Embed Size (px)

Citation preview

Research Note

A Fig Leaf for The Naked Corporation

UDO C. BRAENDLE* and JUERGEN NOLLDepartment of Business Administration, University of Vienna, Bruenner Straße 72, A-1210,Vienna, Austria (*Author for correspondence, E-mail: [email protected])

Abstract. The implementation of the Sarbanes-Oxley Act in the United States and the

German Law of transparency and disclosure (TransPuG) lead to a claim for more disclosureof information with the goal of a ‘‘naked corporation’’ such that all information is available tothe (potential) investors. In this article we pick up this debate and present arguments that the

‘‘naked corporation’’ does not offer an efficient degree of disclosure, as we have to distinguishbetween more and better information. Concerning the latter the new regulations are critical.Cognitive limitations and bounded rationality highlight the risk of information overload.

Asymmetric information illustrates that self induced disclosure can do better than a manda-tory one. Therefore the legislator should not be asked for specific informational contents butfor regulations on the way of information provision.

Key words: Disclosure, Governance, Information Overload, Naked Corporation, Sarbanes-Oxley Act

JEL Codes: K22, G34, D82

1. Introduction

A bullish market increases the number of investors and the concern in con-tinuous trade. Stock market collapses, on the other hand, stimulate economicmeasures to avoid further losses (Coffee, 2001, p. 64). The last few years werestamped by collapses and culminated in the scandals of Enron, WorldCom,and Parmalat. To recover investors’ confidence, which is the key element ofhighly developed stock markets, legislators reacted by passing laws instead oftrusting in the markets or Corporate Governance Codes which were passed inalmost every country (Becht et al., 2002).

In June 2002, as soon as the scandal of WorldCom was publicly known,the American Government and the U.S. Securities and Exchange Commis-sion (hereafter: SEC) as the regulatory authority passed a federal law, the socalled Sarbanes-Oxley-Act (hereafter: SOA). According to this act, the SECis responsible that the SOA is implemented and enforced. With the help of

Journal of Management and Governance (2005) 9:79–99 � Springer 2005

DOI 10.1007/s10997-005-1567-2

several measures the SOA tries to recover investors’ confidence in U.S.-companies by the following means. The supervisory function of the board isstrengthened by audit committees. Certain activities of the board membersare regulated more strictly. These activities concern transactions like insidertrading (Posner and Scott, 1980, p. 120). With the threat of higher penalties,the management should be forced to identify more with the financial con-cerns of the company. One of these measures is that the chief executives(CEO) and chief financial officers (CFO) of America’s biggest companieswith annual revenues of more than $1.2 billion have to swear in front of anotary that ‘‘to the best of [their] knowledge’’, their latest annual andquarterly reports neither contain an ‘‘untrue statement’’ nor omit any‘‘material fact’’ relevant to investors. The independence of the accountantsshould be guaranteed by the introduction of the Public Company AccountingOversight Board which should supervise the accountants. In other words, it isan additional institution which supervises the supervisor. Other importantparts of the SOA – and that is our main concern in this contribution –provide wider and more strictly enforced disclosure rules. It is not surprisingthat the last point makes up a big part of this federal law as one of the mainreasons for the collapse of Enron and WorldCom was the inefficient and falsedisclosure of information.

This paper’s starting point is the trend towards more (mandatory)disclosure. Not only Common Law legislators in the Anglo-Saxon coun-tries follow this path as demonstrated by the SOA. Civil Law countries inEurope as well have passed similar regulations to provide for moretransparency and disclosure. In Germany, for example, laws for moremandatory transparency and disclosure were enacted (TransPuG 2002,KonTraG 1998). Table I offers a short overview on recent legislation indifferent countries. Full disclosure and transparency, the so called ‘‘nakedcorporation’’ (Tapscott and Ticol, 2003), seems to be a tide, motivated, inlarge parts, by the assumption that more information is better than less.This article starts with an agent based approach leading to the proposalfor future legislation on disclosure issues. With that so-called hybridstrategy in mind we scrutinise its inherent assumptions, i.e. whether moreinformation will always be better. In that context the possibility ofinformation overload and its negative consequences are discussed whichencourage a critical reflection of mandatory disclosure as well. At the endwe examine the arguments in favour of more mandatory disclosure andprovide an overview on existing empirical literature. We will conclude thatthe current trend towards more mandatory disclosure should be reassessedand that legislators in general should not regulate the information contentto be disclosed but the way of information provision and the kind ofmonitoring to ensure correctness and validity of the information.

80 UDO C. BRAENDLE AND JUERGEN NOLL

Table

I.Examplesforthecurrenttrendtowardsmore

disclosure

State

Laws

Content

Germany

GesetzzurKontrolleundTransparenz

imUnternehmensbereich

(KonTraG

1998),

Transparenz-

undPublizitatsgesetz

(TransPuG

2002),

GermanCorporate

Governance

Code(2002)

Withthehelpofmore

transparency

anddisclosure

endangering

developments

forthecontinuityofcompaniesshould

bedetectedearly.

Theindependence

ofGermansupervisory

boardsaswellasauditors

should

bestrengthened,thusrestoringconfidence

inthemanagem

ent

ofGermancorporations.

Austria

FederalStock

Market

ExchangeLaw

In§83thisLaw

stipulatesthateveryinform

ationwhichcould

influence

the

price

ofsecurities

hasto

bedisclosedbythemanagem

entim

mediately.

France

TheFrench

FinancialSecurity

Act

(2003)

TheAct

coversawidescopeofissues,includingthedisclosure

ofauditfees.

United

Kingdom

Greenbury

Report

(1995),Combined

Codeon

Corporate

Governance

(2003)

TheGreenbury

Report

wasoneofthefirstcodes

formore

transparency

anddisclosure

ofmanagerialcompensation.TheCombined

Coderequires

more

disclosure

intended

toincrease

transparency.

USA

Sarbanes-O

xleyAct

(SOA

2002),FinalNYSE

Corporate

Governance

Rules(2003)

SOA

andtheNYSECorporate

Governance

Ruleswereenacted

torestore

thelost

investors’confidence

after

therecentfinancialscandals.The

protectionofinvestors

withthehelpofmore

disclosure

seem

sto

bethe

aim

.Strictliabilityformisstatements

tightenthelaw.

Canada

New

Disclosure

Requirem

entandAmended

Guidelines

(2002)

ThisReport

oftheToronto

Stock

Exchangecontains15recommendations

forthedisclosure

ofthecompanies’corporate

governance

system

s.

A FIG LEAF FOR THE NAKED CORPORATION 81

2. Asymmetric Information and Agency Theory

There are different kinds of information. A fundamental distinction lies in theverifiability of information. Verifiable information can be readily examinedfor truthfulness once it is revealed, non-verifiable information must betrusted as it cannot be checked. That leads to incentive problems such as howto get managers, for example, to provide correct information on subjects thatare not verifiable. Another distinction can be made based on the criterion ofobservability. (Table II summarizes the different kinds of information.) Butsince we confine our analysis to information which is made observable –either voluntary or compulsory – we need not deal with that characteristic.Furthermore, we restrict our analysis to verifiable information since this isthe only kind which can be (meaningfully) governed by legal regulations. Theforced disclosure of non-verifiable information would be useless because thecorrectness of the disclosed information could not be monitored and nosanctions could be imposed for providing wrong data. Such informationwould be similar to ‘‘cheap talk’’ which is futile. Courts have to be able todetermine whether a market player possesses the relevant information andwhether (s)he disclosed it correctly. Otherwise courts cannot sanction a partyfor failing to adhere to the regulations.

In the relationship between investors and companies or between share-holders and management respectively we are always confronted with asym-metric information. One side has specific information in which the other is

Table II. Verifiability and Observability of Information

Verifiable Unverifiable

Observable Information which can be watched

by an outside party and proven to a

third party, e.g. the quantity

of a good.

Information which a party can

observe but cannot substantiate at

an acceptable cost to a third party

(such as a court), e.g. the quality

of art can be determined by

audience members but cannot be

subject to a trial in court.

Unobservable This is an impossible combination

since if a person doesn’t observe

information then this person cannot

prove it to anybody else.

Actions or qualities which cannot

be seen and therefore cannot be

proven either. The typical example

is a manager’s effort which cannot

be observed since many other

factors are responsible for the

company’s success too.

82 UDO C. BRAENDLE AND JUERGEN NOLL

interested in. In the economic literature the topic of asymmetric informationemerged into a broad area of research. Already two Nobel prizes wereawarded for five proponents of this area (1996 Mirrlees and Vickrey, 2001Akerlof, Spence and Stiglitz).

In general a principal–agent-relationship exists if an agent accomplishes atask for a principal and either an agent’s quality or an agent’s action is notdirectly observable (and verifiable) for the principal. Therefore an incentivecompatible contract has to be signed depending on an observable (and oftenverifiable) outcome which provides insight in the unobservable informationsuch that the agent acts according to the principal’s objective.

Agency theory is applicable to corporations because of the separation ofownership and control. This problem was already mentioned by AdamSmith, but only in 1932 ‘‘rediscovered’’ by the seminal book of Adolph Berleand Gardiner Means. They documented the extent to which control shiftedfrom shareholders to the managers. The investors or shareholders (as prin-cipals) want their agents (managers) to maximize the value of their investedcapital. But the managers act opportunistically and may be better off pur-suing some other strategy. Writing an incentive compatible contract guar-anteeing a maximization of investor value is not an easy task. Even if such acontract exists, it does not necessarily hinder the managers to find new moreor less legal ways to increase their own benefit. According to Hart (1995) asecond best solution is attainable via an optimal incentive contract. Thedesign of such contracts is the main concern of a large part of classicalcontract theory (cf. Schweitzer, 1999). But writing such a contract gives riseto agency costs (Jensen and Meckling, 1976) which stem from the asymmetricdistribution of information between principals and agents combined with thefact that the results are not perfectly correlated with efforts of the insiders.

Summing up, agency theory shows us how to use observable informationto draw conclusion about unobservable qualities and actions. Where doesthis theory come into play for our concern – determining an optimal amountof information disclosure? Table III gives an overview on the methods wewill discuss now.

We stated above that only verifiable data can be meaningfully made objectof regulation. But since observability and verifiability are not necessarilycongruent, it is possible that the agent has verifiable information but wouldopt for not making it observable because of negative inferences which couldbe drawn upon it about other unobservable qualities or actions. In otherwords, the management refuses to disclose hard data which would hurt theirinterests. In such a case writing an incentive compatible contract could be onepossible mechanism to make the managers work and disclose correctly. Butthis approach is restricted to those who are closely connected to the companyand can therefore conclude contracts with the managers. For the generalaudience, i.e. for the securities’ market, this possibility is excluded.

A FIG LEAF FOR THE NAKED CORPORATION 83

Table

III.

Waysto

conquer

theasymmetricinform

ationproblem

Method

Pros

Cons

Incentive

compatible

contracts

Thesecontractsoffer

thepossibilitythattheagent

revealshisprivate

inform

ationwithoutenforcem

ent.

Restrictedto

partieswhichare

closely

connectedto

the

company.Forthegeneralaudience

(i.e.securities’

market)thispossibilityisexcluded.

Self-induced

disclosure

Companiescandecidebythem

selves

whichinform

ation

todisclose,asforeach

companyother

data

are

relevant.

Monitoringcostsare

reduced.

Market

mechanismsmayfaildueto

thelemon

market

theory

orexternalities.Therefore

an

underproductionofinform

ationmaybetheconsequence.

Mandatory

disclosure

rules

Inform

ationprovisionisguaranteed.Theinvestors/

shareholderscanrely

oncertain

inform

ation.

Legislators

donotknow

whichkindofinform

ationis

importantto

investors

andshareholdersatwhichtime.

Highmonitoringcosts.Risksofprovidingmore

butnot

betterinform

ationresultingin

inform

ationoverload.

Hybridstrategy

Themarket

shalldecidewhichkindofinform

ationto

bedisclosedtrustingin

themarket

mechanisms.The

Law

shallregulate

inwhichwaydisclosedinform

ationis

validated.Certain

‘‘minim

um

standards’’ofdisclosure

providebasicinform

ation.

Monitoringcosts,butless

thanwithamandatory

regim

esince

thecompletenessofdiscloseddata

doesn’thaveto

bechecked

thatmuch.

84 UDO C. BRAENDLE AND JUERGEN NOLL

Another approach goes back to Grossman (1981), Milgrom (1981) andJovanovic (1982). Starting point is the notion that the company’s manage-ment itself has got sufficient incentives to disclose information for theinvestors, even without the interference of the legislator (self-induced disclo-sure). If disclosure costs are negligible, rational investors would assume non-disclosing firms to have lower quality than those who disclose. This motivatesfirms of relatively high quality among the non-disclosing set to reveal privateinformation. As long as the unveiled information concerns verifiable data,rational investors can (and will) draw conclusions from the voluntarily dis-closed information. So the company with the best private information willreveal it in order to set itself apart from the rest and gain a competitive edgein the financial market. This will trigger a process of unravelling of beneficialnews of firms until only the one with the worst news is left over withoutunravelling. Given the dataset’s assumed verifiability firms cannot engage indishonest behaviour without being confronted with effective remedies onbehalf of consumers and authorities. So voluntary disclosure is a possibleoutcome (Baird et al., 1994).

This unravelling result is closely connected to the signalling theory, wherethe owners of information disclose this information as long as the disclosurehas got an economic advantage (Spence, 1973). To stand out from the crowdof the other companies, each of them has an incentive to disclose good news.The companies will disclose information as long as the optimal level of dis-closure is reached. And this optimum is reached when the costs of providingadditional information is not compensated by a higher issuing price. And if acompany wants to get highest issuing price, it has to make sure beforeissuing, that there will be continuous information even in the secondarymarket, ‘‘a believable pledge in continue disclosure’’ (Easterbrook andFischel, 1984, p. 669).

The third possible way out of the mentioned situation is mandatory dis-closure regulation. If one doesn’t trust in the market mechanism to provokeself-induced disclosure or in the ability to write incentive compatible con-tracts, one could still take the road to the legislator. In that case, rules wouldhave to be enacted stating exactly which kind of (verifiable!) information hasto be made public under which circumstances and an authority would have tobe set up to monitor the firms’ compliance with the rules. Although this is themomentary trend, there is a major drawback. Legislators do not (and cannot)know which kind of information is important to investors and shareholdersat which time. Therefore a meaningful (and beneficial in terms of marketefficiency) system of mandatory disclosure is close to impossible to imple-ment. For each company other data are relevant at different times.

This leads to two consequences. Either the rules are very general such that‘‘all relevant data has to be disclosed immediately’’ (as in the AustrianFederal Stock Market Exchange Law). Then standards according to what

A FIG LEAF FOR THE NAKED CORPORATION 85

information meets these criteria have to be developed by the monitoringauthorities and firms are encouraged to flood the market with informationjust to be on the safe side. Or, on the other hand, the law may give anexhaustive list of information items to be disclosed at certain occasions.Then, of course, nobody can guarantee that again the really importantinformation is not forgotten in that list. In both cases a mandatory disclosuresystem runs into the risk of letting firms provide more, but not betterinformation.

We therefore propose a hybrid strategy to tackle the asymmetric infor-mation problem. The market, i.e. the companies, shall decide which kind ofinformation to be disclosed trusting in the mechanisms of voluntary infor-mation provision. Only very basic information, e.g. annual reports, should beclaimed for by Law. Additionally, if there is too much scepticism that themarket mechanism leading to self-induced disclosure alone will work,shareholders could be endowed with the right to ask for specific data in away, for example, that a specific percentage of the shareholders can demandinformation at any point of time. (Such rules are already applied in somecountries, e.g. § 112 of the Austrian Public Corporation’s Act states thatevery shareholder can demand information at the general assembly and thataccording to § 106 of that Act (a group of) shareholders holding five percentof the corporation’s capital can demand the convening of an extraordinarygeneral assembly.) Even the mere existence of such rights should incentivisethe managers to take steps in order to avoid these additional assemblies byproviding shareholders with enough information.

Anyway, the Law shall concentrate on regulating in which way disclosedinformation is validated. The provision of such procedural regulation issufficient and rules concerning the content of the information shall be leftout. Since we only talk about verifiable data, it can be examined by thirdparties. Whether an accountant or any other institution should check the

Table IV. Direct and indirect costs of mandatory disclosure

Costs User Producer

Direct Reading bulky annual

and analyst reports, studying

of more stock-market news, etc.

‘‘Production’’ of more and more

information in form of extensive

folders and reports.

Indirect Additional costs due to bounded

rationality. This leads to

inefficient investments which

is accompanied by a loss of

yield return.

Companies can only send out diminished

signals as noise in the market increases.

Therefore companies are hindered to stand

out from the crowd. This in turn leads to

under- or overinvestment. Especially the latter

is a huge problem for companies.

86 UDO C. BRAENDLE AND JUERGEN NOLL

information provided to the market for correctness, should be regulated inorder to ensure a certain standard of confidence in disclosed information. Ofcourse, such a system produces monitoring costs as well, but to a much lesserextent than mandatory disclosure since not every piece of information has tobe checked whether it encompasses all the content required by law.

The justification of our hybrid strategy is based on the theory that moreinformation alone is not always better and that under certain circumstancesmay even be responsible for worse outcomes for the investors. Therefore wewill lay the foundation for this theory in the next sections in which we dealwith the costs of information and the consequences of bounded rationality.

3. Better Versus More Information – The Costs of Information Provision and

Processing

Disclosure rules are designed to solve the informational asymmetries thatexist between companies and investors. The idea behind mandatory disclo-sure rules is to promote informed investor decision making, capital marketintegrity and efficiency. It is commonly viewed that as soon as investorsreceive the information they could protect themselves against corporateabuses and mismanagement.

But for a regulation regime based on disclosure to work two things areneeded. First, information has to be disclosed. The above mentioned addi-tional regulations of a SOA or TransPuG ensure that the companies disclosemore and more information. Accordingly they have to bear the costs ofdisclosure (‘‘production costs’’). These costs can be direct or indirect. For thecase of self induced disclosure the companies only abide the direct costs.Mandatory disclosure is responsible for an extension of the direct costs (moreinformation has to be produced) but as well for additional indirect costs dueto weaker signals because of increasing noise. The latter leads to over- orunderinvestment, where naturally underinvestment is the main problem forfirms.

But disclosure of information is not enough. Analysts, brokers, investorsand other capital market participants have to use the disclosed informationefficiently. To put it another way, capital market participants need not onlyto have access to more information, they must be able to process it in aneffective way. For the ‘‘user’’ of information mandatory disclose bearsadditional costs as well. Those can be direct or indirect too. On the one hand,more information has to be processed which takes time and draws on otherresources. On the other hand, the indirect costs due to bounded rationalityand the resulting information overload are bad for the investors as they leadto inefficient investments with a loss in yield return. In Table IV a conciseoverview on the issue of costs due to more information can be found.

A FIG LEAF FOR THE NAKED CORPORATION 87

With regard to the recent financial scandals investors in general do notneed more, but better information. Using the distinction between the ‘‘supplyside’’ and ‘‘demand side’’ of information (Macey, 2003) we see that recentregulations only dealt with the ‘‘supply side’’, i.e. the production and for-matting of information. The needs of the ‘‘demand side’’, i.e. to have goodinformation at hand in order to interpret it and translate it into good tradingdecisions, have been readily overlooked. The ultimate objective of disclosurerules should be better information, irrespective of the amount of information,because only better information leads to better decisions and better decisionsin turn account for better investments.

At the moment securities regulation seems to be motivated, in largepart, by the assumption that more information (= enhancement on the‘‘supply side’’) alone can do the trick and solve the disclosure problem.That’s the reason why we see rules implying the mandatory disclosure ofmore and more information in the sequel of the scandals mentionedabove. Disclosure on a real-time basis is the logical consequence of theongoing trend towards ensuring the timeliness and accuracy of informa-tion provided to the capital markets (SOA § 409). In addition, the SEChas proposed adding eleven new items that must be filed on Form 8-K(Release No. 33-8106) and wants to expand disclosure requirements withrespect to the removal, and election of directors and the appointment ofnew officers. The companies are required to disclose material changes toits articles of incorporation or bylaws. Last but not least, the SEC sepa-rately has proposed requiring companies to file current reports describingcertain insider transactions in company securities and insider loans. Thesenew disclosure requirements are expected to result in over 215,000 addi-tional Form 8-K filings p.a. at a cost of over $89,500,000 p.a. (ReleaseNo. 22-8090). Management’s discussion and analysis (hereafter: MD&A) isanother area where disclosure was expanding fast after Enron. Manybelieve that an extended MD&A can go a long way toward remedying theshortcomings in the mandatory disclosure regime that contributed to therecent corporate and accounting scandals (Release No.33-6711). Further-more new disclosure rules concerning off-balance sheet transactions (SOA§ 401), reconciliations of pro-forma financial information with the regis-trant’s financial condition and result of operation (§ 401), insider stocktransactions (§ 403), internal control systems (§ 404), codes of ethics forsenior financial officers (§ 406) and CEO and CFO certifications offinancial statements (§§ 302 and 906) were introduced by the SOA.

All in all, the trend is obvious. Companies are obliged to disclose moreand more data. But will these also result into being better information for theinvestors? In the next section we deal with the question whether moreinformation will always be better for a decision maker.

88 UDO C. BRAENDLE AND JUERGEN NOLL

4. Why Not a Naked Corporation – When is More Not Better

We restricted our analysis to verifiable and observable information. Never-theless, we can state that more such information does not necessarily meanbetter information. Market participants rarely want information for its ownsake. They want information to decide well and better protect their interests.Disclosure is merely the chosen means to the end of informed investordecision making. So how much information does an investor need to attainthat goal? Let us start our quest for the optimal amount of information at theminimum amount of information.

The minimum amount of information of a given security is its price.According to Grossman and Stiglitz (1980) informed agents transmit infor-mation to the market through trade. This information is impounded in theprices. According to the semi-strong efficient market hypothesis prices reflectall publicly available information. As long as a sufficient number of marketparticipants are informed (Fama, 1970, p. 388), all information would moreor less immediately flow into the price of the securities. Therefore ‘‘theuninformed traders can take a free ride on the information impounded by themarket: they get the same price received by the professional traders withouthaving to do any of the work of learning the information...’’ (Easterbrookand Fischel, 1991). But whether an increase in public information, i.e. moredisclosed data, really creates higher efficiency in a competitive market isquestionable. As shown by Schredelseker (2003) in his numerical experimentsmore public information on the one hand improves the precision of esti-mations but on the other hand increases the joint error of all those traderswho rely on joint but not perfect information. If the latter effect is dominant,we have to expect increasing efficiencies with growing public information. Inthis case market efficiency falls with a rise in public information.

But furthermore the price cannot even reveal all information since acertain degree of noise is necessary for the functioning of the market in orderfor the informed traders to profit from their informational advantage. Soprices can only be partially revealing. If prices were perfectly revealing theinformed traders would have no incentive to reveal their information in thefirst place. In fact we observe in markets that rational investors try tospeculate against irrational investors. Black (1986) called them informationtraders and noise traders respectively. People who trade on noise are irra-tional in the sense that they trade even though, from an objective point ofview, they would be better off not trading. Of course, in their ‘‘own world’’they are subjectively perfectly rational. This might happen as they may thinkthe noise they are trading on is hard information or perhaps they just like totrade (cf. Laffont, 1985). Most of the time, the noise traders as a group willlose money by trading, while the information traders as a group will makemoney. With an increasing amount of noise, the prices will have more noise

A FIG LEAF FOR THE NAKED CORPORATION 89

incorporated in them and consequently it will become more profitable forpeople to trade on information. The farther the price of a stock gets from itsvalue, the more aggressive the information traders will become. Neverthelessthe information traders can never be sure to be trading on information ratherthan noise.

Taking all this into consideration prices are only partially revealing.Therefore more information in addition to the price is needed. But as theutility function depending on the amount of information can also be char-acterised by diminishing marginal gains and as there are costs of processinginformation too, we have to be very careful when we demand more infor-mation. Some reasons for the mentioned concavity lie in the asymmetricinformation situation, in the investors’ bounded rationality and in the con-sequential danger of information overload. We will deal with those aspects inthe following sections.

5. Bounded Rationality and Limited Cognitive Abilities

The new securities regulation is in large parts motivated by the assumptionthat more information is always better than less and hat ensured access togreater amounts of material data. Legislators seem to be in agreement withBrandeis: ‘‘Publicity is justly commended as a remedy for social and industrialdiseases. Sunlight is said to be the best disinfectant, electric light the mostefficient policemen.’’ (Brandeis, 1914). But little attention has been paid to thequestion of how investors, analysts, brokers and other market participantssearch and process information and make decisions. The way people processinformation and make decisions is extremely complicated and the product ofa number of psychological factors and can therefore lead to informationoverload with bad consequences.

The neoclassical economic theory assumes that actors are rational, know-ing all possible future outcomes and choosing the optimal strategy accord-ingly. This happens immediately and without costs (Kreps, 1990, p. 745).Herbert Simon (1955) describes the ‘‘economic man’’ who is perfectly ra-tional as follows: ‘‘This man is assumed to have knowledge of the relevantaspects of his environment which, if not absolutely complete, is at leastimpressively clear and voluminous. He is assumed also to have a well-organisedand stable system of preferences, and a skill in computation that enables him tocalculate, for the alternative courses of action that are available to him, whichof these will permit him to reach the highest attainable point on his preferencescale.’’ In this sense the problem of gathering and processing information isnot seen. In a world of fully informed actors institutions regulating theprovision of information are neither explainable nor necessary. Actors simplyneed to be supplied with more information to better evaluate their options

90 UDO C. BRAENDLE AND JUERGEN NOLL

and make better decisions. If this was the case, more information wouldalways better than less.

Within the new institutional economics the assumption of full rationality isrelaxed and the economic actors are viewed to be only boundedly rationalwhich points out that they do not have perfect information and/or may notbe able to process all available data adequately. Herbert Simon was oneof the first to point out the existence of bounded rationality and many oth-ers followed (Simon, 1957; Kirman, 1993 Conlisk, 1996). Findings frombehavioural organisation theory, behavioural decision theory, surveyresearch, and experimental economics confirmed this line of thought.Bounded rationality asserts that decision makers are intendedly rational, i.e.they are goal-oriented and adaptive, but because of human cognitive andemotional architecture, they sometimes fail, even in important decisions. As aresult, individuals tend to economize on cognitive effort and time whenmaking decisions by adopting heuristics that simplify complicated tasks.According to Simon, individuals tend to ‘‘satisfice’’ rather than optimise andmight therefore fail to search for and process certain information. Imperfectrationality causes a restricted dealing with information, as economic actorsare budget constrained, i.e. the unrestricted acquisition of information isimpossible due to cost reason. Moreover too much information is not wished,as individuals can only deal with a certain amount of it. As people havelimited cognitive abilities to process information, ‘‘more information isalways better’’ does no longer hold and disclosure problems may arise.

This is very important for the amount of mandatory disclosure, as a task issaid to become more complicated as it involves the processing of moreinformation. Individuals are making decisions in all sorts of ways. Whichstrategy to take depends on how much information an individual considersand processes and the tradeoffs a person makes between the attributes thatinfluence which alternative to choose. Several decision strategies exist; theyrange from elimination by aspect, over lexicographic strategy to weightedadding strategy (equivalent to a cost-benefit analysis). Faced with a simplertask, the decision maker is more likely to consider all options and use a moreaccurate procedure that evaluates more information. Studies show that whenfaced with complicated tasks that involve a lot of information, individualstend to adopt simplifying decision strategies that require less effort but areless accurate too (Paredes, 2003). The net result of using a less accuratedecision strategy when having more information at hand is often an inferiordecision. To put it another way, individuals may make better decisions usinga more complex decision strategy on less information than using a simpledecision strategy on more information. Or to take Paredes’ words in contextto Brandeis, sunlight can also be blinding.

It is worth mentioning in this context that information overload is onlyrelevant for those who Black called information traders because noise traders

A FIG LEAF FOR THE NAKED CORPORATION 91

don’t care about the amount of information at all since they decide on othercriteria in the first place, i.e. fun or newspaper headlines. But noise traders areresponsible for only a small part of daily trades. On the contrary, rationalinvestors (or ‘‘information traders’’) are responsible for the majority oftrading volumes. (Just think about institutional investors such as CalPerswith invested assets of $ 166 billion.) For such rational investors which swaylarge amounts of assets information overload is indeed a highly importantphenomenon. These traders are faced with the challenge to process allavailable company and market data in order to come to beneficial conclu-sions. If they get lost in the middle of a pile of irrelevant data high losses arepossible. Of course, brokers develop methods to overcome the informationoverload. A broker may, for example, instead of reading three analyst reportsthoroughly only scan through ten of them or he may choose to read only tworeports, e.g. those with the best and worst prognosis, and disregard all others.In either way, it is possible that valuable information got lost by using such asimplifying strategy.

Although experts might be better in determining what to ignore and whatto focus on and therefore might be better in searching and evaluatinginformation (Ettenson et al., 1987), it does not mean that experts could notdo better with less information. There are several studies and experimentsshowing that experts can become overloaded, although they can use moreinformation than ‘‘small’’ investors (Biggs et al., 1985; Shanteau, 1989;Hirshleifer and Teoh, 2002).

Despite the problem of information selection where the receiver of theinformation picks out some data from the plenitude and neglects the restwhich could leave him with a worse informational decision basis as if hewould have been provided with less, but accurate information in the firstplace, there is a possible waste of resources too. It is easily conceivable that alot of data contain redundancies. These generate costs for their productionand distribution as well as their processing. If five reports are similar, forexample, it would have been sufficient to read the first but the similarity canonly be known after the reports have already been read and time has beenwasted.

6. Arguments in Favour of Mandatory Disclosure?

The restoration of the lost confidence of investors was a popular argumentfor more mandatory disclosure in recent times. The financial scandalsencouraged the adversaries of self induced disclosure to doubt its impact.Therefore we want to analyse the arguments for mandatory disclosure andshow that most of them are not applicable.

A common line of argument rests on the lemon market theory. In hisseminal paper Akerlof (1970) has shown that a market breaks down if quality

92 UDO C. BRAENDLE AND JUERGEN NOLL

cannot be well signalled. Applied to our subject one could say that withoutmandatory rules ‘‘good’’ securities are not traded at an adequate price aswithout the protection of mandatory disclosure the market would discountall the securities. We agree that a market without any information will breakdown. But this argumentation neglects that the market is not withoutinformation. Agency theory knows at least two mechanisms to induce vol-untary disclosure (as mentioned above) which can mitigate the adverseselection problem (Spence, 1973 and 1974). The quality signals of a companythen resemble guarantees in a used car market preventing the marketbreakdown (Grossman, 1981; Easterbrook and Fischel, 1991).

Another reason that companies don’t disclose voluntarily all the infor-mation which is relevant to the investors, might be the effect on investmentdecisions of shareholders. These externalities (Manne, 1966; Benston, 1973;Easterbrook and Fischel, 1991) can occur in context with disclosure. Illus-trative examples are Research & Development (R&D)-projects where dis-closure might attract additional investors but also lures the competitors. Anyinvestor or competitor can use the information without reducing the degreeof utility. This results in free riding as a company can neither burden theinvestors nor the competitors with the costs of disclosure. Therefore the costsof not disclosing the information, i.e. the discounting by the investors, couldbe lower than the losses through the use of the disclosed information bythe competitors (Foster, 1980, p. 521). So the theory argues for mandatorydisclosure, as then each competitor will profit in the same way.

We do not question the existence of externalities, but the assumptions ofthis theory. We think no company will disclose all its R&D-projects in detailas most investors cannot do anything with this information or judge thetechnical impact of an invention. As a consequence companies would,without mandatory disclosure, publish just enough information concerningR&D that the investors do not discount.

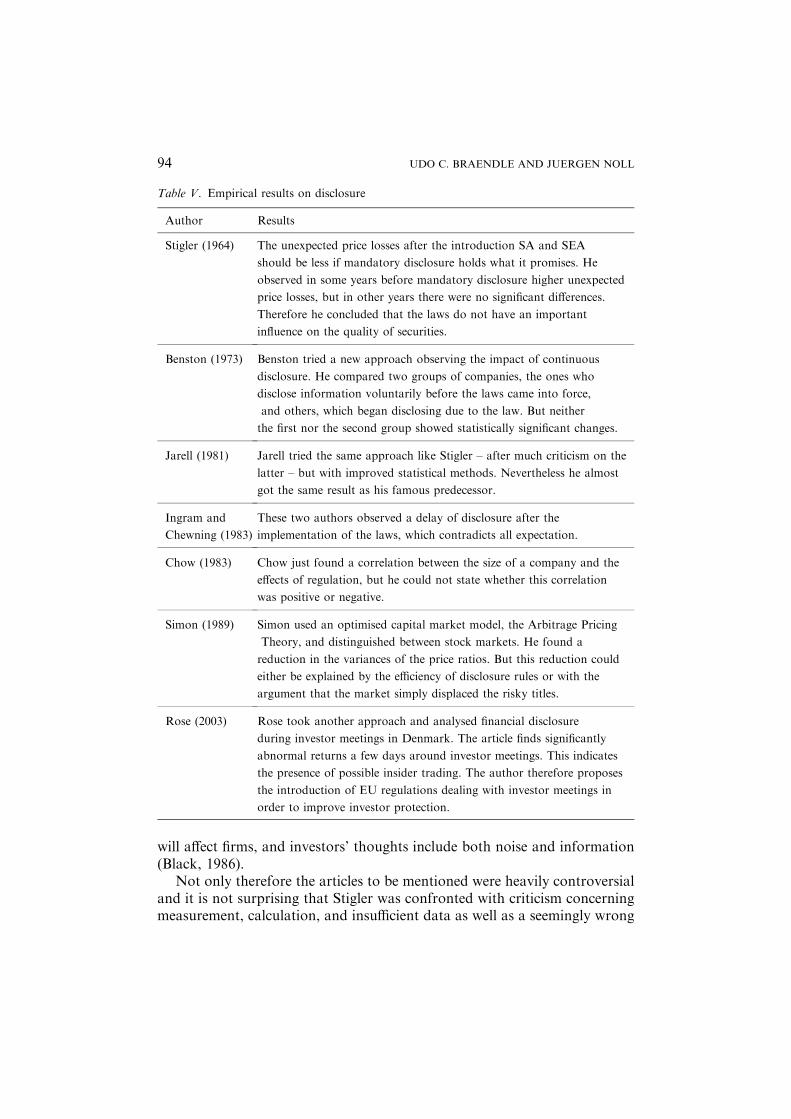

7. Empirical Results on Disclosure

Empirical studies in finance are easier to do than empirical studies in eco-nomics in the sense that data on security prices are generally of higher qualityand more readily available than the data in general economics. Neverthelessthere are major pitfalls in trying to interpret the results of studies of securityprices. All approaches to prove evidence for the inefficiency of SA and SEAtherefore rest on simplifying assumptions. Event studies, which look at stockprice reactions to announcements that affect a firm, were the general device ofthese empirical articles. They would be a very reliable way to find out howcertain events affect firms if there were no noise in stock prices. In fact,though, the stock price reaction tells us only how investors think the events

A FIG LEAF FOR THE NAKED CORPORATION 93

will affect firms, and investors’ thoughts include both noise and information(Black, 1986).

Not only therefore the articles to be mentioned were heavily controversialand it is not surprising that Stigler was confronted with criticism concerningmeasurement, calculation, and insufficient data as well as a seemingly wrong

Table V. Empirical results on disclosure

Author Results

Stigler (1964) The unexpected price losses after the introduction SA and SEA

should be less if mandatory disclosure holds what it promises. He

observed in some years before mandatory disclosure higher unexpected

price losses, but in other years there were no significant differences.

Therefore he concluded that the laws do not have an important

influence on the quality of securities.

Benston (1973) Benston tried a new approach observing the impact of continuous

disclosure. He compared two groups of companies, the ones who

disclose information voluntarily before the laws came into force,

and others, which began disclosing due to the law. But neither

the first nor the second group showed statistically significant changes.

Jarell (1981) Jarell tried the same approach like Stigler – after much criticism on the

latter – but with improved statistical methods. Nevertheless he almost

got the same result as his famous predecessor.

Ingram and

Chewning (1983)

These two authors observed a delay of disclosure after the

implementation of the laws, which contradicts all expectation.

Chow (1983) Chow just found a correlation between the size of a company and the

effects of regulation, but he could not state whether this correlation

was positive or negative.

Simon (1989) Simon used an optimised capital market model, the Arbitrage Pricing

Theory, and distinguished between stock markets. He found a

reduction in the variances of the price ratios. But this reduction could

either be explained by the efficiency of disclosure rules or with the

argument that the market simply displaced the risky titles.

Rose (2003) Rose took another approach and analysed financial disclosure

during investor meetings in Denmark. The article finds significantly

abnormal returns a few days around investor meetings. This indicates

the presence of possible insider trading. The author therefore proposes

the introduction of EU regulations dealing with investor meetings in

order to improve investor protection.

94 UDO C. BRAENDLE AND JUERGEN NOLL

alternate hypothesis (Friend and Herman, 1964, p. 382). This doubt can bereduced as Jarell and Simon later on got almost the same results, like thedecrease of the variance. The other articles as well were not free of criticism.Nevertheless the empirical results give reason to the assumption that wideparts of the capital market were efficient before the introduction of SA andSEA and an improvement of transparency was limited to smaller stockmarkets (Simon, 1989). Although the studies were criticised of referring to areaction of the market 70 years ago, the results are still relevant and shouldlead to a rethinking of regulative measures.

The basis for the most empirical research on the effect of mandatorydisclosure are the two Laws that were established to regulate the securitiesmarket of the United States after the great crash 1929, namely the SecuritiesAct 1933 (SA) and the Securities Exchange Act 1934 (SEA). The reason forthe 1929 crash was – not undisputable – seen in the inadequate and deferredway of informing investors and the consequently overvalued stock prices(Friend and Herman, 1964, p. 382). Event studies came up, where the situ-ation before and after SA and SEA could be compared. Chicago-economistStigler (1964) was the first trying an approach, followed by Benston (1973),Jarell (1981), Ingram and Chewning (1983), Chow (1983) and Simon (1989).A very recent event study was done by Rose (2003). Stigler’s assumption wasthat the unexpected price losses should be less if the mandatory disclosingholds what it promises, namely to inform the investor better about the valueof the securities. Only then the investor would be protected from overratednew issues. Jarell tried the same approach – after much criticism on Stigler –with improved statistical methods. Both compared a period of a few yearsbefore and after the implementation of the laws and got almost the sameresults. They observed in some years before mandatory disclosure higherunexpected price losses, but in the other years there were no significant dif-ferences. Moreover they recognised that the variance of the price ratios hasdecreased the risk of volatility (Stigler, 1964, p. 124; Jarell, 1981, p. 613).Nevertheless this reduction was not explained by the efficiency of the dis-closure rules but with the argument that the market simply displaced therisky titles. Therefore both authors conclude that the laws don’t have animportant influence on the quality of the securities.

One decade later Benston (1973) tried a new – and heavily observed –approach observing the impact of continuous disclosure. He compared twogroups of companies. The ones who disclosed information voluntary beforethe laws came into force, and others, which began disclosing due to the law.Benston found that neither the first nor the second group of companiesshowed statistically significant changes in the chart-development after theimplementation of the laws. ‘‘There appears to be little basis for legislationand no evidence that it was neither needed nor desirable’’ (Benston, 1973,p. 132).

A FIG LEAF FOR THE NAKED CORPORATION 95

Ingram and Chewning (1983) observed a delay of disclosure after theimplementation of the laws, which contradicts all expectations. Chow (1983)just found a correlation between the size of a company and the effects ofregulation, but he could not state whether this correlation was positive ornegative. Simon (1989) used an optimised capital market model, the Arbi-trage Pricing Theory, and distinguished between stock markets. Like Stiglerand Jarell, he found a reduction in the variance of the price ratios as well.

Recently Rose (2003) took another approach and analysed financial dis-closure during investor meetings in Denmark. The article finds significantlypositive abnormal returns a few days around investor meetings. This indi-cates the presence of possible insider trading. The author therefore proposesthe introduction of EU regulations dealing with investor meetings in order toimprove investor protection as the current securities regulations would beinadequate to secure efficient stock markets. Inspiration – according to theRose – could be taken from the new SEC regulation. This contribution ofRose however is exposed to certain scepticism. Especially because the articleis based on the wrong assumption that insider trading is something bad. Wecannot start an extensive discussion which would easily fill another paper.Nevertheless, the economic literature is quite ambivalent concerning insidertrading and there are several arguments against the denunciation of insidertrades (cf. Manne, 1966; Bainbridge, 1986; Ma and Sun, 1998). Furthermorewe disagree on Rose’s claims for the introduction of EU rules dealing withinvestor meetings as the term insider trading is definitely wrong in thiscontext. Even if participants of general meetings get an informationaladvantage there, this would legally never be count as an insider trade. Inaddition a general meeting is in no way secret and everybody who shouldersthe ‘‘time-and-trouble-costs’’ of attending hours of (boring) general meetingsshould profit from the information there. It is absurd to see something unfairin this procedure. Just think about annual reports. We do not ask for amandatory annual report for every shareholder to prevent ‘‘unfair’’ trades ofinvestors who read the report. Table V summarises the empirical research onmandatory disclosure.

8. Conclusion

Our discussion boils down to the observation that investors do not neces-sarily need more but better information. Full transparency of companies(i.e. the ‘‘naked corporation’’), SOA in the US and the TransPuG inGermany ask for more information but blind out the investors and theircapability to process information. We showed that investors are subject tocognitive limitations and, because of bounded rationality, face the risk ofinformation overload. In other words they risk making less accurate

96 UDO C. BRAENDLE AND JUERGEN NOLL

decisions when dealing with more information as they adopt less complicateddecision strategies to simplify the decision process.

Although we surely admit that the enforcement of annual reports, ad-hoc publicity and profit warnings is useful, we claim for reassessment ofmandatory disclosure enforcing a fully transparent company. Voluntarydisclosure with only some fundamental legal requirements should do muchbetter than mandatory disclosure. Therefore the implication for the legislatorlooks as follows: Don’t regulate the kind and amount of data but provideclear methods of validating information and monitoring to ensure truthful-ness and correctness of disclosures. These regulations include stipulationsregarding to the institution which has to check the accuracy of the infor-mation. This institution (or person in case of an accountant) certainly has tomeet criteria with respect to qualification and it (he) must be furnished withthe rights to ask the company for all relevant data in order to check theinformation to be disclosed. Furthermore shareholders (under certain cir-cumstances which need to be clearly defined) could be entitled to demandinformation directly if they are not content with amount of informationsupplied by the firm. This would act as a kind of ‘‘emergency disclosure’’.

This shift from substantive regulations concerning the information con-tent to procedural regulations dealing only with the way of validatinginformation (and only a few mandatory disclosure rules) seems better suitedto overcome the asymmetric information problem between shareholders andmanagers at a lesser cost than the other presented regimes. It includes aspectsof the other methods but avoids (or at least mitigates) their drawbacks.Furnishing shareholders with the right to demand the convening of anextraordinary general assembly provides for a substantial threat. This helpsto incentivise the managers to disseminate enough information in order toavoid such a convening. While endowing shareholders with a powerful toolsuch legislation circumvents the problem that not all shareholders can con-clude an incentive compatible contract with the managers directly. Our hy-brid strategy also accounts for the mechanism of voluntary disclosure butcomplements it by protecting a certain level of information quality. At last,very restrictedly the provision of some basic content is stipulated but incontrast to a full-fledged mandatory disclosure regime the content of addi-tional information is left to the needs of the market and therefore lessmonitoring costs arise.

References

Akerlof, G.: 1970, ‘‘The Market for ‘‘Lemons’’: Quality Uncertainty and the Market Mech-anism’’, Quarterly Journal of Economics 84: 488–500.

Bainbridge, S.: 1986, ‘‘The Insider Trading Prohibition: A Legal and Economic Enigma’’,

University of Florida Law Review 38: 35–68.Baird, D.G., R.H. Gertner and R.C. Picker: 1994, Game Theory and the Law (Cambridge).

A FIG LEAF FOR THE NAKED CORPORATION 97

Becht, M., P. Bolton and E. Roell: 2002, Corporate Governance and Control, ECGI Working

Paper, Brussels.Benston, G.: 1973, ‘‘Required Disclosure and the Stock Market: An Evaluation of the

Securities Exchange Act 1934’’, American Economic Review 62: 132–155.

Berle, A. and G. Means: 1932, The Modern Corporation and Private Property (New York).Biggs, S., J. Bedard, B. Gaber and T. Linsmeier: 1985, ‘‘The Effects of Task Size and Similarity

on the Decision Behaviour of Bank Loan Officers’’, Management Science 31: 970–981.

Black, F.: 1986, ‘‘Noise’’, Journal of Finance 41: 529–543.Brandeis, L.: 1914, Other People’s Money And How The Bankers Use it (New York).Chow, C.: 1983, ‘‘The Impacts of Accounting Regulation on Bondholder and Stockholder

Wealth: The Case of the Securities Acts’’, Journal of Accounting Review 58: 485–520.Coffee, J.: 2001, ‘‘The Rise of Dispersed Ownership: The Role of Law and the State in the

Seperation of Ownership and Control’’, Yale Law Journal 111: 1–80.Conlisk, J.: 1996, ‘‘Why Bounded Rationality’’, Journal of Economic Literature 34: 669–700.

Easterbrook, F. and D. Fischel: 1984, ‘‘Mandatory Disclosure and the Protection of Inves-tors’’, Virginia Law Review 70: 669–715.

Easterbrook, F. and D. Fischel.: 1991, The Economic Structure of Corporate Law (Cam-

bridge).Ettenson, R., J. Shanteau and J. Krogstad: 1987, ‘‘Expert judgment: Is more information

better?’’, Psychological Reports 60: 227–238.

Fama, E.: 1970, ‘‘Efficient Capital Markets: A Review of Theory and Empirical Work’’,Journal of Finance 25: 383–417.

Foster, G.: 1980, ‘‘Externalities and Financial Reporting’’, Journal of Finance 35: 521–533.

Friend, I. and E. Herman: 1964, ‘‘The SEC through a Glass Darkly’’, Journal of Business37: 382–405.

Grossman, S.: 1981, ‘‘The Informational Role of Warranties and Private Disclosure aboutProduct Quality’’, Journal of Law and Economics 24: 461–483.

Grossman, S. and J. Stiglitz: 1980, ‘‘On the Impossibility of Informationally Efficient Mar-kets’’, American Economic Review 70: 393–408.

Hart, O.: 1995, Firms, Contracts, and Financial Structure (Oxford).

Ingram, R. and E. Chewning: 1983, ‘‘The Effect of Financial Disclosure Regulation onSecurity Market Behavior’’, Journal of Accounting Review 58: 562–580.

Jarell, G.: 1981, ‘‘The Economic Effect of Federal Regulation of the Market for New Secu-

rities Issues’’, Journal of Law and Economics 24: 613–675.Jensen, M. and W. Meckling: 1976, ‘‘Theory of the Firm: Managerial Behaviour, Agency

Costs and Ownership Structure’’, Journal of Financial Economics 3: 305–360.Jovanovic, B.: 1982, ‘‘Truthful disclosure of information’’, Bell Journal of Economics 13: 36–

44.Kirman, A.: 1993, ‘‘Ants, Rationality, and Recruitment’’, Quarterly Journal of Economics 108:

137–156.

Kreps, D.: 1990, A Course in Microeconomic Theory (New York).Laffont, J.: 1985, ‘‘On the Welfare Analysis of Rational Expectations Equilibria with

Asymmetric Information’’, Econometrica 53: 1–29.

Ma, Y. and H.-L. Sun: 1998, ‘‘Where Should the Line Be Drawn on Insider Trading Ethics?’’,Journal of Business Ethics 17: 67–75.

Macey, J.: 2003, ‘‘A Pox on Both Your Houses: Enron, Sarbanes Oxley and the Debate

Concerning the Relative Efficiency of Mandatory Versus Enabling Rules’’, WashingtonUniversity Law Review Quarterly 81: 329–355.

Manne, H.: 1966, Insider Trading on Stock Market (New York).Meier-Schatz, C.: 1989, Wirtschaftsrecht und Unternehmenspublizitat (Zurich).

98 UDO C. BRAENDLE AND JUERGEN NOLL

Merrill Lynch: 2002, TechStrat Barometer, 26.02.02 Weekly Wisdom for Technology Inves-

tors.Milgrom, P.: 1981, ‘‘Good news and bad news: Representation theorems and applications’’,

Bell Journal of Economics 12: 380–391.

Paredes, T.: 2003, Blinded by the Light: Information Overload and its Consequences forSecurities Regulation, Working Paper 03–02–02 (Washington University in St. Louis).

Posner, R. and K. Scott: 1980, Economics of Corporation Law and Securities Regulation

(Boston).Rose, C.: 2003, ‘‘Impact of investor meetings/presentations on share prices, insider trading

and securities regulation’’, International Review of Law and Economics 23: 227–336.

Schredelseker, K.: 2003, On the Value of Information in Financial Decisions – A SimulationApproach, University of Innsbruck Working Paper.

Shanteau, J.: 1989, ‘‘Cognitive Heuristics and Biases in Behavioral Auditing: Review, Com-ments, and Observations’’, Accounting, Organizations and Society 14: 165–177.

Simon, C.: 1989, ‘‘The Effects of the 1933 Securities Act on Investor Information and thePerformance of New Issues’’, American Economic Review 79: 295–318.

Simon, H.: 1955, ‘‘A Behavioral Model of Rational Choice’’, Quarterly Journal of Economics

69: 99–118.Spence, M.: 1973, ‘‘A Job Market Signaling’’, Quarterly Journal of Economics 87: 355–379.Spence, M.: 1974, Market Signaling – Information Transfer in Hiring and Related Screening

Processes (Cambridge).Stigler, G.: 1964, ‘‘Public Regulation of the Securities Market’’, Journal of Business 37: 213–

225.

Tapscott, D. and D. Ticol, : 2003, The Naked Corporation: How the Age of Transparency WillRevolutionize Business (Free Press).

A FIG LEAF FOR THE NAKED CORPORATION 99