Embed Size (px)

Citation preview

Advances In Management Vol. 5 (10) Oct. (2012)

(59)

Case Study:

A Study of Capital Structure of a Firm Trivedi Savita

Dayananda Sagar College of Engineering, Kumara Swamy Layout, Bangalore – 560078, INDIA

Abstract

The strength of a company’s balance sheet can be

evaluated by three broad categories of investment-

quality measurements; working capital adequacy, asset

performance and capital structure. The capital

structure is how a firm finances its overall operations

and growth by using different sources of fund. For stock

investors a strong balance sheet is an important

consideration for investing in a company’s stock. The

study tells about the capital structure of a firm. The

term capital structure refers to the relationship between

the various long terms sources financing such as equity

capital, preference capital and debt capital. During the

study theoretical approach (Net income approach and

net operating approach) is used to find out firms value.

Keywords: Capital structure, policies, theories, approaches,

ratio analysis, findings and suggestions.

Introduction

Capital structure: Investopedia explains that a company’s

proportion of short and long-term debt is considered when

analyzing capital structure. When people refer to capital

structure, they are most likely referring to a firm’s debt-to

equity ratio which provides insight into how risky a company

is. The capital structure is how a firm finances its overall

operations and growth by using different sources of fund.

Capital structure is referred to as the ratio of different kinds

of securities raised by a firm as long-term finance. Debt

comes in the form of bond issues or long-term notes payable,

while equity is classified as common stock, preferred stock or

retained earnings. Short-term debt such as working capital

requirements is also considered to be part of the capital

structure.

In company’s capital structure, equity consists of a

company’s common and preferred stock plus retained

earnings which are summed up in the shareholders’ equity

account on a balance sheet. This invested capital and debt,

comprises a companies’ capitalization. A newly formed

company may adopt any of the capital structures like Simple,

Compound or Complex Capital Structure.

There are four basic components of capital structure viz.

equity share capital, preference share capital, retained

earnings and long term borrowings. “All the items on the left

hand side of the firm’s balance sheet excluding the current

liabilities are sources of capital”. The long-term funds can

broadly be divided into two categories viz. owner’s capital

and borrowed capital.

Capital Structure Policy: Capital structure policy involves a

trade-off between risk and return. Using more debt raises the

riskiness of the firm’s earnings, but a higher proportion of

debt generally leads to a higher expected rate of return.

Therefore, the optimal capital structure is the one that strikes

a balance between risk and return to achieve our ultimate goal

of maximizing the price of the stock. Firms which have

articulated their capital structure policy seem to follow one of

the following five policies:

1. Policy A: No debt should be used in any circumstances.

2. Policy B: Debt should be employed to a very limited

extent.

3. Policy C: The ratio of debt to equity should be

maintained around 1:1.

4. Policy D: The ratio of debt to equity should be kept

within 2:1.

5. Policy E: Debt should be trapped to the extent it is

available.

Capital Structure Theories

Capital Structure is the major part of the firm’s financial

decision which affects the value of the firm and it leads to

change EBIT and market value of the shares. There is a

relationship among the capital structure, cost of the firm. The

aim of effective capital structure is to maximize the value of

the firm and to reduce the cost of capital.

Modern Approach: Following approaches are included:

1. Net Income Approach

2. Net Operating Approach

3. Modigliani Approach

Net Income Approach: According to this approach capital

structure decision is relevant to the valuation of the firm. In

other words a change in the capital structure causes a

corresponding change in the overall cost of capital as well as

the total value of the firm. This approach states that the

higher debt content in the capital structure will result in

Advances In Management Vol. 5 (10) Oct. (2012)

(60)

decline in the overall or weighted average cost of capital.

This will cause increase in the value of the firm and

consequently increase in the value of equity shares of the

company. Reverse will happen in a converse situation.

Assumptions: Net Income Approach is based on the

following three assumptions:

1. There are no corporate taxes.

2. The cost of debt is less than cost of equity capitalization

rate.

3. The debt content does not change the risk perception of

the investors.

The value of the firm on the basis of NI Approach can be

ascertained as follows:

V=S+B

where V= Value of firm; S=Market Value of Equity,

B= Market Value of Debt.

Market value of equity can be ascertained as follows:

s=NI/Ke

where S= Market Value of Equity, I= Earnings available for

equity shareholders and Ke= Equity Capitalization Rate.

1. Net Operating Income: This is just opposite of Net

Income approach. According to this approach, the market

value of the firm is not at all affected by the capital

structure changes. The market value of the firm is

ascertained by capitalizing the net operating income at

the overall cost of capital (k) which is considered to be

constant. The market value of equity is ascertained by

deducting the market value of the debt from the market

value of the firm.

2. Assumptions: The Net Operating Income (NOI)

approach is based on the following assumptions:

i. The overall cost of capital (k) remains constant for

all degrees of debt-equity mix or leverages.

ii. The market capitalizes the value of the firm as a

whole and, therefore the split between debt and

equity is not relevant.

iii. The use of debt having low cost increases the risk of

equity shareholders, this result in increase in equity

capitalization rate. Thus, the advantage of debt is set

off exactly capitalization rate.

iv. There are no corporate taxes

Value of the Firm: According the NOI Approach, the value

of the firm can determined by the following equations:

V=EBIT/K

where V = Value of firm, K = Overall cost of capital and

EBIT= Earnings before interest and tax.

Value of Equity: The value of equity (S) is a residual value

which is determined by deducting the total value of debt (B)

from the total value of the firm (V). Thus, the value of equity

(S) can be determined by the following equation:

S= V-B

where S= Value of Equity, V= Value of Firm, B= Value of

Debt

Equity capitalization rate = Ke= EBIT-1 / V-B

Traditional Approach

According to this theory, the value of the firm can be

increased initially or the cost of capital can be decreased by

using more debt as the debt is cheaper source of funds than

equity. Thus optimal capital structure can be reached by a

proper debt-equity mix. Beyond a particular point, the cost of

equity increases because increased debt increases the

financial risk of the equity shareholders.

Methodology

The primary data are collected by conducting discussions

with concerned officers and staff either individually or

collectively. Some of the information had been verified or

supplemented with personal observations. The secondary data

were collected from already published sources such as annual

reports and internal records. The data includes: Collection of

required data from annual reports of the firm (name of the

firm not disclosed) 2005-2009, reference from text books and

relating to financial management and also from the firm’s

website.

Value of the firm can be determined in using several

techniques. These include DCF, CAPM, Relative valuation

and theoretical method. We only use the theoretical methods.

Cost of equity was calculated with CAPM and assumed to be

constant for all the years. The value of the firm should not be

negative; as per our study gave a negative value of the firm.

In net income approach, we calculated firm’s value through

market value of debt and equity .But in net operating income

we calculated firm’s value through overall cost of capital.

Literature review

Myers, Stewart C.12

in his article “The Capital Structure

Puzzle” gave the information on the capital structure of the

firms and how they choose the debt, equity hybrid securities

issued by them. The author wrote “This paper's title is

intended to remind you of Fischer Black's well-known note

on "The Dividend Puzzle," which he closed by saying, "What

should the corporation do about dividend policy? We do not

Advances In Management Vol. 5 (10) Oct. (2012)

(61)

know." I will start by asking, "How do firms choose their

capital structures?" Again, the answer is, “We do not know."

Further he wrote, “By contrast, we know very little about

capital structure. We do not know how firms choose the debt,

equity or hybrid securities they issue. We have only recently

discovered that capital structure changes convey information

to investors.

Wippern, Ronald F.11

examined the optimal capital structure

and the value of the firm and stated the expected earnings

stream from the assets and the rate that the stream is

capitalizes. Boness A. James et al10

have examined the

relationship between stock price behaviour and changes in the

capital structure of a firm.

Schwartz9 discussed a self-

contained theory of the capital structure of the individual

firm. The author suggests that there is a single optimum

capital structure for any firm. Hackbarth8 in his article

“Managerial Traits and capital structure decisions” examined

the well-documented managerial traits into a tradeoff model

of capital structure to study their impact on corporate

financial policy and firm value. Sagnar et al5 wrote that

Managing working capital involves organizing your

company's short-term resources to sustain ongoing activities,

mobilize funds and optimize liquidity. Banos et al6 in their

research examined that how the determinants of cash

conversion cycle (CCC) plays a important role on utilization

of working capital. Bauer7 believes that organizations can

leverage innovative methods to utilize working capital while

balancing the needs of suppliers, procurement, finance, AP

and treasury.

Analysis of Financial Statement

Years Net Profit Net Sales

2005 46.11 318.12

2006 36.18 455.09

2007 -115.21 412.87

2008 6.13 593.14

2009 105.51 768.35

Ratio Analysis

1. Current Ratio: It represents the ratio of current assets to

current liabilities. It is also called working capital ratio. It

is calculated by dividing current assets by current

liabilities.

Current Ratio = Current Assets

Current Liabilities

2. Debt-equity Ratio: This ratio indicates the relative

proportion of debt and equity in financing the assets of a

firm. This ratio is computed by dividing the total debt of

the firm by its net worth.

Debt-equity Ratio = Debt

Equity

3. Gross Profit Ratio:-This ratio expresses the relationship

between gross profit and sales. This ratio is calculated by

dividing gross profit by net sales.

Gross Profit Ratio = Gross profit x 100

Net sales

4. Net profit ratio:It is determined by dividing the net

income after tax to the net sales for the period and

measure the profit per rupee of sales.

Net Profit Ratio = Net profit x100

Sales

5. Proprietary RatioThis ratio shows the long term

solvency of the business. It is calculated by dividing

shareholders’ funds by the total assets.

Proprietary ratio = Shareholders fund

Total assets

6. Return on Total Resources: This ratio is also known as

return on gross capital employed. It is measured the

profitability of investment.

Return on Total Resources =

Net profit x 100

Total assets

Particulars 05 06 07 08 09

Current Ratio 2.97 2 1.94 1.87 1.76

Liquid Ratio 2.53 1.68 1.68 1.55 1.52

Debt-equity Ratio 0.94 0.92 4.35 2.9 1.33

Gross Profit Ratio 19.22 12.78 -24.01 3.93 18.13

Net Profit Ratio 14.49 7.95 -27.9 1.03 13.73

Return on Total Resources 7.03 5.21 -8.81 0.42 4.89

Proprietary Ratio 0.51 0.52 0.19 0.26 0.43

Capital Structure Analysis (Net Income

Method)

COST OF EQUITY CPITALIZATION: It is calculated

with the help of CAPM (Capital Asset Pricing Model). Under

CAPM model, we have to find out how much is the risk free

return, beta of securities and expected return on market

portfolio. To calculate equity capitalization, we have to apply

the given formula:

Advances In Management Vol. 5 (10) Oct. (2012)

(62)

Ke = Rf + beta (Rm-Rf)

where Ke = Equity Capitalization, Rf = Risk Free Return,

Beta = Beta of Security, Rm = Expected Return on Market

Portfolio.

Market Return

Years Closing Price Percentage Change

2000 1263.55

2001 1059.05 -16%

2002 1093.5 3%

2003 1879.75 72%

2004 2080.5 11%

2005 2836.55 36%

2006 3966.4 40%

2007 6138.6 55%

2008 2959.15 -52%

2009 5201.05 76%

2010 6134.5 18%

Average = 24%

Equity Capitalization

Risk

Free Beta

Market

Return

Risk

free

Equity

Capitalization

8.22 0.88 24 8.22 22.1064

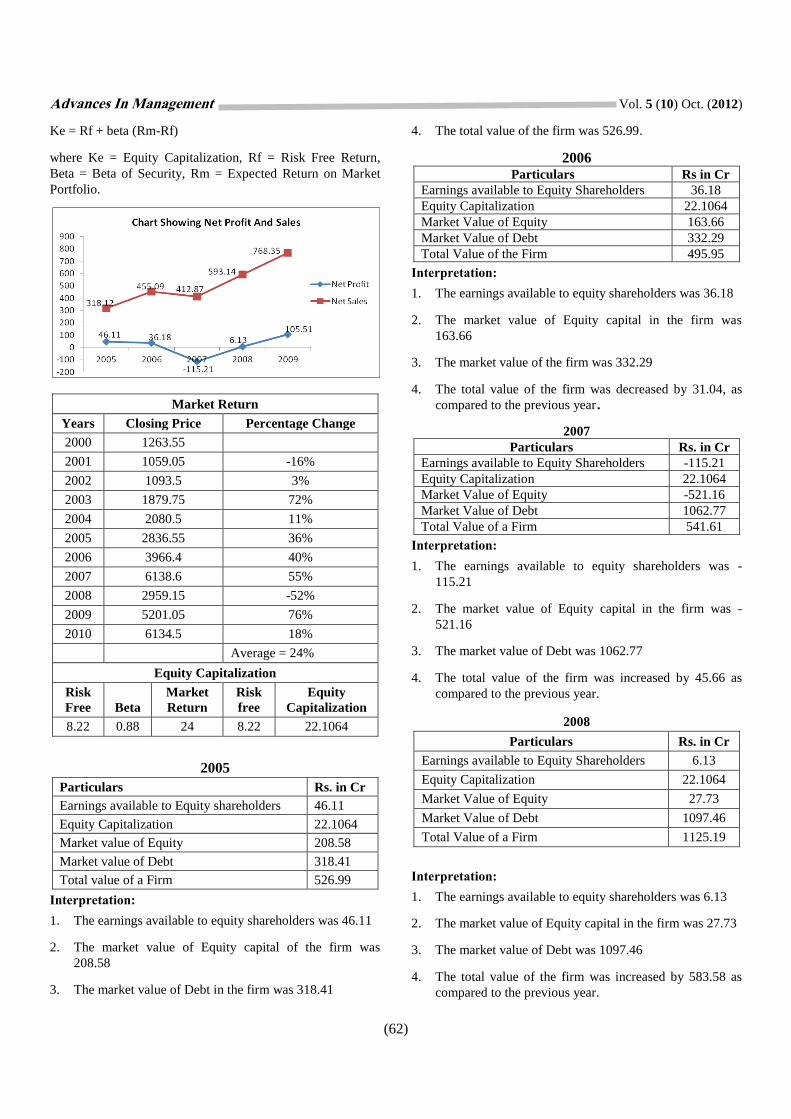

2005

Particulars Rs. in Cr

Earnings available to Equity shareholders 46.11

Equity Capitalization 22.1064

Market value of Equity 208.58

Market value of Debt 318.41

Total value of a Firm 526.99

Interpretation:

1. The earnings available to equity shareholders was 46.11

2. The market value of Equity capital of the firm was

208.58

3. The market value of Debt in the firm was 318.41

4. The total value of the firm was 526.99.

2006 Particulars Rs in Cr

Earnings available to Equity Shareholders 36.18

Equity Capitalization 22.1064

Market Value of Equity 163.66

Market Value of Debt 332.29

Total Value of the Firm 495.95

Interpretation:

1. The earnings available to equity shareholders was 36.18

2. The market value of Equity capital in the firm was

163.66

3. The market value of the firm was 332.29

4. The total value of the firm was decreased by 31.04, as

compared to the previous year.

2007

Particulars Rs. in Cr

Earnings available to Equity Shareholders -115.21

Equity Capitalization 22.1064

Market Value of Equity -521.16

Market Value of Debt 1062.77

Total Value of a Firm 541.61

Interpretation:

1. The earnings available to equity shareholders was -

115.21

2. The market value of Equity capital in the firm was -

521.16

3. The market value of Debt was 1062.77

4. The total value of the firm was increased by 45.66 as

compared to the previous year.

2008

Particulars Rs. in Cr

Earnings available to Equity Shareholders 6.13

Equity Capitalization 22.1064

Market Value of Equity 27.73

Market Value of Debt 1097.46

Total Value of a Firm 1125.19

Interpretation:

1. The earnings available to equity shareholders was 6.13

2. The market value of Equity capital in the firm was 27.73

3. The market value of Debt was 1097.46

4. The total value of the firm was increased by 583.58 as

compared to the previous year.

Advances In Management Vol. 5 (10) Oct. (2012)

(63)

2009

Particulars Rs. in Cr

Earnings available to Equity Shareholders 105.51

Equity Capitalization 22.1

Market Value of Equity 477.28

Market Value of Debt 1232.24

Total Value of a Firm 1709.52

Interpretation:

1. The earnings available to equity shareholders was 105.51

2. The market value of Equity capital in the firm was

477.28

3. The market value of Debt was 1232.24

4. The total value of the firm was increased by 584.33, as

compared to the previous year.

Market Value of Equity

Years Value

2005 208.58

2006 163.66

2007 -521.16

2008 27.73

2009 477.28

Market Value of Debt

Years Value

2005 318.41

2006 332.29

2007 1062.77

2008 1097.46

2009 1232.24

Total Value of a firm

Years Value

2005 526.99

2006 495.95

2007 541.61

2008 1125.19

2009 1709.52

Comparison with Share Price and Firm Value

Years Price/Share Firm Value

2005 308.85 526.99

2006 369.05 495.95

2007 283.5 541.61

2008 89.35 1125.19

2009 239.1 1709.52

CAPITAL STRUCTURE ANALYSIS (Net

Operating Income Method)

2005

Particulars Rs. in Cr

EBIT 46.11

Cost of Equity 22.11

Cost of Debt 8.6

Fraction of Debt 0.49

Fraction of Equity 0.51

Overall Cost of Capital 15.55

Total Value of a Firm 2.96

Advances In Management Vol. 5 (10) Oct. (2012)

(64)

Interpretation:

1. The EBIT of the firm is 46.11

2. The cost of equity is 22.11

3. The cost of debt is 8.6

4. The fraction of debt is 0.49

5. The fraction of equity is 0.51

6. The overall cost of capital is 15.55

7. The value of a firm was 2.96

2006

Particulars Rs. in Cr

EBIT 36.18

Cost of Equity 22.11

Cost of Debt 8.6

Fraction of Debt 0.48

Fraction of Equity 0.52

Overall Cost of Capital 15.64

Total Value of a Firm 2.32

Interpretation:

1. The EBIT of the firm is decreased by 9.93

2. The cost of equity is 22.11

3. The cost of debt is 8.6

4. The fraction of debt is decreased by 0.01

5. The fraction of equity is increased by 0.01

6. The overall cost of capital is increased by 0.09

7. The value of a firm was 2.32

2007

Particulars Rs. in Cr

EBIT -115.21

Cost of Equity 22.11

Cost of Debt 8.6

Fraction of Debt 0.81

Fraction of Equity 0.19

Overall Cost of Capital 11.12

Total Value of a Firm -10.35

Interpretation:

1. The EBIT of the firm is -115.21

2. The cost of equity is 22.11

3. The cost of debt is 8.6

4. The fraction of debt is increased by 0.33

5. The fraction of equity is decreased by 0.33

6. The overall cost of capital is decreased by 4.52

7. The value of a firm was -10.35

2008

Particulars Rs. in Cr

EBIT 6.13

Cost of Equity 22.11

Cost of Debt 8.6

Fraction of Debt 0.74

Fraction of Equity 0.26

Overall Cost of Capital 12.06

Total Value of a Firm 0.51

Interpretation:

1. The EBIT of the firm is 6.13

2. The cost of equity is 22.11

3. The cost of debt is 8.6

4. The fraction of debt is decreased by 0.07

5. The fraction of equity is increased by 0.07

6. The overall cost of capital is increased by 0.94

7. The value of a firm was 0.51.

2009

Particulars Rs. in Cr

EBIT 105.51

Cost of Equity 22.11

Cost of Debt 8.6

Fraction of Debt 1.57

Fraction of Equity 0.43

Overall Cost of Capital 14.39

Total Value of a Firm 7.33

Interpretation:

1. The EBIT of the firm is increased by 99.38

2. The cost of equity in the firm is 22.11

3. The cost of debt is 8.6

4. The fraction of debt is increased by 0.83

5. The fraction of equity is increased by 0.17

6. The overall cost of capital is increased by 2.33

7. The value of a firm was 7.33.

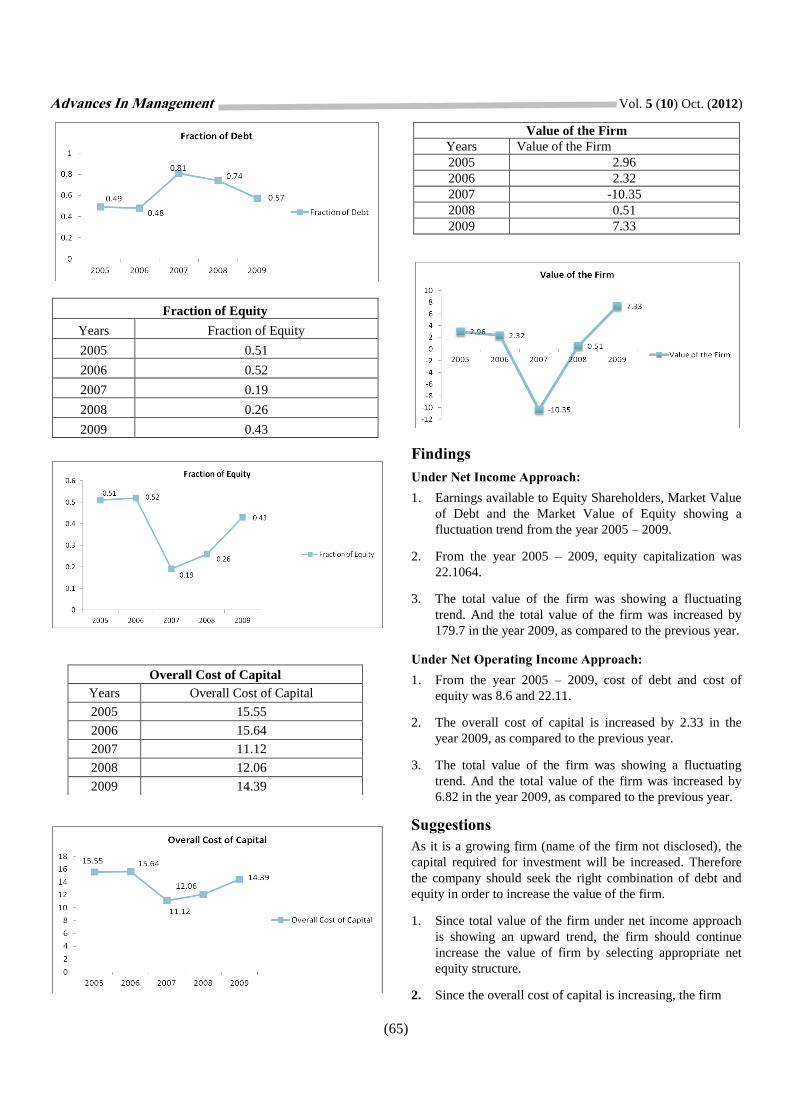

Fraction of Debt

Years Fraction of Debt

2005 0.49

2006 0.48

2007 0.81

2008 0.74

2009 0.57

Advances In Management Vol. 5 (10) Oct. (2012)

(65)

Fraction of Equity

Years Fraction of Equity

2005 0.51

2006 0.52

2007 0.19

2008 0.26

2009 0.43

Value of the Firm

Years Value of the Firm

2005 2.96

2006 2.32

2007 -10.35

2008 0.51

2009 7.33

Findings

Under Net Income Approach:

1. Earnings available to Equity Shareholders, Market Value

of Debt and the Market Value of Equity showing a

fluctuation trend from the year 2005 – 2009.

2. From the year 2005 – 2009, equity capitalization was

22.1064.

3. The total value of the firm was showing a fluctuating

trend. And the total value of the firm was increased by

179.7 in the year 2009, as compared to the previous year.

Under Net Operating Income Approach:

1. From the year 2005 – 2009, cost of debt and cost of

equity was 8.6 and 22.11.

2. The overall cost of capital is increased by 2.33 in the

year 2009, as compared to the previous year.

3. The total value of the firm was showing a fluctuating

trend. And the total value of the firm was increased by

6.82 in the year 2009, as compared to the previous year.

Suggestions

As it is a growing firm (name of the firm not disclosed), the

capital required for investment will be increased. Therefore

the company should seek the right combination of debt and

equity in order to increase the value of the firm.

1. Since total value of the firm under net income approach

is showing an upward trend, the firm should continue

increase the value of firm by selecting appropriate net

equity structure.

2. Since the overall cost of capital is increasing, the firm

Overall Cost of Capital

Years Overall Cost of Capital

2005 15.55

2006 15.64

2007 11.12

2008 12.06

2009 14.39

Advances In Management Vol. 5 (10) Oct. (2012)

(66)

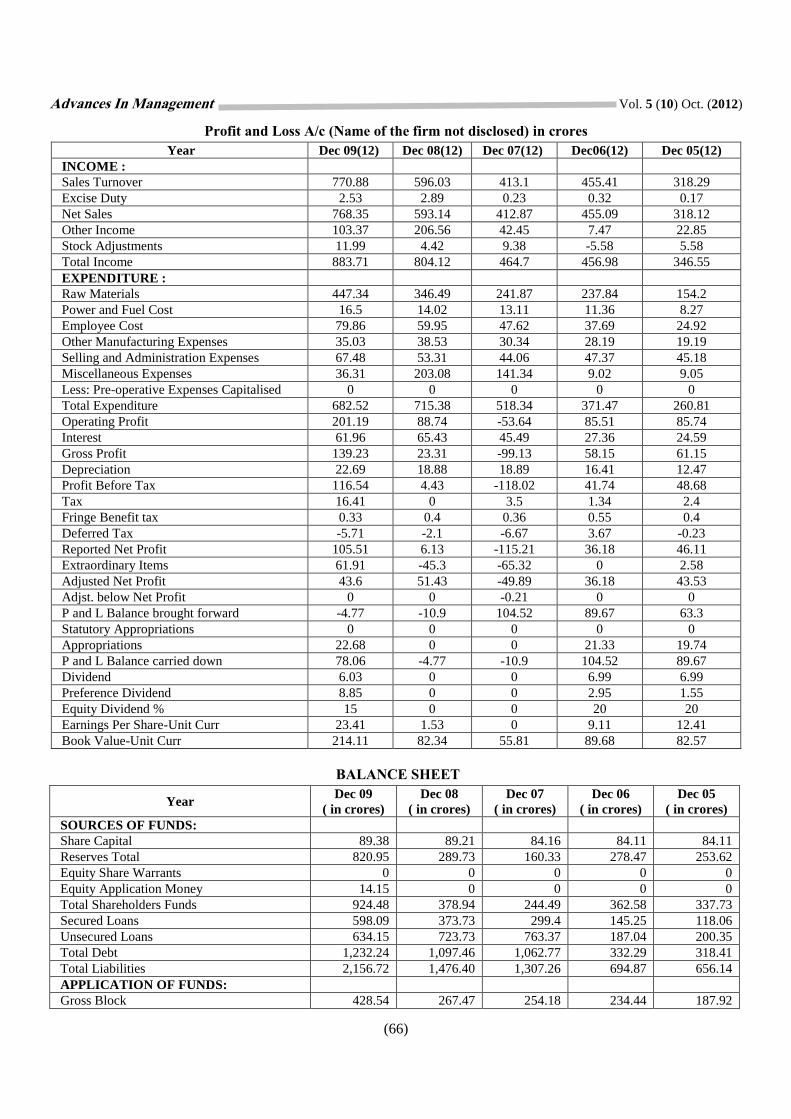

Profit and Loss A/c (Name of the firm not disclosed) in crores

Year Dec 09(12) Dec 08(12) Dec 07(12) Dec06(12) Dec 05(12)

INCOME :

Sales Turnover 770.88 596.03 413.1 455.41 318.29

Excise Duty 2.53 2.89 0.23 0.32 0.17

Net Sales 768.35 593.14 412.87 455.09 318.12

Other Income 103.37 206.56 42.45 7.47 22.85

Stock Adjustments 11.99 4.42 9.38 -5.58 5.58

Total Income 883.71 804.12 464.7 456.98 346.55

EXPENDITURE :

Raw Materials 447.34 346.49 241.87 237.84 154.2

Power and Fuel Cost 16.5 14.02 13.11 11.36 8.27

Employee Cost 79.86 59.95 47.62 37.69 24.92

Other Manufacturing Expenses 35.03 38.53 30.34 28.19 19.19

Selling and Administration Expenses 67.48 53.31 44.06 47.37 45.18

Miscellaneous Expenses 36.31 203.08 141.34 9.02 9.05

Less: Pre-operative Expenses Capitalised 0 0 0 0 0

Total Expenditure 682.52 715.38 518.34 371.47 260.81

Operating Profit 201.19 88.74 -53.64 85.51 85.74

Interest 61.96 65.43 45.49 27.36 24.59

Gross Profit 139.23 23.31 -99.13 58.15 61.15

Depreciation 22.69 18.88 18.89 16.41 12.47

Profit Before Tax 116.54 4.43 -118.02 41.74 48.68

Tax 16.41 0 3.5 1.34 2.4

Fringe Benefit tax 0.33 0.4 0.36 0.55 0.4

Deferred Tax -5.71 -2.1 -6.67 3.67 -0.23

Reported Net Profit 105.51 6.13 -115.21 36.18 46.11

Extraordinary Items 61.91 -45.3 -65.32 0 2.58

Adjusted Net Profit 43.6 51.43 -49.89 36.18 43.53

Adjst. below Net Profit 0 0 -0.21 0 0

P and L Balance brought forward -4.77 -10.9 104.52 89.67 63.3

Statutory Appropriations 0 0 0 0 0

Appropriations 22.68 0 0 21.33 19.74

P and L Balance carried down 78.06 -4.77 -10.9 104.52 89.67

Dividend 6.03 0 0 6.99 6.99

Preference Dividend 8.85 0 0 2.95 1.55

Equity Dividend % 15 0 0 20 20

Earnings Per Share-Unit Curr 23.41 1.53 0 9.11 12.41

Book Value-Unit Curr 214.11 82.34 55.81 89.68 82.57

BALANCE SHEET

Year Dec 09

( in crores)

Dec 08

( in crores)

Dec 07

( in crores)

Dec 06

( in crores)

Dec 05

( in crores)

SOURCES OF FUNDS:

Share Capital 89.38 89.21 84.16 84.11 84.11

Reserves Total 820.95 289.73 160.33 278.47 253.62

Equity Share Warrants 0 0 0 0 0

Equity Application Money 14.15 0 0 0 0

Total Shareholders Funds 924.48 378.94 244.49 362.58 337.73

Secured Loans 598.09 373.73 299.4 145.25 118.06

Unsecured Loans 634.15 723.73 763.37 187.04 200.35

Total Debt 1,232.24 1,097.46 1,062.77 332.29 318.41

Total Liabilities 2,156.72 1,476.40 1,307.26 694.87 656.14

APPLICATION OF FUNDS:

Gross Block 428.54 267.47 254.18 234.44 187.92

Advances In Management Vol. 5 (10) Oct. (2012)

(67)

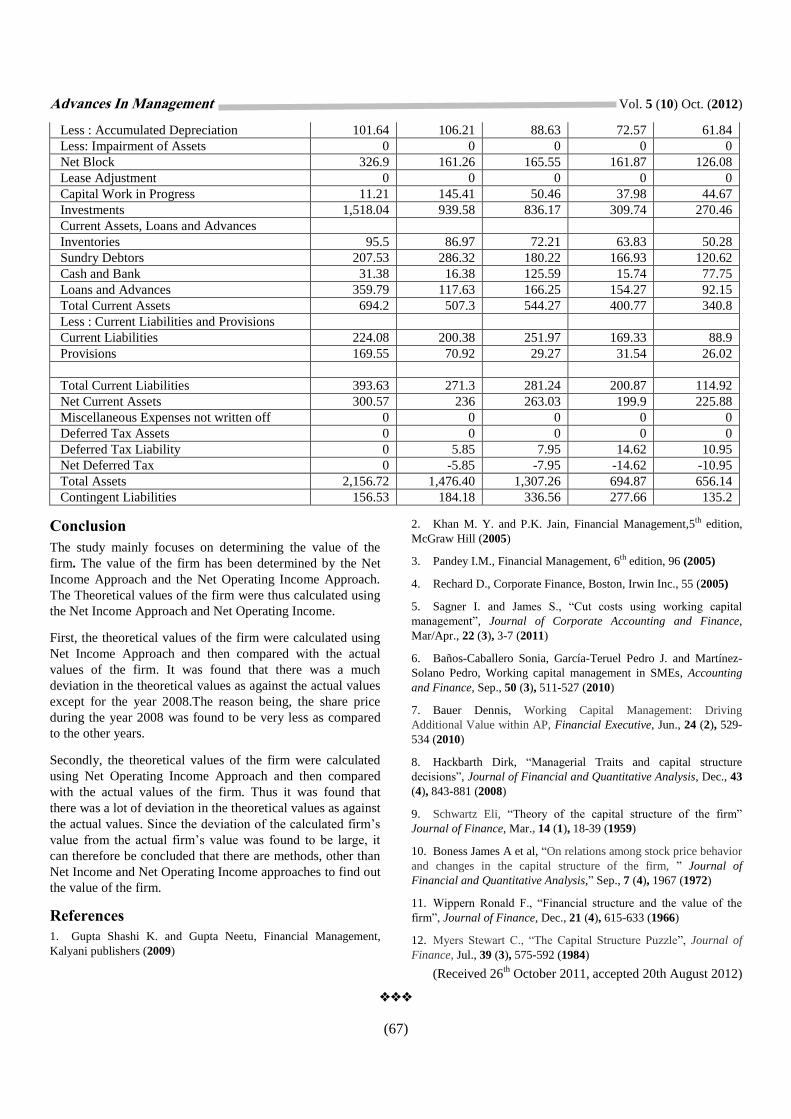

Less : Accumulated Depreciation 101.64 106.21 88.63 72.57 61.84

Less: Impairment of Assets 0 0 0 0 0

Net Block 326.9 161.26 165.55 161.87 126.08

Lease Adjustment 0 0 0 0 0

Capital Work in Progress 11.21 145.41 50.46 37.98 44.67

Investments 1,518.04 939.58 836.17 309.74 270.46

Current Assets, Loans and Advances

Inventories 95.5 86.97 72.21 63.83 50.28

Sundry Debtors 207.53 286.32 180.22 166.93 120.62

Cash and Bank 31.38 16.38 125.59 15.74 77.75

Loans and Advances 359.79 117.63 166.25 154.27 92.15

Total Current Assets 694.2 507.3 544.27 400.77 340.8

Less : Current Liabilities and Provisions

Current Liabilities 224.08 200.38 251.97 169.33 88.9

Provisions 169.55 70.92 29.27 31.54 26.02

Total Current Liabilities 393.63 271.3 281.24 200.87 114.92

Net Current Assets 300.57 236 263.03 199.9 225.88

Miscellaneous Expenses not written off 0 0 0 0 0

Deferred Tax Assets 0 0 0 0 0

Deferred Tax Liability 0 5.85 7.95 14.62 10.95

Net Deferred Tax 0 -5.85 -7.95 -14.62 -10.95

Total Assets 2,156.72 1,476.40 1,307.26 694.87 656.14

Contingent Liabilities 156.53 184.18 336.56 277.66 135.2

Conclusion

The study mainly focuses on determining the value of the

firm. The value of the firm has been determined by the Net

Income Approach and the Net Operating Income Approach.

The Theoretical values of the firm were thus calculated using

the Net Income Approach and Net Operating Income.

First, the theoretical values of the firm were calculated using

Net Income Approach and then compared with the actual

values of the firm. It was found that there was a much

deviation in the theoretical values as against the actual values

except for the year 2008.The reason being, the share price

during the year 2008 was found to be very less as compared

to the other years.

Secondly, the theoretical values of the firm were calculated

using Net Operating Income Approach and then compared

with the actual values of the firm. Thus it was found that

there was a lot of deviation in the theoretical values as against

the actual values. Since the deviation of the calculated firm’s

value from the actual firm’s value was found to be large, it

can therefore be concluded that there are methods, other than

Net Income and Net Operating Income approaches to find out

the value of the firm.

References

1. Gupta Shashi K. and Gupta Neetu, Financial Management,

Kalyani publishers (2009)

2. Khan M. Y. and P.K. Jain, Financial Management,5th edition,

McGraw Hill (2005)

3. Pandey I.M., Financial Management, 6th edition, 96 (2005)

4. Rechard D., Corporate Finance, Boston, Irwin Inc., 55 (2005)

5. Sagner I. and James S., “Cut costs using working capital

management”, Journal of Corporate Accounting and Finance,

Mar/Apr., 22 (3), 3-7 (2011)

6. Baños-Caballero Sonia, García-Teruel Pedro J. and Martínez-

Solano Pedro, Working capital management in SMEs, Accounting

and Finance, Sep., 50 (3), 511-527 (2010)

7. Bauer Dennis, Working Capital Management: Driving

Additional Value within AP, Financial Executive, Jun., 24 (2), 529-

534 (2010)

8. Hackbarth Dirk, “Managerial Traits and capital structure

decisions”, Journal of Financial and Quantitative Analysis, Dec., 43

(4), 843-881 (2008)

9. Schwartz Eli, “Theory of the capital structure of the firm”

Journal of Finance, Mar., 14 (1), 18-39 (1959)

10. Boness James A et al, “On relations among stock price behavior

and changes in the capital structure of the firm, ” Journal of

Financial and Quantitative Analysis,” Sep., 7 (4), 1967 (1972)

11. Wippern Ronald F., “Financial structure and the value of the

firm”, Journal of Finance, Dec., 21 (4), 615-633 (1966)

12. Myers Stewart C., “The Capital Structure Puzzle”, Journal of

Finance, Jul., 39 (3), 575-592 (1984)

(Received 26th

October 2011, accepted 20th August 2012)

Copyright of Advances in Management is the property of Advances in Management and its content may not be

copied or emailed to multiple sites or posted to a listserv without the copyright holder's express written

permission. However, users may print, download, or email articles for individual use.