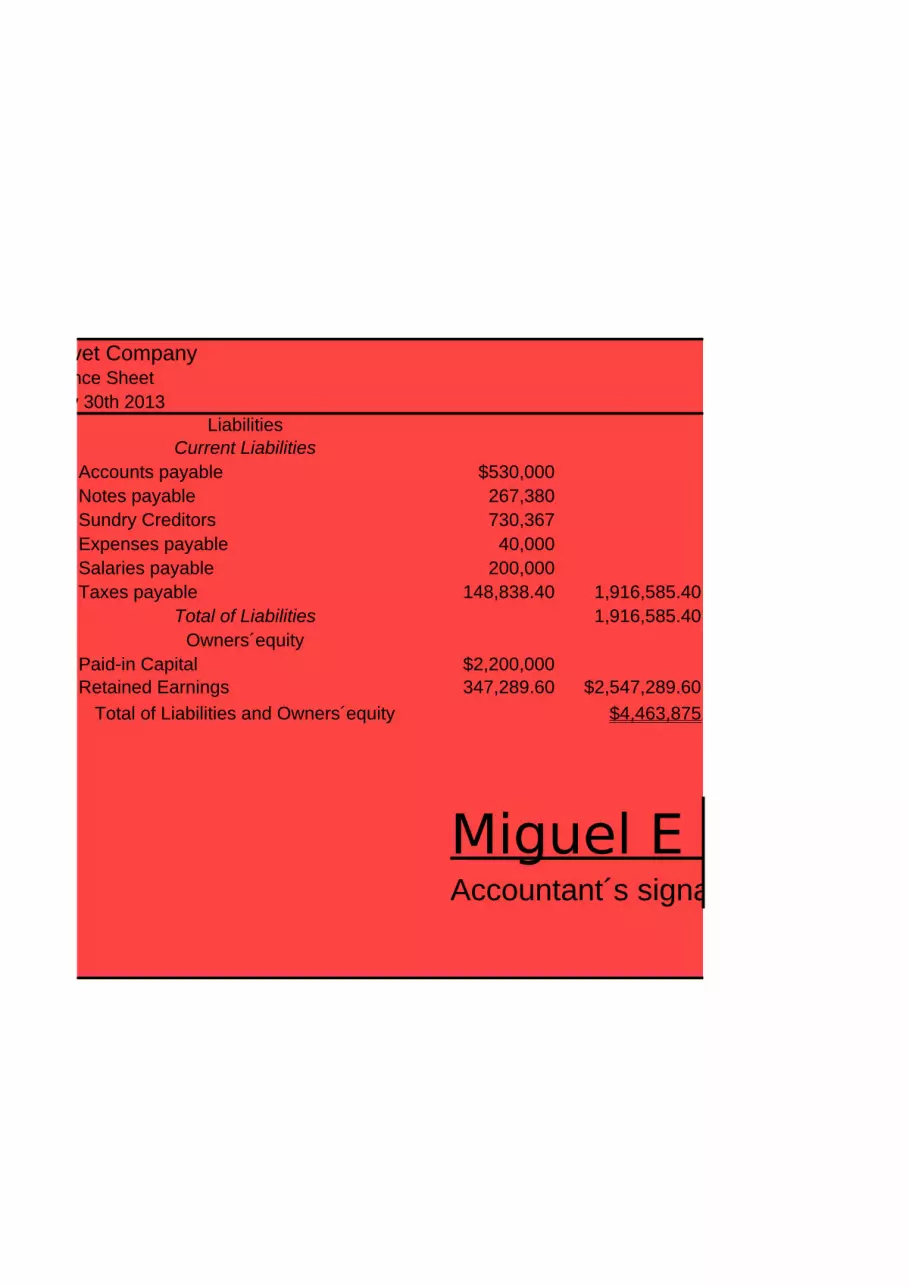

Blue Velvet CompanyBalance Sheet

At July 30th 2013Liabilities

Current LiabilitiesAccounts payable $530,000Notes payable 267,380Sundry Creditors 730,367Expenses payable 40,000Salaries payable 200,000Taxes payable 148,838.40 1,916,585.40

Total of Liabilities 1,916,585.40Owners´equity

Paid-in Capital $2,200,000Retained Earnings 347,289.60 $2,547,289.60

Total of Liabilities and Owners´equity $4,463,875

Miguel E RdzAccountant´s signature

References

Miguel E RdzAccountant´s signature

K-1K-2K-3K-4K-5K-6

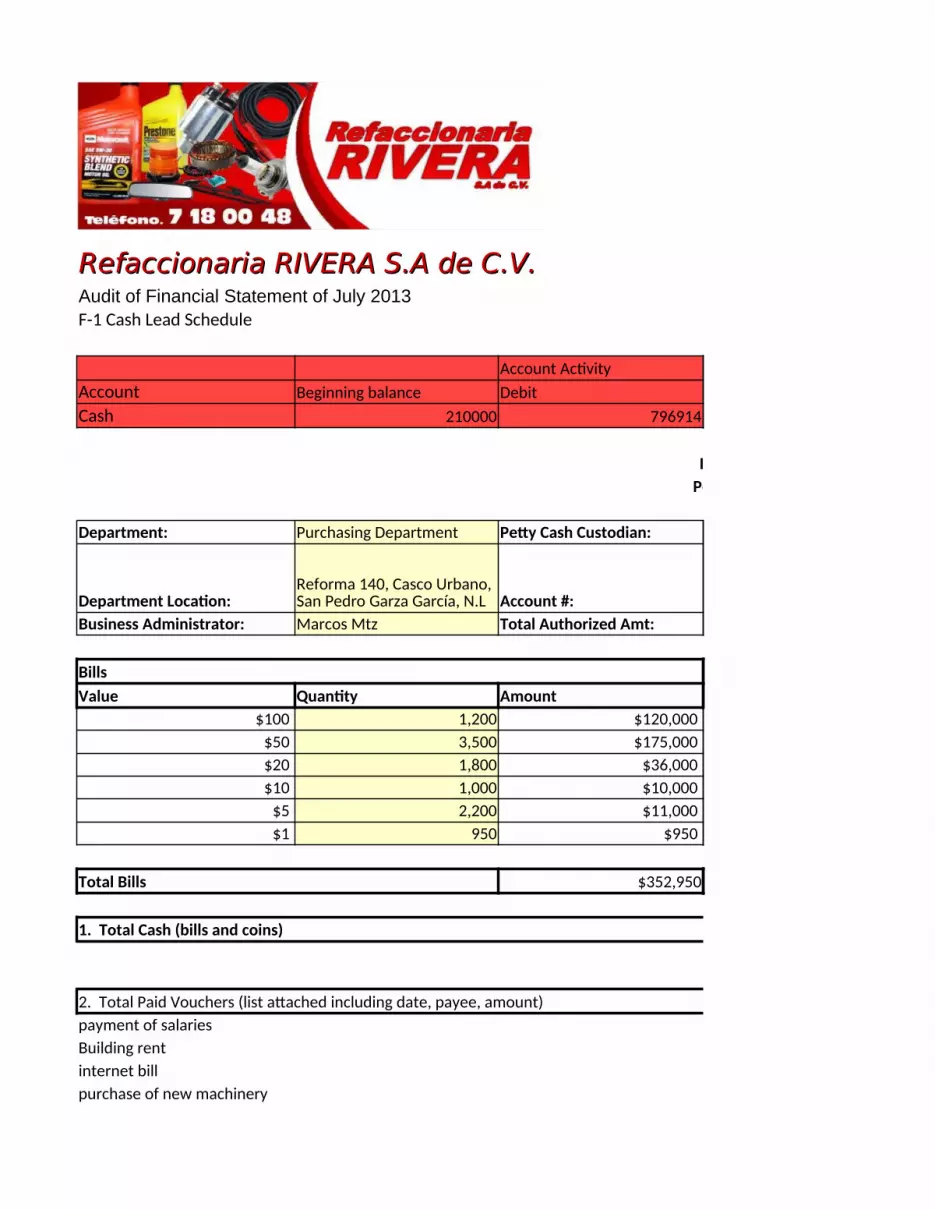

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-1 Cash Lead Schedule

Account ActivityAccount Beginning balance DebitCash 210000 796914

Blue Velvet CompanyPetty Cash Count Sheet

Department: Purchasing Department Petty Cash Custodian:

Department Location: Account #:Business Administrator: Marcos Mtz Total Authorized Amt:

BillsValue Quantity Amount

$100 1,200 $120,000 $50 3,500 $175,000 $20 1,800 $36,000 $10 1,000 $10,000

$5 2,200 $11,000 $1 950 $950

Total Bills $352,950

1. Total Cash (bills and coins)

2. Total Paid Vouchers (list attached including date, payee, amount)payment of salariesBuilding rentinternet billpurchase of new machinery

Reforma 140, Casco Urbano, San Pedro Garza García, N.L

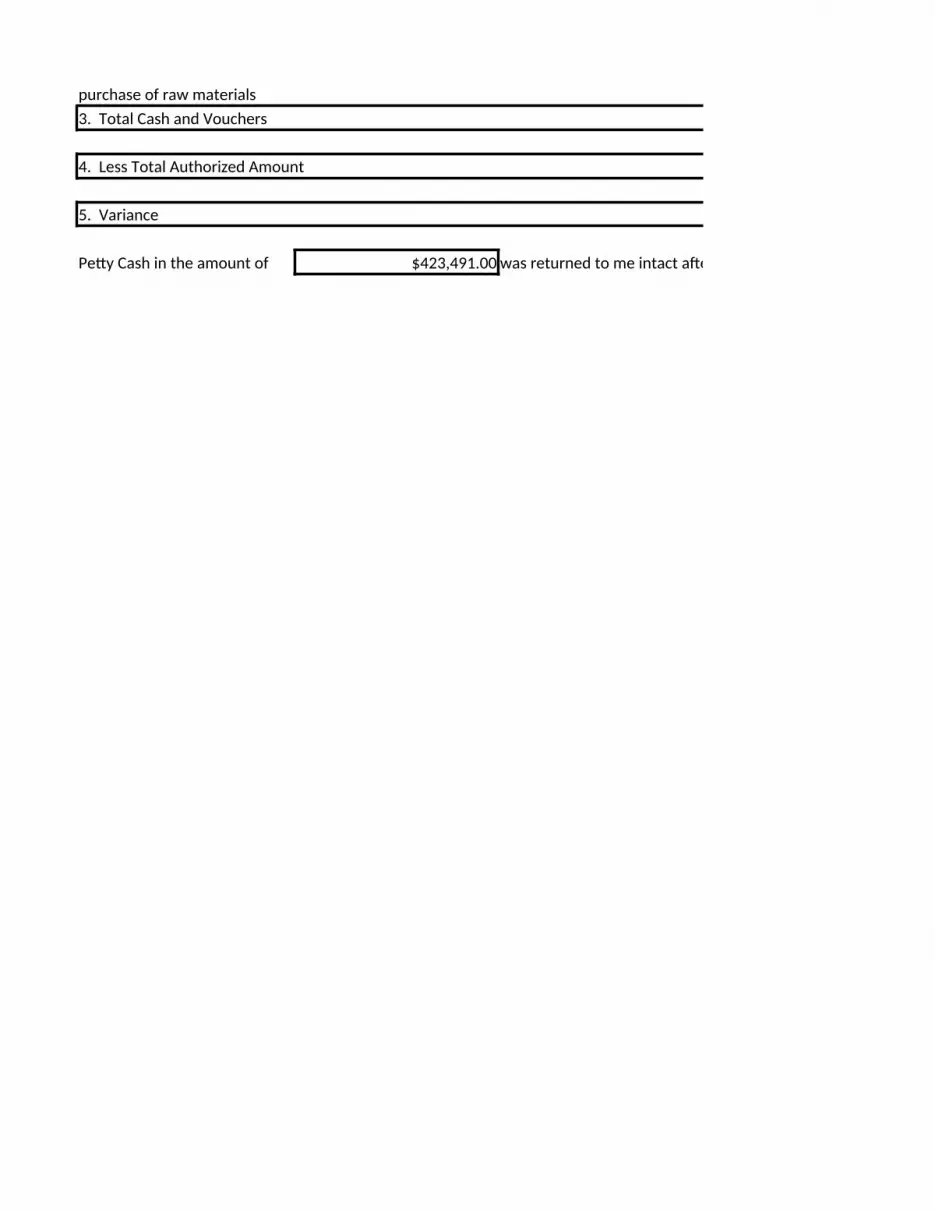

purchase of raw materials3. Total Cash and Vouchers

4. Less Total Authorized Amount

5. Variance

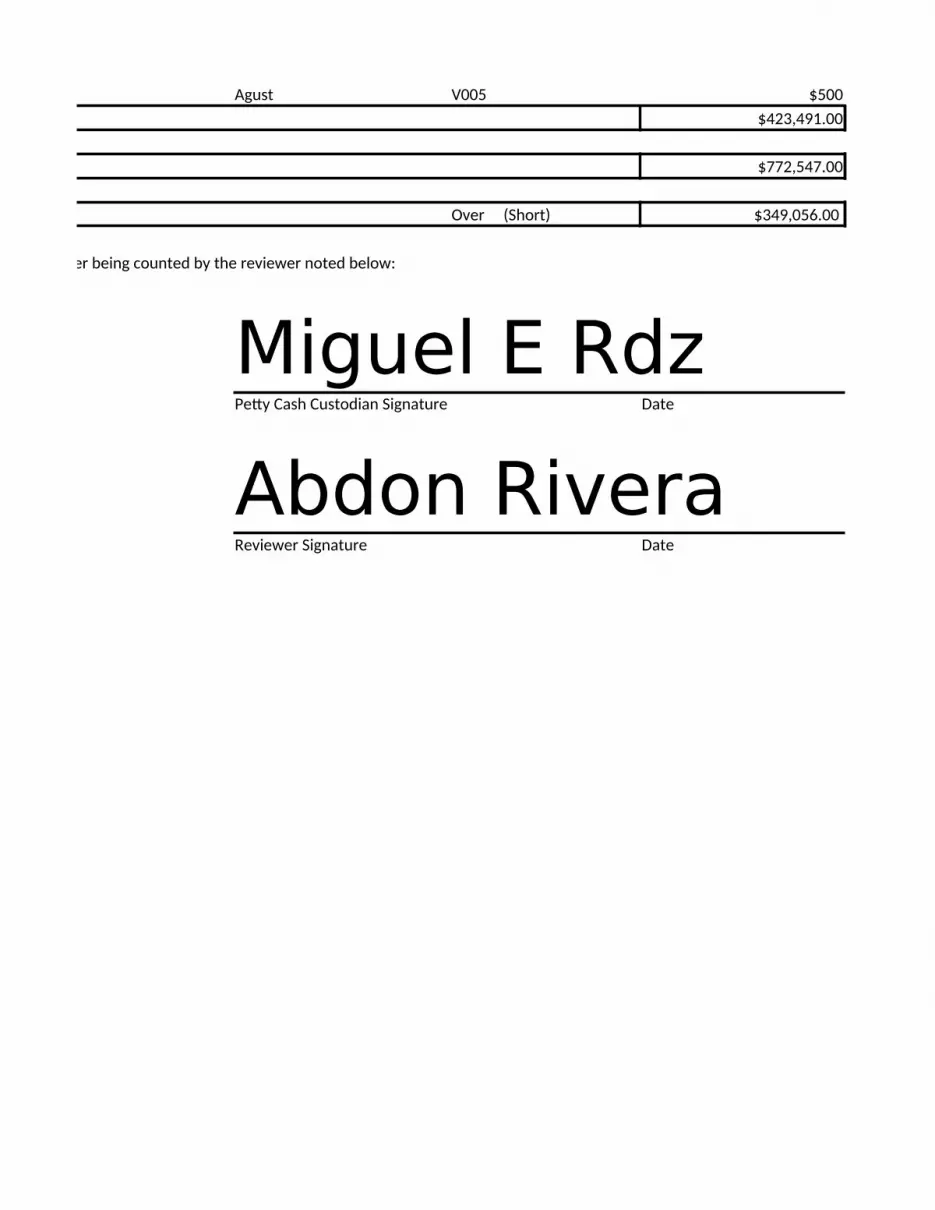

Petty Cash in the amount of $423,491.00 was returned to me intact after being counted by the reviewer noted below:

Ending balancesCredit Debit Credit

234367 772,547

Blue Velvet CompanyPetty Cash Count Sheet

Miguel E Rdz Date: 11/7/2014

250 Time: 05:00 p.m$772,547.00 Reviewer: Abdón Rivera González

CoinsValue Quantity Amount

$1.00 500 500.00$0.50 400 200.00$0.25 800 200.00$0.10 900 90.00$0.05 980 49.00$0.01 200 2.00

Total Coins $1,041.00

$353,991.00

# Vouchers: $ Vouchers:$69,500.00

June V001 $50,000.00June V002 $15,000.00June V003 $3,000.00July V004 $1,000

Return to Balance Sheet

Agust V005 $500$423,491.00

$772,547.00

Over (Short) $349,056.00

was returned to me intact after being counted by the reviewer noted below:

Miguel E RdzPetty Cash Custodian Signature Date

Abdon Rivera Reviewer Signature Date

F-1-1

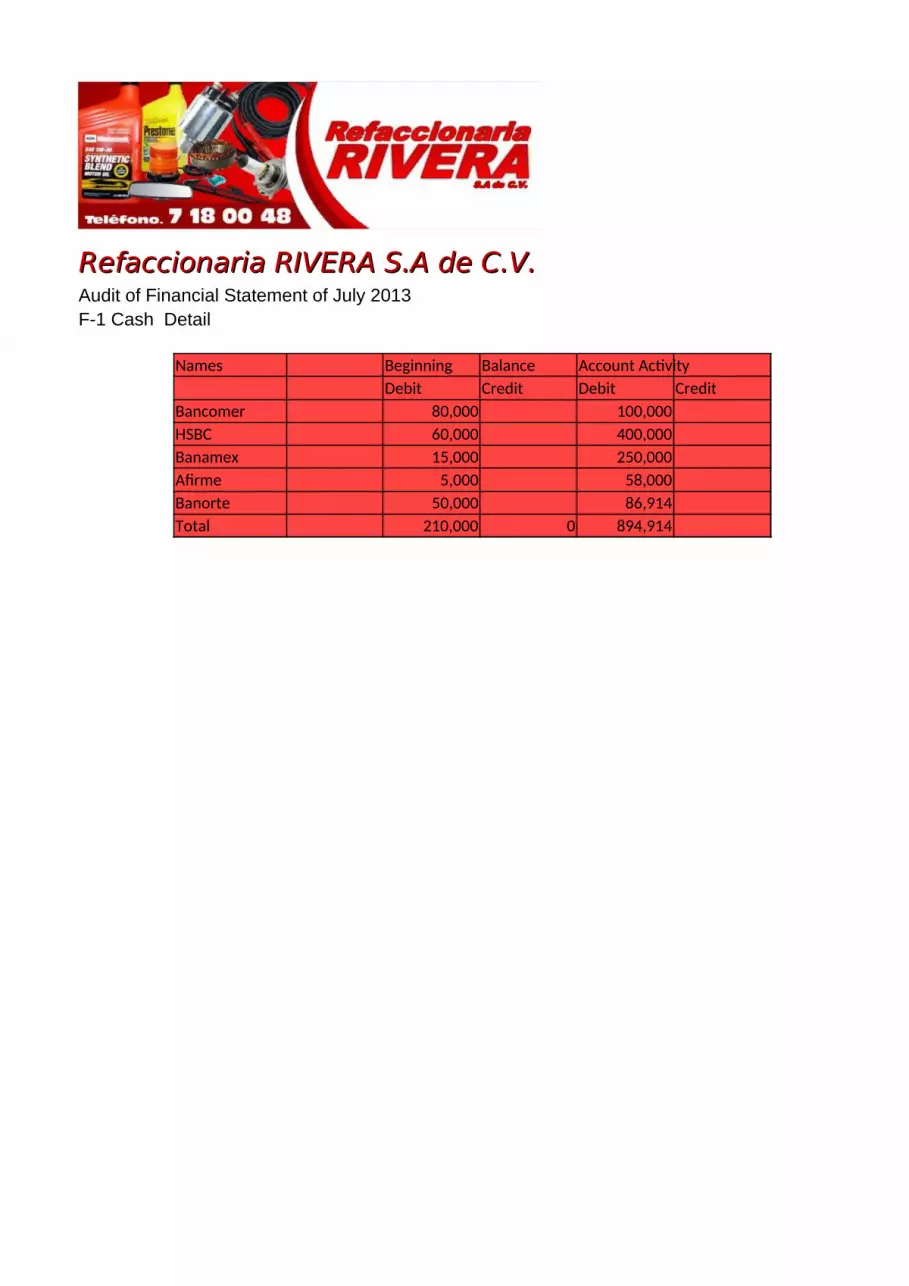

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-1 Cash Detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

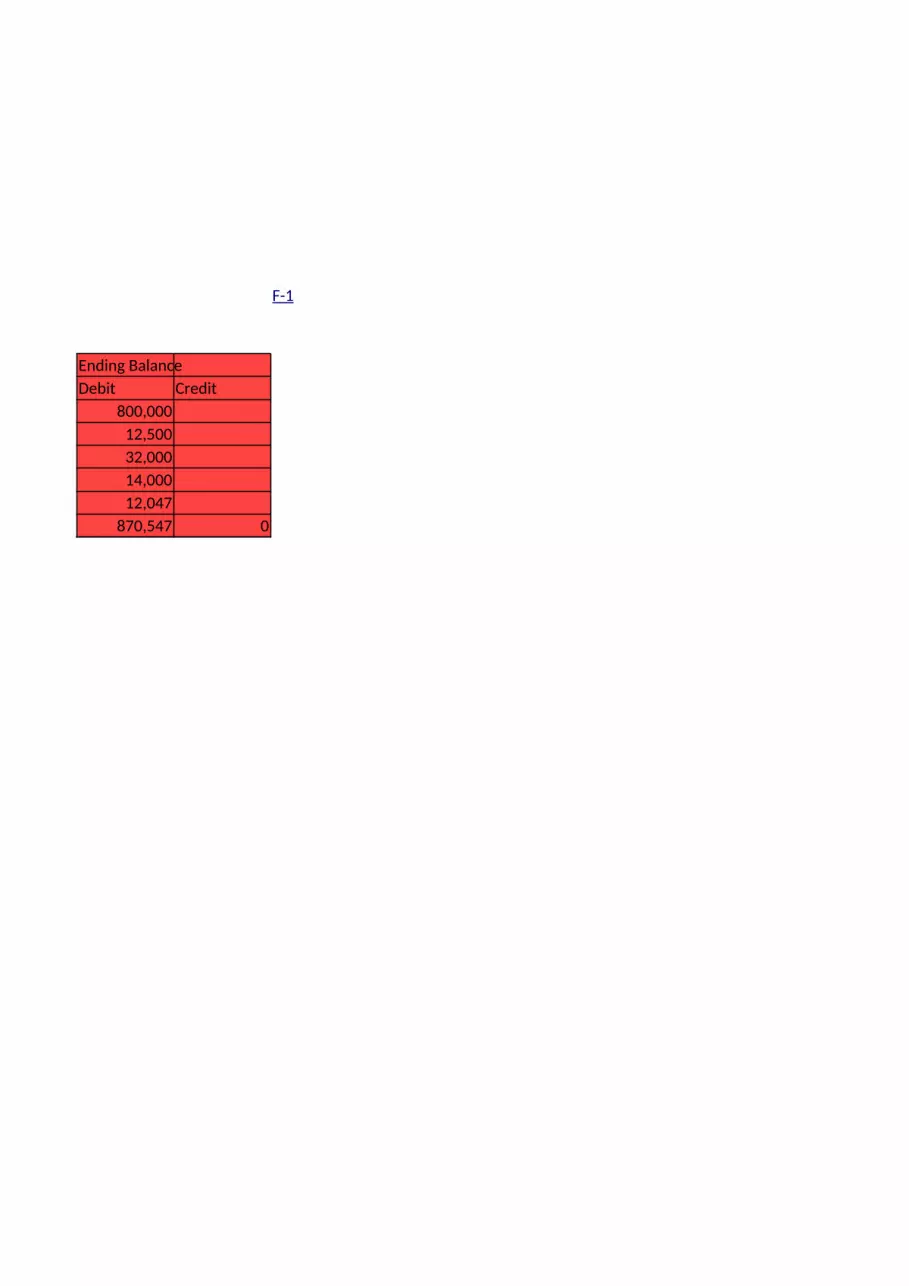

Bancomer 80,000 100,000HSBC 60,000 400,000Banamex 15,000 250,000Afirme 5,000 58,000Banorte 50,000 86,914Total 210,000 0 894,914

Ending BalanceDebit Credit

800,00012,50032,00014,00012,047

870,547 0

F-1

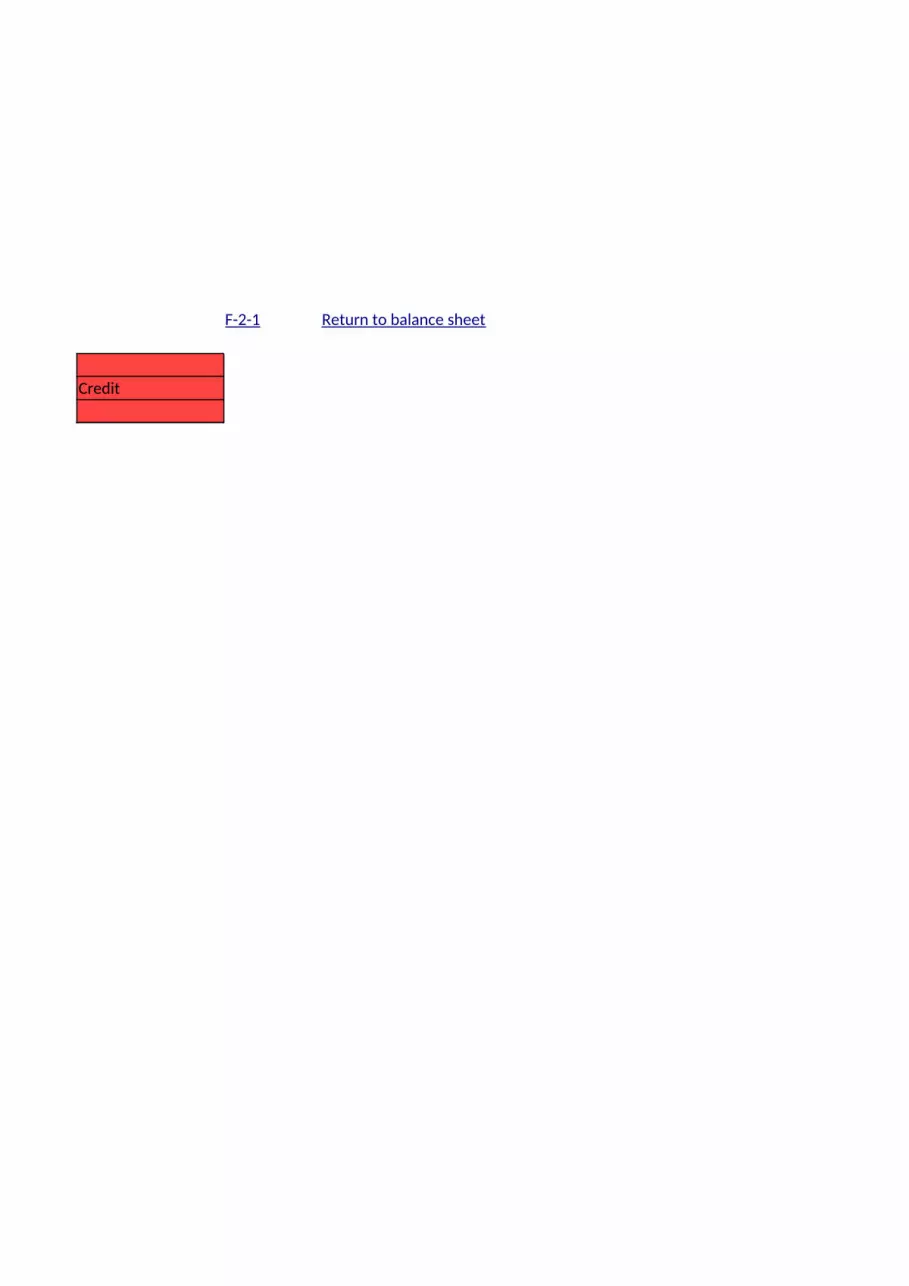

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-2 Banks Lead Schedule

Account Activity Ending balancesAccount Beginning balance Debit Credit DebitBanks 200,000 200,000 256,000 144,000

Credit

F-2-1 Return to balance sheet

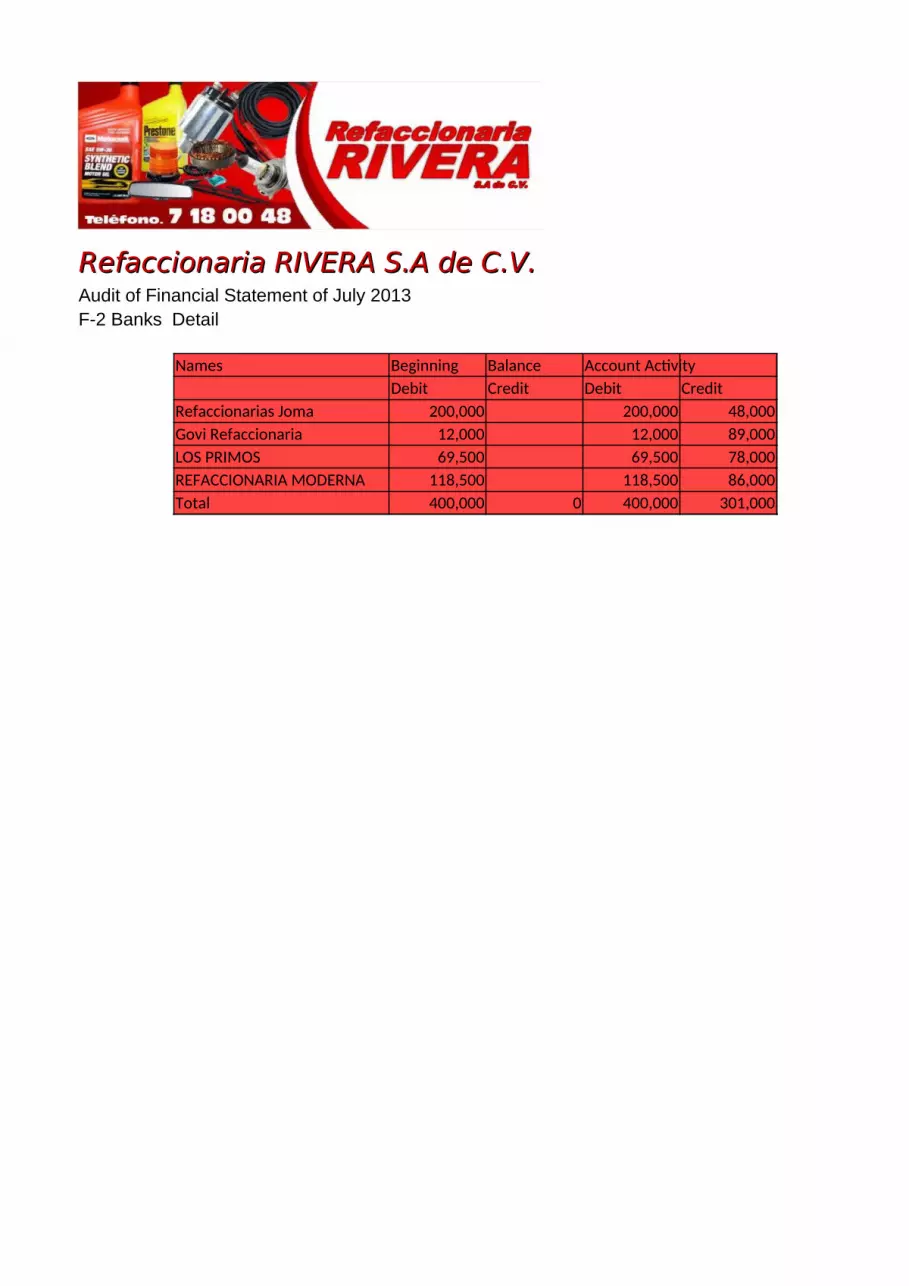

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-2 Banks Detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

Refaccionarias Joma 200,000 200,000 48,000Govi Refaccionaria 12,000 12,000 89,000LOS PRIMOS 69,500 69,500 78,000REFACCIONARIA MODERNA 118,500 118,500 86,000Total 400,000 0 400,000 301,000

Ending BalanceDebit Credit

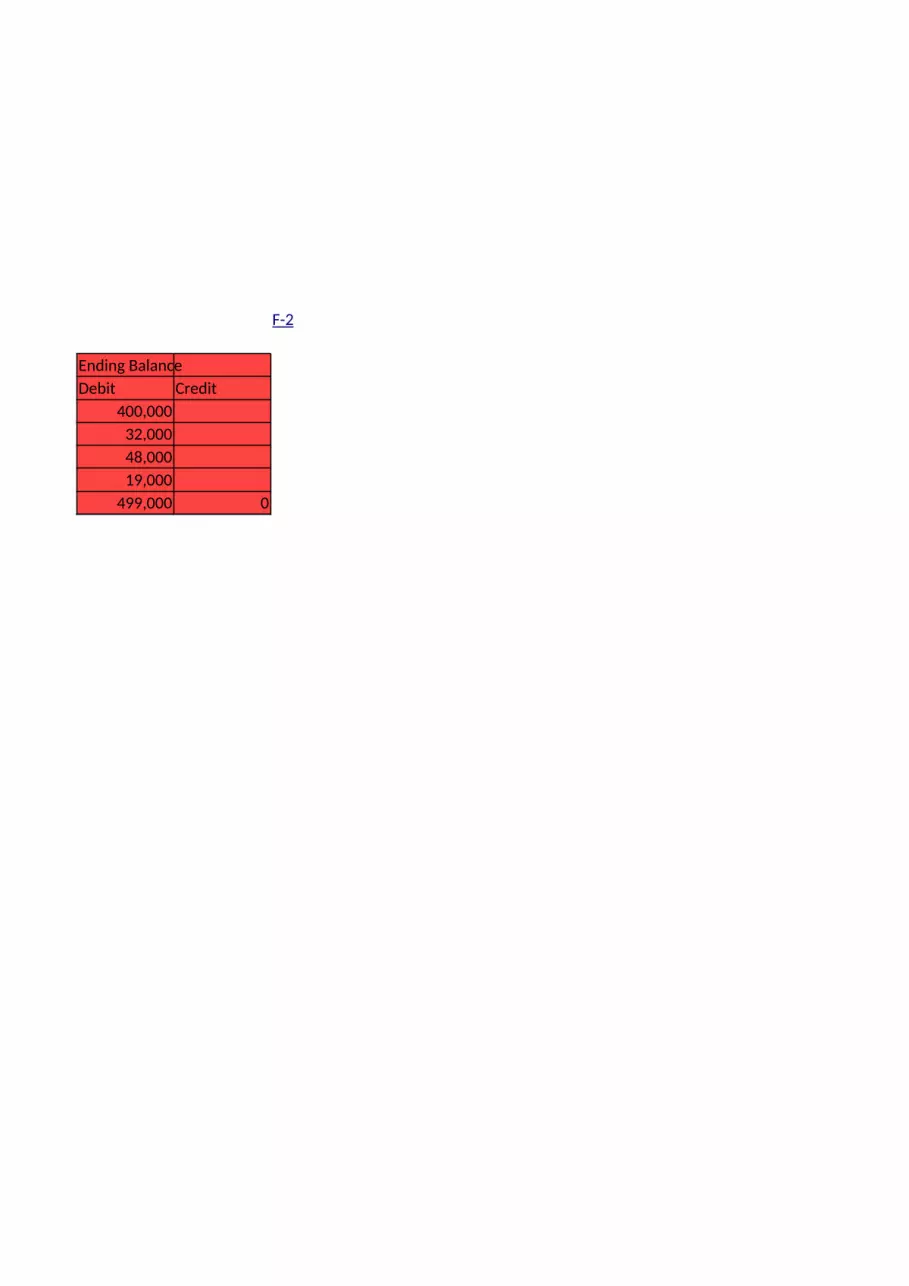

400,00032,00048,00019,000

499,000 0

F-2

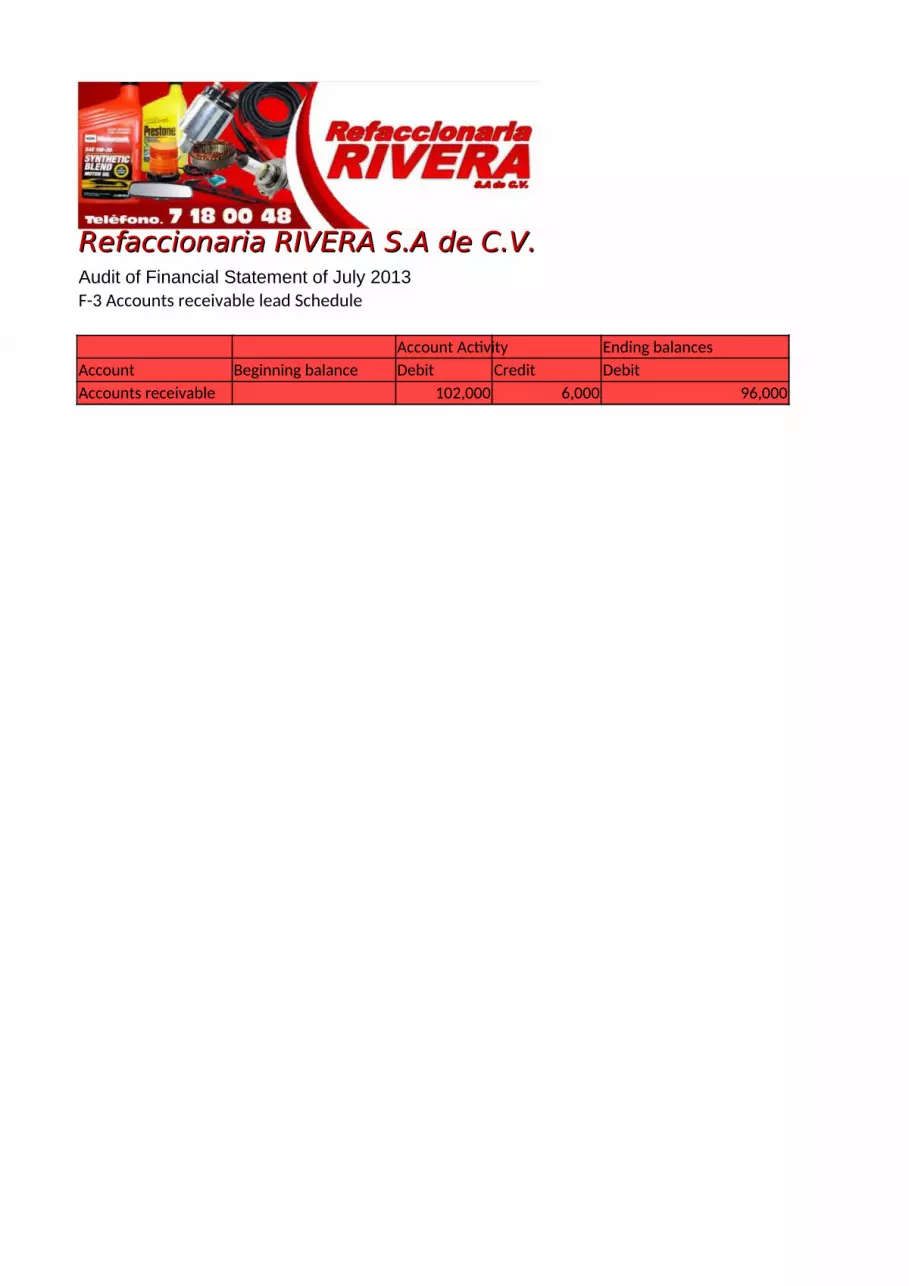

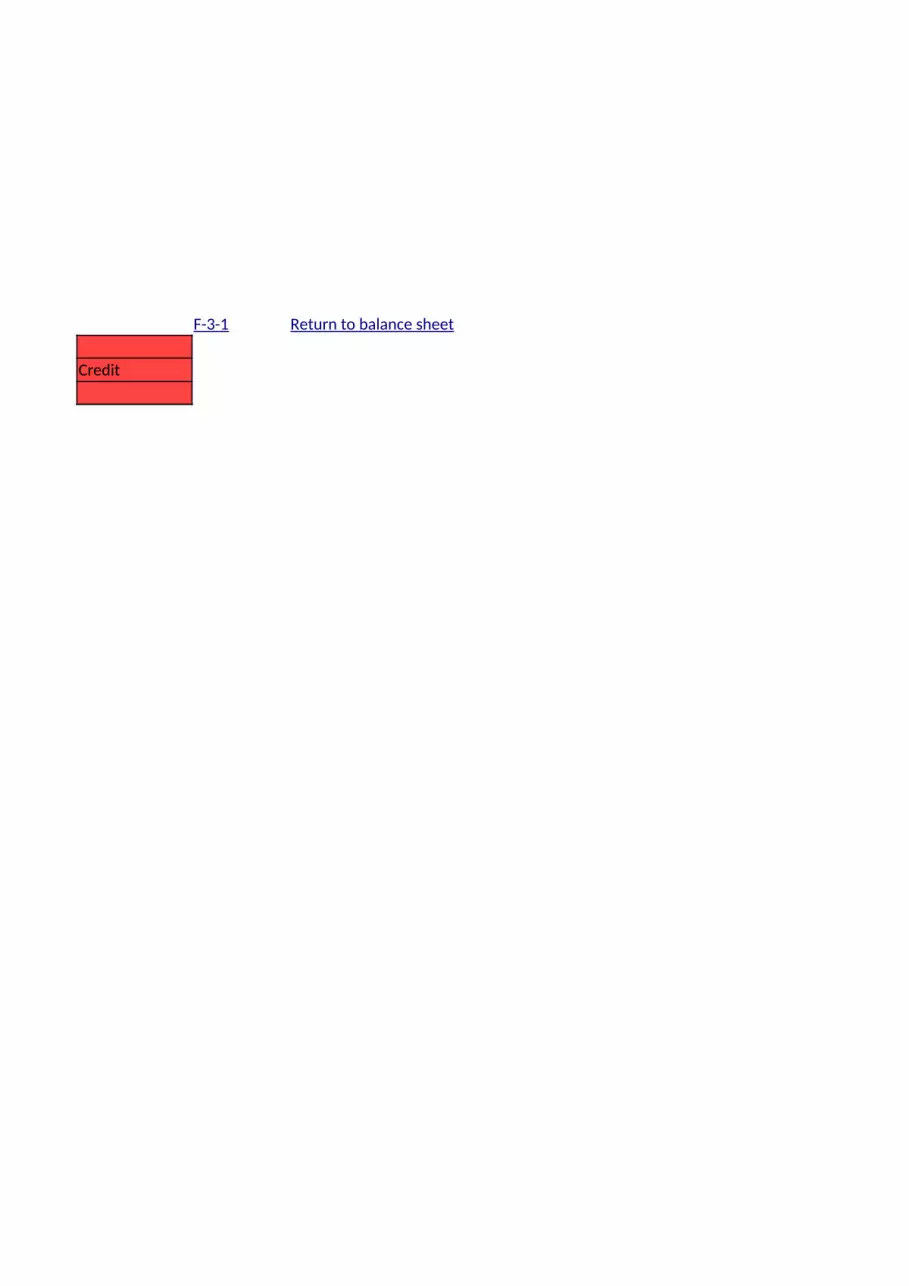

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-3 Accounts receivable lead Schedule

Account Activity Ending balancesAccount Beginning balance Debit Credit DebitAccounts receivable 102,000 6,000 96,000

Credit

F-3-1 Return to balance sheet

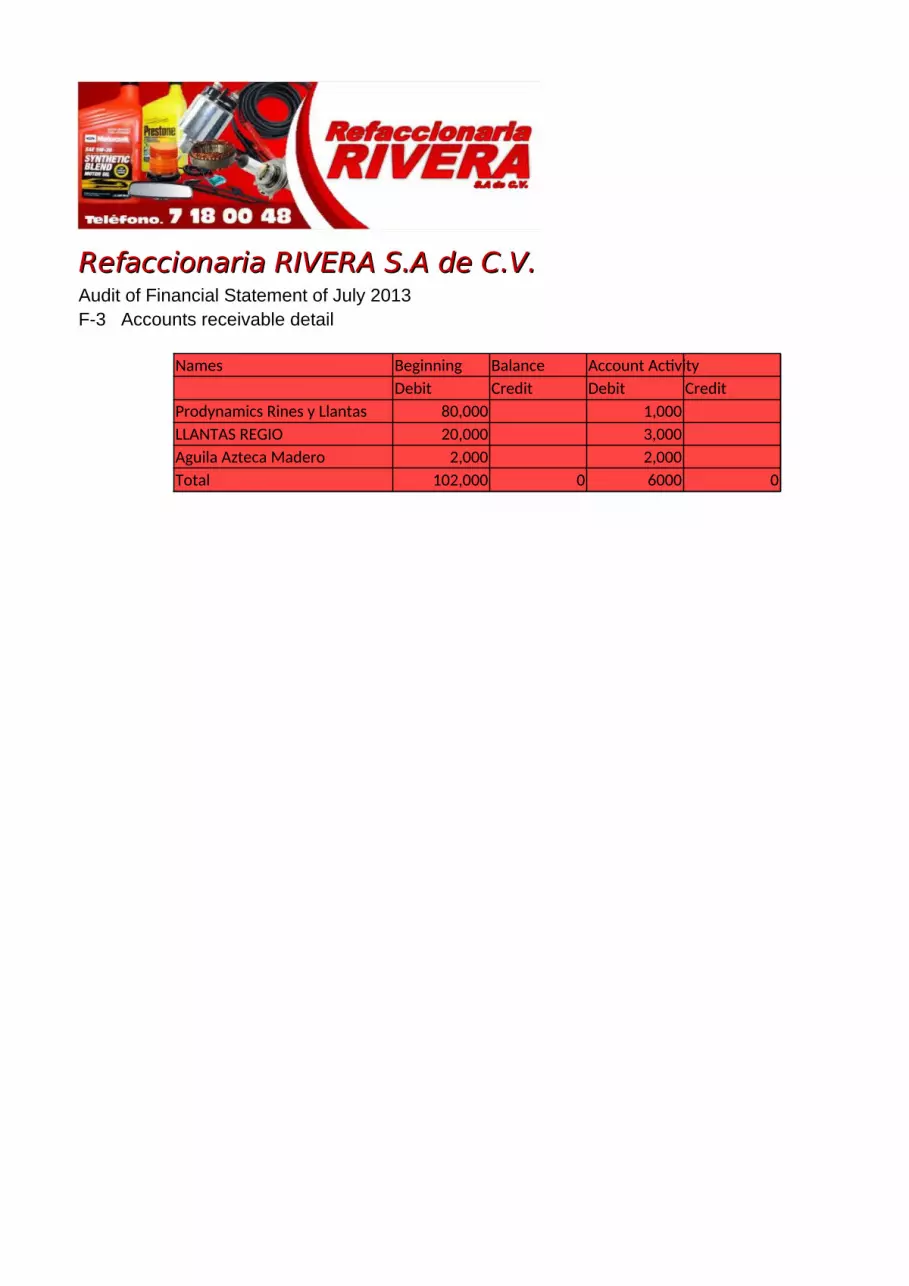

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-3 Accounts receivable detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

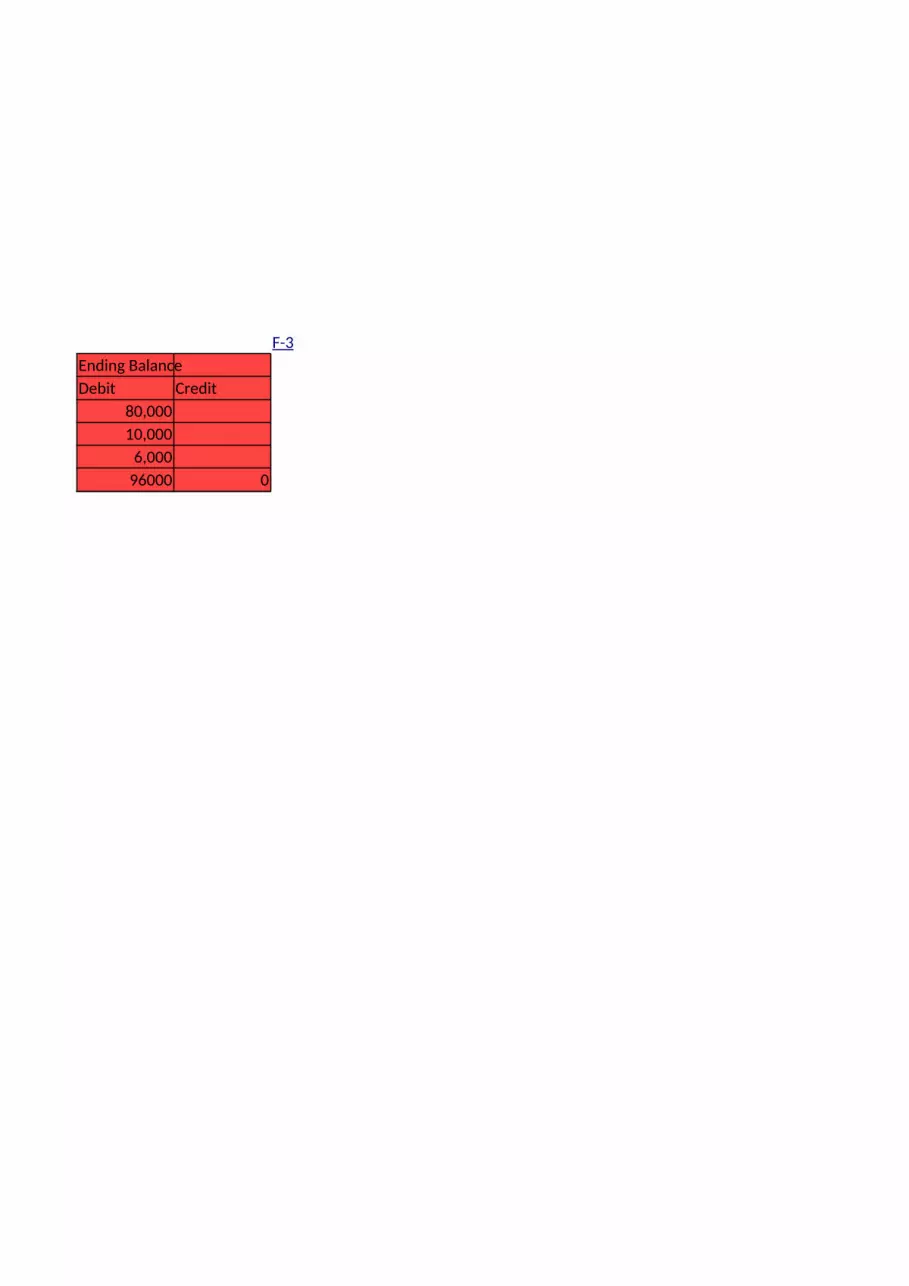

Prodynamics Rines y Llantas 80,000 1,000LLANTAS REGIO 20,000 3,000Aguila Azteca Madero 2,000 2,000Total 102,000 0 6000 0

Ending BalanceDebit Credit

80,00010,000

6,00096000 0

F-3

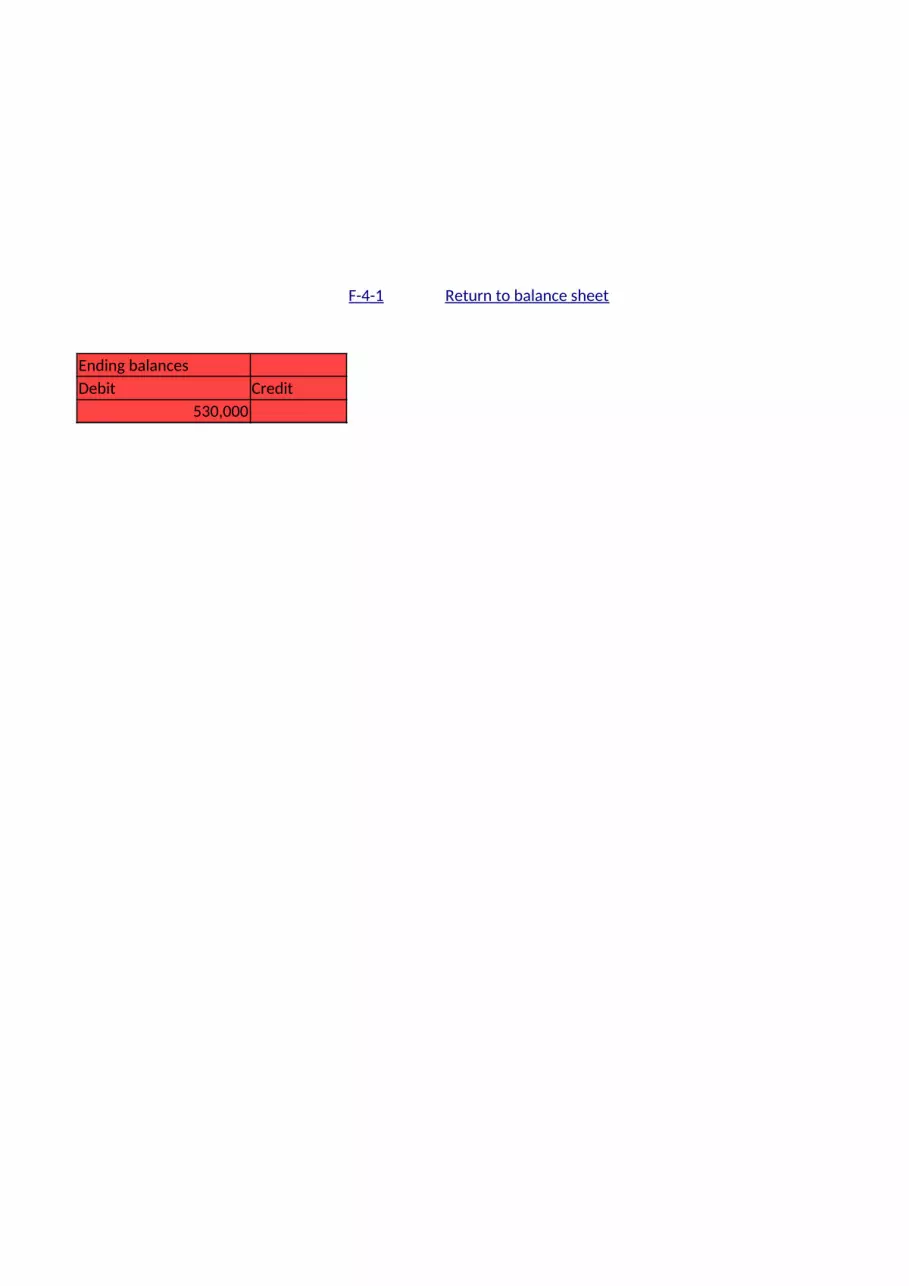

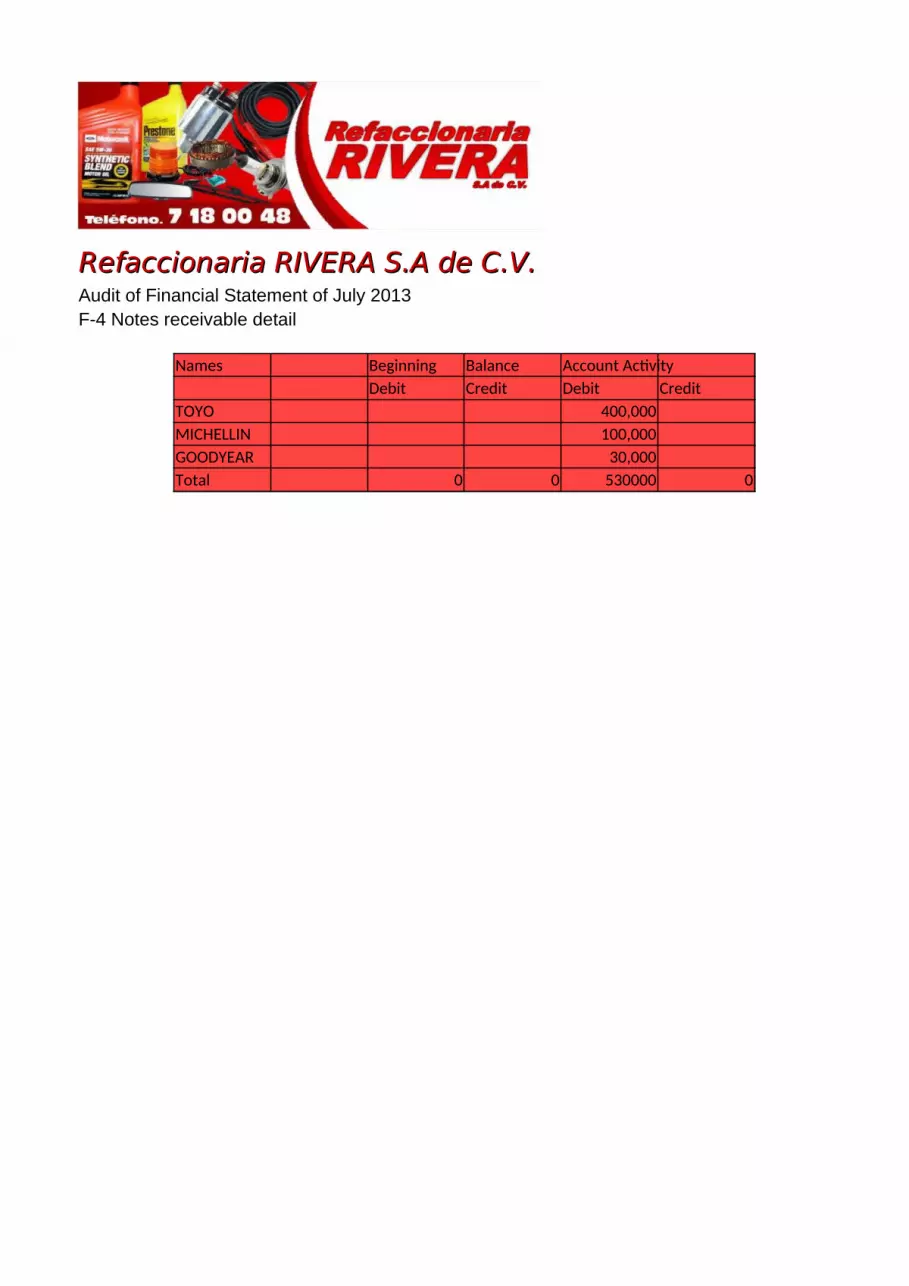

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-4 Notes receivable lead Schedule

Account ActivityAccount Beginning balance Debit CreditNotes receivable 530,000

Ending balancesDebit Credit

530,000

F-4-1 Return to balance sheet

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-4 Notes receivable detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

TOYO 400,000MICHELLIN 100,000GOODYEAR 30,000Total 0 0 530000 0

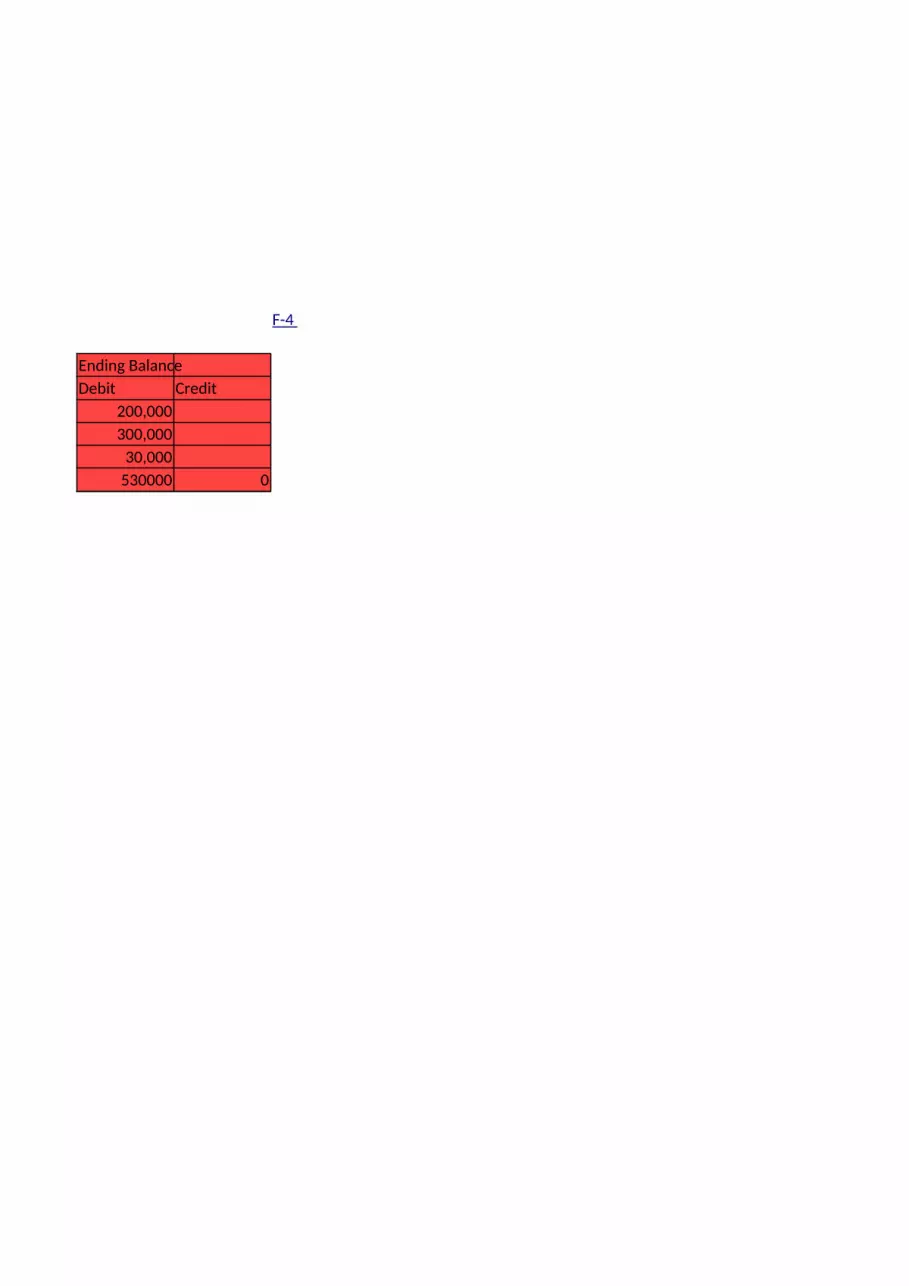

Ending BalanceDebit Credit

200,000300,000

30,000530000 0

F-4

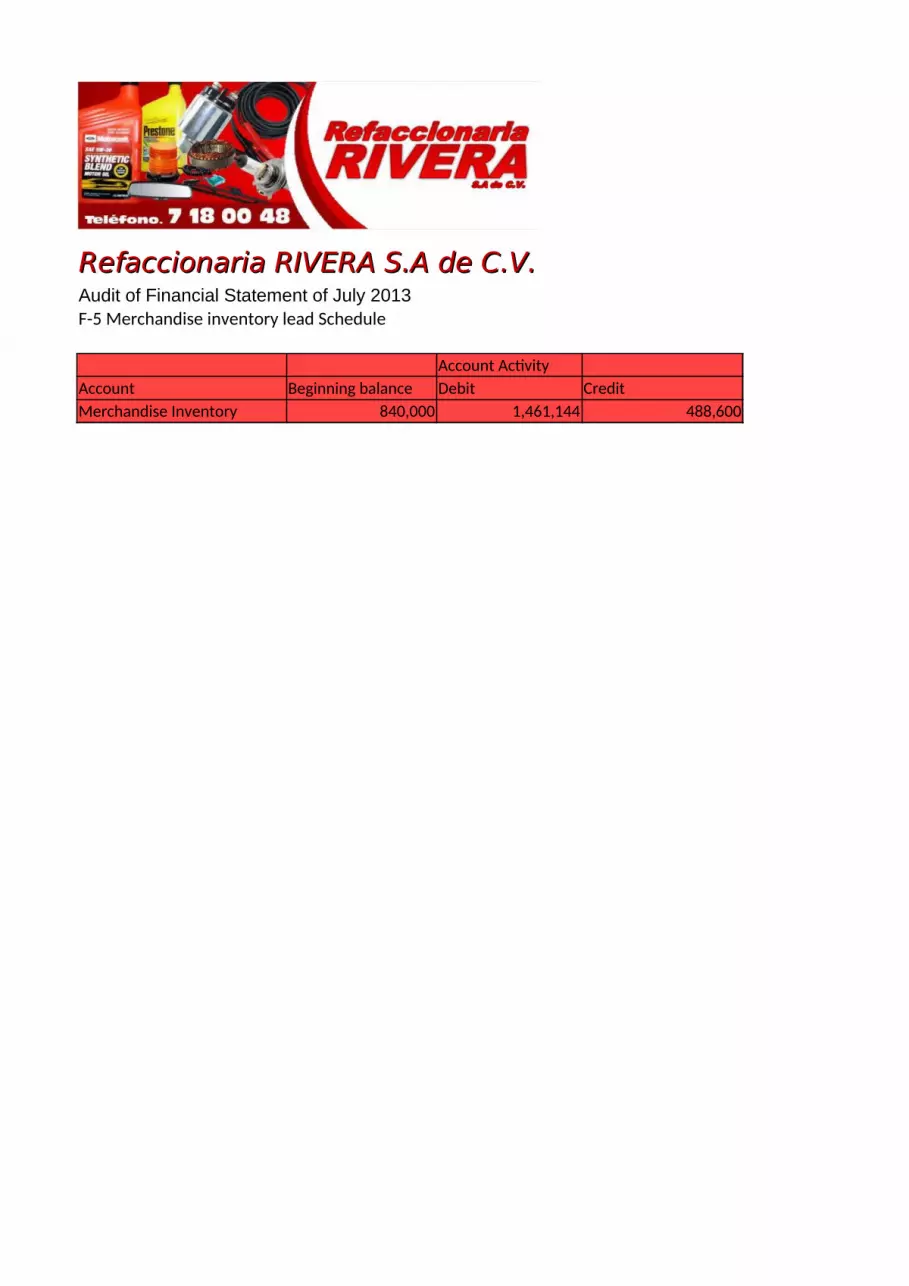

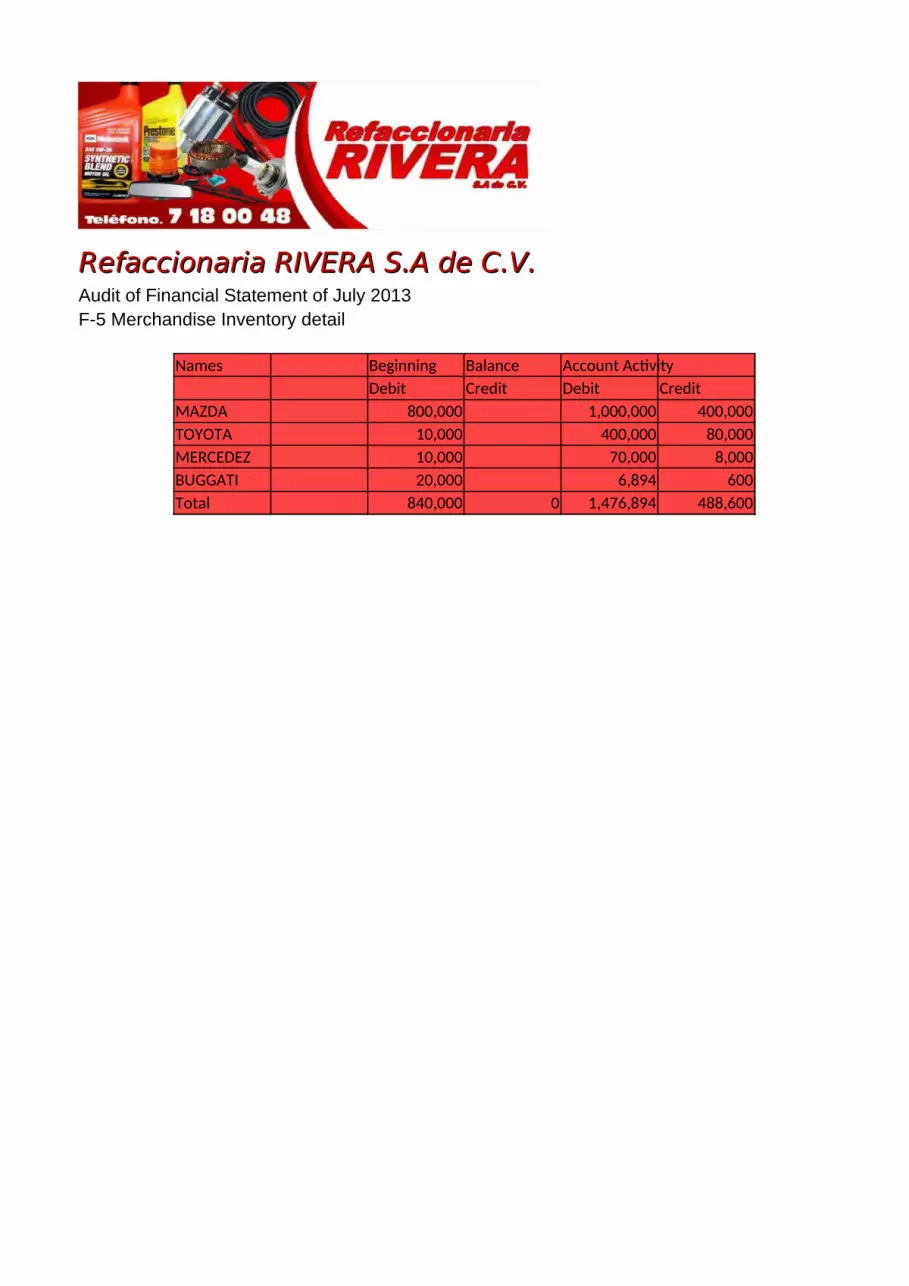

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-5 Merchandise inventory lead Schedule

Account ActivityAccount Beginning balance Debit CreditMerchandise Inventory 840,000 1,461,144 488,600

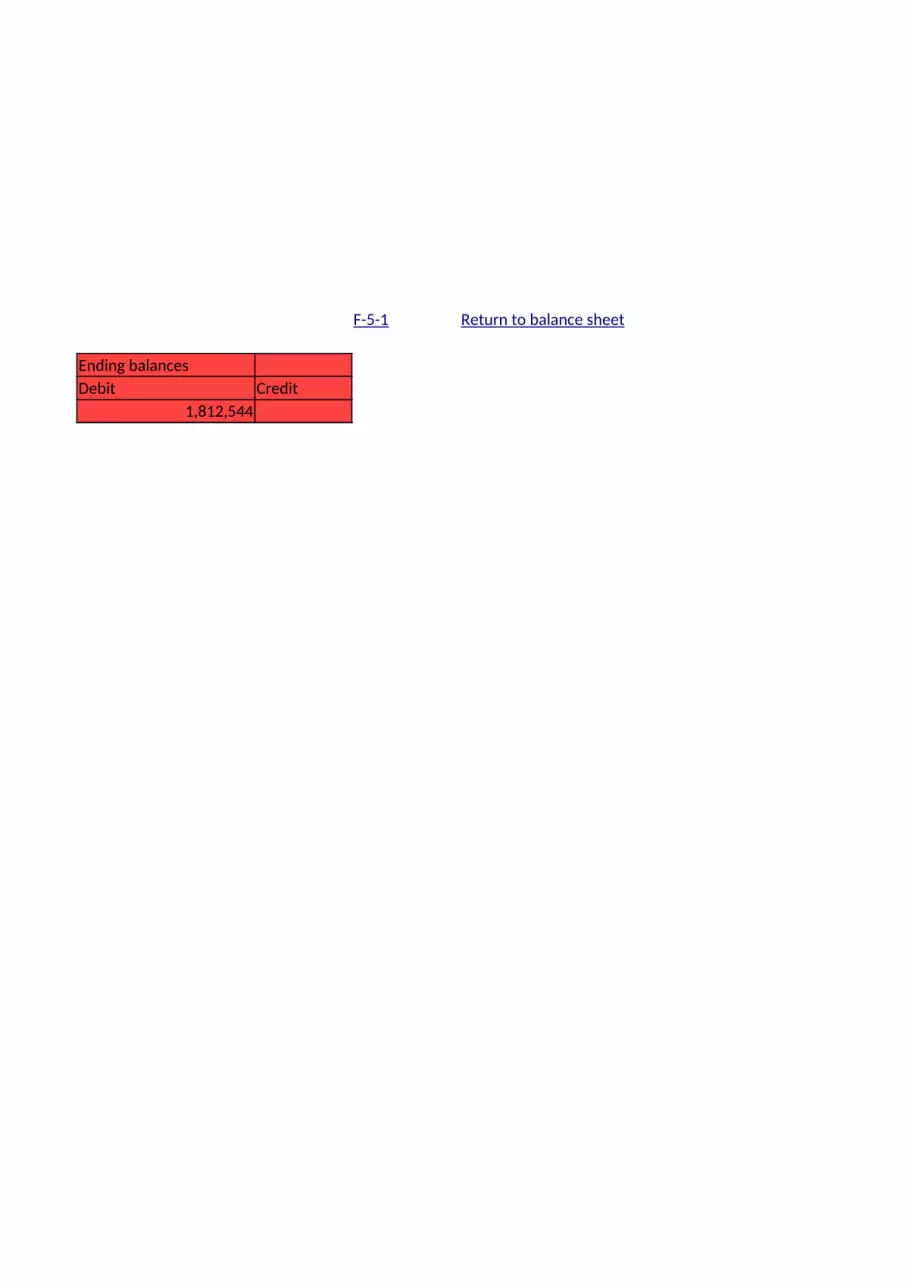

Ending balancesDebit Credit

1,812,544

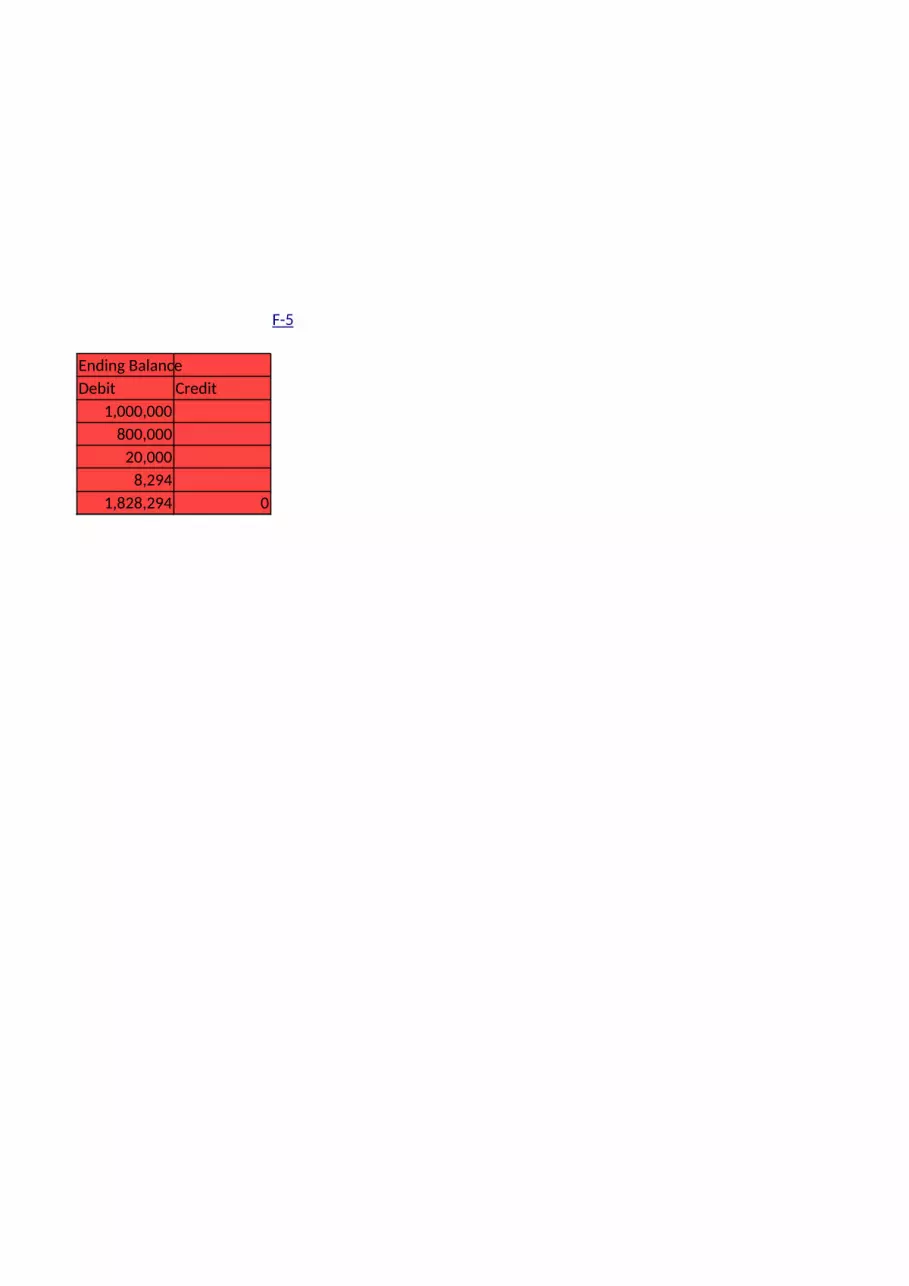

F-5-1 Return to balance sheet

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-5 Merchandise Inventory detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

MAZDA 800,000 1,000,000 400,000TOYOTA 10,000 400,000 80,000MERCEDEZ 10,000 70,000 8,000BUGGATI 20,000 6,894 600Total 840,000 0 1,476,894 488,600

Ending BalanceDebit Credit

1,000,000800,000

20,0008,294

1,828,294 0

F-5

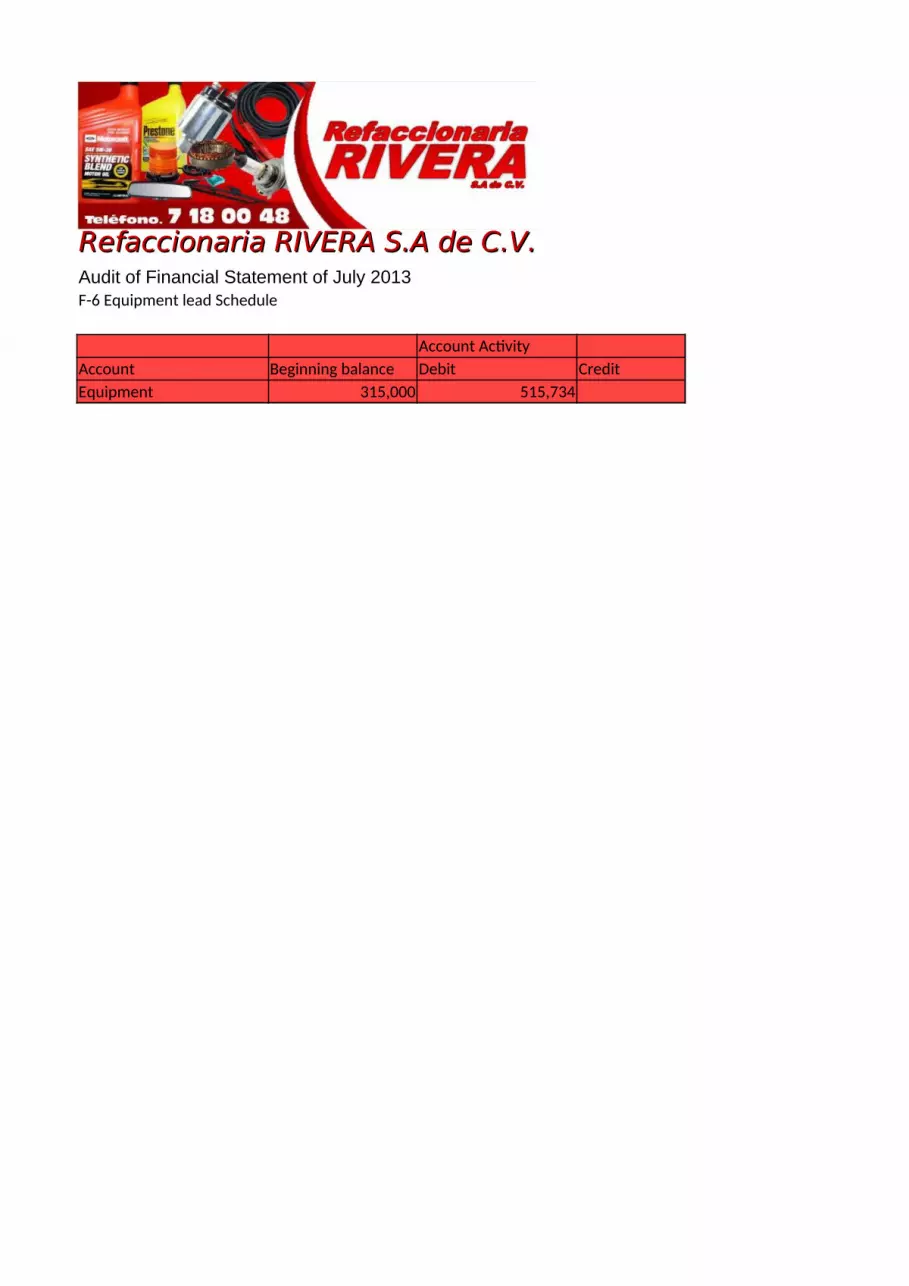

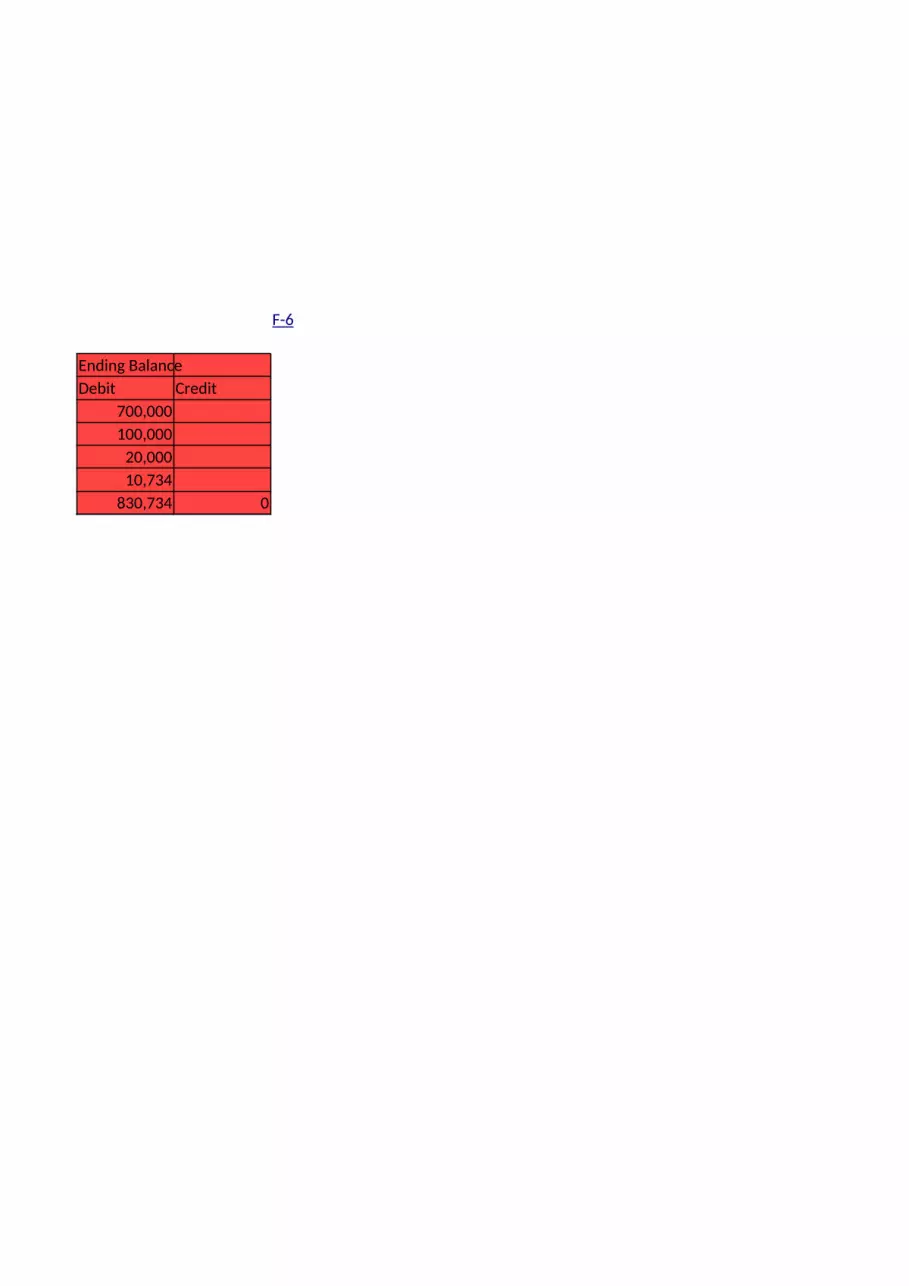

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-6 Equipment lead Schedule

Account ActivityAccount Beginning balance Debit CreditEquipment 315,000 515,734

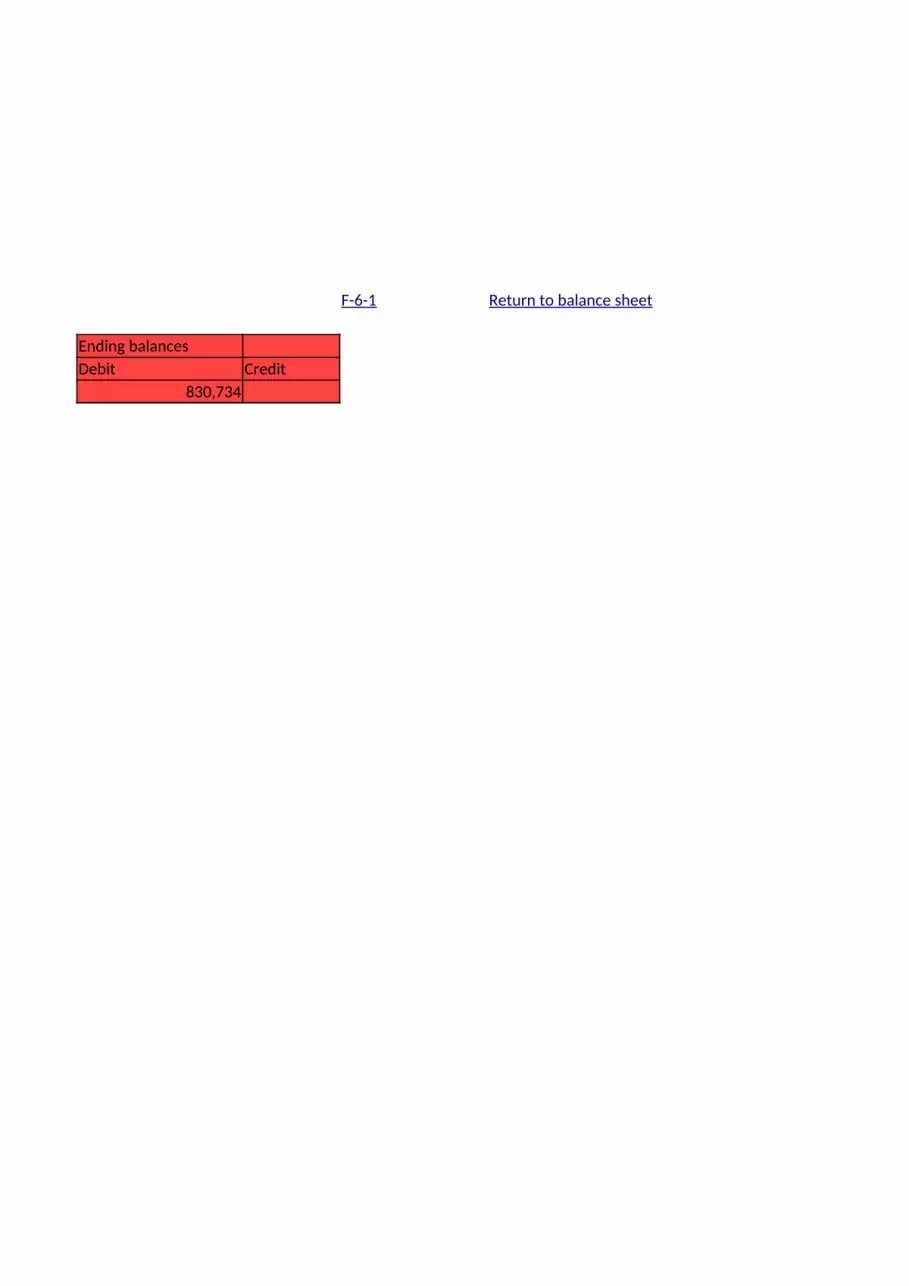

Ending balancesDebit Credit

830,734

F-6-1 Return to balance sheet

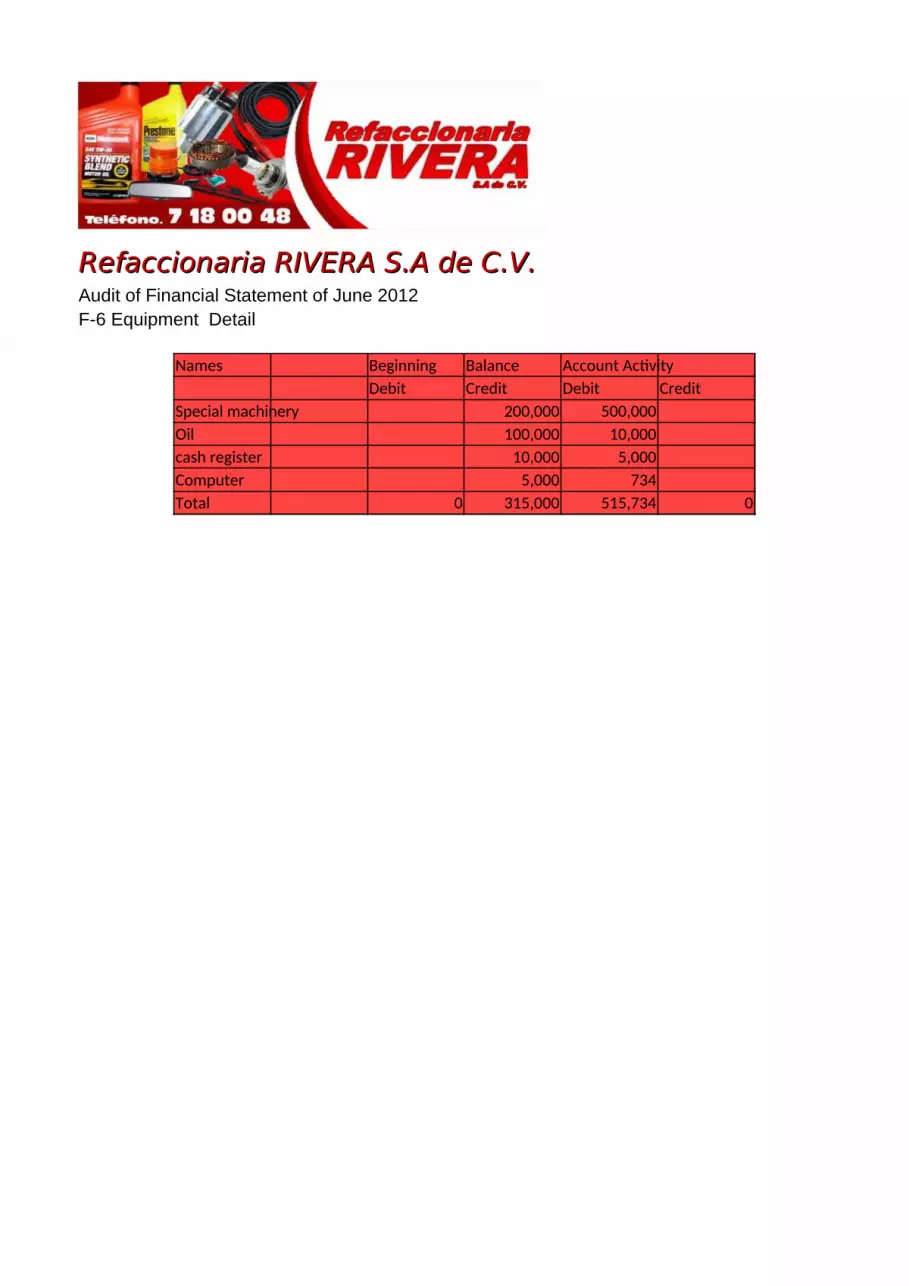

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of June 2012F-6 Equipment Detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

Special machinery 200,000 500,000Oil 100,000 10,000cash register 10,000 5,000Computer 5,000 734Total 0 315,000 515,734 0

Ending BalanceDebit Credit

700,000100,000

20,00010,734

830,734 0

F-6

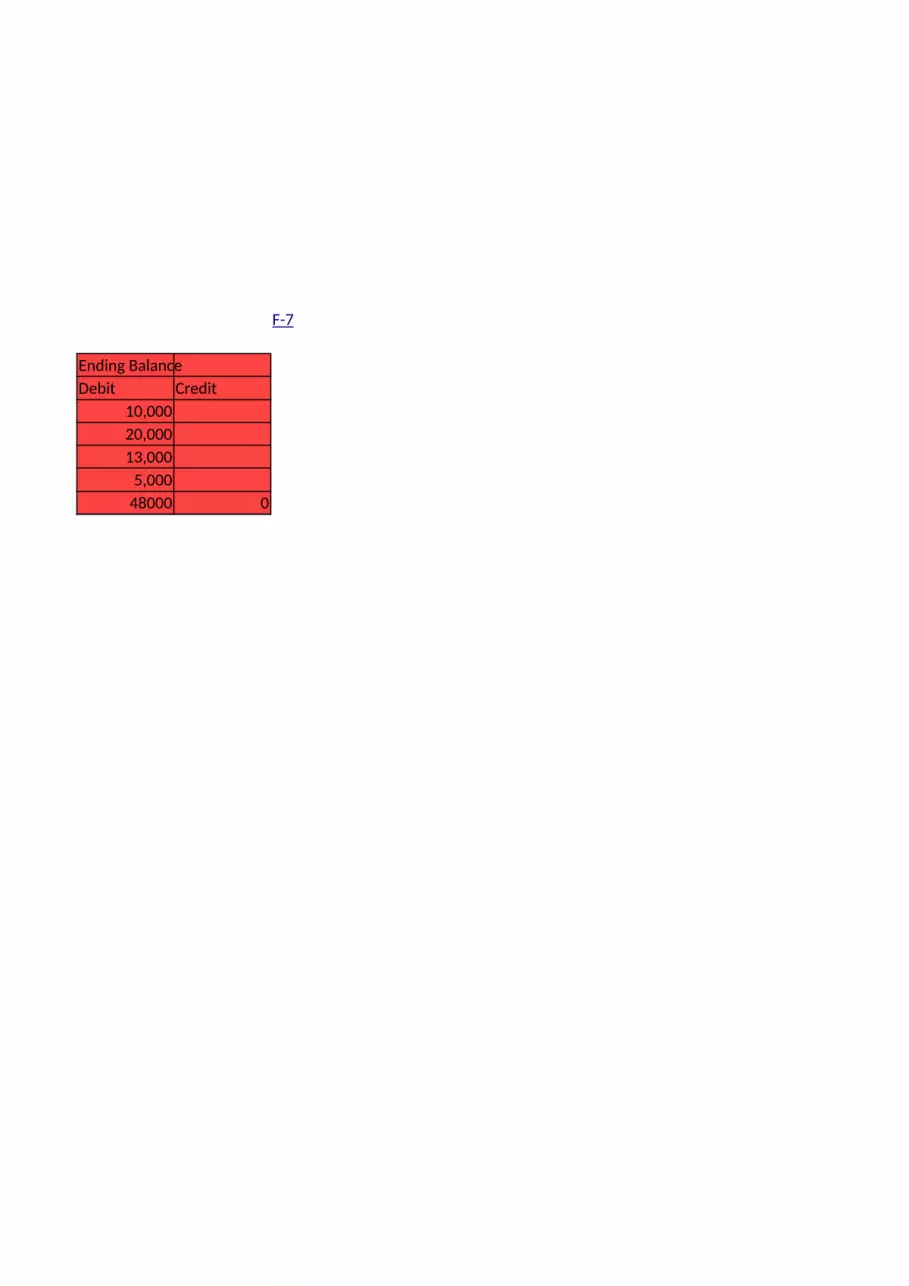

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-7 Computer Equipment lead Schedule

Account ActivityAccount Beginning balance Debit CreditComputer Equipment 48,000

Ending balancesDebit Credit

48,000

F-7-1 Return to balance sheet

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-7 Computer equipment detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

Apple Inc. 20,000Sony Corporation 10,000HP 5,000Lenovo 13,000Total 0 0 48000 0

Ending BalanceDebit Credit

10,00020,00013,000

5,00048000 0

F-7

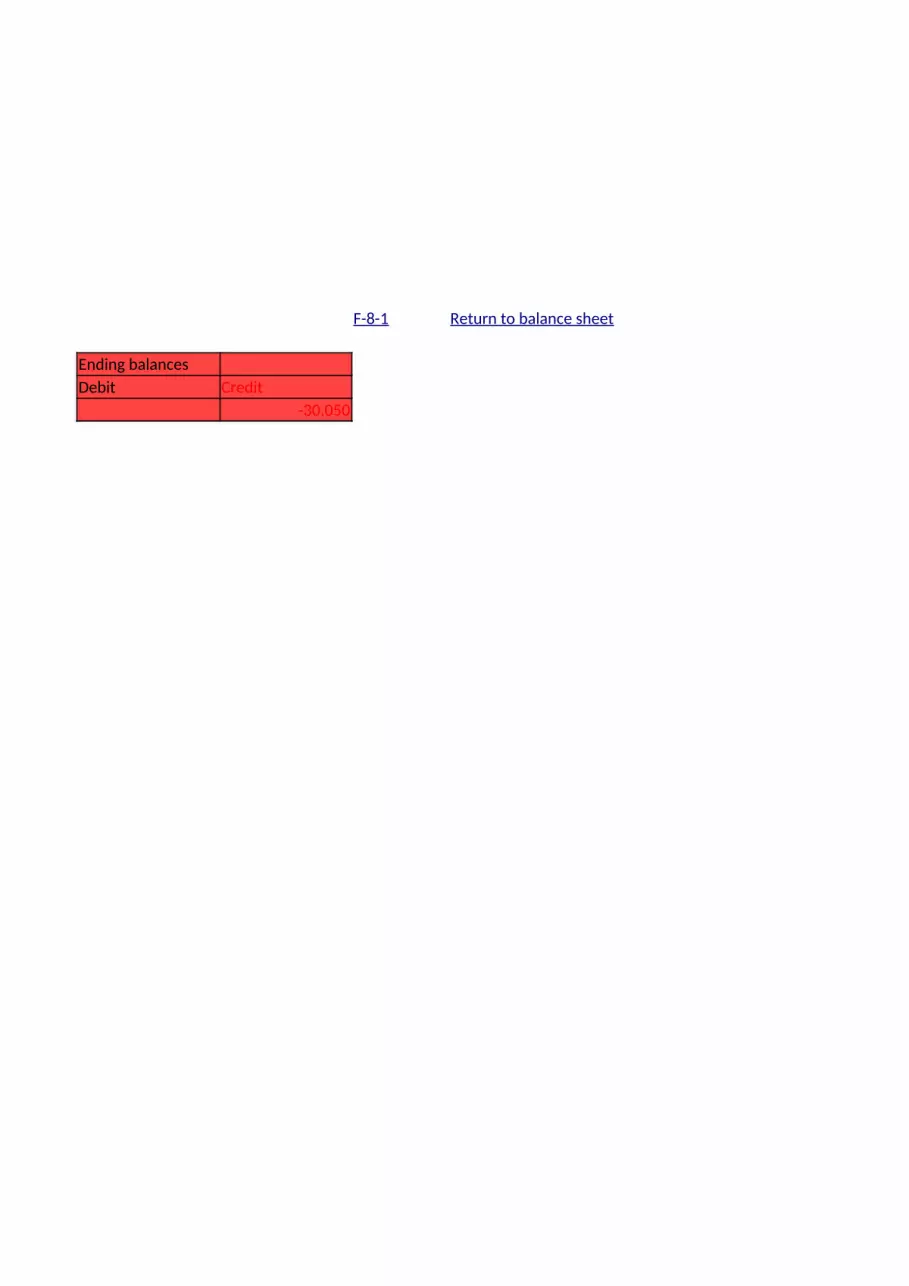

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-8 Accumulated Depreciation Lead Schedule

Account ActivityAccount Beginning balance Debit CreditAccumulated depreciation 20,000

Ending balancesDebit Credit

-30,050

F-8-1 Return to balance sheet

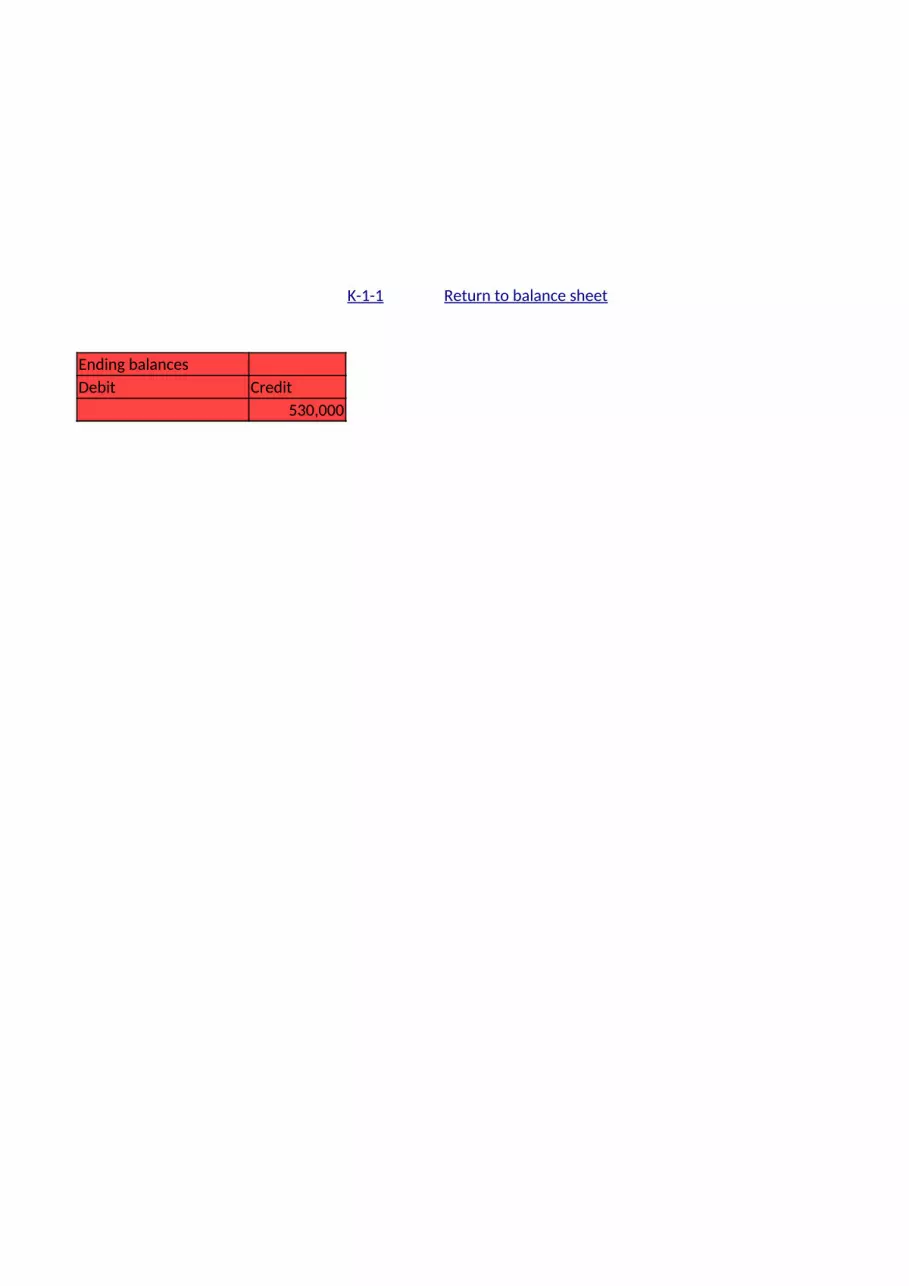

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-1 Accounts payable Lead Schedule

Account ActivityAccount Beginning balance Debit CreditAccounts payable -250000 20,000 300,000

Ending balancesDebit Credit

530,000

K-1-1 Return to balance sheet

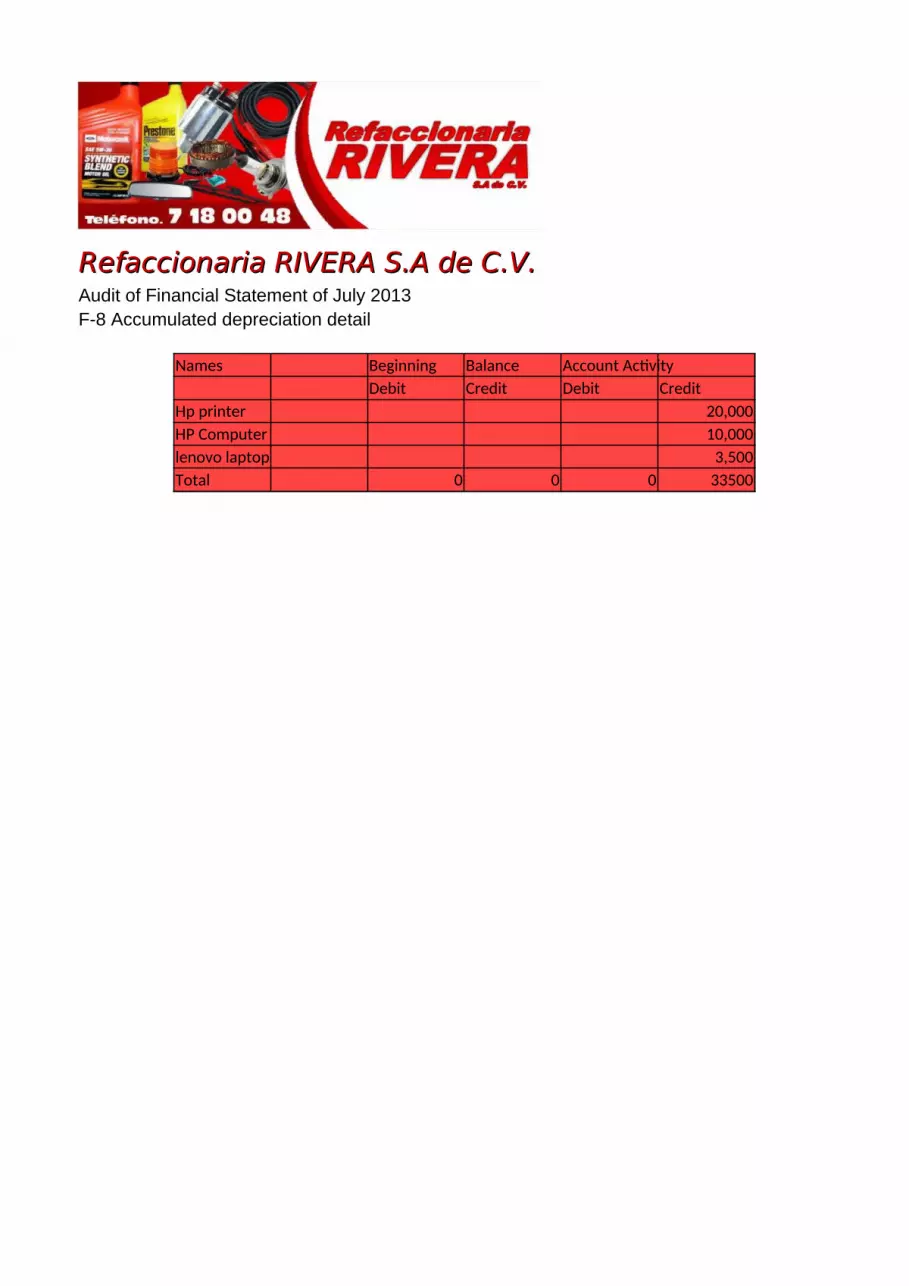

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013F-8 Accumulated depreciation detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

Hp printer 20,000HP Computer 10,000lenovo laptop 3,500Total 0 0 0 33500

Ending BalanceDebit Credit

30,0003,000

5000 33500

F-8

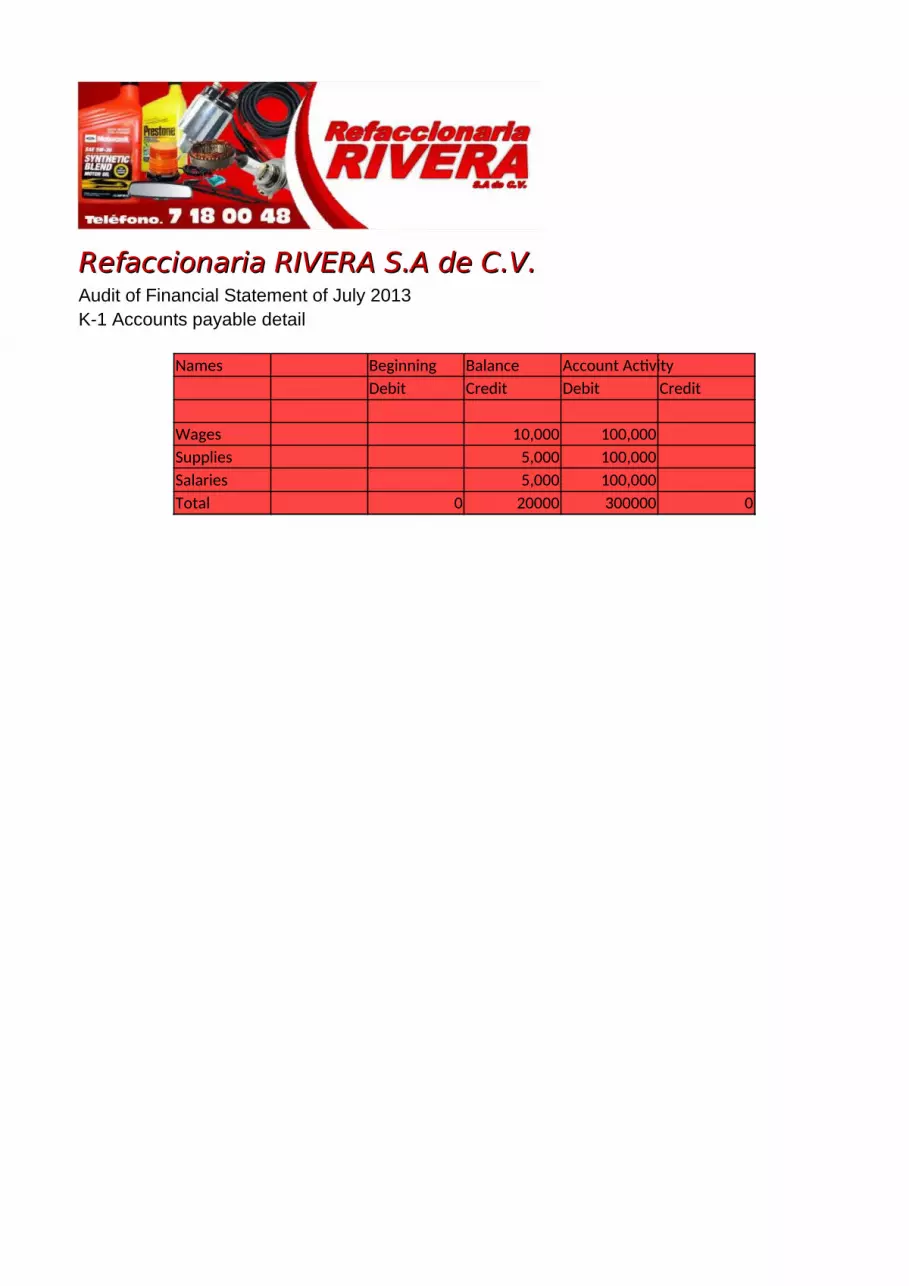

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-1 Accounts payable detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

Wages 10,000 100,000Supplies 5,000 100,000Salaries 5,000 100,000Total 0 20000 300000 0

Ending BalanceDebit Credit

500,00020,00010,000

0 530000

K-1

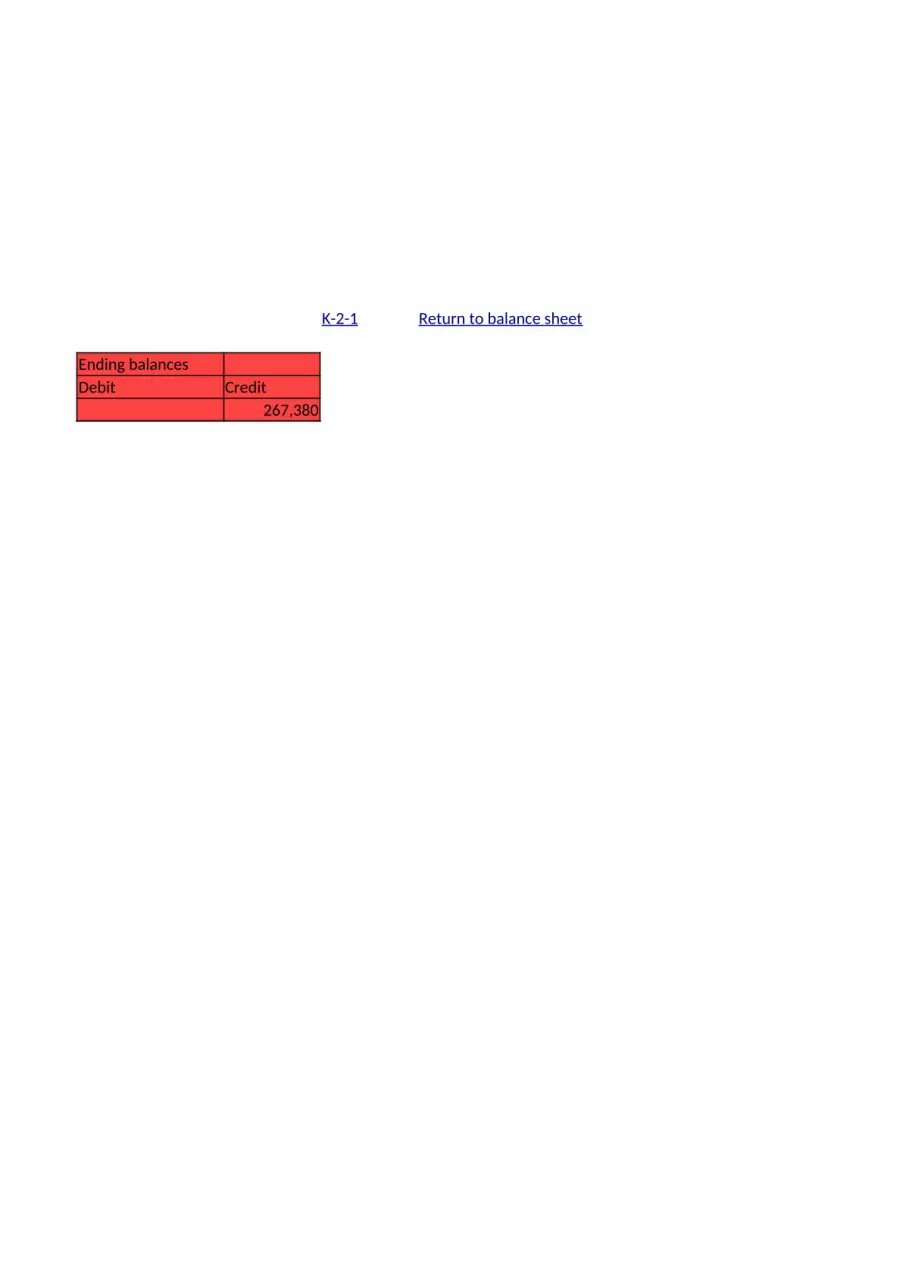

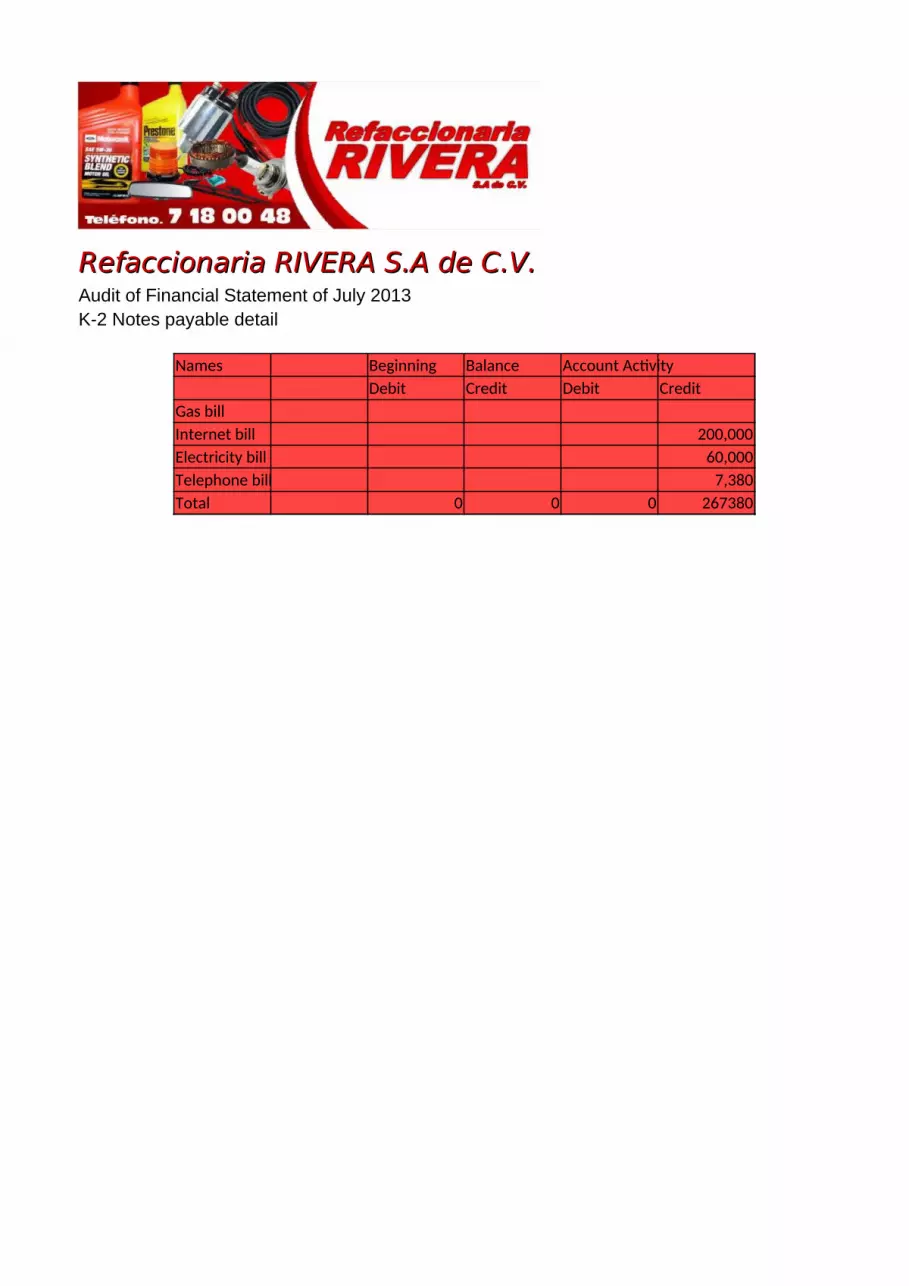

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-2 Notes payable lead Schedule

Account ActivityAccount Beginning balance Debit CreditNotes payable 267,380

Ending balancesDebit Credit

267,380

K-2-1 Return to balance sheet

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-2 Notes payable detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

Gas billInternet bill 200,000Electricity bill 60,000Telephone bill 7,380Total 0 0 0 267380

Ending BalanceDebit Credit

100,000100,000

67,3800 267380

K-2

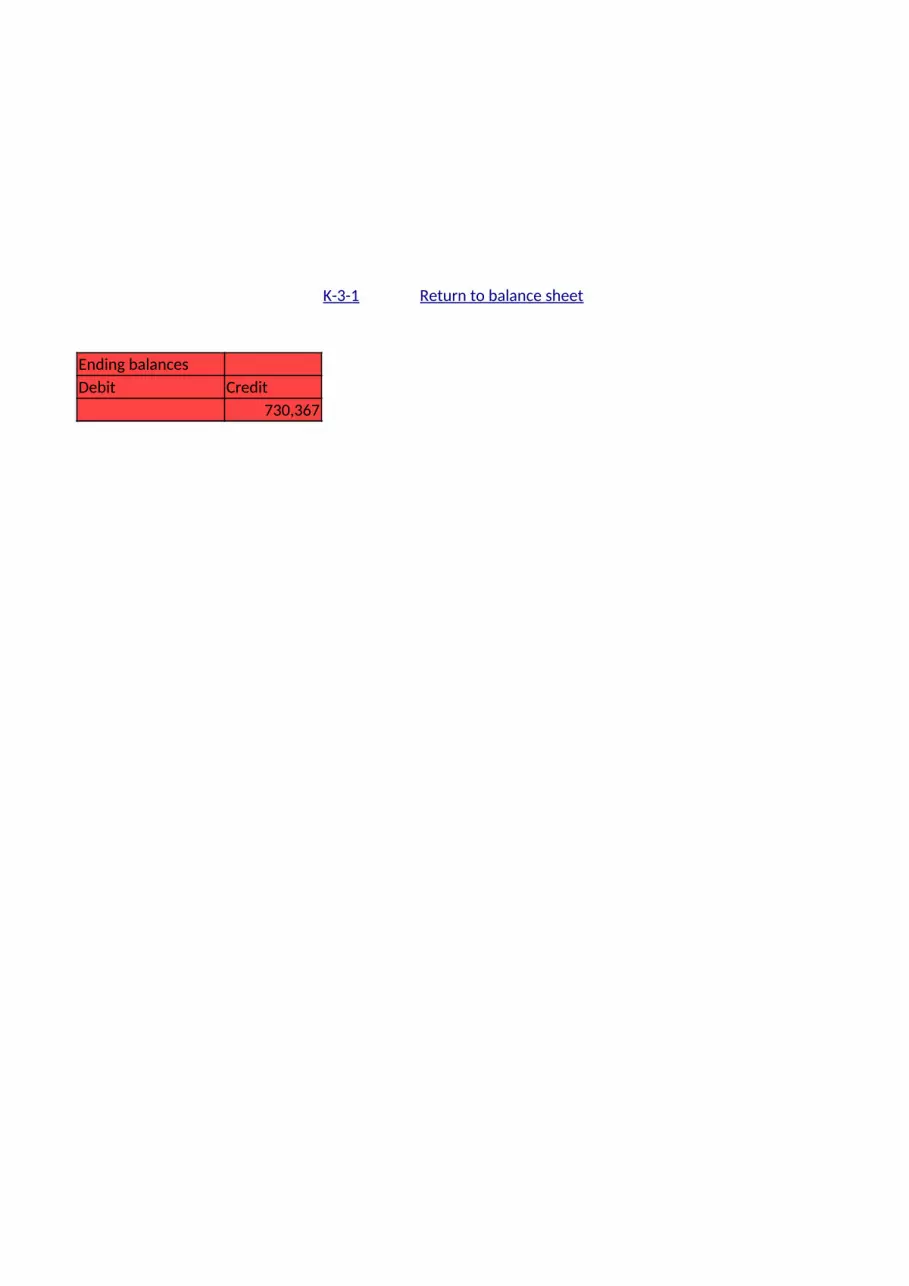

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-3 Sundry Creditors lead Schedule

Account ActivityAccount Beginning balance Debit CreditSundry creditors -315000 415,367

Ending balancesDebit Credit

730,367

K-3-1 Return to balance sheet

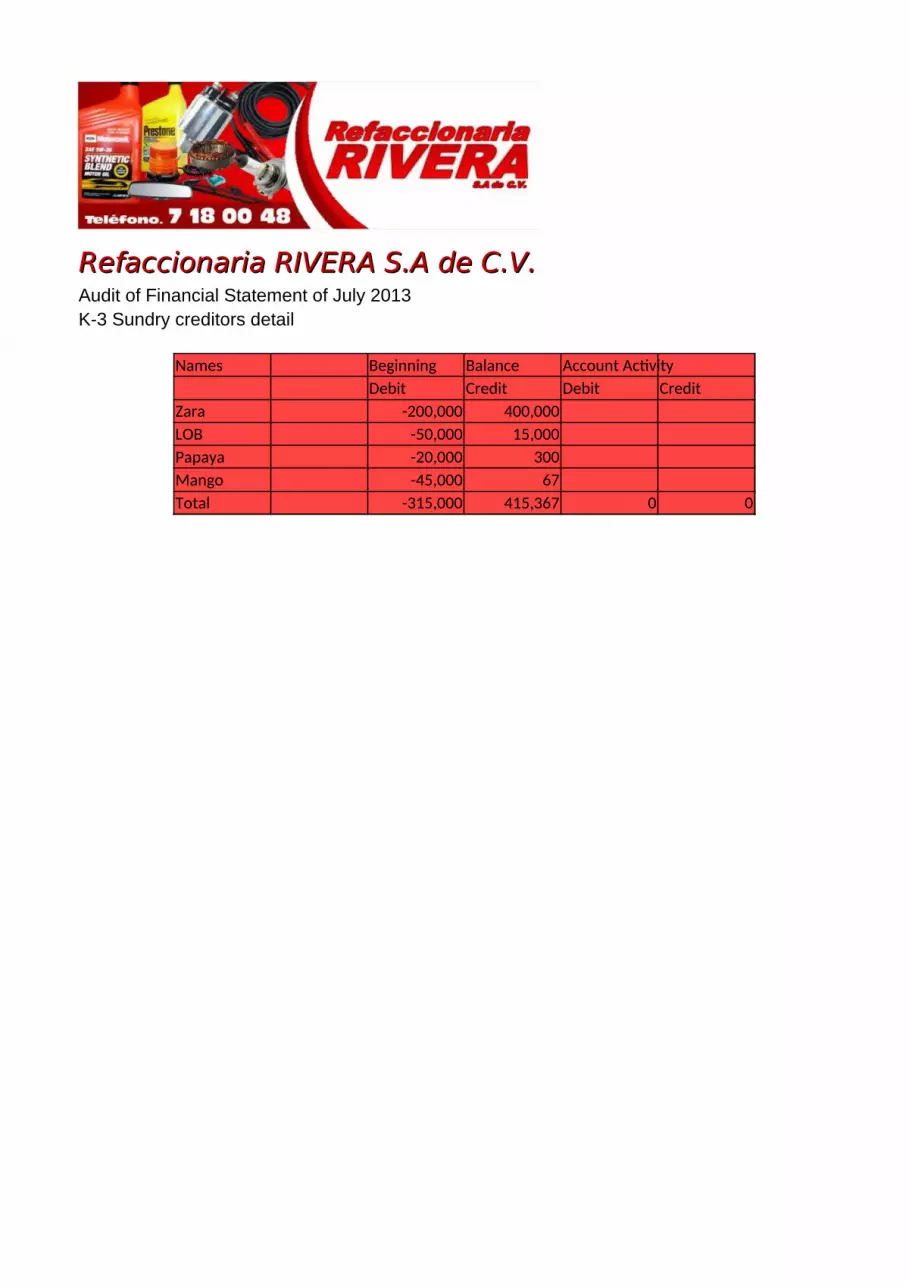

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-3 Sundry creditors detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

Zara -200,000 400,000LOB -50,000 15,000Papaya -20,000 300Mango -45,000 67Total -315,000 415,367 0 0

Ending BalanceDebit Credit

700,00030,000

30067

0 730,367

K-3

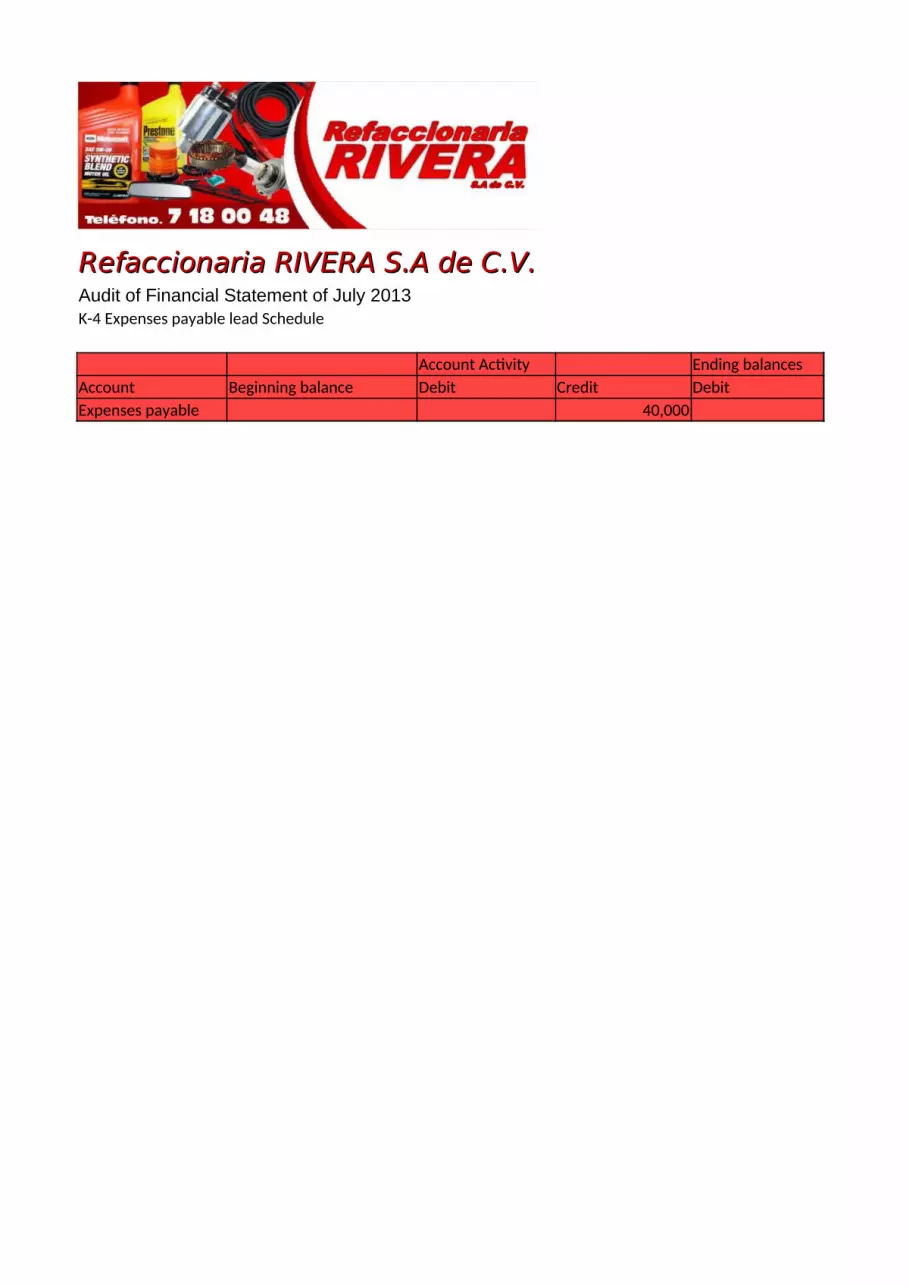

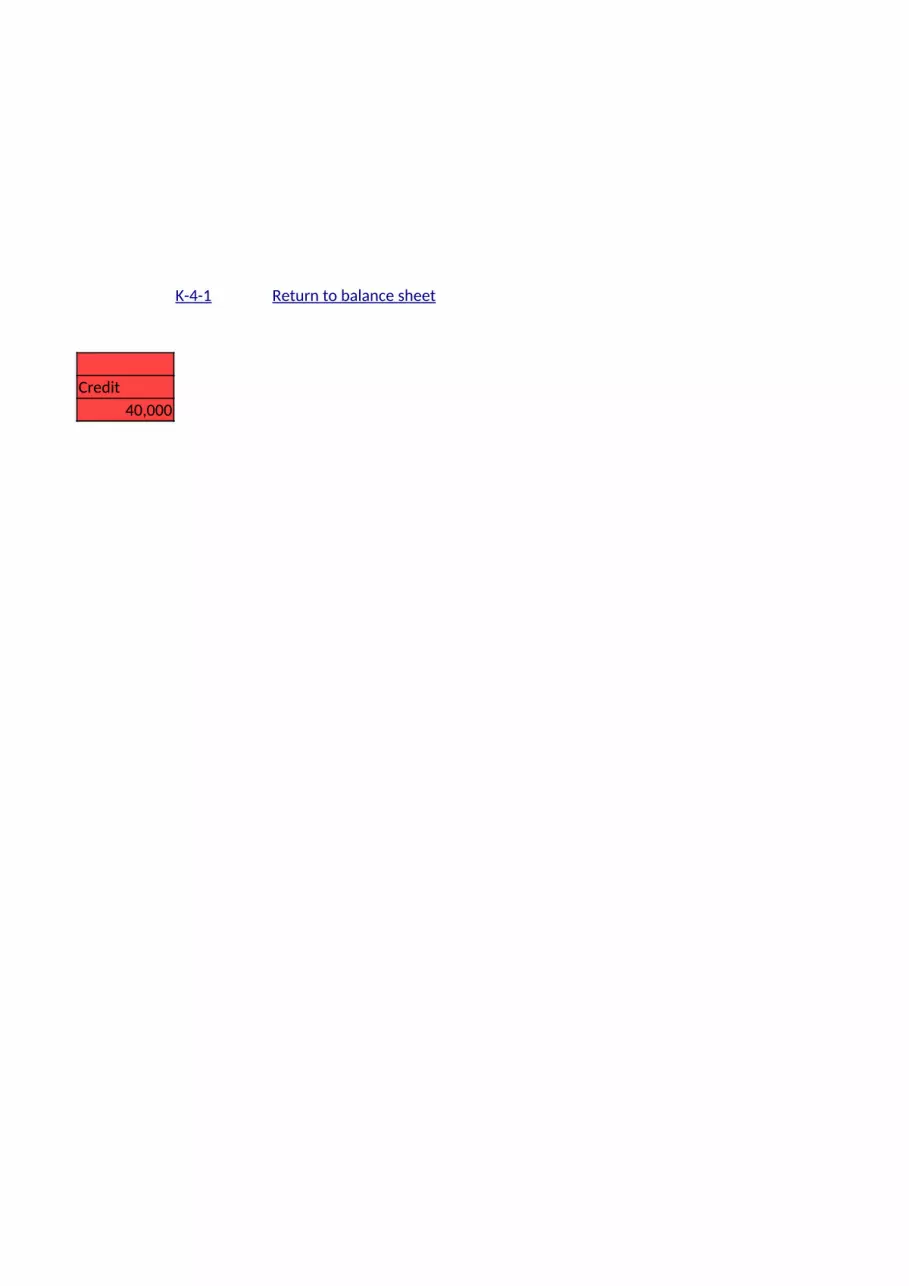

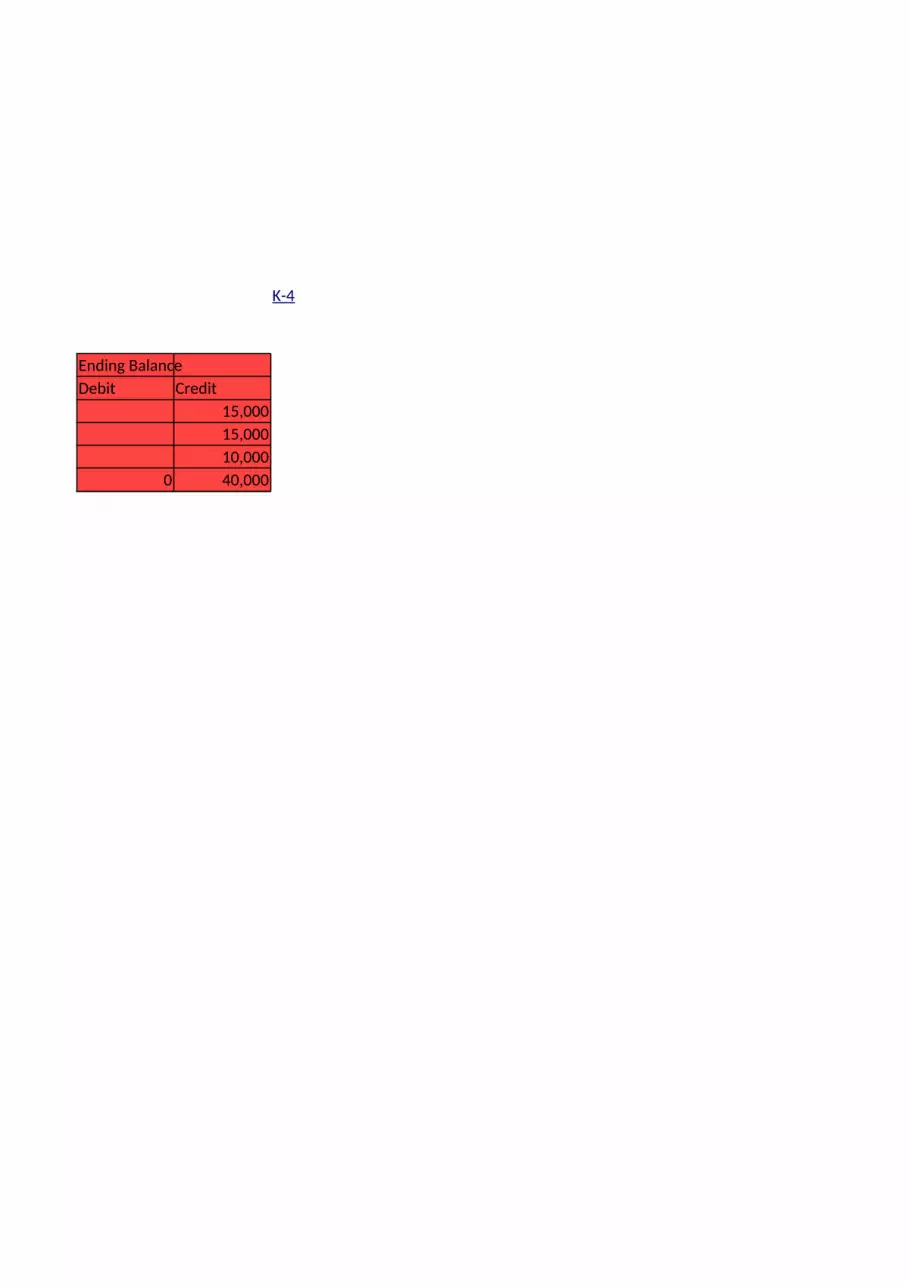

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-4 Expenses payable lead Schedule

Account Activity Ending balancesAccount Beginning balance Debit Credit DebitExpenses payable 40,000

Credit40,000

K-4-1 Return to balance sheet

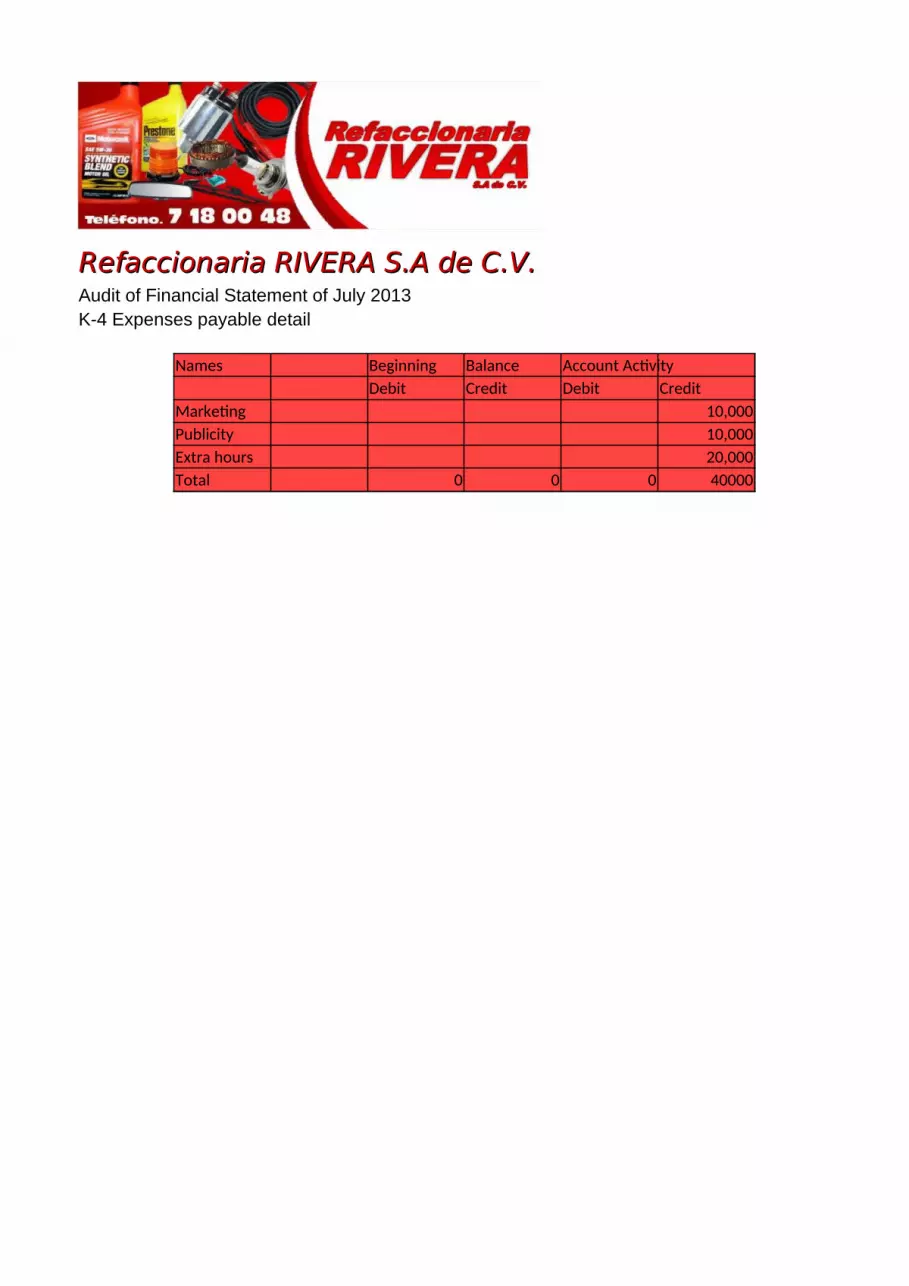

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-4 Expenses payable detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

Marketing 10,000Publicity 10,000Extra hours 20,000Total 0 0 0 40000

Ending BalanceDebit Credit

15,00015,00010,000

0 40,000

K-4

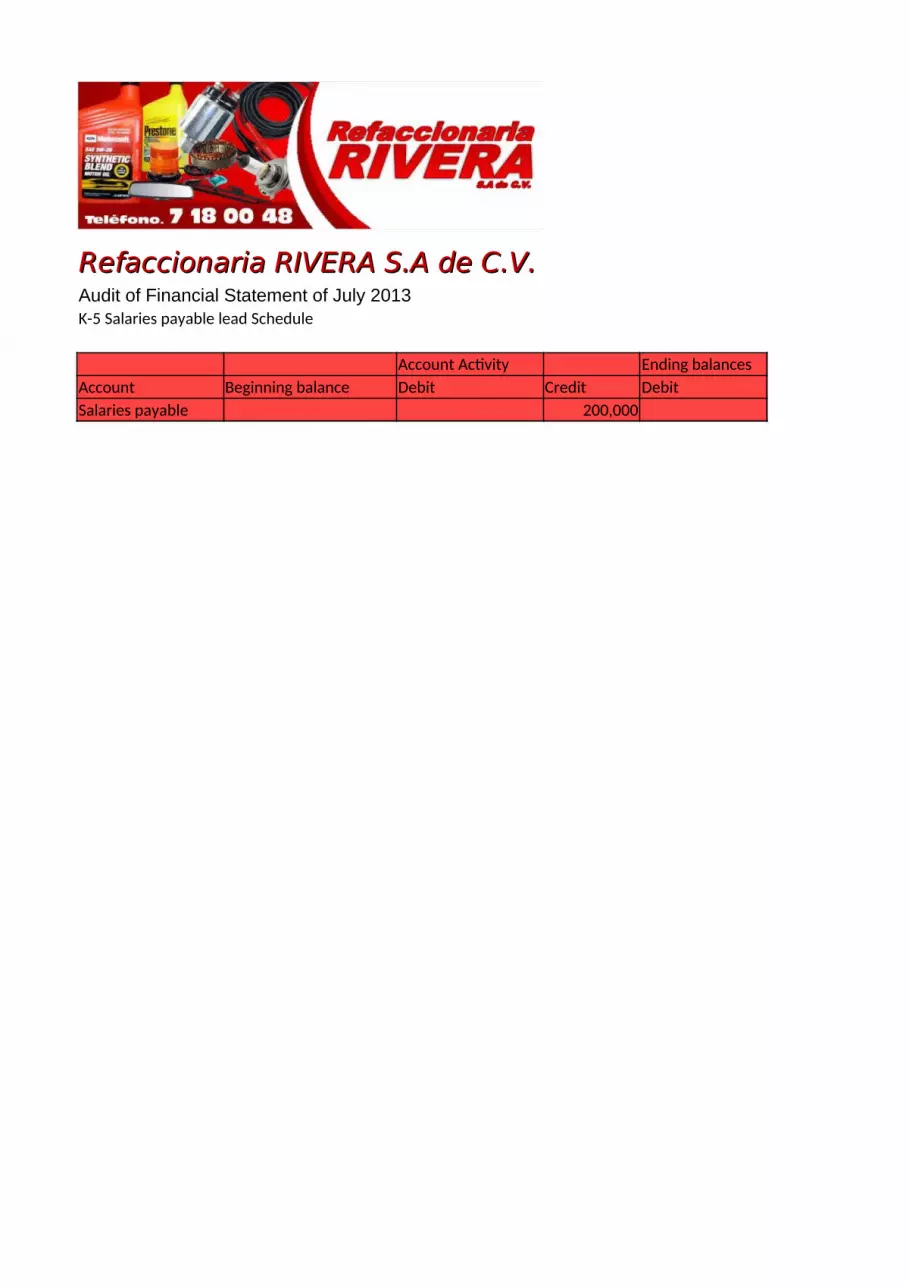

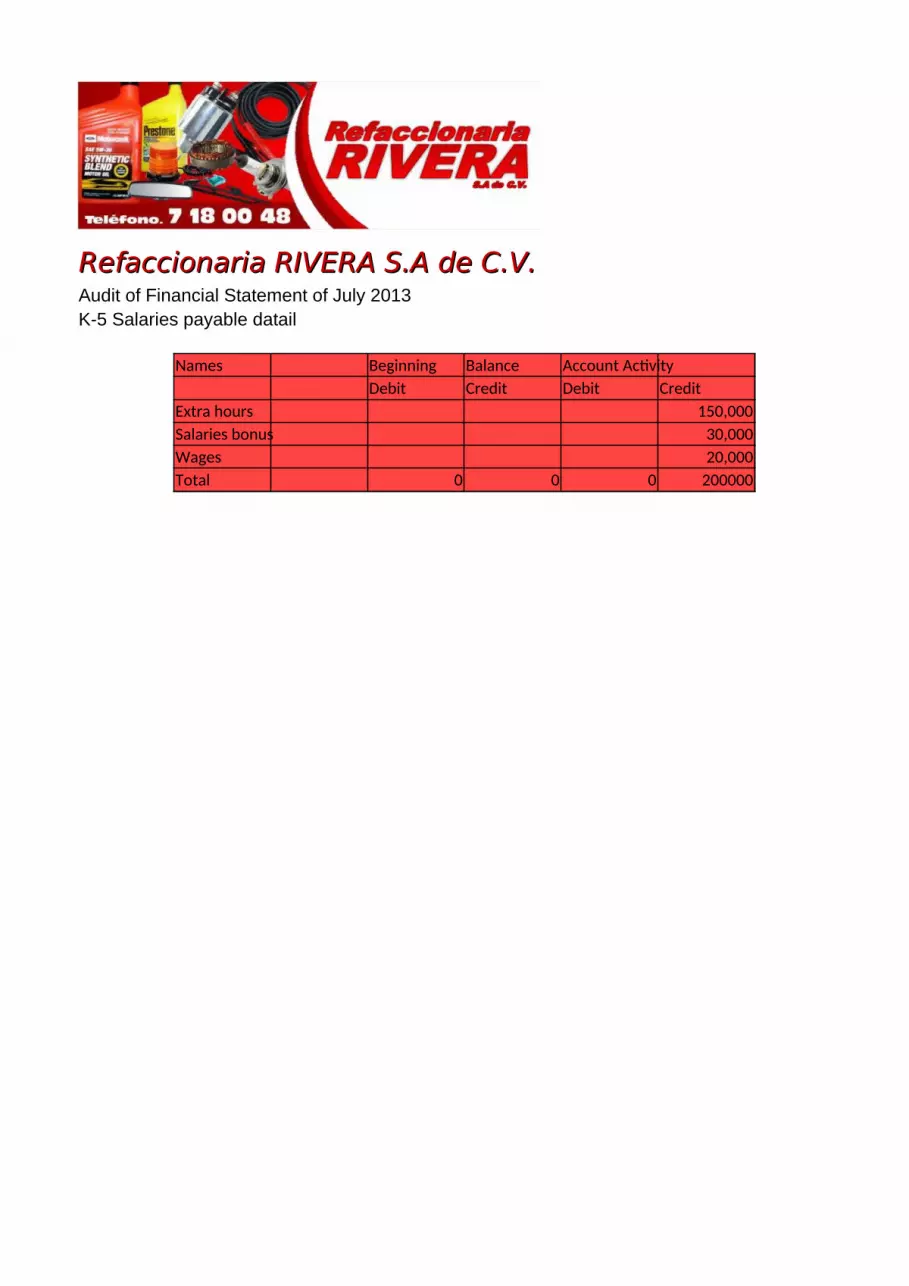

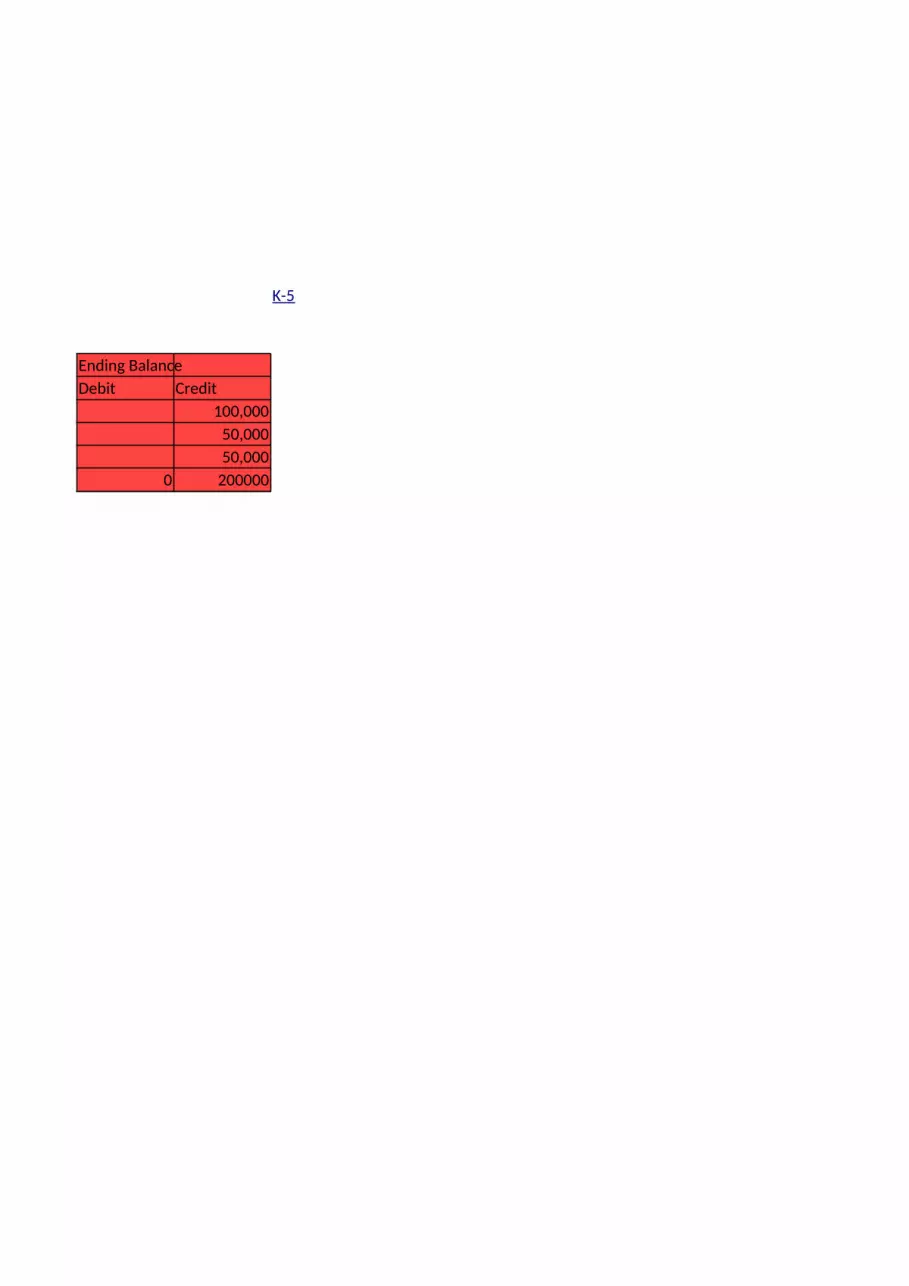

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-5 Salaries payable lead Schedule

Account Activity Ending balancesAccount Beginning balance Debit Credit DebitSalaries payable 200,000

Credit200,000

K-5-1 Return to balance sheet

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-5 Salaries payable datail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

Extra hours 150,000Salaries bonus 30,000Wages 20,000Total 0 0 0 200000

Ending BalanceDebit Credit

100,00050,00050,000

0 200000

K-5

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-6 Taxes payable lead Schedule

Account Activity Ending balancesAccount Beginning balance Debit Credit DebitTaxes payable 148,838.40

Credit148,838.40

K-6-1 Return to balance sheet

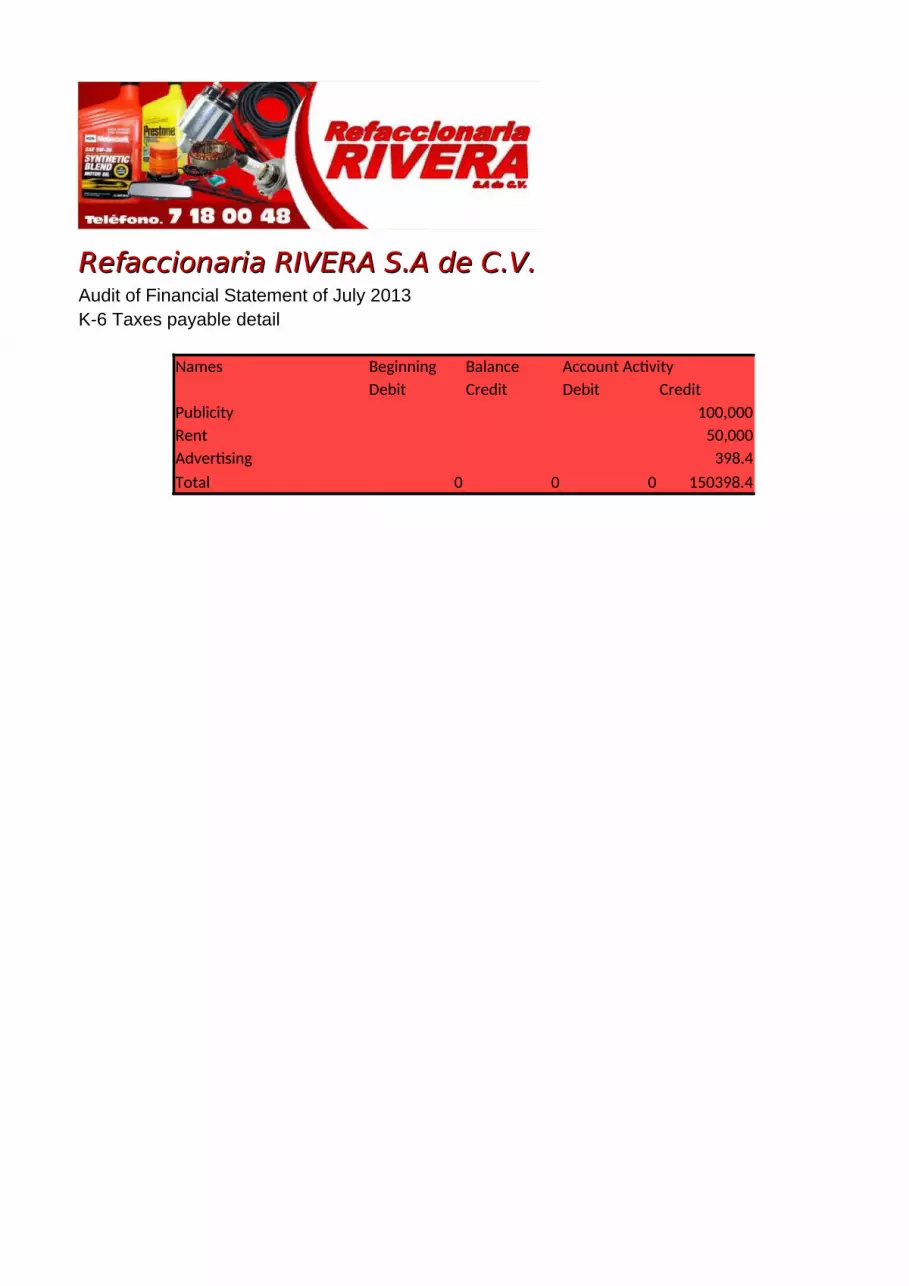

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013K-6 Taxes payable detail

Names Beginning Balance Account ActivityDebit Credit Debit Credit

Publicity 100,000Rent 50,000Advertising 398.4Total 0 0 0 150398.4

Ending BalanceDebit Credit

398.4100,000

50,0000 150398.4

K-6

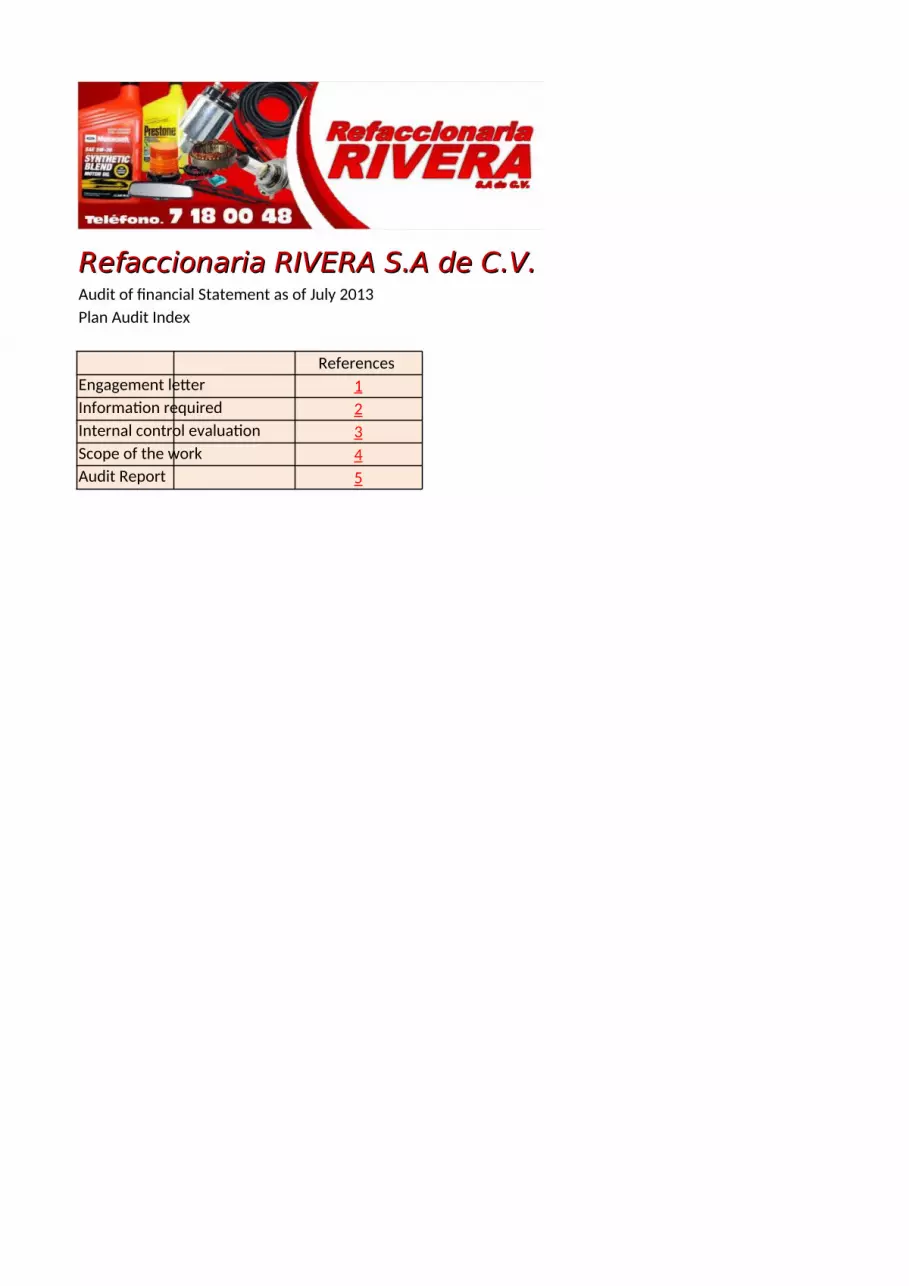

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of financial Statement as of July 2013Plan Audit Index

References Engagement letter 1Information required 2Internal control evaluation 3Scope of the work 4Audit Report 5

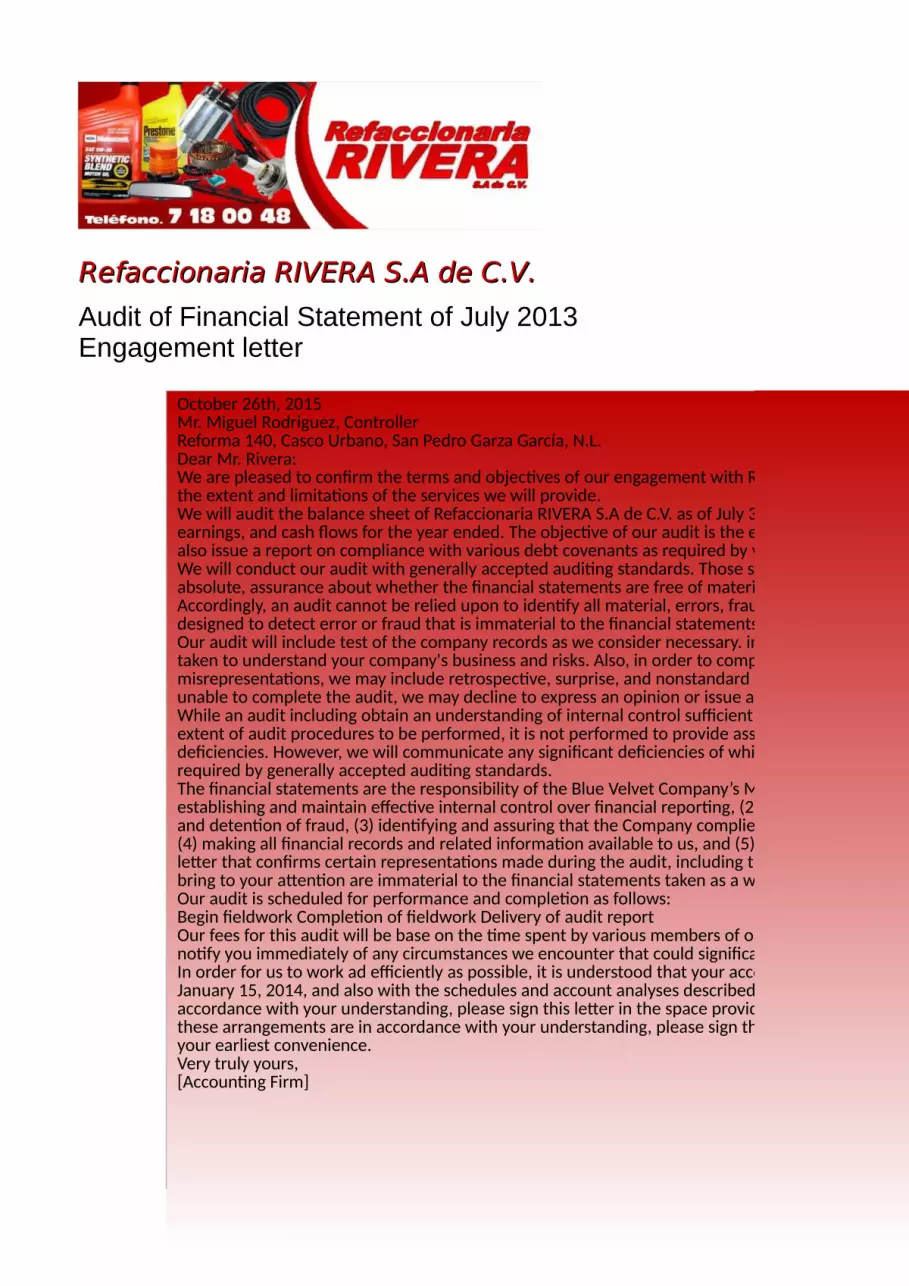

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of Financial Statement of July 2013Engagement letter

October 26th, 2015Mr. Miguel Rodriguez, Controller Reforma 140, Casco Urbano, San Pedro Garza García, N.L.Dear Mr. Rivera:We are pleased to confirm the terms and objectives of our engagement with Refaccionaria RIVERA S.A de C.V. for July, 2013 and to clarify the extent and limitations of the services we will provide.We will audit the balance sheet of Refaccionaria RIVERA S.A de C.V. as of July 30th, 2013 and the related statements of income, retained earnings, and cash flows for the year ended. The objective of our audit is the expression of an opinion on the financial statements. We will also issue a report on compliance with various debt covenants as required by your debt agreement with Western Financial Services. We will conduct our audit with generally accepted auditing standards. Those standards require that we obtain reasonable, rather than absolute, assurance about whether the financial statements are free of material misstatement, whether cause by error or fraud. Accordingly, an audit cannot be relied upon to identify all material, errors, fraud, or illegal acts that may exist. Also an audit is not designed to detect error or fraud that is immaterial to the financial statements.Our audit will include test of the company records as we consider necessary. important among our audit planning procedures will be steps taken to understand your company's business and risks. Also, in order to comply with professional obligations to identify misrepresentations, we may include retrospective, surprise, and nonstandard procedures in our audit plan. If, for any reason, we are unable to complete the audit, we may decline to express an opinion or issue a report as a result of the engagement.While an audit including obtain an understanding of internal control sufficient to plan the audit and to determine the nature, timing, and extent of audit procedures to be performed, it is not performed to provide assurance on internal control or to identify significant deficiencies. However, we will communicate any significant deficiencies of which we become aware and make any other communications required by generally accepted auditing standards.The financial statements are the responsibility of the Blue Velvet Company’s Management.. Management is also responsible (1) establishing and maintain effective internal control over financial reporting, (2) establishing systems and procedures for the prevention and detention of fraud, (3) identifying and assuring that the Company complies with the laws and regulations applicable to its activities, (4) making all financial records and related information available to us, and (5) at the conclusion of the engagement, proving us with a letter that confirms certain representations made during the audit, including that the effects of any uncorrected misstatements that we bring to your attention are immaterial to the financial statements taken as a whole.Our audit is scheduled for performance and completion as follows:Begin fieldwork Completion of fieldwork Delivery of audit reportOur fees for this audit will be base on the time spent by various members of our staffs at our regular rates, plus direct expenses. We will notify you immediately of any circumstances we encounter that could significantly affect our initial fee estimate of $120,000.In order for us to work ad efficiently as possible, it is understood that your account staff will provide us with a year-end trial balance by January 15, 2014, and also with the schedules and account analyses described on the separate attachment. If these arrangements are in accordance with your understanding, please sign this letter in the space provided and return a copy to us at your earliest convenience. If these arrangements are in accordance with your understanding, please sign this letter in the space provided and return a copy to us at your earliest convenience.Very truly yours,[Accounting Firm]

October 26th, 2015Mr. Miguel Rodriguez, Controller Reforma 140, Casco Urbano, San Pedro Garza García, N.L.Dear Mr. Rivera:We are pleased to confirm the terms and objectives of our engagement with Refaccionaria RIVERA S.A de C.V. for July, 2013 and to clarify the extent and limitations of the services we will provide.We will audit the balance sheet of Refaccionaria RIVERA S.A de C.V. as of July 30th, 2013 and the related statements of income, retained earnings, and cash flows for the year ended. The objective of our audit is the expression of an opinion on the financial statements. We will also issue a report on compliance with various debt covenants as required by your debt agreement with Western Financial Services. We will conduct our audit with generally accepted auditing standards. Those standards require that we obtain reasonable, rather than absolute, assurance about whether the financial statements are free of material misstatement, whether cause by error or fraud. Accordingly, an audit cannot be relied upon to identify all material, errors, fraud, or illegal acts that may exist. Also an audit is not designed to detect error or fraud that is immaterial to the financial statements.Our audit will include test of the company records as we consider necessary. important among our audit planning procedures will be steps taken to understand your company's business and risks. Also, in order to comply with professional obligations to identify misrepresentations, we may include retrospective, surprise, and nonstandard procedures in our audit plan. If, for any reason, we are unable to complete the audit, we may decline to express an opinion or issue a report as a result of the engagement.While an audit including obtain an understanding of internal control sufficient to plan the audit and to determine the nature, timing, and extent of audit procedures to be performed, it is not performed to provide assurance on internal control or to identify significant deficiencies. However, we will communicate any significant deficiencies of which we become aware and make any other communications required by generally accepted auditing standards.The financial statements are the responsibility of the Blue Velvet Company’s Management.. Management is also responsible (1) establishing and maintain effective internal control over financial reporting, (2) establishing systems and procedures for the prevention and detention of fraud, (3) identifying and assuring that the Company complies with the laws and regulations applicable to its activities, (4) making all financial records and related information available to us, and (5) at the conclusion of the engagement, proving us with a letter that confirms certain representations made during the audit, including that the effects of any uncorrected misstatements that we bring to your attention are immaterial to the financial statements taken as a whole.Our audit is scheduled for performance and completion as follows:Begin fieldwork Completion of fieldwork Delivery of audit reportOur fees for this audit will be base on the time spent by various members of our staffs at our regular rates, plus direct expenses. We will notify you immediately of any circumstances we encounter that could significantly affect our initial fee estimate of $120,000.In order for us to work ad efficiently as possible, it is understood that your account staff will provide us with a year-end trial balance by January 15, 2014, and also with the schedules and account analyses described on the separate attachment. If these arrangements are in accordance with your understanding, please sign this letter in the space provided and return a copy to us at your earliest convenience. If these arrangements are in accordance with your understanding, please sign this letter in the space provided and return a copy to us at your earliest convenience.Very truly yours,[Accounting Firm]

Return to Plan audit index

October 26th, 2015Mr. Miguel Rodriguez, Controller Reforma 140, Casco Urbano, San Pedro Garza García, N.L.Dear Mr. Rivera:We are pleased to confirm the terms and objectives of our engagement with Refaccionaria RIVERA S.A de C.V. for July, 2013 and to clarify the extent and limitations of the services we will provide.We will audit the balance sheet of Refaccionaria RIVERA S.A de C.V. as of July 30th, 2013 and the related statements of income, retained earnings, and cash flows for the year ended. The objective of our audit is the expression of an opinion on the financial statements. We will also issue a report on compliance with various debt covenants as required by your debt agreement with Western Financial Services. We will conduct our audit with generally accepted auditing standards. Those standards require that we obtain reasonable, rather than absolute, assurance about whether the financial statements are free of material misstatement, whether cause by error or fraud. Accordingly, an audit cannot be relied upon to identify all material, errors, fraud, or illegal acts that may exist. Also an audit is not designed to detect error or fraud that is immaterial to the financial statements.Our audit will include test of the company records as we consider necessary. important among our audit planning procedures will be steps taken to understand your company's business and risks. Also, in order to comply with professional obligations to identify misrepresentations, we may include retrospective, surprise, and nonstandard procedures in our audit plan. If, for any reason, we are unable to complete the audit, we may decline to express an opinion or issue a report as a result of the engagement.While an audit including obtain an understanding of internal control sufficient to plan the audit and to determine the nature, timing, and extent of audit procedures to be performed, it is not performed to provide assurance on internal control or to identify significant deficiencies. However, we will communicate any significant deficiencies of which we become aware and make any other communications required by generally accepted auditing standards.The financial statements are the responsibility of the Blue Velvet Company’s Management.. Management is also responsible (1) establishing and maintain effective internal control over financial reporting, (2) establishing systems and procedures for the prevention and detention of fraud, (3) identifying and assuring that the Company complies with the laws and regulations applicable to its activities, (4) making all financial records and related information available to us, and (5) at the conclusion of the engagement, proving us with a letter that confirms certain representations made during the audit, including that the effects of any uncorrected misstatements that we bring to your attention are immaterial to the financial statements taken as a whole.Our audit is scheduled for performance and completion as follows:Begin fieldwork Completion of fieldwork Delivery of audit reportOur fees for this audit will be base on the time spent by various members of our staffs at our regular rates, plus direct expenses. We will notify you immediately of any circumstances we encounter that could significantly affect our initial fee estimate of $120,000.In order for us to work ad efficiently as possible, it is understood that your account staff will provide us with a year-end trial balance by January 15, 2014, and also with the schedules and account analyses described on the separate attachment. If these arrangements are in accordance with your understanding, please sign this letter in the space provided and return a copy to us at your earliest convenience. If these arrangements are in accordance with your understanding, please sign this letter in the space provided and return a copy to us at your earliest convenience.Very truly yours,[Accounting Firm]

October 26th, 2015Mr. Miguel Rodriguez, Controller Reforma 140, Casco Urbano, San Pedro Garza García, N.L.Dear Mr. Rivera:We are pleased to confirm the terms and objectives of our engagement with Refaccionaria RIVERA S.A de C.V. for July, 2013 and to clarify the extent and limitations of the services we will provide.We will audit the balance sheet of Refaccionaria RIVERA S.A de C.V. as of July 30th, 2013 and the related statements of income, retained earnings, and cash flows for the year ended. The objective of our audit is the expression of an opinion on the financial statements. We will also issue a report on compliance with various debt covenants as required by your debt agreement with Western Financial Services. We will conduct our audit with generally accepted auditing standards. Those standards require that we obtain reasonable, rather than absolute, assurance about whether the financial statements are free of material misstatement, whether cause by error or fraud. Accordingly, an audit cannot be relied upon to identify all material, errors, fraud, or illegal acts that may exist. Also an audit is not designed to detect error or fraud that is immaterial to the financial statements.Our audit will include test of the company records as we consider necessary. important among our audit planning procedures will be steps taken to understand your company's business and risks. Also, in order to comply with professional obligations to identify misrepresentations, we may include retrospective, surprise, and nonstandard procedures in our audit plan. If, for any reason, we are unable to complete the audit, we may decline to express an opinion or issue a report as a result of the engagement.While an audit including obtain an understanding of internal control sufficient to plan the audit and to determine the nature, timing, and extent of audit procedures to be performed, it is not performed to provide assurance on internal control or to identify significant deficiencies. However, we will communicate any significant deficiencies of which we become aware and make any other communications required by generally accepted auditing standards.The financial statements are the responsibility of the Blue Velvet Company’s Management.. Management is also responsible (1) establishing and maintain effective internal control over financial reporting, (2) establishing systems and procedures for the prevention and detention of fraud, (3) identifying and assuring that the Company complies with the laws and regulations applicable to its activities, (4) making all financial records and related information available to us, and (5) at the conclusion of the engagement, proving us with a letter that confirms certain representations made during the audit, including that the effects of any uncorrected misstatements that we bring to your attention are immaterial to the financial statements taken as a whole.Our audit is scheduled for performance and completion as follows:Begin fieldwork Completion of fieldwork Delivery of audit reportOur fees for this audit will be base on the time spent by various members of our staffs at our regular rates, plus direct expenses. We will notify you immediately of any circumstances we encounter that could significantly affect our initial fee estimate of $120,000.In order for us to work ad efficiently as possible, it is understood that your account staff will provide us with a year-end trial balance by January 15, 2014, and also with the schedules and account analyses described on the separate attachment. If these arrangements are in accordance with your understanding, please sign this letter in the space provided and return a copy to us at your earliest convenience. If these arrangements are in accordance with your understanding, please sign this letter in the space provided and return a copy to us at your earliest convenience.Very truly yours,[Accounting Firm]

Return to Plan audit index

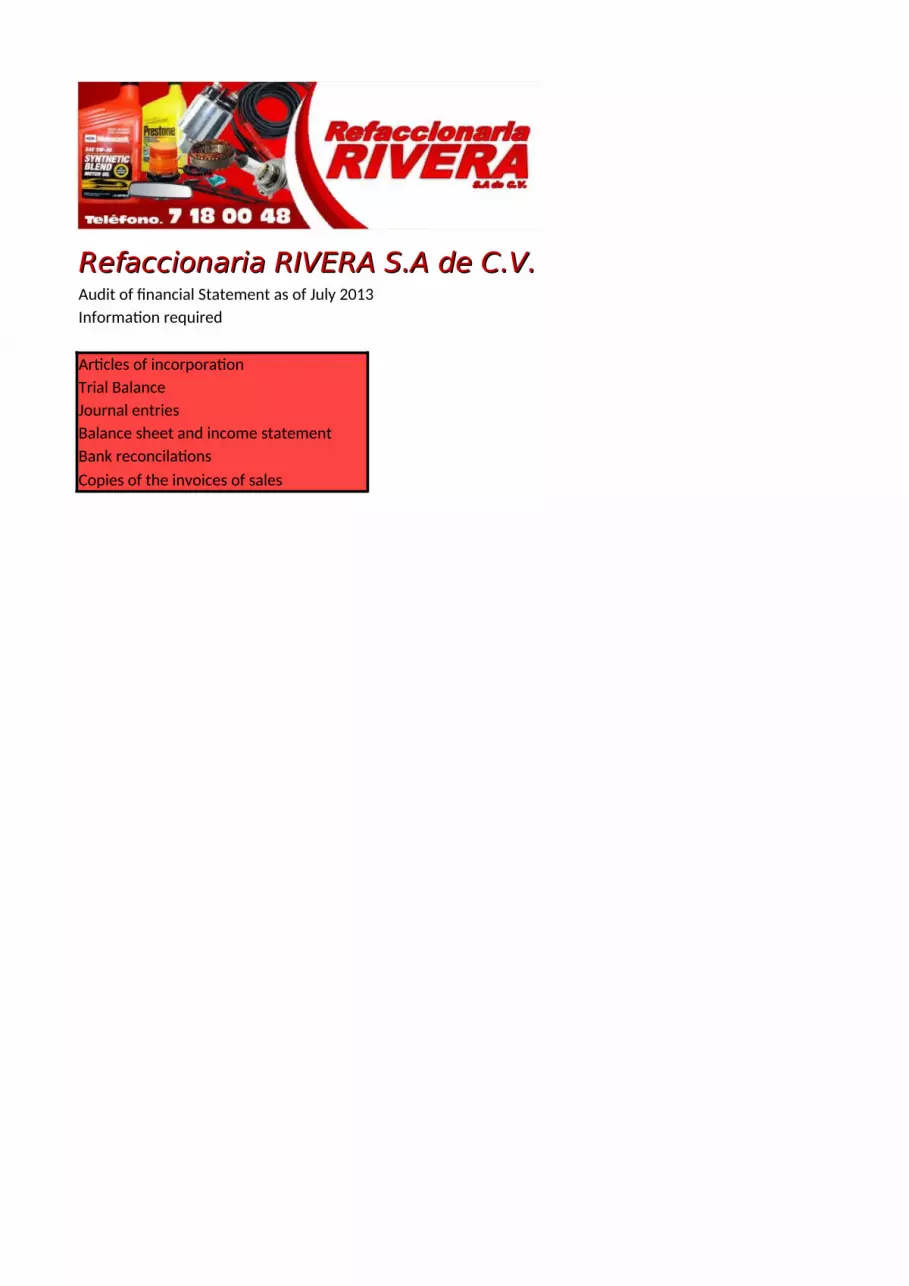

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of financial Statement as of July 2013Information required

Articles of incorporation Trial Balance Journal entriesBalance sheet and income statement Bank reconcilationsCopies of the invoices of sales

Return to Plan audit index

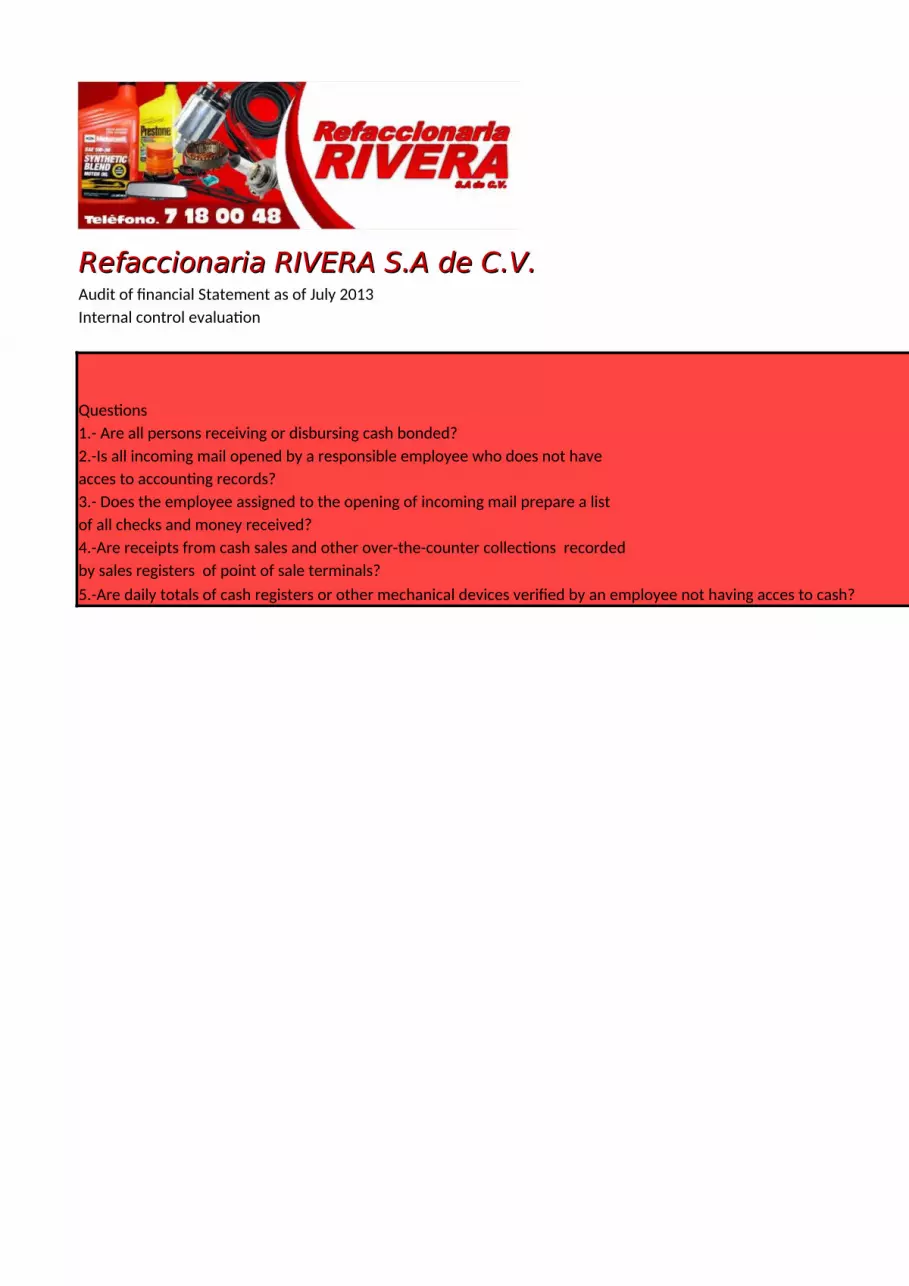

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of financial Statement as of July 2013Internal control evaluation

Questions1.- Are all persons receiving or disbursing cash bonded?2.-Is all incoming mail opened by a responsible employee who does not haveacces to accounting records?3.- Does the employee assigned to the opening of incoming mail prepare a list of all checks and money received?4.-Are receipts from cash sales and other over-the-counter collections recordedby sales registers of point of sale terminals?5.-Are daily totals of cash registers or other mechanical devices verified by an employee not having acces to cash?

AnswersWeakness

No Appl. Yes No Major Minor Remarksx

xx

xx

xx

X

Return to Plan audit index

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of financial Statement as of July 2013Scope of the work

To the users of this audit practice:The purpose of this practice is to understand and provide an introduction to the financial statement audit to develop the elements of competency required to plan an audit applied tests identify risks of fraud and the design of controls to mitigate and detect failures in controls. The student must be able to use the technical language required to prepare the audit plan.

The basis of the practice were the same numbers used in semester I and II, (accounting class), the teacher insert the beginning balances hipothetically just to understand the preparation of the financial statements and how the process of the accounting works, since the class are not accountants they are focus of business process.

All the transactions and the company for this case are not real, is just for the purpose of the practice of this semester.

Return to Plan audit index

To the users of this audit practice:The purpose of this practice is to understand and provide an introduction to the financial statement audit to develop the elements of competency required to plan an audit applied tests identify risks of fraud and the design of controls to mitigate and detect failures in controls. The student must be able to use the technical language required to prepare the audit plan.

The basis of the practice were the same numbers used in semester I and II, (accounting class), the teacher insert the beginning balances hipothetically just to understand the preparation of the financial statements and how the process of the accounting works, since the class are not accountants they are focus of business process.

All the transactions and the company for this case are not real, is just for the purpose of the practice of this semester.

Refaccionaria RIVERA S.A de C.V.Refaccionaria RIVERA S.A de C.V.Audit of financial Statement as of June 2012Audit Report

To the memebers of Refaccionaria RIVERA S.A de C.V.

We have audtited the acompanying balance sheet of Refaccionaria RIVERA S.A de C.V. as of July 30th 2013, and the related statements of operation, stock holders equity and cash flows for each of the months of the year 2013. These financial statements are the responsabilities of the companies managements. Our responsabilities is to express an opinion on these financial statements based on our audits.We conduct our audits in accordance with generally accepted auditing standards (Mexico). Those standards requeried that we plan and perform the audit to obtaind resonable assurance about whether the financial statements are free of material misstatement. An audit includes, examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includesassessing the accounting principles used as significant estimates made by management, as well evalueting the overall financial statement evaluation presentation. We believe that our audits provides a reasonable basis for our opinion.In our opinion the financial statements referred to above present fairly, in all material respects, the finacial position of the comany as of December of 2013, and the resoult of its operations and its cash flows for the period endend in July 30th 2013, in conformity with generallyn accepeted acconting principles (Mexico).

Abdón Rivera GonzálezOctober 26th 2014.

Return to Plan audit index

To the memebers of Refaccionaria RIVERA S.A de C.V.

We have audtited the acompanying balance sheet of Refaccionaria RIVERA S.A de C.V. as of July 30th 2013, and the related statements of operation, stock holders equity and cash flows for each of the months of the year 2013. These financial statements are the responsabilities of the companies managements. Our responsabilities is to express an opinion on these financial statements based on our audits.We conduct our audits in accordance with generally accepted auditing standards (Mexico). Those standards requeried that we plan and perform the audit to obtaind resonable assurance about whether the financial statements are free of material misstatement. An audit includes, examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includesassessing the accounting principles used as significant estimates made by management, as well evalueting the overall financial statement evaluation presentation. We believe that our audits provides a reasonable basis for our opinion.In our opinion the financial statements referred to above present fairly, in all material respects, the finacial position of the comany as of December of 2013, and the resoult of its operations and its cash flows for the period endend in July 30th 2013, in conformity with generallyn accepeted acconting principles (Mexico).

Abdón Rivera GonzálezOctober 26th 2014.