Embed Size (px)

Citation preview

http://ccba.jsu.edu/accounting/INDEX.HTML

Introduction to Adjusting Entries

Adjusting entries are accounting journal entries that convert a company's accounting records to the accrual basis of accounting. An adjusting journal entry is typically made just prior to issuing a company's financial statements.To demonstrate the need for an accounting adjusting entry let's assume that a company borrowed money from its bank on December 1, 2013 and that the company's accounting period endson December 31. The bank loan specifies that the first interest payment on the loan will be due on March 1, 2014. This means that the company's accounting records as of December 31 do not contain any payment to the bank for the interest the company incurred from December 1 through December31. (Of course the loan is costing the company interest expense every day, but the actual payment for the interest will not occur until March 1.) For the company's December income statement to accurately report the company's profitability, it must include all of the company's December expenses—not just the expenses that were paid. Similarly, for the company's balance sheet on December 31 to be accurate, it must report a liability for the interest owed as of the balance sheet date. An adjusting entry is needed so that December's interest expense is included on December's income statement and the interest due as of December 31 is included on the December 31 balance sheet. The adjusting entry will debit Interest Expense and credit Interest Payable for the amount of interest from December 1 to December 31.Another situation requiring an adjusting journal entry arises when an amount has already been recorded in the company's accounting records, but the amount is for more than the current accounting period. To illustrate let's assume that on December 1, 2013 the company paid its insurance agent $2,400 for insurance protection during the period of December 1, 2013through May 31, 2014. The $2,400 transaction was recorded in the accounting records on December 1, but the amount represents six months of coverage and expense. By December 31,one month of the insurance coverage and cost have been used upor expired. Hence the income statement for December should report just one month of insurance cost of $400 ($2,400

divided by 6 months) in the account Insurance Expense. The balance sheet dated December 31 should report the cost of fivemonths of the insurance coverage that has not yet been used up. (The cost not used up is referred to as the asset Prepaid Insurance.The cost that is used up is referred to as the expired cost Insurance Expense.) This means that the balance sheet dated December 31 should report five months of insurancecost or $2,000 ($400 per month times 5 months) in the asset account Prepaid Insurance. Since it is unlikely that the $2,400 transaction on December 1 was recorded this way, an adjusting entry will be needed at December 31, 2013 to get theincome statement and balance sheet to report this accurately.The two examples of adjusting entries have focused on expenses, but adjusting entries also involve revenues.This will be discussed later when we prepare adjusting journal entries.For now we want to highlight some important points.

There are two scenarios where adjusting journal entries are needed before the financial statements are issued:

Nothing has been entered in the accounting records for certain expenses or revenues, but those expenses and/or revenues did occur and must be included in the current period's income statement and balance sheet.

Something has already been entered in the accounting records, but the amount needs to be divided up between two or more accounting periods.

Adjusting entries almost always involve a

balance sheet account (Interest Payable, Prepaid Insurance, Accounts Receivable, etc.) and an

income statement account (Interest Expense, Insurance Expense, Service Revenues, etc.)

accrual basis of accounting.

The accounting method under which revenues are recognized on the income statement when they are earned (rather than when the cash is received). The balance sheet is also affected at the time of the revenues by either an increase in Cash (if theservice or sale was for cash), an increase in Accounts

Receivable (if the service was performed on credit), or a decrease in Unearned Revenues (if the service was performed after the customer had paid in advance for the service).

Under the accrual basis of accounting, expenses are matched with revenues on the income statement when the expenses expireor title has transferred to the buyer, rather than at the timewhen expenses are paid. The balance sheet is also affected at the time of the expense by a decrease in Cash (if the expense was paid at the time the expense was incurred), an increase inAccounts Payable (if the expense will be paid in the future), or a decrease in Prepaid Expenses (if the expense was paid in advance).

Definition of 'Accrual Accounting'

An accounting method that measures the performance and position of a company by recognizing economic events regardless of when cash transactions occur. The generalidea is that economic events are recognized by matching revenues to expenses (the matching principle) at the time in which the transaction occurs rather than when payment is made (or received). This method allows the current cash inflows/outflowsto be combined with future expected cash inflows/outflows to give a more accurate picture of a company's current financial condition.

Financial statementsUsually financial statements refer to the balance sheet, income statement, and statementof cash flows, statement of retained earnings, and statement of stockholders' equity.

The balance sheet reports information as of a date (a point in time). The income statement, statement of cash flows, statement of retained earnings, and the statement ofstockholders' equity report information for a period of time (or time interval) such as a year, quarter, or month.

To learn more, see Explanation of Balance Sheet.

IncurredA word used by accountants to communicate that an expense has occurred and needs to be recognized on the income statement even though no payment was made. The second part of the necessary entry will be a credit to a liability account.

Income statementOne of the main financial statements (along with the balance sheet, the statement of cash flows, and the statement of stockholders' equity). The income statement is also

referred to as the profit and loss statement, P&L, statement of income, and the statement of operations. The income statement reports the revenues, gains, expenses, losses, net income and other totals for the period of time shown in the heading of the statement. If a company's stock is publicly traded, earnings per share must appear on the face of the income statement.

To learn more, see Explanation of Income Statement.

balance sheetOne of the main financial statements. The balance sheet reports the assets, liabilities,and owner's (stockholders') equity at a specific point in time, such as December 31. Thebalance sheet is also referred to as the Statement of Financial Position.

interest expenseThis account is a non-operating or "other" expense for the cost of borrowed money or other credit. The amount of interest expense appearing on the income statement is the cost of the money that was used during the time interval shown in the heading of the income statement, not the amount of interest paid during that period of time.

liabilitiesObligations of a company or organization. Amounts owed to lenders and suppliers. Liabilities often have the word "payable" in the account title. Liabilities also includeamounts received in advance for a future sale or for a future service to be performed. To learn more, see Explanation of Balance Sheet.

interest payableThis current liability account reports the amount of interest the company owes as of thedate of the balance sheet. (Future interest is not recorded as a liability.)

prepaid insuranceA current asset which indicates the cost of the insurance contract (premiums) that have been paid in advance. It represents the amount that has been paid but has not yet expired as of the balance sheet date.

A related account is Insurance Expense, which appears on the income statement. The amount in the Insurance Expense account should report the amount of insurance expense expiring during the period indicated in the heading of the income statement.

expensesCosts that are matched with revenues on the income statement. For example, Cost of GoodsSold is an expense caused by Sales. Insurance Expense, Wages Expense, Advertising Expense, Interest Expense are expenses matched with the period of time in the heading ofthe income statement. Under the accrual basis of accounting, the matching is NOT based on the date that the expenses are paid.Expenses associated with the main activity of the business are referred to as operating expenses. Expenses associated with a peripheral activity are nonoperating or other expenses. For example, a retailer's interest expense is a nonoperating expense. A bank'sinterest expense is an operating expense.

Generally, expenses are debited to a specific expense account and the normal balance of an expense account is a debit balance. When an expense account is debited, the account credited might be Cash (if cash was paid at the time of the expense), Accounts Payable (if cash will be paid after the expense is recorded), or Prepaid Expense (if cash was paid before the expense was recorded.) To learn more, see Explanation of Income Statement.

revenuesFees earned from providing services and the amounts of merchandise sold. Under the accrual basis of accounting, revenues are recorded at the time of delivering the serviceor the merchandise, even if cash is not received at the time of delivery. Often the termincome is used instead of revenues.

Examples of revenue accounts include: Sales, Service Revenues, Fees Earned, Interest Revenue, Interest Income. Revenue accounts are credited when services are performed/billed and therefore will usually have credit balances. At the time that a revenue account is credited, the account debited might be Cash, Accounts Receivable, or Unearned Revenue depending if cash was received at the time of the service, if the customer was billed at the time of the service and will pay later, or if the customer had paid in advance of the service being performed.

If the revenues earned are a main activity of the business, they are considered to be operating revenues. If the revenues come from a secondary activity, they are considered to be nonoperating revenues. For example, interest earned by a manufacturer on its investments is a nonoperating revenue. Interest earned by a bank is considered to be part of operating revenues. To learn more, see Explanation of Income Statement.

Adjusting Journal EntriesAll adjusting entries (other than error corrections) will always involve at least one account on the balance sheet and at least one account on the income statement.

I. Deferral AdjustmentsA deferral involves a past exchange of cash that has initially been recorded on the balance sheet rather than on the income statement. The name deferral comes about because therecording on the income statement is deferred (postponed) to a later time.

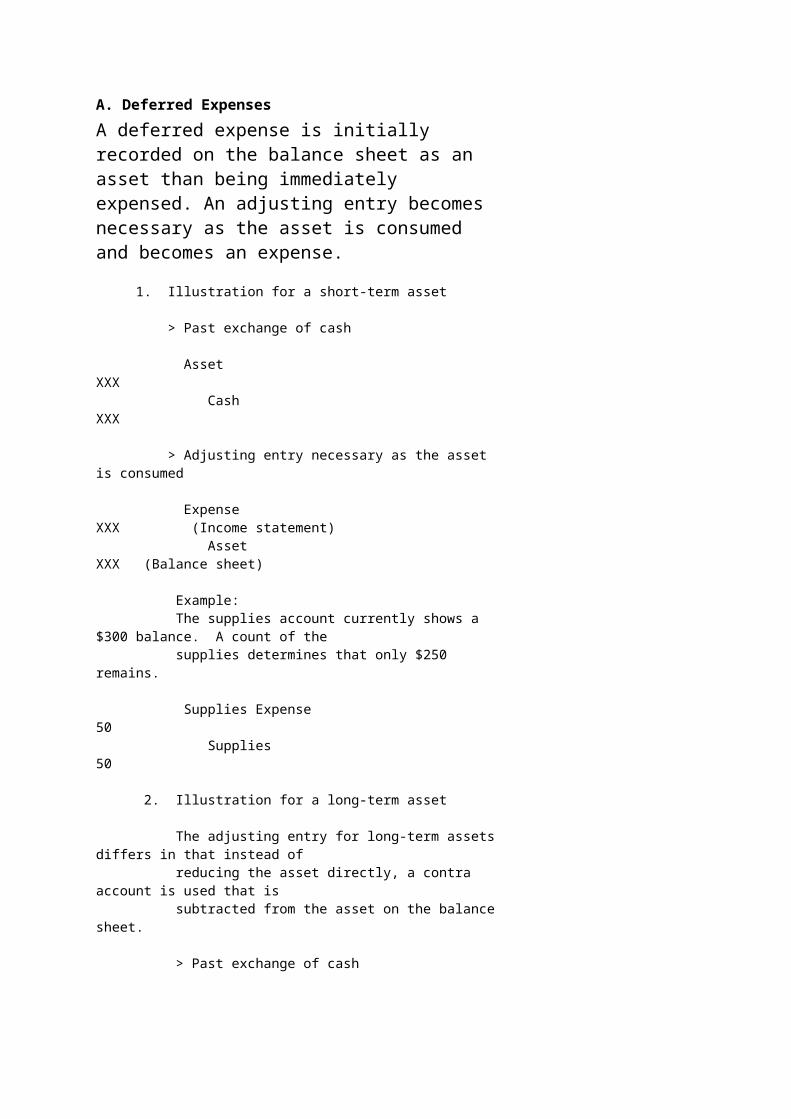

A. Deferred ExpensesA deferred expense is initially recorded on the balance sheet as an asset than being immediately expensed. An adjusting entry becomes necessary as the asset is consumed and becomes an expense.

1. Illustration for a short-term asset

> Past exchange of cash

Asset XXX Cash XXX

> Adjusting entry necessary as the asset is consumed

Expense XXX (Income statement) Asset XXX (Balance sheet)

Example: The supplies account currently shows a $300 balance. A count of the supplies determines that only $250 remains.

Supplies Expense 50 Supplies 50

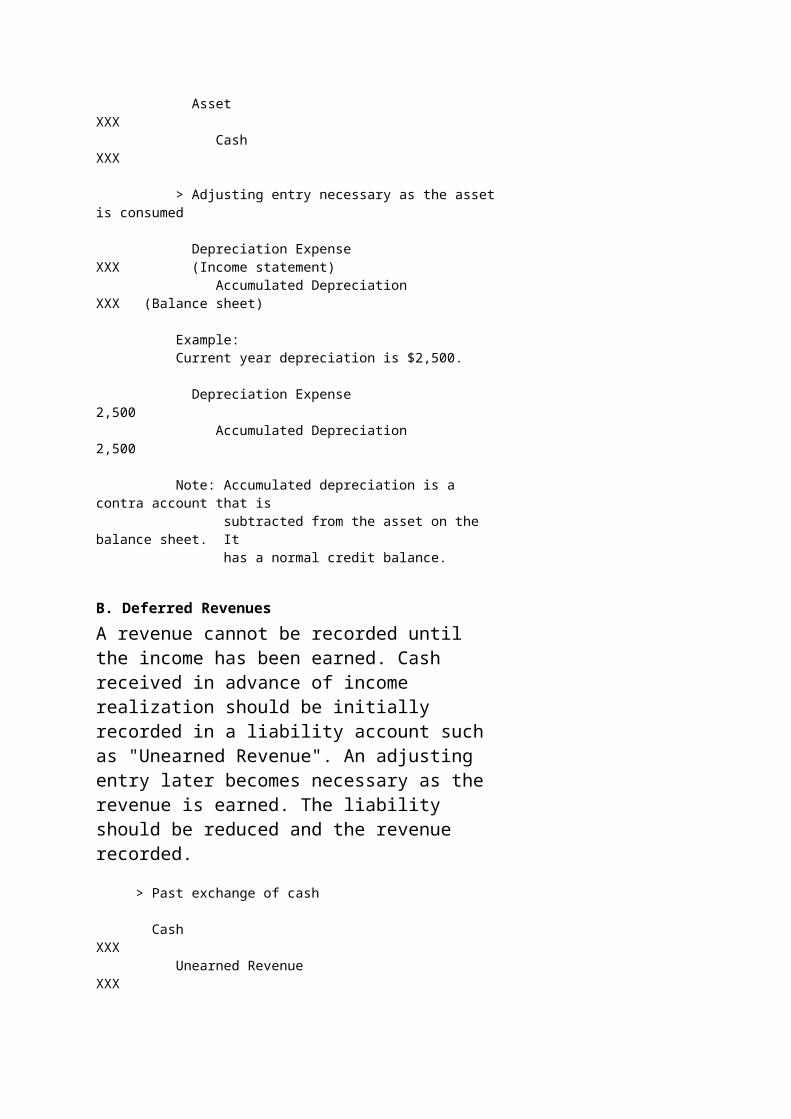

2. Illustration for a long-term asset

The adjusting entry for long-term assets differs in that instead of reducing the asset directly, a contra account is used that is subtracted from the asset on the balance sheet.

> Past exchange of cash

Asset XXX Cash XXX

> Adjusting entry necessary as the asset is consumed

Depreciation Expense XXX (Income statement) Accumulated Depreciation XXX (Balance sheet)

Example: Current year depreciation is $2,500.

Depreciation Expense 2,500 Accumulated Depreciation 2,500

Note: Accumulated depreciation is a contra account that is subtracted from the asset on the balance sheet. It has a normal credit balance.

B. Deferred RevenuesA revenue cannot be recorded until the income has been earned. Cash received in advance of income realization should be initially recorded in a liability account such as "Unearned Revenue". An adjusting entry later becomes necessary as the revenue is earned. The liability should be reduced and the revenue recorded.

> Past exchange of cash

Cash XXX Unearned Revenue XXX

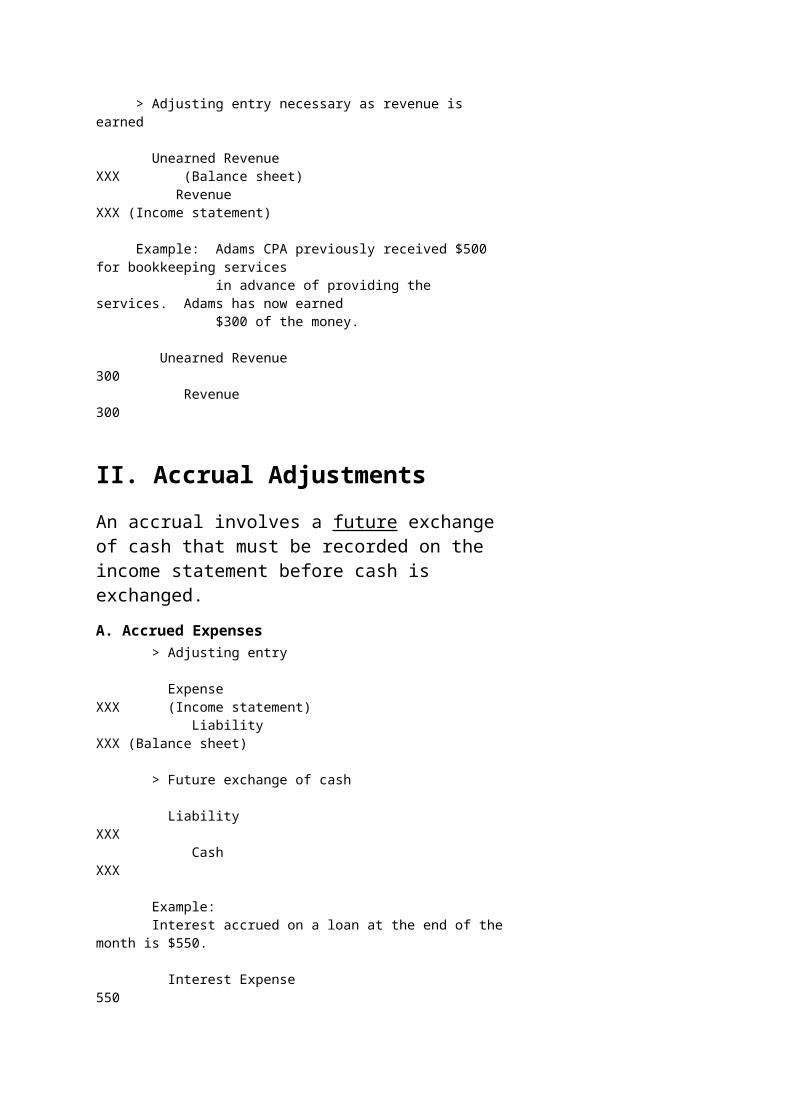

> Adjusting entry necessary as revenue is earned

Unearned Revenue XXX (Balance sheet) Revenue XXX (Income statement)

Example: Adams CPA previously received $500 for bookkeeping services in advance of providing the services. Adams has now earned $300 of the money.

Unearned Revenue 300 Revenue 300

II. Accrual AdjustmentsAn accrual involves a future exchangeof cash that must be recorded on the income statement before cash is exchanged.A. Accrued Expenses > Adjusting entry

Expense XXX (Income statement) Liability XXX (Balance sheet)

> Future exchange of cash

Liability XXX Cash XXX

Example: Interest accrued on a loan at the end of themonth is $550.

Interest Expense 550

Interest Payable 550

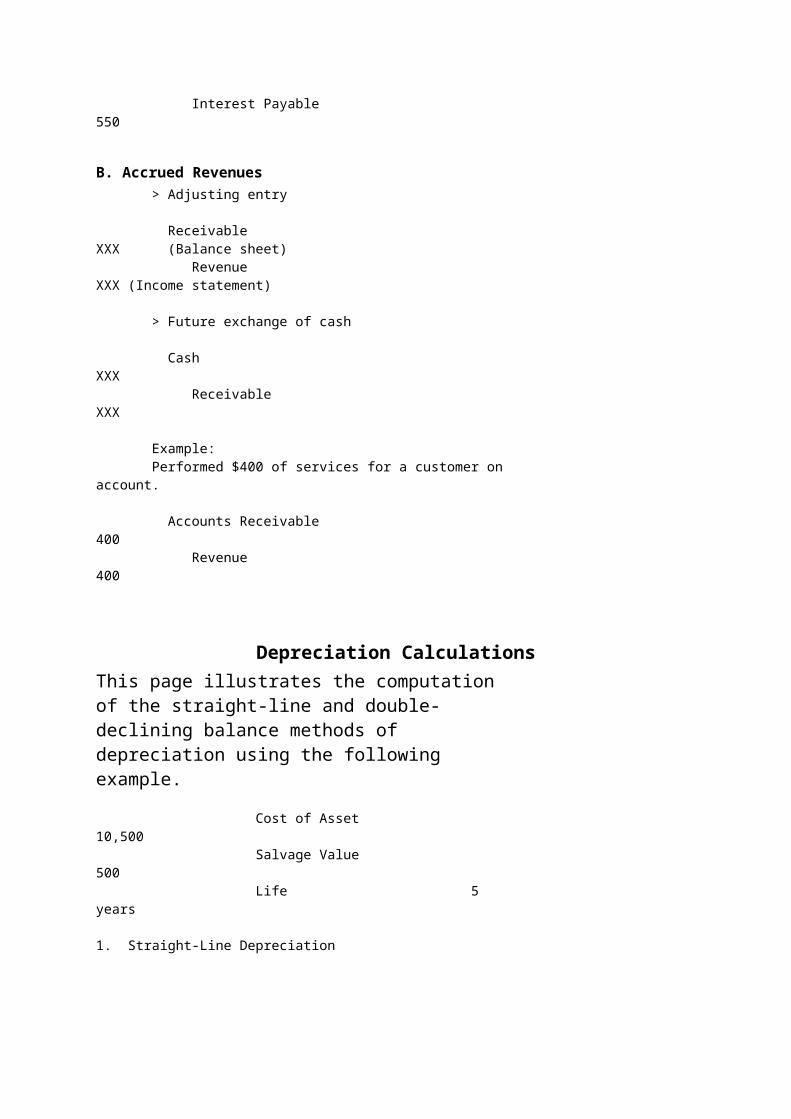

B. Accrued Revenues > Adjusting entry

Receivable XXX (Balance sheet) Revenue XXX (Income statement)

> Future exchange of cash

Cash XXX Receivable XXX

Example: Performed $400 of services for a customer onaccount.

Accounts Receivable 400 Revenue 400

Depreciation CalculationsThis page illustrates the computationof the straight-line and double-declining balance methods of depreciation using the following example.

Cost of Asset 10,500 Salvage Value 500 Life 5 years

1. Straight-Line Depreciation

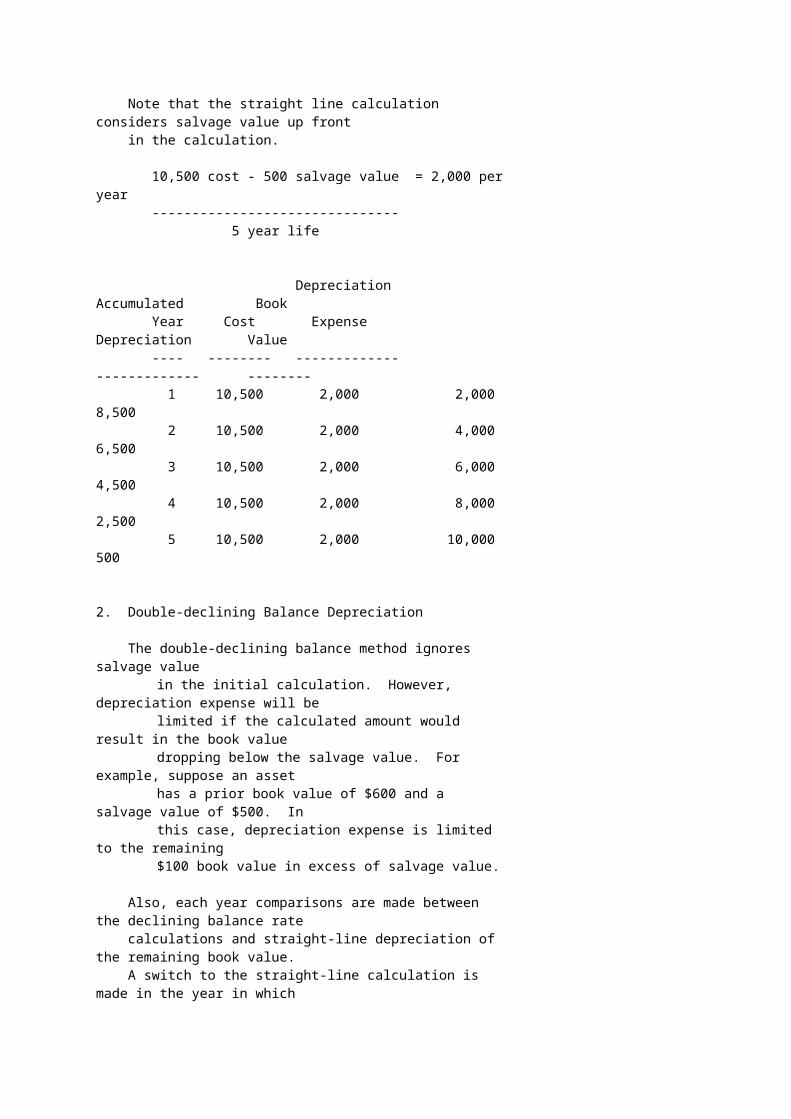

Note that the straight line calculation considers salvage value up front in the calculation.

10,500 cost - 500 salvage value = 2,000 peryear ------------------------------- 5 year life

Depreciation Accumulated Book Year Cost Expense Depreciation Value ---- -------- ------------- ------------- -------- 1 10,500 2,000 2,000 8,500 2 10,500 2,000 4,000 6,500 3 10,500 2,000 6,000 4,500 4 10,500 2,000 8,000 2,500 5 10,500 2,000 10,000 500

2. Double-declining Balance Depreciation

The double-declining balance method ignores salvage value

in the initial calculation. However, depreciation expense will be

limited if the calculated amount would result in the book value

dropping below the salvage value. For example, suppose an asset

has a prior book value of $600 and a salvage value of $500. In

this case, depreciation expense is limited to the remaining

$100 book value in excess of salvage value.

Also, each year comparisons are made between the declining balance rate calculations and straight-line depreciation of the remaining book value. A switch to the straight-line calculation is made in the year in which

the straight-line calculation exceeds the declining balance rate calculation.

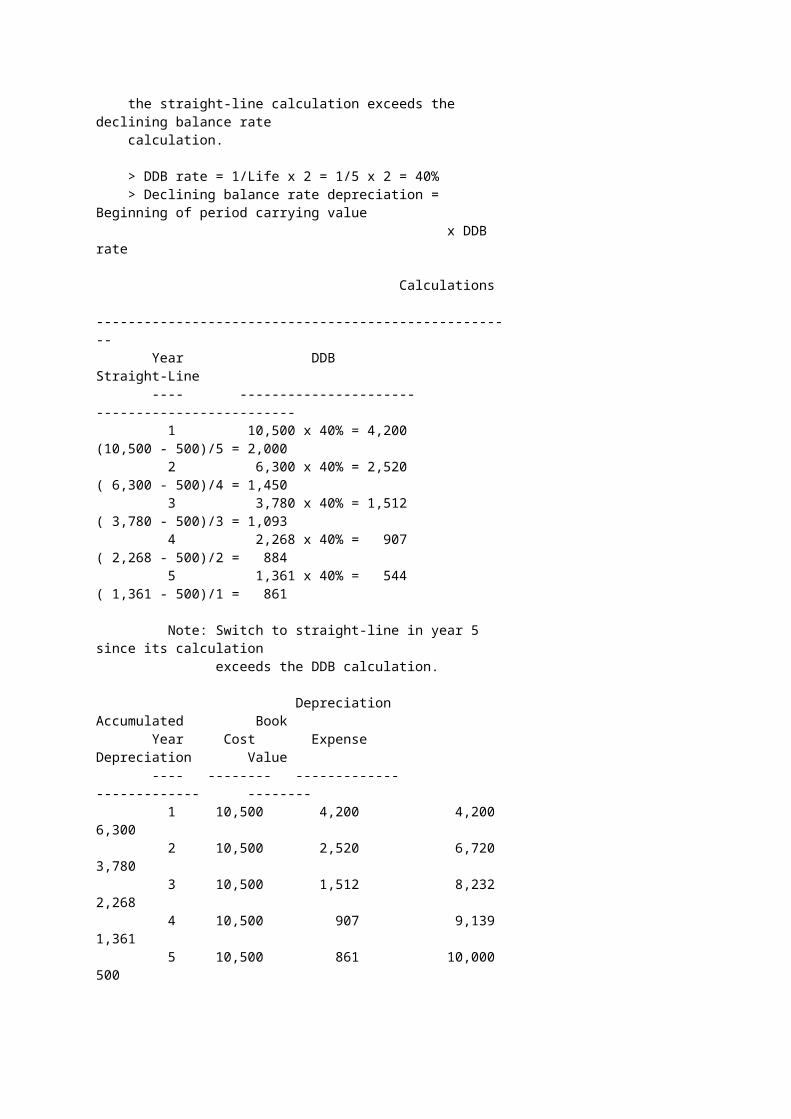

> DDB rate = 1/Life x 2 = 1/5 x 2 = 40% > Declining balance rate depreciation = Beginning of period carrying value x DDB rate

Calculations ----------------------------------------------------- Year DDB Straight-Line ---- ---------------------- ------------------------- 1 10,500 x 40% = 4,200 (10,500 - 500)/5 = 2,000 2 6,300 x 40% = 2,520 ( 6,300 - 500)/4 = 1,450 3 3,780 x 40% = 1,512 ( 3,780 - 500)/3 = 1,093 4 2,268 x 40% = 907 ( 2,268 - 500)/2 = 884 5 1,361 x 40% = 544 ( 1,361 - 500)/1 = 861

Note: Switch to straight-line in year 5 since its calculation exceeds the DDB calculation.

Depreciation Accumulated Book Year Cost Expense Depreciation Value ---- -------- ------------- ------------- -------- 1 10,500 4,200 4,200 6,300 2 10,500 2,520 6,720 3,780 3 10,500 1,512 8,232 2,268 4 10,500 907 9,139 1,361 5 10,500 861 10,000 500

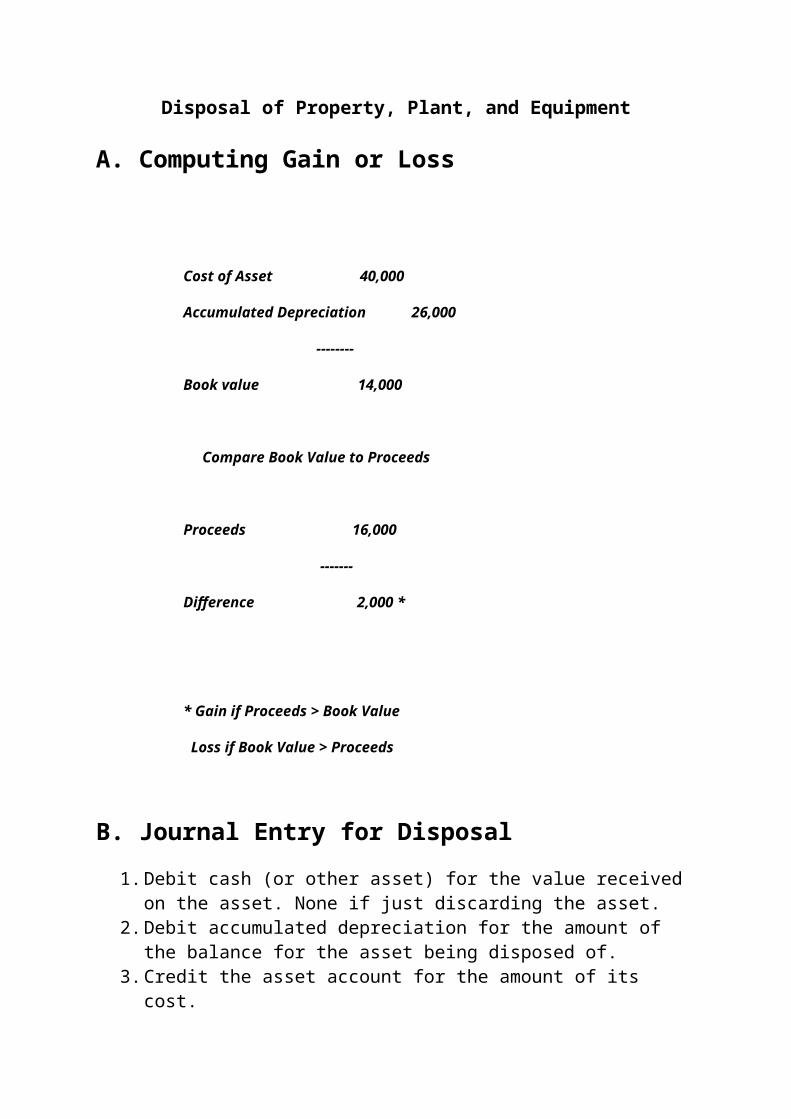

Disposal of Property, Plant, and Equipment

A. Computing Gain or Loss

Cost of Asset 40,000

Accumulated Depreciation 26,000

--------

Book value 14,000

Compare Book Value to Proceeds

Proceeds 16,000

-------

Difference 2,000 *

* Gain if Proceeds > Book Value

Loss if Book Value > Proceeds

B. Journal Entry for Disposal1.Debit cash (or other asset) for the value received

on the asset. None if just discarding the asset.2.Debit accumulated depreciation for the amount of

the balance for the asset being disposed of.3.Credit the asset account for the amount of its

cost.

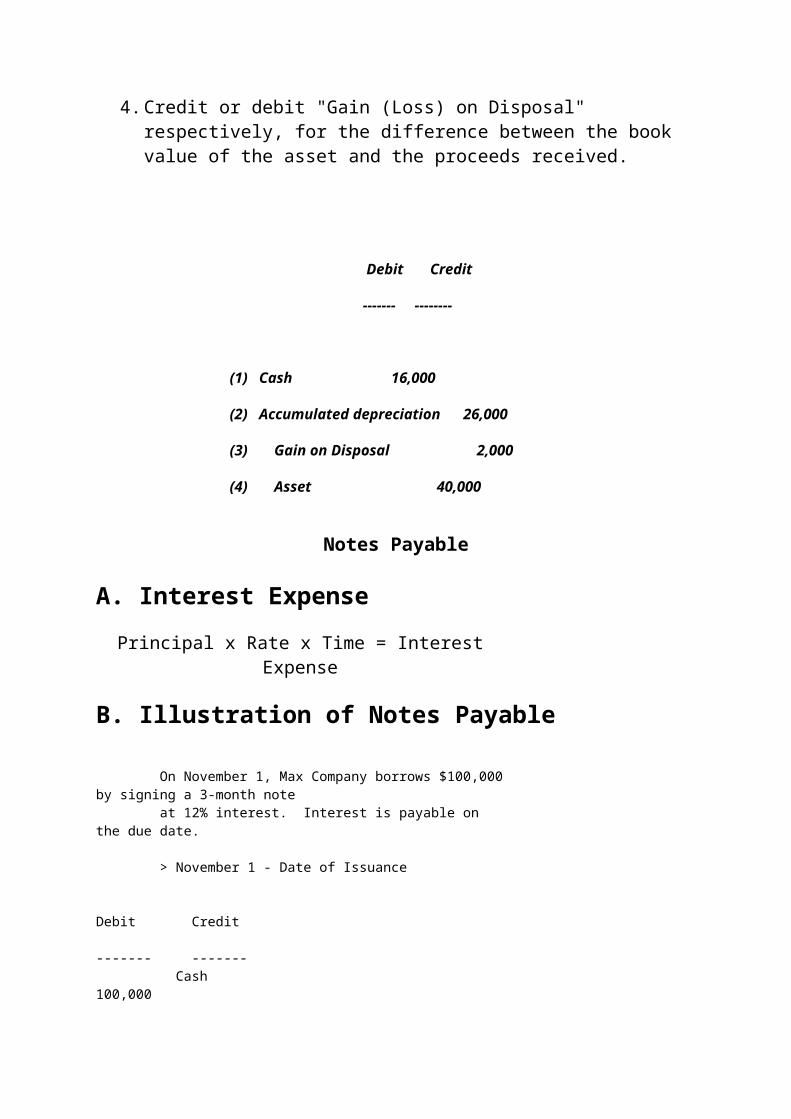

4.Credit or debit "Gain (Loss) on Disposal" respectively, for the difference between the book value of the asset and the proceeds received.

Debit Credit

------- --------

(1) Cash 16,000

(2) Accumulated depreciation 26,000

(3) Gain on Disposal 2,000

(4) Asset 40,000

Notes Payable

A. Interest ExpensePrincipal x Rate x Time = Interest

Expense

B. Illustration of Notes Payable

On November 1, Max Company borrows $100,000by signing a 3-month note at 12% interest. Interest is payable on the due date.

> November 1 - Date of Issuance

Debit Credit ------- ------- Cash 100,000

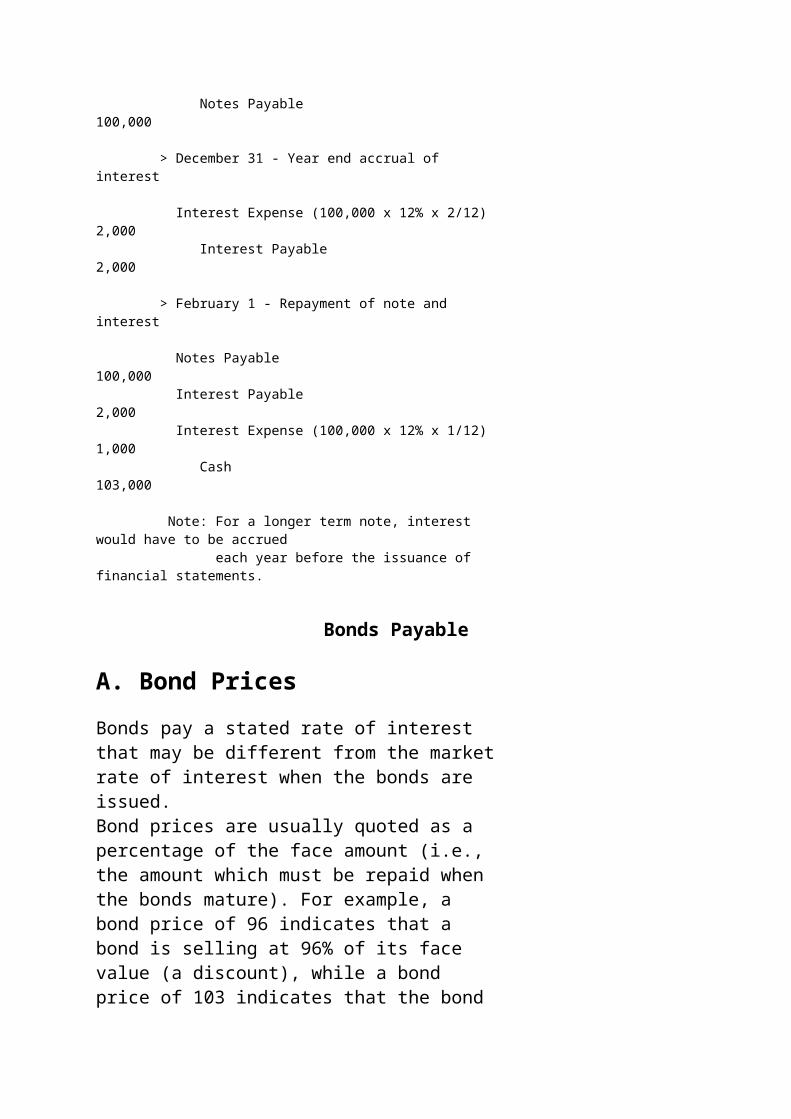

Notes Payable 100,000

> December 31 - Year end accrual of interest

Interest Expense (100,000 x 12% x 2/12) 2,000 Interest Payable 2,000

> February 1 - Repayment of note and interest

Notes Payable 100,000 Interest Payable 2,000 Interest Expense (100,000 x 12% x 1/12) 1,000 Cash 103,000

Note: For a longer term note, interest would have to be accrued each year before the issuance of financial statements.

Bonds Payable

A. Bond PricesBonds pay a stated rate of interest that may be different from the marketrate of interest when the bonds are issued.Bond prices are usually quoted as a percentage of the face amount (i.e., the amount which must be repaid when the bonds mature). For example, a bond price of 96 indicates that a bond is selling at 96% of its face value (a discount), while a bond price of 103 indicates that the bond

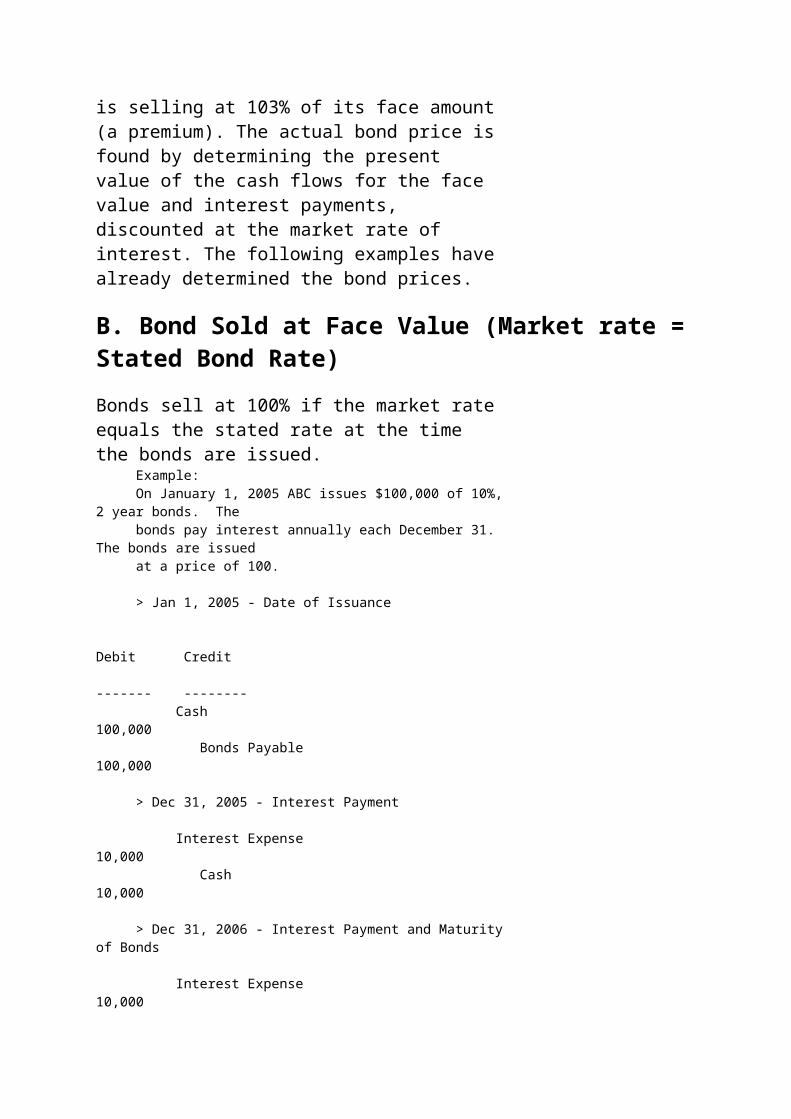

is selling at 103% of its face amount(a premium). The actual bond price isfound by determining the present value of the cash flows for the face value and interest payments, discounted at the market rate of interest. The following examples havealready determined the bond prices.

B. Bond Sold at Face Value (Market rate =Stated Bond Rate)Bonds sell at 100% if the market rateequals the stated rate at the time the bonds are issued. Example: On January 1, 2005 ABC issues $100,000 of 10%,2 year bonds. The bonds pay interest annually each December 31. The bonds are issued at a price of 100.

> Jan 1, 2005 - Date of Issuance

Debit Credit ------- -------- Cash 100,000 Bonds Payable 100,000

> Dec 31, 2005 - Interest Payment

Interest Expense 10,000 Cash 10,000

> Dec 31, 2006 - Interest Payment and Maturityof Bonds

Interest Expense 10,000

Cash 10,000

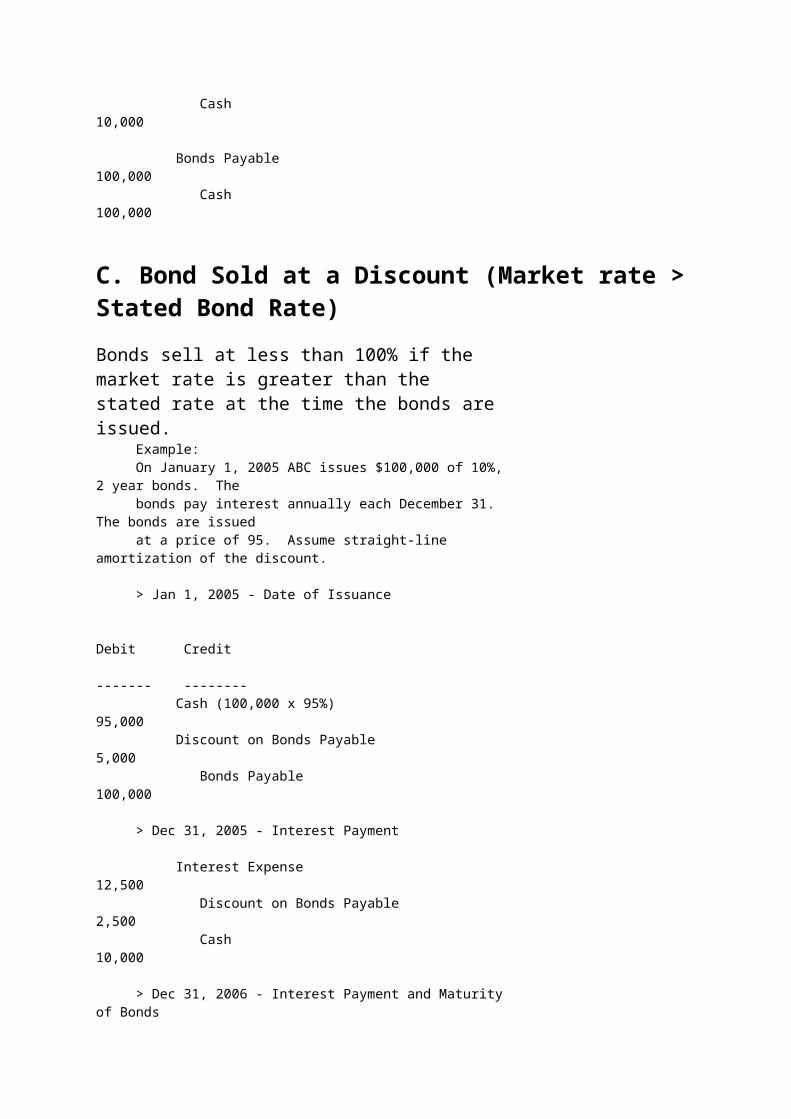

Bonds Payable 100,000 Cash 100,000

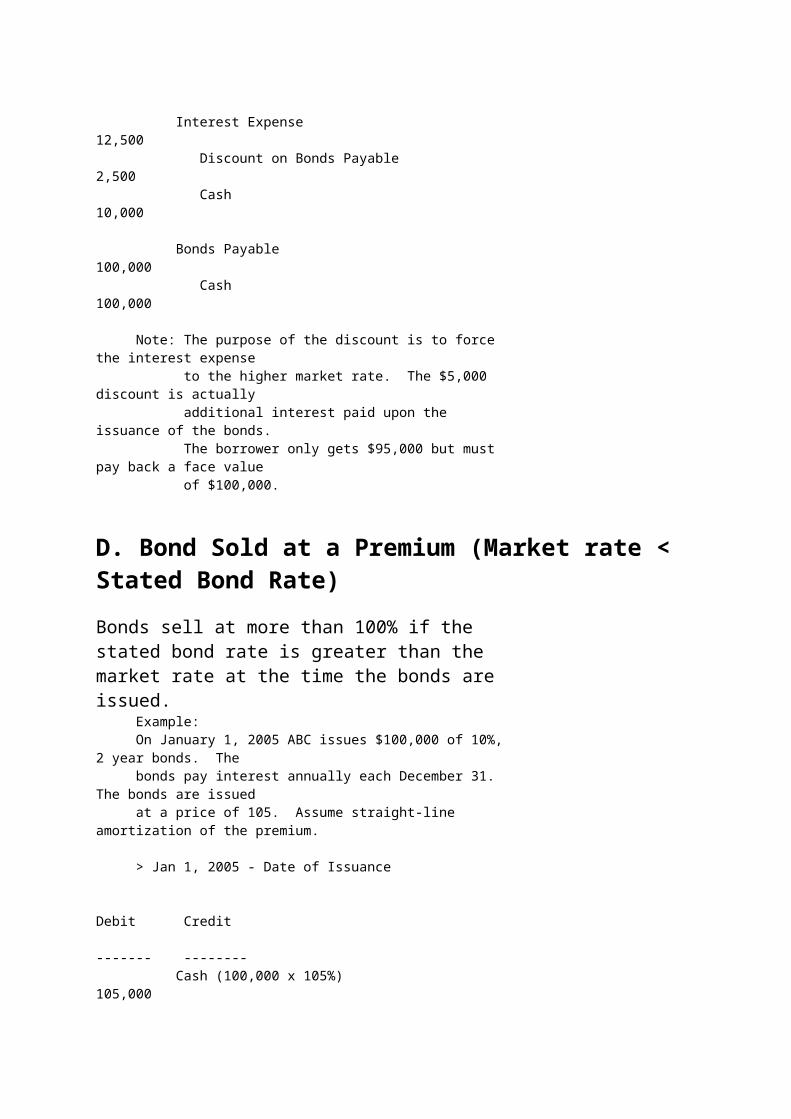

C. Bond Sold at a Discount (Market rate >Stated Bond Rate)Bonds sell at less than 100% if the market rate is greater than the stated rate at the time the bonds areissued. Example: On January 1, 2005 ABC issues $100,000 of 10%,2 year bonds. The bonds pay interest annually each December 31. The bonds are issued at a price of 95. Assume straight-line amortization of the discount.

> Jan 1, 2005 - Date of Issuance

Debit Credit ------- -------- Cash (100,000 x 95%) 95,000 Discount on Bonds Payable 5,000 Bonds Payable 100,000

> Dec 31, 2005 - Interest Payment

Interest Expense 12,500 Discount on Bonds Payable 2,500 Cash 10,000

> Dec 31, 2006 - Interest Payment and Maturityof Bonds

Interest Expense 12,500 Discount on Bonds Payable 2,500 Cash 10,000

Bonds Payable 100,000 Cash 100,000

Note: The purpose of the discount is to force the interest expense to the higher market rate. The $5,000 discount is actually additional interest paid upon the issuance of the bonds. The borrower only gets $95,000 but must pay back a face value of $100,000.

D. Bond Sold at a Premium (Market rate < Stated Bond Rate)Bonds sell at more than 100% if the stated bond rate is greater than the market rate at the time the bonds areissued. Example: On January 1, 2005 ABC issues $100,000 of 10%,2 year bonds. The bonds pay interest annually each December 31. The bonds are issued at a price of 105. Assume straight-line amortization of the premium.

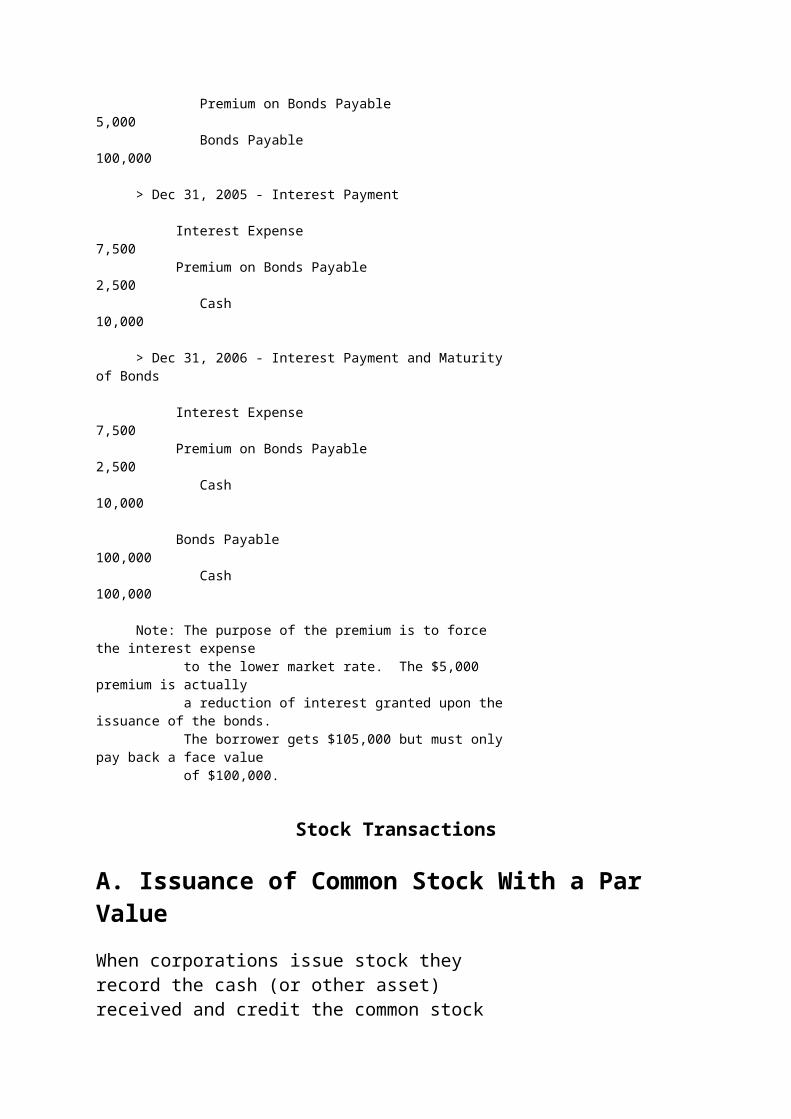

> Jan 1, 2005 - Date of Issuance

Debit Credit ------- -------- Cash (100,000 x 105%) 105,000

Premium on Bonds Payable 5,000 Bonds Payable 100,000

> Dec 31, 2005 - Interest Payment

Interest Expense 7,500 Premium on Bonds Payable 2,500 Cash 10,000

> Dec 31, 2006 - Interest Payment and Maturityof Bonds

Interest Expense 7,500 Premium on Bonds Payable 2,500 Cash 10,000

Bonds Payable 100,000 Cash 100,000

Note: The purpose of the premium is to force the interest expense to the lower market rate. The $5,000 premium is actually a reduction of interest granted upon theissuance of the bonds. The borrower gets $105,000 but must onlypay back a face value of $100,000.

Stock Transactions

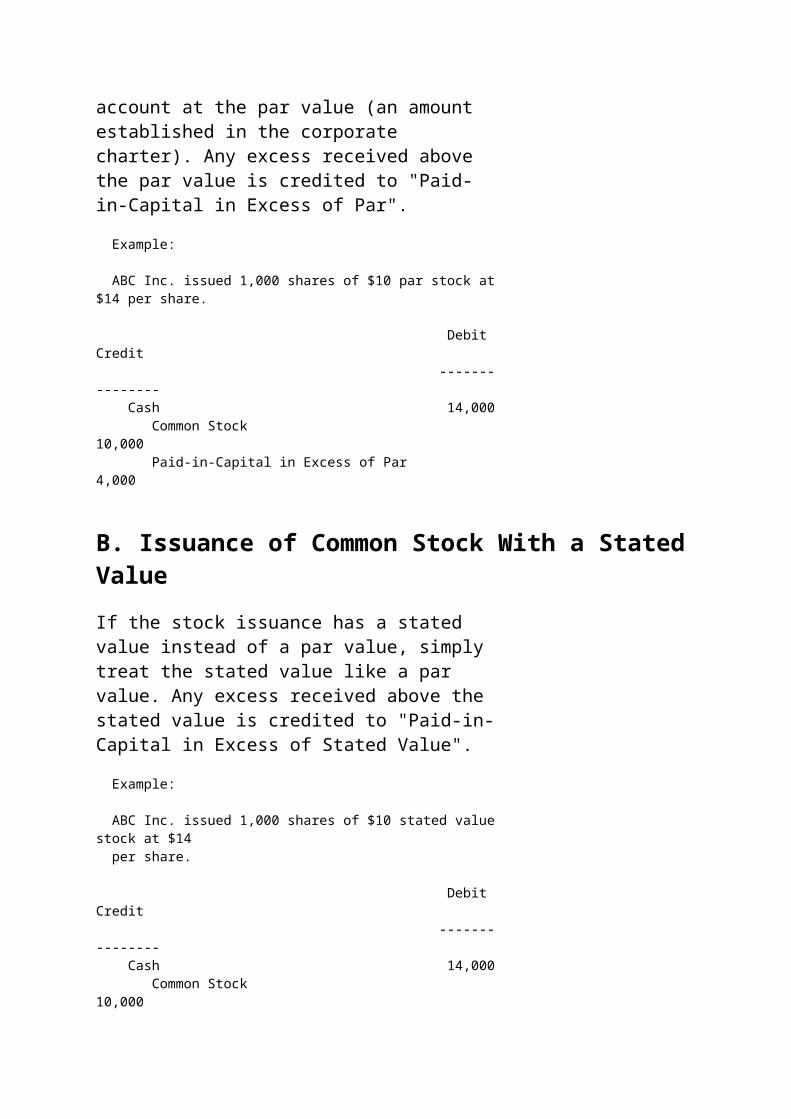

A. Issuance of Common Stock With a Par ValueWhen corporations issue stock they record the cash (or other asset) received and credit the common stock

account at the par value (an amount established in the corporate charter). Any excess received above the par value is credited to "Paid-in-Capital in Excess of Par".

Example:

ABC Inc. issued 1,000 shares of $10 par stock at $14 per share.

Debit Credit ------- -------- Cash 14,000 Common Stock 10,000 Paid-in-Capital in Excess of Par 4,000

B. Issuance of Common Stock With a StatedValueIf the stock issuance has a stated value instead of a par value, simply treat the stated value like a par value. Any excess received above the stated value is credited to "Paid-in-Capital in Excess of Stated Value".

Example:

ABC Inc. issued 1,000 shares of $10 stated value stock at $14 per share.

Debit Credit ------- -------- Cash 14,000 Common Stock 10,000

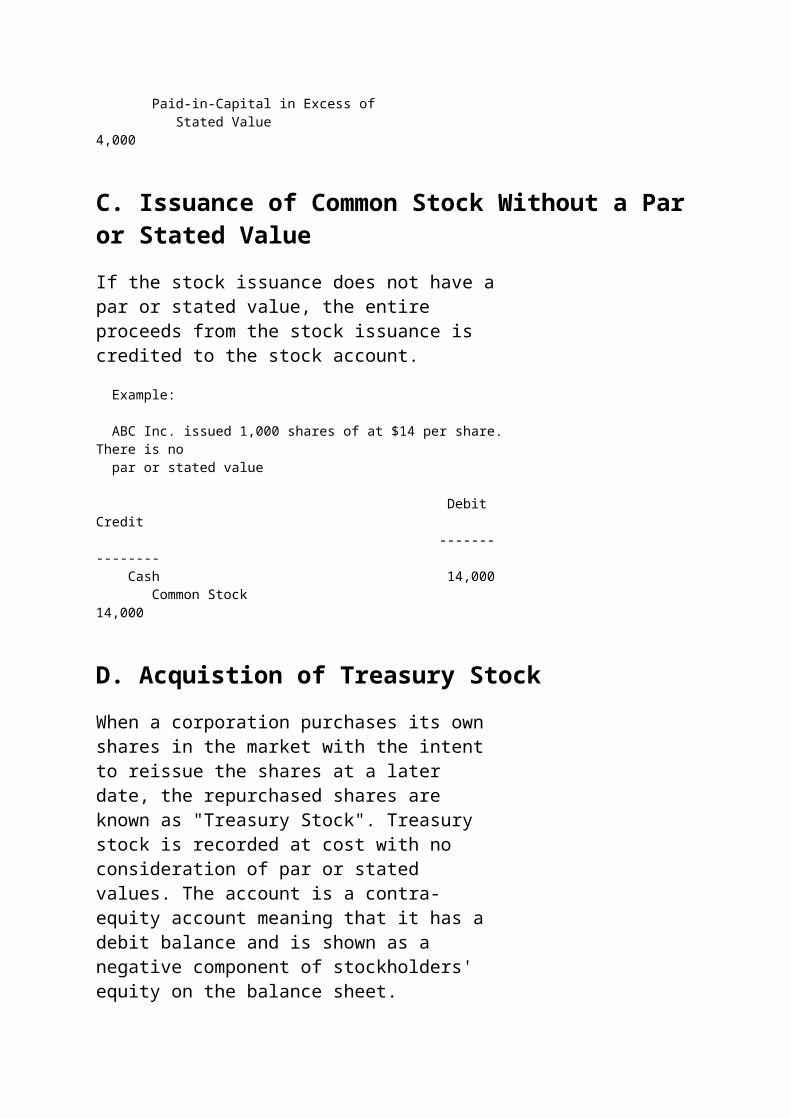

Paid-in-Capital in Excess of Stated Value 4,000

C. Issuance of Common Stock Without a Paror Stated ValueIf the stock issuance does not have apar or stated value, the entire proceeds from the stock issuance is credited to the stock account.

Example:

ABC Inc. issued 1,000 shares of at $14 per share.There is no par or stated value

Debit Credit ------- -------- Cash 14,000 Common Stock 14,000

D. Acquistion of Treasury StockWhen a corporation purchases its own shares in the market with the intent to reissue the shares at a later date, the repurchased shares are known as "Treasury Stock". Treasury stock is recorded at cost with no consideration of par or stated values. The account is a contra-equity account meaning that it has a debit balance and is shown as a negative component of stockholders' equity on the balance sheet.

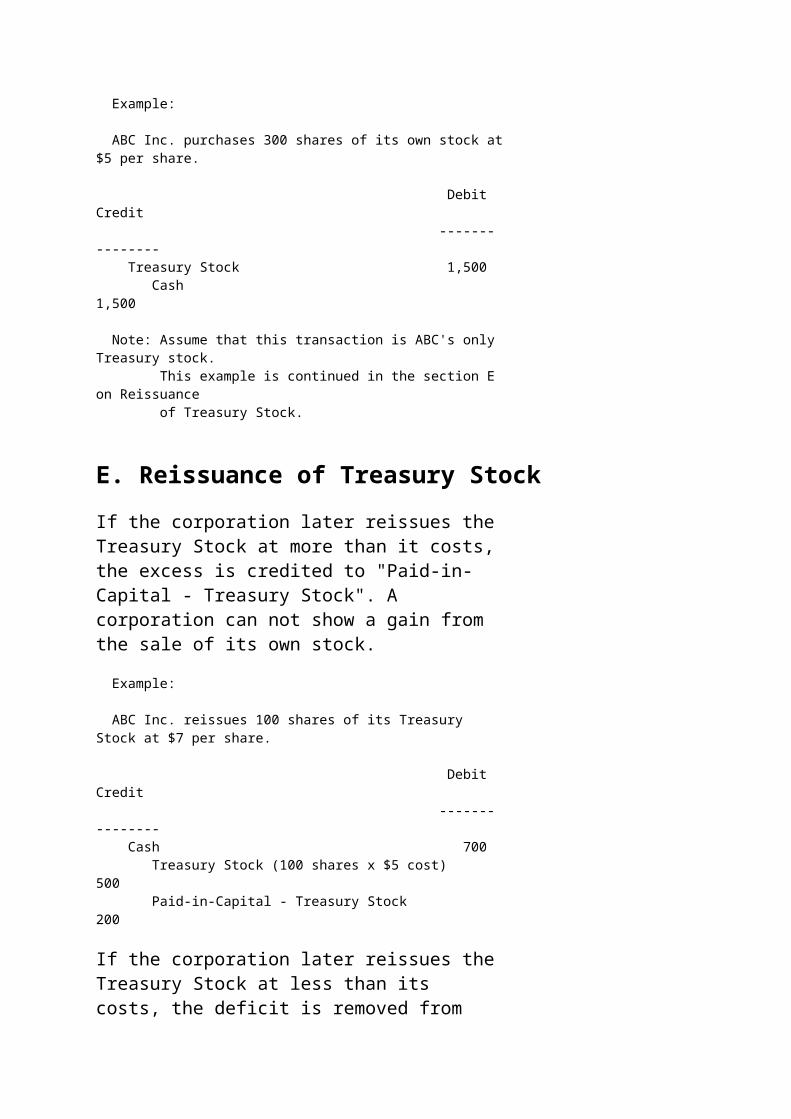

Example:

ABC Inc. purchases 300 shares of its own stock at$5 per share.

Debit Credit ------- -------- Treasury Stock 1,500 Cash 1,500

Note: Assume that this transaction is ABC's only Treasury stock. This example is continued in the section E on Reissuance of Treasury Stock.

E. Reissuance of Treasury StockIf the corporation later reissues theTreasury Stock at more than it costs,the excess is credited to "Paid-in-Capital - Treasury Stock". A corporation can not show a gain from the sale of its own stock.

Example:

ABC Inc. reissues 100 shares of its Treasury Stock at $7 per share.

Debit Credit ------- -------- Cash 700 Treasury Stock (100 shares x $5 cost) 500 Paid-in-Capital - Treasury Stock 200

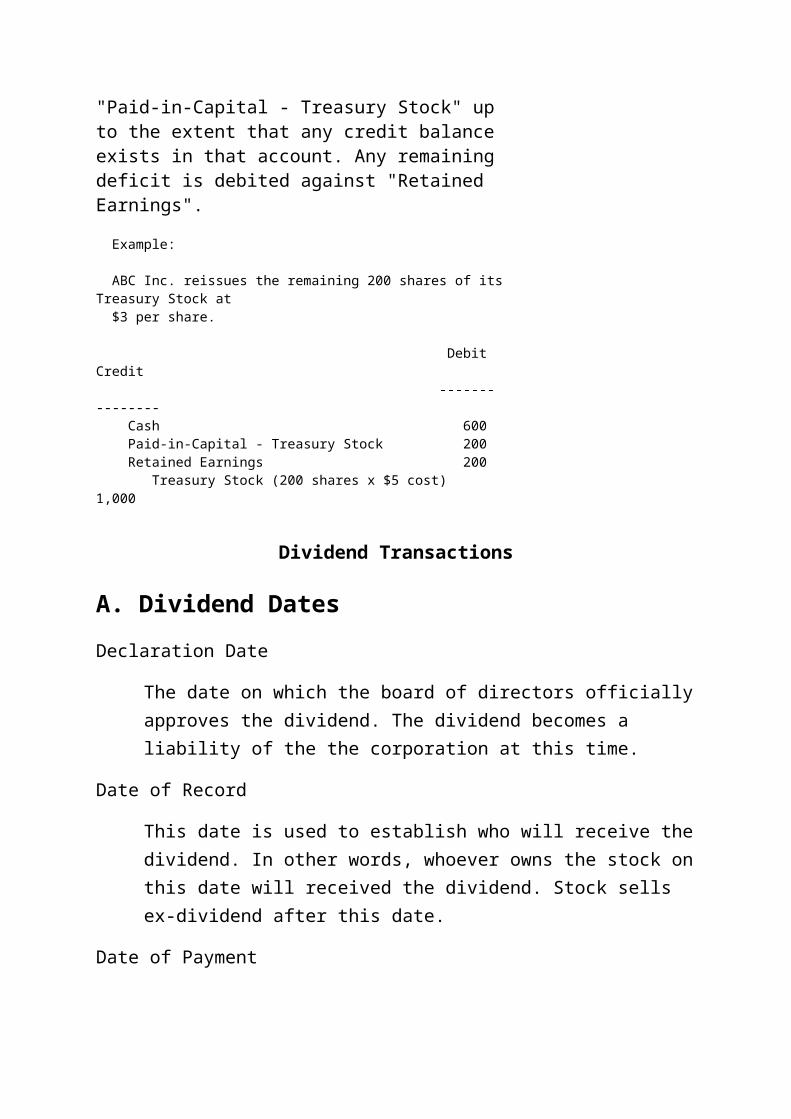

If the corporation later reissues theTreasury Stock at less than its costs, the deficit is removed from

"Paid-in-Capital - Treasury Stock" upto the extent that any credit balanceexists in that account. Any remainingdeficit is debited against "Retained Earnings".

Example:

ABC Inc. reissues the remaining 200 shares of itsTreasury Stock at $3 per share.

Debit Credit ------- -------- Cash 600 Paid-in-Capital - Treasury Stock 200 Retained Earnings 200 Treasury Stock (200 shares x $5 cost) 1,000

Dividend Transactions

A. Dividend DatesDeclaration Date

The date on which the board of directors officiallyapproves the dividend. The dividend becomes a liability of the the corporation at this time.

Date of Record

This date is used to establish who will receive thedividend. In other words, whoever owns the stock onthis date will received the dividend. Stock sells ex-dividend after this date.

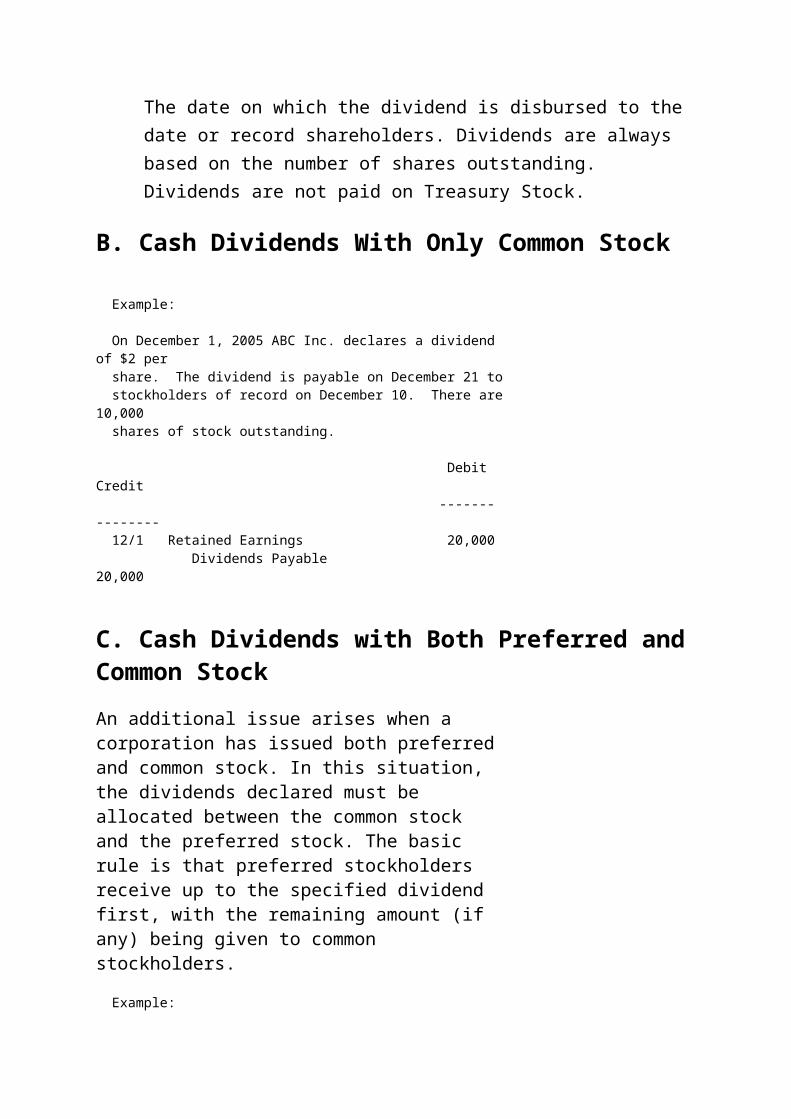

Date of Payment

The date on which the dividend is disbursed to the date or record shareholders. Dividends are always based on the number of shares outstanding. Dividends are not paid on Treasury Stock.

B. Cash Dividends With Only Common Stock

Example:

On December 1, 2005 ABC Inc. declares a dividend of $2 per share. The dividend is payable on December 21 to stockholders of record on December 10. There are10,000 shares of stock outstanding.

Debit Credit ------- -------- 12/1 Retained Earnings 20,000 Dividends Payable 20,000

C. Cash Dividends with Both Preferred andCommon StockAn additional issue arises when a corporation has issued both preferredand common stock. In this situation, the dividends declared must be allocated between the common stock and the preferred stock. The basic rule is that preferred stockholders receive up to the specified dividend first, with the remaining amount (if any) being given to common stockholders.

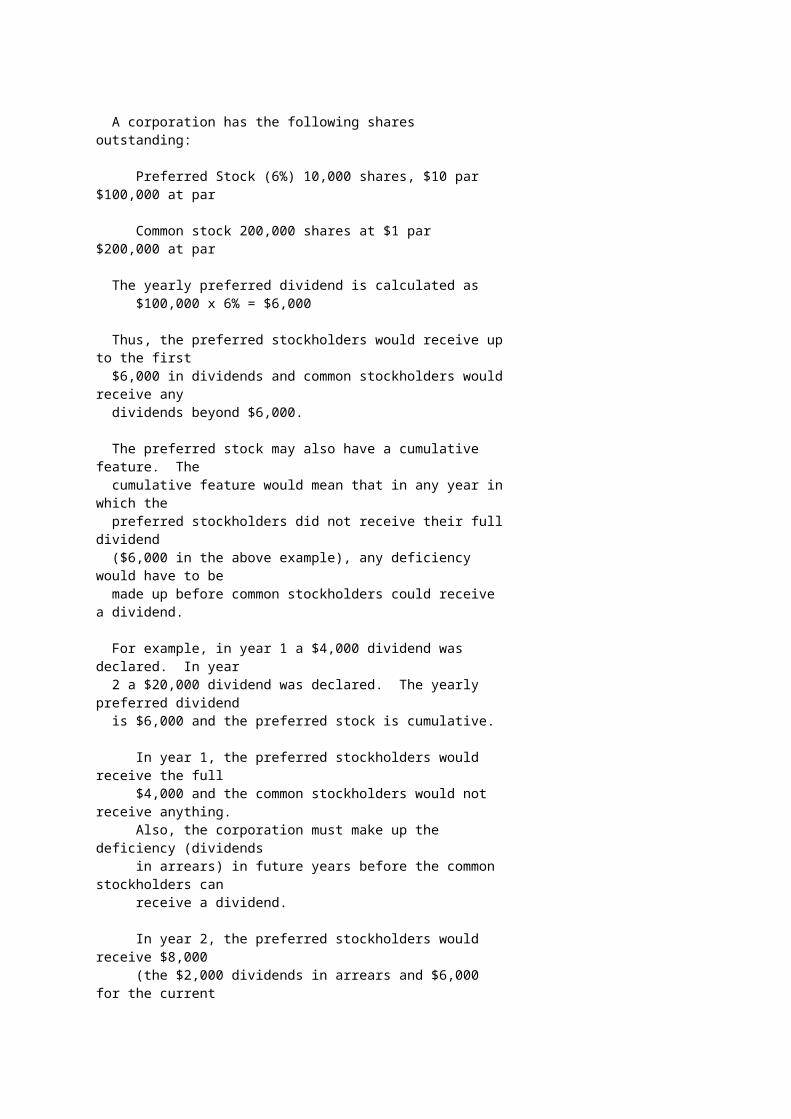

Example:

A corporation has the following shares outstanding:

Preferred Stock (6%) 10,000 shares, $10 par $100,000 at par

Common stock 200,000 shares at $1 par $200,000 at par

The yearly preferred dividend is calculated as $100,000 x 6% = $6,000

Thus, the preferred stockholders would receive upto the first $6,000 in dividends and common stockholders wouldreceive any dividends beyond $6,000.

The preferred stock may also have a cumulative feature. The cumulative feature would mean that in any year inwhich the preferred stockholders did not receive their fulldividend ($6,000 in the above example), any deficiency would have to be made up before common stockholders could receive a dividend.

For example, in year 1 a $4,000 dividend was declared. In year 2 a $20,000 dividend was declared. The yearly preferred dividend is $6,000 and the preferred stock is cumulative.

In year 1, the preferred stockholders would receive the full $4,000 and the common stockholders would not receive anything. Also, the corporation must make up the deficiency (dividends in arrears) in future years before the common stockholders can receive a dividend.

In year 2, the preferred stockholders would receive $8,000 (the $2,000 dividends in arrears and $6,000 for the current

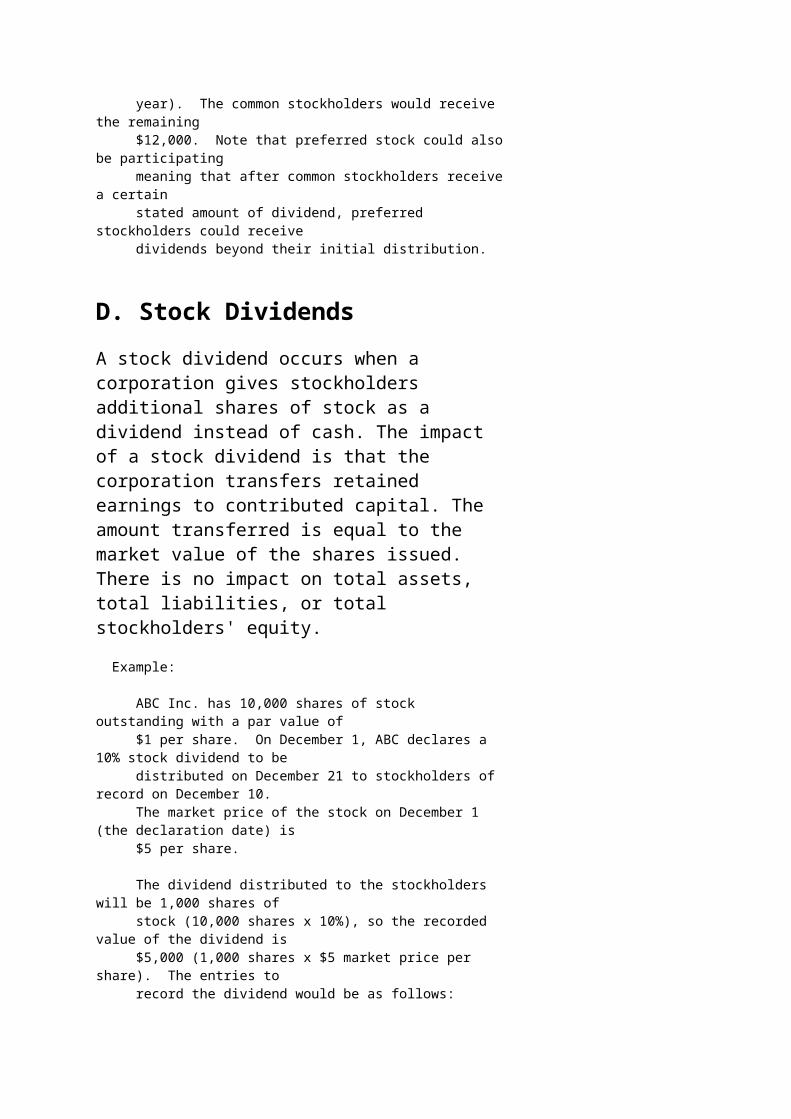

year). The common stockholders would receive the remaining $12,000. Note that preferred stock could alsobe participating meaning that after common stockholders receivea certain stated amount of dividend, preferred stockholders could receive dividends beyond their initial distribution.

D. Stock DividendsA stock dividend occurs when a corporation gives stockholders additional shares of stock as a dividend instead of cash. The impact of a stock dividend is that the corporation transfers retained earnings to contributed capital. The amount transferred is equal to the market value of the shares issued. There is no impact on total assets, total liabilities, or total stockholders' equity.

Example:

ABC Inc. has 10,000 shares of stock outstanding with a par value of $1 per share. On December 1, ABC declares a 10% stock dividend to be distributed on December 21 to stockholders of record on December 10. The market price of the stock on December 1 (the declaration date) is $5 per share.

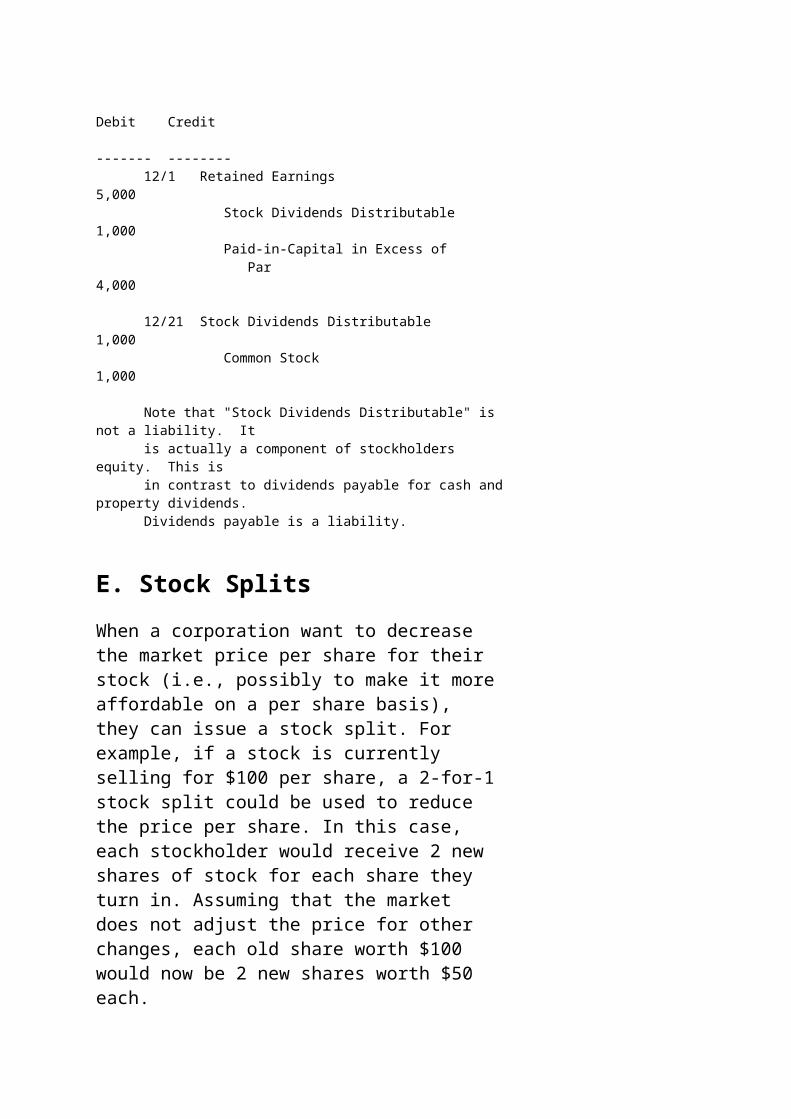

The dividend distributed to the stockholders will be 1,000 shares of stock (10,000 shares x 10%), so the recorded value of the dividend is $5,000 (1,000 shares x $5 market price per share). The entries to record the dividend would be as follows:

Debit Credit ------- -------- 12/1 Retained Earnings 5,000 Stock Dividends Distributable 1,000 Paid-in-Capital in Excess of Par 4,000

12/21 Stock Dividends Distributable 1,000 Common Stock 1,000

Note that "Stock Dividends Distributable" is not a liability. It is actually a component of stockholders equity. This is in contrast to dividends payable for cash andproperty dividends. Dividends payable is a liability.

E. Stock SplitsWhen a corporation want to decrease the market price per share for their stock (i.e., possibly to make it moreaffordable on a per share basis), they can issue a stock split. For example, if a stock is currently selling for $100 per share, a 2-for-1stock split could be used to reduce the price per share. In this case, each stockholder would receive 2 new shares of stock for each share they turn in. Assuming that the market does not adjust the price for other changes, each old share worth $100 would now be 2 new shares worth $50 each.

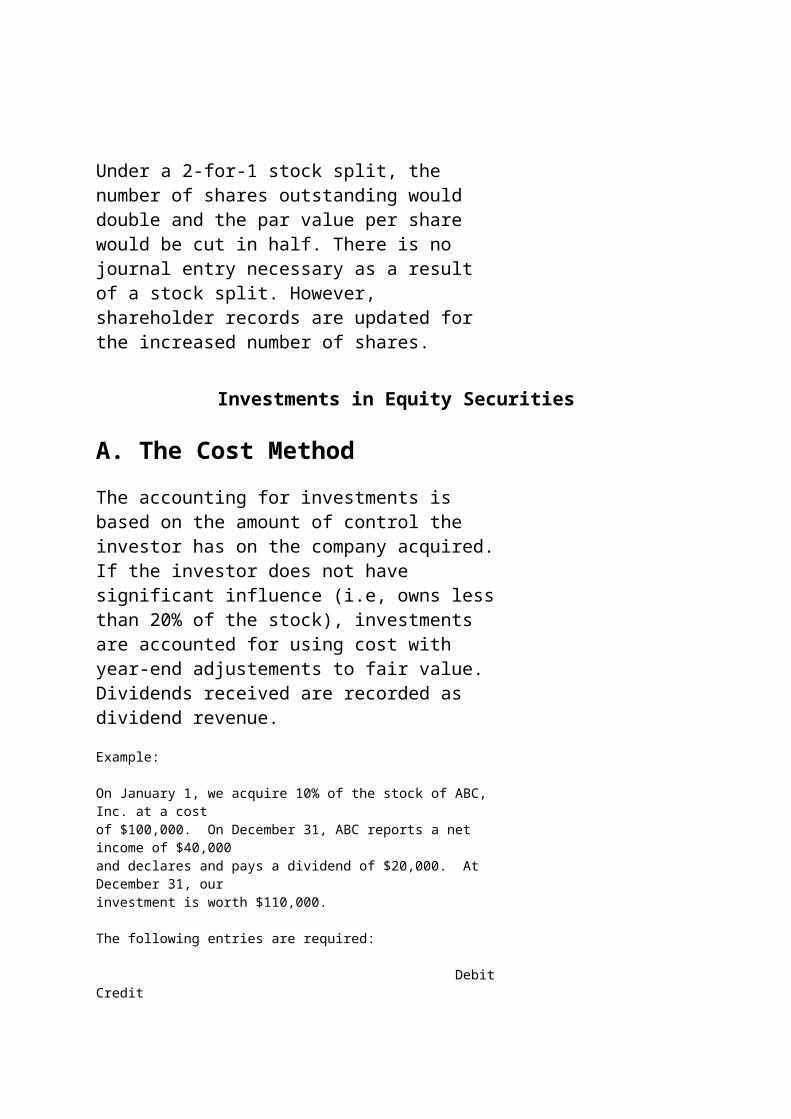

Under a 2-for-1 stock split, the number of shares outstanding would double and the par value per share would be cut in half. There is no journal entry necessary as a result of a stock split. However, shareholder records are updated for the increased number of shares.

Investments in Equity Securities

A. The Cost MethodThe accounting for investments is based on the amount of control the investor has on the company acquired.If the investor does not have significant influence (i.e, owns lessthan 20% of the stock), investments are accounted for using cost with year-end adjustements to fair value. Dividends received are recorded as dividend revenue.

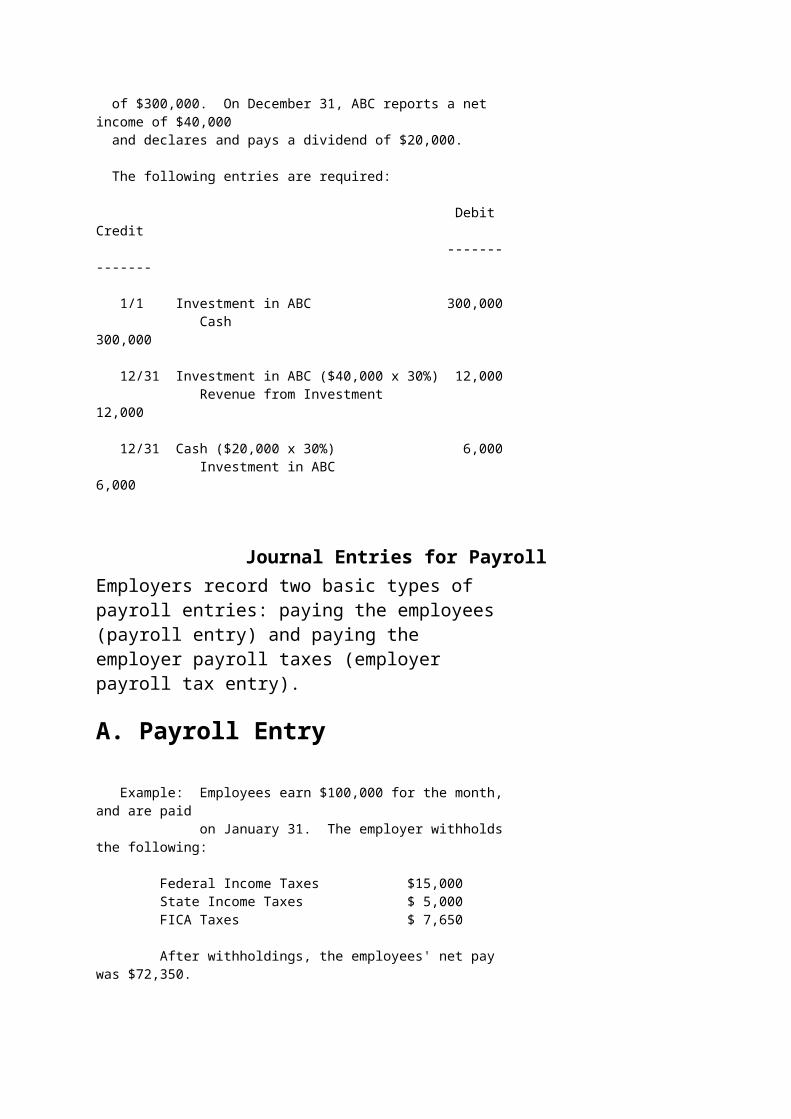

Example:

On January 1, we acquire 10% of the stock of ABC, Inc. at a costof $100,000. On December 31, ABC reports a net income of $40,000and declares and pays a dividend of $20,000. At December 31, ourinvestment is worth $110,000.

The following entries are required:

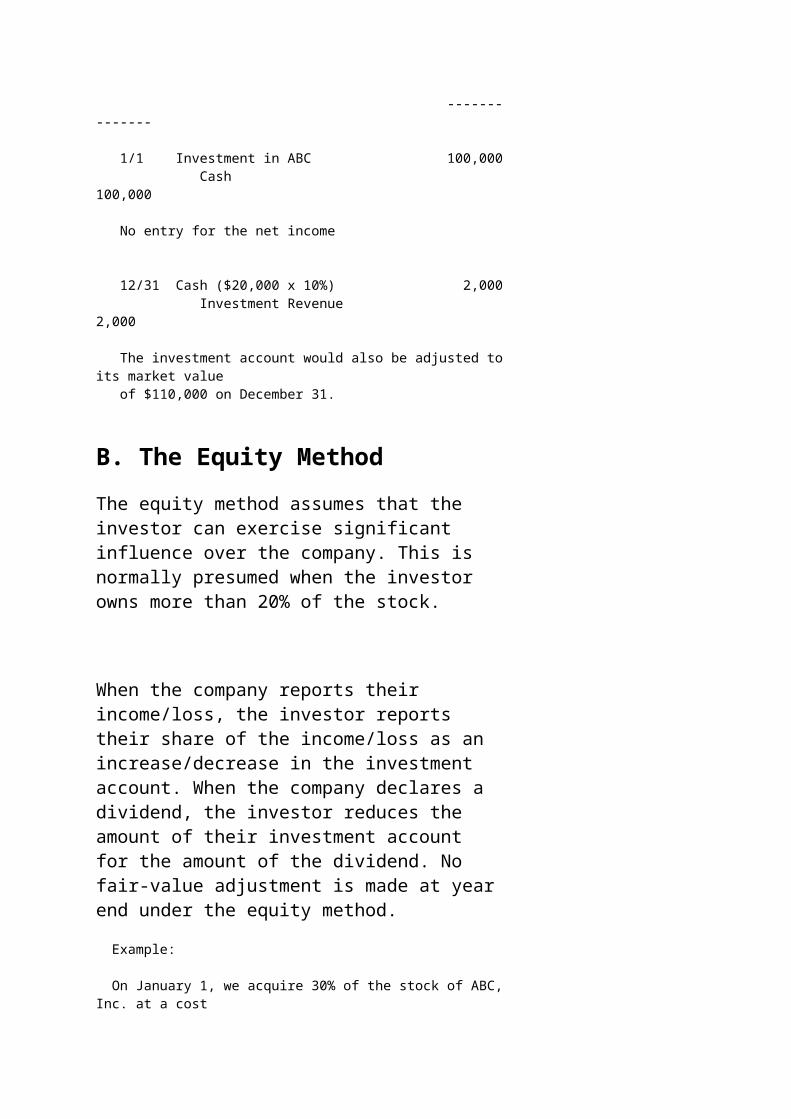

Debit Credit

--------------

1/1 Investment in ABC 100,000 Cash 100,000

No entry for the net income

12/31 Cash ($20,000 x 10%) 2,000 Investment Revenue 2,000

The investment account would also be adjusted toits market value of $110,000 on December 31.

B. The Equity MethodThe equity method assumes that the investor can exercise significant influence over the company. This is normally presumed when the investor owns more than 20% of the stock.

When the company reports their income/loss, the investor reports their share of the income/loss as an increase/decrease in the investment account. When the company declares a dividend, the investor reduces the amount of their investment account for the amount of the dividend. No fair-value adjustment is made at yearend under the equity method.

Example:

On January 1, we acquire 30% of the stock of ABC,Inc. at a cost

of $300,000. On December 31, ABC reports a net income of $40,000 and declares and pays a dividend of $20,000.

The following entries are required:

Debit Credit --------------

1/1 Investment in ABC 300,000 Cash 300,000

12/31 Investment in ABC ($40,000 x 30%) 12,000 Revenue from Investment 12,000

12/31 Cash ($20,000 x 30%) 6,000 Investment in ABC 6,000

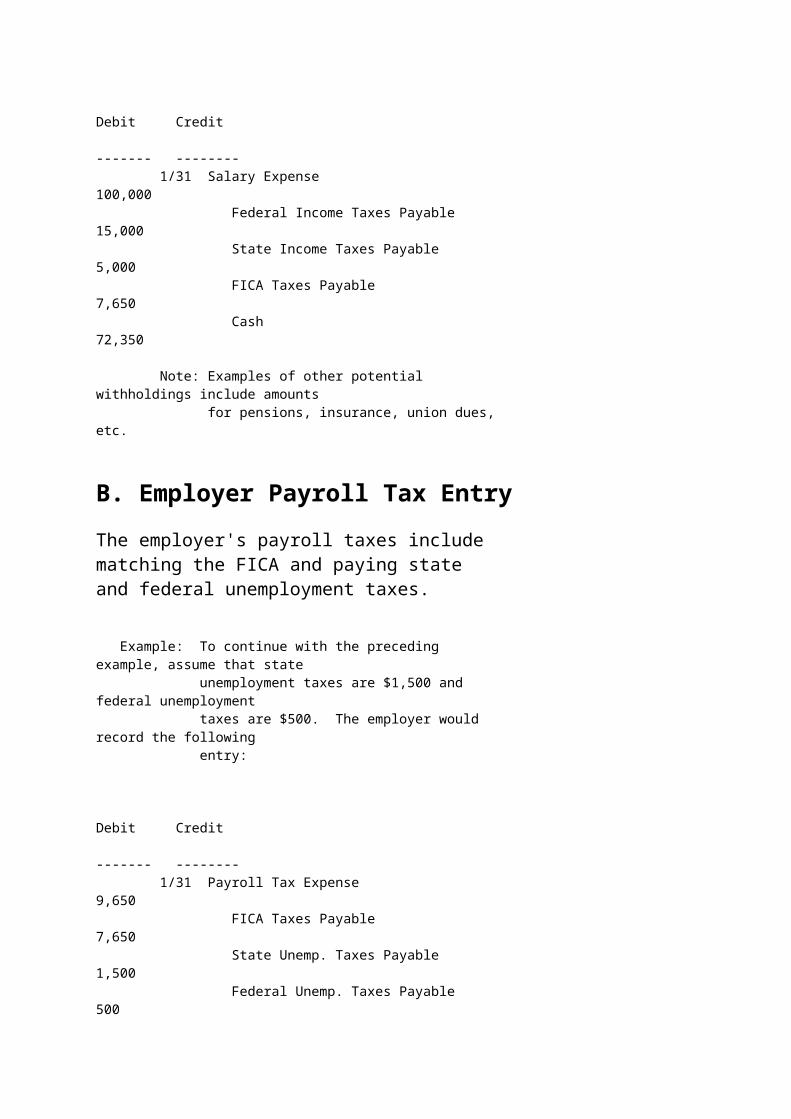

Journal Entries for PayrollEmployers record two basic types of payroll entries: paying the employees(payroll entry) and paying the employer payroll taxes (employer payroll tax entry).

A. Payroll Entry

Example: Employees earn $100,000 for the month,and are paid on January 31. The employer withholdsthe following:

Federal Income Taxes $15,000 State Income Taxes $ 5,000 FICA Taxes $ 7,650

After withholdings, the employees' net pay was $72,350.

Debit Credit ------- -------- 1/31 Salary Expense 100,000 Federal Income Taxes Payable 15,000 State Income Taxes Payable 5,000 FICA Taxes Payable 7,650 Cash 72,350

Note: Examples of other potential withholdings include amounts for pensions, insurance, union dues, etc.

B. Employer Payroll Tax EntryThe employer's payroll taxes include matching the FICA and paying state and federal unemployment taxes.

Example: To continue with the preceding example, assume that state unemployment taxes are $1,500 and federal unemployment taxes are $500. The employer would record the following entry:

Debit Credit ------- -------- 1/31 Payroll Tax Expense 9,650 FICA Taxes Payable 7,650 State Unemp. Taxes Payable 1,500 Federal Unemp. Taxes Payable 500

Note: The taxes will be remitted to variousgovernment agencies at a later date.

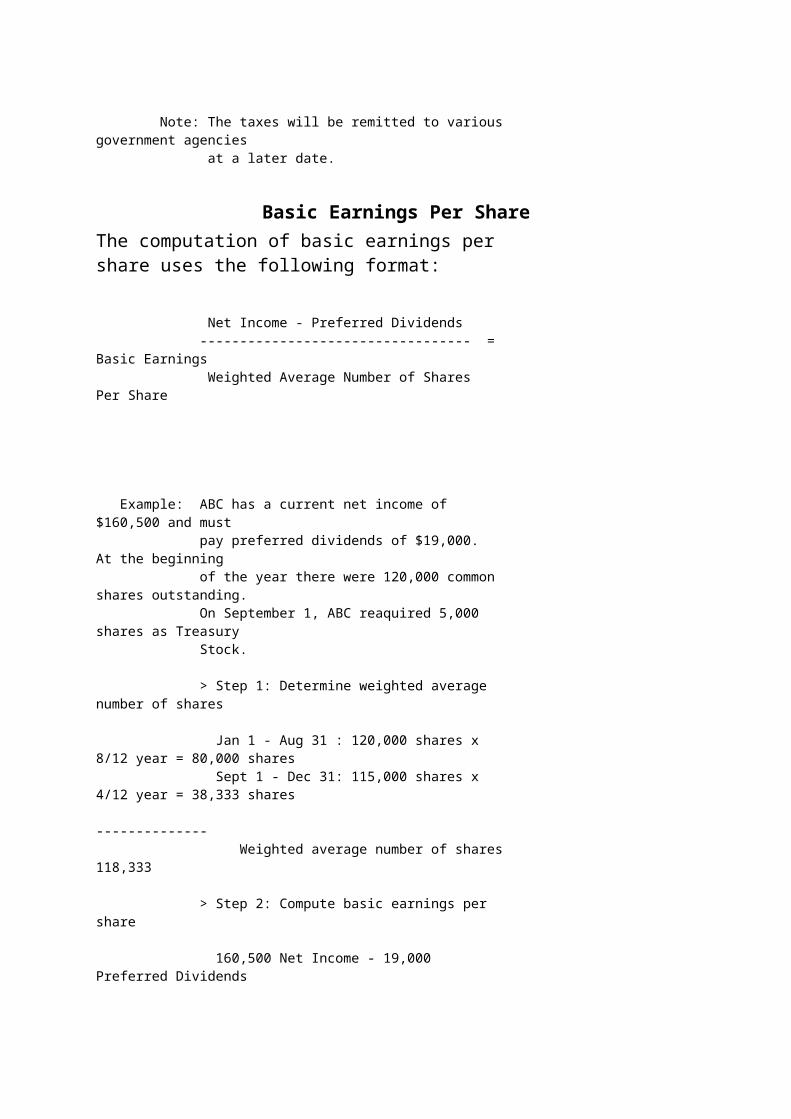

Basic Earnings Per ShareThe computation of basic earnings pershare uses the following format:

Net Income - Preferred Dividends ---------------------------------- = Basic Earnings Weighted Average Number of Shares Per Share

Example: ABC has a current net income of $160,500 and must pay preferred dividends of $19,000. At the beginning of the year there were 120,000 common shares outstanding. On September 1, ABC reaquired 5,000 shares as Treasury Stock.

> Step 1: Determine weighted average number of shares

Jan 1 - Aug 31 : 120,000 shares x 8/12 year = 80,000 shares Sept 1 - Dec 31: 115,000 shares x 4/12 year = 38,333 shares -------------- Weighted average number of shares118,333

> Step 2: Compute basic earnings per share

160,500 Net Income - 19,000 Preferred Dividends

----------------------------------------------- = 1.20 118,333 weighted average number of shares

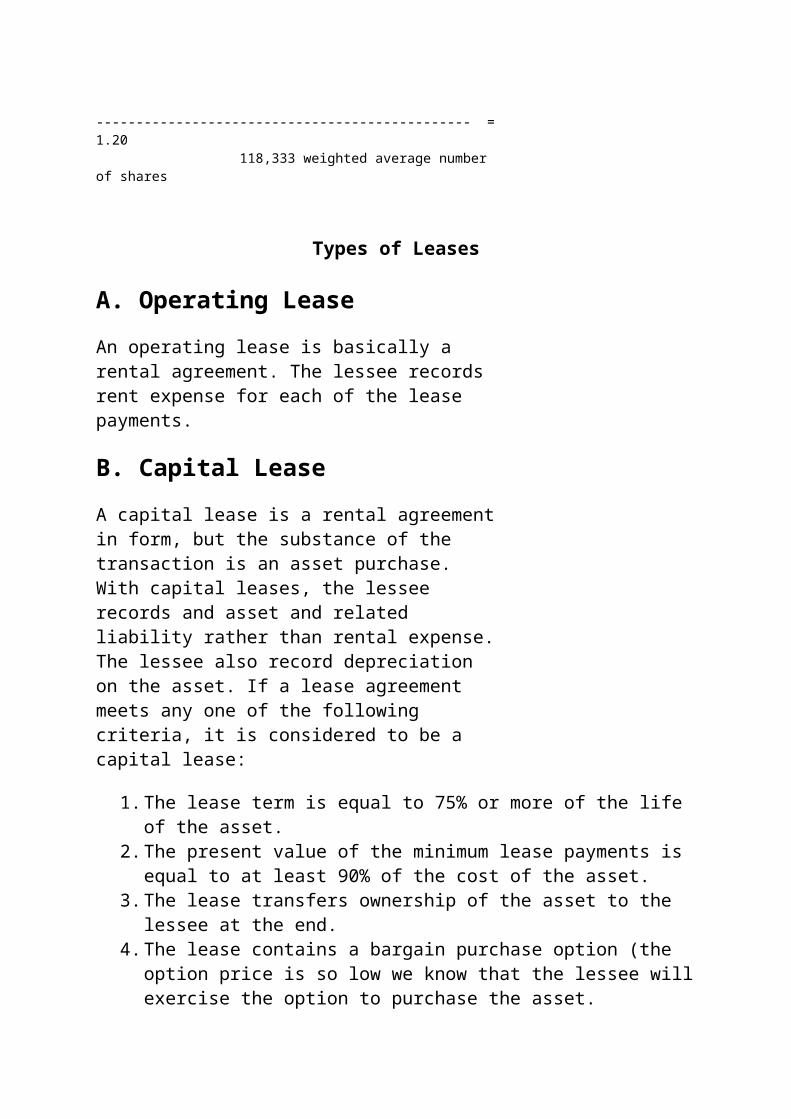

Types of Leases

A. Operating LeaseAn operating lease is basically a rental agreement. The lessee records rent expense for each of the lease payments.

B. Capital LeaseA capital lease is a rental agreementin form, but the substance of the transaction is an asset purchase. With capital leases, the lessee records and asset and related liability rather than rental expense.The lessee also record depreciation on the asset. If a lease agreement meets any one of the following criteria, it is considered to be a capital lease:

1.The lease term is equal to 75% or more of the life of the asset.

2.The present value of the minimum lease payments is equal to at least 90% of the cost of the asset.

3.The lease transfers ownership of the asset to the lessee at the end.

4.The lease contains a bargain purchase option (the option price is so low we know that the lessee willexercise the option to purchase the asset.

Adjusting Entries

Adjusting entries are journal entries that are used at the end of an accounting period to adjust the balances invarious general ledger accounts. These adjustments are made to more closely align the reported results and financial position of a business to meet the requirements of an accounting framework, such as GAAP or IFRS.This generally involves the matching of revenues to expenses under the matching principle, and so impacts reported revenue and expense levels.

The use of adjusting journal entries is a key part of the period closing processing, as noted in the accounting cycle, where you convert a preliminary trial balance into a final trial balance. It is usually not possible to create financial statements that are fully in compliance with accounting standards without the use of adjusting entries.

An adjusting entry can used for any type of accounting transaction; here are some of the more common ones:

To record depreciation and amortization for the period To record an allowance for doubtful accounts To record a reserve for obsolete inventory To record a reserve for sales returns To record the impairment of an asset To record a warranty reserve To record any accrued revenue To record previously billed but unearned revenue as a liability To record any accrued expenses To record any previously paid but unused expenditures as prepaid expenses To adjust cash balances for any reconciling items noted in the bank reconciliation

As shown in the preceding list, adjusting entries are most commonly of three types, which are:

Accruals. To record a revenue or expense that has not yet been recorded through a standard accounting transaction.

Deferrals. To defer a revenue or expense that has been recorded, but which has not yet been earned or used. Estimates. To estimate the amount of a reserve, such as the allowance for doubtful accounts or the inventory

obsolescence reserve.

When you record an accrual, deferral, or estimate journal entry, it usually impacts an asset or liability account. For example, if you accrue an expense, this also increases a liability account. Or, if you defer revenue recognition to a later period, this also increases a liability account. Thus, adjusting entries impact the balance sheet, not just the income statement.

Since adjusting entries so frequently involve accruals and deferrals, it is customary to set up these entries as reversing entries. This means that the computer system automatically creates an exactly oppositejournal entry at the beginning of the next accounting period. By doing so, the effect of an adjusting entryis eliminated when viewed over two accounting periods.

A company usually has a standard set of potential adjusting entries, for which it should evaluate the need at the end of every accounting period. You should have a list of these entries in the standard closing checklist. Also, consider constructing a journal entry template for each adjusting entry in the accounting software, so there is no need to reconstruct them every month.

Adjusting Entry Examples

Depreciation: Arnold Corporation records the $12,000 of depreciation associated with itsfixed assets duringthe month. The entry is:

Debit Credit

Depreciation expense 12,000

Accumulated depreciation 12,000

Allowance for bad debts: Arnold Corporation adds $5,000 to its allowance for doubtful accounts. The entry is:

Debit Credit

Bad debts expense 5,000

Allowance for doubtful accounts 5,000

Accrued revenue: Arnold Corporation accrues $50,000 of earned but unbilled revenue. The entry is:

Debit Credit

Accounts receivable - accrued 50,000

Sales 50,000

Billed but unearned revenue: Arnold Corporation bills a customer for $10,000, but has not yet earned the revenue, so it creates an adjusting entry to record the billed amount as a liability. The entry is:

Debit Credit

Sales 10,000

Unearned sales (liability) 10,000

Accrued expenses: A supplier is late in sending Arnold Corporation a materials-related invoice for $22,000,so the company accrues the expense. The entry is:

Debit Credit

Cost of goods sold (expense) 22,000

Accrued expenses (liability) 22,000

Prepaid assets: Arnold Corporation pays $30,000 toward the next month's rent. The company records this as aprepaid expense. The entry is:

Debit Credit

Prepaid expenses (asset) 30,000

Rent expense 30,000

Month-End Activities

Month-end activities can be done at any time after the last entries of the month have been completed. The system is smart enough to allow you to generate all thereports excluding the current month. This way you can continue working and generate the month-end reports when it is convenient.

Generating Late ChargesOnce all the activity for the month has been completed,you can generate late charges as follows:

1.Complete all billings for the day so that there areno open charges.

2.Run pre-billing report turning on the feature to apply late charges for the time period you have chosen: 30 or later, 60 days or later or 90 days.

3.A list of all customer sites who will receive a late charge will be generated.

4.You can now print a late charge invoice, or post itand have the charge appear on the customer statement. (make sure you date the posted late charges within the month you are sending statementsso the charge is included).

5.Done.

Customer StatementTAC supports various statement types for you to choose from:

1.Standard statement of open invoices and site balances.

2.Customer statement that is for multiple sites.3.Cardex statement that lists charges for the current

period and balance for the site.

Fuel by MonthYou can use the material tracking system to track orders and receipts of fuel by vendor. You can run the material usage report by vendor to verify the gross receipts of fuel.

Delivery Ticket ControlPress the F4 button and select schedule date range fromstart of year to end of week and select only open tickets (work orders). This should create an empty list, if not, then a work order has been created and not converted to an invoice. Check with your drivers for a missing ticket.

Sales ReconciliationSales reconciliation reports print out the reported sales for the selected time period. Two of the most popular are 1) market type 2) state and county for sales tax reporting. There are several other alternatives including

Sales source Sales credit Accounting codes Sales code Invoice listing Customer codes Unit type Invoice date range

You do not have to close out one month to start another, and all the reports can be exported to Excel so you can import them into an accounting system of your choice.

Cash ReconciliationCash reconciliation reports print out the reported receivables for the selected time period. Two of the most popular are 1) market type 2) state and county forsales tax reporting. There are several other alternatives, including payment credit listing.

You do not have to close out one month to start another, and all the reports can be exported to Excel so you can import them into an accounting system of your choice.