Embed Size (px)

Citation preview

A

STUDY

ON

FOOD AND DAIRY INDUSTRY

Management Research Project -I

Submitted

In the partial fulfillment of the Degree of

Master of Business Administration

Semester-III

By

Name Exam No.

Shikha Modi 12044311052 Vishal Patel 12044311119 Priyanka Prajapati 12044311131 Zalak Prajapati 12044311133 Dhara Shah 12044311146 Vishesh Shah 12044311147

Under the Guidance of:

Prof. (Dr.) Mahendra Sharma

Prof. & Head,

V. M. Patel Institute of Management.

&

Prof Harsha Jariwala, Asst. Professor

Prof. Abhishek Parikh, Asst. Professor

V. M. Patel Institute of Management.

Submitted To:

V. M. Patel Institute of Management,

Ganpat University,

Kherva.

(2013)

i

CERTIFICATE BY THE GUIDE

This is to certify that the contents of this report entitled “Food And Dairy Industry” by

ShikhaMod(12044311052),VishalPatel(12044311119),PriyankaPrajapati(12044311131),Zala

kPrajapati(12044311133),DharaShah (12044311146),Vishesh Shah (12044311147)submitted

to V. M. Patel Institute of Management for the Award of Master of Business Administration

(MBA Semester -III) is original research work carried out by them under my supervision.

This report has not been submitted either partly or fully to any other University or Institute

for award of any degree or diploma.

Prof. (Dr.) Mahendra Sharma,

(Professor & Head)

V. M. Patel Institute Of Management,

Ganpat University.

Date:

Place: Kherva

ii

CANDIDATE’S STATEMENT

We hereby declare that the work incorporated in this report entitled “Food And Dairy

Industry” in partial fulfillment of the requirements for the award of Master of Business

Administration (Semester - III ) is the outcome of original study undertaken by us and it has

not been submitted earlier to any other University or Institution for the award of any Degree

or Diploma.

Date:

Place: Kherva

Shikha Modi

Vishal Patel

Priyanka Prajapati

Zalak Prajapati

Dhara Shah

Vishesh Shah

iii

PREFACE

Industrial activity plays an important role in economic development of our country. The

knowledge of present market scenario is very much essential and keeping that in view, our

college gave us a very good opportunity of industrial interaction in terms

of Management Research Project-I.

As a part of Our Academic requirement of MBA program, we have selected FOOD AND

DAIRY INDUSTRYas the industry to be analyzed under the subject named MRP-1. The

reason to choose Food and Dairy Industry is very obvious. One, that industry has very

interesting history and background. It is concerned with basic Infrastructure development as

well as continuous changing advanced technology. Secondly, it has opportunistic future and

directly impact on economy. Industry has a very rich area of analyzing. Through this kind of

Industry Analysis we can have good exercise of learning and also help us to understand

current trend of industry with its all-possible dimensions.

The report covers all the landmark changes in Dairy industry and competitive markets being

driven by globalization. It would also provide you the idea of analyzing, crafting,

formulating, evaluating, implementing and executing business strategies related to the Food

and DairyIndustry in today’s volatile markets.

iv

ACKNOWLEDGEMENT

We would like to take this opportunity, to express our most sincere gratitude to Dr.

Mahendra Sharma Professor & Head, V.M.Patel institute of management for his assistant to

give chance for prepare MRP-I reports.

We would also like to thanks to Ms. HarshaJariwalafor her assistant and support without

which this project would not successfully completed. She provides us all necessary guidance.

We are heartily thankful Mr. Abhishek K Parikhfor them support in preparing this report.

We would also like to thanks to all faculty members of V.M. Patel Institute of Management,

Ganpat University. Kherva, Mehsana.

v

EXECUTIVE SUMMERY Objective of the Study:

The project is taken with an objective to analyze various product offered by Food andDairy

industry provider and to study Food and Dairy industry in depth .To know the functioning of

Food and Dairy industry in Gujarat.To analyze the Food and Dairy industry, taking in to

accounts the intensity of competition amongst the companies. To do the comparative

assessment of selected dairies based on various perimeter current ratios, Inventory turnover

ratio,Debt equity ratio for analyzing Food and Dairy industry in Gujarat.

Through the presence of such industries, a wider range of food products could be sold and

distributed to the distant locations. The term 'food and dairy' is mainly defined as a process of

value addition to the agricultural or horticultural produce by various methods like grading,

sorting and packaging.Benefits of food and dairy include toxin removal, preservation, easing

marketing and distribution tasks, and increasing food consistency. In addition, it increases

seasonal availability of many foods, enables transportation of delicate perishable foods across

long distances and makes many kinds of foods safe to eat by de-activating spoilage and

pathogenic micro-organisms.The industry is becoming increasingly automated, and is

therefore seeing labour costs decline. The advantages of food and dairy include greater food

consistency, longer shelf life, removal of toxins, reduction of food borne diseases and cheaper

food. The global fresh meat market is expected to produce 300 million tons by 2015. A rising

global population and extensive urbanization are driving forces for the market.

The company has also introduced the major areas like Nestle India Limited, Cadbury India

Limited, Jubilant Food works Limited, Britannia Industries Limited, GlaxoSmithKline

Consumer healthcare Limited.

In strategic analysis we include Economic Features, Porter’s five force model, Driving Force

Model, Strategy Group Mapping, PEST Analyses, SWOT Analysis.

Financial analysis is an assessment of the effectiveness with which are employed in a firm,

efficiency and profitability of its operations, andvalue and safety of debtors' claims against

the firm'sassets. We also analyze Ratio Analysis and Trend analysis.

CONTENTS

Sr No. Particular Page No.

Certificate by the Guide i

Candidate’s Statement ii Preface iii Acknowledgement iv Executive Summary v Chap 1 INTRODUCTION OF THE INDUSTRY 1 1.1 Introduction 2 1.2 History Of Food And Dairy Industry 7 1.3 Global Food And Dairy Industry 10 1.4 Food And Dairy Industry In India 12 Chap 2 MAJOR PLAYERS OF THE INDUSTRY 17 2.1 Net Profit Based Major Players Of The Industry 18 Chap 3 STRATEGIC ANALYSIS 32 3.1 Introduction 33 3.2 Economic features 34 3.3 Porter’s five force model 37 3.4 Driving force 40 3.5 Strategic group mapping 42 3.6 PEST analysis 45 3.7 SWOT analysis 48 3.8 Key factors for future competitive analysis success 51 3.9 Product life cycle (PLC) 53 3.10 Conclusion 59 Chap 4 FINANCIAL ANALYSIS 60 4.1 Objective of the financial analysis 61 4.2 Ratio Analysis 63 4.3 Trend analysis 74 Chap 5 BUSINESS PLAN 78 5.1 Project at a glance 79 5.2 Company description 80 5.3 Selection of location 81 5.4 Industry and competitive analysis 83 5.5 Market and sales strategy 84 5.6 Operation, management and organization 85 5.7 Financial analysis 86 Chap 6 FINDINGS &CONCLUSION 89 6.1 FINDINGS

6.2 CONCLUSION 90 92

BIBLIOGRAPHY 93 ANNEXURE 94

1

CHAPTER 1

INTRODUCTION TO INDUSTRY

1.1 Introduction

1.1.1 Major Areas

1.1.2 Benefits Of Food and Dairy Industry

1.1.3 Food and Dairy Nutshell

1.2 History Of Food And Dairy Industry

1.2.1 History of Food Laws

1.3 Global Food And Dairy Industry

1.4 Food And Dairy Industry In India

1.4.1 Key Growth Drivers Of Food And Dairy Sector In India

1.4.2 Key Opportunities In Food and Dairy Sector

1.4.3 Challenges Faced By The Industry

2

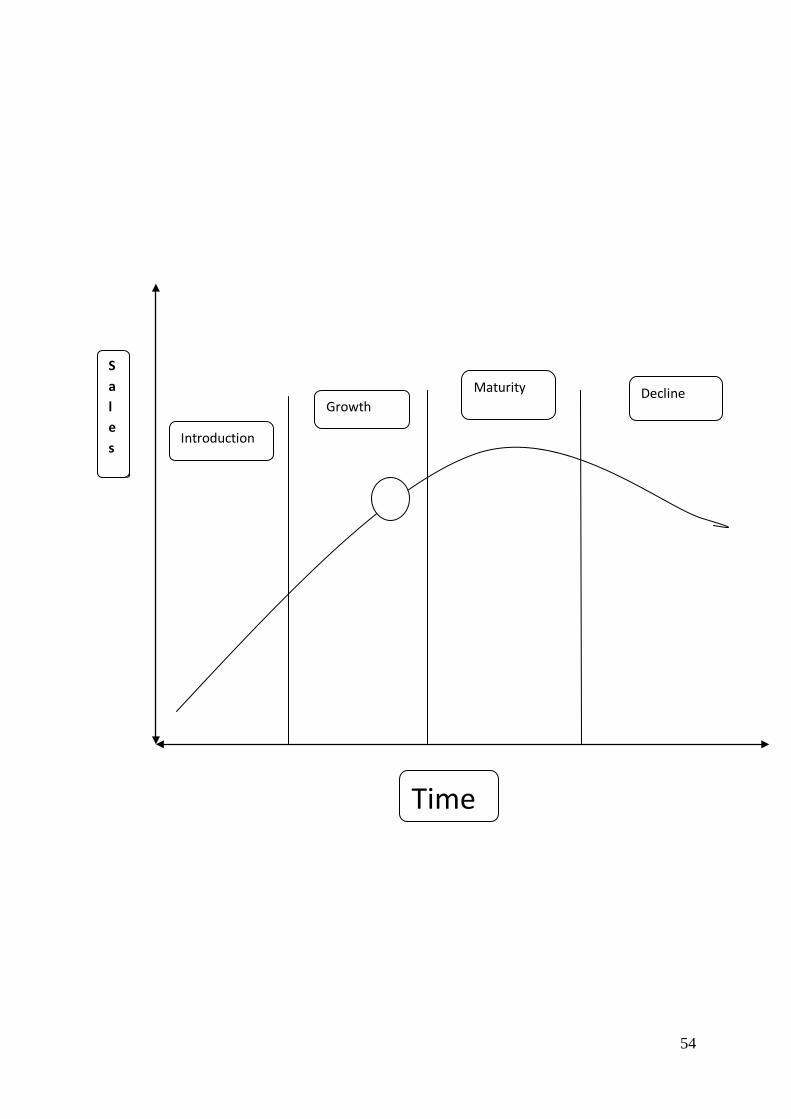

1. 1 INTRODUCTION

Food and dairy sector is indispensable for the overall development of an economy as it

provides a vital linkage and synergy between the agriculture and industry. It helps to

diversify and commercialise farming; enhance income of farmers; create markets for

export of agro foods as well as generate greater employment opportunities.

Through the presence of such industries, a wider range of food products could be sold

and distributed to the distant locations. The term 'food and dairy' is mainly defined as a

process of value addition to the agricultural or horticultural produce by various methods

like grading, sorting and packaging. In other words, it is a technique of manufacturing

and preserving food substances in an effective manner with a view to enhance their shelf

life; improve quality as well as make them functionally more useful. It covers spectrum

of products from sub-sectors comprising agriculture, horticulture, plantation, animal

husbandry and fisheries.

Food and dairy industry is one of the largest industry in India and is ranked 5th in terms

of production, consumption and export. Earlier, food and dairy industry was largely

confined to the food preservation, packaging and transportation, which mainly involved

salting, curdling, drying, pickling, etc. However, over the years, with emerging new

markets and technologies, the sector has widened its scope. It has started producing many

new items like ready-to-eat food, beverages, processed and frozen fruit and vegetable

products, marine and meat products, etc. It also includes establishment of post-harvest

infrastructure for processing of various food items like cold storage facilities, food parks,

packaging centres, value added centres, irradiation facilities and modernised abattoir.

The food and dairy sector comprises of two segments- Primary processed food and Value

added food. Primary segment comprises of packaged fruit and vegetables, milk, flour,

rice, spices etc. and constitutes around 62% in value terms of the processed foods. Value

added segment includes processed fruits and vegetables, juices, jam &jelly etc and holds

around 38% share in the total processed food.

3

In an emerging country like India, where growth with equity is a primary policy thrust,

the optimum development of the food and dairy sector will contribute significantly in

tackling several developmental concerns such as disguised unemployment in agriculture,

rural poverty, food security, food inflation, improved nutrition, prevention of wastage of

food etc. By serving as a bridge between agriculture and manufacturing and by dealing

with a basic need of all Indian citizens – the assured supply of healthy and affordable

food at all locations in the country, this sector has the potential to be a major driver in

India‘s growth in the coming years. In fact the food and dairy sector has been growing

faster than the agriculture sector.

The food and dairy industry includes a diverse group of companies involved in the

processing of products like fish, meat, milk, crops and water. It includes millions of

Small & Medium Enterprises (SMEs) worldwide and also some of the largest companies

in the world. Many of these companies deliver products directly to consumers, while

others specialize in Business-to-Business activities (ingredients, commodity markets).

Some companies directly participate in all areas of food production, from farming

activities through to final production and retail. Others are concentrated more at the top

end of the production chain or buy through commodity markets.

In fact, Food and dairy one of the world‘s largest industries from the perspective of the

number of companies involved in the sector, as well as in terms of its total economic

value.

4

1.1.1 Major Areas

The sector comprises of the following major areas –

Fruits & Vegetables

Beverages, Juices, Concentrates, Pulps, Slices, Frozen & Dehydrated products,

Wine Potato Wafers/Chips etc.

Fisheries

Frozen & Canned products mainly in fresh form

Meat & Poultry

Frozen and packed mainly in fresh form, Egg Powder

Milk & Dairy

Whole Milk Powder, Skimmed milk powder, Condensed milk, Ice cream, Butter

and Ghee

Grain and Cereals

Flour, Bakeries, Biscuits, Starch Glucose, Cornflakes, Malted Foods, Vermicelli,

Pasta Foods, Beer and Malt extracts, Grain based Alcohol.

Consumer Industry

Chocolates, Confectionery, Soft/Aerated Beverages/Drinks

Plantation

Tea, coffee, cashew, cocoa, coconut etc

5

1.1.2. Benefits of Food and dairy industry

Benefits of food and dairy include toxin removal, preservation, easing marketing and

distribution tasks, and increasing food consistency. In addition, it increases seasonal

availability of many foods, enables transportation of delicate perishable foods across long

distances and makes many kinds of foods safe to eat by de-activating spoilage and

pathogenic micro-organisms. Modern supermarkets would not exist without modern food

and dairy techniques, long voyages would not be possible and military campaigns would

be significantly more difficult and costly to execute. Processed foods are usually less

susceptible to early spoilage than fresh foods and are better suited for long distance

transportation from the source to the consumer. When they were first introduced, some

processed foods helped to alleviate food shortages and improved the overall nutrition of

populations as it made many new foods available to the masses. Modern food and dairy

product also improves the quality of life for people with allergies, diabetics, and other

people who cannot consume some common food elements. Food and dairy products can

also add extra nutrients such as vitamins.

The significant benefits for different stakeholders involved in food and dairy are:

Farmer – higher yield, better farm realization, lower risk

Consumer – greater variety, lower prices, new products

Companies – new business opportunities, demand growth

Economy/Government – Employment generation, reduced rural migration

6

1.1.3 Food and dairy in a nutshell

There are different stages of processing of food as depicted hereunder –

• Agriculture

• Food processing

• Transport

• Retailing

• Consumption

• Waste

Primary Processing relates to conversion of raw agricultural produce, milk, meat and fish

into a commodity that is fit for human consumption. It involves steps such as cleaning,

grading, sorting, packing etc. Food and dairy Industries usually deal with higher levels of

processing where new or higher value food products are manufactured.

7

1.2. HISTORY OF FOOD AND DAIRY INDUSTRY

Food and dairy dates back to the prehistoric ages when crude processing incorporated

slaughtering, fermenting, sun drying, preserving with salt, and various types of cooking

(such as roasting, smoking, steaming, and oven baking). Salt preservation was especially

common for foods that constituted warrior and sailors' diets, until the introduction of

canning methods.

Evidence for the existence of these methods can be found in the writings of the ancient

Greek, Chaldean, Egyptian and Roman civilizations as well as archaeological evidence

from Europe, North and South America and Asia. These tried and tested processing

techniques remained essentially the same until the advent of the industrial revolution.

Examples of ready-meals also exist from preindustrial revolution times such as the

Cornish pasty and Haggis. During ancient times and today these are considered

processing foods. Food and dairy products has also helped create quick, nutritious meals

to give to busy families.

Modern food and dairy production technology in the 19th and 20th century was largely

developed to serve military needs. In 1809 Nicolas Apart invented a vacuum bottling

technique that would supply food for French troops, and this contributed to the

development of tinning and then canning by Peter Durand in 1810. Although initially

expensive and somewhat hazardous due to the lead used in cans, canned goods would

later become a staple around the world. Pasteurization, discovered by Louis Pasteur in

1862, was a significant advance in ensuring the micro-biological safety of food.

In the 20th century, World War II, the space race and the rising consumer society in

developed countries (including the United States) contributed to the growth of food and

dairy with such advances as spray drying, juice concentrates, freeze drying and the

introduction of artificial sweeteners, colouring agents, and preservatives such as sodium

benzoate. In the late 20th century products such as dried instant soups, reconstituted

fruits and juices, and self cooking meals such as MRE (Meal Ready-to-Eat) food ration

were developed.

8

In Western Europe and North America, the second half of the 20th century witnessed a

rise in the pursuit of convenience. Food and dairy companies marketed their products

especially towards middle-class working wives and mothers. Frozen foods (often credited

to Clarence Birdseye) found their success in sales of juice concentrates and "TV dinners".

Processors utilised the perceived value of time to appeal to the post-war population, and

this same appeal contributes to the success of convenience foods today.

9

1.2.1 History of Food laws

Food laws were among the earliest of enactments known to man. Governments over

many centuries have endeavoured to provide for the safety and wholesomeness of man‘s

food by legal provisions and appropriate punitive action. Over the years also, rude forms

of fraud, such as adding worthless substances to food or extracting valuable constituents

from it, have been followed by sophisticated methods of adulteration more difficult to

detect. The birth of modern chemistry in the early nineteenth century made possible the

production of materials possessing properties similar to normal foods which, when

fraudulently used, did not readily attract the attention of the unsuspecting purchaser.

Later, better analytical methods were used in food control work to detect adulterants.

When scientists demonstrated that some adulterants were dangerous to health, the

aroused public demanded laws that would both protect their health and prevent fraud.

―Food Laws‖ in one form or another, such as religious tenets or prohibitions, were

inherent in all ancient civilizations and have come down to us from early times. It was

not until the late nineteenth and early twentieth century — with the urbanization of

societies and the depopulation of rural areas—that food laws, as understood today, were

prepared. This process was hastened by pressure that developed as the public rebelled

against the generally unhygienic conditions of the period.

Since the end of World War II, there have been major changes in the food and dairy

industry, and this development continues today; at the same time, our knowledge of the

risks, actual and potential, has considerably increased. Reorientation and further

consolidation of food laws have therefore become necessary to protect the health of the

consumer from the many new risks to which he has become exposed and over which he

has little personal control.

10

1.3 GLOBAL FOOD AND DAIRY INDUSTRY

The Global Processed Food and dairy Industry is valued at US $ 3.2 trillion and accounts

for over 3/4th of global food sales. Despite the large size of the industry, only 6% of the

processed food is traded the world over as compared to bulk agricultural commodities

where 16% of produce is traded. Growth of the sector has been the highest in developed

economies, especially across Western Europe, North America, Japan and Australia. USA

is the single largest consumer of processed food and accounts for 31% of global sales.

The food and dairy sector has seen substantial growth in developing economies with

increase in GDP, per capita income and the resultant changes in lifestyle. Organized

retailing and availability of better processing technologies too have contributed to the

accelerated growth of the sector.

The food and dairy industry is characterized by intense competition, with the most

reliable firms performing well by focusing on efficiency in terms of fast processing and

distribution. The global economic recession had less effect on the food processing

industry than other industries due to rising demand for pre-packaged food.

The industry is becoming increasingly automated, and is therefore seeing labour costs

decline. The advantages of food and dairy include greater food consistency, longer shelf

life, removal of toxins, reduction of food borne diseases and cheaper food. The global

fresh meat market is expected to produce 300 million tons by 2015. A rising global

population and extensive urbanization are driving forces for the market.

Asia-Pacific demand is growing in tandem with disposable incomes and meat

consumption. Asia-Pacific leads the food and dairy industry in terms of market share.

Market growth in countries in Eastern Europe and Asia-Pacific continues as developing

countries enjoy a more favourable economic climate, with larger disposable incomes and

improved living standards. Demand for food that is light on preparation time continues to

grow in developed countries. Germany, The US, France and Austria are among the major

exporters of food processing machinery while the US, the UK, Germany and France lead

11

in importing. China‘s processed food industry is expected to continue showing close to

35% yearly growth from 2010 through 2013, mainly due to higher standards of living and

improved economic conditions. China‘s processed food market was left relatively

unscathed by the economic downturn. Growth will continue to be lead by meat

processing, with a forecast yearly growth of more than 15% for the next few years. Other

leading food market segments in China are dairy products and ready meals. Growth will

likely continue as China‘s 25% rate of processed food production catches up with the

average 80% rate in developed nations such as the US.

The main driving force behind the global food industry is technological innovation,

which concentrates on satisfying consumer demand for more tastes and easy-

topreparefoods. Companies are focusing on innovation to boost profits, with 60% of large

companies and over 40% of medium sized enterprises investing in process and product

innovation. Over 99% of the EU food and beverage industry is comprised of small-and-

medium-sized enterprises. Danish, French and Greek food and dairy companies dedicate

a sizeable part of their profit to research and development, while other countries such as

Austria, Hungary and the Czech Republic lag further behind. The main aims of research

and development within the food and dairy industry are better quality food, enhanced

taste, cheaper prices and greater convenience. Other industries recruited in the process

include nanotechnology, biotechnology and other advanced information technology

fields. Companies cut production costs by: reducing waste; employing effective

manufacturing techniques used in other industries; optimizing automation to cut back on

labor costs; and finding ways to cut down on input materials such as energy.

12

1.4 FOOD AND DAIRY INDUSTRY IN INDIA

The Indian food and dairy industry stands at $135 billion and is estimated to grow with a

CAGR of 10 per cent to reach $200 billion by 2015. The food and dairy industry

contributed 7% to India‘s GDP. The industry employs around 13 million workers directly

and about 35 million indirectly. The industry is segmented into sectors namely, milk and

allied products (dairy), meat and poultry, seafood, bakery and confectionery, fruit and

vegetables, grain, pulses and oilseeds (staple) products, alcoholic and non-alcoholic

products (beverages), and packaged foods. The classification is not distinct as many

processed products overlap different segments.

India ranks No. 1 in the world in production of Milk (Fresh, whole, buffalo), Pulses,

Ginger, Chick Peas, Bananas Guavas, Papayas and Mangoes. Further, India ranks No. 2

in the world in production of Rice, Wheat, Potatoes, Garlic, Cashew Nuts, Groundnuts,

Dry Onion, Green Peas, Pumpkins, Gourds, and cauliflowers. With the huge production

base India can easily become the leading food supplier to the world and at the same time

serving its vast growing domestic market with over a billion people.

Investments in the registered food and dairy units have been growing in the recent years.

In 2007-08 the fixed capital of registered food and dairy units have increased by 18.93%

over the previous year. Food and dairy industry in India is increasingly seen as a potential

source for driving rural economy as it brings synergy between industry and agriculture.

A developed food and dairy industry is expected to lead increase in farm gate prices

translating into increased rural incomes, reduce wastages, ensure value addition, promote

crop diversification, generate employment opportunities as well as export earnings. With

such a large and diversified production base coupled with low manpower cost and

modern technology, the Indian food processing sector is poised for growth, if the

advantages are leveraged optimally.

The growth is driven by the fact that the central government has given a priority status to

all agro-processing businesses. Government incentives in the field of mega food parks,

cold chain and exports benefits are also playing an important role in promoting food and

dairy.

13

The major challenges are investments at different points of the supply and value chain,

proper research, farm and lab connectivity, up gradation of technology, increase in farm

holding, skill and manpower training, backend and front-end integration and cold chain

integration.

The opportunities in the food and dairy industry are vast. However, there is a need to

improve technology and productivity to be competitive globally. As the economy grows,

the food and dairy industry will offer bigger opportunities to the new as well as the

existing players.

India has the second largest arable land of 161 million hectares and has the highest

acreage under irrigation. Next to China, India ranks second largest food producer in the

world and has the potential to immerge the biggest with its food and agricultural sector.

India accounts for less than 1.5% of international food trade despite being one of the

world‘s major food producers, which indicates huge potential for both investors and

exporters.

Advantage India

India is one of the largest food producers in the world.

India has diverse agro-climatic conditions and has a large and diverse raw

material base suitable for food processing companies.

India is looking for investment in infrastructure, packaging and marketing.

India has huge scientific and research talent pool.

Well developed infrastructure and distribution network.

Rapid urbanization, increased literacy, changing life style, increased number of

women in workforce, rising per capita income leading to rapid growth and new

opportunities in food and beverages sector.

50 per cent of household expenditure by Indians is on food items.

Strategic geographic location (proximity of India to markets in Europe and Far

East, South East and West Asia).

14

1.4.1 Key growth drivers of Food and dairy Sector in India

Increasing spending on health and nutritional foods.

Increasing number of nuclear families and working women

Changing lifestyle

Functional foods, fresh or processed foods

Organized retail and private label penetration

Changing demographics and rising disposable incomes

15

1.4.2 Key opportunities in Food and dairy Sector

Processable varieties of crop

Contract farming

Investments in infrastructure through Public Private partnership (PPP)

Mega Food parks

Logistics and cold chain infrastructure

Food safety Management Systems

Machinery and packaging

16

1.4.3 Challenges faced by the industry

High level of wastage of agricultural produces is primarily on account of the inherent

disadvantages faced by the sector. This sector is characterized by preponderance of small

farmers, small scale & tiny processors, outdated technology, poor infrastructure and a

maze of middle men. Therefore, this sector needs support in terms of creation and

strengthening of infrastructure which individual farmers and processors will not be in a

position to create and sustain. Further, there is also a need for strengthening R&D

activities in food and dairy sector for innovation of technology which suits local needs,

popularization of appropriate technology, skill development and creation of an

institutional framework supportive of the industry. The major challenges facing the sector

are illustrated below:

17

CHAPTER 2

MAJOR PLAYERS OF

THE INDUSTRY

2.1 Net Profit Based Major Players Of The Industry

2.1.1 Nestle India Limited

2.1.2 Jubliant Food works Limited

2.1.3 Britannia Industry Limited

2.1.4 Cadbury India Limited

2.1.5 Glaxosmithkline Consumer Healthcare Limited

18

2.1 NET PROFIT BASED MAJOR PLAYER OF INDUSTRY

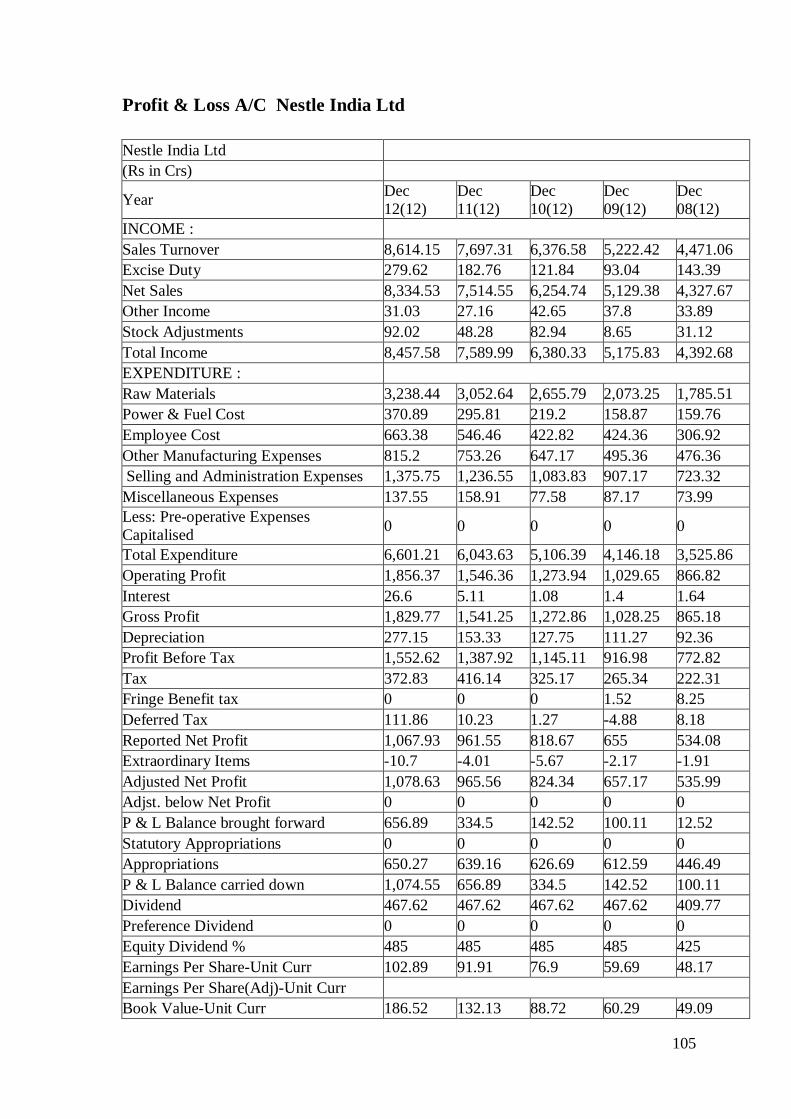

2.1.1 Nestle India Ltd.

Nestle India Ltd, one the biggest players in FMCG segment, has a presence in milk &

nutrition, beverages, prepared dishes & cooking aids & chocolate & confectionery

segments. The company is engaged in the food business. The food business incorporates

product groups, such as milk products and nutrition, beverages, prepared dishes and

cooking aids, chocolates and confectionery. Nestle India manufactures products under

brand names, such as Nescafe, Maggi, Milky bar, Milo, Kit Kat, Bar-One, Milkmaid and

Nestea.

The company has also introduced products of daily consumption and use, such as Nestle

Milk, Nestle Slim Milk, Nestle Fresh 'n' Natural Dahi and Nestle Jeera Raita. The

company's brands include milk products and nutrition, prepared dishes and cooking aids,

beverages, and chocolates and confectionery. Their milk products and nutrition includes

Nestle Everyday Dairy Whitener, Nestle Everyday Ghee, Nestle Milk, Nestle Slim Milk

and Nestle Dahi. Beverages Include Nescafe Classic, Nescafe Sunrise Premium, Nescafe

Sunrise Special and Nescafe Cappuccino. Nestle India is a subsidiary of Nestle S.A.

The company has presence across India with 7 manufacturing facilities and four branch

offices spread across the region. The four branch offices in the country help facilitate the

sales and marketing of its products. They are in Delhi, Mumbai, Chennai and Kolkata.

The company's head office is located in Gurgaon , Haryana.

Nestle India Ltd was incorporated in the year 1956. The company set up their first

production facility in the year 1961 at Moga in Punjab. In the year 1967, they set up their

second plant at Choladi in Tamil Nadu as a pilot plant to process the tea grown in the

area into soluble tea. In the year 1989, they set up a factory at Nanjangud in Karnataka.

In the year 1990, the company entered into the chocolate business by introducing Nestle

Premium Chocolate. In the year 1991, they entered in joint venture floated by the parent

in collaboration with BM Khaitan group to set up facilities to manufacturing a range of

Soya based products. In the year 1993, they set up a factory at Samalkha in Haryana. In

the year 1995, the company launched the company's worldwide legendary brand

chocolate, Kitkat.

19

The company commissioned two factories in Goa at Ponda and Bicholim in the year

1995 and 1997 respectively. In the year 1999, the company launched the product, Nestle

Growing Up Milk nationally. In April 2000, they forayed into the Ultra Heat Treated

(UHT) liquid milk market. In the year 2001, the company launched Nestle Pure Life

bottled water. Within few months, they again launched their second water brand-San

Pellegrino - in the Indian market. The company also made their foray into the iced tea

segment.

In the year 2004, a project has been initiated to upgrade the production technology for

infant nutrition products at the Samalkha factory. Nestle India Ltd recognised for its

outstanding performance in Exports by the Coffee Board of India in the Export Awards

2004-05 as the Best Exporter of Instant Coffee, Best Exporter to Russia & CIS Countries

(coffee) and Best Exporter for Far East Countries (coffee). The company bestowed the

UDYOG RATNA award by the PHD Chamber of Commerce and Industry to recognise

Nestle's significant contribution to the economic development of Punjab for the year

2005. The company set up a new department -the Channel & Category Sales

Development (CCSD) to develop new solutions for the various channels and customers

and improve the implementation of commercial plans in the market.

In the year 2006, the company set up their seventh factory at Pantnagar in Uttarakhand.

In the year 2007, CNBC Asia presented the company with the India Innovator of the year

award. The company's four factories were awarded the internationally recognised

external certification ISO 14001 for adherence to environmental processes and OSHAS

18001 for Health and Safety.

In the year 2008, the company launched Nestle Nesvita Pro-Heart Milk with Omega-3 in

Mumbai. Nestle Nesvita Pro-Heart is part of daily diet and has Omega-3 heart friendly

nutrients scientifically known to help manage cholestrol. As part of their ongoing

commitment to offering best in class nutrition products to Indian consumers, the

company launched NESTLE NAN 3, a follow-up formula for older infants.

During the year, MAGGI PICHKOO Tomato Ketchup was launched in a unique easy to

handle day pack to drive affordability, taste and convenience for a larger number of

20

consumers. The company also launched another pioneering product, MAGGI Bhuna

Masala, to cook tasty and healthy everyday meals, more conveniently. The company also

launched Nestle Kitkat Mini and Nestle Bar One Mini, at Rs 3 price to expand the

repertoire of offerings. Similarly, they launched Nestle Kitkat Chunky at Rs15 to

strengthen the range of wellness oriented Nestle products that consumers can choose

from. The company's three more factories were awarded the internationally recognized

external certification ISO 14001 for adherence to environmental processes and OSHAS

18001 for Health and Safety. With this, all the seven factories of the company now have

ISO 14001 and ISO 18001 certifications. In the year 2009, the company provided inputs

to the group R&D for development of an innovative product Maggi Bhuna Masala. They

launched Maggi Nutri-Licious Pazzta. During the year, Maggi further leveraged their

strengths to drive affordable nutrition and launched two new products, namely, Maggi

Rasile Chow and Maggi Masala-ae-Magic. They launched Nestle Kitkat in a new unique

single finger format and Nestle Much Guru pack at the higher price point.

The company acquired the Healthcare Nutrition business of Speciality Foods India Pvt

Ltd with effect from January 1, 2010. In the year 2010, the company expanded the

installed capacity of Milk Products and Nutrition by 3,983 MT to 147,546 MT. Also,

they increased the installed capacity of Prepared Dishes & Cooking aids by 14,028 MT to

205,017 MT.

In the year 2011, the company increased the installed capacity of Milk Products &

Nutrition by 14,561 MT to 162,107 MT, Prepared dishes & Cooking aids by 21,430 MT

to 226,447 MT and Chocolate & Confectionery by 3,283 MT to 36,052 MT.

21

1.2.2 Jubilant food works Limited

Jubilant Food works Ltd, a Jubilant Bhartia Group Company is a food service company.

The company offers a menu of quality pizza and side dishes to their customers. They

operate their stores pursuant to a Master Franchise Agreement with Domino's

International, which provides them with the exclusive right to develop and operate

Domino's pizza delivery stores and the associated trademarks in the operation of stores in

India, Nepal, Bangladesh and Sri Lanka. The pizza stores in Sri Lanka are operated by

their sub-franchisee, DP Lanka. There are currently five Domino's stores in Sri Lanka, all

in Colombo.

The company was the largest pizza chain in India and one of the fastest growing multi-

national fast food chains between 2006-2007 and 2008-2009, in terms of number of

stores. Their Domino's pizza stores in India are generally located in neighbourhood

markets in urban areas. They also operate pizza stores located in food courts in shopping

malls and in institutional campuses.

Jubilant Food works Ltd was incorporated on March 16, 1995 as a private limited

company with the name Domino's Pizza India Pvt Ltd. The company entered into a

master franchise agreement with Domino's International for north and west regions in

India.

In January 1996, the company opened their first Domino's pizza store. In September 14,

1996, the company was converted into a public limited company and the name was

changed to Domino's Pizza India Ltd. In the year 1998, they extended master franchise

agreement with Domino's International to whole of India and Nepal.

In the year 2001, the company made a tie-up with Hindustan Coca-Cola Beverages Pvt

Ltd. In the year 2003, they became the subsidiary of Jubilant Enpro Pvt Ltd. In the year

2004, they launched '30 minutes or free' campaign. In the year 2005, the company

entered into master franchise agreement for Sri Lanka and Bangladesh.

22

In the year 2009, the company launched 'Pizza Mania'. Also, they began to offer pasta

and choco lava cake to their customers as a side item. They opened 60 new stores during

the financial year 2008-09.

In September 17, 2009, the company entered into a trademark license agreement with

Domino's International whereby Domino's International conferred on the company a non-

exclusive right to use the trademarks and service marks ('Domino's Trademarks') in India.

In September 23, 2009, the company entered into an agreement with Domino's

International for the grant of the exclusive right and license to establish and operate a

commissary and to sell and distribute products using the know-how in the Territory and

the exclusive right and license to prepare, process and produce Products using the

technical knowledge in the Territory.

In September 24, 2009, the company changed their name from Domino's Pizza India Ltd

to Jubilant Foodworks Ltd. The company plans to open between 65 and 70 stores during

the financial year 2009-10, of which they opened 31 stores as of November 30, 2009 in

the existing cities.

As of November 30, 2009, the company operated 286 stores in India located in 22 states

and union territories, including in 59 cities across the country, and, through a sub-

franchisee, DP Lanka, five stores in Sri Lanka. As of November 30, 2009, we did not

operate any stores in Nepal and Bangladesh.

The company plans to expand their presence by entering into new cities and towns where

they currently have no operations. They plan to open new stores in cities and towns

which would be located within less than one day travel distance from their existing

commissaries in order to minimize additional capital expenditure and ensure quality

control.

Further, the company's Master Franchise Agreement with Domino's International

requires them to open 25 stores each, in 2011 and 2012 and they continue to evaluate

various new locations for further expansion. They are also exploring the possibility of

opening stores in the New Delhi and Mumbai airports on sub-franchise or sub-lease

basis.

23

2.1.3 Britannia Industry Limited.

Britannia Industries Limited (BIL) is a major player in the Indian Foods market with

leadership position in Bakery category. Its brand portfolio includes Tiger, Marie Gold,

Good Day, 50:50 and Treat. The Company was born in 21st March of the year 1918 as a

public limited company. The Company's plants are situated in Kolkata, Delhi, Chennai,

Mumbai and Uttarakhand. In 1921, it became the first company east of the Suez Canal to

use imported gas ovens. Britannia's business was flourishing. But, more importantly,

Britannia was acquiring a reputation for quality and value. As a result, during the tragic

World War II, the Government reposed its trust in Britannia by contracting it to supply

large quantities of 'service biscuits' to the armed forces.

A new factory was established in the year 1924 at Kasara Pier Road in Mumbai. In the

same year, the Company became a subsidiary of Peek, Frean & Company Limited, U.K.,

a leading biscuit manufacturing company, and further strengthened its position by

expanding the factories at Calcutta and Mumbai. In 1952, the Kolkata factory was shifted

from Dum Dum to spacious grounds at Taratola Road in the suburbs of Kolkata. During

the same year automatic plants were installed in Calcutta and later in 1954 the automatic

plants were installed in Mumbai plant, also in the same year the development of high

quality sliced and wrapped bread in India was initiated by the company and was first

manufactured at Delhi and a new bread bakery was set up at Delhi in the year 1965.

Britannia Biscuit Company takes over biscuit distribution from Parry's during the year

1975. In 1976, the company had introduced Britannia bread in Calcutta and Chennai.

During the year 1978, the company made Public issue, in that Indian shareholding

crossed 60%.

The Company re-christened from Britannia Biscuit Company Limited to Britannia

Industries Limited with effect from 3rd October of the year 1979. The Company had

signed a 10-year technical collaboration agreement with Nebico Pvt Ltd., Nepal during

the year 1980 for the supply of know-how relating to manufacturing, packaging and

marketing of biscuits and selection of plant and machinery. During the year 1989, BIL's

24

Executive Office was relocated to Bangalore. During the year 1990, two new brands of

biscuits, Elaichi Creamand and Petit Beurre were launched. Also, in the same year a new

cashew badam variant of the brand Milk Bikis and brand extension of pure magic biscuit

Vanilla cream were launched, Fruit bread was launched in Delhi. The Company launched

two new speciality brands in the year 1991 viz., Britannia milk bread and Britannia

brown bread in Delhi and extended nationally its main brands Petit Beurre and Elaichi

Cream. In 17th August of the year 1991, the Company handed over its Soya unit at

Vidisha, MP to SM Dychem Ltd. BIL had celebrated its Platinum Jubilee in the year

1992. After a year in 1993, Wadia Group had acquired the stake in ABIL, UK and

becomes an equal partner with Group Danone in BIL. The Company was in re birth

phase during the year 1997, new corporate identity 'Eat Healthy, Think Better' leads to

new mission of 'Make every third Indian a Britannia consumer' and in the same year BIL

entered into the dairy products market. In 1998, BIL had launched Half/Half, a soft cake

filled with cream in two variants, chocolate-vanilla and vanilla-orange. The Company

had rolled out its flavored milk brand Zip-Sip' in tetrapaks in the year 1999. Zip-Sip had

been launched in Mumbai and some markets in the South.

Forbes Global Ranking was rated the company during the year 2000, Britannia among

Top 300 small companies. In the same year, the company had launched Britannia

Milkman Butter, a product under the Milkman brand. BIL made its fund in-principle

agreement to acquire 49 per cent of Kwality Biscuits in the year 2001 through internal

accruals. During the year 2002, the company had entered into a joint venture with the

Fonterra Cooperative Group, New Zealand's biggest company and one of the leading

diary co-operative groups in the world and the Britannia New Zealand Foods Pvt. Ltd

was born. Pure Magic, the company's product was winner of the Worldstar, Asiastar and

Indiastar award for packaging in the same year 2002. After a year, in 2003, BIL had

launched 'Treat Duet', most successful of the year and Britannia Khao World Cup Jao

rocks the consumer lives yet again. During the year 2004, Britannia accorded the status

of being a 'Superbrand' and the brand Good Day added a new variant Choconut in its

range. Reviewed marketing alliance with the Kolkata-based Thacker Dairy Products Pvt

Ltd.

25

In the year 2005, Britannia New Zealand had launched health drink for adult. The new

plant in Uttaranchal, commissioned during the year 2005, it was ahead of schedule. In the

same year, launched yet another exciting snacking option the Britannia 50-50 Pepper

Chakkar. BIL had forged a strategic alliance with CCD Daily Bread Pvt Ltd in the year

2006, a Bangalore based Company engaged in manufacturing and retailing of premium

breads, cakes snacks and high end ready to eat foods. In the year 2007, Britannia

industries formed a joint venture with the Khimji Ramdas Group and acquired a 70

percent beneficial stake in the Dubai-based Strategic Foods International Co. LLC and

65.4% in the Oman-based Al Sallan Food Industries Co. SAOG. The company was rated

as the No 1 Most Trusted Food Brand in a survey conducted by AC Nielsen ORGO-

MARG and published in Economic Times in the year 2007. Britannia launched Iron

fortified 'Tiger Banana' biscuits, 'Good Day Classic Cookies', Low Fat Dahi and

renovated 'MarieGold' during the period of 2008. BIL was ranked 27th place in the list of

India's Fastest Growing Large Companies by Business Today, Special on June of the year

2008.

26

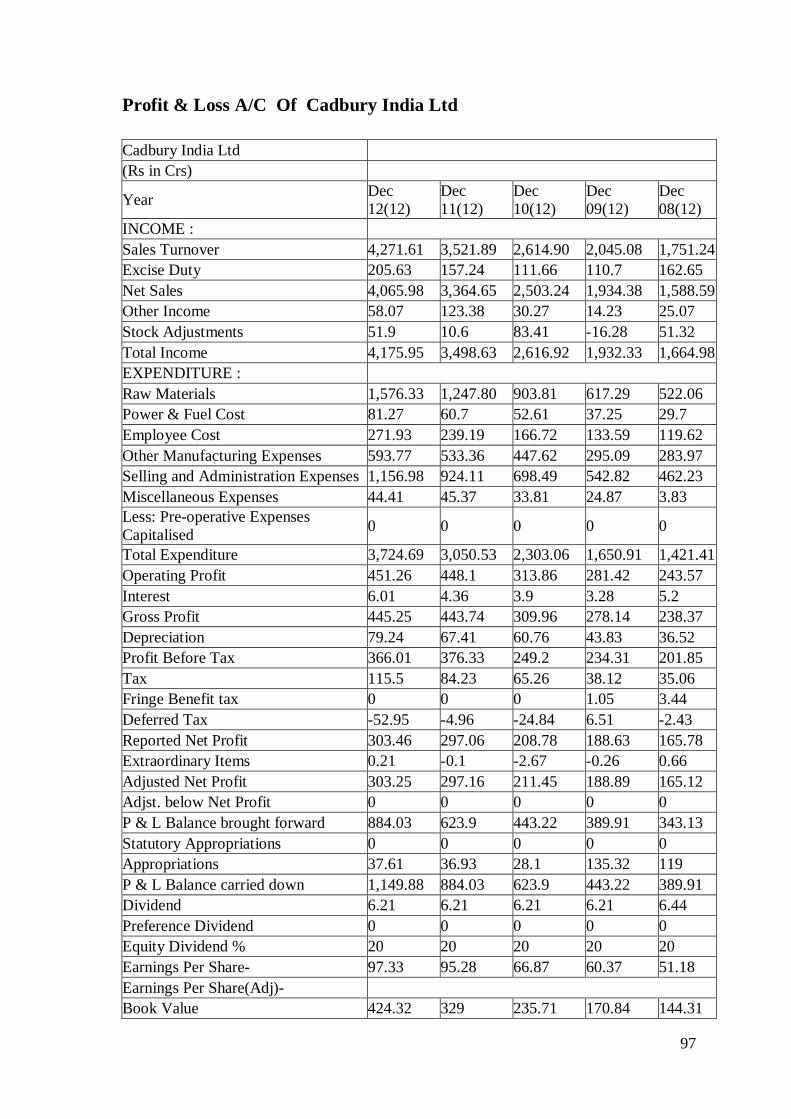

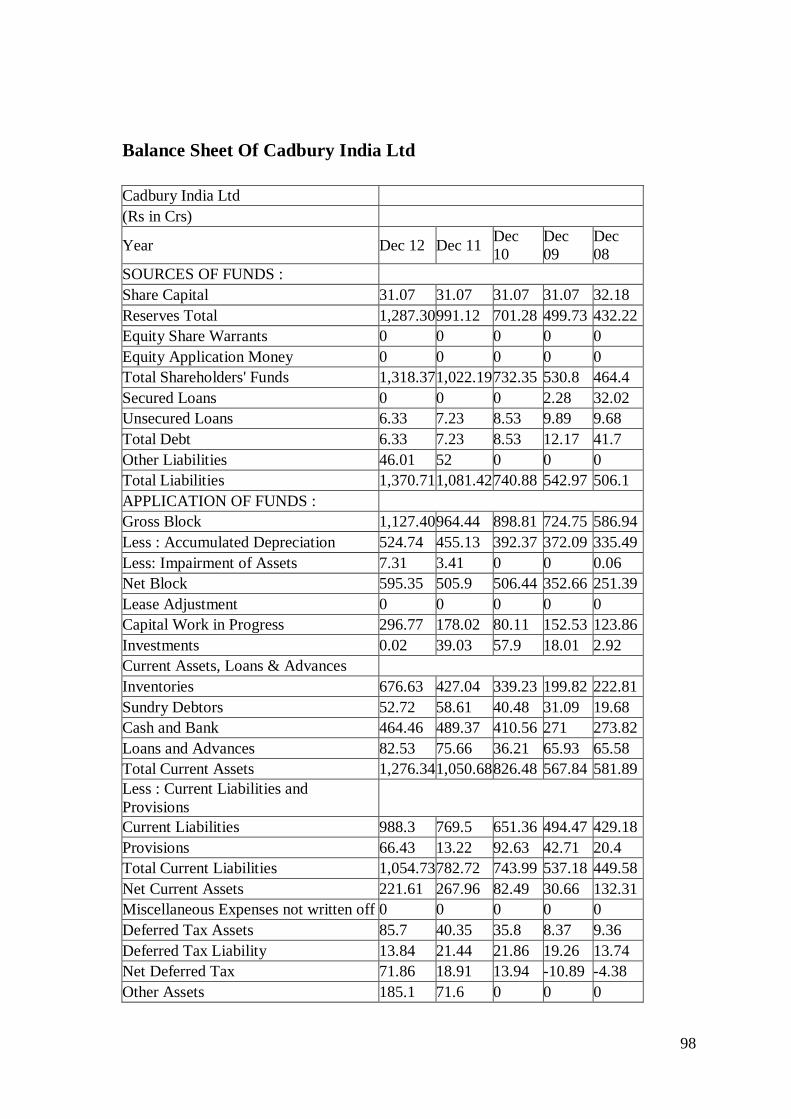

2.1.4 Cadbury India Limited.

Cadbury India Ltd, a subsidiary of Cadbury Schweppes Overseas Ltd is a leading global

confectionery company with an outstanding portfolio of chocolate, gum and candy

brands. The company manufactures and sells chocolate blocks, slabs, or bars; coated

wafer biscuits; malted food; and sugar confectionery. They also export their products to

Sri Lanka, Dubai, Ghana and Maldives.

The company has manufacturing facilities at Thane and Induri in Maharashtra, Malanpur

in Madhya Pradesh, Bangalore in Karnataka and Baddi in Himachal Pradesh and 4 sales

offices at Mumbai, Kolkata, New Delhi, and Chennai. The corporate office is in Mumbai.

The company operates in four categories namely, Chocolate Confectionery, Milk Food

Drinks, Candy and Gum category.

In the Chocolate Confectionery business, the company has maintained their undisputed

leadership over the years, which has some key brands, namely Cadbury Dairy Milk, 5

Star, Perk, Eclairs and Celebrations. In the Milk Food drinks segment, the main product

is Bournvita, which is the leading Malted Food Drink in the country. In the medicated

candy category Halls is the undisputed leader and in the gums category the company

launched the worldwide dominant bubble gum, with the name Bubbaloo.

Cadbury India Ltd was incorporated in the year 1948 as a private limited company with

the name Cadbury Fry (India) Pvt Ltd. The company began their operations in India by

importing chocolates. In the year 1950s, the company started the manufacture of

Chocolate and Bournvita. Also, they launched Cadbury's Fruit & Nut.

In the year 1960s, the company set up a Cocoa Research Centre in Kerala. They set up

their first plant in India at Thane in Maharashtra. Also, they launched Cadbury's Tiffins,

Nut Butterscotch, Caramels, Crackle, 5 Star and Gems.

27

In the year 1970s, the company commissioned the Malt Extract Plant at Induri in

Maharashtra. The name of the company was changed from Cadbury Fry (India) Pvt Ltd

to Cadbury India Ltd. They launched Cadbury's Eclairs during this period. In the year

1980s, the company was converted into a public limited company. In the year 1990s, the

company launched the Sugar Confectionery business with Trebor Googly. They launched

Cadbury's Perk, Cadbury's Truffle and Picnic during this period.

In the year 2002, the company increased the production of Malted Foods from 6,570

tonnes to 7,900 tonnes. In December 2002, Cadbury Schweppes Plc UK acquired the

global non-chocolate confectionary business of Pfizer Inc, USA namely Warner Lambert

India Pvt Ltd. In the year 2003, Halls and Clorets were manufactured and successfully

marketed by the company. Also, the company increased the production capacity of

Malted Foods by 700 tonnes to 8,600 tonnes.

Cadbury Schweppes Plc through their subsidiaries, Cadbury Schweppes Overseas Ltd

and Cadbury Schweppes Mauritius Ltd acquired equity shares of the company in excess

of 90% with led to delisting of the company's equity shares from The Stock Exchange,

Mumbai with effect from January 20, 2003 and National Stock Exchange Ltd, Mumbai

with effect from February 7, 2003. In the year 2005, the company increased the production capacity of Malted Foods by

4,600 tonnes to 13,200 tonnes and Hard Boiled confectionery & Gums by 1,026 tonnes to

8,651 tonnes. In the year 2006, they increased the production capacity of Malted Foods

by 9,000 tonnes to 22,200 tonnes and Hard Boiled confectionery & Gums by 1,489

tonnes to 10,140 tonnes. In the year 2007, the company expanded the production

capacity of Malted Foods by 4,200 tonnes to 26,400 tonnes and Hard Boiled

confectionery & Gums by 6,630 tonnes to 16,770 tonnes and in the year 2008, they

expanded the production capacity of Hard Boiled confectionery & Gums by 7,830 tonnes

to 24600 tonnes.

28

In March 2008, the company launched Cadbury Lite for consumers with diabetes, which

contains a sugar substitute called Maltilol that ensures a low glycemic index in the

product. In May 2008, the company joined hands with Tamil Nadu Agricultural

University for a research project to promote Cocoa cultivation in Tamilnadu.

In October 2008, the company launched their dark chocolate Cadbury Bournville Fine

Dark Chocolate in India, which is the fastest growing segment in the confectionary

category. The chocolate is available in four different variants namely, Rich Cocoa,

Almond, Hazelnut and Raisin & Nut. In February 2009, they launched Cadbury Bourn

vita Li'l Champs, their latest offerings for children.

The company is setting up a new manufacturing facility (Unit 2) at Baddi, Himachal

Pradesh. The construction of the unit is progressing well and is expected to be fully

operational in the year 2009.

29

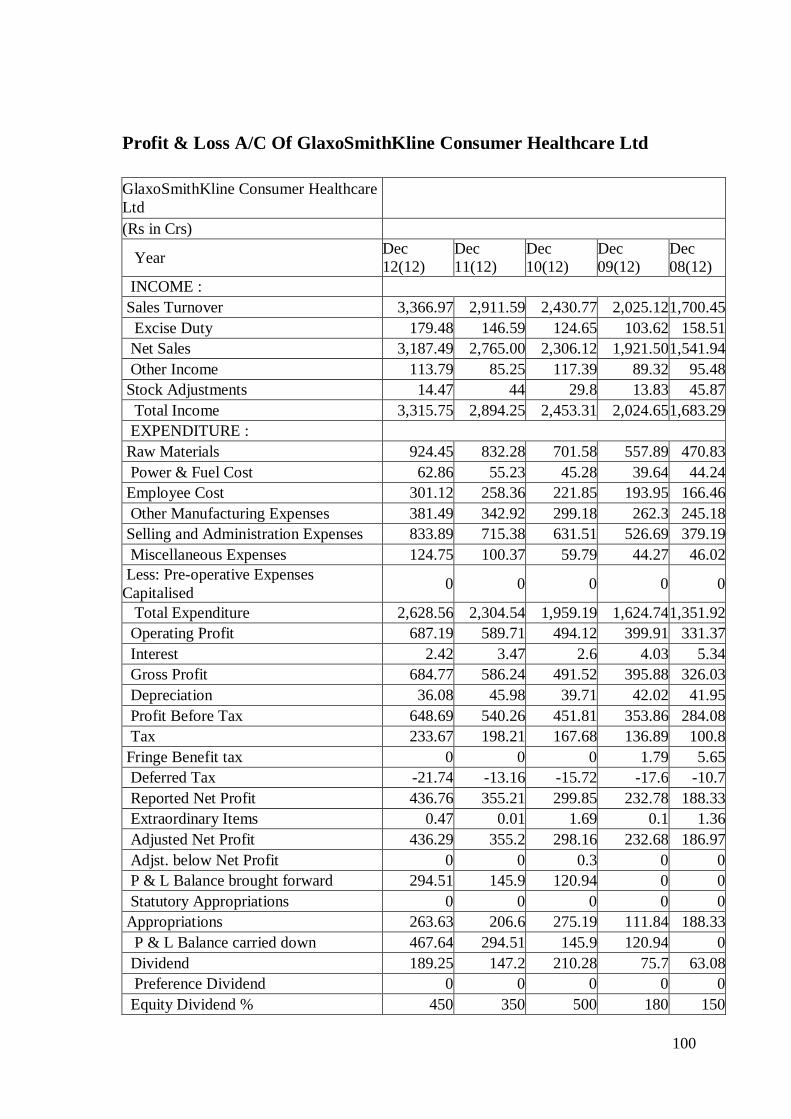

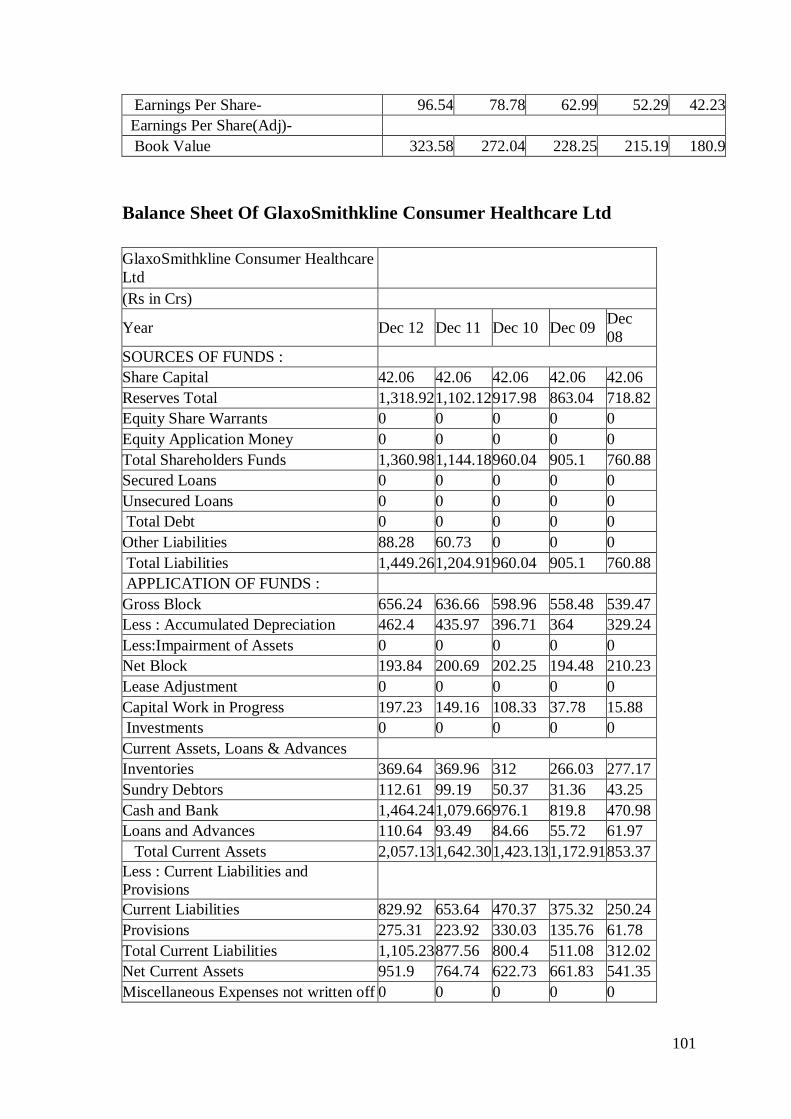

2.1.5 GlaxoSmithKline Consumer health care Limited

GlaxoSmithKline Consumer Healthcare Ltd is one of the largest players in the Health

Food Drinks industry in India. The company is an Indian associate of GlaxoSmithKline

plc, UK. The company's principal activities are to manufacture and distribute a wide

range of healthcare foods, drugs, pharmaceuticals and dairy products. The products

include malted milk food, malted foods, biscuits, energy and protein foods, milk

powders, ghee, milk fluid and milk cream. The company has their manufacturing

facilities located at Nabha in Punjab, Rajahmundry in Andhra Pradesh and Sonepat in

Haryana.

The products of GSK Consumer are categorized as Nutritional and Over the Counter

(OTC) products. The Nutritional division includes health food drinks like Horlicks,

which includes Junior Horlicks, Mother's Horlicks, Women's Horlicks, Horlicks Lite, and

Horlicks biscuits, Boost, Viva and Maltova. The OTC division promotes and distributes a

number of products in diverse categories, including prominent brands such as, Crocin,

Eno and Iodex.

GlaxoSmithKline Consumer Healthcare Ltd was incorporated in the year 1958 as

Hindustan Milkfood Manufacturers Pvt Ltd and was promoted by Horlicks Ltd. The

company became public in the year 1961. In the year 1969, Beecham plc acquired

Horlicks Ltd and became the majority shareholder in Hindustan Milkfood Manufactures

Ltd and in the year 1979, Beecham India Pvt Ltd merged with the company. In the year

1991, the name of the company was changed to HMM Ltd.

In the year 1989, Beecham plc, UK and SmithKline, USA merged to form SmithKline

Beecham plc. The company became part of SmithKline Beecham and the name was

changed to SmithKline Beecham Brands Ltd. Again, in March 1994, the company name

was changed to SmithKline Beecham Consumer Healthcare Ltd, reasserting their

promise of providing healthcare to consumers.

30

In the financial year 2000, the company acquired two new brands Viva and Maltova

along with their patents and trademarks from Jagatjit Industries Ltd. The company also

tied up the manufacturing capacity of Jagatjit Industries Ltd for the manufacture of Viva

and Maltova on a long term contract.

Glao Wellcom plc and SmithKline Beecham plc merged and form a global organization

GlaxoSmithKline plc. As the company is an associate company of GlaxoSmithKline plc,

the name of the company was changed from SmithKline Beecham Consumer Healthcare

Ltd to GlaxoSmithKline Consumer Healthcare Ltd with effect from April 23, 2002.

In the year 2002, the company commissioned their new Spray Drier plant at Sonepat and

the commercial production was started form July 1, 2002. Also, Gussetted Pouch packing

operations were relocated from Nabha factory to a 'State of Art' greenfield facility set up

by a contracted third party at Mangaldoi, Assam. As a result of restructuring process, the

company's packing facility at Kolkata was closed with effect from September 2002.

The company is a consignment sales agent for marketing, selling & distribution of the

brand Iodex with effect form January 1, 2002. In the year 2004, the company has

launched Junior and Mother's Horlicks, Ready-to-Drink Horlicks & Boost and Hot

Vending Machines. In July 2004, they launched Boost Energy Shake, a new chilled

ready-to-drink variant of Boost in Tamil Nadu. Boost Energy Shake will be available in a

200 ml tetra pack.

In the year 2005, the company opened a new secondary manufacturing site (Legacy

Foods) at Baddi in Himachal Pradesh. In February 2005, they launched Horlicks in a new

Toffee flavour. Toffee Horlicks is the sixth flavour in the Horlicks portfolio. The other

flavours are Chocolate, Vanilla, Honey Buzz, Standard and Elaichi.

In the year 2006, the company increased their installed capacity of Malt Based

Foods/Malted Foods and Ghee by 3260 MT and 924 MT respectively. With this

expansion the total installed capacity of Malt Based Foods/Malted Foods and Ghee

increased to 94060 MT and 4000 MT respectively.

31

In the year 2007, the company increased their installed capacity of Malt Based Foods

and Milkrose Baby Foods by 340 MT and 760 MT respectively. With this expansion, the

total installed capacity of Malt Based Foods and Milkrose Baby Foods increased to

94400 MT and 2200 MT respectively.

In the year 2008, the company launched Women's Horlicks, which is specially

formulated for women. New Women's Horlicks is scientifically designed with a unique

combination of Hemocaltm nutrients which provides 100% of the daily requirement of

iron, calcium, Vitamins B2, B6, B12 & C for healthy blood and its normal function. New

Women's Horlicks has no added sugar and is low-fat. It is available in two exciting

flavors- Chocolate and Caramel in a jar with a unique flip top cap. Also, they launched

Active Base and Boost White during the year. In January 2009, the company launched

'Activ Grow', which is a nutritious product launched for infant population. The product

will be sold through prescription only.

In the year 2009, the company relaunched Boost with a clinically proven claim to

increase stamina by three times recorded a growth of 16.2%. They launched a series of

new products. They launched Horlicks Nutribar, which is a nutritious snack. Horlicks

Biscuits was relaunched with a new strategy and packaging. The company also launched

ActiGrow under the GlaxoNutrition umbrella to tap into the fast growing specialist

nutrition segment. The company also entered the noodles segment with the launch of

Horlicks Foodles, instant noodles with seasoning.

32

CHAPTER 3

STRATEGIC ANALYSIS

3.1 INTRODUCTION

3.2 ECONOMIC FEATURES

3.3 PORTER’S FIVE FORCE MODEL

3.4 DRIVING FORCE

3.5 STRATEGIC GROUP MAPPING

3.6 PEST ANALYSES

3.7 SWOT ANALYSIS

3.8 CONCLUSION

33

3.1 INTRODUCTION OF STRATEGIC ANALYSIS

Strategic analysis is a critical component of the strategic planning process. An integral

part of a company’s evaluation and control program, it provides managers with a

comprehensive assessment of the organization’s capabilities and market factors;

revealing growth opportunities and vulnerabilities. Armed with this information,

managers can more effectively choose from among today’s strategic alternatives to create

the greatest future reward potential.

Strategic analysis is critical for analyzing the competitive context in which an

organization operates and for making reasoned and reasonable recommendations for how

that organization should position itself and what actions it should take to maximize value

creation.

34

3.2 ECONOMIC FETURES

Number Of Rivals: As we seen above, there are major more companies in India which are working in Food

And Dairy industry. Yet Food And Dairy industry is dominated by main four companies

namely :

1) Nestle India Ltd.

2) Cadbury India Ltd.

3) GlaxoSmithKline Consumer Healthcare Ltd.

4) Jubliant Food works Ltd

Buyer Need and Requirements:

Dairy foods are extremely healthy, filling and tasty. Dairy producers and marketers are

making sure the public is aware of the healthfulness of dairy products by marketing their

products worldwide. On Monday, March 6, a dairy marketing research symposium was

held at the Renaissance Hotel in Fort Worth, in which people from the dairy industry

discussed new marketing techniques, as well as new research about the dairy industry.

Dairy products that would appeal to the Hispanic population are milk shakes, liquid

yogurt, flavored milk, coffee with milk and kid-oriented products. "These are products

that are untapped in the United States, but are successful in Latin America," Esch said.

"These products should have duel language on the packets."

The drivers for people to buy organic produce are freshness, taste and lack of pesticides.

The drivers for buying organic dairy products are lack of growth hormones and lack of

antibiotics."Three member families have the highest eating index for organic milk,"

McLaughlin said. "It's the highest in families with kids under six years of age."

Dairy producers and dairy processors are doing their best to protect their interests, as they

should. But they are going to have to cooperate because their fates are intertwined.

35

Degree of Product Differentiation:

While the treatment of an agricultural commodity such as wheat, rice, beef, wool, cheese,

maize and wine as a homogeneous good appears to be reasonable in theory, in practice

differences in production practices, seeds, geographical locations of production, sanitary

and phyto-sanitary measures and food safety requirements make the quality of these

commodities (at least, as they are perceived by consumers) different.

The most prominent forms of product differentiation in international trade in recent years

have been horizontal and vertical product differentiations which are related to differences

in product attributes and quality not just perceived by consumers but also due to

differences in factor contents in each product. While significant progress has been made

during the 1980s in terms of developing the theoretical framework to guide empirical

research aimed at explaining intra industry trade, the progress in applying these models in

international trade in food products has been slow.

Product Innovation:

Opening the world Dairy Leaders Forum at the international Dairy Federation (IDF).

First we must innovate constantly to respond to rapidly changing and increasingly diverse

consumer needs. Secondly, we must harness the power of technology to decrease food

waste, maximize food safety and more people with high-quality dairy products.

And thirdly we must work together to ensure not only the economic future of our

industry, but the social and environmental sustainability of our planet.

36

Supply/ Demand Condition:

The Food And Dairy products has traditionally been unique amongst large countries in

that it has depended to varying degrees on imports to satisfy consumer demand. Milk as a

drink, both in and out of the home, has suffered relentless competition from soft drinks.

Their range of product, packaging and availability has increased and the low raw material

costs enable them to be extensively promoted. The consumption of soft drinks by

children in particular has significantly increased and efforts have been made to

modernize the image of milk in order to compete in this sector.

Milk has traditionally had a good image with most consumers, especially house wives

,but in recent years it has seen a decline. Milk is not now seen to be as essential a part of

the diet as it used to be and there is concern and misunderstanding about its fat content.

Pace Of Technological Change:

In the Food And Dairy industry opening the world Dairy Leaders Forum at the

international Dairy Federation (IDF). First we must innovate constantly to respond to

rapidly changing and increasingly diverse consumer needs. Secondly, we must harness

the power of technology to decrease food waste, maximize food safety and more people

with high-quality dairy products.

And thirdly we must work together to ensure not only the economic future of our

industry, but the social and environmental sustainability of our planet.

Economics Of Scale:

The dairy industry together with the dairy farms produces essential products to meet

nutritional needs of the whole population. This paper defines the dairy industry as the

branch of the food industry that includes enterprises processing milk and producing

various dairy products.

37

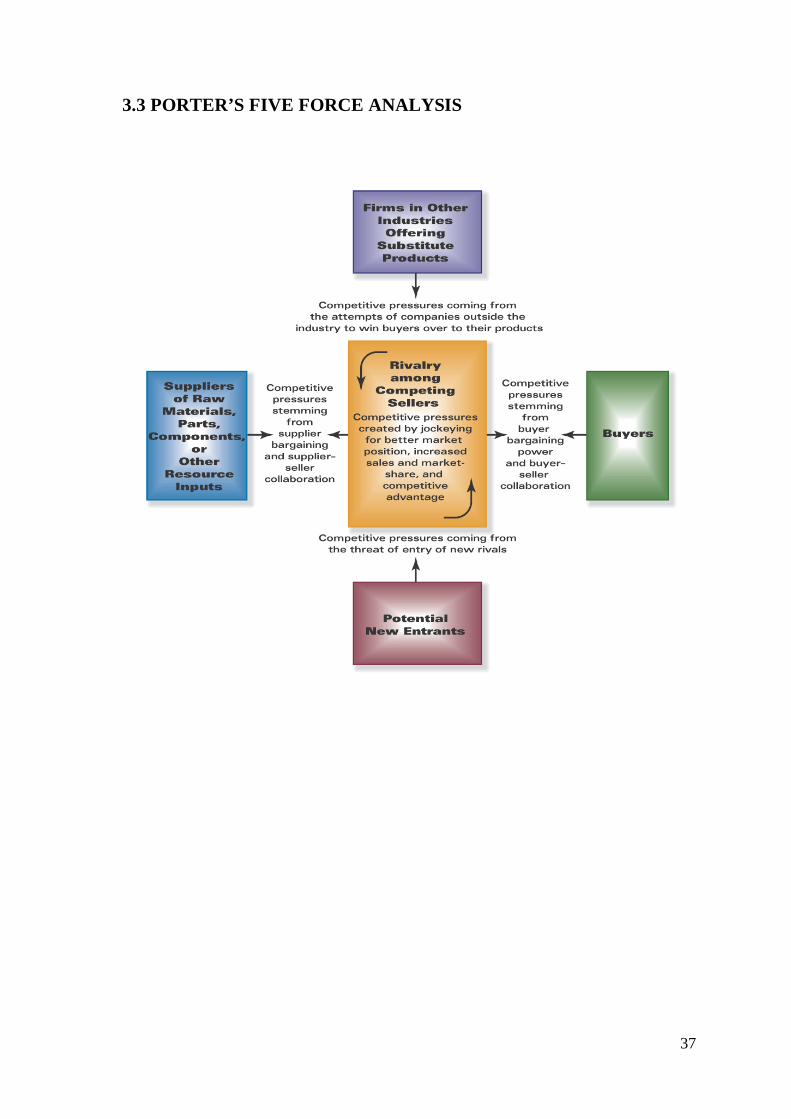

3.3 PORTER’S FIVE FORCE ANALYSIS

38

1) Threats of New Entrants:

In the food and dairy industry there are many restriction of the government and the

barriers to entry in the food and dairy industry.

The barriers to entry in the food and dairy industry are initially low and it is easy for

small local and regional companies to enter into the market, but the barriers to enter the

market nationally are very high. The economies at scale in manufacturing, distribution

costs, and marketing at the national level make it very difficult for start-up companies to

enter into the national market. There are substantial costs in raising the capital needed to

build manufacturing facilities that can mass-produce food and dairy products at the

national level.

In the food and dairy industry the buyer demand is growing rapidly so entry threats are

strong. In this industry the new comers can expect to earn attractive profit. So, entry

threats are stronger.

2) Threats Of Substitutes:

In the food and dairy industry good substitutes are rapidly available or new once are

emerging so competitive pressure from the substitute are stronger. In the food and dairy

industry end users have low cost is switching to substitute so competitive pressure from

substitutes are stronger.

3) Competitive Rivalry among existing players :

In the dairy industry the demand of buyer is growing rapidly so there is rivalry is weaker

in food and dairy industry. In the food and dairy industry there is the buyer cost to

switching brands are very law.

So, it may affect the industry very strongly and in this case rivalry journal stronger.

39

3) Bargaining Power Of Supplier:

The food and dairy product is ready available from many suppliers at the going market

price so supplier bargaining power is weak.

In food and dairy industry seller switching cost to alternative suppliers are low. So

supplier bargaining power is weak. It is directly affected to industry.

In the food and dairy industry the input is easily available from the other supplier so the

bargaining power of supplier is low.

4) Bargaining Power Of Buyer:

The buyer switching cost to competing brands or substitutes products are law so buyer

bargaining power is high in this industry.

Buyers in the food and dairy industry are greatly affected by the economy and the level

of their disposable income. Whenever a buyer’s disposable income declines, they are

more likely to purchase cheaper brands of tobacco, and if a buyer’s disposable income

increases, then they are more likely to buy more expensive brands.

Consumers in the India are now increasingly becoming more concerned with health

issues. Consumer health awareness has hurt the market for tobacco sellers and has also

led to the increase for government regulation.

40

3.4 DRIVING FORCE

Future strategies and innovations:-

It is clear that dairy faces several challenges, especially in the short term. The prospects

for the market in the longer term are still quite good. In general, development of resilient

farming systems and strategies are required. The strategy has to be able to cope with

fluctuations in costs and prices. Looking at the current systems the low input pasture

based systems seem to be the best option. This does not mean that other food and dairy

product will disappear, but they will have to adapt. The footloose This can also be done

by other financial models or by participating in the chain to spread risk. The

development and implementation of these innovations, however, will require time and

funds, so they will not be available very soon.

Globalization:-

Prices of food and dairy commodities were high but dropped at the end of year. The

general expectation is that demand will increase more than production so prices will be

higher in the future, but bigger fluctuations in price are also expected.

Increase in scale:-

The increase in scale seems to be an autonomous process, the current situation, however,

has taught us that not all food and dairy products are resilient in the face of current

circumstances.

Regional trends/driving forces:-

In western regions there is pressure on the consumption of animal-based food products

due to discussion about environmental issues or animal wel-fare, for example. In other

regions consumption of food and dairy will increase because the economy is growing and

income of especially poor people will increase.

41

Abundant availability of raw material:-

India has varied agro climatic conditions it has a wide-ranging and large raw material

base suitable for food and dairy industries. It has a vast coastline of 8000 km, vast marine

land with 10 major ports. India produces annually 90 million tone of milk (highest in the

world), 150 million tone of fruits and vegetables (second largest), 485 million livestock

(largest), 204 million tones food grain (third largest), 6.3 million tones fish (third largest),

489 million poultry and 45,200 million eggs. India's agricultural production base is huge.

42

3.5 STRATEGIC GROUP MAPPING

A strategic group is a concept used in strategic management that groups companies

within an industry that have similar business models or similar combinations of

strategies. For example, the restaurant industry can be divided into several strategic

groups including fast-food and fine-dining based on variables such as preparation time,

pricing, and presentation. The number of groups within an industry and their composition

depends on the dimensions used to define the groups. Strategic management professors

and consultants often make use of a two dimensional grid to position firms along an

industry's two most important dimensions in order to distinguish direct rivals (those with

similar strategies or business models) from indirect rivals. Strategy is the direction and

scope of an organization over the long term which achieves advantages for the

organization while business model refers to how the firm will generate revenues or make

money.

Strategic Group Analysis

Strategic Group Analysis (SGA) aims to identify organizations with similar strategic

characteristics, following similar strategies or competing on similar bases.

Such groups can usually be identified using two or perhaps three sets of characteristics as

the bases of competition.

Examples of Characteristics

• Extent of product (or service) diversity

• Extent of Geographic coverage

• Number of Market segments served

• Distribution Channels used

• Extent of Branding

• Marketing Effort

• Product (or service) quality

• Pricing policy

43

Use of Strategic Group Analysis

This analysis is useful in several ways:

• Helps identify who the most direct competitors are and on what basis they

compete.

• Raises the question of how likely or possible it is for another organization to

move from one strategic group to another.

• Strategic Group mapping might also be used to identify opportunities.

• Can also help identify strategic problems.

There are five steps to make strategy group:

1. Identify two important competitive characteristics that strategically differentiate

firms in an industry from one another:

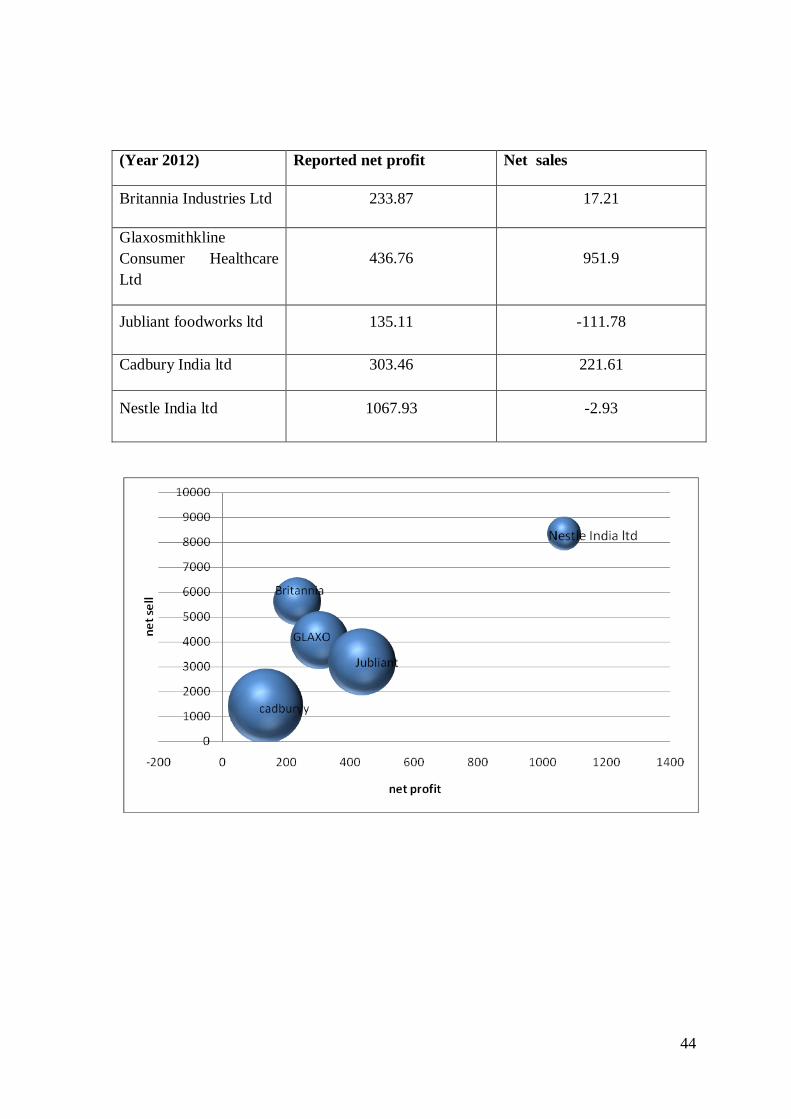

So here there are two factors identify are reported net profit and net assets of the

company they are taken on X axis and Y axis

2. Plot the firm in two variable

In the chart sawn different companies are plotted in X axis and Y axis in respect to their

performance.

3. Draw circles around the firms that are cluster together.

In this step actually find out the close firms which are nearby similar factor that we have

taken in X, Y axes.

4. Indicate potential movement of firms with arrows.

At the last have to saw the potential movement means the strategy for future movement.

44

(Year 2012) Reported net profit Net sales

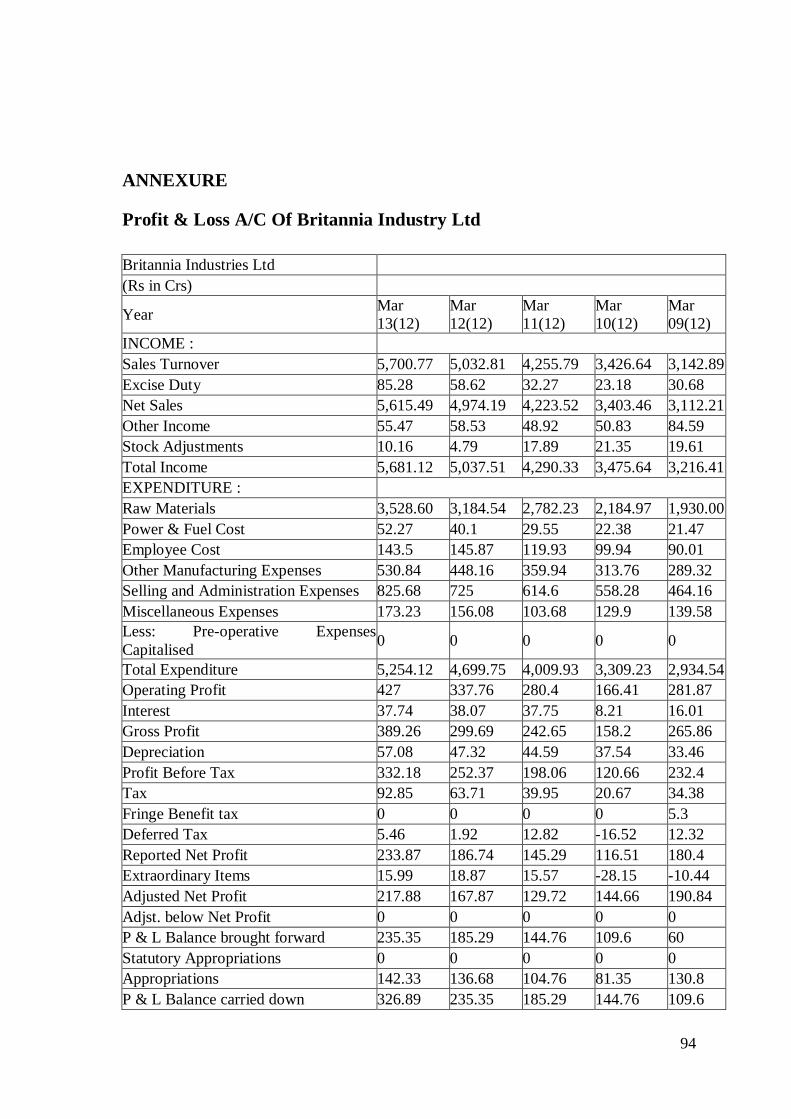

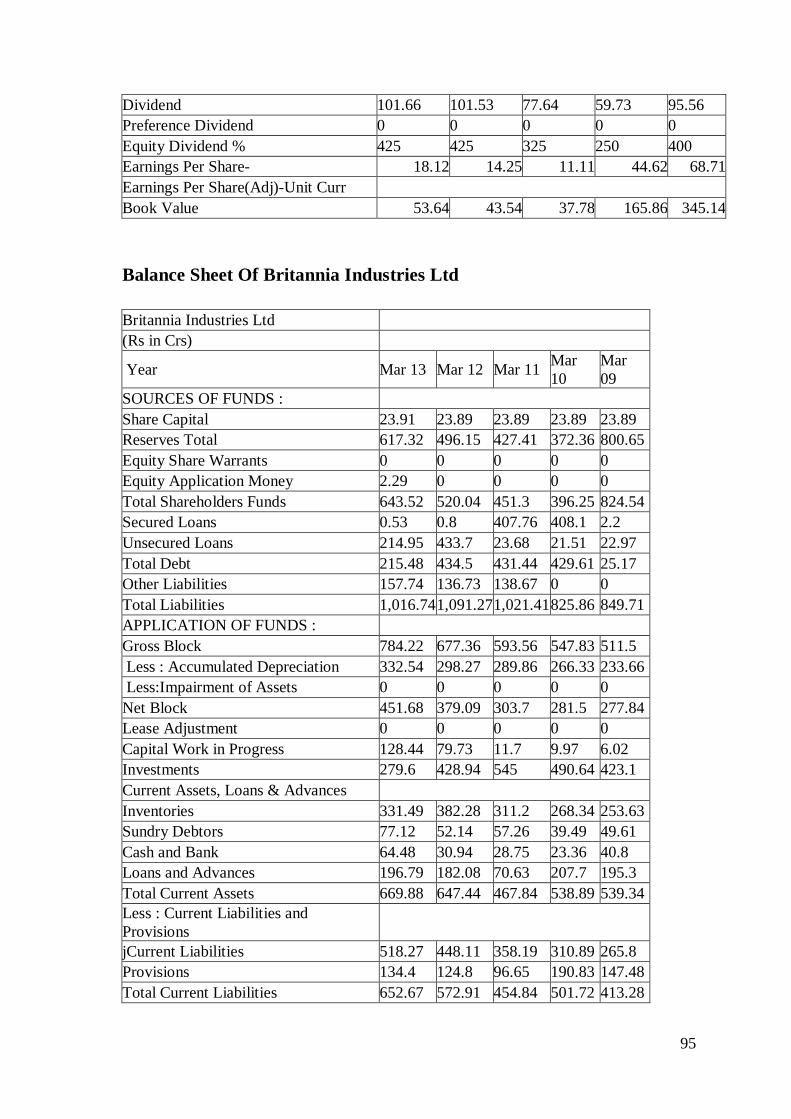

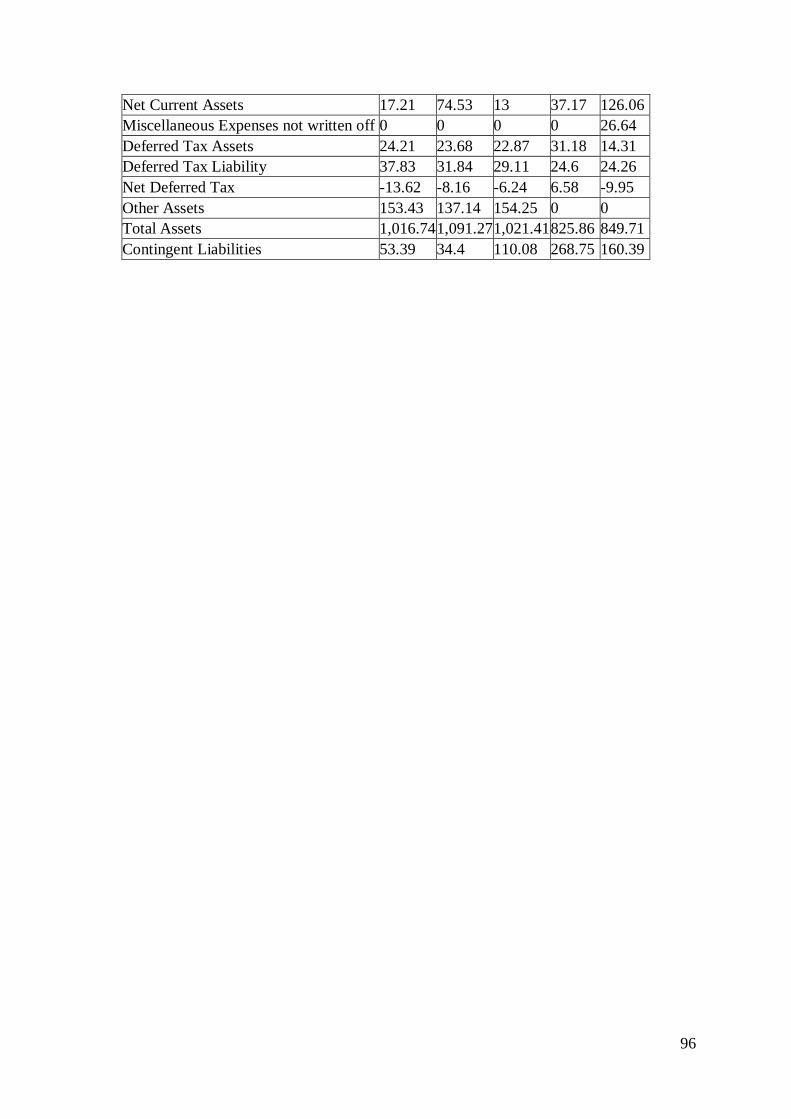

Britannia Industries Ltd 233.87 17.21

Glaxosmithkline Consumer Healthcare Ltd

436.76 951.9

Jubliant foodworks ltd 135.11 -111.78

Cadbury India ltd 303.46 221.61

Nestle India ltd 1067.93 -2.93

45

3.6 PEST ANALYSIS

PEST analysis is concerned with the key external environmental influences on a

business.

The acronym stands for the Political, Economic, Social and Technological issues that

could affect the strategic development of a business.

Identifying PEST influences is a useful way of summarizing the external environment in

which a business operates. However, it must be followed up by consideration of how a

business should respond to these influences.

Business Environment

SOCIAL FORCES

POLITICAL FORCES

ECONOMIC FORCES

TECHNOLOGICAL

46

P:-Political

E:-Economical

S:-Social

T:-Technological

Political

Political factors are how and to what degree a government intervenes in the economy.

Specifically, political factors include areas such as tax policy, labour law, environmental

law, trade restrictions, tariffs, political stability .Political factor may also include goods

and services which the government wants to be provide or be provided (merit goods) and

those that the government does not want to be provided(demerit goods or merit

bads).Further more governments have great influence on the health ,education and

infrastructure of nation .

• Government regulation

Economic

Economic factors include economic growth interest rate, exchange rates and the inflation

rate. These factors have major impact on how businesses operate and make decisions for

example, interest rates affect a firm’s cost of capital and there for to what extent a

business grows and expands. Exchange rates affect the cost of exporting goods and the

supply and price of imported goods in an economy.

• Tax Rate

• Service Tax

47

Social

Social factor include the cultural aspects and include health consciousness, population

growth rate, age distribution, career attitudes and emphasis on safety. Trends in social

factors affect the demand for company’s products and how that company operates. for

example, an aging population may imply a smaller and less –willing workforce (thus

increasing the cost of labour).furthermore, companies may change various management

strategies to adapt to this social trends(such as recruiting older works).

Technological

Technological factors include technological aspects such as R&D activity, automation,

technology incentives and the rate of technological change. They can determine barriers

to entry. Furthermore, technological shifts can affect costs, quality and lead to

innovation.

• Technologies used in industry

48

3.7 SWOT Analysis

STRENGTHS

Cost of production in India is lower by about 40 percent.

Large number of research institutions such as CFTRI,CIFT, NDRI, and NRDC.

Infrastructure development (30 Mega Food Parks)

Income tax rebate for setting up of new agro-processing industries

Cumulative inflow of FDI into the food processing sector

Growing number of fast food chains.

The GOI is in the process of enacting a Food Safety and Standards Bill

A slow but steady transformation of the retail food sector in cities.

India has the second largest arable land in the world. It has diverse agro-climatic zones.

Competitive pricing also enables penetration in the rural markets.'

49

WEAKNESSES

Poor infrastructure still poses a serious challenge to FDI.

Heavily bureaucratic investment processes, government inefficiency, and corruption have also

discouraged foreign investors.

India is still not holding its laws high for protecting copyright issues.

Divergent food habits.

High tariffs, dated food laws, and unscientific sanitary and phytosanitary restrictions.

Lack of grading and standards, poor distribution channels, and onerous government policies.

Low penetration of processed food in domestic markets.

Out of the entire agricultural produce of India only 1% is converted into value added products.

Lacks economies of scale, skilled man power.

OPPORTUNITIES

GOI, in line with its Vision 2015 for the food processing sector, in its 11Th Five Year Plan proposes to

give greater thrust on infrastructure development.

GOI envisages an investment of Rs. 1 trillion in the industry over the next five years, mostly from

private sector and financial institution.

Rising disposable income levels.

Increasing urbanization and exposure to Western culture.

Growing health consciousness among the middle class.

Growing consumerism.

Changing age profile.

Increasing availability of cheap consumer credit.

India is in the middle of two big markets the Middle East and the Far East and we can