Embed Size (px)

Citation preview

Competitiveness in the Canadian Food Industry’

Garth Coffin*, Bruno Larue**, Marc Ban&* and Randall Westpen*

*Macdonald Campus of McGill University, Sainte-Anne-de-Bellevue, Quibec; and * “Universiti Laval, Sainte-Foy, Quebkc.

Concerns about competitiveness in the Canadian food industry have generated a number o/ studies, inquiries and other initiatives on the subject. This paper examines the concept and measurement of competitiveness, the findings of severalstudies andsome of the methodological issues involved in analyzing this phenomenon. While there is general agreement that the concept has most relevance at the level of the firm where it can be described as “the ability to projtably gain and maintain market share, ” it has been applied mostly at the industry and country levels where there is less agreement on measurement and interpretation. This is reflected by a remarkable lack of consensus among studies of the Canadian food indusny. The methodological issues most in need of being resolved are those relating to appropriate measurement and the relationship between strategic behaviour o f f irms and the determinants of competitiveness as found in the environment o ffirms.

Plusieurs etudes ont ete realisees sur la competitivite de I ’industrie agro-alimentaire canadi- ennne. Ce papier a pour but i) d’enumerer et de commenter les definitions et mesures de competitivite couramment utilisees, ii) de synthetiser les aspects methodologiques et resultats d’etudes antkrieures, iii) de discuter des implications de la reglementation sur I ‘inocuite des aliments sur la competitivite. I1 semble y avoir concensus sur la pertinenence du concept de competitivite au niveau de la firme. Malheureusement, la majoritk des ktudes ont analyse la competitivite aux niveaux des industries ou despays pour lesquels I ‘interpretation des resultats et les mesures sont sujet a controverse. Les resultats de ces etudes sont en general contradic- toires, II nous apparait primordial dhmeliorer les mesures de competitivite defaGon a mieux capturer le comportement strategique des firmes et les caractdristiques de I ’environnement dans lequel elles operent.

Can. J. Agric. Econ. 41: 459-473. 459

460 CANADIAN JOURNAL, OF AGRICULTURAL ECONOMICS

tiveness in 1992 (The Gazette, July 29, 1992, p.Bl).

In response to these concerns there have been numerous stules, inquiries, papers, re- ports, committees and conferences as well as business and government decisions made in the name of competitiveness. With respect to the agri-food industry, in 1989 Agnculture Minister Mazinkowski established a Task Force to examine Canada’s competitiveness and the Canadian Agri-food Competitiveness Council now exists to foster development in that direction.

Although one can find many journal arti- cles dealing with specific aspects or determi- nants of competitiveness, relatively little has been published on the analytics of “competi- tiveness” in general and in the food industry in particular. Tlus paper attempts to address, at least partially, those deficiencies by sum- marizing the findings of existing studies and by examining some methodological issues. The role of both economic theory and strategic management are considered as well as the implications of food safety for competitive- ncss. First, however, we must consider what is meant by h s term, and how it is generally measured.

THE CONCEPT AND MEASUREMENT OF COMPETITIVENESS

The term “competitiveness” has come to mean many things to many people. As re- ported by Abbott and Bredahl(1992), the sud- den popularity of th~s term, together with a corresponding explosion of interpretations, prompted Robert Reich to remark that “rarely has a term in public lscourse gone so directly from obscurity to meaninglessness without an intervening period of coherence.” (Wall Street Journal, July 2, 1992). Abbott and Bre- dahl themselves offer definitions from five chfferent sources to illustmte the diversity of interpretations. In a paper prepared for the same conference, Ash and Brink (1992) draw from no less than 14 definitions.

Competitiveness is a term that has emerged primarily from the business literature. It is a broad concept whch has been applied to de-

scribe the performance of three levels of eco- nomic aggregation: firms, sectors or indus- tries and countries. At the firm level, competitiveness is most easily understood as the f m ’ s ability to earn profits. At the sector level, competitiveness is the ability of a group of like firms to compete with another group of finns in another sector or with the same sector in another country. The country level is un- doubtedly the most controversial of the three levels at which competitiveness is applied, because of its welfare implications. Country competitiveness is a function of the competi- tiveness of a country’s sectors and fums. It refers to the ability of a country to provide a hgh standard of living for its citizens. With the declining ability of govemment treasuries to fund social programs in most economies, interest has grown in the ability of firms and industry to play a key role in social welfare through economic growth and employment, hence the recent interest in applying competi- tiveness at the national level.

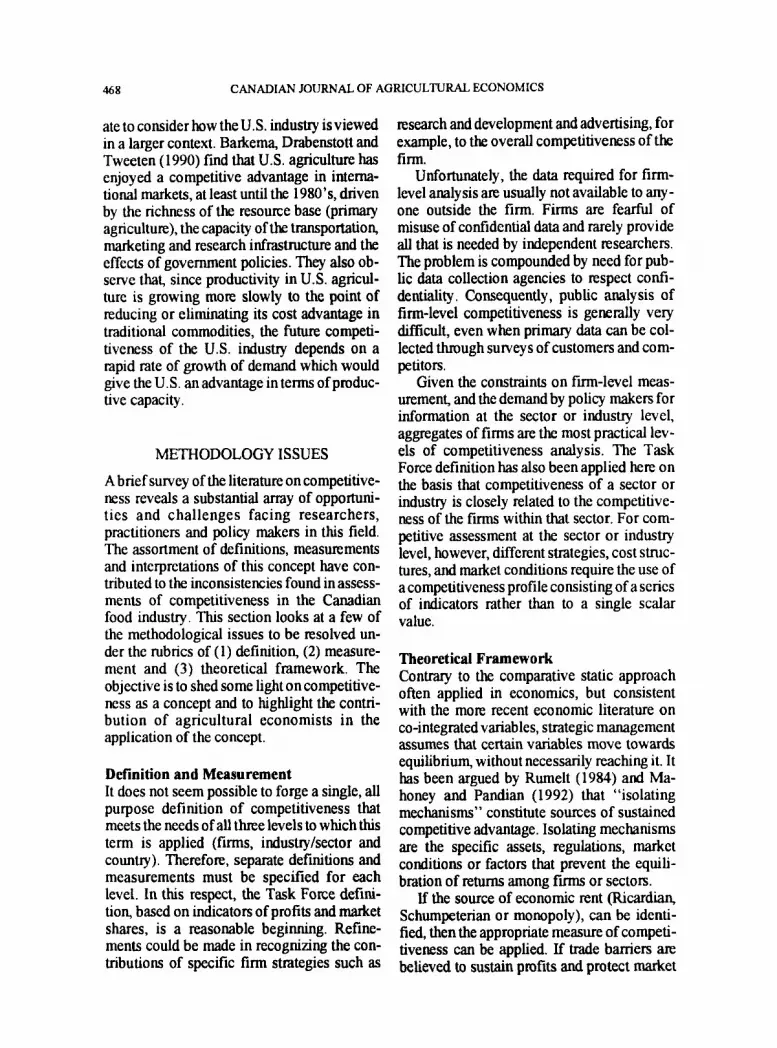

One cannot go far in the literature on com- petitiveness without encountering Michael Porter’s work. Figure 1 is an interpretation of ideas developed i n h s two books on firm-level competitiveness: Competitive Strutegy ( 1980) and CompetitiveAdvantuge (1985). The upper pa~I of Figure 1 contains the key factors de- scribing the environment in whch a firm op- erates. Based on its assessment of these five factors, a firm chooses its competitive strat- egy. In this respect, Porter contends that a firm has only three generic strategy options. The firm creates a competitive advantage through cost advantage, differentiation of products and processes, or focus on a niche.

Choosing the right competitive strategy can be regarded as a necessary but not suffi- cient condtionforcompetitiveness. Fora firm to be successful, it must be effective in all of the activities in which it is engaged, from product development, to production, to cus- tomer service. Porter (1985) separates these activities in two groups: primary and support activities, which are illustrated in the lower half of Figure 1. These are the domain of strategic management. Primary activities comprise inbound and outbound logistics, op-

WORKSHOP PROCEEDINGS 46 1

Porter’s Framework of Firm -Leve I Competitiveness Analysis

Environmental determinants affecting firm strategy:

- potential entrants - bargaining power of buyers - bargaining power of suppliers - substitutes

Competitive strategies low cost focus differenhation

Critical firm activities sustaining competitiveness:

1) primary activities - inbound logistics - operations - outbound logistics - marketing and sales - service

2) support activities - human resources management - technological development - procurement

Source Derived from Porter (1980. 1985)

Fig. 1. Porter’s framework of fm-level competitiveness analysis

erations, marketing and sales, and service. Firm infrastructure, human resource manage- ment, technical development, and procure- ment are classlfied as support activities to the primary functions of making and lstributing goods and sewices.

Porter’s third book, Competitive Advan- tage o fNations ( 1990) identifies four determi- nants of national competitive advantage. The first determinant relates a country’s competi- tiveness to fm strategy, structure, and ri- valry. The second and third determinants

relate factors and demand conditions to com- petitiveness. The last determinant is the re- lated and supporting industries category. These four determinants represent the corners of the Porter “Diamond” of National Com- petitive Advantage. Government policies are not listed as determinants; the role of govern- ment is to condition the four determinants and thus create the necessary linkages to stimulate entrepreneurship and competitiveness .

Following the Porter approach, the Task Force on Competitiveness in the Agri-Food

462 CANADIAN JOURNAL OF AGRICULTURAL ECONOMICS

Industry defines competitiveness as, “ ... the ability to profitably gain and maintain market share in the domestic andor export market.” (Agnculture Canada, 1990) This definition has an apparent simplicity and practicality which prompted Abbott and Bredahl(l992) to categorize it as “ ... a pragmatic definition adopted to describe sector performance in a way that has meaning for managers” @. 1). In that context, t h ~ s definition is more a specifi- cation of two performance indicators (profits and market share), and the arena in which they may be applied (domestic and export mar- kets), to assess the competitiveness of a firm (or industry), than it is an explanation of that phenomenon.

The intent of these measures is to indicate the success of a fm in pursuing its competi- tive strategy. Since t h ~ s is a dynamic process, the time dimension is crucial. In other words, meaningful measurement of competitiveness must reflect an ability to contend over time with changes in the operating environment which drive rivalry, as described by Porter’s (1 980) Five Forces model. Inasmuch as mar- ket shares can be considered a proxy for future profits, they define the firms competitiveness.

This definition treats competitiveness as a relative concept since indicators for one firm or industry are compared with other firms or industries. In that context, ambiguity in com- parison may arise if one firm (or industry) has highcr profits while another has a larger mar- ket share. The weights placed on current prof- its and market shares depend on i) how well market share approximates future profits and ii) the length of the time period being investi- gated. Market share is a useful measure inas- much as it reaches the limit value of zero over the long term for non-profitable firms. Re- gardless, it is worth repeating that the time path of these measures is important. Changes in profits and/or market share may be more indicative of competitiveness than the abso- lute level of these measures.

There are several variations of these meas- ures of competitiveness incurrent use, reflect- ing data availability or the purpose of the analysis. Most applications have been at the industry or sector level. In this context, van

Duren et a1 (1991), argue that value added relative to sales, employment, wages and the number of establishments may be used as proxies for profits whde export orientation and import penetration ratios are employed as proxy measures of international market share. On the other hand, Scott (1990) is critical of the use of value-added as a proxy for competi- tiveness. He argues that the correlation be- tweenvalue added and technology is weak and while the correlation between value added per employee and investment per employee is stronger, it is of little value given that firms can have high value added per employee but low profits (e.g. U.S. oil refining industry). Scott argues further that, “Literal pursuit of higher value added per employee would lead to gross misallocation of capital resources and to impoverishing the nation rather than im- proving economic performance” (p.85). It is important, therefore to consider value added with respect to several factors of production.

Trade ratios are meaningful only where there is little in the way of trade barriers. Tius limits their usefulness for commodities where trade is regulated. Hazeldine and Feeley (1991) have taken a step in the drection of trade neutral measures with their development of indices using productivity and price ratios. Working with the Task Force definition of competitiveness (see above), they observe both a vertical and horizontal dimension to the concept. In their terms,

“The vertical dlmension measures the abil- ity of a fm or industry to produce and market profitably a unit of output. The horizontal dmension is concerned with how many units are sold, and where.” (p.3)

Given that concern is typically concen- trated in the vertical (profitability) clmension, and given that competitiveness is a relative concept, Hazeldine and Feeley measure com- petitiveness as the product of three ratios: relative productivity, relative output prices and the inverse of relative input prices. They then use U.S. industries as benchmarks to compare the profitability of their Canadian counterparts. This decomposition of profit- ability into differences in the three compo-

WORKSHOP PROCEEDINGS 463

nents permits identification of the source of competitiveness or lack thereof.

Many other measures are also in use. Some of these, such as factor productivity and costs of production, are more aptly described as determinants of competitiveness than as measures of competitiveness, per se. More- over, the interpretation of some of these indi- cators is evolving along with the meaning of the term. For example, a few years ago, to be competitive meant to have prices at or below those of competitors; today, being able to do business at prices higher than those of com- petitors, may be taken as a sign of “competi- tiveness”. In other words, in an age of imperfectly structured markets, product drf- ferentiation and niche marketing, prices higher than those of competitors may be seen as a measure of the success of non-price com- petitive strategies.

THE CANADIAN AGRI-FOOD rNDusTRrEs

Several assessments of the competitiveness of the Canadm agn-food industries, at one level or another, have been undertaken in the past decade. Most have used some variation of market share as one indicator, and most have used the U.S. as a benchmark for comparison. Some have focused on trahtional efficiency measures such as productivity and others have used more general indicators.

As shown in Table 1, the Canadian food processing sector as a whole, is more heavily oriented toward the international market and has been progressing faster in that hrection than its U. S. counterpart since the early 1970’s. In terms of value and degree of processing, it may be found that growth of trade in all cate- gories except the low-value by-products ex- ceeded that of the U.S., and growthof exports in lugh-value products, both processed and unprocessed, have also exceeded that of the world market over the same period (Brukman, 1992, Append~x Table 12). In the aggregate, Canada’s share of world total agri-food ex- ports (primary and processed) has fluctuated between 3.5 and 4.5 percent. With resect to profitability, Barkman (1992,7-9) reports that

return on capital has been higher and has been more stable in the food processing industries than in the manufacturing sector as a whole in Canada. One of the first to specifically examine the

competitiveness of the production sector of Canadian agriculture in recent times was Proulx in his report for the Union des produc- teurs agricoles du Quebec (UPA) in 1986. Although hs study concentrated particularly on Quebec agriculture, in the context of trade negotiationswiththeU.S., hisuseofCanalan and U.S. data for comparisons reveals a broader picture. Based on comparisons of pro- ducer and wholesale prices, growth in market shares and balance of trade, and a definition which explicitly recogfuzes government sup- port, Proulx evaluated 25 commodities in Quebec and concluded that of these, eggs, poultry, cereal p n s and several horticultural crops were considered to be non-competitive.

Brinkman (1987) arrives at similar conclu- sions for similar commohties in Canadian agriculture, with the adhtion of b r y to the list of non-competitive sectors. In relying on trahtional measures such as productivity and costs of production, he argues that such meas- ures are better long run indicators of ‘‘true” competitiveness than market shares whch might have been bought withgovernment help in the short run but wluch might be drfficult to maintain. Brinkman also recognizes a role for product quality and exchange rates as detenni- nants of competitive position whch he disag- gregates into the various sectors (resources, farm, agribusiness, etc.). On the whole he considers wheat and pork to be our most com- petitive commolties (see Table 2).

Most investigations of sector or national competitiveness prior to 1987 follow the ap- proach that a sector is considered competitive if it is able to produce a good for lower cost (taking into account any subsihzation) whle remunerating its factors of production as well as other activities would. Such studies are typically comparisons of factor productivity across different countries. Frank (1977), Bald- win and Gorecki (1979) and Hazelhne, Gui- ton and Wall (1988) compare labour productivity in Canada and the U.S. in more

464 CANADIAN JOURNAL OF AGRICULTURAL ECONOMICS

TABLE 1 TRADE ORIENTATION OF THE

CANADIAN AND U.S. FOOD INDUSTRIES, (INCLUDING FISH,) 1972 AND 1986

Canada -- United States 1972 1986 1972 1986

YO YO IMPORT PENETRATIONA 7 9 1 3 0 3 5 3 8 EXPORT ORIENTATION' 9 7 1 4 6 3 0 4 1

A Import share of domestic consumption Export share of domestic shipments

SOURCE: Barkman, Patricia Overview of Chanqes in the Performance and Structure of Canada's Food and Beveraqe Processinq Industries Working Paper APD 92-2 Policy Branch, Agriculture Canada, July 1992 (Appendix Table 9)

than 15 processing industries. In their respec- tive studies of the competitiveness of various food processing industries Lanoie (1984, 1986)andHunt (1987) useproductivity,costs, economies of size, and other performance measures derived from industrial organization and trade theory. For the most part, their analyses compare these performance indica- tors and determinants of competitiveness with those of the U. S. without expressing an overall assessment of the Canadian industries.

Hazeldine, Guiton and Wall (1988) found Canadan labour productivity in 1982 in all but one industry (mixes and cereals) to be lower than U.S. productivity (Table 2). By this measure, therefore, nearly all of Canada's in- dustries appear to be uncompetitive. How- ever, it is imprudent to draw such conclusions; US. industries may simply be substituting more capital for labour because of Merenj wage rates, technology or production scale. In response to this shortcoming, Hazeldine et al compared total factor productivity (TFP) for the same year and found that Canadian pro- ductivity was higher in almost half of the surveyed industries, and was very close to that

of the US in all but two (breweries, wineries) of the twenty surveyed infustries (see Hazeld- ine, Guiton, Wall 1988).

West (1 987) defines competitiveness as the ability to produce and sell profitably inforeign or domestic markets. Trade performance and prices are used to assess the competitiveness of Canadian processing industries. Export on- entation (percentage of Canadian stupments sold in export markets), import penetration (percentage of domestic demand served by imports) and the ratio of shipments to domes- tic consumption are used to class@ Canadian industries relative to theirU.S. counterpartsas more competitive (High), equally (Moderate) or less competitive (Low) inTable 2. By these measures, West found all Canadian industries examined to be either highly or moderately competitive.

In contrast to West, results of the Hazeldine and Feely (1991) analysis, using their com- petitiveness index based on relative produc- tivity combined with output and input price mtios, suggest that, in the aggregate, the Ca- nadian food industry is not very competitive with that of the U. S. According to the average

F

Brin

knia

n, 1

987

Whe

at, P

ork

Wes

t. 19

87

Feed

grain

s,Oils

eeds

Da

iry, P

oultr

y Be

ef

Haz

eldi

ne, G

uito

n, W

all,

1988

(lab

our

prod

uctiv

ity in

19

82)

Haze

ldin

e, Gu

iton,

Wall

, 19

88 (t

op1

fact

or

prod

uctiv

ity in

19

82)

Mea

t pro

cess

ing,

Poul

ty

proc

essin

g, F

roze

n fr

uit

and

vege

table,

Flu

id m

ilk, C

erea

l flo

ur, S

ugar

and

cho

colat

e co

nfec

tione

ry, P

otato

chi

ps,

othe

r foo

d pr

oduc

ts

Frozen v

eg.

Mea

t and

Pou

lt M

ilk,

Butte

r anf

Milk

Pow

der

Flou

r and

Fee

d Ve

getab

le oi

l Sh

orte

ning

and

Mar

garin

e

Haze

ldin

e an

d Fe

ely (

1991

)

Cann

ed fr

uit a

nd v

egeta

bles

, Br

ewer

ies, W

iner

ies

Juic

e Br

eakf

ast C

erea

ls Br

ead

Rolls

Pa

sta

Chip

s and

Pop

corn

Pe

anut

But

ter

Mar

tin, W

estgre

en, v

an

Red

Mea

t W

heat

base

d pr

oduc

ts

TA

BL

E 2

S

umm

ary

ofC

omD

etiti

vene

ss o

f C

anad

ian

Aar

i-Foo

d In

dust

ries

Poul

t$

Froz

en v

egeta

bles

Da

iry p

rodu

cts

MEP

SURE

EM

PLOY

ED

Su a

r Re

% M

eat

Chew

ing C

um

Choc

olate

Fr

ozen

Fru

it Br

eald

asl F

ood,

Flou

r Mixe

s

cost

of ro

duct

ion

from

a

com

moi

ty st

andp

oint

irnpo

rts/d

omes

tic

prod

uctio

n;

expo

rts/p

rodu

ctio

n;

perc

entag

e of

dom

estic

co

nsum

ptio

n se

rved

by

Cana

dian

ind

ustrv

Labo

ur p

rodu

ctivi

tv as

measured b

y va

lue

adde

d pe

r em

ploy

eeA

Cana

daAJ

.S. c

ompa

rison

s of

total

fac

tor

prod

uctiv

ity

Indu

stria

l Milk

Br

ead

Poul

try

Vege

table

oils

Cann

ed fr

uit &

veg

etabl

es

Flui

d M

ilk

Flou

r Bi

scui

t so

ft dri

nk

Feed

Com

etit

iven

ess

indew

(c

o~P

)= re

l. pr

oduc

tivity

(Ca

n.AJ.S

.) X

?el.

out

ui r

ice

(can

.nPs

.) R r

el. in

put

pric

e (U

.S./C

an.)

net

expo

rl or

ient

atio

n ra

tio

com

petit

ive

ratio

: Ca

nada

's ra

tio o

f va

lue

adde

d to

the

US,

qres

s!

as a

per

cent

age

o sa

les

Fish

pro

duct

s, Ca

ne a

nd b

eet

suga

r, Br

eakf

ast c

erea

l, Re

d M

eat

Feed

Ba

ke

prod

ucts

Soft

hnnl

oyeg

ehbl

e oil

AII

sect

ors

exce

pt m

ixes

and

ce

reals

Dairy

pro

ducts

(ex

cl. m

ilk),

Mixe

s an

d ce

real

s, Fe

ed,

Bisc

uits,

Bak

eries

, Che

wing

p

m, C

ane

and

beet

suga

r

Soft

drin

k

Cann

ed v

eg.

Chee

se

Ice

crea

m

Suga

r Be

er &

Wine

Sm

okin

g to

bacc

o

ea,

coffe

e,

The

clas

sific

atio

n cr

iteria

def

ine

high

ly c

ompe

titiv

e, in

dust

ries

as

thos

e wi

th h

i er

labo

ur p

rodu

ctiv

ity, t

haq

the

U.S.

Indu

strie

s of

.mod

erat

e co

mpe

titir

ness

are

thos

e in

whi

ch l

abou

r pr

oduc

tivity

is c

lose

to t

hat

of th

e ".

?cou

nter

part.

In

dust

ries

with

low

labo

ur p

rodu

ctiv

ity r

elat

ive

to th

e U.

S. a

re o

f low

com

petit

iven

ess.

' Dai

ry a

nd p

oultr

y in

dust

ries

wer

e ad

mitt

edly

diff

icul

t to

clas

sify

beca

use

of th

e tra

de r

estri

ctio

ns w

hich

app

ly to

the

se p

rodu

cts.

466 CANADIAN JOURNAL. OF AGRICULTURAL. ECONOMICS

of their index for 1986 data, weighted by shipments of the 40 industries, Canadiancom- petitiveness was five percent below the US. benchmark. This was attributed to a lower productivity (by six percent) and higher input prices (by four percent) which offset lugher output prices (by eight percent) in Canada.

Again however, Hazeldine and Feely ob- served considerable variation among indus- tries. They found nine that were competitive relative to the U.S. (several of which enjoy import protection in Canada), and eight that hada profitability ratio of less than0.8 relative to the U S . The results for selected industries are shown in Table 2. Another approach is the “competitiveness ratio” used by Martin, WestgrcnandvanDuren(1991), wluch meas- ures the proportion of value added in Canadian industries per dollar of sales compared to their US. counterpart. Industries that add more value than the US are identified here as highly competitive, those that add about the same value per dollar of sales, moderately competi- tive, and those that add signrficantly less of low competitiveness. Net export orientation ratios were also considered.

Cousineau et a1 (1 992) also use value added ratios with respect to sales, employees and wages as their competitiveness indicators along with net trade ratios. The net export orientation ratio, a measure of the proportion net exports to total sales, is also used as a measure of the ability to capture export mar- kets. Positive net export orientation ratios sug- gest that the industry is highly competitive, while strongly negative ratios suggest that the country’s competitive strength in that industry is relatively low. Their findings are reported in Table 2.

Several other studies deal with more spe- cific aspects of competitiveness or its determi- nants. For example, West and Cooper (1988) assess the expected effects of the Canada4.S. Trade Agreement (CUSTA) on Canadian processing industries, Landreville (1989) ex- amines the effects of policies in other coun- tries on Canadian trade, and Dhaliwal(l990) looks at the role of economies of scale in the cost competitiveness of food and beverage industries. Also in the context of CUSTA, and

in response to requests from producer and processor organizations, the Canadm Inter- national Trade Tribunal (CIW conducted an inquiry into the competitiveness of the Cana- dian fresh and processed fruit and vegetable industries. Lambert and Romain (1992) ana- lyzed the competitiveness of Quebec and On- tario dairy processors in two ways. They compute labour productivities and attempt to explain their variations by regressing them on variables such as firm size, the ratio of non- production and production workers, capital stock, etc. They also conducted a survey and linked management’s perception of determi- nants of competitiveness to firm charac- teristics. Their findings suggest that Canadian dauy processors are moderately competitive with those of the U.S. for certain products (ice cream, yogurt and fluid milk) and less so for others (cheese, butter and milk powder).

The findings presented in Table 2 reflect these various measures of competitiveness. In some cases they use the same indicators but interpret them dfierently. For example, one analysis uses value added per labour input (employee or hour) as a measure of labour productivity, another as an indicator of profit- ability. Under the cimmstances, however, one would expect a degree of correspondence among studies as to which sectors are com- petitive. While there is some convergence in this respect, there is also considerable diver- gence for certain industries or commodities. This is illustrated in Table 3.

Ifa particular sector or commodtty appears in more than two of the three categories (high, moderate or low) of competitiveness, or at opposite ends of the scale, we have an obvious lack of precision and/or consistency in meas- urement. This happens for 12 of the 18 indus- tries or commodities identified in Table 3. In another four cases, the competitiveness as- sessments fall into two of the three categories specified. In fairness when assessments based on total labor productivity are discounted, which the authors themselves have done, the consensus for six industries broadens.

Finally, since the US. agriculture and food industry has been used as the benchmark for studies of the C&an system, it is appropri-

WORKSHOP PROCEEDINGS 467

TABLE 3 Variations oii the coniDcli~i\viicss assessment of selcctctl Canadian indiistries rclativc to U S .

I

INDUSTRY OK COMI’ETITIVENESS Coniriiodi ty

H I G H MODERATE LOW

MEAT AND Cousincau el al; l lCW (lfp)’; llFC SLAUCIITERING hiW)West

llccf I’roiih llrinloiian; I l l

Pork Drinkiii:ui; I’roiilx IIF

Coiisineau el al; MWV; I’OUI.1’RY PRO(;. l lCW (lfp); I I F

IISII I’HOCISSOHS WCSl

IICW (lfp,llp); llritikiiim Cousineau d al; I I G W I (1988)

SOI:’I’ DRINK htAN1IF. I l lGW (111)) I Coiisincnii cl al; Wesl; 1IF

Ilrinhiian; Proulx

l lGW (IlP)

Brinkman

Coiisincau el al; 111:; l lGW (llll)

I IF

Cousiiicau el al; I IF ; IlCW (tip)

LiWV: 111:

Coiisine;iii el al; Wesl; l lGW (Ill’)

hlW’; l lGW (ilp)

Wcsl; I lGW (lfp,llp); MWV

l lGW (IlP)

468 CANADIAN JOURNAL OF AGRICULTURAL ECONOMICS

ate to consider how theU.S. industry isviewed in a larger context. Bakema, Drabenstott and Tweeten (1990) find that U.S. agriculture has enjoyed a competitive advantage in interna- tional markets, at least until the 1980’s, driven by the richness of the resource base (primary agriculture), the capacity of the transportation, marketing and research infrastructure and the effects of government policies. They also ob- serve that, since productivity in U.S. agricul- ture is growing more slowly to the point of reducing or eliminating its cost advantage in Wt iona l commodities, the future competi- tiveness of the U.S. industry depends on a rapid rate of growth of demand whch would give the U S . an advantage in terms of produc- tive capacity.

METHODOLOGY ISSUES

A brief survey of the literature on competitive- ness reveals a substantial m y of opportuni- ties and challenges facing researchers, practitioners and policy makers in this field. The assortment of definitions, measurements and interpretations of this concept have con- tributed to the inconsistencies found in assess- ments of competitiveness in the Canadian food industry. This section looks at a few of the methodological issues to be resolved un- der the rubrics of (1) definition, (2) measure- ment and (3) theoretical framework. The objective is to shed some light on competitive- ness as a concept and to highlight the contri- bution of agricultural economists in the application of the concept.

Definition and Measurement It does not seem possible to forge a single, all purpose definition of competitiveness that meets the needs of all three levels to which this term is applied (firms, industryhector and country). Therefore, separate definitions and measurements must be specified for each level. In this respect, the Task Force defini- tion, based on indicators of profits and market shares, is a reasonable beginning. Refine- ments could be made in recognizing the con- tributions of specific firm strategies such as

research and development and advertising, for example, to the overall competitiveness of the firm.

Unfortunately, the data required for firm- level analysis a~ usually not available to any- one outside the firm. Firms are fearful of misuse of confidential data and rarely provide all that is needed by independent researchers. The problem is compounded by need for pub- lic data collection agencies to respect confi- dentiality. Consequently, public analysis of firm-level competitiveness is generally very difficult, even when primary data can be col- lected through surveys of customers and com- petitors.

Given the constraints on firm-level meas- urement, and the demand by policy makers for information at the sector or industry level, aggregates of firms are the most practical lev- els of competitiveness analysis. The Task Force definition has also been applied here on the basis that competitiveness of a sector or industry is closely related to the competitive- ness of the firms within that sector. For com- petitive assessment at the sector or industry level, however, Mferent strategies, cost struc- tures, and market conditions require the use of a competitiveness profile consisting of a series of indicators rather than to a single scalar value.

Tbeoret ical Framework Contrary to the comparative static approach often applied in economics, but consistent with the more recent economic literature on co-integrated variables, strategic management assumes that certain variables move towards equilibrium, without necessarily reachng it. It has been argued by Rumelt (1984) and Ma- honey and Pandian (1992) that “isolating mechanisms” constitute sources of sustained competitive advantage. Isolating mechanisms are the specific assets, regulations, market conditions or factors that prevent the equili- bration of returns among fm or sectors.

If the source of economic rent (R~cardm, Schumpeterian or monopoly), can be identi- fied, then the appropriate measure of competi- tiveness can be applied. If trade barriers are believed to sustain profits and protect market

WORKSHOP PROCEEDINGS 469

share, then these isolating mechamsms may be inconsistent with social objectives such as economic growth and employment and devel- opment of high quality products, associated with competitiveness. If sources of heteroge- neity in resource distribution sustain Ri- cardian rents (remuneration of scarce resources), then competitiveness will be sus- tained through strategies that exploit imper- fect markets for resources. Innovative capacity may also create competitive advan- tage. In such a case, a true measure of com- petitiveness would be the ability of a fm to introduce new products so as to replace exist- ing ones---Schumpeter’s process of creative destruction.

Which of these rents reveals important in- formation about competitiveness? Restricting assessment to any single measure provides only a partial picture of the ability of a fm to compete. Profits and market share data should be complemented with information on the per- formance of human and physical capital. The number of new products launched, the eco- nomic lifespan of products on the supermarket shelves, improvements to existing products, the rate of change in the number of products and the number of buyers (as well as volume) provide information on the ability of firms to motivate consumer choice and deliver a desir- able product.

COMPETITIVENESS AND FOOD QUALITY

For obvious reasons, the global agri-food sec- tor is subject to a large number of sanitary and phyto-sanitary regulations affecting the loca- tion and design of plants as well as production and marketing techques. Techca l regula- tions are typically complicated and vary from country to country. All other tlungs being equal, the volume of trade between countries with similar techca l regulations should be higher than that between countries with differ- ent standards. If technical regulations about food reflect the preferences and attitudes to- ward risk in a country, then the above state- ment about the degree of harmonization in standards and the volume of trade is simply an

extension of Linder’s hypothesis, which pre- dicts that countries with similar preferences will trade more with each other (Thursby and Thursby, 1987). Hence, the harmonization of standards could in theory sigruficantly alter the pattern of competition in international markets.

Harmonization is difficult because techni- cal regulations not only reflect preferences and attitudes toward risk but also region or country speclfc factors such as climate and disease history. This lack of harmonization can be regarded as a form of product differen- tiation that can be exploited to create a com- petitive advantage. Larue (1991) found that Canadian wheat received apremium 0verU.S. and Austdian wheats that goes beyond qual- ity differences. Thus “return” for a good repu- tation can be attributed, at least in part, to the marketing regulations encouraging consis- tency in the supply of a high quality product.6

Unfortunately, the complexity of techca l regulations coupled with the hfficulty in ac- cusing a country of worrying too much about food safety makes sanitary and phyto-sanitary regulations effective trade barriers. The use of technical regulations for food as trade barriers is facilitated by the different orientations taken by the GAIT’S standards code for agricultural and competing products. Unlike standards for manufactured products whch are based on product characteristics, agricultural standards focus strictly on production and processing methods (Bredhal and Forsythe, 1989). Ad- justments to processes by Canadian f m to allow them to export to certain countries could be very expensive. Lanciotti (1991) discusses some of the adjustments required of Canadm pork processors to export to EEC countries. Her survey confirms that the competitiveness of the Canadian pork sector is negatively af- fected by consumers’ health concerns and other non-tariff barriers.

Food safety concern is a double-edged sword for Canadian processors. On the one hand, it provides an opportunity to create a competitive advantage through product differ- entiation On the other hand, the extent by which firms can create a competitive advan- tage by supplying products with different food

470 CANADIAN JOURNAL OF AGRICULTURAL ECONOMICS

safety attributes is mitigated by the irrelevance of standards that were designed for turnqf- the-century production agriculture and infant processing industries.

THE ROLE OF AGRICULTURAL ECONOMISTS

Historically, agricultural economists have contributed to the competitiveness issue by supplying analyses about narrowly-defined aspects of competitiveness, such as those ele- ments of the environment depicted in the up- per portion of Figure 1. There is no doubt that estimates of total factor productivity, capacity utilization, efficiency frontiers, disembod- ied/embo&ed technologml change,’ elastici- ties of scale, of size, scope, and of substitution, expenditures elasticities, price transmission elasticities, import demand and advertising elasticities, rates of return on advertising and R&D, oligopoly/oligopsony power, compara- tive advantages, etc. provide useful informa- tion about competitiveness. The usefulness of economic studies in measuring competitive- ness is not restricted to industries competing on a cost basis. Despite a rich knowledge of individual determinants of competitiveness, agricultural economists have not indulged ex- tensively in comprehensive analyses of the aggregate effects of these determinants on strategic behaviour of firms and, in turn, on the competitiveness of an industry. Part of the Mficulty lies in adequately measuring dimen- sions of the environment in which the firm operates. Following Dess and Beard (1984), Wholey and Brittain (1989) and Cas- trogiovanni (1991), Bank (1992) has de- scribed the environment of selected food processing industries in Canada and e U.S.

aggregation of all the decisions and interven- tions occurring in the firm’s environment. These dmensions, along with the concentra- tion ratios of each industq are then used to explain the industry price-cost margins.

The appeal of Uus approach is that it endo- genizes differences in industry environments. The knowledge and familiarity of agricultural

in thr e dimensions-m luficence, P dyna- mism, 5 and complexity I!? ---representing an

economists with factor con&tions, demand conditions, government policy and other ele- ments of the environment is a strength to build from. This is a significant area of comparative advantage for agricultural economists (West- gren and Cook 1986).

SUMMARY AND CONCLUSIONS

Competitiveness in the Canad~an food indus- try is an important and legitimate concern in the context of global recession, trade negotia- tions and the changing role of government. In Uus paper we discuss the concept, its measure- ment, assessments of the Canadian food in- dustry, some methodological issues, the implications of food safety issues and the role of agricultural economists in competitiveness analysis.

Competitiveness is a complex concept. It has Merent meanings, and implications at different levels of economic aggregation such as f q industry or country. Porter (1980, 1985, 1990) addresses all three levels in his synthesis of industrial organization and busi- ness theory. Drawing on his work, some ana- lysts have tended toward the notion that competitiveness can be described as “ability to profitably gain and maintain market share.” Accordingly, one approach to measurement or assessment of competitiveness has been to use market share and profitability measures as evidence of that ability in terms of results. Another approach has been to use productivity measures and input and output prices as key determinants of the ability to compete.

Studies of competitiveness of the Canadian food industry using both approaches have pro- duced a wide range of results. In most cases there appears to be little comspondence be- tween the total factor productivity approach and the profits/market share approach, even though both employ some variation of value- added in the processing industry. Conse- quently, it is Micult to draw conclusions even about individual sectors, let alone the food industry in its entirety. In fact, talung the results of these studies as a whole, the findmgs can be said to be somewhat ambiguous, some- times counter-intuitive and frequently contra-

WORKSHOP PROCEEDINGS 471

dlctory. To the extent that it is possible to find any consensus, it is interesting that the cane and beet sugar refining industry which is highly concentrated, imports raw materials and sells to other manufacturers who export finished product to the protected U S . market is regarded as one of our most competitive industries.

Clearly, there is still much to be done inthe development of the concept, measurement and theory of competitiveness. Dlfferent measures are required for dlfferent levels of aggregation and improvements are needed on the value added, trade and price ratios which have been used. In view of the complexity of the concept, efforts to compress competitiveness assess- ment into a single value may not be helpful. But the largest challenges remain in modelling the behaviour of firms and industries in re- sponse to environmental factors such as gov- ernment policy, the actions of competing firms, buyers and suppliers. Development and refinement of the theory in this area will re- quire expertise in both economic theory and strategic management. Agricultural econo- mists have a role to play in t h ~ s development, building on their contributions of the past through analysis of factor and product markets and other determinants of competitiveness.

NOTES ’Prepared for CAEFMS Workshop-AIC Confer- ence at St. John’s Nfld. August 1993 2Media coverage of competitiveness has been ex- tensive. An electronic search of Canadian Business and Current Affairs publications (DIALOG on Disk) for the past five years (1 988 to March 1993) identifies 1 182 citations with the word “competi- tiveness” in the title. 3Assuming increasing return to scale and non-ho- mothetic costs. 3ndustnes are classified in ‘Table 2 as highly com- petitive d the Canadian TFP was higher than the u s , moderate if it was close (O.~-CANRTS<~ .o) and low drelative TFF’ was below 0.8. ’Some differences may be exacerbated by different time periods for which data are collected. kame and Lapan (1992) provide an alternative explanation based on market structure as to why quality consistency is less of a problem for the

Canadian Wheat Board than its rivals from the united states. 7An excellent example of how these concepts relate to the ablitity of a fm to profitably maintain mar- ket share is Tremblay (1 987). In his study on the potential sources of economies of scale in the U S . brewing industry, he introduces in a translog short run cost function, disembodied technological change affecting all f m s in the industry, embodied technological change specific to individual firms, and output growth rate to take into account the influence of marketing variables on the scale of production. Embodied and disembodied techno- logical change are shown to lower costs while f m s experiencing rapid growth are “low cost” only in periods characterized by high economies of scale. This implies that demand side variables also matter in explaining market shares. ‘Munificence is a measure of the environment’s capacity to support growth. It can be measured as the growth in demand, the level of slack resources (such as government funding) or imputed from the product life cycle (early stages offer high growth environments). ’Dynamism is a measure of the degree of variability (demand, input prices, etc.) that is difficult to pre- dict. Dynamic environments make long range plan- ning difficult because predicting the competitive climate is difficult, but promote Schumpeterian rents. ”Complexity describes the degree of interconnect- edness and dependence of ae focal organization on other oganizations. A fm requiring a greater num- ber of inputs from a large number of suppliers for instance, faces a more complex environment than the single input f m .

REFERENCES Abbott, Willip and Maury Bredahl1992. Com- petitiveness: Dejnitions, Useful Concepts and Is- sues. Paper presented at the International Agricultural Trade Research Consortium’s Sym- posium on Competitiveness In International Food Markets. Annapolis, Maryland. August. Agriculture Canada 1990. Report to Minister of Agriculture of the Task Force on Competitiveness in the Agri-Food Industry. June. Ankli, RE. 1992. Michael Porter’s Competitive Advantage and Business History. Business and Economic History 2 1: 228-236. Ash, Ken, and Lars Brink 1992. The Role of Competitiveness in Shaping Policy Choices. Work- ing Paper APD 92-5. Ottawa: Agmulture Canada.

472 CANADIAN JOURNAL OF AGIUCULTURAL ECONOMICS

Baldwin, John R and Paul K Gorecki 1986. The Role of Scale in Canada-US. Productivity Differ- ences in the Manufacturing Sector 1970- 1979. Royal Commission on the Economic Union 6 . Ottawa: University of Toronto Press. Banik, M. 1992. Performance Eflects ofStrategic Groups and Task Environments in FoodManufac- turing Industries: Augmenting the Bain-Mason Paradigm. MSc. Thesis, McGill IJniversity, Mont- real. Barkema, Alan, Mark Drabenstott and Luther Tweekn 1990. The Competitiveness of Agricul- ture in the 1990's. in Kristen Allen (Ed.) Agricul- tuml Policies in a New Decade. W a h g t o n , D.C.: Resources for the Future and National Planning A ssoc lation. Barkman, Patricia 1992. Overview of Chunges in h e Pe$ormance and Structure of Canada's Food and Beverage Processing Industty. Working Paper APD 92-2. Policy Branch. Agriculture Canada. July. Bredhal, ME. and KW. Forsythe 1989. Harmo- nizing Phyto-Sanitary and Sanitary Regulations. World Economy 1 3: 19 1 -206. Brinkman, George L 1987. The Competitive Po- sition of Canadian Agriculture. Canadian Journal ofilgricultuml Economics 35: 263-288. Canadian International Trade Tribunal 1991. An fnquiry Into the competitiveness of the Cana- dian FRsh and Processed Fruit and Vegetable Industry. Reference no. GC-90-001, Ottawa: Min- ister of Supply and Services. Castrogiovanni, G.J. 1991. Environmental Mu- nificence: A Theoretical Assessment. Academy of Management Review. 16(3): 542-565. Cousineau, Linda, Marc Ban& Larry Martin, Randall Westgren and Roger Paguaga 1992. Pro$le of Canada's Food Processing Industry. Report prepared for the Grocery Products Forum and Employment and Immigration Canada. Guelph, Ontano: George Moms Centre. Dess, G.G. and D.W. Beard. 1984. Dimensionsof Organizational Task Environments. Administmtive Science Quarterb 29: 52-73. Dhaliwal, Najinder S. 1990. Role of Economies of Scale in Cost Competitivenessof Canadian Food and Beverage Processing Industries. Food Market Commentary 1 1 : 4047. Ottawa: Agriculture Can- ada. Frank, J.G. 1977. Assessing Trends in Canada's Competitive Position: The Case of Canada and the IJnited States. Ottawa: Conference Board. Gazette 1992. Stop bickering: industry. July 29:Bl.

Hazeldine, Tim, Steve Guiton and Robert Wall 1988. Assessing the 'Canadian School' of open economy industrial organization N: Empin'cs. Vancouver: University of British Columbia, De- partment of Agricultural Economics. Hazeldine, Tim and David J. Feely. 1991. Pm- ductiviq, Costs and Competitiveness of Canadian Food Manufacturing Industn'es. Final Report for the Food Policy Task Force, Industry Science and Technology, Canada. June. Hazeldine, Tim 1989. Market Power or Relative Efficiency? An Examination of Profitability Per- formance in the Canadian Food and Beverage Sec- tor. Agribusiness: An International Journal 5 :

Hunt, L 1986. The International Competitiveness of Canadian Fruit and Vegetable processing indus- tries. FoodMarket Commentary 8 : 44-6 1. Ottawa: Agriculture Canada. Lambert, R and R Romain 1992. Structure et performance de I'industrie de la tmnsfonnation des produits laitiers du Qulbecjbce au nmveau contexte commercial. Working Paper no. 17, GRAAL, Dtipartement d'hconomie male , Univer- site Laval. Lanciotti, C. 1991. Technical Regulations in the Canadian Pork Industry. MSc. Thesis, Depart- ment of Agricultural Economics and Business, University of Guelph. Landreville, D. 1989. Trade in processed food and beverage products and how selected countries' policies affect it. Food Market Commentary 11: 15-33. Ottawa: Agriculture Canada. Lanoie, C. 1984. Competitive position of the Ca- nadian meat paclung and processing industry. Food Market Commenta ry 6: 234 1. Lanoie, C. 1986. Comparison of the Canadian and United States food and beverage industries. Food MarketCommentary7: 41-57. Ottawa: Agnculture Canada. Larue, R 1991. Is Wheat a Homogeneous Prod- uct? Canadian Journal ofAgricultura1 Economics 39: 103-1 17. Ottawa: Agriculture Canada. Larue R and HE. Lapan. 1992. Market Struc- ture, Quallty and World Wheat Markets. Canadian Journal ofAgricultuml Economics 40: 31 1-328. Proulr, Yvon 1986. Le libre-kchange et Iagncul- ture. Union des producteurs agricoles du QuCbec. Montreal, mai. Mahoney, J.T. and J.R Pandian 1992. The Re- source-Based View within the Conversation of Strategic Management. Strategic Management Journal 13: 363-380. Martin, LJ., RE. Westgren, and E. van Duren 1991. Agribusiness Competitiveness Across Na-

25-42.

WORKSHOP PROCEEDINGS 473

tional Boundanes. American Joumol of Agricul- tuml Eccmomics, 73: 1456-1464. Porter, ME. 1980. Competitive Stmtegy. New York: Free Press. Porter, ME. 1985. Competitive Advantage. New York: Free Press. Porter, ME. 1990. The Competitive Advantage of Nations. New York: Free Press. Reich, Robert 1992. Wall Street Journal. July 2. Rumelt, R 1984. Towards a Strategic Theory of the Firm, in R.Lamb (Ed.), Competitive Stmtegic Management. Englewood Cliffs, NJ:Prentice-Hall. Scott, B. 1990. Creating Comparative Advantage, in P. King, International Economics andEccmomic Policy: Reader New York: McGraw Hill. Thursby, J.C. and Thursby MC. 1987. Bilateral Tmde Flows, the Linda’s Hypothesis and Ex- change ksks. The Review of Economics and Sta- tistics 69: 488495. Tremblay, V.J. 1987. Scale Economies, Techno- logical Change, and Fin-Cost Asymmetries in the U S . Brewing Industry. Quarterb Review of Eco- nomics and Business 27: 71-86. Van Duren, Erna, Larry Martin and Randall Westgreo 1991. Assessing the Competitiveness of

Canada’s Agrifood Industry. Canadian Journal of Agricultuml Economics 39: 727-738. Van Duren, Erna, Larry Martin and Randall Westgren 1992. A Fmmework for Assessing Na- tional Competitiveness and the Role of Private Stmtegy and Public Policy. Paper presented at the International Agricultural Trade Research Consor- tium on Competitiveness in International Food Markets. Annapolis, Maryland. August. West, Donald 1987. Productivity and the Interna- tional Competitiveness of the Canadian Food and Beverage Processing Sector. Food Market Com- mentary 9: 18-36. Ottawa: Agriculture Canada. West, Donald and Pamela Cooper 1988. Eflecb of the Canada-US. Free Tmde Agreement on the Canadian Food and Bevemge Processing Sector. Food Market Commentary 10: 25-39. Ottawa: Ag- riculture Canada. Westgren, RE. and ML Cook. 1986. Strategic Management and Planning. Agribusiness; An In- ternational Journal. 2: 477489. Wholey, D.R. and J. Brittain. 1989. Charac- terizing Environmental Variation. Academy of Management Journal. 32: 867-882.